Aswath Damodaran's Blog, page 16

August 28, 2019

From Shareholder wealth to Stakeholder interests: CEO Capitulation or Empty Doublespeak?

Last week. the Business Roundtable, composed of the CEOs of some of America’s largest companies, put out a press release that hinted at a fundamental, perhaps revolutionary, shift in corporate focus. In the statement, the CEOs seemed to be saying that corporations should be run to protect all corporate stakeholders, defined to include customers, society and employees, rather than hew to its conventional objective of maximizing shareholder wealth. The reason that I say “seemed to” is because the document was written in CEO-speak, full of platitudes and open to interpretation. I will confess that I have a personal interest in this debate since I teach and write about corporate finance, a discipline built around shareholder wealth maximization, and valuation, which is about measuring it.

The Business Roundtable Speaks: A flawed message from a flawed messenger The Business Roundtable, tracing it history back to 1972, and restricting its membership to CEOs of major corporations, lobbies for business-friendly legislation and has a history of making statements about corporate purpose that are usually completely predictable and not very newsworthy. This year’s statement, at least on the surface, breaks with this past with its talk of stakeholder interests and rather than give you my interpretation of the statement, I will quote directly from it:

While each of our individual companies serves its own corporate purpose, we share a fundamental commitment to all of our stakeholders. We commit to: Delivering value to our customers. We will further the tradition of American companies leading the way in meeting or exceeding customer expectations. Investing in our employees. This starts with compensating them fairly and providing important benefits. It also includes supporting them through training and education that help develop new skills for a rapidly changing world. We foster diversity and inclusion, dignity and respect. Dealing fairly and ethically with our suppliers. We are dedicated to serving as good partners to the other companies, large and small, that help us meet our missions. Supporting the communities in which we work. We respect the people in our communities and protect the environment by embracing sustainable practices across our businesses. Generating long-term value for shareholders, who provide the capital that allows companies to invest, grow and innovate. We are committed to transparency and effective engagement with shareholders. The use of the word “stakeholders: and an explicit listing of how corporations should act in each of their interests has drawn extensive attention from a diverse group of individuals, each drawing its own conclusions and making its own criticisms. Critics of shareholder wealth maximization viewed this statement as vindication, an acceptance of their long-term tenet that focusing on shareholder wealth has given rise to income inequality, loss of good manufacturing jobs and societal costs. Supporters of shareholder wealth maximization considered the statement to be not only ill-advised but also a craven concession to populist forces. Cynics argued that it was more political document than restatement of purpose, smoke and noise that signified nothing. Journalists have concluded that this statement is, in fact, a fundamental restatement of corporate purpose, driven by political pressures.

While the statement was signed by 181 CEOs, including Bezos (Amazon), Tim Cook (Apple), Brian Moynihan (B of A) and Mary Barra (GM), I found it odd that Jamie Dimon, the CEO of JP Morgan Chase, was the person who was chosen to deliver the message. To give Mr. Dimon his due, he is a very good banker and has excellent political skills, a plus at the top of a money center bank, but he is definitely not someone that I would view as putting shareholder interests first. Over the last decade, Jamie Dimon has repeatedly clashed with his own stockholders, first over his decision to chair the board of directors that is supposed to oversee him and multiple times about his compensation. He has technically won these fights at annual meetings, but with some of the highest opposition among large, widely held public companies, and he has been well protected by his ineffectual and mostly rubber stamp board of directors. Jamie Dimon talking about shareholder wealth is about as believable as Madonna singing “like a virgin” or Kim Kardashian speaking about the importance of privacy.

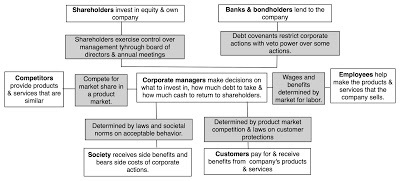

The Stakeholders in a Corporation To most laymen, the debate about whether to focus on shareholders or stakeholders may seem like an obscure one that has few consequences for their lives, but it is of huge import and the best way to get perspective is to see who these stakeholders in the modern corporation are and what their relationship is with public companies:

Stakeholders therefore have different legal relationships with the company and divergent interests, implying that actions that make one stakeholder group better off may make other stakeholder groups worse. It is this conflict that makes the discussion of which group has primacy in decision making so heated and political.

Versions of CorporatismIn the section below, I will present five different perspectives on how corporations are run, and I will let you draw your own conclusions on which one best describes current corporate behavior and argue that your that choice will determine, in large part, what you think should be the norm.

1. Cutthroat Corporatism

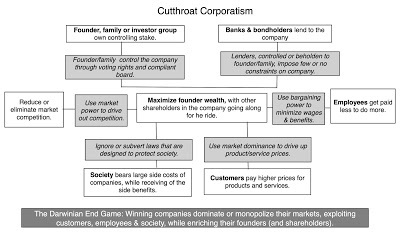

The most extreme view of corporations is what describe as cutthroat capitalism, where the strong companies drive out the weak and the end game is stockholder wealth maximization (often with a founder/family being the prime beneficiary) at almost any cost:

In the late nineteenth century, the robber barons of the age (Andrew Carnegie, John D. Rockefeller and others) hewed to this template to build some of the greatest companies of the time, some of which survive to this day. They were ruthless in their march towards domination, crushing competitors through fair means or foul, bending society to their will and exploiting customers and employees. Their overreach led to Teddy Roosevelt’s election and the subsequent passage of antitrust laws, but much as we tend to view these corporate chieftains as villains, they played a major role in making the US a global economic power. In the century since, there are other companies that have aspired for dominance, using what many critics have viewed as ruthless and perhaps even illegal ways to exercise market dominance. Lest you view this model of corporate behavior as a historical artifact, many of today's companies have, at least in some aspects of their behavior, have been accused of following this model.

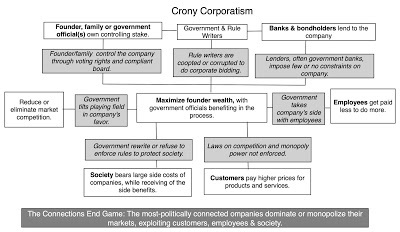

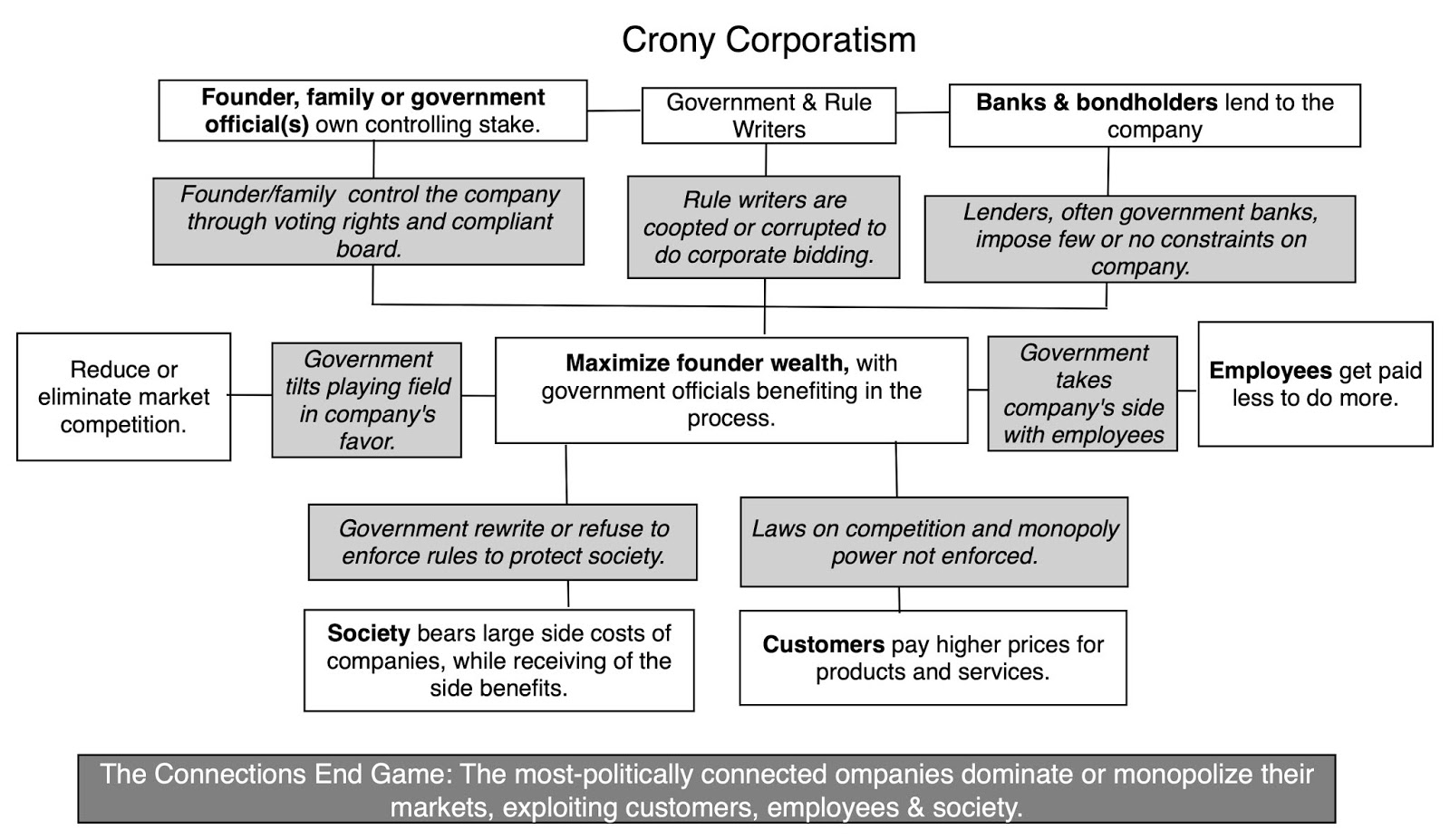

2. Crony Corporatism A variant of this win-at-all-costs corporatism is crony corporatism, where the end game is still market dominance but the base is built less on economies of scale, efficient operations and product differentiation, and more on connections to government and rule writers, with the objective being tilting the scales of competition in the company’s favor: While the end result of cutthroat and crony capitalism is the same, i.e., large market-dominating companies that give short shrift to employees and customers, it can be argued that since the winners are the most connected, not the most efficient, crony capitalism offers all of the costs of cutthroat capitalism, with none of the benefits. While family group companies in some emerging markets obviously fit this mould, I think that an argument can be made that there is an element of cronyism in many developed markets.

While the end result of cutthroat and crony capitalism is the same, i.e., large market-dominating companies that give short shrift to employees and customers, it can be argued that since the winners are the most connected, not the most efficient, crony capitalism offers all of the costs of cutthroat capitalism, with none of the benefits. While family group companies in some emerging markets obviously fit this mould, I think that an argument can be made that there is an element of cronyism in many developed markets.

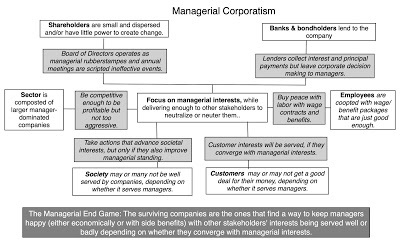

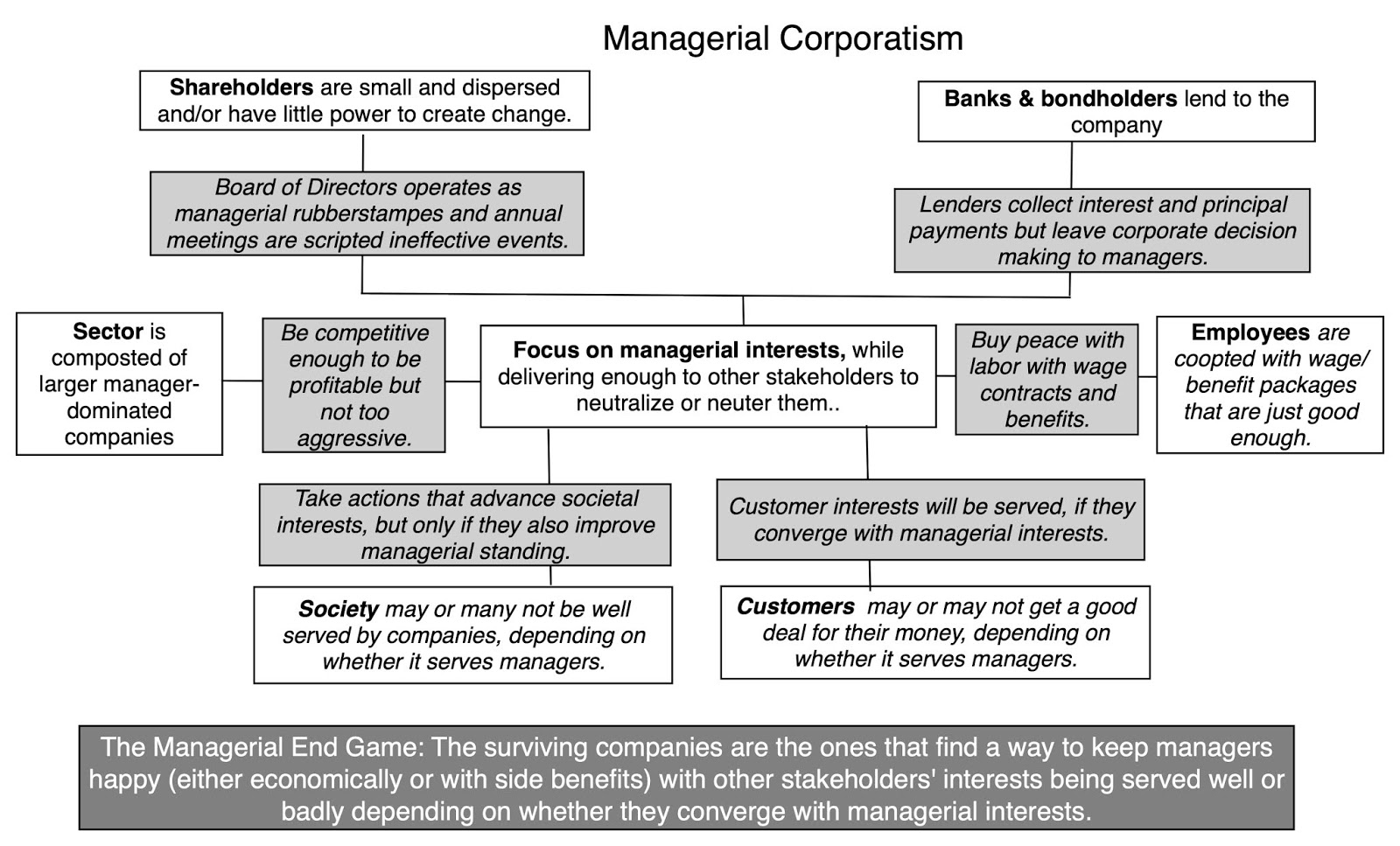

3. Managerial CorporatismThere is a third version of corporatism that comes to the forefront, especially as public companies age, founders/families are replaced with professional managers and shareholdings get dispersed among lots of shareholders with small (percent) stakes. In this version, it is the professional managers whose interests drive decision making in the company, with other stakeholders viewed as side players.

Note that the managers who make corporate decisions often own little equity in the company, or if they do, get it as part of compensation packages, often determined by boards of directors that operate less as checks and more as rubber stamps. The question of how well other stakeholders do in this version depends in large part on whether their interests converge on those of managers; if there is convergence, their interests will be advanced, but only because it happens to advance managerial interests as well, and if not, they will find themselves paying the price to make managers better off. This was the default for US companies in the decades after the second world war, with long tenures for CEOs and little or no shareholder activism, and overall economic prosperity allowing for a coopting of other stakeholder: solid wage gains for employees, corporate charity and restrained competition.

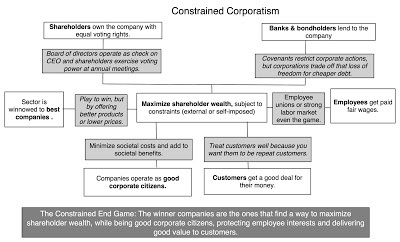

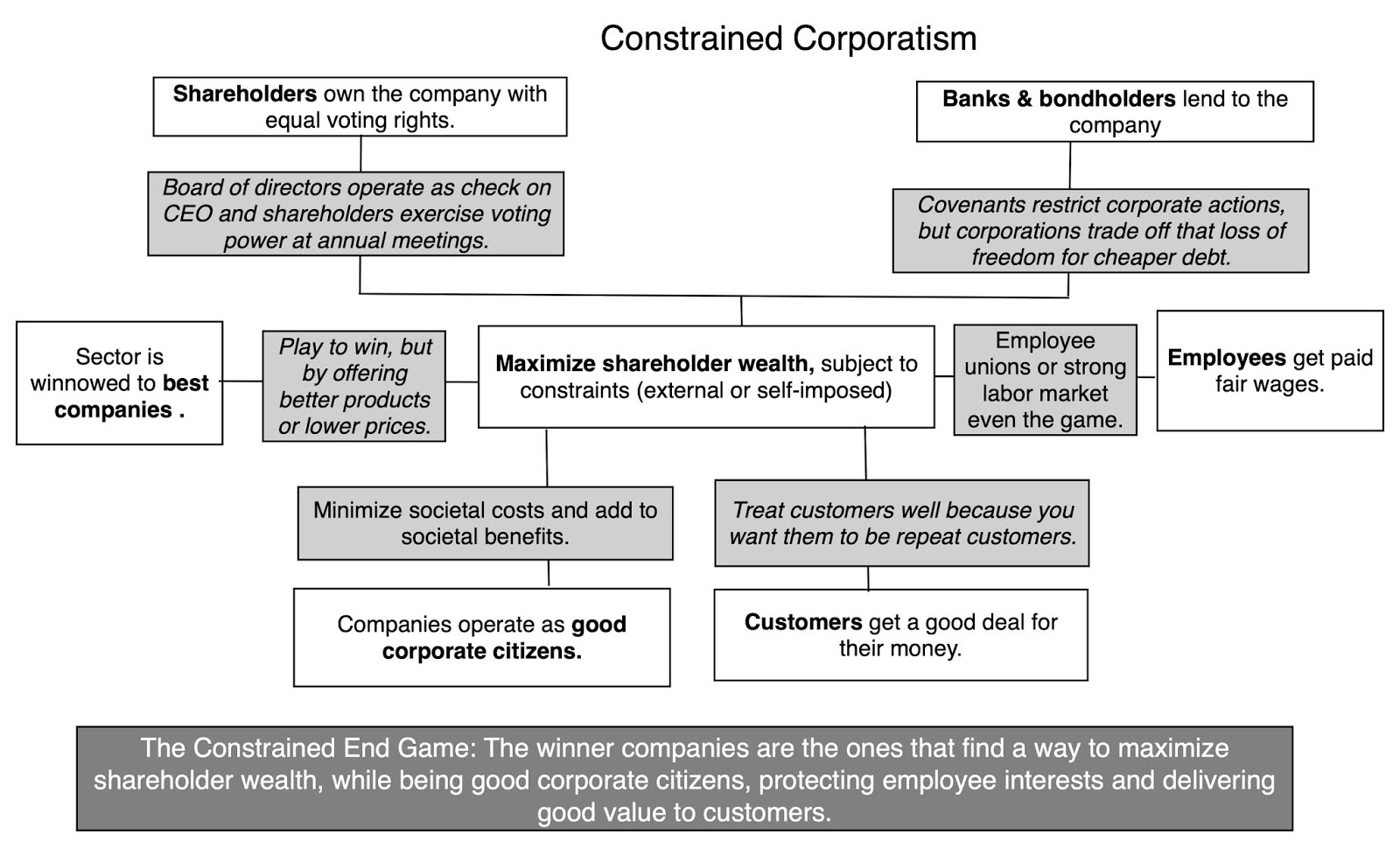

4. Constrained Corporatism I suspect that there are very few people, even among true believers in free markets and capitalism, who will defend cutthroat or crony capitalism. There are some who are nostalgic for managerial corporatism, pointing to the solid stock returns, well-paying jobs and societal side benefits that came with it, not seeing that these stakeholder benefits were made possible by US economic dominance during the period, and the ease with US companies could make money. It is no coincidence that shareholder activism rose to the surface in the 1980s, as US economic power slipped and managerial interests were served at the expense of not just shareholders, but other stakeholders. While this activism resulted in leveraged buyouts in some companies, it also gave rise to a version of shareholder wealth maximization that I center my corporate finance decision making, that I call constrained corporatism, where companies preserve the primacy of shareholders, while constraining how they interact with other stakeholder groups: The efficacy of this version of corporatism depends largely on how well the constraints protect other stakeholders and what drives companies to adopt the constraints in the first place, with three possible drivers for the latter:Government-imposed constraints: Governments can write laws or draw up rules that constrain how corporations treat stakeholders, with labor laws determining not only how much workers get paid but also conditions under which they can be hired or fired, product laws capping prices on some products and protecting customer interests in others and anti-trust laws determining whether product markets stay competitive. European governments have been far more aggressive with this approach than the US, but the globalization of businesses has not only weakened the protections offered by these laws, but also put companies covered by them at a competitive disadvantage, relative to companies that operate in countries without these laws and restrictions.Self-imposed constraints: In this variant, companies voluntarily adopt constraints on their interactions with other stakeholder groups, often choosing to pay higher wages (than they could get away paying) to their employees, charging customers less for products/services than they could have, given their pricing power, and turning away investments that they could pursue legally, for profits, because of the costs that it will create for society. In effect, the essence of these constraints is that the profit settles for less profit than it could have made if it have as an unconstrained player. The problem with self-imposed constraints is that your capacity to adopt them will be correlated with how profitable you are to begin with, with companies with more slack built into their business models being in a better position than companies facing profit pressures in an intensely competitive market. Market-driven constraints: In this final variation, companies adopt constraints on how they treat stakeholders because it makes them more valuable companies, even as they settle for less profits, at least in the near term. That seeming contradiction can be explained by two factors. The first is that whatever costs the company faces in the short term from imposing the constraints may be overwhelmed by benefits in the long term; paying employees more may yield more loyal and better employees, offering customers better deals may lead to more repeat business and being a good corporate citizen may operate as advertising, attracting more customers to the company. To top it all off, investors who care about any or all of these behaviors may be more inclined to invest in your shares, pushing up stock prices. The second is that companies that exploit customers and employees or acquire a reputation for being bad corporate citizens will have few defenders when it does make a mistake or have a problem, inevitable in the long term, leading to potentially catastrophic costs.As an advocate for shareholder wealth maximization, I would love to live in a world where the market rewarded companies that try to do the right thing, since it would make good behavior entirely consistent with value maximization. That said, I am a realist and accept that some constraints have to be imposed by governments, regulators and rule writers, and that some companies, especially ones with strong profitability and substantial slack in their business models, may accept self constraints.

The efficacy of this version of corporatism depends largely on how well the constraints protect other stakeholders and what drives companies to adopt the constraints in the first place, with three possible drivers for the latter:Government-imposed constraints: Governments can write laws or draw up rules that constrain how corporations treat stakeholders, with labor laws determining not only how much workers get paid but also conditions under which they can be hired or fired, product laws capping prices on some products and protecting customer interests in others and anti-trust laws determining whether product markets stay competitive. European governments have been far more aggressive with this approach than the US, but the globalization of businesses has not only weakened the protections offered by these laws, but also put companies covered by them at a competitive disadvantage, relative to companies that operate in countries without these laws and restrictions.Self-imposed constraints: In this variant, companies voluntarily adopt constraints on their interactions with other stakeholder groups, often choosing to pay higher wages (than they could get away paying) to their employees, charging customers less for products/services than they could have, given their pricing power, and turning away investments that they could pursue legally, for profits, because of the costs that it will create for society. In effect, the essence of these constraints is that the profit settles for less profit than it could have made if it have as an unconstrained player. The problem with self-imposed constraints is that your capacity to adopt them will be correlated with how profitable you are to begin with, with companies with more slack built into their business models being in a better position than companies facing profit pressures in an intensely competitive market. Market-driven constraints: In this final variation, companies adopt constraints on how they treat stakeholders because it makes them more valuable companies, even as they settle for less profits, at least in the near term. That seeming contradiction can be explained by two factors. The first is that whatever costs the company faces in the short term from imposing the constraints may be overwhelmed by benefits in the long term; paying employees more may yield more loyal and better employees, offering customers better deals may lead to more repeat business and being a good corporate citizen may operate as advertising, attracting more customers to the company. To top it all off, investors who care about any or all of these behaviors may be more inclined to invest in your shares, pushing up stock prices. The second is that companies that exploit customers and employees or acquire a reputation for being bad corporate citizens will have few defenders when it does make a mistake or have a problem, inevitable in the long term, leading to potentially catastrophic costs.As an advocate for shareholder wealth maximization, I would love to live in a world where the market rewarded companies that try to do the right thing, since it would make good behavior entirely consistent with value maximization. That said, I am a realist and accept that some constraints have to be imposed by governments, regulators and rule writers, and that some companies, especially ones with strong profitability and substantial slack in their business models, may accept self constraints.

5. Confused Corporatism

In some sectors and in some markets and during some time periods, markets will not do the job, leaving us as the mercy of bad behavior by some or many corporate players. It is therefore not surprising that stakeholder wealth maximization is seen as an alternative corporate model:

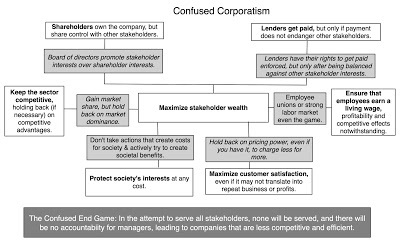

It is quite clear that the corporate mission in this version of corporatism has been enlarged to cover all stakeholders, often with very different interests at heart. On the surface, it may look like constrained capitalism, but unlike it, in this version, you have multiple objectives, with no clear sense of which one dominates. Your job as a top manager or CEO is to pay not just a fair, but a living wage, even if you cannot afford it as a company, but also deliver maximum value to your customer, preserve society’s best interests and ensure that your business stays competitive, while also making sure that you deliver the returns your stockholders and lenders desire. In my view, it is destined to fail for three reasons:Conflicting interests: By treating the interests of all stakeholders as equivalent, it ignores the reality that decisions in companies, almost by definition, will make stakeholders better off and others worse off. Since some of these costs and benefits will be not easily translated into numbers, it is not clear how managers will be able to decide what investments to take, what businesses to enter and exit, how to finance these businesses and when and how much cash to return to shareholders. No accountability: The fact that there are multiple stakeholders with conflicting interests also leaves CEOs and top managers accountable to none of them, with the excuse with any group that was ill-served during a period being that other group’s interests had to be met. Decision paralysis: If one of the problems at large companies has been the time it takes to make decisions, I will predict that expanding decision making to take into account the interests of all stakeholders will create decision paralysis, as the “on the one hand, and on the other” arguments will multiply, often with no way to resolve them, since some stakeholder interests will remain fuzzy and non-measurable.To those who believe that stakeholder wealth maximization will usher in a period of common good, with society, customers and employees benefiting from more compassionate corporatism, I offer you two cautionary counter examples. First, you may want to take a look at government-owned and run companies not just in the socialist economies but in many capitalist ones. The managers of these companies were given a laundry list of objectives, resembling in large part the listing of stakeholder objectives, and told to deliver on them all. The end results were some of the most inefficient companies on the face of the earth, with every stakeholder group feeling ill-served in the process. Second, let me use a second illustration not from the corporate sector, but s setting that I am intimately familiar with, because I have spent almost four decades of my life in it. Research universities in the United States are entities built without a central focus, where the stakeholder group being served and the objective is different, depending on who in the university administration you talk to, and when. The end result is not just economically inefficient operations, capable of running a deficit no matter how much tuition is collection, but one where every stakeholder group feels aggrieved; students feel that they pay too much in tuition and have too little say in their education, faculty believe that their rights are being chipped away by no-nothing administrators and the communities feel disrespected and cheated. If you want publicly traded companies to look like research universities in terms of economic efficiency or taking care of stakeholder group interests, confused capitalism is your answer.

Revisiting the MessageTo be fair to the CEOs, there is enough ambiguity in the Business Roundtable statement for readers to read into it whatever they want it to mean, but there are three possible interpretations:A Public Relations Move: It is undeniable that the public perception of corporations has become more negative over the last few decades, and politicians have noticed. Populists on both sides of the political divide have found that the public buys into their framing as corporations as self-interested entities that don’t care about employees, customers or society, with their focus on shareholders being the reason. CEOs have noticed, and the Business Roundtable’s statement may be just a restatement of constrained corporatism.A Return to the Past: Since the business roundtable is composed of CEOs, many of whom have felt the heat of activist investors and pushy shareholders, the cynic in you may lead you to conclude that what the CEOs in the Roundtable would like to see is a return to the good old days of managerial corporatism, where they could rule their companies with little push back, and that this push for stakeholder interests is a diversionary tactic.The Conspiratorial Twist: There is a third twist, and it does require a conspiratorial mindset. Note that the CEOs who are in the Roundtable represent the status quo, large and established companies, many of which find their business models being disrupted by young, start-ups. One way to preempt disruption is to increase the costs of doing business and having to take care of all stakeholders does that, but it is a cost that established companies may be able to bear better right now than their disruptive competitors. ( If you are skeptical, remember I said that you need a conspiratorial mindset. Conclusion I know that this is a trying time to be a corporate CEO, with people demanding that you cure society’s ills and the economy’s problems, with the threat of punitive actions, if you don’t change. That said, I don’t believe that you can win this battle or even recoup some of your lost standing by giving up on the focus on shareholder wealth and replacing it with an ill-thought through and potentially destructive objective of advancing stakeholder interests. In my view, a much healthier discussion would be centered on creating more transparency about how corporations treat different stakeholder groups and linking that information with how they get valued in the market. I think that we are making strides on the first, with better information disclosure from companies and CSR measures, and I hope to help on the second front by connecting these disclosures to intrinsic value. As I noted earlier, if we want companies to behave better in their interactions with society, customers and employees, we have to make it in their financial best interests to do so, buying products and services from companies that treat other stakeholders better and paying higher prices for their shares.

YouTube Video<!-- /* Style Definitions */ p.MsoNormal, li.MsoNormal, div.MsoNormal {mso-style-unhide:no; mso-style-qformat:yes; mso-style-parent:""; margin:0in; margin-bottom:.0001pt; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraph, li.MsoListParagraph, div.MsoListParagraph {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpFirst, li.MsoListParagraphCxSpFirst, div.MsoListParagraphCxSpFirst {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpMiddle, li.MsoListParagraphCxSpMiddle, div.MsoListParagraphCxSpMiddle {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpLast, li.MsoListParagraphCxSpLast, div.MsoListParagraphCxSpLast {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} .MsoChpDefault {mso-style-type:export-only; mso-default-props:yes; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} @page WordSection1 {size:8.5in 11.0in; margin:1.0in 1.0in 1.0in 1.0in; mso-header-margin:.5in; mso-footer-margin:.5in; mso-paper-source:0;} div.WordSection1 {page:WordSection1;} /* List Definitions */ @list l0 {mso-list-id:107892614; mso-list-type:hybrid; mso-list-template-ids:-1051446148 -136563048 67698691 67698693 67698689 67698691 67698693 67698689 67698691 67698693;} @list l0:level1 {mso-level-start-at:0; mso-level-number-format:bullet; mso-level-text:-; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:"Times New Roman",serif; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin;} @list l0:level2 {mso-level-number-format:bullet; mso-level-text:o; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:"Courier New";} @list l0:level3 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Wingdings;} @list l0:level4 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Symbol;} @list l0:level5 {mso-level-number-format:bullet; mso-level-text:o; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:"Courier New";} @list l0:level6 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Wingdings;} @list l0:level7 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Symbol;} @list l0:level8 {mso-level-number-format:bullet; mso-level-text:o; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:"Courier New";} @list l0:level9 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Wingdings;} @list l1 {mso-list-id:1225413654; mso-list-type:hybrid; mso-list-template-ids:32023186 67698703 67698713 67698715 67698703 67698713 67698715 67698703 67698713 67698715;} @list l1:level1 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level2 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level3 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l1:level4 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level5 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level6 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l1:level7 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level8 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level9 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l2 {mso-list-id:1374112990; mso-list-type:hybrid; mso-list-template-ids:1719568348 67698703 67698713 67698715 67698703 67698713 67698715 67698703 67698713 67698715;} @list l2:level1 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level2 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level3 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l2:level4 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level5 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level6 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l2:level7 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level8 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level9 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} </style></div></div></div></div>--><style class="WebKit-mso-list-quirks-style"><!-- /* Style Definitions */ p.MsoNormal, li.MsoNormal, div.MsoNormal {mso-style-unhide:no; mso-style-qformat:yes; mso-style-parent:""; margin:0in; margin-bottom:.0001pt; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraph, li.MsoListParagraph, div.MsoListParagraph {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpFirst, li.MsoListParagraphCxSpFirst, div.MsoListParagraphCxSpFirst {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpMiddle, li.MsoListParagraphCxSpMiddle, div.MsoListParagraphCxSpMiddle {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpLast, li.MsoListParagraphCxSpLast, div.MsoListParagraphCxSpLast {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} .MsoChpDefault {mso-style-type:export-only; mso-default-props:yes; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} @page WordSection1 {size:8.5in 11.0in; margin:1.0in 1.0in 1.0in 1.0in; mso-header-margin:.5in; mso-footer-margin:.5in; mso-paper-source:0;} div.WordSection1 {page:WordSection1;} /* List Definitions */ @list l0 {mso-list-id:727152184; mso-list-type:hybrid; mso-list-template-ids:88906506 67698703 67698713 67698715 67698703 67698713 67698715 67698703 67698713 67698715;} @list l0:level1 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level2 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level3 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l0:level4 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level5 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level6 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l0:level7 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level8 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level9 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} </style></div>-->

The Business Roundtable Speaks: A flawed message from a flawed messenger The Business Roundtable, tracing it history back to 1972, and restricting its membership to CEOs of major corporations, lobbies for business-friendly legislation and has a history of making statements about corporate purpose that are usually completely predictable and not very newsworthy. This year’s statement, at least on the surface, breaks with this past with its talk of stakeholder interests and rather than give you my interpretation of the statement, I will quote directly from it:

While each of our individual companies serves its own corporate purpose, we share a fundamental commitment to all of our stakeholders. We commit to: Delivering value to our customers. We will further the tradition of American companies leading the way in meeting or exceeding customer expectations. Investing in our employees. This starts with compensating them fairly and providing important benefits. It also includes supporting them through training and education that help develop new skills for a rapidly changing world. We foster diversity and inclusion, dignity and respect. Dealing fairly and ethically with our suppliers. We are dedicated to serving as good partners to the other companies, large and small, that help us meet our missions. Supporting the communities in which we work. We respect the people in our communities and protect the environment by embracing sustainable practices across our businesses. Generating long-term value for shareholders, who provide the capital that allows companies to invest, grow and innovate. We are committed to transparency and effective engagement with shareholders. The use of the word “stakeholders: and an explicit listing of how corporations should act in each of their interests has drawn extensive attention from a diverse group of individuals, each drawing its own conclusions and making its own criticisms. Critics of shareholder wealth maximization viewed this statement as vindication, an acceptance of their long-term tenet that focusing on shareholder wealth has given rise to income inequality, loss of good manufacturing jobs and societal costs. Supporters of shareholder wealth maximization considered the statement to be not only ill-advised but also a craven concession to populist forces. Cynics argued that it was more political document than restatement of purpose, smoke and noise that signified nothing. Journalists have concluded that this statement is, in fact, a fundamental restatement of corporate purpose, driven by political pressures.

While the statement was signed by 181 CEOs, including Bezos (Amazon), Tim Cook (Apple), Brian Moynihan (B of A) and Mary Barra (GM), I found it odd that Jamie Dimon, the CEO of JP Morgan Chase, was the person who was chosen to deliver the message. To give Mr. Dimon his due, he is a very good banker and has excellent political skills, a plus at the top of a money center bank, but he is definitely not someone that I would view as putting shareholder interests first. Over the last decade, Jamie Dimon has repeatedly clashed with his own stockholders, first over his decision to chair the board of directors that is supposed to oversee him and multiple times about his compensation. He has technically won these fights at annual meetings, but with some of the highest opposition among large, widely held public companies, and he has been well protected by his ineffectual and mostly rubber stamp board of directors. Jamie Dimon talking about shareholder wealth is about as believable as Madonna singing “like a virgin” or Kim Kardashian speaking about the importance of privacy.

The Stakeholders in a Corporation To most laymen, the debate about whether to focus on shareholders or stakeholders may seem like an obscure one that has few consequences for their lives, but it is of huge import and the best way to get perspective is to see who these stakeholders in the modern corporation are and what their relationship is with public companies:

Stakeholders therefore have different legal relationships with the company and divergent interests, implying that actions that make one stakeholder group better off may make other stakeholder groups worse. It is this conflict that makes the discussion of which group has primacy in decision making so heated and political.

Versions of CorporatismIn the section below, I will present five different perspectives on how corporations are run, and I will let you draw your own conclusions on which one best describes current corporate behavior and argue that your that choice will determine, in large part, what you think should be the norm.

1. Cutthroat Corporatism

The most extreme view of corporations is what describe as cutthroat capitalism, where the strong companies drive out the weak and the end game is stockholder wealth maximization (often with a founder/family being the prime beneficiary) at almost any cost:

In the late nineteenth century, the robber barons of the age (Andrew Carnegie, John D. Rockefeller and others) hewed to this template to build some of the greatest companies of the time, some of which survive to this day. They were ruthless in their march towards domination, crushing competitors through fair means or foul, bending society to their will and exploiting customers and employees. Their overreach led to Teddy Roosevelt’s election and the subsequent passage of antitrust laws, but much as we tend to view these corporate chieftains as villains, they played a major role in making the US a global economic power. In the century since, there are other companies that have aspired for dominance, using what many critics have viewed as ruthless and perhaps even illegal ways to exercise market dominance. Lest you view this model of corporate behavior as a historical artifact, many of today's companies have, at least in some aspects of their behavior, have been accused of following this model.

2. Crony Corporatism A variant of this win-at-all-costs corporatism is crony corporatism, where the end game is still market dominance but the base is built less on economies of scale, efficient operations and product differentiation, and more on connections to government and rule writers, with the objective being tilting the scales of competition in the company’s favor:

While the end result of cutthroat and crony capitalism is the same, i.e., large market-dominating companies that give short shrift to employees and customers, it can be argued that since the winners are the most connected, not the most efficient, crony capitalism offers all of the costs of cutthroat capitalism, with none of the benefits. While family group companies in some emerging markets obviously fit this mould, I think that an argument can be made that there is an element of cronyism in many developed markets.

While the end result of cutthroat and crony capitalism is the same, i.e., large market-dominating companies that give short shrift to employees and customers, it can be argued that since the winners are the most connected, not the most efficient, crony capitalism offers all of the costs of cutthroat capitalism, with none of the benefits. While family group companies in some emerging markets obviously fit this mould, I think that an argument can be made that there is an element of cronyism in many developed markets.

3. Managerial CorporatismThere is a third version of corporatism that comes to the forefront, especially as public companies age, founders/families are replaced with professional managers and shareholdings get dispersed among lots of shareholders with small (percent) stakes. In this version, it is the professional managers whose interests drive decision making in the company, with other stakeholders viewed as side players.

Note that the managers who make corporate decisions often own little equity in the company, or if they do, get it as part of compensation packages, often determined by boards of directors that operate less as checks and more as rubber stamps. The question of how well other stakeholders do in this version depends in large part on whether their interests converge on those of managers; if there is convergence, their interests will be advanced, but only because it happens to advance managerial interests as well, and if not, they will find themselves paying the price to make managers better off. This was the default for US companies in the decades after the second world war, with long tenures for CEOs and little or no shareholder activism, and overall economic prosperity allowing for a coopting of other stakeholder: solid wage gains for employees, corporate charity and restrained competition.

4. Constrained Corporatism I suspect that there are very few people, even among true believers in free markets and capitalism, who will defend cutthroat or crony capitalism. There are some who are nostalgic for managerial corporatism, pointing to the solid stock returns, well-paying jobs and societal side benefits that came with it, not seeing that these stakeholder benefits were made possible by US economic dominance during the period, and the ease with US companies could make money. It is no coincidence that shareholder activism rose to the surface in the 1980s, as US economic power slipped and managerial interests were served at the expense of not just shareholders, but other stakeholders. While this activism resulted in leveraged buyouts in some companies, it also gave rise to a version of shareholder wealth maximization that I center my corporate finance decision making, that I call constrained corporatism, where companies preserve the primacy of shareholders, while constraining how they interact with other stakeholder groups:

The efficacy of this version of corporatism depends largely on how well the constraints protect other stakeholders and what drives companies to adopt the constraints in the first place, with three possible drivers for the latter:Government-imposed constraints: Governments can write laws or draw up rules that constrain how corporations treat stakeholders, with labor laws determining not only how much workers get paid but also conditions under which they can be hired or fired, product laws capping prices on some products and protecting customer interests in others and anti-trust laws determining whether product markets stay competitive. European governments have been far more aggressive with this approach than the US, but the globalization of businesses has not only weakened the protections offered by these laws, but also put companies covered by them at a competitive disadvantage, relative to companies that operate in countries without these laws and restrictions.Self-imposed constraints: In this variant, companies voluntarily adopt constraints on their interactions with other stakeholder groups, often choosing to pay higher wages (than they could get away paying) to their employees, charging customers less for products/services than they could have, given their pricing power, and turning away investments that they could pursue legally, for profits, because of the costs that it will create for society. In effect, the essence of these constraints is that the profit settles for less profit than it could have made if it have as an unconstrained player. The problem with self-imposed constraints is that your capacity to adopt them will be correlated with how profitable you are to begin with, with companies with more slack built into their business models being in a better position than companies facing profit pressures in an intensely competitive market. Market-driven constraints: In this final variation, companies adopt constraints on how they treat stakeholders because it makes them more valuable companies, even as they settle for less profits, at least in the near term. That seeming contradiction can be explained by two factors. The first is that whatever costs the company faces in the short term from imposing the constraints may be overwhelmed by benefits in the long term; paying employees more may yield more loyal and better employees, offering customers better deals may lead to more repeat business and being a good corporate citizen may operate as advertising, attracting more customers to the company. To top it all off, investors who care about any or all of these behaviors may be more inclined to invest in your shares, pushing up stock prices. The second is that companies that exploit customers and employees or acquire a reputation for being bad corporate citizens will have few defenders when it does make a mistake or have a problem, inevitable in the long term, leading to potentially catastrophic costs.As an advocate for shareholder wealth maximization, I would love to live in a world where the market rewarded companies that try to do the right thing, since it would make good behavior entirely consistent with value maximization. That said, I am a realist and accept that some constraints have to be imposed by governments, regulators and rule writers, and that some companies, especially ones with strong profitability and substantial slack in their business models, may accept self constraints.

The efficacy of this version of corporatism depends largely on how well the constraints protect other stakeholders and what drives companies to adopt the constraints in the first place, with three possible drivers for the latter:Government-imposed constraints: Governments can write laws or draw up rules that constrain how corporations treat stakeholders, with labor laws determining not only how much workers get paid but also conditions under which they can be hired or fired, product laws capping prices on some products and protecting customer interests in others and anti-trust laws determining whether product markets stay competitive. European governments have been far more aggressive with this approach than the US, but the globalization of businesses has not only weakened the protections offered by these laws, but also put companies covered by them at a competitive disadvantage, relative to companies that operate in countries without these laws and restrictions.Self-imposed constraints: In this variant, companies voluntarily adopt constraints on their interactions with other stakeholder groups, often choosing to pay higher wages (than they could get away paying) to their employees, charging customers less for products/services than they could have, given their pricing power, and turning away investments that they could pursue legally, for profits, because of the costs that it will create for society. In effect, the essence of these constraints is that the profit settles for less profit than it could have made if it have as an unconstrained player. The problem with self-imposed constraints is that your capacity to adopt them will be correlated with how profitable you are to begin with, with companies with more slack built into their business models being in a better position than companies facing profit pressures in an intensely competitive market. Market-driven constraints: In this final variation, companies adopt constraints on how they treat stakeholders because it makes them more valuable companies, even as they settle for less profits, at least in the near term. That seeming contradiction can be explained by two factors. The first is that whatever costs the company faces in the short term from imposing the constraints may be overwhelmed by benefits in the long term; paying employees more may yield more loyal and better employees, offering customers better deals may lead to more repeat business and being a good corporate citizen may operate as advertising, attracting more customers to the company. To top it all off, investors who care about any or all of these behaviors may be more inclined to invest in your shares, pushing up stock prices. The second is that companies that exploit customers and employees or acquire a reputation for being bad corporate citizens will have few defenders when it does make a mistake or have a problem, inevitable in the long term, leading to potentially catastrophic costs.As an advocate for shareholder wealth maximization, I would love to live in a world where the market rewarded companies that try to do the right thing, since it would make good behavior entirely consistent with value maximization. That said, I am a realist and accept that some constraints have to be imposed by governments, regulators and rule writers, and that some companies, especially ones with strong profitability and substantial slack in their business models, may accept self constraints.5. Confused Corporatism

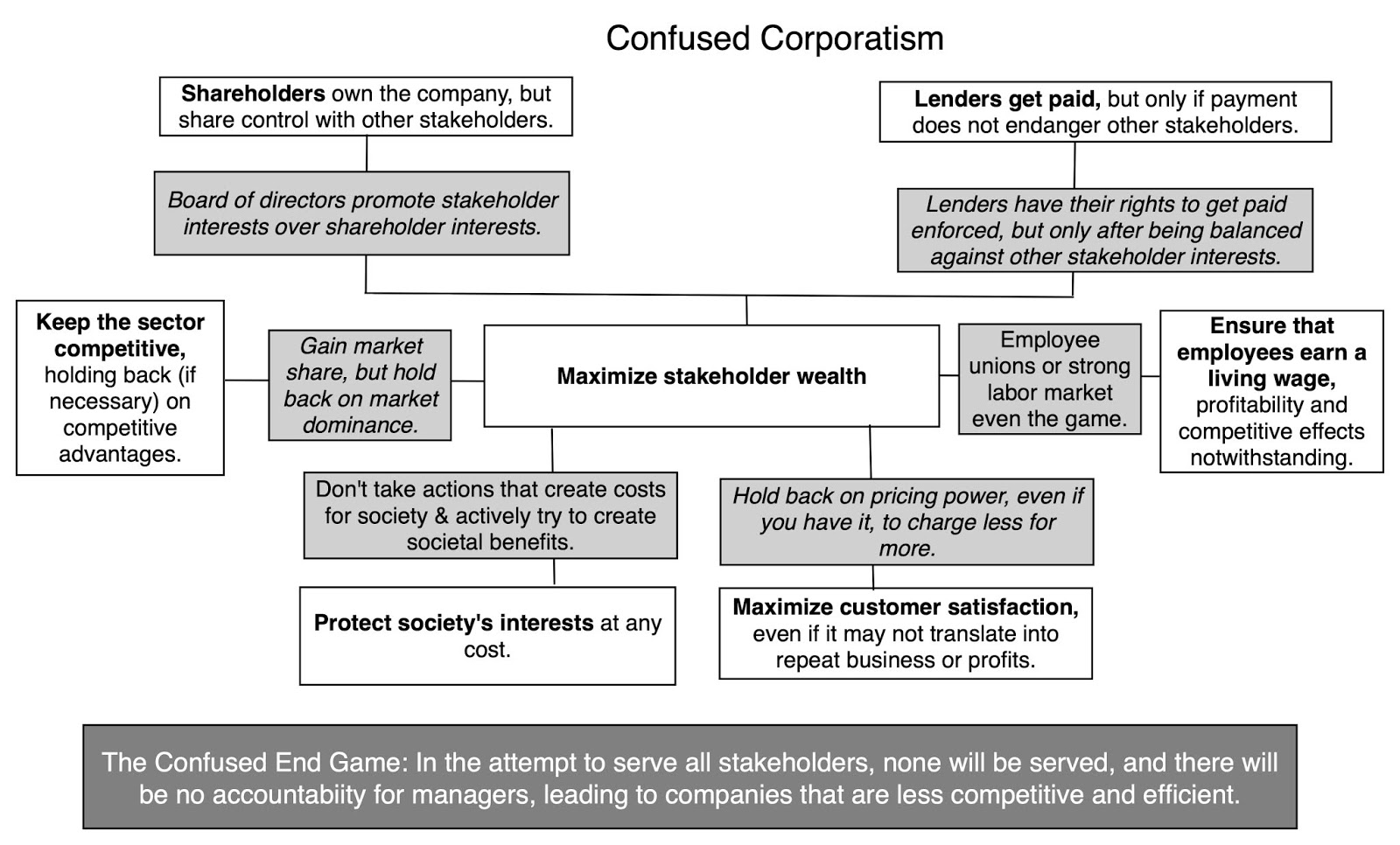

In some sectors and in some markets and during some time periods, markets will not do the job, leaving us as the mercy of bad behavior by some or many corporate players. It is therefore not surprising that stakeholder wealth maximization is seen as an alternative corporate model:

It is quite clear that the corporate mission in this version of corporatism has been enlarged to cover all stakeholders, often with very different interests at heart. On the surface, it may look like constrained capitalism, but unlike it, in this version, you have multiple objectives, with no clear sense of which one dominates. Your job as a top manager or CEO is to pay not just a fair, but a living wage, even if you cannot afford it as a company, but also deliver maximum value to your customer, preserve society’s best interests and ensure that your business stays competitive, while also making sure that you deliver the returns your stockholders and lenders desire. In my view, it is destined to fail for three reasons:Conflicting interests: By treating the interests of all stakeholders as equivalent, it ignores the reality that decisions in companies, almost by definition, will make stakeholders better off and others worse off. Since some of these costs and benefits will be not easily translated into numbers, it is not clear how managers will be able to decide what investments to take, what businesses to enter and exit, how to finance these businesses and when and how much cash to return to shareholders. No accountability: The fact that there are multiple stakeholders with conflicting interests also leaves CEOs and top managers accountable to none of them, with the excuse with any group that was ill-served during a period being that other group’s interests had to be met. Decision paralysis: If one of the problems at large companies has been the time it takes to make decisions, I will predict that expanding decision making to take into account the interests of all stakeholders will create decision paralysis, as the “on the one hand, and on the other” arguments will multiply, often with no way to resolve them, since some stakeholder interests will remain fuzzy and non-measurable.To those who believe that stakeholder wealth maximization will usher in a period of common good, with society, customers and employees benefiting from more compassionate corporatism, I offer you two cautionary counter examples. First, you may want to take a look at government-owned and run companies not just in the socialist economies but in many capitalist ones. The managers of these companies were given a laundry list of objectives, resembling in large part the listing of stakeholder objectives, and told to deliver on them all. The end results were some of the most inefficient companies on the face of the earth, with every stakeholder group feeling ill-served in the process. Second, let me use a second illustration not from the corporate sector, but s setting that I am intimately familiar with, because I have spent almost four decades of my life in it. Research universities in the United States are entities built without a central focus, where the stakeholder group being served and the objective is different, depending on who in the university administration you talk to, and when. The end result is not just economically inefficient operations, capable of running a deficit no matter how much tuition is collection, but one where every stakeholder group feels aggrieved; students feel that they pay too much in tuition and have too little say in their education, faculty believe that their rights are being chipped away by no-nothing administrators and the communities feel disrespected and cheated. If you want publicly traded companies to look like research universities in terms of economic efficiency or taking care of stakeholder group interests, confused capitalism is your answer.

Revisiting the MessageTo be fair to the CEOs, there is enough ambiguity in the Business Roundtable statement for readers to read into it whatever they want it to mean, but there are three possible interpretations:A Public Relations Move: It is undeniable that the public perception of corporations has become more negative over the last few decades, and politicians have noticed. Populists on both sides of the political divide have found that the public buys into their framing as corporations as self-interested entities that don’t care about employees, customers or society, with their focus on shareholders being the reason. CEOs have noticed, and the Business Roundtable’s statement may be just a restatement of constrained corporatism.A Return to the Past: Since the business roundtable is composed of CEOs, many of whom have felt the heat of activist investors and pushy shareholders, the cynic in you may lead you to conclude that what the CEOs in the Roundtable would like to see is a return to the good old days of managerial corporatism, where they could rule their companies with little push back, and that this push for stakeholder interests is a diversionary tactic.The Conspiratorial Twist: There is a third twist, and it does require a conspiratorial mindset. Note that the CEOs who are in the Roundtable represent the status quo, large and established companies, many of which find their business models being disrupted by young, start-ups. One way to preempt disruption is to increase the costs of doing business and having to take care of all stakeholders does that, but it is a cost that established companies may be able to bear better right now than their disruptive competitors. ( If you are skeptical, remember I said that you need a conspiratorial mindset. Conclusion I know that this is a trying time to be a corporate CEO, with people demanding that you cure society’s ills and the economy’s problems, with the threat of punitive actions, if you don’t change. That said, I don’t believe that you can win this battle or even recoup some of your lost standing by giving up on the focus on shareholder wealth and replacing it with an ill-thought through and potentially destructive objective of advancing stakeholder interests. In my view, a much healthier discussion would be centered on creating more transparency about how corporations treat different stakeholder groups and linking that information with how they get valued in the market. I think that we are making strides on the first, with better information disclosure from companies and CSR measures, and I hope to help on the second front by connecting these disclosures to intrinsic value. As I noted earlier, if we want companies to behave better in their interactions with society, customers and employees, we have to make it in their financial best interests to do so, buying products and services from companies that treat other stakeholders better and paying higher prices for their shares.

YouTube Video<!-- /* Style Definitions */ p.MsoNormal, li.MsoNormal, div.MsoNormal {mso-style-unhide:no; mso-style-qformat:yes; mso-style-parent:""; margin:0in; margin-bottom:.0001pt; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraph, li.MsoListParagraph, div.MsoListParagraph {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpFirst, li.MsoListParagraphCxSpFirst, div.MsoListParagraphCxSpFirst {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpMiddle, li.MsoListParagraphCxSpMiddle, div.MsoListParagraphCxSpMiddle {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpLast, li.MsoListParagraphCxSpLast, div.MsoListParagraphCxSpLast {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} .MsoChpDefault {mso-style-type:export-only; mso-default-props:yes; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} @page WordSection1 {size:8.5in 11.0in; margin:1.0in 1.0in 1.0in 1.0in; mso-header-margin:.5in; mso-footer-margin:.5in; mso-paper-source:0;} div.WordSection1 {page:WordSection1;} /* List Definitions */ @list l0 {mso-list-id:107892614; mso-list-type:hybrid; mso-list-template-ids:-1051446148 -136563048 67698691 67698693 67698689 67698691 67698693 67698689 67698691 67698693;} @list l0:level1 {mso-level-start-at:0; mso-level-number-format:bullet; mso-level-text:-; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:"Times New Roman",serif; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin;} @list l0:level2 {mso-level-number-format:bullet; mso-level-text:o; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:"Courier New";} @list l0:level3 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Wingdings;} @list l0:level4 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Symbol;} @list l0:level5 {mso-level-number-format:bullet; mso-level-text:o; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:"Courier New";} @list l0:level6 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Wingdings;} @list l0:level7 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Symbol;} @list l0:level8 {mso-level-number-format:bullet; mso-level-text:o; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:"Courier New";} @list l0:level9 {mso-level-number-format:bullet; mso-level-text:; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in; font-family:Wingdings;} @list l1 {mso-list-id:1225413654; mso-list-type:hybrid; mso-list-template-ids:32023186 67698703 67698713 67698715 67698703 67698713 67698715 67698703 67698713 67698715;} @list l1:level1 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level2 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level3 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l1:level4 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level5 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level6 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l1:level7 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level8 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l1:level9 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l2 {mso-list-id:1374112990; mso-list-type:hybrid; mso-list-template-ids:1719568348 67698703 67698713 67698715 67698703 67698713 67698715 67698703 67698713 67698715;} @list l2:level1 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level2 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level3 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l2:level4 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level5 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level6 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l2:level7 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level8 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l2:level9 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} </style></div></div></div></div>--><style class="WebKit-mso-list-quirks-style"><!-- /* Style Definitions */ p.MsoNormal, li.MsoNormal, div.MsoNormal {mso-style-unhide:no; mso-style-qformat:yes; mso-style-parent:""; margin:0in; margin-bottom:.0001pt; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraph, li.MsoListParagraph, div.MsoListParagraph {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpFirst, li.MsoListParagraphCxSpFirst, div.MsoListParagraphCxSpFirst {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpMiddle, li.MsoListParagraphCxSpMiddle, div.MsoListParagraphCxSpMiddle {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} p.MsoListParagraphCxSpLast, li.MsoListParagraphCxSpLast, div.MsoListParagraphCxSpLast {mso-style-priority:34; mso-style-unhide:no; mso-style-qformat:yes; mso-style-type:export-only; margin-top:0in; margin-right:0in; margin-bottom:0in; margin-left:.5in; margin-bottom:.0001pt; mso-add-space:auto; mso-pagination:widow-orphan; font-size:12.0pt; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} .MsoChpDefault {mso-style-type:export-only; mso-default-props:yes; font-family:"Calibri",sans-serif; mso-ascii-font-family:Calibri; mso-ascii-theme-font:minor-latin; mso-fareast-font-family:Calibri; mso-fareast-theme-font:minor-latin; mso-hansi-font-family:Calibri; mso-hansi-theme-font:minor-latin; mso-bidi-font-family:"Times New Roman"; mso-bidi-theme-font:minor-bidi;} @page WordSection1 {size:8.5in 11.0in; margin:1.0in 1.0in 1.0in 1.0in; mso-header-margin:.5in; mso-footer-margin:.5in; mso-paper-source:0;} div.WordSection1 {page:WordSection1;} /* List Definitions */ @list l0 {mso-list-id:727152184; mso-list-type:hybrid; mso-list-template-ids:88906506 67698703 67698713 67698715 67698703 67698713 67698715 67698703 67698713 67698715;} @list l0:level1 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level2 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level3 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l0:level4 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level5 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level6 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} @list l0:level7 {mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level8 {mso-level-number-format:alpha-lower; mso-level-tab-stop:none; mso-level-number-position:left; text-indent:-.25in;} @list l0:level9 {mso-level-number-format:roman-lower; mso-level-tab-stop:none; mso-level-number-position:right; text-indent:-9.0pt;} </style></div>-->

August 13, 2019

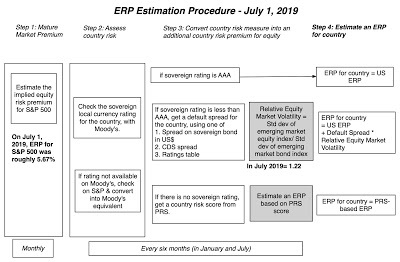

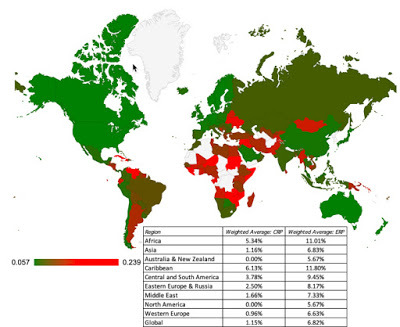

Country Risk: A Mid-year 2019 Update

One of the consequences of globalization is that investors, analysts and companies can no longer stay focused on just their domestic markets, but have to also understand the risks and opportunities elsewhere in the world. When developed market companies first embarked on the journey of expanding into emerging market growth economies, investors pushed up their stock prices, primarily because of the potential that they saw in these markets for expansion. Over time, though, we have learned that, as with much else in business, this strategy comes with additional risk, not just from changing exchange rates, but from unstable economic and political forces. This growth/risk trade off explains why some companies have gained from value from globalizing and others have lost. In this post, I look at country risk through many lens, but with the end game of being able to incorporate it into decision making both for investors and businesses.

The Sources of Country Risk

When companies invest outside their domestic markets, the most immediate risk that they are exposed to is exchange rate risk, since revenues, profits and cash flows are affected by changing exchange rates. That risk, though, is but a piece of the puzzle, a symptom of economic fundamentals and affected by political crises. Digging deeper, the factors that make some countries riskier than others can be broadly classified into the following groups:

1. Life Cycle: I have used the construct of a corporate life cycle to talk about companies at different stages in the life cycle, and how they differ on cash flow generation and growth potential. It is also generally true that younger companies, deriving more or most of their value from future growth, are riskier than more mature companies, where the bulk of their value coming from investments already made. The same construct can be applied to countries, with emerging economies that are growing rapidly being more exposed to global shocks than mature countries. It should come as no surprise, therefore, that in almost every market crisis over the last decade, emerging markets have paid a much large price in terms of lost economic growth and lower market value than developed markets.

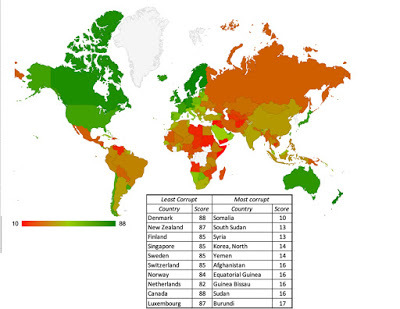

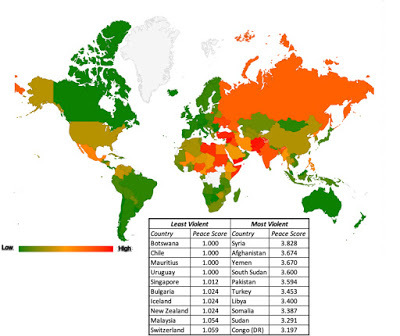

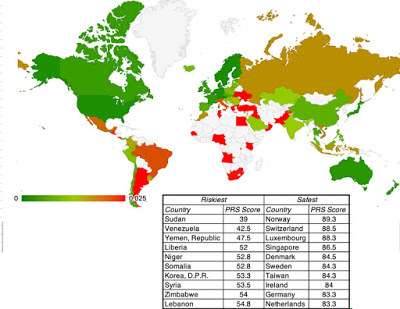

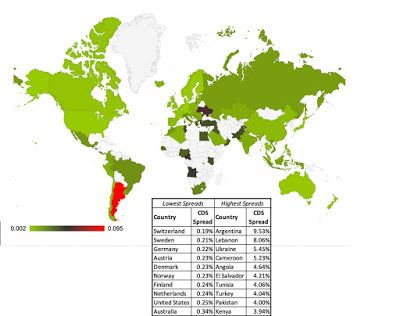

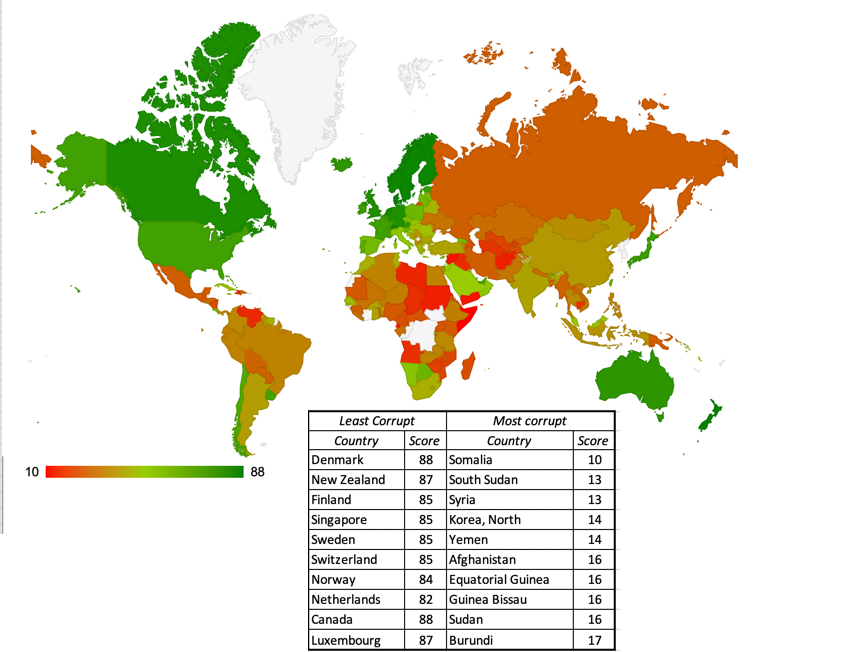

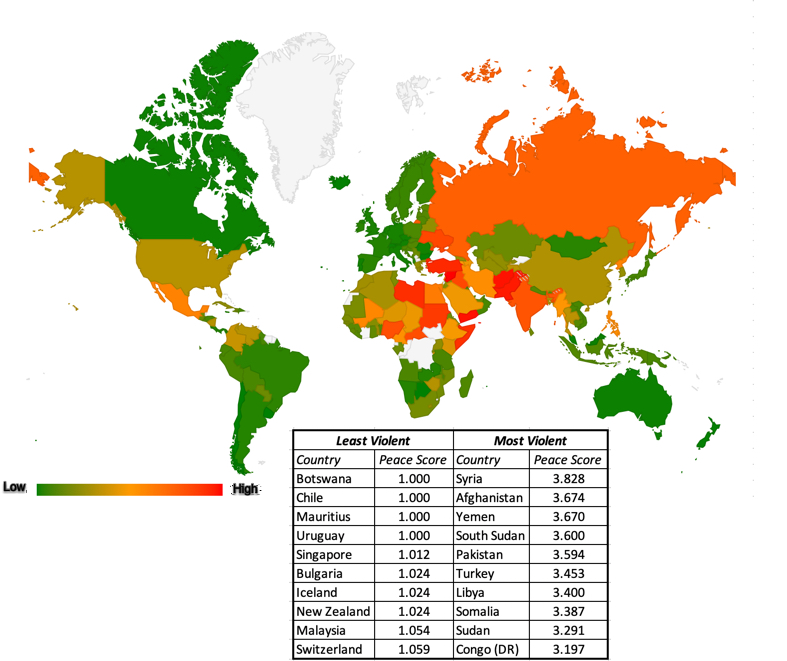

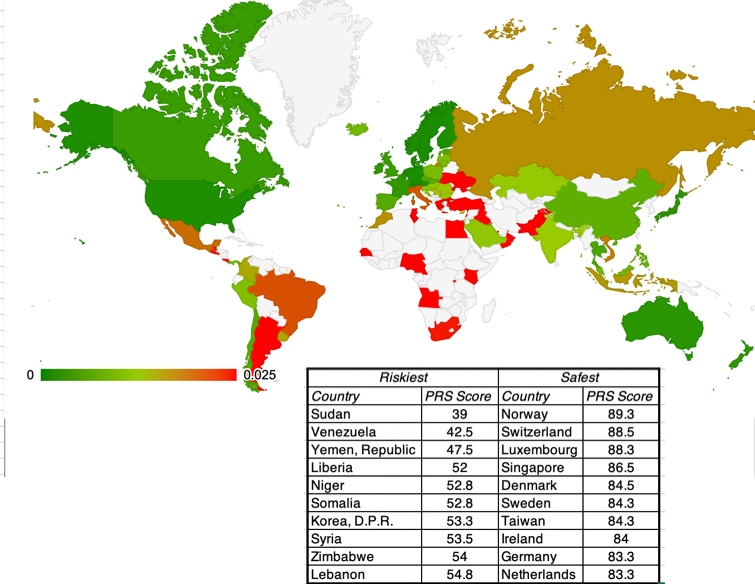

2. Political Risk: If the last few years have taught us a lesson, it is that politics can affect economic and market risk, not just in emerging markets, but also in developed ones. While there are many forms of political risk, ranging from abrupt changes in fiscal and monetary policy to regime change, there are at least two measurable manifestations of this risk in the form of corruption risk and exposure to violence.Corruption Risk: There are parts of the world where the costs of doing business include greasing palms and paying off intermediaries, and the roots lie deep, resisting feel-good quick fixes. While anecdotal stories of corruption and its consequences are plentiful, there are services to try to measure corruption levels across countries. Transparency International, for instance, derives a corruption score, by country, and in its 2019 report, provides a listing of the ten least and most corrupt countries in the world in the figure below, with higher scores indicating less corruption) for 2018. Source: Transparency InternationalThe effect of corruption upon business is insidious, making winners of those most willing to play the bribery game and losers of those who resist. In an earlier post, I argued that corruption creates the equivalent of an informal tax, pushing down after-tax income to companies.Physical Violence: When talking about risk in investing or business, we tend to focus on financial risk, but it is undeniable that adding the threat of physical violence, from war, terrorism or crime, makes it more difficult to operate a business. There are services again that measure exposure to violence in different countries, and while each brings its own biases, the Institute of Economics and Peace has created and reports on a Global Peace Index, measuring exposure to violence, by country.

Source: Transparency InternationalThe effect of corruption upon business is insidious, making winners of those most willing to play the bribery game and losers of those who resist. In an earlier post, I argued that corruption creates the equivalent of an informal tax, pushing down after-tax income to companies.Physical Violence: When talking about risk in investing or business, we tend to focus on financial risk, but it is undeniable that adding the threat of physical violence, from war, terrorism or crime, makes it more difficult to operate a business. There are services again that measure exposure to violence in different countries, and while each brings its own biases, the Institute of Economics and Peace has created and reports on a Global Peace Index, measuring exposure to violence, by country.