Adam Tooze's Blog, page 20

April 30, 2022

Ones & Tooze Bonus: Why is May Day so Violent in Berlin?

This wonderful, nearly ten minute tangent did not quite make its way into our latest episode. But we thought many of you would appreciate Cameron and Adam’s Berliner discussion. So here’s that whole segment as a bonus May Day special.

Find more episodes and subscribe at Foreign Policy

April 29, 2022

Ones & Tooze: How The Labor Movement Got Its Day

In this episode of Cameron and Adam look ahead to the upcoming May Day celebration and discuss the roots of this holiday as well as the current state of the labor movement. In the second segment they talk about the economic impact of the massive outpouring of refugees from Ukraine both for Ukraine and for the host countries receiving Ukrainians.

Find more episodes and subscribe at Foreign Policy

April 27, 2022

Chartbook #117: Nazi billionaires

Source: Harper Collins

Journalist and historian David de Jong started work at Bloomberg just shortly after Zucotti park was violently cleared of protestors, on the orders of Mike Bloomberg, his new boss. As he describes it:

In the wake of the previous years’ financial crisis, the tension between the 1 percent and the 99 percent was palpable around the globe. Though I was hired to cover American business dynasties such as the Kochs and the Waltons (who control Walmart), I was soon asked to add the German-speaking nations to my beat …

This provides the rather striking opening to his highly readable study of ultra wealthy German families – the Quandts, the Flicks, the von Fincks, the Porsche-Piëchs and the Oetkers – and their entanglement with Hitler’s National Socialist regime.

The Nazi regime and business has been studied again and again. There were the muckraking (in the historical sense of the term) investigations that accompanied the Nuremberg trials.

Then there were the hard fought battles of the Cold War. The work of Marxisant business historians in West Germany regularly appeared with passages inked out by the order of the courts. In the US in the 1980s David Abraham, Henry Ashby Turner, Gerald Feldman et al did bloody battle over the responsibility of German business for Hitler’s rise to power. Out of that conflict emerged the first generation of new business histories led by Peter Hayes’s highly influential study of IG Farben. In the 1990s the new focus on the Holocaust and forced labour litigation triggered a further wave of studies. In some cases there were commissioned by the firms themselves. In other cases they were the work of independent academics.

There is not enough space to do justice to this huge literature in a single newsletter. I will return to it.

Though he draws on all these earlier studies, de Jong’s book is as a history of German business in the Nazi era that reflects the preoccupations of the years since 2008, the Occupy movement, and the discourse of the 1 v. 99 percent. It is, if you like, a post-Piketty history of Nazi Germany.

The families at the heart of de Jong’s book were not necessarily the most influential business people in the Nazi regime. He isn’t talking about the CEOs of IG Farben, or Rheinmetall or Krupp. His selection is dictated by two criteria – closeness to the Nazi regime in political and personal terms – and prominence and wealth in the postwar period.

The Quandt’s tick both boxes most emphatically. As owners of BMW – though that is not how their money was made – they are amongst the wealthiest people in the world. The current generation are descendants of Magda Goebbels who killed herself and all but one of her children in the Führer bunker in 1945. Magda’s first husband, Günther Quandt (1881-1954) to whom they owe their name, was a major supplier of arms, ammunition and batteries to the Nazi war effort and a gigantic employer of forced labour.

Friedrich Flick was an early sponsor of the Nazi movement and Germany’s wealthiest man twice over. His son Friedrich Karl Flick recalcitrantly denied any wrong-doing on his family’s behalf and frittered away their fortune. So that the youngest members of the family are perhaps worth a mere 1.8 billion euros each.

The von Finck family, which straddle Bavaria, Austria and Switzerland, were founders of the twin titans of Allianz Insurance and Munich Re. They supplied Hitler’s regime with an Economics Minister, helped build Hitler’s art collections and profited handsomely from the Aryanization of Rothschild assets in Vienna. Their parsimony has ensured that they have stayed in the top ranks of German billionaires down to the present day.

Rudolf-August Oetker the founder of Oetker’s dramatic postwar growth was a volunteer in the Waffen-SS officer who eagerly enrolled in training courses at Dachau concentration camp. When he died in 2014 he left his 8 children from three marriages with a brand name known throughout Germany – for baking goods – and equal shares of a fortune worth $12 billion at the time.

The Porsche-Piëchs built Hitler’s Volkswagen – a factory to rival that of Ford. As de Jong shows they not only took advantages of the Nazi seizure of power to boot out their Jewish business partner Adolf Rosenberger, but have systematically written him out of history ever since.

Though many of these stories are well known, de Jong assembles a compelling and horrifying group portrait. And his points of emphasis are thought-provoking.

Of late the literature has tended to focus on forced labour, slave labour, contacts between business and the SS. De Jong’s families were involved in that.But, tellingly, de Jong starts not in the 1940s but in 1933.

On Monday, February 20, 1933, at 6 p.m., about two dozen of Nazi Germany’s wealthiest and most influential businessmen arrived, on foot or by chauffeured car, to attend a meeting at the official residence of the Reichstag president, Hermann Göring, in the heart of Berlin’s government and business district. The attendees included Günther Quandt, a textile producer turned arms-and-battery tycoon; Friedrich Flick, a steel magnate; Baron August von Finck, a Bavarian finance mogul; Kurt Schmitt, CEO of the insurance behemoth Allianz; executives from the chemicals conglomerate IG Farben and the potash giant Wintershall; and Gustav Krupp von Bohlen und Halbach, chairman-through-marriage of the Krupp steel empire.

The purpose of that meeting was not to sell big business on anti-semitism, Hitler’s plans for world conquest, or the Holocaust. Hitler’s regime as we now know it was not up for for debate. The purpose of the meeting was to raise money with which to end German democracy.

“Private enterprise cannot be maintained in the age of democracy,” the forty-three-year-old chancellor said. “It is conceivable only if the people have a sound idea of authority and personality. Everything positive, good and valuable, which has been achieved in the world in the field of economics and culture, is solely attributable to the importance of personality.”

What Hitler and his movement needed was money with which to win the election of March 5 1933. It was to be a decisive vote.

“the last election,” according to Hitler. One way or another, democracy would fall. Germany’s new chancellor intended to dissolve it entirely and replace it with a dictatorship. “Regardless of the outcome,” he warned, “there would be no retreat . . . There are only two possibilities, either to crowd back the opponent on constitutional grounds . . . or a struggle will be conducted with other weapons, which may demand greater sacrifices.” If the election didn’t bring Hitler’s party into control, a civil war between the right and the left would certainly erupt, he intimated. Hitler waxed poetic: “I hope the German people recognize the greatness of the hour. It shall decide the next ten or probably even hundred years.”

What Hitler, Goering and Schacht had in mind was a fund equivalent to $20 million in today’s money with which to win the election and end Germany democracy. They had no problem raising the funds.

The day after the meeting, February 21, 1933, thirty-five-year-old Joseph Goebbels, who led the Nazi propaganda machine from Berlin as the capital’s Gauleiter (regional leader), wrote in his diary: “Göring brings the joyful news that 3 million is available for the election. Great thing! I immediately alert the whole propaganda department. And one hour later, the machines rattle. Now we will turn on an election campaign . . . Today the work is fun. The money is there.” Goebbels had started this very diary entry the day before, describing the depressed mood at his Berlin headquarters because of the lack of funds. What a difference twenty-four hours could make.

If the choice was between consolidating Hitler’s or continuing the Weimar Republic, by 1933 the German business community knew which way it would swing.

This had not always been their choice. In the 1920s they had learned to live with the Weimar Republic and its Western-facing foreign policy. But after ten years of what they regarded as intolerable instability, with the Communist Party surging, the economy in deep crisis and little prospect of a return to the international economic order of the 1920s, they made their choice.

They were not the only ones. As I argued in Deluge, faced with the collapse of Anglo-American hegemony in the Great Depression, Italian and Japanese elites also swung to a nationalist course.

They got more than they had bargained for. German business was not without influence at the technical level in the Third Reich. In technical and industrial terms they shaped what was possible. Some who were considered untrustworthy or insufficiently enthusiastic were bullied or even lost control of their businesses. But that was far from being the majority experience. For the most part the trade offs offered by the Nazi regime were extremely attractive. There is much more to say about this but businesses profited handsomely. But any illusion they might have had that they were backing a conservative nationalist government in which figures like the publisher Alfred Hugenberg or the military high command would call the shots were soon dispelled. They had embarked on a dramatic va banque adventure dominated by Hitler’s vision of racial war.

De Jong does a skillful job of interweaving family history with the drama and violence that began in 1938 with the Anschluss of Austria and continued down to the stabilization of the 1950s.

Defeat was a shock but it did not end the prosperity of this cluster of families. All of them survived the war. Their fortunes were if not intact, then at least the basis for regrowth. And this is the bigger point to highlight about de Jong’s account. It is a story of continuity, a story of relentless accumulation across some of the most massive caesura in modern history.

To that extent it runs counter to one of the findings commonly taken away from the inequality studies of recent years, that war was one of the very few forces that disrupts entrenched wealth inequality. This is the headline, for instance, of Walter Scheidel’s The Great Leveler: Violence and the History of Inequality from the Stone Age to the Twenty-First Century.

Does the emphasis on continuity in a study like de Jong’s contradict that basic idea?

Of course, one might take refuge in the fact that de Jong’s study is not an exercise in quantitative history. It is to be regretted that it does not include a quantitative tracking of the fortunes of his subjects.

By starting with the families whose wealth continued to accumulate he has built in survivorship bias. We don’t learn about the wealthy Germans – if there were any such persons – whose fortunes were destroyed by the war and the subsequent division of Germany. It was clearly bad for the landowners of East Prussia.

Focusing on the billionaires with Nazi connections gives us a distorted impression of wealth in Germany today. In the list of the top 30 German fortunes today, the Quandts and the von Fincks are flanked by families like the Herz’s who made their fortune in coffee after the war, or the Albrechts who are heirs to the Aldi retail fortune. The 2021 top 30 billionaire list for Germany is here and as far as I can see Nazi-related fortunes make up a small minority of the group.

But, survive the Quandts and the von Fincks did. And before dismissing them as flukes it is interesting to consider some other possible implications of de Jong’s history.

To start with, what do the German data tell us about the impact of World War II on wealth and income inequality in that country? What kind of shock did the Nazi regime, the war and postwar division deliver to wealth in general?

We owe the best estimates on this score to the recent work by N. H. Albers, Charlotte Bartels and Moritz Schularick in their 2020 paper The Distribution of Wealth in Germany, 1895-2018

As a baseline they use Prussian data, which yield this fascinating breakdown of wealth in Prussia before World War I.

Tracking the wealth share of the top one percent shows it falling monotonously from just before World War I through to the 1970s.

The data are patchy but what is striking is not so much the impact of the wars as such, but the Great Depression of the 1930s and postwar fiscal measures, notably the Lastenausgleich (Burden Equalization) legislation passed in West Germany in 1952, building on Weimar and Nazi-era precedents.

According to the careful estimates by Albers et al, postwar wealth taxes in West Germany had twice the impact on the top 1 % share as did the destruction of property predominantly owned by the wealthy during the war.

These are fascinating data and the postwar wealth tax legislation of West Germany are a topic to return to.

But relating these data to de Jong’s narrative still poses problems. In relying on large statistical aggregates to measure the wealth distribution are we actually able to capture the history of the largest fortunes? When we say that wars tend to redistribute wealth, whose wealth is it that gets redistributed? Is it the wealth of the ultra-ultra-rich or merely that of the very rich? The 0.0001% or the 1%? It would be fascinating to know whether the records of the Lastenausgleich tax allow one to throw light on these questions.

In the mean time there is at least one study that does dig into the top 1 percent income share.

Fabien Dell of INSEE and Paris-Jourdan calculates top 1 percent and top 0.01 percent shares for German and Swiss incomes.

The income data broadly follow the story of declining inequality shown by the wealth data. But in the income data we see a major recovery of the share of the top 1 percent during the period of the Nazi regime between 1933 and 1940.

And this is even more pronounced in the data for the top 0.01 percent. Their share doubles between the Weimar Republic and the outbreak of World War II. And what is also striking is how robust the top 0.01 share of national income remains after 1945. In 2000, on Dell’s data, it is still comfortably above the levels measured for the Weimar Republic.

Income and wealth inequality are two different things. But as Dell points out, the incomes of those in the top 1 percent are heavily driven by capital income. So his data strongly confirm the supposition that the Nazi regime was very good for Germany’s wealthy class.

On closer inspection, in short, the appearance of contradiction between the aggregative view of inequality trends and the importance of war shocks and de Jong’s case study approach dissolves. Indeed, the two views seem to complement each other.

World War I, the revolution, hyperinflation, Weimar democracy and the great depression delivered a nasty shock to German wealth, which shows up clearly in a break in the income and wealth inequality data. To guard against any further erosion at the hands of democracy, the wealthy placed a bet on Hitler and between 1933 and 1940 Hitler’s regime delivered handsomely on the bargain. War damage was severe, but not devastating. There was plenty of opportunity for plunder in the occupied territories and, in the event that Germany had won, the most prominent collaborators of the regime would not doubt have been rewarded even more amply. It was a high risk gamble but not an unfathomable one. I explore the politics of the moment of maximum risk in 1939-1940 at length in Wages of Destruction. Defeat was a shock, but not, in the end, a disaster. West Germany delivered capitalist democratic stability anchored safely within the US orbit. That was a deal that German elites had been willing to accept in the 1920s under far more precarious circumstances. The price of postwar stability was some redistribution to stabilize a society crowded with refugees, homeless and displaced persons. That shifted wealth shares. But what might have been a dramatic moment for wholesale redistribution by way of a 50 percent flat rate levy on all wealth assessed in 1948, was instead commuted into a manageable tax. As Albers et al put it succinctly:

Instead of paying the full amount in 1952 (due in Lastenausgleich tax), households and companies (that had done well out of the war) made quarterly amortization payments including interest until 1979. The combined annual payment amounted to 4-6% of the total initial amount of 1948, depending on the asset type (Albers, 1989, p. 288). Put differently, the main levy thus corresponded to an annual wealth tax of 2-3% on the initially assessed net wealth in 1948. This implied that it could be paid from the returns of private wealth rather than its substance

This confirms the most fundamental point conveyed by in-depth narratives like de Jong’s. Continuity achieved by all means necessary.

De Jong alerts us to the structures of ownership and influence which perdure even if the book value of assets is written down, a family member or two falls out of favor for a while, or business is bad for a few years. Wealth and privilege persist – or perhaps we should better say they are produced and reproduced – through their anchoring in law and through networks of social contacts and relationships of trust and kinship.

They also persist through crafting self-protective narratives that legitimize and defend wealth. This is where history and, in particular, business histories come in. It can serve as legitimizing device for wealth, or as a powerful check and source of accountability.

De Jong’s book, as much as anything, is an intervention in the discourses that surround modern German wealth and its history. As he himself acknowledges it is not the most scholarly or archival study of German business and the Nazi regime. There are plenty of those, nowadays even commissioned by the businesses themselves, for the sake of transparency, of course. But, they remain untranslated and veiled in scholarly apparatus. They tend non-accidentally to disappear from view. The result is a culture of apparent transparency but de facto ignorance or even denial.

The challenge as de Jong reminds us is to reactualize this history. To continually find new ways to bring it into the present. The result is a fresh and highly readable account. But for me it is less the novel framing of de Jong’s story that I admire than the fact that he has taken up this Sisyphean labour of rolling the heavy boulder of history up the hill again.

April 24, 2022

Chartbook #116: The end of crypto’s “Wild West”? The battle to shape the future of digital assets in US-UK-EU.

Bitcoin has no reason to exist. It delivers no meaningful benefit for society. It is a form of gambling, propelled by naked greed and generating vast quantities of CO2 emissions.

This was the uncompromising and hostile position towards crypto taken on behalf of the ECB by Executive Board member Fabio Panetta in December 2021, a campaign which Panetta continues today.

I am looking forward very much to being in conversation with Panetta and my colleague Jan Svejnar tomorrow. Join us at the link below:

Looking forward to discussion “For a Few Cryptos More: The Wild West of Decentralized Finance” with Fabio Panetta, Member of the ECB Executive Board, Jan Svejnar, and Adam Tooze on April 25 at 1:00 pm (EDT). RSVP for livestream at https://t.co/XABdsRZQtL pic.twitter.com/xvnYAH3Zzn

— European Institute (@ColumbiaEurope) April 20, 2022

Panetta’s stance is the hard edge of what amounts to a global push to regulate the crypto currency business, a push which has gathered significant pace in recent months.

China has taken the lead by going a long way towards banning both the use of crypto as a means of payment and bitcoin mining. Egypt, Morocco, Algeria, Bolivia, Bangladesh and Nepal have followed China’s lead.

Countries that have restricted the ability of banks to deal with crypto-assets or prohibited their use for payment transactions include Nigeria, Namibia, Colombia, Ecuador, Saudi Arabia, Jordan, Turkey, Iran, Indonesia, Vietnam and Russia.

In the financial centers of the West, in EU, UK and US, regulators, politicians and lobbyists are jostling to decide what will be the rules of the game.

It seems that we have reached a turning point in the development of the industry. For many this is the end of the “Wild West” phase of crypto’s development. This may mean some restriction of commercial and technical freedom. Will that mean the beginning of the end? The withering away of a speculative bubble? Or will it have the effect of establishing crypto as a recognized part of the financial ecosystem?

What is forcing the debate is the scale of crypto’s growth.

As recently as 2019 the global Financial Stability Board took a look at the crypto industry and judged that it posed no serious risk. Weeks later Facebook launched its bid to establish a global currency – libra. That got regulators’ attention. It turned out it was important and the regulators did not like what they saw. Faced with a wall of official hostility, at the start of 2022 Facebook finally abandoned the project.

Libra failed, but today, whether for better or for worse there is a growing sense that the crypto industry as a whole – tokens like bitcoin and tether and the exchanges that service them – is too big and dynamic to ignore. Accounting for the size of the business is tricky. But according to the White House the market capitalization of cryptocurrencies was in the order of $3tn in November 2021, up from $14bn five years ago. 16 per cent of American adults have bought, used or traded cryptocurrencies.

This gives the industry significant commercial and political weight, enabling its lobbyists to claim that the crypto industry will be an important source of competitiveness and growth.

If China is shutting down, what kind of regime will emerge in the historic hub of North Atlantic finance between Wall Street the City of London and Europe?

In the US, SEC Chair Gary Gensler is, like Panetta, a critic of bitcoin. As WSJ reports. He has let it be known that he

doesn’t see much long-term viability for cryptocurrencies… Mr. Gensler likened the thousands of cryptocurrencies in existence to the so-called wildcat banking era that took hold in the U.S. from 1837 until 1863 in the absence of federal bank regulation. “I don’t think there’s long-term viability for five or six thousand private forms of money,” Mr. Gensler said … So in the meantime I think it’s worthwhile to have an investor-protection regime placed around this.”

Gensler has demanded that crypto trading and lending platforms should register with the SEC since otherwise they risk being found responsible for offering unregistered securities in violation of federal law.

Last September, the SEC put Coinbase – a cryptocurrency exchange with a market capitalisation of $41bn – on notice that it would be sued if Coinbase went ahead with plans to launch a new digital asset lending product. Coinbase soon abandoned hte idea.

In other measures, the SEC posted a new guideline recommending that crypto exchanges record the digital assets of customers on their balance sheets as assets and liabilities. Crypto companies must also disclose the “nature and amount of crypto assets” they are holding for customers.

Gensler is amongst the most important voices warning of the false promise of stability offered by so-called stablecoins like Tether. The two largest stablecoins, Tether and USD Coin, are now worth a combined $133bn. They have attracted increased scrutiny from regulators because it is unclear whether they can really offer the backing in dollars and Treasuries that they promise to their clientele. Were that clientele to lose confidence it would not simply inflict losses, as would be the case with bitcoin. In the case of stable coins it would unleash a chain reaction akin to a bank run. Unlike bitcoin, which has no “backing” other than its scarcity and is close to being a pure speculative asset, the promise of asset-backing makes stable coins into an extension of the shadow banking system.

Gensler is not alone in expressing concerns.

“Tether is a financial Chernobyl waiting to happen,” says one former US financial regulator. “It should never have been allowed to grow so big unchecked.”

As reported by the WSJ:

Acting Comptroller of the Currency Michael Hsu said … the crypto industry is on a path that resembles that of credit derivatives ahead of the 2008 financial crisis. He expressed doubt that cryptocurrency is achieving its goal of promoting financial inclusion and criticized crypto instruments that promise steady yields to investors for failing to explain how those returns are generated. “I have seen one fool’s gold rush from up close in the lead-up to the 2008 financial crisis,” Mr. Hsu said in remarks to the Blockchain Association, a crypto lobbying group. “It feels like we may be on the cusp of another with cryptocurrencies and decentralized finance.”

To attempt to claw back some measure of regulatory power, the SEC is expanding the meaning of “securities dealer” as it tries to set stricter accounting standards for crypto exchanges.

But in making this regulatory push, Gensler and his colleagues face an increasingly vociferous and bipartisan lobby.

So far this has been most effective at the state level. El Salvador gets all the headlines for its adoption of bitcoin as legal tender, but Colorado is set to become the first US state where you can pay taxes in bitcoin, which is tantamount to the same thing. Florida is bidding to become America’s crypto capital.

And in Congress as well, as this important FT report spells out, the “crypto caucus” has increasing influence.

A bipartisan mix of libertarians, business champions and tech utopians is uniting on legislation to help the sector grow.

They want to define clear boundaries to what a security is and what a broker is so as to ensure that regulators like Gensler cannot engage in “rulemaking by enforcement”.

as regulators such as Gensler try to apply existing investment rules to an entirely new type of asset, there is a growing sense in Congress that elected representatives must step in to clarify what is legal and what is not. The defenders of the industry are now coalescing around several pieces of crypto legislation that would help define what kind of an asset digital coins are, and what responsibilities their issuers and traders have to consumers and within the market.

The battle over the future status of crypto in the US was opened in earnest by the Executive Order issued on March 9 2022, by the White House on the “Responsible Development of Digital Assets”.

On the face of it this was “incremental”, containing instructions for government agencies to examine the industry and report back. The issues to be assessed include the familiar issues of “crypto concern” – financial stability, consumer protection, money laundering, sanctions-busting, equitable access, climate risks etc.. Indeed, the Executive Order could be taken as carte blanche for a major regulatory push.

But, in fact, it delighted crypto lobbyists. And with good reasons. What matters above all are the opening lines of the executive order:

Digital assets, including cryptocurrencies, have seen explosive growth in recent years, …. Surveys suggest that around 16 percent of adult Americans – approximately 40 million people – have invested in, traded, or used cryptocurrencies … The rise in digital assets creates an opportunity to reinforce American leadership in the global financial system and at the technological frontier, but also has substantial implications for consumer protection, financial stability, national security, and climate risk. The United States must maintain technological leadership in this rapidly growing space, supporting innovation while mitigating the risks for consumers, businesses, the broader financial system, and the climate. And, it must play a leading role in international engagement and global governance of digital assets consistent with democratic values and U.S. global competitiveness.

The vital point is that the Executive Order takes the scale and growth of the crypto industry as a given. Rather than putting the future of the business in question it asserts that America must maintain leadership in this space. This is the language that the crypto caucus is desperate to hear.

“The EO was incredibly important in that it talked about US leadership in this area,” says Ari Redbord, head of government affairs at TRM Labs, which uses blockchain to investigate crypto fraud. “We may be moving away from this position of saying we have to ban cryptocurrency, thinking maybe we need to lead in this space.”

The immediate impact of the Executive Order was to unleash a relief rally in bitcoin in the days that followed.

In the rhetoric of their advocates, digital assets are being aligned with the history of the internet itself. We are at a moment, we are told, analogous to that legendary moment in the 1990s when the Clinton administration set the parameters that defined the world wide web and America’s dominance in the platform business. Whether this makes sense or not, and it surely a gross exaggeration, such analogies serve to generate political momentum. As the FT reports in gushing tones:

If members can find agreement, this could prove to be as seminal a moment as the mid-1990s, when members of Congress passed legislation that was to set the rules of the road for the internet. Legislation such as the 1996 Communications Decency Act, for example, provided the legal framework, which allowed the likes of Google, Amazon and Facebook to conquer the world. Supporters of cryptocurrencies believe US companies could similarly come to dominate the world of digital assets, but only if they have clear rules under which to grow. “We are in a similar moment with cryptocurrencies to the one we were in 30 years ago in the early days of the internet,” says Wyden (Senator for Oregon).

Not coincidentally, at the same time as the Clinton administration was defining the legal parameters of the internet boom, it was also unleashing a wave of financial deregulation, which contributed to the growth of market-based finance and the crash of 2008. The congruence between neoliberal tech and financial deregulation in the 1990s is far too rarely noted. To highlight it, is one of the important contributions of Gary Gerstle’s new history of neoliberalism.

This has about it the hallmarks of an all-American story. But one of the motivations for action is foreign competition which supposedly threatens American’s leadership.

Likewise, in the 1990s one of the driving forces behind the deregulation of Wall Street was competition between New York and the City of London. It was the sprawling trans-Atlantic operations of American and European banks that defined the direction of financial modernization to which national regulation needed to bow.

Unsurprisingly, in 2022, on the other side of the Atlantic the debate about crypto in the UK is following a similar trajectory to that in the US.

The United Kingdom is far and away the leading driver of crypto activity in European finance. And stable coins are far more dominant in Europe than in the US.

As in the United states, in the UK there is a divergence between on the one hand officials within the Bank of England and regulators who regularly express concern about crypto risks and, on the other hand, a political lobby that adopts a more growth-centered approach.

The Bank of England has roundly declared that bitcoin could become worthless.

The Bank of England’s Prudential Regulation Authority is increasing its staff and its budget to deal with crypto risks. Its funding comes from a levy raised on the financial industry itself.

As in the US, the Financial Conduct Authority wants companies offering crypto products and services to apply for registration. So far over 100 firms have applied but only a minority have been granted licenses conditional on strict anti money laundering rules.

As in the United States, in the UK the main focus of attention is on stable coins.

The UK Treasury also released long-awaited plans to regulate issuers of stablecoins — crypto tokens intended to mirror the value of other assets such as US dollars. One of the Treasury’s proposals is to adapt existing laws that govern electronic money, such as funds stored on mobile phone apps, to cover stablecoins, bringing them under the purview of the Financial Conduct Authority. This would require stablecoin issuers to hold equal reserves of pounds sterling for the tokens issued, which could not be used for purposes such as lending. The moves on crypto policy follow clashes between the industry and the FCA around its licensing regime for money laundering controls, which some industry participants have said was pushing firms to move overseas.

On the other hand, under pressure from heavy lobbying, the UK government has loudly declares that it wants to see London develop into a crypto hub.

The UK Treasury recently made headlines when it asked the Royal Mint, the agency responsible for creating British currency, to mint an NFT.

“We want this country to be a global hub — the very best place in the world to start and scale crypto companies,” City Minister John Glen said. “If there is one message I want you to leave here today with, it is that the UK is open for business, open for crypto businesses.”

As the FT reported:

We see enormous potential in crypto,” Glen said. “We aren’t going to lower our standards, but we are going to sustain our technological neutral approach.” The minister added that the government would study the possibility of issuing government debt using distributed ledger technology.

Compared to the US, the crypto business is far less developed in the EU, but the regulatory debate actually began earlier and in a more systematic way. As this useful ING report summarizes the state of play as of the end of March 2022:

The European Commission launched its proposal for a Markets in Crypto Assets Regulation (MiCAR) back in September 2020. The European Parliament’s Economic and Monetary Affairs Committee adopted MiCAR with amendments on 14 March, and the regulation will now move to discussions among the European Commission, Parliament and Ministers of Finance (the so-called “trilogue”). Once they converge, MiCAR can be established. Of course at that point supervisors will need time to prepare the new regulatory regime and draft technical standards, explaining how they will interpret and apply concepts in MiCARs. Based on the European Council’s MiCAR draft, provisions on stablecoins would start to apply in early 2024, while other provisions would apply in early 2025.

The regulatory system started with a preoccupation with money laundering. It has now expanded to address issues of consumer protection and financial market stability. Once more stable coins are at the center of the discussion since it is the promises of stable value that they make to their users that pose the stability risks.

It is not certain how far the European regulations will actually apply to bitcoin, for the basic reason that regulations apply to the legal entity responsible for issuing digital assets and in the case of bitcoin and other decentralized financial networks there is no entity that meets that definition.

The entire logic of crypto assets is that ownership is verified not by a single institution but by algorithmic consensus. Not only is that legally vague. It is also computationally expensive. And on both scores bitcoin ran into difficulty in Europe.

In fact, in March of 2022 the main concern of the crypto lobby was that the European parliament would issue a de facto ban of bitcoin by outlawing the immensely energy intensive practice of bitcoin mining.

On March 14 2022, a crucial European Parliament committed debated a motion put by the Greens and Social Democrats to phase out “proof of work” protocols in the EU. But they did not find the votes to pass the ban. Led by Stefan Berger the conservative MEP serving as rapporteur a more permissive wording carried day. Rather than banning energy intensive algorithms, the parliament resolved to reward more energy efficient systems, like Ethereum by including them in the notorious EU taxonomy of “green” business practices. MEPs ask the Commission to present MEPs with a legislative proposal to include in the EU taxonomy (a classification system) for sustainable activities.

Berger insists that by shunting crypto regulation into the dog-fight that is the EU’s green taxonomy the issue stays alive. That was not the view taken by other members of the comittee.

“We are disappointed that the rapporteur did not keep his word, breached previous broadly accepted agreements and gave up, given external pressures, to defend the interests of a part of the crypto industry,” Green MEP Ernest Urtasun said in an emailed statement.

In any case, in light of energy costs in the EU it is hard to imagine that it will become the base for large-scale mining activity.

Rather than regulating energy use, what the EU’s new regulations require for crypto exchanges is a disclosure of those buying and selling digital assets. Crypto firms such as exchanges would have to obtain, hold, and submit information on those involved in transfers.

The industry has protested that this will stifle the industry. “This regulation harms crypto innovation without a commensurate anti-money laundering benefit,” Cameron Winklevoss, co-founder and president of Gemini, said in a statement emailed to Protocol. Coinbase CEO Brian Armstrong blasted the proposal as “anti-innovation, anti-privacy, and anti-law enforcement.” Coinbase Chief Policy Officer Faryar Shirzad warned it could mean recording and reporting transactions through self-hosted wallets “even if there is no reason to suspect wrongdoing.”

Stefan Berger (EPP, DE), the lead MEP and by no means an enemy of fintech, robustly defended the compromise:

“By adopting the MiCA report, the European Parliament has paved the way for an innovation-friendly crypto-regulation that can set standards worldwide. The regulation being created is pioneering in terms of innovation, consumer protection, legal certainty and the establishment of reliable supervisory structures in the field of crypto-assets. Many countries around the world will now take a close look at MiCA.”

The vote by the parliament is just the first step in a protracted process of European negotiation over new legislation. The fight with the crypto lobby has only begun. Aa one industry representative remarked. “There hasn’t been strong enough or coordinated efforts across our industry in Europe.” That is likely to change.

And this means that the next stage in the European regulatory push is crucial. As Panetta has noted from the ECB side,

“Europe is leading the way in bringing crypto-assets into the regulatory purview. The finalisation of the Regulation of Markets in Crypto-Assets (MiCA) will harmonise the regulatory approach across the European Union (EU). In a similar way, the European Commission’s legislative proposals to create an EU AML/CFT single rulebook will bring all crypto-asset service providers within the scope of the relevant EU framework, which will also provide the basis for a harmonised European approach to supervising them. Most importantly, the proposed Regulation on information accompanying transfers of funds and certain crypto-assets (FCTR) will ensure that crypto asset transfers that include at least one cryptoasset service provider can be traced just like traditional funds transfers and that suspicious transactions can be blocked.”

But what is crucial is that swift negotiations between the European Commission, European Parliament and the Council of the European Union, build the regulatory momentum. And Europe’s regulatory measures need to ensure that they are not hamstrung by conventional legal categories and extend to crypto-asset activities that are undertaken without service providers and on a peer-to-peer basis.

****

If this is a moment of regulatory sea change for the crypto industry there are striking parallels in timing between the US, UK and Europe. That is not a matter of coincidence. Their financial systems are closely knit together and their regulators exist in a close communication and rivalry.

Figures like Panetta and Gensler agree on the need to bring an end to the Wild West epoch of crypto. To do that, it is clearly essential to adopt a coordinated approach through bodies like the Financial Action Task Force, which lays out global guidelines on issues like money laundering.

But in the push for a common approach, they will also have to contend with the fact that they are operating within political and institutional settings with strikingly different colorations.

The Executive Order by the Biden Presidency frankly declares its national goal of maintaining American national leadership, understood as a matter of national advantage and in line with Washington’s power to impose financial sanctions.

The UK is bidding to attract global business to the City of London as a financial hub.

The EU parliament starts from the premise that its job is to create a defensible regulatory structure and hopes that the effect will be to set a global standard. It is counting, in short, on what Anu Bradford has dubbed “Brussels effect”, through which the EU’s regulatory power gains leverage on a global scale.

If there is one issue that spans all three major financial hubs as a matter of common concerns it is financial stability. The coming period will be a revealing test of whether that is sufficient to achieve anything like a unified approach. In any case, the struggle to define the place of crypto in the global financial system – whether as a speculative aberration or a permanent feature – has well and truly begun.

****

I love putting out Chartbook. I am particularly pleased that it goes out for free to thousands of subscribers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options:

April 22, 2022

Chartbook #115: The Marshall Plan Revisited

The damage being done to the Ukrainian economy every day by the Russian attack is mounting up at a dizzying pace. The bill, simply in terms of physical destruction, is likely in excess of $100 billion and counting.

Perhaps unsurprisingly this has triggered calls for a Marshall Plan for Ukraine.

I took up the theme in a new piece for New Statesman.

Having had Alan Milward as a Phd supervisor at the LSE and having taught the Marshall Plan for more than a decade at Cambridge, it was a return to old intellectual haunts.

If you fancy reading just one, short thing on the Marshall Plan make it the fantastic essay by David Reynolds in Foreign Affairs from 1997. This piece is Reynolds at his brilliant best. I defy anyone to pack more narrative and crucial detail into 15 pages.

As Reynolds observes, part of the problem of writing the history of the Marshall Plan is that propagandistic hype was an integral part of the plan and contributed materially to its political effectiveness. The legend is part of the project. Nevertheless,

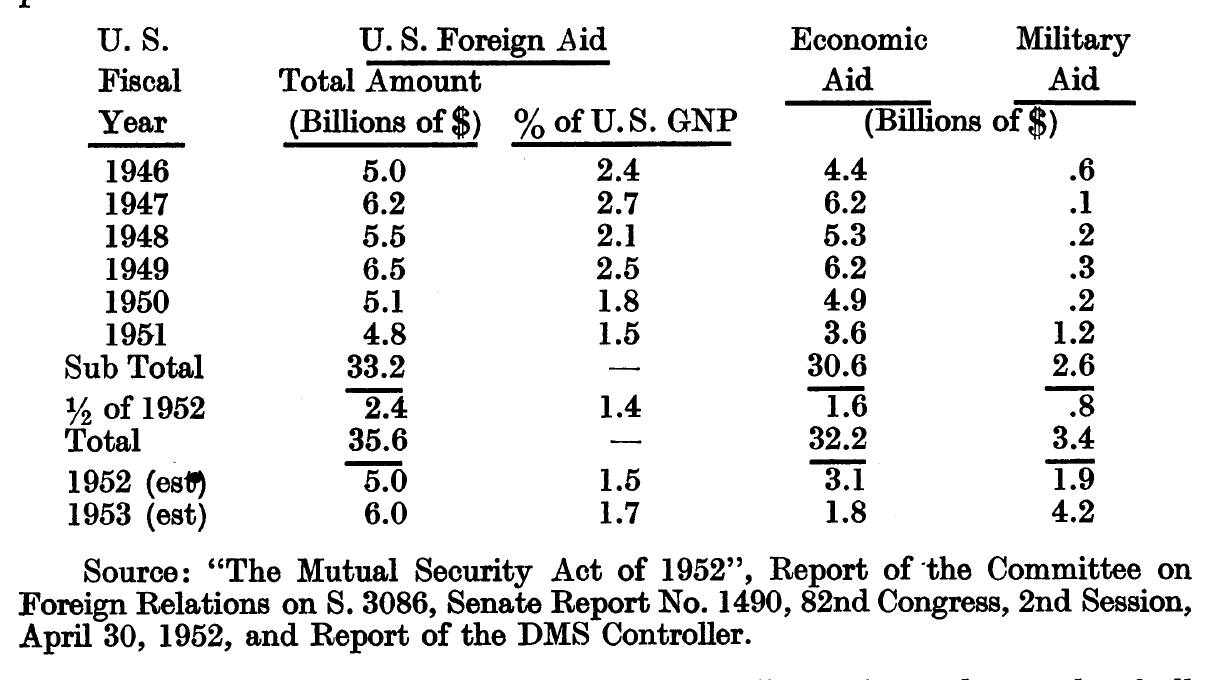

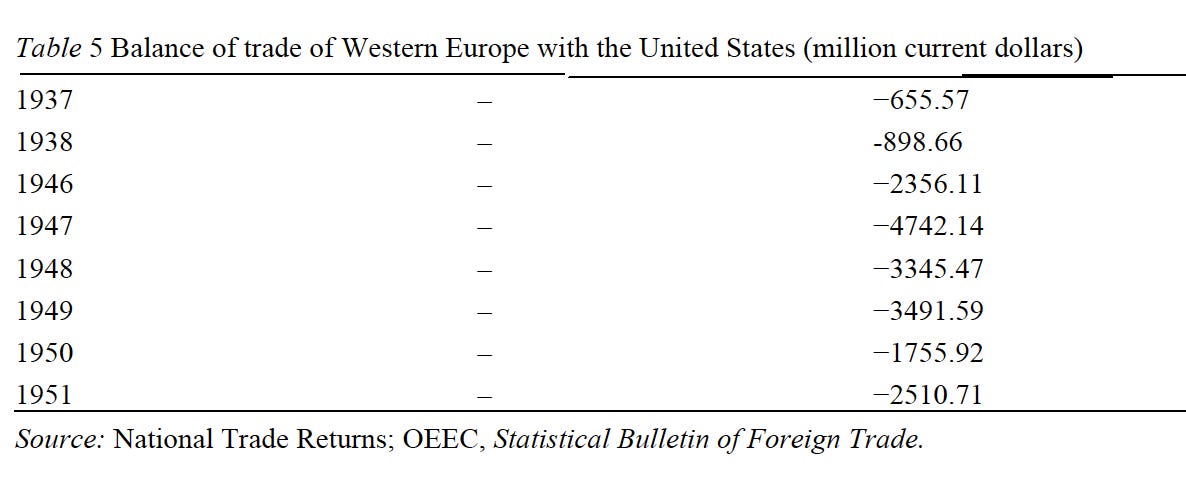

amid the fuzzy figures and revisionist rollback a clear contrast stands out. Between 1948 and 1951, the United States pumped about $13 billion into Western Europe. Between 1948 and Stalin’s death in 1953, the Soviet Union extracted some $14 billion from Eastern Europe.18 These statistics are crude but telling. They deserve a place in any history of postwar Europe

Indeed, by focusing on the $13 billion that can be attributed immediately to the Marshall Plan, we understate the scale of American financial engagement after 1945. Relief and financial assistance was delivered in many forms both before and after the Marshall Plan.

Source: Josef Berolzheimer in the FinanzArchiv 1953/54

As this table makes clear, if we take in view the overall flow of American aid to the rest of the world, the years of Marshall Plan disbursement do not particularly stand out. Already in 1946-7 the US was making large bilateral loans and supporting UN relief efforts. What made the Marshall Plan so different was the effort to craft a general program for longer-term economic rehabilitation and to do so on a coordinated European basis, rather than simply to compile national shopping lists.

Berolzheimer’s article, from which the data are taken, is a real find. As a note explains, Berolzheimer was a

staff member of the Mutual Security Agency. … He wishes to express his gratitude to Dr. Gerhard Colm, National Planning Association, for the review of the manuscript and valuable suggestions, and to Miss Anita E. Yale, MSA, for her assistance in preparing the statistical material.

The acknowledgement of Colm and the title of the essay – “The Impact of U.S. Foreign Aid Since the Marshall Plan on Western Europe’s Gross National Product and Government Finances” – are telling. The Marshall Plan was, amongst other things, a classic expression of the new era of macroeconomic governance and it was evaluated in those terms.

As Berolzheimer notes:

To measure the effect of United States foreign aid, the change of the gross national product may be the best available yardstick.

Any economist today is likely to agree with using gnp as a yardstick. The cautious way that Berolzheimer stated the point is telling. In the early 1950s, the conventional framework of macroeconomic analysis could not yet be taken for granted.

If one applied the metric of GDP, what was obvious, already at the time, was that many claims on behalf of the Marshall Plan were, likely, exaggerated. In relation to the national income of the recipient countries, the Marshall Plan was large but not overwhelming.

This was the basis for the revisionist critique of Marshall Plan hype delivered by Alan Milward in his famous book the The Reconstruction of Western Europe 1945-1951.

Published in 1984 Reconstruction remains, almost forty years later, by far the most heavy-weight economic assessment of the Plan. As Milward sought to establish, the Marshall Plan was not necessary to Europe’s recovery.

As Milward explained in a critique of Michael J. Hogan’s work, The Marshall Plan: America, Britain, and the Reconstruction of Western Europe, 1947-1952. New York: Cambridge University Press, 1987.

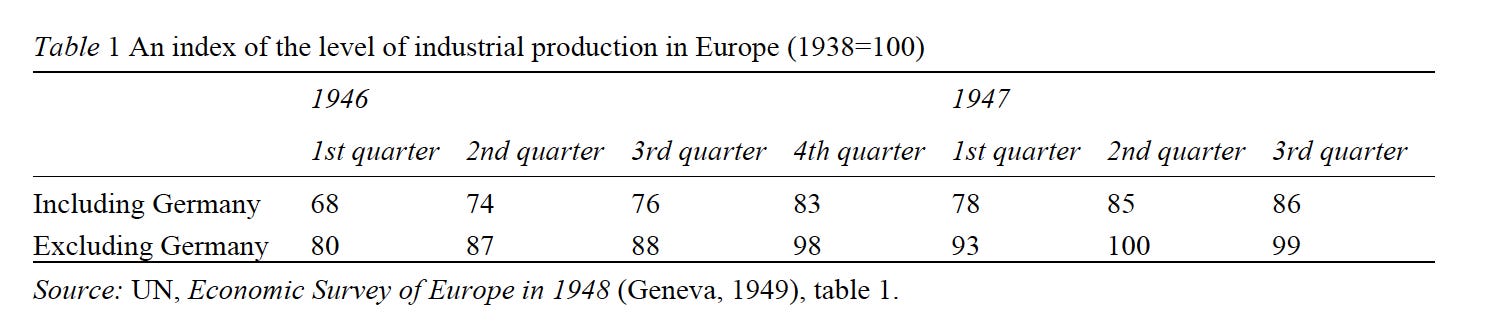

The official view, still loudly shouted by official American agencies throughout 1987 in a round of commemorative conferences in West European capitals and echoed in a blandly conformist radio program by the BBC, was that the Marshall Plan had “saved” Europe. Beneath this public conformity, however, the discussion had begun about whether the official line was true and from what, if anything, Europe had been “saved.” My own work argued that the alleged economic crisis of the summer of 1947 in Western Europe did not exist, except as a shortage of foreign exchange caused by the vigor of the European investment and production boom.”

The boom that Milward is talking about is depicted in these indices for European industrial production before the arrival of the Marshall Plan.

Source: Milward, The Reconstruction

The result of this strong burst of growth was a dollar shortage driven by Europe’s hunger for imports from the dollar zone and its lack of exports.

Source: Milward, The Reconstruction

It was these deficits that were covered by American aid.

But was that aid essential to support reconstruction? To test this proposition Milward conducted a counterfactual exercise in which he imagined levels of food consumption and food import in Europe being frozen at their 1947 levels. According to his estimates, assuming this level of austerity, all the Marshall Plan recipients excepting France and the Netherlands would have been able to pay for their imports of machinery and raw materials. On that basis Milward declares the Marshall Plan not to have been economically necessary.

But, as Milward himself concludes, all this means is that we have to shift the argument from strictly economic concerns, to the terrain of political economy. Not freezing the level of consumption at the diminished level of 1947 was precisely the point. Imposing such austerity in Italy would, given the strength of the Italian Communist Party, have been very dangerous. And as even Milward must concede the Marshall Plan really did matter in France. It could not have realized its ambitious investment goals without American assistance, even if it had frozen consumption at 1947 levels. But if the Marshall Plan mattered in France, then it mattered for Europe as a whole. Why? Because, France was pivotal to the project of European integration.

It was not the sheer scale of the Marshall Plan that was crucial but its role in breaking bottlenecks – both economic and political.

The UK was the country that received the largest allocation but where, given the size of the UK economy, it mattered least in proportional terms. Nevertheless, as Jim Tomlinson pointed out in an excellent article in 2000, the role of funding provided by the Marshall Plan was to ease what Janos Kornai termed a “shortage economy”, in which bottlenecks became self-reinforcing.

Above all the Marshall Plan was a tool for driving European integration. American influence was crucial in cajoling the French into abandoning the original anti-German vision of the first drafts of the Monnet Plan in favor, in 1950 of proposal for the European Coal and Steel Community.

Less well-known but more important from an economic point of view was American sponsorship of the European Payments Union, the essential monetary stepping stone between the financial autarchy of the 1940s and the final adoption of Bretton Woods norms of convertibility in 1958.

On the history of the European Payments Union, Albert O. Hirschman left a characteristically charming memoir. At the time Hirschman was heading the European desk at the US Federal Reserve. He helped to bypass the vigorous opposition from the Treasury to the idea of creating an American-backed European monetary zone separate from the dollar sphere.

On the importance of the EPU, to which the Marshall Plan allocated $600 million dollars in support in its final stages, Barry Eichengreen is essential reading.

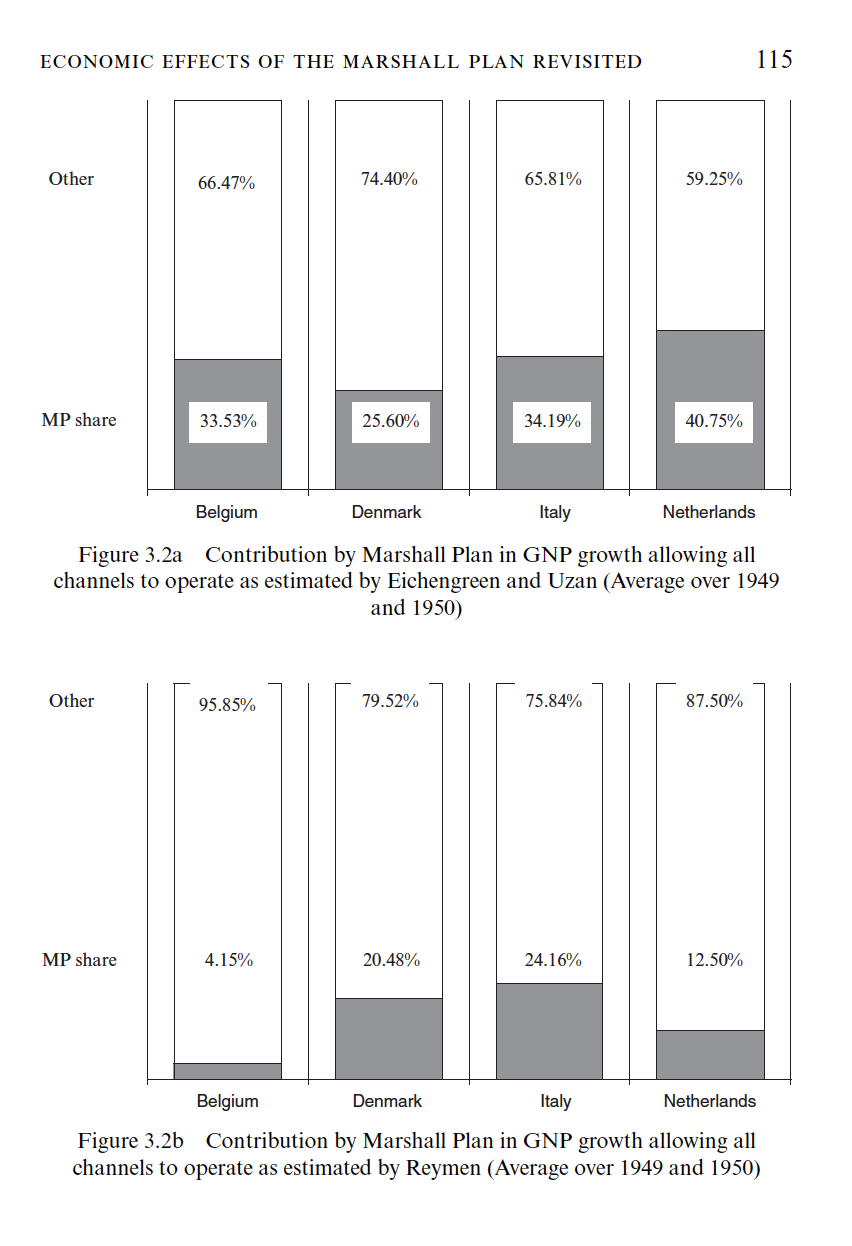

In 2004 JOHN AGNEW and J. NICHOLAS ENTRIKIN then of UCLA published a collection of essays – THE MARSHALL PLAN TODAY. Model and Metaphor – that summarized the state of the art in the economic history of the Marshall Plan.

The tone was far from the triumphalism of the 40th anniversary in 1987. The results of an econometric exercise conducted by Dafne C. Reymen were typical.

The macoreconomic mode of analysis that the Marshall Plan had done so much to promote – with its focus on aggregative investment and growth – had now come to bury the Marshall Plan myth, with honor, but nevertheless to bury it.

The most recent major work on the Marshall Plan by Benn Steil offers a judicious conclusion:

“DID THE MARSHALL PLAN work? to the extent that it was intended to allow the United States to disengage from Europe militarily, the answer is no. The Truman administration was ultimately obliged to conclude, reluctantly, that it had to commit to a military alliance, NATO, to bring its vision to reality. The Marshall Plan and NATO are therefore best understood as two parts of a wider European security policy, which was itself embedded in an emerging Grand Strategy of Soviet containment. But on this level, as a component of a broader strategy, the Marshall Plan did indeed work.

In invoking the Marshall Plan at this moment as an answer to the crisis of Ukraine that broader conclusion should be born in mind. Beyond the myth, a Marshall Plan is not a magic bullet! To be successful it must be part of a broader strategy. And given Ukraine’s needs it will need to be on a huge scale.

****

I love putting out Chartbook. I am particularly pleased that it goes out for free to thousands of subscribers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options:

Ones & Tooze: Who Wins and Who Loses With Inflation

In this episode Cameron and Adam discuss how inflation is having an impact on wide swaths of the US economy and what tools are available to curb the rise. Adam also looks back at past inflation crisis to help decipher what course may be most prudent this time around. In the 2nd segment, the two discuss the critical state of Sri Lanka’s economy which has suspended payments of its 51 billion dollars of foreign debt. Adam says Sri Lanka’s crisis may be a harbinger for other devloping economy which are still reeling from the impact of the Covid-19 crisis.

Find more episodes and subscribe at Foreign Policy

April 21, 2022

Does Ukraine need a Marshall Plan?

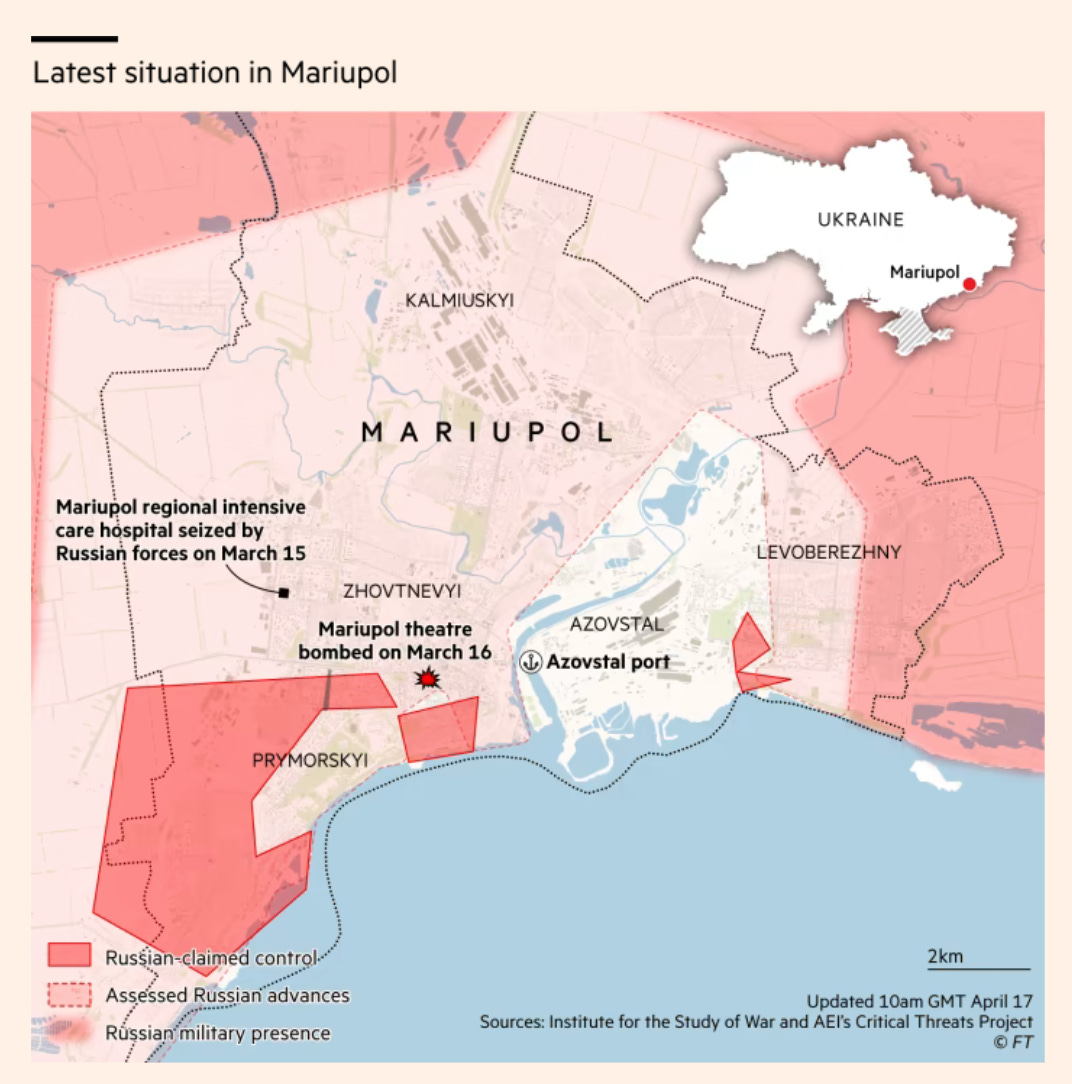

Amid the twisted girders, ruined walls and underground tunnels of the Azovstal plant, Ukraine’s defenders are making their last stand in the siege of Mariupol. The steel factory dates to 1933 and the era of high-Stalinism. It was ruined by Hitler’s Wehrmacht before his forces retreated in 1943, and restored in the postwar period as one of the hubs of Soviet industry. Now the steel plant is being ruined again, this time by Russian forces. Assuming it is returned to Ukraine, will Mariupol’s steel complex become the site for a Ukrainian revival fuelled by Marshall Plan aid from the West?

That is what Azovstal’s owner, the billionaire oligarch Rinat Akhmetov, is asking for. “We will definitely need an unprecedented international reconstruction programme, a Marshall Plan for Ukraine,” Akhmetov declared to CNN. “I trust that we all will rebuild a free, European, democratic and successful Ukraine after our victory in this war.”

Vladimir Putin’s war against Ukraine has unleashed a revival of Cold War liberalism in American and European political discourse and punditry. Nato is back. The West is rallying. Against that backdrop it was only a matter of time before the call went out for a Marshall Plan for Ukraine. America’s fabled aid programme is widely credited with kick-starting western Europe’s miraculous recovery after 1945. It provided the material foundation for the era of so-called embedded liberalism – the synthesis of normative principles and institutions that underpinned the postwar order.

Read the full article at The New Statesman

April 18, 2022

Chartbook #114: Azovstal – Mariupol’s final battlefield

The vast complex of the steel mill of Azovstal is where the last defenders of Mariupol are making their stand.

What kind of place is this? A giant steel works sprawling over several square kilometers. It has tunnels in which the fighters are withstanding the bombardment. But how did it end up there? What brought us to this point of a factory fight in Southern Ukraine?

At moments like this, history truly reveals its quality as a pal·imp·sest – a manuscript or piece of writing on which the original writing has been effaced to make room for later writing but of which traces remain. The search functions of the internet reinforce that quality, constantly surfacing long-forgotten pieces from a different era.

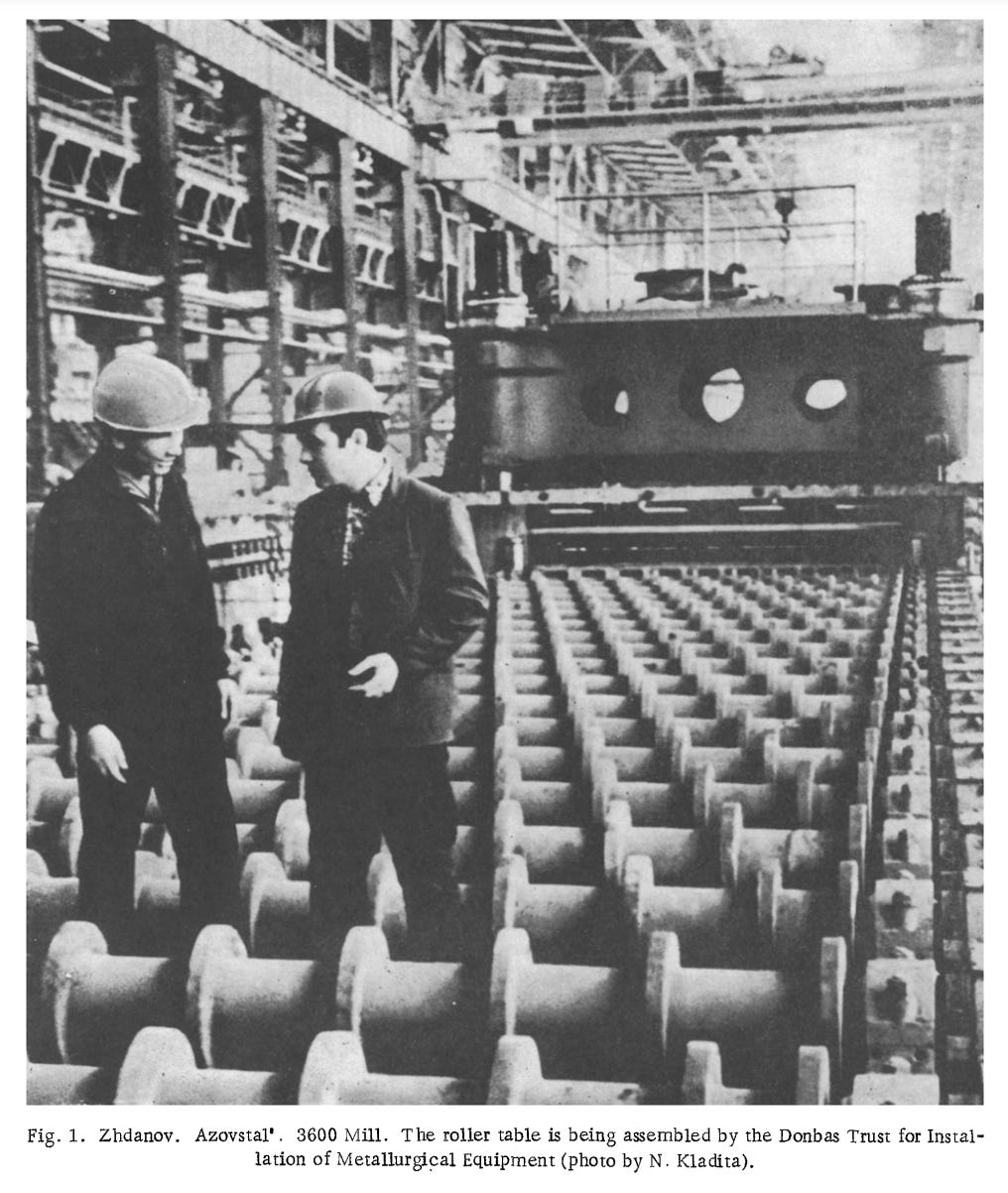

Google “Avostal”. You find this. From 1973 – the high-Soviet era.

A MOST IMPORTANT PROJECT OF THE THIRD, DECISIVE YEAR THE COUNTRY’S MOST POWERFUL 3600 MILL OF THE AZOVSTAL’ PLANT HAS PRODUCED THE FIRST SHEET Ya. Brodskii

Brodskii, writing in 1973 is already writing a history, looking back to the moment of Azovstal’s foundation in 1933:

This was long ago – 40 years ago, during the years of the first five-year plans, years of romanticism and heroism, years that gave rise to the Magnitogorsk Metallurgical Combine, Kuznetsk, Dniepr hydroelectric station, Ural Heavy Machinery Plant… A country was being built, a country was being created. The words “first,” “first-born” were the most widespread at this unforgetable time. “First steel,* “first plant,” “first tractor !” We leaf through the pages of the newspapers of the 1930’s– these stern and impassioned chronicles of our life.

“Magnitogorsk– express telegram- on February 1 at 7:30 p.m. blast furnace No. 1 of the Magnitogorsk Metallurgical Combine produced the first pig iron.”

Knznetsk, April i. The incandescent blast is producing the first Kuznetsk metal. ~

“Makeevka, January 28. The first Soviet blooming mill passed the test perfectly.” …

So many ~firsts” appeared at that time … The first Soviet pig iron, tractors, blooming mills, steel, and automobiles were born in the foothills of the Ural mountains, in the spurs of Alatau, and on the shores of the Dniepr.

Azovstal’ Plant-‘SouthernMagnitogorsk” as it was called by people who arrived to build this metallurgical giant- rightfully numbers among the first-born of Soviet industry. The resolution of the Central Committe of the Communist Party of the Soviet Union (Bolsheviks) on August 8, 1929, called for the immediate development of a plan for using Ketch ores and in connection with this the construction of plants in the Azov region. This resolution gave rise to the design and construction of the Azovstal’ Plant. … Tens of thousands of builders from Russia, Belorussia, Georgia, and Kazakhstan arrived at the shores of the Azov Sea to erect one of the countries most powerful metallurgical enterprises, the Azovstal’ Plant.

Ya. Gugel’, who a year before had constructed the Magnitogorsk Metallurgical Combine, directed the project. Every day brought news about the feats of labor of the builders. Record after record was established by the concrete workers, diggers, carpenters, and assemblers. And there, on August 10, 1933, the enormous bright red banner of the KIM (Communist Youth International), raised by the assemblers of Stepan Zumadzhi’s brigade, flew in the night sky above the top of the first blast furnace. And several hour later, at 3:44 a.m., the order was given to blow in the furnace. Thus began the life of still another first-born of Soviet industry. This was long ago, 40 years ago … And here, today, four decades later, we again speak about the heroic labor on the shores of the Azov Sea.

1930s USSR – Chief of Newly Built AZOVSTAL METALLURGICAL (Steel) PLANT

To imagine Azovstal’s birth, consult Stephen Kotkin’s Magnetic Mountain: Stalinism as a Civilization, the classic study of Magnitogorsk, which, according to legend, was inspired by taking office hours with Michel Foucault during a visit to Berkeley.

Azovstal was not the first steelworks at Mariupol (the city was renamed Zhdanov during the Stalinist era, after its most famous son). That honor belongs to the Ilych Metallurgical Complex (MIMC). As an anniversary piece noted:

The IMC enterprise was started on the basis of the works of the Nikopol’–Mariupol’ joint-stock company Providence. February 13, 1897, is considered the birthday of the IMC. On that day, the pipe shop produced its first real product, namely, pipes for laying the Baku–Batumi kerosene pipeline. In 1897, the openhearth furnaces and the rolling shops were put into operation. In 1898, the enterprise had already begun to operate according to the complete metallurgical cycle and it had become the largest works in the southern part of the Russian Empire. In 1914, for fulfilling largescale state orders, there had been put into operation a unique 4500 armoring rolling mill. After 1927, after nationalization and renewal, the works continued to develop as a polytechnical enterprise. In 1930, the first turn of the pipe-rolling shop, which had been the largest in Europe, was put into operation. During the years of the first 5-year plans, the works became the initiator and founder of rapid steelmaking practice; in 1935, it reached the first All-Union record in the steelmaking productivity; and in 1936, it achieved the world record in yield of steel from a square meter of the furnace hearth. In the prewar period, production of armor for the T-34 tank at the works, which played a noticeable role in winning the war with Germany, was perfected for the first time.

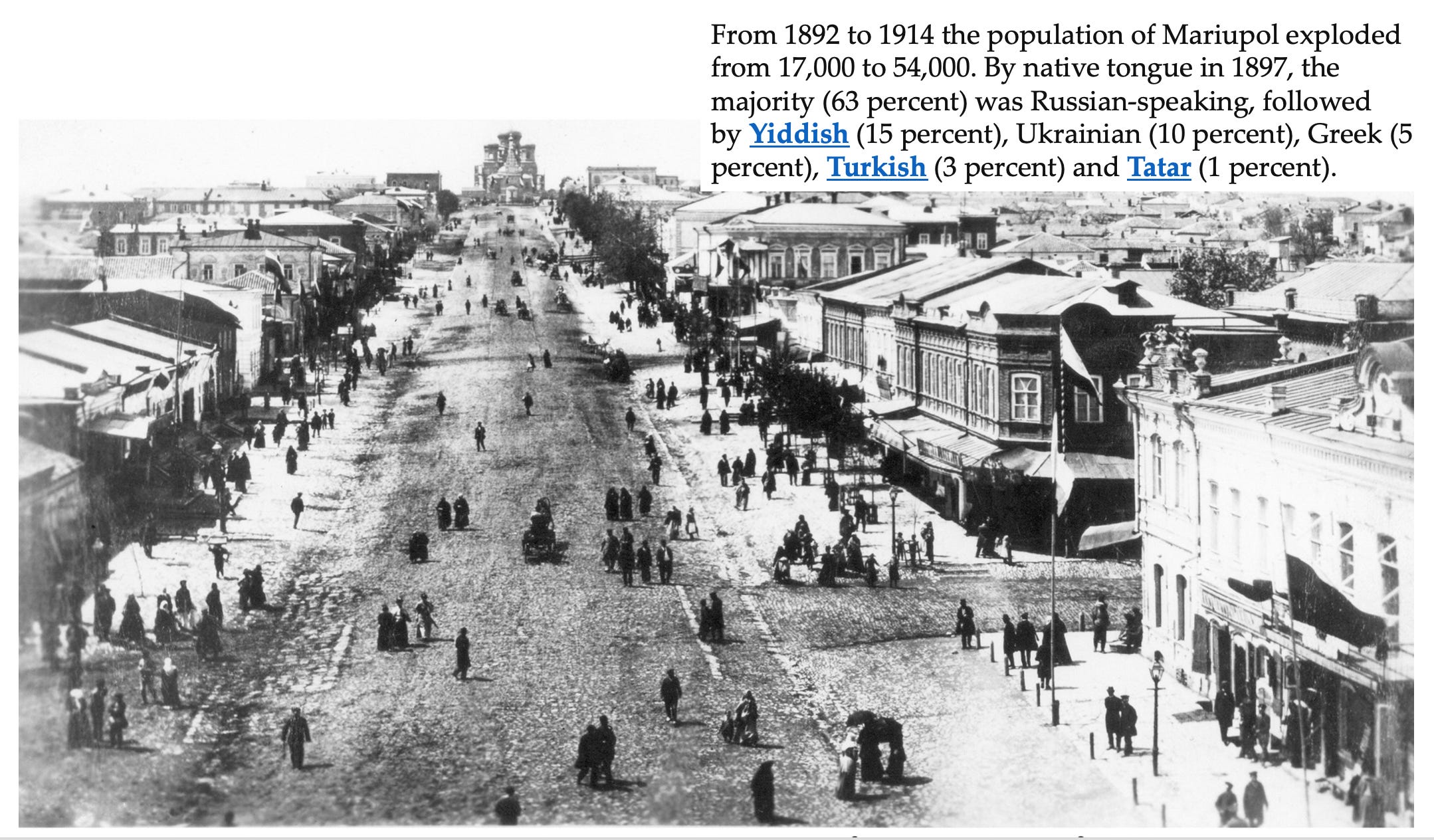

First the railway, then grain export, then steelmaking transformed the sleepy ethnically and culturally-Greek enclave of Mariupol first into a bustling Imperial Russian boom town and then into a Soviet construction site.

On Mariupol’s history the online Encylopedia of Ukraine is excellent.

In the late 19th century Mariupol was developed as a shipping port for the Donets Basin. In 1882 it was linked with Donetsk by railway, and in 1886–9 the commercial port was built. The main exports were coal and grain. By 1900 the port was handling 1 million t of freight, and the tonnage doubled in the next decade. At the turn of the century a tube-rolling and two metallurgical plants were built (the Nikopol, in 1897 by the American businessmen Rothstein and Smith, and the Russian Providence, in 1899 by a Belgian company). Easy access to raw materials, labor, and a port for export were the main attractions. From that time the town’s heavy industry grew rapidly.

From 1892 to 1897 the population of Mariupol almost doubled, from 17,000 to 31,100. By native tongue in 1897, the majority (63 percent) was Russian-speaking, followed by Yiddish (15 percent), Ukrainian (10 percent), Greek (5 percent), Turkish (3 percent) and Tatar (1 percent). By the beginning of the First World War the city’s population had jumped to 54,000.

As a later director of the Azovstal steelworks explained, what drew the people in was a peculiarly beneficial combination of raw materials:

The “Azovstal” Works makes use of the enormous deposits of phosphorus-containing Ketch ores which lie almost on the surface and are transported to the Works by the Azov sea after beneficiation and sintering, and of the Donets coal processed into high-grade coke at the coke and by-product plant. Limestone required for the blast furnace and the open-hearth furnace processes is obtained from the Elenovskie quarries, situated in the vicinity of the Works. Krivoi Rog ores are also employed in the blast-furnace charge. The Works is thus situated in the center of sources of raw materials

By 1939 under the impact of Soviet development, Mariupol’s population had surged to 227,000 – from 17,000 in 1892!

In 1941, the German invaders killed the Jewish population they could find, ruined the town and on their retreat laid waste to the steel plants. The population by 1943 came to only 85,000. The devastation the Germans left behind was total.

huge heaps of tens of thousands of tons of stones, lumps of concrete, mutilated steel structures and equipment were !ying all over the Works. In September, 1943, there was no water, electricity or steam either in Mariupol or at the Works. Under those difficult conditions the metallurgists of the ~Azovstal” and the constructors of the ~Azovstalstroi ~ began the reconstruction of their Works, The seemingly impossible task was accomplished with the help of the strong will and the courageous spirit of the Soviet people. In October, 1944, the power station was rebuilt and in July, 1945, No. 8 blast furnace was blown in.

The subequent reconstruction was dramatic, as V.V. Leporskii then plant director at Azovstal recalled in 1963.

A sintering mill, two blast-furnaces, six open-hearth furnaces, a large-capacity blooming mill, a rail-structural mill, a heavy grade mill, a ball-bearing mill, a mill for rail reinforcements, and others were built; the construction of housing, hospitals, schools, movie theatres, and culture palaces developed extensively. Construction has proceeded at a rapid pace. The 1940 level of production of iron and steel has now been exceeded several times; labor productivity per worker has increased by 4.7 times throughout the plant. The plant has been a profitable installation since 1960. …. In 1962 a collective of innovators of the plant won first place in the district competition, and in the All-Union contest in 1962 for introducing inventions the plant “Azovstal’ ” won third place. The cadres grow and improve with the plant. This year over 5 thousand persons are enrolled in institutes, technical schools, schools for advanced training, and industrial-technical courses.

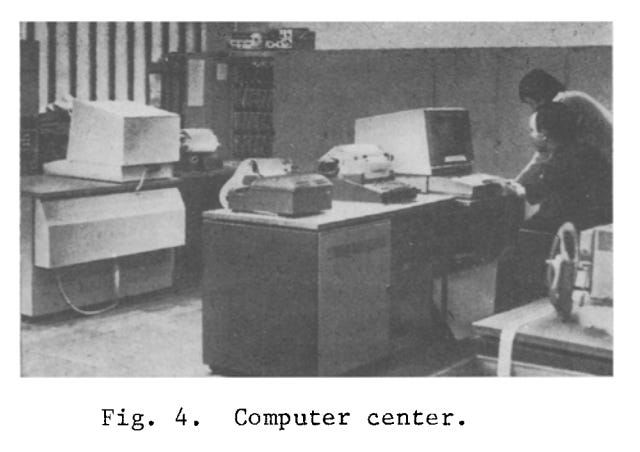

As its workforce became more and more sophisticated, in 1973, the plant was celebrating the introduction of the first computer-controlled processes.

Computers, according to a prescribed program, monitor the heating of the slabs and control the operation of the stands and heat treatment of the sheet. In the future computers will be connected to the automatic production control system of the entire Azovstal’ Plant which is being created.

Source: COURSE OF THE AZOVSTAL ~ PLANT IN THE TENTH FIVE-YEAR PLAN A. M. Sedakov

The trail of Azovstal’s heroic commemoration goes cold in the 1980s and 1990s. As Kimitaka Matsuzato of Tokyo University explains in her excellent essay on Mairupol’s local politics, the city stagnated amidst the overindustrialization of the late Soviet period.

In 1993, the sixtieth anniversary of the plant, V.A. Sakhno published an almost apologetic piece noting:

The combine is now encountering problems in producing metal with prescribed properties. While the product mix is becoming more complex, Azovstal’ is having difficulties obtaining charge materials of consistently high quality. The same holds for deoxidizers and alloying additions. It has also become necessary to significantly reduce energy consumption during steel production. At the same time, clients are demanding metal of higher quality

And then, the oligarchic power struggles of the Donbas broke loose. In November 1996 Mariupol’s two steelworks, long-time competitors, were suddenly merged into a single conglomerate. As the Steel Times reported, the local population were dumbfounded.

Ukrainians ‘taken aback’ by Azovstal/Ilyitsh merger Steel Times; London Vol. 224, Iss. 11, (Nov 1996): 383.

By the early 2000s the owner of the former crown jewel of Soviet industrialism, Azovstal, was Rinat Akhmetov, perhaps the richest of Ukraine’s oligarchs and certainly one its toughest. As Leonid Bershidsky, Bloomberg’s columnist described it:

In early 2014, Mariupol was a typical mid-sized post-Soviet industrial city, dominated by two major steelworks, both under the control of the country’s richest oligarch, Rinat Akhmetov, and the port used to export their output. …. Backed by Akhmetov’s political clout and resources, the Party of Regions of then-president Viktor Yanukovych held sway. The population, including tens of thousands of Azov Greeks — descendants of the city’s 18th-century Orthodox Christian founders, resettled by Russia from still-independent, Muslim-run Crimea — was predominantly Russian-speaking and had little to do with Ukrainian ethnicity or culture.

In short, it was the kind of city that fit in nicely with semi-official plans by some Kremlin officials and ethnonationalist ideologues in Russia to create a separatist state called Novorossiya in eastern and southern Ukraine. During the chaotic spring of 2014, thousand-strong mobs hunted through the city for Ukrainian nationalists supposedly sent from the country’s west to suppress them, the city council building was seized by rebels who flew Russian flags from it, and a gun battle took place for the police headquarters. The post-revolutionary Ukrainian authorities were too weak to re-establish order quickly, and it fell to local irregulars, some of them ultranationalists with openly racist views and swastika tattoos, to fight off the Communists and pro-Russian activists who sought to make Mariupol, located in the Donetsk Region, part of the self-proclaimed Donetsk People’s Republic. ….

Somehow Mariupol avoided being taken by the separatists. ….

In early 2015, with the war in eastern Ukraine still in its active phase, the eastern suburb of Mariupol came under heavy shelling from the separatist side, and dozens of civilians died (Akhmetov stepped in with a large personal donation to repair the damaged infrastructure). That brought home to the residents that their city was now on the front line for the long term. But when a ceasefire negotiated in Minsk took effect later that year, the relative benefits of this status began to manifest themselves. With eastern Ukraine’s biggest city, Donetsk, under separatist control, Mariupol became the center of the region’s Ukrainian part, and the administrations of both Petro Poroshenko and Volodymyr Zelenskiy have sought to turn it into a showcase of what the Donbas could become under Ukrainian authority.

Akhmetov is a pivotal figure in Ukrainian politics. In 2021 an open trial of strength appeared to have begun with President Zelensky and the parliament. The Rada passed legislation threatening to crack down on oligarchs, raise taxes and railway fees. Akhmetov was accused by Zelensky of plotting a coup against him.

With the invasion, however, Akhmetov has committed to the national cause. As CNN reports

Ukraine’s richest man has pledged to help rebuild the besieged city of Mariupol, a place close to his heart where he owns two vast steelworks that he says will once again compete globally. For now, though, his Metinvest company, Ukraine’s biggest steelmaker, has announced it cannot deliver its supply contracts and while his financial and industrial SCM Group is servicing its debt obligations, his private power producer DTEK “has optimised payment of its debts” in an agreement with creditors.

“Mariupol is a global tragedy and a global example of heroism. For me, Mariupol has been and will always be a Ukrainian city,” Akhmetov said in written answers to questions from Reuters.

On Friday, Metinvest said it would never operate under Russian occupation and that the Mariupol siege had disabled more than a third of Ukraine’s metallurgy production capacity.

Akhmetov praised President Volodymyr Zelenskiy’s “passion and professionalism” during the war, seemingly smoothing relations after the Ukrainian leader last year said plotters hoping to overthrow his government had tried to involve the businessman.

Akhmetov called the allegation “an absolute lie” at the time.

“And the war is certainly not the time to be at odds… We will rebuild the entire Ukraine,” he said, adding that he returned to the country on Feb. 23 and had been there ever since.

Akhmetov did not say where exactly he was, but that he had been in Mariupol on Feb. 16, the day some western intelligence services had expected the invasion to begin. “I talked to people in the streets, I met with workers…,” he said.

“My ambition is to return to a Ukrainian Mariupol and implement our (new production) plans so that Mariupol-produced steel can compete in global markets as before.”

“I am confident that, as the country’s biggest private business, SCM will play a key role in the post-war reconstruction of Ukraine,” he said, citing officials as saying the damage from the war has reached $1 trillion.

“We will definitely need an unprecedented international reconstruction programme, a Marshall Plan for Ukraine,” he said, in reference to the U.S. aid project that helped rebuild Western Europe after World War Two.

“I trust that we all will rebuild a free, European, democratic, and successful Ukraine after our victory in this war.”

Whilst Akhmetov sees a future for Azovsteel as the site of yet another industrial renaissance this time under a Ukrainian Marshall Plan, in the tunnels of his factory, Ukrainian marines of the 36th brigade, a large number of Azov brigade combatants, soldiers from the 56th Infantry Brigade, as well as border guards and volunteer fighters are, to all appearances, preparing to fight to the last bullet.

What they seem to be enacting is not the Marshall Plan, but something closer to Stalingrad.

April 17, 2022

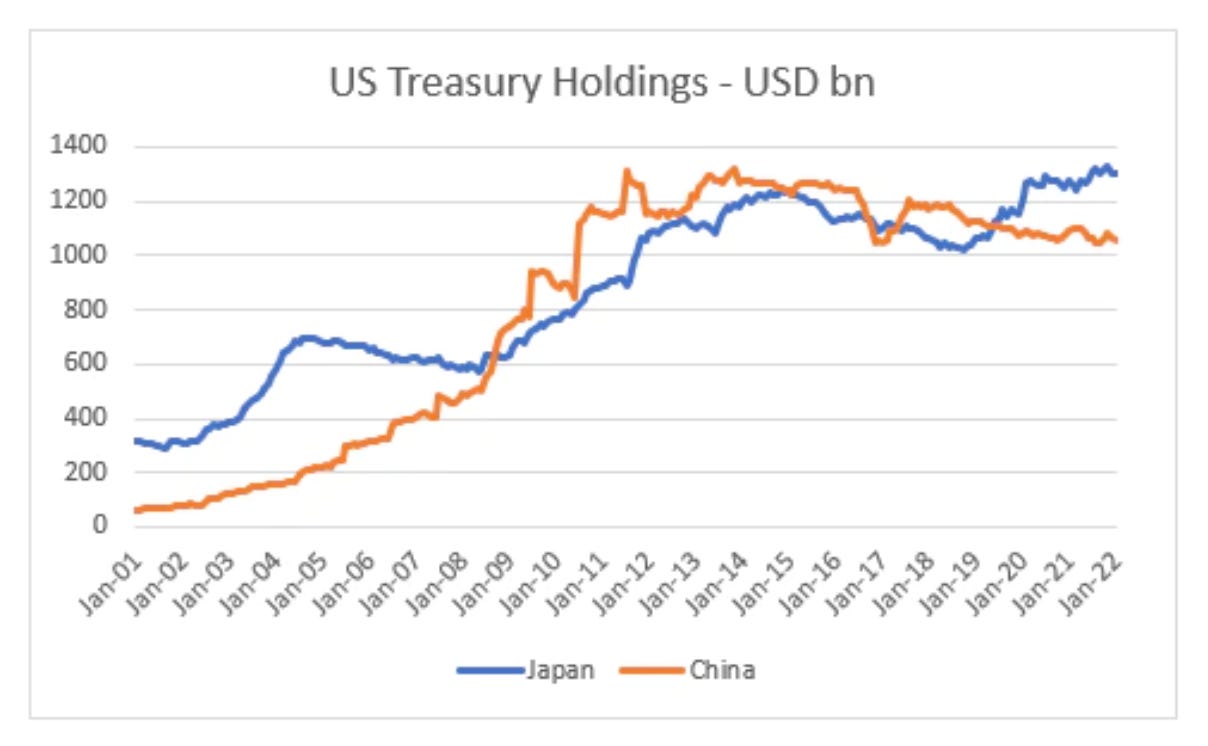

Chartbook #113: Tension in the dollar-system. Could a plunging Japanese Yen upset the US Treasury market?

Every moment of stress in the global financial system is a test of lines of interconnection and power. The most obvious example of this right now is the sanctions regime imposed on Russia. That has provoked a surge in debate about possible alternatives to the dollar, ruble-yuan systems, commodity-based networks of finance etc. The line I have been taking in Chartbook is that talk of alternatives to the dollar is not so much premature as reflective of an unease with the present, which finds relief in Finance-fictions (Fin-Fi) that are less predictive than expressive. A realistic analysis needs to resist the temptation to escape into the future and instead to stay with the actually existing dollar system and its troubles. The urgent question to ask is how the lines of power and influence continue to operate within this system.

As US monetary policy tightens in response to the surge in global inflation, the effect is felt around the world. In the first instance this reads like a story of collateral damage. But might there be blowback? Might the effects of US tightening on the wider world affect the United States itself? If so where will that blowback come from? Emerging Asia, or the advanced economies?

As I argued in Chartbook #108, one group of economies that are badly affected are the low-income and EM economies who see their borrowing costs rise.

The fear is of another “taper tantrum”, as in 2013-4 when Ben Bernanke hinted that the Fed was thinking about slowing its asset purchases (QE3) and this triggered a sudden tightening in funding costs for EM. In 2022 we again facing warnings of a global debt crisis. Sri Lanka is the most obvious casualty so far. There may be more to come.

This prospect ought to matter to US policy makers from a regional policy and geo-economic point of view. The fate of hundreds of millions of people hangs in the balance. But the question in Washington and New York will be: what are the implications for the US economy of this global reverberation from Fed tightening?

Certainly as far as Sri Lankan crisis is concerned, the implications for the US economy are negligible. US exports to Sri Lanka amount to a few hundred million dollars annually. There are no substantial financial connections.

This asymmetry in relations is true even for some very large emerging market economies. In 2020 the US Federal Reserve did not see fit to extend a central bank liquidity swap line to Indonesia. Why not? Because first and foremost the Fed’s interest in global financial stability is dictated by its responsibility for US financial stability and it is not plausible to argue that a liquidity squeeze in Indonesia will blow back seriously on the United States.

This asymmetry of monetary power is very pronounced with regard to the emerging markets and low income countries integrated into the dollar system. But weighted in dollar-terms they are small parts of the system. They are not too big or too systemic to fail. With regard to the big nodes in the system – Europe and East Asia – the interactions are two-way.

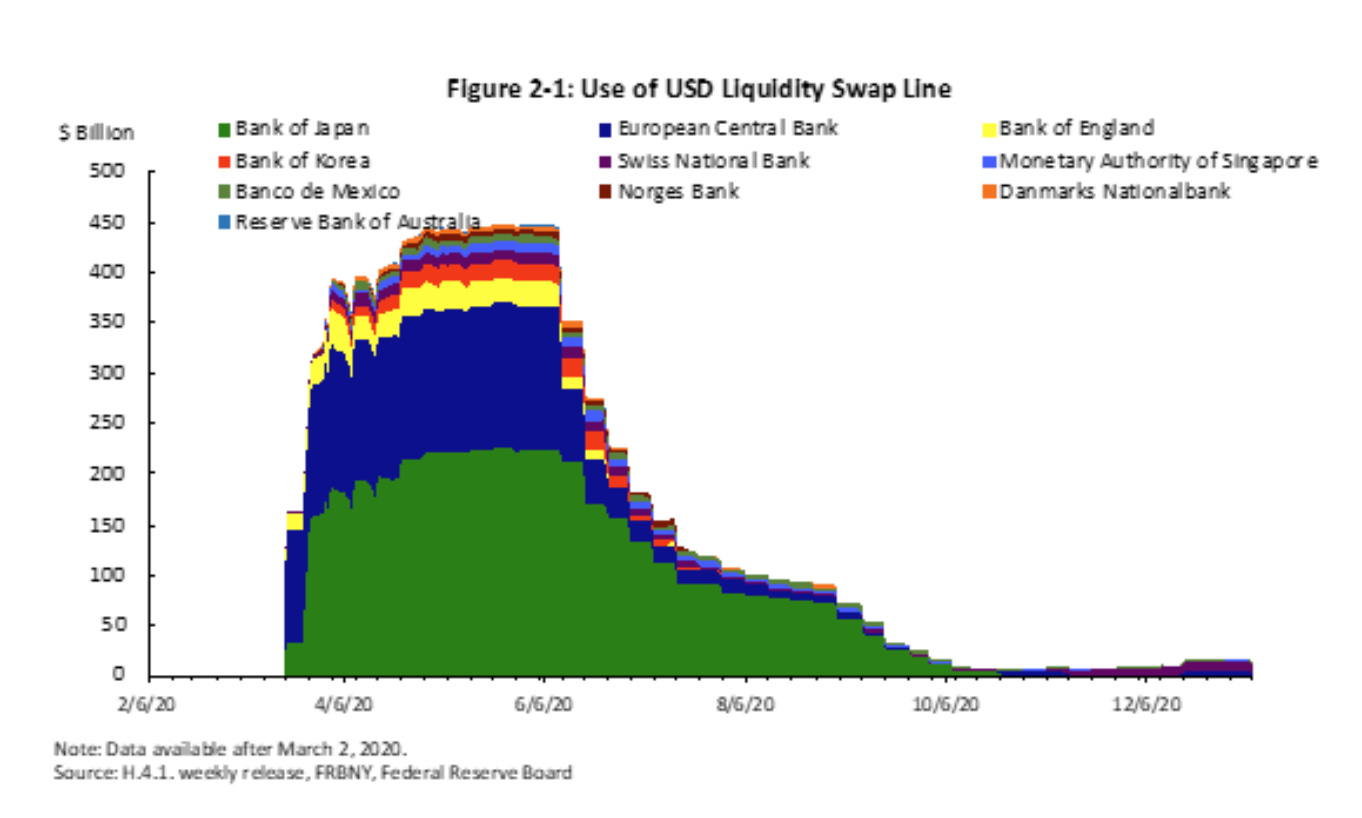

In the North Atlantic financial system, centered on the axis between Wall Street and the City of London, the influences run both ways and the response from US policy-makers reflects that. In the 2008 financial crisis the Fed extended as much liquidity support to European banks as it did to American banks. The Fed dispensed this largesse because it did not want to find out how an acute crisis at Barclays or Deutsche Bank might blow back on the US financial system.

In 2020 the swap lines were put in place again. And this time rather than the ECB it was the Bank of Japan that was the main taker of dollar liquidity.

Source: Junko Oguri Yale SOM 2021

In 2022 as well, it is, once again, not the Euro-US axis that is being tested, but the Japan-US axis.

For the world economy, the biggest news of recent weeks is not so much the vicissitudes of the ruble, but the sudden movement in the Yen-dollar exchange rate. From a high of 102 Yen to the dollar over the winter of 2020-2021 the Yen has plunged to 128 per dollar and is heading towards 130, a devaluation not seen since the early 2000s. That is a thirty percent relative movement across one of the major currency pairings in the world economy. Balance sheets involving trillions of dollars in both yen and dollars are affected.

Source: Daily Shot

Why the devaluation? Japan is currently running a trade deficit. It is a major commodity importer and paying the price. But macroeconomic fundamentals do not explain this currency movement. Inflation in the US is running far ahead of Japan. What explains the movement are market reactions to central bank policy. Most of the depreciation is driven by the discrepancy between the Fed’s increasingly adamant commitment to monetary tightening and the Bank of Japan’s continued stimulus.

Historically, the big swings of the dollar and the yen tend to track the relative stance of central bank policy. The Yen strengthened between 2007 and 2012 under the impact of the financial crisis and Fed loosening. Then, when Japan adopted the massive monetary stimulus policies of Abenomics, this depreciated the yen.