Adam Tooze's Blog, page 17

July 1, 2022

Ones & Tooze: What NATO Expansion Means for Europe and the World

NATO is enlarging its rapid response force from 40,000 to 300,000, in light of Russia’s invasion of Ukraine—a huge expansion. But who will foot the bill and how will the force operate in practice? Adam and Cameron discuss these and other questions in the first segment of the episode. Then, to mark the July 4th holiday, they dive into the history and economics of…hot dogs.

Find more episodes and subscribe at Foreign Policy

Chartbook #132 Nowcasting – the immediate outlook for the US economy

As the Fed has announced its pivot to a tighter monetary policy, financial conditions in the US – a broad gauge of borrowing conditions – are now tightening more steeply than at any time since the early 1980s.

Source: FRB

Meanwhile, the inflation numbers remain stubbornly high. They will ease, presumably, only when the economy slows down significantly. The question is a. how rapidly inflation comes down and b. how hard the American economy lands. In the Fed’s fantasy, the economy turns swiftly, inflationary pressures rapidly recede and, consequently, the tightening of interest rates does not have to be too extreme.

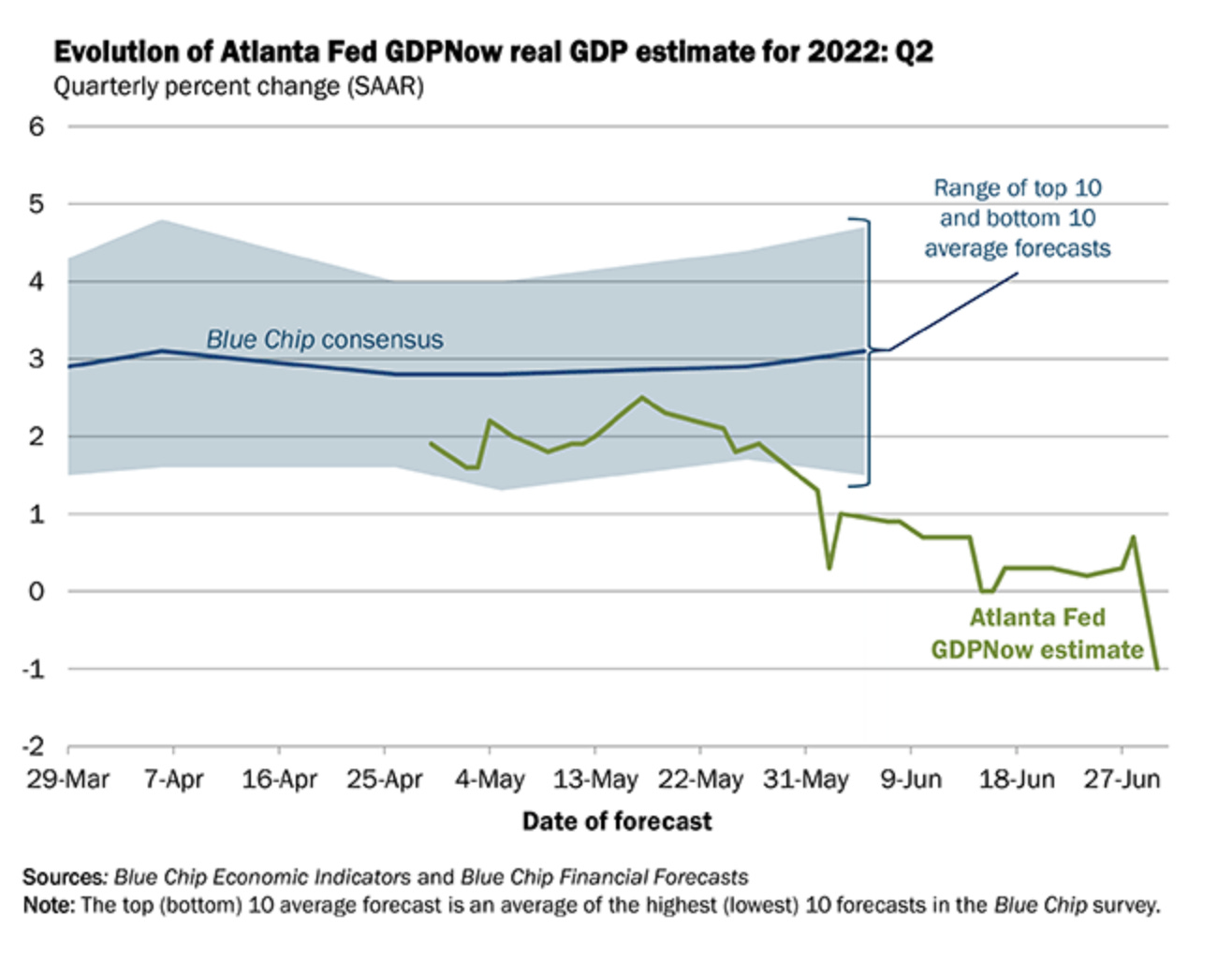

We are too early in the process to tell how rapidly the ship will turn. But talk of recession is already everywhere. Indeed, a recession may come sooner than many think. In the first quarter of 2022, thanks in part to bad trade data, US GDP contracted in real terms. Now, the Atlanta Fed’s widely cited Nowcasting model is predicting negative growth for Q2.

Source: Atlanta Fed

In this short video Patrick Higgins of the Atlanta Fed explains the logic of his model.

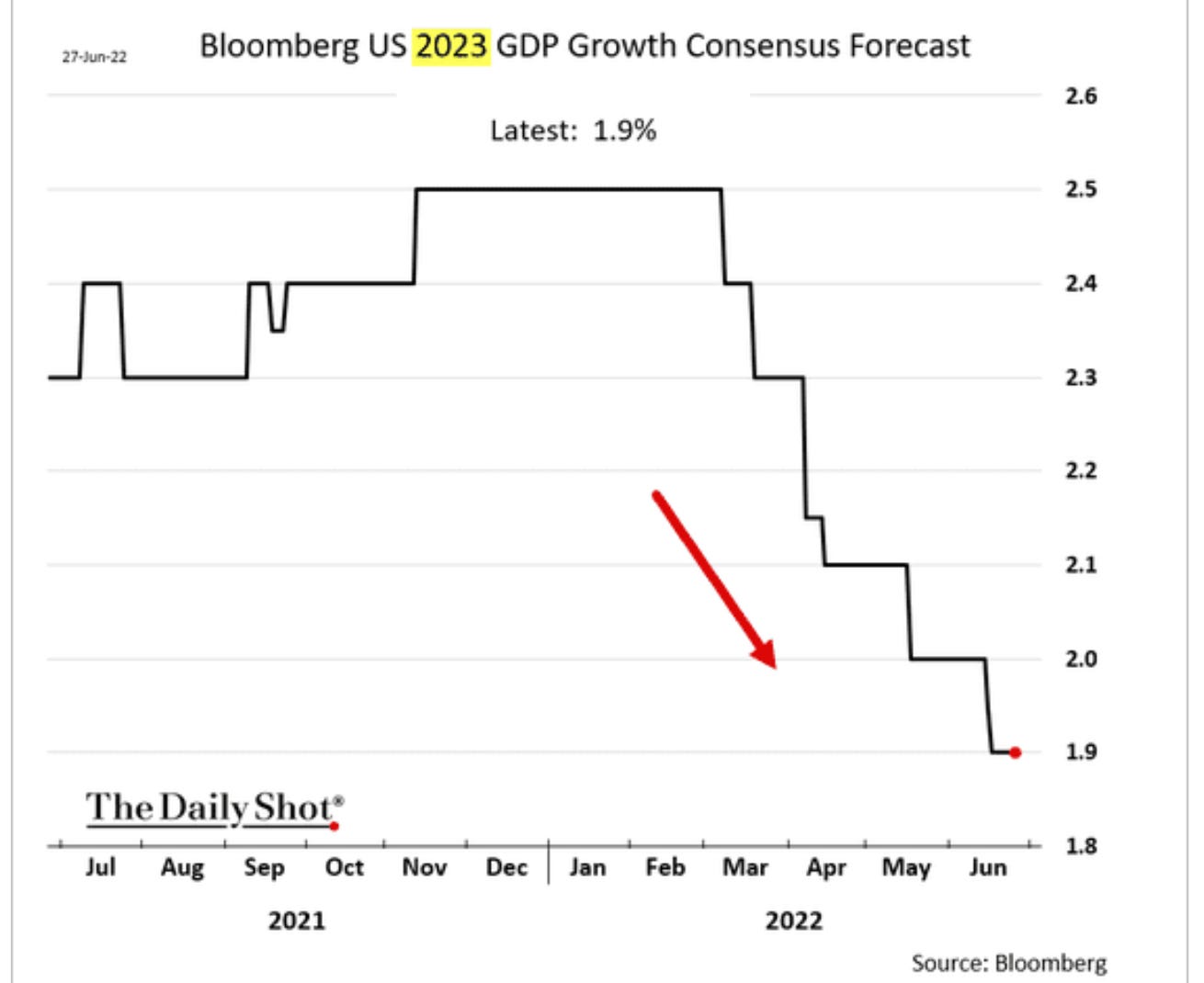

Were the Atlanta Fed to prove correct, we could already be in a technical recession i.e. undergoing two consecutive quarters of GDP contraction. That is not what the majority of economists expect. When asked when they expect the next recession, 71 percent of economists surveyed by Deutsche Bank expect that it to arrive in 2023. It is worth saying that if a recession does arrive in 2023 the consensus view seems to be that it will be mild – two quarters of mild contraction. The Bloomberg Consensus Forecast for 2023 as a whole, is for growth of 1.9 percent. That is not exciting. It is far less than was expected in the spring, but it is much better than nothing.

Source: Daily Shot NB: It is hard to overstate how excellent the Daily Shot newsletter is. If you can afford a subscription, it is worth every cent.

Meanwhile, real-time evidence is accumulating of a slowdown that is already underway. In the giant US housing market, mortgage applications to purchase a home dropped sharply last week and are now down 24% relative to 2021.

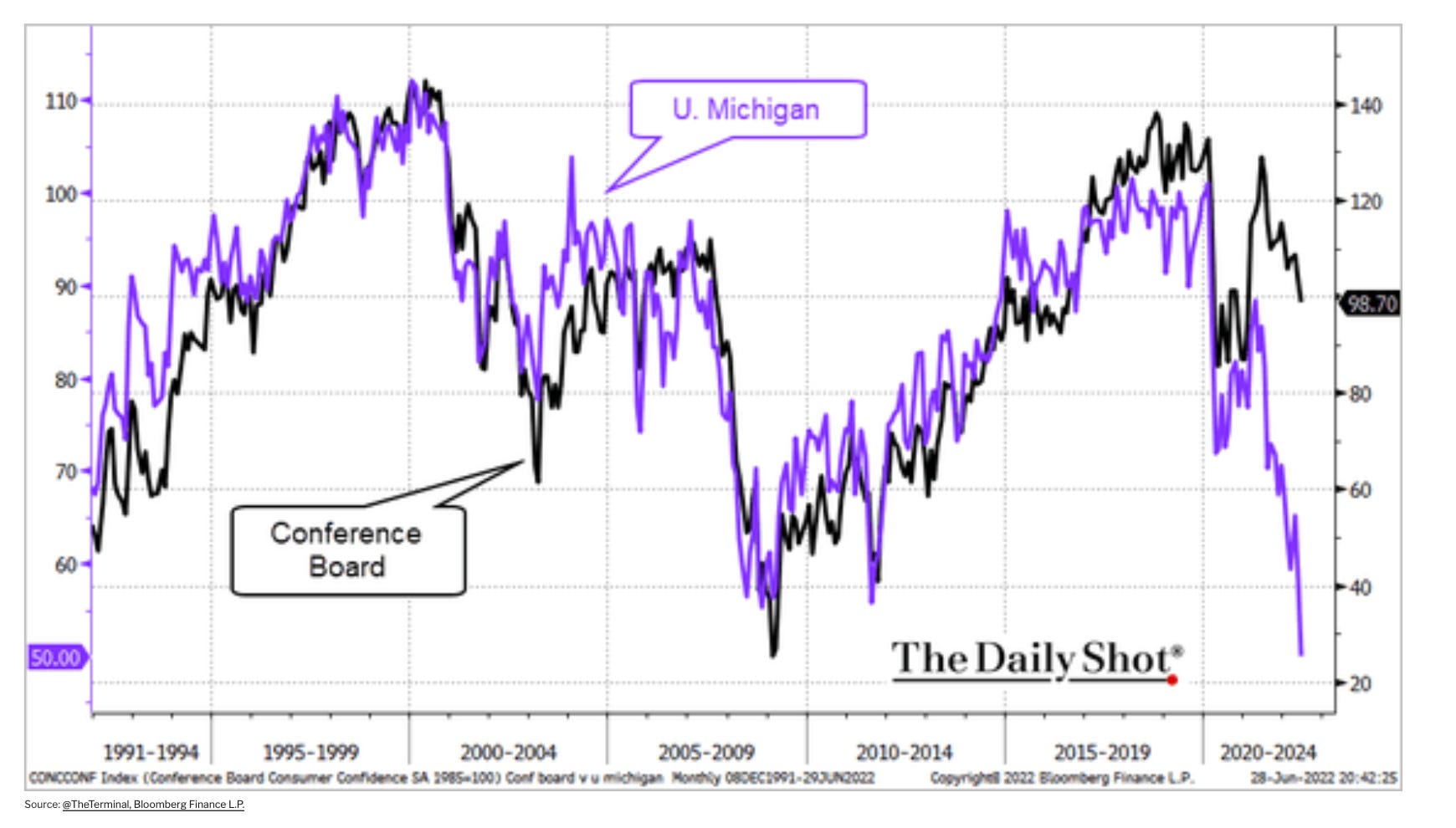

American consumers are the largest single source of demand in the world economy and like their counterparts in Europe, they are in a deeply pessimistic mood. Consumer sentiment as measured by the University of Michigan tanked in 2021. Now, the Conference Board indicator, which normally shows less pronounced swings, has also turned sharply in a negative direction.

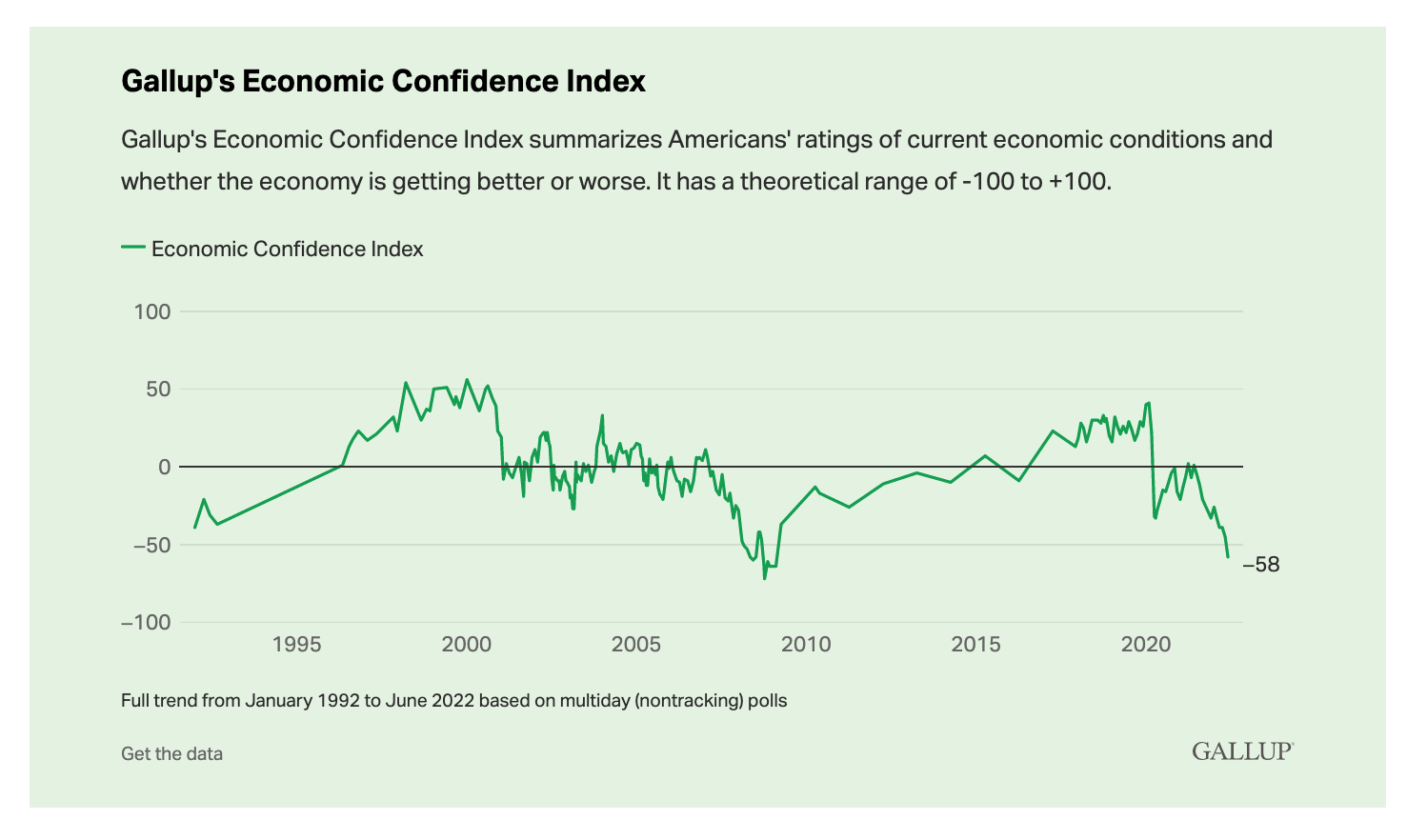

The economic confidence index compiled by Gallup is at levels last seen during the 2008 crisis.

It is far too early to call it a new trend, but, in real terms, US personal spending fell in May to what is presumably an annualized total of $13.896 trillion.

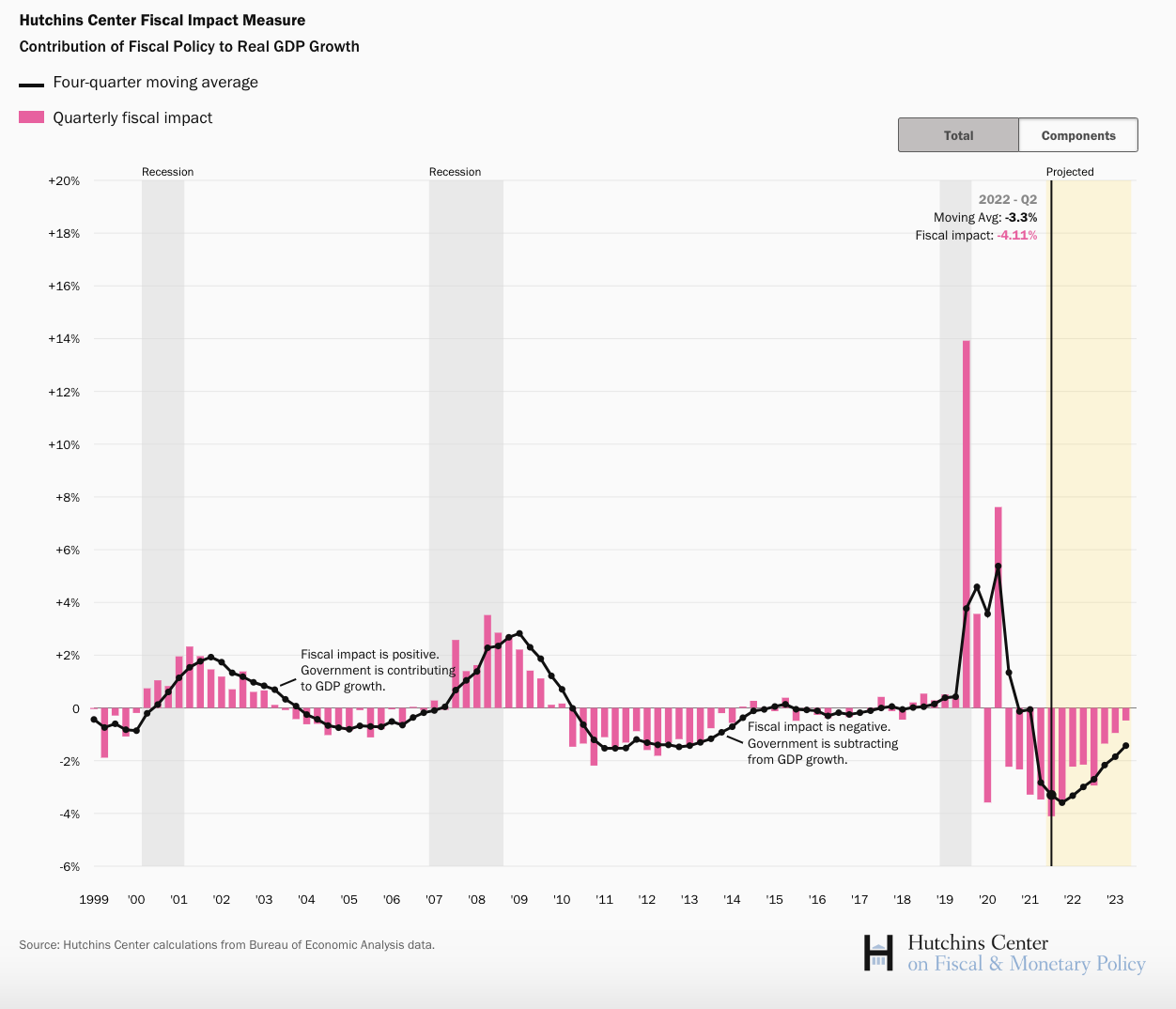

One other major source of aggregate demand, is American government spending. After the stimulus of 2020 and 2021, fiscal policy is now exercising a drag effect on the US economy.

Source: Brookings

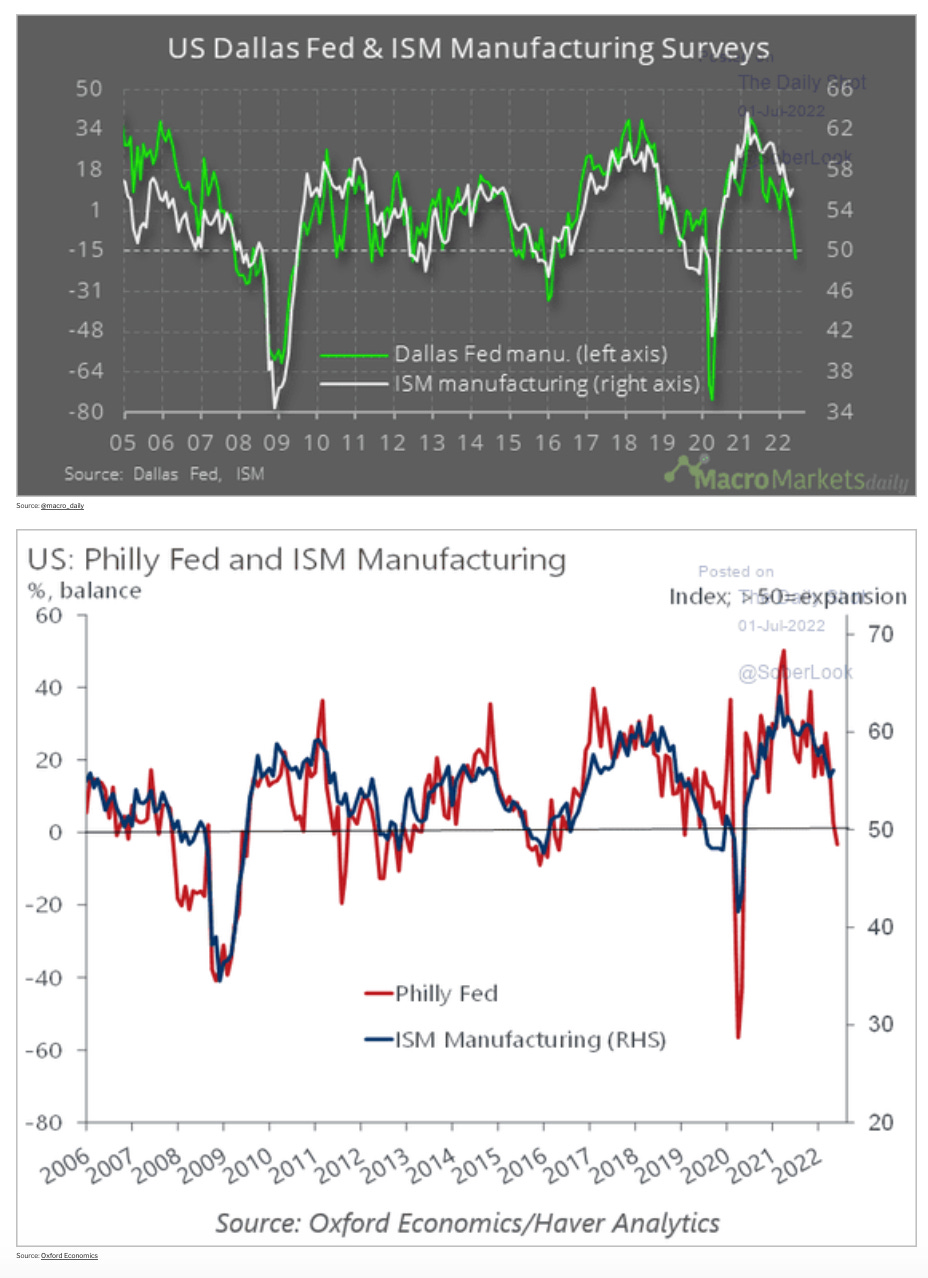

All the surveys of manufacturing in the Federal Reserve regions are now pointing in a negative direction.

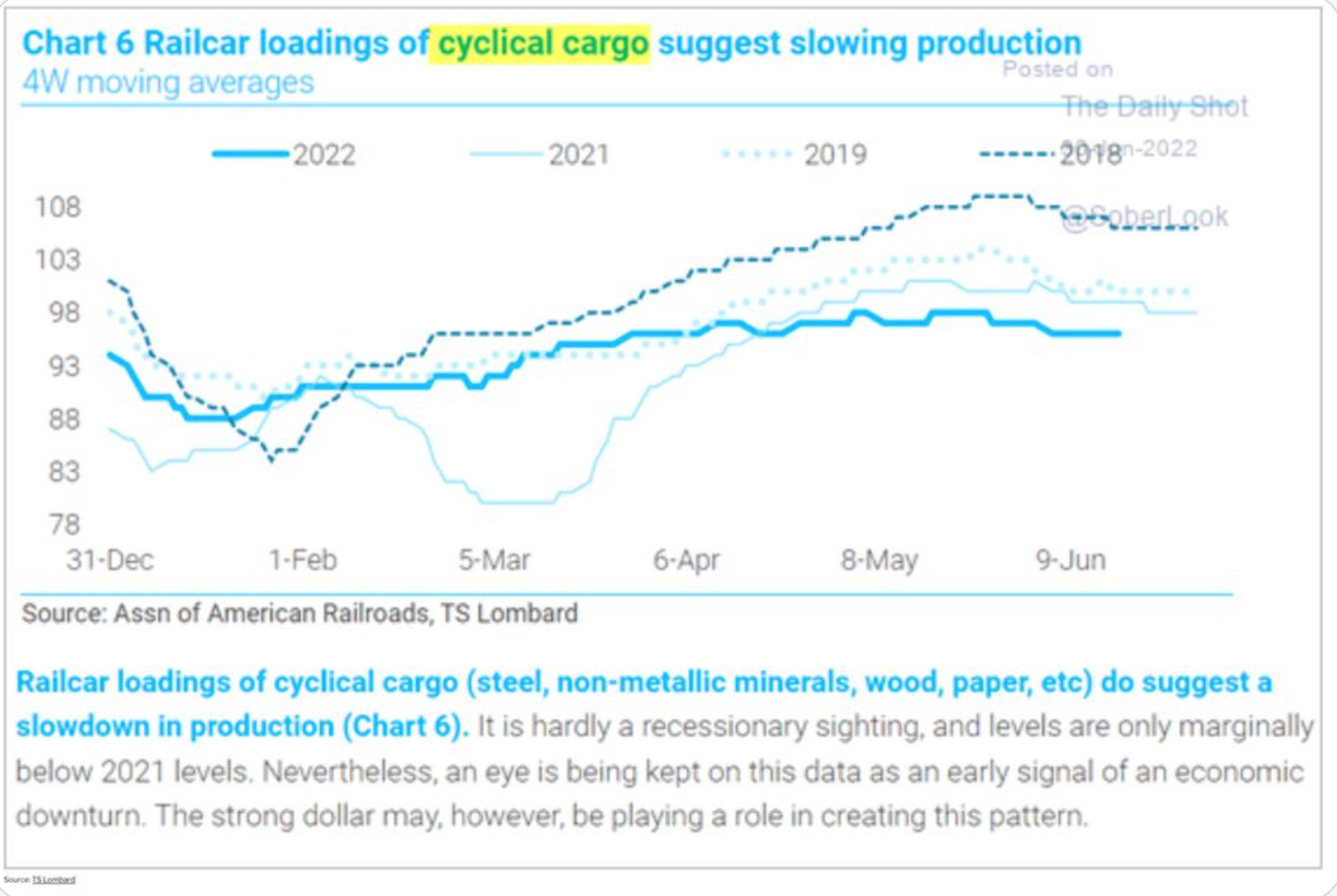

On America’s railroads the loading of cyclical inputs to production – steel, wood, paper etc – is well below the rates seen in recent years.

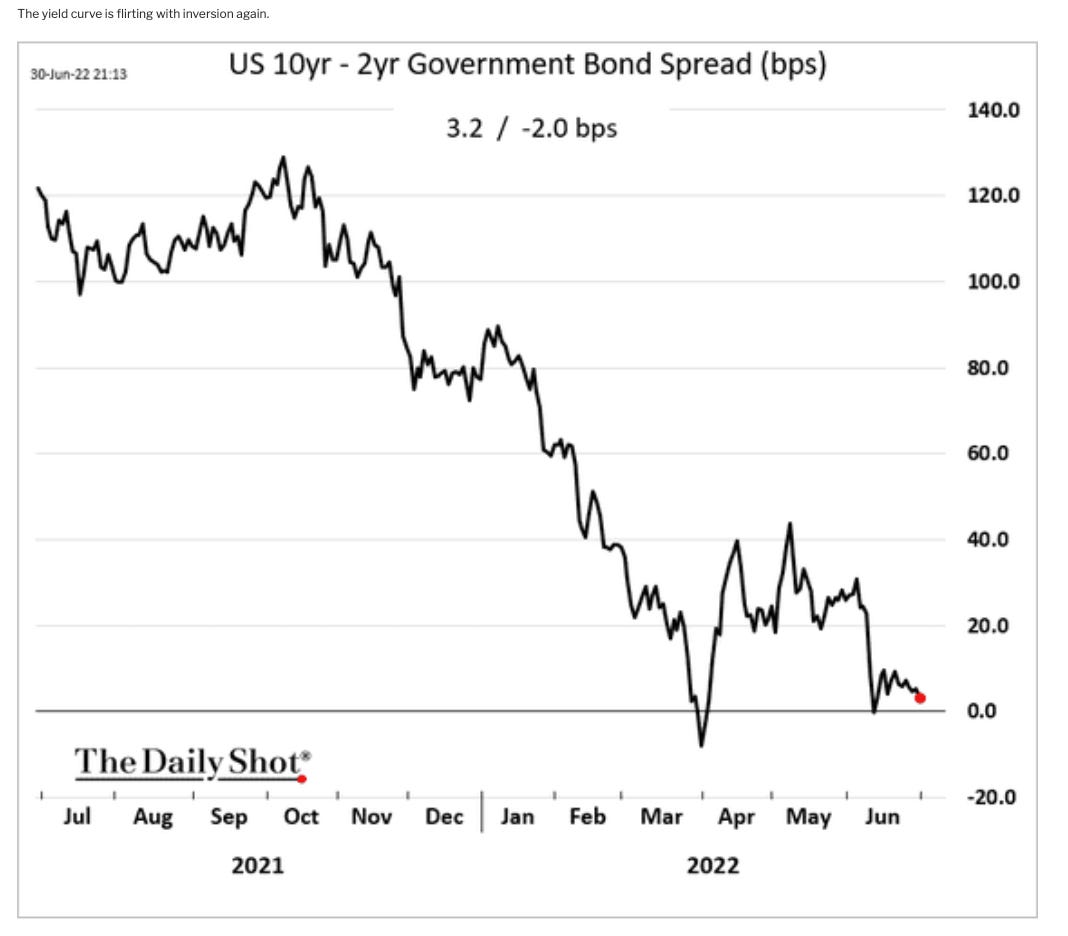

As the conviction of a recession has grown in financial markets, longer-dated US Treasury debt has become more attractive (its value is less likely to be eroded by inflation) and the yield spread between short-term and long-term debt has tightened.

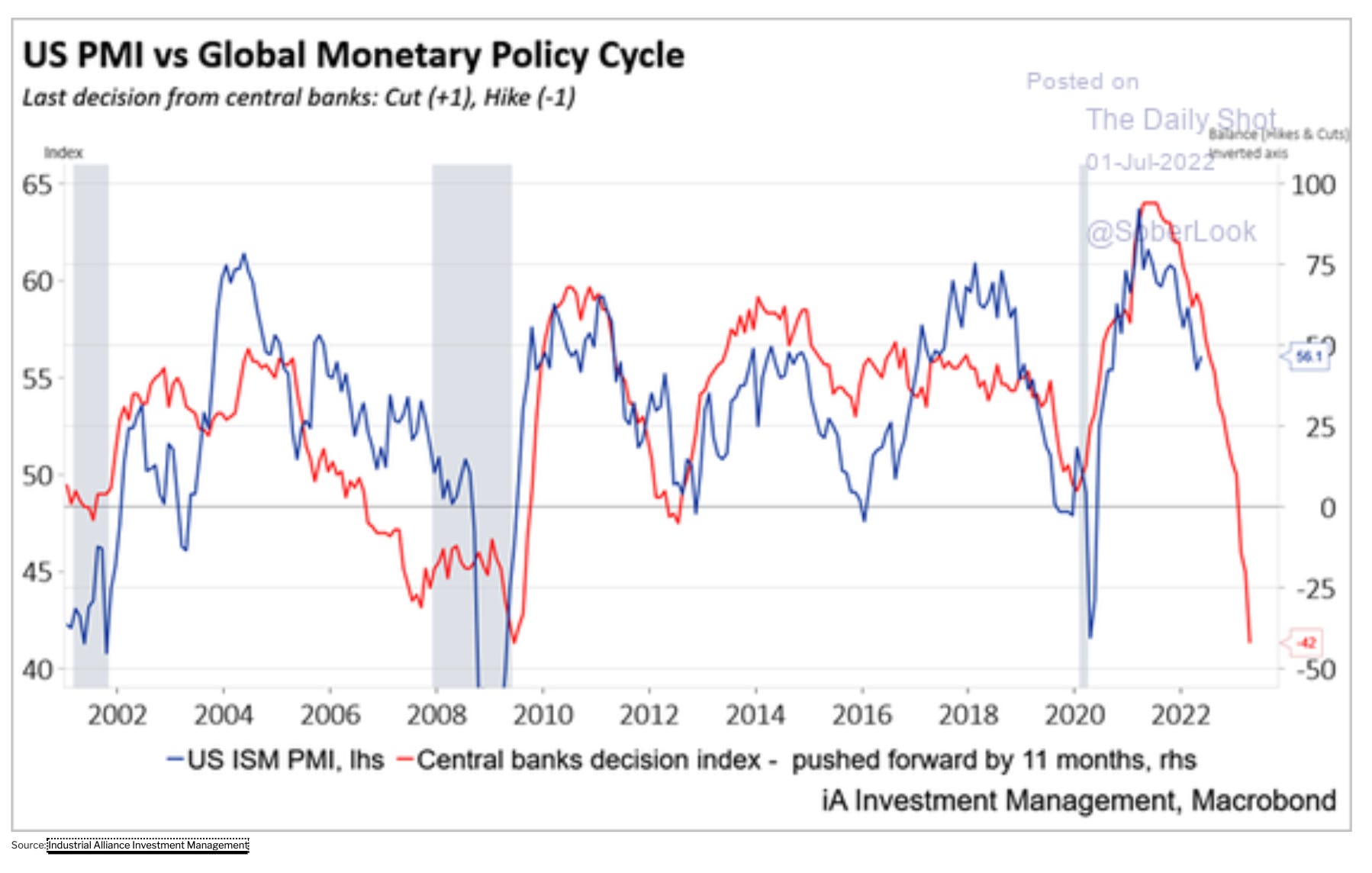

The Fed is the lead elephant of the central banks, but the tightening of policy by central banks around the world generally betokens nothing good for US business. It would be surprising if we did not see a significant drop in the US Purchasing Managers Index in the coming months.

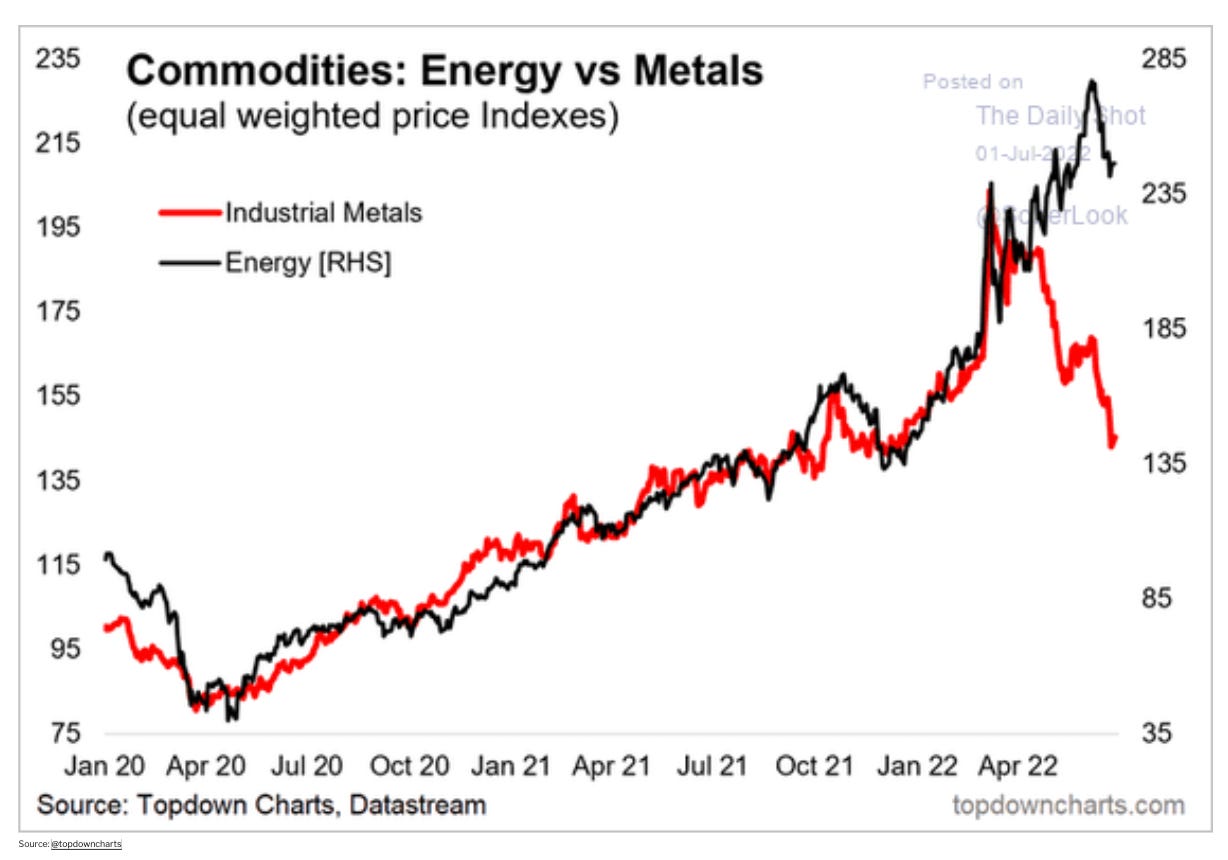

The shock of Russia’s war on Ukraine has concentrated global attention on the prices for energy and food. This reinforces the impression of a world facing an inflationary wave. But with regard to the business-cycle, the price of industrial metals may be a more telling indicator. Copper, known as the commodity with an economics PhD, has sold off hard, today hitting 17-month lows.

All told, you might say that this is a gloomy outlook. And there are those who are increasingly skeptical of the possibility of a soft landing. But, it is surely far too early to tell. If the aim of the game is to control inflation by bringing about a slowdown, then the evidence we are seeing, so far, is precisely what you would look for. What remains to be seen is how the different recessionary forces interact, and whether they brew up into really heavy weather.

*****

I love writing Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

June 26, 2022

Chartbook #131 Calibrating the polycrisis – with the help of the Bank of International Settlements

The polycrisis we are in the midst of, is fast-moving, complex, heterogeneous, interconnected, explosive. One comfort, at least intellectually, is that we are in it together. If you are feeling confused and overwhelmed you aren’t on your own. No one is outside the current conjuncture. There are different vantage points, with different perspectives, but no single point and no single theory that encompasses our reality and provides an absolute point of view.

That is a source of conflict, of course, but also of potential solidarity and cooperation.

In intellectual terms what we have at our disposal are tools for mapping. I’ve been experimenting with Krisenbilder (crisis pictures) and, in the last Chartbook, with a crisis-matrix. But tracking vectors of influence only takes you so far. It is far easier to draw maps of interconnections than to gauge their quantiative scale and importance.

Quantification is not the high road to social and economic knowledge. Without conceptual reflection, quantification is often misleading or, even, meaningless. But without it, we are also adrift. Without quantification, we have no sense of proportion, no way of scaling the importance of key interactions. No way of prioritizing and managing trade offs. No way of gauging the balance of forces.

Quantification is also, however, technically demanding. It can be expensive and it presupposes power relations that allow data to be extracted, collected and processed. This gives certain observatories a privileged role in mapping the polycrisis.

The Bank of International Settlements is one such observatory. The economists and statisticians at the BIS have for many years now made their organization into one of the key observatories of financial capitalism, remarkable not only for the wealth of the data they gather but also for the sophistication of their conceptualizations. The politics of the BIS may at root be conservative. Institutionally, the BIS sits at the very heart of financial power. But in their conceptual framings the analysis offered by BIS economists has often been nothing short of radical.

All this makes the Annual Economic Report from the BIS essential reading. I am going to be feasting off it for the coming week. Today, I want simply to read the first chapter of the Annual Economic Report, as a highly sophisticated, quantified mapping of the polycrisis.

Like the World Bank, the BIS economists start by remarking on the rollercoaster we have been on since 2020. In 2021, global GDP is estimated to have grown by 6.3% in real terms, its fastest rate in almost 50 years. Now, as the World Bank pointed out in its Economic Prospect a few weeks ago, we are experiencing the sharpest slowdown in growth in 80 year. Not the lowest growth, by any means, but the sharpest downshift in growth prospects. Together these two simple quantitative statements convey some of the drama of our current moment.

What is driving this? Again the BIS has data to hand. Global data on retail and leisure activity – an astonishing number to have at our finger tips – slowed suddenly over the winter of 2021-2 as Omicron hit. Then came Putin’s war on Ukraine. It is tempting to attribute our entire malaise to this wanton act of aggression, but the data clearly refute that simplistic idea.

The war has depressed GDP growth expectations and this is associated to some degree with the share of a country’s trade going to Russia. But the association is not strong and the effect is not large. So far, a least, as far as the world economy is concerned, Russia’s war in Ukraine is secondary to other disruptive shocks.

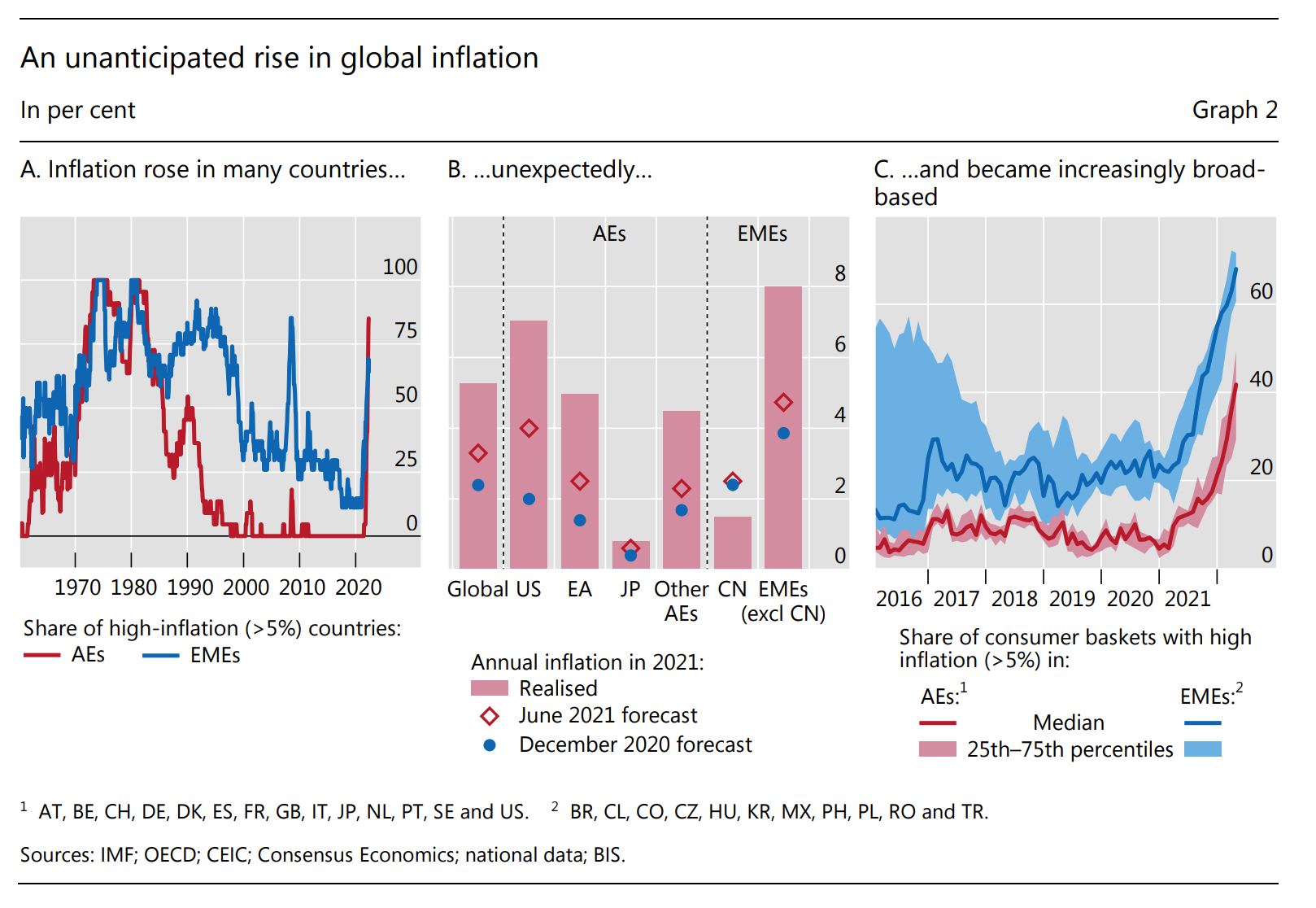

The source of the pessimism about future growth is less the war than the sudden surge in inflation and the likely reaction of central banks to that surge. In the second half of 2021, in the months following the last BIS Annual Economic Report, inflation rose rapidly – initially driven by energy and other commodities – and then broadened out, so that by the spring of 2022, in advanced economies, where inflation is normally more sluggish, 40 percent of the goods counted in the inflation indices were experiencing inflation of more than 5 percent.

Of course it is true that Putin’s war on Ukraine has delivered a nasty shock to commodity markets and this feeds through to inflation. But how large is this effect? As the BIS comments

Estimates of the effect of commodity price increases across a broad panel of countries indicate that a 30% increase in oil prices, combined with a 10% rise in agricultural prices – roughly in line with those seen since the start of the year – has historically been associated with a 1 percentage point increase in inflation in the following year.

So Putin’s war is stoking inflation, but so far at least, it is not the main driver.

Furthermore, though inflation is widespread it is not general to the world economy. China and Japan, which dominate the East Asian economic region, have seen a very modest inflation.

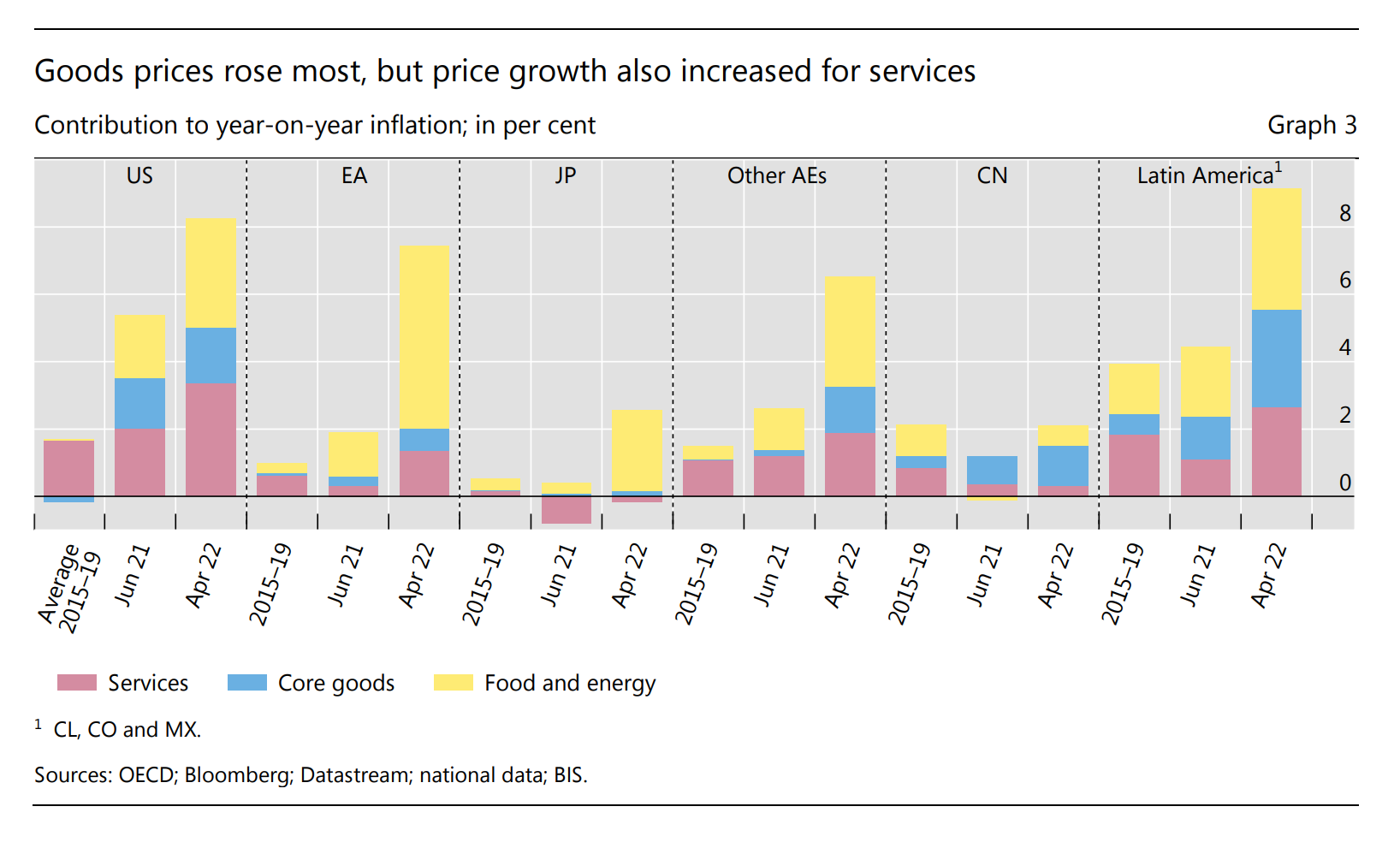

Inflation in Europe has been far more rapid. But as of April 2022 more than two-thirds of inflation came from food and energy. This makes for an interesting contrast with the Americas – both in the United States and Latin America – where inflation is fast and involves all areas of the economy, including services (which are by far the largest part).

As the BIS remarks, the combination of inflationary and recessionary forces that we are currently facing, along with financial stability risks is “historically unprecedented”. It is worth saying that when the BIS says this, it is not merely an impressionistic remark intended to convey the drama of the moment, or an overused journalistic cliché. It is a precise statement based on the comparison of the current conjuncture with all relevant data in its database, stretching back to 1945. It is all the more attention-grabbing for that.

To repeat: In the last 18 months we have seen the fastest global growth in 50 years, followed by the most rapid slowdown, creating what is in the BIS’s view, a global economic configuration unprecedented in history.

Specifically, we have never seen such a combination of already rapid inflation and rapidly slowing growth with elevated financial vulnerabilities, notably high indebtedness against a backdrop of surging house prices. As the BIS spells out.

Prior to the mid-1980s, recessions were generally preceded by high inflation and the associated monetary tightening while the financial system was largely repressed. Since then, Covid aside, recessions have typically followed financial cycle peaks, with inflation remaining subdued during expansions and hence calling for relatively little monetary policy tightening.

As the BIS goes on to remark, “(t)he absence of historical parallels makes for a highly uncertain outlook”.

In the current conjuncture, if you aren’t puzzled you don’t get it. This isn’t your common or garden slowdown. Admitting to disorientation is a sign of honesty and realism.

What worries the BIS is that in seeking to tame this unfamiliar configuration of forces, central banks may have to resort to a monetary tightening that will result in very large real economic costs and those in turn could have serious social and political consequences.

The historic paradigm for a “hard landing” is the “Volcker shock” of 1979. But our inflation rates are not those of that period, nor are wage and price-setting today governed by a similar power balance. On this, see earlier Chartbooks discussing BIS work on the wage-price spiral and more to come this week.

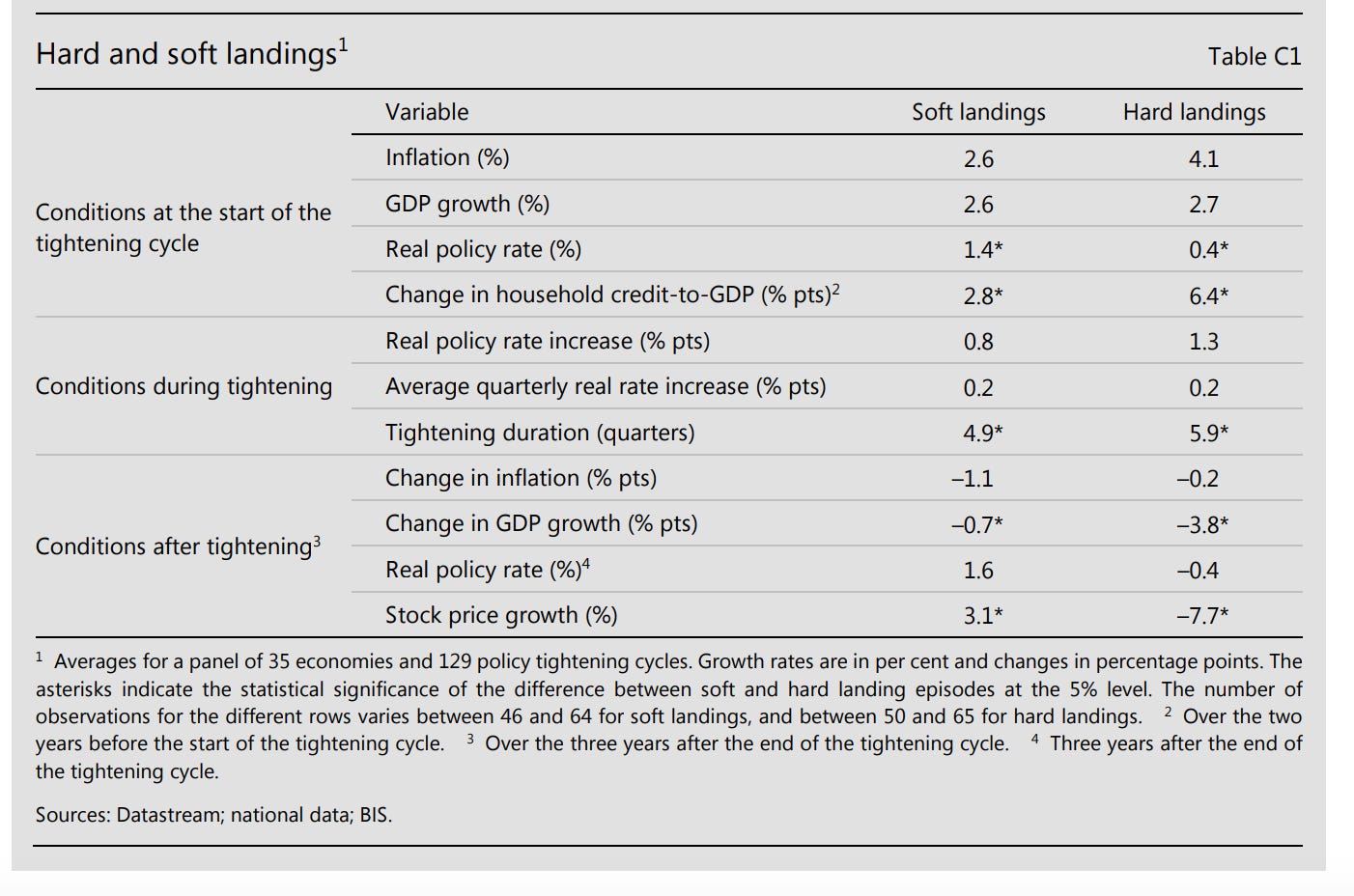

Though it was dramatic and paradigm-defining, the “Volcker shock” was highly unusual. What about the experience more generally with monetary policy tightenings? Surveying the experience of 35 countries over the period 1985–2018, the BIS concludes that historically, about half of all monetary policy tightening cycles have ended in soft landings. In half of all cases, central banks that tightened monetary policy for three consecutive quarters managed to do so without provoking a recession (i.e. two quarters of negative growth).

That sounds like good news. A hard landing is not foreordained. Bu what worries the BIS, are the very different conditions in which hard and soft landings occurred.

As the BIS warns:

hard landings are more likely when monetary tightening is preceded by a build-up of financial vulnerabilities. In particular, faster growth in credit relative to GDP prior to a tightening episode is associated with hard landings (Table C1, top panel). Intuitively, financial vulnerabilities are likely to reinforce the contractionary effects of tighter monetary policy on GDP growth. Moreover, heightened vulnerabilities mean that a growth slowdown is more likely to trigger a recession. The influence of credit growth on the probability of a hard landing is also consistent with the observation that financial cycle peaks have tended to coincide with recessions since the early 1980s, lining up with the sample in this exercise.3 Financial vulnerabilities are more likely to emerge when interest rates are low. Reflecting this, hard landings are also commonly associated with low real interest rates prior to the start of the tightening episode. For example, the average real policy rate at the start of tightening cycles that end in hard landings is 0.4%, compared with 1.4% at the start of those that end in soft landings. Inflation is also on average higher before hard landings than it is before soft ones, although the difference between the two is not statistically significant.

A credit build-up facilitated by low interest rates is precisely what describes our situation in 2022-23. A hard-landing may no be foreordained, but what the BIS is telling us, is that central bankers have never attempted to stop an inflation as rapid as the one we have seen in the first half of 2022, with the level of debt build-up we have seen since the early 2000s.

How bad could things get? As the central banks led by the Fed tighten policy, how might the different elements of the polycrisis interact?

One important channel is the debt service ratio – the share of private income that goes to pay interest owed on debts. In recent years, corporate finances and real estate markets have been fueled by historically low rates. Until the summer of 2021 the expectation was that those would persist for the foreseeable future. Now, markets are pricing in a significant rate rise. In agreement with central bankers they project rates rising to c. 3 percent over coming years. That has been enough to trigger a market sell off and significant symptoms of a slowdown in manufacturing and employment in the United States. The BIS, however, has long been suspicious of the complicity between complacent markets and compliant central bankers. What if, fighting inflation requires a more significant rate shock? Assuming that a Volcker-scale shock is unrealistic – he pushed rates to close to 20 percent – what if, the Fed tightens rate at the same pace that Alan Greenspan did between 2004 and 2006. This would imply tha they would reach five percent by 2024.

The center piece of the analysis in the first chapter of the BIS report, is a simulation of the outlook for twelve advanced economies, with their GDP weighted by PPP – in effect a synthetic unitary advanced economy – based on data compiled since the 1980s. Looking forward, the BIS evaluates three scenarios. A hypothetical scenario in which central banks do not engage in tightening. One in which they tighten at the rate that the market is currently pricing in. And one in which they tighten more aggressively, at the rate that the Fed adopted in 2004-6.

Clearly, if policy rates go to 5 percent rather than 2.5 percent, the impact on house prices, equity markets and GDP will be much more severe. But how bad, is bad? Even with a severe tightening, the BIS is not forecasting anything like the shock of 2008 either in real estate or equity markets. There is a significant loss in GDP, but this is relative to the growth trend of the hypothetical “no-change in rates” scenario. It is not obvious to the naked eye whether even this worst-case scenario actually implies a serious recession.

The BIS seems somewhat sheepish about this rather undramaic conclusion, adding:

these results may understate the GDP response to tighter monetary conditions, which would occur against a backdrop of historically high debt levels, whose effects on growth may be felt more keenly when asset prices are falling, and the growth headwinds of the higher commodity prices and enhanced geopolitical uncertainty described above.16

Furthermore

the results of this simulation exercise are purely illustrative. In particular, they are based on average historical relationships since the mid-1980s, which may have evolved over the past four decades. The use of cross-country averages also masks considerable variation in exposure to higher policy rates across jurisdictions. And, even for individual countries, the simulations are subject to considerable uncertainty.

What kind of risks might such a high-level exercise in simulation be missing?

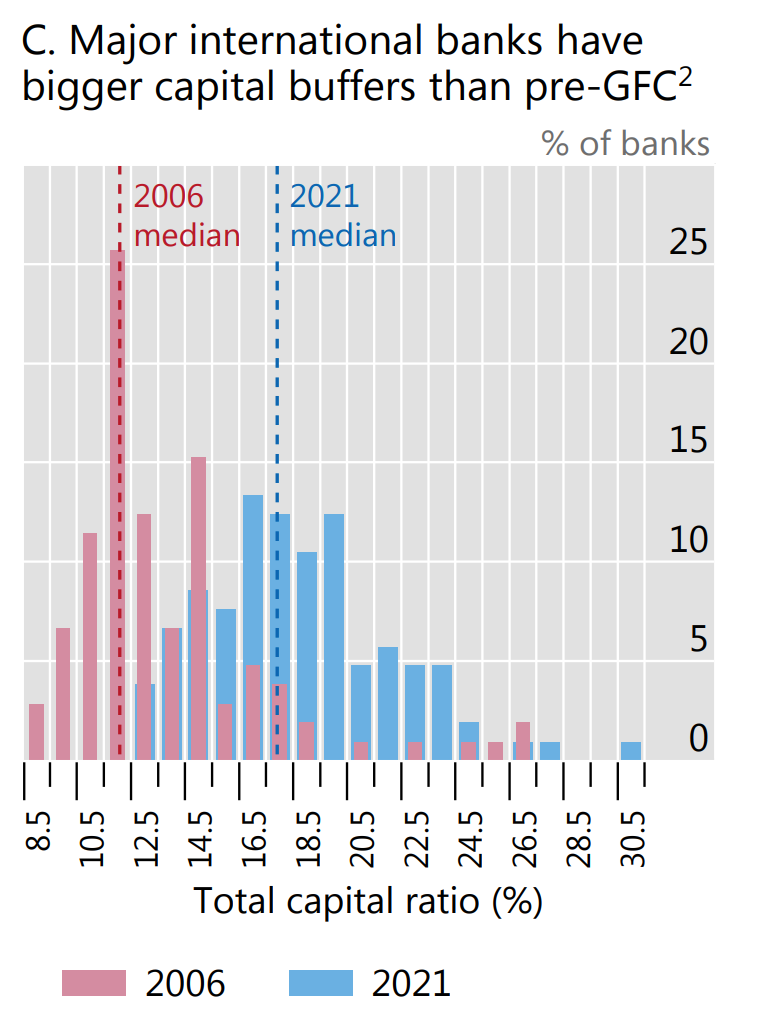

One obvious concern is that a sudden tightening in interest rates may produce a wave of bankruptcies amongst stressed debtors unleashing havoc in the banking system – the 2007-8 scenario. According to the BIS, in a “2004 tightening” scenario, bank credit losses might rise to the level seen after 2008. But, as the BIS immediately adds, there is good reason to think that thanks to macro-prudential regulation and changes in the banking business, the banking system today is more resilient than it was in 2008.

The main worry may not be in banks but in what the BIS rather primly calls non-bank financial institutions i.e. shadow banking.

The collapse of Archegos Capital Management in April 2021, and the attendant stock market disruptions, is a leading example. In that instance, not only was the capital of Archegos largely wiped out, but several banks that provided it with prime brokerage services also took significant hits to their own capital buffers.

Or, remember back in February and March 2022, when we were worrying about financialised commodity markets.

These markets came under strain when the war in Ukraine broke out, as sharp rises in commodity price volatility triggered large margin calls in derivatives markets. The frantic search for cash to meet those calls briefly led to stress in dollar funding markets, as reflected in the spreads to OIS of forward rate agreement rates (Graph 19.A). At the same time, some futures markets saw substantial increases in initial margin requirements, leading some commodity traders to stop hedging their exposures in those markets and absorb price risk themselves (Graph 19.B). This, in turn, saw commodity end users, such as airlines, face difficulties hedging their own exposures. While the tensions ultimately eased, the underlying vulnerabilities could resurface if price volatility spikes again.

Then there are sovereign debt markets. The biggest of all is in the US and already in September 2019 there were ructions in the Treasury repo market. In March 2020 the market stalled and in late 2021

liquidity in US Treasury markets diminished as broadening inflationary pressures led investors to anticipate an imminent policy shift. Market conditions worsened further as the review period progressed, with implied volatilities in fixed income markets near historical peaks, particularly for short-term rates (Graph 19.C).

The Eurozone too would feel the pressure with spreads between Bunds and Italian sovereign debt rising alarmingly.

All of these are polycrisis mechanisms, which have been exposed in the last few years. So far they have been contained. But that was against a backdrop of near-zero or even negative interest rates, with benign inflation.

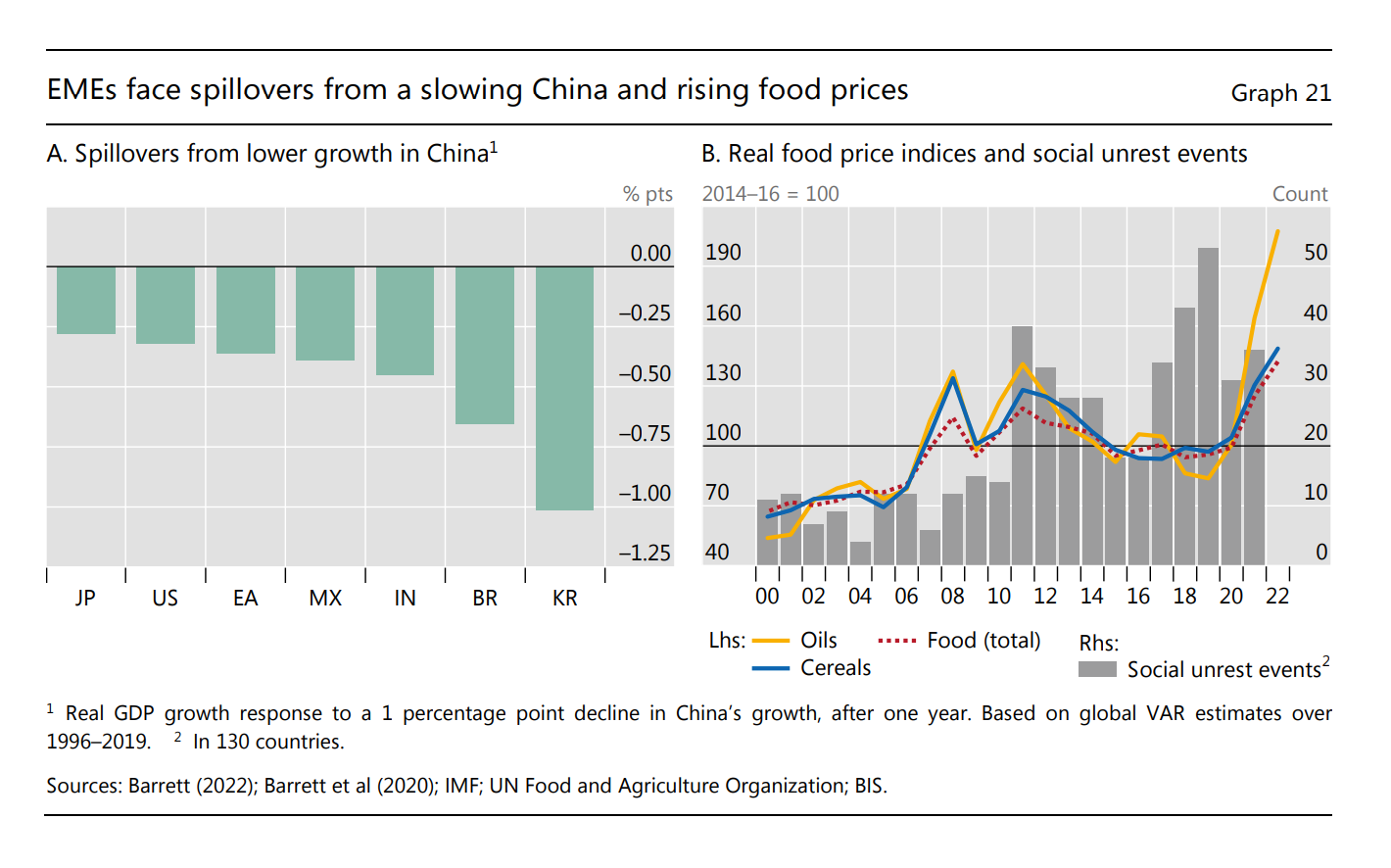

The simulation exercise that anchors Chapter 1 of the BIS report is centered on advanced economies. But as the BIS points out, in a world of rising rates it is the emerging market economies that will feel the pressure most intensely. And it is in relation to the Emerging Markets that the analysts of the BIS really allow free rein to their polycrisis-imagination. Here, it is not just economic forces, but the pandemic and social and political risks that weigh in the balance. As they remark:

Many EMEs (emerging market economies) are highly exposed to stagflationary risks. Growth prospects had already deteriorated pre-pandemic, with potential growth rates on average 2 percentage points lower than before the GFC (2008). In addition, in many EMEs pandemic scarring is more evident than in AEs. By the first quarter of 2022, the median length of full school closures due to Covid-19 had amounted to 29 weeks in Latin America and 16 weeks in emerging Asia, compared with six weeks in AEs.19 Labour force participation is also recovering more slowly. In Latin America, in particular, participation rates in 2021 were some 2 percentage points below pre-pandemic levels.20 Many EMEs are highly exposed to slower Chinese growth, especially countries in emerging Asia and some commodity exporters (Graph 21.A). And, in countries where vaccination rates lag, health and economic activity could be more vulnerable to further pandemic waves. Even if growth does not decline, higher inflation tends to be more disruptive in EMEs. Since inflation expectations are less well anchored in some of these countries, not least in Latin America, larger nominal policy rate increases are required to control inflation. Surging food prices are also more disruptive. Sharp rises in food prices have been associated with social instability and the imposition of export controls in the past, with recent price levels surpassing those seen during the food price spike of 2011 (Graph 21.B).21 And while regulated food and energy prices, and the associated subsidies, will lower the immediate pass-through to headline inflation in some EMEs, they come with a fiscal cost and can create economic distortions.22 Combined with growing demands for social spending in the pandemic’s aftermath, larger fiscal deficits could eventually feed through into exchange rate depreciations and inflation (Chapter II).

This remarkably rich description of the polycrisis at work is accompanied by a panel that seeks to quantify two elements of this risk.

The sheer incongruity of these two graphs is worthy of note. On the left you have a macroeconomic assessment of the impact of a slowing Chinese economy on the GDP of economies around the world. It shows that South Korea and Brazil are far more exposed than Japan. Meanwhile, on the right you have a graphic illustrating the association between rising prices for cooking oil, food and cereals and incidents of social unrest across no less than 130 countries.

And if this were not enough, to illustrate the extraordinarily far-flung nature of the current polycrisis, the upshot of the BIS’s policy analysis is even more illustrative.

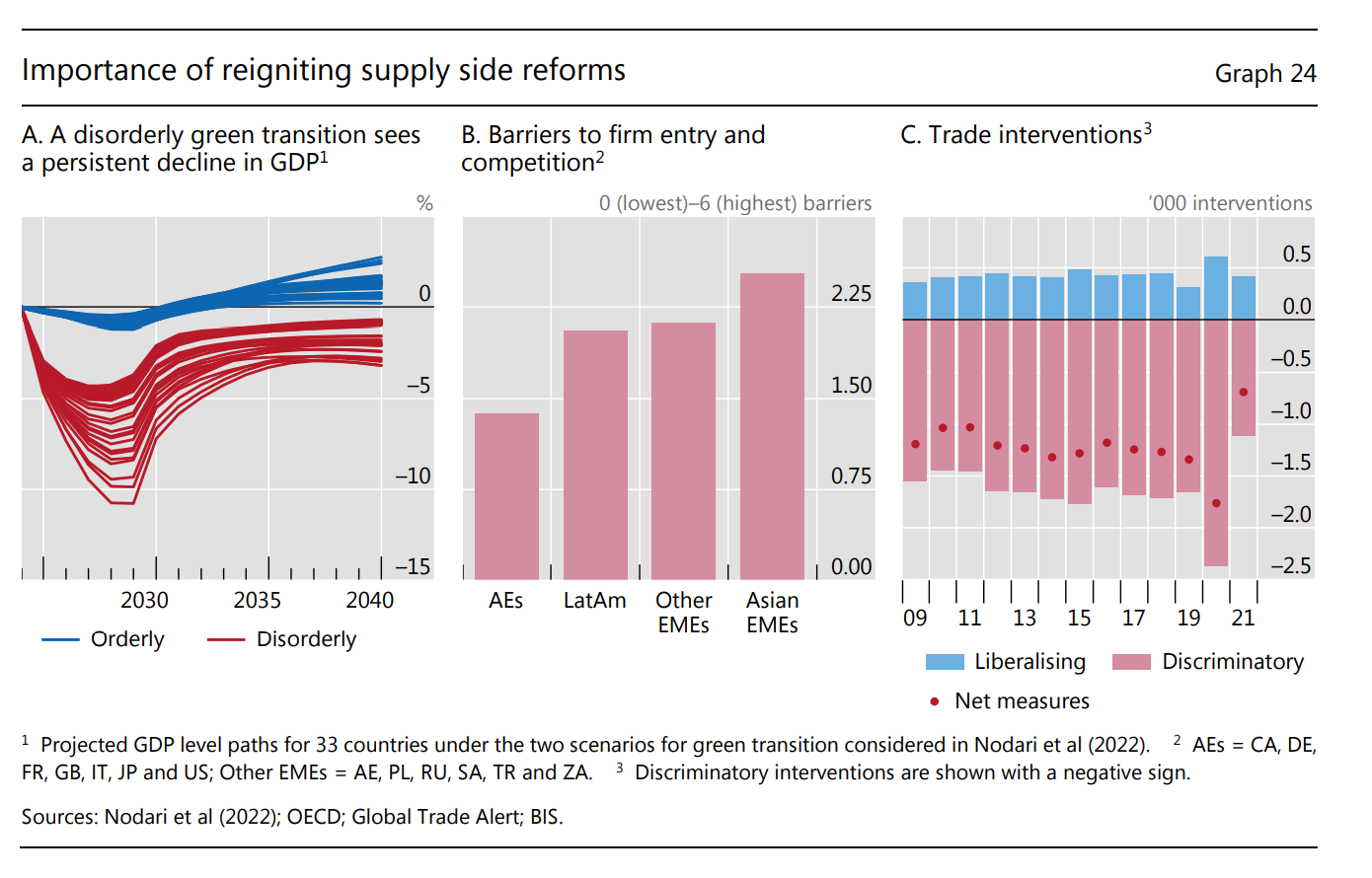

Clearly, the BIS thinks that halting the current inflationary surge is associated with risks that ramify in many different directions – from loss of exports to China, to food riots, by way of shadow banking failures and possible ructions in financialized commodity markets. To have any hope of managing such a multiplicity of heterogeneous risks you need a policy toolkit that is similarly multi-faceted. Central banks can raise interest rates, but they should also be using macroprudential tools to manage risk in the financial system. Fiscal policy has a role to play. But above all the BIS, which has a distinctly Austrian flavor to its analysis, wants policy-makers to refocus on so-called supply-side policies to boost economic growth.

So what does that entail? Well, unsurprisingly, the BIS favors the kind of neoliberal measures that promote competition in markets (panel B) and reduce impediments to international trade (panel C). The former pertains to political economy. The latter to geopolitics. But then look at panel A!

In the midst of managing the most rapid bout of inflation since the 1980s, the BIS thinks it is relevant – along with worrying about food riots in low-income countries – for policy-makers to focus on ensuring a timely, and efficient energy transition. Why? How does the energy transition connect to the current inflation problem and the proper stance of macroeconomic policy?

Simulations suggest that an orderly transition that features a timely increase in green energy investment could impose relatively small near-term costs and deliver persistent long-term gains, measured in terms of economic output (Graph 24.A). By contrast, a disorderly shift, where the adoption of clean energy technology lags but carbon-intensive energy sources are shut down rapidly, would involve significant costs in both the short and long run.

Ultimately, supply side factors determine the basic trade offs between prices and output. Macroeconomic stabilization policy – monetary or fiscal can only do so much. And the supply side is, well, everything – the entire structure of production and distribution of commodities, human bodies, natural resources, and energy flows. It is across that biopolitical, geopolitical and geoeconomic terrain that the polycrisis is playing out, in interconnected, resonating, complex movements, punctuated by violent spasms of crisis.

*****

I love writing Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

June 24, 2022

Ones & Tooze: How Flying Got to be so Miserable

On this episode, Adam and Cameron explain why flight disruptions and cancellations are the new normal. They also discuss the economics of summer vacation.

Find more episodes and subscribe at Foreign Policy

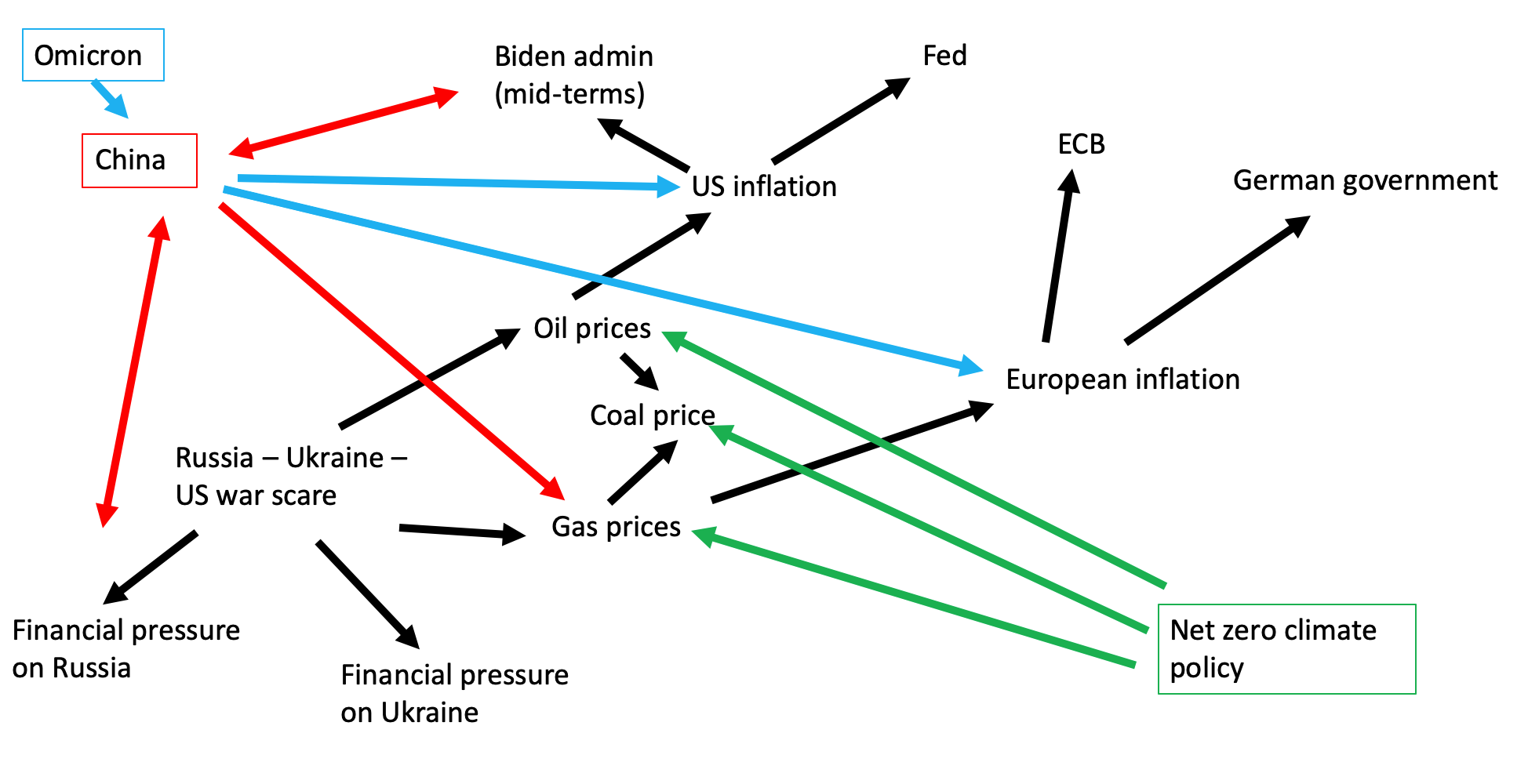

Chartbook # 130 Defining polycrisis – from crisis pictures to the crisis matrix.

In Chartbook #73, back on January 21st this year, I proposed Krisenbilder – crisis pictures – as a way of making sense of what then looked like a complicated pattern of stresses around the world scene.

I proposed the schematic because it seemed a useful way of mapping interconnected forces in a heuristic way. As it turned out, it succeeding in capturing quite a lot of the dynamics that have subsequently convulsed the world.

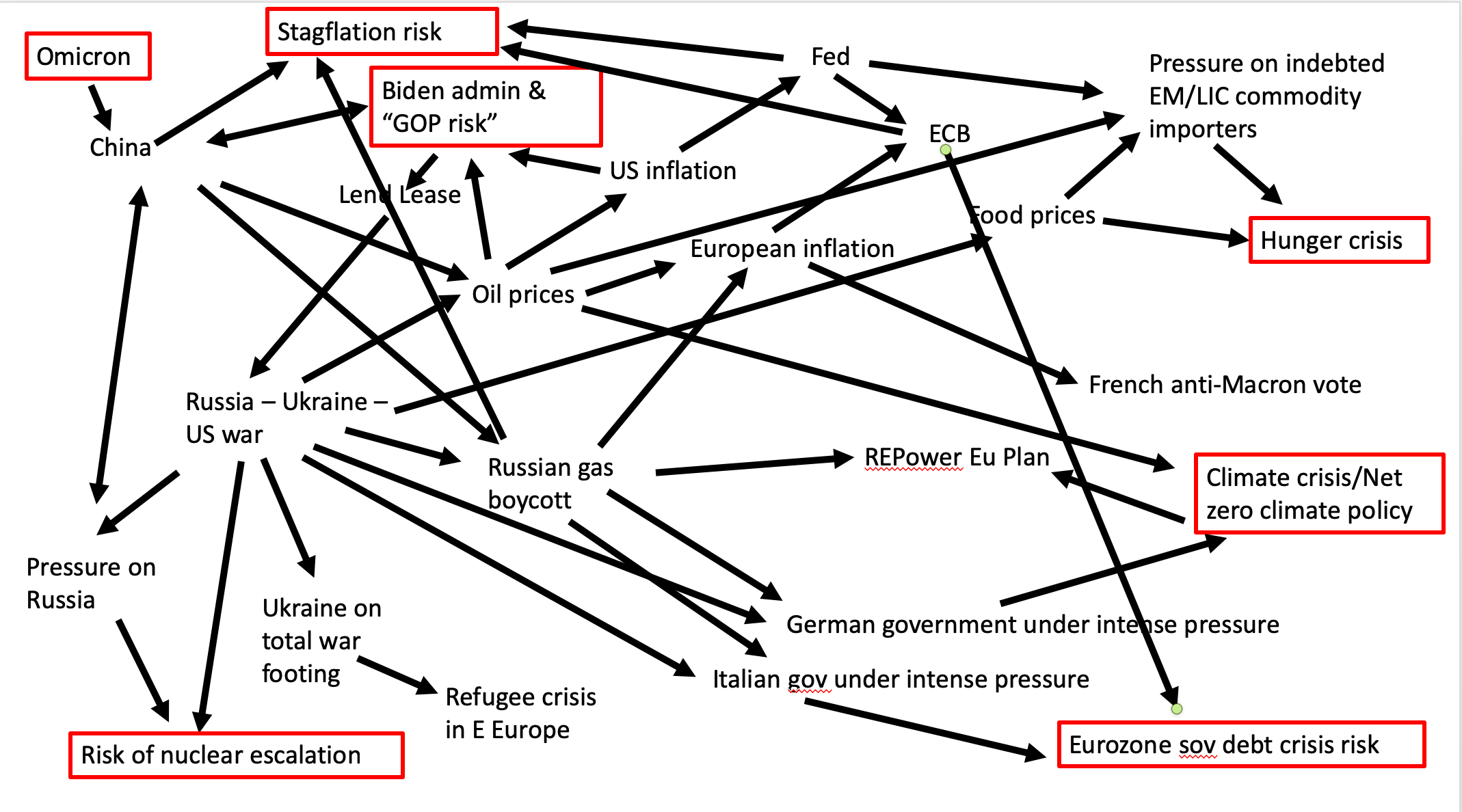

That was January 21st. The war unleashed by Russia on February 24th has added spectacularly to the scale of tension and the complexity of the interconnections.

What was once a relatively legible map has become a tangled mess.

I don’t claim any originality for the exercise. All of these connections are routinely discussed in intelligent analysis. But pulling all these well-known influences together in a single chart does convey a sense of what a complex situation we are dealing with.

To make matters even more complicated, this synchronic presentation obscures the historical genesis of these forces. Stresses in energy and food markets were already very evident in 2021. The war has had the impact it has because it has exacerbated existing tensions. Food prices were already rising in 2021 and provoking warnings of a crisis to come. Energy markets were stressed well before the war broke out. Now both stressors are knotted together with the war.

I have highlighted in red what emerge as a series of macroscopic risks, all of which may come to a head in the next 6-18 months.

All of them, from the risk of nuclear escalation to global stagflation, are familiar from public commentary on the crisis. The selection is debatable. Should the EM/LIC debt crisis be classified as a macroscopic risk? Perhaps.

What seems worthy of note is, first of all, how many radical challenges there are on our radar. I count seven, without even including a debt crisis in several EM/LIC.

Second, what is striking is the deep uncertainty that surrounds several of them (e.g. new COVID variants, or nuclear escalation). These are tail risks which can no longer be ignored but to which it is hard to attach a real probability.

Thirdly, they are all happening at once and several of them reinforce each other. By early 2023 it is entirely possible that we will see a dangerous new COVID variant that defeats even the best vaccines, a shift to active use of nuclear weapons in the war in Ukraine, a rampant Republican party under the banner of MAGA, global stagflation and a fossil fuel ramp up to meet escalating energy shortages, furthermore in Europe the breakup of Mario Draghi’s coalition in Italy, helping to trigger surging spreads in the Eurozone met by an inadequate response from the ECB.

We would be unlucky if all of those things did happen. But it is well nigh inconceivable that at least one of them will not. The defeat of the Democrats in the US, is surely the most likely outcome in the upcoming midterm elections.

Some of these crises are what you might call overarching. A lethal new COVID variant would be a game-changer in ever respect. The same could be said for a move by Russia to the use of nuclear weapons.

Other forces of crisis tend of offset each other. A new wave of COVID-lockdowns in China would likely help to break momentum in commodity markets and tend to push prices for things such as oil and iron down downwards, easing inflationary pressure.

Other effects are more ambiguous. If a Trumpite GOP storms back to power in Washington that will likely reduce the pressure in Congress to up the ante in the struggle with Russia. On the other hand it may make the Biden administration more aggressive, since foreign policy will be one of its only trump cards (no pun intended), and one around which it might find majorities in the Senate.

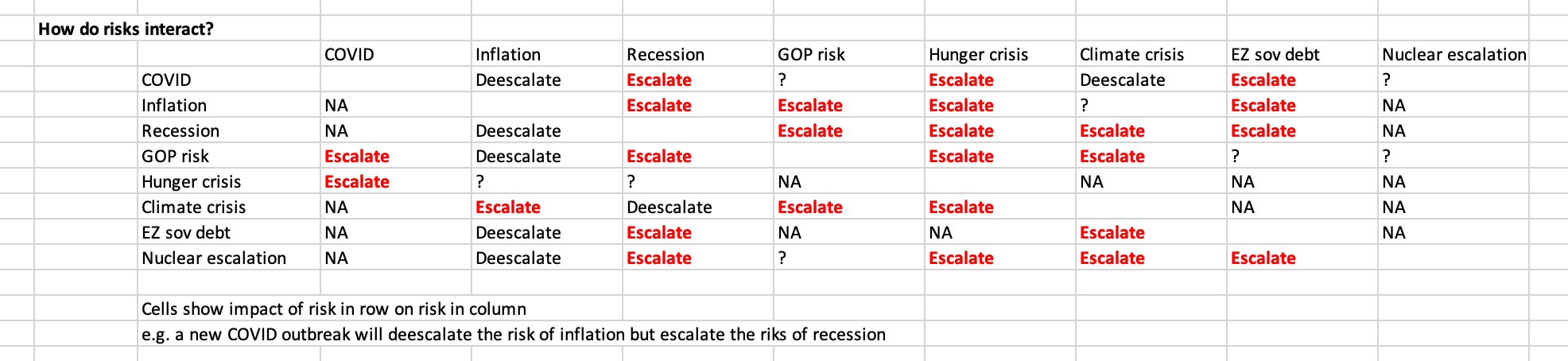

To try and summarize these effects I compiled the following, entirely provisional and highly debatable matrix of interactions between the different macroscopic risks facing us over the next 6-18 months. The question that the table asks is how do the risks listed in each row of column 1, affect the risks laid out from left to right across the table.

For sake of clarity I have divided the stagflation risk into a risk of recession and a risk of accelerating inflation.

What this matrix helps us to do is to distinguish types of risk by the degree and type of their interconnectedness.

The risk of nuclear escalation stands out for the fact that it is not significantly affected by any of the other risks. It will be decided by the logic of the war and decision-making in Moscow and Washington. A food crisis does not make a nuclear escalation any more, or less likely. On the other hand, a nuclear escalation would, to say the least, dramatically escalate several of the other risks.

Continuing inflation will likely function as a driver of several other risks, but those risks in turn (COVID, recession, EZ sov debt crisis) will likely deescalate the risk of inflation. I would not say that this is a forecast, but it does bias me towards thinking that inflation will be transitory. Most of the big shocks that we may expect, tend to be deflationary in their impact.

Conversely, a recession seems ever more likely in part because the effect of most of the bad shocks we may expect – from COVID, mounting inflation, or a fiscal deadlock in Congress – point in that direction.

The obvious next step is to ask whether the feedback loops in the matrix are positive or negative. So, for instance, a recession makes a Eurozone sovereign debt crisis more likely, which in turns would unleash serious deflationary pressures across Europe. Conversely, inflation in fact seems self-calming. The effects it produces tend rather the dampen inflation than to feed an acceleration. At least as I have specified the matrix here.

A global hunger crisis seems alarmingly likely in part because all the other major risks will exacerbate that problem. A hunger crisis, however, will largely affect poor and powerless people in low-income countries, so it is unlikely to feedback in exacerbating any of the other major crises. It is an effect of forces operating elsewhere, rather than itself a driver of escalation.

To this extent the matrix becomes a way of charting the power hierarchy of uneven and combined development. Some people receive shocks. Others dish them out.

I am not committed to this sketch, or this matrix in anything other than a heuristic way. The analysis could be multiplied and expanded in many directions. With regard to the hunger crisis, for instance, our conclusions of its likely impact would be different if we add in the question of migration.

Several of the interactions I have labeled are highly debatable. Some I have simply left blank, NA or marked with a question mark. Is it right, for instance, to assign an escalatory effect to the climate crisis on inflation? In this case I am invoking the greenflation concept of which I am somewhat skeptical. Likewise I say that a recession would exacerbate the climate crisis because I expect it to lead to a recession in green investment. But these effects, their scale and sign are up for debate.

Overall, what the combination of the crisis picture and the matrix help us to see is that not only do we face multiple macroscopic risks hedged with great uncertainty, but their interactions tend to be escalatory.

This is not inevitable, this is not a prophecy of doom. But it is an assessment of multiple and compounding risks.

It may perhaps be taken as the definition of the polycrisis, the concept borrowed by way of Jean-Claude Juncker, that I invoked in my book Shutdown.

A polycrisis is not just a situation where you face multiple crises. It is a situation like that mapped in the risk matrix, where the whole is even more dangerous than the sum of the parts.

****

I love putting out Chartbook. I am particularly pleased that it goes out for free to thousands of subscribers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options:

June 19, 2022

Chartbook #129 Love Actually, the Columbia MA Commencement 2022 and the global future.

While sorting through a pile of clothes preparing for a summer trip, I came across the folded text of the Columbia MA Commencement speech that I had the privilege of giving this year.

It brought back to me some of the emotions of May 2022. It was good to reread it.

“Well, hello, graduating cohort of 2022. First things first. Congratulations on this wonderful occasion.

You are taking a graduate degree from

Columbia university

. That is a huge deal. Let me say that again. That is a huge achievement.

It has taken a lot to get you here.

You and everyone who has supported you deserve huge congratulations. Families. Teachers take a bow!

It’s a beautiful occasion. YOU are all looking great. As my daughter tells me, Columbias’s light blue just looks great with everything.

I, on the other hand, have to borrow my regalia on occasions like this. When I was at your stage, when I was your age, I was so socially maladjusted that I managed to avoid attending every single one of my graduations. Seriously, I attended not one. And since then I have lived to regret it.

On that score all of you here today are definitely smarter than I was back then.

You are absolutely right to be here. Occasions like this should be marked.

And I and my colleagues are delighted to share the occasion with you.

It is one of the great privilege of anyone who teaches at a university like this to work with students like you. To share your enthusiasm, your ambition, your goals. It energizes and sweeps you along.

Over the winter break, a gang of masters students lobbied me to run a reading group on the political economy of climate change. After Glasgow COP26 there was so much energy that I allowed myself to be arm-twisted. Before we knew it we had 15-20 people attending regularly. It started on zoom. It was a bit improvised, but it was also hands down the best discussion and brain food all academic year. A bunch of reading group members are graduating today. Shout out to them.

The only bad thing about today is that it does close a chapter. But, as far as the reading group goes, the energy was so good that the plan is continue meeting by zoom in permanent session. The common interests that bind us together are not going away, any more than your education in the wider sense of the word ends here.

That reading group was born out of the urgency of the moment. And, man, has there been enough urgency to go around these last few years, both in national and global affairs.

It has been exhilarating and terrifying. Perhaps, above all, confusing. This is not how the future looked around the late 1990s when many of you here were born. This isn’t the end of history we were promised. Indeed, it is now almost a cliché to say that history has restarted.

But saying that is the easy bit. If that is the case, how then do we orientate ourselves?

You can do so by holding firmly to some values. If you are clear about those. Great. But defining and debating those values raises a whole host of problems -philosophical & political. It is contentious. If we can agree on goods, which matter most?

That is part of the confusion of our moment. Setting Russia aside, what are we to make of the great divide between the West and China, which affects so many of you here today? Or, the collapse in the moral authority of American democracy and its constitution that is ongoing all around us? Neither were anticipated in the late 1990s.

Failing comprehensive normative agreement, a problem like climate has the advantage that we can orientate ourselves towards it pragmatically.

We can focus our collective energies on C02 reduction. That promises the chance of collective success. We spend so long bemoaning difficulty and failure. Imagine for a second, instead, that through our collective efforts we do actually manage to get to somewhere close to net zero by 2050. We might have to reevaluate our darker thoughts about our species.

With good reason, climate is one of the problems that preoccupies rich countries and we orientate ourselves towards the Paris climate agreement of 2015. But the climate treaty was not the only global pact sworn in 2015. 2015 was also the year of the UN agreement on Sustainable Development Goals. For the rich world overwhelmingly represented here, it is the sustainable bit that is the challenge. But for billions of others in Latin America, in Asia and above all in Africa it is development that is the key. That is a huge and vastly complex question, but if there is one thing we know about it, it is that development is impossible without the thing that we celebrating here this afternoon. Education – knowledge formation and transmission.

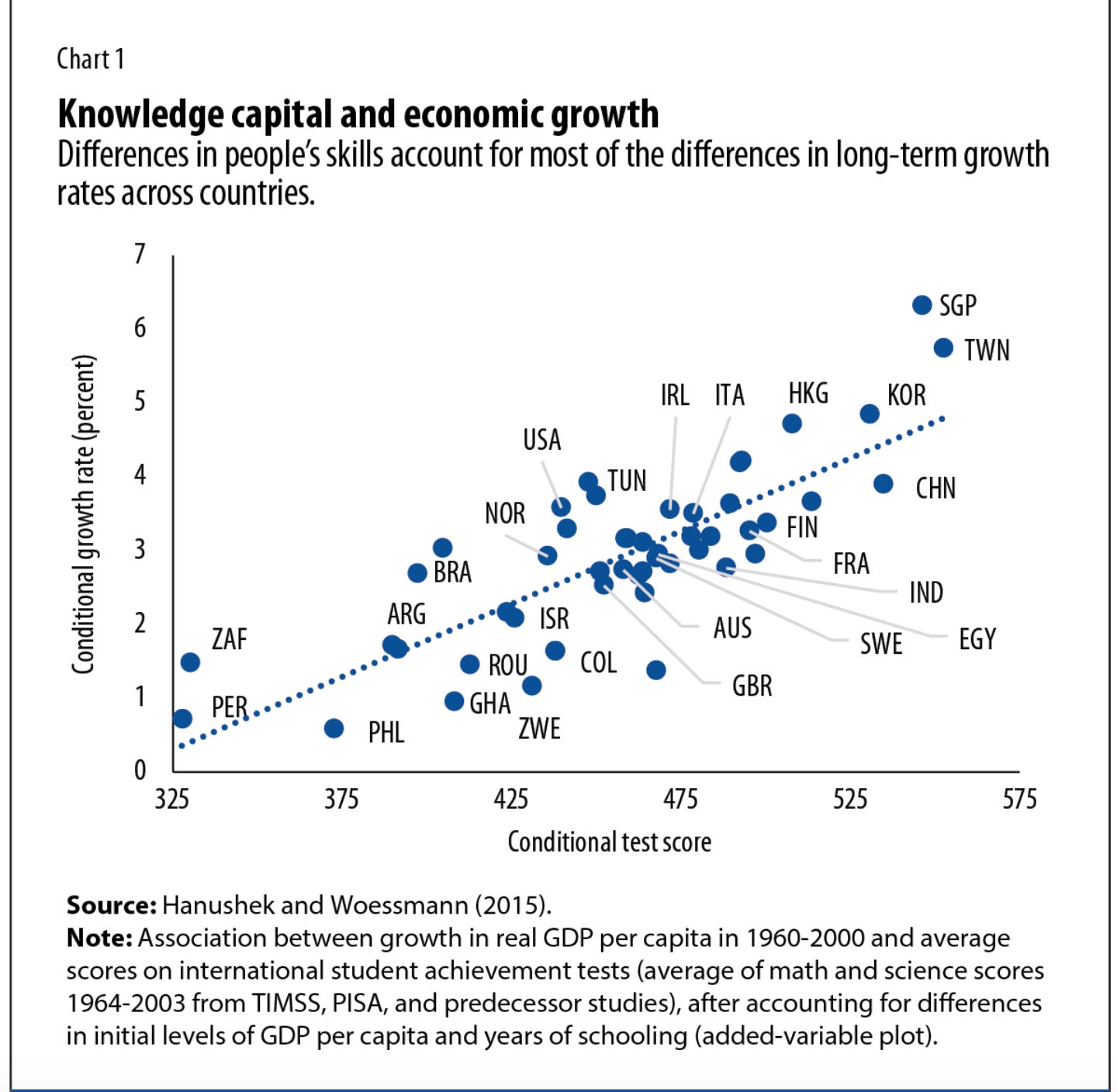

We don’t just know this in our gut, we know this because we researched it. A report from the IMF came out just a few weeks ago on basic skills and their significance fore economic growth. Powerpoint, I figure, is not appropriate for commencement speeches, but, if it were, I would show you the regression and the relationship is linear and strong. Without basic skills no development.

Basic skills are what everyone here takes for granted. But imagine how you navigate our world without basic literacy and numeracy. That is a challenge for literally billions of fellow humans. Addressing that grotesque imbalance in the world, is a huge challenge. But, as another clichés says, it is also a huge opportunity. As far as human potential goes, the extraordinary development of Asia in recent decades is thrilling. But as for the planet as a whole, we really ain’t seen nothing yet. Think of all the potential that can still be unlocked in the 7.8 billion people we share this world with

To bring this home, focus for a second on something else, focus on your body and the bodies of all the people around us. And think of the stuff that is inside us. The stuff without which we would literally not be able to assemble her today.

Vaccines. In the spring of 2020 I sat at a safe social distance with an eminent colleague in medicine who told me: “Corona virus vaccine are a long shot. We have never developed a single effective vaccine.”

Nine months later we had done not one but a whole portfolio and when I say “we” I mean scientists literally all over the world. It is a triumph. A triumph of molecular biology and pharmaeceutical production.

My dad, an eminent 1st generation molecular biologist, died last year of causes unrelated to COVID. Despite spending his final 18 months in lockdown, he died happy because all around him he could see molecular biology saving the world.

The story of the vaccines is the story of a triumph, but also a story of failure. An epic failure because despite the huge and obvious advantages to comprehensive vaccination, spelled out in trillions of dollars by no lesser authority than the IMF, as of this weekend I have four vaccines in my arm, whilst a third of the world’s population has none.

We triumphed in science and failed in economics and politics. And as a result, right here, right now we are riding our luck. Who knows what the flu season of 2022 will bring. One more reason to savor this moment, this summer, with our masks off and fingers crossed.

COVID was a trial run and though by the end of 2021 it had cost at least 15 million lives in excess deaths according to the WHO’s conservative estimates, it was in the broader scheme of things a lucky escape. The lesson we must learn is that in the 21st century to come, we need to do much, much better. And to do better we will need not just scientists and technicians, but managers, lawyers, politicians, social workers, educators, journalists, administrators, statisticians, committed business people, regular citizens. In other words we are going to need you.

I don’t even need to tell you it. You know it. Your experience here in this city and on this campus in the emergencies we have lived through together, teach you that. And in that clarity and determination on your part lies our best hope. Thank the lord that we have you – thrillingly talented, energetic well-equipped young people.

And imagine how many more there are to come. How much more potential there is out there. Right now in the world, there are roughly 720 million young people in the age bracket between ages of 18 and 22, in the age bracket relevant for graduation ceremonies. And there are literally billions behind you. You and your brothers and sisters, young people below the age of 25 make up an astonishing 42 percent of the world’s population.

Now imagine just for a second, all of you in that 18-22 bracket, all 720 million actually benefiting from higher education. Let us not argue over the curriculum. Whatever it is, just imagine your entire cohort worldwide progressing through high school and from there to further education and training.

720 million of your contemporaries either graduating or looking forward to it. Imagine this scene here today, 700 Columbia MA graduates, multiplied a thousand fold and then a thousand fold again. Imagine today’s rejoicing over educational achievement multiplied a million-fold.

I visualize it somewhat like the closing credits of everyone’s favorite Christmas movie, Love Actually, where they start with one couple embracing in an airport arrival hall and then multiply out in a dizzying tessellated explosion.

That should be our future, every year, henceforth forever.

If that isn’t an optimistic vision I don’t know what it is.

On that dizzying note, may I offer you and everyone who helped to get you here, on behalf of my colleagues, the staff and the University our very warmest congratulations on being part of that future.

Allow us to wish you the very best in the next chapter in your exciting lives.

June 17, 2022

Ones & Tooze: The Fed Interest Rate Hike

It has been a rocky week for the U.S. economy, with record high inflation reports and the Federal Reserve increasing benchmark interest rates by three-quarters of a percentage point. This is the steepest hike in close to thirty years. In this episode, Adam and Cam make sense of this spike and ponder what the Biden administration should do to curb inflation – if anything.

Later on, they set their eyes on Colombia, which has a presidential election on Sunday. For the first time ever in Colombia, one of the two leading candidates, Gustavo Petro, is left-wing. Adam and Cam analyze why right-wing economics has been such a large part of Colombian history and what Petro’s proposed policies could do for the country.

Find more episodes and subscribe at Foreign Policy

June 12, 2022

Chartbook #128: Mission command – NATO’s Strangelove vision of freedom enacted on the Ukraine battlefield

Russian forces attempted to cross the Siverskyi Donets river in eastern Ukraine this month using a pontoon bridge, but their tanks and armoured vehicles were picked off by Ukrainian artillery. So they tried it again. And again. And again. The Russian army made nine attempts to cross the river in the second week of May, according to Ukrainian defence chiefs. Russia lost about 80 tanks or other vehicles and more than 400 men in the ill-fated operation … It is part of a pattern of Russian behaviour since the invasion began three months ago. By contrast, Ukraine’s forces have proved to be agile, using the leeway afforded to company and even platoon commanders to shape their tactics according to the conditions on the ground.

Why have Ukrainian forces been able so far to withstand Russia’s assault on their country? It is a historic surprise a shock which offers a Rorschach blot onto which to project more or less ideological interpretation. In Washington in the spring of 2022 they have been summoning the Marshall Plan, Lend Lease and 1941. Classic Atlanticism in the form of NATO has made a come back. Weapons like the Javelin resonate with what Rayner Banham dubbed the “gizmo theory” of American power.

But it is reductive to explain Ukraine’s success through foreign aid, money and equipment alone. Against the odds Ukraine’s fighting forces are displaying remarkable resilience and skill. Ukraine’s soldiers appear to have absorbed experience from years of fighting in Donbas. But their success is also attributed, in much commentary, to military reforms introduced since 2014 under the influence of NATO. Western observers have seized on the contrast between the initiative shown by the Ukrainians and the dysfunctional repetitive behavior shown by the Russians on the banks of the Siverskyi Donets. For many observers it appears to confirm on the battlefield the cultural stereotypes of freedom versus disciplines that now associate Ukraine with the West against Russian “autocracy”.

This crude ethno-cultural distinction has a counterpart in technical military discourse. Whereas the Russians are laboring under rigid, top-down discipline, what Ukraine’s military have apparently learned from NATO is “mission command”.

In recent weeks, the FT, Economist and Atlantic magazines have all run stories attributing the Ukrainian military’s success to the adoption of the NATO practice of mission command. The Economist’s piece was written by no lesser figure than a former Ukrainian defense Minister, Andriy Zagorodnyuk”. As he puts it:

Reforms in the Ukrainian army in recent years are now proving their worth, too. Many were inspired by the organisational structure of Western forces. One of the most important changes Ukraine made was to elevate the role of non-commissioned officers—senior enlisted men, like sergeants, who supervise troops—in the manner of NATO armies. This allows knowledge and skills to be passed on to soldiers. The Western principle of “mission command” has also been adopted by Ukraine’s forces. It allows the officers in charge of small units greater power over decisions, rendering those units more agile. The Russians have stuck with a top-heavy Soviet organisational structure instead.

Ben Hall, who wrote the description of the failed Siverskyi Donets river-crossing I cited above for the FT, lays out the argument in archetypal form:

Decentralised mission command — following strategic objectives set by military chiefs while giving lower ranks tactical autonomy — is standard Nato doctrine. Ukraine’s forces began to study it after independence in 1991, but only embraced it after Russia started its separatist war in the eastern Donbas region in 2014. Kyiv adopted far-reaching defence reforms in 2016 and US, UK and Canadian forces provided extensive training. “We have a different style and Ukraine’s is pretty similar to western doctrine — the freedom to adapt and achieve the goals according to their understanding of the situation,” said Mykhailo Samus, director of the New Geopolitics Research network … “The Soviet model is to follow the exact written instructions of their commanders.” Blindly following orders from high command and persisting with failed tactics on the battlefield have been features of Russia’s full-scale invasion ….

For Hall and his Ukrainian interlocutors the difference is not just a matter of culture:

“For a Russian infantry officer the risk of being punished by his commander is much more significant than the risk of losing his men or being killed himself,” said Oleksiy Melnyk, a former Ukrainian Air Force officer who spent 10 years under Soviet command. “If you see this order is a way to disaster, you have to tell your commander. That is what Russian officers are afraid of the most.”

By contrast, Ukraine has adopted a Western military style that focuses on empowerment, decentralization and even entrepreneurial virtues:

… Ukraine is building a corps of non-commissioned officers, corporals and sergeants who can make tactical decisions on the battlefield and are regarded as the backbone of western armies. … Ukraine’s military retained some of the culture of the volunteers battalions created hastily to defend the country in 2014 and subsequently incorporated into the army and national guard. “Many of them were formed and structured almost like civilian companies or non-governmental organisations,” he said. “They didn’t pay so much attention to military rank but to people with real leadership skills who could take command.”

Since the 1980s, “mission command” has, indeed, been a key element of NATO doctrine. It is commonly seen as a way to harness the freedom and initiative of fighting forces and thus easily segues with broader notions of Western culture and individualism. But where does this idea of “mission command” come from? What kind of “Western” idea is it?

Amongst NATO forces the first to adopt the term “mission command” or “mission tactics” were American marines and then the American Army in the 1980s editions of the basic field manual, FM 100-5. As was acknowledged at the time, the phrase is not originally English. “Mission command” is a loose translation of the German concept of Auftragstaktik. Its introduction to US and NATO doctrine was the fruit of the intensified interaction in the 1970s and 1980s between the US Army and the Bundeswehr in West Germany.

Opening the door to this intellectual transfusion was the work of an entire generation of officers and military intellectuals who shaped the US military and strategic debate down to the recent past. It involved agencies like US Army Training and Doctrine Command (TRADOC), successive editions of FM 100-5 and a bevy of defense intellectuals like William S Lind, war-gamers and military consultants. The process of trans-Atlantic transfusion generated its own hew histories of modern warfare. And it has since become the object of a cottage industry of commentary. A hundred years after Daniel Rodger’s famous trans-Atlantic progressive dialogue, this was another Atlantic Crossing.

I became fascinated with this military-intellectual nexus because it so clearly shaped the military history around which I fashioned the narrative of Wages of Destruction. The latest and perhaps most comprehensive revisionist history of this period was published in 2021 by Stephen Robinson, The Blind Strategist. John Boyd and the American Art of War. A highly recommended read!

John Boyd was a former fighter pilot who became a defense guru, pedaling lessons in a legendary slide pack which by the end of his career had extended to 1500 slides and presentations that could run to 13 hours straight. Robinson’s title is arch, because the contention of Boyd and his cohort was precisely that there was no such thing as an American art of war. Art is what America military history lacked. It had to be created by borrowing from the Europeans. And this is where the explosive story behind the concept of “mission command” begins.

The open secret amongst military experts is that NATO’s “mission command” concept so widely touted as a precious gift from “West” was, in fact, taken directly from the German military tradition and most immediately from Hitler’s Wehrmacht. And, rather than there being any contradiction, it was in effecting the transfusion from the Wehrmacht to NATO that the military idea of mission command/Auftragstaktik was bracketed with more wide-ranging notions of Western culture, individualism and freedom.

Already in the 1950s the Americans had relied heavily on lessons to be learned from Wehrmacht. Under the leadership of Franz Halder, chief of Army staff under Hitler, the German Military History Program rewrote the Wehrmacht’s World War II combat history for purposes of incorporation into NATO doctrine. For a brief period in the early 1950s NATO envisioned a mobile defense against the Warsaw Pact on the lines of the Wehrmacht after 1942. When the Military HIstory Program was wound up in 1961 President Kennedy awarded Halder the United States Meritorious Civilian Service Award for ‘a lasting contribution to the tactical and strategic thinking of the United States Armed Forces’.

But at that point the actual influence of German military traditions on the US military was at a low point. In the mid 1950s, under the sign of the new generation of thermonuclear weapons, thinking about mobile conventional warfare on the battlefield of West Germany was displaced by all-out nuclear deterrence. By the 1960s America’s own military leadership style was managerial rather than military in the classic sense. McNamara and the Pentagon’s efforts at top-down control in Vietnam exemplified this firepower and bodycount centered vision of warfare. In that conflict it was not even obvious whether there was any room for tanks to be used in earnest.

It was the humiliating withdrawal from Vietnam and the new focus on NATO’s central front in West Germany in the 1970s that sent the US military, and most importantly, the army in search of a new way of thinking about war. On the central front in West Germany, unlike in Vietnam, NATO’s forces would expected to be massively outgunned. They would need to develop a new repertoire of military skills and artistry if they were to prevail.

From the late 1960s the Warsaw Pact undertook a considerable modernization of its conventional forces and appeared to be preparing in the words of Donald Rumsfeld in his Annual Defense Department Report of 1977 for a “relatively prolonged conventional campaign” to precede any use of nuclear weapons. Systematic upgrading of Soviet conventional forces symbolized by the new generation of T72 tanks, meant that technological parity now compounded the obvious numerical superiority of Soviet force. Furthermore, the Israeli encounter with Soviet anti-tank guided missiles in the hands of Egyptian troops in the Sinai in 1973 and the blazing intensity of the defensive battle in the Golan suggested nothing less than a revolution in modern weaponry.

If it was to hold the line, NATO would need to fight like the US army had never fought before. There was no room to retreat and no giant reserves of strategic power to draw on. If one wanted to avoid escalation to full-scale thermonuclear war, NATO would have to try to win the first battle in Germany.

Andrew Bacevich, who was serving with the US Army in Germany in the mid 1970s, puts it eloquently in The New American Militarism. In the wake of Vietnam and the moral confusion of Watergate he remarks “…inside the cocoon of military life, there existed one fixed point of absolute and reassuring clarity. Those of us whose day-to-day routine centered on furiously preparing to defend the so-called Fulda Gap, the region in western Germany presumed to be the focal point of any Warsaw Pact attack, had no need to torment ourselves with existential questions of purpose … our purposes was self-evident: it was to defend the West. … here was the lodestar … this was what we understood to be the American soldier’s true and honourable calling.”

It was not just a professional and moral challenge. It was also cognitive. Analysts like Steven L. Canby a reserve army colonel, and partner with Edward N. Luttwak in C&L Associates railed against the Pentagon planners and their one-sided focus on firepower and a methodology that was mechanical and arithmetic. Canby rejected “Lanchesterian firepower models” and NATO’s addiction to a “systems approach to analysis”. He had nothing but scorn for the “civilian leadership and analytic community” relying on a “methodology independent of substantive knowledge of the subject field … a methodology based upon constrained maximization but unable to define an effectiveness function”. At NATO HQ, military analysis had been reduced to an exercise in “cost minimization and a transnational comparison of inputs”. What Canby, Luttwak and their colleagues in the military reform movement like William S Lind wanted to bring to the fore instead was history, military art and maneuver. Some, like Luttwak, stressed the operational level of war – between strategy and tactics. Others focused on the practices that enabled European militaries and the German militaries in particular to fight war. One key concept was Schwerpunk, the decisive point of attack. Another was Auftragstaktik, what would later be dubbed “mission command”.

In the neoliberal parlance of the day, American commentators translated this into a contract by which “The subordinate agrees to make his actions serve his superior’s intent in terms of what is to be accomplished, while the superior agrees to give his subordinate wide freedom to exercise his imagination and initiative in terms of how intent is to be realized.” Finally, the soldier would be free on the battlefield to accomplish his mission undirected from above. All his faculties would be engaged towards the common end. His subjectivity restored.

The appropriation of German military history thus served a deep purpose in America’s culture wars of the 1960s and 1970s. Auftragstaktik, mission command, was the gothic scissors that cut through the threads that suspended the American fighting-man like a puppet from the dead hand of Mcnamara’s Pentagon.

Auftragstaktik was not invented by Hitler’s Wehrmacht. Anglo-American histories of the term, of which dozens circulated in professional circles, would generally trace the idea back to the age of the legendary chief of staff Helmuth Moltke and his emphasis on the need to adjust war planning to particular circumstances and contingencies. A specifically tactical meaning of the term began to take shape in the later stages of WWI in the “Sturm” tactics adopted by the crack units of the German infantry to mount their final wave of offensives against the trench lines. Figure like Ernst Jünger or Erwin Rommel exemplified the new model of highly motivated, intelligent and independent battlefield leadership. By the 1920s the Reichswehr had become to distill some of that experience in its new manual on Truppenführung (troop leadership).

It was attractive for America’s military reformers in the 1970s to trace the concept of independent decentralized leadership to roots in the 1920s. Finding the idea in the Weimar Republic avoided the odium of association with Nazi Germany. Furthermore, embattled advocates of a new American militarism, could identify with the Reichswehr military commanders who in the Weimar Republic sought to preserve a state within the state, much as Samuel Huntington imagined the American army as a society and polity apart. But the Weimar Republic’s Reichswehr was an army that never fought a war. Its real historical significance is that it served as a vehicle for the Wehrmacht of Nazi Germany.And it was from in-depth study of the Wehrmacht, through cooperation with the Wehrmacht’s successor, the Bundeswehr (which was going through its own process of incorporating its military history) and through actual encounters with surviving Wehrmacht veterans that a new model of war was transferred to the US Army in the late 1970s and 1980s.

This convergence between US Army and Bundeswehr thinking was encouraged by Chief of Staff General Abrams, and was eagerly taken up by TRADOC commander and World War II veteran General William DePuy eagerly followed the hint. He was followed by General Don Starry commander of V Corps in West Germany and later head of TRADOC. The US-German synthesis had close synergy. When General Alexander M. Haig Jr., the new supreme allied commander, Europe, expressed to General DePuy his reservations about the emerging doctrine, DePuy countered that Haig was “ignor[ing] the German origins of a great part of that doctrine” and advised him to “be aware of its almost total coincidence with that of our German allies.” The new 1970s version of US Army Field Manual 100-5 was written in close collaboration with the armoured infantry experts at the Bundeswehr tank school who were at the time developing an updated model of the wartime Panzergrenadier (armored infantry), which would become the standard divisional unit of NATO forces by the 1980.

Timing matters. This German-US transfusion took place not back in the 1950s in the immediate aftermath of World War II, but in a belated return to history in the 1970s and 1980s. This means that the practical influence of lessons learned from the Wehrmacht on the US and NATO reached its height precisely when the wider historical and political debate about the Wehrmacht’s deep involvement in racial war was beginning in earnest. It was the same moment as the scandal surrounding Reagan and Kohl’s visit to the Bitburg cemetery. It was the same moment as that in which Habermas was fighting out the Historikerstreit over the resurgence of nationalist currents.

As Robert M Citino puts it, “in the years after 1982, it became difficult to pick up any American military journal without reading something about the German army.” The German fashion amongst America’s military intellectuals ticked all the boxes. As Michael Swain notes, “the young authors achieved the tone that their generation looked for, a style of war marked by the offensive, maneuver, and surprise – with due attention paid to human as well as material factors of battle.”

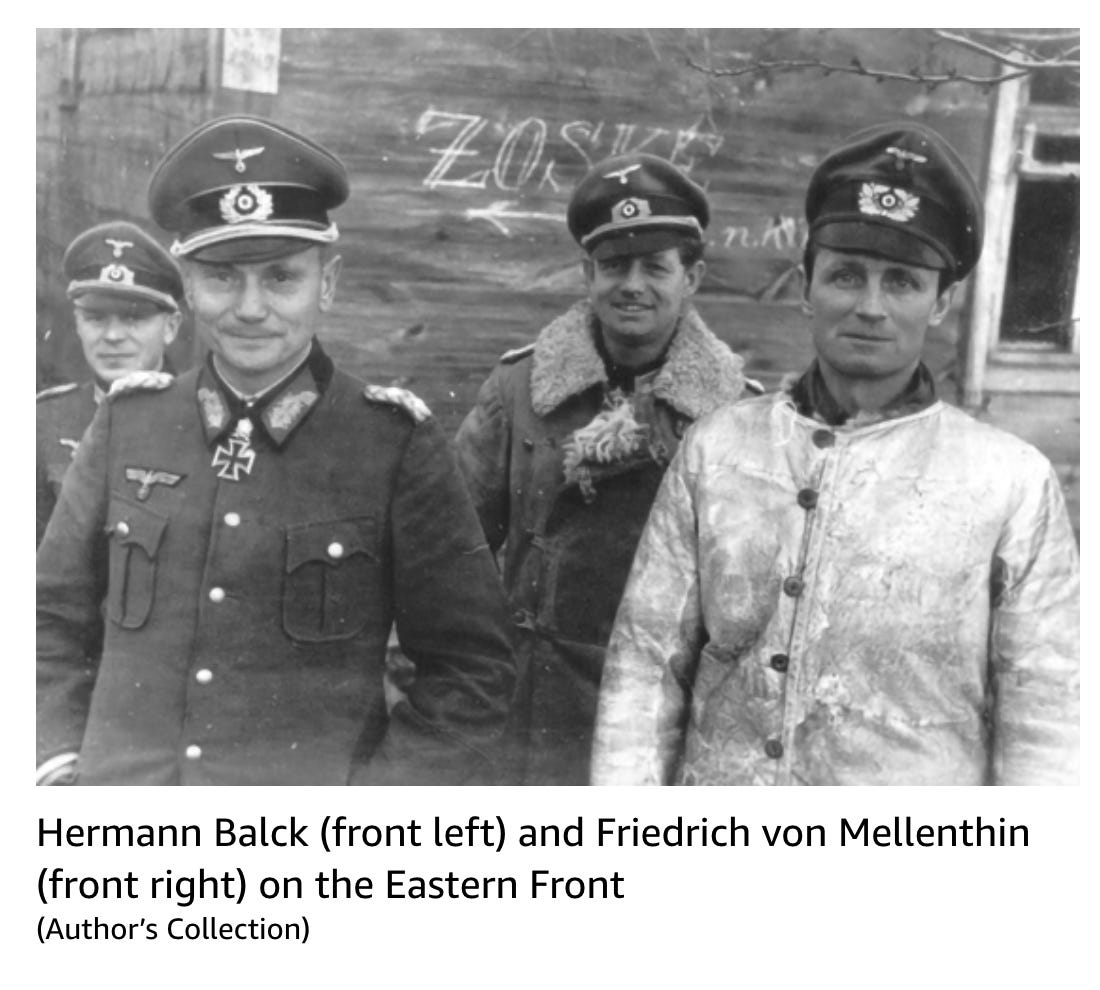

Indeed, the American military were not content with merely reading history they wanted to experience it up close. In May 1980, at one of the military-industrial facilities that dot the beltway of Virginia, history was brought to life. The host was the BDM Corporation, a favoured consultant to the Pentagon, and war-gaming outfit SPIT. The sponsor was Andrew Marshall of the Office of Net Assessment. The rapporteur was General DePuy, recently retired head of TRADOC. The audience included a nameless group of the more intellectually-minded officers of the US Army. But the stars of the show were the foreign guests, two spry, elderly German gentlemen, General Hermann Balck and his former Chief of Staff General von Mellenthin.

Picture: Stephen Robinson

Since the stars of the postwar Blitzkrieg circuit notably Guderian and Halder had died, the American military reformers were now drawing on the second tier. Thanks to his bestseller Panzer Battles Von Mellenthin was a global miltiary history celebrity. But Balck, the senior of the two, was the real sensation. He had held back. Refusing to cooperate with Halder he now found himself at the cusp of the next graph phase in the Cold War as the senior surviving panzer general.

Their combined battlefield record was second to none. But what was less often noted was that Balck had reason to lie low. As a Wehrmacht officer General Balck displayed a gung-ho attitude that had alienated even the Waffen SS during the prolonged and bloody defensive battles in Hungary. In 1947 Balck was convicted by a German court for the murder by firing squad of one of his subordinates to whom he had not even extended the perfunctory court proceedings provided by Nazi military law. He served half of a three year sentence. He was also convicted by a French military court in Colmar to 20 years of hard labour for his role in the scorched earth Operation Waldfest but was never extradited

In the United States in 1979/1980 Balck found himself lionized. And he delivered preicsely what the Americans wanted, an authentically European view of military leadership, presonalistic, dynamic, but not based on technology. To illustrate this point at his own expense John Boyd the marine corps guru liked to tell the story of how during a dinner party he had sought to compliment Balck by suggesting that with his lightening fast reactions he might have become a superb fighter pilot, Balck snapped back: “I am not a technician”.

At the war game in Virginia the attention of the observers was divided between the specifics of the maneuver in which an American solution was contrasted with the solution developed by Balck and von Mellenthin and the more general issue of command style.

As far as the war game itself was concerned, the Germans performed true to type. The challenge, inevitably, was to defend the Fulda Gap. And after only five minutes of urgent discussion the Germans decided that rather than doggedly defending the forward end, as prevailing NATO doctrine would demand, they would entice a Soviet armoured thrust all the way to the outskirts of Frankfurt, before delivering a massive counterblow. Military artistry would allow disproportionate effects to be achieved even with inferior forces. But beyond the maps, what fascinated the Americans was actually to witness these two veterans of German command style close up. General William DePuy made a point of writing up the report himself and first on the list of “interesting themes” to emerge from the four day conference he put quite simply “General Balck and von Mellenthin themselves and their relationship to one another.”

As DePuy went on in a gushing tone: “Those readers who may not have studied the background of the distinguished German participants might not appreciate the full authority with which they speak – authority growing out of an incomparable set of experiences in war against Russians a record of battlefield performance unsurpassed anywhere in the history of modern warfare. … the character and personalities, as well as the personal relationship between these officers, were fascinating and compelling.” Succumbing quite uninhibitedly to the desire for inclusion in the charismatic circle, the preface to the report considered it necessary to add to the short biography of DePuy, a four star general, former vice chief of staff and commander of TRADOC, the tell tale observation that “Balck and von Mellenthin’s respect for General DePuy was evident in their reference to him as a “kindred spirit”.

The Germans were good cop-bad cop buddies of hard-boiled cliché. “General Balck tends to be a man of few words – somewhat brusque almost laconic but deeply thoughtful. He was, and is, clearly a man of iron will and iron nerves.” “Von Mellenthin by contrast was a “more gentle officer on the outside. However, his record and Balck’s esteem tell us that he is also a man of steel at the core.” Twenty five years after the end of a lost war, Balck still exuded “a strong aura of confidence – confidence in himself, in the German Army and in the German soldier. He has no doubt about the superiority of the German over the Russian …” By the fourth day of proceedings “when a large number of interested observers” attended the final session the tone of lacerating self-criticism on the part of the Americans was overwhelming. As DePuy reported “invidious comparisons were being drawn between German and US Armies to the effect that the German leaders were uniformly superior in battlefield tactics. The patent excellence and superb performance of Generals Balck and von Mellenthin … led the audience easily in that direction.”

In an illustration that borders on the parodic, the Army’s leading periodical Military Review actually created a cybernetic model that contrast the remarkable lightening fast, 5-minute decision-making process exhibited by Balck and Mellenthin with the ponderous 14 hour cycle more normal in the US command chain. At the ages of 87 and 76 respectively, Balck and Von Mellenthin were 150 times faster than the standard NATO decision loop.

But the truly telling point was that as far as the Germans were concerned, the entire encounter rested on a misunderstanding. The Americans, with their essentializing reading of the difference between US and Wehrmacht military culture was missing the point. To be more precise. The Americans had hold of the wrong essentialism. For Balck and von Mellenthin far from there being a gulf that separated them from their hosts the more important fact was that Germany and the US were both part of the “West” and exponents of a culture of individualism and this distinguished them both from their potential enemies.

When asked to comment on the rigidity of Syrian offensive formations in the Golan battles of 1973 and possible similarities to Red Army practice, Balck responded with the following bizarre outburst: “Normal European and American countries educate their peoples like we do. There is a different class of prairie people – prairie nations like Hungary, like some peoples in Asia. They are used to flat, open terrain, and they use this kind of attack … then there is a third category: mountain people. They adapt more to the features of terrain. … Prairie people should not be used in modern warfare because that courts disaster.” General DePuy though himself a native of the prairie-state North Dakota did not even flinch.

Balck’s assessment of the Syrians was fully in line with his similarly contemptuous judgement as far as the Soviets were concerned. For Balck and von Mellenthin the German style of warfare was not just a tool that needed to be adopted to bolster NATO, but was nothing less than an expression of the best values of western civilization: intelligence, initiative, mind over matter. According to Balck and von Mellenthin far from being alien to the American mind, Blitzkrieg and manoeuvre warfare, founded as they were on freedom and intelligent individualism were expressions of a common Western civilization. By contrast, whatever technical improvements the Red Army might make, whatever operational skills its generals might possess and whatever fighting qualities were innate to the Russian serviceman, they were forever excluded from the cultural heritage of the West.

As von Mellenthin put it “they are masses and we are individuals. That is the difference between the Russian soldier and the European soldier.” Viewed in these terms Auftragstaktik, mission command, was nothing less than the expression of the inner spirit of Western culture in military form.

If one took this at face value it had radical implications, some of which were teased out in later discussion. NATO’s new art of war could be expressed in a piece of equipment, like an American-German infantry fighting vehicle. Some thought the new convergence could be read off the strange convergence of US helmets with the “Krautpot” familiar from the Wehrmacht. It expressed itself in basic concepts of leadership like “mission command”, but also in operational designs.

If it was true that West Germany was a nearly indefensible strip that did not permit large-scale maneuver operations in which the independence enabled by mission command would show itself to its best effect, then NATO should find a battlefield in which its natural cultural advantage would come to the fore. Samuel Huntington in an article in International Security in 1983 argued that rather than hunkering down in the Fulda gap, NATO should play to its strengths. If the Red Army was indeed “better at implementing a carefully detailed plan of attack than they are at adjusting to rapidly changing circumstances”, the argument popularized by von Mellenthin and Co, then NATO should respond with the ultimate surprise. Any immediate threat of Warsaw Pact assault across the North German Plain should be met by a NATO counter-offensive into East Germany. Of course, NATO would be at a numerical disadvantage. But as the German triumph in 1940 demonstrated one did not need overwhelming material superiority to win a decisive military victory. With the main bulk of Warsaw Pact forces concentrated in the North, NATO spearheads should drive out of the Hof corridor towards Jena and Leipzig and through Czechoslovakia towards Dresden or Prague. It was Manstein’s famous scything blow through the Ardennes, in mirror image. It would throw the Warsaw Pact off balance and give free rein to Western initiative and freedom to carry the day.

Mercifully, NATO never got to test that theory of war in an actual clash with Soviet forces. Instead, the new mode of war was enacted in 1990-1991 in the devastating riposte to Saddam’s invasion of Kuwait. For the generation of American military leaders headed by Powell and Schwartkopf this was the vindication of the entire reform program of the 1970s and 1980s. They had learned their lessons well. But had they really? As one TRADOC historian admits. Desert Storm was “a bit of a historical anomaly:” “It is a rare event for an operational plan to play out as designed.” The plain truth was that in Moltke’s term there had been no enemy “main force” to encounter in Kuwait, an obstacle the encounter with which might have provided a real test of military leadership and skill. The American and Allied troops ploughed across desert as if engaged in a particularly undemanding war game.

This gives to the battle in Ukraine a peculiar historical significance. If Ukraine’s forces really are influenced by the “mission command” model they have learned from NATO this is in fact the first time it is being put to the test against the original intended enemy and in the kind of life-or-death battle that NATO envisioned in the 1970s and 1980s.

But this poses tricky questions. What is the appropriate way to think about the relationship between military and political culture? What are we to make of this twisted genealogy of NATO’s idea of freedom?

In the 1980s the obvious move to make was to argue that the appropriation of military techniques from the odious Hitlerine regime was legitimate so long as military techniques and deeper political values were separable. But that is not the claim currently being made in Ukraine. Instead the association is constantly being drawn. Ukraine’s freedom and initiative on the battlefield are being contrasted to the robotic performance of the Russians. This undeniably converges with the argument made by Wehrmacht veterans like Blank and von Mellenthin in ingratiating themselves to their American acolytes. They too thought of the German way of war as an expression of deeper, common Western values.

There are two ways out of this trap.

One important point of difference is to guard against ethno-cultural determinism. The story told in Ukraine is one of learning, across cultural and social divides. After all, only recently, Ukraine’s military were post-Soviet too and they have been coached to fight differently. Contrary to the Balck von Mellenthin version, there is no good reason to imagine that Russians could not learn the same lessons if their regime would let them.