Adam Tooze's Blog, page 19

May 17, 2022

Chartbook #122: What drives inflation?

Rising prices continue to dominate the headlines. The impact on household budgets is felt above all by those least well off. There is talk of a cost of living crisis that is having impacts on public health.

Meanwhile, fear of persistent and accelerating inflation dominates the monetary policy agenda. Central banks are winding up their asset purchases and hiking interest rates.

But what actually is driving the current inflation?

On both sides of the Atlantic, analysts have been busy decomposing the source of price increases. The results are striking

For the US Josh Bivens of the Economic Policy Institute has compared the factors driving the growth of unit prices between 1979 and 2019 with those contributing to inflation in the US since Q2 2020.

Source: EPI

Whereas in recent decades, unit labour costs (wages/productivity) have accounted for 62 percent of price increases and corporate profits for only 11.4 percent, with non-labour input costs (like energy) making up the rest, since 2020 the balance has been reversed. Since the COVID shock in 2020, wages have accounted for less than 8 percent of US price increases, as against corporate profits which accounted for almost 54 percent. Input costs, notably energy, have accounted for 38 percent.

Striking as they are, these data are consistent with the fact that real wages (nominal wages adjusted for inflation) in the US have fallen since 2021.

Real wages are also under pressure in the Eurozone.

In a fascinating recent presentation the ECB’s Isabel Schnabel showed data which closely matched that of the EPI.

In the eurozone too, unit profits have made a far larger contribution to price increases since 2021 (here measured by the GDP inflator) than have unit labour costs – Q3 2021 being the moment when inflation really accelerated in Europe.

Is there any prospect of this imbalance shifting? Are we likely to see a wage price spiral that would compensate for the shift towards profits we have seen in recent quarters?

There is a lot of excitement in the US right now about the success of unionization drives at Amazon and Starbucks. But what about the macroeconomic perspective?

A team from the BIS consisting of Frederic Boissay, Fiorella De Fiore, Deniz Igan, Albert Pierres-Tejada and Daniel Rees has addressed itself to this question in a timely working paper asking: Are major advanced economies on the verge of a wage-price spiral?

Based on data for BE, CA, DE, ES, FR, GB, IT, NL, PT and US they show that in recent years all the evidence suggests a marked shift in bargaining power against organized labour.

Trade union density is down across advanced economies. Profit mark-ups have risen over the last thirty years whilst the correlation between wage and price inflation – which would be prima facie evidence for wage-price spirals – has declined to zero, or even fallen into negative territory.

As they also note:

… the indexation and COLA clauses that fuelled past wage-price spirals are less prevalent. In the euro area, the share of private sector employees whose contracts involve a formal role for inflation in wage-setting fell from 24% in 2008 to 16% in 2021 (Koester and Grapow (2021)).2 COLA coverage in the United States hovered around 25% in the 1960s and rose to about 60% during the inflationary episode of the late 1970s and early 1980s, but rapidly declined to 20% by the mid-1990s.3

But will this stability last? Will surging profit margins and prices trigger a reaction? In a fascinating twist they point out that whether or not there is a wage-price spiral actually at work in the US economy right now, the financial markets appear to expect such a mechanism to come into effect.

This linkage in the minds of forecasters can be inferred from the data.

… there are tentative signs of inflation expectations unmooring. This is clearest for medium-term expectation measures. Professional forecasts point to inflation of over 4.5% in the United States and much of Europe over the next two years, and above 3.5% in many other AEs. In countries such as the United States where labour markets have tightened the most, job vacancies have become an increasingly important driver of medium-term financial market inflation expectations (Graph 2, fourth panel). As job vacancy rates have substantial predictive power for wage inflation (Domash and Summers (2022)), this could mean that market participants have already priced in the inflationary effects of future wage increases.4

Where might an actual wage-price spiral originate?

Large service sector employers like food services and restaurants have seen a burst of inflation. In a typically astute analysis of the most recent US inflation numbers, Matt Klein over at Overshoot – an essential substack subscription if you can afford it! – has highlighted the strategic significance of the price of restaurant meals for macroeconomic forecasting.

The cost of a sit-down restaurant meal captures the entire economy in a microcosm. Workers cook meals, take orders, and clean using a mix of durable equipment and perishable ingredients. The owner has to rent a venue with a kitchen and comply with whatever local regulations and mandates are imposed by the authorities. And since most restaurant customers consider dining out to be something of a luxury, their willingness to spend (and tip) is going to be sensitive to their own financial situation and prospects.

Thus, despite being a tiny component of the broader price index, there is a remarkably tight relationship between changes in the price index for “full service meals and snacks” and the underlying measure of inflation preferred by Fed officials. The picture does not look good.

On the other hand, as Matt goes on to point out, after a 30 % surge in H1 2021, restaurant worker wages seem to have settled down at a 5 percent rate of increase.

Rather than a permanent acceleration in pay growth, it looks more like a one-time recalibration commensurate with changes in the risks of the job and the opportunities available elsewhere. And since restaurant wages soared before restaurant prices did, the data could be consistent with the idea that price increases may soon abate.

The BIS authors back up Klein’s analysis with some time series tests that compare the spillover effects of wage increases in particular sectors to the wider economy.

Historically, wage increases in leisure and hospitality have been short-lived and spillovers to wages in other sectors limited (Graph 3, first panel). Spillovers from retail trade wages to other sectors are somewhat more persistent, yet still small (second panel).5 The recent increase in manufacturing wages may pose greater risks, as wage growth in this sector has historically had large spillovers (third panel).6

Manufacturing wage increases endure and spillover to the rest of the economy, those in major service sector occupations tend not to. As the authors note, as far as the most unionized sector in the US economy is concerned, the public sector, the news is not good for workers.

In the United States, the pay gap between private and public wages has actually widened since before the pandemic (Morrissey and Sherer (2022)).

The fascinating question in the current moment – to put is somewhat academically – is whether statistical relationships measured in recent decades characterized by persistent low inflation will carry over to a period with more rapid price increases. What if we are entering a period in which agency counts and history is made? That hope is surely what lurks behind the enthusiasm for charismatic labour organizers like Christian Smalls.

As the BIS authors note:

… the key question is whether the empirical regularities observed under low inflation will prove durable as inflation rises. Anecdotally, calls to make up for lost purchasing power in 2021 have been increasing. In the United Kingdom, for example, unions have recently pushed for pay rises of approximately 10%, while in France some unions have called for a 25% increase in the minimum wage. In the United States, several large companies have agreed to include COLA clauses in multi-year wage contracts following strikes in late 2021, and calls to unionise have risen. Pressure to increase minimum wages could rise, following the example of several states that have already done so in 2022, as inflation remains elevated. Public wages, which are set by collective bargaining in some countries and tend to have COLA clauses, could set the benchmark for private sector negotiations. And, if these wage rises do occur, their spillovers to other wages and prices could be larger today than when inflation was low.

Of course, the crucial thing to remember is that workers are not the only actors who might generate spillover effects. As the data for profits show, corporations and management have not been idle. They clearly sensed an opportunity in the aftermath of COVID and have seized it. The question is whether other social forces can do so too.

In light of that one should surely welcome Schnabel’s observation that

So far, workers are bearing the brunt of the inflationary shock, as nominal wage growth has remained muted. Yet only a relatively small number of wage contracts have been renegotiated since inflation started to increase strongly in the second half of 2021. The strength of the wage channel depends on the relative bargaining power of labour. And that bargaining power is arguably strengthening.

The frankness with which Schnabel speaks here of the “bargaining power of labour” is striking. It is striking because it implies not an idealized, atomized view of the labour market, but one that views employment terms as determined by collective struggle in which power is a relevant variable.

One of the basic ideas informing both Crashed and Shutdown was the view that central banks have the agency that they have enjoyed in the last twenty years in large part because they operate in a world of spectacularly lopsided class power. The modern model of the independent central bank may have been born out of the class struggle and inflationary wage-price spirals of the 1970s. But, as the BIS data attest, since the 1990s central bankers have operated in a world in which those forces are dead. You could do adventurous monetary policy precisely because there was no risk of unleashing a trade union-led, wage-price spiral, or even excessive fiscal activism on the part of elected politicians.

The profit surge in the first phase of the COVID recovery only confirms the stark imbalance of our social conditions. The current debate about inflation and wage-price spirals is – more or less openly – a debate about whether that class balance might be about to shift. And if so, will that shift be merely temporary – an effect of labour market tightness for instances – or will the energy of a new generation of union organizers, impelled in part by rising prices, produce a more lasting rebalancing?

It seems unlikely, but the fact that the question is posed at all is surely significant. When the question of distribution is posed as one not merely of dollars and cents but of social power, it becomes far more consequential and radical. It challenges the autonomy of technocrats in the basic sense that it challenges their grip on the main levers of the economy. Whatever distributional outcome those policy-makers prefer – and their preferences may be more or less progressive – it challenges their control and their ability to pursue what they believe to be optimal outcomes.

As the BIS authors unselfconsciously conclude:

Policymakers should be attuned to shifts in inflation expectations and to potential pressure to reinstate institutional structures that made economies more prone to wage-price spirals in the past.

******

I love putting out Chartbook. I am particularly pleased that it goes out for free to thousands of subscribers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press the button below and pick one of the three options.

The annual subscription: the $50 annual bargain rateThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility for the price of a fancy coffee.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions.

May 14, 2022

Chartbook #121: Youth Quake. Why African demography should matter to the world

Once you realize it’s scale, there is no global trend as dramatic today as the revolution in Africa’s demography.

Asia’s return to the center of the world economy dominates the headlines. But in the grand sweep of history that is a rebalancing or restoration not a revolution. Until the 18th century, the Pacific and Indian Oceans were the heart of sophisticated economic activity. That balance was grossly distorted in the “centuries of humiliation” by the rise of the West. Now, thanks to Asian economic growth, the centers of economic activity and population are realigning.

Source: Visual capitalist

The same cannot be said for Africa. Despite optimism in recent years, the relative lack of economic growth in Africa is well-known. Less well-appreciated is the extraordinary historical novelty of it demographic development.

In 1914 according to the best estimates, Africa’s entire population was 124 million and that includes North Africa. Today it is 1.34 billion. Compared to Africa’s roughly elevenfold increase in population, Asia’s population increased by “only” between 3 and 4 times – China’s merely tripled and India’s increased by 4.5 times. Furthermore, whereas Asia’s population is beginning to stabilize – led by that of India and China – Africa’s population will, barring disasters, reach 2.4 billion by 2050 and will go on growing.

Longer term projections are hazardous, but a world with somewhere between 9 and 11 billion total population and close to 4 billion people living in Africa is what current trends would lead one to expect. That means that by 2100 the African share of global population will likely be between 35 and 40 percent. And in 2100 the population of several African countries – Chad, Mali, Niger, Nigeria, and South Sudan – is likely still to be growing.

That is something new under the sun. It means that in sheer quantitative terms Africa’s story increasingly drives world history.

As Edward Paice spells out in his excellent book Youth Quake which I reviewed yesterday in Foreign Policy, our long-range predictions for global population basically depend on the outlook for Africa. Variation in estimates for Africa drive variations in the global total. Spelled out in demographic statistics this is a point of universal significance.

Making those estimates is an uncertain and volatile business because so many large countries in Africa are bucking the pattern of rapid demographic transitions we have recently seen in Latin America and Asia.

One of the things I really appreciate about Paice’s book is the way that it renders the succession of demographic estimates and the discourse about African population as history. We see how estimates are made, how they have been criticized and why they have been modified over time. That debate continues every day in the pages of journals like The Lancet with teams of modelers arguing over assumptions and functional linkages between population, investment, education and fertility.

Through the lens of African demographic modeling Paice explores what to me is one of the most basic dilemmas of orientating ourselves in our turbulent contemporary world. We can’t live with our big quantitative indicators and statistical estimate. Numbers like GDP, global population 2100 etc. are endlessly frustrating in their crudity, their rough approximations, their entanglements with power. And so often they are just plain wrong and misleading. On the other hand we can’t live without those numbers either. Quantitative nihilism or all-encompassing skepticism, whether motivated by mere laziness or radical critique, is not a practical option either. We are much better off having some estimate of where the economy stands or where population will end up, or what the rate of exploitation is, than not. So we need to work hard at getting the numbers as right as we can, even if we doomed to get them wrong.

If it helps with motivation, think of it as a low-key statistical version of a tragic predicament. We have to keep rolling the ball up the hill. We have to keep training our judgement. We can learn to use the numbers intelligently, appreciating both what they cannot be made to say, and where confidence and certainty is growing.

In light of experience, some estimates for Africa’s future population have been adjusted downwards. But in the largest and most significant cases, as Paice shows, the tendency is in the opposite direction. In particular, confidence has grown around the estimate of a population for Africa of 2.4-2.5 billion by 2050. Why? Because of one quiet, but dramatic fact. A large number of the mothers whose children will drive growth to 2050 have already been born. And so, barring utterly unprecedented discontinuities in fertility behavior of which there is no sign in Africa, we can estimate the number of their children and their children’s children and so on.

What Paice’s treatment reveals is something I did not appreciate about contemporary history. In demographic terms, the last ten to twenty years in Africa were, in fact, decisive for global population history. We have been waiting for the demographic transition to arrive, as it has in Asia and Latin America. It has in many societies in North Africa and in South Africa and in some cases in East Africa, but not in many of the largest and most rapidly growing societies across central and West Africa. The sheer size of Ethiopia and Egypt and the momentum of Nigeria, DRC, Tanzania and a handful of others carries us to 2.4-5 billion by 2050 and to even higher numbers by later in the century.

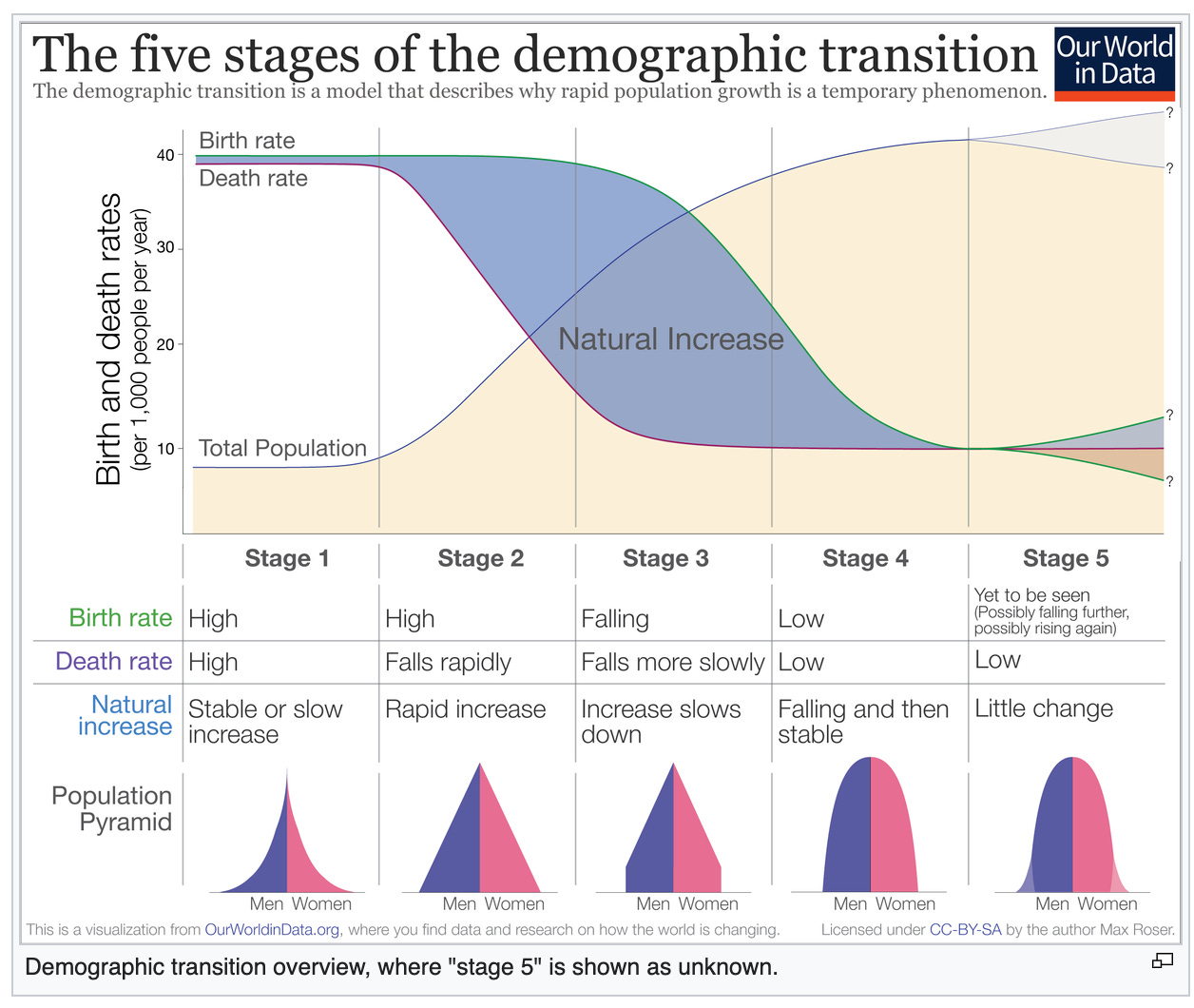

One of the questions that Paice poses is: What is going on with our understanding of the demographic transition?

The model of the demographic transition is a low-profile, but essential building block in our “kitchen sink” models of modernization.

Death rates fall as societies modernize and develop economically. So population growth accelerates. Then, at some point, fertility declines, so population growth slows down. Eventually, it may even go negative as fertility falls below the replacement rate of 2.1 children per woman.

It is a heuristic that has served us well as a device for organizing demographic history. It is a mechanism that has seemed to be speeding up, in Latin America, Southern Europe, North Africa and Asia. The discovery of the last few decades is that in many African societies it is operating far, far more slowly and that is what dictates the future.

This isn’t uniform. Paice is excellent in refusing to treat “Africa” as a block and constantly differentiating between regions and countries, between town and countryside and, even, between different cities. Addis in Ethiopia, for instance, where family sizes are shrinking rapidly has a demographic trajectory different from the rest of a huge country. The strength of the latest generation of population predictions lies in the fact that they are not based on generalizations about the entire continent, but on case by case estimates for each country and region.

Why then is the demographic transition not taking place? In part it is due to the failure to achieve the necessary preconditions for transition above all female education and empowerment. But as Paice tells it, it goes beyond that. African women and African men, in very unequal ways, appear to be making choices to have large families in a way that is unusual by international comparative standards.

This is highly contentious terrain. Theories of power are engaged. Sexist, racist and colonial stereotypes lurk everywhere. I was actually asked to correct a line in the original FP piece by one of the magazine’s regular Africa contributors. We did make a change, but only to state more clearly what Paice has to say on pages 177 and 178. Choice matters. All the evidence suggests that men and women in Nigeria are making different choices about fertility than men and women in Thailand, for instance.

I take the point being made by Paice to be analytical. We thought we had a solid understanding of accelerating demographic transition. This was based on data from Europe, Latin America and Asia fitted into a schematic model. That model is itself so influential that it shapes policy by guiding development policy. In Africa what we are seeing is that that model is not working as expected so we have to dig deeper into the data to understand better what is going on. This leads us to the recalcitrant but undeniable conclusion that choices matter, choices being made by large groups of people. The point is one about choices and agency and the contingency and analytical puzzlement they create. Of course, that agency in fertility choices is exercised is circumstances constrained by hierarchies of power, poverty etc. But the element of agency remains.

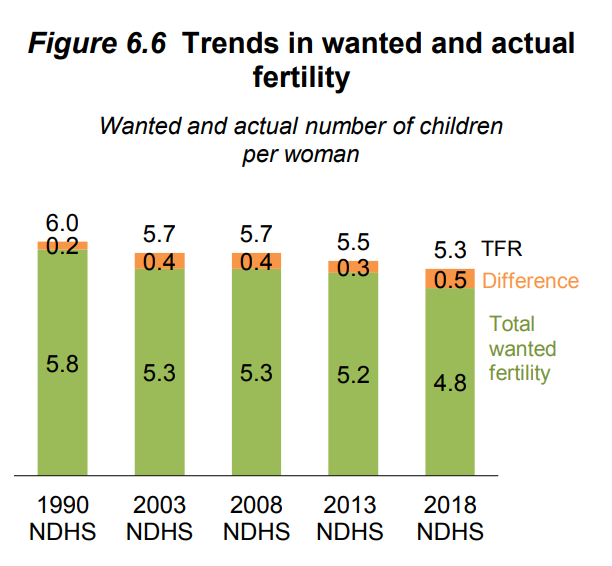

The next question is how we can track and gain a better understanding of the choices being made. One of the things I learned from Paice is how much data we actually have about men and women’s fertility and contraceptive choices around the world. The Demographic and Health Survey – the Nigerian 2018 report is available here – is an absolutely remarkable resource, which collects data on astonishing range of intimate details across large population samples that can be broken down by gender, region, income level, occupation, education level etc. It tracks not just social facts but also attitudes and preferences.

It tells us, for instance, that in a sampled population of 12955 Nigerian women of fertile age with no formal education, 94.8 percent were using no contraceptive methods, either traditional or modern and that in a sample of 2788 Nigerian women with more than secondary education the share using contraception rises. But even with higher education 66.7 percent of Nigerian women in 2018 used no contraception. One is tempted to add “still used”, but that is precisely the question. How relevant are the teleological assumptions of modernization theory? If you divide the population in terms of wealth quintiles it follows a similar gradient. Urbanization appears to make a difference. Amongst Nigerian women in Lagos, across all social categories, the share using no contraception falls to 50 percent.

Why do Nigerian women use so little contraception? There are no doubt many constraining factors but the clear message of the DHS data is that they use little contraception, because they want large families and they are, in their own way, quite successful at matching actual fertility to desired fertility.

As the desired total fertility has gradually fallen between 1990 and 2018 the gap between actual and desired fertility has somewhat widened, but not by a huge amount. It was barely larger in 2018 than it was in 2003.

I would love to know more about the compilation of DHS data. They cover an astonishing range of issues from malaria incidents to domestic violence in remarkable breadth and detail. Taken at face value the DHS data are an astonishing resource for tracking global social change. I am sure they are open to question and argument in many way, but they are a monument to the effort to track and understand our collective development.

The sheer scale of Africa’s demographic acceleration makes it a vastly significant megatrend, which will relativize the dominance of Asia by the mid-century. But it is all the more significant because of the questions it begs about economic development and attendant on that about environmental sustainability.

Given the huge strides in economic development across Asia and the rapid slowdown in population growth notably in India, it is tempting to think of the problem of absolute poverty and its remediation as a residual. India, like other once poor countries, is progressively rolling out basic services to its entire population. In a perverse way, even the COVID epidemic confirmed that. India did a comprehensive lockdown, as did Pakistan and Bangladesh. And India, by way of the Serum institute, was key to the global vaccination effort. At the risk of complacency, across much of Asia, escape from the most extreme forms of poverty seems a matter of time and will become easier as population growth slows.

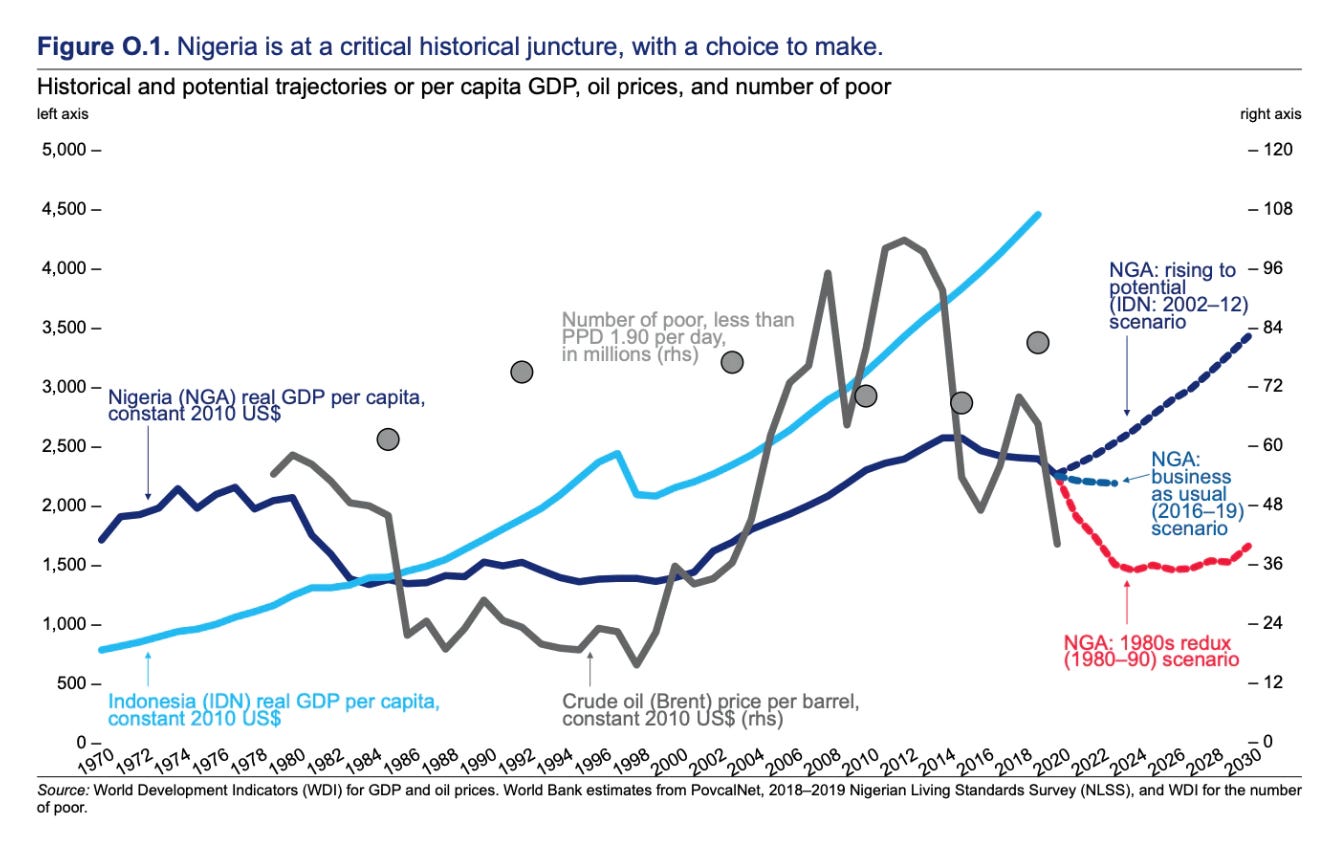

The same cannot be said for much of Africa. It is the combination of fitful and intermittent economic development with the huge dynamic of demographic growth that make the situation so dramatic. In world-historic shift, Nigeria in 2019 counted more absolutely poor citizens than India. COVID temporarily reversed that but the trend is unmistakeable.

This is the graph of Nigeria’s growth in gdp per capita from Chartbook #10 tells the story.

It is the combination, which was once common to large parts of the world but is now increasingly unique to Africa, of very large-scale demographic growth combined with continued mass poverty that gives extreme urgency to calls for infrastructure spending and human development through education.

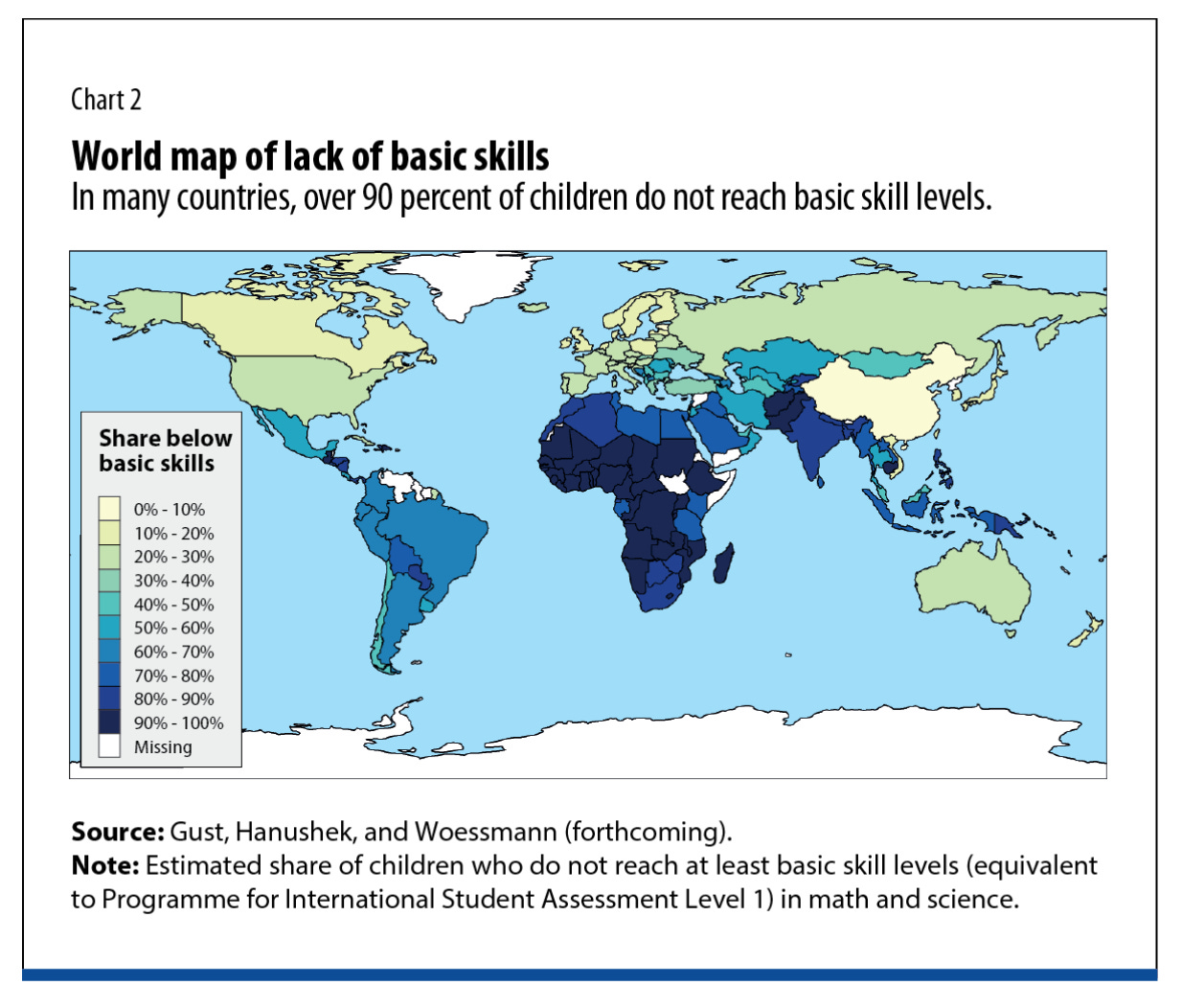

A recent report on basic skills that are essential for economic growth from the IMF paints a stark picture.

In the podcast, Cameron and I discussed repeated European efforts to launch development programs that seem to be spinning their wheels. The global sustainable development goals of 2015 take on their real urgency when you imagine Nigeria or DRC as the challenge.

****

Speaking in medias res, you may wonder whether as a middle-aged white guy who has only been to Africa twice and has no claim to expertise I feel comfortable writing about the contraceptive choices of young African women. No – let me reassure you – I do not! Clearly it is not my place, or anyone like me, to be either authoritative or prescriptive. So what I am doing here is simply to relay and amplify the message.

That, of course, begs another question. Is it coincidental that it is me, middle-aged white guy who is in a position to do that relaying? No it is not! Should it be African voices and African women’s voices addressing this topic? Evidently yes. They speak with far more power and authority, but also at the risk of having the topic pigeon-holed as a matter of particular interest to them, as Africans, as women, whereas, the point that Paice so convincingly makes is precisely that African demography is a matter of truly universal importance. We should all care about the nitty gritty of that DHS data! And that is something it is useful for someone like myself to say.

For me what is at stake is what this remarkable demographic development implies for our understanding of world history. On quantitative grounds alone – let alone qualitative – 21st century history is going to look completely unlike any previous epoch. Africa and Africans will be at the heart of the story.

In this transition, the role that folks like me can perhaps usefully serve is to convey a message that goes something like this:

“African issues, which I suspect you, like me, may previously have not had squarely at the center of your picture of the world, are actually huge and getting huger. When someone comes along who really seems to know their stuff on this topic, pay attention. If you want to have a view of what the world as a whole is going to look like and what, retrospectively, that reveals about our recent past, we are going to have to wrap our minds around this!”

I conclude the FP piece quoting Howard W. French.

“How Africa’s population evolves, and how the continent’s economies develop, will affect everything people near and far assume about their lives today.”a passage from.

That is surely right.

******

I love putting out Chartbook. I am particularly pleased that it goes out for free to thousands of subscribers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options.

May 13, 2022

It’s Africa’s Century—for Better or Worse

In the coming decades, we face a revolutionary shift in the balance of world affairs—and it is likely not the one you are thinking of.

Since the 1990s, the idea that we might be entering an “Asian century” has preoccupied and disorientated the West. However, once we take in view the long sweep of history, the return of China and India to the center stage of world affairs is less a revolution than a restoration.

For most of the last 2,000 years, the great Chinese and Indian empires were the center of world trade and home to the most sophisticated civilizations. Their growing influence in the world today is the rectification of the anomaly that arose in the 1700s as a result of the yawning divergence in per capita income between “the West” and “the rest.” Successive industrial revolutions and waves of colonial conquest created a world in which economic and military power was radically misaligned with population.

Not for nothing, 1900 was the high point of Western racial thought. Although Western public consciousness may have since sought to rid itself of overt racist tropes, it continued to take for granted the anomalous imbalance in economic power between the West and the rest of the world that shaped that thought.

Read the full article at Foreign Policy

Ones & Tooze: Why Low Unemployment Isn’t Better News

The U.S. unemployment rate is 3.6 percent, the lowest it’s been since the pandemic began in March 2020. So why aren’t we celebrating that? Adam and Cam dig into the other things bumming people out about the economy, as well as how low unemployment and inflation impact each other. In this first segment, Adam and Cam also answer the show’s first-ever listener audio question! After that, they look at Africa’s population boom and the economic questions that come along with it.

Find more episodes and subscribe at Foreign Policy

May 12, 2022

After the Zeitenwende: Jürgen Habermas and Germany’s new identity crisis

Vladimir Putin’s invasion of Ukraine has upended world politics and nowhere more so than in Germany. Addressing an emergency session of the Bundestag on 27 February, German chancellor Olaf Scholz declared a Zeitenwende, a turning point in history. Russia’s attack on Ukraine meant Europe and Germany had entered a new age. But what direction is history turning in?

Scholz promised to raise Germany’s defence spending and in March placed a large order for America’s exorbitant F-35 fighter jets. Since then, sanctions on Russia have been tightened and Germany has even agreed to deliver heavy weapons to Ukraine. But Berlin has baulked at an all-out boycott of Russian oil and gas, and what it has to offer Kyiv militarily is limited even compared to other European nations, let alone the United States. Always there is a suspicion of delay, reluctance and fear. In Germany and elsewhere this has been read as nothing less than a crisis of political identity. More than anywhere else in the West, the entire German intellectual class, and every TV talk show and newspaper has been mobilised to debate and criticise Germany’s performance. The situation has been aggravated after Volodymyr Zelensky’s attack on Germany’s long-running détente with Russia in a speech to the Bundestag in March and a stream of remarkably forthright comments from Ukraine’s ambassador to Berlin.You can tell matters are becoming really serious because Jürgen Habermas, the 92-year old doyen of German philosophy and political commentary, has entered the ring, for once on the side of the government.

Read the full article at The New Statesman

May 10, 2022

Chartbook #120: St Javelin, Lockheed & the arsenal of democracy

If there is a weapon that symbolizes the war in Ukraine, it is the FGM-148 anti-tank infrared guided missile also known as Javelin. Images of St Javelin which shows Mary Magdalene holding a Javelin launcher in the style of an Eastern Orthodox church painting have become memes. Sticker and merchandise sales from the official site have raised over $800k for Ukraine’s resistance.

The portable, highly accurate Javeline missile allows small teams of infantry to take on armored columns at ranges of up to 4 kilometers. It fits perfectly with the David and Goliath narrative of the war in Ukraine, on which more in a future Chartbook.

Miraculous though it may seem, the Javelin is not a gift from god. Its development goes back to the early 1980s when the US Army specified its requirement for an Advanced Anti-Tank Weapon System. Initial exploratory research work was done by Ford Aerospace (laser-beam riding), Hughes Aircraft Missile System Group (imaging infrared combined with a fiber-optic cable link) and Texas Instruments (imaging infrared). Full-scale development began in 1989 as a joint venture between Texas Instruments and Martin Marietta, with production beginning in 1994 and deployment in 1996. It is now the property of Raytheon and Lockheed Martin.

If the Javelin missile on the battlefield today has a mother it is not a faux orthodox Saint, but Linda Griffin, a Senior Assembler at Lockheed Martin’s missile plant in the county seat of Troy, Alabama.

With family in the military, Linda and the Javelin anti-tank missile team fully recognize how critical this work is. https://t.co/jBS4FKY6Qd pic.twitter.com/E9HEgEN5QW

— Lockheed Martin (@LockheedMartin) May 3, 2022

Lockheed’s Troy plant is not large. All told it employs around 600 direct and contractor staff, of which 265 support Javelin production.

Over the last 25 years Ms Griffin’s has personally handled every one of the 50,000 Javelins produced by Lockheed in Troy. She made that proud boast in the course of a corporate reception for President Biden on a recent tour of the plant.

This week, we were proud to show @POTUS the Javelin anti-tank missile final assembly line and how we are on a mission to support our customers and allies in mission success. pic.twitter.com/YVT48ZssLb

— Lockheed Martin (@LockheedMartin) May 6, 2022

Everyone loves the Javeline. Visiting the factory Biden had a message that fitted right in with his promise of a foreign policy for the American middle class.

“Being the arsenal of democracy also means good-paying jobs for American workers in Alabama, in the states all across America, where defense equipment is manufactured and assembled,” Mr. Biden said Tuesday.

So far the Biden administration has delivered 5500 Javelin missiles to Ukraine from its stockpiles. That accounts for about a quarter of the extant stock in the US. What America aims to do now is to raise production from its current level of c. 2000 per annum to a maximum capacity of 6,000 per year. The question is how fast that can be done.

The problem is that the missiles each contain about 250 microchips which are in short supply. And labour is scarce too. Lockheed opened its plant in Troy in 1994. As Doug Cameron reports for the WSJ

Companies such as Lockheed tend to locate facilities producing munitions in more remote areas, in part because of the hazard associated with sensitive materials, which has also historically helped keep costs down. … .

As Jim Taiclet, CEO of Lockheed told an event last year: “The good thing about where our locations tend to be is they’re not necessarily in Palo Alto, for example, where there’s direct competition.”

The Javlin is a late product of what Ann Markusen et al famously called the “Gunbelt”, a remapping of the US economy produced by the military-industrial complex. From World War II onwards, jobs were relocated from the industrialized and unionized North to the low-wage South. CEO Taiclet is right. Pike county Alabama, of which Troy is the capital, is not Palo Alto.

The median income for a household in the county was $25,551 …. Males had a median income of $27,094 versus $18,758 for females. The per capita income for the county was $14,904. About 18.50% of families and 23.10% of the population were below the poverty line, including 29.90% of those under age 18 and 21.90% of those age 65 or over.

America’s military hardware may have arrived on the Ukrainian battlefield like a miracle, but in per capita income terms the gap between the production site of the Javelin missile in Alabama and Eastern Europe is not as wide as you might imagine.

As Doug Cameron reports, times are good in Troy. The unemployment rate fell to 2.4% in March 2022, half the level four years earlier. Lockheed is due to host its latest job fair at Kennesaw State University near its facility in Marietta, Ga.

On the eve of Russia’s invasion of Ukraine and amid a national labor shortage, Lockheed was offering to pay $16 to $20 an hour for trainee assembly workers at the plant, and a $1,500 signing bonus for college graduates with the security clearance required for many of the positions …. The company currently lists 26 vacancies at the Troy plant, including missile assemblers, quality supervisors and engineers.

Lockheed fells the urgency of the moment.

Jim Taiclet, Lockheed’s chief executive, said that though it has been awaiting contracts for fresh Javelin production, it was prepared to invest in hiring, tooling and potential supplier support.“For something this urgent, we’re going to go ahead and invest in it ahead of need,”

“I went over to the Pentagon with my team and basically told the senior leadership there, ‘Look, we’re already investing in increasing the capacity, please make it right and give us the contracts and agreements we need down the road, but we’re going to start investing now,’” he was quoted as saying by Inside Defense.

“Please make it right!” is quite the phrase. According to multiple reports, Taiclet and other defense industrial CEOs have been in regular meetings with the Pentagon to ramp up production.

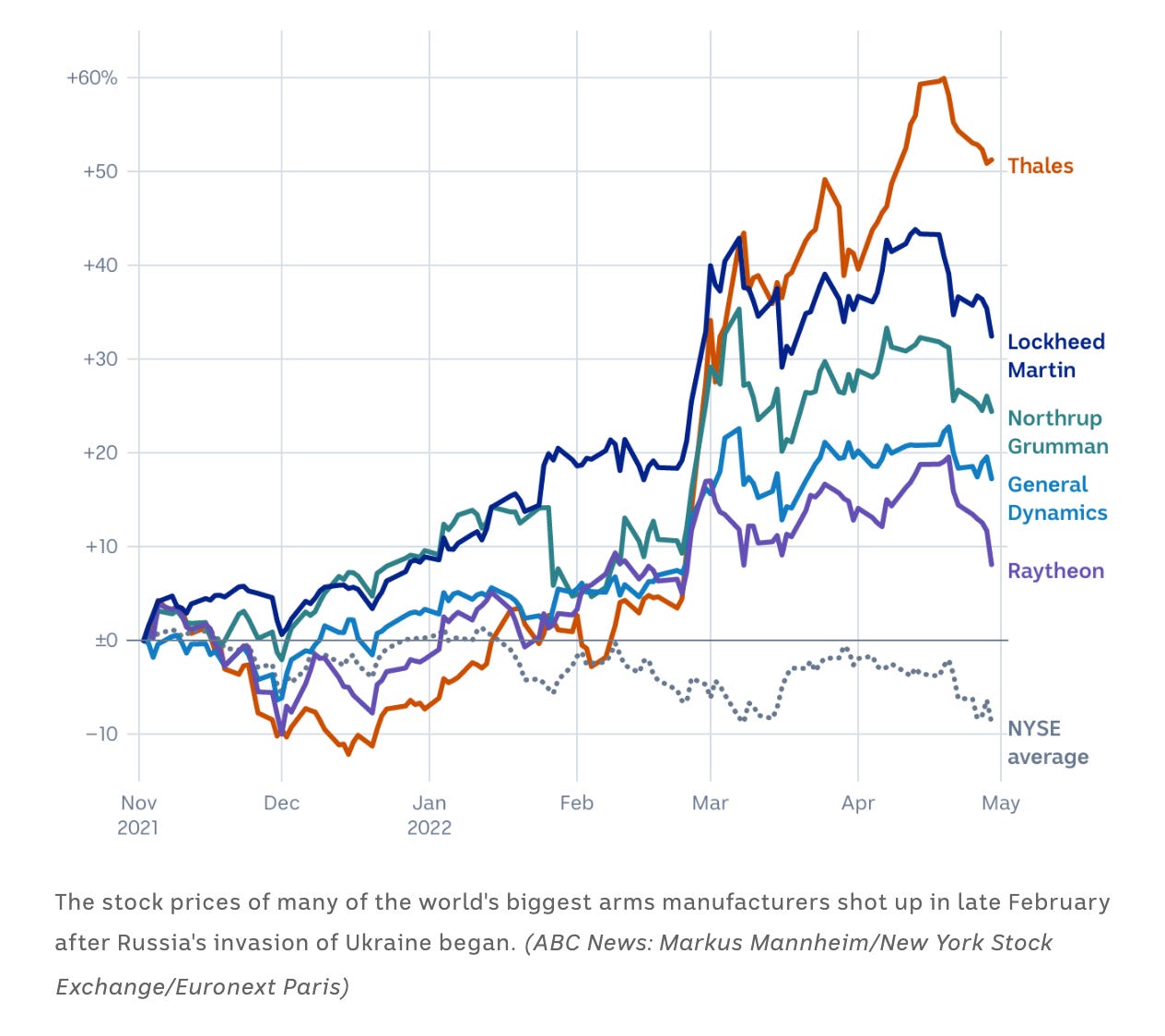

At the start of the year the sales of America’s contractors were declining under the impact of supply shortages. But since February 2022 the story has turned. On earnings calls Lockheed Martin, Raytheon Technologies, Boeing, Northrop Grumman and General Dynamics — prime contractors for the US Department of Defense — have all acknowledged the surge of business coming their way. Their stocks are bucking an otherwise bearish market.

Worldwide, in 2021 global defence spending topped $2tn for the first time, according to the Stockholm International Peace Research Institute.

The war in Ukraine has put the focus on land weapons systems, but the really big ticket items in naval and aerospace will be driven by mounting tension between West and China. Defense consultants affect a professional, somber tone, but in truth they can hardly disguise their glee. As one remarked to the FT.

“The depressing reality is that the last 30 years of [relative peacetime] might just be an aberration,” said Richard Aboulafia, an aerospace consultant at AeroDynamic Advisory. “[People thought:] ‘We won the cold war. Now, that’s the end of naked human aggression — excellent — let’s go start a unicorn petting zoo and everything will be fine.’ And it didn’t work.”

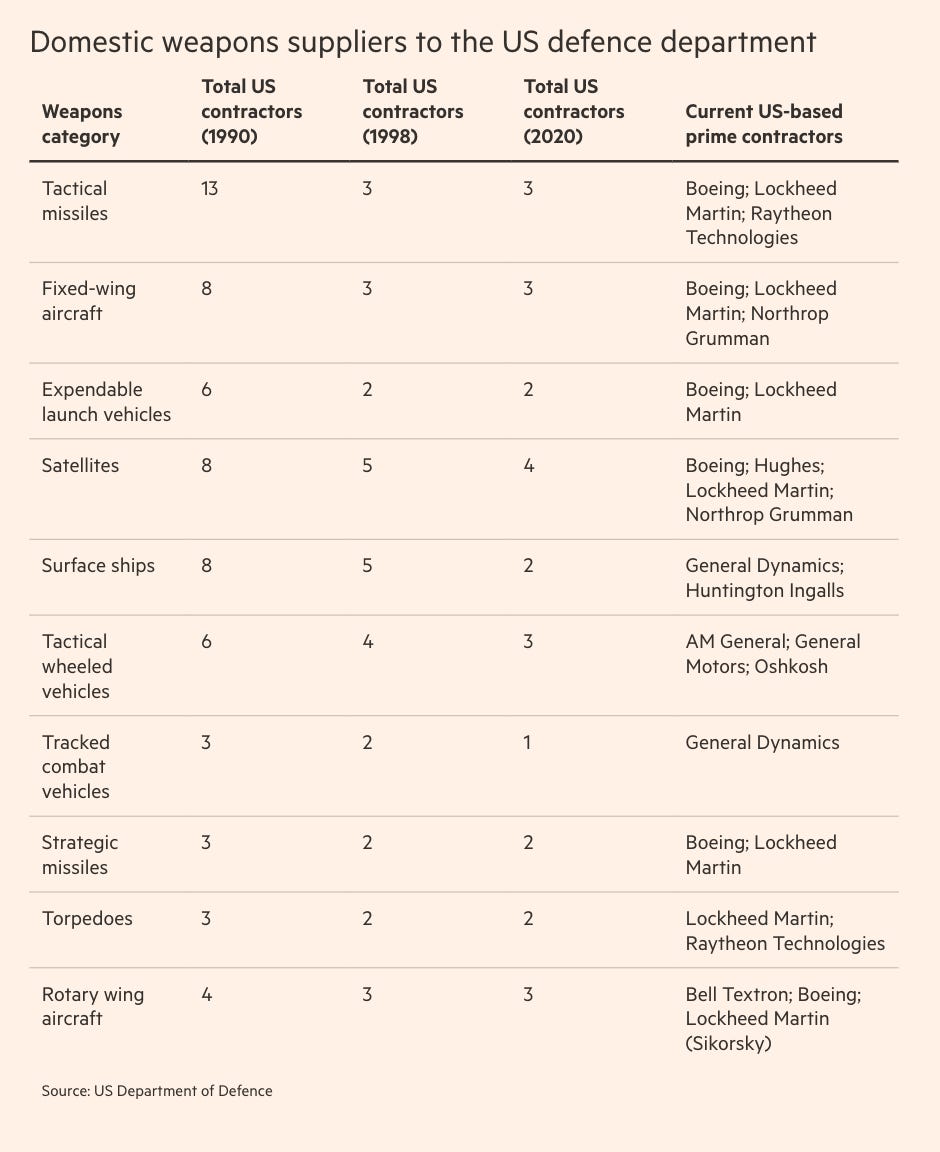

Now is a moment for defense industrial lobbyists to demand investment in a sector, which has changed dramatically since the end of the Cold War. In the early 1990s the Pentagon worked with 51 prime defense contractors. Today it deals with five diversified corporations, of which Lockheed is, by some margin, the largest.

In 2020, defense contracts accounted for 58 per cent of Pentagon spending, the highest level in 20 years, according to CSIS. Of the $421bn doled out in contracts that year, 36 per cent went to the Big Five contractors, up from 19 per cent in 1990.

In the arguments of lobby groups like the National Defense Industrial Association macroeconomics and oligopolistic special pleading go hand in hand.

The trade group has warned about the combination of worker shortages and supply chain kinks…. “A surge of new demand when there is a positive output gap would likely result in production shortages, price inflation and a lack of investment in new productive capacity,” it said in a January report on the defense industrial base.

The jostling for position within the industry is full of intrigues that play out up and down the supply chain.

The two key contractors for the Javelin are Lockheed and Raytheon Technologies Corp., which makes the famous fire and forget missile control system in Tucson, Ariz. As far as the Javelin is concerned, Lockheed and Raytheon seem to rub along amicably enough. The same cannot be said for the solid fuel rocket which after an initial soft launch, ignites at a safe distance from the tank hunters and propels the missile to its target thousands of meters away.

In 1990 the US had eight manufacturers of rocket motors. Now it has two. For the Javelin the key supplier is Aerojet Rocketdyne, of El Segundo California. After Northrup Grumman bought its lone rival Orbital ATK Inc. in 2018. Rocketdyne is now the only independent producer of rocket motors.

Unsurprisingly, given Northrop’s move, Lockheed was until early in 2022 maneuvering to snap up Aerojet for $4.4 billion. It was blocked by the Federal Trade Commission on antitrust grounds. Even the Pentagon is concerned about the degree of consolidation in the rocket motor sector.

The collapse of the Lockheed takeover has triggered a knock down drag out fight within Aerojet over the future of the company. This would be a storm in a tea cup were it not for the fact that space rocketry, missile defense and cutting-edge technology such as hypersonic missiles all depend on Rocketdyne motors.

In rocketry right now there is a lot of excitement about Mach 5 hypersonic weapons. Deep space exploration is also on the minds of America’s military-industrial rocketeers. Representative Don Beyer recently told a gathering: “The work you’re doing isn’t just about engineering work and science. You’re imagining and realizing the future of humanity.” And as Rep Frank Lucas told the gathering “Our nation once again stands at the threshold of deep space exploration.”

Lockheed Martin is Aerojet’s biggest customer, accounting for a third of sales, but its rocket motors are used on other military and commercial missiles and space vehicles developed by companies including Boeing Co. and Raytheon Technologies Corp.

As far as Lockheed is concerned “space”, at roughly 18 percent of revenue is a bigger segment than missiles and fire control, which account for less than 16 percent. Lockheed’s space division makes Trident II D5 Fleet Ballistic Missile for U.S. Navy, Orion Multi-Purpose Crew Vehicle spacecraft for NASA, GPS III for US Air Force. The missile division is responsible for the Patriot Advanced Capability-3 (PAC-3) and Terminal High Altitude Area Defense systems, Multiple Launch Rocket System, Hellfire and Joint Air-to-Surface Standoff Missile.

All of this puts Troy Alabama and its Javelin anti-tank missiles at $70k per missile in perspective.

Javelins are popular, they are demotic, they put a “middle class” (aka working class) face on the military-industrial complex – Linda Griffin take a bow – but they are negligible in business terms. To see how the war in Ukraine makes a really significant impact on Lockheed’s business you have to look up, not at ground-hugging anti-tank missiles, but into the sky, to the fast jets roaring overhead.

Aerospace at 40 percent of turnover is by far the largest of Lockheed’s business segments. Lockheed makes the C-130 Hercules, the F-16 Fighting Falcon and F-22 Raptor and above all it is the lead contractor for the F35.

The F35 is perhaps the most complex and expensive manufacturing operation ever undertaken. Total life time costs of the program for the Pentagon out to 2070 are estimated at $1.7 trillion. According to one estimate, European clients of Lockheed should expect to spend $700-800 million for every single F35 they purchase.

The F35 is controversial and massively expensive. It is also a calling card, passport and passkey to the American alliance. When Turkey’s Erdogan contracted with Russia for its SS-400 anti aircraft system, he was cut out of the supply-chain. Poland has bought the system as a down payment on its special relationship with the US.

Which brings us to the spring of 2022 and Chancellor Olaf Scholz’s famous historic rupture (Zeitenwende). Scholz declared that Germany would henceforth aim to raise its defense spending to at least 2 percent of GDP and set aside a special 100 billion euro fund to make good for years of underinvestment. Three weeks later Germany reversed a decision taken in 2019 against the F35 and announced that it was placing an order for 35 Lockheed planes, with which to replace outdated Tornado’s in the tactical nuclear strike role.

For Lockheed that is a nice bit of business. But presumably the greater significance of the move is the shockwave it has sent through Europe’s rival aerospace system. In France Berlin’s decision has provoked consternation.

In 2017 – the year of the Trump shock – France and Germany teamed up to form the Future Combat Air System, Europe’s flagship defence project to build a new European fighter jet, FCAS. It was seen as a central building block for the region’s defence and procurement policy and a marker of strategic autonomy. After the F35 decision Berlin insists that it remains committed to European cooperation, but Dassault and Thales are clearly concerned. Dassault and Airbus, which represents Germany in the European FCAS project, were already at loggerheads over technological sharing. Now Germany’s F35 decision means that Germany may not need more new fighters before 2050, whereas France will want to replace its Rafale jets by 2035. European experts however insist that arguing over the F35 is an excuse. The real problems lie in the inherent difficulty of the project, the lack of high level political commitment and the battle between Dassault and Airbus. If the Germans drift back in to America’s orbit, France may feel it no longer needs them as a partner. It is not just American contractors who are benefiting from the defense boom.

Francis Tusa, editor of newsletter Defence Analysis, argued that what helped to shift the balance in the relationship between Airbus and Dassault in recent months were significant export orders for the French company’s Rafale, including from the United Arab Emirates. “Team France no longer needs Germany in the programme. They have orders coming out of their ears,” he said, adding that he expected further orders for the fighter that could take production through to 2036.

Meanwhile, America’s top brass were delighted. In May 2018, Lieutenant general and Inspector of the German Air Force Karl Müllner found himself out of a job after stating publicly stating his preference for the F-35. Now General CQ Brown Jr, Chief of Staff of the United States Air Force could congratulate Team Luftwaffe on their F35 decision. “I recently heard the F-35 referred to as the “partnership plane” … I couldn’t agree more.

****

I love putting out Chartbook. I am particularly pleased that it goes out for free to thousands of subscribers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options:

May 7, 2022

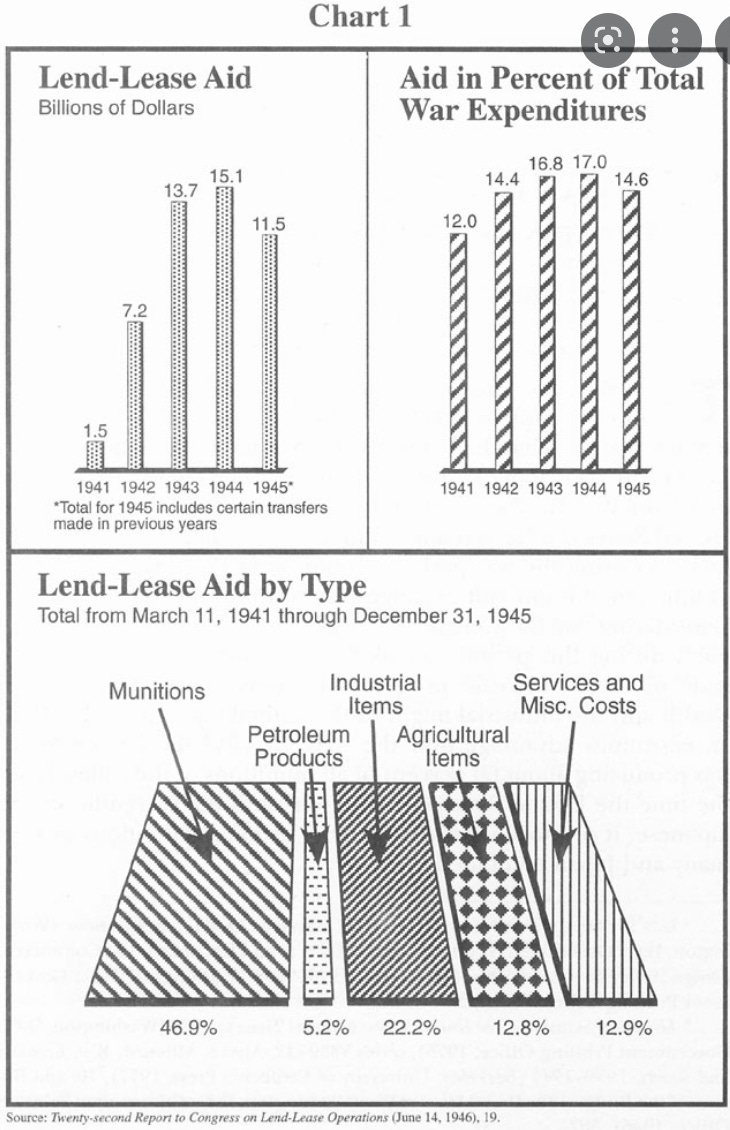

Chartbook #119: Lend-Lease & Escalation

Containers of Dodge trucks awaiting shipment to Russia under the lend-lease agreement, August 1943. Library of Congress, Washington, D.C.; Alfred T. Palmer, photographer (LC-USE6-D-002838)

In 2022, we wait with bated breath to see how Putin will mark “Victory day”, the day of celebration that marks the Soviet Union’s defeat of Nazi Germany. Meanwhile, in Washington DC as well, they are summoning the ghosts of the past. If Putin evokes the Great Patriotic war, on our side the references are to the Cold War, World War II, the spirit of the enlightenment, ancient battle of democracy against autocracy and so forth.

To offer lessons and inspiration at times of crisis is a classic role for history. Indeed, it is, perhaps, the classic role for public history, But, in this role, history is closest to myth-making. It serves as much to close off, as to open debate. “We all know that appeasement was a disaster, so …. ” etc etc.

To deny the significance of history in this role would be naive and unrealistic. After all, sometimes we need to act and often we need inspiration.

But, there is also a role for critical history. Not to prejudge the question at hand but precisely to ensure that quasi-mythic history is not being used to foreclose the evaluation of the options that are available to us and the likely consequences of those decisions. Capsule histories, long ago smoothed into triumphant narratives promise outcomes far neater than what we can actually expect.

In this sense, critical history is not merely academic pea-shooting. It is part of the daily struggle to preserve a realistic attitude. It is part of the daily struggle to orientate ourselves in medias res – in the middle of things – in the actual middle of the actual things, here and now and not in the 1940s.

During the spring meetings of the Bretton Woods institutions a few weeks ago, the talk was of the Marshall Plan. I discussed in the New Statesman and in a previous Chartbook whether that example is really relevant to our situation.

The historical Marshall Plan was more complicated and less massive than is commonly imagined. It was also a postwar program. That does not mean that the Marshall Plan was innocent in geopolitical terms. On the contrary, it was a key driver of Cold War division of Europe. By the 1950s it merged with US military assistance to drive the rearmament of Europe and Asia. But the Marshall Plan is not remembered for starting World War III. Instead, we invoke it like a comfort blanket – a big fix for a big problem with a happy end.

The program under which America bankrolled and supplied Allied victory in World War II was Lend-Lease. Launched in March 1941 It was originally intended to back the British Empire, Greece, China in their separate struggles against Nazi Germany and Imperial Japan. After the Nazi invasion of the Soviet Union American assistance was extended to the Soviet Union as well.

Vastly larger than the Marshall Plan and launched into a middle of on-going wars, Lend Lease was a dramatic act of escalation. As the best known history of Lend-Lease remarks: “The Lend-Lease Act marked the point of no return for American policy regarding Hitler’s Germany.” Lend Lease tied together the separate struggles in Europe and Asia to create by the end of 1941 what we properly call World War II.

Source: Hyperwar

It is striking – to say the least – that already in January 2022, before Putin’s invasion, the US Congress had taken up Lend-Lease as the historical inspiration for a legislative measure that frees the Biden administration’s hands in providing aid to Ukraine.

The Ukraine Democracy Defense Lend-Lease Act was unanimously approved by the Senate and passed by the House of Representatives by a vote of 417 to 10. Now, according to remarks made by press secretary Psaki, Biden may sign it into law on May 9th.

Will a new Lend Lease Act be America’s answer to Putin’s “Victory day”?

As well-informed defense journalists point out, the Lend Lease Act of 2022 adds very little to Biden’s already extensive powers to support to Ukraine. Far more consequential in that regard are the $33 billion in additional aid that Biden has requested. But that isn’t the point of the Congressional measure:

… this is the actual genius of the Ukraine Democracy Defense Lend-Lease Act. Even if the exemption of certain lease provisions isn’t going to do anything that existing authorities don’t already cover, invoking the memory of Lend-Lease is an entirely different issue. Frankly, nobody will wax poetic about the 1961 Foreign Assistance Act. … But Lend-Lease is a term that is ingrained in the American story.

… it’s the spirit of the law that’s vital here. … Achieving something other legislative proposals have not, it has set the proper tone for the conversation. The clear decision of the American people, as represented in Congress, to put the power of American industrial might, guided by Ukrainian hands, into the fight against Russian aggression.

“The American story” was very much to the fore, when, in supporting the measure in the House, Speaker Nancy Pelosi invoked the legacy of her father who was one of the House members who followed FDR’s call to vote for the original bill.

81 years ago, President Franklin Delano Roosevelt came here to the Congress of the United States, to the House of Representatives – where I’m proud to say my father, Thomas D’Alesandro, served as a Member of Congress – and President Franklin Roosevelt delivered a bold and historic request.

Symbolism aside, the scale of the aid now being envisioned by the Biden administration is unprecedented. As Ben Freeman and William Hartung point out at Responsible Statecraft

if Congress signs off on this new request the U.S. will have authorized $47 billion in total spending to Ukraine. That’s more than the Biden administration is committing to stopping climate change and almost as much as the entire State Department budget.

This is twice the maximum amount of money ever provided in a single year to the Afghan army (as opposed to money spent by the US in Afghanistan) and seven times the US military aid budget for Israel. The total request amounts to one third of Ukraine’s prewar GDP. As far as Ukraine is concerned, the US is bankrolling a total war effort and the US political class has with near unanimity declared that the appropriate historical analogy for this effort is 1941 – “All measures short of war”.

As Lockheed Martin has announced it is ramping up production of Javelin anti-tank missile systems to meet the unexpected surge in demand. As Chief executive James Taiclet announced.

“I went over to the Pentagon with my team and basically told the senior leadership there, ‘Look, we’re already investing in increasing the capacity, please make it right and give us the contracts and agreements we need down the road, but we’re going to start investing now,’”.

In a short piece in The Guardian last week I queried what the implications might be of this discursive move. What history are we summoning in evoking the Lend-Lease act of 1941?

Last year, the 80th anniversary of 1941 saw the publication of three substantial books that throw new and often alarming light on that moment.

As Stephen Wertheim – one of the founders of the Quincy Institute for Responsible Statecraft – spells out in his book Tomorrow, the World following the collapse of British and French resistance on the continent of Europe to early 1941, American strategists shifted from the Wilsonian stance of wanting to arbitrate world affairs from a vantage point of armed neutrality, to a full-throated interventionism. What was now envisioned was that that the United States should reshape the world order through direct and massive engagement on a global scale. Though this shift in strategy began within the Roosevelt administration in 1940, it was in 1941, with Lend Lease, that it broke into the open.

In order to supply the fight against the Axis, Roosevelt sought the assent of Congress, as he had not done over the destroyers deal (in 1940). He wagered that noninterventionists, if brought into the open, would suffer a crushing defeat. He was right. The Lend-Lease Act, debated in January and February and passed in early March, removed the cash-and-carry restrictions and empowered Roosevelt to designate future recipients of aid. Under international law, no neutral could assist a belligerent as America was aiding Britain. Interventionist lawyers thus decided that America was not a neutral. Led by Quincy Wright, the political scientist and international lawyer, they popularized the category of nonbelligerent to characterize the U.S. position.31 By shedding the vestiges of neutrality, Roosevelt freed up interventionists to think and speak about the kind of world for which the Anglophone Allies stood. Even before the LendLease Act passed, Borchard lamented that noninterventionists had been “out-shouted.”32

Roosevelt’s wager that he could defeat the non-interventionist would be vindicated. But as Wertheim reminds us it was more of a stretch than the bards of the “American story” might be comfortable remembering.

In 1940-1941, polling by Gallup showed considerable opposition to greater intervention in the war against Hitler and Mussolini. The original Lend-Lease act passed through Congress against far tougher opposition than the revival of the Act has faced in 2022. Eventually, it passed the House by 260 to 165 and the Senate 60 to 31.

As Wertheim points out, it was in the course of the Lend-Lease debate, in February 1941, that Henry Luce launched his appeal for his fellow Americans to take up the mantle of the “American Century”, an idea that continues to hang over the “American story” today.

The question that must haunt us today is whether Lend Lease in 1941 set America on an inescapable path towards war. Both critics and supporters of FDR always insisted that Lend Lease had in effect set a trap. As Warren F Kimball reports in The Most Unsordid Act. Lend-Lease 1939-1941

A day or so after Roosevelt’s announcement of the Lend-Lease idea, Hull (Secretary of State) remarked to Breckinridge Long (Assistant Secretary) that, depending upon Hitler’s actions, America could be in the war within ten days or six months. Long, who was closely akin to Joseph Kennedy in his views of the situation, was more inclined to believe that America’s belligerency would depend on the amount and type of aid given to Great Britain. Either way, both men found their thoughts running in the direction of war as a result of the President’s newly announced program.

On the other side of the Atlantic, Britain of course devoutly hoped that Lend Lease was just the beginning and the US would soon be dragged, willy-nilly into the war. As the debate raged, Britain waited anxiously to know how the Congressional vote would go. As Kimball reports,

H. Duncan Hall, who was attached to the British Embassy in Washington at the time, captured the tense emotion: “For the first time in its history the United Kingdom waited anxiously on the passage of an American law, knowing that its destiny might hang on the outcome. London waited with an imperfect knowledge of American legislative processes and little understanding of American public opinion.” 73 The effects of the Great War, long hidden from public view, had wrought a permanent change in the Britain of Castlereagh, Kipling, and Churchill. The king was dead—long live the king!

But, as Cordell Hull had remarked, assuming that American public opinion would not back a unilateral declaration of war by the United States, the future depended not on Washington or London, but on the reaction in Berlin.

In Wages of Destruction, back in 2006, this is how I described the reaction of Germany to the announcement of Lend-Lease.

The first line of the report from the Washington embassy on lend-lease, received by the Foreign Ministry, the Wehrmacht high command, the army and the Air Ministry, stated bluntly: ‘The Lend-Lease Act currently before Congress . . . stems from the pen of leading Jewish confidants of the President. It is intended to give him the possibility of pursuing without limitation his policy of influencing the war through all means “short of war”. With the passage of the law the Jewish world-view will therefore have firmly asserted itself in the United States.’ It then went on to itemize the huge deliveries that could now be expected by ‘England, China and other vassals’.46

For me, as for Tobias Jersak and an interpretive line that runs back to Saul Friedländer’s early book Prelude to downfall: Hitler and the United States 1939–1941 (1967), Lend Lease was a key moment in the escalating tension between the United States and Nazi Germany that impelled not just military strategy but also the radicalization of the regime’s racial policy.

The idea that FDR was under the control of Jewish influence did not originate with Lend-Lease but in earlier antagonism between the Third Reich and the United States. The attention of Nazi racial ideologues had shifted to the US over the winter of 1938-1939 following FDR’s denunciation of the Kristallnacht pogrom and the so-called war of words between Hitler and the White House.

Most openly the coming confrontation with the United States was anticipated by Hitler in his ominous speech to the Reichstag of 30 January 1939 in which he linked the prospect of a world war i.e. a war with the United States, to the threat that European Jewry would be annihilated.

Throughout 1939 and 1940 German military planners paid anxious attention to America’s armaments efforts and purchases in the US by Britain and France. Regime literature directed towards the inner core of the Nazi party and the SS was studded with references to Jewish influence in the United States.

Against this backdrop, Lend-Lease was a dramatic escalation that confirmed the Nazi’s worldview. Britain and the United States were linked in an antagonistic alliance, motivated by dark forces bent on Germany’s destruction.

In the compass of the very short Guardian piece, the editors and I decided to bracket this dimension of the history of 1941. It is simply too explosive and too easily misread as some kind of absurd equation between Hitler and Putin. But if you want to wrestle with the actual history of Lend Lease you cannot side step its entanglement in Hitler’s Manichean anti-semitic worldview.

2021 saw the publication of two new historical studies that reinforce this line of interpretation. As we learn from Klaus Schmider’s meticulous reconstruction of the build-up to the German declaration of war on the United States on December 11, in Hitler’s Fatal Miscalculation (2021), Hitler was, indeed, deeply concerned about Lend-lease. As he told his entourage on March 24 1941:

‘the Americans have finally let the cat out of the bag; if one felt so inclined, it would be legitimate to interpret this as an act of war. He was now in a position to allow a war to break out without further ado. However, right now, it was not something he was keen on. The war with the US was sure to come sooner or later anyway. Roosevelt and the Jewish financiers have no other choice to than to strive for this war, since a German victory in Europe would mean enormous financial losses for the American Jews. It is merely regrettable that as yet no planes existed which could bomb American cities. This is a lesson he would like to teach the American Jews. To be sure, this new Lease Law would bring him additional major problems. He had now come to the conclusion that its success could only be prevented by ruthless naval warfare.’

When Hitler met Japan’s Foreign Minister in April 1941 he told him that war with the United States was already “taken into account”.

As Lend-Lease deliveries ramped up, this set the stage for the Atlantic Charter meeting between FDR and Churchill on 14 August 1941, from which would emerge the United Nations. That too, as Tobias Jersak first argued, was interpreted in Berlin as a tightening of the global conspiracy against the Nazi regime. And that had ominous implications.

Throughout the autumn of 1941 as the struggle on the Eastern Front entered its climactic stage, references multiply to Hitler’s prophecy i.e. his Reichstag speech of 30 January 1939.

In his address to the troops of Army Group Centre on 2 October ahead of the final push to Moscow (operation Typhoon), Hitler linked the decisive battle for Moscow directly to the racial struggle not just on the soil of the Soviet Union but worldwide. Germany was now at war both with Bolshevik Russia and capitalist Britain, behind which stood the United States. Superficially different, the two economic systems were in fact fundamentally alike. Bolshevism was no better than the worst kind of capitalism. It was a creator of poverty and destitution and ‘the bearers of this system’, ‘in both cases’, were ‘the same: Jews and only Jews!’ The assault on Moscow was to deliver a ‘deadly thrust’ against this arch-enemy of the German people.”

Hitler’s problem was how to conduct that global war. Without a powerful navy or a strategic air force he had few ways to strike at the British Empire, let alone the United States. It was that calculation that ultimately bound Nazi Germany to Imperial Japan and drove Hitler towards his declaration of war on the United States on December 11.

As Brendan Simms and Charlie Laderman make clear in their extraordinary reconstruction of the events between Pearl Harbor and Germany’s declaration of war, Hitler did not stumble into war, his declaration of war on December 11 1941 was a deliberate gamble.

Simms and Laderman’s book deserves far more attention than it has received. Its effort to reconstruct a week in global history – perhaps the most fateful week in history – on a minute by minute basis strikes me as a fascinating and original way of writing the history of an “event”. Others may know better, but I have never read a historical account that starts with a map of global timezones. In the current moment, it is hauntingly evocative.

The pay off from Simms and Laderman’s meticulous blow by blow account is to sharpen our sense of how vertiginously contingent the escalation to global war seemed in the second week of December 1941, even as it was happening. Above all they highlight the fact that the immediate impact of Pearl Harbor was not to confirm the logic of Lend Lease but – to the horror of London and Moscow – to cause Lend Lease to be suspended. If Hitler’s intention was to ally himself with Japan so as to divert resources from the Atlantic to the Pacific, his strategic vision was, for those few days at least, massively confirmed.

Indeed, as Simms and Ladermann argue, FDR was convinced that Japan was acting essentially as a German proxy. He refused to credit Japan with strategic autonomy. Hitler knew better and it was with a view to binding Japan to the German cause that he took the decision to declare war on the United States. After all, as far as Hitler was concerned, war between Germany and the United States was already “taken into account”.

As Simms and Ladermann remark:

It was Hitler’s declaration of war on the United States, much more than Pearl Harbor, that created a new global strategic reality and, ultimately, a new world. America did not enter “the war”—the conflict with Hitler—on December 7, 1941. Rather, the United States was plunged that day into a new and initially separate struggle against Japan. America did not truly join the war until December 11, 1941, and unlike the First World War, the United States did not take the initiative. It was, as British air marshal Arthur Harris had predicted, “kicked into the [European] war.”

As Roosevelt’s speech writer Robert Sherwood put it, Hitler had followed Japan in solving Roosevelt’s “sorest problems”. For Hitler too this was a moment of culmination. On 12 December, the day after Hitler’s declaration of war, Goebbels spoke to the Gauleiter, the regional officials of the Nazi party, and spelled out the connection.

“Regarding the Jewish question, the Führer is determined to clear the table. He warned the Jews that if they were to cause another world war, it would lead to their own destruction (30 Jan 1939). Those were not empty words. Now the world war (the war with the USA, AT) has come. The destruction of the Jews must be its necessary consequence. This question is to be regarded without sentimentalism. We are not here to have sympathy with the Jews, but rather with our German people. If the German people have sacrificed 160,000 dead in the eastern campaign, so the authors of this bloody conflict will have to pay for it with their lives.”

It was no coincidence that within a few weeks of Hitler’s declaration of war on the United States, Reinhard Heydrich and the State Secretaries would convene at the conference center on the Wannsee to scheme out what they called the final solution of the Jewish question in Europe. Originally, the Wannsee meeting had been scheduled for December 9 1941. It marked the culmination of a year-long planning project that had been set in motion over the winter of 1940-1941 when the invasion of the Soviet Union and the global escalation of the war came clearly into view. Heydrich’s meeting was put back to 20 January 1942, on account of the crisis on the Eastern front and the declaration of war on the USA.

Behind the sugar-coated narrative of a “good war” won by the “arsenal of democracy” – “the American story” evoked in Congress in recent weeks – lurks the actual history of the haphazard and contingent unleashing of an apocalyptic world war. To complete the picture, it was in October 1941 that Roosevelt issued an executive order green-lighted the atomic bomb program and cooperation with the British on scientific research.

****

In openly declaring our intention to adopt all measures short of war to ensure Russia’s military defeat and in invoking Lend Lease in doing so, we must surely ask ourselves that question, what is our theory of Putin? And beyond Putin what is our model of the escalatory dynamics at work in 2022?

In swathing ourselves in historic garments, are we inviting Putin to do the same? Are we inviting him to fully inhabit the role of the maniacal dictator who can only be crushed out of existence? Are we, as in 1941, crossing the point of no return? Are we, consciously or not, assuming further escalation?

In so doing, are we assuming that escalation will have the same kind of “happy end” that World War II eventually had for the United States in 1945? The kind of “happy end” that makes Lend Lease into a myth shrouded in good feelings – a grand chapter. in the “American story”?

Or, are we, in fact, hoping that 2022 unfolds as 1941 did not? That Putin is not suicidal? That this time the escalation remains confined to Ukraine and Russia? That this becomes, as some American strategists envisioned Lend Lease in 1941, a calculated exercise in using the dogged resistance of a client – then the British now Ukrainians – to attrit a geopolitical antagonist?

These are not comfortable questions. So much so that merely raising them can lay you open to accusations of defeatism. But that is beside the point. Supplying weapons may well be the best thing to do under the circumstances. It is certainly what the Ukrainian government is asking for. But to weigh the consequences of our actions and the risks attendant on them, to assess the costs and who pays them is a basic imperative of responsible politics. In so doing we need a clear head and democracy demands that clarity is not just something that is achieved behind closed doors.

Ukrainians at this moment may need history to give them courage. For us to revel in mythic references to the 1940s and “the American story” is a shameful, sentimental self-indulgence. If we are to evoke the past at all, let us do so in a critical and exploratory fashion, not to “prove” facile points one way or another, but to better understand how we arrived at this moment and to infer what its possibilities and risks might be.

May 6, 2022

Ones & Tooze: Why the U.S. Stock Market is Tanking

The U.S. stock market has dropped more in recent days than any other period since March 2020, the beginning of the pandemic. Adam and Cameron analyze why this is happening, beyond obvious reasons like the Fed interest rate increasing, and how much we should worry about it. Later in the show, they look at the economics behind the arms race in the war in Ukraine.

Find more episodes and subscribe at Foreign Policy

May 4, 2022

Is escalation in Ukraine part of the US strategy?

In the spring of Russia’s war on Ukraine, Washington DC seems haunted by the ghosts of history. The US Congress has passed the Ukraine Democracy Defense Lend-Lease Act of 2022 to expedite aid to Ukraine – just as Franklin D Roosevelt did, under the Lend-Lease Act, to the British empire, China and Greece in March 1941.

The sums of money being contemplated in Washington are enormous – a total of $47bn, the equivalent of one third of Ukraine’s prewar GDP. If it is approved by Congress, on top of other western aid, it will mean that we are financing nothing less than a total war.

Lend-Lease was a wartime intervention. The vast majority of the goods delivered were armaments. Monty’s army in the north African desert fought with Lend-Lease Sherman tanks. After 1942, the great Soviet counter-offensives were carried by Lend-Lease trucks.

What made this so extraordinary is that at the moment the Lend-Lease programme was launched in March 1941, the US was not in the war. Lend-Lease was the decisive moment in which the US, while not a combatant, abandoned neutrality. It forced jurists to come up with a new term to describe a stance of “non-belligerence”. In broader terms it marked the emergence of the United States as the hegemon that, for better and for worse, it remains today.

Read the full article at The Guardian

May 1, 2022

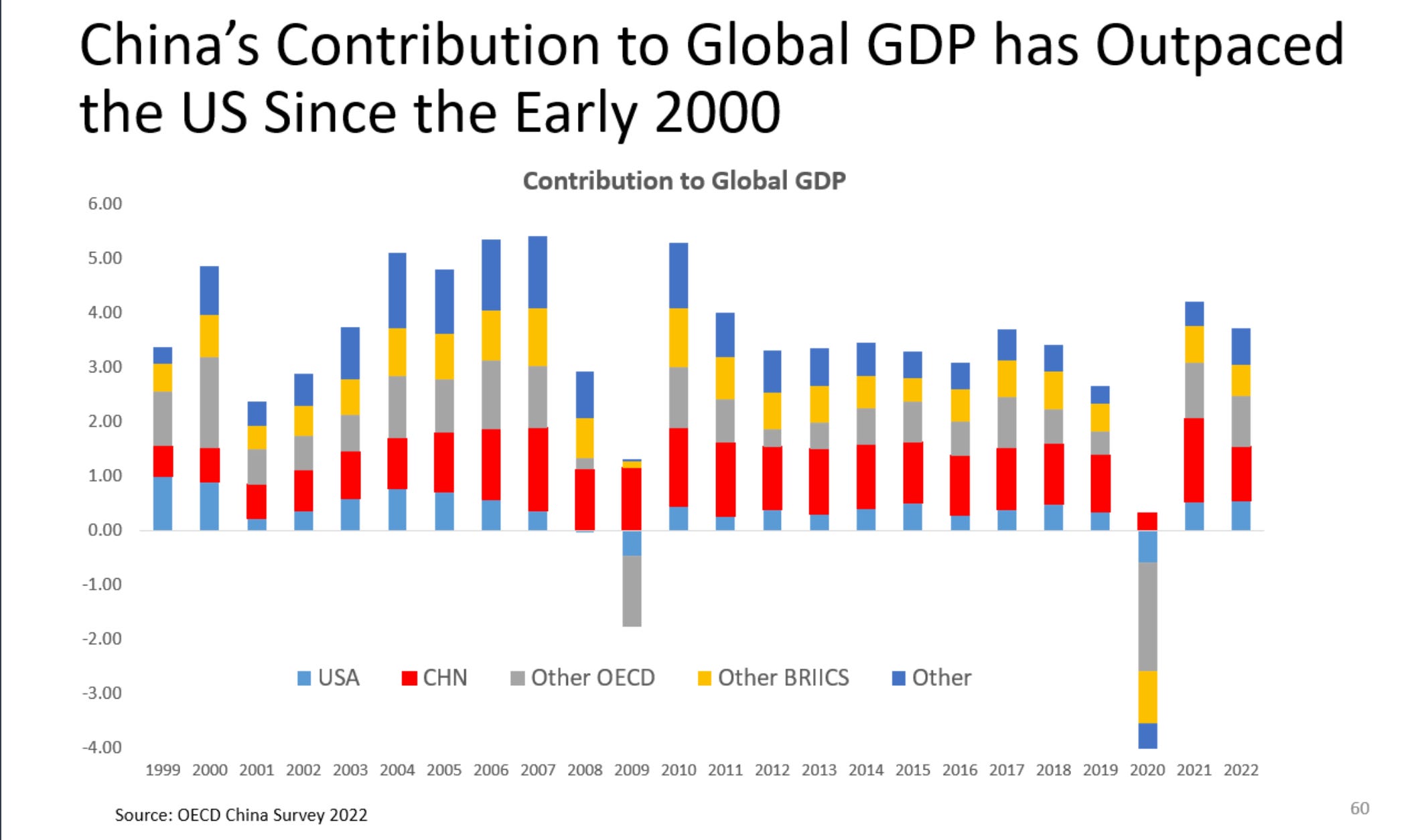

Chartbook #118: China’s growth prospects

The shift in Western discourse on China over the last five years has been dramatic. Trade wars, tech wars, COVID, Xi Jinping’s crackdowns, the real estate bubble, Omicron and now Putin’s war have all contributed. On this shift hinges our entire outlook for the global economy and world affairs more generally.

The front page of the FT this weekend was full of China gloom.

Faced with a cumulation of difficulties local commentators are so concerned that remarkably critical remarks are leaking to Western media

Weijian Shan, a veteran China investor, said in a recent recorded video meeting that the country was embroiled in a “man-made” crisis. “Large parts of [the] Chinese economy including Shanghai have been semi paralysed and the impact on the economy is going to be very profound,”

Covid lockdowns continue to disrupt logistics around the economy.

Foreign investors have recently pulled money out of China at a rapid rate, which goes hand in hand with a dramatic devaluation of the yuan.

All of this matters as much as it does, because the increasing polarization of global politics around the simplified axis of democracy v. “autocracy” (as seen through the lenses of many Western commentators) cuts across the interconnectednes of the global economy to which China over the last twenty years has been essential.

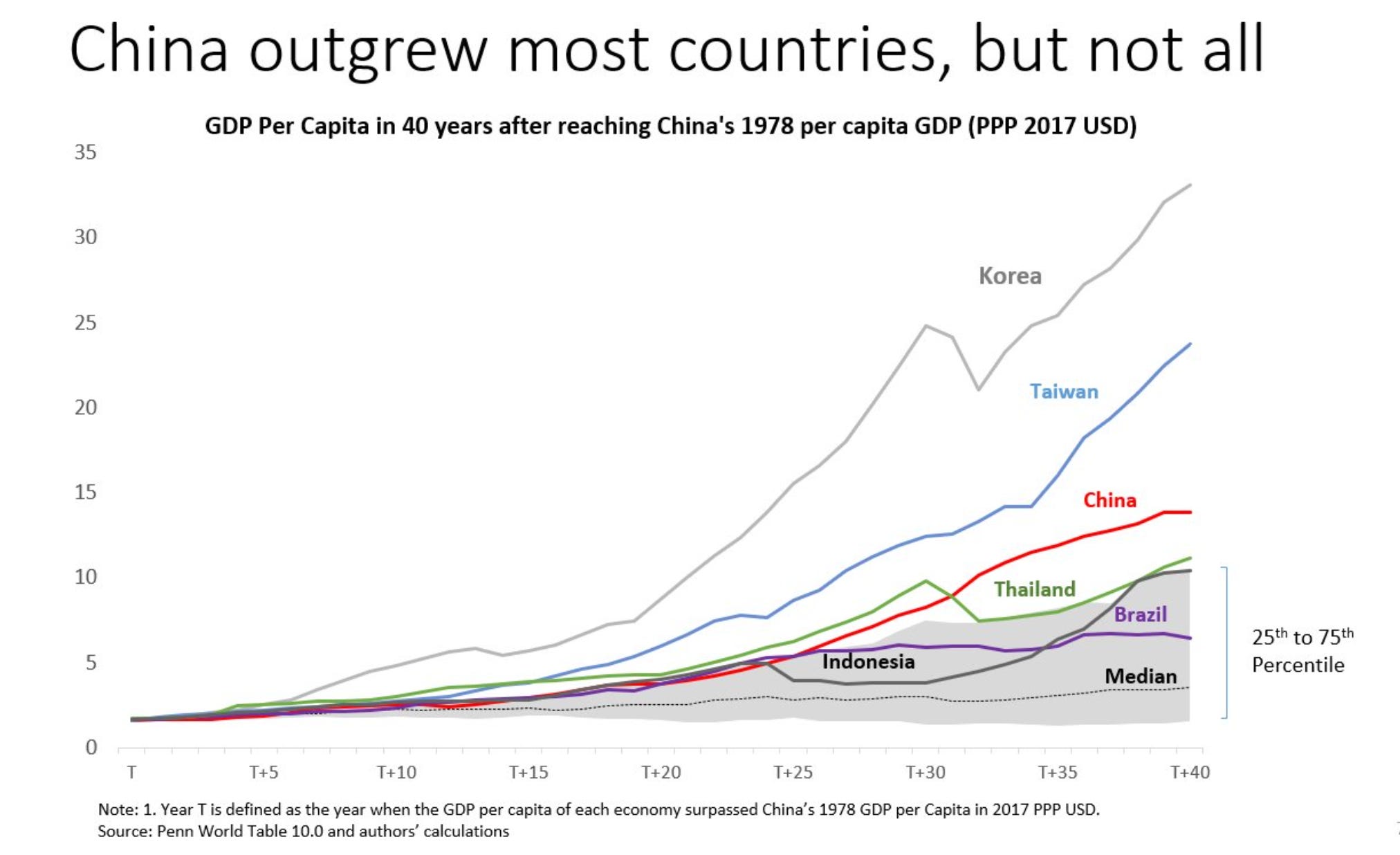

So this makes the question of China’s growth prospects into one of the key questions. of world affairs. And on this question – How Fast Can China Grow? – I strongly recommend this recent report by the Lowy Institute and this excellent presentation by Bert Hofman ex of World Bank, now National University Singapore.

Hofman starts by making the nice point that though China has grown very fast it was outpaced from a similar GDP per capita baseline by South Korea and Taiwan.

Of course those are much smaller countries with different initial conditions. I wonder how that comparison would look, if one applied the “California school” move to the present day i.e. compare S Korea and Taiwan not to China as a whole but to China’s most rapidly growing regions – Shanghai, Beijing, Shenzhen, Chongqing, Guangzhou.

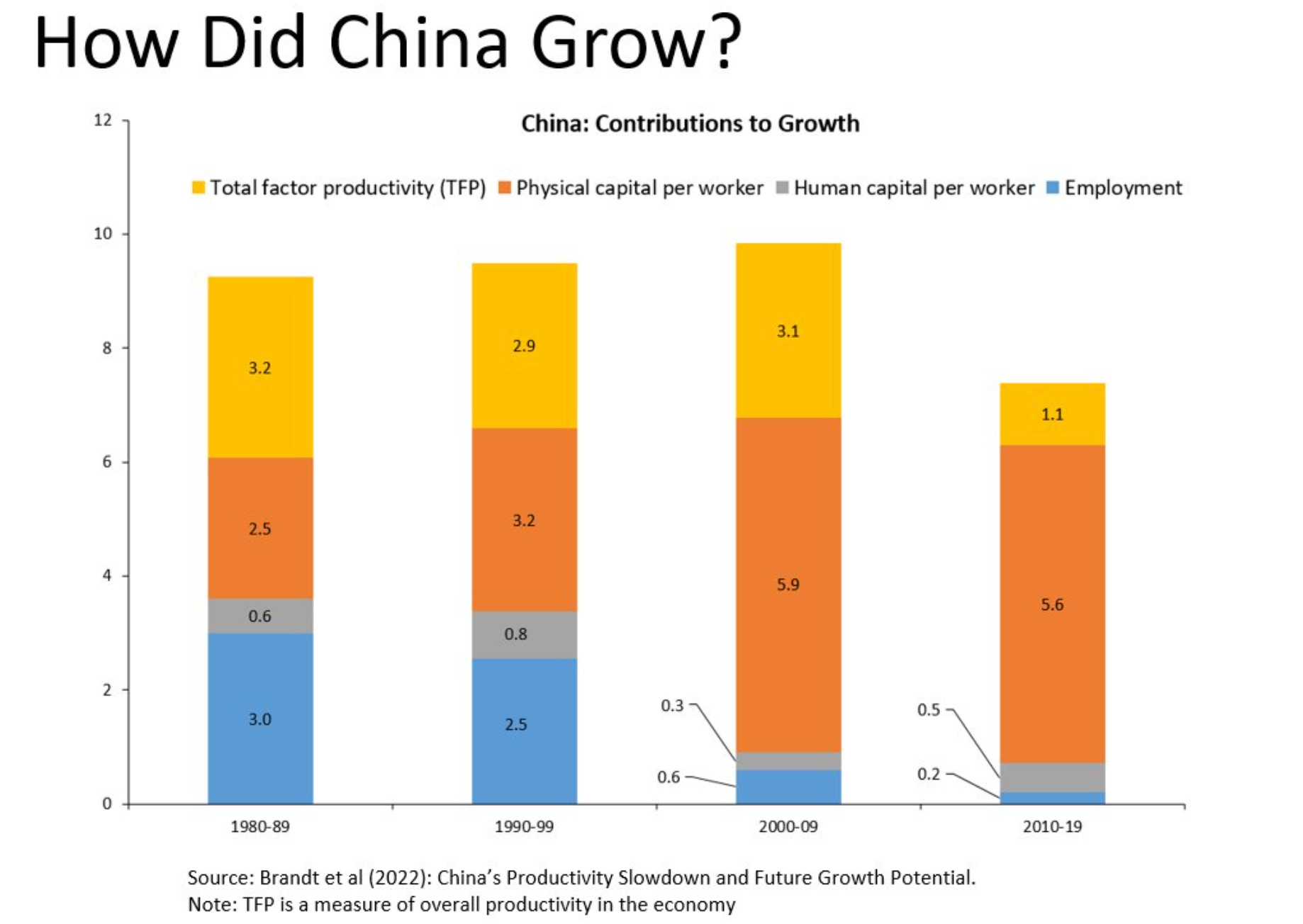

What is clear is that the pattern of growth in China has shifted in recent years and not in a good direction.

Clearly, the contribution of physical capital investment to growth has become dominant since 2000. But what it substitutes for is not productivity growth, but the decline in labour input from 2000, which comes earlier than I would have expected. When TFP growth slowed down after 2007, capital input also slowed and the result was simply a slow down in overall growth.

The upshot of this remarkable burst of growth is that the Chinese economy is large, but in gdp per capita terms it still lagged Brazil and lagged far behind Russia, ahead of the current crisis.

The good news is that this implies huge potential for catchup. As we all know, China faces demographic headwinds. But particularly with regard to the labour force there is vast unexplored potential both with regard to rural elementary and secondary education and tertiary education. As Hofman points out, China’s tertiary enrollment is soaring.

This is changing rapidly, though. By 2020, according to China's statistics, almost 60 percent of the age cohort is enrolled in tertiary education, up from less than 8 percent only 2 decades ago. China is almost following the steep trajectory that Korea followed in the 80s and 90s pic.twitter.com/FXC5TnEu9i

— Bert Hofman(郝福满) (@berthofmanecon) April 28, 2022

China is in a technological race and it knows it. The Economist recently had an excellent survey on China’s tech strategy and regional development.

As the Economist described it:

Mr Xi’s strategy is best understood as a weighty bet that China is on track to become the world’s centre of innovation over the next decade. A shift towards homegrown tech is altering the geographical layout of China’s manufacturing machine. New investment and migration are being rerouted from rich coastal hubs to inland cities such as Zhuzhou. A second feature is an unprecedented rise in the number of new tech companies. The government is nurturing thousands of groups, big and small, in the fields of data science, network security and robotics. Mr Xi and his advisers are also taking firmer control over markets. Their ability to direct capital flows is already evident in how private-equity groups invest in China.

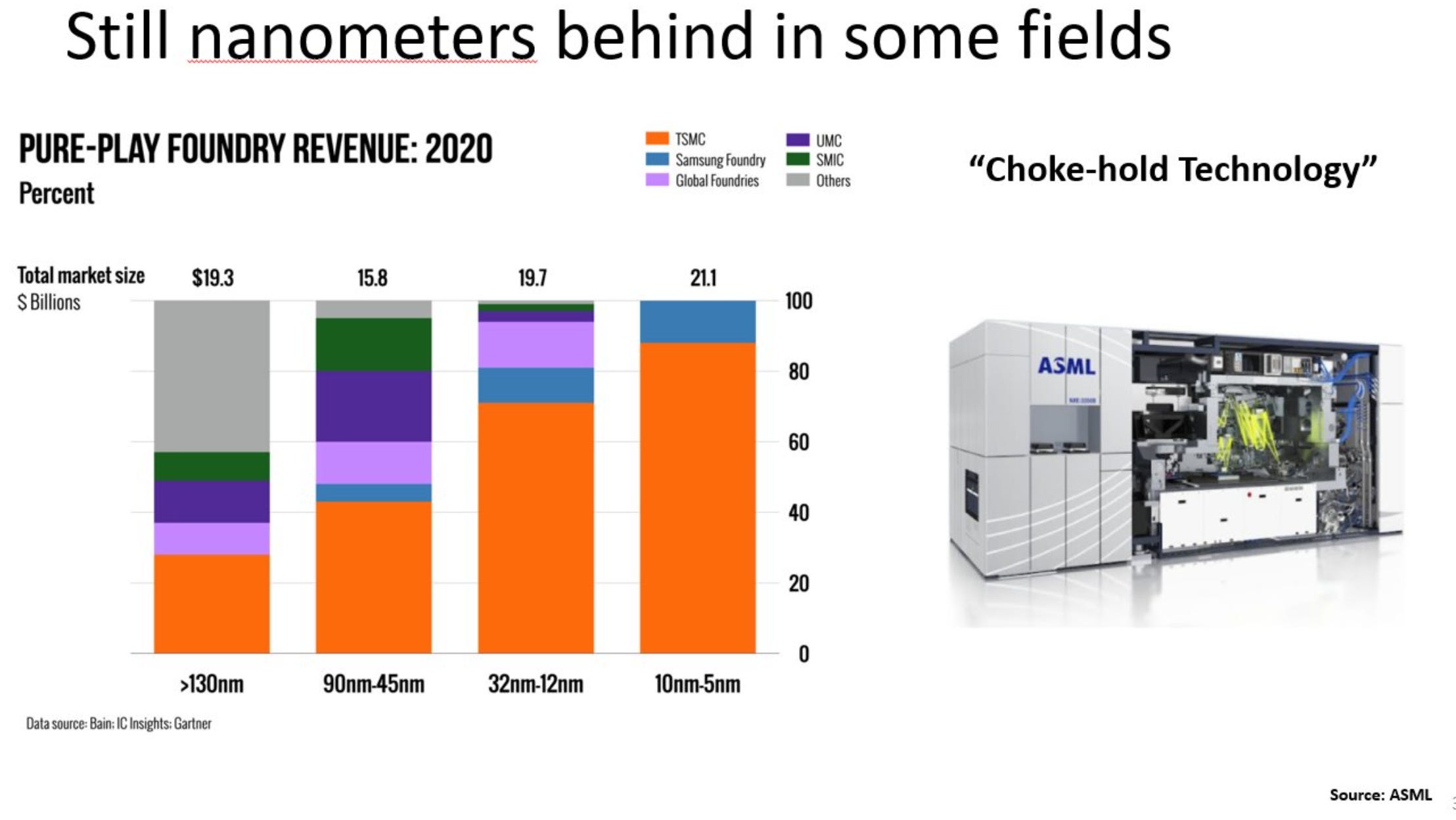

The crucial battlefield is clearly microchips and, as Hofman points out, citing data from ASML, China (like everyone else) still has a very, very long way to go to match TSMC and Samsung.