Adam Tooze's Blog, page 2

June 23, 2023

Ones & Tooze: The United States vs Europe

Europeans recall a time when their economy was substantially larger than America’s. But in the past 15 years, the United States has surged while Europe has declined. On the show this week, Adam and Cameron discuss why that is and what the implications are on both sides of the Atlantic.

Find more episodes and subscribe at Foreign Policy.

June 16, 2023

Chartbook 221 The IRA (& the Fed) debate – bringing hegemony back in.

What is the IRA? Is it a game-changing new industrial policy? Or is it the old wine of neoliberal de-risking in new bottles, in which the state stands ready to socialize the losses whilst capital privatizes the profits? The argument has gone back and forth in recent months. It is a debate about technical questions of policy. What tools of policy are these and what can we expect them to do? But it is about far more than that. The administration has made the IRA into centerpiece of what Jake Sullivan has dubbed the new “Washington consensus”, making it the opening of a new era in economic policy. The skeptics, by contrast, see mainly continuity with the past. Nor is this merely a scholastic debate. The argument is ultimately about what we can reasonably expect from reformism. The IRA matters because as far as climate policy is concerned, it is the best that the American democratic process is likely to deliver any time soon. So, if you are skeptical about the IRA you must face the question of what you actually expect policy to deliver over the next thirty years, the thirty years that are decisive for addressing the climate crisis.

***

For a snapshot of the ongoing debate, I recommend again this fascinating discussion.

In an extremely helpful new blogpost, JW Mason proposes a taxonomy within which to clarify and locate some of the contending positions in the debate.

Mason’s taxonomy focuses attention on two axes: how far is industrial policy driven by direct state engagement v. how far does it operate at arms-length through incentives? On the other hand, how far is green industrial policy broad-brush offering general financial incentives for green investment, as opposed to more fine-grained focus on key sectors and technologies?

Skeptics like Daniel Gabor, Mason suggests, can be seen as placing the focus on the form of policy action, prioritizing the question of direct versus indirect state action. Insofar as the IRA operates by way of tax incentives it remains within the existing, hands-off paradigm. A big green state would be far more directly involved. Those who see more promise in the IRA would not disagree with this judgment as to form but would insist that what makes the IRA different is that it engages in relatively fine-grained targeting of investment in key sectors.

It is tempting to see this as a distinction between economists who are more focused on issues of finance as opposed to those who are, at least in this case, more interested in the issue of prices, information and the mechanisms for resource allocation.

Mason’s taxonomy is very helpful, but because it remains at the level of the instruments and targets of policy it does not surface three other dimensions critical to understanding the stakes in the debate.

The three dimensions I have in mind are

The relationship of economic policy to the underlying balance of class forces. The mediation of those forces through the electoral system by actors within the political system, specifically in the US case, the two parties, which each consists of at least three inner-party factions (the left-wing, Dem loyalist, blue dog, v. GOP “centrist” open to bipartisan deals, GOP loyalist, freedom caucus).The agenda, expertise & de facto autonomy of state institutions, and their associated fields of expertise and societal interests, most notably those clustered around the Fed & the Pentagon and within the energy system.Take all three dimensions together and you might say you have the question of hegemony. I take this question to concern both the domestic and global position of America’s liberal elite. And I take it not as an accomplished fact, but on the contrary as an open question and thus an absolutely overriding preoccupation of the Biden administration.

***

These three dimensions of thinking about economic policy in the current moment first surfaced for me in my exchange with Daniela Gabor and Josh Mason over Fed policy, which is now a few months back. Daniela and I went back and forth over the question of whether the Fed’s abrupt and, for many, unexpected hike in interest rates, constituted a significant break in the policy regime. I see the end of the so-called “Fed put”, under which the Fed tacitly underwrote equity valuations, as highly significant both in itself and because it signifies how loosely knit any policy regime is. Faced with the shock of the polycrisis I see the Fed displaying a higher degree of autonomy than many credited it with, both in delaying the hike and then in delivering a shock more than any we have seen since the days of Paul Volcker. Gabor, by contrast, offered a sophisticated defense of the continuity between the current policy regime and the basic logic of a market-driven model of financialization.

Some of these same questions were also in play in Josh Mason’s excellent reply to Dylan Riley’s roundhouse critique of Biden’s industrial policy in Sidecar.

If the current administration is, as Riley pointed out, not in the business of seizing the commanding heights of American capitalism, that leaves the question open of what the policy is actually about. To answer this question it seems to me that we need to go beyond Mason’s illuminating two by two typology, to address the underlying societal power balance, the logic of politics, and the agenda and autonomy of the state and its institutions.

To map either of these questions, to properly characterize either the Fed’s unexpectedly severe pivot, or the IRA we need to bring into focus not just the choice of instruments but the question of the underlying societal power balance, the logic of politics, and the agenda and autonomy of the state.

Before I say anything else I should add that I am fully aware that on all three of my added dimensions – class balance politics and state institutions – in raising the question of hegemony as I am, I am wading into very deep water and doing so quickly. So please take these points as suggestive rather than definitive. I am trying to widen the conversation not to end it.

***

To go back to Mason’s grid, the most dismissive reading of the IRA hinges not just on the fact that it relies on indirect incentives, but that this technical choice reflects the power of class forces which in turn help to condition the limits of “realistic” political strategy. Acting indirectly by offering a generous program of subsidies – “bottomless mimosa” (Tim Sahay) – makes minimal demands on the state and enabled a majority to be built in Congress. Whilst delivering a significant change in energy policy, it effectively underwrites the status quo of the political economy. Nor should we expect anything else because there is really no reason to think that there has been any underlying shift in the class balance in American society, any time recently, and certainly not since January 2021 with the inauguration of the Biden-Harris administration.

Of course, the Biden administration takes climate seriously and they promise to deliver a (foreign) policy for the American middle class. But note that this is not a policy “by” or “of” the middle class but “for” them. It is a top-down agenda driven by the interest of the Democratic Party leadership in assembling majorities. Avoiding a repetition of Clinton’s embarrassment at the hands of Trump in 2016 is the name of the game. For the Biden team, this is essential if American democracy as they cherish it, is to be saved.

The critics of the IRA contrast it to something far more ambitious, often described as “the big green state”. What this would entail is far more than an adventurous choice of policy instruments. For a “big green state” to be conceivable, we have to imagine not just different instruments of policy and a greater degree of state involvement, we have to imagine a shift in the balance of class power, or at the very least a shift in the basic intentionality of majority-formation. We have to imagine something like a Bernie Sanders-led Democratic party or a Corbynite Labour party that would assemble majorities with a view to restructuring the state and building institutions capable of counter-balancing or even shifting the underlying balance of class power. Beyond the instruments chosen and their targets, it is the fact that the IRA lacks this transformative ambition that leads the skeptics to see it broadly speaking as continuous with the previous regime of neoliberal de-risking rather than marking a profound break. In the absence of even prima facie evidence of a shift in the class balance or any radical break in the operation of politics or the state machinery, why would you expect anything else? The fact of a Democratic administration, after Obama and Clinton, predisposes them even more to this view.

***

The Big Green State is a hypothetical standard against which the IRA clearly falls far short. But does imply that the IRA is nothing more than a continuation of the old regime of neoliberal de-risking by other means? I would argue not.

First, we have to take seriously the political crisis – the threatened impasse of the two main American political parties and the Trumpist threat – that shaped the passage of the IRA and the urgency with which it has been appropriated and discursively enlarged by the Biden team so that it now stands for a new Washington consensus. One can be skeptical about the macroeconomic scale of the IRA or the conservatism of its policy instruments, whilst recognizing the significance and reality of the political crisis to which the Biden team is trying to address itself. After Trump, they are filled with a real sense that they cannot simply go on as before. Neoliberalism has hit a limit point. They do not buy the self-imposed discursive limits that defined the Obama administration and were personified by figures like Larry Summers. This is a significant break.

Second, the Biden folks are serious about climate. On this front as well they do not believe that things can go on as before. So, as Mason and others argue, it matters very much how the carrots are directed and what kind of investment is unleashed. Furthermore, though the use of tax benefits may be indirect, there is real expertise being built in the Department of Energy. Not a big green state perhaps, but in the hands of figures like Jigar Shah, director of the loan office at the Department of Energy, a little green state is taking shape.

Furthermore, if the Biden administration falls far short in its ambition of the Great Society, let alone the New Deal and if the benefits so far delivered for American organized labour have been modest, there is nevertheless a distinctive new vision of trying to build a new coalition of green capital, progressive environmentalism and organized labour. The aim of the game falls far short of the ambition of the Green New Deal, but this is real socio-political-economic engineering. The aim of the game is to build sufficiently powerful interest group coalitions to make important parts of the agenda proof against repeal. This was already in play in the passage of the IRA, which would probably not have happened if it had not been for the mobilization of the green energy lobby and unions. In short the box in Mason’s diagram which highlights fine-grained capital investment has empowered people, organizations and businesses building expertise and interest in it.

Finally, if it is abstract and ahistorical to ignore this wider agenda behind the IRA that makes it more than merely the continuation of derisking in another guise, it is abstract and ahistorical also to ignore the remarkable fusion within the Biden administration between economic policy and the national security state. As Grey Anderson points out in a brilliant contribution in Sidecar, it is a sign of the times that the programmatic statement on economic policy of the Biden administration should be made by the National Security Advisor. Meanwhile, the Treasury Secretary gives speeches on economic relations with China, framed by the question of whether the two countries can avoid war. And the connection runs all the way down the hierarchy. Last week Jigar Shah, of the Department of Energy, tweeted out an image of Rosie the Riveter framed by wind turbines, with an appeal for Americans of today to emulate the greatest generation, who in a matter of a few short years turned American from a military non-valeur into the greatest superpower the world has ever seen.

He endorses a call for America to declare war on climate change.

Of course, the talk in Washington in the first half of 2023 has been all about war, but what has been top of the agenda is war with China, not climate policy.

Beyond neoliberalism, in conditions in which the grip of financial capital on power is loosened, when the state elite faces a challenge like the rise of China, we should expect policy innovation. But we should not expect economic policy to harken only to progressive impulses. To bolster their political coalition, to conduct an innovative new policy on a wafer-thin majority, to pursue their deeply held commitment to American leadership, the Biden economic technocrats turn to national security, to the Pentagon and the think tanks of the Beltway as natural partners.

There is a big green state in the United States, the biggest the world has ever seen, with an annual budget rising towards $ 1 trillion, but it wears fatigues and its preferred shades of green are camouflage and khaki.

***

In a much less politically dramatic but more economically consequential key, I would see the Fed’s pivot in similar terms, as a display of autonomy by a state institution in the face of a threat to one of its core agenda items i.e. price stability. It has done so at the price of inflicting huge losses on bonds and other financial assets. And the stability lending it has put in place to prop up the banks, is no more than a series of stabilization measures to enable it to force through its agenda of price stabilization whilst avoiding a major financial crisis. As Gabor has argued, at some rather abstract level this may still conform to a basic vision of market-based and price-driven finance. But it is a long way removed from the go-go partnership between the Fed and the markets, first initiated by Alan Greenspan. In terms of the internal class politics that mesh the investing class and upper-middle-class owners of 401ks with the Fed, it has come as a considerable shock.

In a very different world, central banks would be pursuing a green agenda of disciplining private capital and driving the energy transition both by penalizing dirty lending and encouraging capital to flow into the green energy investment. This is what some of us once imagined might be possible as the monetary backstop to a green new deal. That hope has been disappointed. Instead, the IRA, as its title suggests, was introduced in combination with a program of tax hikes that were intended, at least notionally, to reduce the Federal deficit. The fact that the fiscal conservatism of the IRA has attracted so little attention, compared to the structure of its financial subsidies, is indicative of a broader disconnect in the discussion between the IRA and macroeconomics.

As I have noted in a previous Chartbook, whatever the political economy of the IRA, the most significant thing about it from the point of view of the energy transition is not that it is shaped in the form of tax benefits and does not realize the Big Green State, but that it is simply not big enough. It is not just conservative in its form. It is also conservative in its dimensions.

That is explicable only in terms of the dimensions of politics and class power that I am highlighting in this post. Biden wanted to do a much larger version of Build Back Better. The Sanders camp wanted a program that was an order of magnitude larger. It was not possible given the resistance put up by lobbies and by Joe Manchin’s veto. It was possible to pass the bill even in its current modest dimensions only because it was twinned with “pay-fors”.

This question of the IRA’s quantitative dimension though crude, is important to its wider interpretation in two key respects.

On the one hand, it further emphasizes the crucial significance, stressed by Mason and others, of targeting. The IRA’s measures have to be targeted because they were so tightly hedged around by political and financial constraints. This is not some scattershot liquidity measure in which hundreds of billions can be tipped into a repo market in a matter of weeks. It is a carefully calculated gamble on the likely take-up of EV when middle-class Americans are offered an inducement of $7500 on the right models. It is likely the first piece of legislation that has ever been benchmarked in this way.

Secondly, the fact that the Biden team are willing to hang their hats to this degree on a measure that is so modest in its size is indicative of the underlying political impasse that in turn marks the historical specificity of the IRA. As no one knows better than Daniela Gabor, the IRA is not how financialized neoliberalism looks when it is operating in its element. When the Fed is in its pomp, it does genuine revolutions, on the scale of trillions and it does them completely silently. Fashioning the three mangled pieces of legislation that emerged from the last session of Congress – the bipartisan infrastructure bill, the CHIPS Act and the IRA – into the basis for a new Washington consensus, is, by comparison, a truly audacious act of political marketing. We should not forget the mood of desperation that filled the halls of Congress twelve months ago, when it seemed as though the efforts to corral the Democratic majority would fail, America would miss its opportunity to pass significant climate legislation for the third time and the Democrats were headed for certain defeat in the mid-terms. If the IRA is a continuation of anything it is a continuation of the act of defying gravity which Tim Geithner described as the basic condition of American liberal elites since the 1990s. But since then, on all three fronts – climate, China and the struggle over the future of America’s political system – the stakes have only gone up.

There are, as Gabor rightly reminds us underlying structures of neoliberal capitalism, which shape the form of policy. There are also, as Mason’s taxonomy usefully highlights, the strategic intentions of the planners in the Biden administration. There may even be something like a little green state emerging. But, ultimately, what we see expressed in the Biden administration’s new industrial policy is America’s liberal elite struggling to craft a policy and a narrative that goes with it, to justify their claim both to domestic and global hegemony.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week

June 15, 2023

Ones & Tooze: Ukraine’s Daunting Economic Rebuild

On today’s episode, Adam and Cam look at the devastating impact Russia’s war on Ukraine has had on Ukraine’s infrastructure – in particular the destruction of the Kakhovka dam. In the second segment, the two reflect back on the life of former Italian Prime Minister Silvio Berlusconi and try to parse out how much his personal scandals impacted the national economy.

Find more episodes and subscribe at Foreign Policy.

June 13, 2023

Chartbook 220 Biden’s “new industrial policy”: Revolution in the making, or an exercise in defying gravity?

Now you see it. Now you don’t. Thinking about the Biden administration’s new industrial policy I am trying to square two realities in my head.

On the one hand the infrastructure, CHIPs and Inflation Reduction Acts seem to be translating into a real investment and construction boom.

All told, according to Bloomberg’s reckoning:

Laws Congress approved last year (2022) together offer about $420 billion in funding to incentivize the domestic production of chips and clean-energy technologies. Add the infrastructure bill Biden signed in 2021, which requires that all iron, steel and other construction materials used in public-works projects be made in the US, and you’ve got about $2 trillion in federal spending over 10 years.

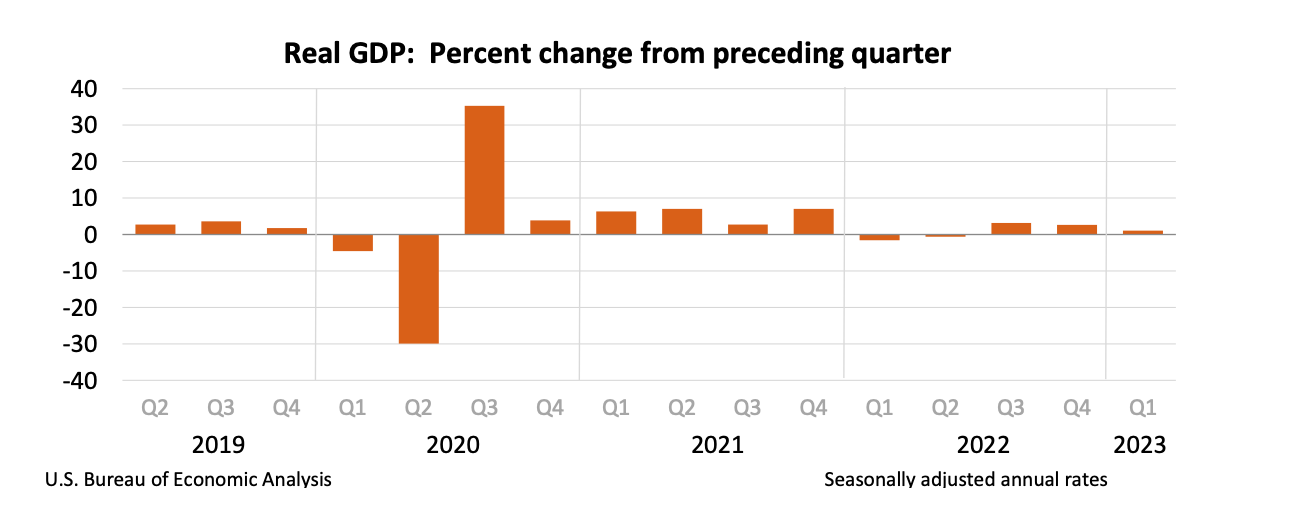

On the other hand, the lack luster figures out of America’s Bureau of Economic Analysis show overall growth slowing fast. Falling investment is retarding America’s growth, not accelerating it. Nor should that be a surprise. It is one of the intended effects of jacking up interest rates to fight inflation.

Source: BEA

Enthusiasts for the IRA cite estimates from Goldman Sachs suggesting that the eventual total of spending unleashed by that piece of legislation alone may run to as much as 3 trillion dollars or more. This conjures up images of an

American

economy and American society transformed, with the IRA delivering the green equivalent of the shale revolution.

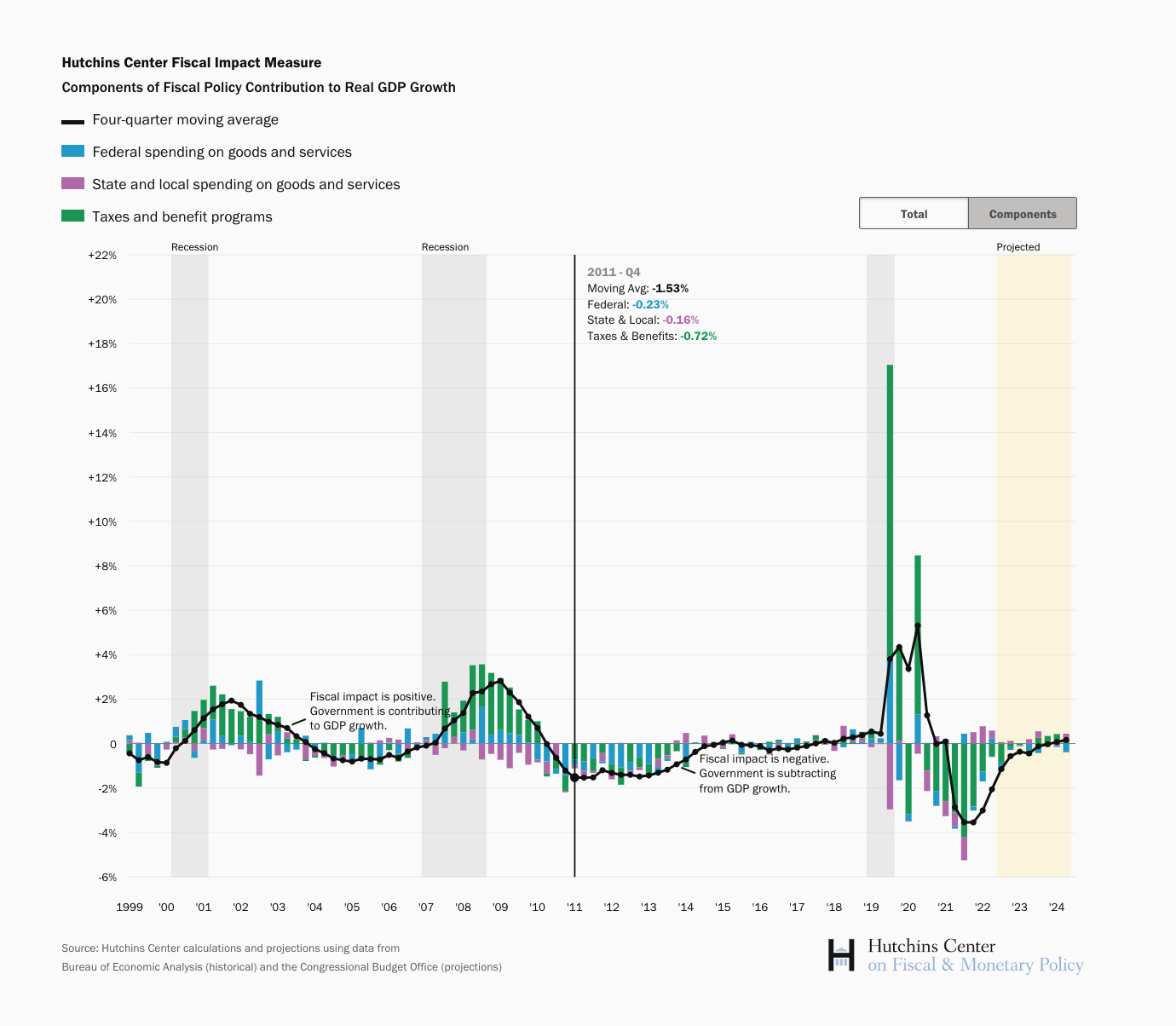

On the other hand we have the estimates from Eli Asdourian, Nasiha Salwati, Louise Sheiner, and Lorae Stojanovic at the Hutchins Center at the Brookings institution which show that since the drama of 2020 and 2021, fiscal policy has moved towards a neutral setting.

In 2020 and Q1 2021 the stimulus packages voted by Congress delivered a huge and economically appropriate stimulus. Then, already in Q2 2021, many months ahead of the Fed’s monetary tightening, the fiscal impact turned negative. By Q2 2022, as the IRA finally passed through Congress and the inflation scare built to its height, fiscal policy was exercising a drag on the US economy to the tune of 4.8 percent. This was counter-cyclically appropriate. And, since then, the pressure has eased. But compared to the COVID-era stimulus programs of 2020 and 2021, the IRA barely seems to register.

This is consistent with macroeconomic modeling of the IRA, which consistently show its effect to be tiny. What then are we to make of this cognitive dissonance? A bright new dawn of industrial policy on the one hand, macroeconomic normality on the other?

This question might be seen as a quantitative extension of the skeptical questions asked by observers like Daniela Gabor about the political economy of the Biden administration’s new industrial policy.

Whilst Daniela Gabor is asking is whether the IRA opens the door to a new political economy, or whether it is merely the old wine of financialized de-risking in new bottles, what I’m trying to figure out is how big the intervention actually is. Even allowing for the possibility that the political economy is new, does the Biden administration’s “new industrial policy” really have the heft to make a transformative difference?

***

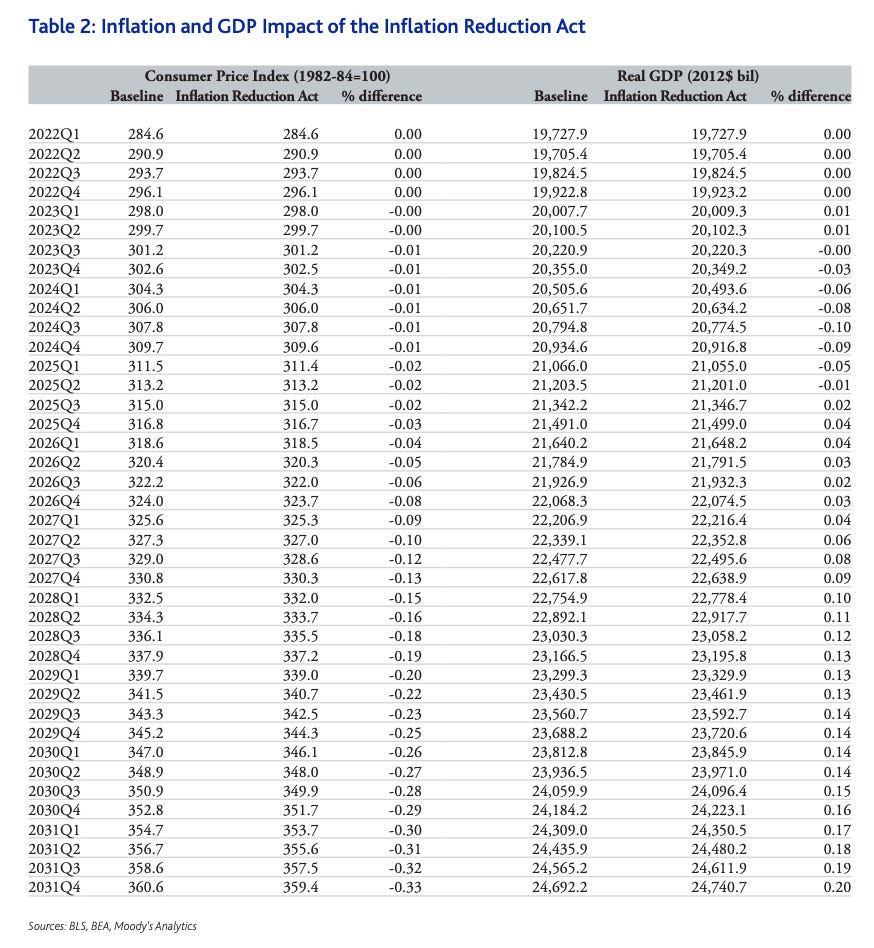

The first macroeconomic evaluation of the IRA I’ve been able to find, that by Mark Zandi’s team at Moody’s Analytics from August 2022, arrived at very modest totals for both the GDP and inflation impact.

The total impact on growth and inflation never amounts to more than a fraction of one percent.

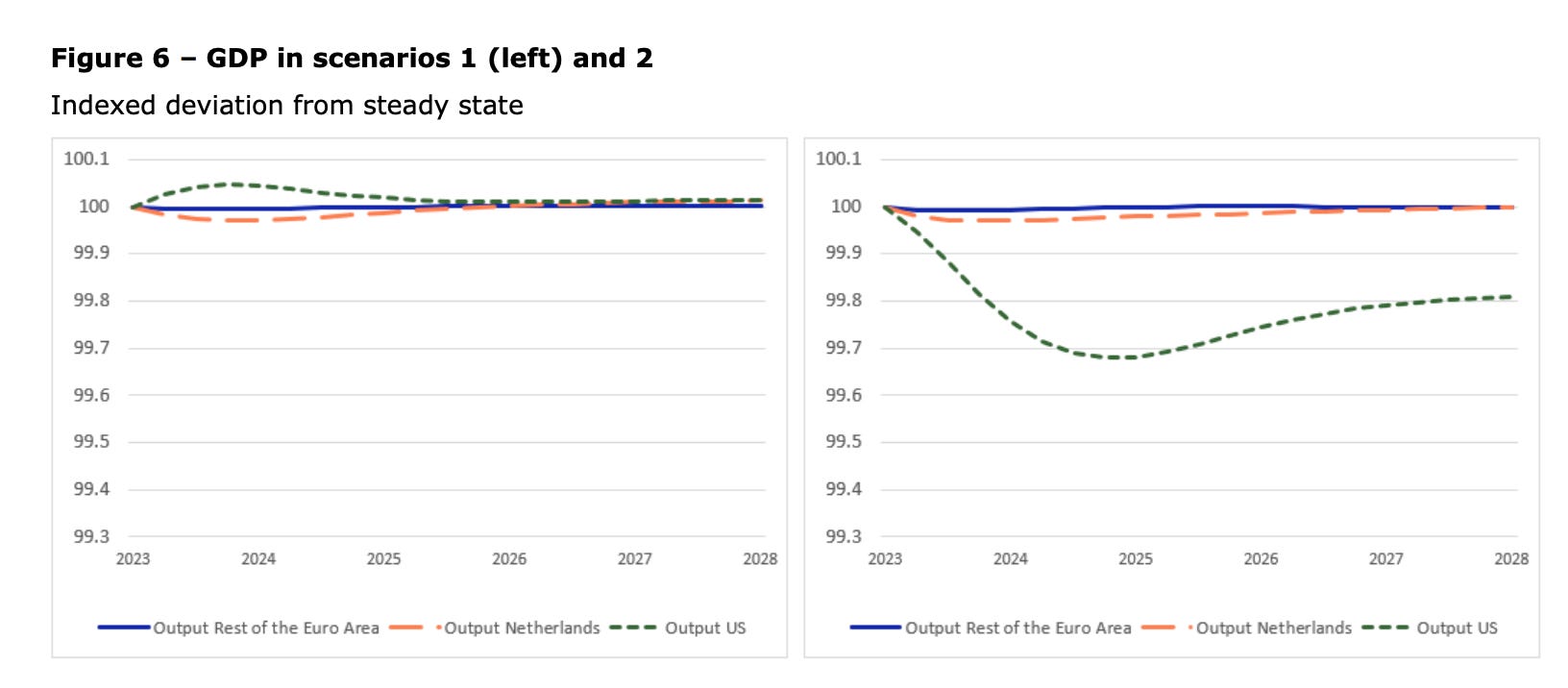

These data were calculated back in August 2022. If you know of more recent evaluations please let me know. When economists at the Dutch National Bank attempted their own macroeconomic analysis of the IRA, published in May of this year, they found nothing to reference other than the Moody’s exercise. The DNB’s results confirm Zandi et al’s conclusions. Using conventional models, the macro impact of the IRA looks negligible.

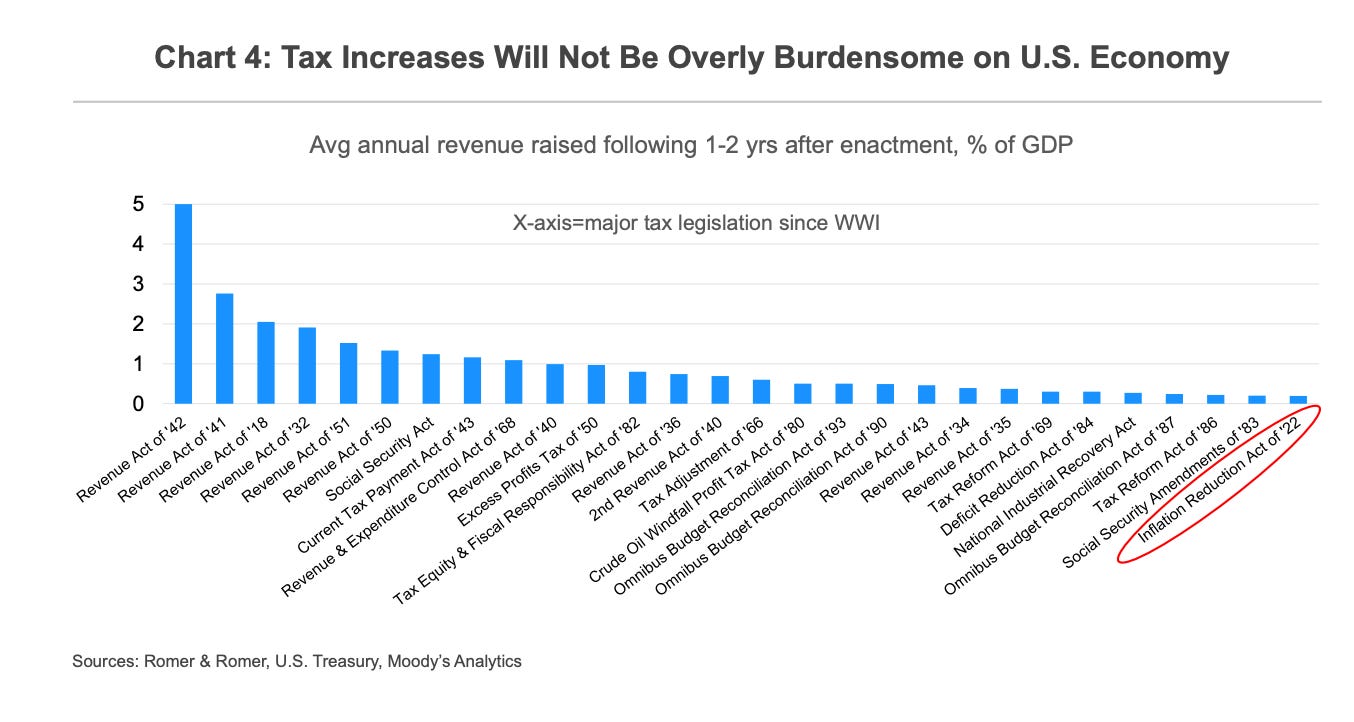

The DNB’s Scenario 2 involves an increase in corporate taxation to pay for the IRA tax breaks. But as Moody’s points out, in historic terms the IRA ranks low amongst tax measures reeform measures.

I have yet to see a macroeconomic evaluation of the entire $ 2 trillion “new industrial policy” trifecta. That is clearly substantially larger than the IRA alone, but, divided over a decade, it amounts to an annual injection of less than one percent of GDP, not allowing for financing costs.

***

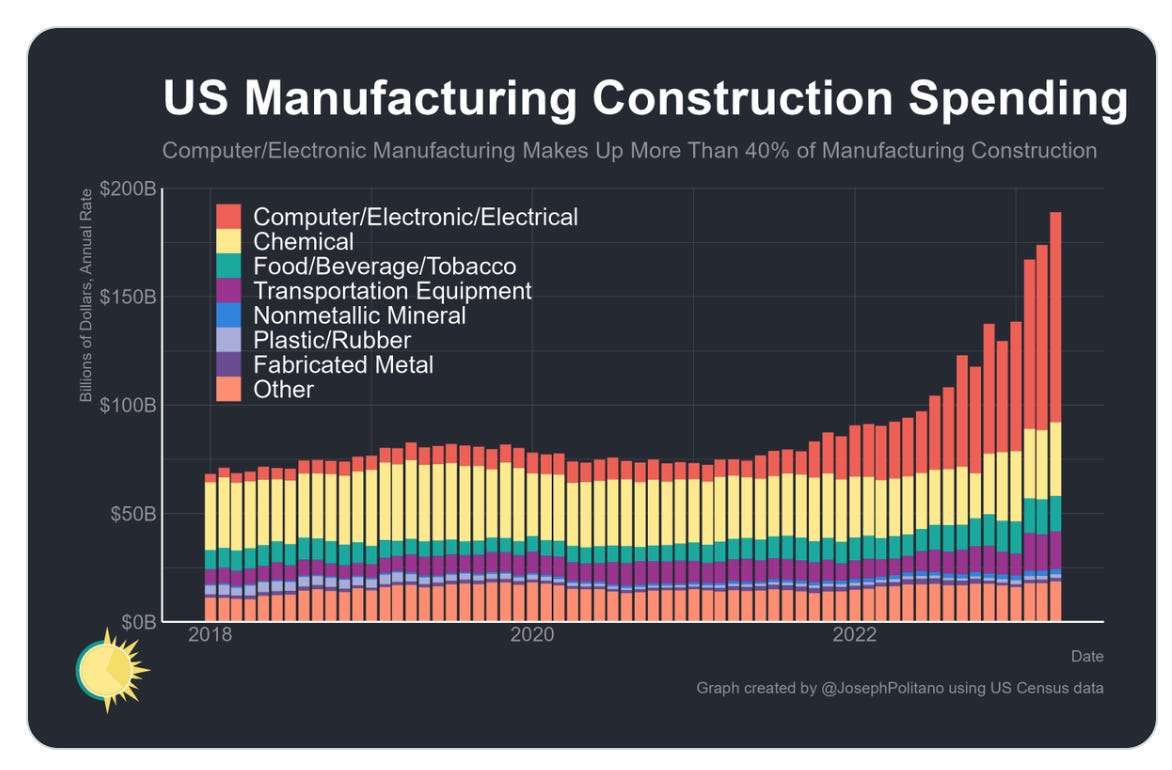

In any case, enthusiasts for the new industrial policy will likely argue that such macroeconomic evaluations miss the point. The aim of the IRA and other legislation passed since 2021 is not to deliver a giant green stimulus but to act as a targeted incentive to investment in the energy transition and the new Cold War tech-race with China. And on those fronts, it seems, the IRA, Chips and the infrastructure bills are delivering. On twitter a dramatic graph of US manufacturing construction has beeen making the rounds.

Source: Joey Politano

This is, no doubt, a dramatic picture. There has been a huge surge in construction in the exorbitantly capital-heavy microchip sector. This has ben supported by a smaller step-up in investment in transportation equipment, presumably in the battery and EV segment.

These numbers are consistent with project-level data compiled by Amanda Chu at the FT. As of April 2023 this came to $139 billion in announced projects for semiconductors and $65 billion for clean energy.

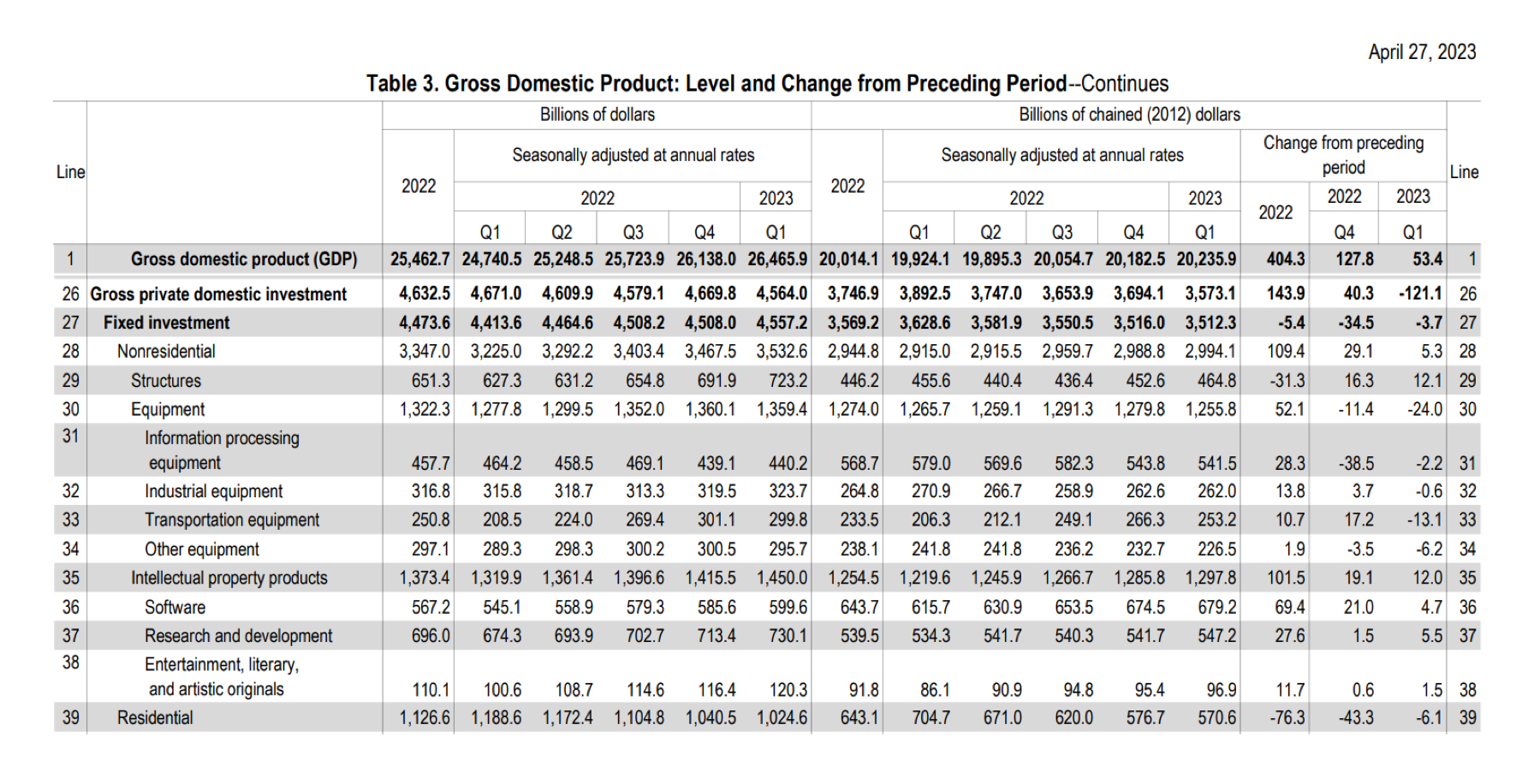

But how does this intensified investment in the heavily subsidized sectors relate to broader investment spending in the US economy at large? If one looks into the national accounts, as laid out by the Bureau of Economic Analysis, it is easy to see how an exciting story about factory construction in two key sectors can be reconciled with with a lack luster story about investment in the economy at large.

The construction surge in manufacturing which is causing so much excitement, amounts to an increase of $100-120 billion per annum, raising the current annualized rate to $200 billion. Investment in structures as a whole across the entire US economy is more than three times that. According to the BEA, investment in structures increased between 2022 and the first quarter of 2023 (on an annualized basis) from $651 billion to $723 billion. Gross private investment as a whole runs to over $4.5 trillion and is trending down, not up.

So the upshot is that we have a particular sectoral boom nested within a much less exciting aggregate picture.

The story turns completely around if we move from nominal figures to investment measured in constant dollars. In inflation-adjusted terms, total investment in structures is up only 5 percent. Equipment investment is down. And Gross Private Domestic Investment in the first quarter of 2023 is down by 5 percent in real terms.

The aggregate numbers also put in context the larger claims made for the longer-term impact of the IRA. Let us assume that the Goldman Sachs prediction comes true and the IRA does generate $ 3 trillion in investment over ten years. That is a lot of money. But in 2021 the US already invested over $80 billion in its electricity grid. $ 300 billion in transportation equipment. Hundreds of billions went into fossil fuels. The lesson is simple, in an economy the size of the American one, $300 billion per annum in investment, which in part replaces existing spending on the fossil fuel economy, is an incremental rather than a revolutionary change.

***

Of course, you could say that all broad-based economic industrial transformations start this way. It is famously true that investment in IT and digitization took years to show up in broad-based productivity increases. Likewise, the industrial revolution of the 18th and 19th centuries worked its way slowly across the economy. The green industrial revolution has already begun in electricity generation and in the accelerating transition in motor vehicles. It will spread pervasively across the entire economy. If measures like the IRA help to accelerate these trends that will be their ultimate historical vindication. It seems likely that 2022 will come to be seen as an important turning point in the history of the American energy transition. But whilst acknowledging this, it is important to be realistic about the quantitative scale of what is going on and above all to be realistic about its likely short-run impact on American society and thus on its politics. This is worth saying because the Biden administration sees its new industrial policy as three-pronged. It is designed to address the climate crisis, the challenge of Chinese competition and the inequality and divisions within society that have undermined American democracy. It may be good politics to talk up this ambition. They would no doubt have done more, if Congressional majorities had enabled them to do so. At the very least the Biden team can claim that they see the problems and have attempted creatively to respond to them. In terms of political messaging that may be enough. Let us hope so. For my part I’m reminded of that phrase that Obama’s Treasury Secretary Tim Geithner used to me in describing the challenge facing America’s liberal governing class. Theirs, he remarked, is an exercise in defying gravity.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week

June 9, 2023

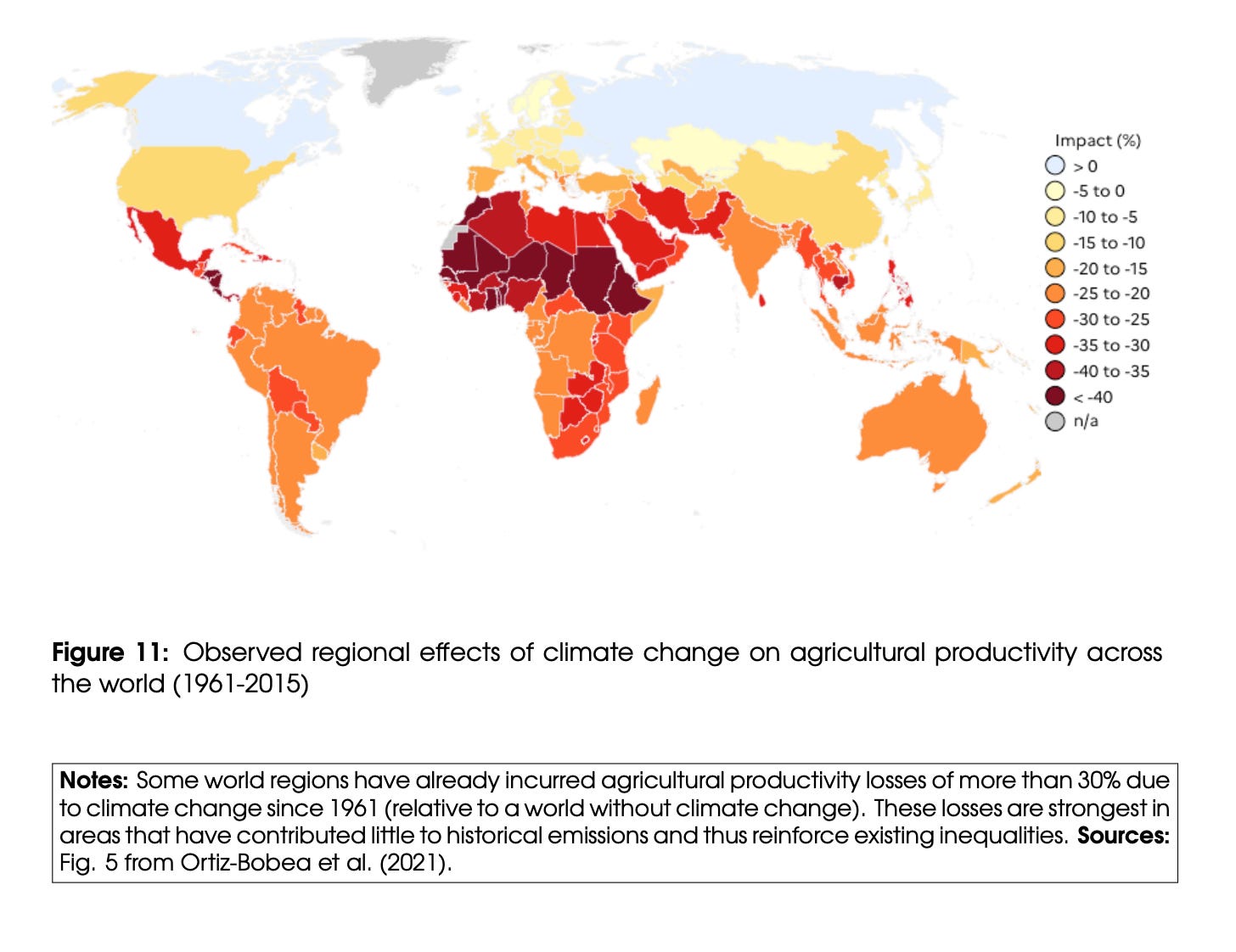

Chartbook 219 The triple inequality of the “global” climate problem.

The climate crisis is often discussed as a global problem which requires a collective mobilization of humanity. This can be inspiring. Against the backdrop of the fraught geopolitics of today, it can even be comforting to imagine that there are at least some problems that “we” have in common. As is brought out by the Climate Inequality Report 2023, authored by the team of Lucas Chancel, Philipp Bothe, and Tancrède Voituriez, this “global” vision of the problem is profoundly misleading.

The reality of the “global climate problem” is, in fact, defined by a triple inequality. The impact is suffered most by those who have least contributed to the crisis and are least able to pay. Those of us who are most responsible and have most ability to contribute to the solution, currently suffer and are threatened in the future with relatively less impact.

The juxtaposition of the three dimensions of the climate problem is stark and should orientate all future debate.

***

The driver of the climate change is not humanity in general, but those who have benefited from substantial economic development, around the world and across national borders. Globally, 89 percent of emissions are due to the 4 billion people in the top half of the global income distribution. 48 percent are due to the 800 million people in the top ten percent of the income distribution. 17 percent of all emissions are generated by the top one percent alone – 80 million people. Within the top one percent, there are further upward gradations.

Source: Climate Inequality Report 2023

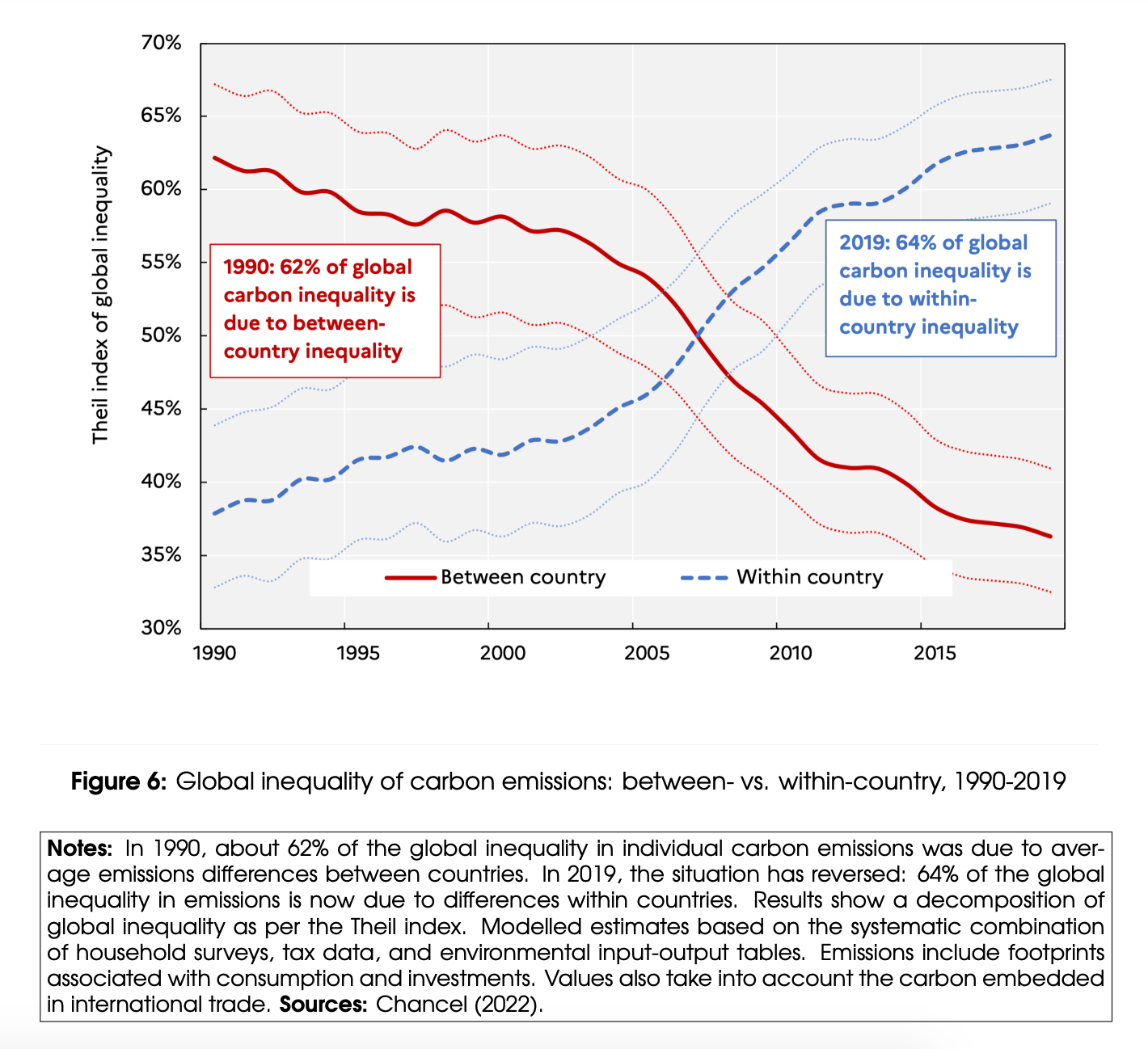

Since the 1990s, the distribution of CO2 emissions has tracked global inequality trends, as charted, for instance, by Branko Milanović. In 1990 the problem of climate justice was, in large part, one of between-country inequality. 62 percent of carbon inequality was down to the gap between rich country and poor country emissions. This reflected the polarization of the world economy at the time.

Today, almost two thirds of the inequality of emissions is down to income differences within countries. In terms of per-capita emissions, the new Asian upper class and middle-class have caught up with, or even over taken their Western peers. East Asia’s top ten percent of income earners now have higher per capita annual emissions than their European counterparts.

The “good news” is that given this pattern of inequality the carbon budget is no real constraint on global action on extreme poverty. A comprehensive program to raise the entire global population above the $3.2 per day poverty threshold would add only 5 percent to total global emissions. That is one third of the annual emissions of the top 1 percent.

The urgency of doing so is that we are running out of carbon budget at an alarming rate. In 2020 the remaining carbon budget for a reasonable chance of stabilization at 1.5 degrees centigrade was 300 billion tons. We are currently eating into that at the rate of 37 billion tons per annum. De facto that puts us on course, best case, for some kind of stabilization in the 2-3 degree range by 2050.

***

Every fraction of degree is worth fighting for, in light of the impacts that are already being felt around the world.

The climate modeling shows that though very negative effects of climate change will be evident everywhere, the most intense impacts will be in regions in which there is a preponderance of poverty, underdevelopment and state failure and which are least responsible for the climate crisis.

There, is a perverse negative correlation between the level of emissions and the likely impact of climate change on extreme temperature variation. If I read this chart right, some of the most significant polluters may actually see climate stabilization in coming decades.

As was demonstrated in the last twelve months in Pakistan and Mozambique, the population exposed to poverty and the risk of dramatic flooding due to extreme weather is concentrated in Asia and sub-Saharan Africa.

The impact of climate change is already being felt by farmers across the Southern hemisphere and in particular in Latin America, Asia and Africa.

By 2100 large parts of Africa, the Middle East and poorer parts of the Sub-continent are likely to see a surge in climate-related mortality.

Overall, the impact of the increasingly extreme climate conditions will be to polarize economic development between a large group of developing countries whose economic prospects turn decidedly bleak from 2050 and a smaller cluster of rich countries whose growth may actually be enhanced according to some modeling.

Whether or not climate impacts will really remain so contained is, surely, an open question. The modeling that Chancel et al build on, would seem to include no dramatic tipping points, large-scale migration flows etc. They do point to at least one spillover effect – infectious disease. In a climate-changed world, infectious diseases like dengue fever may not remain confined to the tropics. By 2050 more than half the world’s population may be at risk.

***

When it comes to remedies to address the crisis, Chancel et al are forthright. The resources are all stacked on the side of those least badly affected by the crisis and most responsible for it. The flow of funding from the rich countries to the developing world are notoriously inadequate. Capital markets prefer rich countries and extract a painful spread from lower income borrowers. This interesting chart shows the stark disparity in taxing capacity between Europe and African states.

What is the solution? Chancel et al come from the “Piketty school” of inequalities studies, which has long favored a global wealth tax. They propose a modest 1.5 to 3 percent tax on global wealth starting at $100 million. According to their calculations this would yield $295 billion per annum.

This is obviously an extremely attractive and equitable idea, but it presumably has no chance of realization in practice. Too much “political capital” and institutional architecture for a relatively modest flow of income. If the aim of the game is urgently to raise $300 billion per annum for adaptation investment and sustainable development, there are other more viable routes for doing so. In global debt markets this is a modest sum. Of course, this defers the question of social justice within the rich states – someone ultimately has to service debts contracted etc etc – but the priority has to be mounting an urgent response to the crisis threatening the developing world. They see the path to development and the route of poverty closing before their eyes.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week

June 8, 2023

Ones & Tooze: The Economics of High Art

An exhibition in Amsterdam of the Dutch painter Johannes Vermeer’s works has been sold out for months. But what’s in it for the museum hosting the collection? Adam and Cameron discuss the economics of high art and blockbuster art shows.

Also on the podcast: The economics of professional basketball.

Find more episodes and subscribe at Foreign Policy.

June 2, 2023

Chartbook 218: “So far from god” … friend-shoring and the debate in Washington over whether to bomb Mexico.

As tension over Taiwan mounts and military alliances form around South China Sea we face the remarkable situation that the world’s principal artery of trade and investment is threatened by talk of war. You might think that economic stakes to the tune of trillions of dollars would rule out the possibility of a clash. But both the Chinese and the US currently envision fighting not just over the sovereignty of Taiwan but also over far more trivial territorial disputes.

At the same time, Europe is engaged in an economic struggle with Russia, a development which many also judged would be impossible given the stakes involved. Admittedly, some dismiss the sanctions as so ineffective that they amount to a phony war. Be that as it may, the antagonism is real.

Unsurprisingly, this surge in geopolitical tension raises talk of near-shoring and friend-shoring. But that begs the question, where is safe?

As far as the United States is concerned one immediately thinks of the North American region – what was once NAFTA and since 2020 has been rebadged as USMCA. Taken together, the USMCA is far and away the most important hub of US trade. It is indispensable for manufacturing systems, including first and foremost the North American motor vehicle complex.

Here, surely, lies the core of a pacified economic zone. This has launched a debate about Mexico’s evolving role in global supply chains and its ability to take advantage of the opportunities opened up by decoupling from China.

Clearly, the USMCA is a case of near-shoring. But what about the politics? As far as Canada is concerned, the label of friend-shoring will do. But look to the South and your answer depends on how you judge the fraught relations between the US and Mexico. On top of chronic tensions over migration, in Washington right now there is a live debate about whether the next President should order the bombing of Mexico. Surreal as it may seem, a vocal part of the US political elite is contemplating the use of military force not just with regard to China, but with regard to the other main artery of US economic globalization as well. Freakish as this may seem, given the prominence of the figures involved, and the structures of underlying conflict, it would be dangerous to dismiss this as political theatre.

***

Listeners of Ones and Tooze have been calling for some time for us to do an episode of Mexico. Cam and I took on the challenge this week.

It is at best a first bite at this huge topic. There is so much more to cover on the broader development of the Mexican economy, a fuller assessment of NAFTA/USMCA etc. We will revisit it certainly before the elections in 2024.

***

The most important take away for me in putting together the episode is, that if Mexican-American relations demonstrate anything it is that the naivety of eliding near-shoring and friend-shoring. Proximity brings safety and harmony only if you have sorted out your neighborly relations. That is far from being the case between Mexico and the USA. As the famous saying goes, “poor Mexico, so far from god, so close to the US”.

Think – in bullet point form – about the factors that shape this tension:

Since independence in 19th century, the Mexican state’s existence has been defined by its need to maintain autonomy from its more powerful Northern neighbor.Racism and cultural condescension projected from the rich WASP North to the poor, Spanish-speaking, Latinx, Catholic South, frame the entire relationship.The nationalist ideology of the Mexican revolution built a firewall between US and Mexican politics. Those embers cooled over the course of 20th century, but as Mexico’s President since December 2018, Andrés Manuel López Obrador (AMLO) demonstrates, the flames of nationalism can be easily rekindled, not just on the US side.Mexico’s oil industry once integrated the country into the world economy as a fossil fuel exporter and major player in OPEC. Nationalized in the 1930s it gave the Mexican national economy a powerful base. The decline of the industry in recent decades is profoundly discomforting for nationalist. They see no good future for Mexico as a near-shoring manufacturing replacement for China.Migration from Mexico to the USA, which expanded massively from the late 1960s to the 2010s, is a unifying link at a personal level and a huge source of remittances – $60 billion per annum plus – but the “unresolved” stance of the US towards migration and the mounting crisis in Central America creates millionfold human misery and a running sore in political terms.Build the Wall: Right-wing xenophobic political entrepreneurs in the USA repeatedly mobilize around the migration issue. Increasingly, this is not simply a Mexican-American but a Central American issue as well.The drugs wars, again shaped by proximity, have been a half-century disaster. The cartels profoundly challenge the rule of law and the authority of the Mexican state.The explosion of Fentantyl consumption and supply raises the issue of narcotics to a new level of urgency and China’s role in the trade gives the issue a particular toxicity.In global geoeconomic terms, a fact which the US takes too easily for granted, is that Mexico, has hitherto chosen a path not so much of non-alignment as neutrality. Likewise, Mexico has been by-passed by the huge rise in China’s economic influence in Latin America. In an increasingly polarized world, in which America’s influence declines in relative terms, this neutrality may be harder and more expensive for Mexico to maintain.Given the huge level of entanglement between Mexico and the United States and the many crises that arise – an obvious case of polycrisis – the political architecture to resolve tensions between the two countries is astonishingly fragile. USMCA (the replacement for NAFTA since 2000), is not – like the EU – a “whole-of-government” affair, but is owned by specialized trade ministries. Leader-level meetings take place on the whim of the political personalities involved. They ceased during the Trump period. The lack of powerful institutional anchoring means that both governmental practice and political discourse on both sides is relatively disinhibited in imagining alternative futures for the Mexican-US relationship. It is hard to know what can be ruled out and what must be ruled in. It is as though Franco-German relations had to be continuously reinvented without institutional continuity.In short, the boundaries of what is “near” and what is “friendly” are not given in US-Mexican relations. They are constantly negotiated, defined and redefined in an unequal, historically path-dependent power-play between the two countries.

***

Since Russia’s invasion of Ukraine and the election of Lula, all eyes in the Western hemisphere have been on Brazil and how it has positioned itself between Washington and Moscow. By comparison, it is remarkable how low Mexico has flown under the radar, receiving only a passing mention in the roster of the new non-aligned movement, overshadowed by the likes of Lula and Modi.

This was true also of the original non-aligned movement originated in the 1950s, in which Mexico’s place was that of an observer. Likewise, Mexico played no role in BRICS in the early 2000s. The Vincente Fox administration of the time did not make an easy bedfellow with the pink tide led by Lula’s Brazil. The shift to the left under AMLO since December 2018 and the polarization of global geopolitics has reopened these questions.

Since Russia’s invasion of Ukraine, Lopez Obrador has maintained a position of neutrality in the conflict. AMLO has roundly condemned the United States for rushing aid to Ukraine whilst ignoring the refugee crisis and the disastrous security situation in Central America. At the start of the war a clutch of House Deputies from AMLO’s coalition raised heckles by launching a “Mexico-Russia Friendship Committee”. Mexico has refused to sanction Russia or to send military assistance to Ukraine and has condemned the European Parliament for sending military aid to Kyiv.

Mexico is not oblivious to the stakes involved. Together with France, Mexico proposed a resolution to the U.N. General Assembly that gained overwhelming support, blaming Russia for the humanitarian crisis in Ukraine and calling for an immediate cease-fire for the sake of millions of civilians. But when it came to the General Assembly on the matter of Russia’s suspension from the Human Rights Committee whereas Argentina, Chile, Colombia, Costa Rica, Ecuador, Guatemala, Honduras and Peru all voted in favor of the resolution and Bolivia, Cuba and Nicaragua voted against, Mexico joined Brazil and El Salvador in abstaining.

Zelensky has spoken to the Mexican parliament, but at the invitation mainly of opposition deputies. For AMLO himself, the priority is to end the war. He has denounced the backing of Ukraine by the US and its Western allies as a cynical proxy war, summarized by the motto: “I’ll supply the weapons, and you supply the dead.”

Not only has Mexico refused to join the American-led coalition against Russia, AMLO’s foreign minister, Marcelo Ebrard, one of leading candidates to succeed him in 2024, has expressed sympathy for the values of BRICS. South Africa’s Foreign Minister Naledi Pandor claimed in an interview that she had received an approach about a possible BRICS membership for Mexico. This rather remarkable claim was picked up by DW, but seems not to have been confirmed or denied.

For the most part the USA has thought it best to comment as little as possible on Mexico’s positioning. It suits everyone to give Brazil pride of place. But America’s commander for the Northern Command General Glen VanHerck has warned a Senate Committee, that the GRU – Russia’s military intelligence – has deployed the largest proportion of its spies to Mexico. As in the Cold War, Moscow’s oversized embassy in Mexico City appears like an espionage center. Those remarks led President Lopez Obrador to respond in typically combative style: “Mexico is a free country, independent and sovereign, we are not a colony of Russia, China or the United States.”

***

One of the structural forces driving Brazil’s non-alignment with the US front on Ukraine is the rise of China. China’s booming trade with the Latin American region has been one of the dramatic stories of the last two decades. Between 2002 and 2019 trade volume exploded from $17 billion to $315 billion per year, whilst China’s investment in the region in the 2010s exceeded $150 billion. For Brazil and Chile, China is now the leading trade partner, not the US.

Mexico was, until recently, an exception to this pattern. As a low-wage manufacturing hub with a declining oil sector, its complementarities with Chinese growth were less obvious. Mexico’s share of China’s investment and trade in Latin America was tiny. Indeed, opposing China’s “invasion” of the Western hemisphere has been a source of legitimacy for Mexican politicians. The Fox administration (2000-2006) aligned with angry Mexican manufacturers facing the shock of China’s admission to the WTO. Stereotypes of aggressive and intrusive Chinese predominate in the Mexican media.

Again, there are signs of change in Sino-Mexican relations. Mexico now recognizes China as a key partner. But as Washington has made clear, on China the stakes are high. Although China is not mentioned explicitly in the USMCA Treaty, Article 32.10 stipulates that if any of the three trade partners intends to enter into a free trade agreement with a “non-market economy,” it must inform the other partners at least three months prior to commencing negotiations. If an agreement is reached with the “non-market” partner, the parties to the USMCA are free to abrogate the trilateral agreement. In terms of geoeconomic alignment, Article 32.10 signals that Mexico has to choose, between the US and China.

In less formal terms, one veteran diplomat has remarked that the United States made clear to Mexico that it would face sanctions if it joined China’s Belt and Road Initiative. Washington asked President Peña Nieto explicitly not to join the Asian Investment Infrastructure Bank.

In 2020 Beijing spied an opportunity to gain leverage. The world faced the COVID pandemic. The US in the last year of the Trump administration was preoccupied with domestic crises. China stepped in to supply Mexico with 35 million doses of CanSino vaccine. This elicited a friendly exchange of messages with Secretary of Foreign Affairs Marcelo Ebrard who had made an official visit to Beijing in 2019. Ebrard followed up with the promise that Mexico “will expand the strategic partnership of both nations.”

And this is not merely talk. The Mexican border state of Nuevo León with its capital Monterrey, has positioned itself as a key hub for the flourishing China-Mexico investment relationship. The state’s governor, the brash, 35-year Samuel García, went to Davos to declare that “Nuevo León is having a geopolitical planetary alignment”. What that means in practice is that of the $7 billion in foreign investment that has poured into the state since October 2021, 30 percent came from China, second only to the US.

As relations between China and the US deteriorate, it is not only Western firms that have to adjust, Chinese producers too are looking for ways to maintain access to the US market. This is not the kind of inter-governmental agreement that would trigger Article 32.10 of USMCA, but it nevertheless rewires US-Mexican-Chinese economic relations.

However, to talk about Mexican-American-Chinese relations right now by reference to Chinese furniture factories in Monterrey, would be a bit like talking about Taiwan and mentioning only the microchips. The real questions about near-shoring and friend-shoring come into focus when we move from the legal to the illegal economy, from furniture and motorvehicles to organized crime, the lethal synthetic opioid epidemic in the United States and above all Fentanyl.

***

The rise of the Fentanyl business has given a catastrophic twist to the long-running disaster of the Mexican-American drug wars. Fentanyl embodies a perverse kind of triangular globalization in which Fentanyl and its precursors flow from China to Mexico, where the cartels manufacture them into illegal narcotic product, which is then trafficked to the United States and exchanged for cash and weapons. The weapons enable the cartel to build and consolidate their extra legal power bases and compete for turf. The cash is partly recycled into the illegal economy, partly laundered. Increasingly, Chinese money laundering channels take advantage of the billions in drug dollars to evade the exchange controls that China put in place in 2015.

The overall values of these flows is estimated to run to many tens of billions of dollars per annum. This is perhaps one tenth of the volume of legal trade between Mexico and the United States, but amplified by intense violence it is enough to create havoc. Annually, the cartel wars claim the lives of perhaps as many as 30,000 Mexicans. In the US the addiction epidemic claims over 100,000 lives of which roughly three quarters are down to Fentanyl.

In an ideal world of governmental fantasy, the United States, China and Mexico would identify the surge of drugs as a common global problem. They would cooperate to identify and interdict the drug producers and smugglers. Meanwhile, the US would introduce sweeping social reforms and public health policies to cut the demand for drugs, which is the ultimate source of the problem. The US would also introduce gun controls, suppress the legal trade in firearms and comprehensively control firearms exports. High-powered assault weapons and ammunition would no longer be freely available to the cartels to import to Mexico. Meanwhile, the Mexican state would rid itself of corruption, suppress the challenge to state authority from the cartels and embark on extensive economic development programs to provide alternative sources of income.

Clearly, in 2023 we are very far from any such fantasy. Not only is geopolitical and political tension reducing cooperation but clashes over the narcotics crisis are raising political tension in a dangerous way.

It has not always been so. There were moments of Sino-American cooperation around Fentanyl suppression in the 2010s, but all counter-narcotics cooperation has been suspended by China since Pelosi’s visit to Taiwan. Likewise, Mexican American cooperation has been run down by the AMLO government which views the American DEA officers operating in Mexico as a fundamental intrusion on Mexico’s sovereignty. In the US, the structural factors that drive deaths of despair are as prevalent as ever. Comprehensive gun control has no chance in Congress. AMLO, though he has deployed the military in the drug wars, shows no sign of making a decisive breakthrough to reassert control. Increasingly, the best to be hoped for is to reduce the level of violence. This, however, not only perpetuates the disastrous situation in many communities in both Mexico and the United States. It also holds open the door to a further escalation in political tension between the United States and Mexico. This is exploited particularly by Republicans on the US side as a issue on which to demonstrate red-blooded all-Americanism and as a useful stick to beat Biden with. In so doing Republican trouble makers and ideologues reaching for the hammer with which America’s political elite often seeks to treat problems, one of America’s undisputed strong suits: military power.

***

When Trump was in the White House this impasse triggered wild speculation about US military strikes against Mexico. According to his Defense Secretary Esper, Trump in 2019 asked for options to use military force against the Mexican cartels unilaterally.

In opposition, the GOP has not calmed down. Inside Trump’s entourage they apparently consider the failure to launch strikes into Mexico as one of the missed opportunities of his Presidency.

As Alexander Ward reported for Politico in April 2023:

” In recent weeks, Donald Trump has discussed sending “special forces” and using “cyber warfare” to target cartel leaders if he’s reelected president and, per Rolling Stone, asked for “battle plans” to strike Mexico. Reps. Dan Crenshaw (R-Texas) and Mike Waltz (R-Fla.) introduced a bill seeking authorization for the use of military force to “put us at war with the cartels.” Sen. Tom Cotton (R-Ark.) said he is open to sending U.S. troops into Mexico to target drug lords even without that nation’s permission. And lawmakers in both chambers have filed legislation to label some cartels as foreign terrorist organizations, a move supported by GOP presidential aspirants.”

Rolling Stone, which broke the story, describes the mood in the Trump camp as bellicose

“‘Attacking Mexico,’ or whatever you’d like to call it, is something that President Trump has said he wants ‘battle plans’ drawn for,” says one of the sources. “He’s complained about missed opportunities of his first term, and there are a lot of people around him who want fewer missed opportunities in a second Trump presidency.”

Lindsay Graham has weighed in promising that “We’re going to unleash the fury and might of the United States against these cartels,”. He called on President Biden to “give the military the authority to go after these organizations wherever they exist.”

In the pages of the Wall Street Journal, Trump’s Attorney General and long-time warrior of the American right, “Bill” Barr dressed up a legal case for intervention, making sure to distance himself from any “nation-building” ambitions.

The cartels have Mexico in a python-like stranglehold. American leadership is needed to help Mexico break free. We can’t accept a failed narco-state on our border, providing sanctuary to narco-terrorist groups preying on the American people.

Meanwhile, Senator John Kennedy of Louisiana made explicit the utter contempt for America’s neighbor that runs through Republican thinking about Mexican-American relations. Speaking of the question of enlisting AMLO and the Mexican government in America’s drug enforcement efforts Kennedy remarked:

“Make him a deal he can’t refuse … Without the people of America, Mexico, figuratively speaking, would be eating cat food out of a can and living in a tent behind an Outback.”

These outrageous remarks came not off the record, but during a Senate appropriations subcommittee hearing in which Kennedy was pressuring Drug Enforcement Administration administrator, Anne Milgram to unleash the US military and law enforcement officials on Mexico to “stop the cartels”.

The setting for Kennedy’s comments is telling. Given the US constitution, Biden administration officials and America’s military leaders, though they are opposed to any unilateral moves against Mexico, are forced to reply to even the most outrageous demands from the Republican side. The surreal result is that Washington is now engaged in an earnest debate about whether or not to bomb Mexico. In this debate the opponents of bombing America’s neighbor and one of its most important trading partners are forced to justify their refusal on first principles.

As Melissa Dalton, the Assistant Secretary of Defense for Homeland Defense and Hemispheric affairs told House Armed Services Committee members: “In terms of weighing the advantages and disadvantages of some of the steps that are under consideration in terms of use of force or certain designations, I think we need to be clear-eyed about what some of the implications might be for the lines of cooperation we do have with Mexico … I do worry, based on signals — very strong signals we’ve gotten from the Mexicans in the past, concerns about their sovereignty, concerns about potential reciprocal steps that they might take to cut off our access, if we were to take some of these steps that are in consideration.”

As Politico somewhat blandly remarks, it would appear that “President Joe Biden doesn’t want to launch an invasion”. This is admittedly something of a relief. Given Trump’s preferences it should not be taken for granted. When asked by journalists, National Security Council spokesperson Adrienne Watson affirmed that “The administration is not considering military action in Mexico.”

In recent Senate and House hearings about the President’s defense budget request, Chairman of Joint Chiefs General Milley and Defense Secretary Lloyd Austin faced multiple questions from Republicans asking about the possibility of U.S. military intervention or for some greater role for troops in stopping the inbound flow of drugs. Milley, who as America’s top military officer must pay homage to the principle of civilian supremacy, was reduced to stating that he would not “recommend” unilateral strikes on Mexico.

The problem for those favoring restraint is that the situation is truly disastrous, they have no good alternatives to offer and America’s planetary conception of its own security provides no official with any wiggle-room. It is their duty to protect Americans everywhere from every threat and to use the tools at their disposal to do so.

So in March 2021, Head of U.S. Northern Command General Glen VanHerck stated that 30%-35% of Mexico constitutes an “ungoverned space”, which as he warns opens the door to cartels and their foreign friends. That then raises the question of how any American President could stand by and allow a lethal threat to America to develop on its border without acting. As the explosive memo to a putative President Trump highlighted by Rolling Stone, remarks: “It is vital that Mexico not be led to believe that they have veto power to prevent the US from taking the actions necessary to secure its borders and people.”

At one level this is an outrageous carte blanche for an infringement of Mexican sovereignty and a forever war on drugs. At another level it is merely the assertion of the basic principle of self-defense in the face of an unregulated transnational threat on America’s borders. America’s sovereignty and the paramountcy of its own interests means that Mexico can have no veto. To concede anything less is tantamount to treason. And perhaps most disturbingly it is not altogether easy to separate this argumentative logic from the national security proviso around which Janet Yellen organized her recent speech on Sino-American economic relations. Or for that matter to distinguish this assertion of national autonomy on drugs policy from the belligerent defense of America’s position on steel tariff in the face of censure by the WTO. As USTR Spokesperson Adam Hodge put it:

The United States has held the clear and unequivocal position, for over 70 years, that issues of national security cannot be reviewed in WTO dispute settlement and the WTO has no authority to second-guess the ability of a WTO Member to respond to a wide-range of threats to its security.

Connecting the dots to intervention in Mexico, Barr in his WSJ pieced spelled out the logic: :

Under international law, a government has a duty to ensure that lawless groups don’t use its territory to carry out predations against its neighbors. If a government is unwilling or unable to do so, then the country being harmed has the right to take direct action to eliminate the threat, with or without the host country’s approval.

***

In conventional debate about the new era of geopolitics we still draw neat boundaries. Russia and China are linked, which then prompts the search for wholesome and safe near-shoring and friend-shoring options. USMCA and EU-US relations are conventionally allocated to that bucket. This assignment broadly overlaps with other new dichotomies like the one favored by President Biden between democracies and autocracies.

Republican discourse disrupts this neat packaging with its lack of enthusiasm over Ukraine. But also with the disinhibited aggression which it directs towards Mexico.

You might be tempted to dismiss the rantings of Trump, Graham or Kennedy. But it would be dangerous to discount it merely as political theater – the GOP might very well win in 2024. We do not know what lessons might be learned by a second Trump Presidency.

Furthermore, their expostulations reveal a more general tendency. Faced with truly entangled problems of domestic and global governance thrown up by the polcyrisis, there is an in-built bias in the American government system, dramatically reinforced by the political entrepreneurship of America’s nationalist right-win to reach for military solutions. The Ukraine crisis has provoked this tendency in Europe. Taiwan does this in East Asia and the drugs and migration problems does the same even on America’s own border with Mexico. In each case the underlying conflicts are very real. But so too is the common thread in the American response. As the Ukraine case demonstrates this is very much a bipartisan tendency. The distinctive contribution of the Republicans is the openness with which their disinhibited nationalism forces the American political class to discuss its options.

One cannot but must admire the efforts by Biden’s team to devise a logic for this dangerous new world. Jake Sullivan’s speech at Brookings is the clearest effort to date to do that. But as I argue in my op-ed for the FT this weekend, to imagine cleverly engineered industrial policy as the basis for a new Washington consensus seems wildly optimistic.

What we must surely fear is the only real common denominator of policy-making in Washington right now is the Pentagon budget, where the financial demands of America’s new theaters of conflict run together. Tellingly it was the one element of Federal spending which the two parties in Washington could agree to exclude from. the brinksmanship of the budget ceiling stand off.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week

Ones & Tooze: Tech’s New Trillionaire

It’s a great time to be in the AI business. Just ask Nvidia, the AI chip company that doubled in value this year. Cameron and Adam discuss whether it’s overvalued… or worth every penny.

Also on the show: the economics of Mexico.

Find more episodes and subscribe at Foreign Policy.

June 1, 2023

Why America’s economic policy muddle matters

The messy nature of decisions is important both for US citizens and the world

May 31, 2023

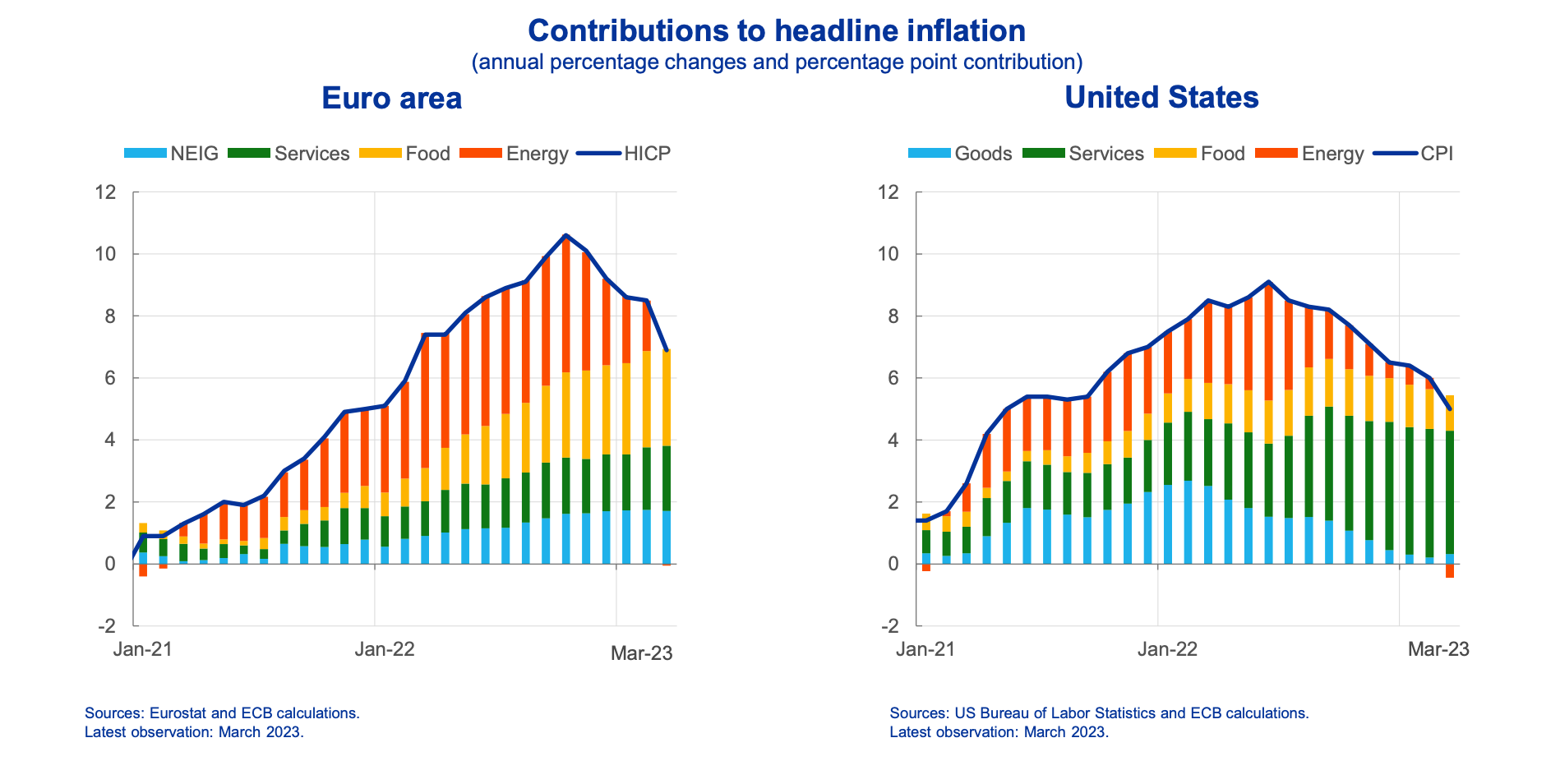

Chartbook 217 The inflationary surge of 2022 – trans-Altantic comparisons and European hotspots.

In the US the obsession with the inflation, the Fed, interest rates and financial stability has been displaced from the headlines by an overriding preoccupation with fiscal policy. In the brief interval between the two, Janet Yellen and Jake Sullivan brought the world up to speed on the parameters of what is being dubbed the “new Washington consensus”. More from me on this kaleidoscopic alternation in the FT at the weekend.

Meanwhile, in Europe, the debate about inflation goes on. Culling recent speeches by Philip Lane and Isabel Schnabel results in an interesting composite picture of the distinctive features of both the European and American inflations.

Source: ECB

The surge of European inflation past the US peak of 8 percent is largely attributable to the more painful surge in both energy and food prices in Europe.

In the US, by contrast, the acceleration of services inflation has come to dominated the story.

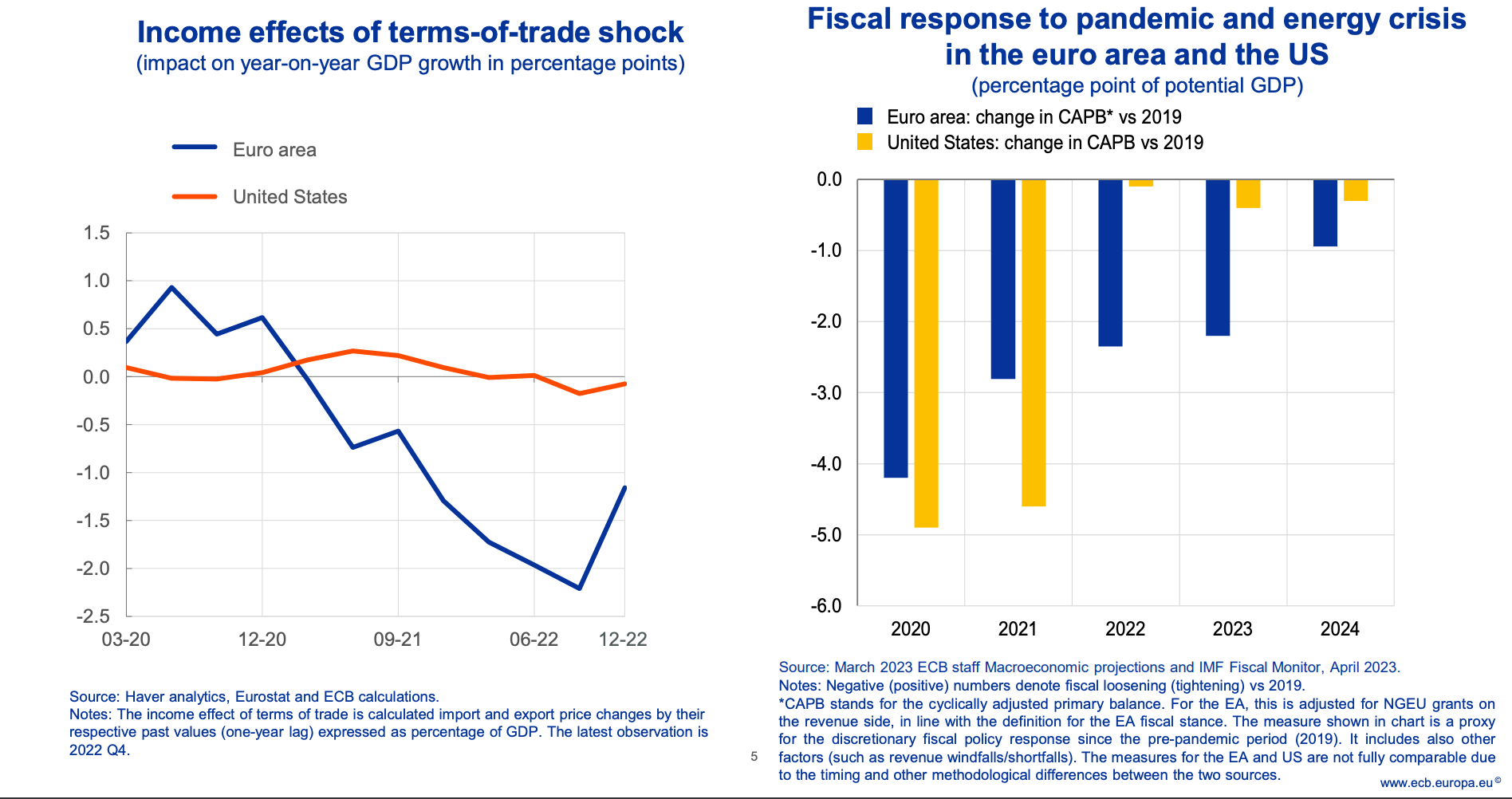

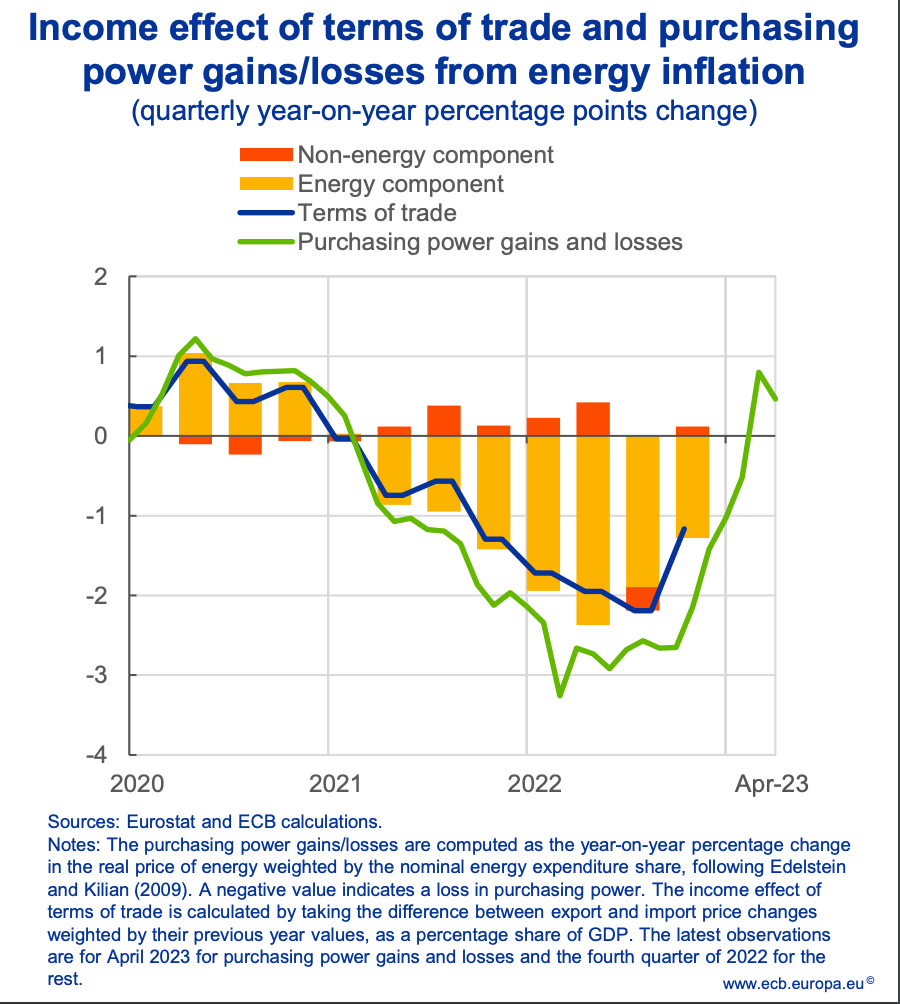

The surge in the prices of imported energy and food inflicted a terms of trade shock on the European economy to the tune of 2 percent of GDP. The impact on the US which is a major exporter of both food and energy was broadly neutral.

Overwhelmingly this terms of trade shock came from energy.

Source: ECB

There is a striking difference between Europe and the US also with regard to the fiscal response to the succession of shocks that hit the world economy between 2020 and 2022. The US fiscal response to COVID was more generous but also contracted more sharply, whereas under the impact of the Ukraine war, the fiscal taps in Europe have remained open.

Whereas the European economy has barely recovered above its 2019 level, the US has clocked up a solid 5 percent growth, driven by a considerable surge in private consumption and particularly the private consumption of goods.

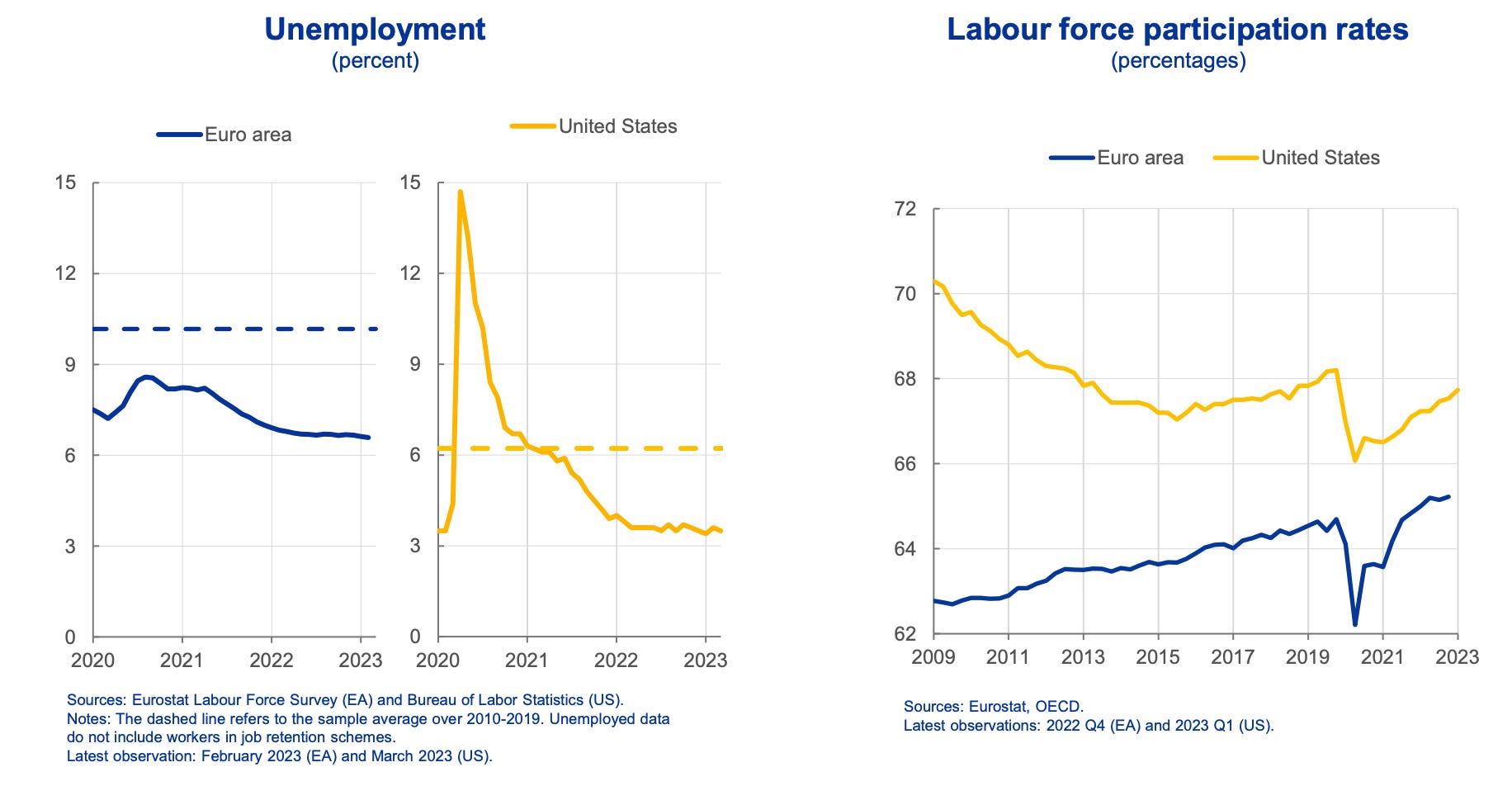

Both in the US and the EU, the recovery from the 2020 shock has produced a strikingly low level of unemployment. But whereas in the EU labour market participation is somewhat higher today than one might have expected on the basis of pre-crisis trends, the US has seen a retreat from the workforce both of younger and older works.

Charts by ABN AMRO bring out the different trajectory of labour market participation in to sharp focus (beware the different scales here).

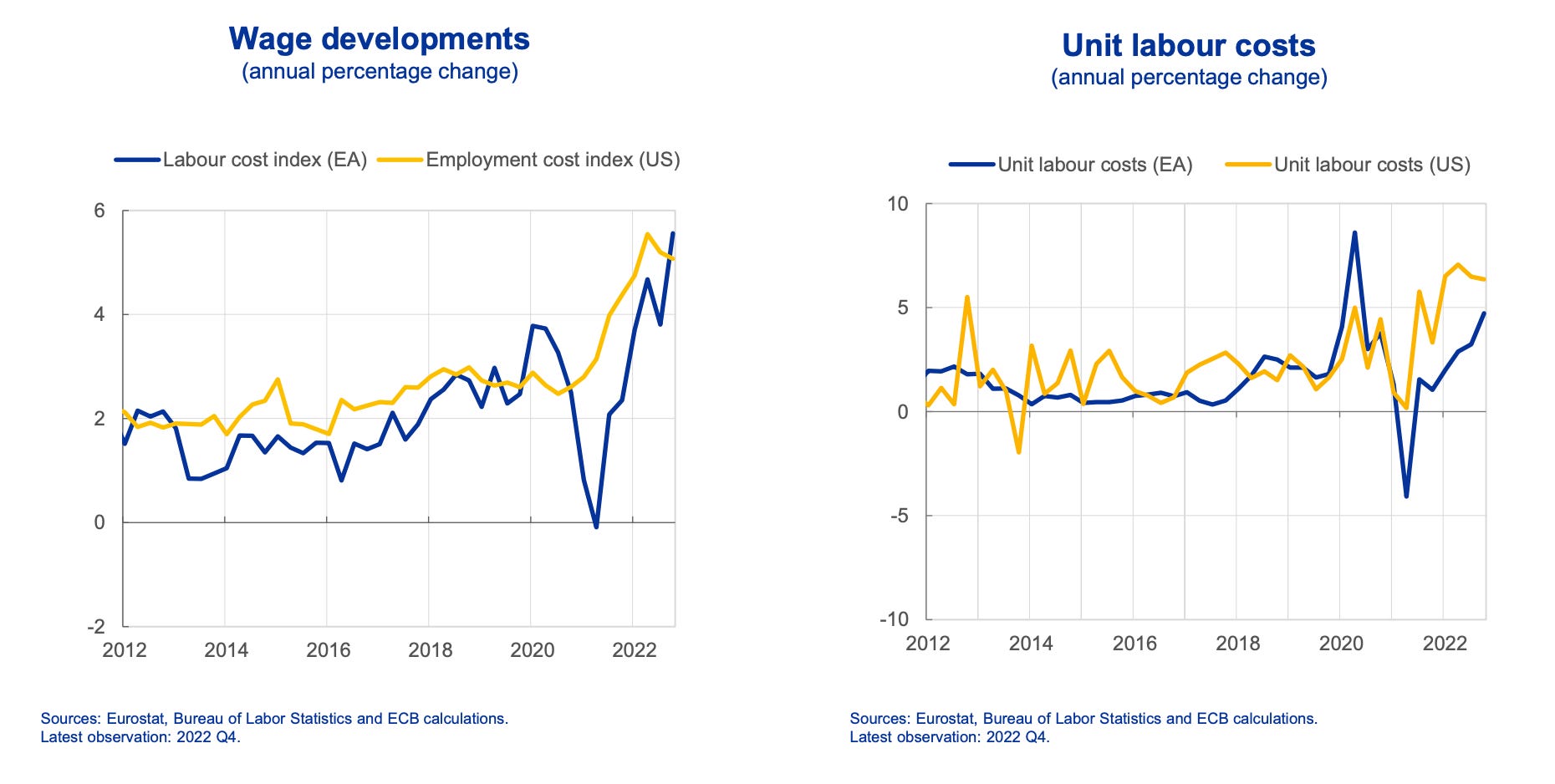

In both the US and Europe labour market tightness has led to a considerable acceleration in the growth in nominal wages.

In both cases, nominal wages have struggled to keep up with prices. As a result, if one accepts a cost-push model of pricing, rising unit labour costs can account only for a share of the price increases.

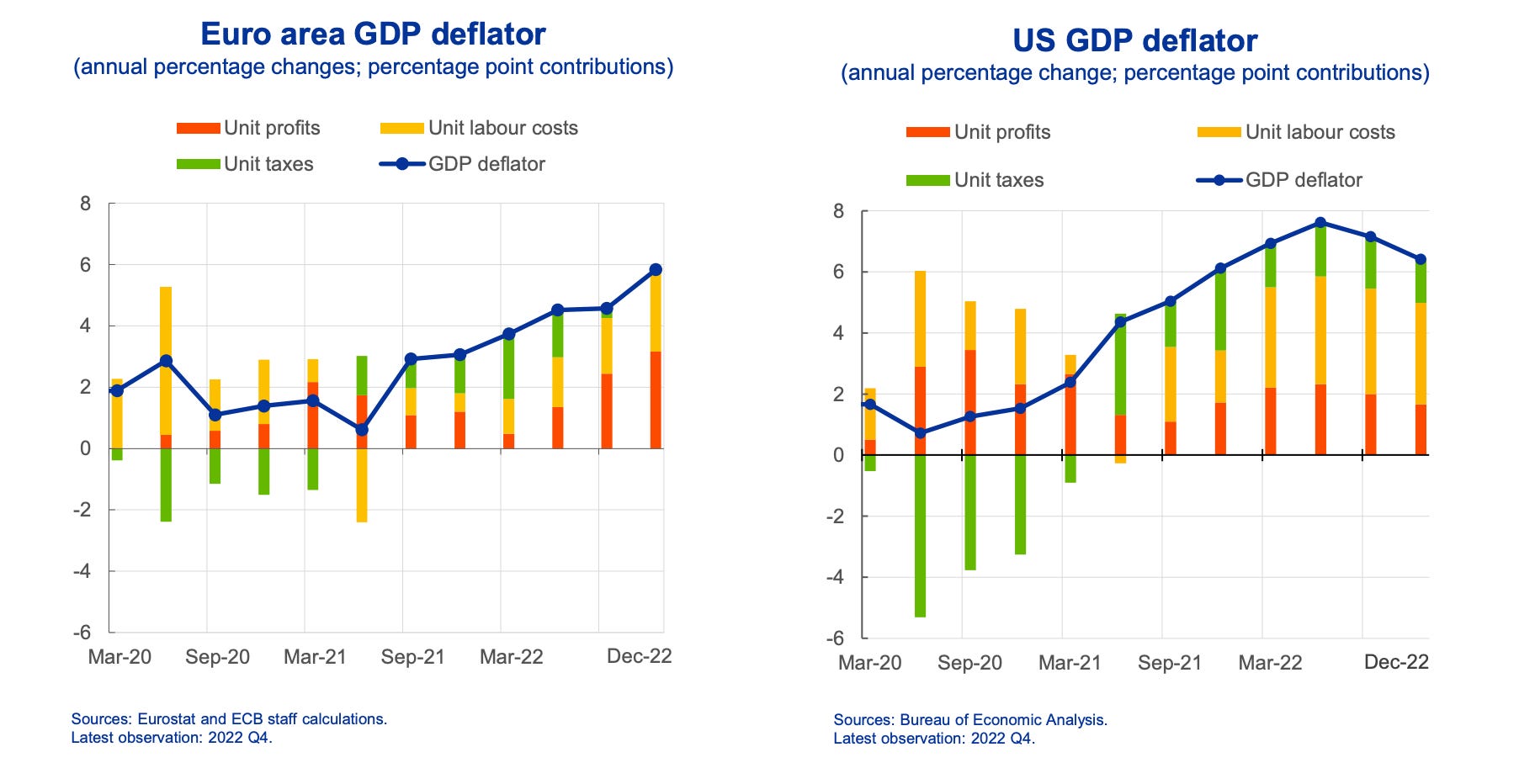

In a striking turn in the public argument, the ECB is willing to credit surging profit margins in Europe with a larger share of inflationary pressure than wages. In the United States, at least according to the ECB’s methodology the lion’s share of cost pressure comes from the size of unit labour costs.

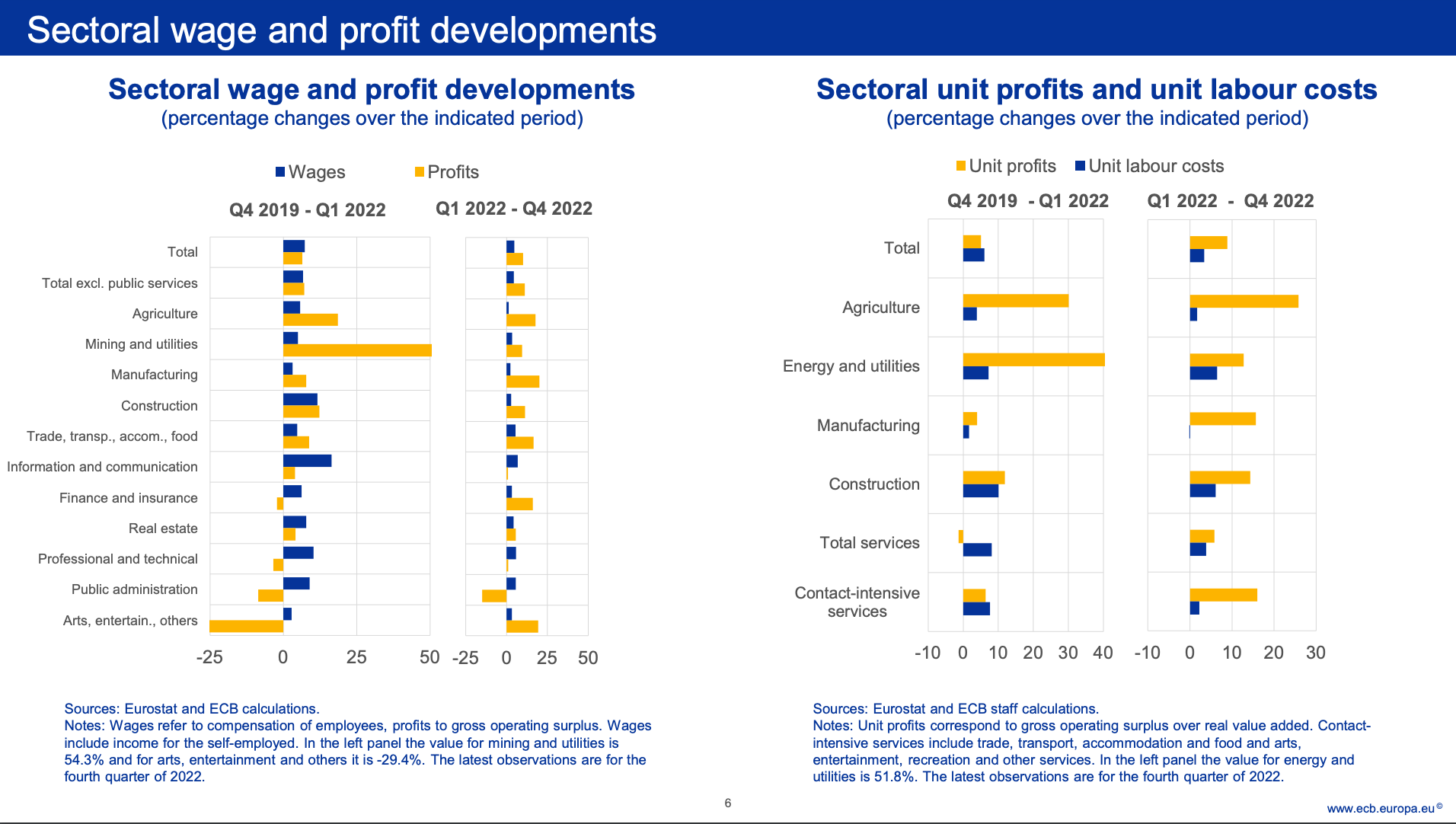

Sectoral data for the euroarea point to construction and agriculture-food as the key sectors for inflation.

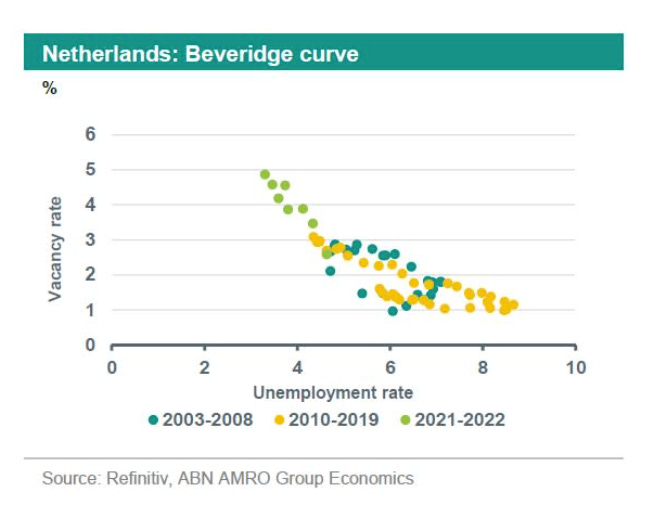

The very different ways in which the labour market shocks delivered by COVID were handled is brought out by a comparison of the Beveridge curves for the US and the Netherlands. In the US the shock is visible in the dislocation of normal relations between vacancies and unemployment. The scale of mismatch in the demand and supply of labour is brought out by the much higher level of vacancies for any given level of unemployment between 2021 and 2022.

By contrast, the Netherlands appears too have absorbed the shock simply by moving along the normal trade off curve. As the economy has bounced back fast from the COVID shock, unemployment has fallen and vacancies are at record levels.

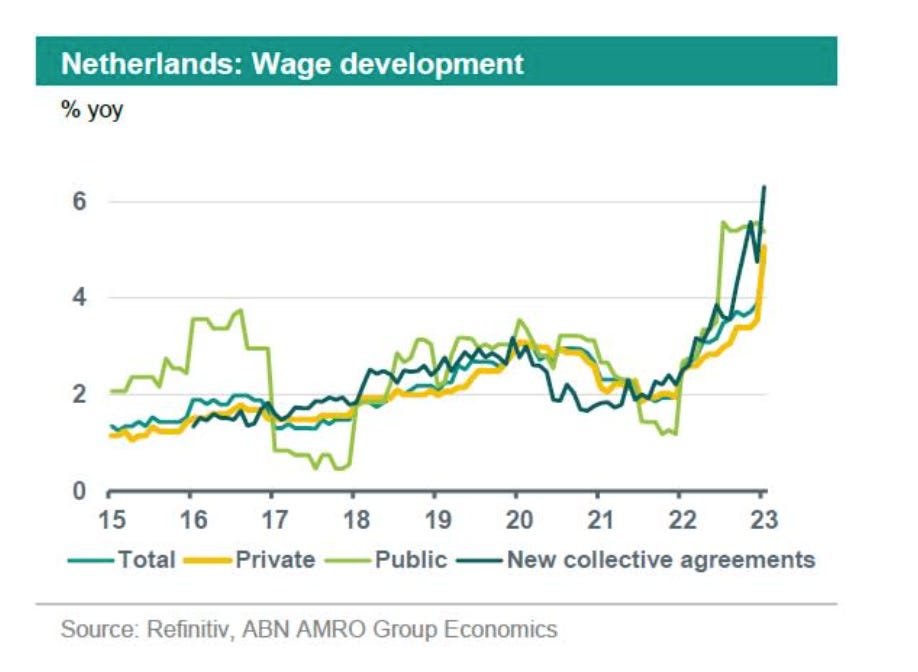

With inflation surging above 14 percent in September 2022 and food prices continuing at rapid pace, it is unsurprising that wage inflation in the Netherlands. is surging as well.

The upshot is that inflationary pressures may have been broadly similar on both sides of the Atlantic, but the underlying dynamics of terms of trade, fiscal policy and labour market dynamics differ in important ways. Currently the Fed is ahead of the ECB in the tightening cycle. Core inflation in Europe is now running ahead of that in the US. Germany may have already turned into recession. But other important parts of the EU economy are still “overheating”. Those wishing to anticipate the future moves of the ECB will be well-advised to track hot spots like the Netherlands.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you will receive the full Top Links emails several times per week

Adam Tooze's Blog

- Adam Tooze's profile

- 767 followers