Adam Tooze's Blog, page 9

December 23, 2022

Ones & Tooze: Is Biden Killing the World Trade Organization?

The United States is challenging the very authority of the World Trade Organization—which it helped establish decades ago. Adam and Cameron discuss why and what a weakened WTO would mean for the world.

Also on the show: Why Americans give more to charity than anyone else in the world (hint: it’s less about altruism and more about how Americans organize themselves).

Find more episodes and subscribe at Foreign Policy

Chartbook #182 Washington’s disruptive new consensus.

If you travel to South Korea or Europe right now, the talk in international economic policy circles is all about one thing: America’s “giant” Inflation Reduction Act and its $500 billion in subsidies for green energy and industry in the United States.

I did an op ed for the FT on the question of how Europe is reacting to the IRA.

Cameron Abadi and I took up the issue of US trade policy more generally on the podcast this week, focusing less on the IRA and more on the WTO.

Whilst in Berlin I did an interview with Handelsblatt (in German) addressing the question of the future of German industry.

There is certainly something afoot in US international economic policy. If we put together the buy (North) American and local content clauses in the IRA, clashes with the WTO over Trump’s tariffs, the Chips Act and the ongoing “tech war” with China, two questions force themselves on us:

Are we witnessing a fundamental shift in the politics of trade in the US? Is there a new Washington consensus?

If so, how should America’s “partners” react?

The answer to the first question is that it is still early days, but all the signs are that we are indeed witnessing a profound shift in the positioning of US power towards the world economy. Already in the 2016 Presidential election the US Chamber of Commerce was alarmed to note that none of the three leading candidates – Trump, Sanders or Clinton – could be described as favoring further trade liberalization. It was an open secret that if Clinton had been elected, her team were going to abandon the TPP, the ambitious 12-nation Pacific trade partnership that Obama’s team had negotiated. Trump did so on his first day in office.

Six years on, the shift in both policy and politics is more dramatic than ever. Of course, the Biden administration talks nicely and backed the Nigerian Ngozi Okonjo-Iweala as a popular new head of the WTO, after her predecessor the Brazilian Roberto Azevêdo abruptly resigned. But good vibes aside, the Biden administration has done little or nothing to help in reanimating the WTO as a functioning global organization. Trump’s opposition left the WTO without a functioning appellate procedure for disputes. Nothing has changed on that score. And the administration has been anything other than supportive of the efforts by concerned groups of nations, including the EU, to put in place alternative conflict management procedures.

The bon homie of the Biden administration means that, unlike under Trump, this disruption barely breaks surface and makes it harder in fact for commentators and the rest of the world to orientate themselves. It looks like the US is abandoning the structures of global trade that it did so much to build between 1945 and the early 2000s. It smells as though it is. It sounds as though that is the plan. Can it possibly be true?

The tone of Paul Krugman’s recent piece in the New York Times is telling. The leading trade economist of his generation cannot avoid the conclusion that something dramatic is happening. The willingness of the Biden team to flaunt the view of the WTO and its partners, Krugman writes,

… is a very big deal, much bigger than Trump’s tariff tantrums. The Biden administration has turned remarkably tough on trade, in ways that make sense given the state of the world but also make me very nervous. Trump may have huffed and puffed, but Biden is quietly shifting the basic foundations of the world economic order. … But if the United States, which essentially created the postwar trading system, is willing to bend the rules to pursue its strategic goals, doesn’t this run the risk of protectionism growing worldwide? Yes, it does.

Though Krugman pronounces himself a bit “nervous” he concludes by affirming the Biden administration’s stance, both on China and climate: “The GATT (sic) is important, but not more important than protecting democracy and saving the planet.”

Of course, we need to check any assessment of the politics of trade in the US against the macroeconomic facts on the ground. As Michael Pettis reminds us, it is a little “surreal” when economic powers that run huge and persistent trade surpluses, like China and the EU, accuse the United States, which runs the largest persistent trade deficit, of protectionism.

1/6

— Michael Pettis (@michaelxpettis) September 27, 2022

It's a little surreal when the country with the largest persistent trade surplus in the world accuses the country with the largest persistent trade deficit in the world of protectionism and “ideologicalised” industrial subsidies.https://t.co/Zpp5zR1020 via @scmpnews

But check out this response from the US Trade Representative to a WTO panel finding on steel and aluminium and tell me that you don’t feel a cold wind blowing.

“The United States strongly rejects the flawed interpretation and conclusions in the World Trade Organization (WTO) Panel reports released today regarding challenges to the United States’ Section 232 measures on steel and aluminum brought by China and others. The United States has held the clear and unequivocal position, for over 70 years, that issues of national security cannot be reviewed in WTO dispute settlement and the WTO has no authority to second-guess the ability of a WTO Member to respond to a wide-range of threats to its security. These WTO panel reports only reinforce the need to fundamentally reform the WTO dispute settlement system. The WTO has proven ineffective at stopping severe and persistent non-market excess capacity from the PRC and others that is an existential threat to market-oriented steel and aluminum sectors and a threat to U.S. national security. The WTO now suggests that the United States too must stand idly by. The United States will not cede decision-making over its essential security to WTO panels. The Biden Administration is committed to preserving U.S. national security by ensuring the long-term viability of our steel and aluminum industries, and we do not intend to remove the Section 232 duties as a result of these disputes.”

Nor is it just national security that is at stake. Especially when it comes to the Inflation Reduction Act there is great enthusiasm across the spectrum of progressive think tanks in the United States for a new era of industrial policy. This embraces climate policy and the anti-China stance, invoked by Krugman to justify from the WTO rules. It also extends to what was formerly the agenda of Build Back Better and the Green New Deal i.e. a vision of domestic economic and social reconstruction, impelled by a broad-based agenda of energy transition and green industrialization.

If you want to get a sense of the thinking within this ecosystem there is no better source than Todd Tucker at the Roosevelt Institute, whose twitter account delivers a rolling drumbeat of new policy initiatives.

Recognizing the shift that was happening towards a new "Washington Consensus" and the need to help make meaning of it, we pulled off a major gathering on industrial policy in October. https://t.co/EyIMfbAjz1

— Todd N. Tucker (@toddntucker) December 22, 2022

In commentary in the Washington Post, Tucker posits a clash between, on the one hand, a rigid adherence to the existing trade regime which goes hand in hand with carbon pricing as the main tool for decarbonization, and, on the other hand, the kind of approach favored by the Biden administration, which focuses on the more “politically attractive” route of national industrial subsidies.

Countries like the United States are trying to fight the climate crisis by offering industries green incentives, rather than simply taxing industrial emissions. That’s likely to require some assurance that the WTO will permit exceptions for what countries deem to be nationally appropriate decarbonization pathways. If WTO trade panelists don’t offer more deference to national policymakers than these two recent cases suggest, we are likely to see greater calls by environmental groups for a substantial paring back of trade rules for the duration of the climate emergency.

Behind phrases such as “politically attractive” and “nationally appropriate decarbonization” there is a complex agenda of coalition-building which sees green industrialism as a better future for the American working-class and American society in general. The show case was a recent Progressive Industrial Policy summit.

Progressive Industrial Policy: 2022 and Beyond.

— Todd N. Tucker (@toddntucker) October 13, 2022

Video from our @rooseveltinst forum is now live!

17 speakers, 6 sessions, hundreds of thinkers and doers gathered.

What did it all mean? Here are Five Takeaways from your truly.https://t.co/4PfqMvXf9O #IndustrialPolicy2022

But even setting aside issues of American social and economic order, if you read the recent treatments of decarbonization policy by leading US experts such as Victor and Cullenward and Victor and Sabel respectively, they too favor an approach to decarbonization that focuses not on global carbon pricing, but on driving innovation through national and transnational industrial networks. In 2021, the putative EU-US steel and aluminium club proposed at COP26 in Glasgow were seen as a promising step towards cooperation. But, as Tucker points out, this EU-US deal is likely to. be challenged by the Chinese. And none of this can disguise the fact that the Inflation Reduction Act with its strong emphasis on production within North America and local content rules is a step back from wider international cooperation. This is why I refer in my FT piece to the IRA as a “morbid symptom”. Though it is the largest climate action ever passed by the US Congress and though it may promise an acceleration of decarbonization in the US, it is devoid of any international or global vision. It is the product of a deadlocked Congress that can rally majorities only when they are draped in the Stars and Stripes and larded with anti-Chinese measures. I would love to be told otherwise, but I would be staggered if anyone in the fevered negotiations on Capitol Hill in July 2022 from which the IRA suddenly emerged, ever considered its WTO conformity, or the likely reaction of America’s major global partners.

Of course, advocates of the new Washington consensus will tell you that there is more to US industrial policy than the legislation dictated by Joe Manchin. And even the legislation extracted from Manchin offers substantial support for industrial innovation. Nor are the subsidies on offer confined to US businesses. So long as they produce in the United States and meet the local content rules, European and other foreign firms can qualify. But whereas the negative impacts on Europe and Korea may be a matter of absent mindedness, the same cannot be said with regard to the IRA’s hostility towards China and this constitutes a de fact challenge to globalization as we know it.

Which brings us to the reaction of the rest of the world to the Inflation Reduction Act and the extraordinarily late but heated response from the EU. Already in August South Korea was making representations to the US over the blatant discrimination they feared against their auto champion, the #3 auto manufacturer in the world Hyundai/Kia. Remarkably, Europe barely seems to have noticed the IRA until November, when in the aftermath of the COP27 negotiations in Egypt, a flurry of European protest began. One is tempted to suggest that it was the insistent boasting of the US delegation at the COP talks that alerted the Europeans to the IRA’s scale and its possible implications.

Right now, as far as high-level political discussion is concerned, the IRA is a hotter subject of discussion in Europe than it is in the United States. If Stanley Cohen once defined the social phenomenon of the “moral panic”, one is tempted to say that what the Inflation Reduction Act has unleashed in Europe is a “policy panic”: an echo-chamber of zealous and intense responses to a perceived existential threat.

One might also say that whilst the aggressive new Washington Consensus concerned mainly measures against China, Europe could afford to be complacent. With the Inflation Reduction Act, core European industrial interests in the auto sector are now seen to be in harms way.

Europe can no longer escape the reality that something quite fundamental and comprehensive is changing in America’s approach to the world economy. But how dramatic is that shift as far as Europe is concerned and what should Europe’s response be? This is where the question of realism arises. Not realism in the sense of academic international relations theory, which is actually a highly schematic account of the world, but realism in the sense of self-reflective effort to engage with a complex reality that includes “others”, in this case the United States, and its peculiar view of the world.

If you followed the European rhetoric and that of the boosters of the Biden administration you might easily arrive at the conclusion that the Inflation Reduction Act is a dramatic and large-scale intervention. The headline figure of $500 billion in spending is large. And, of course, in a piece of legislation over 700 pages long, there are lots of important spending items.

But whether judged against the size of US economy, the problems of American society and its economic structure, or the challenge of decarbonization, the Inflation Reduction Act is modest. That shouldn’t be surprising. Remember how the sausage was made. What we are left with, is what Manchin could somehow agree to.

Will the IRA take the United States a long way towards its decarbonization targets? Hopefully. There is no way of being certain. The IRA does not set a carbon cap, as an emission trading system does. It is all carrots and no sticks. Whether the tax incentives are large enough to induce the desired effect, we can only hope. That hope is informed by detailed modeling by a bevy of think tanks. They are super-smart people and their calculations are rigorous, but as they would be the first to acknowledge, they are hypotheticals.

I read the entire Inflation Reduction Act so you dont have to and just published my section-by-section summary of every #climate and #energy provision in the bill, along with notes on how REPEAT Project modeled each one https://t.co/8P0sKKdvqi (Senate Inflation Reduction Act tab)

— JesseJenkins (@JesseJenkins) August 5, 2022

As far as subsidy to renewal energy expansion is concerned, the IRA’s $ 385 billion sounds like a lot. But it is spread over a decade and must be placed in relation to a US economy that runs to $22 trillion. In relation to US GDP the IRA offers half the level of subsidy that Europe has already committed to green energy. As Daniel Gros coolly remarks, given its limited scale, the IRA has no more chance of reindustrializing America along green lines than Trump’s tariffs did of restoring the rustbelt. For all the European scaremongering, I’ve yet to meet anyone who thinks that the “buy America” provisions will restore Ford or GM to global leadership in EV. GM is almost as heavily committed to China as VW and Ford’s EV strategy in fact relies heavily on cooperation with VW. The more serious worry amongst representatives of the German car industry I’ve spoken to, is the impact of the IRA on the automotive supply chain and specifically batteries. They worry that America’s large subsidies for the on-shoring of battery production will draw investment away from Europe. But it seems strange to treat this as a zero sum question. If there is one thing that we know for certain, it is that the world is going to need truly vast capacities for battery production and whatever efforts they make, neither Europe nor North America will be the main supplier. Whatever efforts both undertake will be dwarfed by China. If German carmakers want more locally produced batteries then they either need to lobby for even more subsidies or draft their own local content rules. The French have long been arguing for “buy European” clauses.

In short, a realistic assessment suggests that the EU’s exaggerated reaction to the IRA has less to do with the actual IRA than with Europe’s own deep and very serious anxieties about itself. This is what echoes through concerns about the size of the American package and the urgency with which it is being pursued. In light of the fact that NextGen EU was passed by Europe already in 2020 and the passage of the American Inflation Reduction Act was in fact agonizingly protracted, and involved profound embarrassment for the Biden administration, this European talk is revealing. Apparently advocates of a bigger and more active Europe, cannot do without external reference points.

One could chide the Europeans for losing the plot, but instead what I suggest in the FT piece is that we should take their own political processes seriously. Europe’s political class currently have a bit of complex about issues of sovereignty and strategic autonomy. This is not helped by the ubiquity of Jean Monnet’s famous functionalist quip that Europe is a product of crisis and the accumulated solutions that have emerged to those crises. That was always an inadequate description. There may, indeed, be a functionalist logic impelling one crisis and one solution after another. But that process is is not deterministic and it is actuated and shaped by politics. Crises have to be defined. Solutions are found or not. Since the early 2000s with shattering referendum results on the European Constitution and the reemphasis on inter-governmentalism this has has been an increasingly uphill battle. It isn’t by accident that the concept of polycrisis was coined by Jean-Claude Juncker as Commissio President. The pandemic and Putin have delivered further staggering shock. The least you can say about the current storm over the paper-tiger of the IRA, is that this is a fight that the European political elite have chosen for themselves.

It is tempting, in fact, to cite the policy panic over the IRA as a continuation of Luuk van Middelaar’s narrative of contemporary Europe. Europe is getting more political, tougher, more Machiavellian. It is learning to define its enemies. It recognizes the advent of the new Washington Consensus on the world economy, as a crisis. It has declared an exception.

This Schmittian logic is convincing up to a point and may, in fact, be in the minds of European actors. But, is it the best way to imagine the politics of industrial policy or the energy transition? Why start with polemics rather than alliances and friendship? And let us not allow a definition of sovereignty as the ability to stand up to global bullies, whether Putin or the new economic nationalists in Washington, to occlude the question of judgement. Not every fight is a good fight. Not every provocation demands a response. And if you ask whether this is a moment to pick a fight with the Biden administration over the IRA, to push back against the new Washington consensus in the name of WTO conformity, the answer is surely obvious. No it is not.

Does this imply surrendering to US hegemony? No. It simply implies focusing on real challenges, doing what is needed and avoiding unnecessary polemics with an indispensable ally. For all Europe’s vanity about its climate policies, there is a huge amount to be done. Europe’s own EV program needs urgently to be accelerated. And in this regard, though the IRA may favor investment in US and US jobs, Detroit is a relatively spent force. As far as climate policy is concerned, wrangling the European automotive lobby is every bit as serious a challenge.

Does this imply moving beyond the principles of international trade as they were conceived in the 1990s and 2000s. Yes it does. And what the recent pivot makes clear, is that though the US was the principal force behind the old Washington consensus on globalization, it, in fact, has less invested in its foundational principles than Europe. This is a conclusion that should not be a conclusion that is surprising in light of the histories of global neoliberalism produced by Quinn Slobodian and Rawi Abdelal. As Cameron and I discus on the podcast, principles of equal treatment, restraint, rule of law matter deeply to Europe for its own internal reasons. They help to hold the complex structure of the EU with its 27 member states together. The idea of a rule-bound international trading order simply does not have that significance for America’s political economy. If national political imperatives dictate a new era of national industrial policy, so be it.

The lesson is clear. America will do things its way. Given the precarious balance of its domestic politics there is room for nothing else. But noxious as it may be, the Inflation Reduction Act is not an existential threat to European economic interests. Nor is there need to rub the nose of the Biden administration and its outriders in the mess left by their abandonment of 1990s globalism. The point is not lost inside the Beltway. The advocates of the new Washington Consensus quite explicitly acknowledge the shipwreck, in America itself, of policies once pushed by the Democratic Party elite. What is called for now is cooperative action to accelerate decarbonization by whatever means work. They may call it a new Washington Consensus but this is not a vision of order like that of the 1990s. It is not an ordoliberalism writ large. It is an ad hoc agenda for problem-solving action. Rather than clear rules and norms, it entails a mass of decisions and policy-choices. And those will entail conflicts and demand politics and diplomacy. In light of the urgency of the polycrisis that is a healthy disillusionment. It is a sign that economic policy is catching up with reality.

***

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. I’m glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, click here:

December 22, 2022

An arms race on industrial policy is the last thing Europe needs

Making a fuss over America’s Inflation Reduction Act is gratuitous and counterproductive.

Read the full article at the Financial Times

December 19, 2022

Chartbook #181: Finance and the polycrisis (6): Africa’s debt crisis

On December 13 Ghana reached staff-level agreement on a $3 bn IMF credit package. In addition it is seeking to negotiate a 30 percent haircut with private creditors on tens of billions in bonds. Already in September Ghana’s 2026 eurobonds plunged to a record low of 59.30 cents on the US dollar. By the end of October yields had surged to 38.6 %, up from less than 11% at the end of 2021. Meanwhile, inflation is headed to 40 percent and the cedi is the worst performing currency not just in Africa but of all currencies in the world.

You could shrug and say that this is Ghana’s second IMF deal in 3 years and its 17th since independence in 1957. Plus ça change. But it is more than a national crisis. It is the latest sign that the entire model of market-based development financing is in crisis.

The fact that borrowers like Ghana find themselves in trouble at this moment is not surprising. The hiking of interest rates occurs in waves and whenever it happens it hits the weakest. We don’t call it a global dollar credit-cycle for nothing. This year, as the Fed has hiked, the average emerging-market dollar yield has doubled to over 9%. Debt issued by stressed frontier market borrowers has seen yields surging to 30 percent or more.

But to treat the news from Ghana as “just another predictable crisis”, is to trivialize and to fail to grasp the significance of the current moment.

Ghana is an important African success story. In recent times it has been the site of sustained efforts to improve labour practices and the terms of trade for peasant cocoa farmers. In 2020 its stress-free elections contrasted favorably to the democratic anxiety in the United States. Ghana has been praised for its efforts to extend health insurance to 70 percent of the population, topped up with cash benefits for the poorest. Accra boasts a vibrant fashion and design culture. The interior is touted as destination for adventurous trekking tourists.

An ample flow of money was key to this success story. And not just the volume of funding mattered, but how it flowed.

Up to the Millenium, the main form of lending to Africa was concessional bilateral lending by Paris Club members. That ended in the early 2000s with the Heavily Indebted Poor Countries Initiative backed by the International Monetary Fund and World Bank. That wrote down a huge slice of unpayable debt. In the aftermath, new bilateral concessional lending by the Paris group of creditor countries was reduced to a trickle. Instead, led by the United States they have provided support above all in the form of grants and development assistance. This is less encumbering than concessional loans, but it is also restricted in volume. In a substantial economy like Ghana, let alone an economy the size of Nigeria, grants and development assistance are unlikely ever to achieve transformational scale.

Meanwhile, lending by the World Bank and other Multilateral Development Banks has provided a relatively steady flow of funding. But the big new player in the development finance scene is China. At its peak in 2017 Chinese development lending was larger than that of the World Bank. China’s large-scale funding met much suspicion and has now run out of stream. Much of it has had to be renegotiated with stressed borrowers. Which leaves the question. What is the development vision that “the West” actually offers to the developing world? Over the last twenty years, insofar as the West has had a model of development funding, it has been one of public-private partnership: develop the financial infrastructure of borrowing countries so as to enable them to attract funds from private lenders on global markets.

source: @David_McNair

Since 2008 the surge in non-Chinese private lending dwarfs all other funding flows to Africa. In part it was driven by genuine development on the part of the borrowers. But, in the era of quantitative easing, it was also impelled by the search for yield in frontier markets. As QE is replaced by QT and interest rates in the US rise sharply, that funding model that is now in question.

The Ghana crisis matters beyond its immediate impact, because it was the poster child for this model of private finance. Ghana issued its first eurobond for $750mn in 2007 and has since become a leading example of a country financing development through private borrowing abroad. Of Ghana’s total public debt of US$55.1 billion (78% of GDP) in March 2022, 40.2% (US$28.3 billion) was owed to external parties. And of the external debt, about 57% was owed to commercial creditors. Amongst the big names currently holding Ghanian debt are Boston-based Fidelity that holds $94.5 million of Ghana’s dollar bonds. Goldman Sachs Group Inc. and PIMCO have $72.2 million and $68.5 million on their books respectively.

It wasn’t just hype. Ghana has one of the best educated labour pools in Africa and relatively good governance. It is the world’s second-biggest grower of cocoa and Africa’s No. 2 gold producer. It began exporting oil in late 2010. In 2011 growth peaked at 14% pa and rapid growth continued through the 2010s. But with hindsight the early 2010s were the crest of the boom. From 2014 the going for Ghana and other developing economies got rough. Headwinds included the spillovers from the slowdown in China and the 2014-2017 commodities price slump. The budget was thrown out of balance by spending ahead of hotly contested elections in 2012 and 2016 and the economy struggled with a power crisis that locals dubbed the ‘dumsor’.

Despite these difficulties, the administration of President Nana Akufo-Addo, elected in January 2017, initiated a major national development push. The government scrapped fees for high school students. The Ghanaian state also had to deal with an insolvent and fraud-riddled financial system. Between 2017 and 2019, the Bank of Ghana led a reform push that shut down banks, savings and loans, micro-financial institutions, finance houses, and investment institutions. To cushion the shock to financial confidence, the government raised another $3 billion in bonds to pay customers of the defunct banks and financial companies. In 2021, Accra embarked on the restructuring of the finances of the power sector. Crucially, it absorbed the unpaid power bills of Ghana’s state-owned enterprises onto the public balance sheet.

By 2019 the deficit had surged to such a degree that Ghana was forced to negotiate a deal with the IMF. Within months, the conditions of that program were then torn to shreds by the impact of the COVID crisis. Ghana’s situation is truly one of polycrisis.

The lockdowns and border closures of 2020 and the fall of oil prices, resulted in lost revenue to the Ghanaian government of US$2 billion. On top of that COVID-19 expenditures increased total government expenditure by US$1.7 billion, giving a total fiscal impact of almost US$4 billion in 2020. Meanwhile, the promised assistance from rich countries in the form of vaccines and financing failed to materialize.

With inflation surging and interest rates going up, it is little wonder that President Akufo-Addo spoke ominously of a confluence of “malevolent forces”. And this beleaguered situation only intensified in 2022. In February Moody’s downgraded Ghana’s sovereign debt from B3 to CAA1. The finance ministry responded by accusing the rating agencies of “what appears to be an institutionalised bias against African economies”. The government blamed a 50 per cent fall in the cedi on “speculators” and black marketeers.” As recently as October the President insisted that any suspicion of debt restructuring was far from the truth. Bondholders had nothing to fear. Ghana would prove the ratings agencies wrong and honor all its debts.

But the wheels were already coming off the bus. By the summer of 2022 Moody’s estimated that Ghana’s debt had reached 80 per cent of GDP and debt interest payments would take 57.7% of government revenue, which is second in the world only to Sri Lanka on 72.8%. The IMF puts Ghana’s debt-to-GDP ratio even higher at 90.7% compared to only 31.3% in 2011. At least $3.5 billion in loans and bonds come due next year. Bright Simons of the Imani think-tank described Ghana’s most recent budget as a “Frankenstein’s mash-up”.

Unable to access international markets, Ghana’s government has increasingly resorted to taking out domestic loans. But given soaring inflation it has been forced to offer interest rates of almost 30%. When the government risked defaulting on local debt, the central bank stepped in to provide funding thus jeopardizing its own legal lending thresholds.

Nor was the pressure coming only from the financial markets. Surging inflation has fed through to local business and consumers. In October, in the Ashanti region, which is normally loyal to the President’s New Patriotic Party (NPP) party, traders mounted strikes and jeered the Presidential convoy. The protests also extended to Accra’s commercial hubs. The Ghana Union of Traders Association demanded action to address the “free fall of the cedi”. Along with traders, drivers are a key link in Ghana’s economy. After mounting a series of protests earlier in 2022, Ghana’s drivers announced a 40 percent hike in fairs to make up for the spiraling costs of petrol and tires. Perhaps most worrying is the situation in farming where farmers have reduced acreage and switched crops in response to soaring fertilizer prices and the collapsing cedi. The worry is that this will lead to a shortage of maize and spiraling prices for consumers. Faced with this increasing dislocation and uproar, parliamentarians began calling for Finance Minister Ken Ofori-Atta, a former investment banker and Yale-SOM alumnus, to resign.

Finally, in November the government capitulated and announced that it would open talks with the IMF with a view to to securing $3bn in funding that would enable it to produce a coherent budget for 2023. To balance the books it also needed concessions from its creditors. The government wants a haircut and a suspension of interest payments on foreign bonds for three years. Domestic debt investors would be asked to exchange existing securities for new ones with a reprofiled schedule of interest payments rising from zero coupon to 10%. To restore creditor confidence the President is promising to impose savage fiscal discipline with a view not only to ending deficits but reducing debt to 55% of gross domestic product by 2028. To support the currency the Bank of Ghana is hiking interest rates fast. As a desperate emergency measure, vice president, Mahamudu Bawumia, announced that Ghana would require large mining companies to sell 20% of the metal they refine to the nation’s central bank, for local currency, allowing the government then to barter the gold for essential fuel imports. Meanwhile the government has hired Lazard Ltd, Global Sovereign Advisory and Hogan Lovells US LLP to advise it in the negotiations with the creditors. Some of the bondholders have turned to Rothschild & Co and Orrick, Herrington & Sutcliffe LLP as advisers.

***

The situation in Ghana is bad, but it is by no means alone. Whereas in 2008 the African continent was largely insulated from the shock of the global banking crisis, it is now, as a result of being more integrated into the global economy, feeling the pinch from global movements in prices and interest rates. Since 2020, Zambia, Chad, Mali and Ethiopia have either defaulted or entered talk to restructure their debt. Tanzania, Mozambique and Benin have attracted emergency support from the IMF.

Ethiopia, Africa’s second-most populous country with a population of 118 million people, requested a debt restructuring in early 2021. It has been held up by the civil war that erupted in November 2020.

Nigeria, on paper Africa’s largest economy and a major oil producer, ought to be one of the beneficiaries of higher oil prices. Earlier this year Nigeria’s Bank of Industry and Federal Government issued Eurobonds at only moderately increased interest rates. But Nigeria is hobbled in its ability to profit from the commodity market surge because its oil production is languishing at less than half the level it reached in early 2020. It has no refining capacity. The state budget is burdened by a fuel price subsidy that consumed $12 billion this year. The World Bank warns that by 2025 debt service could rise to 169% of government revenue. Plans to issue $950 million in debt on international markets were cancelled in May, due to unfavorable conditions. Ideally, Nigeria would borrow mainly on domestic markets, but at less than 15 percent the rates offered on local debt are less than inflation which is running at 21 percent, so debt offers attract disappointing bids. Finance Minister Zainab Ahmed is looking for ways to reprofile Nigeria’s debts. But no one wants to engage in humiliating debt restructuring ahead of the upcoming election.

Kenya also started 2022 planning to make a new issue, but cancelled a KSh115bn ($982m) Eurobond sale last June after yields doubled to 12%. Instead, it is now in talks with its Chinese creditors.

When the headlines announce that Ethiopia, Kenya and Ghana are all in trouble, that could be read as a series of national stories. But it is more than that. General narratives are fashioned out of particular cases and over the last 15 years Kenya, Ethiopia and Ghana have been amongst the most important success stories of the African continent. The current rash of crises puts that entire narrative in play.

Narratives are not merely window-dressing. They matter, because they fuel optimism and sustain belief, which infuses the assessment of analysts and credit rating agencies. Narratives are amongst the tools with which capital allocators manage the uncertainty inherent in any investment, but which is particularly intense in “frontier market” settings. Every investment implies a narrative. A crisis of the narrative thus puts the future in doubt, in every sense.

You might be tempted to say that we are better off not believing in stories. Instead, it is better to face realities. If debts are unsustainable, what we need are restructuring and a concerted effort to work out realistic funding terms.

Bad debts contracted for failed project risk becoming an albatross. If they cannot be paid, the one thing we know about debts is that they should be written off. The creditors take losses. The borrower suffer a loss of credit rating and then you reevaluate. This is not aberrant. It is normal. It need not be confrontational. As Ghana’s Deputy Finance Minister John Kumah reassured the press, there was no question of Accra unilaterally defaulting. “We know our bondholders, it’s not like it’s a big market out there. So it’s a matter of just constructing discussion and seeing how best we can all come to a position that protects either side and save the economy.” The question, of course, is who pays the the price. How large is the haircut imposed on the creditors? How brutal is the adjustment required of the borrowers? And how attritional and damaging is the process of restructuring itself?

In 2020 the G20 proposed the Common Framework for coordinating bilateral official creditors when it becomes clear that debt is fully unsustainable. But to enter on that process was judged by most borrowers to be too dangerous and uncertain. So far there are only three countries desperate enough to want to entrust their fate to the Common Framework, all of them are in Africa – Zambia, Chad and Ethiopia.

And beyond the resolution of any particular debt crisis the next question that must be top of the agenda is simply: what comes next? If debt is not sustainable, how is Africa’s urgent and huge need for capital to be met? The current level of poverty across much of Africa and the pressure of population growth can make calculations of debt sustainability and long-term viability seem quaint. Africa has no long-term, sustainable future without investment.

Ghana illustrates this pressure in microcosm. At independence in 1957, at the beginning of its trajectory of repeated renegotiations with the IMF, Ghana’s population was roughly 6 million. Today Ghanas’s population is 33 million, more than five times larger. Ghana’s capital Accra is now one of the hubs in a giant conurbation that stretches from Abidjan in Ivory Coast to Lagos in Nigeria. This huge and rapidly growing population desperately needs capital investment to meet basic needs, let alone keep up with rapidly-developing Asian economies.

Once Africa and Asia shared the condition of poverty. Increasingly, that is no longer the case. Of the people worldwide facing acute food insecurity at the end of 2022, two thirds are in sub-Saharan Africa – 123 million people or 12 percent of sub-Saharan Africa’s population. Of that desperate group, one-third have become acutely food insecure since the start of the pandemic in 2020.

In the areas of most acute deprivation, chronic poverty and environmental shocks compound each other. The four-season drought in the Horn of Africa is resulting in what the World Food Programme has declared to be the world’s worst food emergency. And the distress is further compounded by state-failure and armed conflict, notably in DRC, Ethiopia and South Sudan.

To handle such challenges, Africa need competent and capable states and they need funding. Take, for instance, the case of Kenya.

While it is struggling to balance its books, Kenya’s soldiers are being heavily recruited, amongst others by France, as a contribution to the East African Community Ragional Force in DRC. The intervention is aiming to stabilize parts of DRC occupied by the M23 – which is likely backed by Rwanda. Contributors to the joint intervention pay for their contingents themselves. The budget currently planned by the Kenyan ministry of defence for the intervention is estimated to be around €37m ($38m) for the first six months but it could easily rise to €50m over a year if the operation is extended. Kenya also contributes to Amisom, the African Union’s peacekeeping mission in Somalia. But Kenya’s financial situation is precarious and it is engaged in talks with both the IMF and its Chinese creditors. So concerning is the situation that it has been raised with the G7 and the EU, which may use the European Peace Facility (EPF) to help to pay for Kenyan peace-keeping.

For all the short-term funding difficulties, the question of development cannot be dodged. The ambition to turn “billions” of dollars of development lending into “trillions” that was announced in 2015 in conjunction with the Sustainable Development Goals, was not mere rhetoric. Only investment on that scale can match the needs of an African population that by 2050 is expected to reach 2.5 billion.

***

How are such sums to be raised? The question is daunting in its immensity and its implications. It would be utterly presumptuous to opine about it in short hand here. Instead, let us refer to what is surely the most constructive development agenda of the current moment, the Bridgetown Agenda championed by Prime Minister Mia Mottley of Barbados and forcefully articulated by advisors like Avinash Persaud. This is commonly presented as an answer to the question of how to mobilize funding to address the climate crisis. But, as far as Africa is concerned, the question of building a sustainable energy infrastructure is at the heart of the problem of development. Climate and development are one and the same problem. So the Bridgetown Initiative may serve as a framework for thinking about sustainable development more broadly.

The Bridgetown Agenda has many facets and aims at a comprehensive redesign of global financial architecture, but for our purposes the key point is the functional assignment that Initiative proposes between funding streams and types of sustainable development challenge.

The limited amount of grant funding, exponents like Persaud argue, should be focused on providing generous and timely relief in situations of acute crisis – natural disasters, health crises, the most urgent needs of postwar reconstruction and survival.

For adaptation challenges and their equivalents in other areas of development e.g. health and education, areas where investment is essential to ensure resilience and provide a platform for growth, but will not generate an immediate revenue stream, the most appropriate form of finance, of those available at scale, are concessional loans.

Presumably, loans might fund either specific projects or deficits incurred in the course of making generational investments in health and education. But whether they are contracted at home, in local or foreign currency, they beg the question of repayment.

The same goes for financing of those sectors where revenue streams are forthcoming, but risks are too high to allow unassisted private financing. In this case, to ensure that funding is available, development bodies should offer derisking by means of guarantees or first loss involvement. The terms of those deals will need to be carefully scrutinized to ensure an equitable distribution of risk and reward between all parties and they too pose the question of debt service. Derisking must not imply depoliticization. The devil, as critics like Daniela Gabor powerfully remind us, is in the detail.

Justice and the urgency of the situation dictates that there should be a large contribution at all three stages from funding bodies in Europe and the US in the form of grants, concessionary finance and derisking. But, strengthening African capacity is ultimate goal and this is why so many expert commentators place so much emphasis on the question of state capacity and above all fiscal capacity.

A fiscally competent state can borrow because it can tax. The acid test is the ability to borrow in your own currency whether from foreign or domestic lenders. Expanding local capital markets has been a priority of recent development thinking. This goes hand in hand with expanding local banking systems, which as in the global North, are often deeply entangled with public debt. In Ghana the banking sector holds half of the country’s domestic debt. In good times this is an engine of financial expansion as in the financial history of the West amply demonstrates. But in bad times it risks accelerating a doom-loop in which declining sovereign credit ratings drag down the financial standing of the banking system. The key is to ensure steady growth, feeding an adequate tax base.

For many African states this is a huge challenge. As David Pilling writes about Nigeria in the FT:

One measure of the trust that a nation’s people have for the state is the amount of tax they are willing to pay. However grudgingly, under an unwritten social contract people agree to part with a share of their income in the belief that the state will spend it more or less wisely. The public goods provided range from schools, hospitals and roads to police, national defence and the running of the government itself. Everyone benefits from improved services, a better educated and healthier population, safer streets and protected borders. On this measure, trust in Nigeria’s state is at rock bottom. According to the IMF, the country collected 6.3 per cent of gross domestic product in tax in 2020, the lowest proportion in the world, and far below the bare minimum the World Bank says is necessary for a functioning state.

Nigeria’s tax to GDP ratio is one fifth that of the average OECD country. More relevantly it is one fifth that of Tunisia and one fourth that of Morocco.

Source:

Remarkably, Nigeria’s tax-take as a share of GDP actually decreased between 2010 and 2010. By contrast, that of Ghana increased, by roughly 3 percent. It isn’t enough.

Of course, it is true that it is easier to build a tax state at higher levels of income. But comparative data show the range of performance across Africa at similar levels of development.

Ghana does better than Nigeria, but it needs more. In Accra the Institute for Fiscal Studies argues that Ghana could raise an additional $47 million through extending personal income tax to the informal sector. It could raise $157 million in property tax and abolishing tax exemptions would bring in $790 million. But the biggest slice would be obtained by taking a 55% share of the revenue of the extractive sector, equivalent to the share that Nigeria takes from its oil industry or Botswana takes from mining. That would yield $4 billion. The reason that Ghana’s share of extractive revenues is so low, according to the IFS, is the small ownership share of national resource companies compared to international investors.

The quid pro quo, according to Ghanaian reformers, should be an all-out effort to ensure prudent management of public finance. A recent Auditor-General’s report identified about $1.8 billion worth of irregularities in public finance. As Adu Owusu Sarkodie puts in The Conversation:

When these irregularities are checked, the government will gain the confidence and support of the citizens. … Unfortunately, the pervasive and deeply entrenched nature of the country’s Fourth Republican clientelist politics which manifests in a ‘winner take all’ approach to governance has often distorted a much-needed national debate on what needs to be done and how it must be done

If we abstract from the 21st-century framing what every vision of sustainable development implies, is a giant transformation in political economy, a combined social and political transformation, centered on capital markets and the tax state. At other times and in other places, this might have been seen as the blueprint for a bourgeois revolution. Such a revolution entails the development of property right and markets, but public finances too are a critical arena of transformation and struggle.

What Joseph Schumpeter wrote in his essay “The crisis of the tax state” about the European state in the aftermath of the gigantic financial effort of World War I, is no less true for African states faced with the awesome development challenges of the 21st century.

“fiscal measures have created and destroyed industries, industrial forms, and industrial regions even where this was not their intent, and have in this manner contributed directly to the construction (and distortion) of the edifice of the modern economy and through it of the modern spirit …. The spirit of a people, … its social structure, the deeds its policy may prepare … all this and more is written in its fiscal history. He who knows how to listen to its message here discerns the thunder of world history more clearly than anywhere else.”

****

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. I’m glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, click here:

December 17, 2022

Chartbook #180: Do you ski? The political economy of snow, slopes and skiing

The ski business worldwide.

Source: Vail

Do you ski? As a matter of lifestyle and recreational distinction, it is a question up there with “do you play golf?” or “do you play chess?”.

Of course, if you are born in cold regions of the world, or in the mountains, the answer, regardless of social class and cultural milieu, is likely, “yes, of course, I ski”. For everyone else, it’s a telling question indeed.

For those mulling the seasonal question, Ones and Tooze is to hand this week to help you sift through the noise, with an episode on the war in Ukraine and the economics of snow.

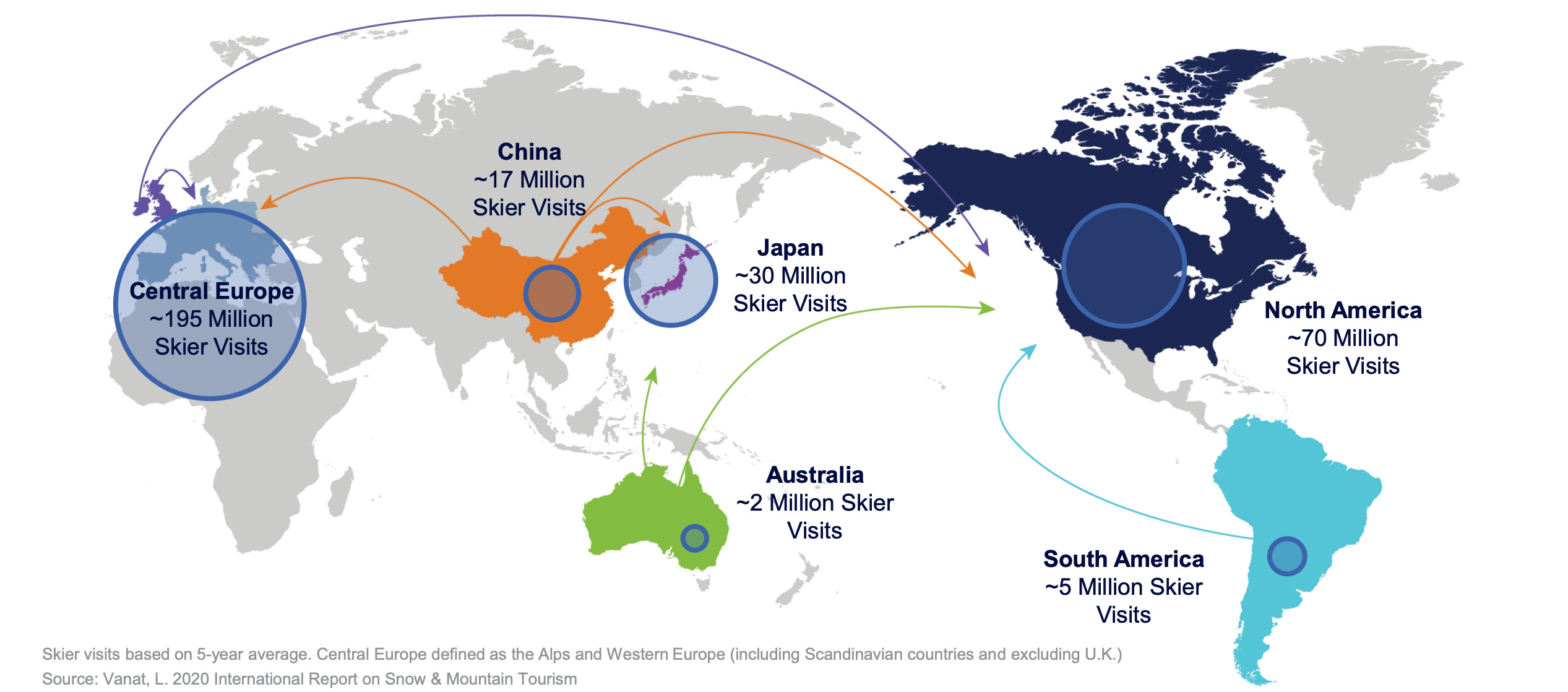

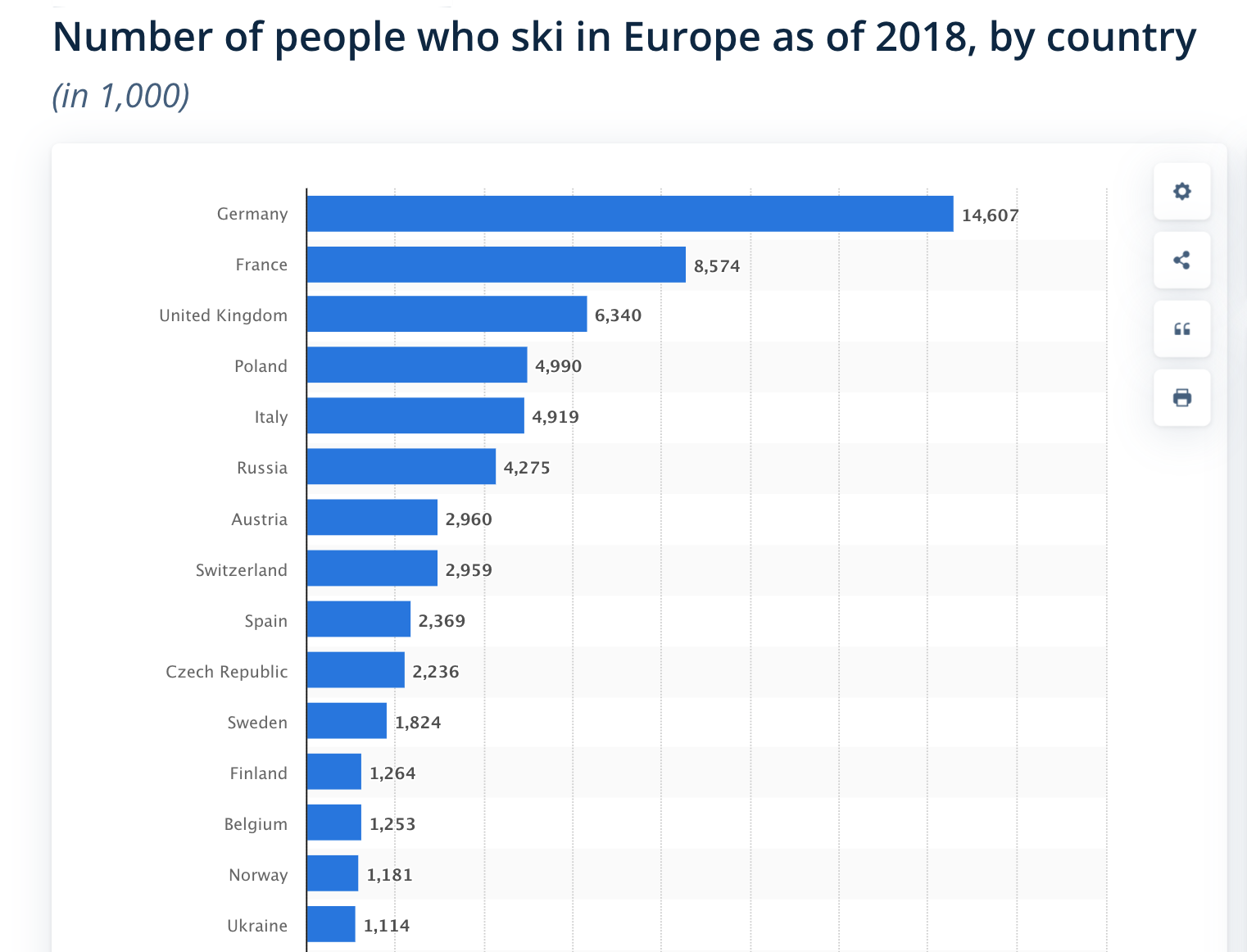

https://embed.podcasts.apple.com/us/p...Of 8 billion total population worldwide, it is thought that about 135 million people regularly ski, so about 1.5 percent. There are c. 2000 alpine skiing destinations in the world with the vast majority in North America, Asia and above all Europe. Unsurprisingly, given that the cost of even a short skiing trip can easily run into many thousands of dollars per person – allowing for travel, lodgings, ski pass and equipment – skiers are an affluent group. Roughly 20 million of the world’s skiers in any one year are in the US, if you include snowboarders. 15 million or so come from Germany.

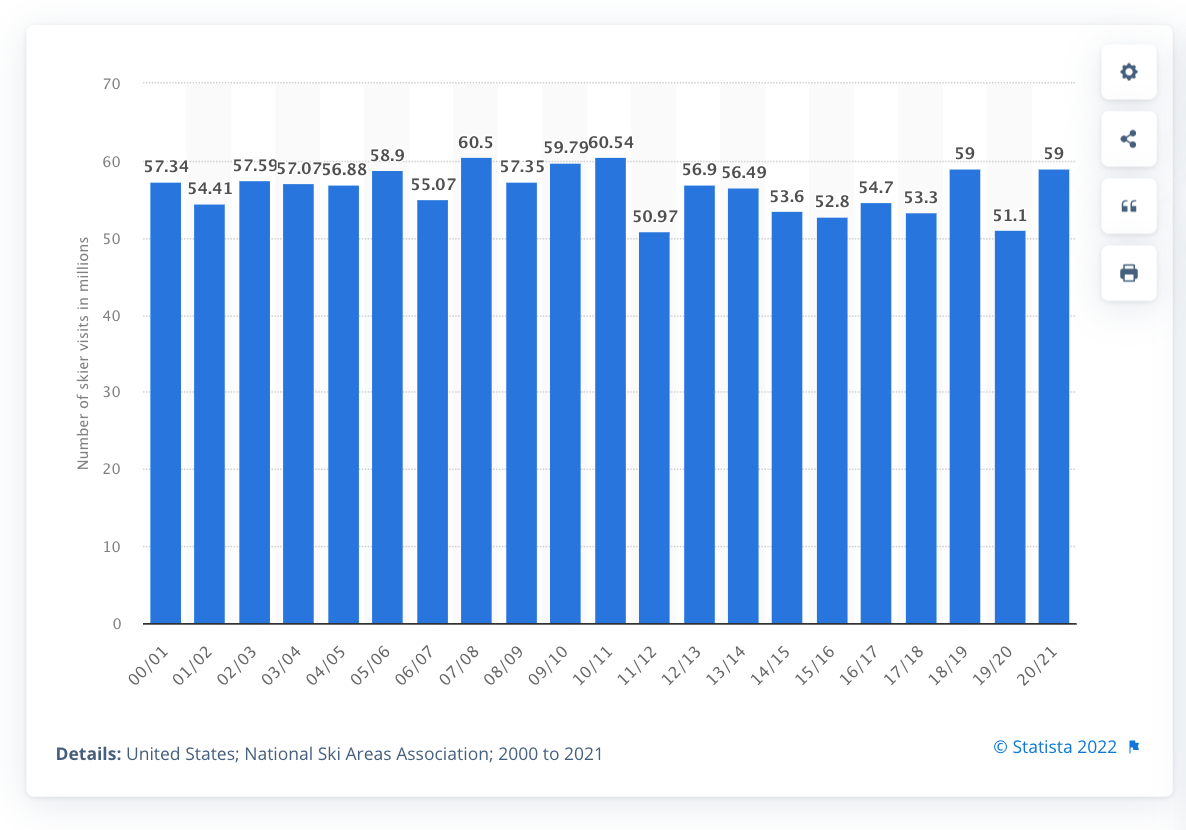

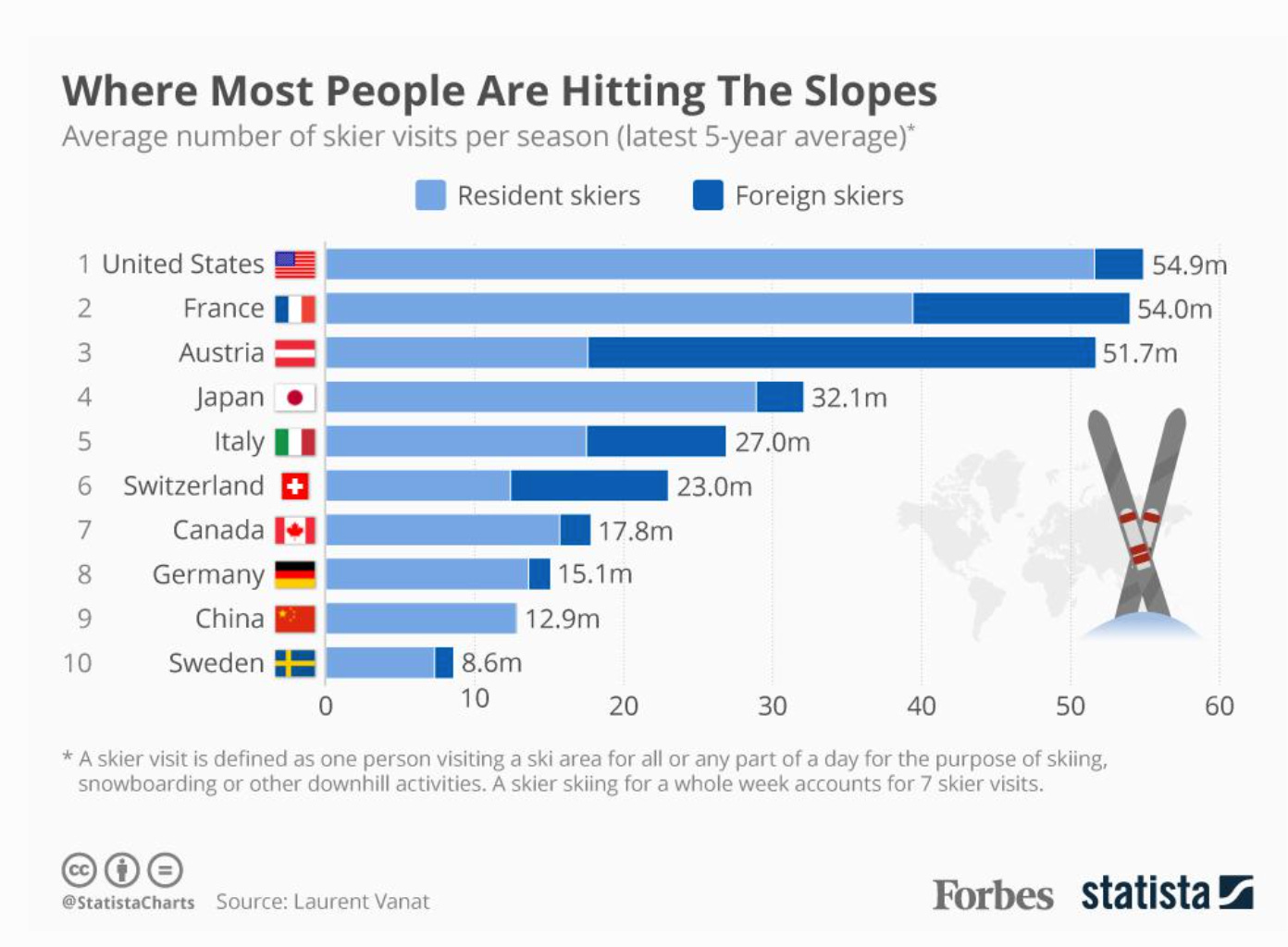

Despite economic growth, the number of skiers worldwide is increasing very slowly. Globally, the annual number of skier-days has plateaued at around 400 million. The Alps account for 43 percent of all skier days globally and Europe is by far the largest alpine market, with typically around 210 million skier days a year. In the US, the number of skier-days has been static between 50 and 59 million per annum for the last 20 years.

Source: Statista

In a world in which both population and incomes generally trend up, a static number implies that participation in skiing is trending down. In some markets, notably in Europe, the downward trend in participation is very pronounced indeed. Skiing is, in short, becoming more, not less exclusive.

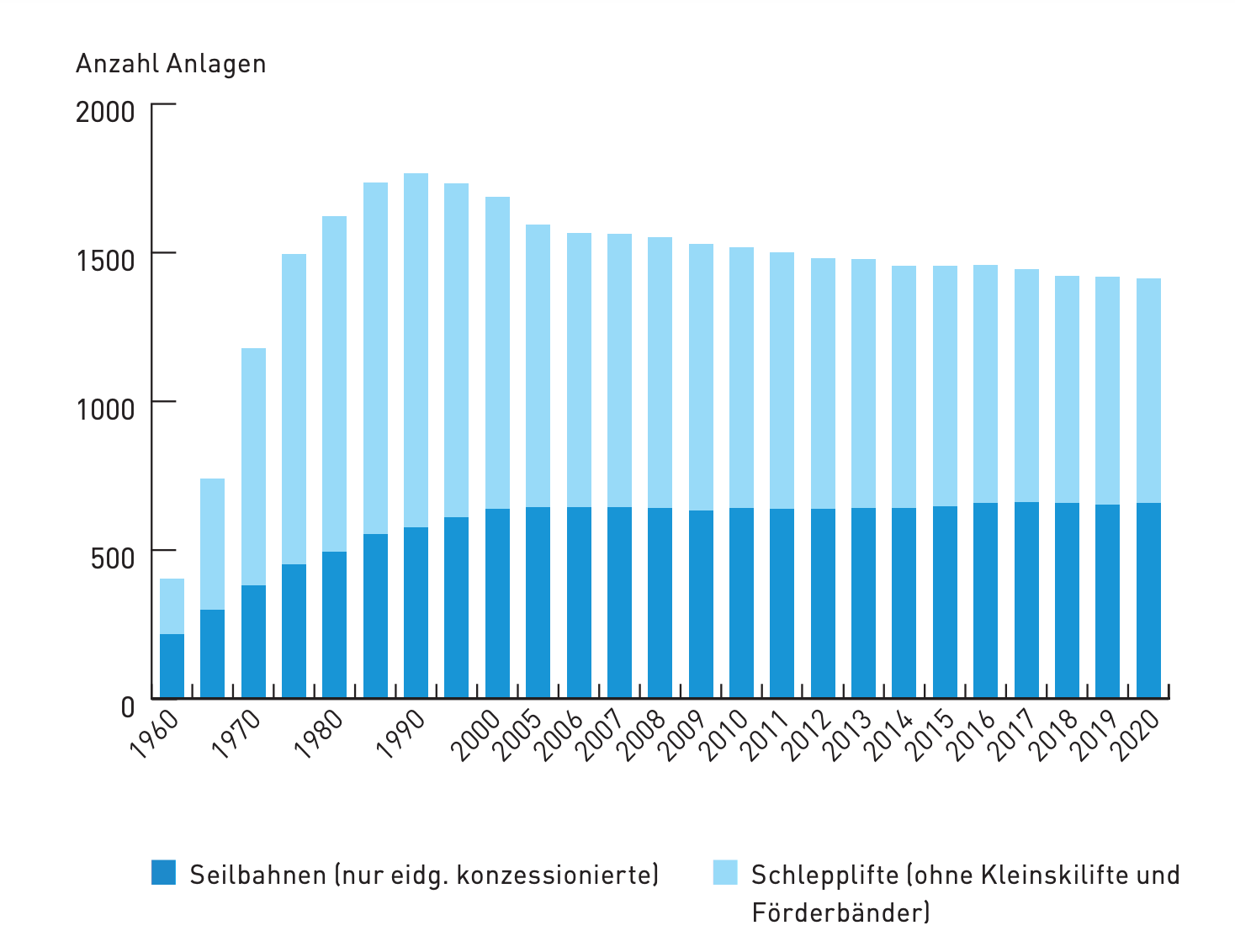

This is an effect of changing habits. Skiing is seen as a bit of a period piece, a sport that “was once” chic. Nor is this merely a matter of fashion perception. It reflects the actual history of the industry. Take, the history of the ski lift system in Switzerland.

Source: Fakten und Zahlen zur Schweizer Seilbahnbranche

The period of growth in the Swiss ski resort industry was between the 1960s and the 1990s when capacity increased fourfold. Since then it has been static. Old systems are being improved and maintained, but no new lifts are being built. In the US there is more expansion. But the point stands. The boom in skiing happened thirty to fifty years ago. It shaped two generations of enthusiasts, who presumably pass on their passion to their children, but is not driving dynamic growth in the 21st century.

This keys with my own biography. Having recently moved to Germany, in the early 1970s my parents took us on one fraught outing to the slopes, where, even as a child, I remember a lot of anxious talk about money and where I discovered a painful and embarrassing skin rash brought on by exposure to high levels of UV light.

You might wager that the current plateau in the skiing business had something to do with climate change. A warmer world means that there is less snow to go around. More on that below. But, beyond lifestyle currents and the natural environment, the factor we should not ignore is political economy and corporate strategy. A market will remain static if there is no reason to invest in expansion, if the status quo is profitable for the major players.

The political economy of winter sports is not a large field. But in researching Ones and Tooze this week, I stumbled across a rather brilliant piece of work by a student at UT Austin, Adam L. Roossien, whose 2017 undergraduate thesis, “Industry v. Lifestyle: A sociological study of downhill snow skiing in North America” opened my eyes to a facet of global capitalism I had never considered before. Thank you Mr Roossien! Thank you to google scholar for serving up such excellent stuff!

You might think of the ski industry as epitomized by rustic Swiss chalets, cute mountain villages, glamorous “ski instructors”, a staple of 1970s erotic fantasy, tingling apres-ski and sun-burned young folk in the surfer/skateboarder/snowboarder vein. Roossien’s essential insight is that the industry is far better understood as an example of capitalist monopolization. As he points out, between 2000 and 2017 “the price of downhill snow skiing has risen nearly 200%. Over the last five years, this price escalation has picked up, and the price of downhill snow skiing has risen 75%.” To paraphrase Warren Buffet, the business logic is not so much one of building moats, but of buying mountains.

Mountain slopes are a limited resource. In Europe great resorts like Val d’Isère began to be developed in the interwar period. In the thinly populated mid-West of the United States, the slopes were prospected a generation later. This, for instance, is how the story of the Vail resort is told:

Vail Resorts was founded as Vail Associates Ltd. by Pete Seibert and Earl Eaton in the early 1960s. Eaton, a lifelong resident, led Siebert (a former WWII 10th Mountain Division ski trooper) to the area in March 1957. They both became ski patrol guides at Aspen, Colorado, when they shared their dream of finding the “next great ski mountain.” Siebert set off to secure financing and Eaton engineered the early lifts. Their Vail ski resort opened in 1962.[2]

Today, ski resorts are in regions tightly protected by national parks and nature reserves. You cannot build new resorts. Corporate interests have taken advantage of this tight regulation to establish dominant positions in the two largest Alpine ski areas in the world – the US and the French Alps.

Roossien’s muckraking thesis is an American one, but the strategy appears to begin in France with the Compagnie des Alpes, founded in 1989 and establishing a dominant position in the best-known French resorts – including Tignes, Val d’Isèere and Chamonix.

In the US it is Vail that has expanded since 1996 to establish an overwhelmingly dominant position. Along with slopes of Vail itself, the Vail Corporation also owns Beaver Creek, Breck, Park City and Whistler. Depending on the measure used, Vail controls 40-50 percent of the skiing market in the United States.

Vail’s vision is to own as many of the best mountains, slopes and resorts as possible, raise these to a high level of high-priced service by investment and then to feed demand for high-profile glamorous destinations from more local and regional resorts. To warrant billions of dollars of investment in a high-end and exclusive leisure segment, the corporate strategy is to turn unpredictable revenue from ski lift passes, purchased as and when, into a business-model based on advanced commitments. To do so, in 2008 Vail introduced the EPIC ski pass that gives access to large part of its network. In exchange skiers make an advanced and non-refundable commitment to the purchase of a pass that now costs in the region of $1000 per season.

The risk of bad weather or changed holiday plans is thus transferred from the company to the purchaser of the pass. As Vail describes it in a 2022 investor presentation.

“Our North American season pass program has grown dramatically over the past three years as we have focused on our core strategy of shifting guests from lift tickets into advance commitment to drive stability and long-term value for the business. … We expect to have approximately 2.3 million guests in advance commitment products this year, generating over $800 million of revenue and representing over 70% of all skier visits committed to our 40 North American and Australian resorts in advance of the season in a non-refundable pass, an increase of over 1.1 million guests in the program from the 2019/2020 season, including all pass products for our North American and Australian resorts.

More broadly Vail has re-envisioned the resort business as a data-driven subscription-based business model where the aim is to know as much as possible about the high-income, high-net worth segment and tie them into regularly annual down-payments on ski passes. Currently, Vail boasts of having data on over 22 million skiers in the US and estimates that it covers 53 percent of all North American destination guests.

The result is to turn skiing into an increasingly corporate, exclusive pursuit. This may be profitable, but Roossien’s thesis is that it is ultimately a model that is destined to self-destruct.

… Vail’s corporatization (of skiing) is leading to the severe marginalization and destruction of snow skiing subculture. Due to downhill snow skiing’s foundational dependence on its rich and distinct subculture, this cultural destruction is causing a deterioration of the sport itself.

Interestingly, Vail seems to be well-aware of the narrow socio-cultural base of its market segment in the United States. This is why it aims for long-run global expansion. It is targeting Europe, where it is attracted by the “broader demographic appeal of skiing relative to North America”, and Asia, where it sees huge growth potential beyond the bounds of North American ski culture. In Vails’ corporate vision, expanded and upgraded Japanese ski slopes will meet mounting demand from both Australia and China.

In 2022, hanging over any discussion of snow is the question of global warming. Even under more normal conditions, weather was always a risk factor for the ski business. The only guarantee of snow is altitude and correct positioning on mountain slopes to catch precipitation, but higher altitudes makes resorts less accessible and more expensive to maintain. Climate change makes these risks even more serious. The European Environment Agency reports that the length of snow seasons in the northern hemisphere has decreased by five days each decade since the 1970s and the Alps are warming faster than practically anywhere else on earth.

The answer, increasingly, is the large-scale deployment of snowmaking machinery that allows slopes to be brought into use and kept going more reliably. In addition resorts engage in “snow farming”, to build up drifts, and “snow grooming” to maintain attractive conditions for skiing.

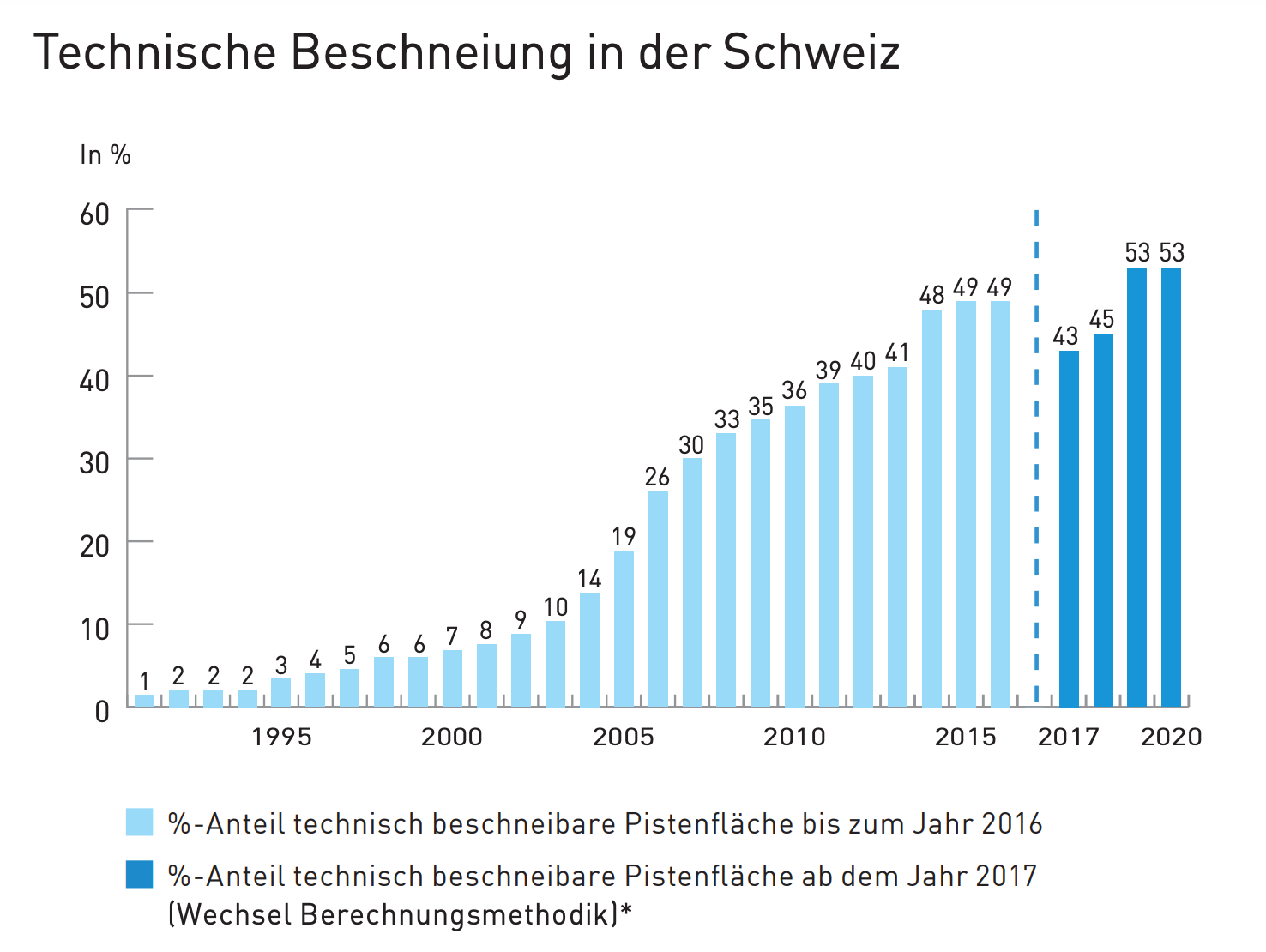

The first snow cannon was invented in the early 1950s and resorts in the Catskills became the first in the world regularly to use artificial snow. By the 1970s snow cannon were in widespread use in Europe as well and since the early 2000s there has been a huge surge. Here are the numbers for the share of Swiss slopes that can be provided with “technical snow”.

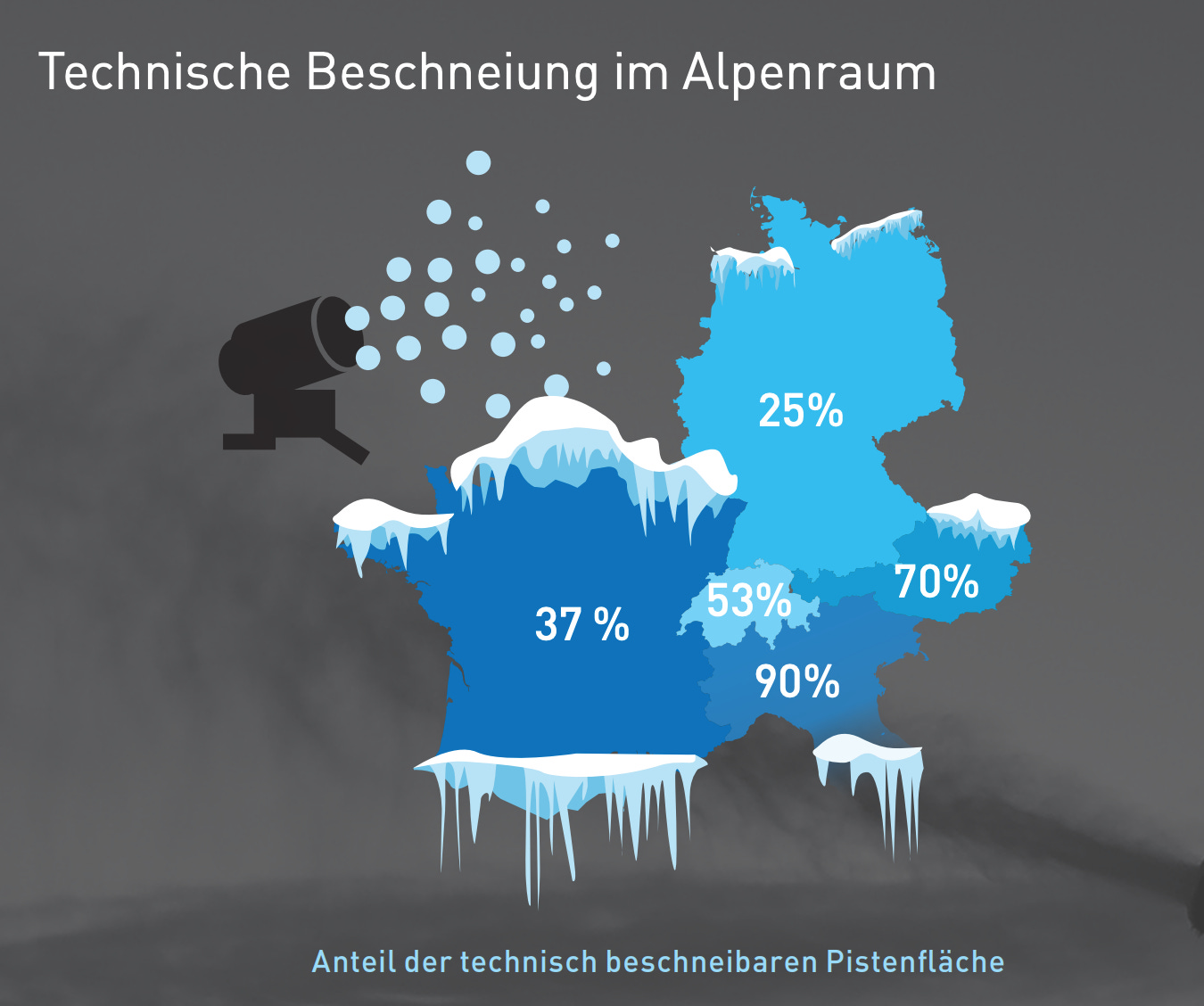

Currently, Switzerland has a stable share of 50 percent of its slopes that are worth maintaining with artificial snow. That places it between the German and French slopes, which tend to rely on natural snowfall and the Italian Alps where snowmaking equipment was introduced in the 1980s and 90 percent of the slopes are today maintained with artificial snow.

Since 2000 none of the winter Olympics would have been possible without artificial snow and snow farming.

FYI: Snow canons are artificial devices and they are bad news for the environment, but they are not quite the nightmare one imagines. Crucially, they do not involve, as you might fear, gigantic amounts of outdoor ice-making, as in the horror vision of “ski slopes in the desert”. Standard snow canons, are operated in low temperature environments where water freezes naturally. By pumping water and dispersing it as a spray, they increase the cooling effect through evaporation, and create a mist that freezes into artificial snow crystals. The electric power demands are modest, essentially for pumping and dispersing the water spray and if the electric power is supplied from renewable sources e.g. alpine solar, then the main concern is the gigantic consumption of water. What you are replacing with artificial snow is less the low temperatures than the lack of precipitation at key moments in the year. Nevertheless, in the Alps in particular, the future of skiing is the future of a giant environmental engineering project.

That innocent seasonal question, “do you ski?”, does indeed carry a lot of weight.

****

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. I’m glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, there are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.Several times per week, paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images. To get the full Top Links and become a supporter of Chartbook, click here

December 15, 2022

Ones & Tooze: Ukraine So Far

Adam and Cameron look back at the first 10 months of Russia’s war in Ukraine and its economic impact around the world. The also discuss the economics of…snow—just in time for the winter.

Find more episodes and subscribe at Foreign Policy

December 12, 2022

Chartbook #179 Finance and the polycrisis (5) The hunt for the next market fracture.

What will bend, what will break? That is the question about the global financial system that I have been asking in this mini-series on Chartbook.

The same question was taken up a week ago under the title “Financial instability: the hunt for the next market fracture” by a crack FT-team consisting of Eric Platt and Kate Duguid , Tommy Stubbington and Jonathan Wheatley and Leo Lewis.

The piece is so close to my own analysis that it caused me to pause and to compare notes. How do we think and write about stresses in the global financial system now?

Eric Platt opens the compilation with a short overview. His opening line aptly summarizes the common sense: “After a decade of falling interest rates and central bank largesse, global financial markets are facing a reckoning.”

This line is echoed by a roundup in the Economist.

The plunging markets are the result of a decades-old macroeconomic regime falling apart. High inflation, not seen in the rich world since the 1980s, is back, which in turn has brought to an end ten years of near-zero interest rates. As a result, the rule book of investing is being rewritten

Whereas the Economist goes on to assess portfolio allocation choices under the new circumstances, the FT team is more focused on the immediate anxiety of market fragility and as Eric Platt explains that is above all a matter of liquidity.

Soaring inflation is being met by rising interest rates, the slowing of central bank asset purchases and fiscal shocks, all of which are sucking liquidity, the ability to transact without dramatically moving prices, out of markets. Violent, sudden price moves in one market can provoke a vicious loop of margin calls and forced sales of other assets, with unpredictable results.

That in turn makes market participants very jumpy. In the words of one interviewee they start trading on “impulse”. And in our world of the polycrisis there are plenty of “impulses” to move the markets. As Platt summarizes it:

Disparate shocks — like the closure of the nickel market in London, structured product blow-ups, the bailout of European energy providers or the rapid pensions crisis in the UK sparked by turmoil in the country’s government debt prices — are being scrutinised as oracles of wider dislocations to come.

This strikes me as a fairly characteristic statement of the polycrisis condition.

Highly disparate disruptions, which are themselves the result of structural factors (e.g. reorganization of the UK pension industry), political decisions (Trussnomics) and macroeconomic policy (Bank of England policy) combine with the broader unwinding of the familiar lowflation setting against the backdrop of pandemic-recovery (oof the polycrisis stretches sentence structure) to leave market participants trying to figure out what is what. As Platt summarizes it, they are left asking the question: How does the clutch of disparate shocks we are experiencing in the current moment, relate to further dislocations that will be wider and are yet to come?

You might be tempted to say that this is the situation of every actor in modern history. But as The Economist points out, for several decades investors have in fact been able to operate within a framework that was defined by the mantra of TINA – There is No Alternative (to a risk-on strategy of yield and growth-chasing in a lowflation zero-rate world). Now we are in a world of TARA – There is A Real Alternative.

So, at least as far as recent decades go, this sense of disorientation is new. But how historically unique is it?

Is the current sense of polycrisis merely another symptom of the breakdown of neoliberalism, TINA etc etc? That was the case made to me recently by Paul Krugman. I will return to that in a future post.

In the mean time let us focus on the present and the question of what might break. Following Platt’s introduction, the FT essay consists of a series of short pieces by each of the contributors.

European repo markets – Tommy Stubbington

US Treasury market illiquidity – Kate Duguid

Japanese government bond market dysfunction – Leo Lewis

Stuck in (corporate and private credit) – Eric Platt

Chartbook #174: Finance and the polycrisis (4) Fed effects & European corporate bond market.

EM market defaults – Jonathan Wheatley

It’s a good list. I have many of the same items on my worry list too. But I also wonder whether it is significant that it is a list rather than a single “integrated” essay, as in The Economist presentation. Is the list a characteristic response to the polycrisis? Is that one of the things that triggers intellectual dissatisfaction with the polycrisis term? That it seems like a “laundry list”.

Lists lack structure. They beg the question of order and weighting. What is the underlying principle that organizes the separate points? Are they an expression of our mental incapacity to satisfying synthesize or to discern the deeper underlying logic? Are they, indeed, something worse, a failure to face up to the stark fact that at the root of everything there is one basic causal driver? Capitalism, for sake of argument. To that extent is the “baggy” (not to say carrier bag) theory of polycrisis an ideological snare, a failure of intellectual backbone, of moral fibre on the part of the analyst?

Obviously, I think not. In fact, I’m persuaded by the opposite point of view. If you are not willing to face the “baggy”, inchoate nature of our current situation, if you are not willing to take seriously the possibility that our situation is historically novel (as in a product of the “great acceleration”, of which there is a dawning awareness in social and environmental sciences since the 1970s etc etc) and that this fundamentally challenges our existing frameworks of analysis (as grasped amongst others by Ulrich Beck), then you are involved in a kind of escapism that may turn out to be dangerous. But let’s come back to that on another, more leisured occasion.

Let’s pivot, as we must in this day and age, from broad considerations of the anthropocene and the polycrisis to more technical issues of macrofinance. Because, as you would expect, there are some really interesting features in the FT’s list.

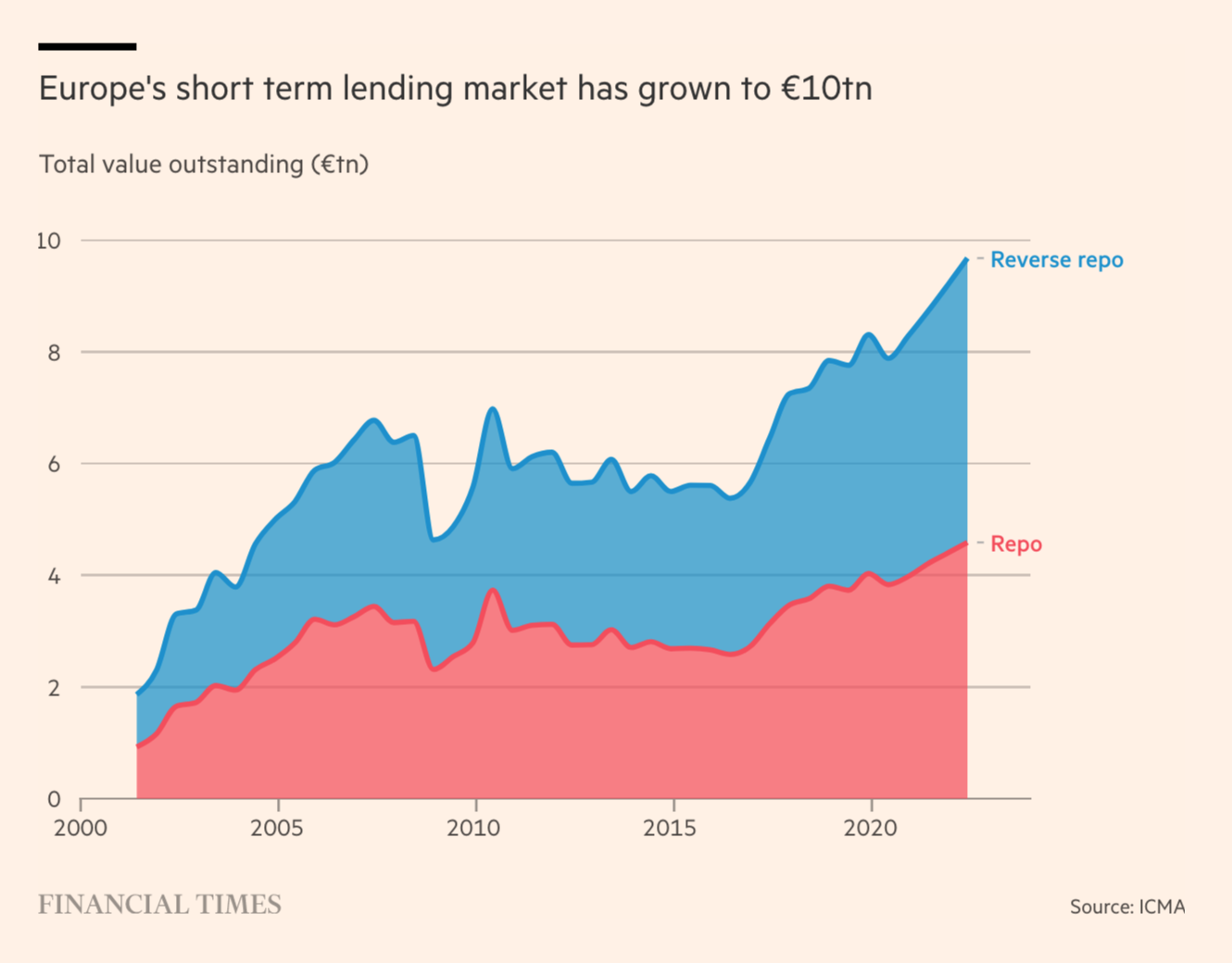

I did not have the Eurozone repo market high enough on my list of worries. One thing that Tommy Stubbington highlights is just how big the Eurozone repo market has become.

The issue in the repo market is that quantitative easing purchases by the ECB means that there is not enough super safe, short-term government debt in private hands for large-scale investors to use as the basis for short-term cash loans. Excess demand for that category of debt means that prices are high and yields low counteracting the effort by the ECB to raise interest rates to counter inflation. The result is an unstable tug of war. The securities industry is lobbying for the ECB to ease the tension by introducing the kind of standing reverse repo facility that the Fed put in place in 2013 with which to supply the US Treasury market with a flexible supply of collateral. But the ECB has actually pushed back against the idea. Watch this space.

On the other side of the Atlantic the Treasury market is not looking healthy either. I reviewed the wide-ranging debate about Treasury market conditions in Chartbook #172. In her contribution to the FT roundup Kate Duguid nicely summarizes the position by stressing that structural distortions may now be so severe that it may not even take a major shock, as in 2020, to unleash a self-propelled round of fire sales.

“… in the event of a crisis, structural problems may exacerbate any sell-off, as was seen in March 2020. But the current liquidity issues in the Treasury market also mean it may not take an event as disruptive as the onset of a global pandemic to spark a big sell-off. If some mis-step prompted a dash for cash, investors could have trouble selling Treasuries, leading to huge swings in prices, producing big enough gaps in prices to lead to forced selling.”

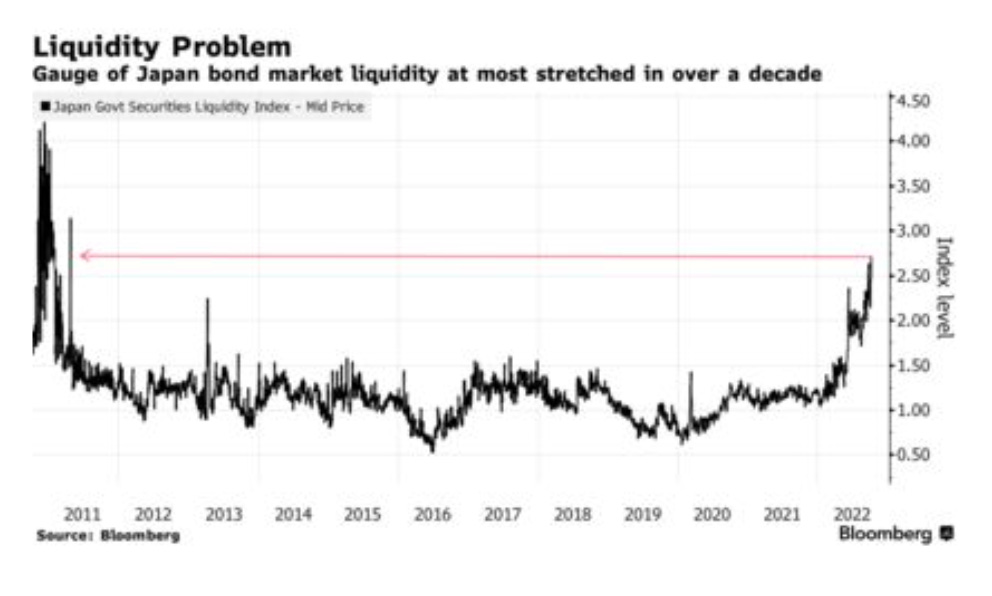

Both the Eurozone and the US sovereign debt markets are clearly sticky right now. But if you want to see a government bond market that is altogether ruled by central bank policy, look to Japan. The Japanese market is dominated by years of yield curve control exercised by the Bank of Japan, which have driven interest rates to zero and held them there. The question here is if and when the BofJ might shift position. The interesting point noted by Leo Lewis is that there is a significant difference of opinion between Japanese and Japan-based analysts who remain convinced of the BofJ’s commitment, and foreign analysts who don’t find it plausible that the Bank of Japan can in the long run buck the global trend towards higher rates. Something has to give.

This year the Bank of Japan has engaged in bond purchases at a rate not seen since 2017. To ward off speculative attacks it has offered on occasion to purchase unlimited quantities of 10-hear Treasuries. As a result it now owns half of Japan’s government debt.

In the meantime Japan’s bond market no longer works like a “normal” market. What this means is that for three sessions strait in October the Japanese 10 year bond failed to trade at all.

“There is no incentive to buy the 10-year notes from a carry income perspective or for trading purposes,” said Ataru Okumura, a strategist at SMBC Nikko Securities Inc. in Tokyo. “It’s hard for investors to hold 10-year bonds for the longer-term as the sector being the BOJ’s yield curve target makes it expensive relative to other parts of the curve.”

As one market participant observed:

“I hope the BOJ will realize soon that it’s destroying the bond market,” said Ayako Sera, a strategist at Sumitomo Mitsui Trust Bank Ltd. in Tokyo. “It could at least stop conducting the fixed-rate operation every day once the Fed stops hiking rates.”

Even allowing for the exceptional circumstances in the 10-year bond market, which is where the BoJ concentrates its interventions, the overall liquidity in Japanese government debt has fallen to levels not seen for more than a decade.

In short, the major public debt markets of the world – US, Europe, Japan – are looking far from healthy. In addition there are concerns about the corporate debt market on both sides of the Atlantic.

I addressed the European corporate debt crunch in an earlier Chartbook in this series. Recently, Eric Platt and Harriet Clarfelt warned of the shock to the US junk-bond market. Issuance so far this year has fallen to levels not seen since 2008. At $101bn they are less than a quarter of the issuance of $464bn in 2021. This is hardly surprising in light of the collapse in prices.

Less debt issuance points to funding stresses for business. But that is what one would expect at this point in the business cycle. That is bending not breaking. As far as financial stability is concerned the big concern is that a fire sale dynamic might develop that would destabilize open ended bond funds. They remain one of the critical weak links in the global financial system.

Finally, Jonathan Wheatley, addresses concerns about risks in the emerging market economies. Currently, the credit rating agencies say that 26 developing countries are either at risk of default or already in default. This is alarming, but as Wheatley points. out the scale of the problem is not systemic. As Wheatley reports, the “15 countries with bonds trading at distressed levels in October made up just 6.7 per cent of the benchmark JPMorgan EMBI sovereign eurobond index”. This may be callous, but it is reassuring from the point of view of overall financial stability. As Wheatley points out, however, beyond the immediate crisis cases a more serious concern should be that contagion may spread to larger EM economies. Recently, Poland, Colombia and South Africa have all seen yields on domestic 10-year bonds rise to record levels.

In recent weeks, the market situation for the big EM has eased somewhat. Colombia has been welcomed back to the market. With all the talk of the Fed easing the pace of monetary tightening, is the worst of the shock over? It would certainly be nice to think so.

But, debt levels are high. After the initial shock of rates rising, the system will have to adjust to living at those elevated levels. In that scenario, the sustainability of the Bank of Japan’s position is a huge question mark. There are major institutional fragilities in repo markets and in open-ended investment funds. All three major sovereign debt markets are showing signs of dysfunction. And one thing we must count on is that there will be more shocks to come.

****

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. I’m glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button.

Several times per week, paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

There are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.To get the full Top Links and become a supporter of Chartbook, click here

December 9, 2022

American hubris

Great powers, both past and present, are haunted by three interconnected preoccupations: they are tempted by a sense of national superiority and claims to manifest historic destiny. Those pretensions tend to provoke fears of decline, which then give rise to projects of rebirth.

The European empires that once fancied themselves great, most notably the British and French, are extreme examples. As France decolonised after 1945, Charles de Gaulle made “grandeur” a watchword of national policy. For the British elite, despite the increase in standards of living, decline was an obsession throughout the postwar period. Under the sign of “cool Britannia” and Tony Blair’s embrace of Europe in the 1990s, that shadow lifted. But since the banking crisis of 2008 and the Brexit referendum of 2016, the question has returned with ever-greater force. While the Brexiteers promise a “global Britain”, the average standard of living in Britain is declining for the first time in modern history. Nationalist bluster about “Britannia unchained” obfuscates a cool-eyed and practical appraisal of Britain’s actual position in the world.