Adam Tooze's Blog, page 10

December 2, 2022

Chartbook #177 Beijing’s tragic COVID dilemma

A dictator’s embarrassment is generally a cause for celebration. But what if it also threatens a national tragedy and a bona fide global problem?

Xi Jinping’s assertion of total personal control over the Chinese regime in October was an ominous turn in Chinese history and a cause for mourning amongst friends of liberty everywhere. Since 2020 a major anchor of Xi’s personal authority has been the “all out people’s war to stop the spread of the corona virus,” that has put “the people and their lives above all else” i.e. Zero Covid.

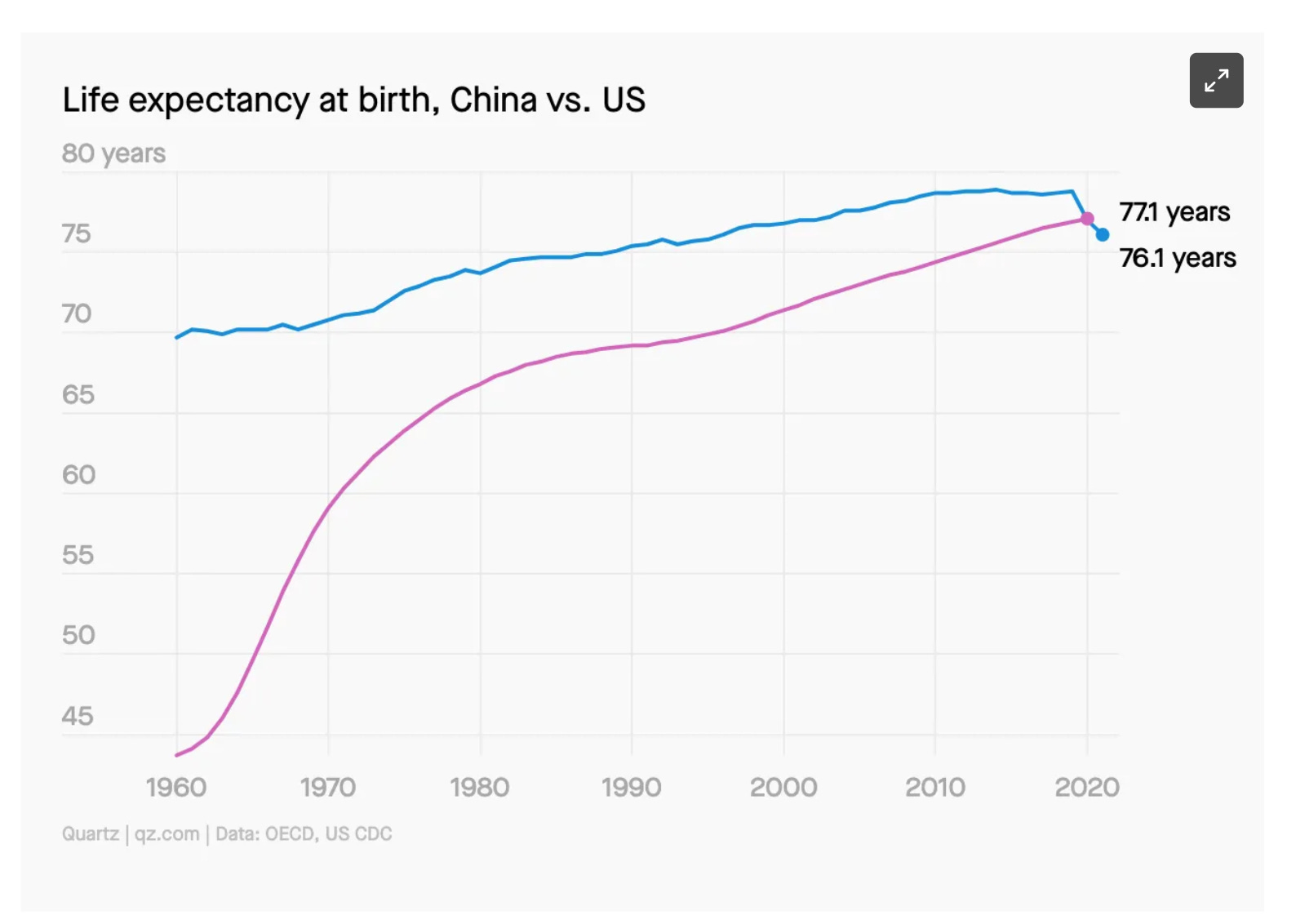

Amongst Xi’s regime’s proudest boasts is the fact that China has registered only slightly more than 5000 COVID deaths compared to more than 1 million suffered by the US. From 15 May 2020 to 15 February 2022, whilst many thousands around the world were dying from COVID every day, there were only two COVID-19 deaths in mainland China. Even allowing for propagandistic understatement of the Chinese numbers, Xi’s China has clearly been far more successful in protecting its population from the worst effects of virus than any country in the West. As a result, it cannot be stated too often, China’s life expectancy overtook that in the United States in 2021, a truly historic marker.

But now, only weeks after Xi’s triumphant party Congress, the zero covid policy is in crisis. The disease is spreading and China’s population is no longer willing to put up with it.

Desperate locked-in workers and indignant students have taken to the streets. Bottle-throwing residents have waged pitched battles with riot police. Chinese diaspora communities have braved the ominous presence of embassy security officials to stage protest meetings.

This is clearly a test of Xi’s authority, the most profound since he has taken power. One must profoundly admire the courage of the protestors and sympathize with the outrage and desperation triggered by successive waves of capricious lockdowns. In large parts of China, ordinary life has become hard to sustain. At the same time it is hard to resist Schadenfreude at the expense of Xi. Xi Jinping’s ‘myth of infallibility’ is being tested.

But as attractive as it may seem to side with the protests against Zero Covid this begs the question. What is the policy alternative? The fact that abandoning zero COVID would be a blow to Xi does not make that the right policy. The dilemma facing Beijing goes beyond the question of Xi’s legitimacy. As ludicrous as zero COVID has come to seem, as oppressive and capricious as its intrusions are in the everyday lives of Chinese people, it has saved huge numbers of lives. And if Beijing were to follow the demand to abandon the policy, this would likely result in a public health disaster not just for the CCP but for China.

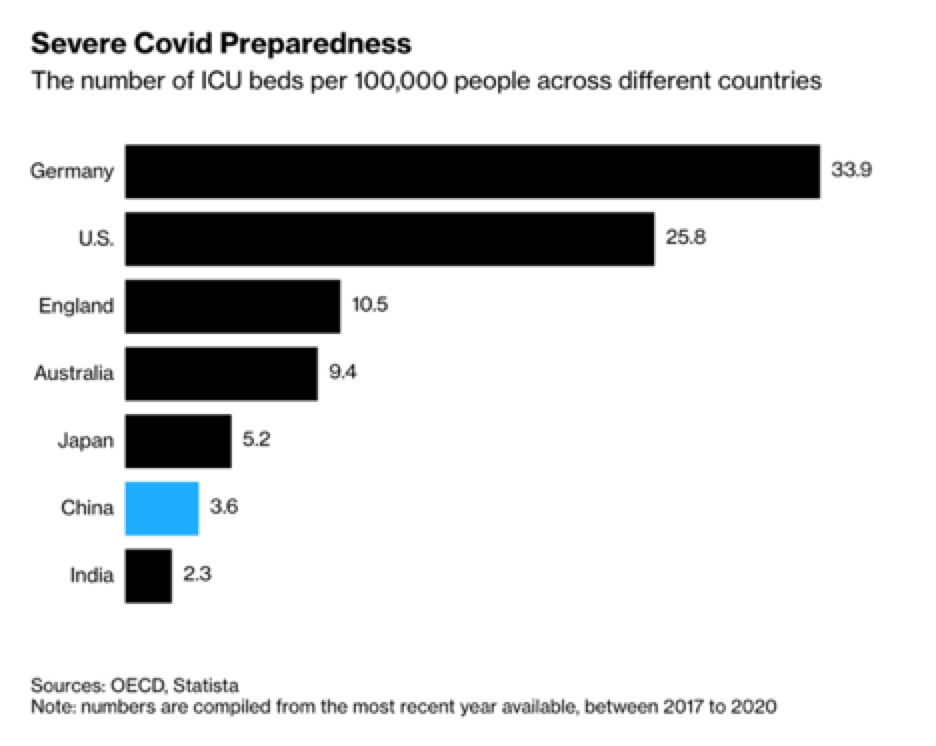

Omicron is less dangerous than Delta but its infectiousness is extremely high. If the pandemic is allowed to run unchecked, hundreds of millions of people will become infected. Even with a low rate of severe cases, China’s medical system will be placed under impossible strain, not just in a handful of cities as in 2020, but across the country. Hundreds of thousands of vulnerable people, if not more, will likely die.

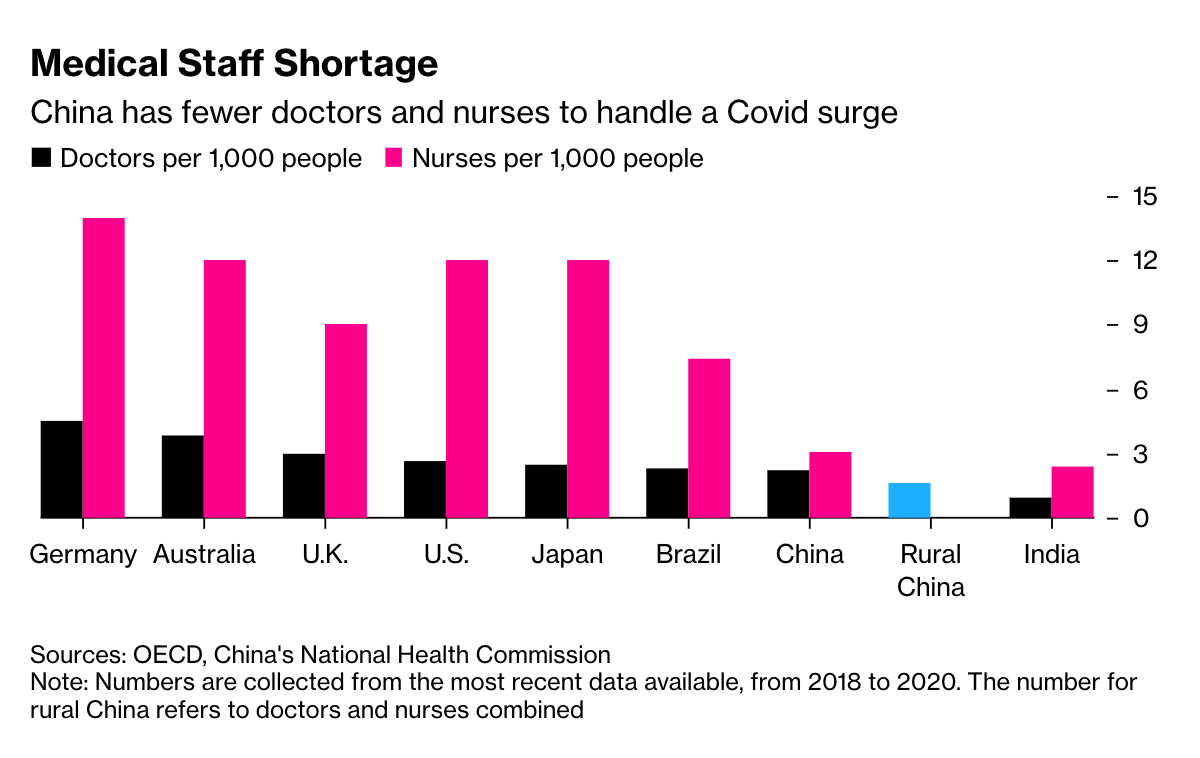

It bears repeating that though China may be a remarkable economic success story, it is still a middle-income country and its welfare net and health care provision are fragile, especially in the countryside, where hundreds of millions of people still live.

All told, by the end of 2021, 970,036 community hospitals had been established in mainland China, employing more than 3 million healthcare workers (around 1 community hospital for every 1,400 residents)6. These millions of local healthcare workers could provide a frontline force with which to contain a nationwide COVID-19 outbreak, but they would require training and investment, which Beijing has so far failed to deliver.

In May 2022 during the emergency in Shanghai, a paper in Nature Medicine estimated that lifting China’s COVID restrictions could results in a “tsunami” of infections. Based on the vaccination rate as of the spring of 2022 the Nature authors predicted that China would need more than 15 times the number of intensive care beds that are actually available. Their modeling suggested a likely toll of 1.55 million deaths. That is a grim figure. An estimate by The Economist, predicted something closer to 680,000, assuming that all intensive care needs can be met, which is far too optimistic.

It is worth noting that even the worst case scenarios do not foresee a catastrophe for China on the scale of America’s or Europe’s botched handling of the crisis. Scaled to population, America’s 1 million deaths would be equivalent to over 4 million in China. That does not seem on the cards. But the figure of between 500,000 and 1.5 million deaths are predicted by most studies would nevertheless be a shattering disaster. Scenes of chaos in hospitals like in Wuhan in January and February 2020 or Hong Kong in early 2022, played out hundreds of times across China are a nightmare that no one can wish for.

In 2020 Beijing avoided this horrifying scenario with a short, sharp national lockdown that contained the epidemic to a cluster of cities in one province. Omicron is so infectious that at this point the outbreak may already be too widespread to be contained without truly draconian nationwide measures – something akin to a nationwide application of Shanghai’s measures in the spring of 2022. But that is itself a horrifying prospect and, as Shanghai now demonstrates, it is not one that offers any long-term solution. Nothing guarantees that Shanghai will not have to go into lockdown again some time in the coming months.

Some optimists say that Omicron is simply not that dangerous. But, if Hong Kong is anything to go by, elderly Chinese should go in fear, especially those who are unvaccinated, of whom there are far too many.

To make a continuation of zero COVID bearable, the regime would need to implement a much kinder and more reasonable quarantine model than that applied in Shanghai. But how to implement that across the largest population in the world in tens of thousands of cities, small towns and villages? It is a mind-boggling challenge. On November 11 the regime issued a new playbook with 20 key parameters to guide local officials in managing the trade offs. Whether that will be enough is anyone’s guess. The hard lesson from Shanghai was that targeted lockdown measures did not work to contain Omicron, whereas the blanket lockdown did. If, as seems likely, Beijing, the CCP and local authorities fail to find a compromise, they, like their Western counterparts in 2020 and 2021, will fail in every direction. They will fail to contain the epidemic. They will damage the economy seriously and provoke further outrage.

If on the other hand Beijing abandons Zero Covid completely, given the infectiousness of Omicron it could be facing an epidemic running at the rate of tens of millions of new infections per day. The disruption of repeated Zero-Covid-lockdowns is huge, but as Europe and the US struggled to digest in 2020, a rampant pandemic has significant economic costs too.

***

There are no simple answers. Xi’s regime is weighing huge risks. Anyone who imagines that that can be a matter of indifference to the rest of the world or is tempted to indulge in Schadenfreude has not learned the first lesson taught in February 2020 – what happens in Wuhan does not stay in Wuhan.

Apart from the human catastrophe facing China, a new wave of the pandemic raises a serious risk of further mutation. Some medical experts argue that precisely because the Chinese population is largely immunonaive it is less likely to mutate new and dangerous strains of the disease.

Let us hope they are right. But the very fact that we are weighing these options points to the basic fact that at this moment Xi’s China has become time machine taking us backwards in time, not decades, to the era of Mao, or centuries, to the age of the imperial dynasties – the vistas that came to mind at the time of the Party Congress – but to the dark days of 2020 – first to the drama of Wuhan and then on from there to the horror of Bergamo and New York’s chaotic emergency rooms. Our problems then are China’s problems now, how to weigh up mass casualties against huge economic loss.

Unlike the first strain of COVID, the Omicron variant that is now overwhelming China’s zero COVID policy, did not originate in China. Omicron was a product of the sweeping global pandemic, which Zero COVID for two years protected China against. Now with the disease threatening to accelerate again, it is us who once again should guard against the assumption that China is “not our problem”.

There is a way out of Beijing horrendous impasse: mass vaccination and an ample supply of anti virals to help patients fight the disease. But that begs the question.

China was the first country to vaccinate. It has vaccines which when used in a triple dose are highly effective against hospitalization and death. The lack of mRNA vaccines is not the issue. Furthermore, the overwhelming majority of China’s huge population have completed the basic two-course regime. Where Beijing has failed is in rapidly delivering the third and fourth round of boosters and in ensuring that the most vulnerable population, those over 60, are properly covered. As of the latest figures cited by Bloomberg, “only 69% of those aged 60 and above and just 40% of over 80-year-olds have had booster shots.” That leaves tens of millions of elderly with no protection at all. They are the people who died in Hong Kong.

As far as I am aware there is no fully convincing explanation for this failure to provide comprehensive coverage particularly of the elderly.

There are a lot of good studies in the specialist literature in medical sociology and psychology that help to explain some of the vaccine resistance.

China became a victim of its own haste in rolling out vaccines on a rough and ready basis to those under the age of 60. This created the perception that the vaccines were not properly tested or safe for use amongst more fragile elderly people.

China has an unfortunate track record of vaccine scandals and the lack of good data on the safety and efficacy of China’s shots among the elderly in homegrown vaccine’s clinical trials does not build confidence.

Health workers have been cautious about recommending vaccines for those with high blood pressure or autoimmune disorders and given the negligible chance of COVID infection, there seemed little reason to take the risk. In most of China, COVID has never been more than a news report. Thanks to the success of the 2020 measures, many cities have never logged a single case and elderly people regard the threat as very remote.

The Chinese population and the regime also suffered from “other people’s problem”-syndrome. Not unreasonably they convinced themselves that COVID was an issue for the failed and degenerate West. Rather than joining a broad global front to endorse precautionary vaccination and boosting with whatever vaccinations were too hand, Beijing allowed the media to spread questions about the efficacy and safety of vaccines in general.

But the real question, given the CCP-regime’s supposed grip on society, is why personal attitudes and public opinion matter at all. Why did the regime not impose vaccine mandates?

One part of the explanation may be that the primary aim of zero Covid was to minimize the number of cases. It thus made sense to prioritize vaccinating the more mobile, younger population, rather than elderly people who can be sheltered by simply staying at home.

Remarkably, at the city level where the vaccination program have to be delivered, the authorities have repeatedly shrunk from forcing the issue. During the height of its bout with COVID, Shanghai city authorities gave cash rewards and did vaccination house calls for the elderly. That raised the delivery of a first course of vaccine to nearly 70% of the elderly group. But without a booster that offers only little protection.

When Beijing attempted to impose the first vaccine mandate in China, the result was an embarrassment. Even with essential retail outlets exempted from the vaccine requirement, within 48 hours the public outcry against coercion forced a retreat. In September, China’s National Health Commission clarified that whilst cash incentives and insurance for “vaccine accidents” are considered acceptable, vaccinate mandates were rejected as national policy. A Health Commission expert declared that

These practices (mandates) violate the principle of vaccination and also cause inconvenience to the masses. Wu Liangyou said that the new crown virus vaccination should be carried out in accordance with the principles of knowledge, consent, voluntariness and seeking truth from facts, and emphasized that the introduction of vaccination policies and measures must be rigorous and prudent, carefully evaluated, to ensure compliance with laws and regulations, and strictly aside by the bottom line of safety. It is reported that the National Health and Health Commission will guide all localities to make good use of health codes and vaccination codes, and resolutely put an end to the two-code joint inspection and compulsory vaccination.

The squeamishness of the regime when it comes to shots is remarkable. Clearly, the CCP-regime does not resist coercive measures. One can hardly imagine anything more coercive in peace time than the closed loop production system in which workers are confined to their factories. Nor does it shrink from costs. The gigantic testing apparatus of Zero Covid that allows a hundred million people to be tested in a single days is very costly. According to the Economist:

The 35 largest firms producing covid-19 tests raked in some 150bn yuan ($21bn) in revenues in the first half of 2022 alone. A broker, Soochow Securities, has estimated China’s bill for covid testing at 1.7trn yuan this year, or around 1.5% of gdp. That number, which some consider an underestimate, equates to nearly half of all China’s public spending on education in 2020.

This highlights the need to understand the complexity of CCP rule, the way in which the appropriate limits of its coercive power are defined and the way in which it prefers certain tactics and instruments to others.

Even after the Hong Kong debacle was clearly visible in early 2022, rather than prioritizing vaccination Beijing preferred to counted on grit and generalized discipline. As the Economist puts it:

In the spring of 2020 the collective self-sacrifice of hundreds of millions of Chinese surprised the world, when their willingness to stay indoors for weeks halted the outbreak that began in Wuhan. Mr Xi over-learned the lessons of that success, declaring self-discipline, vigilance and isolation the key to defeating the pandemic.

Those worked against the original variants of COVID, but against a strain as infectious as Omicron, zero COVID is fighting a losing battle. Even now, in early December, Beijing is still shrinking from vaccine mandates and promising, instead, that “big data” will allow it to target the most vulnerable for special protective measures. Ironically, that confirms the common place of Beijing’s omniscience whilst actually demonstrating the limits of its grip.

Even in the best-case scenario, assuming Beijing’s new vaccination targets are met, it will not be before early 2023 that the vulnerable elderly population have the protection they urgently need and will allow Beijing to escape its impasse.

In any case, the dilemmas facing Beijing go far beyond the authority and legitimacy of Xi Jinping. As The Economist put it in a truly excellent summary of the situation:

… Mr Xi faces the choice between enforcing zero-covid even more strictly, even though that would invite a recession and public fury, or allowing the disease to spread very widely, with calamitous loss of life. Attempting to chart a middle path is only helpful if he uses the time he gains to raise vaccination rates, stock up on antivirals and expand icus. And not only are all Mr Xi’s options unpalatable; he is running out of time to choose one.

***

I love putting out the newsletter for free to thousands of readers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options.

Several times per week, paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

There are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.

Ones & Tooze: China’s Zero COVID Fiasco

China was one of the first countries to produce a COVID vaccine but nearly three years into the pandemic, only 50 percent of its population is vaccinated. Why is that? And why did Chinese leaders opt for lockdowns instead of a more aggressive vaccination campaign? On this episode, Cameron and Adam unpack the issue and assess what sustained protests could mean for China and the world.

Find more episodes and subscribe at Foreign Policy

November 28, 2022

Chartbook #176 The protests in China – a reading list

墨尔本州立图书馆前 民众举行悼念活动 pic.twitter.com/F1Ac5GLtWO

— 李老师不是你老师 (@whyyoutouzhele) November 28, 2022

A round up of reading and twitter threads I have fond useful to understand the stakes in the wave of protests around China triggered by news of the fire-deaths in Urumqi, Xijniang.

For news and images from China follow @whyyoutouzhele who is one of the most trusted sources of inside reports and footage from the protests.

Trust is a crucial issue because the internet is flooded with trolls and surveillance accounts that are either spreading disinformation or trawling for leads on behalf of China’s security services. Protests and vigils not just in China but around the world are being shadowed by Chinese security personnel. The Chinese diaspora is haunted by suspicion of surveillance and agent provocateurs.

On the story of how news of the urumqi fire victims spread through Chinese social media, this China Digital Times report is excellent. As the piece by Oliver Young describes it:

Enraged by the government’s censorship of criticisms about the Urumqi fire, one WeChat essayist wrote a satirical piece titled “Good, Good, Good, Good, Good, Good, Good: Good, Good, Good, Good, Good, Good, Good, Good, Good, Good, Good, Good, Good!” The body text mimicked the form of a normal WeChat essay, but replaced all the characters and images with the character “Good.” Although censors promptly deleted the essay, it sparked a round of creative imitation, with other netizens substituting various characters into the “Good” essay’s template. Many of these were also scrubbed by censors. CDT has translated a sample of the derivatives (and their comment sections) below:

The courage, imagination and dark humor of the protestors is inspiring.

As @tony_zy commented archly:

When police ask the protesters not to chant “no more lockdowns”, so they chant this instead: “MORE LOCKDOWNS!” “I WANT TO DO COVID TESTS!” Folks. Let me remind you this brave effort also encapsulates the highest Chinese wisdom: weaponized passive aggressiveness.

At Tsinghua University, students resorted to formulae:

Students from the elite school Tsinghua University protested with Friedmann equation. I have no idea what this equation means, but it does not matter.

— Nathan Law 羅冠聰 (@nathanlawkc) November 27, 2022

It's the pronunciation: it's similar to "free的man" (free man)—a spectacular and creative way to express, with intelligence. pic.twitter.com/m5zomeTRPF

One of the myths about China is that it is such an oppressive regime that protests is unheard of. In fact, protests by workers, peasants, students and other groups occur relatively frequently and even brief acquaintance with China will impress you with how little respect is shown to regular uniformed police. The backchat and taunting of police is not as shocking as it might at first seem.

On the wider historical setting and the implications of the current protest wave this thread is excellent.

I've been studying various aspects of #protest & contentious #politics in #China for 25 years.

— William Hurst (@wjhurst) November 27, 2022

What's happening now is novel, interesting, & potentially quite important. But we need to be careful about drawing conclusions or making predictions. A:

1/22@CamGeopolitics @NCUSCR

The trigger for the current wave of protests are the draconian zero COVID restrictions and the tragic consequences they have for ordinary people across China, the authoritarian spirit those measures articulate, and the way in which they have become identified with Xi and his personalistic conception of rule. But one trivializes the dilemma facing Beijing if one reduces this to a matter of Xi’s personal pride. The threat of a public health disaster is as real in China in 2022 as in China and the rest of the world in 2020. The disastrous dilemma that Beijing faces today is the result of the failure to contain the pandemic outside China in 2020 and 2021 and Beijing’s staggering failure to strengthen its own defenses against Omicron.

The Covid situation in China is not looking good right now. The authorities have trapped themselves into a situation from which there's no obvious escape strategy. Whatever they choose – or will be forced – to do next will be very costly.

— Prof Francois Balloux (@BallouxFrancois) November 27, 2022

1/

China's population is not particularly young nor healthy and its healthcare system is fragile, in particular outside major cities. It would be easily overwhelmed by any significant surge in Covid-19 cases.

— Prof Francois Balloux (@BallouxFrancois) November 27, 2022

5/https://t.co/uTDDszDu8G pic.twitter.com/xqBq8NFrQE

China's population is not particularly young nor healthy and its healthcare system is fragile, in particular outside major cities. It would be easily overwhelmed by any significant surge in Covid-19 cases.

— Prof Francois Balloux (@BallouxFrancois) November 27, 2022

5/https://t.co/uTDDszDu8G pic.twitter.com/xqBq8NFrQE

Hong Kong faced a similar challenge in early 2022 and the result was a public health disaster. Cumulative COVID mortality in Hong Kong surged to alarming levels.

Would mRNA's cut it?

— Richard from Sydney (4

We here in Oz have used mRNAs extensively, as has NZ, and if you applied out last 12 months deaths to China, you get between 500,000 and 1,000,000 dead.

So "mRNAs" don't appear to be an actual "solution" here, more a "fail safe"

They need a MUCH better vax pic.twitter.com/VwUWNdUr18) (@RichardfromSyd1) November 28, 2022

What is at stake here is not merely Xi’s obstinate insistence on his pedantic zero-COVID policy, but the question of whether Beijing is willing to consciously and publicly the distinct risk of a pandemic outbreak that will likely cause mass death and a fundamental challenge to China’s fragile health system. This would be a disaster for Xi and his narrative. But it would also be a disaster for China. It would be a return to the nightmare of Wuhan in February 2020, or New York in March 2020 and presumably Beijing would then be forced to respond with even more draconian lockdowns and a desperate fight to save its hospitals. Furthermore, with all the experience of the last two years in front of it and the disaster of Western policy widely advertised, Beijing would be accepting this national fiasco consciously. As Balloux says the situation is not one of caprice, but of disastrous impasse. There is no obvious escape strategy.

The only realistic option is a massively accelerated vaccination campaign aimed above all at the most resistant group i.e. the very elderly. That would perhaps create the breathing space for more selective and intelligent lockdown policies. In the mean time, the likelihood is that Beijing will continue with its current policy and respond to the protests by activating emergency plans for repression of “sudden public incidents”. On the repressive scenario planning of the regime, this by @hcsteinhardt is excellent.

There is some speculation on how the state will respond to recent contentious events in China. The state conceptualizes these as "sudden public incidents" 突发公共事件. Detailed contingency plans exist at every level, instructing authorities how they should respond. A brief

— Christoph Steinhardt (@hcsteinhardt) November 27, 2022

As Steinhardt describes it in his 2020 article in Journal of Contemporary China “Defending Stability under Threat: Sensitive Periods and the Repression of Protest in Urban China”

… stability maintenance during sensitive periods appears much less rigid and more managerial than is often presumed. This points to a rather fine-tuned coercive apparatus in China’s urban centers. The state preempts some protests when it manages both previously known and sudden periods of sensitivity. Yet, it still tolerates a considerable amount of contention and avoids costly bouts of responsive repression even during periods when it perceives the political order as more vulnerable than usual.

Given the disastrous impasse Beijing faces and the likelihood of a crackdown to come, is there an alternative to despair?

On twitter two sorts of reflection on this theme have caught my eye. One cites the fabulously entitled essay about the shock of 1989 by Timur Kuran “Now out of Never. The Element of Surprise in the East European Revolution of 1989”

Great essay, which you can find here: https://t.co/jWPVDlH3Gq https://t.co/3OwLndiE6E

— Michael Pettis (@michaelxpettis) November 28, 2022

I was also reminded (h/t QW) of Lu Xun’s famous Preface to Call to Arms of 1922:

"Yet I could not erase all possibility of hope, for hope lies in the future. I could not rely on my own present evidence in its lack, to refute his assertion that it might exist one day."

— eileen chengyin chow (@chowleen) November 27, 2022

-Lu Xun, from Preface to Call to Arms, 1922. #everynightapoem #ofsorts #救救孩子 pic.twitter.com/oqjDlsjz4s

To sign up for Chartbook Newsletter click here:

November 26, 2022

Chartbook #175 Fortune Favors the Brave: the making of crypto ideology, Vesuvius and the romantic sublime.

Nov 26

Cryptonaughts.

“History is filled with almosts. With those who almost adventured, who almost achieved, but ultimately, for them it proved to be too much. Then, there are others. The ones who embrace the moment, and commit. And in these moments of truth . . . they calm their minds and steel their nerves with four simple words that have been whispered by the intrepid since the time of the Romans. Fortune favours the brave.”

I’ve been mulling these lines ever since I first saw the ad spot for crypto.com done by Matt Damon during a football game back in the autumn of 2021.

Following the FTX collapse, I returned to the crypto.com spot for my latest op ed for the FT, which is running this weekend.

The spot was for Crypto.com, which in 2021 described itself as the world’s fastest-growing cryptocurrency platform, serving over 10 million customers and issuing the Crypto.com Visa Card — what they claimed was the world’s most popular crypto card program. Crypto.com describes itself as

“committed to building the future of the internet: Web3. Powered by cryptocurrency, Web3 will be more fair and equitable, owned by the builders, creators and users. The new ad, “Fortune Favors the Brave,” which stars Matt Damon, is directed by Oscar-winner and Chicago-born Wally Pfister and produced by David Fincher, highlights the company’s own ethos, while inspiring those who want to change the course of history with a timeless phrase first uttered thousands of years ago. Created by San Francisco-based Pereira O’Dell, the gorgeous 60-second video centers around Damon taking viewers on a historical journey of brave men and women in the hopes of inspiring people to be their bravest selves.”

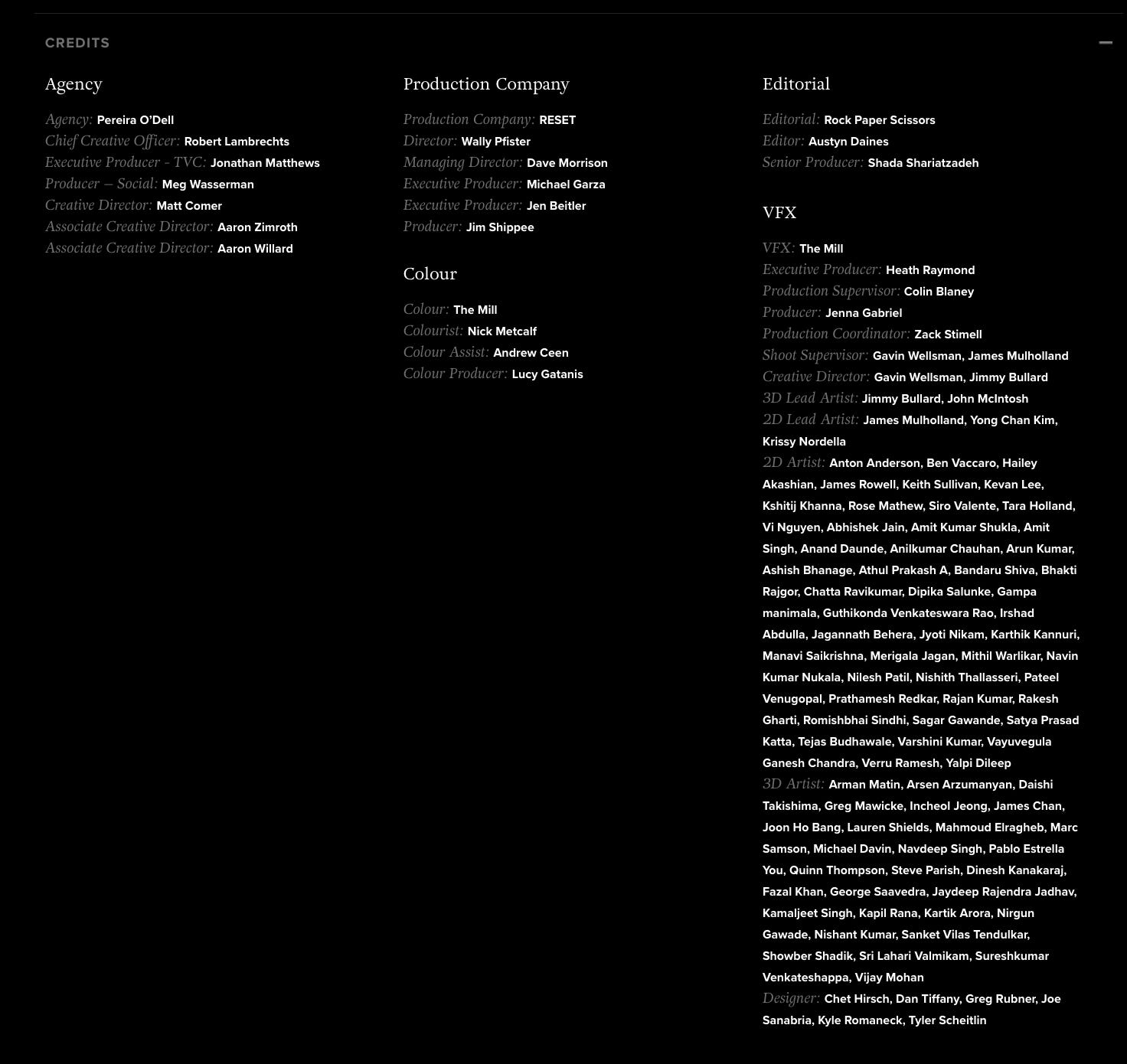

Credit for the ambitious spot goes to VFX agency, The Mill, who proudly declare that the campaign, in the autumn of 2021, “coincides with the early stages of mainstream adoption of cryptocurrency. The campaign … pays homage to those who got us to this point and is an invitation to those who will soon join the journey toward financial independence and self-determination.”

The team involved in producing this vision includes:

Wally Pfister, the Director, earned his reputation as cinematographer for such films as The Dark Knight, The Prestige and Moneyball. His longstanding collaboration with director Christopher Nolan netted him several Academy Award nominations, and in 2011 he won the award for his groundbreaking work on Inception. He now specializes in high-end star-studded adverts:

As Crypto.com Co-Founder and CEO, Kris Marszalek declared. “We’re very excited to introduce our company to a global audience inviting them to our secure platform with a message focused on financial independence and self-determination.”

The link to Damon was provided by Water.org, Damon’s global nonprofit organization that brings safe water and sanitation to people in need. Crypto.com made a $1M direct donation to Water.org to support their mission and launched “initiatives to encourage more than 10M users around the world to support the cause”.

As the press releases had it:

“Together, Crypto.com and Water.org believe in equal access to the platforms and life-changing resources that support self-determination. Through this unique partnership, crypto users across the globe can join in to support this mission. “Much like what we’re doing with Water.org, Crypto.com is a cryptocurrency platform that shares my commitment to empowering people around the globe with the tools needed to take control of their futures,” said Matt Damon. “They have built a crypto platform that is accessible and puts people first.”

The spot was introduced to US audiences during Fox Sports’ broadcast of Thursday Night Football with the Packers taking on the Cardinals. It was then to be rolled out across Crypto.com’s portfolio of global brand partnerships ranging from Formula 1, UFC, Paris Saint-Germain, and the NBA’s Philadelphia 76ers, to the NHL’s Montreal Canadiens, esports team Fnatic, Aston Martin Cognizant Formula 1 Team, and Lega Serie A, the Italian Football league.

This gives an impression of the reach of crypto’s influence. It was budgeted at $100 million, encompasses more than 20 countries and will run for “several months.” Launched at the same time as FTX’s $20 million U.S. ad campaign, featuring football quarterback Tom Brady and his wife Gisele Bündchen, the crypto.com-Damon campaign represented the peak of crypto’s commercial visibility.

In the FT piece I address the notions of history and agency mobilized by the bombastic advertising script. What does it mean to say that fortune favors the brave? Are success and failure not matters of judgement and power? How has a system of digital tokens supposedly devised for a world of zero-trust, morphed into something akin to a faith-based community, fueled by a glitzy ethic of historical agency and voluntarism.

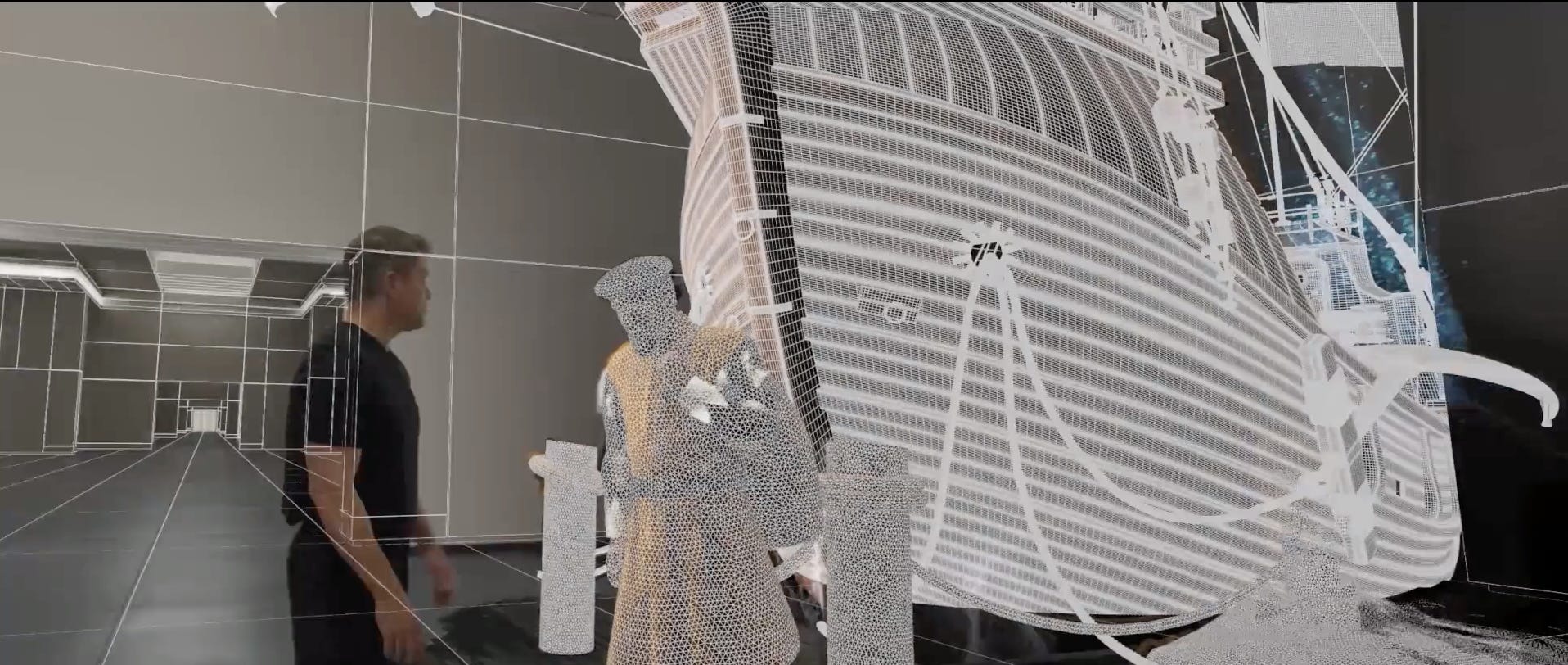

For a fascinating expansion of the crypto.com’s ideological script and its visual representation, it is worth checking out the “Making of”-video that documents the filming of the 1-minute spot. Thankfully, this is available for your viewing pleasure on Vimeo.

The film-makers describe how they construct a hybrid world of VFX and live action, in which Damon marches through an empty white hall – what they call “the museum of bravery” – in which images appear around him as examples of perseverance and bravery. These include a virtual renderings of Magellan-like figure ….

An Edmund Hillary-like figure scaling a snowy mountain…

A couple picking up courage to announce their mutual attraction.

And a multi-ethnic group of astronauts featuring tell-tale reference to the mythic founder of bitcoin.

As the top management of crypto.com tell the camera:

Fortune favors the brave is not just a line for a campaign. It is genuinely how cyrpto. com sees the world. … Fortune favors the brave is deeply personal. It is how we live. It is what we believe in. This decade belongs to cyrpto!

The spot is impressive not only for its visuals but also for its historical sweep. It is also, however, impressively weird.

The phrase “fortune favors the brave” is generally attributed to Pliny the Elder, the obsessive scholar and Roman Fleet commander. He uttered it on the fateful night of August 24 79 AD when the volcano Vesuvius erupted and buried Herculaneum and Pompeii. As recalled 25 years later, at the request of Tacitus, by his nephew Pliny the Younger, Pliny the Elder ignored the advice of his helmsman and steered directly towards the eruption, hoping to pull off a famous rescue. Instead, he was overwhelmed, lost control of the situation and finally, in ridiculous circumstances, succumbed to the fumes, becoming one of the thousands of casualties.

Generations of scholars have debated the meaning of the incident as described by Pliny the Younger. Umberto Eco for one argued that the younger Pliny was an apologist for his dead uncle. But recent revisionist scholarship by Tom Keeline, argues the opposite. Uncle Pliny was an anti-model, a man so stuck in his obsessive pursuit of scholarly learning that he could not respond appropriately or successfully to the unprecedented situation:

We see a man who not only is not in control of the situation (although as commander of the fleet he was certainly supposed to be), but who altogether fails to understand it. He appears brave, in a sense, and just as he is given full credit in 3.5 for being a man of great learning, he is here acknowledged to be fearless—but this fearlessness is throughout presented as recklessness.51 He sets a course where others rightly fear to tread, and we see him clearly linked to his practices in Ep. 3.5.15:

In itinere quasi solutus ceteris curis, huic uni uacabat.

When traveling he was as it were free from all other cares and devoted himself to this (i.e., studia) alone.

The Elder thus continues his normal routine, as he has been doing all along, but this is fundamentally the wrong course of action.52 Just as in Ep. 3.5, he has someone at his side to take down his every word as he travels. Our man of science has his head somewhere in Cloudcuckooland, not in the real world of people living and dying. While a volcano is spewing death and destruction he is focused on dictation. Then conditions worsen. Ash begins falling on the ship, and it gets hotter and denser the closer they get to the coast; soon they are being bombarded by actual rocks (Ep. 6.16.11). Here the Elder hesitates a moment, but he determines to brazen it out (Ep. 6.16.11):

Cunctatus paulum an retro flecteret, mox gubernatori ut ita faceret monenti “Fortes” inquit “fortuna iuuat: Pomponianum pete.”

Unsure for a moment whether he should turn back, when the helmsman warns him to do just that he says: “Fortune favors the bold: head for Pomponianus!”

He does not know what he should do, and he receives sound advice from a seaman who plainly does. Perversely, however, this impels him in the oppositedirection, and with a misapplied proverb he presses on.53 Rather than favoring him, Fortune will soon take his life.

You might say that evoking Pliny’s famous phrase was more apt than Damon or crypto.com realized.

For a beautifully produced and version of Pliny the Younger’s text translated by Benedicte Gilman and illustrated by Barry Moser, check out Ashen Sky.

But Vesuvius does not belong only to the classical tradition. In the 18th century, the volcano would become one of the quintessential sites of the romantic sublime. Here is Goethe describing his first encounter with the volcano in 1787.

But, what enabled Goethe and others to appreciate the volcano was not simply personal courage, or inclination, but, as a recent article by John Brewer shows, a network of expertise, local guide knowledge and tourist promotion that made the volcano into a European hub.

This article examines the activities of guides on the volcano Mount Vesuvius in the late eighteenth and nineteenth centuries. They worked in a double capacity—as aids to savants seeking to unlock the scientific secrets of the volcano and as the creators of a tourist infrastructure that helped visitors enjoy the sublime experience of a steadily erupting volcano. The essay examines their contribution to scientific knowledge of the volcano and their role in developing sublime tourism, a phenomenon that, despite an earlier existence, burgeoned in the late eighteenth century. It argues that guides were vital to both, but that a long-standing attempt to circumscribe their role as knowledge makers grew more and more effective in the nineteenth century, as mineralogists’ concern with specimens (shared by so many visitors and amateurs) gave way to geologists’ concern for the interrelations of rocks and strata, and as the Neapolitan state developed scientific institutions, notably the volcanic observatory with its instruments on the slopes of the volcano, that took over functions previously served by the guides. Though the guides—or some of them—were able to profit from the flow of visitors, not least because of their special knowledge and skills, their activities were also transformed as the growth of a state infrastructure of roads and railways pushed them to the margins, and as transnational organizations, like the Thomas Cook travel agency, absorbed their labor.

From failed Roman commanders, to the intermingling of tourism, commerce and science – in the end, perhaps, the unconscious evocation of Pliny and the Vesuvius disaster at the height of the crypto boom, by Matt Damon, crypto.com and their image-makers was less incongruous than it at first seemed.

November 25, 2022

Regulators can’t keep turning a blind eye to crypto craziness

Stopping a hyped-up project that promises to disrupt the status quo requires decisiveness and courage

Read the full article at the Financial Times

November 15, 2022

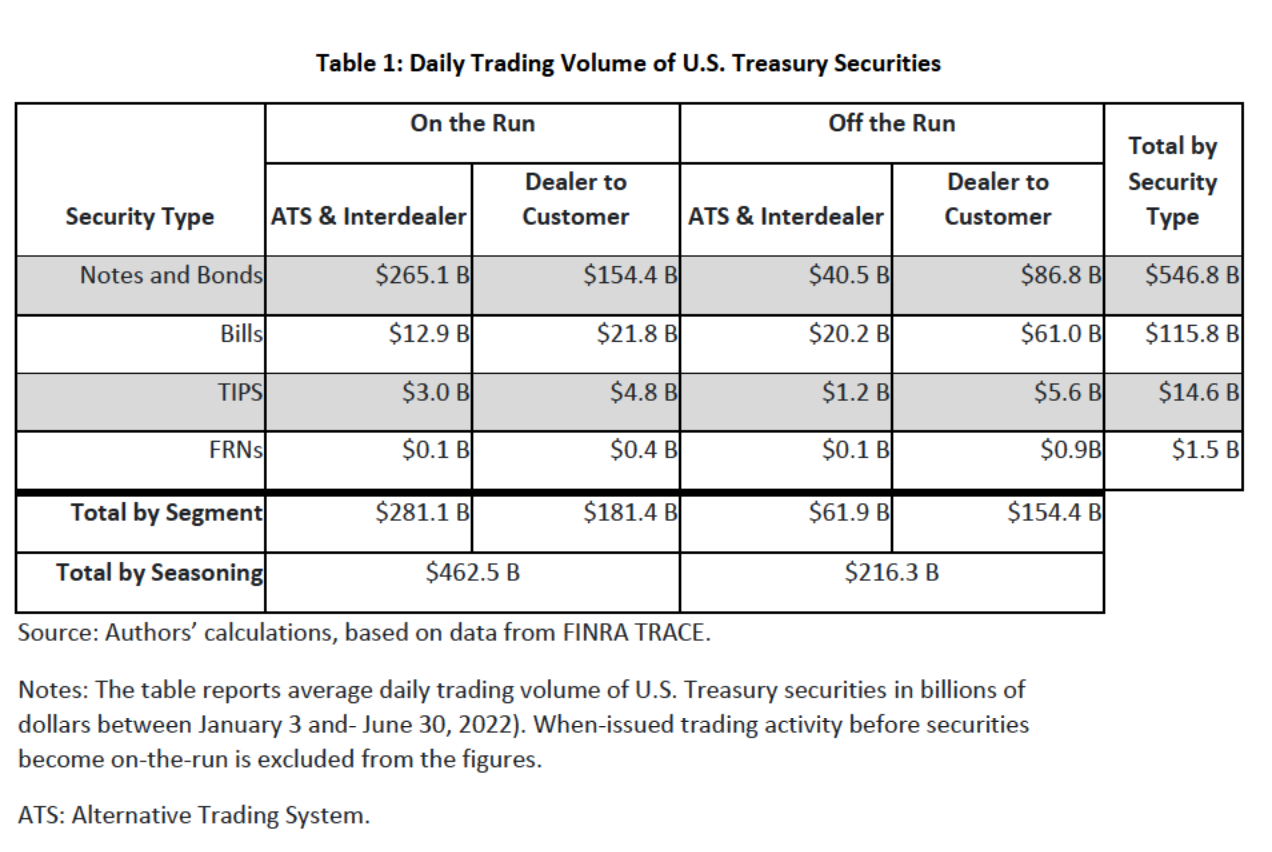

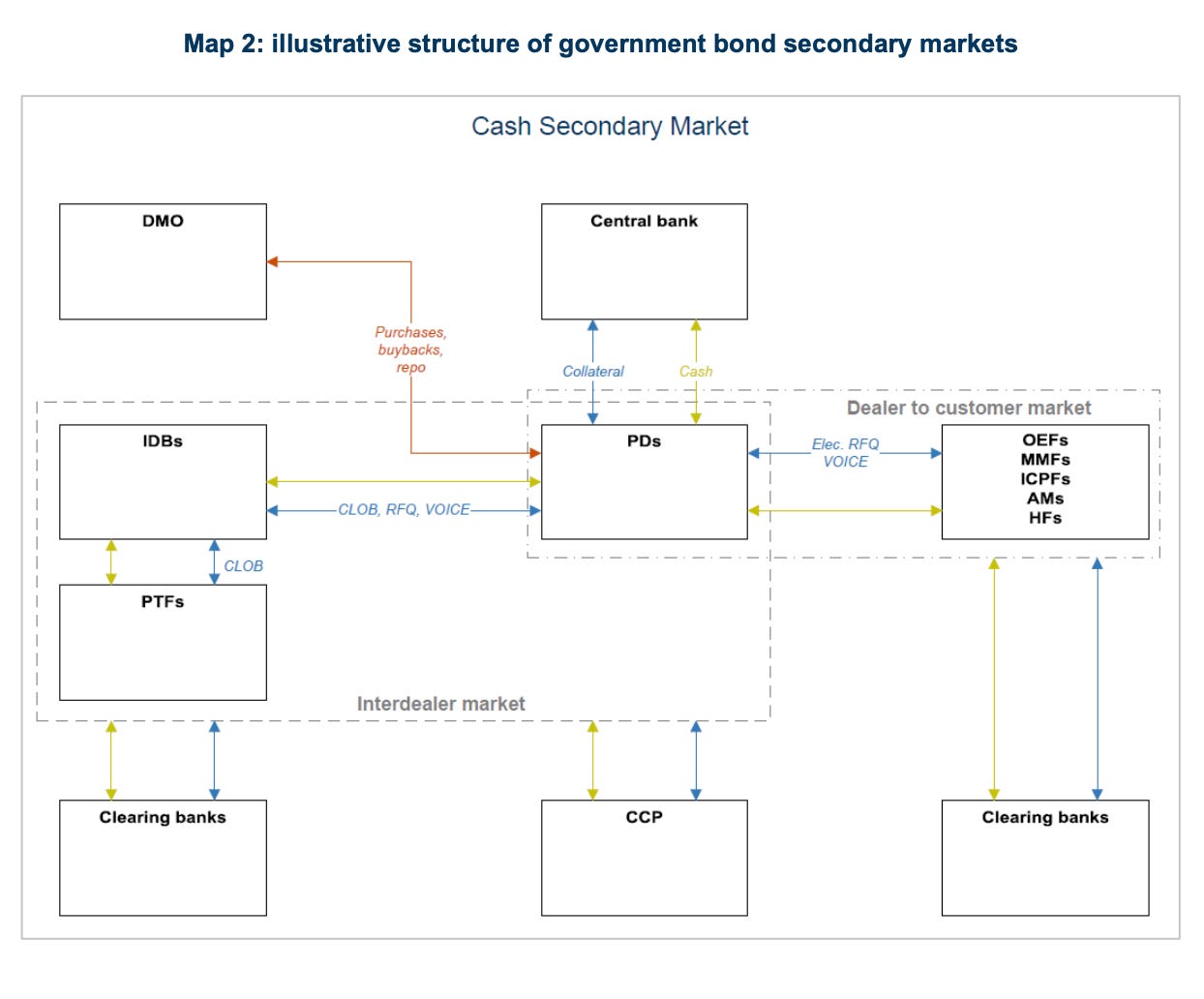

Chartbook #172: Finance and the Polycrisis (3) US Treasuries – how fragile is the world’s most important market?

If there is one financial market that could put in doubt the stability of the entire global financial system it is the $23 trillion US Treasury market.

Source: Fed Financial Stability Report

The housing market may be the biggest single macroeconomic force. US residential real estate alone is worth $53 trillion. But it is illiquid. US equities are valued at $46 trillion. They can be easily bought and sold, but no two equities are alike. You have to pick and choose. The $23 trillion market for US government debt offers a relatively smooth spectrum of homogenous assets that differ only in terms of their duration, ranging from a few weeks to 30 years. They trade on a curve defined in terms of maturity. They are safe assets with no serious default risk offering an extremely liquid market, which provides the ideal platform for financial engineering supercharged with algorithmic high frequency trading. As the largest pool of fixed-income, safe assets, the Treasury market registers vibrations from every piece of economic and policy news in a matter of millisecond. Every day hundreds of billions of Treasuries change hands in hundreds of thousands of trades.

Source: NYFED

The prices and yields that result from these trades set the benchmark for all other borrowing and lending. The question that haunts the markets right now is what happens when the entire structure of interest rates lurches violently upwards in response to a sudden surge in inflation and the promise of severe central bank action?

The risk is not that Treasuries suddenly become worthless, as a result of US government default or hyperinflation. Nor is there much prospect of a geopolitically motivated bear raid on the US by its foreign enemies. The risk is more mundane, the risk is that the market, driven by greed and fear, will stop working, that prices and yields will become anomalous and upset trillions of dollars in portfolio allocations unleashing a landslide, as hedge funds, banks and other investors scramble for cash.

So large a shock would this be that there is little prospect that it would be allowed to play out to its full catastrophic extent. We dont live in the 1930s anymore. There is an answer to such a crisis – the central bank. But if the Fed were forced to step in, it would imply a shuddering reversal of policy. The shock would move from the markets to the institutions. Credibility would be in tatters. It would amount to a severe intra-elite crisis. Something like the UK suffering but at the heart of the worldâs financial hegemony.

You might counter that in 2020 the Fed dealt with a crisis in the US Treasury market and emerged with its reputation for competent crisis-management enhanced. But that malfunction was triggered by a pandemic, a shock that, as far as the financial system was concerned, was exogenous. If something similar were to occur in 2022/23 there would be no excuse. Of course, the inflationary surge that began in 2021 is itself attributable, whether demand- or supply-induced, to COVID. But today what is causing the stress in financial markets is not inflation as such but the policy response of the central banks. They are raising rates as the macroeconomic situation demands. If they cannot do so without triggering a malfunction in the worldâs most important financial market, then, âHoustonâ, we have a problem.

***

For many readers of this newsletter, the 2008 banking crisis will be the benchmark of financial terror. But in 2008 the American government balance sheets was the platform from which the rescue of the banks was mounted. The Treasury market remained solid. Indeed, investors ran to safety in Treasuries. Only in weaker members of Eurozone – Ireland was the prototype – did we see a full doom-loop develop in which a banking crisis overloaded the public balance sheet, precipitating a public debt crisis, which in turn destabilized the private financial system.

The US Treasury market is not immune to shocks. It wobbled badly in September 2019 in the so-called repo market crash. But the real scare came in March 2020 when the Treasury market stopped working for several weeks. This precipitated a panic even more acute than in 2008 and a truly gigantic intervention by the Fed. On several days in late March 2020 the Fed bought more bonds than Ben Bernankeâs Fedâs bought in an entire month at the highpoint of the first round of Quantitative Easing. This story is at the heart of Shutdown, my book about 2020.

It is important to emphasize, in light of the comparison with the Eurozone, that what caused the panic in March 2020 was not concern about the solvency of the US government. The volume of Treasuries has continuously increased because of the deficits run over the last quarter century. And ahead of 2020 the balance sheets of the main actors in the Treasury market were stuffed full by the large deficits run by the Trump administration. In relation to GDP, US government debt was rising and it surged at a wartime rate due to the COVID stimulus. But that was not what the panic of March 2020 was about. Nor is the deficit and new public debt issuance the main worry in 2022. What matters is what private financial actors – banks, investment funds, hedge funds – do with Treasuries and their constant need to churn them through a liquid market. What concerns us is not a crisis of public finances, but a crisis triggered by the private use of public debt.

Source: FSB

For all that public debt is a liability of the taxpayer, it is also an asset. You buy assets to benefit from appreciation and their yield. You can use them as collateral for further borrowing. Crucially, you need to be able to sell them in an emergency. That is what US Treasuries normally offer you. But in March 2020 the market stopped working. There were too many sellers and not enough buyers, so the price of highly rated entirely safe securities suddenly plunged and yields surged. To avoid disaster the Fed stepped in as the buyer of last resort. It also offered repo facilities, i.e. loans against Treasury collateral, in the hope that if they could be used to raise funds by way of the Fed, private investors would have less reason to sell their holdings. The combined effect was to flush trillions of dollars of liquidity into the system and to stop the run.

In 2020 inflation was not a concern. Prices were falling. Today, with prices rising the Fed is trying to reverse course. It is trying to tighten monetary conditions. It is raising interest rates and rather than buying Treasuries to provide liquidity, it is selling them, draining reserves out of the financial system. Between September and November the Fed planned a $95 billion tightening. The question is whether the Treasury markets can take it. Without the Fed as the buyer of last resort, will private investors still be able to buy and sell Treasuries smoothly or will the market again become dysfunctional?

***

The signs of stress are clearly there. Both anecdotal evidence and some quantitative indicators suggest a worsening liquidity situation.

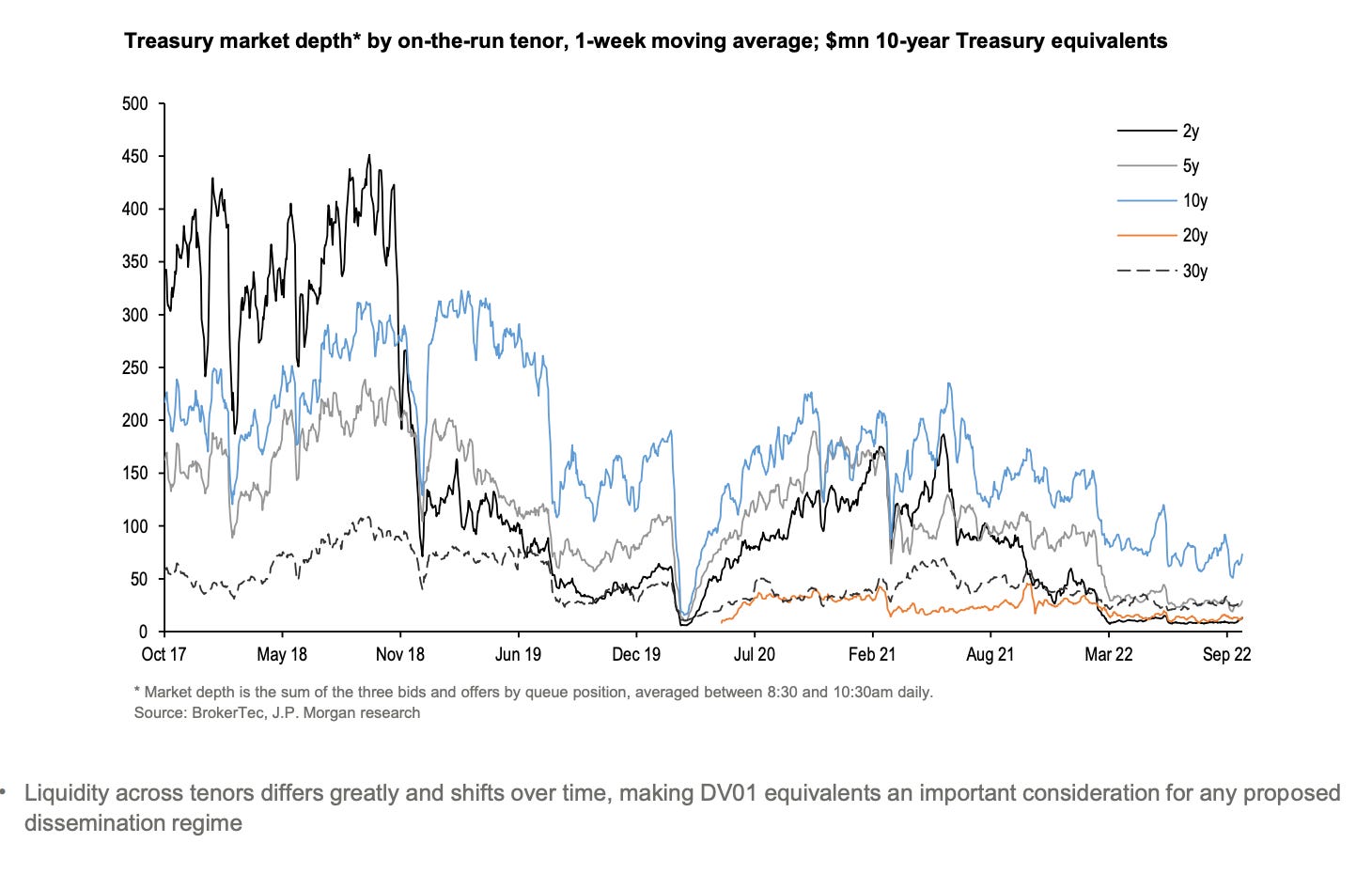

The market depth for US Treasuries varies by duration. It collapsed entirely in March 2020, but though it has recovered, it remains well below 2019 levels.

Source: US Treasury

Bid-to-ask ratios that measure how difficult it is to sell Treasuries are at uncomfortably high levels. And, at the primary Treasury auctions, when fresh Treasuries are sold, there is a noticeable weakness of new demand.

Clearly, market conditions are not easy. But the difficulty is to decide how serious these signs are. There are technical reasons discussed in the Fedâs latest Financial Stability Report why some of the commonly cited indicators may exaggerate the liquidity squeeze. Furthermore, as market participants point out, it is not surprising that liquidity should be somewhat tight right now. As we move from one level of interest rates to another, you would expect more volatility and with more volatility you should expect less liquidity. This is a normal market adjustment.

The worry expressed by several market participants to the FT is that causality is also beginning to run the other way around. It is not just that volatility is driving illiquidity. Illiquidity is beginning to cause volatility. If both effects operate at the same time they form a vicious spiral in which volatility surges and liquidity collapses. Given this possibility the question of what is the precipitating factor may become moot. The terrifying thing about a run is that it operates by itself. If you hold treasuries for liquidity and a surge of panic-selling causes the market to seize up, then on precautionary grounds you must try to sell too, so as not to miss your chance. Whatever your underlying long-term motivation, you must join the crowd.

As a recent paper from the New York Fed by Thomas Eisenbach and Gregory Phelan shows, this kind of run dynamic with âprecautionary sellingâ appears to have built up in Treasury markets in 2020. It would be disastrous if it were to recur.

***

At this point you might wonder why this vital market is so opaque. If this is the most important financial market, if this is the sovereign debt of the most powerful state, why is there so much uncertainty and volatility?

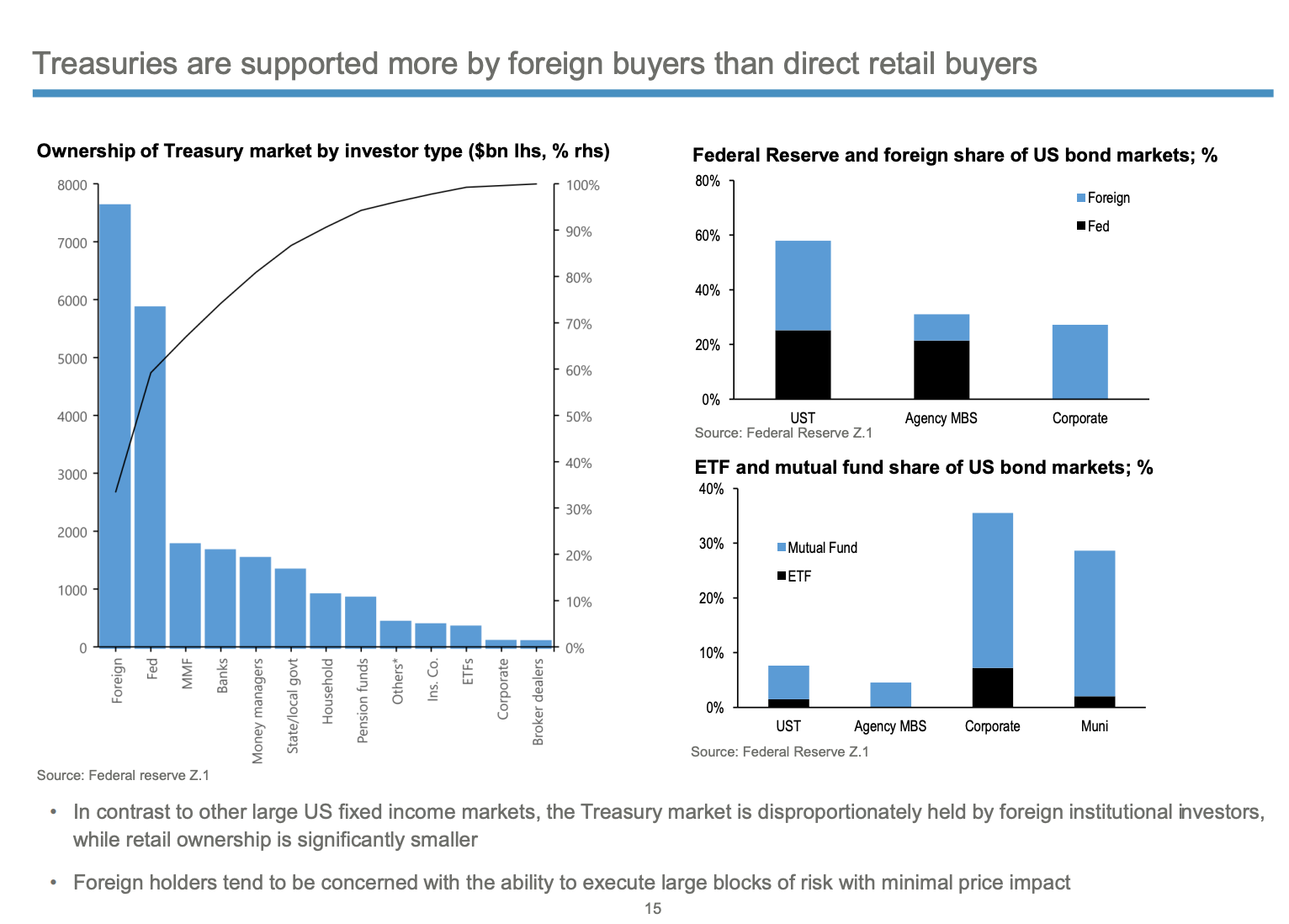

Part of the problem is that the range of investors holding treasuries is huge. The largest single group of Treasury investors are reserve managers from across the entire world.

Source: US Treasury

Given the scale of foreign involvement, shocks emanating from anywhere in the world will reverberate in the market. Foreign sales were an important part of the shock in 2020, when there were significant emerging market reserve sales. In 2022, given the savage devaluation of the yen and the prospect of a major course correction by the Bank of Japan, the main worry are sales by Japanese investors. We will return to that in a future installment of this series.

But pointing finger at foreign investors can be a way of diverting from the main problem. Japanese pension funds and banks are just one part of the giant transnational system of shadow banking for which US Treasury bonds are the rocket fuel. The main hub of this system is not in Tokyo but in New York.

The emergence of this system from the 1950s onwards is beautifully chronicled by Tracy Alloway in an extraordinary essay for Bloomberg which draws heavily on the work of the brilliant Josh Younger. As Younger put it:

âIn the early 1950s, the Federal Reserve and Treasury leaned heavily on dealers to jump start a âfreeâ Treasury market â one where prices were set by investors not the government,â explains Younger. âIn many ways, weâre still living with the legacy of those policy decisions. The Treasury market today is arguably only as healthy as the shadow banking system on which those dealers depend.â

The system that has emerged is fragmented and unstable. The Financial Stability Board provides the following map for the secondary market, with further complexity added by repo and futures markets.

Source: FSB (PD = primary dealer, HF = hedge fund. Check out the paper for the full legend)

As Vanderbilt Law Professor Yesha Yadav points out, it is not just the markets themselves, but the regulators of the markets that are fragmented.

Whereas equities or corporate bonds are overseen by a primary regulator (the SEC), Treasuries are supervised by five or more major agencies, none of which has lead status. The Treasury writes the rules, the Federal Reserve Bank of New York (N.Y. Fed) facilitates debt auctions, the SEC and the Financial Industry Regulatory Authority (FINRA) supervise securities firms that trade Treasuries, the Fed monitors banks, and the Commodity Futures Trading Commission (CFTC) oversees the derivatives markets linked to Treasuries.8

Though this kind of fragmentation is typical of the US administrative state, it is highly dysfunctional in the case of a market as large, dynamic and essential as the Treasury market. Yadav joins other academics, notably Darrell Duffie of Stanford, in calling for central clearing to achieve greater transparency and security in trading. Her conversation with David Beckworth on his Mercatus podcast makes for great listening.

As The Economist neatly summarized the options, reform entails one of three options:

allowing the banks to trade more bonds with investors (by loosening reserve requirements on the banks – their preferred option

), let investors trade more bonds with each other (with some kind of clearing or improved trading mechanism), or let investors trade or swap more bonds with the Federal Reserve (by way of a widened repo facility).

So important is the US Treasury market that it has attracted the attention of the G30 and the Financial Stability Board that advises the G20 and the IMF has also chimed in (as linked above).

***

The US authorities are not oblivious to the need for reform. The 2020 crisis was serious.

The Inter-Agency Working Group for Treasury Market Surveillance (IAWG), which was formed in 1992 after the Salmon brothers auction bidding scandal convenes staff from the U.S. Department of the Treasury, the Board of Governors of the Federal Reserve System, the Federal Reserve Bank of New York (FRBNY), the Securities and Exchange Commission (SEC), and the Commodity Futures Trading Commission (CFTC), has taken on task of coordinating reform discussions across the different branches of government.

The most consequential recommendations to date have come from Gary Gensler and the SEC. The SEC is pushing for an extension of central clearing both in Treasury Trading and in repo. It also wants to have more oversight over the firms involved in the market. Earlier this year it proposed that all firms that trade more than $25bn in Treasuries per month to, in future, be registered and regulated as dealers. This has triggered furious blowback back from market makers, investment funds and other firms â almost everyone but the primary dealers, who are already heavily regulated – who all denounced the suggestions as dangerous. They will cause key actors to limit their involvement thus deepening the liquidity problems.

Given the asymmetry of information between market participants, regulators and journalists, and given the lack of overall information, the Treasury market is one in which forming an independent judgement is truly difficult.

And in any case as Alexandra Scaggs of FT Aphaville has noted, tinkering with regulations affecting one group of market participants alone is a partial fix at best.

There isnât much the SEC can do about high levels of Treasury issuance and economic uncertainty (thatâs the job of Treasury, Congress and the Fed). But it can expand its surveillance into Treasury markets to get a better idea of who these price-sensitive traders are, and put de facto limits on leverage. If the goal were solely to create a robust Treasury market structure independent of political pressures, which is surely a fantasy in the US, regulators could be focusing on systemic solutions to deal with funding costs in times of crisis. They could look into clearing solutions, or make more policy about countercyclical changes in dealer regulations. But if regulators are instead using the Pottery Barn rule, the hedge-fund focus makes perfect sense.

A conference will be held on November 16th (tomorrow) with industry players and experts at New York Fed to address the issues.

***

Will there be a market incident before new regulations come in place? It cannot be ruled out. But if it were to occur, we already know how it would be contained. The Fed would buy assets and offer expanded repo facilities to all comers. That is what all the central banks did in 2020. It is what the Bank of England briefly did after the nasty incident with Trussonomics. But if this is the future, it raises the question: are we on a ratchet in which macroeconomic shocks and weak market structure force central banks repeatedly to intervene? Each time they expand their balance sheets and flush liquidity into the system, expanding commercial bank reservers. Then, when they seek to reverse course and ânormalizeâ, they unleash market stress, which causes them to intervene again.

That appeared to be the case in 2019, when Jerome Powellâs first attempt at tightening ended in the repo market shock of September. If we are repeating that cycle now, it forces us to ask: why is it so hard to normalize? Why is it so hard to reverse QE with QT? The answer provided by Raghuram G. Rajan and Viral Acharya in a project syndicate column, and with co-authors in several other papers, is that expanding and shrinking reserves is not symmetrical. It is not symmetrical because of the way that commercial banks respond to the increase in their reserves during the expansionary phase of QE.

When the Fed buys bonds, it does so in exchange for reserves. The bonds that the banks sell to the Fed come from customers who end up with deposits at the banks. The banks make a small interest margin on this trade. But as highly incentivized profit-driven businesses they cannot be satisfied with these slim pickings so they go in search of bigger business.

commercial banks have created additional revenue streams by offering reserve-backed liquidity insurance to others. This generally takes the form of higher credit card limits for households, contingent credit lines to asset managers and non-financial corporations, and broker-dealer relationships that promise to help speculators meet margin calls (demands for additional cash collateral)

And that is what creates the ratchet effect. The commercial banks become more vulnerable to shocks due to their exposure to contingent credit lines. But when the central banks wants to carry out normalization and shrink reserve, the banks are slow to reel in their profitable lines of new business, putting further stress on their balance sheets. If things get rough they can, after all, rely on being able to sell more Treasuries and if that market freezes up, they will count on the Fed to ride to the rescue.

As Rajan and his colleagues point out, normalization after post-2008 QE may never have happened. But history is moving fast. In the wake of second round of gigantic balance sheet expansion we are now embarked on serious monetary tightening, and not just in the US. The stakes are high. A UK-style âincidentâ played out in the US Treasury market would rock the global financial system.

***

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. Iâm glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters.

Several times per week, paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

If you would like to join the group of supporters there are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.November 13, 2022

Chartbook #171 Finance and the polycrisis (2) The global housing downturn.

In this precarious moment – in the fourth quarter of 2022, two years into the recovery from COVID – of all the forces driving towards an abrupt and disruptive global slowdown, by far the largest is the threat of a global housing shock.

There was some anxiety even before 2020 about escalating house prices in hot spots around the world, but the pandemic delivered an unprecedented jolt to housing markets. In 2020 and 2021 house prices surged, causing the IMF to sound the alarm in its October 2021 Financial Stability Report.

In the second half of 2021 inflation accelerated due to supply shocks and in 2022 that surge broadened. With interest rates being pushed up with unprecedented speed, the question now is whether after the unprecedented shutdowns of 2020 and the rapid rebound of 2021, the winter of 2022-3 will see the beginning of a global housing crash. If this were to occur, the impact would be huge.

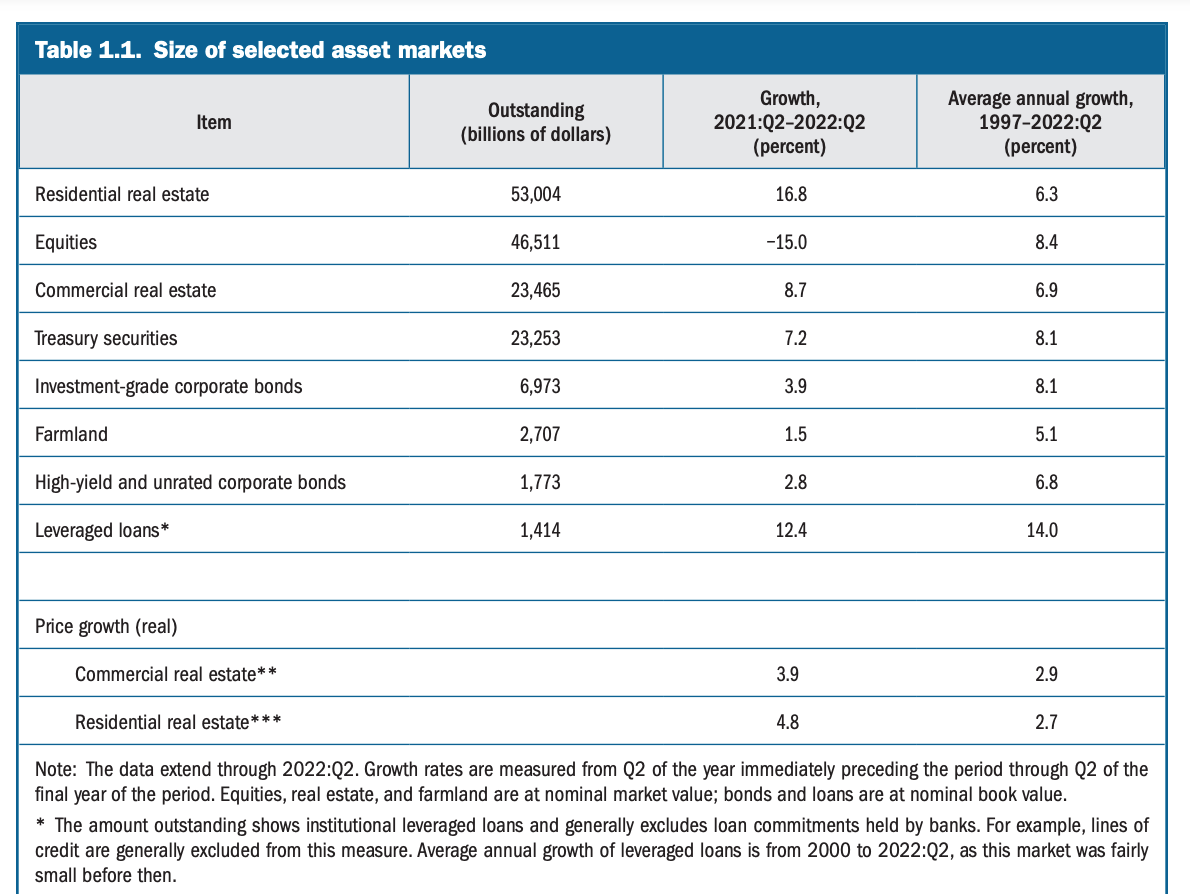

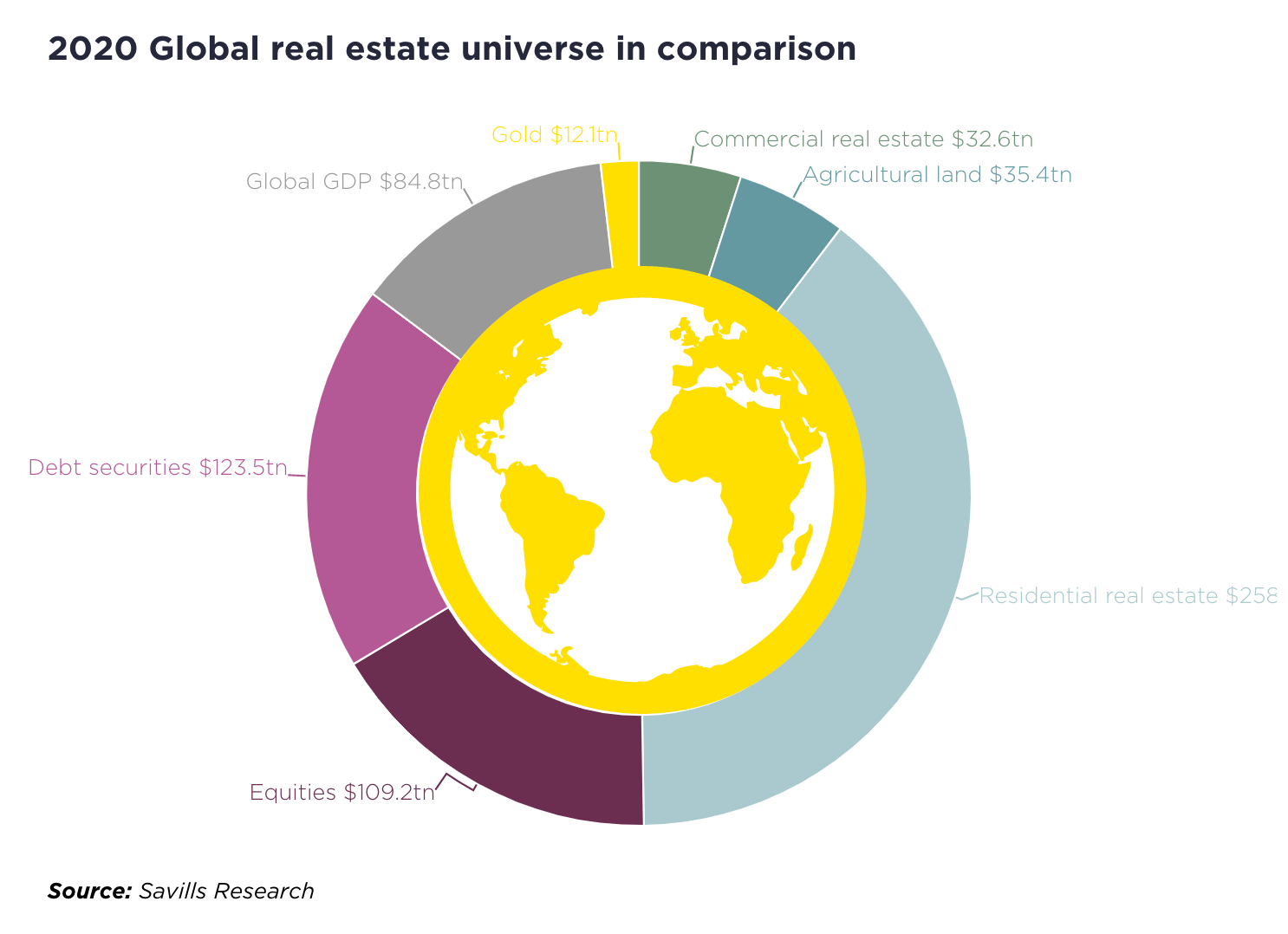

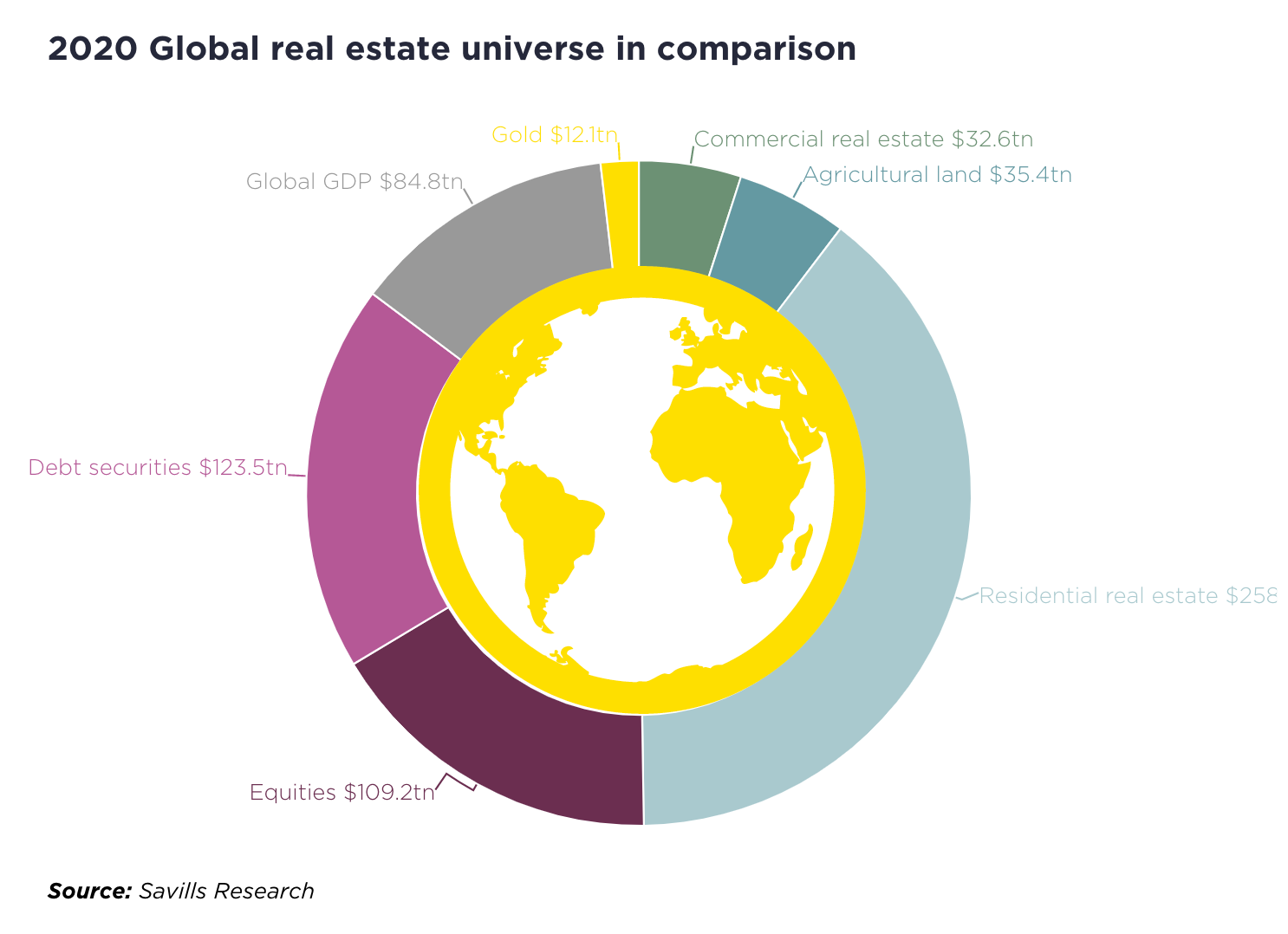

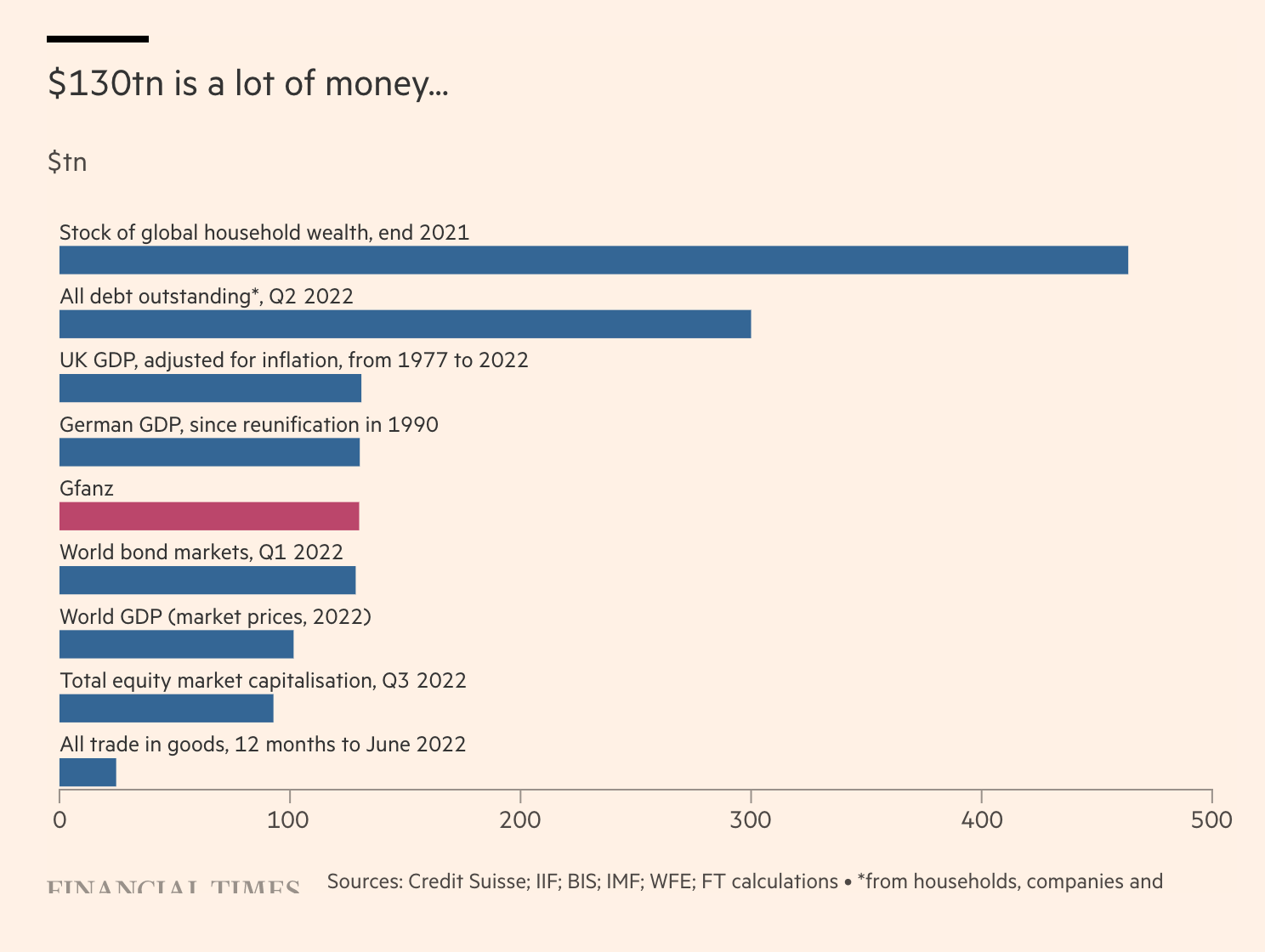

In the global economy there are three really large asset classes: the equities issued by corporations ($109 trillion); the debt securities issued by corporations and governments ($123 trillion); and real estate, which is dominated by residential real estate, valued worldwide at $258 trillion. Commercial real estate ($32.6 trillion) and agricultural land add another $68 trillion. If economic news were reported more sensibly, indices of global real estate would figure every day alongside the S&P500 and the Nasdaq. The surge in global house prices in 2019-2021 added tens of trillions to measured global wealth. If that unwinds it will deliver a huge recessionary shock.

In regional terms, as a first approximation, think of global real estate assets as split four ways, with the US, China and the EU each accounting for c. 20-22 percent and 35 percent or so belonging to the rest of the world.

The housing complex is at the heart of the capitalist economy. Construction is a major industry worldwide. It is one of the classic drivers of the business-cycle. But beyond the constructive industry itself, the influence of housing as an asset class is pervasive. Compared to equities or debt securities, residential real estate is owned in a relatively decentralized way. Homeownership defines the middle class. And for the majority of households in that class, those with any measurable net worth, the home is the main marketable asset.

Middle-class households are for the most part undiversified and unhedged speculators in one asset, their home. Furthermore, since homes are the only asset that most households can use as collateral, they pile on leverage. For households, as for firms, leverage promises outsized gains, but also brings with it serious risks in the event of a downturn. Mortgage and rental payments are generally the largest single item in household budgets. And household spending, which accounts for 60 percent of GDP in a typical OECD member, is also responsive to perceived household wealth and thus to home equity – the balance between home prices and the mortgages secured on it. For all of these reasons, a surge in mortgage rates and/or a slump in house prices is a very big deal for the world economy and for society more generally.

To cushion these risks, many rich societies have a middle-class welfare state that subsidies and supports homeownership, through tax breaks, subsidized housing credit, protections for mortgage debtors and incentives for the private construction of rental accommodation. Homeownership and rental accommodation are at the heart of political economy. These systems are regularly tested by the cyclicality of the real estate market itself, where boom and bust cycles have alternated back to the 19th century and by macroeconomic shocks like the one we are currently experiencing. The kind of policy-driven interest rate hike we are seeing in 2022 sends a shockwave through the system.

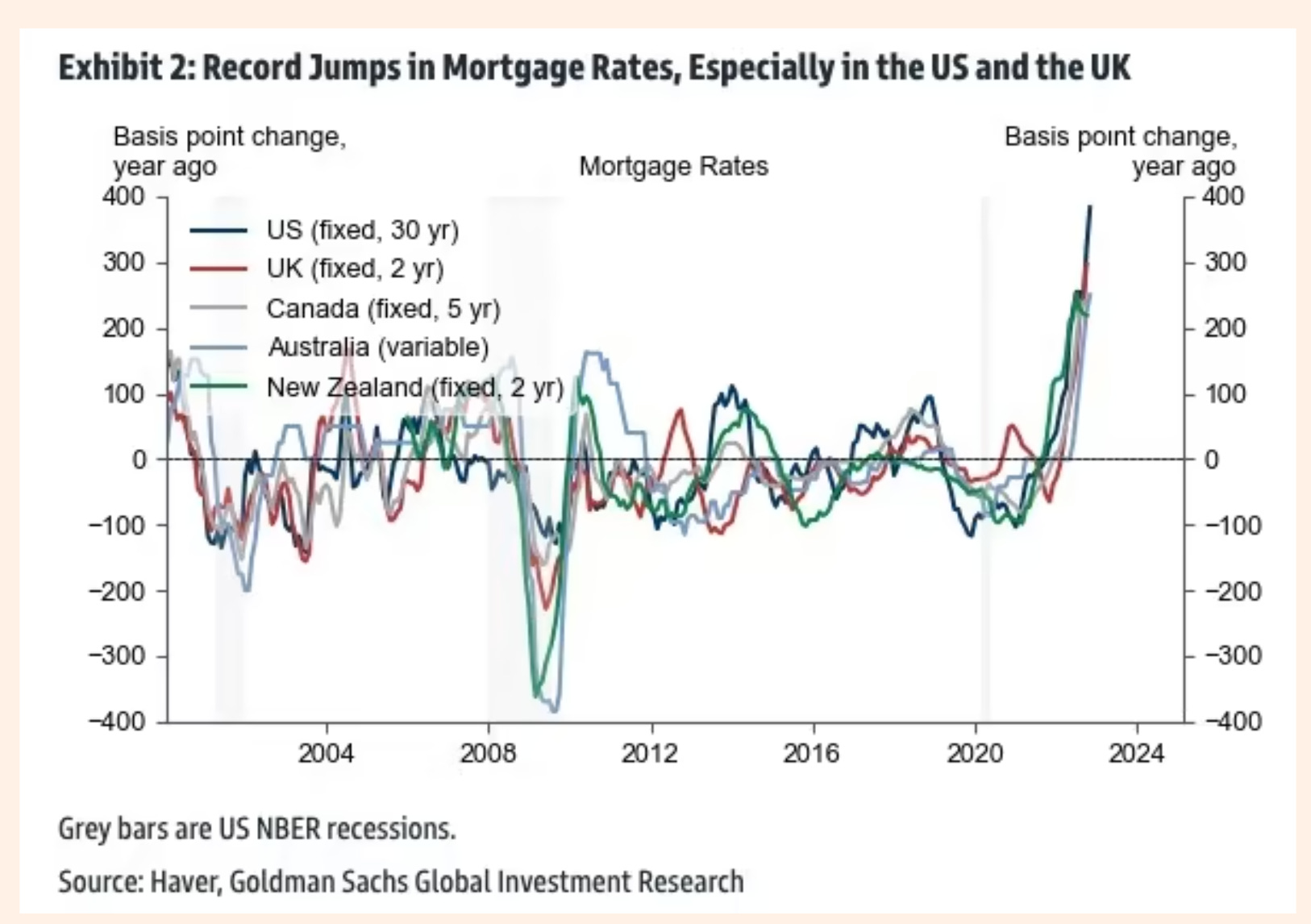

Source: Goldman Sachs via FT Alphaville

The current surge in mortgage costs across much of the english-speaking world, is the most dramatic seen in decades. In the US in the course of barely more than half a year mortgage rates have more than doubled, crossing 7 percent for a 30-year fixed in September.

The impact of rising prices and rising interest rates is to crush affordability. An index of US housing costs in relation to income is at highs not seen since the era of Paul Volcker.

âEveryone is coming to the view that prices are going to decline,â said Mark Zandi, chief economist for Moodyâs Analytics. âUntil that happens, nobody is going to buyâ https://t.co/I3S7Hp7IJy pic.twitter.com/7O43aPEdqL

— Jim Russell (@ProducerCities) September 22, 2022

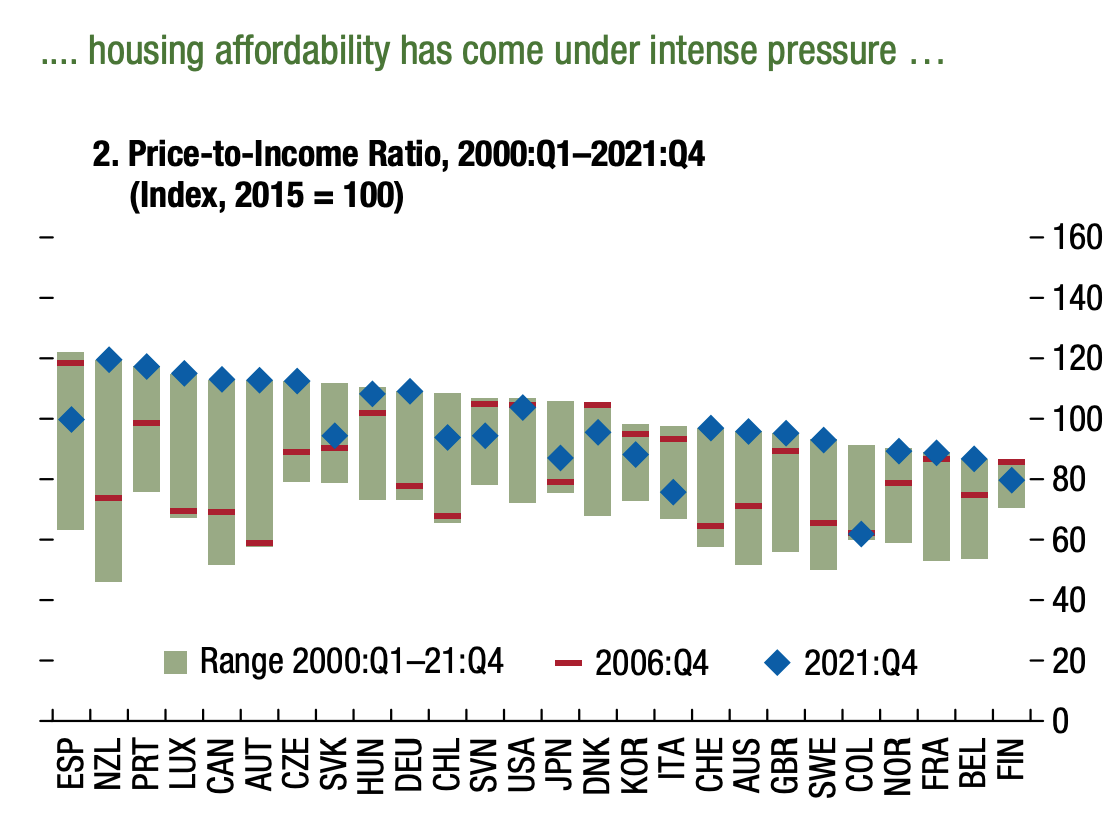

Around the world in 2022 house prices relative to incomes hit historic highs.

Source: IMF GFSR Oct 2022

Unsurprisingly, given these pressures, demand for mortgages is collapsing. As the Economist magazine describes it, the math is simple:

Someone who a year ago could afford to put $1,800 a month towards a 30-year mortgage. Back then they could have borrowed $420,000. Today the payment is enough for a loan of $280,000: 33% less. From Stockholm to Sydney the buying power of borrowers is collapsing. That makes it harder for new buyers to afford homes, depressing demand, and can squeeze the finances of existing owners who, if they are unlucky, may be forced to sell.

By October 2022 reports were coming in from across the United States of rapidly falling housing prices.

— Nick Gerli (@nickgerli1) October 15, 2022

Fastest Housing Crash Markets.

15% Drop in Sale Prices in Oakland, San Jose, & Austin in ONLY 5 MONTHS.

That's warp speed for a Housing Crash. Some of these markets could be down 20-30% by Year End.pic.twitter.com/QZsE1pwngl

The very fact that house prices are falling reverses the psychology of the market. As one housing market expert told the FT:

âThe fact of prices declining rather than rising is a watershed moment ⦠We really havenât seen anything like this since 2010 or 2011. [â.â.â.â] This summer marked the end of that long bull run for home value appreciation in the US.â

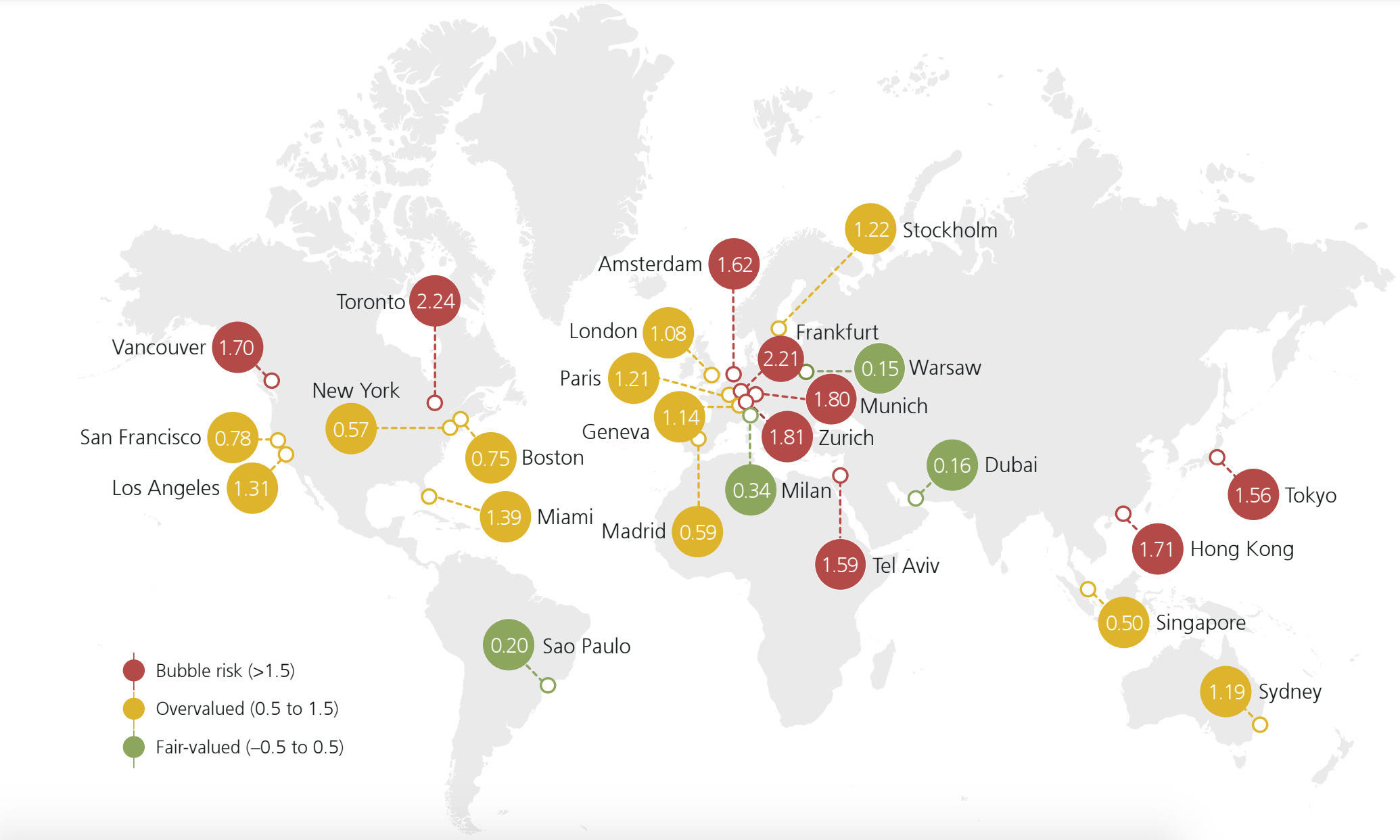

But the US is far from being the most overpriced in the world. Nor is London the greatest hotspot. Canada is probably the most overheated market and it is seeing a savage downturn. According to the FT, Toronto has seen a 96 per cent nosedive in single family home sales and an 89 per cent fall for condos. Across the country as a whole condo prices are down by 9% since the start of the year. In Europe, Amsterdam, Frankfurt, Munich and Zurich, all look set for a selloff, as do Hong Kong and Tokyo in Asia.

Source: UBS

It used to be said that in the United States, housing was the business-cycle. This worked through construction investment. In China this is still to a considerable extent true. But in the West, since the early 2000s, as housing construction has declined as a share of gdp, the link has attenuated. What matters more, as Mian, Rao and Sufi argue, is the impact on household balance sheets and thus on consumption. Most dangerous of all, as Jorda, Schularick and Taylor have argued in various papers, is the potential for a housing setback to trigger a comprehensive financial crisis.

That was the horror scenario that played out in 2008. In 2021 the Chinese regime deliberately pricked its housing bubble and is now struggling to catch the pieces as they fall. How large the impact will be both at home and abroad remains to be seen. That will be the subject of a subsequent post. For the rest of the world a full-scale mortgage-driven banking crisis does not seem like a likely scenario.

First and foremost, mortgage lender seem more robust. Banks in Europe are more tightly regulated. And in the US the entire mortgage finance system has shifted from universal banks like Citi or Bank of America, to non-bank mortgage providers backstopped by Fannie Mae and Freddie Mac, the government-sponsored mortgage banks. Weaker non-bank mortgage lenders in the US are already beginning to fail, but the risks of systemic contagion seem limited, at least so far. Fully two-thirds of US mortgage are today securitized by way of the GSEs, allowing the vast majority of US home buyers to borrow on favorable and fixed terms over a 30 year term.

Furthermore, though the real estate market has boomed in recent years, the deleveraging that occurred after 2008 significantly reduced the overall burden of household debt in the US. Since 2008 mortgage lending in the US has again been concentrated on those with the top creditor scores. In 2019 60% of mortgages went to borrowers with scores above 760. And in the first quarter of 2021 73% of mortgages went to borrowers with very good credit scores. Only 1.4% were granted to subprime borrowers. Even if home prices were to fall significantly, home equity remains strong, so that the percentage of households that would find themselves underwater with negative equity is small. Even a 15 percent price decline is predicted to leave only 3.7 percent of households underwater compared to 28 percent in 2011.

Source: Economist

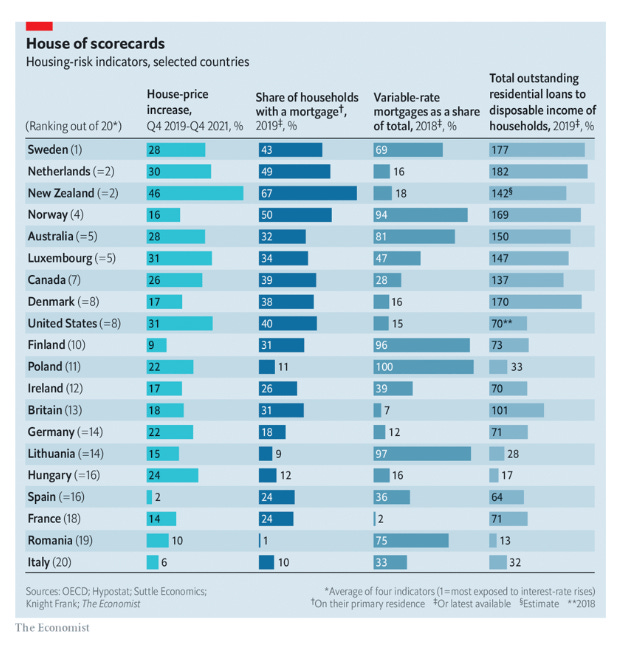

The risk of an acute housing driven crisis is greater in Canada, which is already experiencing dramatic falls in house prices, and in South Korea and the Nordic countries where household debt ratios are very elevated. Swedenâs central-bank boss has likened his situation to âsitting on top of a volcanoâ. 80 percent of Swedish loans have rates fixed for two years or less. Half of all New Zealands mortgages are due for refinancing in 2022. Millions of British homeowners could find themselves under severe pressure from rising mortgage bills. The IMF, meanwhile, is most concerned about emerging markets, i.e. first and foremost China. The IMFâs outlook has darkened considerably in the last 12 months and in its worst case scenarios, housing prices in emerging markets crash by as much as 25 percent. That would be a devastating blow to the emerging global middle class.

Source: IMF

The economic shock delivered by a global housing downturn will be severe. Nothing would more rapidly extinguish the flames of inflation. But the shock will not be confined to the economic sphere. If the polycrisis is also a legitimacy crisis, then amongst the various shocks threatening elite claims to authority, the housing situation is far more serious than, for instance, the debacle in crypto, or even the transitory problem of inflation.

As Robin Wigglesworth at FT Alphaville notes

Mortgage holders tend to be wealthier, and tend to vote. Mortgage rates are therefore uniquely politically sensitive, in a way that other forms of debt are not. Normies donât actually care what 10-year government bond yields do; they do care about the cost of their mortgage.

This raises the question: Will the threat of an impending housing crisis reveal a self-correcting political economy? Will central banks be able to continue raising rates despite the pain that this causes, or will central bankers flinch?

Wigglesworth asks whether we are about to enter, not the age of fiscal or even financial dominance, but what he dubs âmortgage dominanceâ, in which the sensitivity of over-borrowed middle-classes to higher rates puts a constraint on monetary policy. Wigglesworth cites several example from Scandinavia and Canada, where central bankers are already expressing concern about the impact of their tightening on policy.

But it is not Canada or Norway that sets interest rates globally, it is the Fed. And when it comes to mortgage finance the US is the exception. The state-subsidized 30-year fixed mortgage system in the US, backstopped by the so-called Government-Sponsored Enterprises, insulates the majority of US homeowners against any immediate hike in interest costs. This reduces the effectiveness of interest rates as a policy tool but also frees the Fed from âmortgage dominanceâ. Indeed, the Fed itself, thanks to years of asset purchases, owns a quarter of the mortgage-backed securities issued by Fannie Mae and Freddie Mac. All in all, the US mortgage system is something of a closed loop incorporating the finance of middle class home ownership onto the public balance sheet. In that system any losses from defaulting mortgages are ultimately covered by the public balance sheet and thus by taxpayers. But those costs are largely hidden from public sight and have far lower political salience than mortgage rates themselves. So unless the US housing market tips disastrously over the coming months, donât expect political uproar to force the Fedâs hands. It will be the less-well protected homeowners in the rest of the world who will feel the brunt of the pressure.

***

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. Iâm glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button.

Several times per week, paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

There are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.To get the full Top Links and become a supporter of Chartbook, click here

November 12, 2022

Chartbook #170 Finance and the polycrisis (1): What bends? What breaks? What implodes?

As interest rates are driven up to counter inflation, as geopolitical tensions rise and commodity prices grind against each other, the world economy is in a labile place. Under this kind of pressure, what bends, what breaks and what simply implodes?

Amongst the general categories of risks there are:

Recession – a painful but âorderlyâ contraction of economic activity.Big shifts in balance of payments, triggering lurching adjustments in capital flows.The risk of acute energy crises whether due to spiraling prices or sudden stops to supply, these may compound (a) recessions by forcing a shutdown in production, (b) inflict social crises and © trigger market malfunction, thus contributing to â¦.Surprising (and unsurprising) financial âeventsâ.As the shocks add up, they raise the risk of public and private debt crises with dramatic macroeconomic fall out and ever-more complex debt renegotiations for which the institutional structure is very inadequate.The list of more specific stresses, crises and worries so far includes, debt crises like the Sri Lanka disaster, unrest around the world triggered by the surge in energy prices, the FTX implosion, the UK gilt market blow up, the longevity of the BoJ yield curve policy, apparent signs of tightening liquidity in US Treasury markets, worries about global housing markets. One might also add the slow-motion crisis in Chinese real estate, though this is to a large extent internally driven and the extent of the spillover to the rest of the world has yet to be seen.

In a chartbook mini-series I am going to try to map this complex conjuncture of shocks and crises.

***

To start with it is useful to distinguish different crisis logics. First of all we should distinguish crises that are driven (1) by fiscal and monetary policy choices, from (2) exogenous macroeconomic shocks (say in trade flows due to global energy price shocks, or Fed interest rates policy), (3) private balance sheet positioning (risky levels of leverage, or currency mismatch), and (4) the misfiring of complex financial engineering (derivatives, CLOs etc).

The importance of distinguishing between crisis logics is brought home by the narratives that have been spun about the UK Treasury market panic. This has been widely interpreted as a matter of fiscal credibility – with the lesson being that the Chancellor must fill a â50 billion pound black holeâ by hiking taxes and cutting spending.

In fact, much of the action was driven, on the one hand by the policy stance of the Bank of England and on the other hand by derivatives contracts through which pension funds multiplied their exposure to gilts. If you remove support from the gilt market by pivoting to Quantitative Tightening and you do so when the market is spring-loaded with a outsized quantity of derivatives designed to protect you against falling interest rates, then, whatever your fiscal stance, you should clearly be prepared for trouble.

It is not for nothing that Andrew Bailey of the Bank of England feels it necessary to deny on television news that he was responsible for deposing Prime Minister Truss.

To interpret a complex event like the UK financial shock as a simple morality tale of fiscal prudence is not to assert the logic of economics against feckless politics, but the contrary. It is to instrumentalize a crude interpretation of a complex event to impose the political priority of budgetary consolidation.

Getting the politics of interpretation right is important because that in turn determines how you read a factor like âFed interest rate policyâ in the UK context. For those preoccupied with nailing Truss-economics to the wall, it was crucial to discount outside influences. And that tendency was reinforced by the effort on the part of Trussâs apologists to explain away the UKâs disaster by reference to âglobal forcesâ. On the other hand, if we want to understand the UK crisis as part of the global credit cycle and do justice to the role of the Bank of England, then references to the Fedâs role in driving global tightening may actually be from from irrelevant. Both the Bank of England and the ECB are caught up in the dollar-based credit cycle.

On the other hand there are cases where applying Occamâs razor is called for. The simpler the explanation the closer to the truth it comes. One such cases is clearly the crypto-implosion. As Daniela Gabor pointed out already five years ago, FTX was a disaster waiting to happen.

5 years ago, I told you how FTX would fall https://t.co/rVgJEjtcRW

— Daniela Gabor (@DanielaGabor) November 12, 2022

It was either wrong-headed, spectacularly naive or it was a more or less deliberate conceived Ponzi scheme.

Both the UK gilt market debacle and the crypto implosion are distinct from the pressures unleashed by the turmoil in global energy markets, which leaves energy importers facing fearsome increases in costs and spiraling bills for energy subsidies. These really are classic macroeconomic/policy-driven shocks that trigger balance of payments crises, devaluations etc.

But these macroeconomic pressures may be compounded by elements that belong more squarely in the macrofinancial realm – by way of financial engineering or balance sheet effects. For instance, both the UK and Germany can âaffordâ the higher import bills due to the surge in oil and gas prices. Neither the Euro nor the sterling will go into free fall on the news from energy markets. What Europeans are struggling with, are social crises on account of the inability of those on tight budgets to afford huge energy bills, a nasty bout of inflation and financial crises. In a matter of weeks energy supply companies in both Germany and the UK were bankrupted by the maturity mismatch on their balance sheets between long-term energy supply contracts with consumers and surging prices on spot markets. The result were expensive bailouts that added to the stress on government balance sheets.

Meanwhile, in energy markets themselves, it was clear already at the start of the year that trading houses would struggle to access the liquidity they need to make markets in commodities whose value has suddenly multiplied. Meanwhile, Bangladesh, Sri Lanka and Pakistan cannot buy LNG cargos at all, not only because they are too expensive, but because traders do not regard them as creditworthy clients. When there is no shortage of people clamoring for LNG cargos, they are the last in line.

Needless to say, all these macrofinancial complications of energy crises would pale by comparison with a âliquidity hiccupâ in the US Treasury market as in 2020, or a meltdown in global mortgage finance driven by a loss of short-term funding, as in 2008.

***