Adam Tooze's Blog, page 7

February 5, 2023

Chartbook #194 Can Beijing halt China’s housing avalanche? The most important economic-policy question for 2023?

Source: FT

Few things matter more for the world economy in 2023 than China’s fortunes. Not since the reform period began, have there been more serious question marks over the trajectory of China’s growth.

The 2015-6 near-miss crisis, when the RMB depreciated and capital flooded out of China was a more acute moment of danger. Fear of a repetition still hangs over the current scene. But in 2015-6, the growth engine was not spluttering to the same degree. China did not face the kind of labour market pressures it does today, with youth unemployment rising towards 20 percent and graduates uncertain of their future employment. Nor was China in 2015/6 facing an avalanche in its real estate sector.

As 2023 begins, in its Article IV report on China the IMF rather blandly remarks:

As of November 2022, developers that have already defaulted or are likely to default—with average bond prices below 40 percent of face value— represented 38 percent of the 2020 market share of firms with available bond pricing. Despite these strains, the pace of restructuring has been slow, partially hampered by the potential for very large losses for pre-sale homebuyers due to the large backlog of troubled projects. The sector’s contraction is also leading to strains in local governments. Falling land sale revenues have reduced their fiscal capacity at the same time as local government financing vehicles (LGFVs) have also significantly increased land purchases.

However this is calculated precisely, a 38 percent default rate is bad news!

Everyone has long known that the pre-2021 boom in real estate was unsustainable. As the IMF points out

China’s residential housing sales averaged 1.5-1.6 billion square meters per year from 2018-2021, about 30-50 percent higher than estimated annual demand for the next few years based on demographic and housing stock factors.2

In a worrying signs of overheating, more and more floor space was at the initial stage of construction, whilst the pace of completions remained steady at c. 800 million square meters per annum, as it had been for more than a decade. There was a mounting gap between aspirations and the reality of delivery.

The construction boom, in turn, was the main driver of China’s massively unbalanced, investment-heavy, consumption-poor growth. Though, in recent years, the investment share has stabilized and consumption has begun to increase, the imbalance remains huge.

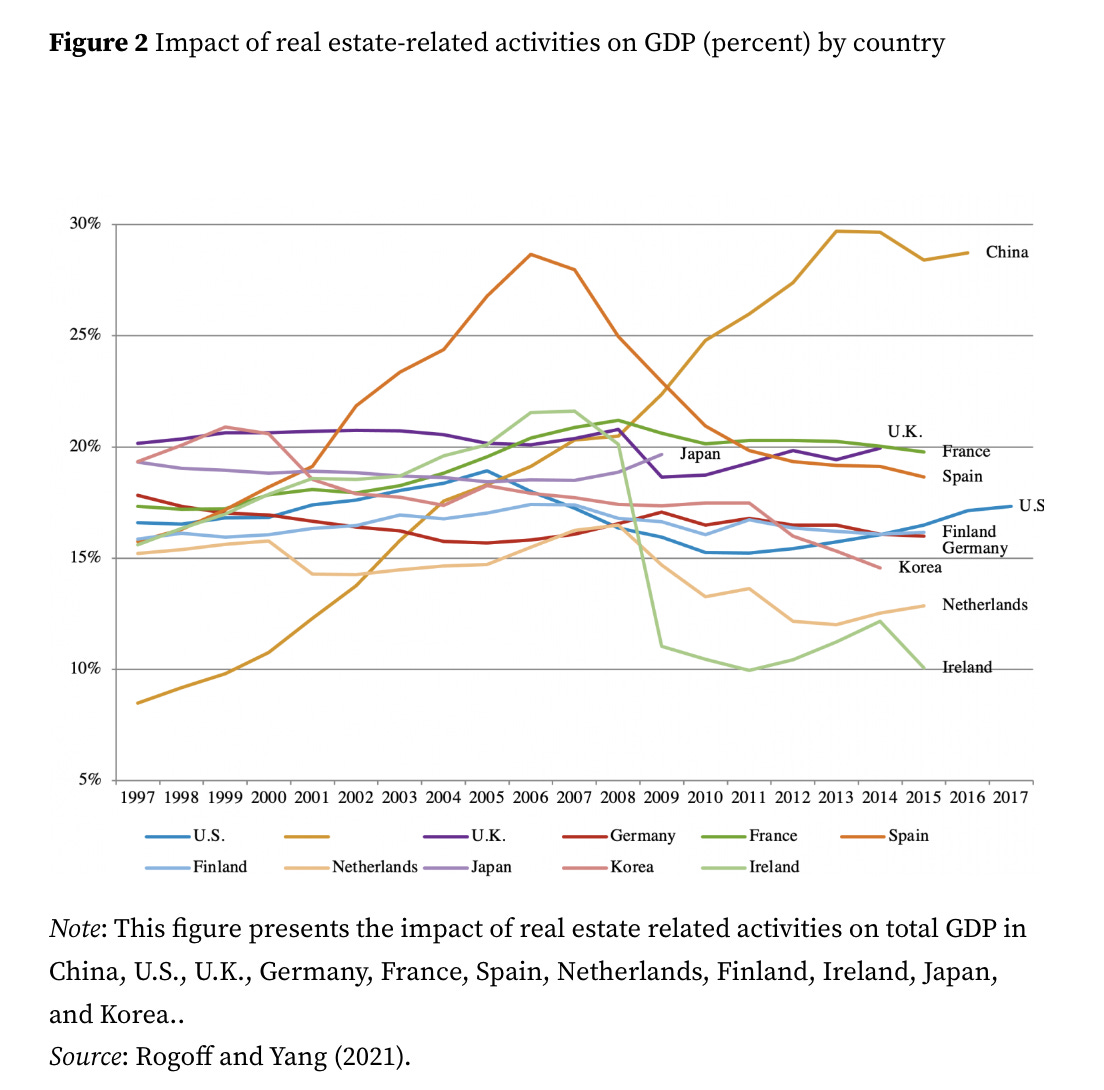

The latest estimates by Rogoff and Yang 2022 suggest that real estate development, directly and indirectly, has driven 25 percent of total economic activity in China.

Ever since the industrial revolution began in earnest in the 19th century, urbanization and real estate investment has driven surges of growth. Paris was transformed. Cities like Berlin and Chicago sprouted in the late 19th century. Stalinism stamped a new urban civilization into existence in the 1930s. Western Europe and Japan experienced rocket-ship growth after 1945 and a transformation of their urban landscapes. China has taken the dynamic of urbanization and growth to a new dimension.

Source: Rogoff 2021

In the late 1990s China still did not have a large private real estate market and real estate accounted for c. 8 percent of GDP. Over the following quarter century China experienced a revolution.

On the basis of census data, Rogoff and Yang estimate that 43 percent of all homes in China had been built since 2010, 68 percent since 2000 and 88 percent since 1990. If you put this in relation to total population it implies that in a single generation, China has built enough homes to house a billion people. The fabric of domestic life has been completely churned over in a matter of decades.

It is the demand for concrete and steel generated by this giant construction boom that has made Chinese growth so dirty. It is important to emphasize this point. As a driver of energy consumption, the rehousing of hundreds of millions of people, dwarfs China’s role as an exporter. It is important, of course, for Europeans and Americans to remind ourselves that in the course of globalization we have exported a substantial chunk of our pollution, much of it to China. But to imagine that it is our out-sourced emissions that drive China’s massive surge in energy consumption and CO2 emissions is to succumb to anachronistic Western-centric thinking. It is domestic forces that drive China’s growth.

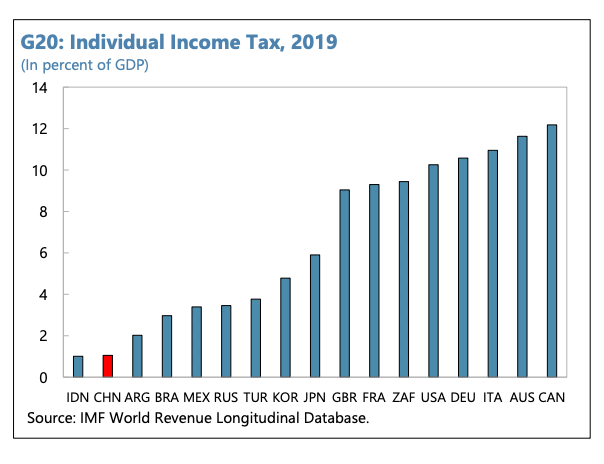

Will 2023 be the year in which China breaks with its heavy-industrial, construction-driven growth-model? Western experts, certainly, are agreed that what China needs is not more physical construction but a burst of institutional state-building. What China needs is a welfare state adequate to its new status as a high-middle income country and that will require a new fiscal constitution. Amongst G20 members China and India rival each other for the lowest share of income tax in GDP.

But whether or not China is to embark on a new growth path, the ongoing crisis in real estate has to be addressed, not to restart the unsustainable boom, but to put out the fire that threatens to consume the sector. Over the course of 2022, housing starts and sales crashed by 40 percent year on year.

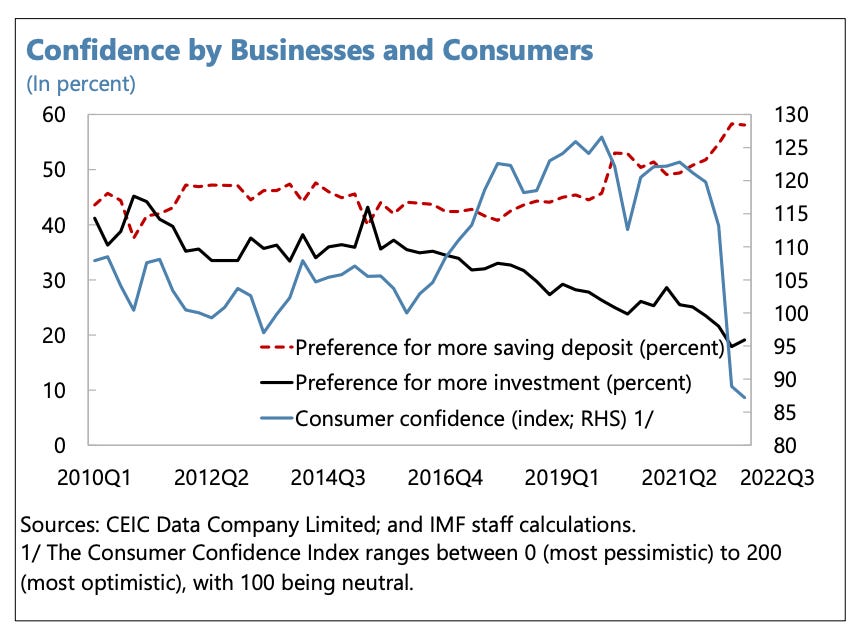

With most households having the majority of their wealth tied up in real estate. It is little wonder that consumer confidence went off a cliff in 2022. If you want a simple explanation for why zero COVID was abandoned, look at this data.

The fear of lockdowns & the imploding real estate bubble made for a truly depressing mixture. Lifting the lockdowns will help to raise the mood. But the pain in the real estate sector remains. Even the best possible outcome – a fully rebalanced recovery – cannot begin without a stabilization in real estate.

On the question of stabilization, China’s real estate crisis is unique not just for its scale. China’s real estate crisis was long predicted. But the crisis did not come about as a result of a “natural” business cycle, as, for instance, in the North Atlantic housing crash in 2007-8. In China the crisis was brought on deliberately in 2021-2022 in an effort to deflate the bubble preemptively. In this respect the situation is unique in economic history. Not only has there never been a housing boom on this scale. But the attempt to deliberately curb it and bring it under control is also unique in its ambition.

As Robin Wigglesworth points out, the IMF report shows the Chinese authorities in a relatively calm mood. It is tempting for Western observers to read this as window-dressing, or whistling in the dark to steady your nerves. We should not rule out the possibility that Beijing truly believes that it can contain and manage the fallout from a wind-down, which it has itself engineered. Abandoning the zero-covid policy, with all its implications, is the first and most important decision, necessary to stabilizing the real estate sector.

Across the board in 2022 Beijing shifted from a restrictive and deflationary course to one of re-stimulating the real estate economy.

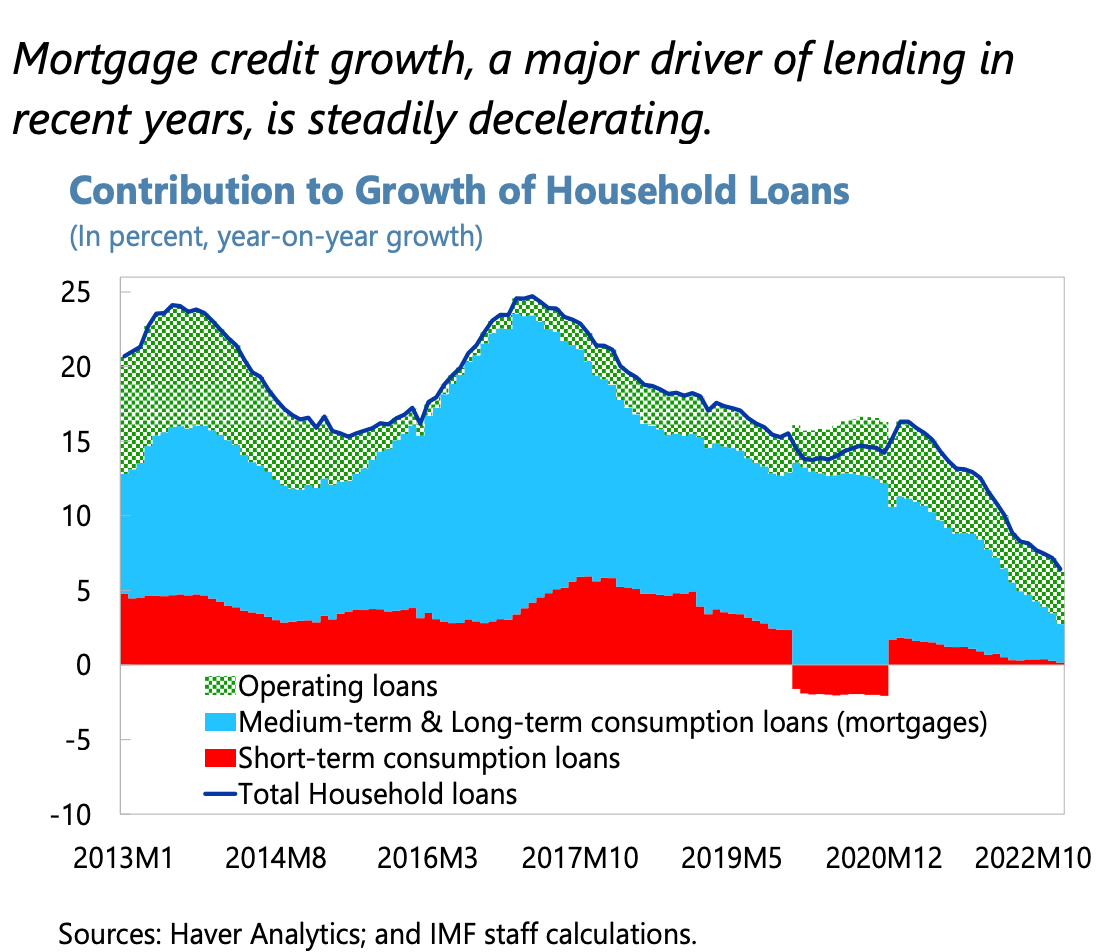

The temptation will be great to use classic monetary policy tools to revive the housing market. A sharp decline in mortgage lending and borrowing from banks to Chinese households has been a key driver of the real estate crash since 2021.

Falling mortgage borrowing has squeezed Total Social Financing, one of the key indicators of economic activity in China’s hybrid public-private, mixed economy.

But should one welcome a revival in mortgage lending? Certainly, reversing the tough red lines policy on real estate credit adopted in 2021 would suggest pragmatism. But it would also demonstrate a failure to break with the existing growth model. As Michael Pettis has tirelessly explained, Beijing would be caught up in repeating the strategy that led China into the unsustainable boom in the first place. Managing the crisis like that would be impressive exercise in what used to be called “fine-tuning”, but in strategic terms it would be a dead end.

A strategy that was directed not towards restarting the boom, but towards cauterizing the wound and restoring a platform of confidence, would instead focus on the most painful element of the crisis, the millions of Chinese households who have made large down-payments on apartments that are only partially completed or not even begun. As the IMF comments:

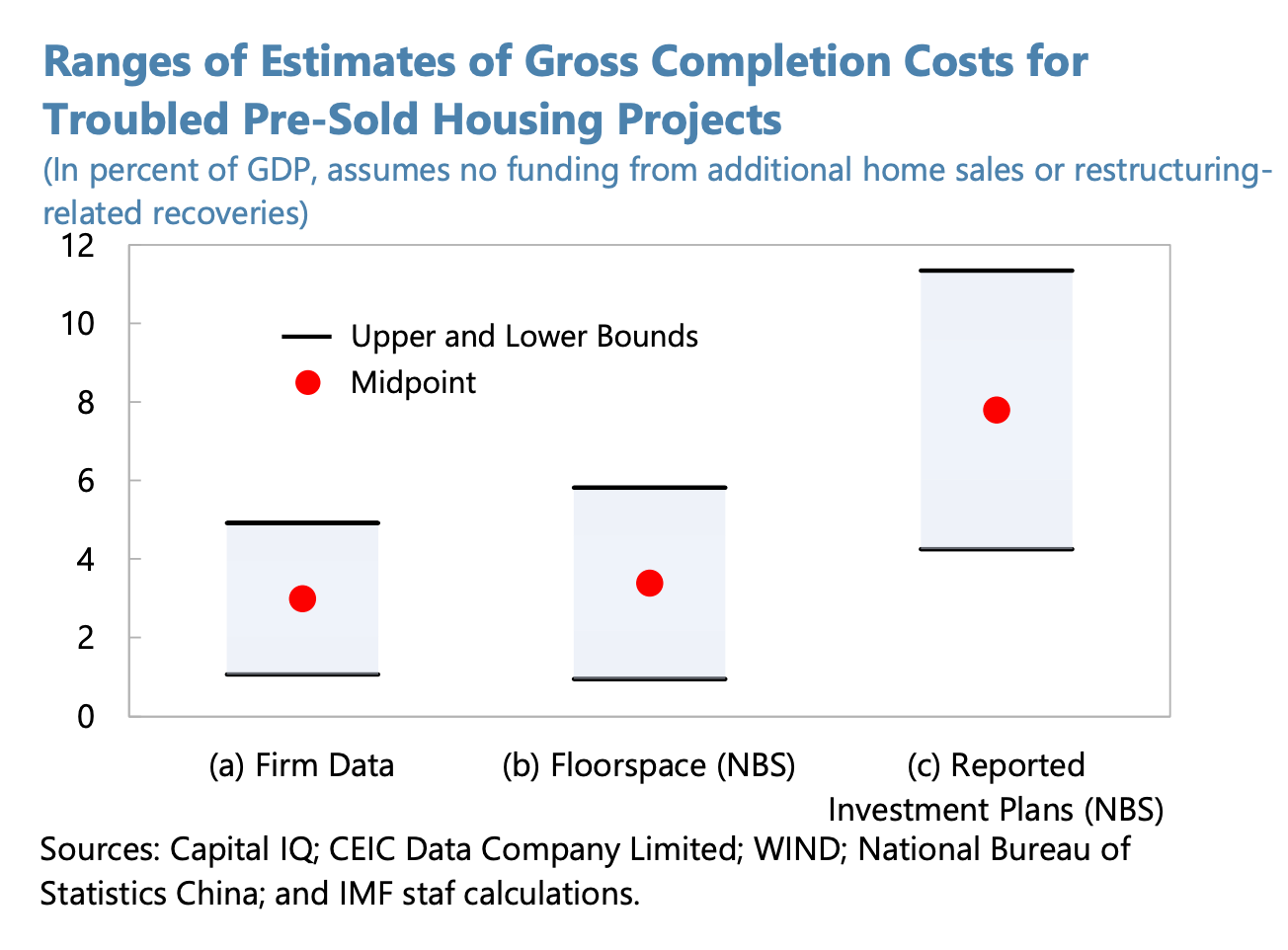

A key underlying challenge to restoring confidence and securing an orderly transition is the large backlog of partially built housing. In the years prior to the crisis, developers expanded their use of presales of unfinished homes as a de facto form of financing, in part by using home purchase deposits to cover the cost of unrelated projects. The annual ratio of housing pre-sales to completions—an indicator of the growth of unfinished housing—reached an average ratio of two in the last four years, up from about one in the decade through 2015. Residential real estate under construction as a result reached 6.9 billion square meters at end-2021, ten times the average floor space completed by the sector each year. The slowdown in sales has sharply limited the availability of funds to finish construction on many pre-sold projects, particularly for distressed developers. The rising risk of non-completion for some of these projects impairs the realizable market value of developer assets, worsening their solvency and liquidity problems, and affects homebuyers’ willingness to purchase homes before they are completed. This not only limits developers’ capacity to continue investment, but risks sizeable losses for households and the banks that funded these purchases via mortgage credit. Homebuyers’ decreased confidence in the pre-sales model also limits the traction of policies aimed at stimulating housing demand. Without stabilization for pre-sold housing demand, a large segment of partially finished housing would be at risk of noncompletion. While significant data gaps make the task of estimating the cost of completing troubled developers’ partially built housing inevitably imprecise, a range of estimates suggests the cost could be significant. The average of the midpoints of three estimation approaches places the gross cost of completing distressed developers’ pre-sold projects—with no funding from additional sales or restructuring recoveries—at roughly 5 percent of GDP, with one approach implying costs well above that.

So, simply to stabilize the Chinese real estate market, not to unleash a new boom but to clean up the most serious overhang from the last few years of excess, will require a commitment of in the order of 5 percent of GDP even if the resources are perfectly targeted. That is a measure of the challenge ahead.

The stakes are immensely high. The housing boom in China since the 1990s is probably the largest single driver of wealth accumulation the world has ever seen. Stopping it was an audacious act of policy. Managing the fall out is a severe test for Beijing. If it were to succeed, it would be an example of macro-prudential economic management on a truly world historic scale. If it fails, the “China dream” promised by Xi is in jeopardy.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, click here:

February 3, 2023

Chartbook #193 Indian nation-building, Modi and the Adani crisis

The upheaval rocking the Adani business empire is one of the dramatic global developments of the last week.

I was delighted that The Wire saw fit to pick up and republish Chartbook #190. I’ve long harbored a secret ambition to join the ranks of the Wire-wallahs. Cam and I also featured the Adani story on the Pod this week.

With continuing losses on the market, the cancelation of the share sale and moves by foreign investors to clarify the extent of their exposure to Adani, it seems clear that the controversy is not going away as quickly as some predicted or hoped.

The Adani controversy is spectacular. But there is a real danger, if we address it as a question of alleged financial malpractice, that we miss the real issue. This is well brought out by the op-ed by Mihir Sharma:

… talk of cronyism misses the point. If Adani didn’t exist, the Indian government would have had to invent him: The development model we have now chosen requires risk-taking “national champions” such as the Adani Group. … Much of what Hindenburg put in its report doesn’t count as news for Indian investors. They have known for years that Adani Enterprises Ltd., the fulcrum of the Adani empire, is loaded down with debt, and that the ultimate source of its funding is remarkably opaque. Adani stock is generally thinly traded; few here will be willing to believe that Adani companies set out to defraud retail investors, even if both public sector banks and state-owned insurers have bet heavily on them. No, Indians’ real fear is something else — that Gautam Adani and his companies simply cannot do what they say they will. Can they build the roads they have promised, improve the ports they have been given, maintain the airports they won in a bid? Until now, nobody else has been able to do so.

You don’t have to agree with Sharma’s critique of “old-fashioned industrial policy”, to see the force of his point. What is really at stake here is not the purity of financial markets, but a model of economic development. Who, if anyone, can get things done?

On the massive reach of the “Two As” (The Adani and Ambani conglomerates) and their implications for India’s political economy, Arvind Subramian is, as usual, enlightening). Here a talk with The Wire about India’s growth prospects.

For a useful (and rather downbeat) macro-take on the Indian setting of the Adani crisis, I found this thread very helpful.

FDI has not contributed to gross capital formation, which speaks to the same issue. pic.twitter.com/QG66f2DqmO

— Marko Papic (@Geo_papic) January 31, 2023

For deeper historical perspective on India’s growth outlook, you may wish to pick up Ashoka Mody’s typically fiery interpretation of India’s economic development since independence, which is being released by Stanford University Press this month.

Trigger warning: Mody’s treatment is a no bolds barred attack on “India boosterism”:

Challenging prevailing narratives, Mody contends that successive post-independence leaders, starting with its first Prime Minister, Jawaharlal Nehru, failed to confront India’s true economic problems, seeking easy solutions instead. As a popular frustration grew, and corruption in politics became pervasive, India’s economic growth relied increasingly on unregulated finance and environmentally destructive construction. The rise of a violent Hindutva has buried all prior norms in civic life and public accountability.

It is particularly striking for its moral tone.

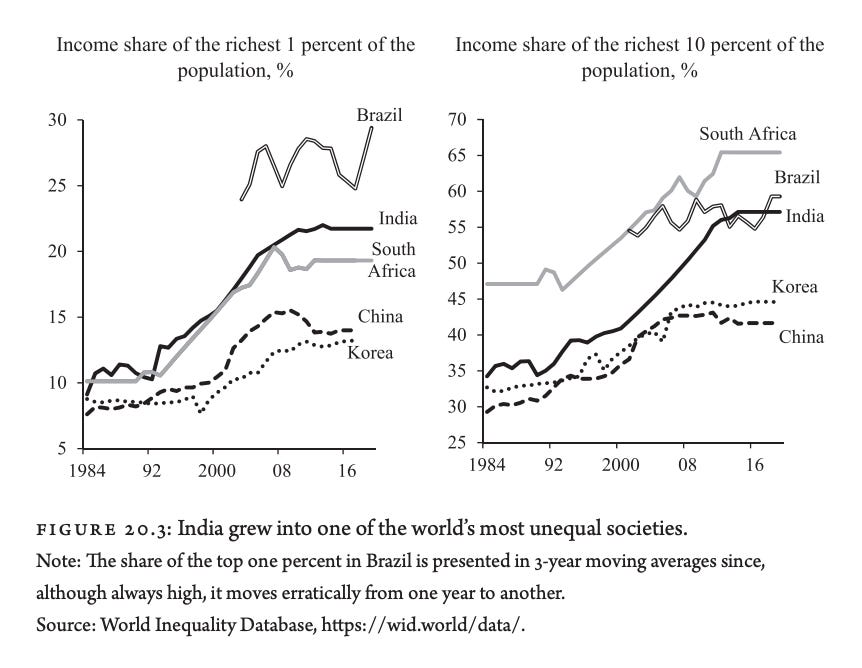

Mody does not deny the growth, which in recent decades has lifted hundreds of millions out of absolute poverty. But he also highlights mounting inequality, which now places India alongside South Africa and Brazil as one of the most unequal societies on earth;

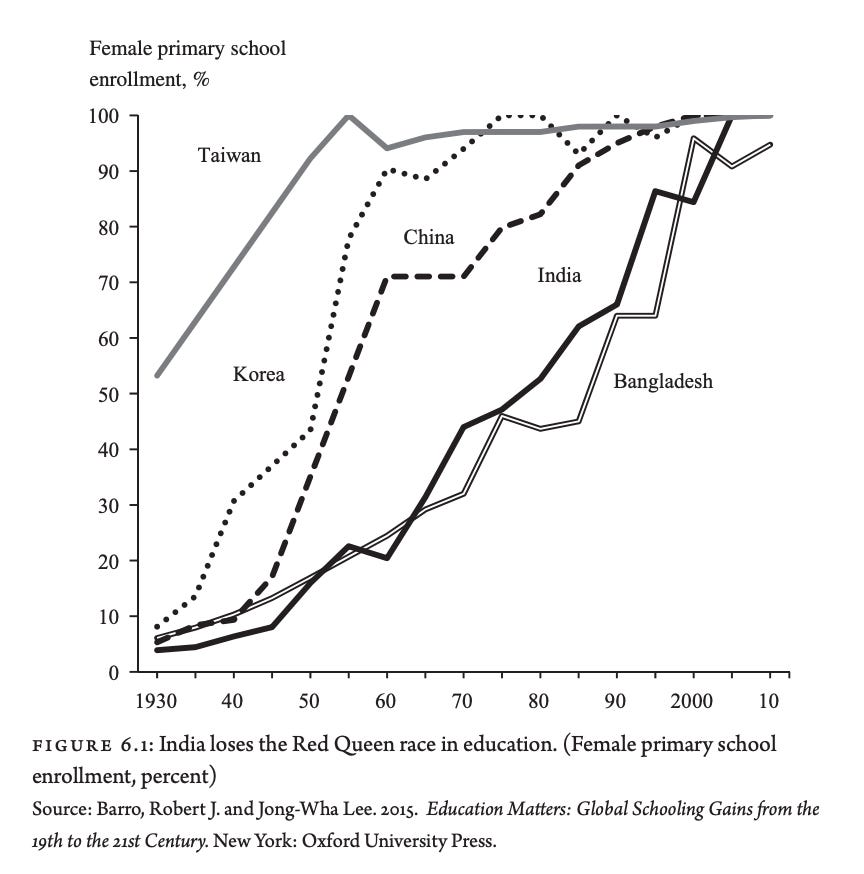

India’s failure to keep up with its Asian rivals above all in female education;

And the chronic problems of unemployment and underemployment that result from failing to find a suitably-sized niche in the global division of labour.

Compiling a list of critical voices like this, you can easily come across as though you don’t appreciate the dramatic transformation in material circumstances which India and Indians have achieved since the 1980s. In fact, a critical perspective on contemporary India and its politics acquires even more force if you reckon with the reality of spectacular change.

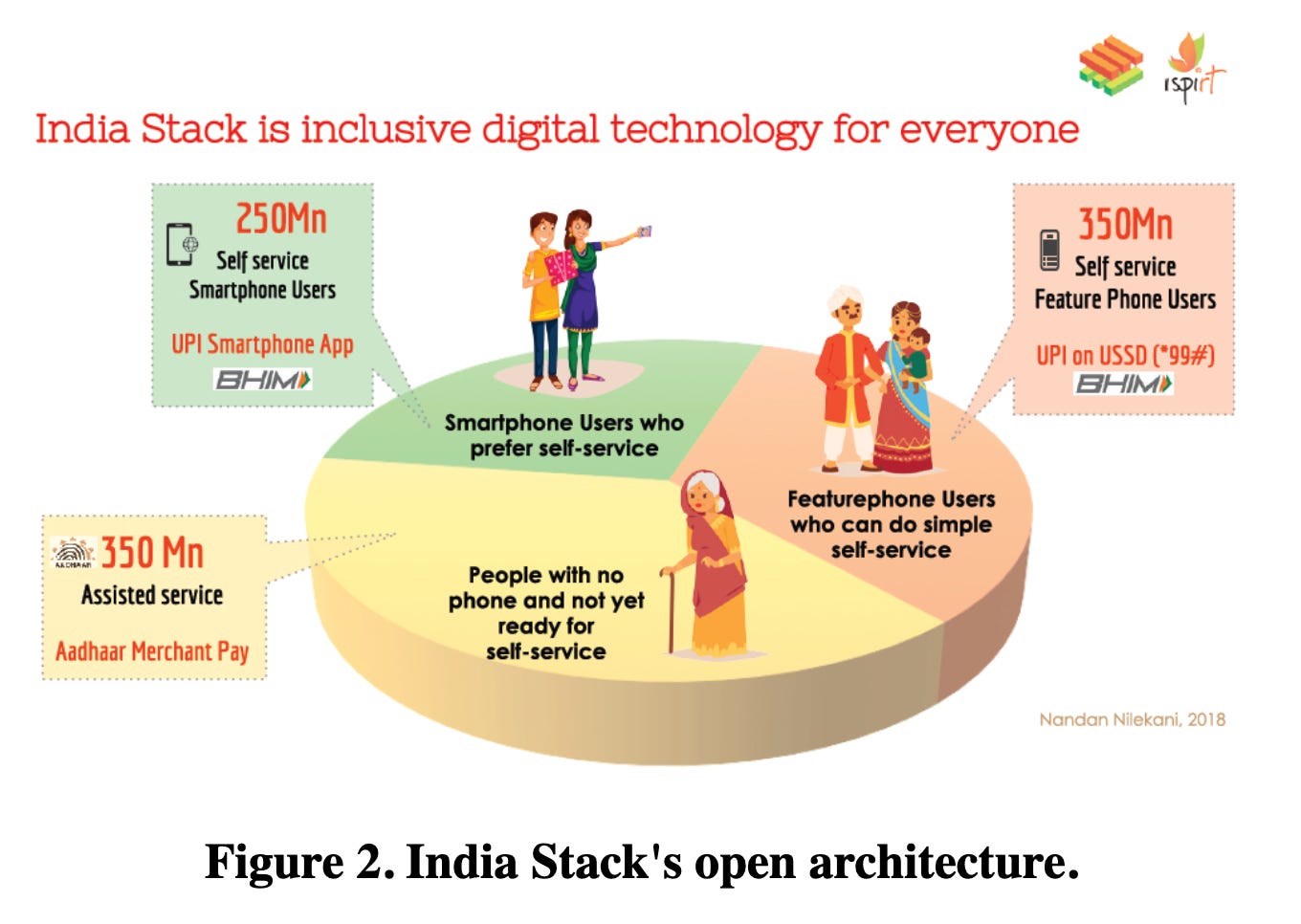

Take the remarkable digital infrastructure known as the “India Stack”, starting with the campaign for complete biometric identification set in train in 2009.

For an uninhibited celebration of digital infrastructure as a mechanism for incorporating hundreds of millions of people, both into the governmental machinery of the Indian state and a national market, see Raghavan et al 2019. The graphic below rather nicely illustrates the way in which technology maps onto a caricatured sociology of 21st-century India. A society split three ways between (1) fully empowered smart phone users, (2) families in more traditional clothing accessing services on simpler cell phones and (3) elderly village dwellers whose access is enabled indirectly by way of Aadhar-tied merchant pay terminals in every village across India.

For a more critical take, locating the Aadhaar system in the history of the Indian state, check out this piece by Kavita Dattani also from 2019. The abstract does a good job of explaining what is at stake.

In many of the ex-colonies of European empires, biometric technology systems are being built under an ethos of welfare and financial service delivery. One case in this broader trend of postcolonial governance is India’s Aadhaar and India Stack. This paper uses this case to explore how the in-sourcing of technology into means of governing, behind a front of participatory “good governance,” is contributing to the historical trajectory of citizenship regimes in India. Through claims of reducing financial “leakages,” Aadhaar, a biometric identification database consisting of fingerprint, iris scan, and photograph, has become compulsory for accessing welfare in India. The Indian government makes a case for Aadhaar using a propaganda discourse of its success, based on weak evidence. The India Stack, a set of cloud-based application programming interfaces (APIs) built on top of the Aadhaar database, offers a digital infrastructure for private companies to verify identities using Aadhaar data and to offer other “services” including “financial services.” The ability to access data, paired with a “revolving door” of individuals between state and corporations, points to an ulterior goal of both Aadhaar and the India Stack: creating winners in the corporate and financial technology sectors. The Indian corporate-state run through a “governtrepreneurism” uses Aadhaar and the India Stack as new digital technologies of governmentality to transform populations into subjects or customers.

To anyone who has to deal regularly with the antiquated pre-digital processes of governance in either the United States or many parts of Europe, the degree of digitization in India often beggars belief.

New Delhi in its role as G20 president is now putting India’s digital stack in the global spotlight. Delhi is selling “India Stack Global” as a model for tech and governance solutions worldwide, but particularly for middle- and low-income countries.

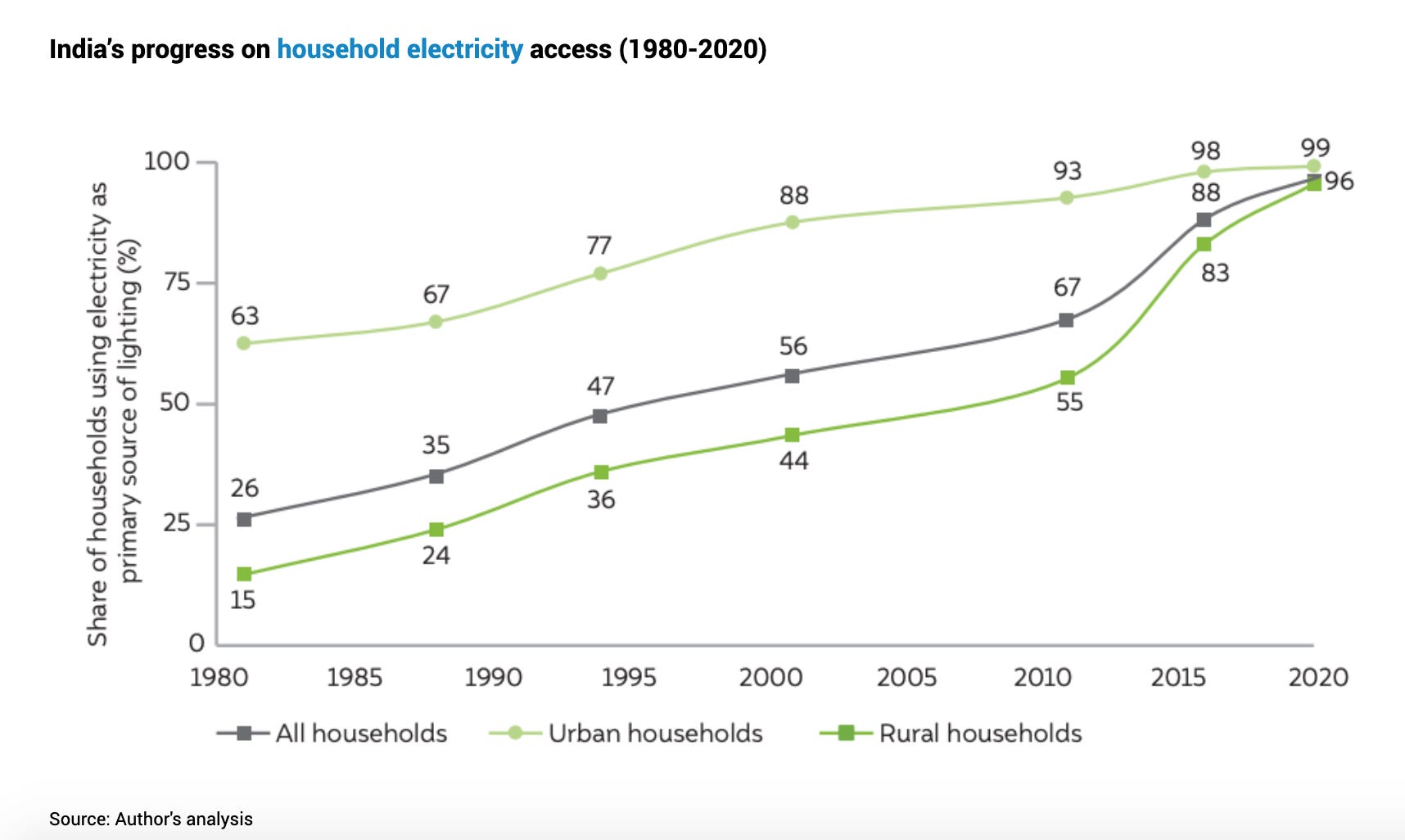

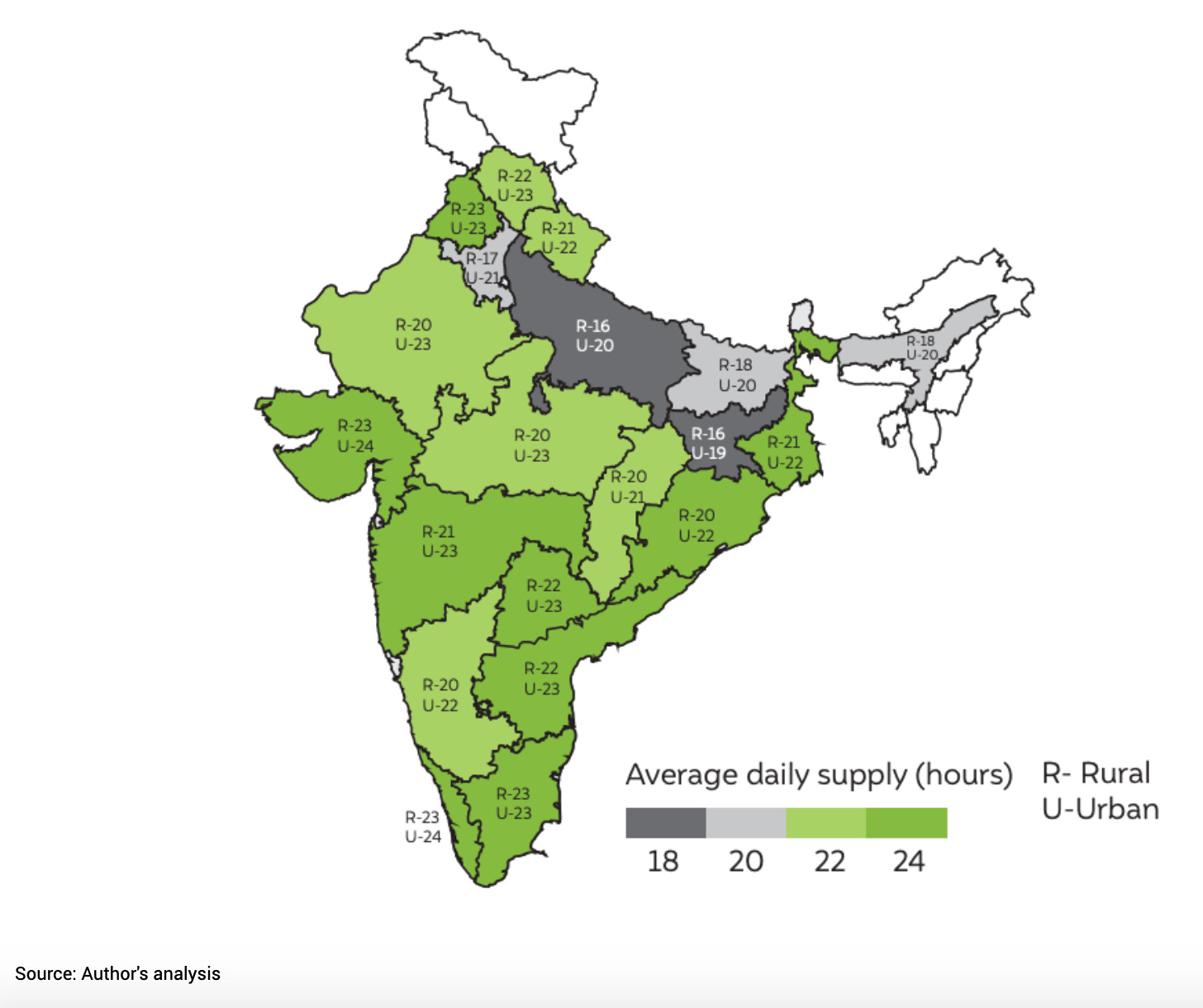

Digitization would be completely unthinkable, if it were not for the progress that has been made in the electrification of India.

These data are from the India Residential Energy Survey as analyzed by Shalu Agrawal et al of CEEW.

Of course, India’s per capita power consumption is still very low compared to China or advanced economies. Nor does connection to the grid mean 24-hour power supply. Especially in the rural North-East, power supply is intermittent. But, a generation ago, less than half of rural households in India had any connection to the power network at all. Now almost 97 percent do.

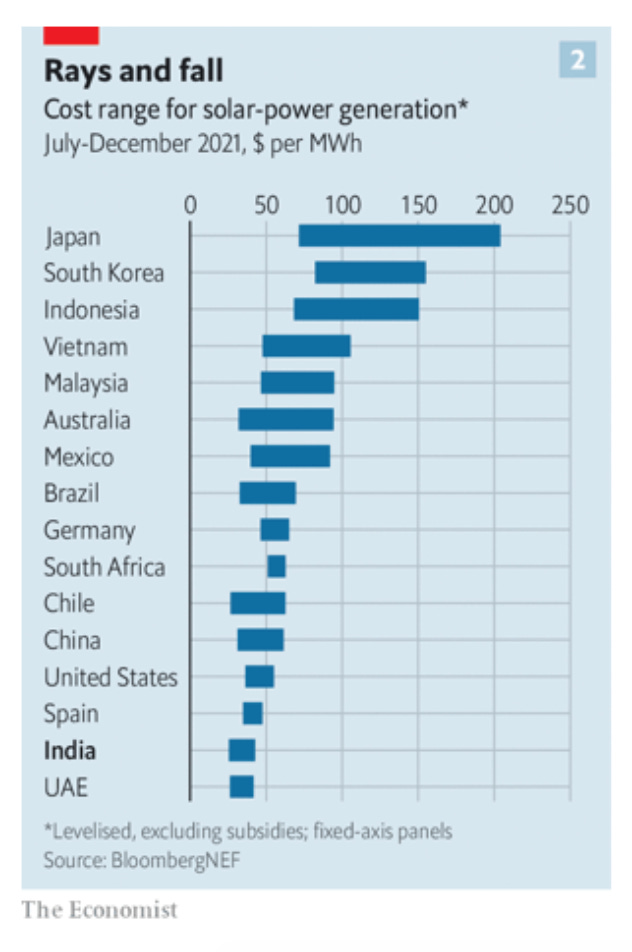

Historically, India’s energy system has been heavily dependent on coal. Gautam Adani is a coal baron notorious for his giant Australian development plans. But since PM Modi has committed India to decarbonization by 2070, Adani has also become a champion of India’s energy future as a renewable energy power house with some of the lowest per unit costs of both solar and wind in the world.

Source: Economist

Both the Ambani and Adani groups have seized on the new agenda, promising to make India a hydrogen champion and “indigenising the entire supply chain”. No longer will the value of India’s currency fluctuate with the oil price even as it did in the last 12 months.

It adds up to an impressive and coherence vision of change. Comprehensive digitization, fed by an encompassing national grid, powered by national renewable energy generation – this is nation-building for real. And it matters all the more in a society in which, as Elizabeth Chatterjee has shown us, electricity has long been seen as an integral part of the national welfare state and the project of nation-building.

However ambiguous this progress and however complex are its explanations – it clearly began decades ago – it has foundational significance for contemporary India. You cannot understand the genuine mass appeal of Prime Minister Modi and the BJP unless you recognize the way in which they have managed to associate themselves with a real and very dramatic transformation and at the same time to cast their opponents as those who for so many decades failed to deliver even the most basic services for India’s population. Following the Gujarat model of privatized infrastructure model, corporate interests are not shamefaced but front and center in this vision of nation-building. Nation-building is the key boast of the Adani group. And it is that model that is at stake in this crisis.

Ones & Tooze: How India’s Adani Group Lost Billions Overnight

When activist short-seller Hindenburg Research issued a scathing report about the

Adani Group this past week, the value of the Indian conglomerate plunged quickly. Adam and Cameron discuss Hindenburg’s findings and what they say about the Indian economy.

Find more episodes and subscribe at Foreign Policy.

February 1, 2023

Chartbook #192 On deglobalisation and polycrisis

Following a panel at Davos on deglobalisation and a flurry of comment about polycrisis, I picked up those themes in my monthly column for the FT. Thanks to my lovely editors, the piece was squeezed into the paper on Tuesday. In this newsletter I want to tease out some of the points buried in the compressed version of the op-ed. The passages in quotes are from my original draft (before editing by the FT team):

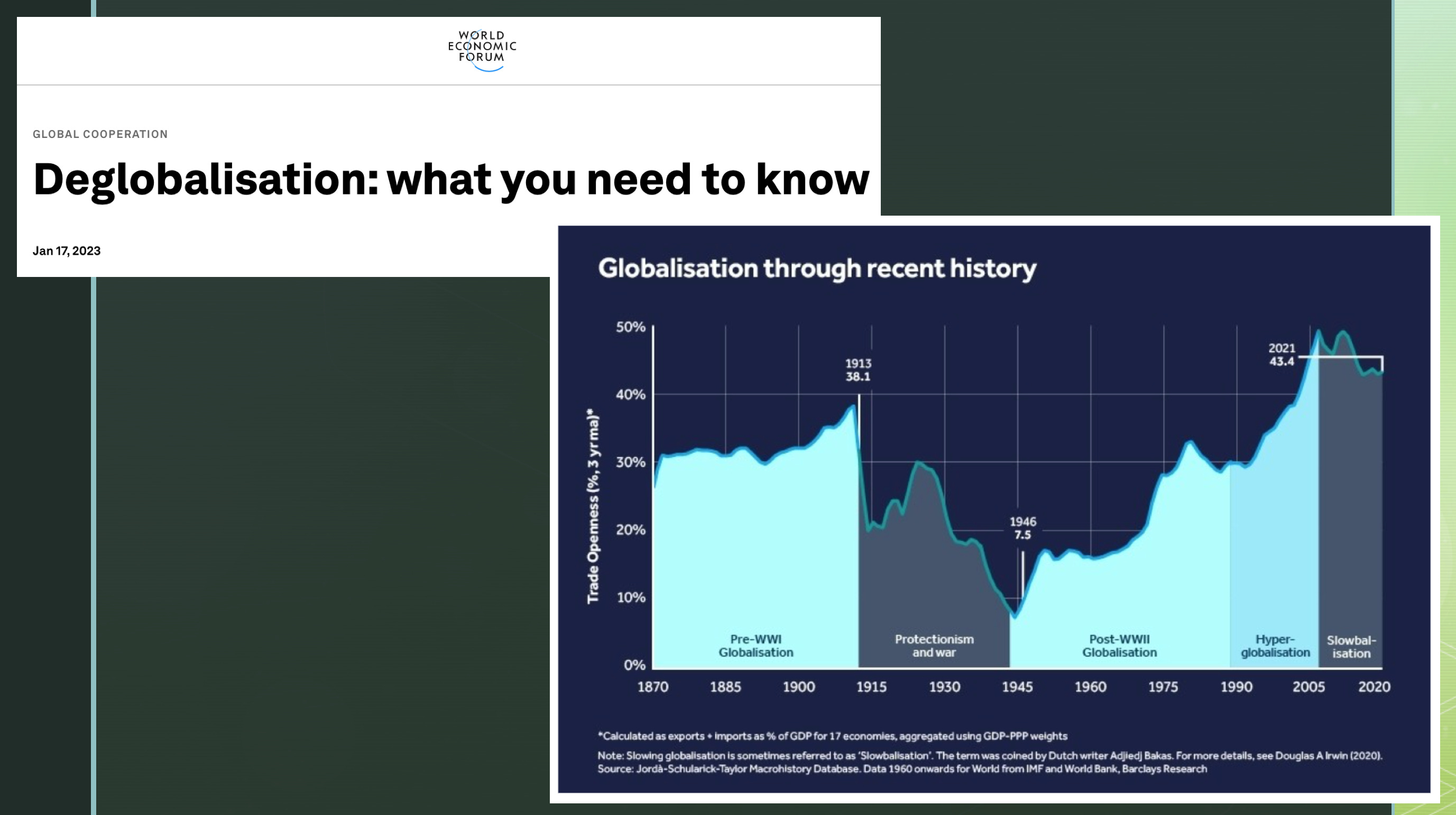

As we begin 2023, the world of economic analysis and commentary is marked by a disjuncture between discourse and data. On the one hand you have feverish talk of deglobalization and decoupling. On the other hand the statistics show an inertial continuity in trade and investment patterns.

Interestingly, this disjuncture is evident in the WEF’s own commentary on the theme and transmitted itself to our panel.

On one hand you have a headline that blares “Deglobalisation: what you need to know”. Meanwhile, the body of the WEF’s essay discusses not deglobalisation, but slowbalisation, or a plateauing of globalization.

A recent report by Aiyat et al of the IMF addresses much the same confused reality and coins the new acronym – geoeconomic fragmentation (GEF).

As the IMF team make clear, the world has been transformed by globalization.

And trade trends between China and the rest of the world and between Emerging Markets hardly suggest a sudden stop to globalization. That dynamic of integration continues.

But there is an undeniable surge in anti-globalisation talk and active consideration of alternatives such as near-shoring and friend-shoring.

How then to reconcile this tension? My FT piece continues:

There are at least three ways to reconcile this tension. Option one: You can cleave to the old religion that economics always wins. In which case you dismiss the talk of deglobalization as journalistic hype.

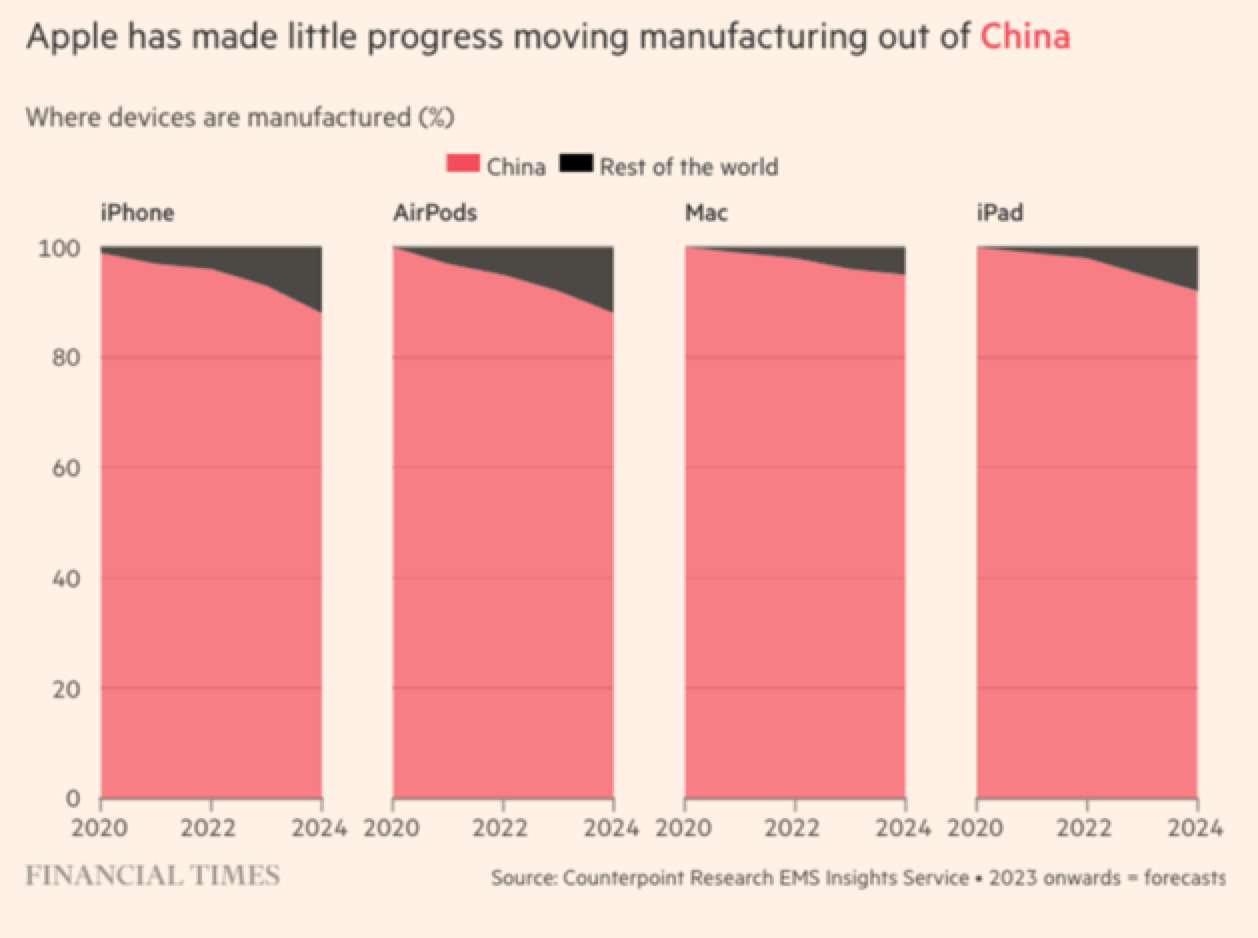

You could, for instance, cite the recent FT analysis which shows just how hard it is proving for Apple to disentangle itself from its Chinese supply chains.

In light of the data, this debunking posture has the air of empiricism and common sense about it. But to hold this view you have, in fact, to believe many things, chief amongst them being that the Biden administration does not mean what it says.

The juxtaposition I am after is between “common sense, empiricist debunking” and the fact that this posture, in fact, rests on rather strong beliefs – an underlying theory that economics and inertia win out. Because otherwise, were you to

… take Washington seriously it is hard to avoid the conclusion that whatever the statistic tell us about the current state of affairs, the United States is bent on revising the world economic system. They intend to reprioritize domestic production and to face up to the historic challenge posed by China’s rise. And the administration is not alone in this. If there is one thing that America’s divided polity can agree on, it is the necessity to confront China.

Think about the latest round of sanctions being targeted at Huawei.

If you take this vision seriously, then you arrive at option two: rather than business as usual, we are on the cusp of a new historical epoch, a new Cold War. And this is not the Cold War of the détente era. In Washington these days even coexistence with CCP-led China is up for debate.

So here we have thesis and antithesis – economic common sense v. geopolitical and ideological confrontation.

Can this extreme tension be sustained? Or will it be resolved dialectically?

If taken at face value this is a scenario of high-stakes confrontation that overshadows every other priority, alliances, economic efficiency or civil liberties. In recent weeks there have been efforts as deescalation; first the G20 meeting between Xi and Biden, then China’s dovish appearance at Davos. But these moves do not presage a return to business as usual. Notably as far as the “chip wars” are concerned, Washington is hardening its stance.

So, if a return to “business as usual” is not on the cards, what kind of “resolution” is, in fact, on offer?

Rather than reconciliation and reconvergence, the Biden team holds out something far weirder. They do not want to stop China’s economic development, they insist, just to put a ceiling on every area of technology that might challenge American preeminence. How that is supposed to work is anyone’s guess. Imagine if China offered the USA a similar deal.

I mean this rhetorical question seriously. Imagine if China was attacking Apple’s manufacturing network, as the United States is attacking not just Huawei but the entire sector of high-tech microelectronics in China. And then imagine that Beijing blandly declared that this should not be taken as an attack on America’s economic development in general; just on the bits that matter for strategic purposes. Imagine how Washington and the American political system would react. Lingering over that scenario puts me in mind of that excellent Larry Summers op-ed from December 2018 in which he surfaces the fundamental difficulty of the American political system in accepting a shift in the balance of world economic influence.

Whether it makes sense or not, the folks in Washington are cooking up something weird. And …

… in its sheer other-worldliness it points to interpretive option number three. We are witnessing not a reversal of globalization, or full-scale decoupling, but a continuation of some aspects of familiar pattern, just on fundamentally different premises. Crucially, we are no longer in a world of peaceful convergence or level playing fields.

I started puzzling over this in earnest back in 2021, in a piece on American grand strategy triggered by the withdrawal from Afghanistan. The puzzle of what future America’s grand strategy envisions, has come only more sharply into focus since.

In the FT piece I offer the image of a patchwork:

A future world economy might be made up of a patchwork of antagonistic coalitions divided by more or less visible data curtains. States that have the resources will launch national policies like the Inflation Reduction Act, which blends green industrialization and “buy American”, with an anti-China stance and a push for friendly supply-chains. That the IRA has caused a ruckus with Europe and South Korea is not a bug. It is a feature.

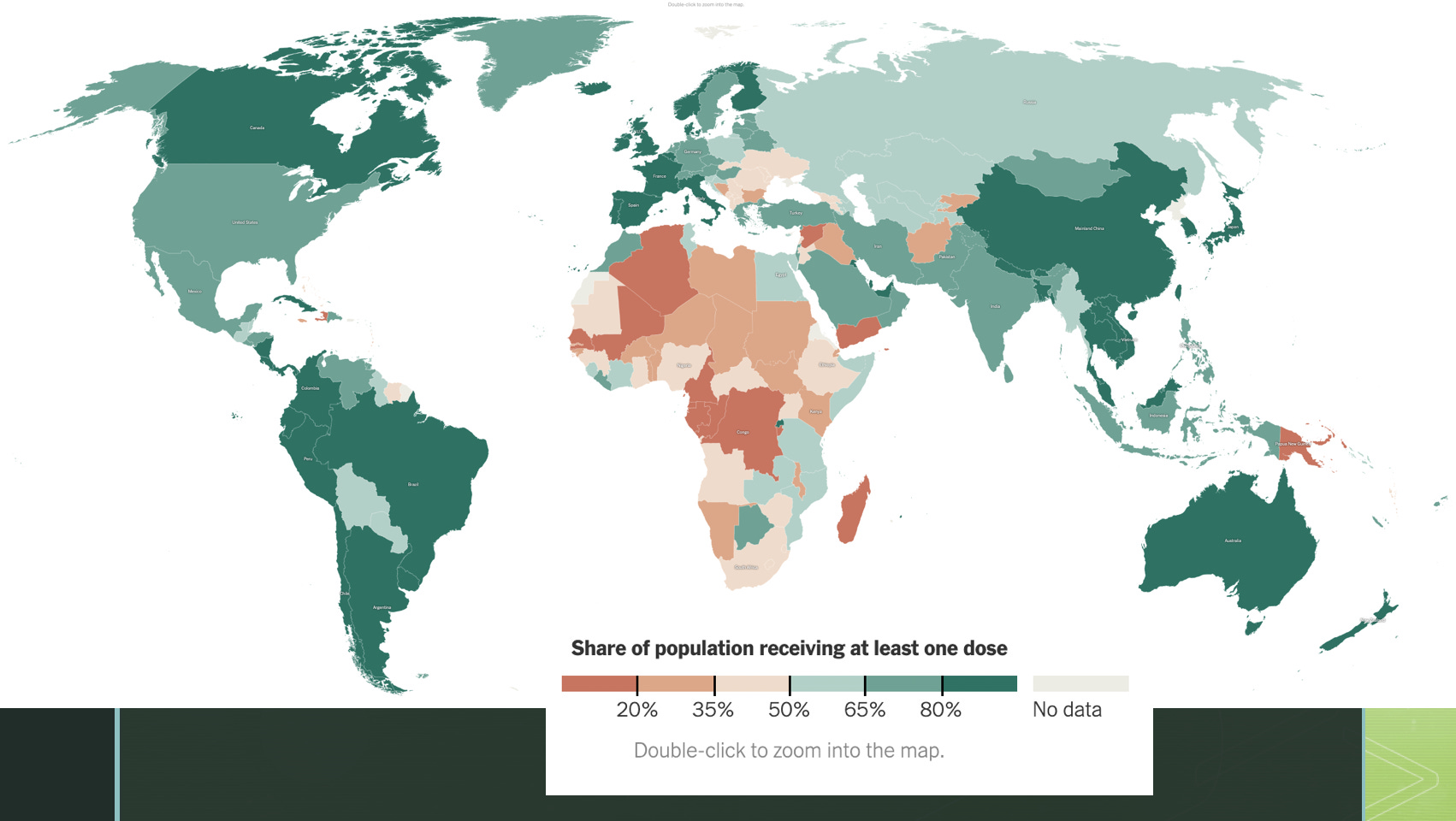

Since Shutdown, I’m haunted by the emblematic quality of the vaccine story.

Perhaps a harbinger of the future is the crazy quilt of COVID vaccines: the United States driving Operation Warp Speed; the Europeans trying to broker a complex bargain that includes exports to the rest of the world; India as a manufacturing hub; China pursuing an inadequate national solution; and one third of the world’s population excluded altogether.

Here is the global COVID-vaccine map as of last week:

As we know, the unequal production and distribution of vaccines was propelled by the policy of the big economic blocs. But it was dependent on global supply chains and has resulted in a highly uneven delivery of COVID-protection.

You might shrug and ask whether this mélange of geopolitics, economic nationalism and the occasional pandemic is really new. Is it not just “history” as we have always known it – unpredictable and red in tooth and claw?

This was Ferguson’s comment on the WEF panel. It is superficially persuasive and was taken up by Dan Drezner in his Vox column on polycrisis. But it is, of course, profoundly question-begging.

When you say, all this talk about polycrisis is “just history”, what exactly do you mean by “history”? The perplexity is only made greater by the throwaway “just”. Once again a seemingly obvious bit of common sense trails behind it a mess of intellectual baggage.

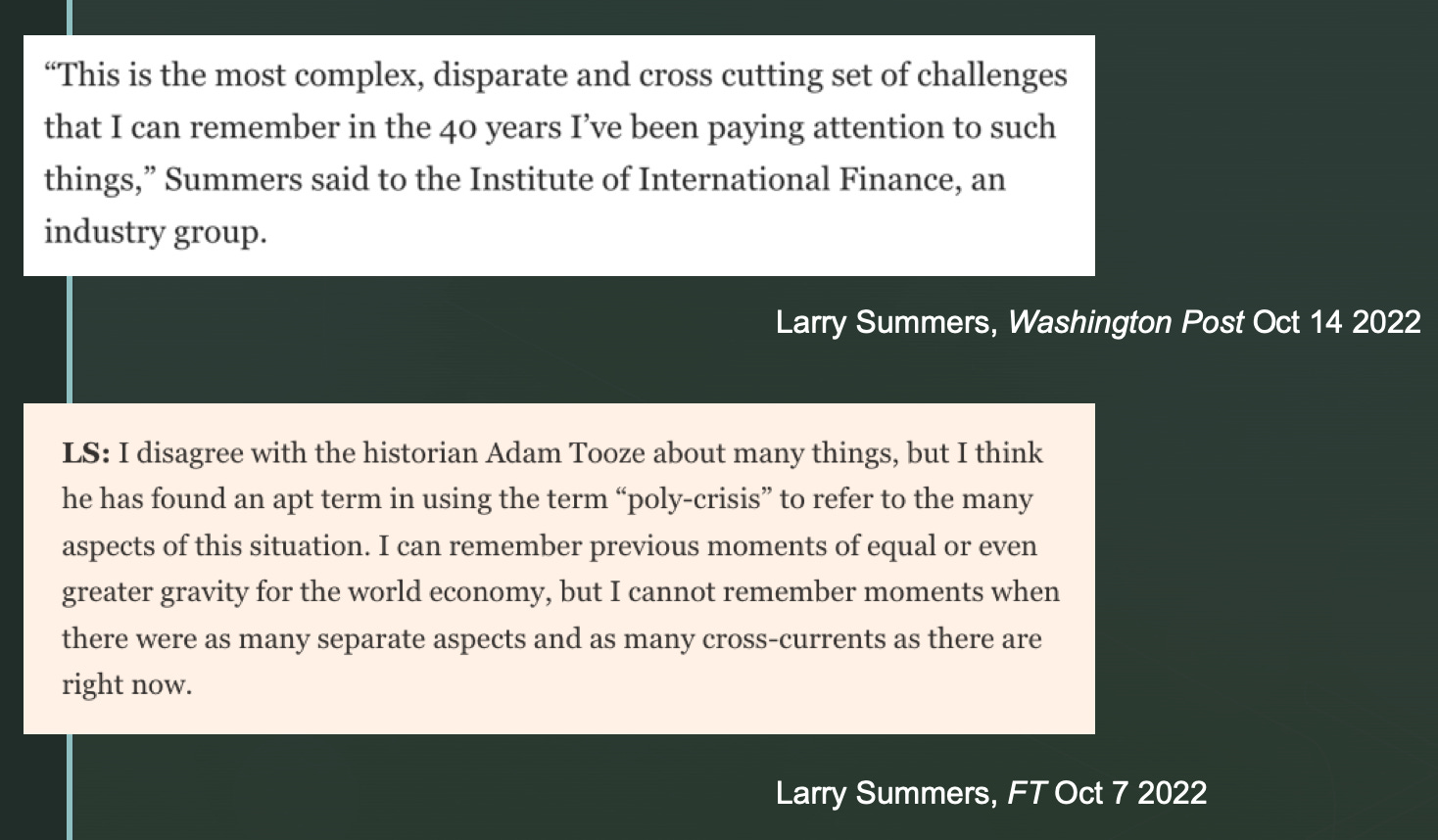

The point was grasped very clearly by Larry Summers in his embrace of the polycrisis concept.

What polycrisis refers to, is the abnormal coincidence of disparate shocks. Of course, to be able to characterize shocks as abnormally disparate you need to have some conception of development that doesn’t satisfy itself by waiving heartily to “just history”. You have to make some assumptions about which kinds of shocks are to be expected and which not.

A concept of polycrisis that is not merely redundant must rest on a more or less explicit philosophy of history.

As Bo Harvey has noted in a truly interesting intervention in the discussion, Marxism provides one obvious framework within which to situate the polycrisis debate. And as Harvey notes that begs the question of exactly what conceptual work is going to be done by the concept of capitalism. This will require much further elaboration.

Meanwhile, Drezner and Noah Smith have not been shy about basing their critique of the polycrisis idea on their own preferred historical theories. Those theories are of the homeostatic, self-equilibrating variety. When they see a shock they look for a negative feedback loop.

What they take issue with is precisely what Harvey so well describes.

‘polycrisis’ in a strict sense would mean not simply the adding together of different crises and treating them as one (the ‘there’s lots of things going on’ definition), but rather a system that is ‘emergent’ out of their interaction and interrelation—a crisis greater than each specific crisis added together. A world subsumed by polycrisis becomes a kind of nightmarish ‘emergent system,’ the roots of which are irreducible to a single cause, thus the necessity of those maps and charts best captured by Krisenbilder (“crisis pictures”).

Drezner and Smith, by contrast, insist on the force of a variety of countervailing and self-equilibrating forces. Clearly, a polycrisis interpretation must be premised on something more open-ended and less complacent. Something more Keynesian, for instance – think multiple bad equilibria with involuntary unemployment – and a growth path steered by repeated crisis-management.

At this point you may be wondering what this long diversion has to do with the topic at hand: the question of globalisation. The connection is the underlying theory of history implied by talk of globalisation.

Globalisation is more than merely a set of mute economic processes. It was a process tied to, energized by and framed by institutions that were shaped by a narrative, a teleological narrative of growth, interconnection and convergence. And this means that you cannot have it both ways. You can’t simultaneously insist that polycrisis is really no more than history in its “normal” disturbed and violent form and that globalization is proceeding as per normal. I don’t think that 1914 is a good point of comparison for our current moment, but if you do go there, as Drezner does, you at least have to do some work to suggest how globalization might be modified by such a confrontation, as Ted Fertik and I did back in 2014. Otherwise, if you blithely dismiss polycrisis as “just history happening”, you are, in fact,

… giv(ing) the game away. The promise of globalization, as it was understood from the 1990s onwards, was precisely that it would usher in a new era. It (globalization) was the dynamic underpinning of the end of history thesis.

Globalization talk, in other words, offers its own philosophy of history, a strong and teleological one.

So to admit not only that a scatter shock of unexpected and diverse shocks is disrupting the world economy, but that they are multiplying and becoming more intense, is, in fact, to admit a fundamental disappointment of expectations.

The polycrisis concept – as seized upon by Summers – registers that shock and thus offers a kind of dialectical “resolution” – admittedly of a weak kind.

Whereas the advocates of “business as usual” declare that it is still “the economy stupid” and the new Cold Warriors rally around the banner of “democracy versus autocracy”, the third position faces the reality of confusion, the kind of confusion registered by a term like polycrisis.

The concept of polycrisis serves as the third moment in the dialectic (thesis-antithesis-synthesis), not because it offers a strong concept of a new world, or a clean break with the past motivated by what is retrospectively reconstructed as a single dominant tension (autocracy v. democracy). Rather the polycrisis concept offers a form of (weak) dialectical resolution precisely because it refuses to flatten the thirty-year switchback of optimism and disillusionment with the steamroller of “just history”. Instead, it retains and makes explicit the sense that our present moment is overshadowed by disappointment and confusion.

Polycrisis, for me, does the work of Aufhebung (sublation). In fact, if you google the term Aufhebung, google yields an image which, though twee, captures a further, for me, important feature of the polycrisis concept.

Not only does polycrisis describe a messy situation and register our surprise and dismay at the degree of the confusion. It is a concept that was itself found amongst the wreckage – in Jean Claude Juncker’s musings about the EU’s situation in 2015/6. It is a “found concept”, an idea “picked up” off the intellectual sidewalk and deposited in our conceptual carrier bag.

What does this found concept do?

Polycrisis has its critics and at Davos 2023 it risked becoming something of a cliché. But as a catchword it serves three purposes. It registers the unfamiliar diversity of the shocks that are assailing what had previously seemed a settled trajectory of global development. It insists that this coincidence of shocks, whether economic, geopolitical, climatic or epidemiological, is not accidental but cumulative and endogenously self-amplifying. And, by its currency, it indexes the moment at which bullish self-confidence about our ability to decipher either the future or recent history has begun to seem at the same time facile and passé.

Only if we stop reducing the radical and unprecedented situation facing us, either with rewarmed ideological polarities – autocracy v. democracy – or the intellectual bludgeon of “just history”, do we have any hope of making sense of our circumstances and of actually thinking in medias res.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, click here:

January 28, 2023

Three ways to read the ‘deglobalisation’ debate

Proponents of business as usual and the new cold warriors are too confident of their ability to predict the future.

Read the full article in the Financial Times

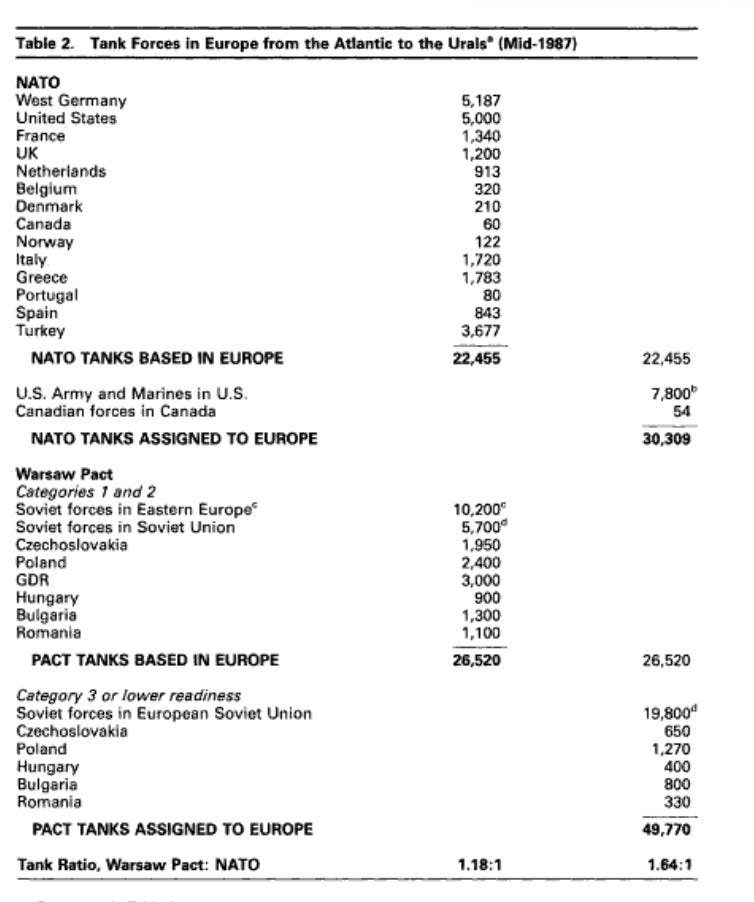

Chartbook #191 Tanks for Ukraine

In Ones and Tooze this week Cameron and I took on the question of tanks for Ukraine.

It, if I am honest, a topic I’ve been waiting to do a session about.

I’ve been preoccupied with tanks since I was a little kid. As a small child, perhaps 6 years old, I remember learning that my birthday, 5 July, was the anniversary of the battle of Kursk, the biggest tank battle in history, fought in July 1943. I was surprised to hear that the battle was not in France or North Africa, but in the Soviet Union and I set out to draw, on a giant folding stack of printer paper, the kind that used to be fed through dot matrix printers, every one of the German and Soviet tanks engaged.

For a fascinating cultural history of the tank as a modern leviathan, check out Patrick Wright’s remarkable book, Tank.

The tank was first deployed by the British army in 1916 on the Somme. The French were the first to truly mass produce a tank, in the form of the Renault FT. The Germans became famous for the Blitzkrieg of World War II. Between 1956 and 1973 the Israelis were the masters of the modern art of mechanized warfare. The American M1 Abrams is arguably the most sophisticated tank ever have been deployed in large numbers.

Like the car you might thus think that the story of the tank was a Western story – a military version of the Fordist story of modernization. And the current reporting of the war in Ukraine tends to reinforce that impression. German, British and American tanks are touted as weapons essential to Ukraine’s war effort, which otherwise tends to be depicted as relying on artillery, reinforced from the West, and plucky infantry, armed with anti-tank rockets, notably, of course, the Javelin.

Such a western-centric, Ford-inspired narrative of the tank inverts the historical record. Along with its rocket program and the Kalashnikov, arguably the main industrial legacy of the Soviet Union for modern history are its tanks – the various iterations of the T-series.

At a rough estimate, of the 73,000 tanks in the arsenals of the world’s armies today, at least 60 percent were either produced in factories of the former Soviet Union or can trace their design to Soviet models.

From the first decade of its existence, the Soviet Union embraced the tank as a key tool of modern warfare. By 1941 the Soviet tank fleet was far larger in numerical terms than that of any Western power. And it was not just a matter of numbers. The Soviet T-34 was the best-balanced design of any tank in the war. In the final stages of World War II, in the campaigns that hurled the Wehrmacht back to the borders of Germany, the Red Army conducted armored warfare on a scale that dwarfed anything seen in the West.

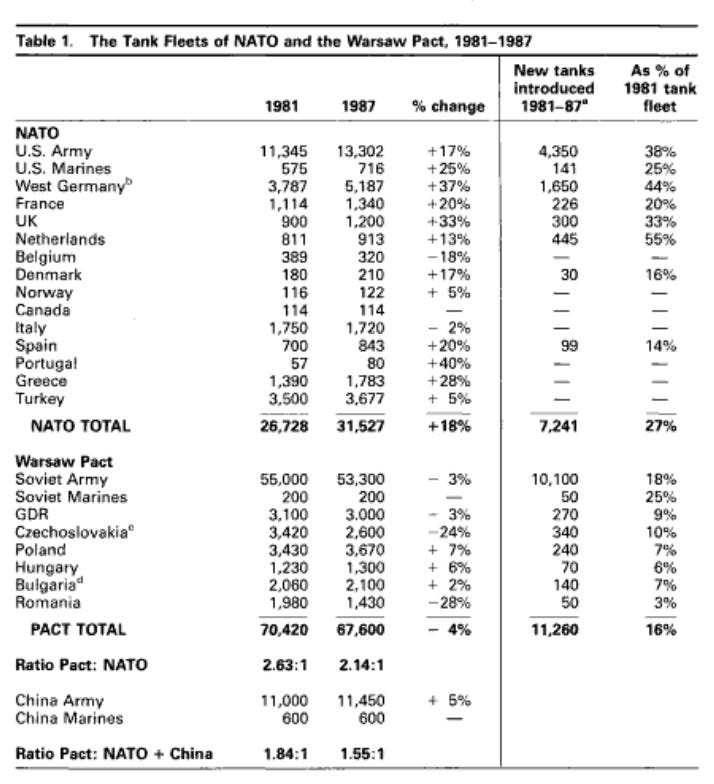

The threat of an armored Soviet assault is what kept NATO planners awake at night from the 1940s onwards. In the 1980s Western analysts anxiously debated the scale and significance of the “tank gap”.

The tank forces facing each other in the Cold War were a truly impressive array.

Even if we narrow the numbers down to those immediately available in Europe, according to the estimates by Chalmers and Unterseher, the total comes to 50,000 vehicles.

The war being fought in Ukraine is being fought between two inheritors of this Cold War armory.

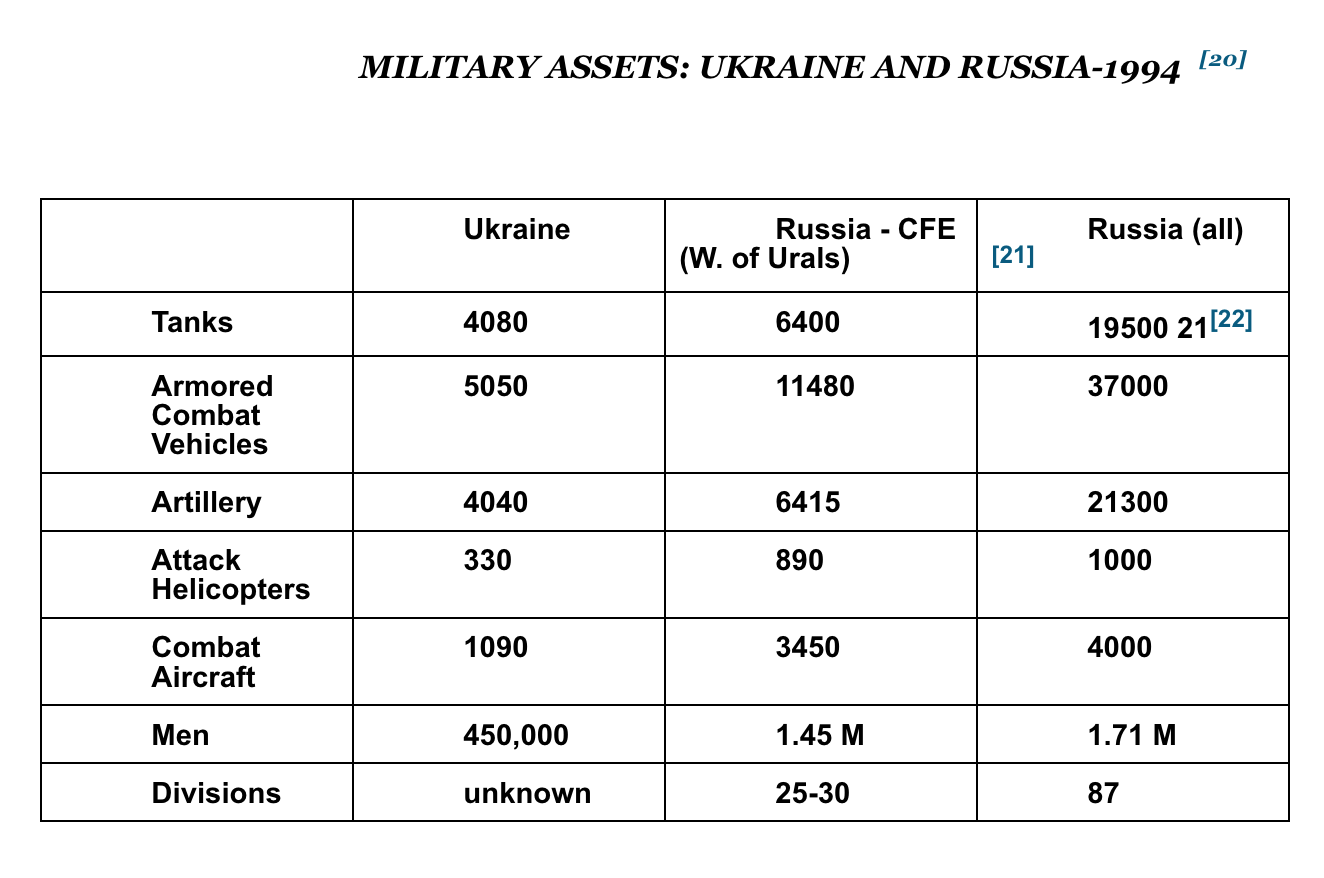

When Barry Posen drew up a defense plan for the newly independent Ukraine in 1994 he assumed that a Russian attack would be met on the Ukrainian side by a tank fleet of 4000 vehicles. It would be a World War II-style encounter writ large, with tank forces maneuvering around each other, as Manstein and the Red Army had done over much the same terrain in 1943.

Over the following years neither Russia or Ukraine maintained their tank fleets at their early 1990s levels. But following a serious effort at modernization, as the war began in February 2022 Ukraine had a fleet of 900 more or less operational vehicles. That is at least three times more than the Bundeswehr at the time. The Russian assault forces is thought to have counted 2800 tanks, with 400 more in the hands of their proxies in the Donbas. Again, these numbers dwarf anything in the European arsenal.

The losses on both sides have been heavy. The Ukrainians are thought to have been losing tanks at rates as high as 100 per month. And though tank-on-tank fighting is not favored by Soviet doctrine, some at least of the anti-tank action has been done by Ukrainian tank forces, many of them firing anti-tank missiles.

But the most original development of the war, as far as the tank forces are concerned, is their deployment as long-range artillery. Rather than firing on flat trajectories for which their guns were designed, Ukrainian tankers are elevating their cannons and firing high-explosive rounds on high trajectories, that allow them to reach ranges of 10 km or more. This is enabled by the use of drone spotters and a technical gadget deployed on tablets, known as the Kropyva, that allows Ukrainian tank gunners both to rapidly calculate and adjust their gun aiming and to cooperate in fire teams.

Equipped with this technology one Ukrainian tank gunner has claimed to have knocked out a Russian T-64 with 20 rounds of high explosive shells, fired from the astonishing range of over 10 kilometers.

#Ukraine: What is possibly the longest tank-to-tank kill ever – a Ukrainian T-64BV tank crew reportedly managed to destroy a Russian tank from a distance of 10600 meters in indirect fire mode using 125mm HE-FRAG projectiles. As claimed, it took 20 projectiles to finish the tank. pic.twitter.com/Rv05uTJroC

—Ukraine Weapons Tracker (@UAWeapons) August 31, 2022

The details of this feat remain contentious. But there is no doubt about the novel uses to which the Ukrainians are putting their substantial tank fleet.

So far in the war in Ukraine the tank forces on both sides have essentially been fighting with similar vehicles. Indeed, the Ukrainians are deploying large numbers of captured Russian tanks. The Western tanks introduce superior new technology. Unlike the counter insurgency wars that they have been deployed into since the early 2000s, where their record is mixed, a fight with Russian T-series tanks is what the Leopards, Abrams and Challengers were designed for. In the two wars in Iraq their superiority was considerable.

But the question in Ukraine is how they will fit into an existing mode of war-fighting and how significant their contribution can be, when the numbers are so small. In the short-run the Ukrainians will be lucky to be able to deploy a force in brigade strength i.e. c. 100 tanks. Even if the total of tanks supplied to Ukraine by its Western friends were eventually to add up to 321 vehicles, that would amount to a single armored division. The crucial question is whether the Ukrainian planners can identify a front or sector where a force of that type can make a decisive difference. Otherwise, it is hard to avoid the impression that their impact will be more one on morale and politics than on the battlefield. Deployed in small packets, their effect can be no more than local.

***

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. I’m glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, click here:

January 27, 2023

Ones & Tooze: Are Tanks Really a Game Changer in Ukraine?

With news that Western countries will send tanks to Ukraine, Cameron and Adam discuss how the weapon system could help fend off Russia—and why it won’t.

Find more episodes and subscribe at Foreign Policy.

Chartbook #190: The Adani crisis – is Modi’s house of cards at risk?

The Adani conglomerate, the business group most closely associated with Modi’s India, is under serious attack in the stock market, following a damning report by researchers at Hindenburg the outfit that specializes in short-selling overhyped tech stocks.

Source: FT

By early Friday morning New York time, Adani’s group had lost $51bn in value. This is a shocking blow to a business that is synonymous with the success story trumpeted by Delhi and the BJP leadership.

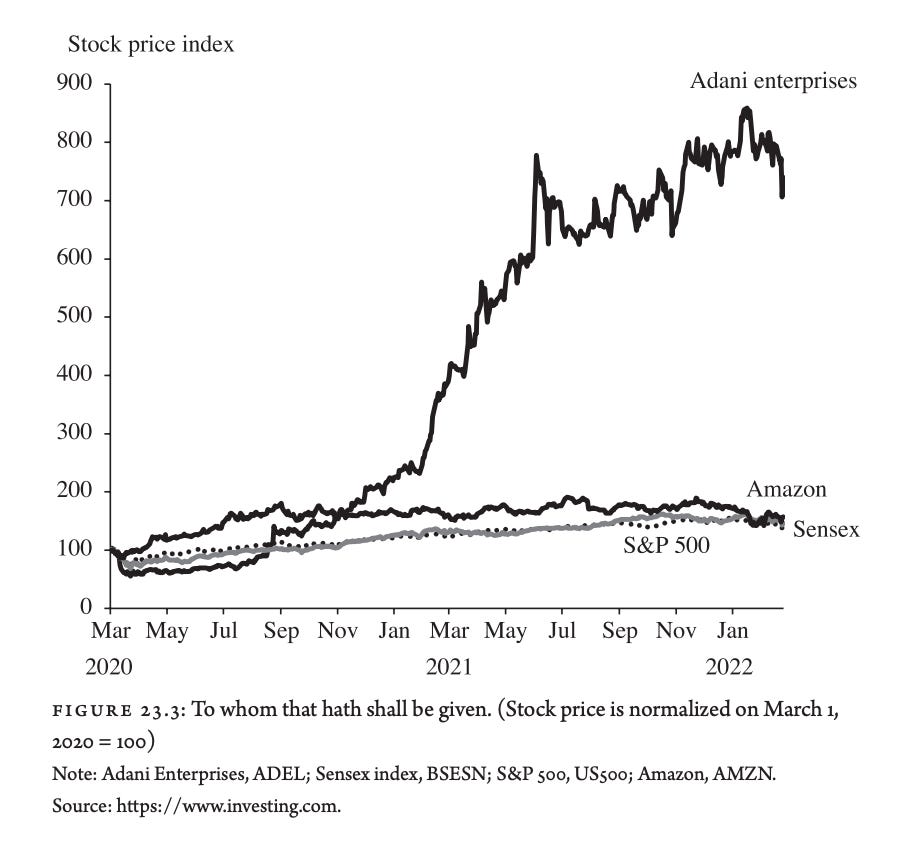

The slump in Adani shares follows breathtaking gains in recent years, including some of Asia’s biggest returns in 2022. The five-year advance in Adani Enterprises trumped even the likes of Elon Musk’s Tesla Inc., vaulting Adani from relative obscurity into the ranks of the world’s richest people.

It is hard to exaggerate Adani’s pivotal significance to the story of India’s rise. Founded in the 1980s as a commodity trading group, Adani has become a conglomerate of both national and global significance. In 2022 he crowned his rise to national prominence as “India’s businessman” by acquiring the three national channels of the NDTV television network.

As Bloomberg reported in September Adani’s rise has literally driven the indices.

Indian billionaire Gautam Adani’s ascent to rank as the world’s second-richest person has helped fuel a world-beating jump in the nation’s stocks and bolstered their clout among emerging-market equities. Eight firms controlled by Adani’s ports-to-power conglomerate, including recent cement acquisitions, have contributed more than a fifth of the 109-member MSCI India Index’s surge since end-June, data compiled by Bloomberg show. The index has outpaced Asian and emerging market peers during the period with a 12% jump.

Since 2020, the surge in Adani’s stock price has easily topped all of the madness in America’s equity markets.

Source: Ashok Mody, India is Broken, forthcoming Feb 2023

As Mody makes clear in his forthcoming book, India is Broken, the rise of Gautam Adani is deeply connected not just with rise of Indian equity market but more specifically with Modi’s vision & the Gujarat connection. As the FT reported back in 2020. Adani’s firms own everything from ports to coal mines.

“Nation building” is Mr Adani’s motto and he likes to talk about helping India achieve energy security.

Adani’s reach extends beyond India to highly controversial mega coal projects in Australia. More recently, the Adani group has positioned itself at the forefront of India’s dramatic Green energy projects. As the Economist reports:

Gautam Adani, the group’s founder and chairman (whose personal fortune of well over $100bn makes him one of the world’s richest people), claims his companies will spend $70bn on greenery in India by 2030. With nearly 5gw of solar generation capacity as of mid-2021, Adani Green Energy, one of the group’s divisions, is already on par with Italy’s Enel Green as the world’s leading developer of solar energy.

At the same time as driving national infrastructure development, Adani personifies the oligarchic linkages and rentier profits generated by licensing system for infrastructure on which Modi’s growth model has heavily relied.

How to make sense of this political economy is one of the critical questions in India today. And what will be revealed by this attack on Adani?

The question of India’s new political economy was first posed in 2012 when analyst Ashish Gupta raised the alarm about bad debts at state banks. The issue was taken up by US-based economist Raghuram Rajan when he was appointed to the Reserve Bank of India in 2014. Rajan and his colleague at Chicago-Booth Luigi Zingales cast India’s problem as one of crony capitalism. Rajan as Reserve Bank Governor only until 2016.

Modi was elected in 2014 on a slate to overcome the corruption of the previous administration. But instead, the entanglement between the Gujurat business clique, headed by Adani and Ambani, and the Modi regime became ever more intense. So intense did it become that it escaped generic categories of corruption or cronyism and put in question the historic model of India’s development. As the FT noted back in 2020.

Some argue the concentration of economic power in family-run conglomerates is a way to fast-track India’s economic development, like the chaebol did for postwar South Korea. But critics say the rapid consolidation of state assets is creating monopolies and stifling competition. “Is India going to move towards the east Asian model or the Russian model? So far the tendency looks towards the latter [more] than the former,” says Rohit Chandra, assistant professor of public policy at the Indian Institute of Technology Delhi. “It’s not clear whether India’s concentration of capital will lead to the long-term benefit of Indian consumers.”

Rupa Subramanya writing in Nikkei Asia warned that India might be sliding from crony capitalism into something more akin to the gangster model of 1990s Russia. It takes courage for Indian journalists or activists to oppose the plans of the government-industrial and media complex. Rather than either South Korea or Russia, the other historic example that comes to mind, as the FT noted, are the Robber Barons of gilded age America.

Whether India’s industrialisation leaves it more closely resembling the US at the turn of the 20th century when the likes of oil magnate John D Rockefeller wielded vast influence, or Russia in the 1990s, Mr Adani’s voracious appetite for dealmaking and political instincts have ensured he will play a central role.

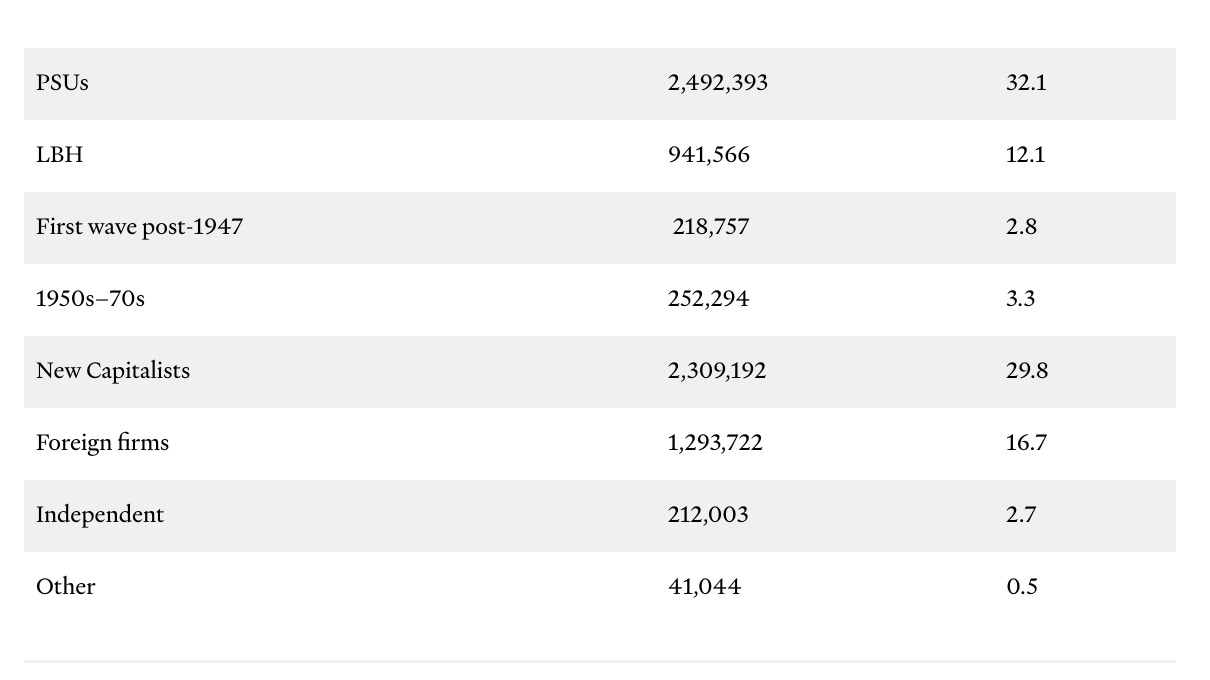

For a deep-dive on the structure of Indian political economy delve into the remarkable survey by Jairus Banaji published by the Phenomenal World at the end of 2022. Against a historical backdrop that sweeps back to independence, Banaji argues that the rise of groups like Adani signifies the fact that “the business families who formed the mainstay of industrial capitalism in the country for a whole three or four decades after Independence have either disintegrated or have been disintegrating and will soon cease to exist as coherent entities, let alone cohesive ones.”

Judged by sales Banaji sees three leading types of corporate capital in India today (whether publicly listed or privately held)

Adani clearly belongs amongst what Banaji calls the “New Capitalists” group, who as he notes are “the most fervent supporters of Prime Minister Modi. This is the case among both bigger groups (Ambanis, Adani, Sunil Mittal (Airtel), Anil Agarwal (Vedanta), the Hindujas, and Sudhir Mehta of the Torrent Group) and some smaller and less solid ones (e.g., the media tycoon Subhash Chandra who recently lost control of his flagships, with Zee Entertainment passing to Sony).”

Reading Banaji’s survey of December 2022 in light of events in January 2023 one can’t help wondering whether he does not understate the particular significance of the Adani-(Ambani)-Modi connection. Banaji’s focus, instead, is on correcting the simplistic critique of crony capitalism, which implies that India might instead enjoy a level playing-field of capitalist competition. Not only does this idealize relations between the state and capital elsewhere in the world. But, as he remarks, this side-steps the question of the “governance of capital” i.e. the relations internal to capital between management and shareholders. And, in particular, it fails to focus on the peculiarly Indian malaise of the promoters, figures like Gautam Adani, “either as a fraction of capital or as a class”. They are the key figures in the process through which old power blocs within the Indian capitalist class are dismantled and remetabolized. The new Insolvency and Bankruptcy Code (IBC) of 2016 has created an arena in which business groups with easy access to capital, amongst which the Adani’s figure prominently, can snap up the assets of ruined competitors.

But what if the biggest promoter-political-capitalist of all were to come under unsustainable pressure? It is not only inequality and power imbalances that are at stake, but the financial stability of the Indian economy.

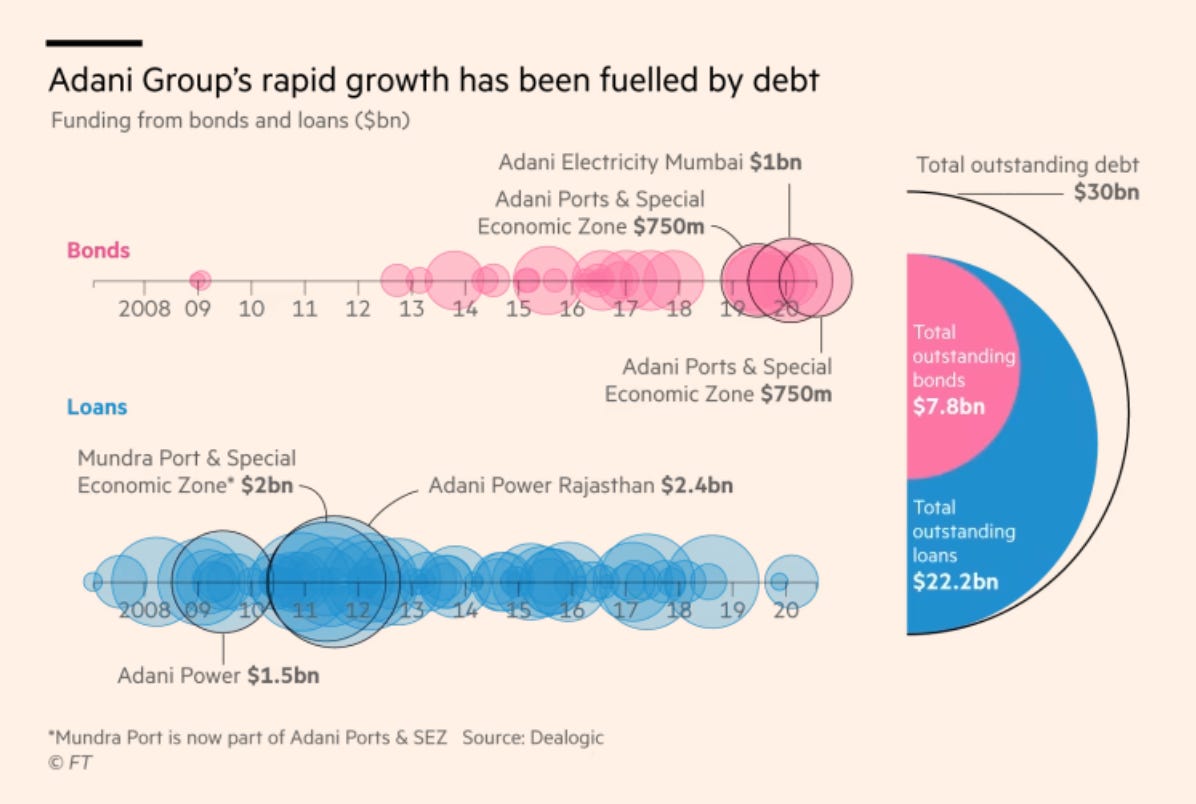

Adani’s growth has been driven by a cycle between rising equity values and corporate debt. Already In 2014 Gautam Adani boasted that his deals were “immensely bankable”. And Wall Street has really begun to take a major interest since his turn to green energy.

Source: FT

The scale of this expansion set off alarm bells already years ago:

Credit Suisse warned in a 2015 “House of Debt” report that the Adani Group was one of 10 conglomerates under “severe stress” that accounted for 12 per cent of banking sector loans. Yet the Adani Group has been able to keep raising funds, in part by borrowing from overseas lenders and pivoting to green energy. “Groups that are perceived as politically connected can still tap the banks for loans,” says Hemindra Hazari, a Mumbai-based banking analyst

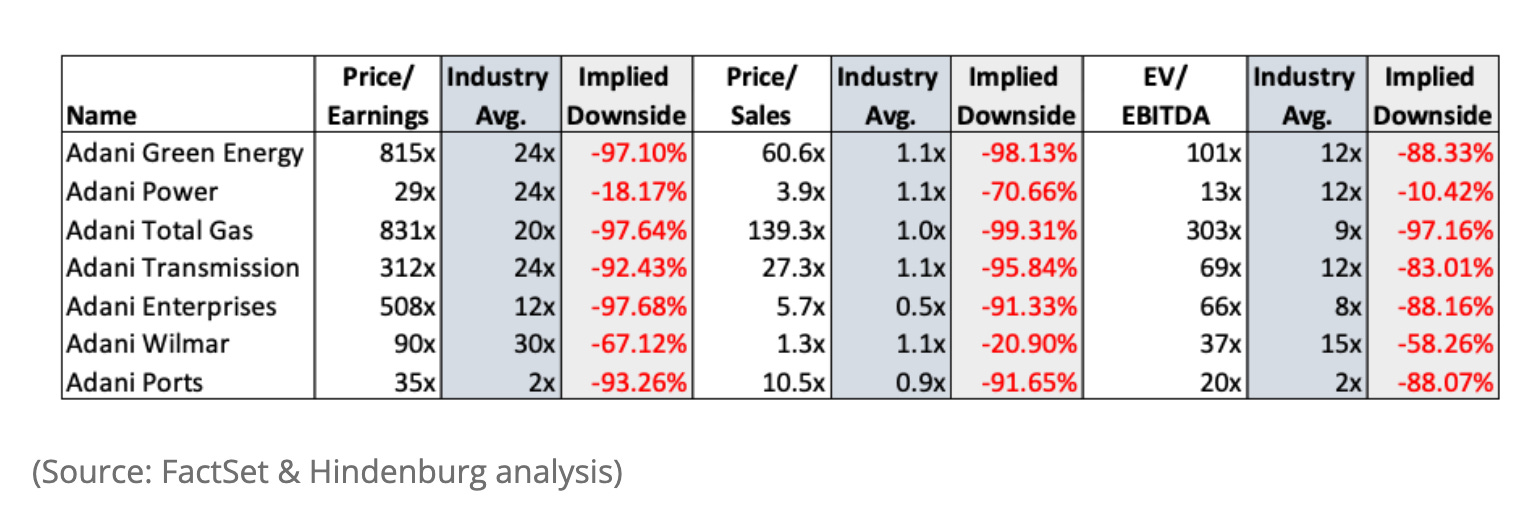

Against this backdrop, the data in the Hindenburg report are both ominous and damning.

The report alleges that the stock values of the Adani Group and thus its ability to raise debt and leverage has been wildly inflated. A valuation of the group at levels more typical of the market and the sectors that it is in, would imply a spectacular devaluation.

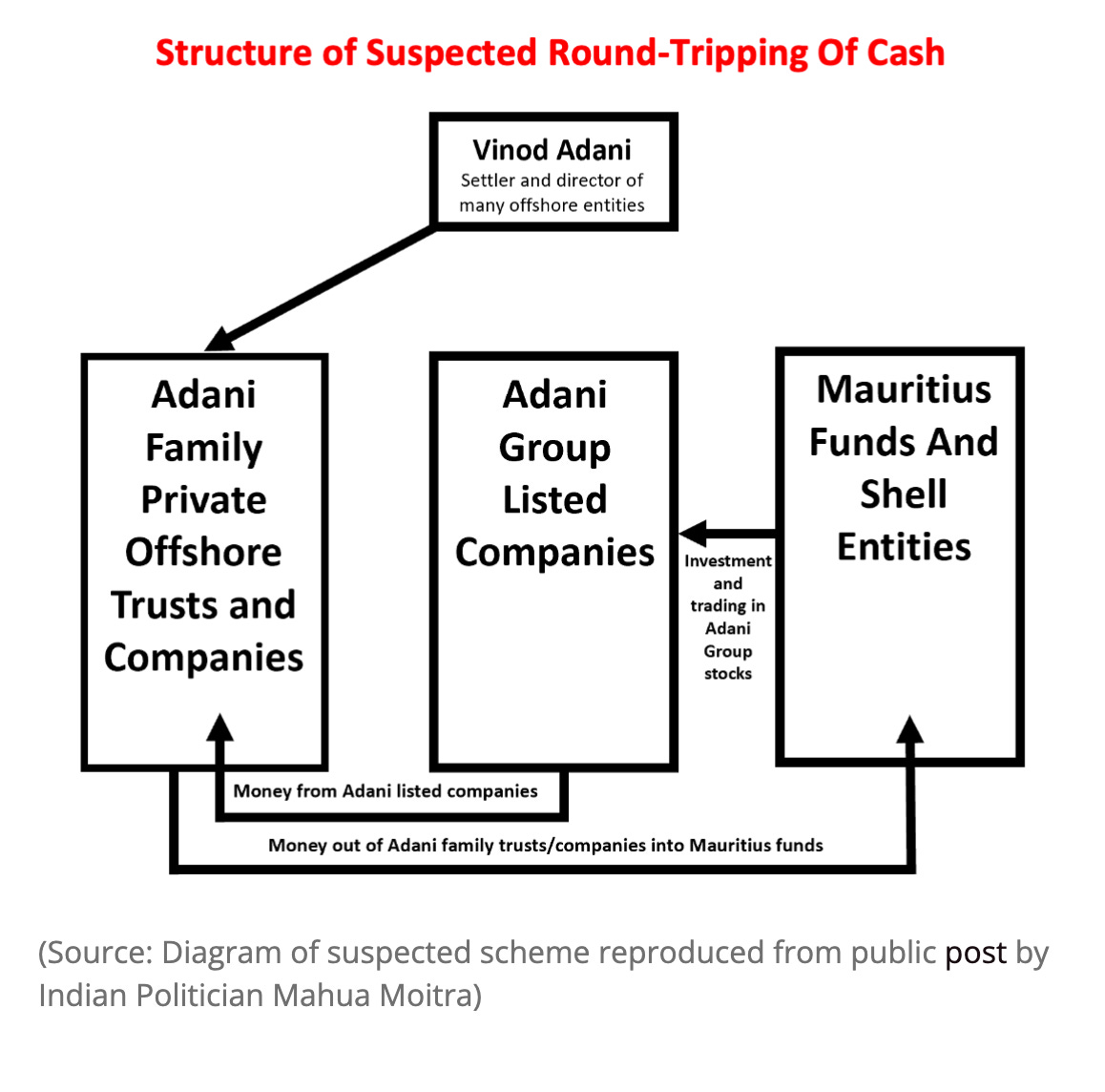

The Hindenburg report traces the mechanisms and personal networks through which stock values have been boosted by a group of circular, inside equity stakes:

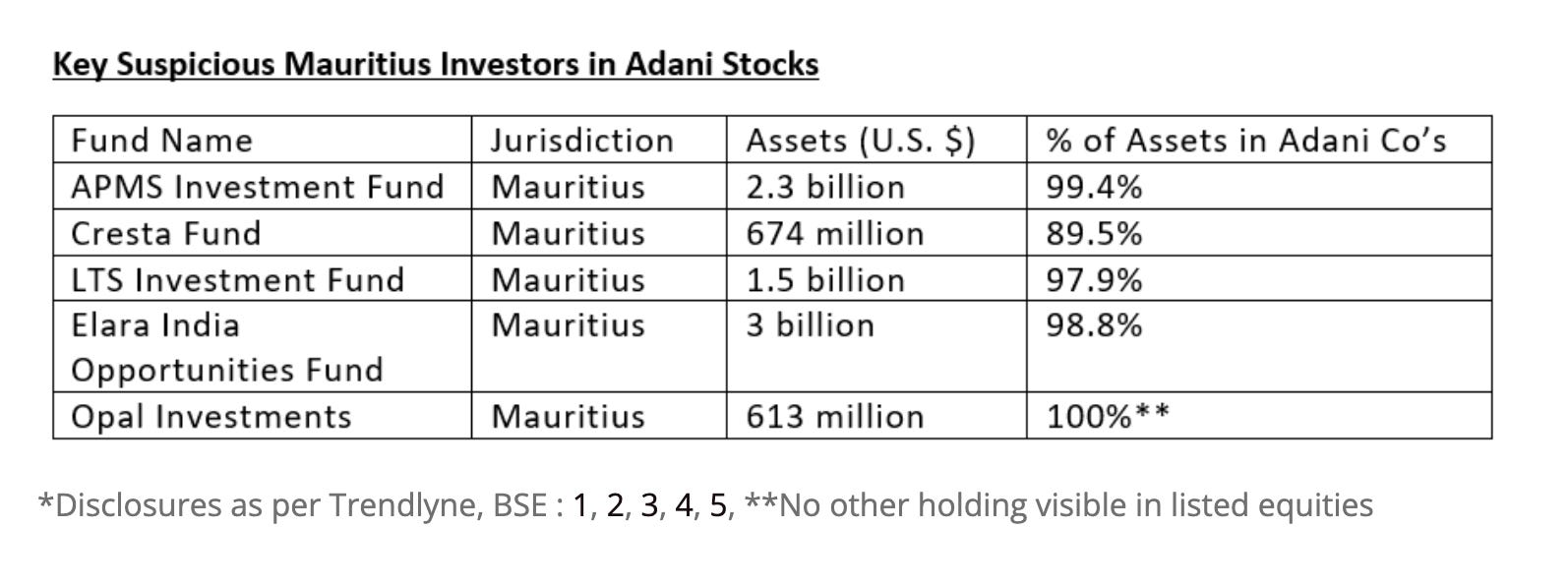

Indian regulations require that a publicly listed company should have at least 25 percent outside shareholders.

Currently, 4 Adani listed companies are on the brink of India’s delisting threshold due to high disclosed promoter (insider) ownership. Adani Tranmission, Adani Enterprises, Adani Power and Adani Total Gas all have inside shareholder percentages of around 74 percent. Suspiciously large stakes in Adani group firms are held by offshore Mauritius-based letterbox firms, which are run by members of Adani entourage and appear to have no other business activity.

Were Adani to find itself in real trouble, there can be little doubt that the real anchor would be the state. Adani’s rise and the fortunes of Modi and the BJP are closely tied.

Unsurprisingly, the opposition Congress party has leapt on the Adani issue. As The Print reports, Party leader Jairam Ramesh has issued a statement.

“State-owned banks have lent twice as much to the Adani group as private banks, with 40 per cent of their lending being done by SBI,” Ramesh said. “This irresponsibility has exposed the crores of Indians who have poured their savings into LIC and SBI to financial risk.”

Congress’s standing is so weak that it is unlikely to pose a real threat. A more serious risk is that the panic spreads from Adani throughout the financial markets, forcing the Modi administration to make painful choices. As Bloomberg reports the shock and anxiety is catching especially amongst global investors who may swiftly reevaluate their weighting of Indian assets.

“The issues strike at the heart of the Indian corporate sector scene where a number of family-controlled conglomerates dominate,” said Gary Dugan, chief executive officer of the Global CIO Office. “By their very nature they are opaque, and global investors have to take on trust the issues of corporate governance.” “After last year’s stellar performance, Indian equities and any high-profile company’s shares are open to downside risk of profit-taking,”

How big the risk to the Indian banking system actually is, is disputed. The CLSA brokerage points out that much of Adani’s debt is in the form of bonds and private Indian banks are on the hook only for a small fraction of its bank borrowing. But contagion is not just a matter of facts and figures. It is a matter of overall risk appetite. Worryingly, on Friday 27 as the depth of the collapse in confidence sank in, the contagion spread to the financial sector. Shares of Indian banks and Life Insurance Corp. of India plunged on Friday.

In 2019, ahead of COVID, India was sometimes describes as a developing country suffering from rich-country banking problems. COVID displaced those concerns to the margins. With the crisis at Adani issues of financial stability come very much back to the fore. Adani’s group has been at the very forefront of the good news narrative that has yielded a series of decisive election victories for Prime Minister Modi. As Mihir Sharma points out, the Indian public is under few illusions about the extent of corruption and feather-bedding, what they expect from the likes of Adani and Ambani is delivery. But that depends on preserving at least a veneer of financial probity and stability. If the panic spreads, if there are huge losses to be absorbed, it is an open question which balance sheet will absorb the damage.

We don’t know what will come next. What we do know is that on Friday 27 January 2023 Gautam Adani suffered the worst financial blow ever experienced by an Asian billionaire. An ill-timed $2.5 billion share sale by the Adani group meant to fund capital expenditures and to pay down the debt of its various units, hangs in the balance. And much more besides. Under intense external pressure, will the Gujarat clique hold together? Will Delhi stay loyal to Adani? If it comes to a bailout will oppositional forces in India go along? What price will Modi pay? What might a dog-fight within the BJP-oligarch cabal look like?

***

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. I’m glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, click here:

January 25, 2023

Chartbook 189 The ECB’s inflation dilemma.

As 2023 begins, policy-makers around the world are still trying to figure out how to respond to the lurching acceleration of inflation that began in the second half of 2021 and that now seems to have crested.

In 2022 it was all hands on deck. In Europe, where the energy price shock was most intense, a wide range of policies were debated and deployed including price controls and large fiscal subsidies. Now, as the sectoral price shock begins to ebb, the focus is less on price controls or large fiscal transfers and once again on the central banks. The balance the central bankers have to strike is delicate and their main instruments – interest rates and quantitative tightening – are blunt. How quickly will they move from QE and QT? Will they continue to raise rates in large or small increments? Where will they stop? What is the terminal rate? And when they might contemplate bringing rates back down again?

The Fed has signaled that though inflation may be slowing it remains far above the 2 percent target and it will remain in contractionary mode. It will continue to raise rates, but at a slower pace than in recent months. The surge in global interest rates driven by the Fed in 2022 was dramatic. It was the most sweeping tightening ever seen. This put pressure on every central bank, even the Bank of Japan, where inflation is only just rising to the target band. The BoJ now faces huge pressure in the bond market to modify its policy of zero interest rates (yield curve control).

The European Central Bank is in a particularly difficult position, not just because the inflationary wave has taken time to unfold in Europe, or because of the idiosyncratic nature of the war shock, and ongoing concerns about energy markets. What is at stake in the ECB’s decision is the problem of how to balance inflation-control with the underlying fragility of the European economy, the divergence between its parts and, for much of Europe, the miserable track record of stunted growth that stretches back to the Eurozone crisis of 2010-12 and the financial crisis of 2008. The ECB’s excessively conservative monetary policy stance, the failure to thoroughly restructure Europe’s banks and the fact that it took until 2012 to stabilize sovereign bond markets and until 2015 to launch active QE, is widely seen as co-responsible for this malaise. The risk is, that adopting a hawkish anti-inflation stance, as many voices on the ECB Council have recently been advocating, the ECB will further jeopardize Europe’s growth prospects. Given the inflation rate in many parts of Europe and the limited tools at the ECB’s disposal, there may be no alternative. But we should be aware of how high the stakes are.

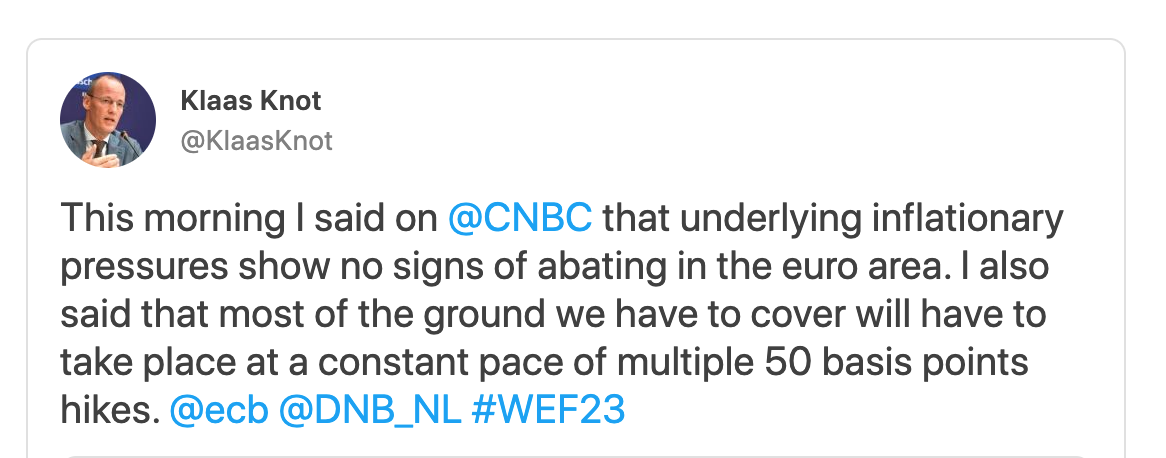

When a key figure like Klaas Knot of the Dutch central bank demands a determined course of large, 50 basis point hikes, the question that lurks in the background is: how much tough monetary policy can Europe actually stand?

Of course, inflation also generates social and political risks and those are to the fore in Europe right now. But the interest rate hike being advocated by the ECB hawks is extremely severe. The Fed may have normalized the 50 basis point hike, but for much of Europe it would the be most severe monetary tightening ever attempted.

should the ECB increase to 3.5% until summer, it would not only be the strongest increase within one year since 1999 but for many EA countries one of the strongest ever, also in Germany, it would be the second largest within one year with 4pp (the largest was 1970 4.5pp) pic.twitter.com/VjW0l6mQrb

— Stefan Bruckbauer (@S_Bruckbauer) January 15, 2023

The Italian debt problem lurks in the background. Rising rates put pressure on the weakest borrowers and at some point that can become a doom-loop. But let us assume that the risk of exploding spreads can be managed between Rome, Brussels and Frankfurt. Let us grant that the unity of the Euro is not in question and focus, instead, on macroeconomics. How much growth retardation, how much more divergence between weaker and stronger regions can Europe take? How toxic and dysfunctional will the social and political consequences of conservative monetary management and very low growth turn out to be?

A tightening on the scale being advocated by Euro-hawks implies taking risks with growth, employment and investment. It will constrain choices in both the public and private sectors. It puts in play every borrowing and spending decision, including priorities like the energy transition, security policy etc. Of course, those are the dilemmas that central bankers professionally weigh up. But in weighing those options in Europe in 2023 it is important to be clear about the historical backdrop.

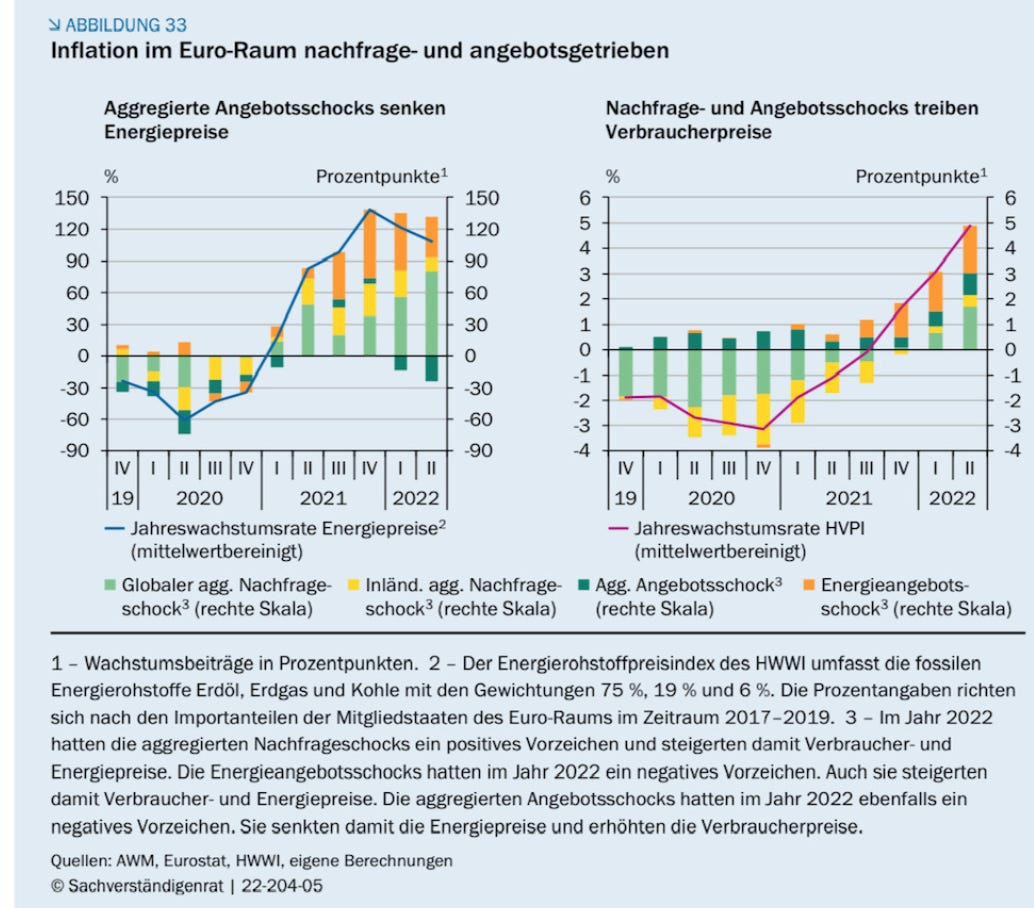

If you want to slow inflation by applying the cosh of interest rate increases to aggregate demand, you have to start by asking whether aggregate demand is the main cause of European inflation. Otherwise, the amount of pain you may have to inflict will be disproportionate. The overwhelming majority of evidence suggests that aggregate demand is far from being the main driver of European inflation. n these figures from the German expert commission which show the surge in inflation in energy prices and consumer prices, the component that is domestic aggregate demand is colored yellow.

But beyond the immediate causes of inflation, in weighing the macroeconomic policy options for 2023 we also need to consider the track record of demand management in Europe over the last 15 years. The benchmark here is not a 2 percent inflation target, but the development of the other major economic hub in the West, i.e. the United States. The conclusion is stark.

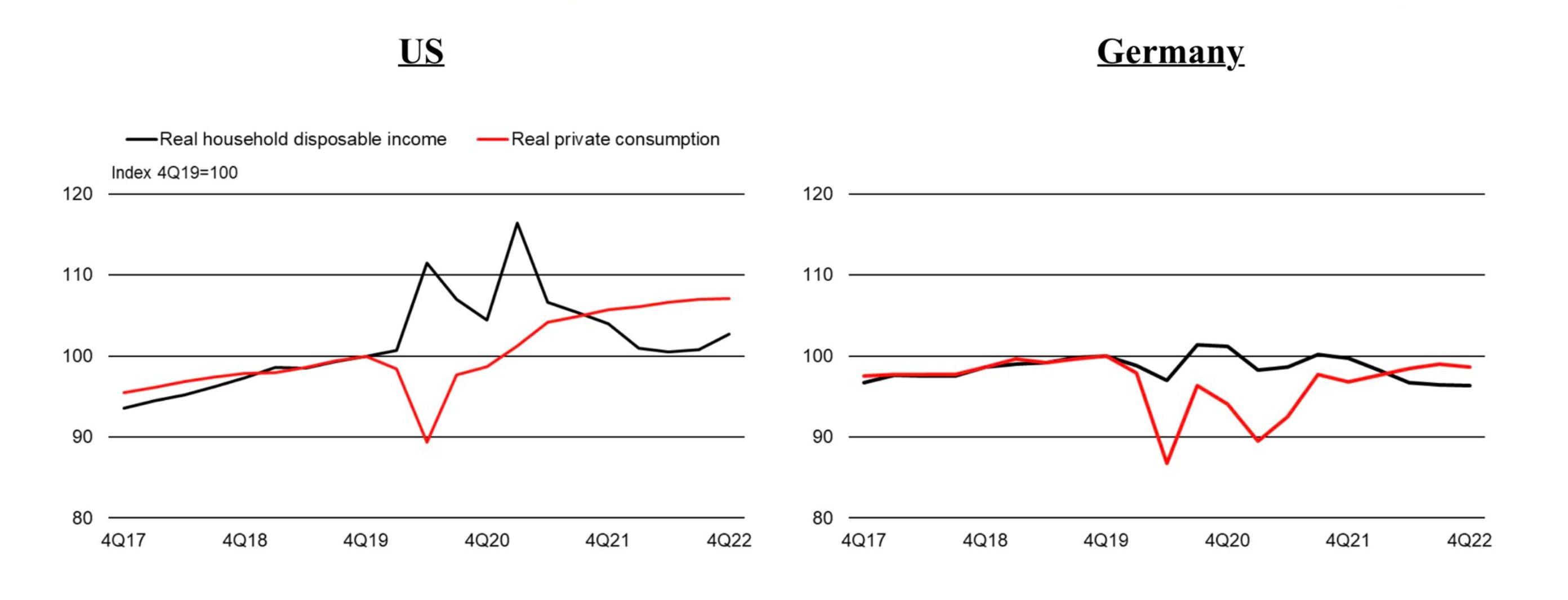

Data from Brad Setser starkly illustrates just how far the trajectory of growth in European domestic demand – consumption, investment, government spending (everything except exports) – has lagged behind that of the United States.

A chart that surprised me —

— Brad Setser (@Brad_Setser) January 20, 2023

US domestic demand stalled last year (at a high level).

But European demand (proxied by the euro area) remained solid in q2 and q3. The fiscal buffering of the energy shock appears to have worked.

Japanese demand growth also topped the US pic.twitter.com/Z0hUsq1jgT

It is important to focus on domestic demand – consumption, investment, government spending – because, following the German example, Europe has relied heavily on exports (foreign demand) to drive growth. This means that Europe’s GDP numbers make Europe’s policy stance look more expansive than it actually has been. Excluding Ireland’s GDP numbers is important because they are spectacularly distorted by its role as an offshore tax haven.

The message of the graph is that over the period since 2007 the trajectory of Europe’s domestic demand has been profoundly depressed. The index here is not annual growth, but total domestic demand relative to the 2007 level. America’s green line shows what a growing economy looks like, adding increments every year. By contrast Europe’s domestic demand took eight years to recover back to its 2007 level. For most of the period between 2007 and 2022 Europe’s domestic demand level has been considerably more depressed than that of Japan.

The COVID shock took Europe to a new low – lower even than in 2012 at the trough of the eurozone crisis. The rebound since 2020 has been relatively vigorous. But, in 2022, Europe’s growth trajectory remained below the modest recovery trend from 2012 to 2020. Indeed, the contrast with the US is even more sharp if we turn up the resolution and look at the rebound from COVID in 2020 and 2021.

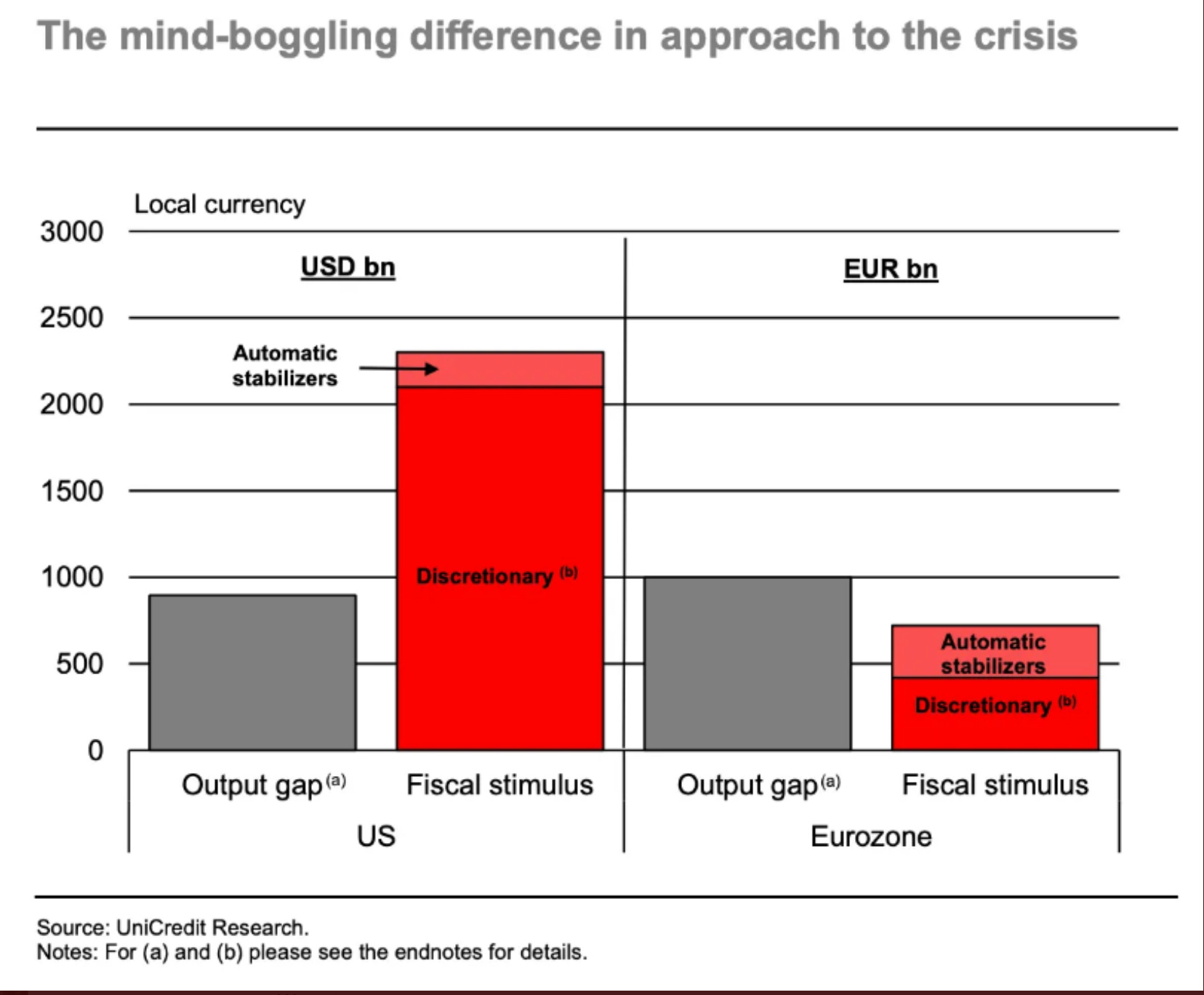

The divergence in European and American policy responses to the Covid-shock is brought out by this stark graph from Erik Fossing Nielsen, chief economists at Unicredit. America’s COVID-stimulus was so gigantic that disposable income actually surged during the pandemic. By 2021 US consumption spending had recovered to its pre-pandemic trend. In Germany, by contrast, the stimulus was more modest and consumption has plateaued and now dipped below its 2019 levels.

So, Europe inflation hawks are advocating for a historic interest rate hike to counteract a temporary inflationary surge, which is not principally driven by aggregate demand, in an economy which for 15 years has been suffering from a chronic lack of domestic demand and which is falling far behind the United States. It is a blunt force, high risk policy which may have historic ramifications for Europe.

Inflation hawks argue that it is crucial to ensure that inflationary expectations do not become entrenched, in the form of persistent wage increases. But, of this there is remarkably little evidence. The “second round effect” of wage increases has been far less pronounced in Europe than in the US or the UK and the rate of wage increases began to slow at the end of 2022.

— Pawel Adrjan (@PawelAdrjan) January 11, 2023

New release of our wage tracker for December

Posted wage growth remains high but is no longer accelerating.https://t.co/eEoneSNhmZ pic.twitter.com/n4rCNHN83q

One of the more likely candidates for a wage-price spiral is France. On France’s idiosyncrasies this expert take from the chief economist of the French Treasury is fascinating.

Last blog post of the year @DGTresor: "A price-wage loop on the Christmas tree?" 1/9 https://t.co/IlBzZI3jcU

— Agnès Bénassy-Quéré (@agnesbq1) December 29, 2022

So if the empirical evidence for a serious inflation problem that would warrant a draconian response is relatively weak, what then motivates the inflation hawks?

Ideology and politics are no doubt one component of the answer. Inflation hawks are uncomfortable with inflation. They regret the fact that the ECB acted too slowly. They want to see more determined action to prove a point. Another answer to the question of who is an inflation hawk in the precincts of the ECB and why, may be which national economies they represent.

Source: ITCMarkets

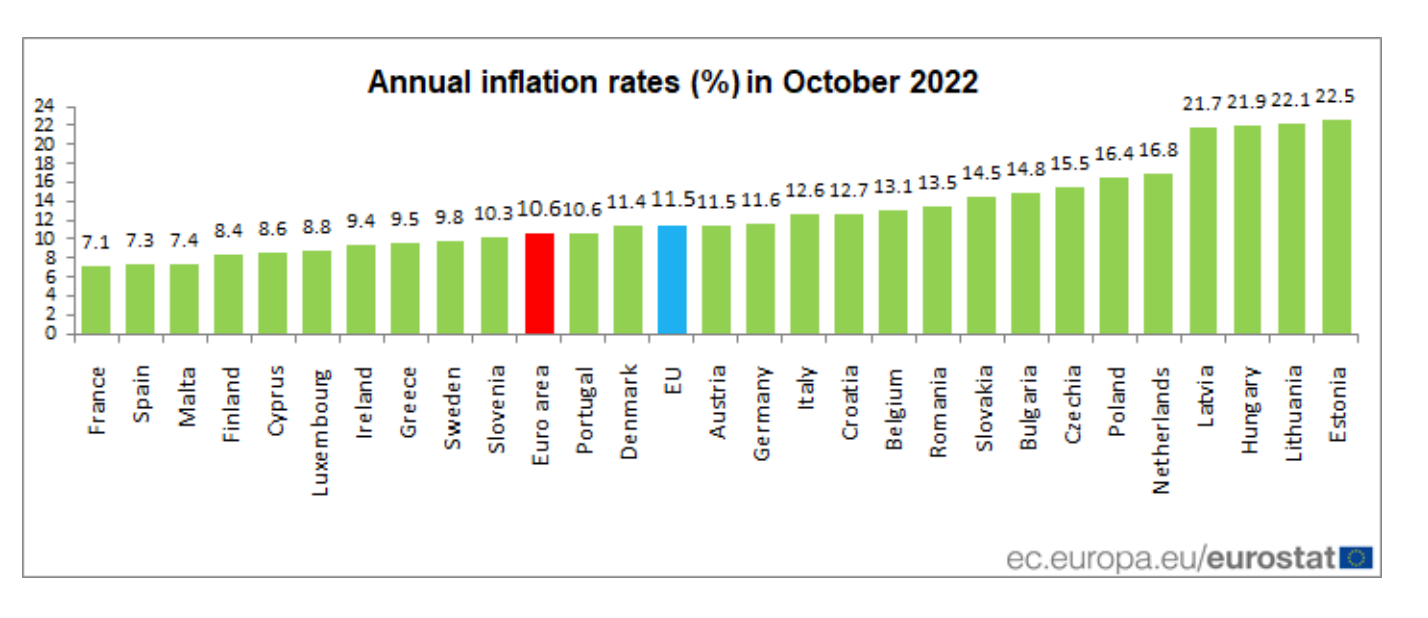

Nationality matters, because the divergences within the Eurozone in terms of macroeconomic balance are so dramatic. Right now, inflation rates in Eastern Europe are dramatically higher than in the West. They are also far higher in the Netherlands (16.8%) than in France and Spain (7%). In light of those numbers it is hardly surprising that the representative of the Dutch central banks feels a responsibility to give absolute priority to fighting current inflation by means of sustained interest rate increases. When inflation exceeds 16 percent your interest in complex rationalizations shrinks.

But history also matters. The failure of aggregate demand management in the Eurozone becomes truly apparent only when we break it down by country.

here you go —

— Brad Setser (@Brad_Setser) January 20, 2023

if Ireland and its tax driven distortions are removed, the euro area on average generated about a half point of domestic demand growth over the last 15ys. 22 tho was ok — pic.twitter.com/mz8pY1VJvI

Whilst Germany falls well short of America’s domestic demand growth, it has at least experienced real growth. By contrast, in Q4 2022 domestic aggregate demand in Italy and Spain was still at levels lower than in 2007. Portugal is barely above. Greece has dropped off the chart altogether. So, whereas for Germany or the Netherlands or the Baltics a temporary interruption to growth, or even a mild recession may be a reasonable scenario, for Italy or Spain it would be a far more alarming prospect.

How then should the ECB proceed?

As Erik F. Nielsen argues in a recent note the ECB needs, urgently, to clean up its communications and step back from a policy-making process guided by “present inflation, political pressure via the tabloids and “gut feelings””. It needs to reassert the role of forward-looking models and clarify its expectations with regard to broader “financing conditions”. It also needs to be clear that if Europe enters a real recession then the terminal rate of 3.5 percent may be too high.

Meanwhile, in light of the difficulty of interpreting the current macroeconomic situation, differences in ideology, political positioning and the real differences between the member states of the EU both currently and over the last 15 years, it is hardly surprising that there are differences of opinion and vigorous debates on the ECB. It would be frankly alarming if this were not the case. Whereas the Fed has embraced this diversity of views, the ECB has tried to obscure these differences. It carefully edits its minutes and dispatches centerists spokespeople like the excellent Philip Lane to spread sweetness and light. Disputes within the bank filter through to the public by way of more or less openly sources journalism and coverage in news outlets like Bloomberg or the FT. Given the tensions within the Eurozone construction it is easy to see why a premium has been put on closing ranks and presenting a unified view. But under the present circumstances that seems increasingly unrealistic. As Shahin Vallée and Sander Tordoir have recently argued in an op-ed for the DGAP the time may have come for the ECB to embrace its differences and to find procedures for allowing the big differences on the Council to be ventilated in public. Under present circumstances however one should expect any new era of openness to begin with a bang not a whisper.

***

Thank you for reading Chartbook Newsletter. I love sending out the newsletter for free to readers around the world. I’m glad you follow it. It is rewarding to write, but it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, click here:

January 22, 2023

Chartbook #188 Archipelago capitalism, the Bahamas and FTX

Back in December last year, the collapse of FTX set off a train of thought, which was less about crypto than about the place of SBF’s arrest, the Bahamas.

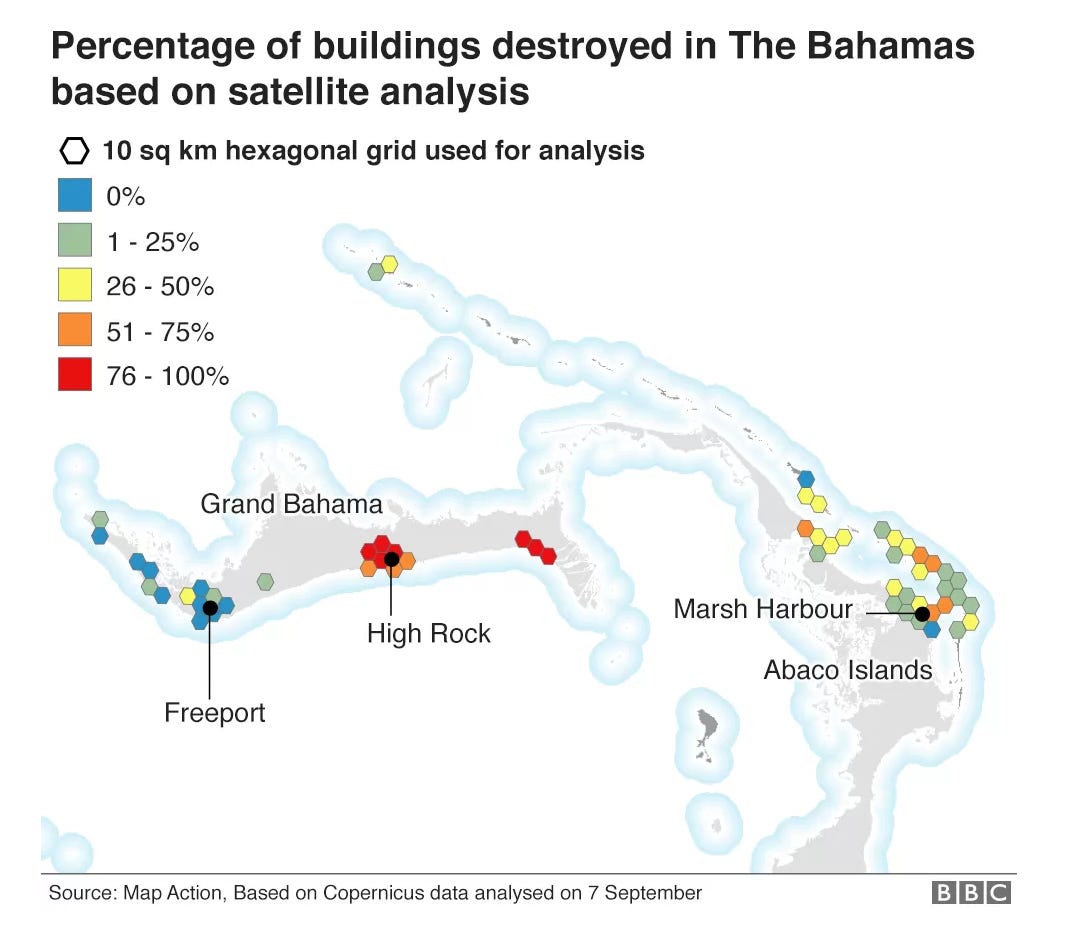

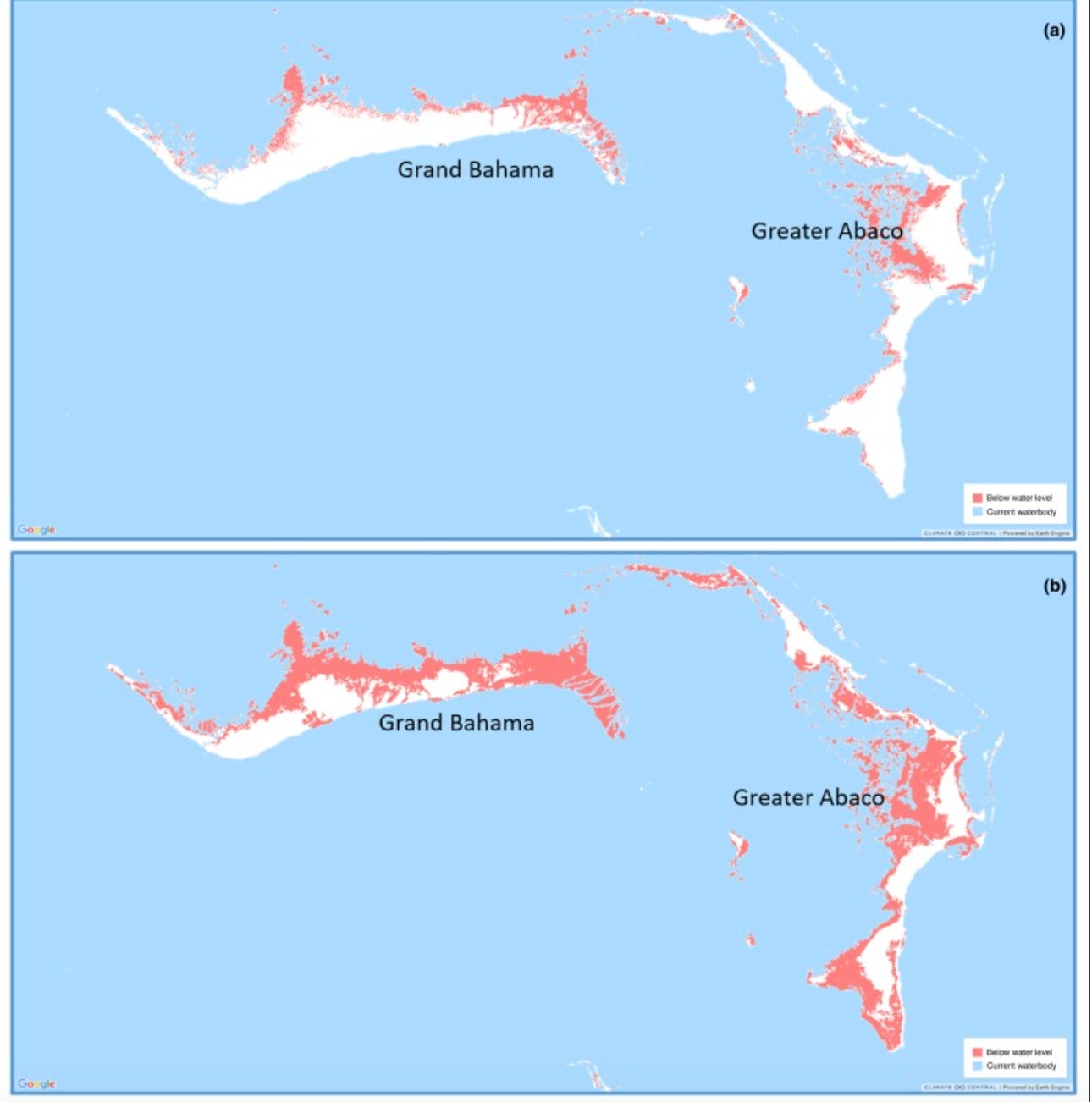

Over last four years, the island chain has taken on an outsized role in my life. In the summer of 2019 Dana and I bought a tiny cottage on the outer islands chain of the Abacos that within weeks was destroyed by hurricane Dorian, the historic storm which swept through the islands between 1 and 3 September 2019.

Wind speeds were sustained at more than 200 mph for several days and in an unusual and ominous development Dorian became stationary. If the storm had hit Nassau or Miami the loss of life and damage would have been immense. Our island was one of those on which 50-75 percent of buildings were destroyed.

All told the damage inflicted by Dorian in those three days came to c. 25 percent of Bahamian GDP and the Bahamas are one of the richest nations in the region.

Within a season or two the vegetation begins to recover from the lashing with salt water. Lives were put back together again. Billions of dollars flowed into reconstruction. But three years on, the scars are still clearly visible. Many ruins remain and the trauma is still live. For those who survived on the islands, all it takes is a thunder storm to revive the memory of those awful days and their prolonged and ghastly aftermath.

Since 2021, on what was left our lot, we have rebuilt a beautiful house (facebook, instagram, vrbo). The experience has been a psychodrama à la Grand Designs mixed with post-hurricane disaster capitalism in the complex economic and social setting of the greater Caribbean.

It has been a journey sustained by the beauty of the scenery, the support and love of dear friends and Dana’s indefatigable energy. It has also been an education. Along the way I’ve been trying to make sense of the experience, in medias res, so to speak. I’ve been wondering about what brought us to these islands and what kind of place they are.

Even before Dorian, feeling the force of a storm shaking what was then our tiny cottage, I wrote in a speculative fashion about the challenges to sovereignty posed by climate change. I wrote about the hurricane itself more or less as it happened. My vision then widened to the Caribbean as a whole and in particular to Haiti and US engagement there. You cannot spend time in the Bahamas with your eyes and ears open without becoming deeply interested in and concerned about Haiti. The majority of the people that built and maintain our house are from Haiti. They are in constant touch with family and friends and business connections there.

And then the FTX/SBF story added another layer. Why was FTX operating out of the Albany resort in Nassau? How did that world relate to the one that we were getting to know on the Abacos?

At one level the answer is obvious. The Bahamas are an offshore financial center. But that begs the question. Why are there offshore financial centers? And why are several of them in the Caribbean?

Over Christmas break I dug into this question in a long read for Foreign Policy.

***

In writing the Foreign Policy piece I was digesting three widely-cited historical and critical projects that have converged on the question of the geographies of capitalism and archipelago capitalism.

One was Quinn Slobodian’s illuminating discussion in Globalists of the relationship between neoliberal economics and the crisis of Empire. He traces the emergence of the original Austrian branch of neoliberalism and the founding of the Mont Pelerin society to the collapse of the Habsburg Empire in the aftermath of World War I. As he argues, Austrian economists of the 1920s saw the democratic nation-state as a threat to the free flow of resources that had been previously secured by Imperial power. A new political economy was required to encase the economy and insulate it from democratic national sovereignty.

As I show in the Foreign Policy piece, it is a logic that can be extended in interesting ways to the way in which offshore finance has found a home in the remnants of the British empire in the Caribbean.

Then in The Code of Capital Katherina Pistor showed us how the English common law functions as one of the key systems worldwide for the encoding of capital. Much of the Caribbean and the wider region including, of course, the United States has inherited the English common law from the original moment of settler colonialism when the region was joined in an interconnected system of plantation slavery and long-range commerce.

Source: Wikipedia

Finally in her ongoing project on archipelago capitalism Vanessa Ogle has explored the way in which decolonization impelled the flow of funds – so-called “funk money” – around the British Empire. As she points out:

In the British Empire and the age of empire more generally, the natural state of affairs entailed legal unevenness—“lumpiness,” as Lauren Benton has characterized it.3 This world was made up of centralized nation-states, multiethnic land empires, overseas empires with their colonies, protectorates, settlements, and dominions, as well as “informal empire” with its regimes of extraterritoriality and legal pluralism. Sovereignty was often attenuated, multiplied, and layered, and authority delegated. Local administrations in overseas territories had considerable leeway in drafting company and bank laws or tax codes and accounting standards for these respective entities and sub-entities. Legal and political unevenness greatly benefited tax avoidance, and capital accumulation more generally, on a global scale.4

This offers a counterpoint to the world of nation state economic policy, “(t)he New Deal, the European welfare state, decolonization, development and modernization projects in the Third World, and the Bretton Woods system” all of which were centered on nation-state-based and government-driven projects. The offshore world by contrast offered enclaves, special economic zones, havens, relaxed regulations and minimal oversight, flags of convenience, anonymous financial and banking institutions.

***

Between the three of them Slobodian, Pistor and Ogle, offer a compelling account of the way in which the world of empire smoothed the passage to that of neoliberal globalization and why the British Empire, in particular, was a complement to the American-centered model of global capitalism after 1945.