Adam Tooze's Blog, page 3

May 12, 2023

Ones & Tooze: Could Green Hydrogen Revolutionize the Energy Sector?

In today’s episode Cameron and Adam take a look at the emergence of green hydrogen and its potential for being a major boon to places like Africa and India. Adam also talks about how this green energy source ,which generates a tremendous amount of heat, will help reduce emissions for creating steel and other industrial processes.

In the second segment, grab your backpack, Cameron and Adam take a look at European travel on the cheap. They discuss low cost travel options, hosteling, and which European countries offer the most bang for the buck. (Hint…try Albania!)

Find more episodes and subscribe at Foreign Policy.

May 10, 2023

Chartbook #214: Why the 2023 banking crisis does not look like 2008, or why one run is not like another.

How does the current rash of banking crises compare to 2008? The GFC was a slow-burning affair. Does what we have seen so far in 2023 resemble the overture in 2007? Could we be in for a major shock to come? It is too early to tell and there may be more to come, but, so far, the differences between 2023 and 2008 are more striking than the similarities.

***

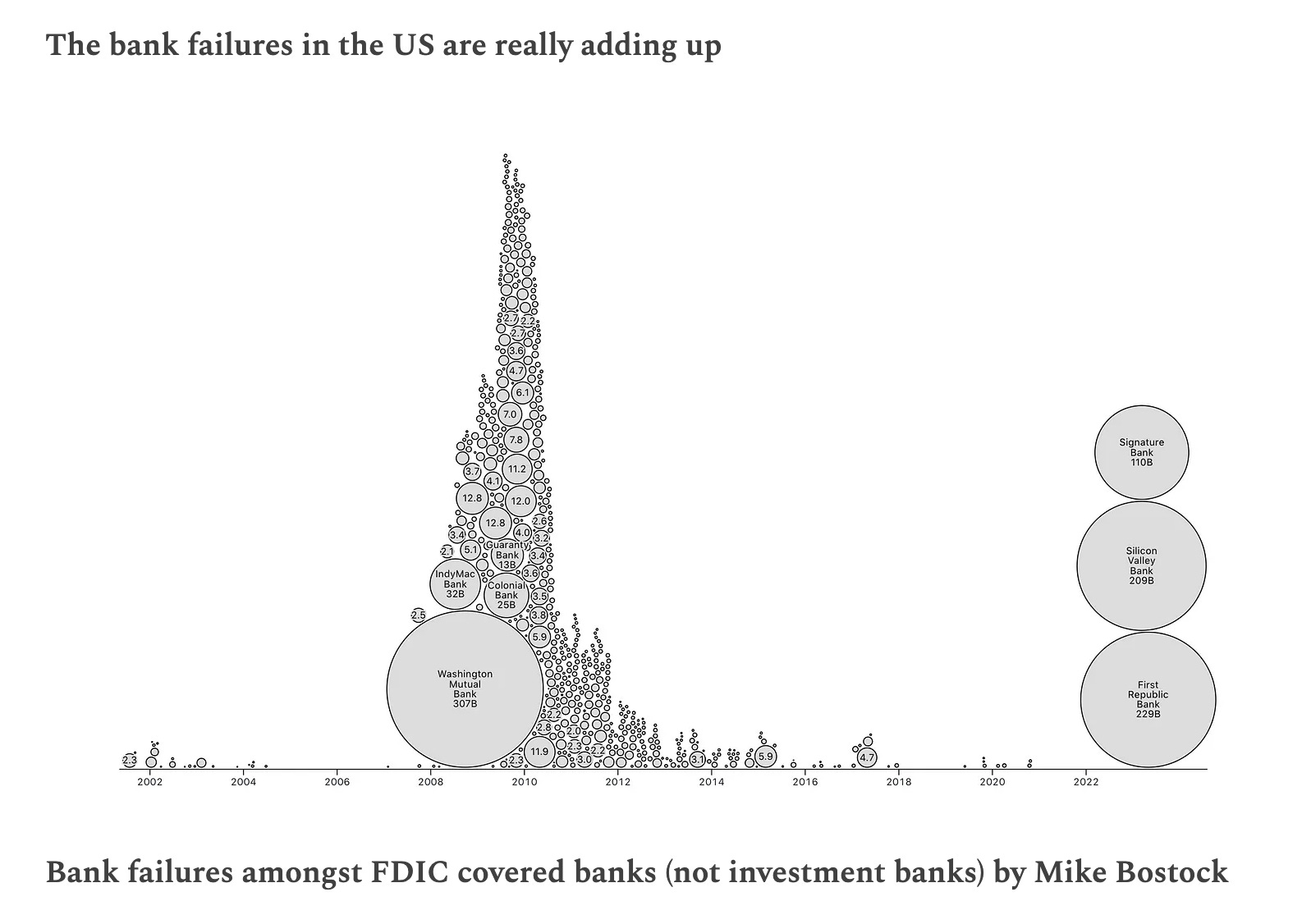

As this fantastic graphic makes clear, there is nothing small about the trio of banking crises that have rocked the US since the beginning of 2023. These are major events.

Admittedly, the graph is based on a wonderfully clever presentation of FDIC data. This means that it does not cover the biggest failure of 2008. The collapse of Lehman Brothers, an investment bank not covered by the FDIC, was roughly the size of all three of the 2023 failures put together – $639 billion in assets. The graph would look quite different if that giant bubble was added in 2008.

But it is not simply the question of balance sheet size that differentiates 2023 from what transpired in 2007-2009.

***

The most basic difference between then and now is the economic backdrop.

The crisis in 2007 was triggered by the unraveling, on both sides of the Atlantic, of a giant, credit-fueled real estate bubble – the culminating point of what Jorda, Schularick and Taylor have called the “great mortgaging”.

Given the historic scale of this housing market bust, even if there had not been bank failures, after 2007 the economies of Spain, Ireland, California and Florida – the economies most heavily dependent on real estate – were in for a deep recession. It was the turning point in house prices that triggered a credit event, spreading losses and panic through the financial system.

Our situation is very different. The immediate source of the shock today is not the business-cycle as such, but the Fed’s interest rate hike, which itself is driven by the need to respond to a historically unique surge in post-COVID inflation. It is the sudden hike in interest rates that has rocked the balance sheets of banks that overcommitted to long-term investments in low-rate assets, whether those be US Treasuries or the jumbo mortgages issued to First Republic’s affluent clients.

Far from facing a significant recession, the Fed’s rates have had to go as high as they have because the real economy is “too” robust. Unemployment in the United States has fallen to record lows. Europe is as close to full employment as it has been in years.

This is not to say that the hike in rates will not in future deliver a nasty shock to the housing market. It surely will. We have already seen some failures of small US mortgage lenders. There is much to worry about in the commercial real estate sector. But, if that is, indeed, the shock to come, it is not what we have seen so far.

SVB had a lot of government-guaranteed mortgage-backed bonds on its balance sheet, but the problem with those was not that they were in default, but that the rates they offered were too low and the bank was facing large mark-to-market losses.

***

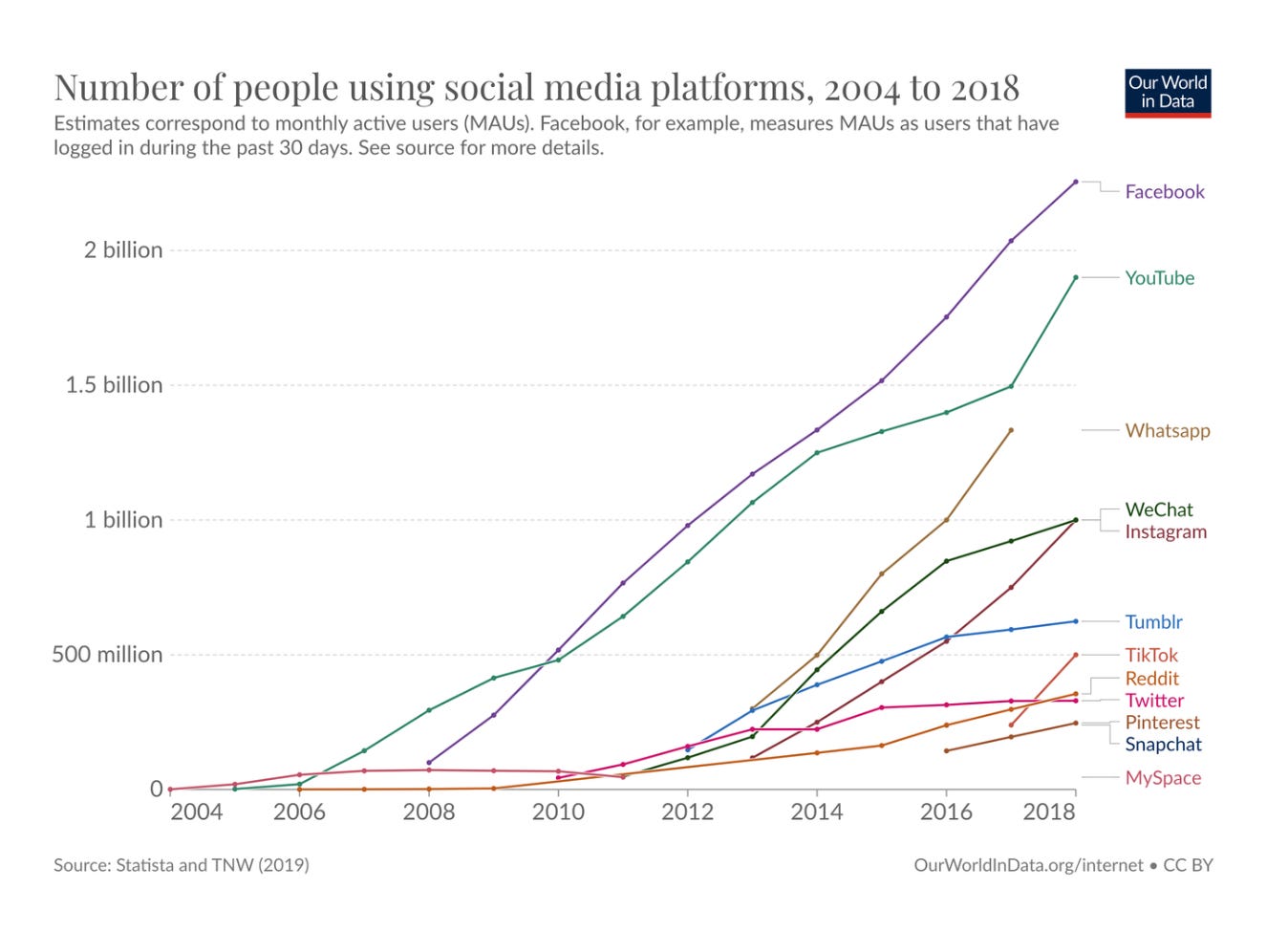

There has been a lot of talk in the current context about the speed of the bank runs on SVB and First Republic. This is commonly attributed to the rise of social media and digital banking. In 2008 both were still in their infancy. Smartphones and platforms like Facebook took off just as Lehman failed.

Source: Our World in Data

Digital communication no doubt speeds up the spread of news. Bank runs are news-driven events. This may have played some role in accelerating how quickly deposits drained out of SVB and First Republic.

But as shocking as they may have been, the fact that the current rash of banking crises have been classic bank runs is good news. Because it was not conventional bank runs that made 2008 so dangerous.

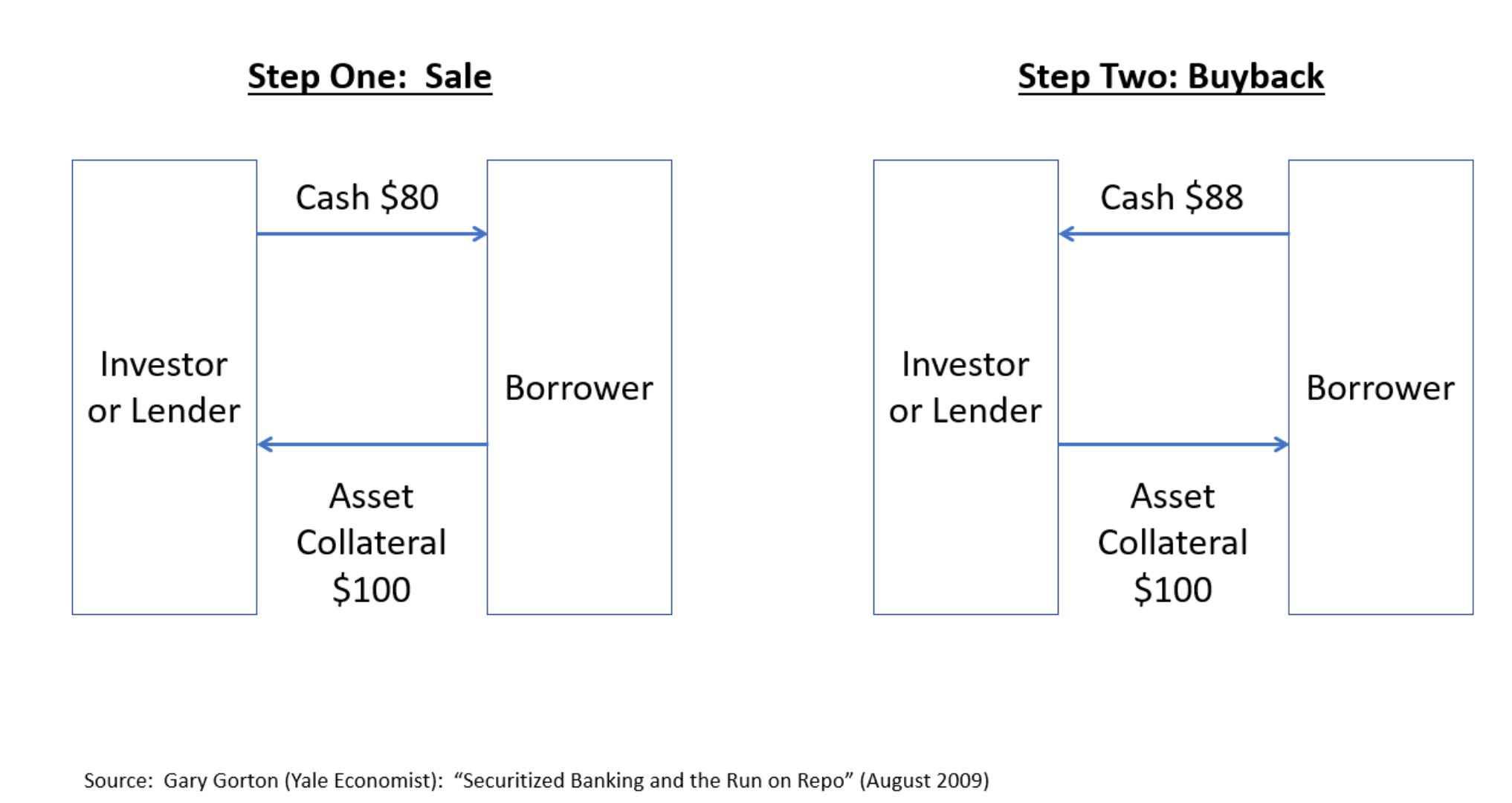

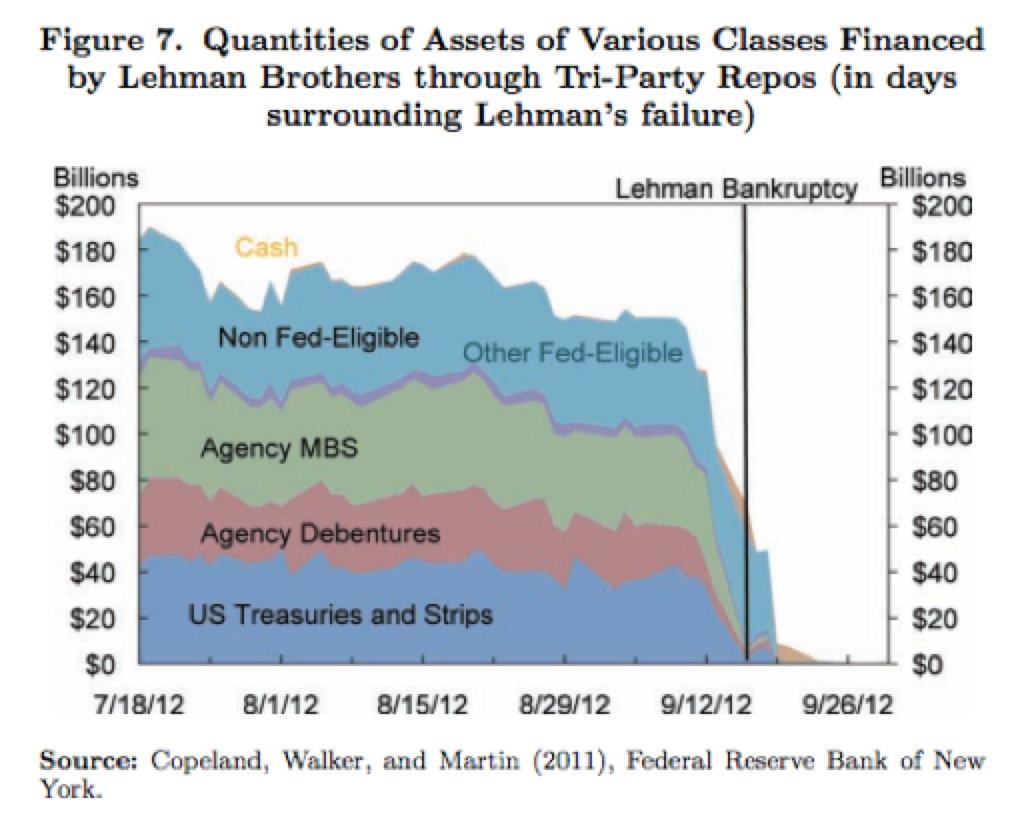

There were classic bank runs in 2007-8, at Northern Rock and Washington Mutual. But the crisis that brought Lehman to its knees in September 2008 was not a run of small depositors or business accounts. Lehman had no mom and pop accounts. What brought Northern Rock, Bear Stearns and then Lehman down was a collapse in their short-term ultra footloose market-based funding. Specifically what killed Lehman was what Gorton and Metrick called a “run on repo”.

Repo is the market, operating between major players in the financial system, through which banks like Lehman financed portfolio of mortgage backed securities and other fixed-income assets. In repo-based banking, funding is obtained not by taking deposits and then investing the funds in interest and profit-yielding assets. Funding is obtained by buying an asset, like a Treasury or a mortgage-backed security and immediately selling it, with the promise to repurchase at some point in the not too distant future, only then to repeat the operation, again and again until the bond matures, or it is disposed of. In the overnight repo market this churn takes place literally every day.

One might imagine the repo markets and its participants as a staggeringly over-sized pawn shop ecosystem. Every day collateral is given, credit is issued and then the original owner redeems the collateral the following day. And this takes place daily on the scale of trillions of dollars.

Clearly, this is spectacularly more elastic, dynamic and labile system than deposit-based banking. A run in this market consists simply in trading parties, who normally show up to sell, buy and repurchase collateral – mainly Treasuries or other fixed-income assets – one day refusing to transact with a particular counterparty. For Lehman this was a $160 billion shock delivered in a matter of days.

To state the obvious, this hidden “run” on Lehman dwarfs anything we have seen in 2023 in terms of scale and speed. The news of Lehman’s situation was no doubt communicated around Wall Street on Blackberries and Nokias, by emails and phone calls. But the medium and the ease of communication was not the point. It was the scale of the market and its structure – a highly volatile system for financing assets of durations measured in years or even decades on ultra-short-term funding – that created the risk.

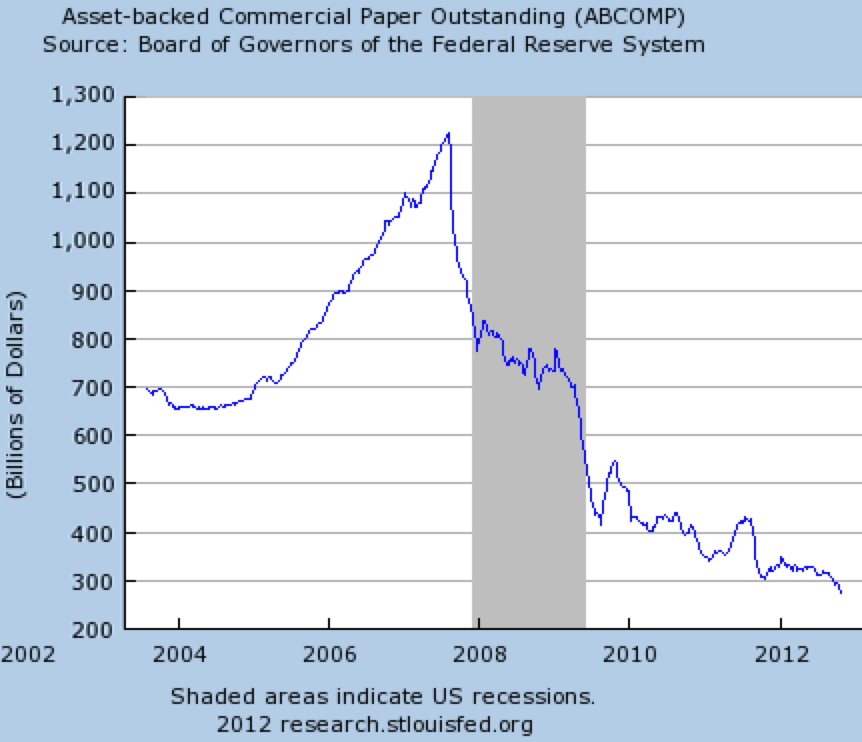

The tension in the market-based funding system for the megabanks of the period began to build up already in 2007. The asset backed commercial paper market began to shut down in August 2007

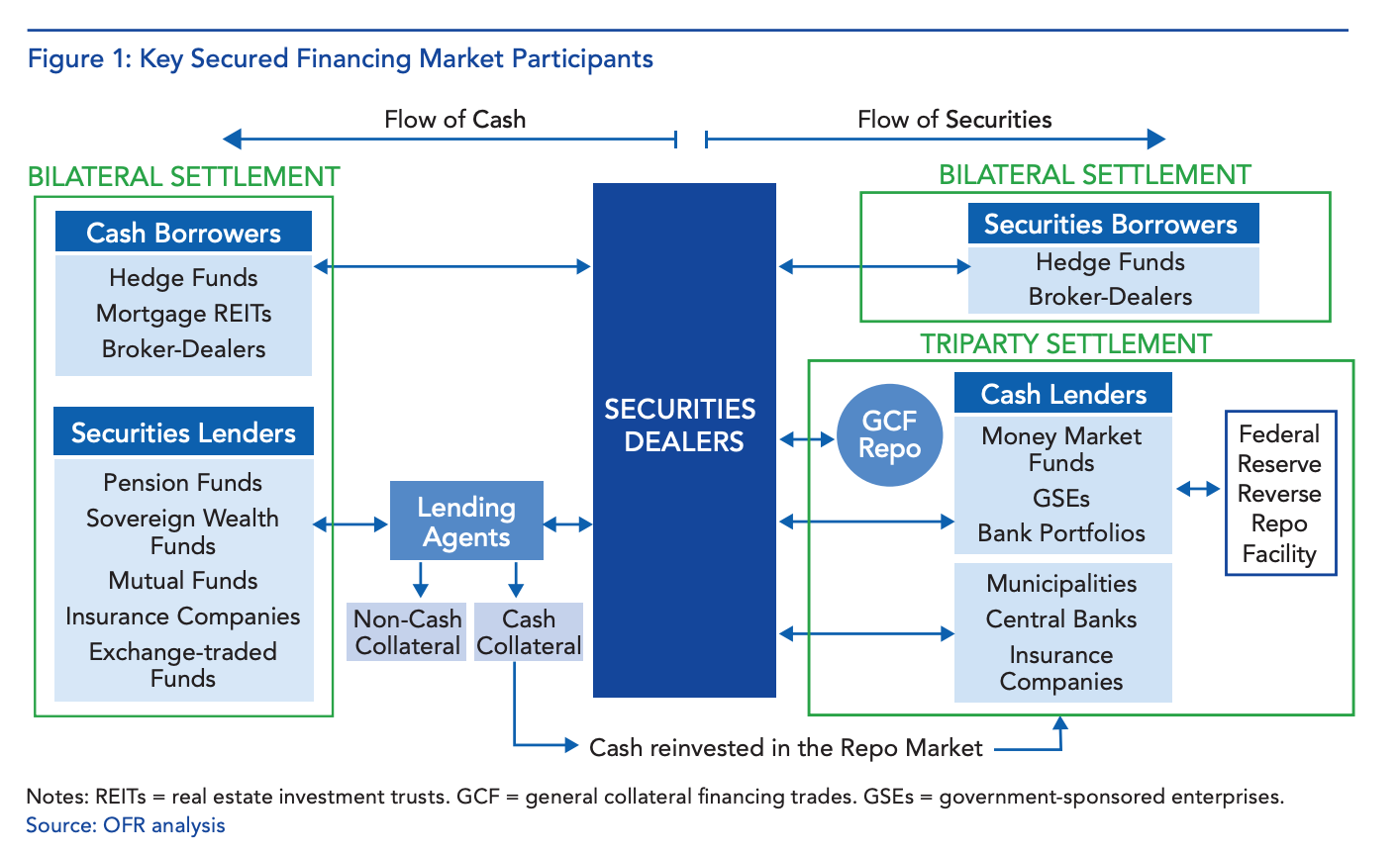

If anything of the kind were to be visible in the current moment, it would be a loud alarm bell ringing. But, so far, rather than a flight from the system of market-funding we have seen depositors withdraw cash from their bank accounts, which in the United States pay virtually no interest, so as to transfer them to money market mutual funds, which are an integral part of the repo market ecosystem.

Source: OFR

Not until we see shockwaves rocking the system of market-based funding, as we did in 2007-8 and again in 2020, will 2023 really begin to register on the Richter scale of financial shocks.

***

Furthermore, you cannot judge a crisis, or any other historical event for that matter, only by what actually happens. To take the measure of a historical moment you have to understand what lurks, as yet unrealized on the horizon – what Reinhart Koselleck called the horizon of expectation.

What made 2007-8 so terrifying was not simply the carnage in the mortgage lending sector, or Lehman’s failure. The terror for those in the financial system, were the dangers that lurked on the balance sheets of the world’s monstrously over-sized universal banks.

Citigroup and Bank of America, the two most vulnerable of the giant banks in the US, were not out of danger until the second half of 2009. Unlike Lehman, they were never allowed to get to the edge of failure because it was not clear that if they had reached that point they could have been contained. Their balance sheets were simply too large and complex. But the market gave its judgement on their true health. Their shares were written down to a fraction of their pre-crisis level.

Beyond the American giants there were also a huddle of huge banks in Europe that were also in deep trouble and had large footprints in Wall Street and in US mortgage funding. It is not for nothing that the Fed disbursed a majority of its direct liquidity support to non-American banks and set up the swap lines to provide even more dollars to the world’s central banks. It is not for nothing that 2008 gave rise to a special regime of regulation for the banks designated as G-SIB.

So far in 2023 those kinds of shadows do not hang over us. Already in 2020, faced with the gigantic COVID shock, the balance sheets of the biggest banks proved relatively robust.

What about Credit Suisse you ask?

Well, the good news about Credit Suisse is precisely that what brought it down was not a 2008-style market-based funding crisis but something akin to a classic bank run. Unusually for a bank of its size, it sustained massive withdrawals by depositors over the best part of six months that made its positions unsustainable.

***

There are aspects of financial history that attract simplistic social psychological generalization. Banks are creatures of confidence. Confidence is fickle, subject to the forces of crowd psychology etc etc. All too easily this produces a rather flat account of financial panics and manias, from the tulip bubble to Lehman. The same mechanisms repeat themselves.

It would be foolish to deny that some generic features of financial economics have real force. A bank with a balance sheet like that of SVB is going to be vulnerable to runs, whatever the historical situation. In this post I’ve referred to a “classic bank run”, i.e. a confidence-driven depositor stampede.

But the existence of SVB, or First Republic or Lehman, in the form that they took before they failed, can be explained only by rather peculiar historical features. The shocks that brought them down were historically unique too. There had never been. a mortgage boom quite like that before 2008. The interest rate shock of 2022-2023 is the most severe since the 1980s and follows a period of uniquely low rates. And how they fail depends critically on the logic of their business model. With hindsight, the funding structures that collapsed in 2008 were the equivalent of driving without seatbelts or smoking indoors, a reflection of time bound and institutionally defined behavioral norms that seem barely comprehensible today.

It cannot be ruled out, of course, that in two or three years time we will look back on this moment and be able to recognize financial structures that with hindsight appear astonishing in their obvious danger. SVB boggles the mind.

There may be more to come, perhaps in the realm of private finance. In any case, it is on the constantly evolving structures of finance and on the suspiciously opaque links in the chain that we should be focusing our attention, rather than relapsing into an account of history viewed as the arena of trans-historic psychological patterns.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you wil receive the full Top Links emails several times per week.

May 6, 2023

Chartbook #213 Expanding the fortress: Why JP Morgan is even more important than you think!

(The) Ouroboros, (is) a mythical animal which swallows itself, starting with the tail. It epitomises paradox and is a pretty good emblem for US banking at the moment. Autocannibalism is not something anyone should try at home.

What a great passage from Jonathan Guthrie in the FT last week!

But is American capitalism best thought of as engaged in autocannibalism, or does it more closely resemble an unbalanced Darwinian competition with one giant apex predator? A predator that is taking advantage of the harsher living conditions for many of its smaller competitors and thus permanently changing the “game”.

***

A reversal of monetary regime like the one we have seen in the last 18 months creates stress and risk for the weakest financial institutions. But it also open opportunities for accumulation and creative destruction. The way key players exploit those possibilities reshuffles the economic and political pack. That in turn shapes what comes to be seen as “structure”, or the “order of things”.

In the financial crisis of 2008 there were two big winners. One was BlackRock, which, as I discussed in Chartbook #82, emerged from the GFC as the dominant asset manager of the following decade. In banking, if there was a big winner in 2008, it was JP Morgan. JP Morgan’s leadership came to regret the terms of their acquisitions during the crisis. As the ultimate owners of Bear Stearns and Washington Mutual JPMC was exposed to huge liabilities. But the deals helped to consolidate JP Morgan’s position both in retail and investment banking.

In the crises triggered by the Fed’s rate hiking cycle in early 2023, it is again JP Morgan Chase that is the dominant player.

What makes JP Morgan Chase stronger than other banks in the U.S. financial system? What is the nature of its relationship with the U.S. government?Could CEO Jamie Dimon’s political influence extend to electoral politics?Cameron Abadi and I discuss all these questions on the Ones and Tooze Podcast this week. Click here for the links.

***

The immediate cause for all our focus on JP Morgan and its CEO Jamie Dimon is that having led the private-sector effort to stabilize First Republic bank, JP Morgan emerged from a frantic weekend of bargaining with the Federal Deposit Insurance Corporation (FDIC) as the only bank that was able and willing to absorb First Republic lock stock and barrel. The FT report on the negotiations by James Politi, Colby Smith, James Fontanella-Kahn, Stephen Gandel and Brooke Masters brings this out brilliantly.

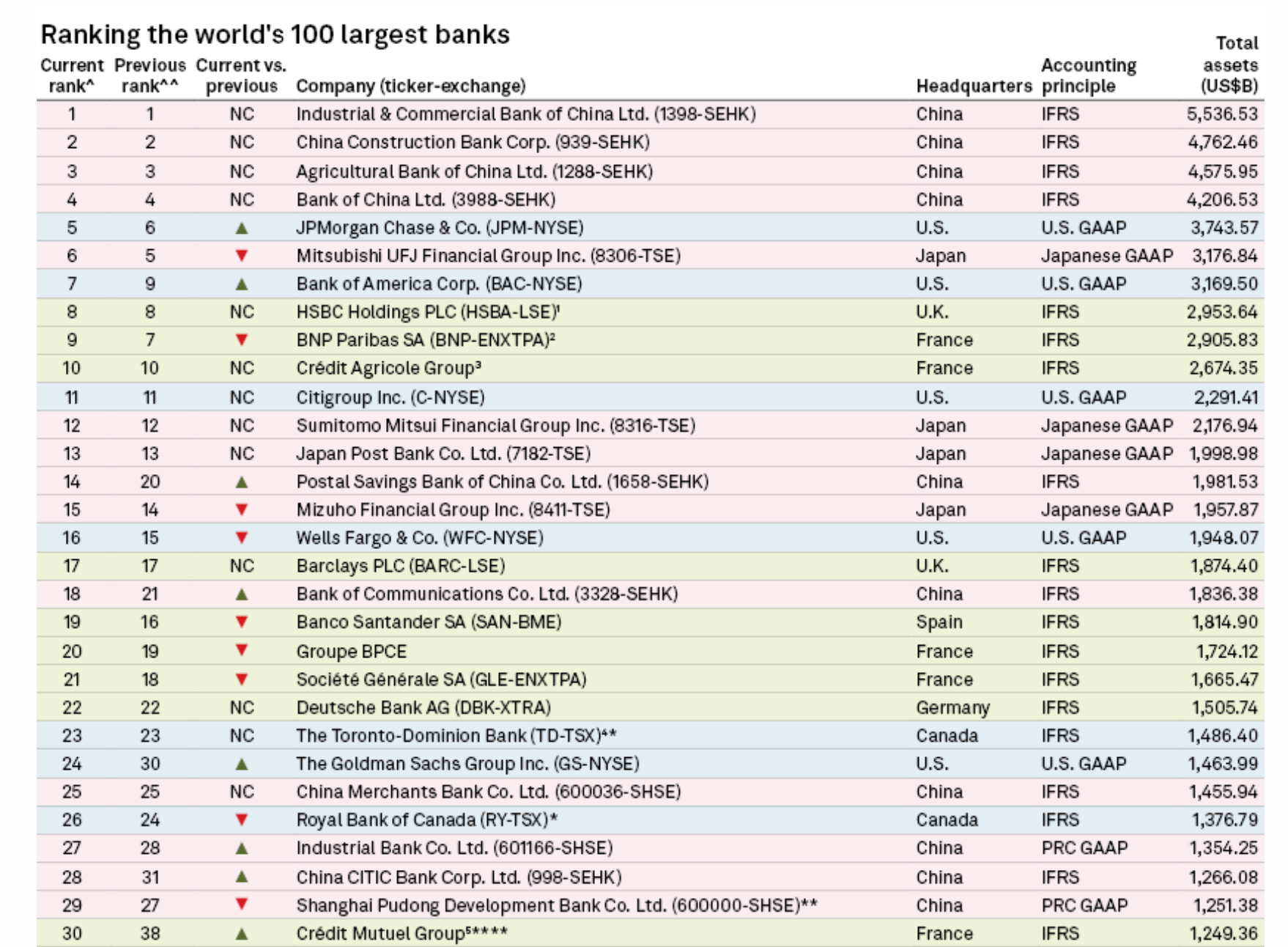

The events of the last few months confirm the fact that JP Morgan Chase now stands head and shoulders above all the other major American banks. Indeed, it is now the premier bank of the non-Chinese world. Here is the SPGlobal ranking of the top 30 global banks as of the spring of 2022.

Source: SPGlobal

JP Morgan is not just the largest non-Chinese bank by size. It is also a universal player with a powerful position in investment banking, retail banking, and asset management.

The crisis has triggered many excellent accounts of how JP Morgan got that way. For something that is somewhat older but goes deeper check out the Economist article from March 2020.

As the Economist report points out, the merger of Bank One and JP Morgan that Jamie Dimon pulled off in 2004 was not doomed to succeed. One of the reasons that JPMC is the only American bank whose return on common equity was higher in 2019 than in 2005 was that in 2005 it trailed so far behind the rest. It is now by some margin the most profitable bank the world has ever seen.

The heritage and the name associated with JPMC goes back centuries. As the FT notes.

Its heritage includes a company started by the US founding father Alexander Hamilton, the investment bank run by legendary financier John Pierpont Morgan as well as lenders that financed the Erie Canal, the Brooklyn Bridge and the UK and French armed forces in the first world war.

But JPMC as a national, universal banking franchise is a new phenomenon.

Even as recently as 1991, the retail bank that would eventually become a global banking juggernaut had only $37bn in deposits. The group now has almost $2.5tn and its market share has grown by 10 times, from 1.5 per cent to 14.4 per cent.

Source: FT

This growth was enabled by legislative changes in the 1990s that liberalized interstate banking. Citigroup was the first to take advantage of these, but Jame Dimon made it his personal mission to crush Citigroup in competition and he has succeeded spectacularly.

Whatever one may say about Dimon he is driven and consistent actor. As the Economist notes:

… in his 2005 letter to shareholders, his first as the boss of jpm, he sketched out a vision for the firm that he has stuck with through thick and thin. It registered not only his loathing of bureaucracy and bloat, but also his fondness for a “fortress balance-sheet”. He wrote of the natural connections between different parts of a large bank—between the commercial and investment banks, the credit-card business and the retail bank, and the cash-management and asset-management arms. In summary, Mr Dimon declared that “size, scale and staying power matter”.

***

We are no longer in the era in which Wall Street bankers regularly occupied the job as US Treasury Secretary. But there can be no doubt that as far as strictly financial and banking issues are concerned, JP Morgan and its CEO Jamie Dimon have privileged access to the Fed, the Treasury and the White House.

Furthermore, JP Morgan occupies a pivotal position as a broker-dealer and market maker for US Treasuries, the most important financial asset in the world. It is not by accident that even Bloomberg relies on JP Morgan’s data to track that all-important market.

And this is the point at which I want to stand back a bit further to ask about JP Morgan’s significance in a more general sense.

***

Common sense commentary on economic policy is demarcated into distinct domains.

Right now industrial policy, climate, competition with China etc, constitutes one such domain. It is to a surprising degree insulated from macroeconomics. This is one of the many weird effects of the Inflation Reduction Act, which coupled tax incentives to private investment with tax increases. The separation between the industrial policy debate and broader macro is reinforced by the fact that thanks to the subsidies and “animal spirits”, investment is chips and green energy is booming regardless of the Fed’s interest rate hike. So the industrial policy debate exists almost in isolation from the recession debate.

The ongoing banking crisis is tied to industrial policy-tech competition by way of concerns for regional business financing and considerations about the structure of the financial system itself. Should the biggest banks be allowed to dominate? What impact might that have on tech and industrial financing? This is the key concern of folks like Robert Hockett and it is rooted in deep American themes:

For much of its history, the US by law kept its banks local and sector-specific. The Founders had known first-hand the evils of concentrated metropolitan banking — ignorance of local borrowers and economic conditions, focus on short-term profits rather than long-term investments, and related problems. … Regional, community and sector-specific industrial banks like Silicon Valley Bank lent “patient capital” to startups and small businesses — the incubators of future industrial renewal. In other words, the banks were willing to wait years before expecting their startup borrowers to turn profits — essential in industries that require time to scale up before they can become profitable.

They stood ready to fuel the new growth where it was needed, knowing as they did both the special needs of their clients in particular sectors — like tech, for example — and economic conditions in the locales where their clients did business.

Capped deposit insurance is now destroying these banks.

Federal deposit insurance coverage is currently limited to $250,000. That would be plenty for you and me, but the startups and other small businesses on which our industrial recovery depends have large payrolls and weekly operating expenses. For them, $250,000 is mere chump change.

They are thus faced with a Hobson’s choice, especially in times of banking distress like the present: Retain the advantages of regionally focused, client-sensitive, sector-specific Main Street banking at risk of losing deposits in bank runs, or flee to the safety of too-big-to-fail, one-size-fits-all global Wall Street banks that know nothing of their regions’ or businesses’ special conditions or needs.

JP Morgan features in this story as the universal bank predator. It is also, of course, the most enthusiastic funder of fossil capital, as the Union of Concerned Scientists documents here. Between the Paris climate deal and the end of 2021 JP Morgan provided $ 382 billion in fossil funding.

Quite aside from this discussion about banks as institutions of the American Republic, there is the domain of macroeoconomics in which we endlessly ruminate over Fed interest rate policy and (to a much lesser degree right now) the fiscal stance. This is the churning daily conversation in financial markets, especially fixed income markets, which are driven by concerns for inflation, rates and yield curves. JP Morgan’s data serve as key indicators of the state of the Treasury market.

This macroeconomic conversation connects to the banking crisis by way of the impact of the interest rate shock on the balance sheets of badly managed banks like SVB and First Republic, at which moment JP Morgan enters the story as the White Knight.

What slips through the cracks is JP Morgan’s role as a macrofinancial actor of decisive importance and as one of the forces shaping those financial markets.

***

Repo is the key to modern market based financial systems. This is the market in which portfolios of assets are funded by “buying” and “selling” them with a commitment to repurchase at intervals as short as overnight. It was the run on repo, not old fashioned bank runs like the ones that we saw at SVB or First Republic, or on Northern Rock in Britain in 2007, that drove the financial crisis of 2008. In a repo run the counterparties to trades that are normally churned every day in volumes of hundreds of billions of dollars, withdraw their funding. This instantly leaves huge portfolios unfunded, triggering defaults and further withdrawals. The collateral, which is the basis for repo, can be seized but the market ceases to function.

As Carolyn Sissoko showed in an important paper, published in the thick of the COVID financial crisis of 2020, the newly merged JP Morgan Chase in the late 1990s and early 2000s was pivotal to the emergence of the repo-based money market.

As Sissoko puts it in admittedly dramatic terms:

… in 1997, notably the year in which the Asian Financial Crisis took place, JPMorgan moved its repo market making ‘into the bank,’ and then in 2000 became one of the core tri-party clearing banks via a merger with Chase Manhattan Corporation. The end result of this bank intermediation of the repo market was to super-charge it with implicit government guarantees, and to convert JPMorgan Chase (JPMC) into a de facto central bank implementing its own monetary policy through the repo market.

Nominally there were two clearing banks in the triparty-repo market, but de facto Bank of New York Mellon was a fig leaf for JPMC dominant position. This central position was also confirmed by work by Grace Xing Hu, Jun Pan , and Jiang Wang. As they found in their data it was the close connection between JPMC and fund manager like Fidelity that shaped the triparty market.

Though the data are more scanty, there can be no doubt that JPMC is also a key player in the bilateral repo market which is far larger than the better documented triparty market. As Sissoko describes the situation in 2008.

During the height of the boom that preceded the 2007-09 crisis, there is every reason to believe that JPMC had the power to define the repo market both by pricing assets and by setting the terms on repos. Indeed, both Bear Stearns and Lehman Brothers failed when JPMC acting as a clearing bank determined that their assets were no longer adequate to support the debt they were carrying. In short, JPMC created a new role in financial markets, the dealer of last resort, a kind of central bank for securities markets that had the capacity, due to the flexibility of too-big-to-fail capital constraints, to price and fund assets over what appeared to be the long-run. Or at least that’s how it appeared until the Bear Stearns failure in 2008.

Sissoko’s story is consistent with the quantitative evidence painstakingly compiled by Gary B. Gorton, Andrew Metrick, and Chase P. Ross in their article “Who ran on repo”. In 2008 at the critical moment in the crisis they show that.

The Flow of Funds data show a significant drop in repo funding to banks and broker-dealers during the financial crisis. The drop was rapid, with net funding to banks and broker-dealers falling from $1.8 trillion in 2007:II to $900 billion in 2009:I. Broker-dealers (AT, most prominently JPMC) also contributed to the run on liabilities by withdrawing funding themselves. Although it is washed out in the net funding numbers, broker-dealers reduced both gross repo assets and gross repo liabilities, with the former dropping by about $490 billion just in 2008:III, the quarter of the Lehman failure.

When JPMC pulled back from Lehman as the first line lender of last resort, it was the Fed that had to step in to backstop the entire banking system of the dollar and eurodollar world.

The key point here is that the growth of JPMC is not simply a corporate success story. And JP Morgan’s power is not limited to its ability to profit from its strong balance sheet or its excellent connections in Treasury, Fed and White House, to snap up rivals. The financial markets, as we know them in the US today, are to a significant extent moulded around JPMC’s business model and its decisions have macroscopic effects. This is the flipside of Jamie Dimon’s posturing as a patriotic servant of financial stability.

***

Perhaps the most dramatic demonstration of this connection came in 2019 with the so-called repo market shock that preceded the COVID crisis. As Nick Dunbar at Risky Finance showed with some excellent number-grubbing, JPMC was at the heart of this story.

As a reminder

On 17 September (2019), the secured overnight financing rate (SOFR), which had hitherto closely tracked the Federal Funds rate, suddenly rocketed up to 10%. For a brief moment, US dollar repo enjoyed the same overnight funding cost as Brazil.

At this moment, banks were not doing their customary job of lending out the cash that the Federal Reserve had provided (via reserve balances). They had stopped purchasing treasury bonds and other securities from counterparties, which they would resell a short time later at a slightly lower price. The Fed had to step in and start lending instead, providing up to $75 billion each day.

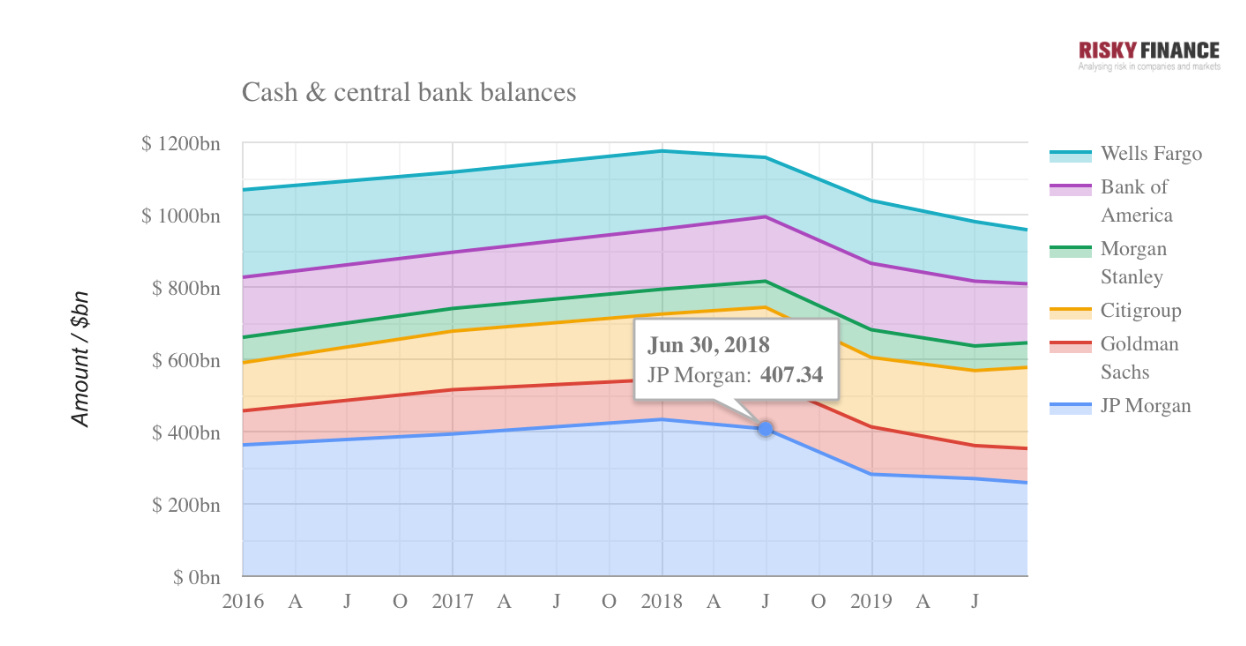

To understand what happened it emerged that one had to understand what was happening at JPMC

Between June 2018 and June 2019, JP Morgan’s cash and reserve balance fell by $138 billion, a decline of more than a third. By contrast, cash and reserve balances for the other five largest US banks barely fell at all during this period, as the Risky finance banking tool shows. … As the Bank for International Settlements noted in its December 2019 quarterly report, the reduction in cash by “top four banks” (read JP Morgan) coincided with a structural change in the repo market – instead of using repo as a funding source as they had done in the past, the

largest US banksJP Morgan instead became a net provider of funding. We see this in the chart of net repo assets versus liabilities of the banks over time. While the BIS took care to anonymise the names of the largest banks in its study, we can be less circumspect. According to Risky Finance data, JP Morgan accounted for 41% of all repo lending by the six biggest US banks at the end of 2016. By June 2019, this had increased to 46%, or $465 billion of repo loans. In effect, JP Morgan was the lender-of-last-resort to the repo market.

Dunbar’s use of the strikethrough – largest US banksJP Morgan – is a brilliant device to highlight the way in which reporting conventions encode, obscure and thus also help to perpetuate structures of power in the operation of our financial system. It makes a big difference politically whether you gesture vaguely and complacently to “markets” or actually name names.

***

Unlike in 2008 or 2019 there is no reason to think that JPMC is a significant driver of the troubles that have befallen the smaller regional banks in the US in recent months. The point to be made here is not to name and shame. But to suggest something more general:

When we tell the story of JP Morgan under Jamie Dimon as a case study in business success we are conforming to conventional ways of thinking about economic reality, which separates macro and micro, economic from business news, managerial success from economic policy deliberation. But in so doing we are understating JPMC significance to the operation of the dollar-based financial system and thus to the political economy not just of the United States but of the world today.

Max Abelson and Hannah Levitt wrap their piece for Bloomberg with a nice set of observations

If you’re tempted to compare it to BlackRock, remember that the money manager’s $9 trillion of assets are in funds it oversees for clients. JPMorgan, by comparison, finances the world (and has an asset management operation that’s itself about a third the size of BlackRock). And it processes more than $5 trillion of payments a day. You can think of it as an empire all its own. Bloomberg Opinion columnist John Authers goes further, calling Jamie Dimon the sun around which the financial system revolves and describing JPMorgan as a kind of public utility, big enough for the government itself to depend on. Dimon likes to say that the bank has a fortress balance sheet, an image that political economist Mark Blyth elaborates on. “If the only game in town is a medieval fortress, I want to be inside,” says Blyth, who runs the William R. Rhodes Center for International Economics and Finance at Brown University. “Hey, we have the castle. Don’t you want to be in the castle? It’s dangerous out there.” In the first three months of the year, as other banks saw savers depart, deposits at JPMorgan rose. But there’s a problem with everyone wanting to be in the castle. “What happens if the castle walls get breached?” Blyth asks. “We’re all screwed.” Economic power in the US runs in eras. As Blyth puts it, after World War II, when society more or less had to be rebuilt, the fiscal capacity of the US Treasury dominated. When inflation became the enemy and the Fed had the power to fight it, fiscal dominance gave way to monetary dominance. Now too-big-to-fail banks’ becoming bigger could usher in something new. “We may be in a world of financial dominance,” he says. “I don’t know, but it sure smells that way.”

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you wil receive the full Top Links emails several times per week.

May 5, 2023

Washington isn’t listening to business on China any more

The waning of the ‘peace interest’ leaves multi-billion-dollar investments hanging by a thread

Read the full article at The Financial Times.

Ones & Tooze: Is JPMorgan Chase Bank Helping the Banking Industry or Itself?

JPMorgan Chase has come to the rescue of the banking industry once again by buying the doomed First Republic Bank. On this week’s show, Adam and Cameron discuss what JPMorgan gets from the deal (spoiler alert: higher profits and even more sway in the U.S. financial system).

Find more episodes and subscribe at Foreign Policy.

May 3, 2023

Chartbook #212 The end of the petrodollar? How macroeconomics may compound geopolitics in shaping the future of the dollar system.

One of the striking features of the speculative talk about the future of the “dollar system” is the degree to which it hinges on highly politicized, small-scale trades between marginal players in the world economy e.g. Bangladesh and Russia, Argentina and China etc, rather than on close observation of the way the dollar functions in connecting giant pieces of the world economy. This lack of macroeconomic perspective is regrettable because it is not just the politics of the world economy that are shifting. The economics of the “dollar system” are not static either. The dollar system is a constantly evolving and shifting assemblage that is entangled with both the global business cycle and structural change in the world economy. In focusing on the geopolitical pressures generated by sanctions and other measures, we may be missing macroeconomic forces that add considerably to the pressure on weaker members of the dollar system.

***

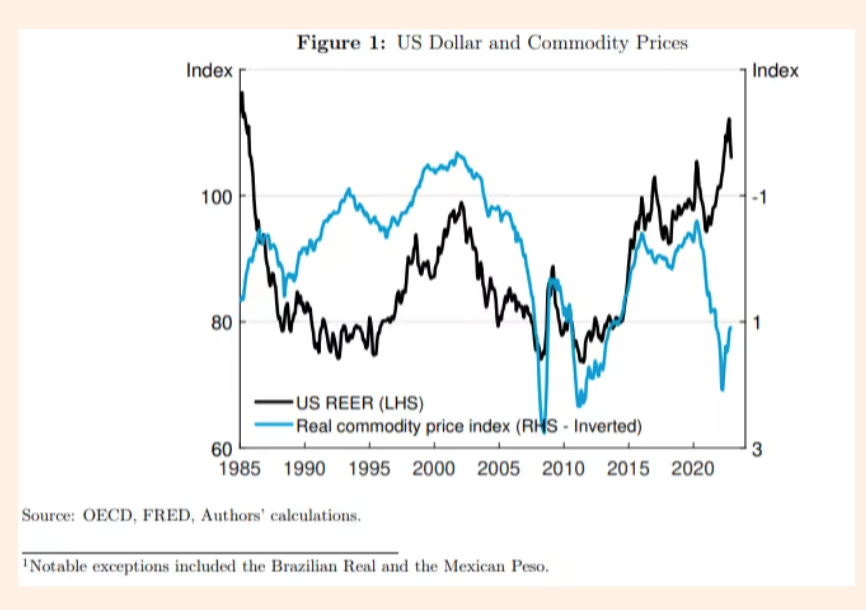

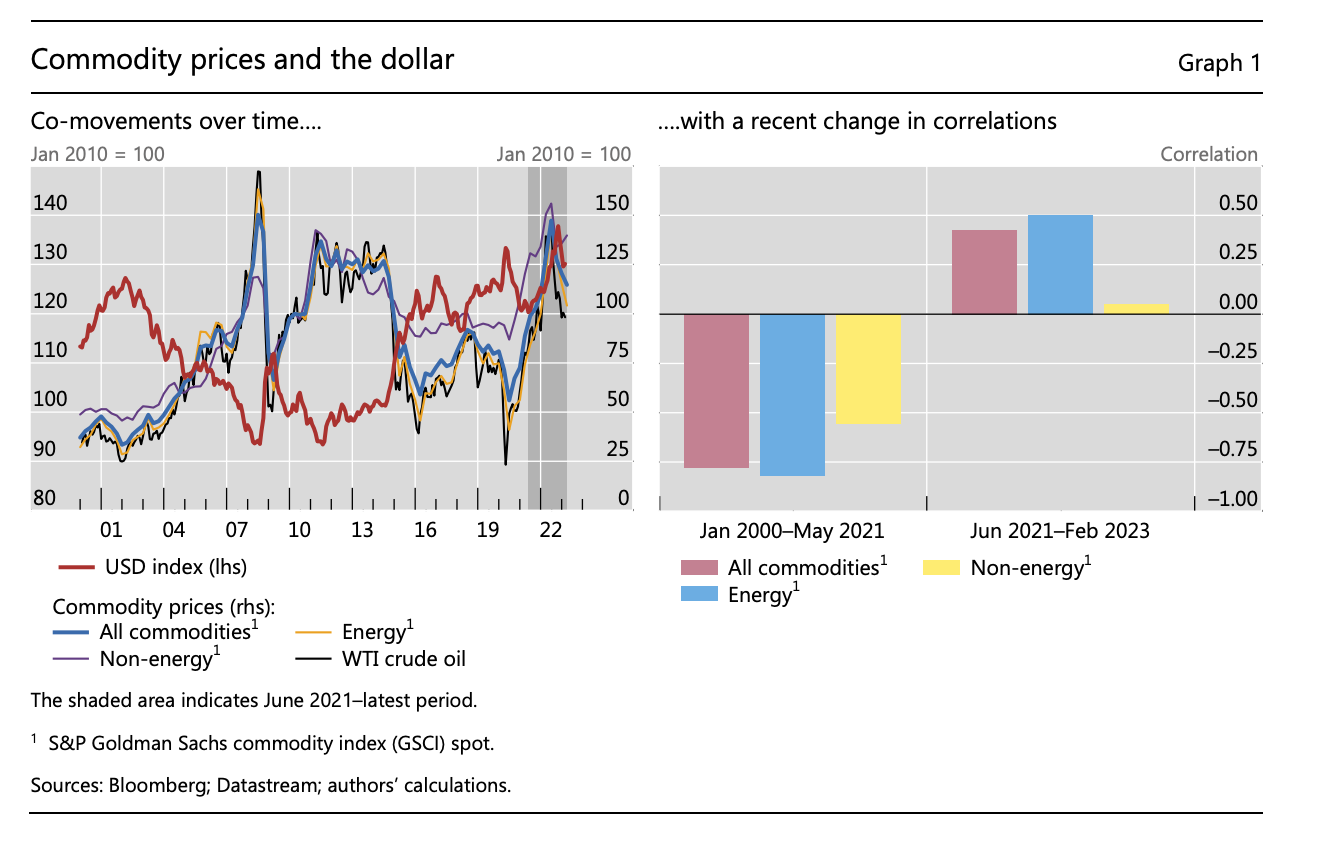

One of the remarkable developments of the global upswing following COVID has been the fact that commodity prices and the dollar have moved up and down together. As is brought out by this nice graphic from the FT, this is a reversal of a negative correlation that has held for forty years.

The logic behind the negative correlation between global commodity prices and the dollar might be explained as follows: Because so many commodities are priced in dollars, a rising dollar generally forced commodity exporters to offer their goods at lower prices so as not to place unreasonable demands on commodity importers. Since 2020 with that pattern reversed, the combined increase in the value of commodities and the dollar has applied huge pressure to importers of oil, gas and food.

This inversion of the commodity-dollar relationship poses a major challenge for the survival of the weaker members of the dollar system.

Was this change in the relationship in the dollar-commodity price nexus a coincidence or should we expect it to continue? A recent report by Boris Hofmann, Deniz Igan and Daniel Rees of the BIS suggests that it reflects structural changes in the US economy.

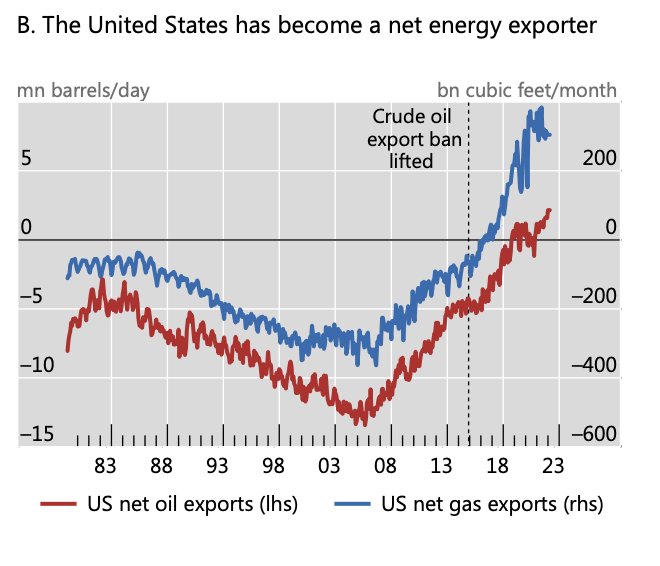

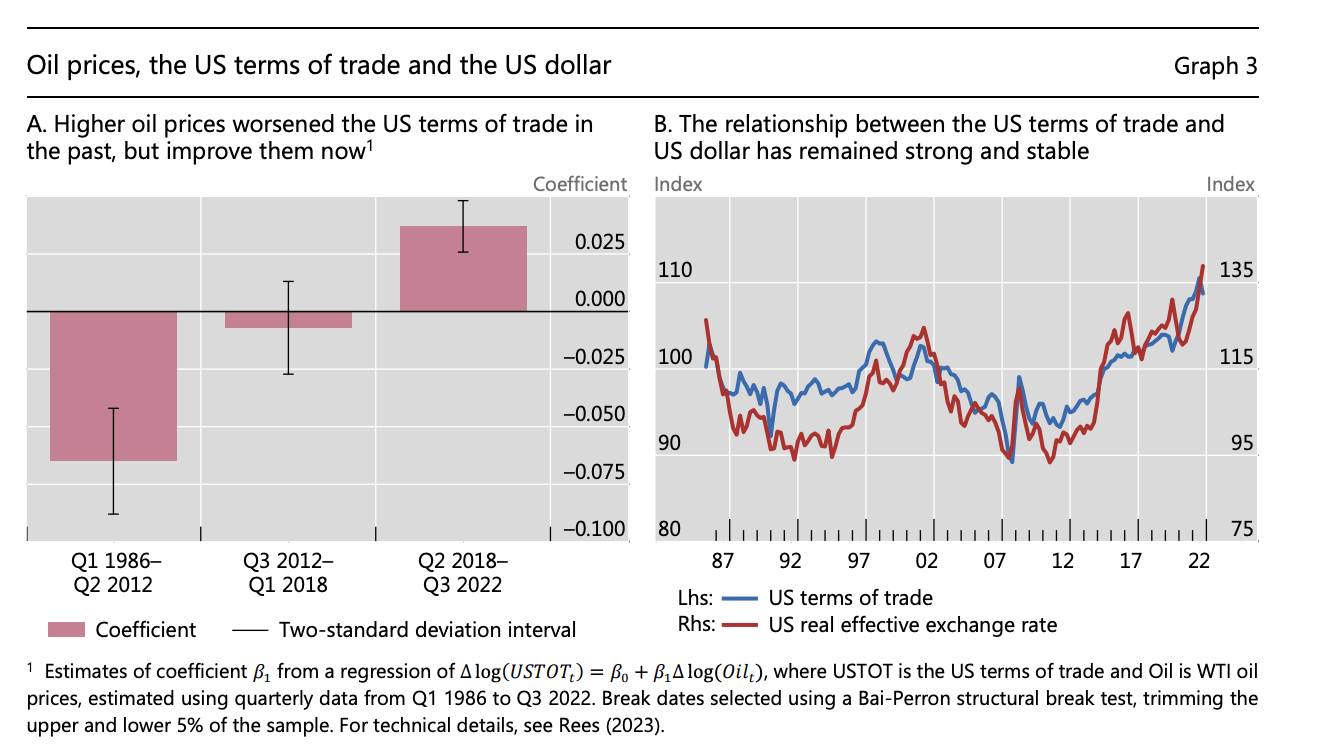

The crucial point is that in the last five years the the US balance in trade in energy has flipped. The US, which used to be a large net importer of oil and gas, has become a major net energy exporter.

This matters because an increase in the price of oil – the lead commodity of the world economy – now improves the terms of trade of the United States. And the terms of trade are strongly correlated with the strength of the dollar.

As the BIS team comments, whereas

“in the past higher energy prices were associated with worsening US terms of trade and a weaker dollar, today these patterns are reversed. A similar positive relationship between the terms of trade and the exchange rate is commonly found for commodity exporters, such as Australia and Canada, but not for commodity importers (see Cashin (2004), Rees (2023)). This suggests that – unless the United States becomes a major net energy importer once more – the combination of higher commodity prices and a stronger US dollar could be more common in the future than it was in the past.

The result of this change in the “commodity price-dollar nexus” is extremely toxic for global growth:

movements in the US dollar now compound the effect of commodity prices changes on the global economy. Commodity price rises tend to stoke inflation and choke off growth in commodity-importing economies, while dollar appreciation tends to do the same outside the United States, especially in emerging market economies. The stagflationary effects of higher commodity prices exert themselves in part through higher consumer prices, which squeeze household incomes, and rising production costs for firms, which dampen investment. The stagflationary effects of a stronger dollar come through its dominant role in global trade and finance.2 The recent confluence of such incidents has significantly increased the risk that weak growth will coincide with high inflation. Consistent with this, inflation surged worldwide while growth fell in in 2022 (Graph 4.A).

The stagflationary impact of the dollar-commodity nexus is compounded by the similar impact of a strong dollar by way of the “credit channel”. A strengthening dollar tightens global dollar-credit and tends to strangle global investment and trade finance. In a recent episode of Odd Lots, Hyun Song Shin explained how the two effects have combined in the current cycle.

***

What does it mean for the dollar system that the US is now a major energy exporter?

One of the constants in the global economy we have known since the 1970s has been the waxing and waning of the flow of petrodollars generated by US oil imports. As the BIS comments:

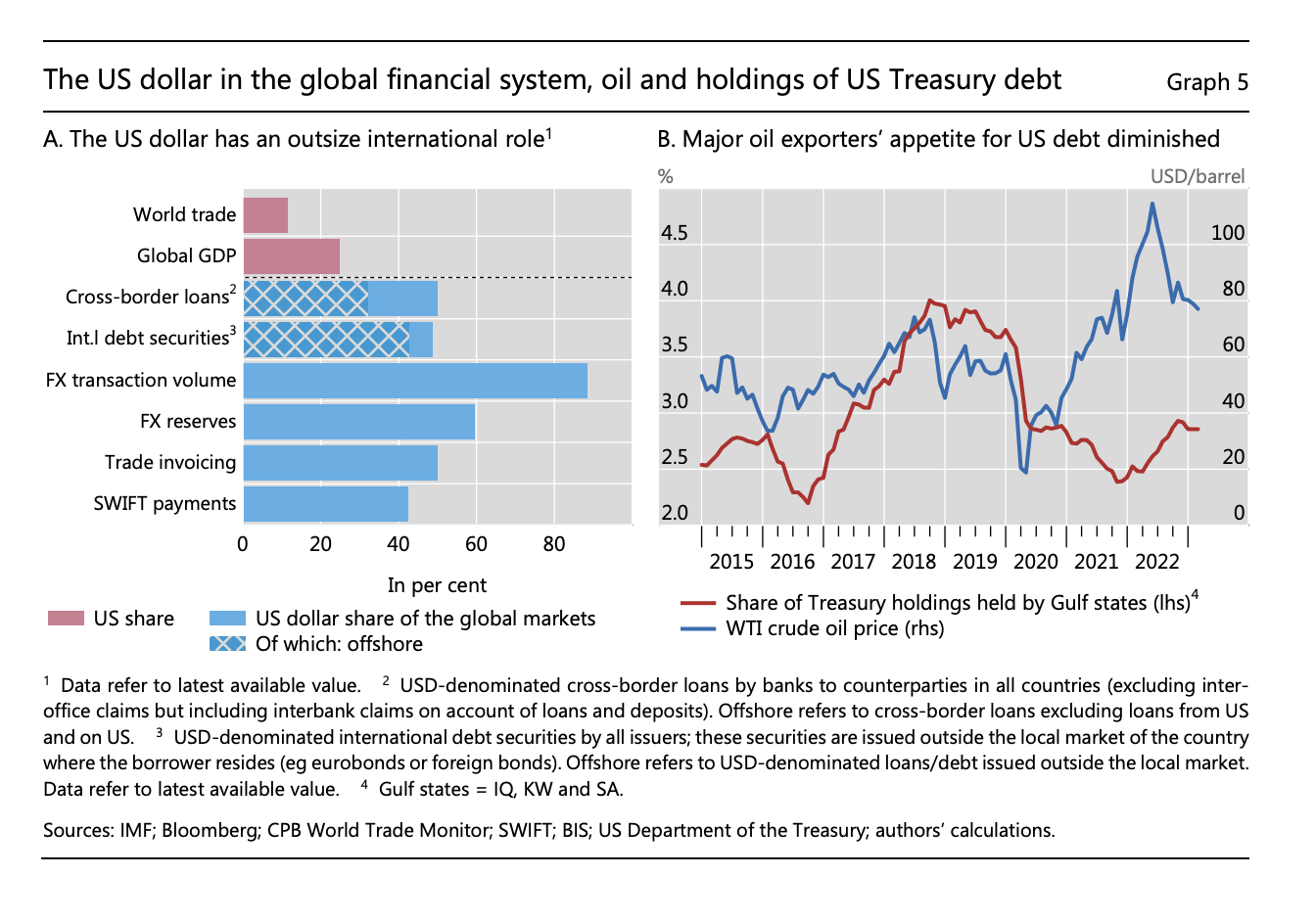

For decades, major oil exporters have priced their oil trades in US dollars. Often petrodollars have been recycled back into US Treasury debt and other US assets, reinforcing the dollar’s reserve currency status, as manifested in its dominant role in global trade and finance (Graph 5.A) and its outsize impact on global economic and financial conditions. Less US oil imports could mean fewer petrodollars flowing into the global financial system. This could reduce liquidity and affect currency choices in trade invoicing and reserve management.

This macrofinancial backdrop adds to the political and geopolitical pressures to move away from dollar invoicing of major commodities. As the BIS team comment:

Some commodity exporters may consider catering to the wishes of their new most important customers, as the stabilising impact of the dollar on their economies weakens. Commodity importers may welcome such a change if it shields their economies from the stagflationary effects of rising oil prices and dollar appreciation. Recent data lend some support to this notion. For instance, the major Gulf States have reduced their investments in US Treasury debt even as oil prices and, hence, oil export revenues have picked up (Graph 5.B), possibly indicating more non-dollar oil export invoicing. Moreover, the share of global trade invoiced in US dollars has declined from its peak in 2014 and the global share of foreign exchange reserves held in dollars has fallen to a three-decade low (Arslanalp et al (2022)).

As the BIS team sagely remark, the conversation about the future of the dollar has been on-going for decades and a shift in the dollar-commodity price correlation observed in the last two years is not going to decide it one way or another. But what this break does point to are are powerful range of pressures beyond geopolitics that affect, above all, the weakest members of the system. This may demand various practical adjustments including additional support from the multilaterial financial institutions. But above all it gives the lie to the idea that it is above all politics and geopolitics that are intruding into an otherwise well-balanced and well-defined system of global finance centered on the dollar. Those forces do, of course, impact global finance, but the dollar system that they are shaping is not in itself equal, balanced or unpolitical. Rather it is highly unequal, crisis-prone and constantly changing. It is by the interaction between macroeconomics, macrofinance and geoeconomics that the dollar system’s future will be decided.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you wil receive the full Top Links emails several times per week.

April 28, 2023

Chartbook #211 Bucking the buck? Debating the global dollar … again!

We are talking about the dollar again.

Debate is stimulated by the fact that the dominance of the dollar is out of of kilter with the increasing multipolarity of the world economy. We are in a period of high geopolitical tension and the US has chosen to weaponize America’s grip on the global financial system in a dramatic fashion.

Naturally, the structural imbalance and the use of financial sanctions triggers other players in the global system to seek ways to extricate themselves from the dollar system.

As Daniel McDowell shows in his important new book, Bucking the Buck, Russia had gone a long way to dedollarizing its financial balance sheet even before the current confrontation with the United States began.

Today Moscow is hatching deals with China to sidestep the American currency.

The Bangladeshi Finance Ministry has announced that it will be paying $318 million to a Russian nuclear power developer in Chinese yuan. As Bangladeshi sources told the Washington Post, “although the decision was made, the transaction is yet to be completed because payment details still need to be resolved. He declined to comment further, citing the diplomatic sensitivity of the issue.” As McDowell has noted on twitter, the Post reports that the deal will rely on the CIPS payments system. CIPS remains heavily reliant on SWIFT for messaging. Given SWIFT sanctions were cited (see above) as an impediment to using USD, this implies that some other messaging system is being used. Seems notable.

Crisis-ridden Argentina has negotiated the right to pay China in yuan for its imports.

Brazil’s new government has loudly proclaimed its desire to uncouple its trade with China from the dollar.

The Saudis and the Chinese are talking about invoicing oil in something other than dollars.

Data show a larger share of Chinese trade has recently been conducted in yuan. And the share of global reserves held as dollars is declining. There is talk of a “stealth dedollarization”.

***

Under the heading of “fin-fi” I’ve written in previous newsletters about the lure of the dedollarization narrative. As the counterpart to the increasingly multipolar world economy it seems only logical that the dominance of America’s national currency should diminish.

What is convincing about this vision is the fact that currency systems are woven deep into the fabric of the economy and the currency system in turn conditions patterns of trade and investment. A changing world economy would seem, necessarily, to need a new currency system to match. But what form will that take? Will it consist in the supercession of dominance dollar by the dominance of some other currency?

We should not look to history as a guide because we have little real experience to guide us. In the modern era there have been only two currency systems – sterling and dollar. The sterling system was ended by two massive world wars. The US-dollar system is, in many respects, quite different from the sterling-gold-City of London system that preceded it – stuff for a future post. Furthermore, since 1945 the dollar system, like the sterling system before it, has itself undergone several dramatic shifts – Bretton Woods, “free” float, the regime of global swap lines. To think of the “dollar system” as a rigid structure with clear limits, rules and boundaries set in Wall Street or Washington DC is misleading. It is far better thought of as a hierarchical and unequal but also open-ended network or assemblage which develops under the impulse of profit, capital accumulation and institutional initiatives from many different sources. Further evolution and modification, more often than not driven by crisis and crisis-fighting, is surely the most likely prospect. And that is what the data actually suggest is happening.

***

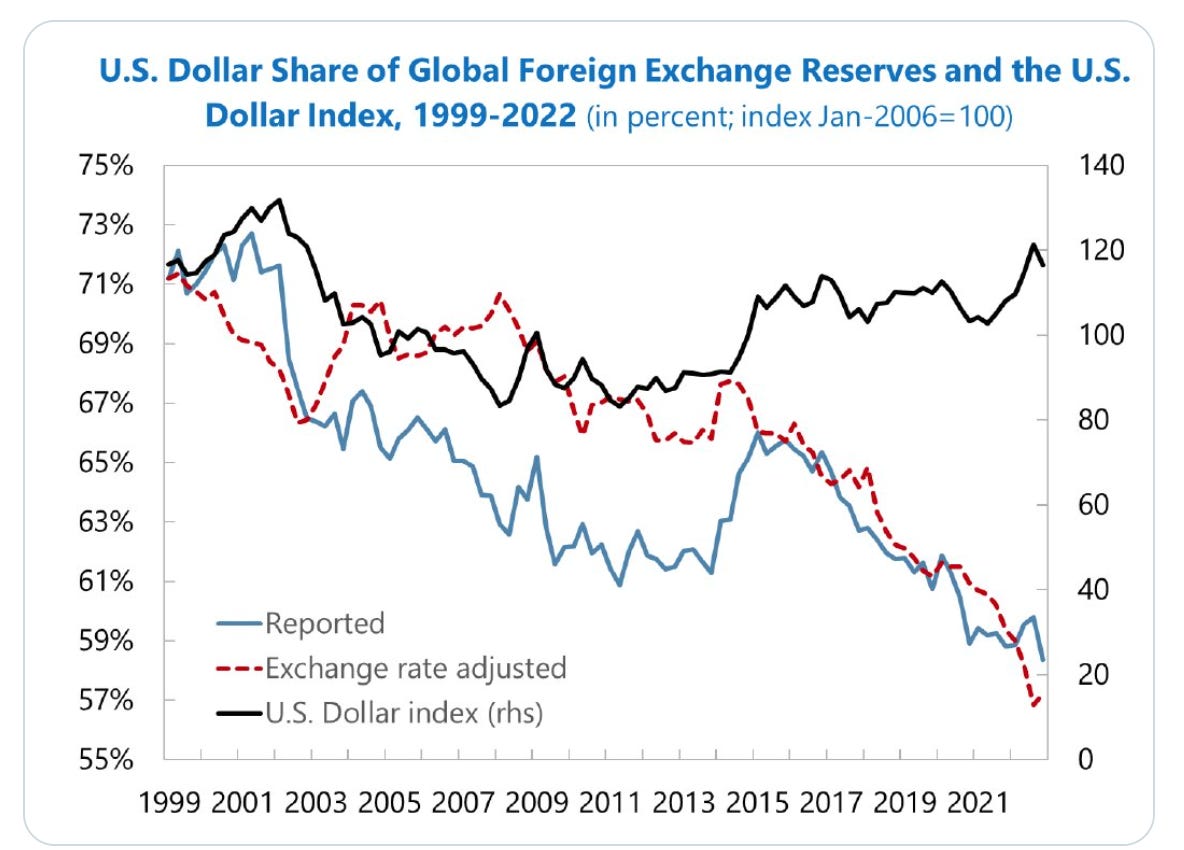

There is a decline in the share of reserves held as dollars. The absolute amount of this decline is sensitive to how we calculate the numbers, particularly the year we pick on which to base the value of the dollar. But the trend in the dollar share is down. What this means, however, depends on how we see the function of reserves in the system.

Since the emerging market financial crises of the 1990s, one of the most important modifications of the dollar system has been the accumulation of gigantic reserves by current account surplus countries. This provides a degree of insurance for states that fear that they might be hit by sudden stops and financial crises. It is a new regime that has seen the EM through both the 2008 and 2020 shock.

In the first phase of accumulation, most of those reserves were invested in US Treasuries. Why? Because those are the most liquid assets and thus most valuable in a crisis. But as reserves have built up, there have been imbalances in the demand and supply of dollar-denominated safe assets. And reserve managers have taken on new roles. As the funds they have to manage have ballooned and the memory of acute crises fades into the past, reserve managers have increasingly come to see themselves as portfolio-managers.

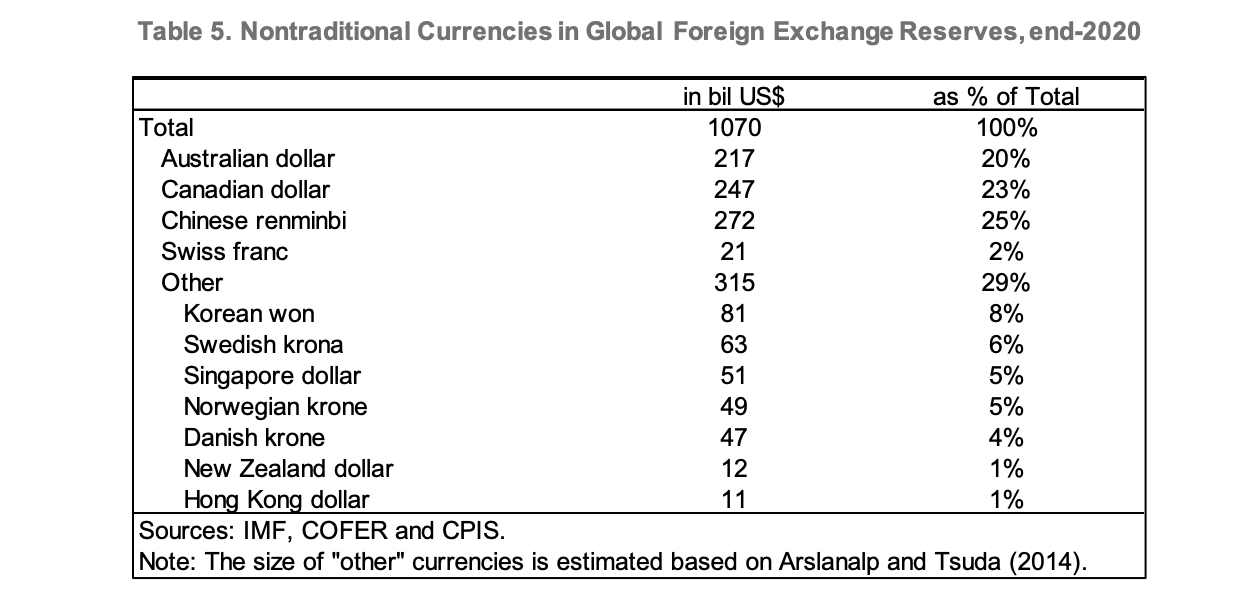

The job of portfolio managers is not to guard the national piggybank but to optimize the balance of risk and return. This entails diversification away from overcrowded US-dollar markets. And where do you put hundreds of billions of dollars worth of reserves, if not into dollars? The obvious pick are assets in other widely-traded advanced economy currencies. This is the trend observed by ; ; who track a rise in reserves held in “nontraditional currencies”.

Assets issued in those currencies offer, on occasion, a balance of risk and return that is marginally better than that of US dollars. But can this really be described as dedollarization? Surely not. The financial systems of all the countries on this list other than China – countries accounting for 75 percent of the total – are firmly anchored within the dollar system, a status indicated by the fact that their central banks are within the privileged circle of those to which the Fed extends dollar swap lines. So far, moves beyond the dollar system defined in these broader terms are of no great significance.

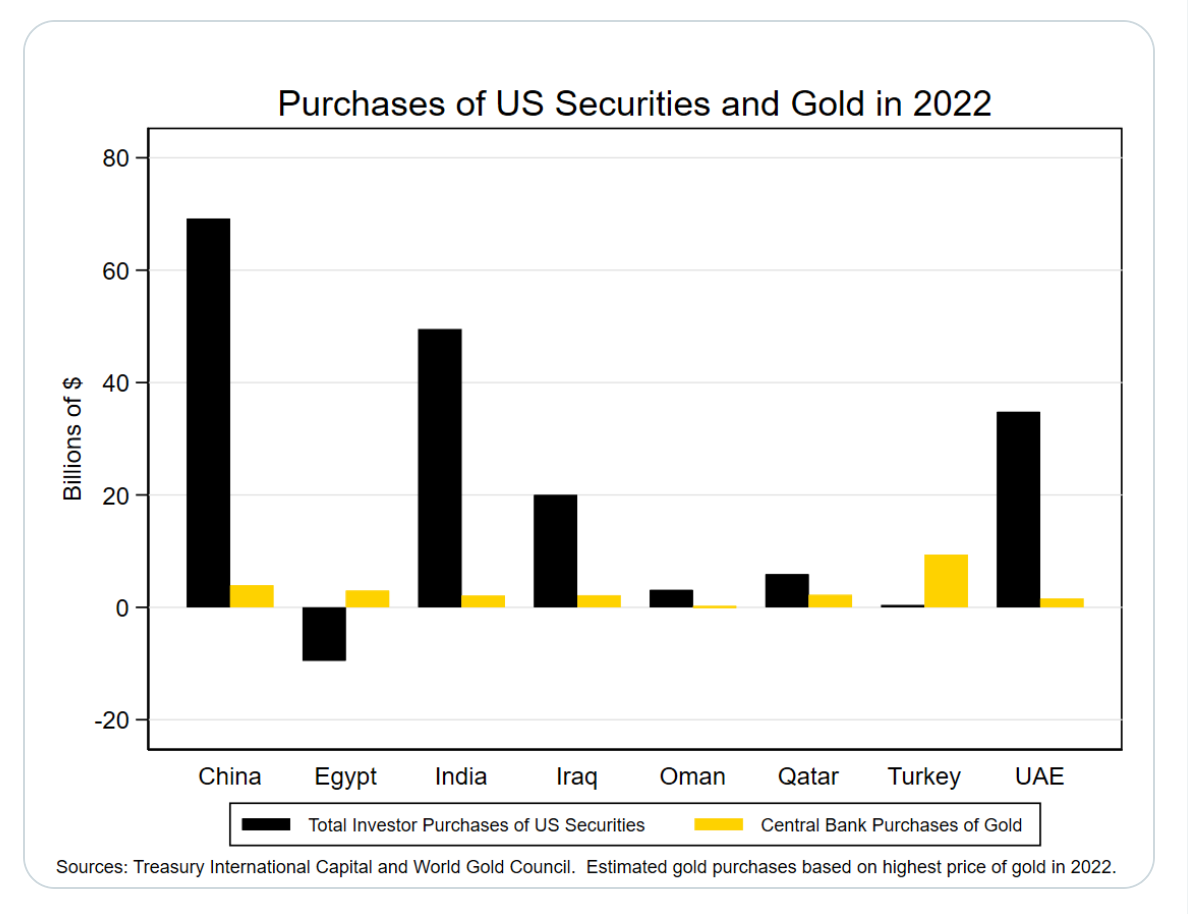

In a piece published in the FT earlier this year, Zoltan Poszar makes much of the fact that some central banks are buying gold. McDowell provides an excellent discussion of the role that gold has played in the dedollarization strategies of Russia and Turkey. But as far as the large central banks are concerned, gold purchases in 2022 were tiny compared to the ongoing accumulation of dollar assets.

Source: Colin Weiss, Twitter

As Colin Weiss points out, 3 of the largest sellers of FX reserves in 2022 were countries that participated in sanctions against Russia: Japan, Switzerland, South Korea. Amongst other sellers were an array of countries that had to sell dollars to resist the sharp depreciations against the US currency in 2022.

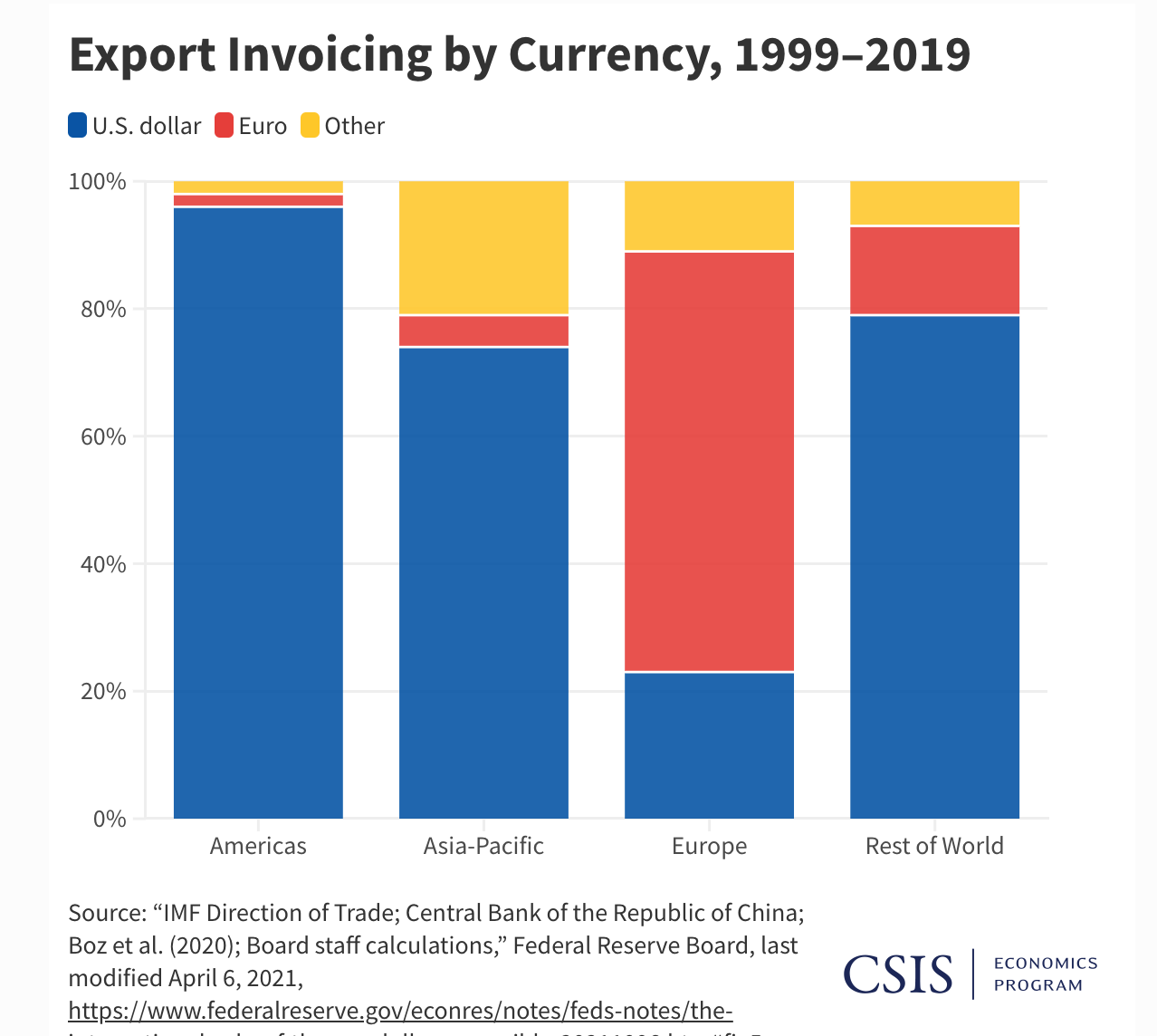

As far as trade is concerned there has been an increase in the share of China’s trade invoiced in yuan. But as Gerard DiPippo and Andrea Leonard Palazzi point out in a very useful CSIS post, this not a secular trend. Rather it is a partial return to levels of yuan-invoicing, which before 2015 were much higher.

Nor is it surprising that China’s trade should be in large part invoiced in its own currency. There is after all ample global demand for Chinese currency with which to buy Chinese goods. Europe conducts a far larger share of its trade in its own currency than does China and that does not constitute a threat to the dollar system.

Why should we be surprised if the Sino-centric Asia-Pacific economy increasingly invoices in yuan?

But that would look quite different from the bilateral deals we have seen in recent months. The deals done since 2022 have been motivated not by commercial but by explicitly political motives, largely centered on Russia’s ostracized position. They have been in large part bilateral agreements. They do not, therefore, suggest the emergence of an alternative yuan-based network of international finance and trade. The Russo-Bangladeshi agreement to transact in yuan is significant in this respect. But it is small scale and transparently politically motivated.

Shifting the trade in oil from dollars to yuan would be a more substantial shift. But it echoes half a century of similar suggestions none of which have so far produced a significant shift. And if the Chinese and Saudis actually followed through it would expose what is the underlying question which is, where the Gulf states would invest their petroyuan. Will the Saudis be willing to invest petroyuan in Chinese government debt in the face of capital account controls?

Were that to happen at scale, it would suggest. not just a modification but a retrenchment of the dollar’s. But, as Javier Blas points out on Bloomberg, the rise of the petroyuan is anyting but inevitable. Apart from anything else, the oil exporters must be concerned about how to contain demands from other countries. How would they react to demands for a petrorupee. Working within the existing status quo, however lopsided it may be, avoids having to pose the question of power and profit anew.

As Blas points out:

Ironically, the only new petrocurrency to emerge of late has been the dirham of the United Arab Emirates. India is using it to settle some oil transactions with Russia, bypassing US sanctions. But for the past 25 years, the dirham has been pegged to the US dollar — another indication that the petrodollar remains the only petrocurrency that really matters.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you wil receive the full Top Links emails several times per week.

Ones & Tooze: Can the US solve the China dilemma?

The Biden administration has a tough dilemma to work out: how to push back against China’s geopolitical ambitions while also maintaining vital economic ties. In this episode Adam and Cameron explore what levers are available to the US and its EU partners to still exert influence and why in the end the existing world powers may need to completely rethink China’s role in global institutions.

And a quick note to our listeners in Berlin… Adam and Cameron will be taping a live episode of Ones and Tooze on May 25 at Prachtwerk Berlin. Click on the link below for tickets. Tickets are almost all sold out so don’t wait!

https://www.podfestberlin.com/event-details/ones-and-tooze-live

Find more episodes and subscribe at Foreign Policy.

April 25, 2023

Chartbook #210 – The Partisans descending from their graves – Pasolini’s “Victory”, April 25th 1964

April 25th is the commemorative day for the final liberation of Italy from fascist rule. It is the occasion for memorials of various stripes. On the left it is the Partisans who stand at the heart of collective memory.

In Italy as elsewhere in Europe, the Communist and Socialist parties were the main forces in the resistance. Their memorial day carried a powerful memory of the sacrifices made by those who fought, moment of liberation and the possibilities that seemed open then. But, as the years passed, European society was marked not so much simply by Cold War restoration as by a whirlwind of neocapitalist transformation. With spectacular economic growth, urbanization, motorization and the birth of consumer society, a social and economic revolution had arrived. But, not the one that was imagined in 1945. The commemoration of the liberation and the radical and revolutionary tradition thus took on an increasingly ambiguous and bittersweet aspect.

No one reflected on this transition more urgently than the polymath, poet, filmmaker, activist, critic Pier Paolo Pasolini.

On 25 April 1945 Pasolini was 23. He had been, as he described himself, a partisan without arms. His brother who had joined the liberal-socialist partisans associated with the Party of Action, was killed in an ambush by Communist-aligned partisans. Piero Paolo Pasolini himself went on to join the Communist Party but was expelled. The party was scandalized by his open homosexuality and left Pasolini to face relentless legal persecution.

The collection of poems that earned Pasolini fame in 1957 was, not for nothing, entitled, Gramsci’s Ashes.

For Gramsci’s Ashes and much more, I highly recommend The Selected Poetry of Pier Paolo Pasolini with a truly marvelous introduction by Stephen Sartarelli which merits a long essay all of its own. As he makes clear, Pasolini sought to weave the very forces of history and history’s disintegration into his poetry. Pasolini’s struggle was to “remain “equal to a present reality [attualità] that one does not possess ideologically.”” A struggle made all the more difficult by the fact that history itself was disintegrating and taking on new forms in the face of the onslaught of neocapitalism.

In the poem Victory, written for April 25 1964, Pasolini reflects in a haunting fashion on the appearance of the ghosts of the Partisans amongst the transformed world of “postwar” Italy.

The poem is available in translation, online at the ZNetwork website.

VICTORYby Pier Paolo Pasolinitranslated by Norman MacAfee with Luciano MartinengoWhere are the weapons?I have only those of my reasonand in my violence there is no placefor even the trace of an act that is notintellectual. Is it laughableif, suggested by my dream on thisgray morning, which the dead can seeand other dead too will see but for usis just another morning,I scream words of struggle?Who knows what will become of meat noon, but the old poet is “ab joy”who speaks like a lark or a starling ora young man longing to die.Where are the weapons? The old dayswill not return, I know; the redAprils of youth are gone.Only a dream, of joy, can opena season of armed pain.I who was an unarmed Partisan,mystical, beardless, nameless,now I sense in life the horriblyperfumed seed of the Resistance.In the morning the leaves are stillas they once were on the Tagliamentoand Livenza — it is not a storm comingor the night falling. It is the absenceof life, contemplating itself,distanced from itself, intent onunderstanding those terrible yet sereneforces that still fill it — aroma of April!an armed youth for each blade of grass,each a volunteer longing to die.. . . . . . . . .Good. I wake up and — for the first timein my life I want to take up arms.Absurd to say it in poetry— and to four friends from Rome, two from Parmawho will understand me in this nostalgiaideally translated from the German, in this archeologicalcalm, which contemplates a sunny, depopulatedItaly, home of barbaric Partisans who descendthe Alps and Apennines, down the ancient roads. . .My fury comes only at the dawn.At noon I will be with my countrymenat work, at meals, at reality, which raisesthe flag, white today, of General Destinies.And you, communists, my comrades/noncomrades,shadows of comrades, estranged first cousinslost in the present as well as the distant,unimagined days of the future, you, namelessfathers who have heard calls thatI thought were like mine, whichburn now like fires abandonedon cold plains, along sleepingrivers, on bomb-quarried mountains. . . .. . . . . . . . .I take upon myself all the blame (my oldvocation, unconfessed, easy work)for our desperate weakness,because of which millions of us,all with a life in common, could notpersist to the end. It is over,let us sing along, tralala: They are falling,fewer and fewer, the last leaves ofthe War and the martyred victory,destroyed little by little by whatwould become reality,not only dear Reaction but also the birth ofbeautiful social-democracy, tralala.I take (with pleasure) on myself the guiltfor having left everything as it was:for the defeat, for the distrust, for the dirtyhopes of the Bitter Years, tralla.And I will take upon myself the tormentingpain of the darkest nostalgia,which summons up regretted thingswith such truth as to almostresurrect them or reconstruct the shatteredconditions that made them necessary (trallallallalla). . . .. . . . . . . . .Where have the weapons gone, peacefulproductive Italy, you who have no importance in the world?In this servile tranquility, which justifiesyesterday’s boom, today’s bust — from the sublimeto the ridiculous and in the most perfect solitude,j’accuse! Not, calm down, the Government or the Latifundiaor the Monopolies — but rather their high priests,Italy’s intellectuals, all of them,even those who rightly call themselvesmy good friends. These must have been the worstyears of their lives: for having accepteda reality that did not exist. The resultof this conniving, of this embezzling of ideals,is that the real reality now has no poets.(I? I am desiccated, obsolete.)Now that Togliatti has exited amidthe echoes from the last bloody strikes,old, in the company of the prophets, who, alas, were right — I dream of weaponshidden in the mud, the elegiac mudwhere children play and old fathers toil —while from the gravestones melancholy falls,the lists of names crack,the doors of the tombs explode,and the young corpses in the overcoatsthey wore in those years, the loose-fittingtrousers, the military cap on their Partisan’shair, descend, along the wallswhere the markets stand, down the pathsthat join the town’s vegetable gardensto the hillsides. They descend from their graves, young menwhose eyes hold something other than love:a secret madness, of men who fightas though called by a destiny different from their own.With that secret that is no longer a secret,they descend, silent, in the dawning sun,and, though so close to death, theirs is the happy treadof those who will journey far in the world.But they are the inhabitants of the mountains, of the wildshores of the Po, of the remotest placeson the coldest plains. What are they doing here?They have come back, and no one can stop them. They do not hidetheir weapons, which they hold without grief or joy,and no one looks at them, as though blinded by shameat that obscene flashing of guns, at that tread of vultureswhich descend to their obscure duty in the sunlight.. . . . . . . . .Who has the courage to tell themthat the ideal secretly burning in their eyesis finished, belongs to another time, that the childrenof their brothers have not fought for years,and that a cruelly new history has producedother ideals, quietly corrupting them?. . .Rough like poor barbarians, they will touchthe new things that in these two decades humancruelty has procured, things incapable of movingthose who seek justice. . . .But let us celebrate, let us open the bottlesof the good wine of the Cooperative. . . .To always new victories, and new Bastilles!Rafosco, Bacò. . . . Long life!To your health, old friend! Strength, comrade!And best wishes to the beautiful party!From beyond the vineyards, from beyond the farm pondscomes the sun: from the empty graves,from the white gravestones, from that distant time.But now that they are here, violent, absurd,with the strange voices of emigrants,hanged from lampposts, strangled by garrotes,who will lead them in the new struggle?Togliatti himself is finally old,as he wanted to be all his life,and he holds alarmed in his breast,like a pope, all the love we have for him,though stunted by epic affection,loyalty that accepts even the most inhumanfruit of a scorched lucidity, tenacious as a scabie.“All politics is Realpolitik,” warringsoul, with your delicate anger!You do not recognize a soul other than this onewhich has all the prose of the clever man,of the revolutionary devoted to the honestcommon man (even the complicitywith the assassins of the Bitter Years graftedonto protector classicism, which makesthe communist respectable): you do not recognize the heartthat becomes slave to its enemy, and goeswhere the enemy goes, led by a historythat is the history of both, and makes them, deep down,perversely, brothers; you do not recognize the fearsof a consciousness that, by struggling with the world,shares the rules of the struggle over the centuries,as through a pessimism into which hopesdrown to become more virile. Joyouswith a joy that knows no hidden agenda,this army — blind in the blindsunlight — of dead young men comesand waits. If their father, their leader, absorbedin a mysterious debate with Power and boundby its dialectics, which history renews ceaselessly —if he abandons them,in the white mountains, on the serene plains,little by little in the barbaric breastsof the sons, hate becomes love of hate,burning only in them, the few, the chosen.Ah, Desperation that knows no laws!Ah, Anarchy, free loveof Holiness, with your valiant songs!. . . . . . . . .I take also upon myself the guilt for tryingbetraying, for struggling surrendering,for accepting the good as the lesser evil,symmetrical antinomies that I holdin my fist like old habits. . . .All the problems of man, with their awful statementsof ambiguity (the knot of solitudesof the ego that feels itself dyingand does not want to come before God naked):all this I take upon myself, so that I can understand,from the inside, the fruit of this ambiguity:a beloved man, in this uncalculatedApril, from whom a thousand youthsfallen from the world beyond await, trusting, a signthat has the force of a faith without pity,to consecrate their humble rage.Pining away within Nenni is the uncertaintywith which he re-entered the game, and the skillfulcoherence, the accepted greatness,with which he renounced epic affection,though his soul could claim titleto it: and, exiting a Brechtian stageinto the shadows of the backstage,where he learns new words for reality, the uncertainhero breaks at great cost to himself the chainthat bound him, like an old idol, to the people,giving a new grief to his old age.The young Cervis, my brother Guido,the young men of Reggio killed in 1960,with their chaste and strong and faithfuleyes, source of the holy light,look to him, and await his old words.But, a hero by now divided, he lacksby now a voice that touches the heart:he appeals to the reason that is not reason,to the sad sister of reason, which wantsto understand the reality within reality, with a passionthat refuses any extremism, any temerity.What to say to them? That reality has a new tension,which is what it is, and by now one hasno other course than to accept it. . . .That the revolution becomes a desertif it is always without victory. . . that it may not betoo late for those who want to win, but not with the violenceof the old, desperate weapons. . . .That one must sacrifice coherenceto the incoherence of life, attempt a creatordialogue, even if that goes against our conscience.That the reality of even this small, stingyState is greater than us, is always an awesome thing:and one must be part of it, however bitter that is. . . .But how do you expect them to be reasonable,this band of anxious men who left — asthe songs say — home, bride,life itself, specifically in the name of Reason?. . . . . . . . .But there may be a part of Nenni’s soul that wantsto say to these comrades — come from the world beyond,in military clothes, with holes in the solesof their bourgeois shoes, and their youthinnocently thirsting for blood —to shout: “Where are the weapons? Come on, let’sgo, get them, in the haystacks, in the earth,don’t you see that nothing has changed?Those who were weeping still weep.Those of you who have pure and innocent hearts,go and speak in the middle of the slums,in the housing projects of the poor,who behind their walls and their alleyshide the shameful plague, the passivity of thosewho know they are cut off from the days of the future.Those of you who have a heartdevoted to accursed lucidity,go into the factories and schoolsto remind the people that nothing in these years haschanged the quality of knowing, eternal pretext,sweet and useless form of Power, never of truth.Those of you who obey an honestold imperative of religiongo among the children who grow with hearts empty of real passion,to remind them that the new evilis still and always the division of the world. Finally,those of you to whom a sad accident of birthin families without hope gave the thick shoulders, the curlyhair of the criminal, dark cheekbones, eyes without pity —go, to start with, to the Crespis, to the Agnellis,to the Vallettas, to the potentates of the companiesthat brought Europe to the shores of the Po:and for each of them comes the hour that has noequal to what they have and what they hate.Those who have stolen from the common goodprecious capital and whom no law canpunish, well, then, go and tie them up with the ropeof massacres. At the end of the Piazzale Loretothere are still, repainted, a fewgas pumps, red in the quietsunlight of the springtime that returnswith its destiny: It is time to make it again a burial ground!”. . . . . . . . .They are leaving . . . Help! They are turning away,their backs beneath the heroic coatsof beggars and deserters. . . . How serene arethe mountains they return to, so lightlythe submachine guns tap their hips, to the treadof the sun setting on the intactforms of life, which has become what it was beforeto its very depths. Help, they are going away! — back to theirsilent worlds in Marzabotto or Via Tasso. . . .With the broken head, our head, humbletreasure of the family, big head of the second-born,my brother resumes his bloody sleep, alone among the dried leaves, in the sereneretreats of a wood in the pre-Alps, lost inthe golden peace of an interminable Sunday. . . .. . . . . . . . .And yet, this is a day of victory.1964Translation copyright © 1982, 2005 by Norman MacAfeeCopyright © 1964 by Aldo Garzanti EditoreIf you would like to read Victory in print along with other fascinating poems and essays I recommend In Danger. A Pasolini Anthology by Jack Hirschman published by Citylights.

Pasolini was killed in 1975 in mysterious circumstances. For those interested, this documentary is fabulous.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters click below. As a token of appreciation you wil receive the full Top Links emails several times per week.

April 24, 2023

America Has Dictated Its Economic Peace Terms to China

By refusing negotiation over China’s rise, the United States might be making conflict inevitable.

How far will mounting tension with China be translated into the economic policy of the United States? After a rash of sanctions and overtly discriminatory legislation, with action on U.S. investment in China pending, and with talk of war increasingly commonplace in the United States, the Biden administration knows that it needs to clarify its economic relations with the country that is the largest U.S. trading partner outside North America.

Read the full article at Foreign Policy

Adam Tooze's Blog

- Adam Tooze's profile

- 767 followers

{kind=link}