Adam Tooze's Blog, page 5

April 4, 2023

Chartbook 208: Global bond markets on the rack – aka Finance & the Polycrisis #11 (sic)

The macrofinancial switchback of COVID-inflation-interest rate hikes has put the global market for fixed-income securities, valued at c $130 trillion, on the rack. The spring of 2023 has seen historically exceptional turbulence, and a sense of foreboding, as other shocks seem to lie ahead. The weakest borrowers have been cut off and some have slid into crisis. As ever, the authorities, above all in the US, have been there to provide a measure of derisking to exposed banks and shadow banks in the core of the system. But what does that mean? Daniela Gabor and I have been going back and forth in recent days on how to characterize this situation.

Are we in a new macrofinancial regime? Perhaps not @DanielaGabor but how about a new macrofinancial conjuncture? https://t.co/XGdetJ4ek3 pic.twitter.com/E1GebVhCSh

— Adam Tooze (@adam_tooze) April 1, 2023

To make a very complex argument simple, I tend to think that we are in a period of considerable flux. By contrast, Daniele Gabor defends the view that in its core functions the derisking state has if anything been confirmed by recent events. I’ll come back to some of the broader interpretative issues in a future post.

***

In the mean time, the exchanges on twitter have brought to mind that last fall I started a series of Chartbook posts called “Finance & the Polycrisis” that were intended to track the swing in financial markets, particularly bonds and real estate, under the impact of the diverse shocks we have been experiencing since 2020.

The series started with 6 posts.

#1 Nov 12 Finance and the polycrisis (1): What bends? What breaks? What implodes?

#2 Nov 13 The global housing downturn

#3 Nov 15 US Treasuries – how fragile is the world’s most important market?

#4 Nov 23 Fed effects & European corporate bond market.

#5 Dec 12 The hunt for the next market fracture.

#6 Dec 19 Africa’s debt crisis

Then, over Christmas and New Year I lost the thread. Christmas trees, inflation, globalization, Ukraine, cocoa occupied my attention. I feel bad that the broader themes of the series dropped out of my mind.

The last real overview was the Jan 3 edition of the Ones and Tooze podcast where Cam and I discussed a range of global financial questions.

Then, in March, financial instability roared back. Chartbook #200 should by rights have been titled Finance and the Polycrisis #7. That was on March 11 Something broke! The Silicon Valley Bank Failure

In that spirit I am rebadging the following posts as part of the series.

#8 March 14 Venture dominance?

#9 March 19 Banking crises, states of exception & the disappointment of sovereignty

And most recently to

#10 April 1 The trillion-dollar rebalancing: A new macrofinancial conjuncture?

Today’s post is #11 in the Finance & the Polycrisis series.

***

Revisiting the series is useful not just as a housekeeping exercise. It brings to mind two of the reasons why I emphasize the novelty of the current situation over the argument for continuity made by Daniela Gabor in our exchange.

The polycrisis we are living in – for me encapsulated in the pandemic-Trump-China-Russia-inflation-climate conjuncture – is a situation of escalating complexity, novelty and radicalism. We have been in the midst of the escalation for a while. One can trace both our current macrofinancial regime and our awareness of the polycrisis back to the 1970s. Indeed, the arms length, depoliticized mode of governance embodied in central-bank-derisked global finance organized around bond markets, was attractive in part because it promised to reduce pressure on politics and states in the face of multiple challenges. But by the same token it is less a “regime” or a particular “form of state” than a constantly evolving series of institutional innovations and improvisations that are subject to both exogenous and endogenous shocks. We are currently in a “hot phase”, which demands not the self-confident operation of familiar mechanisms, but scrambling improvisation and a dramatic readjustment of the horizon of expectations that organize and gives the appearance of coherence to those improvisations.If you follow market discourse closely, which is the aim of the Chartbook series, the overwhelming impression you come away with is not one of a tight knit group of experts who know what they are doing. But rather the contrary. Practically everywhere you look, you see people who are as knowledgeable as it gets scratching their heads, uncertain not just about what happens next, but about what happened yesterday and how some of the basic mechanisms we take for granted actually work.Resuming this series on Chartbook I want to emphasize both the first aspect (1) Polycrisis and (2) the collective puzzlement of people at the heart of global finance, who you might assume really understood what was happening.

Three examples from the coverage of the last week.

***

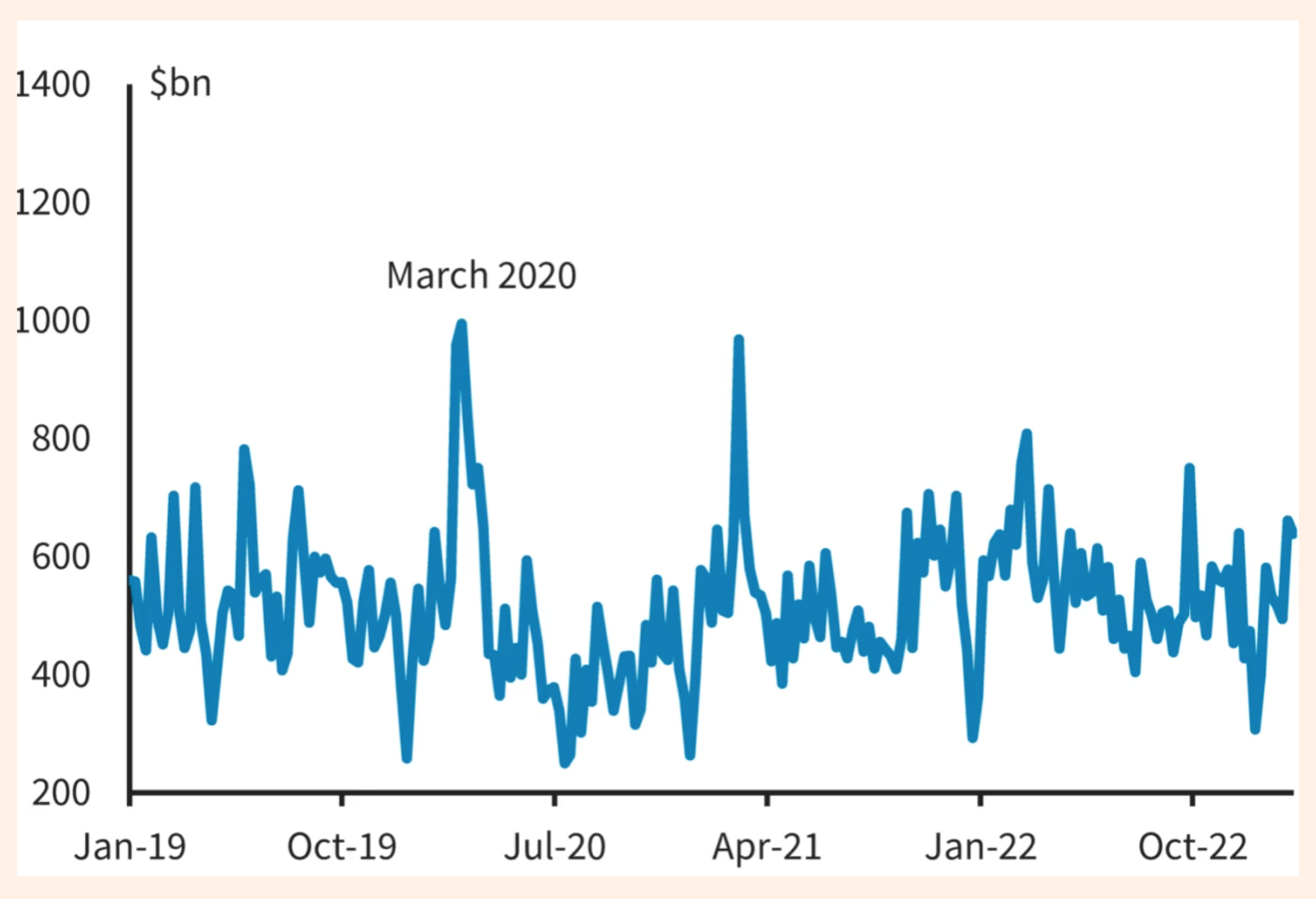

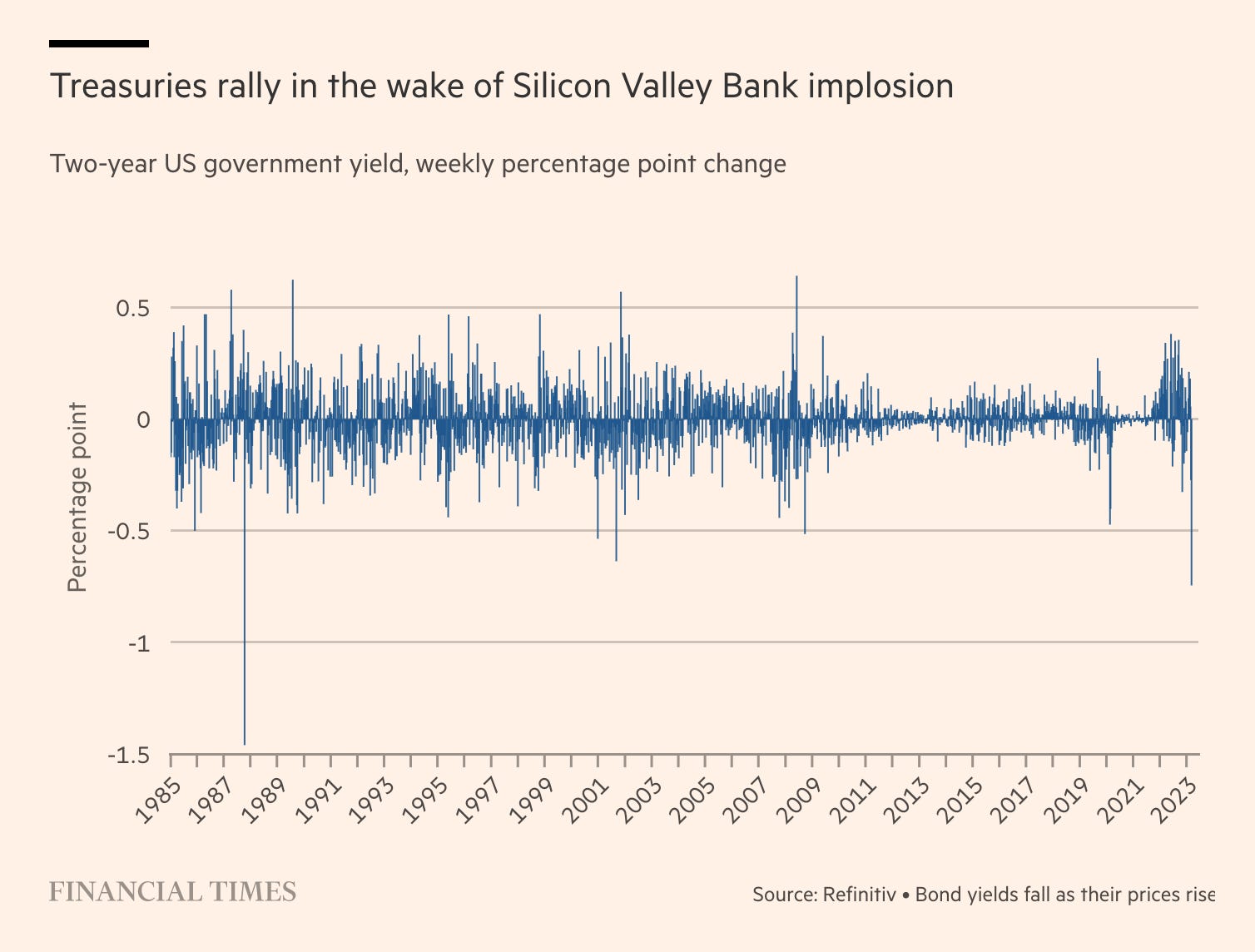

Example 1: A note by Robin Wigglesworth in Alphaville of the FT puzzling, by way of some research by Barclays, over quite how chaotic things were in the US Treasury market in March.

As the screams of agony from macro hedge funds and CTAs have indicated, this month has been, well, mental for the Treasury market. It’s incredible what a small sudden banking crisis can do isn’t it? First, some back-story: A weird anomaly about the US bond market is that Treasuries — arguably the single most important cornerstone of the global financial system — have long been one of the most opaque areas. While dealers have long reported all municipal, corporate or agency bond trades within five minutes to the Financial Industry Regulatory Authority — which collects then in “Trace”, or the Trade Reporting and Compliance Engine, and disseminates them publicly — Treasuries were long exempt. However, after a wild 2014 “flash rally” in Treasuries painfully exposed how little even regulators see in that market, US government debt has been slowly been forced into Trace. And in a bit of luck, Trace switched from weekly to daily Treasury trading reporting on Feb 13 — just in time for this month’s banking crisis. Barclays has pored through the data, and it’s wild. Daily nominal Treasury volumes spiked to as high as $1.2trn on March 13 — the Monday after Silicon Valley Bank collapsed — and daily volumes have averaged as high as $1tn. To put this in context, that is an even greater spasm of trading than what we saw at the peak of the Covid-triggered market panic in March 2020.

So that is remarkable a. because it happened and b. because this is apparently the first time we could actually know that it did, at least in such detail. But what does it mean?

There has been much ink — real and digital — spilled on concerns over the liquidity of the Treasury market in recent years, some of which on Alphaville. But it seems that despite a trading frenzy that surpassed that of March 2020, bid-ask spreads didn’t balloon nearly as violently this time. …. Does this mean that the Treasury market is not nearly as decrepit as some people have been saying? Probably. But the data — especially those gradually increasing bid-ask spreads even for ultra-liquid on-the-run Treasuries — does show why more work is needed to reinforce the world’s most important financial market.

So, maybe the US Treasury market – the foundation of the global financial system – is less broken than many of us fear. Or maybe not. Of course, we do know from 2020 what happens if things go wrong. The Fed steps in. This is a problem with an obvious solution. But that in turn leaves a legacy in the giant inflated balance sheet.

You can see, perhaps, why I prefer to avoid talking about “regimes” or a “derisiking state”, terms which seem to imply a degree of institutional robustness that reflect what you might call a substantivist conception of power, rather than something more fluid, quicksilver (now you see it and now you don’t) and improvised.

To avoid misunderstanding this is not a “historians” argument for particularity against a social scientists preference for concepts. What is at stake is a conceptual not a disciplinary issue. The question is how we think about knowledge and power in modern history, or modern history and power/knowledge. It is a point of difference which needs much further and deeper exploration in future posts.

***

Example 2: The on-going puzzlement and concern about what happens next in Japan.

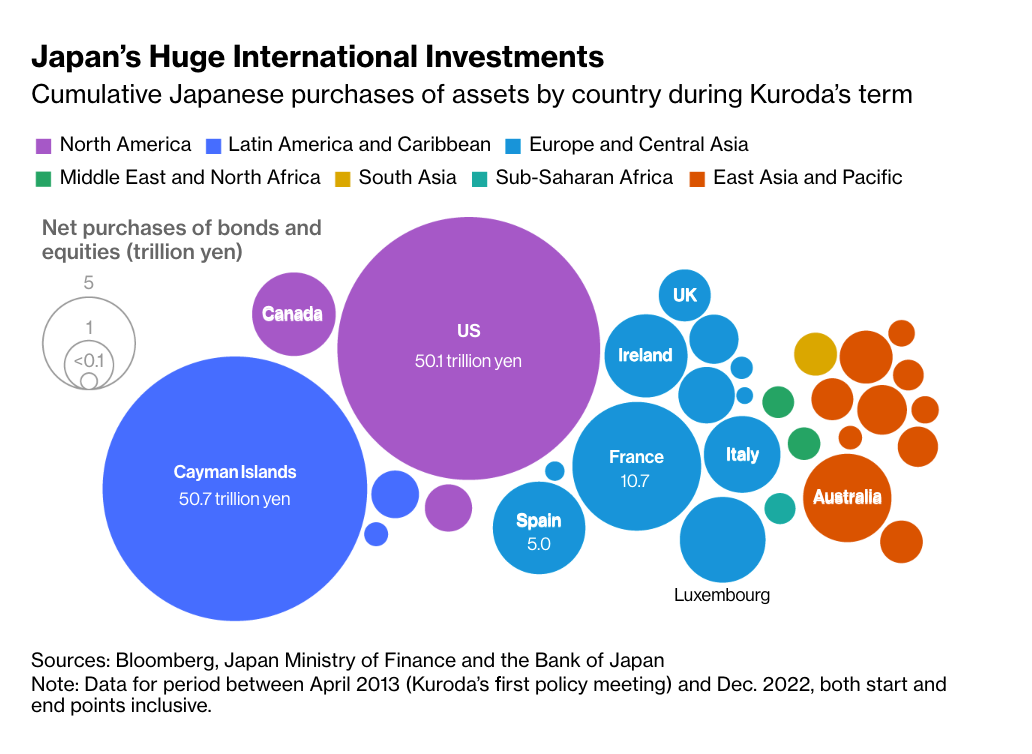

At the beginning of the month the leadership of the Bank of Japan changed hands. Haruhiko Kuroda – the godfather of the biggest bond buying scheme in history – retired to be replaced by Kazuo Ueda. For the occasion Bloomberg ran an excellent round up on the stakes involved in Japan’s monetary policy. Again the headline is striking: A $3 Trillion Threat to Global Financial Markets Looms in Japan

the new governor Ueda … may have little choice but to end the world’s boldest easy-money experiment just as rising interest rates elsewhere are already jolting the international banking sector and threatening financial stability. The stakes are enormous: Japanese investors are the biggest foreign holders of US government bonds and own everything from Brazilian debt to European power stations to bundles of risky loans stateside. An increase in Japan’s borrowing costs threatens to amplify the swings in global bond markets, which are being rocked by the Federal Reserve’s year-long campaign to combat inflation and the new danger of a credit crunch. Against this backdrop, tighter monetary policy by the BOJ is likely to intensify scrutiny of its country’s lenders in the wake of recent bank turmoil in the US and Europe. A change in policy in Japan is “an additional force that is not being appreciated” and “all G-3 economies in one way or the other will be reducing their balance sheets and tightening policy” when it happens, said Jean Boivin, head of the BlackRock Investment Institute and former Deputy Governor of the Bank of Canada. “When you control a price and loosen the grip, it can be challenging and messy. We think it’s a big deal what happens next.” The flow reversal is already underway. Japanese investors sold a record amount of overseas debt last year as local yields rose on speculation that the BOJ would normalize policy.

The BOJ’s bond-buying program was a key global anchor both of lower interest rates and the assumption that they would stay that way for the foreseeable future.

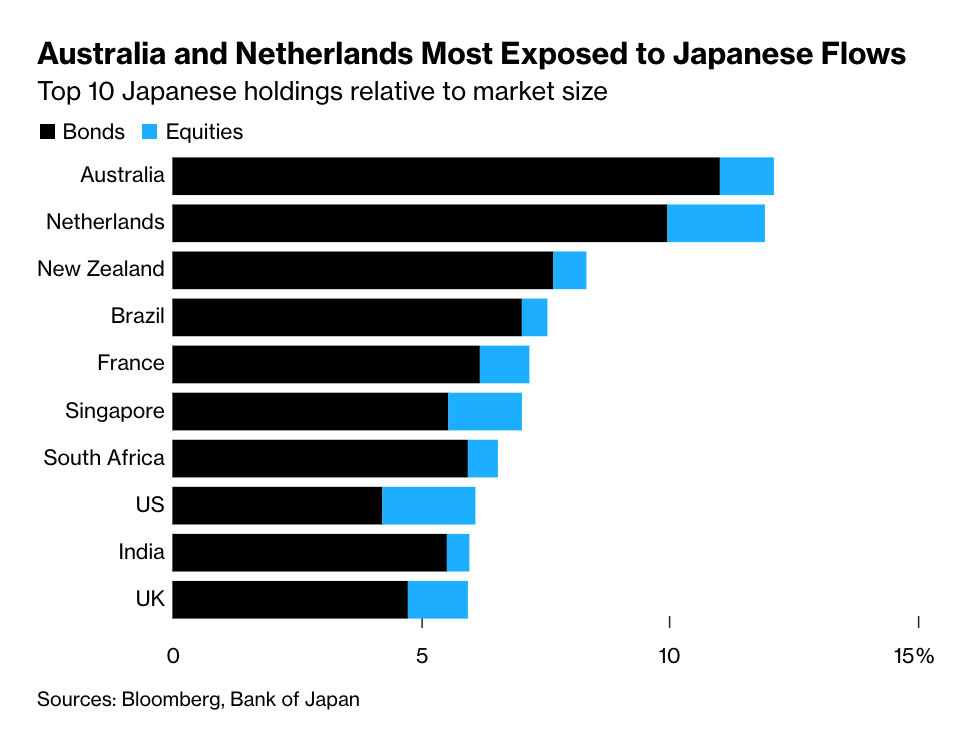

The BOJ has bought 465 trillion yen ($3.55 trillion) of Japanese government bonds since Kuroda implemented quantitative easing a decade ago, according to central bank data, depressing yields and fueling unprecedented distortions in the sovereign debt market. As a result, local funds sold 206 trillion yen of the securities during the period to seek better returns elsewhere. The shift was so seismic that Japanese investors became the biggest holders of Treasuries outside the US as well as owners of about 10% of Australian debt and Dutch bonds. They also own 8% of New Zealand’s securities and 7% of Brazil’s debt, calculations by Bloomberg show. The reach extends to stocks, with Japanese investors having splashed out 54.1 trillion yen on global shares since April 2013. Their holdings of equities are equivalent to between 1% and 2% of the stock markets in the US, Netherlands, Singapore and the UK. Japan’s ultra-low rates were a big reason the yen tumbled to a 32-year low last year, and it has been a top option for income-seeking carry traders to fund purchases of currencies ranging from Brazil’s real to the Indonesian rupiah.

Japanese investors have been burned by the losses suffered by bond investors worldwide. The anticipated turn in BoJ policy adds to the appeal of bringing money home. But when and how will the BoJ initiate its shift in stance? We simply do not know.

As the Bloomberg piece concedes:

To be sure, few are prepared to go all out in betting Ueda will rock the boat once he gets into office. A recent Bloomberg survey showed 41% of BOJ watchers see a tightening step taking place in June, up from 26% in February, while former Japan Vice Finance Minister Eisuke Sakakibara said the BOJ may raise rates by October. A summary of opinions from the BOJ’s March 9-10 meeting showed the central bank remains cautious about executing a policy pivot before achieving its inflation target. And that was even after Japan’s inflation accelerated beyond 4% to set a fresh four-decade high.

The next central bank meeting, Ueda’s first, is scheduled to take place April 27-28.

How to assess this situation? Richard Clarida, who served as Vice Chairman at the Federal Reserve from 2018 to 2022, who is now global economic advisor at Pacific Investment Management Co. remarks:

Ueda “may want to go in the direction to shrink the balance sheet or reinvest the redemptions, but that is not one for day one,” he said, adding Japan’s tightening would be a “historic moment” for markets though it may not be a “driver of global bonds.”

It may or may not be a historic moment. That basic uncertainty about the direction of travel, the sense that policy may be forced to move very large pieces of the global financial puzzle is what suggests to me that what we are seeing, is not just business as usual, but something closer to a conjunctural sea change.

***

Example 3: Developing countries locked out

In recent decades there has been a lot of talk about “development finance” as the high-road to achieving sustainable development. Low-income and developing countries will be incorporated into global financial markets, assisted by various types of “blended” public-private finance, allowing billions in assistance from the advanced economies to be turned into the trillions we all know are necessary for sustainable development. This is what Daniela Gabor calls the “Wall Street consensus”.

It is very hegemonic. It promises big profits for Western investors. But it is also, to a considerable extent, a charade. Not only are the costs and benefits unequally distributed between private investors and tax-payers in both advanced and developing economies. More importantly, the flows of finance enabled by public derisking have been trivial by comparison with the acknowledged need. Judged by its own ambition it has been a crashing failure. The system has come nowhere near enabling trillions of dollars to flow.

Now, as rates shift upwards, another risk is revealed. Once they become reliant on borrowing from bond markets, developing countries can find themselves suddenly locked out, as a result of interest rate movements and risk appetite in the rest of the world.

As Martha Muir writes in the FT.

More than a quarter of emerging market countries have found themselves effectively locked out of international bond markets as recent chaos in the banking sector has prompted investors to shun riskier assets. Even as the effects of the banking sector turmoil recede in developed economies, investors have adopted a “risk off” approach to high-yield debt. This has tipped emerging market countries whose credit status was already shaky into territory where their ability to raise funds is seriously impaired. According to research by Goldman Sachs, around 27 per cent of emerging market sovereigns currently have spreads on yields compared to equivalent US Treasuries of above 9 percentage points, the level at which market access typically becomes restricted. …. Egyptian and Bolivian dollar bonds are among those which have underperformed since the start of the banking panic, with their spreads climbing to 11 and 14 percentage points. Investors say that countries which had plans to issue bonds have avoided coming to market, such as Nigeria and Kenya, whose spreads climbed to 8.95 and 8.4 percentage points respectively in March. … Countries which face restricted access to international debt markets may be forced to turn to the IMF, private market debt sales and currency devaluations. “[Restricted access to debt markets] will push countries to take tough measures at a time where inflation is already high and they’re already struggling with low growth,” said Sara Grut, an emerging markets sovereign credit strategist at Goldman Sachs. “The key question for these countries is, what will be the thing to help them regain market access? One could be that they do very uncomfortable, unpopular reforms, or we see much stronger global growth that improves market sentiment.”

You could say that this shock merely confirms the fact that the global financial architecture is hierarchical and that derisking is a privilege of those in the core. This is true and to that extent you might say, plus ça change. But as manifest as these structural inequalities are, we should not underestimate the element of historical change and the significance of expectations, anchored in narratives, in propelling that change.

Blended finance was the fashion of the early 2000s and early 2010s. It always lived on promise as much as reality. The combination of the modest results actually delivered, followed by the 2014 commodity price shock, COVID, the food price shock of 2022 and now the market pullback of 2023, is enough to induce comprehensive disenchantment. This will not stop the macrofinancial imagination. Currently ,there are efforts to raise excitement around repo markets for African sovereign debt and giant imaginary markets for carbon credits. This imagination matters. It is important in motivating and legitimating action. But, at some point, history does begin to repeat as farce.

***

Does this mean that we are in a new macroeconomic or macrofinancial regime? Cédric Durand in New Left Review’s Sidecar, suggests as much, asking whether we are seeing the end of the hegemony of finance.

To return to the basic conceptual/analytical point, I’m skeptical about any such totalizing, metonymic move. I think our reality is too protean, too dynamic, too explosive to yield to such formulations.

But are the shifts adding up? Is the polycrisis shaking loose the assemblage of improvisations and assumptions we have been living with in recent decades? I think so. That’s the question that this series of posts will continue to track, on the hunch that something is indeed happening.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters and receive the full Top Links emails several times per week, click here:

April 1, 2023

Chartbook 207 Finance & the Polycrisis #10: The trillion-dollar rebalancing: A new macrofinancial conjuncture?

Whats new and whats old in the current conjuncture? I devoted my column this month in the FT to dissecting the forces at work in the recent banking crises and beyond.

What I wanted to push back against was the line of commentary that interprets the current round of banking crises and bailouts as repeating old patterns rather than reflecting a historic sea change in financial markets and policy stance.

Since the piece stirred a flurry of disagreement and quizzical commentary on twitter it seemed worthwhile adding some comments in the newsletter by way of explanation. I include the FT text below in block quotes with further explanation and elaboratorion interspersed.

***

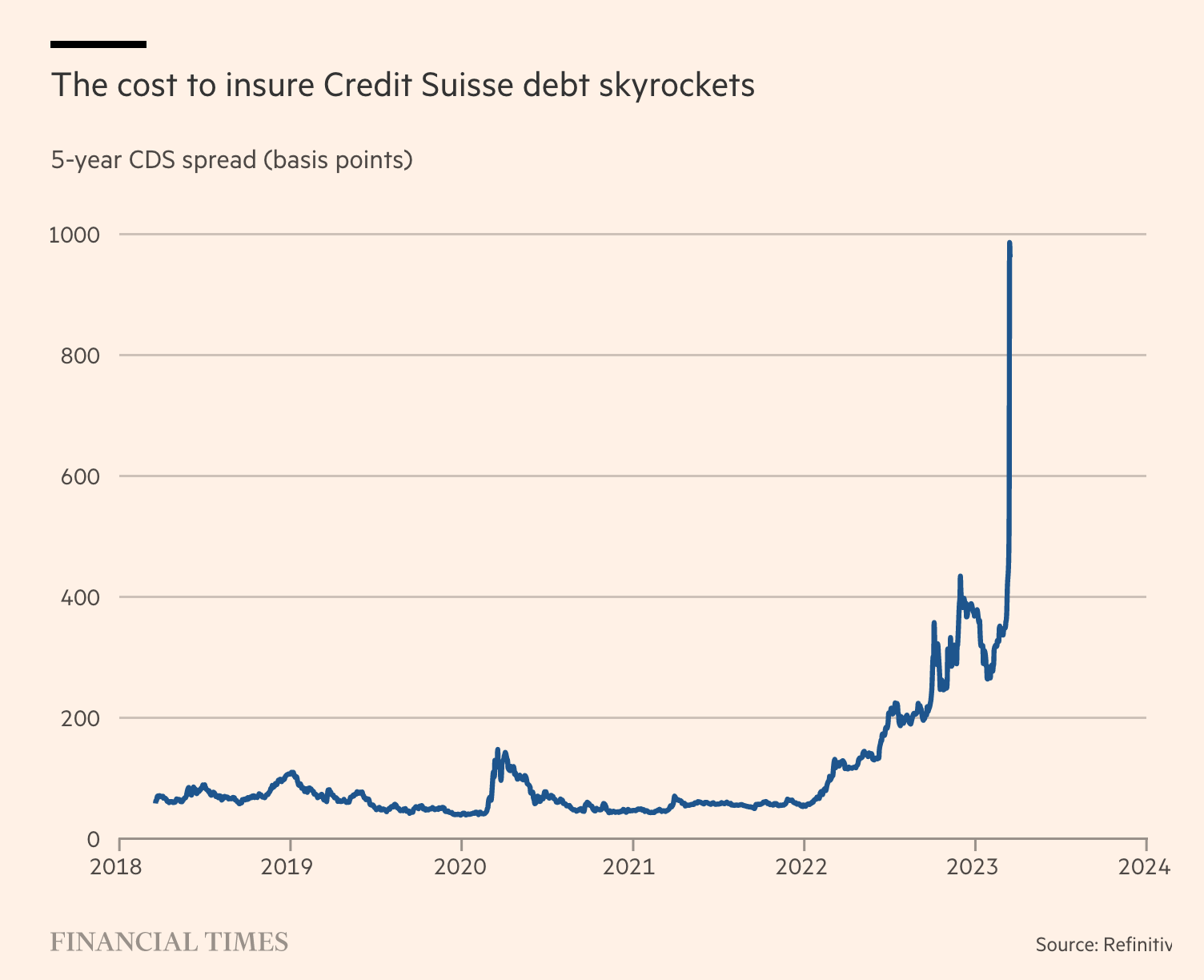

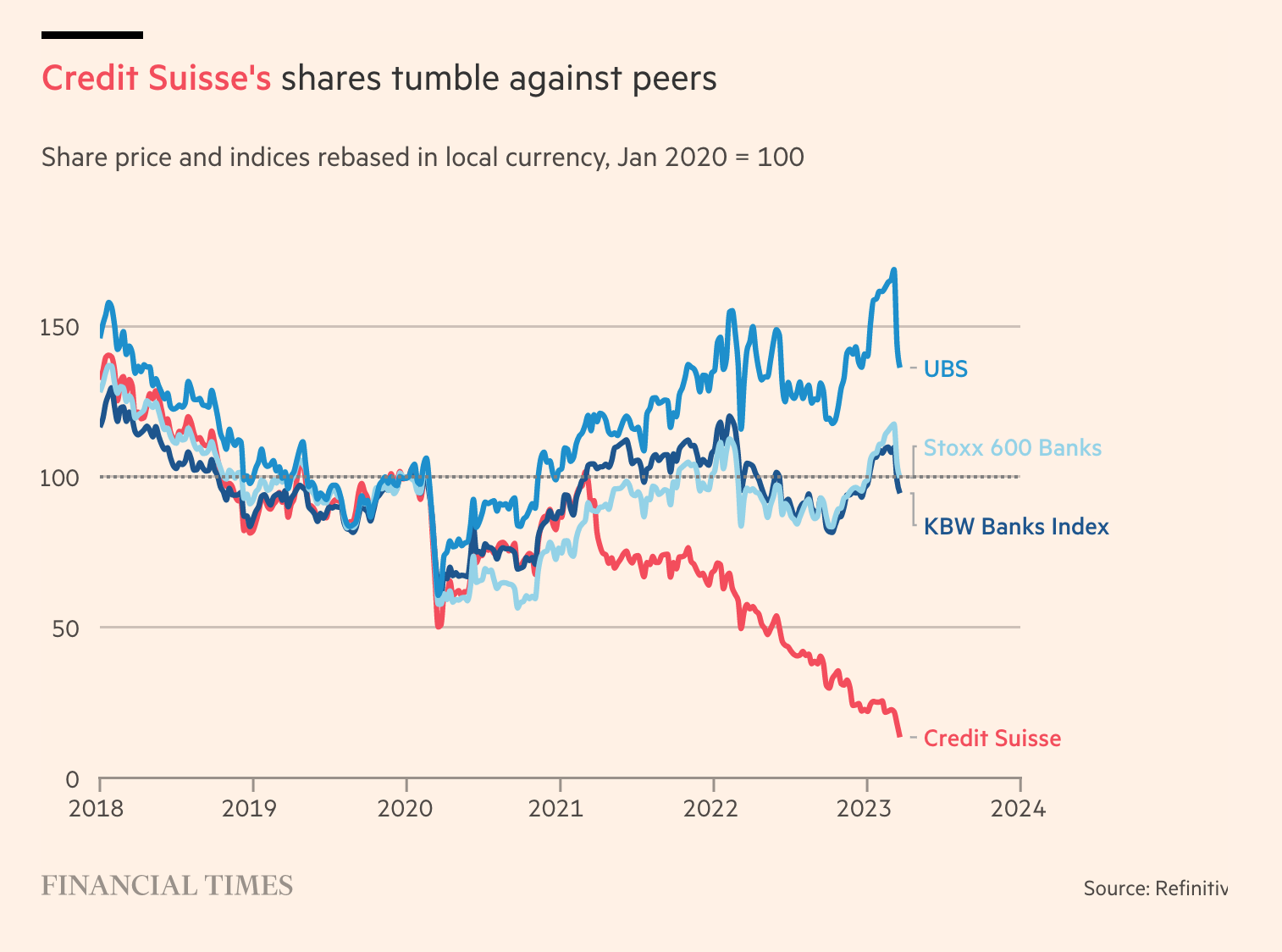

Faced with a rash of banking crises it is tempting to declare, plus ca change. There is nothing more inevitable than death, taxes and bank failures. But what about the bailouts? The publicly subsidised takeover of Credit Suisse by UBS and the hasty extension of guarantees to all SVB’s depositors are just the latest in a recent series of such actions. They suggest that we have entered a new era, one in which thoroughgoing liquidation of financial bubbles is politically unthinkable and so moral hazard and zombie balance sheets pile up.

Both these interpretations are superficially plausible. Put them together and you have a vision of ever larger balance sheets, inevitable crisis and no-less inevitable bailout, opening the path to even greater leverage and risk.

It is fair to say, I think, that this vision is shared by both left and right. I recently heard Cédric Durand espouse a similar line of argument at a EMNP conference at Sapienza in Rome.

But in focusing on the morality play (AT: a word play on moral hazard) of bad bank managers and lax supervision, they mischaracterise the drama we are living through. What defines our current moment is neither the bank failures nor the relatively modest bailouts, but the astonishing macro-financial switchback of 2020-2023. This began with mega-QE in response to the truly unprecedented shock of the Covid-19 lockdowns. The combination of stimulus, supply-chain disruption and Vladimir Putin’s war in Ukraine unleashed the biggest surge in inflation in half a century, which was met, not with monetary easing but with the most comprehensive tightening of monetary policy since the beginning of the fiat money era.

What I am trying to do here is to distinguish the immediate causes of the recent bank failures (such as appalling liquidity management at SVB) and the consequent bailouts, which are familiar and repetitive, from the broader backdrop, which really isn’t.

The COVID shock was uniquely savage and necessitated a uniquely gigantic central bank intervention. The ensuing inflation was the most dramatic since the early 1980s. The interest rate hike we have seen since 2021 has been the most comprehensive ever. The bond markets last year suffered their worst year on record.

This entire sequence defies previous experience and leaves us without obvious or convincing points of orientation.

This is not a case of “plus ca change” but of polycrisis. We would not be here but for the pandemic. And the central bank response too is novel. They are doing what is necessary to stave off further contagion from SVB, but on rates they are sticking to their guns. Since early 2022 in the face of a market rout the Federal Reserve has shown a resolve few people credited them with. Fed chair Jay Powell even half-hinted that a crisis or two might help to take the steam out of the economy. Certainly, those counting on the Fed to soothe their pain over huge losses on bond portfolios have had a rude awakening.

The crucial point here is that the “Fed Put”, the supposed guarantee by the Fed and other central banks that they would back the markets has been voided.

— Joey Politano(@JosephPolitano) June 16, 2022

As it turned out, the Fed’s commitment to the “Put” – an idea that first developed in the late 1980s – had never been tested in an inflationary situation. As a result we had a somewhat exaggerated impression of what became known as “financial dominance” i.e. the idea that the immediate interests of financial markets (rather than longer-term general interest in price stability) drove the Fed.

In 2021, whilst it had its eye on the recovery from COVID, the Fed was slow to raise rates. But when it pivoted to monetary restriction it pivoted fast and hard. If the Fed Put was previously an important assumption underpinning market behavior, and it surely was, it is now gone.

But, one might object, the authorities did step in with expansive new tools to bail out SVB’s depositors. In Chartbook 201 I wrote about “venture dominance”. But venture dominance is exactly that i.e. an important part of business community demanding a local bank bailout. This is a far more limited reaction than the Fed Put. Nor are the recent bank bailouts simply a repetition of earlier episodes.

It makes a difference, it seems to me, whether we are talking, as in 2008, about a comprehensive bailout of the banks that had engulfed themselves in a crisis of their own making. Or, as in 2020, dramatic central bank action to stabilize financial markets whose fragility was exposed by the impact of a pandemic. Or, as in 2023, a limited bailout of the depositors in a medium-sized but well-connected bank whose mismanagement was exposed by a sudden and peculiarly dramatic shift in Fed policy in response to inflation not seen in forty years. These are all bailouts in an extended sense, but not only do they vary in size and the instruments they use, but the shock they are reacting to is different in each case so also is their significance for our interpretation of what some analysts like Danieala Gabor call the “macrofinancial regime”.

In the FT piece I double down on this contrast between the bank bailouts and the monetary policy shock delivered by the Fed, by making a quantitative comparison.

Containing the fallout from SVB and Credit Suisse does involve some element of public subsidy, but those transfers are tiny in comparison with the trillion-dollar balance sheet shift from bond investor to bond issuers triggered by the post-Covid pile-up of inflation and interest rate hikes.

To be clear, this is not intended as a moral judgement. My point is not that the little bit of sugar (bailouts) is small beer by comparison with the pain inflicted through inflation-interest rates on the poor old banks. I make the comparison in support of the claim that the situation we are in is novel and not the repetition of previous bailouts. The historically noteworthy thing here is the monetary policy shock, which many thought the Fed lacked the nerve to deliver.

In the banking system the effect of this shock is visible in the now much-discussed losses on the bank balance sheets. These are mainly unrealized but notionally huge. Some estimates put them in excess of $2 trillion.

They are as large as they are because banks loaded up as much as they did after 2020 on fixed-income assets another underrated shift in the macrofinancial regime.

You can of course maintain that given the measures taken to prop up SVB and the derisking approach to every other aspect of policy, such as green industrial policy, which puts finance at the center of public policy, we are still in the same macrofinancial regime as ever. But, at the very least, we have to acknowledge that we had no way of knowing beforehand how the regime would operate in the face of a price surge. The Fed has clearly and brutally signaled its priorities. It will hike rates even if things break and tidy up the mess afterwards. That might change if a reallybig bank is in trouble. But they clearly believe that since 2008 things have changed and the big banks are now resilient enough. Whether this is true or not remains to be seen but it points to continuous change and modification within the macrofinancial regime, tested by shocks and modified by political interventions (as in the loosening. of banking regulation in 2018 which exempted SVB).

****

I could have left it there. Perhaps I should have. But, instead, I decided to extend the argument.

I’ve been waiting for some time for someone to write about the impact on the value of government debt of the double whammy of inflation and interest rate hikes. I was in part prompted to write my FT op ed by the fact that David Beckworth took up the theme in Barrons.

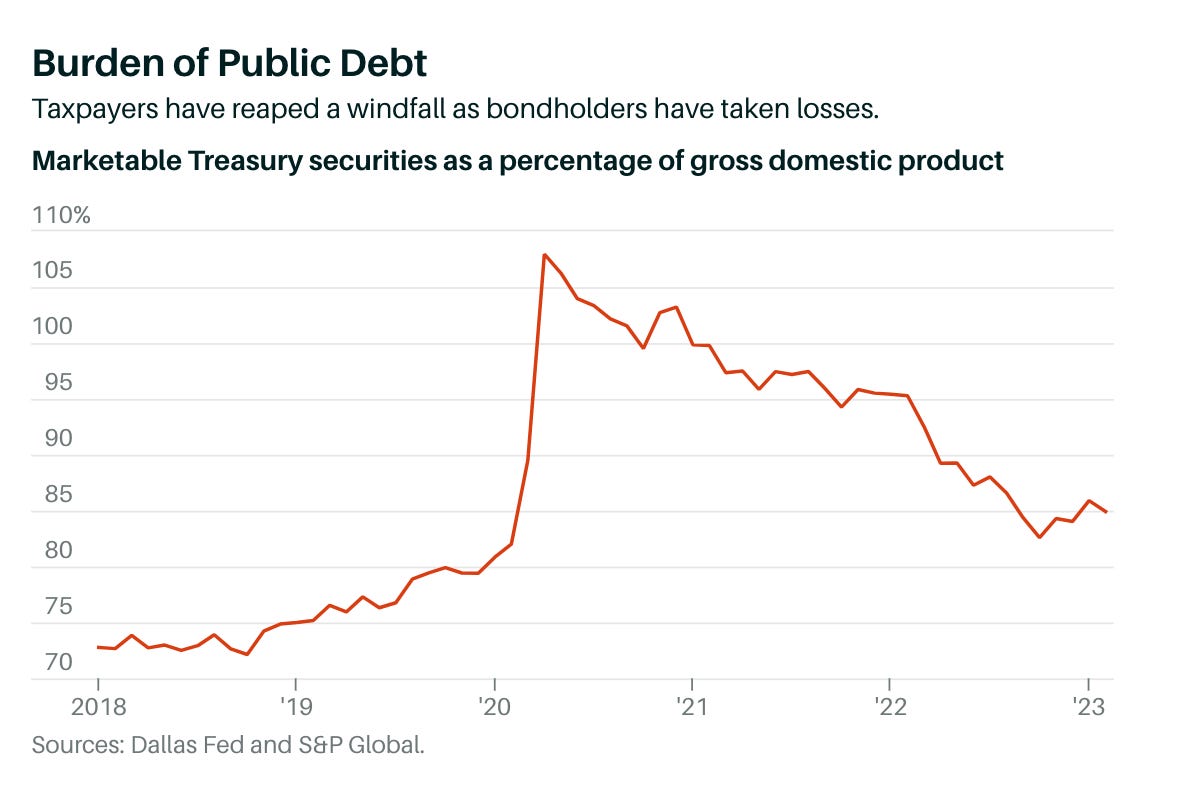

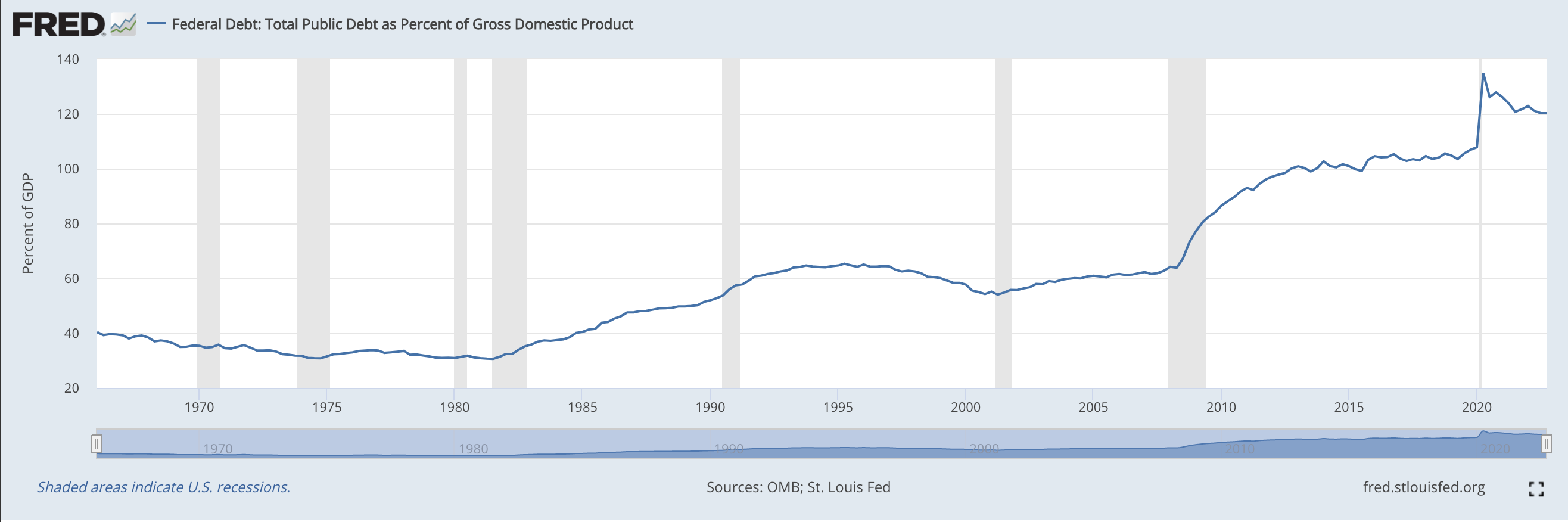

As David Beckworth has pointed out, in the US the ratio of public debt to GDP has plummeted by more than 20 percentage points from its pandemic peak. This spectacular balance sheet shift between debtors and creditors is happening as a result of three forces: the rebound in real output following the Covid shock, the rise in prices and wages which inflates nominal GDP, and the downward revaluation of the stock of bonds as a result of higher interest rates.

This paragraph in my FT piece turned out to be particularly controversial with folks who are deeply invested in the question of how to value debt stocks. Not everyone reading this newsletter may share this passion, so feel free to skip the following pargaraph.

It is controversial to claim that the revaluation of Treasuries and other bonds happening in the market due to the interest rate hike – the revaluation that is marked as an unrealized loss on the balance sheets of banks – really amounts to a transfer of wealth from debtors to creditors. After all, regardless of the market valuation of Treasuries, the taxpayer still has to service the debt and bear the interest burden. If they were to issue new debt to repay the outstanding bonds, the Treasury would do so at the higher interest rates now prevailing, which would negate the purpose of the repayment. The best answer, in defense of counting the debt reduction as real, is to imagine taxpayers actually paying tax with a view to repaying the debts by buying them outright and retiring them. If they did that following the interest rate hike they would realize a gain because purchasing the debt would be cheaper. Critics of the idea respond by pointing out that government debt is not generally repaid, but rolled over into new debt. This may be true, but the logic of the tax-repayment scenario seems sound and as a notional value it corresponds rather neatly to the notional losses on the balance sheet of the banks.

In any case, even if you use more conventional accounting. and focus simply on the surge in nominal gdp relative to national debt – nominal gdp being real gdp adjusted for inflation – it is clear that something very unusual is going on with the US public balance sheet.

In the last sixty years there has never been such a sharp or contrary development of the debt to gdp level as we have seen since 2020: first surging, then plunging and then continuing to tail off, despite continuing large deficits. Debt to gdp is now 15 percentage points lower than it was in Q2 2022 even as debt has increased by $5 trillion. This is because of the dramatic rebound of real output and the surge of prices.

In Europe, using entirely conventional debt accounting, we see a similar effect.

As recently as 2021 we were still worried about how we would cope with insuperable debt levels in a world of secular stagnation and chronic low inflation. Now the nominal GDP of debt-ridden Italy is increasing so fast that, to the third quarter of 2022, its debt-to-GDP ratio fell year on year by almost 7 per cent.

The idea that you can “inflate away” debt is a pretty common place historical observation. This is happening to a modest degree. But here too we must be careful. People who know a lot about bond market point out that permanently higher inflation may reduce the real value of the principal, but because it necessitates higher nominal interest rates, it drives up the burden of debt service. So, it is important to add at this point that my working assumption is that inflation will prove to be transitory. So what we are experiencing is a one-off shock to the price level, after which inflation will subside and rates will come down. What will remain is the reduction in the real value of the debt as expressed in the debt to gdp ratio.

As the FT column continues:

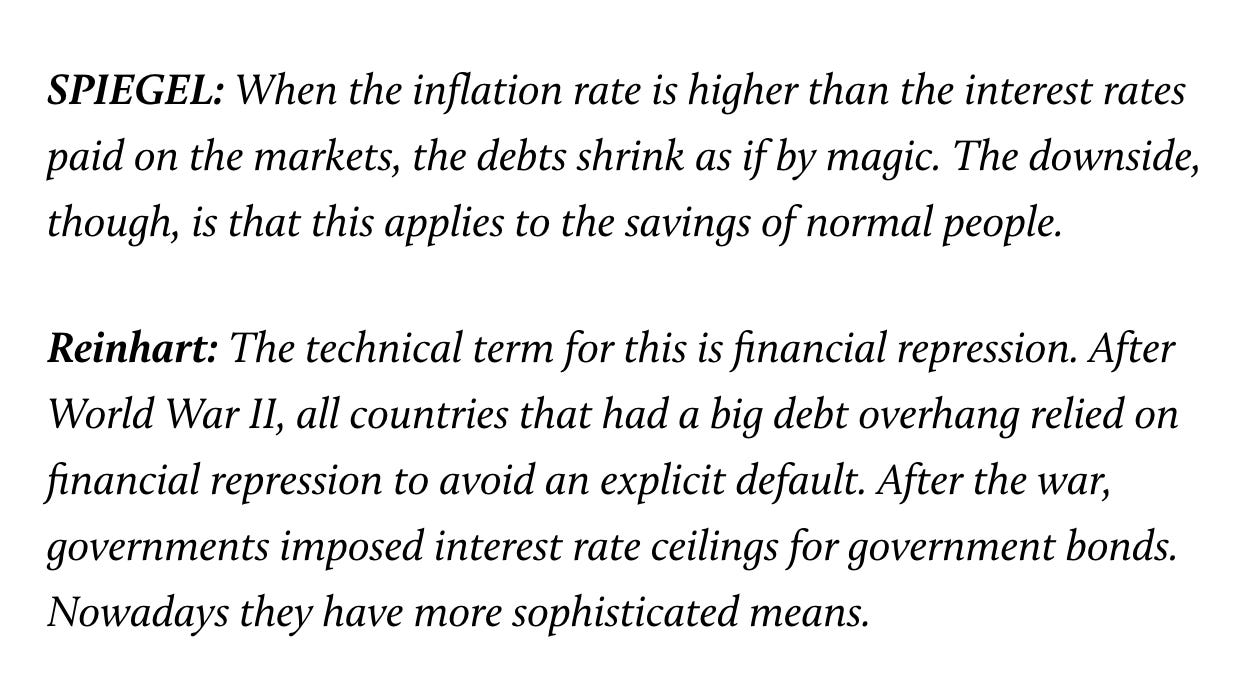

Though no one wants to be seen to be celebrating the inflationary wave, we are, beneath a decent veil of silence, living through one of the most dramatic and powerful episodes of financial repression ever.

This is the next moment in this short piece, in which I managed to upset some readers.

“Financial repression”, is, as they say in German, a Reizwort. If you know a lot of financial history you know that it was a pejorative term invented to describe a situation in which savers and lenders had the screws put on them by borrowers. This is an excellent summary by Jeremy Smith.

In the FT piece I used the term in the way that has, as Smith documents, become common place in financial talk. He quotes, disapprovingly, an interview with Carmen Reinhart in which she gives what I take to be the usual shorthand definition.

To avoid associating myself with a politics that is not mine, rather than saying “we are living through one of the most dramatic and powerful episodes of financial repression ever”, I might have better put my point as follows.

Perhaps I should have said that the last time we saw shifts in those ratios of this size, it was the era of financial repression and it then took much longer (and more complicated institutional mechanisms). @_TimBarker

— Adam Tooze (@adam_tooze) March 31, 2023

But, in any case, if I exaggerate the care for ‘financial repression” it is not to bemoan the fate of creditors, but rather wishful thinking on my part. I’m all in favor of financial repression. It seems evident to me that if high debt to gdp ratios are a problem, the way to deal with that problem is a combination of redistributive taxation on income and wealth and moderate bouts of unanticipated inflation of the kind we have seen since the second half of 2021.

***

Anyway, by this point some of my friends were losing patience with the tone of the article. “First Tooze is saying that the pain from the Fed is so much worse than the bailouts and now he is saying that the poor old financiers are suffering repression”.

Again, this imputes moral purpose than I intended. My intention rather, was to join. up the dots between the now well-known problem of unrealized balance sheet losses, interest rate hikes, inflation and public debt burdens. This is why the FT piece continues as follows:

Now the nominal GDP of debt-ridden Italy is increasing so fast that, to the third quarter of 2022, its debt-to-GDP ratio fell year on year by almost 7 per cent. Though no one wants to be seen to be celebrating the inflationary wave, we are, beneath a decent veil of silence, living through one of the most dramatic and powerful episodes of financial repression ever.

This is what lies behind the trillions of dollars in unrealised losses on the balance sheets of financial institutions around the world.

I then add a further link in the chain, which is the state of central bank balance sheets. They too are suffering book losses on their bond holdings. The central banks bought those bonds from private banks in exchange for reserves. The central banks now pay elevated rates of interest on those reserves. But if those bonds were on the balance sheets of banks, the unrealized losses in the private sector would be even greater.

The figure would be even greater were it not for the fact that central banks, thanks to QE, are also big holders of government debt and are thus sharing the paper losses.

So this is the central point. The novelty of our situation is that we are seeing trillion-dollar repricing on balance sheets all around and this is more telling than the latest rash of bank failures and bailouts.

Beyond the narrative of feckless banks and bailout-happy regulators, the truly systemic question is how we see our financial institutions through this giant trillion-dollar rebalancing. That is what will define this historical episode.

***

Again, I could have left it there. Perhaps I should have. But I had managed to compress the foregoing into 650 words. So, hey, I had another 150 words to play with. What else could I pack in?

(1) We can add a very important caveat:

Though debtors benefit from inflation and the revaluation of debts, they need to brace for the surging costs of debt service. Those who did not stretch the maturity of their obligations in the era of low rates now face an interest rate cliff.

That doesn’t seem to have satisfied the skeptics, but at least it was there.

(2) With 100 words left, I return to those debt to gdp ratios, spell out some of the political implications and rile up the readers one more time:

But if we can adjust to higher debt service and avoid a rash of bank crises, the one-off shock to the price level (NB one-off shock NOT persistently higher inflation) opens up unexpected fiscal space.

“Fiscal space”? This was the final straw.

How on earth can you can say that an increase in interest rates increases fiscal space? Obviously, higher interest rates by themselves don’t – see caveat (1) above – BUT it seems hard to argue with the idea that a one-off fall in the debt-to-gdp does improve your fiscal situation.

This is not to say that I subscribe wholeheartedly to the idea of “fiscal space”. It is a highly conventional construct at best. But it is an influential construct. And, whatever we take fiscal space to be, the debt to gdp ratio is one of its defining parameter. So, if rather than continuing to rise, your debt to gdp ratio falls. Or if you are in a situation where you can run large deficits and the ratio does not go up, then you gain an unexpected degree of freedom.

So, if the lower debt to gdp ratio does confer a degree of freedom, the question is what to do with it. In conclusion I return (1) to what I take to be the starting point – pandemic/polycrisis

We must use this (“fiscal space”) wisely. We need public investment so as to escape the reactive cycle we are currently locked in and to begin anticipating the challenges of the polycrisis, whether in public health, climate change or destabilising geopolitics.

(2) to a wider view of the distributional question and its implications

We must also provide relief to that part of society which is least well equipped to handle these financially-turbulent times. Those in the bottom half of income and wealth distribution are bystanders in the great balance sheet reshuffle. They hold few if any financial assets and pay relatively little tax. They have lived the drama of Covid and its aftermath as a shock to jobs and cost of living crisis. Unlike bond holders or investors, their interest are not represented by lobbyists. Their households are not too big to fail. But if those who run the system imagine they can be ignored, that they are not systemically important, those elites should not be surprised by the strike waves and populist backlash coming their way.

The key point I wanted to make here is that there is a distributional politics that refers to stocks/balance sheets (debtors v. creditors) as well as distributional politics that refers to flows (income, spending). At least half the population in any capitalist society has no financial wealth to speak of and pays relatively little tax and thus has little at stake in the distributional politics of balance sheets. But we should go on connecting the dots. If you gain a degree of freedom on the balance sheet, consider what options it might open up not just for asset accumulation (investment) but also for the flows i.e. various types of payments.

***

So let me restate the thesis.

We are going through a series of heterogeneous shocks which force policy reactions for which there is no obvious historical precedent – polycrisis.

Every domain of society, economy and politics is affected – health care, defense, tech, energy, and finance amongst others.

The financial apparatus is an important piece of the whole, but we live in an age of financialization as much as we do in an age of big tech, biopower, and mounting great power confrontation between China and the US … One could go on. These sectors intersect and interact. The financial system both receives and delivers shocks. No one sector currently dominates.

The financial system or regime is fraught with power plays between powerful and diverse financial interests, the state apparatus and politics. Whether this is a settled regime is an open question. If we can meaningfully talk of a macrofinancial regime, it includes assumptions about the Fed’s reaction function.

The central bank is relatively autonomous, as it demonstrated both in its slow response to inflation and then in going in hard and fast. In 2022 the Fed invalidated the Fed Put as an operative assumption.

I don’t think they did so in a fit of panic or absent-mindedness. I do not subscribe to the “mistake view” on Fed policy. I think they took a considered risk in prioritizing labour market recovery in 2021. That has paid off. Did they underestimate the inflation risk? Perhaps. They certainly took a risk. Were they aware that this exposed fixed income to the possibility of a huge repricing? Clearly, they were. That is what it means to invalidate the Fed Put.

The hike in 2022 has had a dramatic impact on balance sheets. The Fed Put is gone. Whether Treasuries can any longer be considered a safe asset in Gorton’s terms. is surely open to question. As a credit risk yes. But in terms of rates and pricing, surely not. Along with the end of the Fed Put this would seem to imply a significant shift in macrofinancial regime. And we are not done yet. Bonds were first in line. Real estate may be next.

Weaker banks were exposed and as usual the authorities were forced to step in to avoid systemic damage. But that does not demonstrate financial dominance so much as the necessary buttressing and clean up necessary to enable the Fed to continue the main thrust of policy, which is the interest rate hike. Worth half-decent regulation the whole mess could have been avoided. Of course sloppy regulation is not an accident. It is endogenously produced. But SVB is egregious.

“Venture dominance” mattered at the margin in making the authorities more likely to bail out the SVB depositors than depositors in another bank of similar size. It is a bigger deal than the crypto bust and FTX. But all told it was a minor flanking skirmish in a bigger battle in which the Fed is demonstrating not subservience but, for want of a better word, autonomy.

Is there something to rescue for a progressive policy view? To that a qualified yes. The cunning of history has delivered something akin to financial repression. The real thing would be preferable, but you make the best of what the game gives you.

We should use the rapid pace of nominal gdp growth to enable both longer-term policy and short-term support for those hardest hit by the cost of living crisis.

Should we call this a new macrofinancial regime. That would be to go too far. But how about calling it a new macrofinancial conjuncture?

I owe thanks to all the folks whose head-scratching and argument caused me to think this through.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters and receive the full Top Links emails several times per week, click here:

March 31, 2023

We are living through a trillion-dollar rebalancing

Beneath a veil of silence, a hugely dramatic and powerful episode of financial repression is ongoing

Read the full article in The Financial Times.

Ones & Tooze: Berlin Economics

Hosts Cameron Abadi and Adam Tooze talk about Berlin, Cam’s home town, on this week’s episode. They grapple with the recent mayoral election and what it says about the economy there.

Before that, Cam and Adam dig into climate change news. According to the latest report from the Intergovernmental Panel on Climate Change (IPCC), it seems increasingly unlikely the world will be able to limit global warming to 1.5°C. Adam and Cam discuss what countries should be doing with this new information.

Find more episodes and subscribe at Foreign Policy.

March 28, 2023

Chartbook 206: The attack on the Center for Policy Research, India’s leading policy research institution.

Dear friends, I don’t usually employ Chartbook newsletter for campaigning purposes. But then it is not usual for research centers, which I have been attached to and which serve as vital nodes in the global network of thought, to come under gratuitous and direct attack. This is what is happening with the Center for Policy Research in New Delhi which I had the privilege of visiting in the autumn of 2022.

When I arrived in Delhi it had just been raided by the tax authorities. Researchers had had their laptops and phones impounded.

As Vinay Sitapati commented in the Indian Express:

The authorities could have simply posed questions via email. But the raid-like quality of this survey — with bellicose tax officials and tipped-off cameramen — was meant to convey a message.

Now in March 2023, the Center’s future has been put in jeopardy by the suspension of its foreign funding license.

In light of this harassment of the CPR, I joined a list of international researchers in signing a letter of support for CPR. I put the letter and the list of signatories in quotes so that you can clearly distinguish my commentary from the parts that are agreed amongst us. Since this newsletter is read by folks in think-tanks, academia, government and business around the world, Chartbook seemed like the right platform to raise awareness of the CPR’s situation. These are our colleagues who are under attack.

Letter from Concerned International Faculty and Researchers

As researchers and scholars with a deep interest in India, we are shocked and dismayed to learn that the Government of India has suspended Centre for Policy Research’s (CPR) registration under the Foreign Contribution Regulatory Act. Coming on the heels of the Income Tax survey conducted on CPR last year, this action is clearly aimed at undermining a leading research institution and jeopardising its existence. It also sets a dangerous precedent that will impair the pursuit of research and independent judgment in the country.

Established in 1973, CPR is one of India’s oldest and most esteemed policy research institutions. Over the past the five decades, it has served as a vital and resolutely non-partisan centre of knowledge and research on key public policy questions and challenges confronting India and the world. The excellent scholarship produced by CPR has also consistently illuminated and informed Indian public debates. CPR has the rare distinction of working with successive central and state governments as well as a range of other institutions across the country.

For the range of issues that the CPR covers, check out the videos of the CPR Dialogues 2022 covering the clean air crisis

And rural policy issues

As you will be able to judge, this is the kind of engaged, critical, deeply informed expertise that is essential to democratic governance.

The letter goes on:

The governing board of CPR, comprising eminent Indians committed to public service, has held the organization to the highest standards of intellectual rigour and institutional probity.

Former members of the board include figures as distinguished as Dr Manmohan Singh, 13th Prime Minister of India.

Suspending the CPR’s registration is akin to suspending the operation of Brookings or Chatham House on the suggestion that “they have a case to answer”.

As the open letter goes on:

Precisely because it is an Indian institution steeped in the Indian policy milieu, CPR has been a close and indispensable interlocutor to academics and researchers working on India across the world.

As a rank outsider to India, this is what most forcibly struck me about CPR. It offers an open, welcoming and challenging platform for the much-needed conversation with India and about India, a state that will exert a huge influence over the entire world in the 21st century. Check out, for instance, the Q&A that followed my keynote at the CPR dialogues conference in 2022.

And the conversation with Pratap Mehta

Through its rigorous research and active engagement the CPR has earned a reputation for excellence that is second to none among international scholars. It has also facilitated the engagement of a large number of scholars with India over the years and has mentored some of the finest young researchers in India.

During my visit I was schooled on Indian politic, government and much else besides by the President and CEO of CPR, Yamini Aiyar. In December she gave an excellent interview to the Council of Foreign Relations on why think tanks matter to Indian policy. She is one of the most prolific and in-depth commentators on the Indian welfare state.

Sociologist and anthropologist Mekhala Krishnamurthy blew my mind in tireless conversations about India’s digital registrations systems, state capacity and the operations of local farm markets. I came away with a fundamentally new understanding of India’s development challenges and possibilities.

Navroz Dubash took time to introduce me to global climate politics from an Indian point of view. His work along with a global team on Varieties of Climate Governance in Environmental Politics is agenda-setting across the world. ‘India in a Warming World‘, edited by Dubash, is an essential reference work for anyone interested in global climate politics. It is precisely the kind of work through which CPR helps Europeans and Americans to revise their understanding of global issues under the influence of a distinctly Indian point of view.

There were other conversations, more than I can recount here, on the politics of Delhi, Indian foreign policy and European and global history. As the letter goes on:

In turn, CPR’s commitment to rigorous academic inquiry has made it the partner of choice for many universities, research institutions and philanthropic foundations outside India. CPR is a highly valued member of the international research community—one that has considerably enhanced the reputation of Indian academic and research work on the global stage.

The recent moves against CPR by the Indian government amount to an abrogation of the institutional independence that is crucial to the production and dissemination of knowledge. In so doing, they also strike a blow at intellectual freedom and public reason that are cornerstones of Indian democracy. We respectfully urge the Indian government to reconsider its decision. We affirm our full support to the President of Centre for Policy Research and her colleagues.

If you would like to contact me about this issue, please use my website, or my institutional Columbia email. At the time of writing, the list of signatories to the letter is as follows:

Dan Honig Associate Professor University College, London

Karuna Mantena Professor of Political Science Columbia University

Adam Tooze Professor of History Columbia University

Ashutosh Varshney Professor of Political Science Brown University

Prerna Singh Associate Professor of Political Science Brown University

Tariq Thachil Professor of Political Science University of Pennsylvania

Sanjoy Chakravorty Professor of Geography and Urban Studies Temple University

Paul Staniland Professor of Political Science University of Chicago

Mukulika Banerjee Associate Professor of Anthropology London School of Economics

Christophe Jaffrelot Professor of Indian Politics and Sociology King's College London

Andrew Kennedy Associate Professor Australian National University

Pradeep Chibber Professor of Political Science University of California, Berkeley

Ira Katznelson Professor of Political Science and History Columbia University

Jan Werner-Mueller Professor of Social Sciences Princeton University

Sumit Ganguly Professor of Political Science Indiana University

Uday Singh Mehta Professor of Political Science City University of New York

Mark W. Frazier Professor of Politics The New School

Shanta Devarajan Professor of the Practice of International Development Georgetown University

Gary Bass Professor of Politics and International Affairs Princeton University

Lousie Tillin Professor of Politics King;s College London

Parick Le Galès Resarch Professor of Sociology, Politics and Urban Studies Sciences Po

Olle Törnquist Prof. Emeritus of Politics & Development University of Oslo

Poulami Roychowdhury Associate Professor of Sociology McGill University

Michael Burawoy Professor of Sociology University of California, Berkeley

Mike Levien Associate Professor of Sociology Johns Hopkins University

Rina Agarwala Professor of Sociology Johns Hopkins University

Emmerich Davies Assistant Professor Harvard University

Lucas González Professor Escuela de Política y Gobierno

Phil Harrison Professor University of the Witwatersrand

Rajesh Veeeraghavan Assistant Professor Georgetown University

Adam Auerbach Associate Professor American University

Kim Lane Schepple Professor Of Sociology Princeton University

Alexander Lee Associate Professor of Political Science University of Rochester

Anjali Thomas Associate Professor of International

Affairs Georgia Institute of Technology

Jishnu Das Professor Georgetown University

Maitreesh Ghatak Professor of Economics London School of Economics

Pranab Bardhan Professor University of California, Berkeley

Sumitra Badrinathan Assistant Professor American University

Bhumi Purohit Assistant Professor Georgetown/ UC Berkeley

Rani Mullen Professor The College of William & Mary

Alpa Shah Professor of Anthropology London School of Economics

Rachele Brule Assistant Professor of Political Science Boston University

Sanjay Ruparelia Professor Toronto Metropolitan University

Aditya Dasgupta Assistant Professor of Political Science University of California, Merced

Rikhil Bhavnani Professor of Political Science University of Wisconsin, Madison

Christopher Clary Assistant Professor State University of New York, Albany

Pradeep Chhibber Professor of Political Science University of California, Berkeley

Larry Diamond Senior Fellow The Hoover Institution

Irfan Nooruddin Professor Geogetown University

Gyan Prakash Professor Princeton University

Aditi Malik Assistant Professor College of the Holy Cross

Jennifer Bussell Associate Profesor of Political Science University of California, Berkeley

Nayanik Mathur Professor Oxford University

Indrajit Roy Senior Lecturer University of York

Emma Mawdsley Professor of Geography University of Cambridge

Darryl Li Assistant Professor University of Chicago

Megnaa Mehtta Lecturer in Social Anthropology University College, London

John Echeverri- Gent Professor of Politics University of Virginia

Christine Fair Professor Georgetown University

Neil DeVotta Professor of Politics and International Affairs Wake Forest University

Wilhelm Krull Founding Director The New Institute

John Harriss Emeritus Professor of International studies Simon Fraser University

Dinsha Mistree Research Fellow Hoover Institution and Stanford Law

School

Sunil Amrith Professor of History Yale University

Rohit De Associate Professor of History Yale University

Sudipta Kaviraj Professor of Middle Eastern, South Asian and African Studies Columbia University

Atul Kohli Professor of International Affairs Princeton University

Maya Tudor Associate Professor of Government and

Public Policy Oxford University

Gabi Kruks-Wisner Associate Professor of Politics and Global studies University of Virginia

Adam Ziegfeld Associate Professor Temple university

Sanjay Reddy Professor of Economics New School of Social Research

Ravinder Kaur Professor University of Copnhagen

Francesca Jensenius Professor of Political Science University of Oslo

Tanushree Goyal Assistant Professor of Politics Princeton University

Simon Maxwell Former Director Oversees Development Institute

Robert Stavins Professor of Energy & Economic Development Harvard Kennedy School

Mike Hulme Professor of Geography Cambridge University

Matto Mildenberger Assistant Professor University of California, Santa

Barbara

Harald Winkler Professor University of Cape Town

Patrick Heller Professor of Sociology Brown University

Hochstetler, Kathryn Professor of International Development London School of Economics and Political Science

Peter Newell Professor of International Relations University of Sussex

Vinay Gidwani Distinguished University Teaching Professor University of Minnesota

Matthew Lockwood Senior Lecturer University of Sussex

Holdren, John P. Co-Director, Science, Technology, and Public Policy Program Harvard Kennedy School of Government

David Engerman Professor of History Yale University

J. Timmons Roberts Professor of Environmental Studies and Sociology Brown University

Raphael Kaplinsky Emeritus Professorial Fellow Institute of Development Studies, University of Sussex

Carlota Perez Honorary Professor University of Sussex

Rumy Hasan Senior Lecturer University of Sussex

Filippo Osella Professor of Anthropology University of Sussex

Ben Rogaly Professor of Human Geography University of Sussex

Harro von Blottnitz Director Energy Systems Research Group University of Cape Town

Lucy Baker Senior Research Fellow University of Sussex

Stephen Howes Professor of Economics at the Crawford School of Public Policy Australian National University

Matthew Paterson Director, Sustainable Consumption Institute University of Manchester

Milan Vaishnav Director and Senior Fellow, South Asia Program Carnegie Endowment for International Peace

March 26, 2023

Chartbook 205: Does Ukraine’s war economy have a new platform in 2023?

Whilst Xi and Putin maneuver and Russian tactical nuclear weapons trundle towards Belarus, big Western money is flowing into defense stocks.

As one private equity hawk commented: “Before it was seen as something to be ashamed of, so no one talked about investing in defence, but since the war in Ukraine, the dynamic has changed, and investors are bragging about it,” he said.

Meanwhile, I continue to be concerned that we don’t pay enough attention to the economy and society that is bearing the brunt of the struggle, Ukraine itself. Whether Ukraine can sustain another year of war depends not just on the battlefield but events on the home front.

***

A recent interview with Andriy Pyshnyy (Andriy Pyshnyi), the 48-year-old head of the National Bank of Ukraine, by the FT’s Ben Hall, gives an idea of the efforts that have been made since October last year to stabilize the Ukrainian war economy, at least in financial terms.

Andriy Pyshnyy took office in October after a significant clash between the central bank and the national government over the financing of the war effort. As the FT explained, “an “open conflict” with the government” had broken out over the monetary financing of the war, which ““created huge risks for macro-financial stability” when the bank was last year forced to print billions of hryvnia to plug a budget shortfall. “It was a quick remedy, but very dangerous,” said Pyshny … The finance ministry had been unwilling to tap domestic bond markets or raise revenues instead.” This also led to mounting tension with Ukraine’s Western backers who could see the writing on the wall in financial terms.

Pyshnyy’s predecessor Kyrylyo Shevchenko echoed those arguments in an opinion piece in the FT in September, adding to tensions with the government. Pyshnyy, a former banker who lost his hearing at aged 34, replaced Shevchenko in October. On his first day in office he set out to repair relations with the government, meeting finance minister Serhiy Marchenko “until the late hours of the night”. They struck a deal, with the central bank adjusting its bank reserve requirements and the ministry offering lenders more attractive terms. Pyshnyy said the NBU’s aim was to soak up excess liquidity by tougher reserve requirements and gradually return to a floating exchange rate.

Ukraine then entered a probationary period with the IMF.

Ukraine has a poor record of meeting the IMF’s conditions during a succession of bailouts. But Kyiv built confidence by reaching the goals set by the fund during a four-month “programme monitoring with board involvement” (PMB) over the winter, Pyshnyy claimed.

As Pyshnyy spelled out in an interview with the IMF in December, the Fund’s involvement was crucial in sealing the domestic bargain:

The monitoring program is an important step that allows Ukraine to demonstrate its aspiration and readiness for reforms, regardless of the war. This will be also an opportunity to coordinate fiscal, monetary, and other policies, and facilitate interactions between the NBU as the institution with the mandate to ensure price and financial stability, and the Ministry of Finance, which has the mandate to seek necessary financing of the war. Ukraine understands how important it is to use all the potential of the domestic debt market and achieve the important strategic task of financing for the FY2023 budget. We have to finance colossal budget needs of least $38 billion with external funds. We coordinated with the Ministry of Finance and agreed that the financing of next year’s deficit will not be done by the central bank, as this would create additional risks and challenges for macroeconomic stability. Even though we need a record amount of money, the Government of Ukraine, the Ministry of Finance and the NBU plan to finance the budget through cooperation with the donor coalition and the domestic debt market as well as with the assistance from the IMF. We believe that the monitoring program will be one of the key elements that will allow Ukraine to attract financing from the coalition of international partners. They will look for a green light from the IMF. At the same time, we hope it will be the first step to an upper-credit tranche program that Ukraine is counting on next Spring. We are grateful to the IMF team for their intense and professional work during these past two very challenging months. There was continuous communication, 24/7. The two parties held conferences night and day. We finalized our agreement during a missile attack. This added significance to each word that was spoken and each decision that was made.to the IMF, their

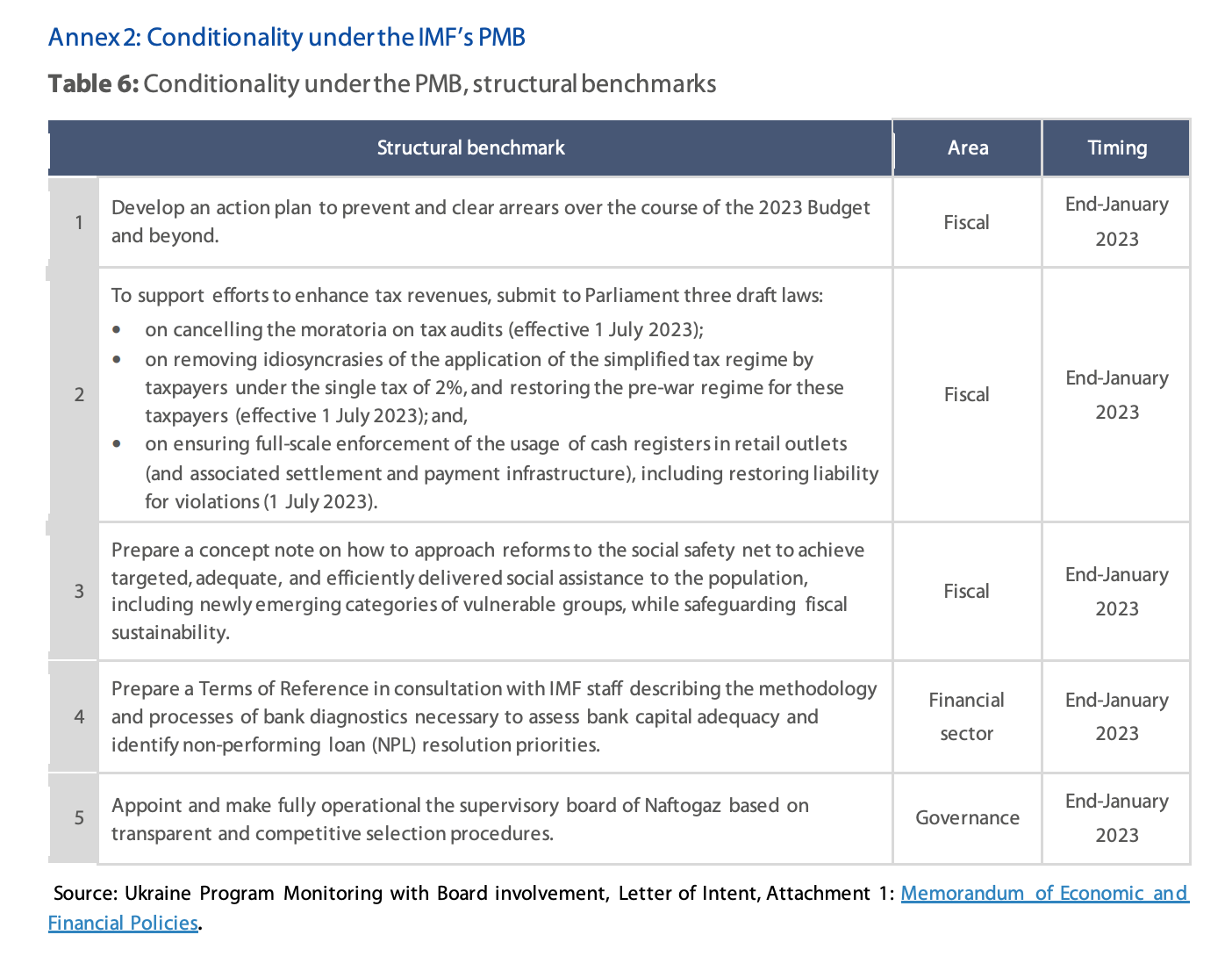

Pyshnyy’s plan seems to have worked. The PMB with the IMF laid out a series of demanding administrative and political conditions for Ukraine.

Source: European Parliament

Successful completion of the Program Monitoring with Board Involvement set the stage on March 21 2023 for the announcement of a $15.6 billion agreement with the IMF.

This has been widely hailed as unprecedented in that it involves the IMF in backing a country involved in an all-out war with little prospect of securing financial viability any time soon. In fact, already in 2014 the IMF crossed the rubicon when it extended financing to Kyiv amidst the chaos and violence that followed the Maidan upheaval and the Russian sponsorship of the Donbas breakaway. In 2023 the quid pro quo from Kyiv, according to Pyshnyy, is “(a)n end to monetary financing, use of domestic bond markets and measures to increase tax revenues have been hard-wired into the IMF deal.” This severely constrains Zelensky’s government, but will certainly be regarded as a victory by the conservative monetary managers at the NBU.

The 48-month Extended Fund Facility (EFF) Arrangement with the IMF is divided into two phases. The first phase, according to the IMF:

…. currently envisioned during the first 12-18 months of the program, will build on the PMB, to strengthen fiscal, external, price and financial stability by (i) bolstering revenue mobilization, (ii) eliminating monetary financing and aiming at net positive financing from domestic debt markets, and (iii) contributing to long-term financial stability, including by preparing a deeper assessment of the banking sector health and continuing to promote central bank independence. New measures that might erode tax revenues will be avoided. The authorities are also committed to continuing reforms to strengthen governance and anti-corruption frameworks, including through legislative changes.

Both the IMF and Kyiv assume that the comprehensive agreement with the IMF will in turn “ensure the coalition of donors commits to providing assistance of about $40bn”. It had the immediate effect of triggering a moratorium on all debt repayment owed to G7 creditors.

So, this appears to be the sequence:

(1) Political crisis between NBU and Zelensky government, September-October 2022

(2) October 2022 Reshuffle at NBU & provisional agreement UNB-government

(3) Winter 2022-2023 IMF probation

(4) March 2023 IMF deal → hope of full external funding for 2023.

***

The question is what price Ukraine will pay for abiding to terms of the IMF deal, what kind of austerity measures and tax increases will be necessary to balance the books without resort to the UNB printing press. These questions are all the more urgent because hope for any substantial recovery of Ukraine’s economy has evaporated under impact of Russian assault on the electricity infrastructure.

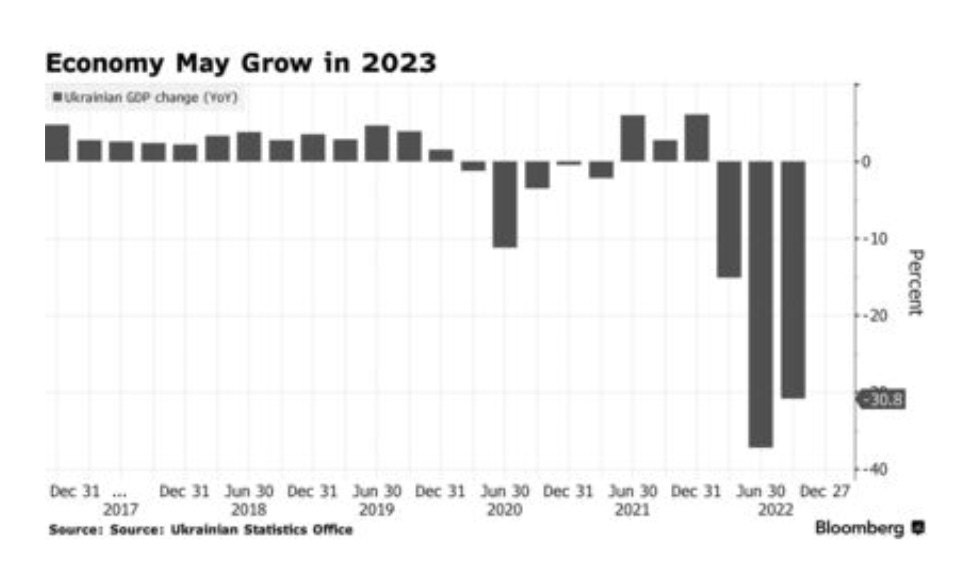

The governor told the FT that “the NBU would next month revise down its forecast for GDP growth in 2023 to just 0.3 per cent, after a 30 per cent fall over the past year, reflecting the impact of Russian missile strikes against Ukraine’s energy infrastructure over the winter.”

As Bloomberg reported, there are some signs optimism from short-run economic data:

One indication that households and business are learning to cope with the war’s impact is monthly increases in payment-card transactions despite increasingly frequent power outages, Pyshnyi said. Another is the number of diesel generators imported this year. Some 500,000 are helping the country continue working in the face of hours-long blackouts, according to the Prime Minister Denys Shmyhal.

But for all the remarkable resilience shown by the Ukrainian economy, the IMF team puts its growth outlook at between -3 and +1 percent for 2023, a stabilization, at best, after the disastrous impact of 2022.

In mid-March the NBU announced new measures to freeze as much purchasing power as possible in savings accounts and other bank deposits.

Meanwhile, the kind of austerity measures that may be in the pipeline are illustrated by an excellent report by Kateryna Semchuk on the OpenDemocracy site. She discusses how “a new salary structure for the Ukrainian military, introduced under the extreme economic pressures of Russia’s war, is leaving them unable to buy combat essentials or pay for medical treatment.” Since high military salaries helped to boost the home economy in the first months of the war, we should now expect a reverse austerity shock. Ukraine’s civilian medical system has been under severe funding pressure.

Ukrainian and European labour unions have expressed concern about the fact that controversial labour market deregulations measures that were blocked by popular protest in 2020 and 2021 are now being pushed through parliament. As Kateryna Semchuk Thomas Rowley report in OpenDemocracy:

Ukrainian trade union leaders have told the EU that they understand the need to limit workplace rights during wartime but are worried about the long-term consequences of deregulation. The reforms have so far “mostly resulted in the deterioration of employment conditions”, according to a December ‘needs assessment’ by the Council of Europe. … Ukrainian social policy analyst Natalia Lomonosova previously told openDemocracy that she feared that the government’s radical wartime socio-economic policy could exacerbate the vulnerable situation of millions of Ukrainians displaced by Russia’s war. The anonymous European diplomat’s summary was stark: “We are witnessing the breakdown of the social state in Ukraine. “Everything apart from the military is now outsourced internationally. Social affairs are more and more outsourced to international donors – which is why international donors should pay more attention to this,” they added. “The Washington Consensus has never been more alive than in Ukraine. It is Ukrainian-initiated, but in the West we accepted it,” the European official said, referring to the policy of pushing developing states to move away from state regulation and towards the free market. “And for Ukraine, this is a way to get closer to the West, and to fight the local oligarchs.”

In an impressive report from December 2022, Luke Cooper discussed the logic of “Market economics in an all-out-war?” that is at work in Ukraine. In the name of anti-corruption drives and austerity Kyiv seems wedded to a minimal state vision, whereas the opposite is actually required. “A genuinely modernizing economic strategy should start from ensuring the capacity of the state to protect its citizens and the environment. Investment in capital projects for a green transition, public services like healthcare and education, and the social safety net, will be critical to ensuring Ukraine’s long-term development.”

***

Often, in discussing the nightmarish trade-offs facing Kyiv in its effort to continue the war, commentators will turn their eyes from the immediate war-effort to the future and the reconstruction to come. As the FT remarks, “The one silver lining is that “The new forecast does not factor in any additional western aid for reconstruction, which Pyshnyy hoped would act as a “silver bullet” for the economy.””

But this only confirms the broader diagnosis offered by the OpenDemocracy authors and other worried observers. Reconstruction will rely not only on the World Bank but on the EU and a bevy of heavy hitters from the side of global fund management. An agreement between President Zelensky and Larry Fink of Blackrock was announced on December 28 2022. The question, as ever, is how real is the promise of public-private blended finance?

The latest World Bank estimate puts the figure for reconstruction costs at $411 billion. Given this huge sum, there is no doubt that private capital will have to be mobilized. But, as Cooper and others argue, this will not flow on anything like the scale required unless Ukraine can establish a truly competent fiscal apparatus. The focus should not be on stripping the state back to its minimal functions, but on building capacity.

As a report for the German Marshall Fund headed by Jacob Kirkegaard, Thomas Kleine-Brockhoff, Bruce Stokes and Ronja Ganster argues:

Even if there is a ceasefire or a settlement, Ukraine’s reconstruction will begin in a volatile environment, possibly including the risk of renewed Russian aggression. In the absence of a policy intervention, this situation will deter privatesector actors, especially foreign ones, from directly participating and investing in reconstruction, possibly for a prolonged period. Insurance premiums, if at all commercially available, will be prohibitively high for private-sector economic activity to commence

The NBU is no doubt right to be concerned about the inflationary impact of monetary financing. Stopping a descent into monetary chaos is essential for home front stability. But a policy of dramatic fiscal austerity that comes at the expense of the fabric of Ukrainian society and the state will have huge long-run costs. The EU, the United States and other outside supporters can soften this dilemma best a. by providing more generous funding and b. by urging Kyiv towards a strategy of civilian as well as military state-building, not by replacing domestic national institutions with international agencies, but by promoting the mobilization of local institutions and agencies. As Luke Cooper puts it, economic and social turmoil are “Ukraine’s critical downstream risk”.

***

Thank you for reading Chartbook Newsletter. It is rewarding to write. I love sending it out for free to readers around the world. But it takes a lot of work. What sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters and receive the full Top Links emails several times per week, click here:

March 24, 2023

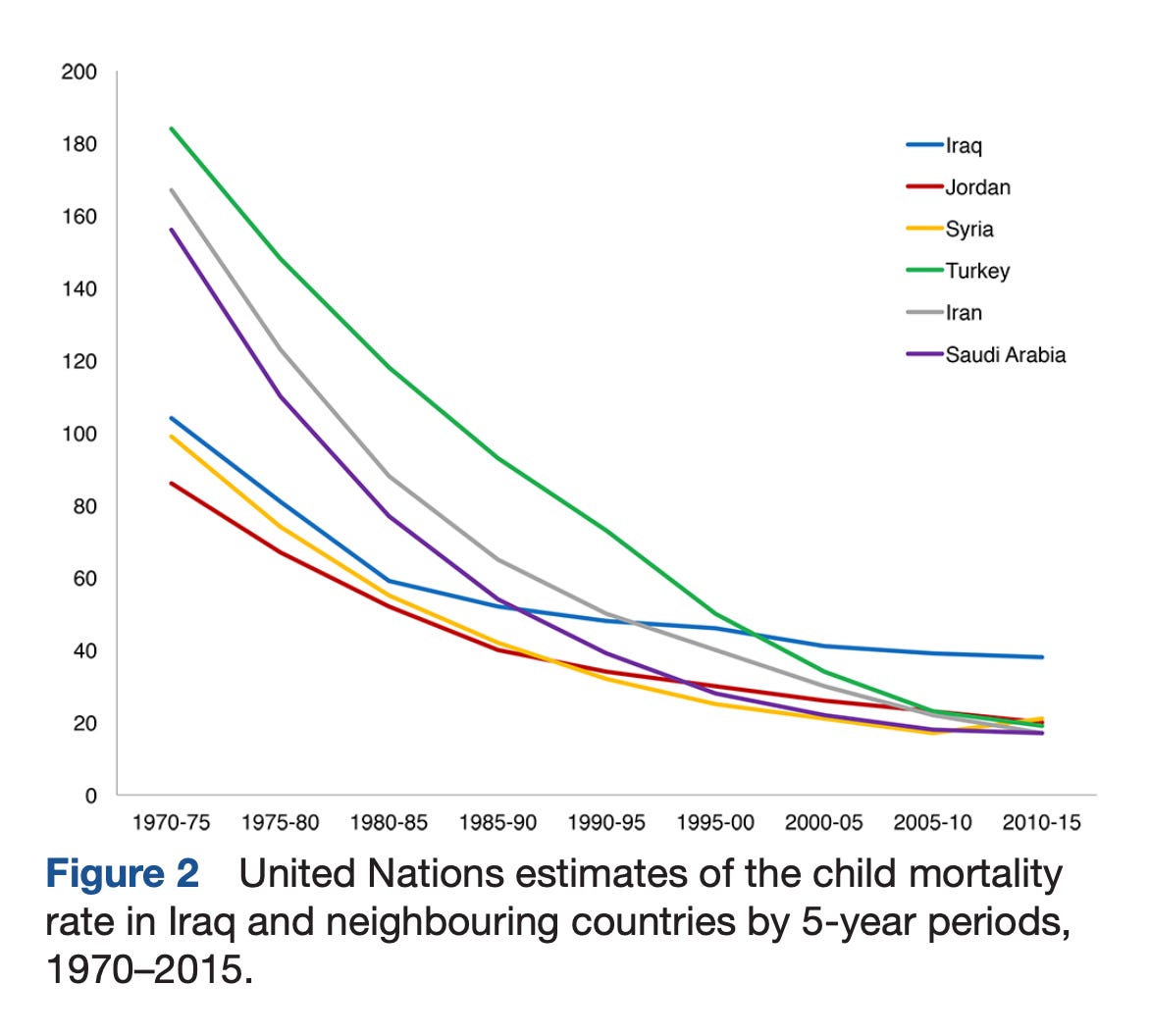

Chartbook 204: Iraq’s economic impasse twenty years after the invasion.

The 20th anniversary of the disastrous invasion of Iraq by the US-UK coalition demands a reckoning. Cameron and I discussed the legacy of the war on the podcast.

Today, Iraq is often described as a state on the brink of disintegration and social and economic disaster. That fragility does not begin with the 2003 invasion, it is a persistent theme in the history of a territory caught between massive power blocs.

For hundreds of years the Ottomans struggled to maintain their grip over the provinces of Mosul, Baghdad and Basra in the face of challenges from the Mamluks. Between 1915 and 1917 the forces of the British empire took three years to take Baghdad in the bloody Mesopotamian campaign. The Iraqi state created in 1921 under the British mandate struggled, from the start, to impose itself against Kurdish rebellions. In 1941 a pro-German coup, led to a large-scale invasion by allied forces who used Iraq as the base for the occupation of Iran and for defeating Vichy forces in Syria. A giant nationalist uprising against British influence over the country was suppressed in 1948 in the course of the disastrous Arab League campaign against Israel. In the 1950s Baghdad answered Egyptian and Syrian unity with abortive efforts to unify with Kuwait, which left it isolated on all sides. In 1958 a military coup overthrew the Hashemite monarchy and declared a Republic whose political history would henceforth be dominated by various factions of the Baath party. Fighting between Baghdad and Kurdish autonomists continued until the mid 1970s. Saddam Hussein who took power in 1979 not only attacked Iran but escalated the brutal struggle to consolidate Baghdad’s grip on Kurdish and Shia regions of the country.

But, for all this political turmoil, from the 1950s onwards, benefiting from increased oil revenues, Iraq experienced rapid economic, social and cultural development. By the end of the 1980s Iraq was widely seen in the Arab world as a relatively successful oil-fueled developmental state. As a US government report on Iraq put it in June 2003:

In the 1980s, Iraq had one of the Arab world’s most advanced economies. Though buffeted by the strains of the Iran-Iraq war, it had – besides petroleum — a considerable industrial sector, a relatively well-developed transport system, and comparatively good infrastructure. Iraq had a relatively large middle class, per capita income levels comparable to Venezuela, Trinidad or Korea, one of the best educational systems in the Arab world, a well educated population and generally good standards of medical care.

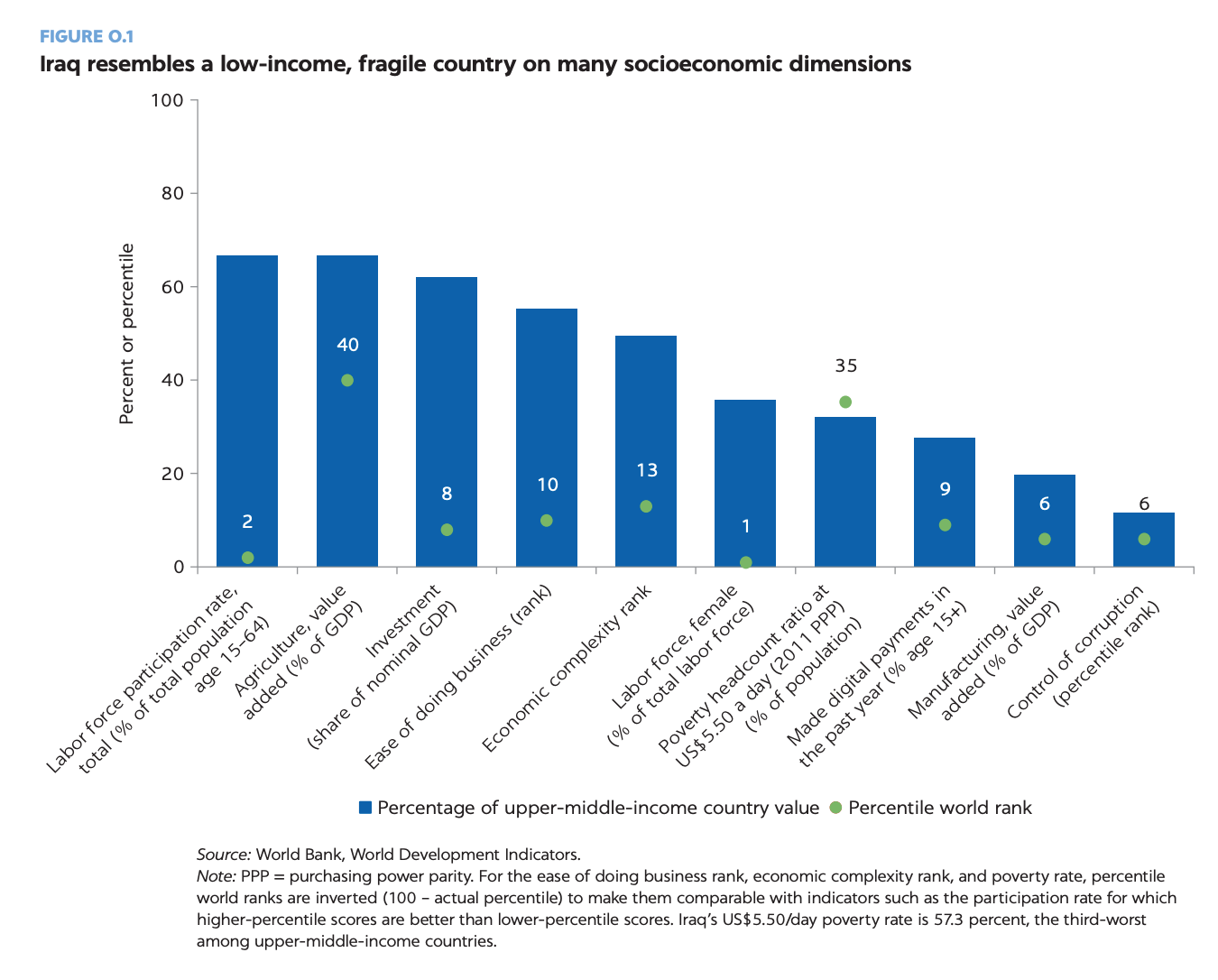

In 1990 that upward-directed trajectory of development was broken. Iraq entered a period of violence and frustrated development that continues down to the present. In 2020 a World Bank report reached the following sobering conclusion:

Although oil wealth has allowed Iraq to obtain upper-middle-income status, in many ways its institutions and socioeconomic outcomes more closely resemble those of a low-income, fragile country. The Iraqi education system once ranked near the top of the Middle East and North Africa (MENA) region, but it now sits near the bottom. Iraq’s rate of participation in the economy is also low, and the country has one of the lowest female labor force participation rates in the world, low levels of human and physical capital, and deteriorating business conditions. Iraq also has one of the highest poverty rates among upper-middle-income countries.

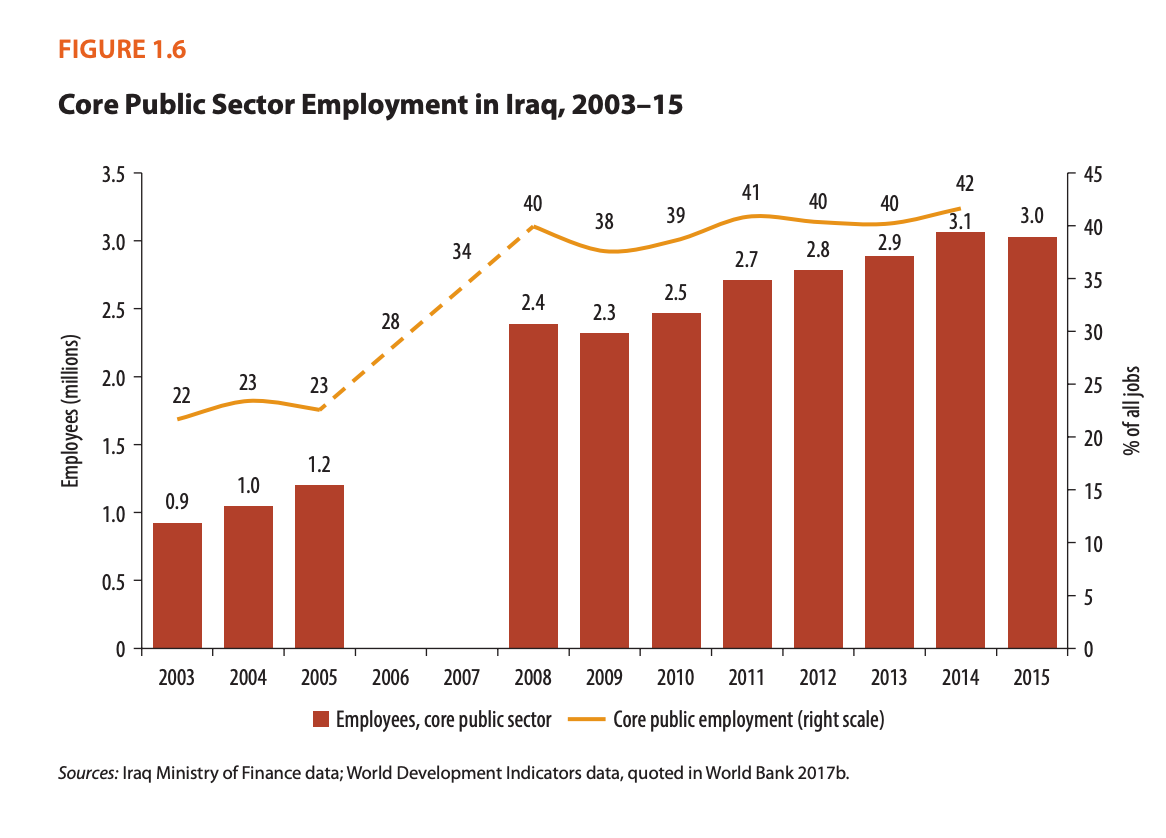

Understanding this trajectory – from modernization champion to fragile low-income society – is crucial to plumbing the depths of the Iraqi crisis. It is all the more striking because Iraq, as a major oil exporter should by-rights have profited from the oil boom of the 2000s and 2010s to catapult itself squarely into the higher middle income bracket of global development. It was not to be. Instead Iraq’s development was derailed by war, sanctions, invasion and civil war. And Iraq’s crisis has spilled over its borders and merged with a polycrisis afflicting Western Asia.

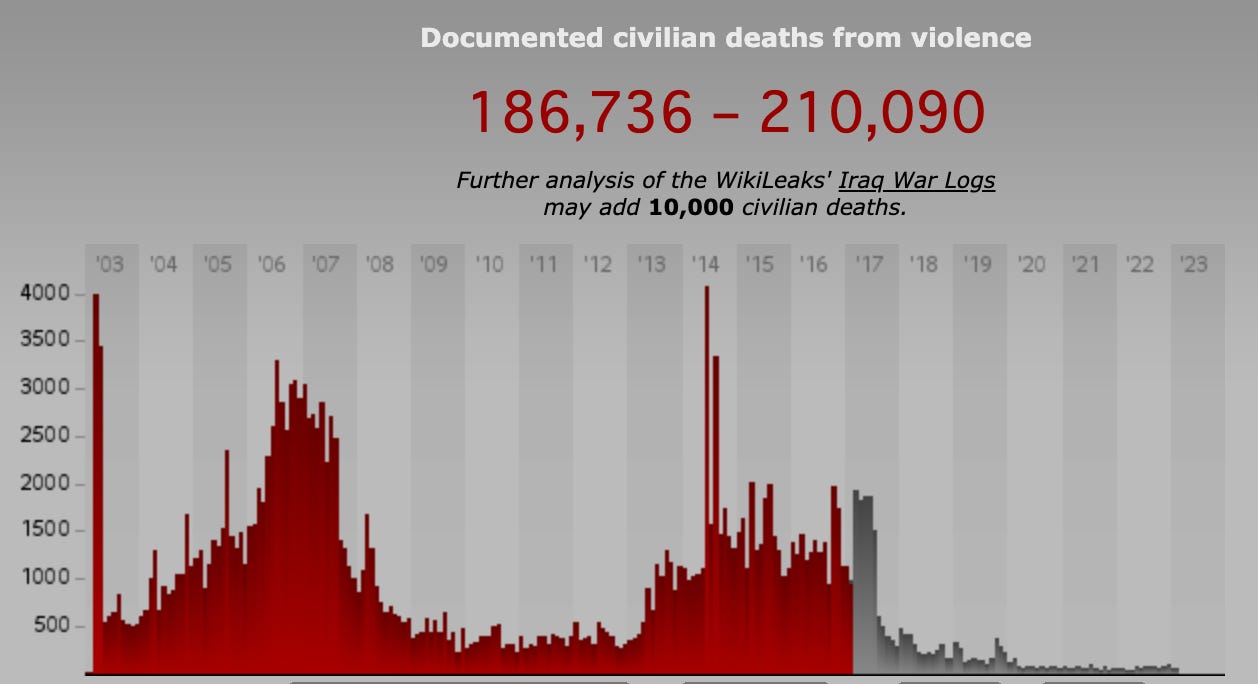

Saddam’s attack on Iran in the early 1980s indicated his violent ambition, but as far as Iraq’s economy is concerned it was the invasion of Kuwait in August 1990 and the US-led riposte that delivered the first devastating shock. After a measure of recovery under the more relaxed sanctions regime of the late 1990s, the invasion of 2003 delivered another devastating blow to the economy and unleashed a phase of insurgency, civil war and state disintegration. This is best tracked by the bloody graph of civilian casualties.

Source: Iraq Body Count

This the narrowest measure of casualties: only those deaths attributable directly to violence. Broader estimates of excess deaths add hundreds of thousands to the death toll.

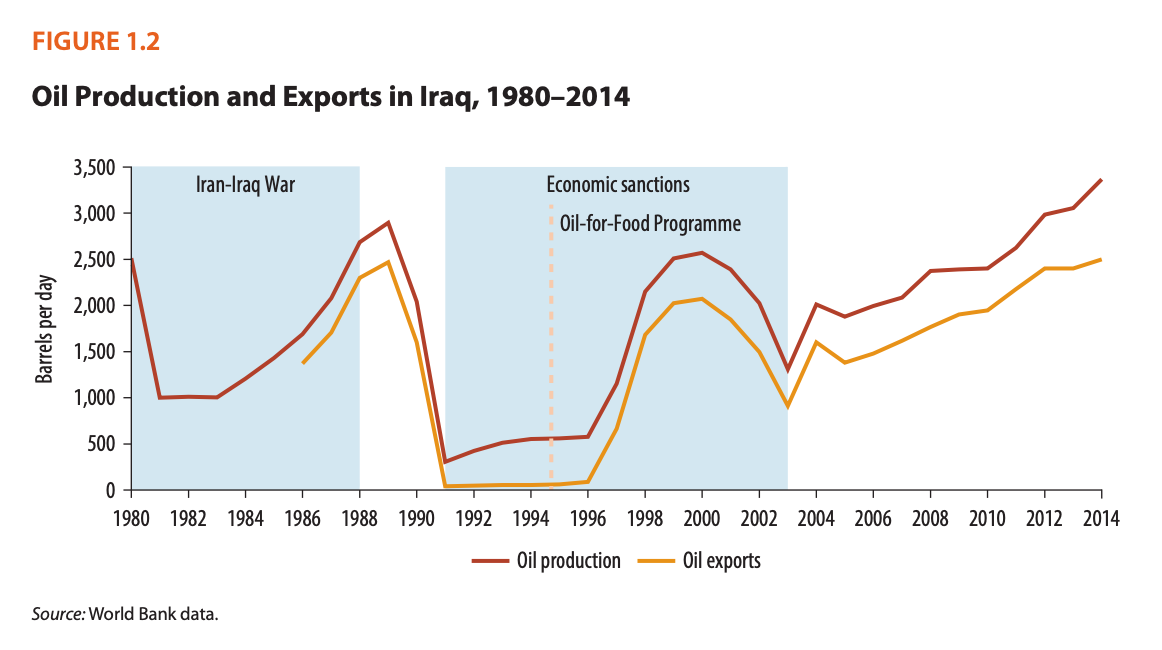

Amidst insecurity and chaos, Iraq was unable to profit substantially from the spectacular oil boom of the early 2000s. Despite sky-high prices it was only after 2010 that Iraq’s oil production exceeded the peaks of 1989 and 2002.

World Bank 2022

And the stabilization after 2010 was to prove temporary. In 2014 two shocks came together. Oil prices plunged, just as the ultra-extremist Daesh movement swept across Northern Iraq and Syria. Having dissolved Saddam’s army, America had been forced to spend $20bn to rebuild Iraq’s security forces. But the demoralized troops proved no match for the radical insurgents. ISIS took control of a huge swath of territory, forcing the mobilization of an international coalition. Tellingly this was anchored not only on a rebuilt Iraqi security forces, but on the autonomous region of Iraqi Kurdistan. Not until 2017 was the ISIS threat brought under control.

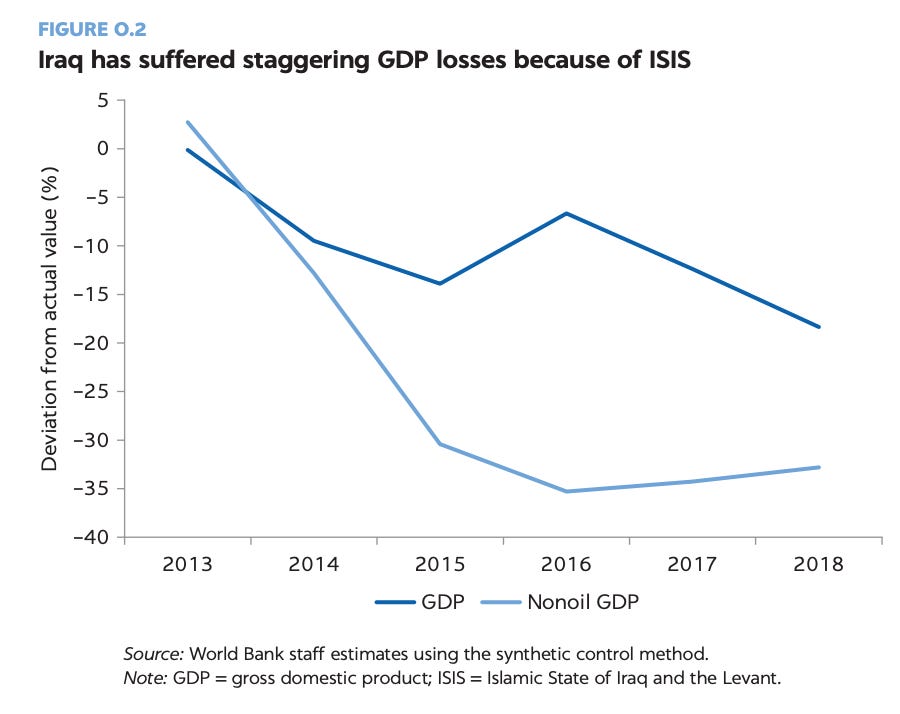

The war against ISIS came at a huge price. In the worst months of 2014 civilian casualties were greater than in 2003 or at the time of the civil war. The economic damage was no less severe. As the World Bank comments:

The country’s per capita GDP is about 18–21 percent lower in 2018 than it would have been if not for the conflict beginning in 2014. In particular, although Iraq’s oil GDP grew steadily during the conflict, the country’s non-oil GDP is estimated to be about 33 percent lower in 2018 than it would have been without the conflict (figure O.2) and has fallen below its peers (figure O.3).

The defeat of ISIS has brought a degree of calm. In terms of military conflict, Iraq is now more quiet than it has been at any time since 2003. This yields a significant peace dividend for economy and society. But the cumulative damage is dramatic. On a purchasing power parity basis, GDP per capita in Iraq today is barely higher than it was in 2003.