Adam Tooze's Blog, page 12

October 21, 2022

Ones & Tooze: Liz Truss, Halloween, and Listener Questions

This week on the show, Cameron and Adam discuss Liz Truss’s resignation, and the economics of Halloween. They also address listener questions.

Find more episodes and subscribe at Foreign Policy

October 17, 2022

Bruno Latour and the philosophy of life: For the late French intellectual in an age of ecological crisis it was crucial to understand ourselves as rooted beings.

As Bruno Latour confided to Le Monde earlier this year in one of his final interviews, philosophy was his great intellectual love. But across his long and immensely fertile intellectual life, Latour pursued that love by way of practically every other form of knowledge and pursuit – sociology, anthropology, science, history, environmentalism, political theory, the visual arts, theatre and fiction. In this way he was, above all, a philosopher of life in the comprehensive German sense of Lebensphilosophie.

Lebensphilosophie, whose leading exponents included figures such as Friedrich Nietzsche and Martin Heidegger, enjoyed its intellectual heyday between the 1870s and the 1930s. It was a project that sought to make sense of the dramatic development of modern science and the way it invaded every facet of life. In the process, it relentlessly questioned distinctions between the subject and knowledge and the foundations of metaphysics. It spilled over into the sociology of a Max Weber or the Marxism of a György Lukács. In France, writer-thinkers such as Charles Péguy or Henri Bergson might be counted as advocates of the new philosophy. Their heirs were the existentialists of the 1940s and 1950s. In the Anglophone world, one might think of the American pragmatists, William James and John Dewey, the Bloomsbury group and John Maynard Keynes.

A century later, the project of a “philosophy of life” acquired new urgency for Latour in an age of ecological crisis when it became crucial to understand ourselves not as free-floating knowing and producing subjects, but as rooted, or “landed”, beings living alongside others with all the limits, entanglements and potentials that entailed.

The heretical positions on the status of scientific knowledge for which Latour became notorious for some, are best understood as attempts to place knowledge and truth claims back in the midst of life. In a 2004 essay entitled “How to Talk About the Body?” he imagined a dialogue between a knowing subject as imagined by a naive epistemology and a Latourian subject:

“‘Ah’, sighs the traditional subject [as imagined by simplistic epistemologies], ‘if only I could extract myself from this narrow-minded body and roam through the cosmos, unfettered by any instrument, I would see the world as it is, without words, without models, without controversies, silent and contemplative’; ‘Really?’ replies the articulated body [the Latourian body which recognises its relationship to the world and knowledge about it as active and relational?] with some benign surprise, ‘why do you wish to be dead? For myself, I want to be alive and thus I want more words, more controversies, more artificial settings, more instruments, so as to become sensitive to even more differences. My kingdom for a more embodied body!’”

Read the full article at The New Statesman.

Chartbook #162 In Memoriam: Bruno Latour

I fell under the sway of Bruno Latour in the early 1990s when I was a grad student at the LSE and I have remained under the influence of his thought ever since.

As much as I describe myself as a Keynesian or “left liberal”, I should probably add that I am a Latourian left liberal.

To be asked to write in Bruno Latour’s memory came as a shock. Not as a surprise – he had been gravely ill for a while – but as a shock.

First I needed arms around me.

Then I needed an idea. And that came with a tweet thread from Pierre Charbonnier, which ended with the appeal that after Latour’s passing our ambition should be to continue his project by continuing to press his questions on truth, modernity and ecology.

Il faut aussi se souvenir que Latour pensait toujours avec des amis, que l’aventure intellectuelle est une aventure collective, et gaie.

— Pierre Charbonnier (@picharbonnier) October 9, 2022

Bye l’ami. pic.twitter.com/VZxMwoE6ZJ

Thinking on Pierre’s appeal, what I realized I wanted to do was not so much to think forward from Latour’s death, but to linger with this event of his death and Latour’s own thought about life and death.

What did Latour write about death and life? The more I thought about it, the more redundant I realized the question to be. In a sense Latour’s entire body of work was about life. It was a Lebensphilosophie. But amidst the abundance of his writing I found the prompt I needed in a 2004 essay on “How to Talk About the Body? The Normative Dimension of Science Studies”.

You can read the resulting essay in the New Statesman.

By way of apology and with no false modesty I should add that this is not a piece of Latour scholarship. It is rather a personal response, by way of his work, to the crisis of his death.

Thinking about the piece took me back to a dinner with Latour in Paris in 2019 only weeks after Notre-Dame burned.

It took me back to our extended conversation about Carl Schmitt.

That conversation began in New Haven 2014 when I had the honor of introducing Latour as the Tanner lecturer.

In preparation for Latour’s visit, the philosophy of history reading group that I helped to organize at Yale had spent a term devoted to Latour’s magnum opus, An Inquiry into Modes of Existence.

In edited form, my introductory remarks for Latour’s lectures were these:

****

Words of Welcome for Bruno Latour

Tanner Lectures, Yale 26 March 2014

Adam Tooze

Stumbling into the second half of term last week, an announcement flashed up on my computer screen: “Award-winning sociologist to give Tanner lectures.” I must admit that it took me a few beats to realize that the email was advertising this wonderful occasion tonight.

It is not that our guest this evening is not award-winning. Of course he is. He has won many prizes. The Bernal prize in 1992, the Legion d’honneur, the Holberg memorial prize, to name just a few.

Nor is it that Bruno Latour could not claim to be a sociologist. In the breakthrough phase of his career he headed the lab at the École des Mines for the sociology of innovation.

But there was, nevertheless, in reading this email advertisement a moment of thought-provoking incomprehension, one of those category mistakes that are the driving motor of Bruno Latour’s most recent book An Inquiry into Modes of Existence (2012 French, 2013 English translation). The incomprehension arises from the yawning gap between what Bruno Latour’s writing has meant to us these last decades and that cookie cutter category of “award-winning sociologist”.

This evening, however, it is not the poor souls in Yale’s public affairs department who face the challenge of finding the right words with which to introduce our speaker, but me. It is not an easy thing to do. It is not easy because Bruno Latour’s influence has been so ramified. Because he is so generously prolific. There are so many “Latours”. But, above all, because if anyone has challenged us to think through the consequences of “fixing” or labelling language, it is Latour. Let me just take a recent quote :

“As I discovered many years ago in this very same laboratory at Salk, what makes scientific accounts so well suited for a semiotic study is that there is no other way to define the characters of the agents they mobilize but via the ACTIONS through which they have to be SLOWLY captured. Contrary to generals like Kutuzov (a references to Latour’s beloved Tolstoy, AT) and rivers like the Mississippi (as understood and fixed by the hydrological engineers), the competences of those agents discerned in laboratory experiments —that is, what they ARE—those competences come to be defined only long after by their performances—that is, by what they DO. … the dumbest of reader is able to imagine, no matter how vaguely, a Russian marshal or the Mississippi River by using his or her prior knowledge. But that’s not the case for as yet ill-defined hormone release factors. Since there is no prior knowledge, every trait has to be generated from some experiment.”

If you substitute for Russian Marshal “award winning sociologist” and for “ill-defined hormone release factors” the intellectual life force that is Bruno Latour , then you have a neat illustration of my problem in introducing our speaker tonight. Fix him and you lose him. Not that Bruno Latour is an enemy of all fixing. He is no luddite breaker of black boxes. No one has helped us more to understand the liberating power of such devices. As he will show in the lectures to come, there are two routes – one through semiotic analysis the other ontological – by which one might unpack the ways in which we institute the bifurcation between “what is animated and what is deanimated.” But let us not kid ourselves, when Bruno Latour gets translated into an “award-winning sociologist” something happens, a closing, a fixing, the rendering of something from a live force, an agent into a mere means.

So let us ask instead, what are the specific forces that keep him in motion? What does this agent, Bruno Latour, do? What effect does he generate? What drives his performance? Specifically in the last few decades? Because with a thinker as dynamic as Bruno Latour you have to run to keep up!

(1)

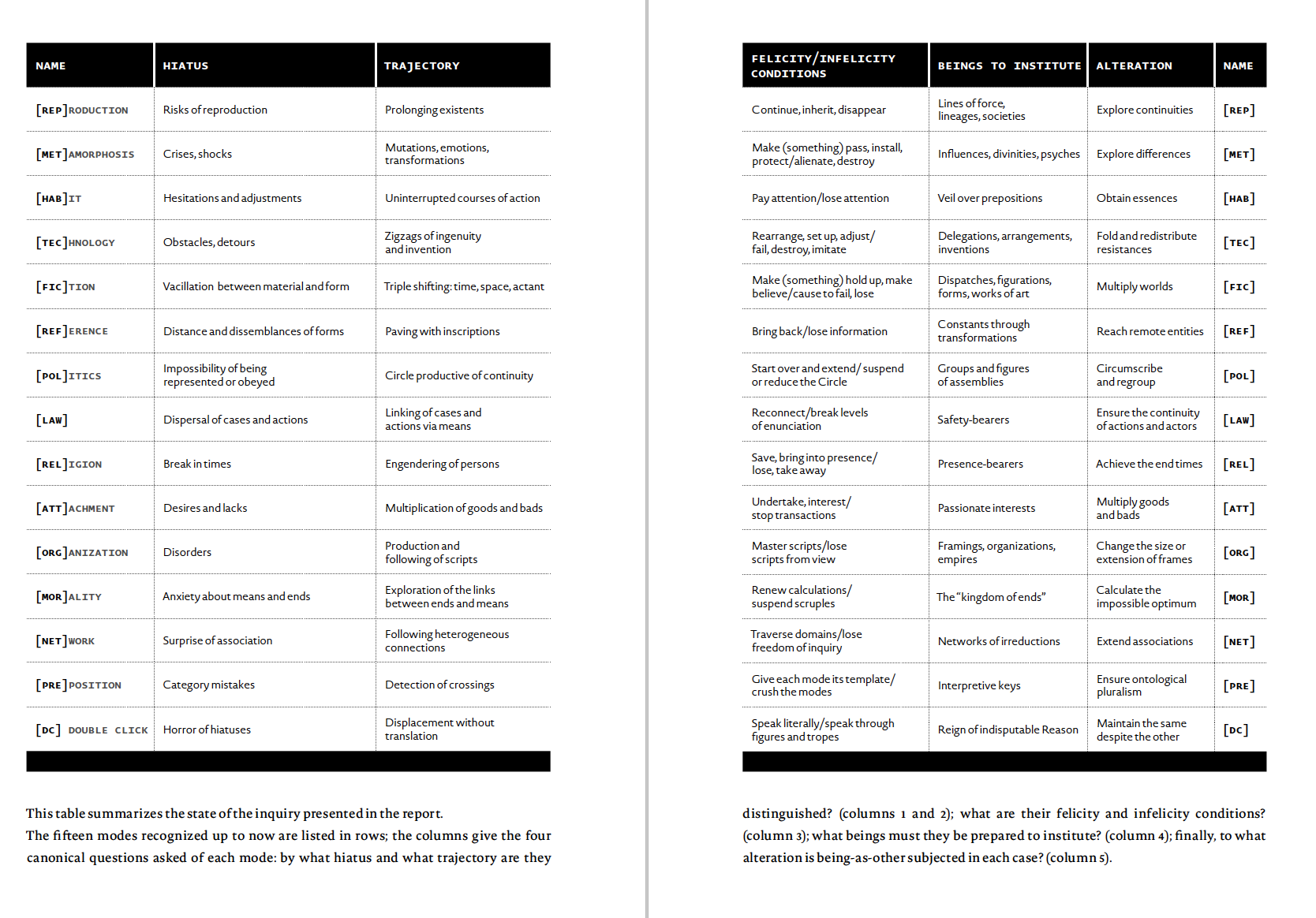

The most dramatic vector of this as yet unfixable agency is certainly the “great reveal”. Bruno Latour has gradually revealed to us and clearly laid out in his latest book that the “science studies Bruno Latour” of the 1970s and 1980s was always actually located within a vastly more capacious philosophical project that can be traced back to that protean moment in French thought in the late 1960s and early 1970s, the moment of Deleuze’s Difference and Repetition, the moment when the mid-career Foucault set out his differences with Derrida on the battlefield between Socrates and the sophists, in the first of the College de France lectures. From this moment Latour like some of his contemporaries, notably Bourdieu, unfolded a truly capacious project that was animated in Latour’s case by the most fundamental questions in ontology and drew above all on the inspiration of Charles Peguy’s early-twentieth-century thought. There were flashes of this in Irreductions the second part of the Pasteurization of France, but it now bursts fully into the sunlight in An Inquiry into Modes of Existence.

Latour’s enquiry into regimes of truth began with his Phd on biblical exegesis, by way of his experiences as a peace corps conscript in Africa and apprentice anthropologist to laboratory studies. Hermeneutics, anthropology and the lab formed a triangle. But Latour has now revealed to us that he always intended to move even further afield, beyond the laboratory to religion and further afield. The luxuriant proliferation of modes of existence, embracing, jostling in AIME is the working through of that original ambition. The number of these modes currently stands at 15, though Latour has suggested that this is a number contingent on the history of modernity and further to be elaborated in the collective project attached to the book.

The floor is open for more suggestions, to add further modes of existence to the list. The making of the list is in itself an irresistible impulse to creativity.

(2)

With this widening of scope has come not just a proliferation of fields, but also a new sense of emphasis. What has moved to the center is economics. Already hinted at in those passages on centers of calculation in Science in Action, but now identified as a central dynamic of the modern, threatening to overshadow all others. To which Latour characteristically responds not with defeatism or rejection, but with a dissection of the compacted incoherence of the field that we call the economic, into three separate realms of passionate interest, organization and accounting and equivalence-making.

(3)

And this focus on the economy gives us a third dynamic. Compounding the move to depth, to ontology, and the move to proliferation to modes of existence, we have a new burst of critical energy, how else to call it? I hesitate only because Bruno Latour is well known as a critic of facile critique. People have long struggled to place him. Is he a radical, a conservative? Perhaps what we realize now is that he is amongst our most articulate, most sophisticated defenders of liberalism. The re-appropriation of that old language, a characteristic move for Latour, is itself part of a constructive reconstruction. Liberal pluralism, he has announced, must be defended against its true antithesis, neoliberalism.

(4)

And Latour as critic is neither measured nor leisurely because in his recent work there is a fourth impulse at work: historical urgency. The advent of the Anthropocene has given a spectacular new urgency both to the philosophical project initiated in the 1970s and the day to day clinch with neoliberalism. The speed with which the environmental condition, the new sovereign, Gaia, has swept up on us, is one of its most awesome features. We are faced with a truly grim prospect: “No time for commerce. No time for solemn oaths.” Latour remarks, “Contrary to Hobbes’s scheme, the “state of nature” seems to have a dangerous tendency to follow, and not to precede or to accompany, the time of the civil compact. to talk of constitutions may come to seem like a strange form of nostalgia”.

What is Latour’s answer? A revival of the agora, a re-appreciation of politics and the political. Latour advocates a turn to Carl Schmitt, but shorn of the ruinous Wagnerian dramaturgy. Latour calls for a reexamination of the processes through which equivalences are made, not by some Smithian “invisible hand”, but through interested energized relations between actors of all kinds. And above all he demands a willingness to follow this through to its logical conclusion, a willingness to pose the question of the optimum, the question of the good, a moral question, understood not in Kantian terms as divorced from the world and its impulses, but on the contrary as inextricably bound up with it. This culminates in the extraordinary claim that the moral is a property of the world, or it is not at all. And a new definition also of the bad. Because it also in the world that the malign inversions manifest themselves that threaten any prospect of agency.

How then to respond? Characteristically, Bruno Latour is not afraid of heading back to the future. If the grandeur of constitutions eludes us at this moment of crisis, what option do we have? Latour’s answer is to take a stand on the institutions that give us some grip on reality. “Rebuild the institutions. To institute the values which we think it’s important to have.” And amongst those institutions, our own, the University is strategic. It is on the fault line within the University between the humanities and the sciences, facing as we now do common enemies in the perverse demands for financial and output accountability, that Bruno Latour will begin his talks this evening. I can’t wait. To have him with us at such a spectacularly fertile moment in his long career is a stroke of good fortune almost too sweet to believe.

****

Subscribe to Chartbook

Subscribe to ChartbookBy Adam Tooze · Thousands of paid subscribers

A newsletter on economics, geopolitics and history from Adam Tooze. More substantial than the twitter feed. More freewheeling than what you might read from me in FT, Foreign Policy, New Statesman.

October 15, 2022

Chartbook #161 Iran’s contested demographic revolution.

Iran is currently convulsed by the fourth wave of mass protests to shake the country since the student uprising of 1999 – the others being 2009 and 2017/2019. Making sense of the drivers of this upheaval is crucial if we are to understand the unfolding poly-crisis in West Asia.

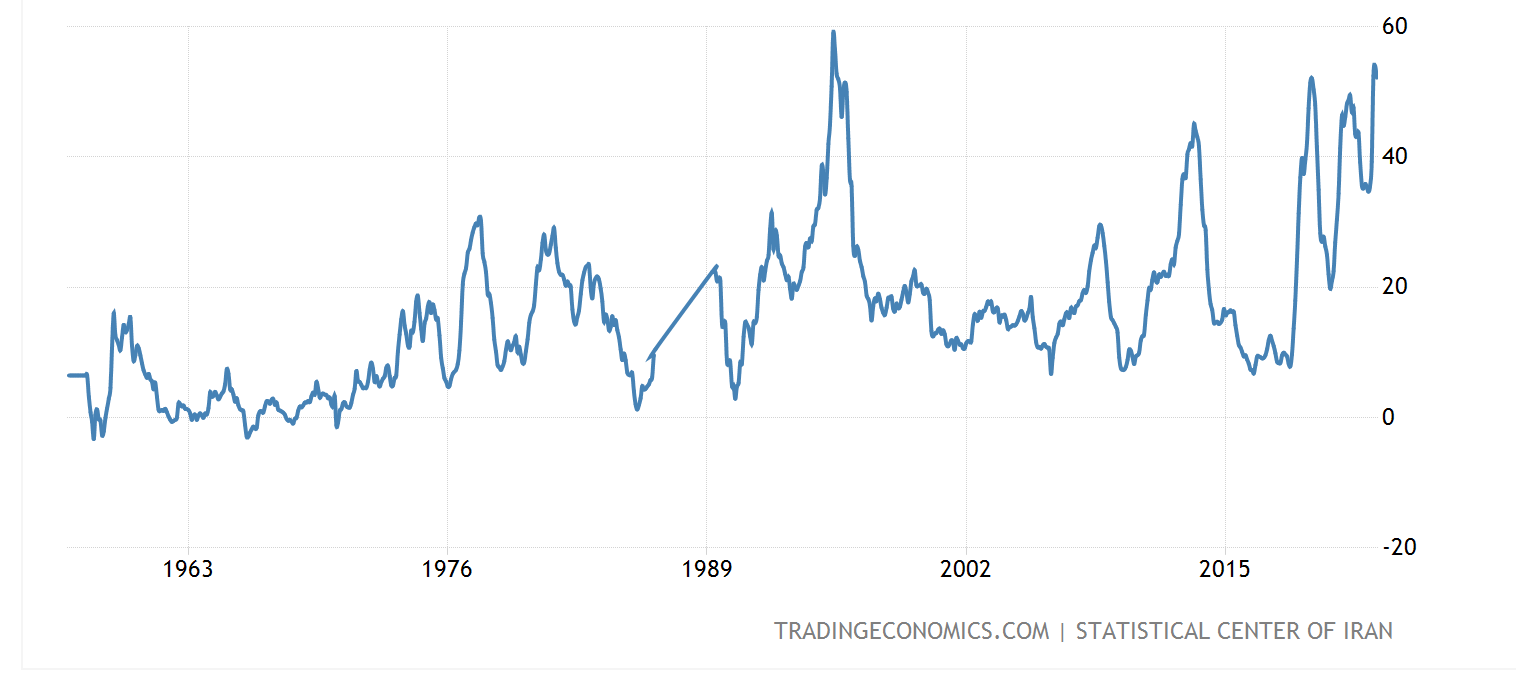

In the case of each protest wave, there have been specific triggers. In the Green revolution of 2009 the issue were the rigged elections. Today, the violent and degrading treatment of Iranian women by the regime’s morality police is in the forefront. In the background are the economic problems of the regime exacerbated by US sanctions. These first triggered protests in 2017 and 2019. Today inflation is running close to 50 percent, which foments a continuous rumble of protests and strikes by workers of all kinds.

Iran’s inflation rate

Source: Trading Economics

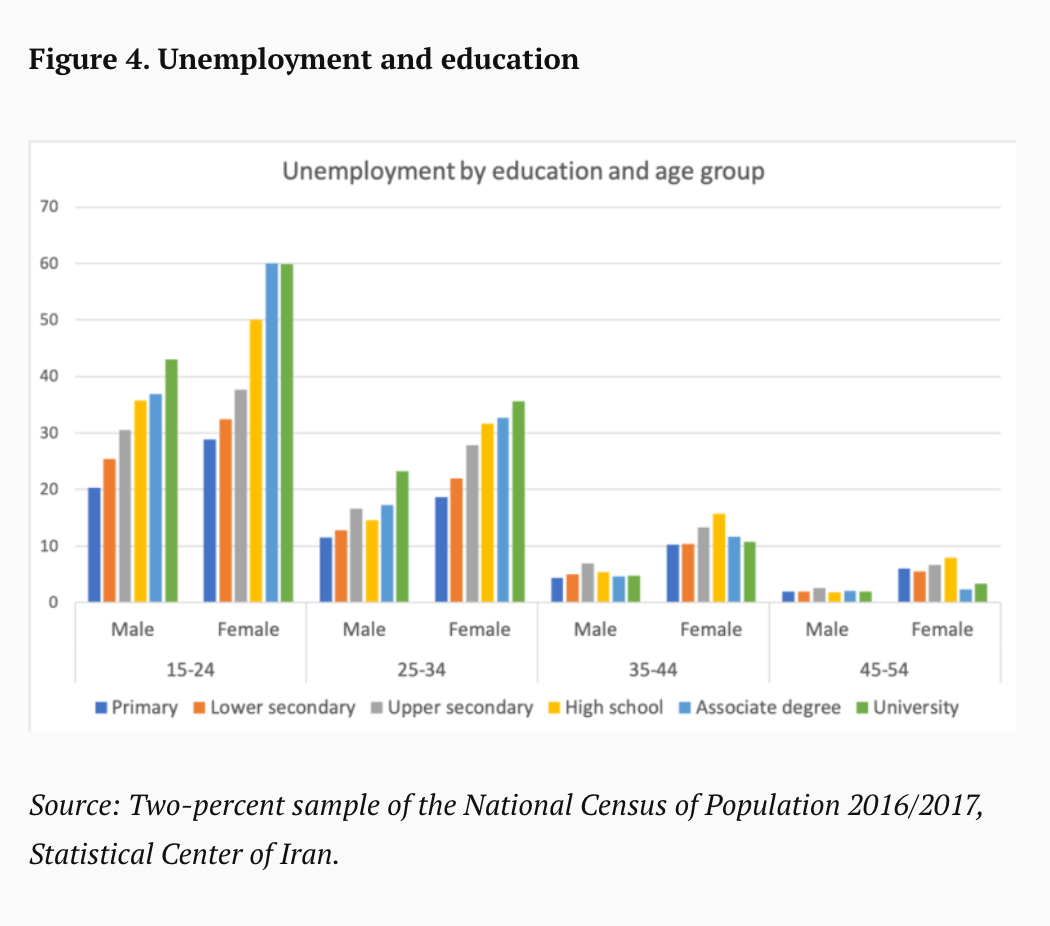

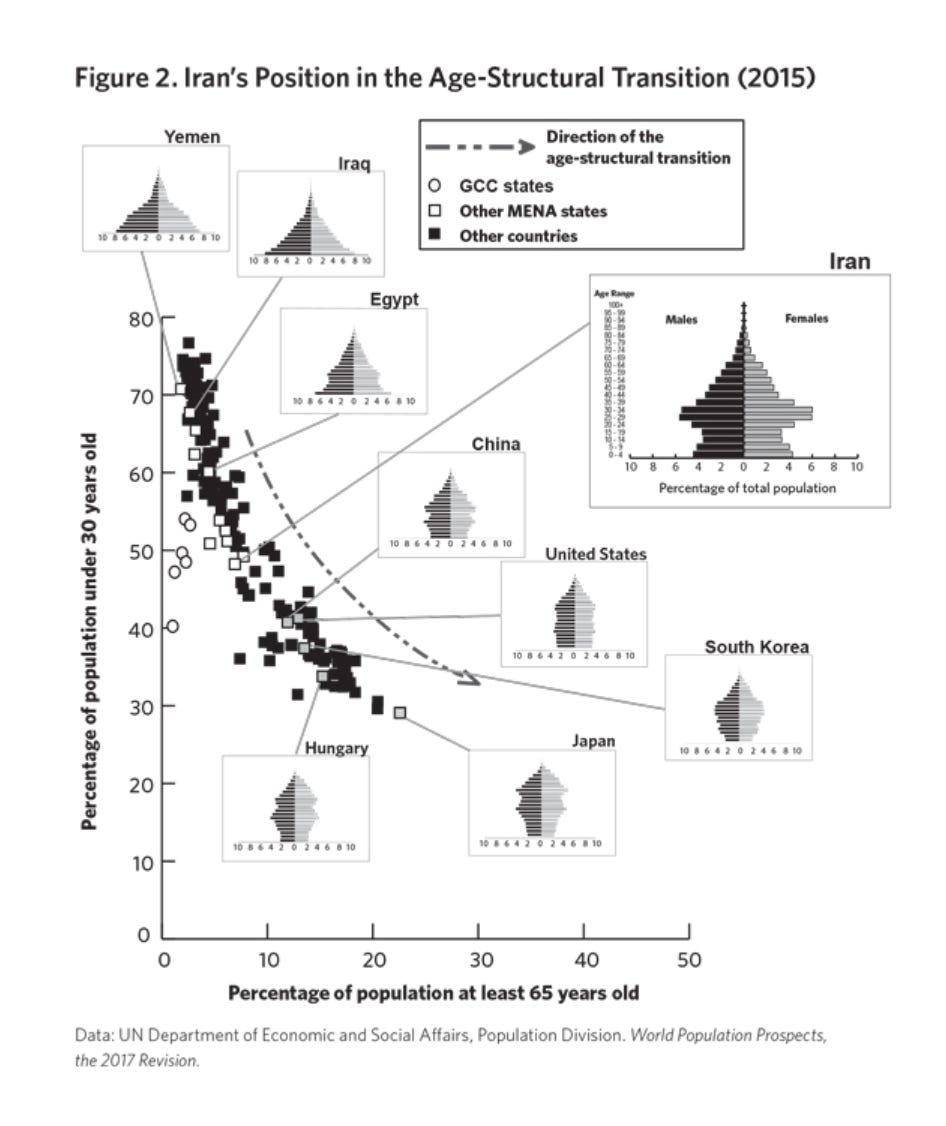

It is tempting also to think of another common factor that unites these protests. Particularly in 2009 Iran was singled out as a locus classicus of the “youth bulge” diagnosis, that then served as a template for making sense of the 2011 Arab Spring. Superficially, it is a compelling analysis. Too many young people, with too much education and not enough jobs make for an explosive mixture. Data for unemployment and education in Iran for 2016/7 show unemployment rising with education up to the age of 34. Rates of unemployment amongst highly educated women run to staggering levels. Clearly this is still a major force in play.

Source: Brookings

The “youth bulge” narrative is where both Cameron Abadi and I started out, when we set out to record the latest episode of Ones and Tooze featuring a segment on Iran. But then I started reading into the subject and found a story that truly surprised me.

Check out the podcast here:

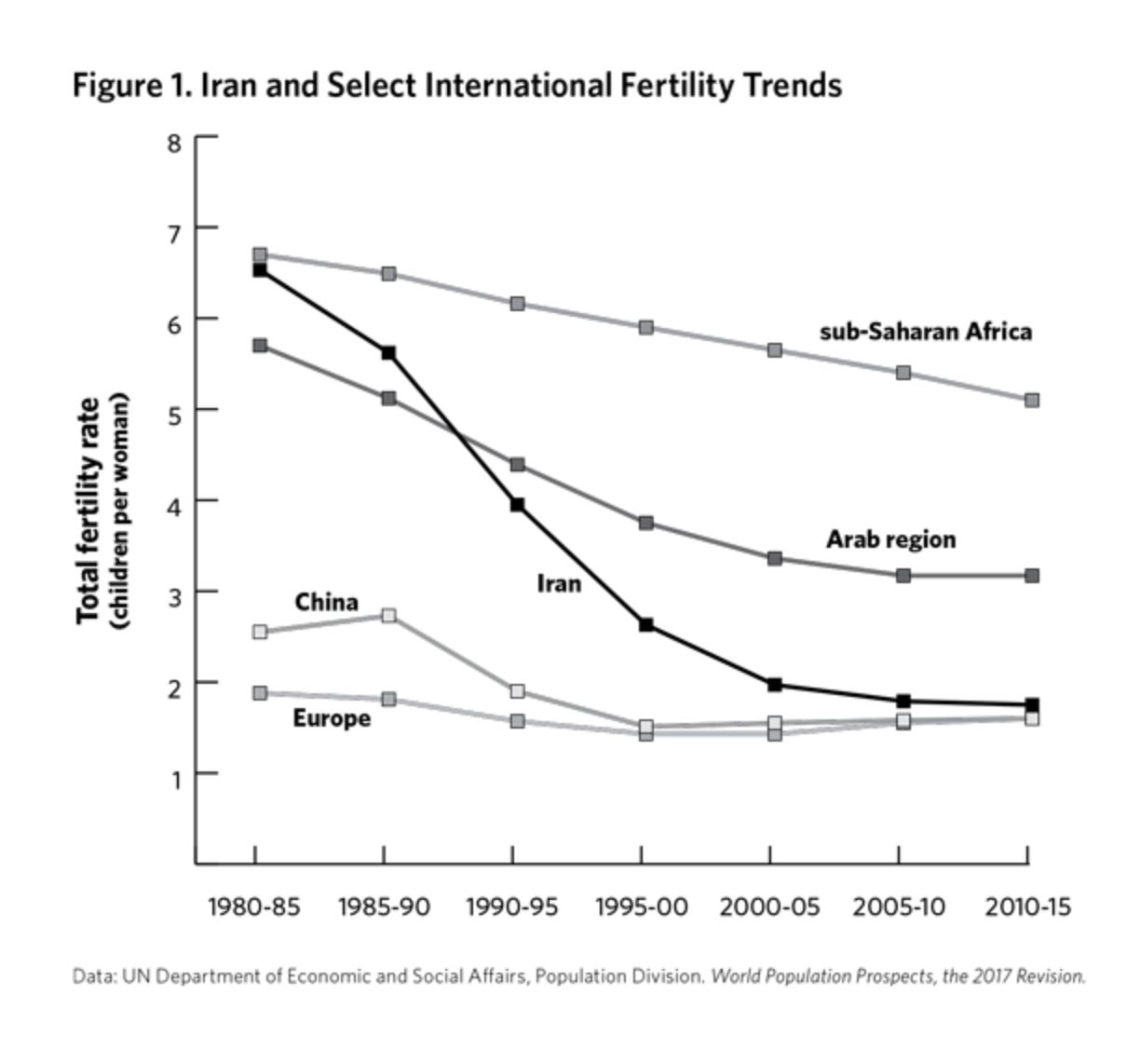

It turns out that though the youth “bulge story” fits well for Iranian society in the late 1990s and early 2000s, Iran is actually in the grips of the dramatic transition ever recorded in demographic history. Between the 1980s and the 2010s Iranian women reduced the rate at which they had children from 6.5 to 2.5, faster than the pace of the one child policy in China. And they did so with the regime’s support.

Demography is thus one more zone in which the contradictions of Iran’s gender regime come to the fore. Iran is a society in which maternal mortality is lower than in the US (admittedly not the lowest bar), but only 5 percent of seats in parliament are taken by women. It is a country in which women in university outnumber males, and in which attainment in secondary education extends to over 70 percent of women over 25 (versus 76 percent for men). But it also a society in which female participation in the formal labour market runs to only 14 percent, by the latest UN count, half the rate reported by Saudi Arabia and on a par with Afghanistan before the Taliban returned to power. On top of all this it is society, which went through the fastest demographic transition on record, which the regime is now seeking to undo.

****

The Shah of course boasted of his program of modernization. His family planning program established in 1966 was under the patronage of no lesser personage than Ashraf Pahlavi, the Shah’s sister. It attracted extensive funding from USAID, but it was largely ineffective in changing behavior. In that respect it had much in common with the Shah’s broader development measures which went skin-deep at best.

In the 1980s under the pressure of the Iran-Iraq war, the initial rhetoric of the Islamic Republic was pronatalist. Ayatollah Khomeini called for e a “20 million man army” and state child subsidies boosted the incomes of the poorest households. It was in the mid 1980s at the highpoint of the war that Iranian fertility reached its peak at over 6.5 children per woman.

This was not sustainable and by the late 1980s contraceptive use was spreading not just in Iran’s cities but in the countryside as well. As Akbar Aghajanian and Amir H Mehryar report in their fascinating 2005 account in the International Journal of Sociology of the Family

In February 1988, Prime Minister Moosavi sent a secret circular to all ministries and government departments asking them to carefully consider the implications of the high rate of population growth revealed by the 1986 census. Then in March 1988 a committee was organized in the Ministry of Plan and Budget, consisting mostly of the technical staff of that ministry and a few academic demographers, to prepare for organization of a population seminar. To facilitate the work of the conference committee, the Prime Minister issued a memorandum to all government ministries declaring that the government was “reconsidering the issue of population growth”. A highly publicized three-day “Population and Development Seminar” was held in Mashad city in September 1988. It was opened with a special message from the Prime Minister. The Ministers of Plan and Budget and Health presented detailed analyses of the implications of unchecked population growth for the socioeconomic development of the country as well as the health and welfare of its citizens.

As Richard Cincotta and Karim Sadjapour spell out in an illuminating Carnegie report, senior regime officials came to see this rapid demographic growth as a ticking time-bomb. The Islamic Republic made extensive welfare and development commitments to its citizens. And in the wake of the war under the presidency of Hashemi Rafsanjani (1989–1997), these pro-poor policies bore dramatic fruit. With the war crisis overcome, over the following decades the material circumstances of life for ordinary Iranians were transformed.

What worried the officials in the Ministry of Economic Affairs and Finance was the cost of these policies in light of Iran’s explosive demographic growth. In collaboration with officials from the public health sector they began urging a deliberate policy of population restriction. And in December 1989 this was adopted as a three-pronged strategy (1) to encourage a spacing of 3 to 4 years between pregnancies; (2) to discourage pregnancy for women aged below 18 and above 35 years; and (3) to limit family size to 3 children. By the early 1990s population restriction had won the argument. Along with electricity and clean water supplies, Iran’s Islamic Republic became a purveyor of free birth-control and family planning advice.

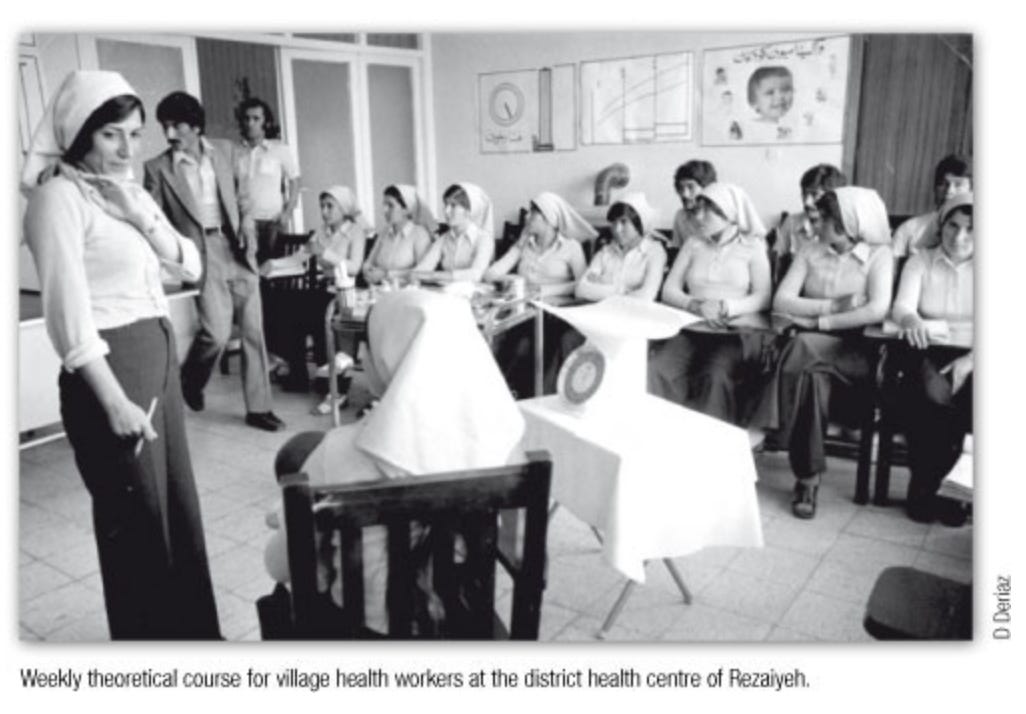

In a shockingly short space of time Iranian men and women embraced a radically new demographic model. This was assisted by state-run voluntary family planning services and counseling. In this regard at least the Shah’s program bore late fruit in that many of the public health technicians and physicians who staffed the Republic’s new birth-control army. received their training before 1979. On the ground the program was backed by local “health houses,” staffed principally by trained female nurses.

Source: WHO

In the poorer urban areas, state-subsidized clinics, pharmacies and doctor’s offices took the lead. By 2000, a remarkable 90 percent of Iran’s families lived within 2 kilometers of a health clinic or family planning delivery unit, with mobile units covering remoter rural areas. By the early 2000s 62 percent of married Iranian women of childbearing age were using modern contraception and Iran was the only Islamic country to have its own production capacity for condoms.

The initial target for the program was to to reduce the Total Fertility Rate to 4 children per woman by 2011. In fact, Iran’s fertility crashed to replacement level of just over 2 children per woman already by 2005 at the end of Mohammad Khatami’s period in office.

This revolutionary transition came as a considerable shock to conservatives within the regime and Khatami’s administration was blamed. Supreme Leader Ayatollah Khamenei denounced “the negative aspects of the Western life style” and with the election of Mahmoud Ahmadinejad as president, the biopolitical stance of the regime abruptly pivoted. Ahmadinejad pilloried family planning as a Western conspiracy and in 2010 he rolled out a program of lavish subsidies for large Iranian families. Ayatollah Ali Khamenei now denounced his governments’ previous population control measures as a “mistake.” In a dramatic declaration of responsibility in 2012 he declared: “Government officials were wrong on this matter, and I, too, had a part. . . . May God and history forgive us.” In 2014 Iran ended free contraception and passed legislation to prohibit vasectomies, enable younger marriages for women, subsidize additional births and curtailed Iran’s unusually progressive pre-marriage education program. It was as part of this same package that women students were also excluded from some professional university majors.

Beyond the struggle over headscarves and other forms of overt discrimination against Iranian women, there is, thus, another battle being waged over the future of Iranian society. It is a struggle conducted in doctors’ offices and in the bedrooms of the country. In combination with the stalled economic development of the period since 2011 it makes for an explosive mixture in which public and private visions of “development” increasingly diverge.

Having unleashed a genuine social revolution, the regime has tried for the last decade to vainly stem the tide. The idea of reversing the demographic transition is most likely hopelessly unrealistic. The most that the regime can presumably hope for is to hold the birth rate above 2 children per woman as opposed to East Asia’s plunge to 1.6. In any event, most credible predictions see Iran’s population stabilizing around 90 million. For the foreseeable future, Teheran would presumably be best-advised to make all it can of the demographic dividend, which the governments of the 1990s and the early 2000s have bestowed on it.

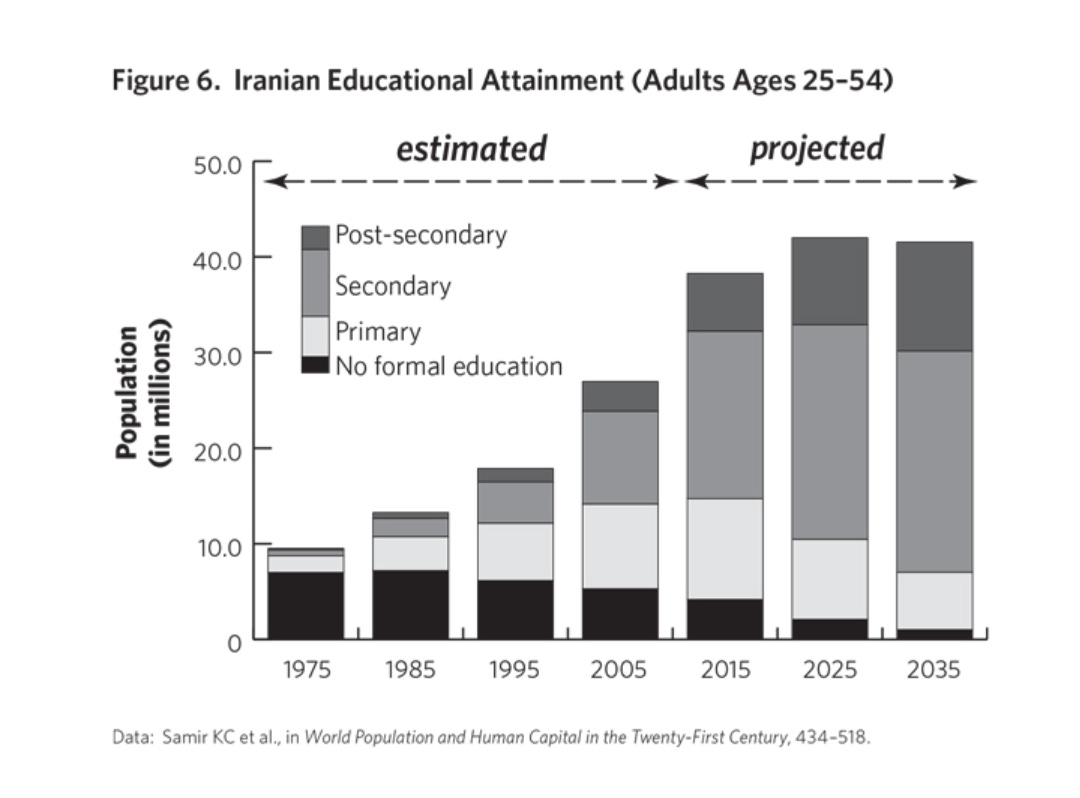

The demographics alone are favorable. The effect is compounded by the rising educational investment per student. In 1975, about 84 percent of women in their prime working ages were without a primary-school education. By the 2010s that proportion had fallen to below 12 percent and was rapidly declining. By 2035, Iran’s workforce educational profile is projected to reach that attained by South Korea in 1995. By 2035 two-thirds or more of Iran’s prime-working-age adults are expected to have an upper secondary or postsecondary education.

The question is whether Teheran can secure the macroeconomic conditions domestically or the international conditions to make the best of this opportunity. Since the 1990s Iran’s median age has surged from round about 19, to more than 31 years of age. That number will only increase in years to come. If it cannot provide growth and employment opportunities, what Teheran will face in years to come is not so much a youth bulge as a national midlife crisis.

*****

I love writing this newsletter. It goes out for free to tens of thousands of readers around the world. But, what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, there are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.Several times per week, as a thank you, all paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

With thanks, AT

To join the supporters club, click here:

October 14, 2022

Jacobin – Inflation and the Cost-of-Living Crisis

On the occasion of Jacobin’s “Inflation” issue release party, Samir Sonti interviewed historian Adam Tooze at the Mayday Space in Brooklyn. This is audio from that recent live conversation. Samir and Adam discuss the causes, threats, and nuances of inflation, as well as ways to combat the cost-of-living crisis in such a way that puts the needs of people before capital.

Get the new “Inflation” issue, and a year-long subscription, for just $20: https://bit.ly/JACOBINRADIO

Chartbook #160 Kindleberger, Mehrling and that Nobel Prize

Newsflash: bank runs can actually happen in market economies and when they do, they do real economic damage. Yup! Economists proved this to their satisfaction in the ‘80s. Not the 1880s, but the 1980s. That was the moment when three intellectual pioneers found a way of fitting banks and bank failures into a workhorse economic model and specified a channel by which the failure of banks raised the cost of credit intermediation. And that matters because, “as we all know”, intermediating between savers and borrowers is what banks do.

I’m not normally into philistinism. I enjoy intellectual activity and game-playing for their own sake. In such an exercise, self-limitation, playing with rules, seeing how far a limited model will go, are all part of the point. But that activity should be pursued with a sense of modesty of purpose and a clear acknowledgement of the limits of the exercise one is engaged in.

What this year’s economics “Nobel” prize does is the opposite. It has the effrontery actually to celebrate one of the weakest dimensions of modern macroeconomic thinking – its extraordinarily limited ability to grasp the macrofinancial instability of modern capitalism. Rather than challenging the dogged refusal of the economics mainstream to take seriously thinkers who face the essential important of finance and its dangers for the modern world head on, it flaunts the tendency of the mainstream to ignore them.

Cameron Abadi and I discuss the award on this week’s Ones and Tooze podcast.

Not only is the award a gratuitous exercise in self congratulation on the part of a discipline that has huge difficulty in shoe-horning reality into its models. It is also untimely.

As Wolfgang Munchau rather unkindly remarked, the prize seems like a retrospective celebration of the heyday of “boomer macro”, the age, in the 1980s, when the new Keynesian synthesis of macroeconomics with microfoundations finally demonstrated to its own satisfaction that bank runs could actually happen and careers could be made, as Ben Bernanke’s was, by demonstrating, by way of a new take on the 1930s Great Depression, that finance might matter for macroeconomics. All this amidst the Volcker shock, the Savings and Loans crisis and the Latin American debt crises … back to the future indeed!

On the podcast I was somewhat unfair in saying that the Prize committee makes no mention of the work of Hyman Minsky. That is not true. The scientific background paper to the award mentions Minsky in a footnote and cites him once en passant in the body of the text. But it does so only to emphasize that Minsky’s thinking was marginal to the mainstream, which insisted in arguing that a debt-deflation could have no macroeconomic impact because its effect, by raising the real value of debts, was merely to redistribute from debtors to creditors. It took Ben Bernanke to establish the real significance of bank failures in a way that the rest of his colleagues could persuade themselves to take seriously.

Along with Minsky, the unapologetic footnote in the Prize committee report also (sort of) cites Fred Mishkin 1978 paper on “Household balance sheets and the Great Depression” (the paper is actually omitted from the bibliography). The committee also mentions Charles P. Kindleberger, who taught at international economics and economic history at MIT.

In 1973 Kindleberger published The World in Depression 1929–39 in which he gave due emphasis to the debt-deflation mechanism. Kindleberger’s was the definitive history of the Great Depression, until Barry Eichengreen published Golden Fetters in 1992.

Coincidentally, Perry Mehrling – the great “money view” economist – has just published an intellectual biography of Charles P. Kindleberger, which I had the pleasure of reviewing in the New Statesman.

As the Sveriges Riksbank Prize committee noted, Kindleberger, like Minsky, held fast to the obvious fact that money mattered. And it mattered not just nationally. Through the channels of global capitalism, it mattered globally.

What Mehrling helps us to understand is that Kindleberger was not just an analyst of inter-national finance, of balance of payments and currency, of the gold standard and Bretton Woods. Kindleberger was something even more interesting. Kindleberger was a theorist of money and banking as inherently transnational, as cosmopolitan, as anchored in a mesh of private balance sheets as well as in the power of empires and nation states.

As Mehrling allows us to see, if we think of money as inter-national, we succumb to a methodological nationalism, which posits the national unit as the primary unit, which is then related to other national units, as one island is connected to another. In fact global money circulates across borders, currencies and balances sheets, with ownership, accounting and control dispersed in space.

So when we metricate the scale of the dollar’s global reach by putting together a chart like this, which compares flows of global finance with national economic aggregates like shares of global GDP, we are engaged in a comparison of apples and oranges.

Source: Obstfeld and Zhou

There is nothing inherently wrong with such a comparison, but we should be clear about the incongruity and its implications.

Hyun Song Shin has given us what is surely the most effective graphic illustration of this point in this brilliant presentation. Inter-national economics offers the island view. Kindelberger’s cosmopolitan understanding of the dollar system is the networked, matrix view.

As Mehrling notes, it was a sad comment on Kindleberger’s lack of influence that his line at MIT was filled after his retirement by Rudiger Dornbusch, who would become perhaps the preeminent inter-national economists of his day. Dornbusch was a thinker of huge influence and reach, but, as an international macroeconomist, his basic conception of the world economy – the island view – was fundamentally at odds with that of Kindleberger.

Mehrling’s book combines a subtle and interesting intellectual history with a conceptual history. He could have gone far further with his historical exploration. That is a point for another time. But even in the sketch form that he offers, the pay-off is huge. As Mehrling suggests, Kindleberger was perhaps better able to analyze money beyond the nation-state framework, because he was trained by a generation of American monetary economists for whom the existence of an independent American national monetary system was anything but a given.

America’s financial system as a national unit, in fact came into existence between the late-19th and the early 20th centuries. And it came into existence under the influence of international forces, most notably the shock of World War I, which helped to weld-together America’s national financial system, under the supervision of the Federal Reserve. America’s national central bank itself had only been founded as recently as 1913.

With dramatic speed, in short, the US moved from a position of peripherality to centrality in the global financial network.

If you follow the Mehrling-Kindleberger line, if the Sveriges Riksbank Prize committee had actually wanted to reward economist who have enabled us to understand the dynamics of the modern global financial system and its interconnections with the real economy, the prize should have gone to the team at the BIS going back to the William White era and the academic economists associated with them today, most notably Hyun Song Shin.

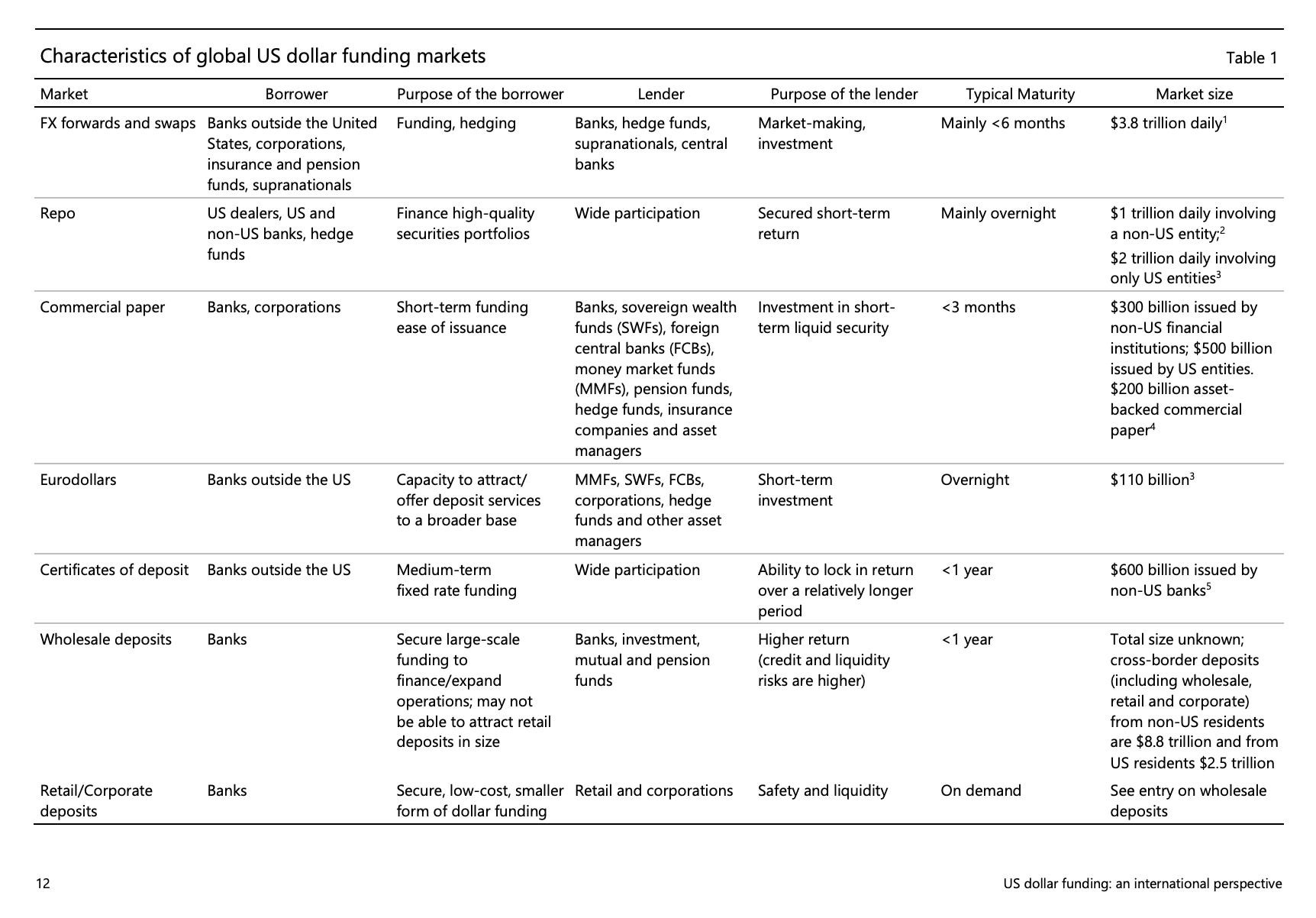

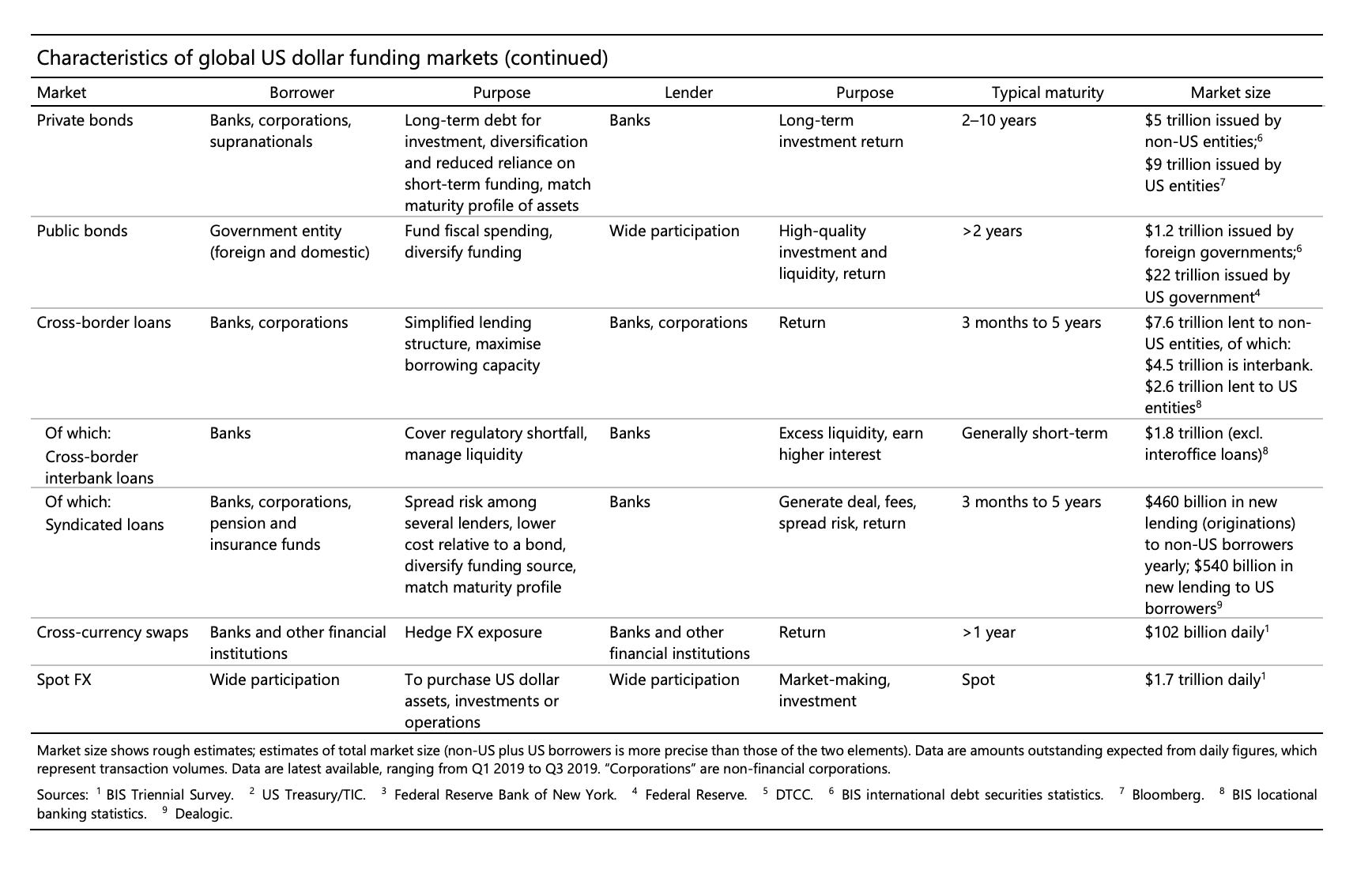

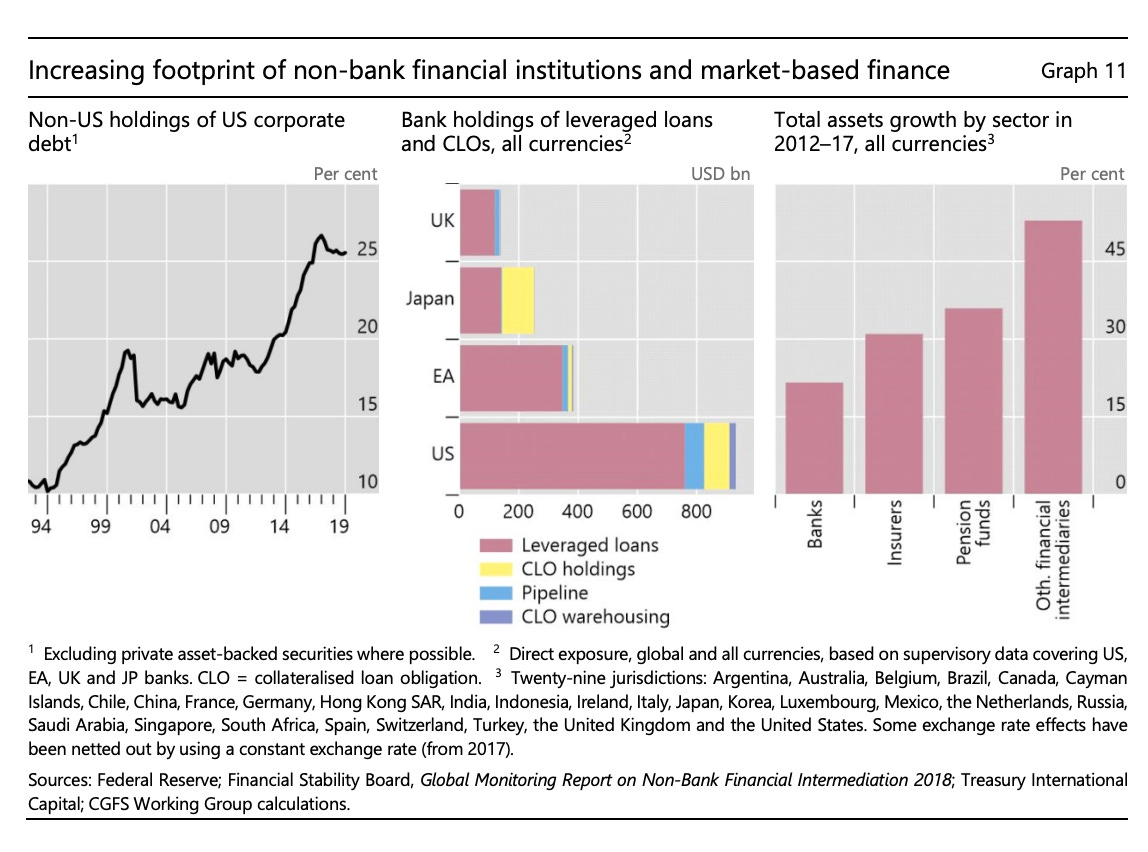

If you want to understand how credit is created globally, don’t start with the neoclassical fable of households savers and borrowers that sits at the heart of the Diamond and Dybvig model (And yes I do know that that does not exhaust D&D’s contribution and that run dynamics of the type they describe happen in market finance too!). If you want to understand the modern system, start with a diagram like this one, as recently drawn by a BIS team.

This is the market-based network of global finance on which the global role of the dollar rests. If you want to understand how ramified the dollar network is, consult this hugely instructive chart, also compiled by the BIS.

I cannot resist quoting extensively from this BIS report since it captures so clearly the forces that underpin the continuing dynamism of the dollar system and speaks so directly to the world as seen by Kindleberger.

The growth of global US dollar funding in recent years has largely been driven by market-based financing. Over the past five years, around three fourths of the increase in international US dollar funding has been in the form of marketable debt securities rather than bank lending. In that time, the stock of US dollar international debt securities has risen relative to global GDP, while bank lending has shrunk relative to global GDP to around its levels of the early 2000s (Graph 10, left-hand panel). As a result, international US dollar debt securities now exceed bank loans, having been around 60% as large a decade ago.20 The increased prominence of market-based funding has reflected a range of factors, some of which are not unique to US dollar activity. As discussed, banks’ asset growth has been limited, as they have focused on improving risk management and repairing balance sheets. While post-crisis banking regulations have improved the safety and soundness of the banking system, the increased cost of intermediation may have also encouraged some activities to migrate outside the banking sector. In addition, there has been strong demand for securities from institutional investors, reflecting rapid growth in their funds under management amid a search for yield in an environment of low global interest rates. NBFIs have also become increasingly important as issuers of debt securities (the dark blue area in the right-hand panel of Graph 10).

Borrowers and lenders of US dollars usually rely on intermediaries. A characteristic of international US dollar funding markets is that they may involve several layers of intermediation that give rise to long and complex funding chains and result in significant interconnectedness for the financial system, more than in most domestic markets. Graph 17 provides illustrative examples where US MMFs act as ultimate lenders; non-US entities are the ultimate users of dollars; and non-US repo dealers, the FICC, central bank FX reserves managers and international banks act as intermediaries. These funding chains cut across jurisdictions and sectors, and add complexity. In addition, it is often the case that whole chains and their interconnections are not visible.

This is a long way from the world with which Kindleberger was familiar, but it is a world which his cosmopolitan (as opposed to international) vision of global finance, was perfectly adapted to analyzing. As Mehrling argues, it constitutes a retrospective vindication of his insistence on the need to understand money’s tentacular flow beyond the boundaries of the nation state.

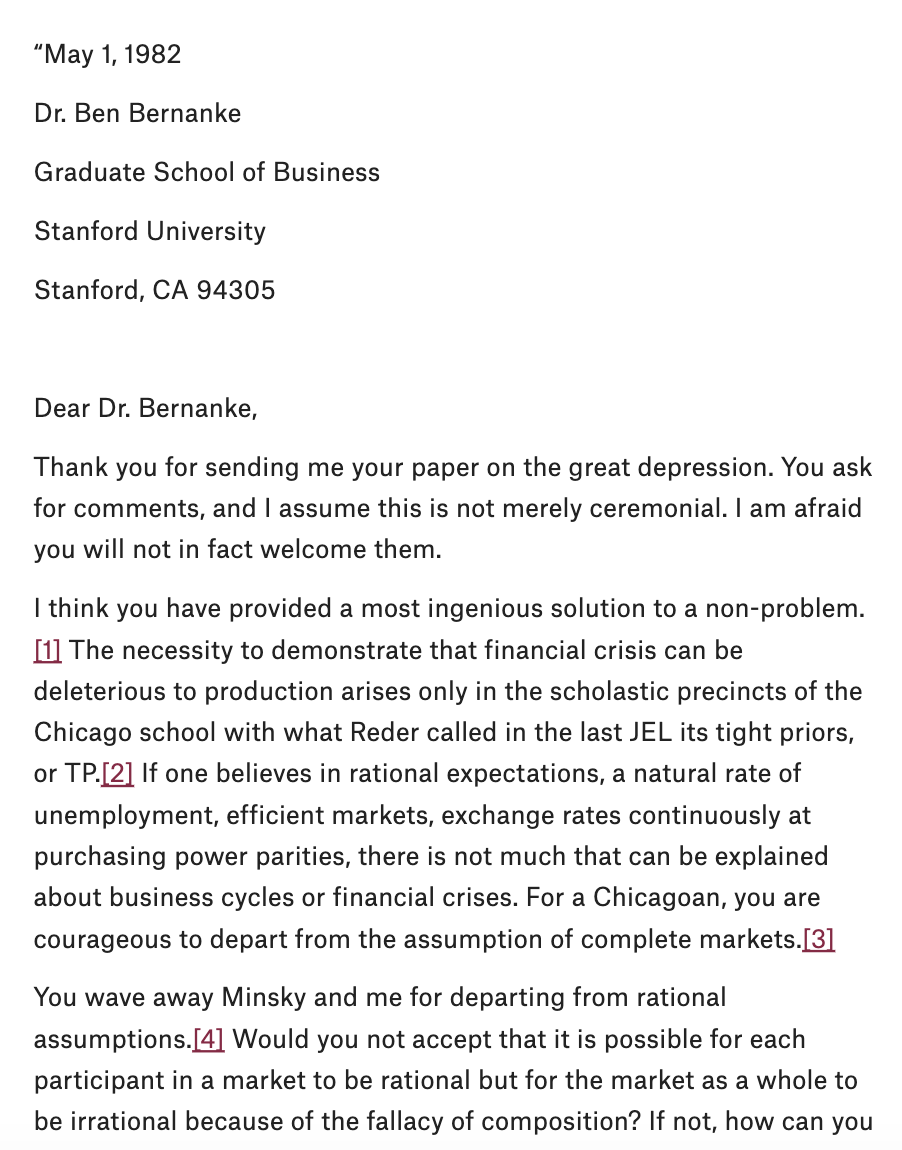

Kindleberger may not have lived long enough to analyze the latest generation of market-based finance. But in the 1980s he was very much alive and kicking. Indeed, he trained many of the cohort of macroeconomists at MIT to which Bernanke belonged. So, when the up-and-coming Ben Bernanke drafted the paper which is cited in the Nobel committee report – Non-Monetary Effects of the Financial Crisis in the Propagation of the Great Depression (1983) – he sent a copy to Kindleberger for comment. Miraculously, Perry Mehrling found Kindleberger’s reply in the archive and has published it on the INET platform.

… and it goes on from there.

****

I love writing this newsletter. It goes out for free to tens of thousands of readers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, there are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.Several times per week, as a thank you, all paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

To join the supporters club, click here:

Ones & Tooze: The Nobel Economics Prize Rewards Bank Run Breakthroughs

In what’s becoming an annual traditional, Adam and Cameron examine the Nobel Economics Prize. This year former U.S. Federal Reserve Chair Ben Bernanke as well as economists Douglas Diamond and Philip Dybvig won for their research on preventing bank runs. Adam notes that while the study of bank runs isn’t new, the work of this trio helped provide greater understanding of the macroeconomic forces behind banking.

In the second segment, the two reflect on the recent protests in Iran and the current role of women in the country. They also take a broader view of the Iranian economy and its tremendous potential if it were to allow full participation from women and was no longer under international sanctions.

Want to see Adam and Cameron’s live show but won’t be in NYC on October 25th? Click here to buy tickets to watch the live stream or on demand for a full week afterward.

Find more episodes and subscribe at Foreign Policy

October 13, 2022

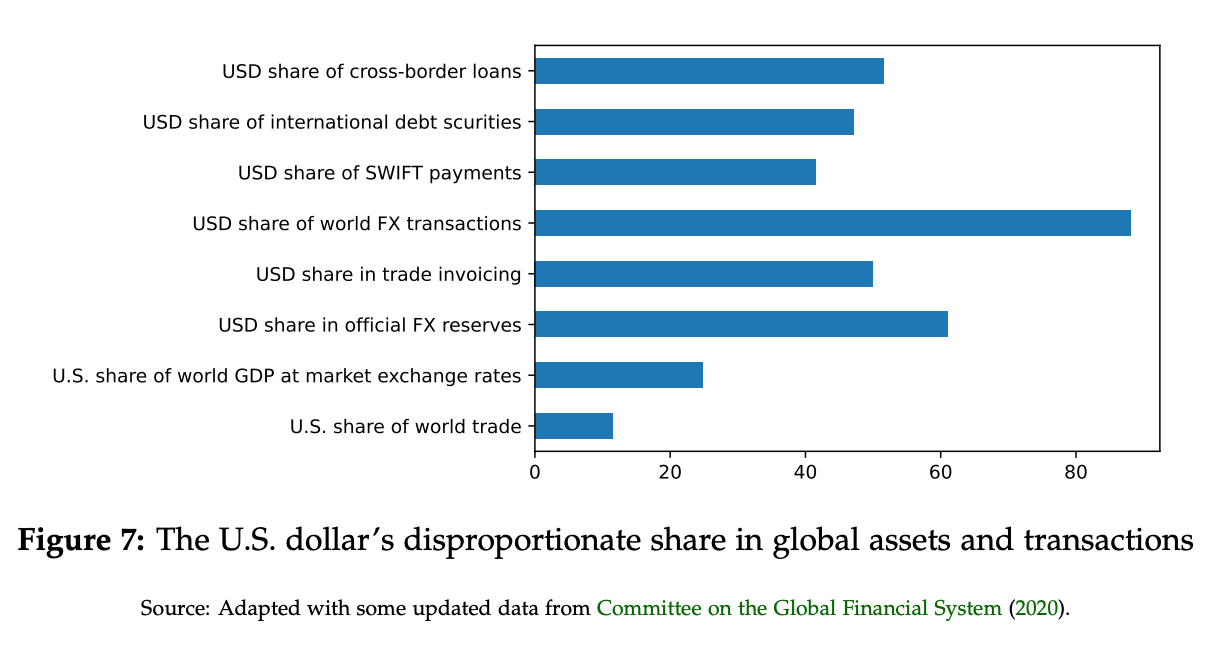

As good as gold: How the dollar has ruled the global economy no matter the crisis at home.

The dollar is king. This year the strength of the US currency has humbled the yen, the euro and the pound sterling. US interest rates are putting pressure on dollar debtors around the world.

This is not a surprise. It is often said that the dollar wins whatever the state of the world economy. It is a safe haven in crisis; in a boom, money surges into the dollar because US business is the prime generator of profits. But what is increasingly hard to ignore is how the dollar’s monetary pre-eminence is out of proportion to America’s actual economic standing in the world.

Thanks to the explosive growth of emerging markets such as China and India, the world economy is increasingly multipolar. As a result, the US accounts for little more than 20 per cent of global GDP and yet its share of currency reserves is closer to 60 per cent and the dollar is involved in 85 per cent of all foreign currency transactions. If currency is conventionally thought of as an attribute of sovereignty, then this preponderance of the dollar would seem to confirm the continued existence of a US financial empire. And yet in 2022 this is at odds with America’s polarised and dysfunctional politics and the great power competition it faces abroad. It seems almost anachronistic that the Federal Reserve still functions as the de facto central bank of the world, like a hangover from the era of the Marshall Plan in the mid-20th century, or the moment of unipolarity in the 1990s.

How long can this anomaly continue? Are there alternatives to the dollar? In times of war the question becomes an urgent one.

Read the full article at The New Statesman

October 4, 2022

The First Global Deflation Has Begun, and It’s Unclear Just How Painful It Will Be

Around the world, rapid economic recovery from the Covid shock unleashed the largest wave of inflation we have seen since the early 1980s. In response, in the summer of 2021, central banks began raising interest rates. Brazil led the way. In early 2022, the Federal Reserve joined in, unleashing a bandwagon effect: Once the Fed moves and the dollar strengthens, other countries either raise their interest rates or face a sharp devaluation, which further stokes inflation.

The outline of this pattern is familiar. But the breadth is new. We now find ourselves in the midst of the most comprehensive tightening of monetary policy the world has seen. While the interest rate increases are not as steep as those pushed through by Paul Volcker as Fed chair after 1979, today’s involve far more central banks.

There are moments when history-making creeps up on you. This is one of those moments. As far as the advanced economies have been concerned, the era of globalization since the 1990s has been one of disinflation and monetary expansion by central banks. Now that balance is being reversed, and on a global scale.

To add to the disinflationary pressure, we are also seeing Covid-era stimulus programs wound up in favor of measures like the Inflation Reduction Act that promise to cut deficits and take demand out of the economy. In the United States in the third quarter, the so-called “fiscal drag” will slow the economy by more than 3.4 percent of gross domestic product, according to an analysis by the Brookings Institution.

Read the full essay at The New York Times

Chartbook #158: Recession risk in a world in the grip of the global dollar cycle.

Did a piece for the NYT riffing on Chartbook #152 on the global anti-inflationary pivot and the attendant recession risk.

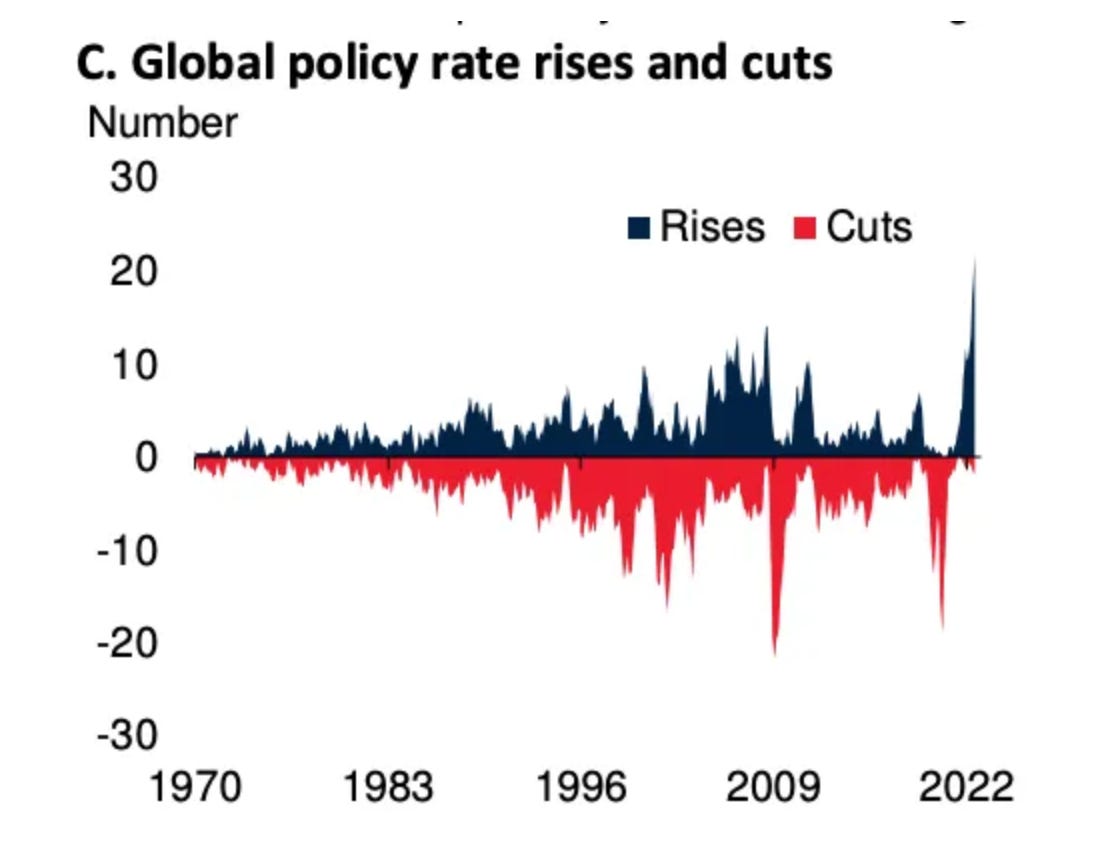

As interest rates rise around the world, as they never have before …

Source: World Bank

… the questions are

Are interest rates too blunt a tool for dealing with a supply-side shock. Will central banks have to use really massive force?In fighting a global inflation on a national basis, will national deflationary pressure reckon with the spillover effects of what is de facto a worldwide tightening?Will something break and produce not a recession but a crisis, a crisis that the global financial architecture and safety nets are not adequate to coping with, so that a crisis becomes a disaster.Thanks to help from Maury Obstfeld, to whom big thanks, I hope I have gotten my spillover risks clearly sorted out this time.

One is the “beggar they neighbor” effects of devaluations, which could lead to a prisoners dilemma style failure of coordination and very suboptimal outcomes. The logic here is as follows: I am unambiguously better off if I appreciate my currency to fight inflation. But other countries can respond. If we all engage in competitive appreciation – reverse currency wars – there may be winners and losers in relative terms, but we all end up with rates that are too high. To avoid this we need to coordinate.

The second effect is the global slack argument – inflation in one country is affected by inflation in another an effect which also operates under deflationary conditions. This is not zero sum. My efforts at deflation help other people to achieve the same desired goal. But, if national decision-makers don’t take this spillover into account, they may end up with more deflation than anyone wants i.e. a global recession.

Clearly what is called for is coordination of policy. That is lacking. Once more, global economic governance falls short of our globalized condition.

The Fed didn’t lead this tightening cycle. Amongst G20 members, Brazil did. It began to raise rates already in the summer of 2021.

But, in early 2022, the Fed took over and since then the global economic story has been dominated by the narrative of Fed tightening and a surging dollar. The dollar in turn puts pressure on everyone around the world – countries and companies – who has borrowed in dollars. The BIS puts that total at in excess of $22 trillion, of which, in rough terms, about a quarter is in Emerging Market and low-income countries. Some will have hedged exchange rate risks associated with that debt. Not everyone will and hedging has its price.

It should be said that there is no consensus around the strong dollar story as far as 2022 is concerned. Robin Brooks of the IIF has been insisting that what is really going on is not so much dollar strength, as weakness in the euro, sterling, the yen and the renminbi. Emerging market currencies have been doing relatively better.

People talk about Dollar strength, but that's really a misdiagnosis for what's going on. First, USD isn't strong against EM (blue). Second, where the Dollar is strong is vs European currencies like Euro and the Pound. We're not seeing a strong Dollar. We're seeing weak Europe… pic.twitter.com/A9WndH4fDl

— Robin Brooks (@RobinBrooksIIF) September 29, 2022

That is a useful corrective as far as currencies are concerned. But, it in on way refutes the broader point that the dollar is king. To avoid devaluation in 2022 what EM central banks have done is to hike interest rates hard and to intervene to prop up their currencies directly. Whether or not it shows up in actual devaluation, the dollar and Fed policy thus dominates the global financial cycle.

This is brought home with real force in an extremely useful and very readable new paper by Maurice Obstfeld of University of California, Berkeley and Haonan Zhou, Princeton University. In a series of vivid charts and tables they lay out how a strong dollar produces deflationary and recessionary pressure across the world economy.

Over the entire period between 1980 and 2021 a one percent appreciation of the dollar is associated with growth in Emerging Market and Developing Economies (EMDE) that is 0.63 percent slower. Furthermore, this association has strengthened since the millennium. The impact on world trade, notably, has increased from -0.39 to -0.61.

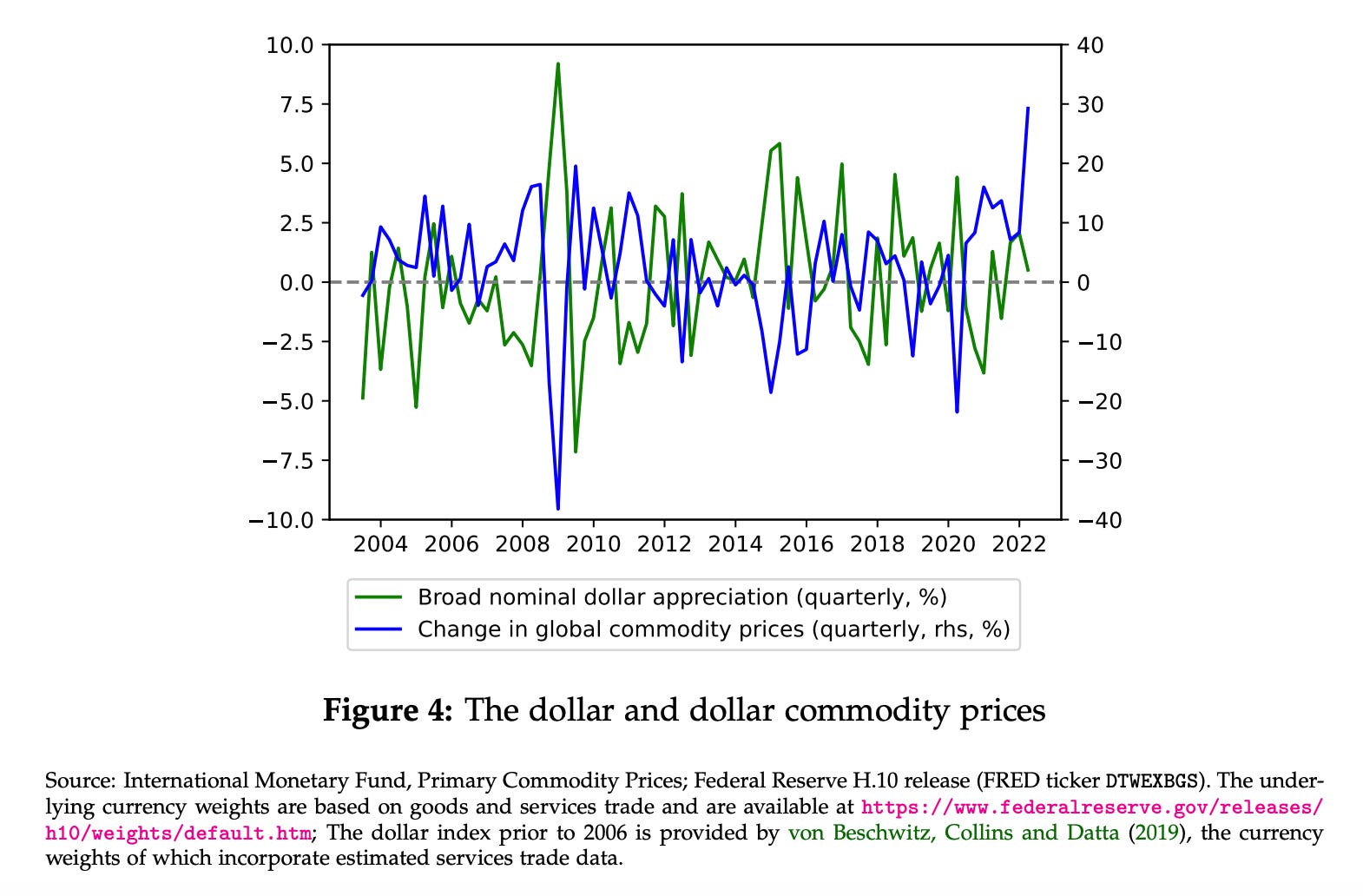

As Obstfeld and Zhou note, the dollar exchange rate moves inversely with global commodity prices (measured in real terms).

As commodity prices fall, not only does the growth in world trade slow down (commodities make up a large part of world trade) but trade in investment goods also slows. By way of trade and investment, fluctuations in the dollar are negatively associated with global growth.

It is worth emphasizing that this is surprising since the promise of the flexible exchange system adopted, in stages and by degrees, since the collapse of Bretton Woods in the early 1970s, was that it would insulate the real economy and real trade flows against the monetary shocks once transmitted by fixed exchange rate systems, or, formerly, the gold standard. But, in practice a large share of the world’s economies remain attached to various kinds of dollar peg, or are so closely associated with economies that are attached to exchange rate pegs that they are de facto linked themselves. In addition, as Silvia Miranda-Agrippino, Hélène Rey and others have shown, the flux of foreign capital across the world is so substantial and the impact of dramatic appreciation and depreciation of currencies so consequential, that central banks around the world track the Fed, willy-nilly. The Fed and US financial markets rule what is in effect a global financial cycle.

In the form of large capital flows this can bring substantial benefits for real economic development. But it also creates risks. In Chartbook #152 I highlighted some recent warnings of the pressures being exerted by the current cycle worldwide. This morning, UNCTAD released its Trade & Development Report for 2022 warning of the risk that the worldwide recovery from COVID may be stalled my an excessive and uncoordinated tightening.

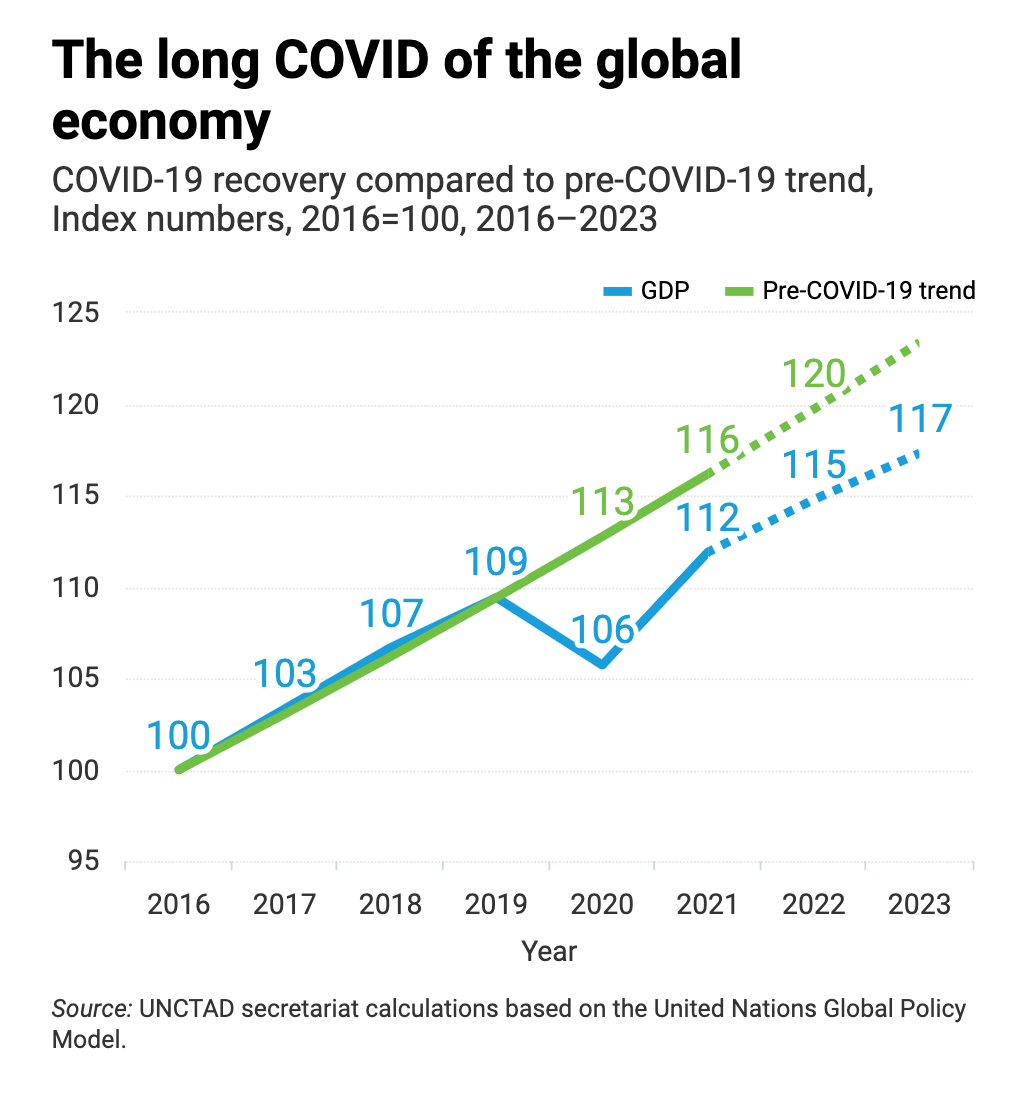

Despite the vigor of the rebound in 2021 the world economy is some way short of its pre-COVID trend.

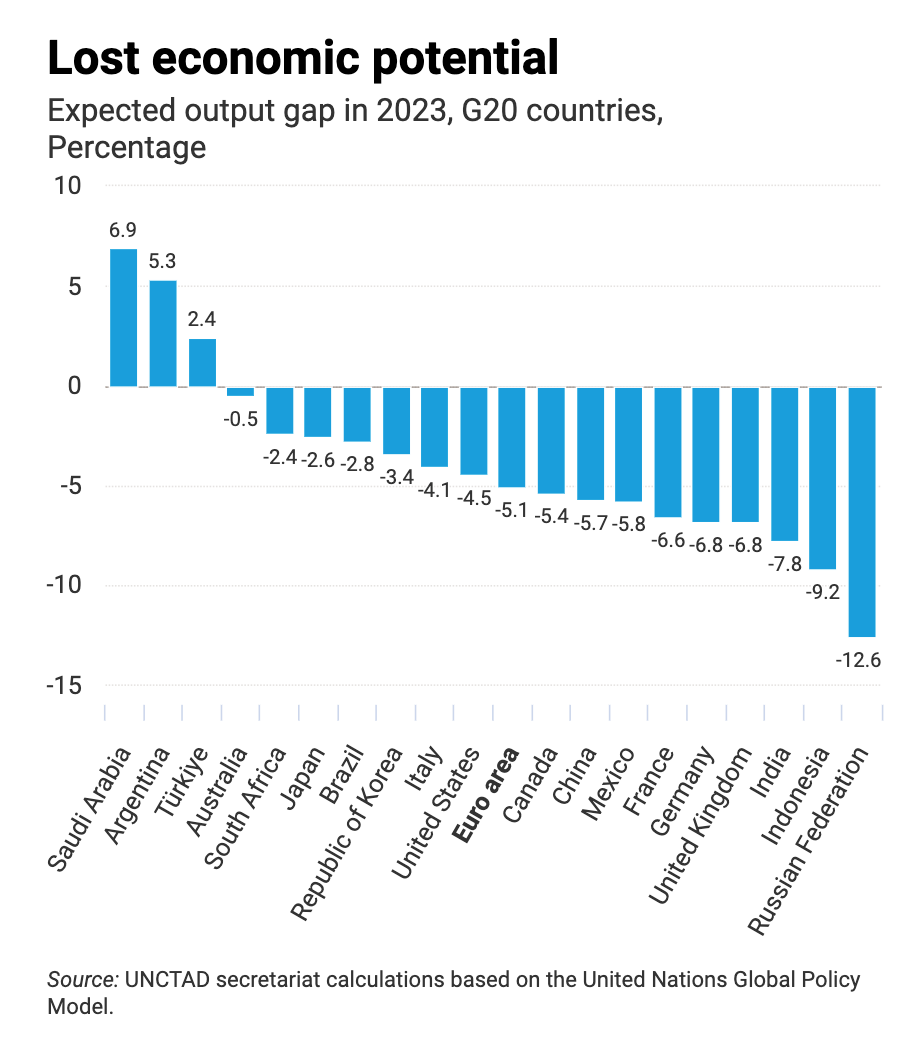

Setting Russia aside as a special case, the shortfall in output relative to pre-COVID trend for several major EM, notably India and Indonesia, are striking. This is a powerful corrective to the rather upbeat narratives for both those economies in 2022. Add in China, with an estimated 5% shortfall by 2023, and weighted by population that is a huge corrective to general complacency about worldwide COVID recovery.

As I argue in the NYT piece, recession is not the only risk. Will things break? In triggering crises it is balance sheets, as much as flow variables such as GDP, that are key. As UNCTAD reminds us:

With 60% of low-income countries and 30% of emerging market economies in or near debt distress, the possibility of a global debt crisis is high.

How long will they be able to withstand the pressure of a global tightening cycle?

Not only are central banks around the world raising interest rates. To fight devaluation they are also spending limited reserves. This is a striking factoid from the UNCTAD report.

Developing countries have already spent an estimated $379 billion of reserves to defend their currencies this year, almost double the amount of new Special Drawing Rights recently allocated to them by the International Monetary Fund (IMF).

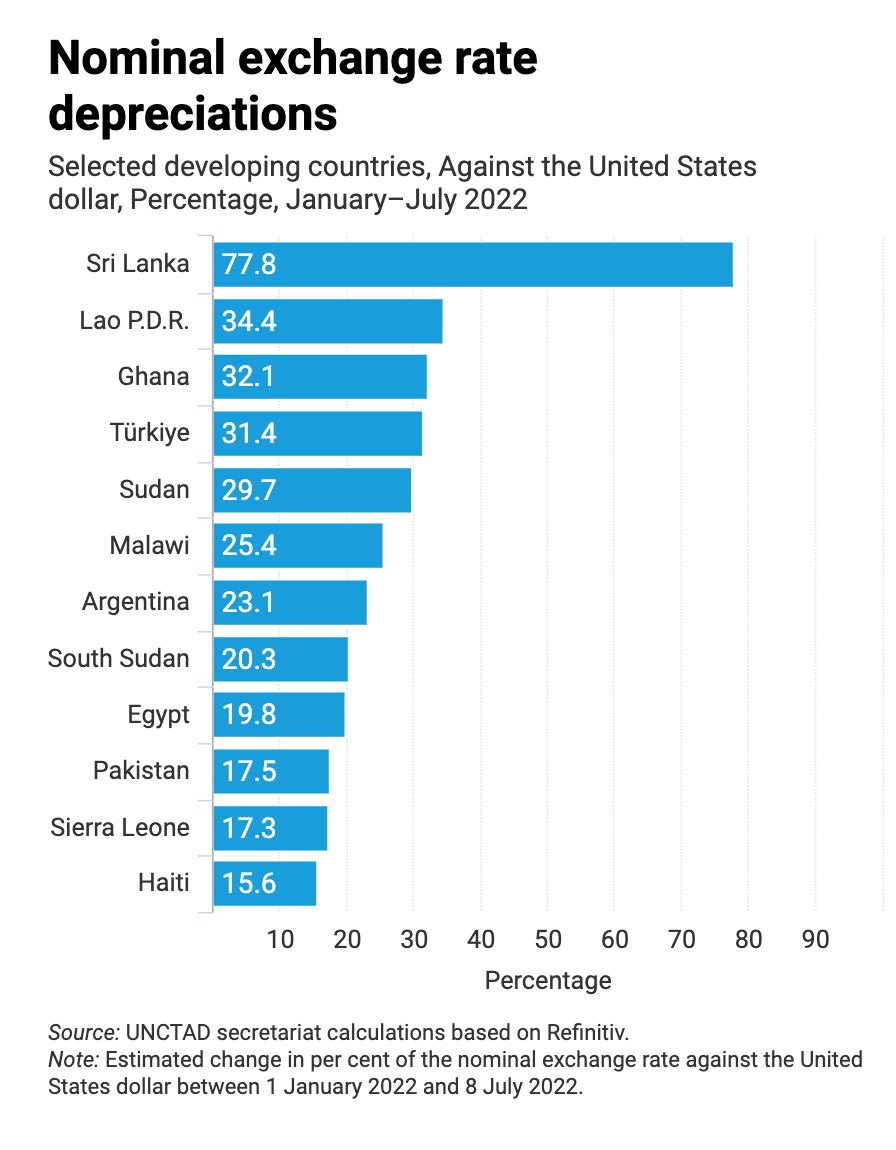

In the first half of 2022 some of the most fragile economies in the world saw sharp devaluations.

This makes for a truly dangerous combination of forces. And if there is one thing we do know about the global financial architecture, it is not set up to deal with large-scale sovereign default. Once again hundreds of millions of people around the world, face huge and radical uncertainty. Not because uncertainty is something about the world that wise people accept, but because we have a financial system that systematically generates risks and we have not created the safety nets that would contain that risk and make it more manageable. And then we engage in uncoordinated policy action which put that entire system under massive pressure. Right now it is not even obvious that policy-makers are aware of the historic scale of the squeeze they are engaged in. In fairness some policy-makers like Lael Brainard are posing the question of global implications of Fed policy. But we need more than the occasional central banker’s speech. We are in what Kant described as a state of “selbstverschuldete Unmündigkeit” or self-inflicted immaturity. It is time to exit that condition.

****

I love writing this newsletter. It goes out for free to tens of thousands of readers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, there are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.Several times per week, as a thank you, all paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

To join the supporters club, click here:

Adam Tooze's Blog

- Adam Tooze's profile

- 767 followers