Adam Tooze's Blog, page 15

August 19, 2022

Ones & Tooze: The Crazy Economics of Book Publishing

For the news data point this week Cameron and Adam look at the proposed merger of Penguin Random House with Simon & Schuster as well as the tragic attack on acclaimed novelist Salman Rushdie. The two then discuss the overall state of the publishing industry and how digitization has impacted the business model for major publishing houses as well as their relationship with libraries.

In the second segment the two discuss the astronomical inflation currently underway in Argentina. Adam gives a historical look back at the Argentine economy and details the decline that has lasted for nearly a century. The two also talk about how uncertainty in the price of food has had a negative impact not only on GDP but mental health as well.

Find more episodes and subscribe at Foreign Policy

Chartbook # 143 China, Africa and a new, “Two World” divide?

As the title suggests, the idea for my newsletter was originally inspired by the stacks of charts – Chartbooks – with which macro analysts at investment houses edify their colleagues. Over time I have drifted away from that model. Instead, the newsletter has taken on the form of a “long read” essay. But, periodically, it is convenient and refreshing to revert to the original idea of Chartbook.

So, ahead of your weekend, here are a batch of charts that offer a snapshot of our world in the summer of 2022.

Start with three from the great Branko Milanovic on global inequality as the key to world history. Milanovic divides the history of the last two hundred years into three epochs: The Age of Empires and Class Struggle, The age of Three Worlds, the Age of Convergence.

If you, theoretically, equalize all countries' mean incomes (but leave national distributions unchanged), you reduce global inequality to 23 points. pic.twitter.com/y5xsMvG4dz

— Branko Milanovic (@BrankoMilan) July 10, 2019

EVERYONE should follow @BrankoMilan and his remarkable blog http://glineq.blogspot.com/

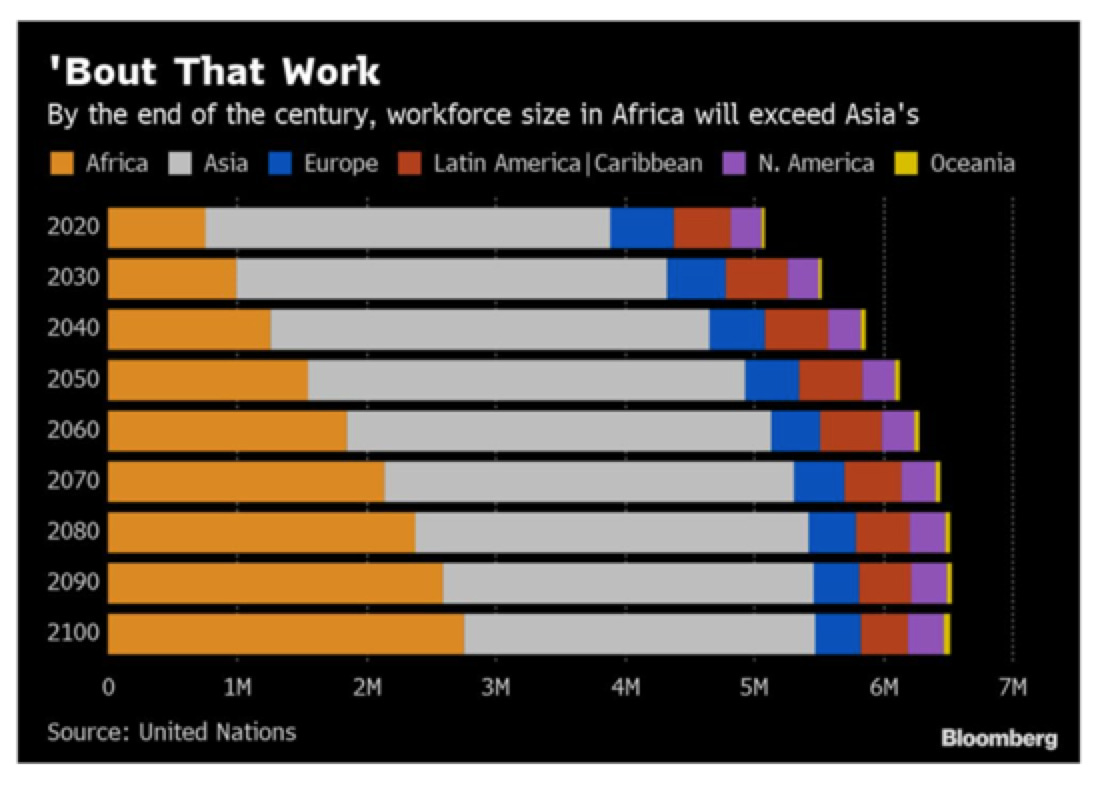

A key factor in the decades ahead will be the demographic development of the world’s workforce. By 2050 the population of Africa of working age will outnumber the working-age population of the world ex-Asia.

Meanwhile, thanks to the logic of the simple equation:

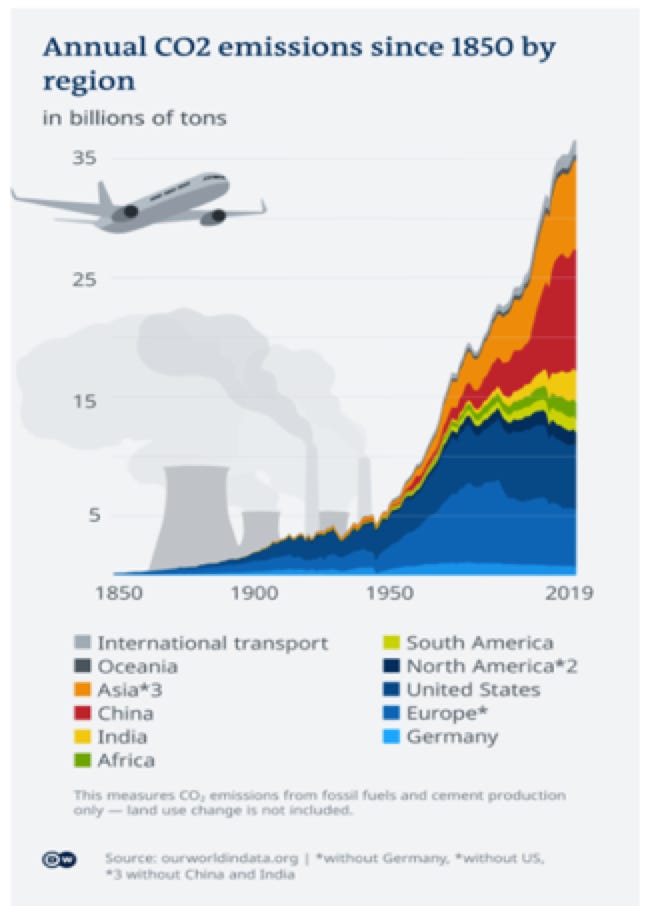

Environmental impact = population * GDP per capita * environmental intensity of unit of GDP

the balance of CO2 emissions around the world has dramatically shifted. And yes these are national numbers so they show where production not consumption is located.

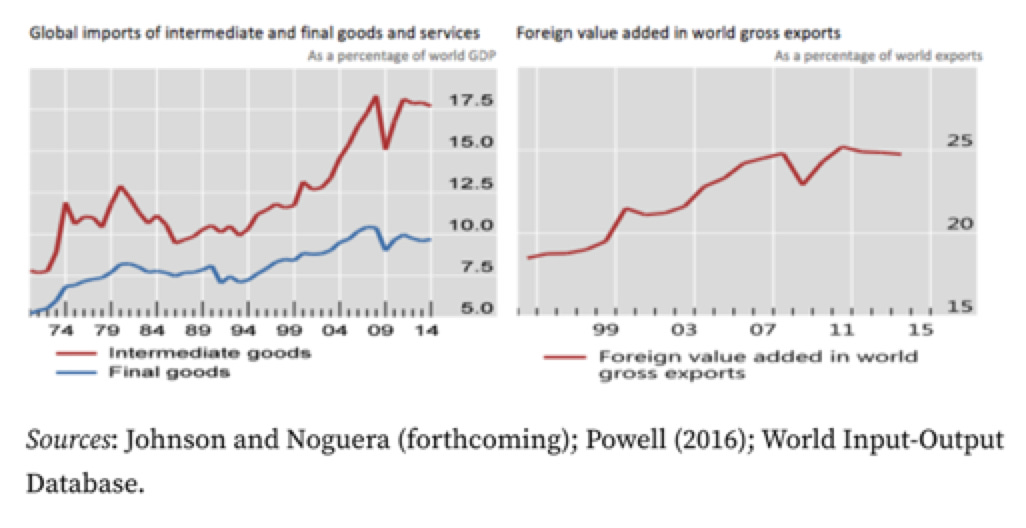

I chose those numbers so as to segue with data for the development of global value chains and the global division of labour in recent decades.

Shifting industrial production from the West to Asia helped to drive the huge surge in Asian CO2 emissions. “Helped” is the operative word here. The basic drivers of Asian economic growth have been domestic, above all, the gigantic process of urbanization and the incorporation of hundreds of millions of people into the urban workforce. That is what drives steel and cement production in China.

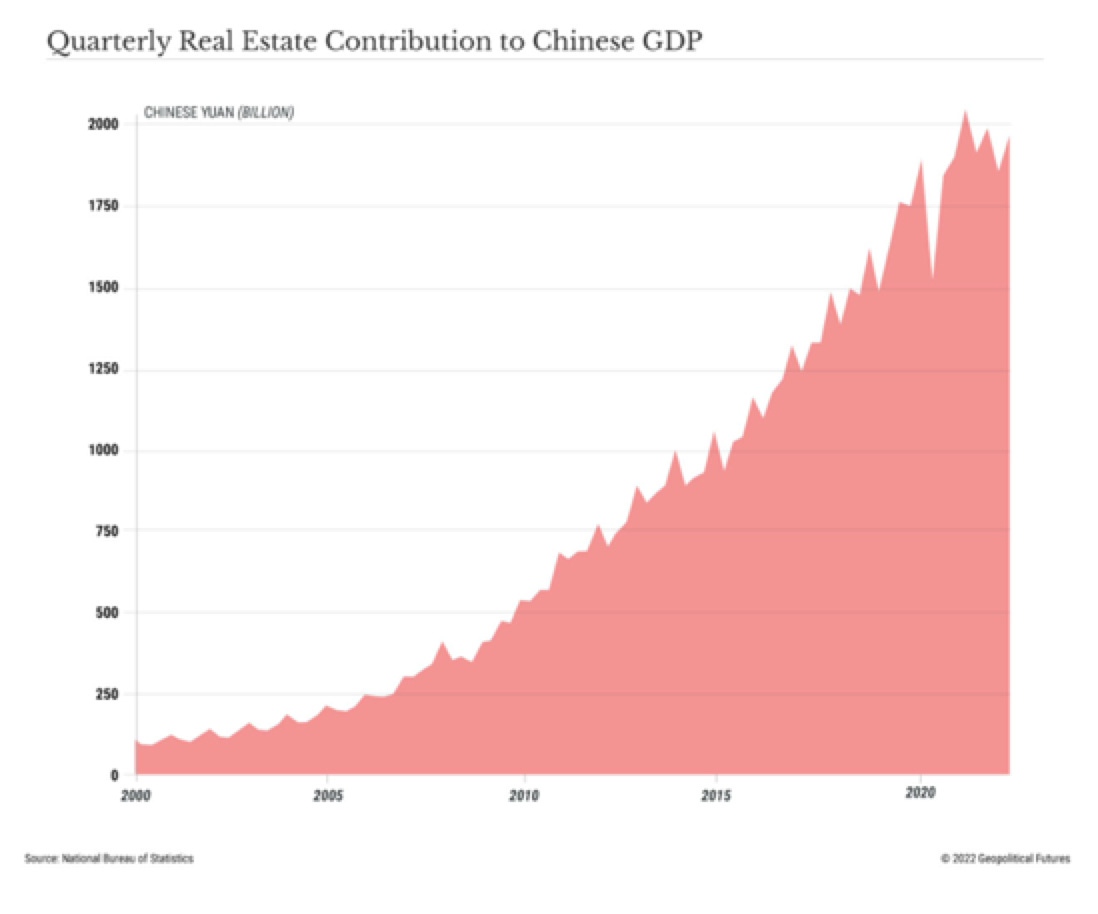

In China as private property rights were established, this has gone hand in hand with the most gigantic real estate boom in history.

China’s property boom is the material base for the growth of China’s middle-class.

Chinese middle-class consumers are now a huge driver of global demand. They are also the great driver of the trend towards global convergence in inequality, which Milanovic’s data reveals so starkly.

The fact that the Chinese real estate boom is now tottering is not just a cloud on the financial horizon. Along with zero covid and the tech war launched by the West, this is the single most ominous cloud hanging over the world economy and the entire developmental narrative of recent decades.

In recent decades China has been the single most significant contributor to global growth (at least in statistical terms, Matt Klein and Michael Pettis may beg to differ on the Keynesian demand-side of this).

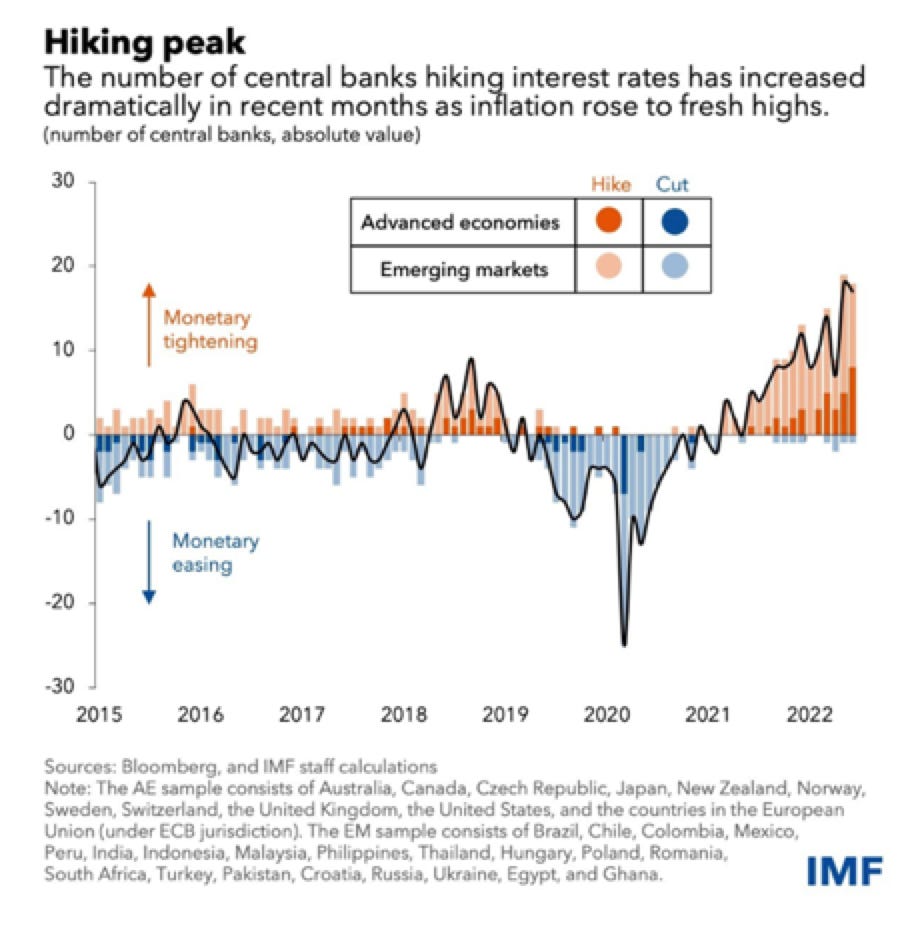

And at this moment, as central banks around the world engage in dramatic coordinated tightening of monetary policy, China remains the most significant source of potential stimulus.

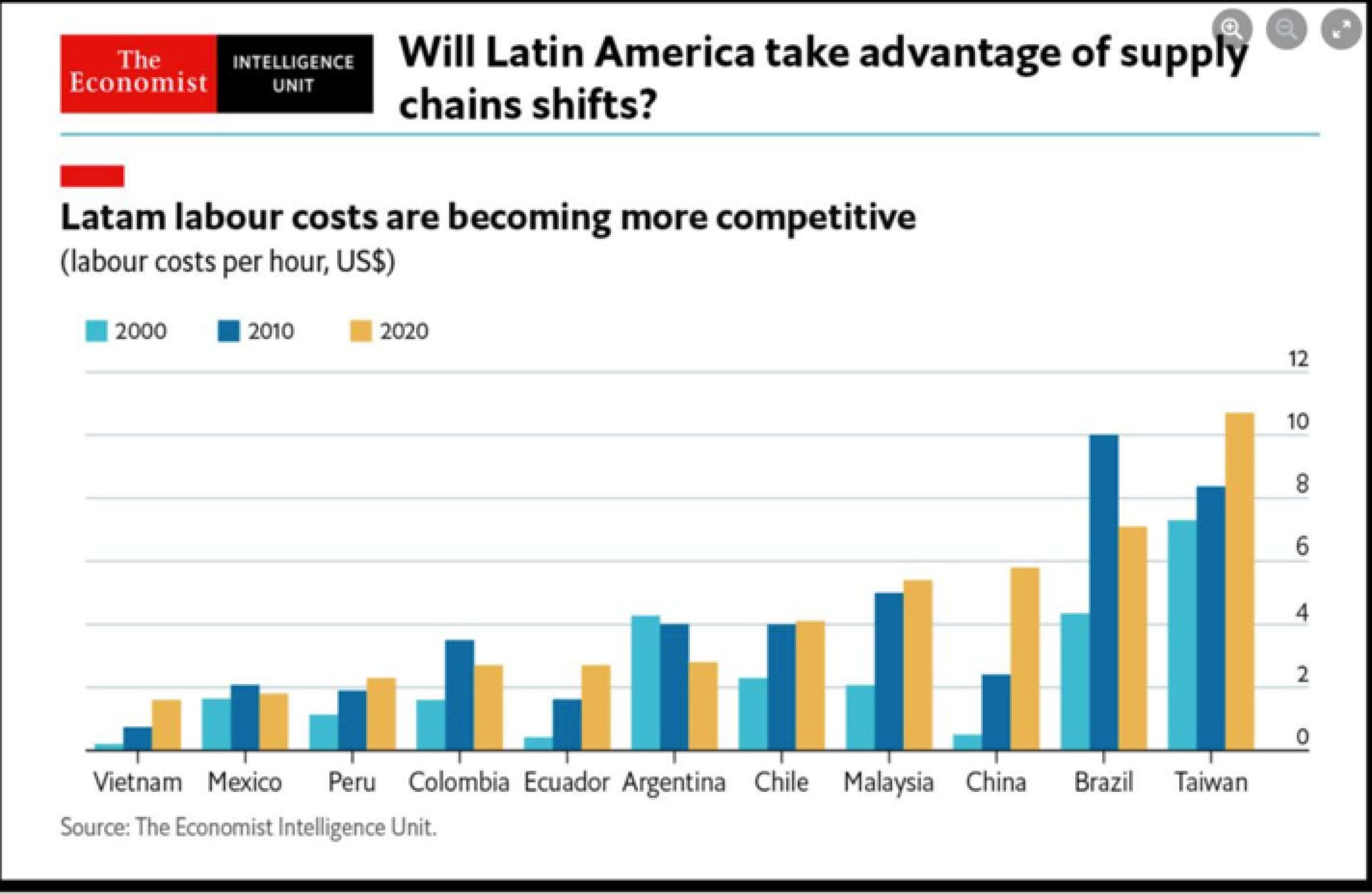

China right now is running an epic trade surplus, but what we should not expect is a resumption of export-led growth based on low labour costs. That model is no longer relevant as far as China is concerned. Thanks to its remarkable development in recent decades it now has relatively high unit labour costs by emerging market standards.

Though Latin American countries have struggled to take advantage of the opportunities this opens up, others have been more quick to move into the slots opened up by China’s development.

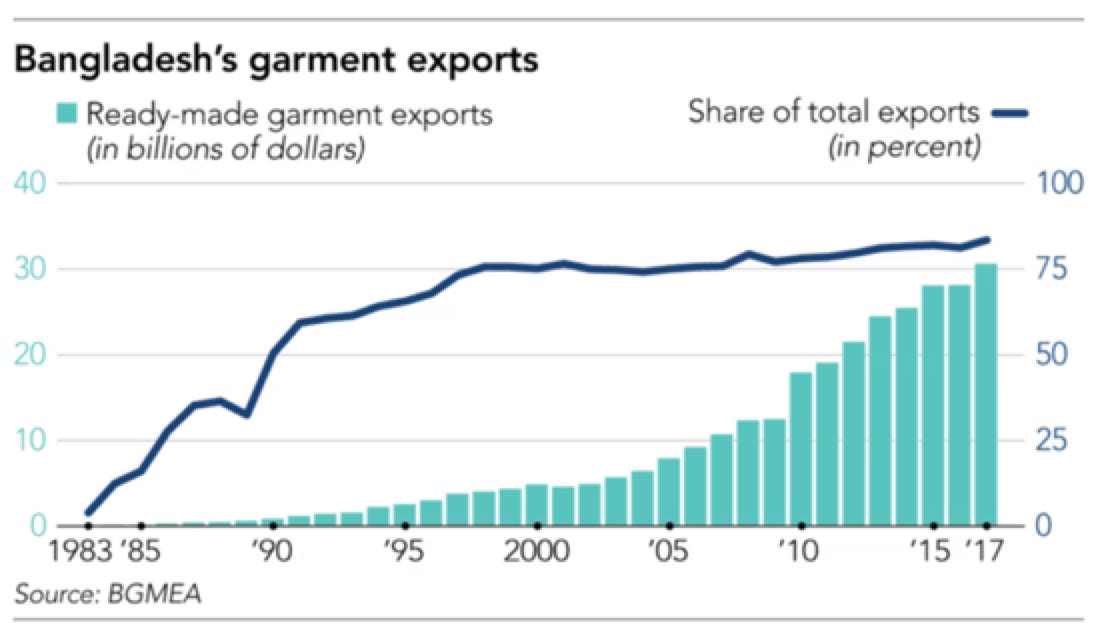

The most remarkable is Bangladesh, whose garment exports have surged spectacularly.

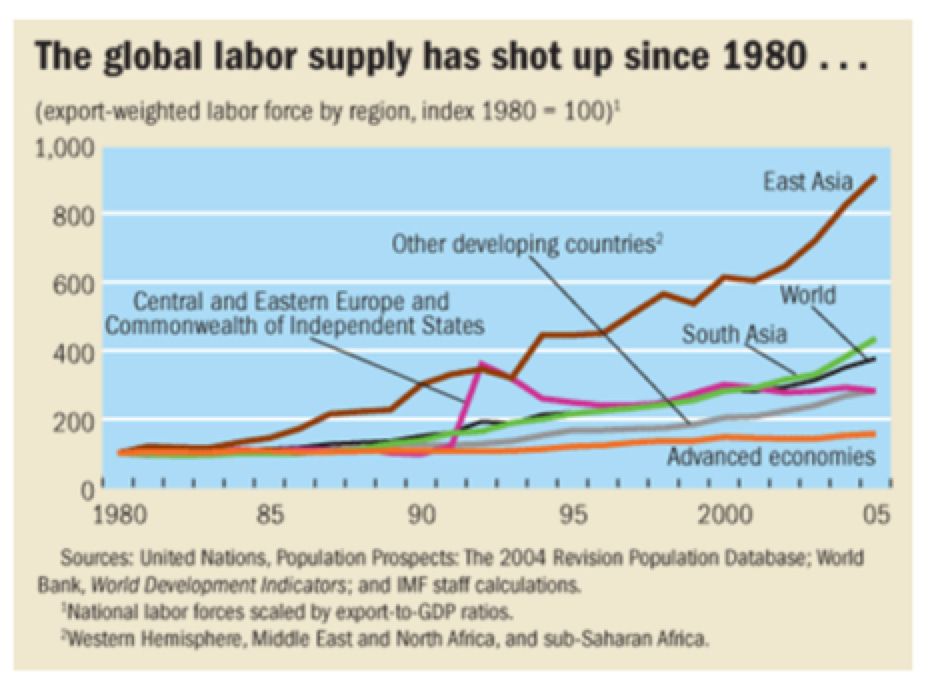

Putting these snapshots together, one way of formulating the question of the future of globalization at the big picture level is as follows: Can we imagine a future in which the huge surge in the working-age of population of Africa is incorporated into the world economy as Asia’s youth bulge eventually was from the 1980s onwards. (Reupping a famous IMF graph from 2007) If Africa were to be incorporated it would continue the convergence dynamics of Milanovic’s third epoch.

If on the other hand Africa is not deeply incorporated into the global division of labour, does this presage a new phase in the history of global inequality? After “Empire and class struggle”, “Three Worlds” and the few decades of “Global convergence”, are we about to enter the era of a new, “two world divide”?

****

I love putting out Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

There are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.August 13, 2022

Chartbook #142: The dollar system’s resilience

This week I did a piece for Foreign Policy on the current strength of the dollar and what it tells us about how the dollar system operates under stress. You could see it as an updating of a longer essay I did back in early 2021 for Foreign Policy on the history of the dollar as the world’s anchor currency. The illustration was kinda great.

The 2021 piece was an an attempt to write a history of the dollar that did without a dramatic ending. It postulated more and more policy improvisation in a context of growing multipolarity as the likely future of the dollar as the leading global currency.

That deliberately low-key interpretation, postulating a future of open-ended, “muddling through”, in turn informed my reaction to the feverish debate about the future of the dollar system unleashed by Putin’s attack on Ukraine in February 2022.

Whereas many analysts were prompted by the war and the dramatic financial sanctions imposed on Russia to imagine futures radically different from the present – scenarios I dubbed finance fiction of “fin-fi” – I argued in Chartbook #107 that we should read this kind of speculative financial writing as symptomatic rather than predictive or realistic. It is a symptom of the following tension:

(2) The world is multipolar and so is global trade. Western policy must adjust to that.

(3) There is a huge asymmetry in the world right now between the financial system that remains spectacularly euro-dollar centered and the new multipolarity of power, trade and economic activity.

(4) Given this asymmetry there is a fascination in the cultural and political sphere with the way this glaring asymmetry could be overcome. Not only that, there is a positive desire to see the asymmetry overcome. There is a relish in the discomfiture of the West. The euro-dollar lock feels like the final frontier of Western power, long overdue for overthrow.

(5) Fin-fi is one of the media in which that sense of impending historical change expresses itself.

(6) Given the situation from which it emerges we should read the proliferating genre of Fin-fin symptomatically. It expresses a world historic tension. In some cases it delineates trajectories and seeks to map strategies for policy and investors. In other cases these texts are better read are acts of diplomacy (Larry Fink) motivated by complex constellations of interests.

(7) We should guard against taking Fin-fi literally as a guide to the future rather than as a fascinating expression of the tensions inherent in our current moment.

(8) Identifying and grasping a tension conceptually, is illuminating and engaging for the reasons stated. But the satisfaction thus derived should not be confused with gauging realistically the likelihood of that tension actually being resolved, certainly not in a “logical” direction.

Despite the obvious interest of certain key players in the global economy in finding alternatives to the dollar, its preeminence in global trade and finance is well buttressed.

If rather than speculating in Fin-Fiction mode about future currency systems, we stay with the troubles of the actually existing dollar system, what became more and more evident from the spring of 2022 was that the dominating story of the coming year would not by new alternatives to the dollar, but the strength of the US currency. In July 2022 the dollar hit the highest level in two decades.

This week’s piece in Foreign Policy picks up on the question of dollar strength and the tensions that it unleashes in the world economy.

For the world economy, the tightening of monetary policy by the Fed unleashes contradictory pressures. The currencies of major US trading partners like Japan have plunged to multi-decade lows.

For those with strong export sectors, selling goods not denominated in dollars, this can be a boon. But those heavily reliant on key imports, which are denominated in dollars, or those who are heavily indebted in dollars suffer an agonizing crunch.

For a typically excellent treatment of the question by the Odd Lots podcast hosted by Tracey Alloway and Joe Weisenthal, see this transcript of their interview with Jon Turek.

In the US economy as well, the sudden appreciation of the dollar unleashes contradictory pressures.

US consumers benefit from lower prices. In the second half of 2022 the strong dollar should be one of the forces helping to bring inflation – both by cheapening imports and slowing the world economy.

Source: Daily Shot

On the other hand, a strong dollar is not necessarily good news for US corporations that generate a lot of profit outside the US.

One of the reasons why earnings tend to be revised down across the board when the US Dollar is strong is that US companies generate a decent portion of their profits outside the United States.

— Alf (@MacroAlf) July 21, 2022

A stronger USD doesn't help there. pic.twitter.com/eMwlUTpYue

And it bears repeating that there are still parts of the US economy – notably export-focused manufacturing – that lose competitiveness and market share when the dollar rises. On this score I once again recommend Neil Irwin’s outstanding essay on the 2016 mini-recession in US manufacturing, which in November 2016 helped set the stage for the election of Donald Trump with the votes of the rustbelt.

Add all this up and you could once again spin a strong narrative of dollar strengthening that ends with a bang. You might even have the makings of a “dollar doom loop”.

In Sri Lanka, of course, there has been a bang, a big bang.

But Sri Lanka suffered that fate because it is a weak, poor, vulnerable and badly governed part of the global economy. The rest of world economy may be fragile and unstable too, but it is not in Sri Lanka’s condition.

To return to an earlier point, the dollar system is well buttressed and it is well buttressed in part because it is enmeshed in a variety of strategies of de-risking. Some of these involve moderating the degree of attachment to dollar finance – by borrowing from foreign sources, for instance, but doing so not in dollars. The big EM markets have learned since the 1990s to manage their risks, a subject I take up (with all the necessary footnotes) in the chapter in Shutdown on the emerging market “toolkit”.

What holds the actually existing system of global finance together is not so much the dollar – pure and simple – so much as the sinews of finance, law and contractual construction knit by key players above all in Wall Street and – as Katharina Pistor has taught us – in London. The systems of English law and the legal code of the state of New York, are the preeminent codes for big debt deals.

To describe this nexus, the nerve center of the dollar system, in the recent Foreign Policy piece, I appropriate the term “Wall Street consensus” coined by Daniela Gabor, our great guide in all things macrofinance. The point of talking about Wall Street rather than the dollar is to highlight the players who actually make the system work, rather than the particular currencies they choose to operate in. But it is not by accident that 90 percent of global forex transactions – $6 trillion per day! – include the dollar as one currency in the pair.

The upshot is that the dollar system is not a giant anachronism with a bulls eye on its forehead – the conceit of the fin-fiction speculative genre. Nor is it a brittle and rigid system, prone to breaking whenever it stressed – as suggested by the doom-lop scenario. It is a sprawling, resilient network of state-backed, commercially driven, profit-orientated transactions, lubricated by the easy availability of dollars, interwoven with American geopolitical influence, a repeated game in which intelligent players continuously gauge their advantages and disadvantages and the (very few) alternatives open to them and then, when all is said and done, again and again come back for more.

****

I love putting out Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

August 12, 2022

Ones & Tooze: Rise of the Green Industrial Complex?

On the show this week: The Inflation Reduction Act isn’t the climate change revolution that some Democrats had hoped for. But it could signal a shift in the power balance between the fossil fuel industry and the renewable energy industry.

Also: How much will it cost to rebuild Ukraine when the war finally ends and who will foot the bill?

Find more episodes and subscribe at Foreign Policy

The World Is Seeing How the Dollar Really Works

2022 has been a year of dollar power—power that manifests itself in both overt and subtler forms.

In the spring, the financial sanctions slapped on Russia’s Central Bank following Russian President Vladimir Putin’s invasion of Ukraine demonstrated the extent of U.S. financial sway, especially when it is exerted in cooperation with America’s European partners. If you export far more than you import and thus hold really large foreign exchange reserves—like Russia’s $500 billion—there really is nowhere else to hold them other than dollars or euros. If it comes to a confrontation, that puts you at the mercy of the financial authorities of the United States and its alliance partners. NATO reveals itself to be a financial power.

Russia has, so far, ridden out the storm, but to do so it has had to close its financial system to the outside world. Its imports have been squeezed to barely more than half their pre-crisis level.

When the sanctions were applied, the shock to Russia provoked the question of whether a monetary system that conferred such one-sided power on the United States could possibly be sustainable. Surely Russia, China, and India would look to build an alternative currency system. This might perhaps be denominated in China’s renminbi and would be centered on the exchange of key commodities. One model might be the kind of deal recently brokered by a leading Indian cement producer, which paid for imports of Russian coal in Chinese currency. To secure funding, you could borrow in the so-called dim sum bond market in Hong Kong, where issuers from around the world issue offshore renminbi debts.

Such a system would secure independence from the United States. But it would take years, if not decades, to reach substantial scale. It also depends on the continuing shortage of key raw materials, which makes it interesting to lock in privileged customer-supplier relations, and the continuing growth of the Chinese economy, which makes it look like the economic champion of the future.

Read the full article at Foreign Policy.

August 10, 2022

Chartbook #141: Is financial uncoupling from China beginning?

Last month, China posted the largest trade surplus for a 30-day period ever recorded by any country in history. As Michael Pettis summarizes it:

“The net result was an astonishing $101.3 billion trade surplus, once again China’s (and the world’s) highest ever monthly trade surplus. China’s trade surplus year to date is 57% higher than last year’s record trade surplus, and amounts to 5% of China’s GDP.”

It was no fluke. July’s number followed an only slightly less staggering figure for June. Amidst the blanket coverage of inflation and the energy crisis, China’s balance of payments is a key indicator of the balance of the world economy.

In the silly Olympics in which countries compete to be “export champions”, China’s surpluses might be taken as a sign that China is “out-competing” its rivals. But, as Michael Pettis points out, the surplus is far better understood as a sign of economic weakness. Imports, driven by domestic economic activity, are lagging far behind the boom in exports as Chinese producers scramble for foreign markets to offset the lack of domestic demand.

8/10

— Michael Pettis (@michaelxpettis) August 7, 2022

It is precisely because the Chinese economy is performing so poorly that export growth and the trade surplus are so high. China's trade performance is a symptom of the problem, and not a locus of strength in an otherwise weak economy.https://t.co/KFqf32sQ7b

For decades Michael Pettis has been diagnosing the excessive reliance of Chinese growth on investment and the inadequate level of domestic consumption. The current conjuncture bears him out.

Matt Klein, Michael Pettis’s co-author in their excellent Trade Wars are Class Wars, expands on their diagnosis in his excellent Overshoot newsletter. As Matt Klein points out, China and the US’s mirror-image responses to the COVID crisis have resulted in mirror-image current account movements. The US stimulated consumption, whereas China relied on infrastructure spending. America’s surging deficit matches China’s mounting surplus.

But the current account is only one side of the balance of payments.

By accounting identity, a trade surplus large enough to create an overall current account surplus must go hand in hand with a build-up of claims on the rest of the world economy on the capital account. This could take several forms, each of which has its own political economy.

In a state-managed system like China’s, with exchange controls regulating the flow of currencies across Chinese borders, the counterpart to a large trade surplus could be the accumulation of forex reserves in official hands. Or it could take the form of private transactions, a private capital outflow, which results in the accumulation by Chinese households or firms of net claims on foreign assets. To offset a current account surplus it is net changes on capital account that matters – the balance of Chinese claims on the rest of the world and foreign claims on China – so the counterpart to a current account surplus could also be a reduction of foreign claims on China, the result being a net shift “in China’s favor”.

The current and capital account are linked by accounting identity – the balance of payments must by definition balance. But capital flows are not simply reflections of trade flows. They have their own logic, governed by interest rate differentials, investor confidence and expectations of future profit. As the Fed tightens interest rates to combat inflation this moves investor to shift money towards the United States. In 2020 Chinese government bonds enjoyed a yield premium over their US rivals. That is no longer true.

Given America’s rapid recovery from the COVID shock, surging prices and huge trade deficit, a tightening of monetary policy is what conventional macroeconomics would prescribe. By attracting foreign capital this should facilitate both the financing and the eventual equilibration of the trade imbalance. But political factors give the development of China’s capital account in the last six months a particular coloration, at least in the eyes of many Western observers. Chinese investment abroad raises more and more overt political questions. Meanwhile foreign investors in China have to weigh the opportunities on offer against mounting anxiety about the policies of Xi’s regime and tension between China and the West.

So how does China’s capital account stand in relation to the giant trade surplus? What has not happened in 2022 so far, is a surge in Chinese foreign investment commensurate with its trade surplus. Chinese investment abroad, as for instance through One Belt One Road, has been run down in recent years. Furthermore, Chinese money is increasingly unwelcome abroad.

The movement of China’s reserves in recent years has been obscured by large transactions taking place on the balance sheets of policy banks. A substantial chunk of dollar earnings may be parked there, but pinpointing precisely where requires forensic accountancy.

Another possible avenue to offset the trade surplus on the capital account would be for Chinese households to acquire claims on foreign economies, whether through tourism, or the purchase of foreign assets. Before 2020, China’s growing tourism deficit was a major item in its balance of payments. Outflows on the tourism account were so large that many suspected that they hid substantial amounts of surreptitious capital flight.

Since 2020 Xi’s zero-COVID policy has put paid to easy flows of people and money across China’s borders. Meanwhile, the regime regards private outflow with increasing considerable suspicion. It is increasingly watchful of any sign of disloyalty and it is haunted by the memory of the near-miss crisis of 2015-6 when a tightening of monetary policy in the US coincided with a sudden loss of confidence in China’s economic growth and a dramatic outflow of Chinese reserves.

Today, confidence may be weaker still than it was in 2015-6. The incentives for rich Chinese to get at least some of their money out of the country are stronger. But the controls on capital outflows that were put in effect in response to the 2015-6 crisis are highly effective. The personal exchange quote of $50,000 per year is tightly policed. China has extended its oversight to overseas casinos, underground banking and bitcoin transactions. High-net worth individuals face long delays in processing passports. Chinese regulators survey business investment plans overseas with an eagle eye. The State Administration of Foreign Exchange has publicly committed to guarding against any risks to the exchange rate from “cross-border capital flows”. As Bloomberg reports:

Chinese regulators have been asked to exercise greater caution when it comes to reviewing new overseas spending and investment plans amid concerns among senior leaders that higher US interest rates could spur capital outflows … State-owned companies were similarly told that they should be cautious when spending and investing overseas, said the people who asked not to be named because they’re not authorized to discuss the matter publicly. No specific targets or limitations have been set on such expenditure abroad, they said.

So, if Chinese households and firms are blocked from acquiring additional claims on the world economy, the other way for the balance of payments to balance, is for foreigners to shed claims on China. And that is what seems to be happening.

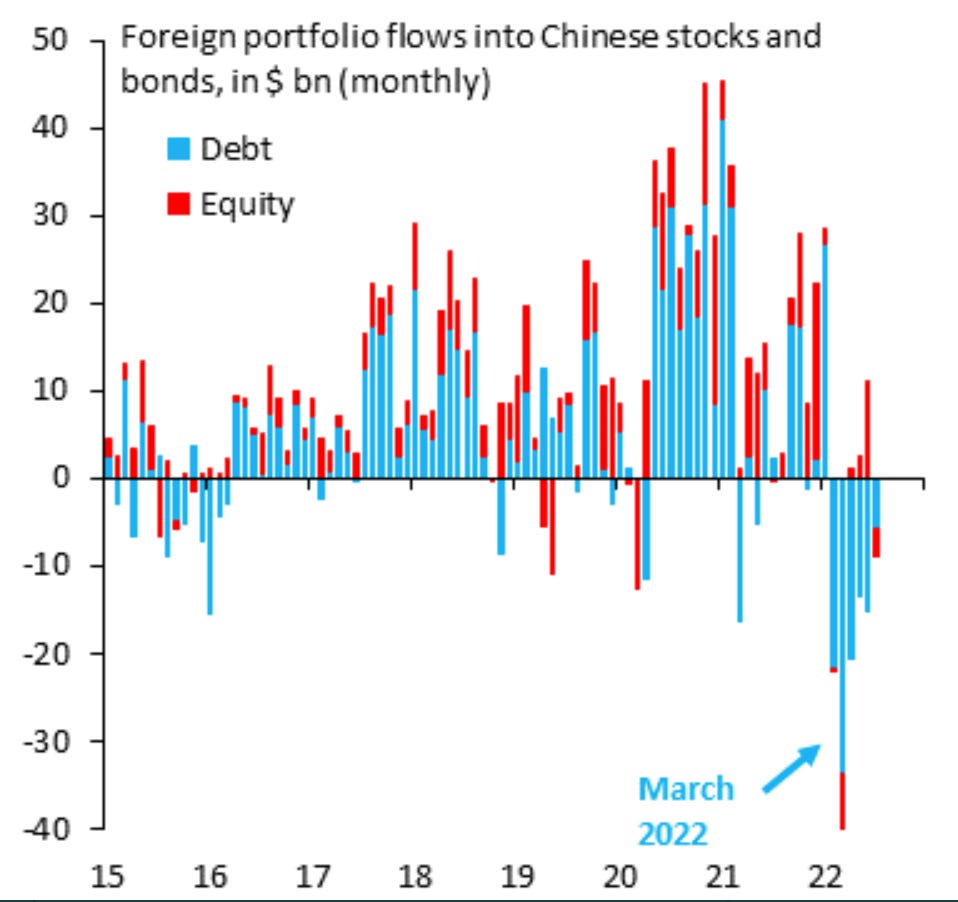

Since the start of 2022 Robin Brooks and his team at the IIF, which, as the trade body of global finance has a privileged insight into capital flows, have been tracking a dramatic reversal in foreign portfolio flows into China. There are some valuation effects in these numbers, as Chinese equity markets have sold off, this reduces the value of foreign claims. But, even allowing for these effects, on net, foreign investors have been off-loading Chinese debt and equities at record rates.

Source: Robin Brooks Twitter (AN ESSENTIAL FOLLOW)

The more benign view is that this sell-off is an effect of shifting interest rate differentials and relative growth rates. The Fed’s interest rate moves are a game-changer. China is not the only export surplus East Asian economy to be experiencing outflows. South Korea, India and Thailand have all been under pressure.

Admitting the grave situation, former vice-finance minister of China, Zhu Guangyao said that “the current US monetary policy adjustment is undoubtedly unprecedented in terms of scale and pace and this is the biggest pressure we are now facing.”

Though the outflows are substantial, they are modest relative to existing stocks of asset holding. China’s trade surplus and its tough foreign exchange controls means that it is not at risk of a dramatic devaluation that could trigger a comprehensive loss of confidence and large-scale capital flight.

One could downplay the data as a largely technical development. But since the outflows began in early 2022, at the same time as Putin’s attack on Ukraine, Western observers have put a far more dramatic and political interpretation on the capital flow out of China.

As one Indian source points, out there may be a direct connection between the war and Chinese capital outflows which has to do with Russian reserve liquidation.

Russia also sold part of its estimated USD 70 billion in reserves allocated to China which was also partly responsible for the huge outflow.

But, significant as this may be, it can account, at most, for only part of the flow.

The tone for Western commentary is set by the IIF itself, which publishes the data, on which reporting of the issue has heavily relied.

As Nikkei Asia comments hawkishly.

Investors are not simply adjusting positions for the short term, but reviewing their long-term strategy as they begin to pay closer attention to China’s political structure and value system –“We are debating whether we should keep investing in China when concerns are mounting about a possible Chinese invasion of Taiwan,” said an official at a leading Japanese pension fund, an active investor in Chinese securities. The exodus marks a sharp contrast to the last few years, when investment in Chinese securities shot up as markets opened and stocks from the country were included in global benchmark indexes. The ratio of Chinese and Hong Kong stocks in major emerging market funds rose to just under 40% a few years ago from little more than 10% in 2008. But that has since (by the spring of 2022) fallen back to 29% due to the triple whammy of the COVID-19 pandemic, tougher regulations on information technology and the Ukraine war. C

As an alternative to China, Nikkei touts friendshoring in finance:

ETFs linked to the Freedom 100 Emerging Markets Index, which uses the degree of a nation’s political and economic freedom as key allocation metrics, logged its largest ever inflow in March at $53 million. Norway’s sovereign wealth fund, the world’s largest, has decided to remove leading Chinese sportswear company Li-Ning from its portfolio in the face of alleged human rights violations. The price of Li-Ning shares fell just over 10% last month.

The Economist takes a similarly dramatic view of the balance of payments data for H1 2022. In its view what is off-putting to global investors is the increasingly “ideological” character of Xi’s regime:

The combination of a nosediving housing market and Xi Jinping’s uncompromising zero-covid policy is just one recent conundrum that has led foreign fund managers to question whether China is losing its pragmatic approach to managing the economy. Mr Xi’s insistence on using prolonged lockdowns to rid China of the Omicron variant and his backing for Russia’s war in Ukraine strike many investors as ideological. Add in the timing of his crackdown on tech groups such as Alibaba, an e-commerce company, and on the leverage of property giants such as Evergrande, and it is not hard to see why some of the world’s largest investment groups are questioning the quality of leadership in Beijing. …

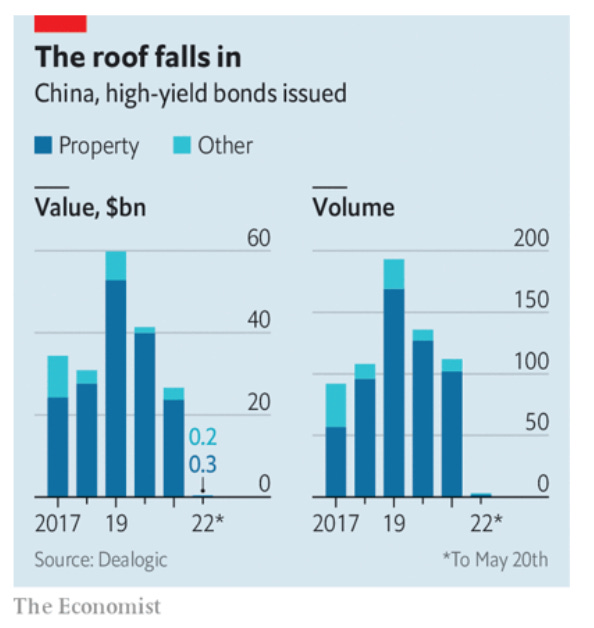

In little over a year Mr Xi’s policies have had a profound—and painful—impact on global markets. They have knocked $2trn from Chinese shares listed in Hong Kong and New York. Chinese initial public offerings in these two cities have nearly ground to a halt this year. China’s property firms have sold just $280m in high-yield dollar bonds so far in 2022, down from $15.6bn during the same period last year.

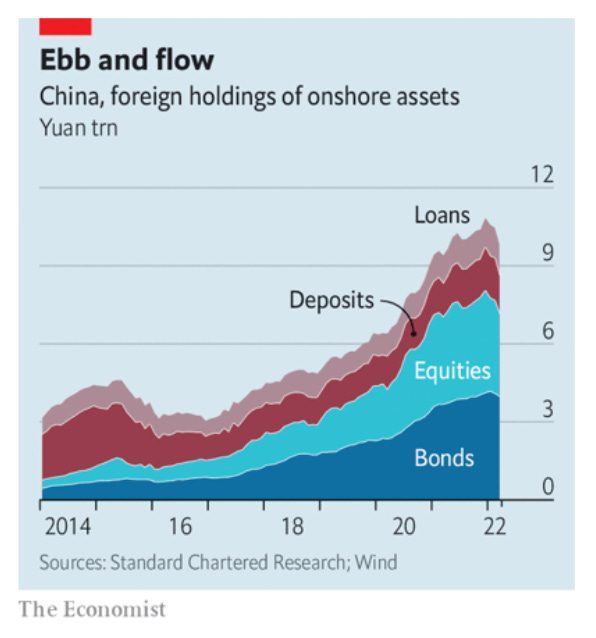

Onshore markets were one of the linchpins of China’s relations with the outside world. The belief that they would continue to open up helped to maintain links with Western financiers hoping to strike it rich. Even as relations between America and China soured during the Trump years, a craving for onshore securities took hold of many of the world’s biggest financial groups. As a trade war dampened global sentiment, regulators in Beijing began expediting long-promised reforms, eventually allowing foreign financial groups to wholly own their onshore businesses.

The policies were a clear sign that Beijing meant business. And the West reciprocated. In 2018 msci added Chinese shares to its flagship emerging-markets index. Other index inclusions followed, creating a flood of foreign capital into onshore Chinese securities. Between the start of 2017 and a peak at the end of 2021, foreign financial exposure to yuan-denominated assets more than tripled to 10.8trn yuan.

That elation has fizzled. … The view from many investors is that, although China has never been more open to foreign capital, it has also not been this ideologically inflexible in recent memory. … Some leading investment groups are starting to air these views in public. BlackRock, a giant asset manager that has been expanding rapidly in China, said on May 9th that it had shifted its six- to 12-month view of Chinese equities to “neutral” from “modest overweight”.

What the Economist now fears is that a pessimistic doom-loop could take hold, with foreign skepticism undercutting those in China who still want to pursue a strategy of opening up:

The gloomy mood has been painful for China’s small and diminishing cohort of liberal technocrats, who are still promoting the idea of an open China that is at least mildly sensitive to the concerns of global investors. For years regulators have used carefully timed reforms to reward loyal long-term investors. As sentiment soured in April they succeeded in delivering long-awaited private-pension reforms in an attempt to woo asset managers. It was a salve regulators had been holding on to, in the expectation that sentiment would worsen early this year, says one fund manager.

It does not help that steps towards opening are “balanced” by repeated assertions of discipline by Beijing. As Al-Jazeera reports:

Last month, the China Securities Regulatory Commission formally issued guidelines mandating the establishment of communist party cells within global hedge funds that operate in China. “I think it will be problematic, but mostly because of the optics back at headquarters in the US,” Gibbs said, noting that many hedge fund managers specifically asked him about the measures at a recent conference he attended in San Francisco. “Those of us who operate in China long term understand the role the party plays and the importance of aligning with their goals for society. Actually, the conversations they have with you are often about issues of social compliance, like labour standards or equality, which is not necessarily a bad thing,” Gibbs added, describing the scrutiny as comparable to “Chinese-style ESG [Environmental, social and governance]”. “But in the US, we see the CCP [Chinese Communist Party] and think of the whole party apparatus, and so the idea of a party official in the boardroom sounds much scarier from an American perspective.”

***

Will financial decoupling gather pace, or will the first half of 2022 prove to be a temporary reversal of the longer-term trend towards integration? Clearly it is premature to reach conclusions.

Certainly a disorderly unwinding – a 2015-6 style shock writ large – with foreign investors leading Chinese money to the exit, seems unlikely. The memory of that incident is still too fresh and is crucial to informing a policy of tight controls.

Relief may also come from an unwinding of the tense constellation of 2022.

If the US economy slows over the rest of 2022 and into 2023, the Fed may pull back from tightening which will relieve pressure on the entire world economy. China’s growth may recover. After Xi’s election to third term on 20 October zero-COVID may be relaxed.

Beijing may continue to expand on the inducements offered to foreign investors, especially those operating in the financial sector. Mounting global tension and political concerns about Xi’s regime are a deterrent, but there is still ample scope for capital reallocation and deepening integration. Beijing has recently launched Swap Connect, a mechanism to allow overseas investors to participate in mainland China’s financial derivatives market. ETFs are being opened to investors through Hong Kong. Beijing is providing larger currency swap lines to support the liquidity of offshore yuan markets.

What 2022 makes clear, however, is that the direction of travel is open as never before. Up to now, Chinese trade surpluses – which as Pettis and Klein remind us can be the result of weakness as well as strength – have gone hand in hand with the deepening of Chinese integration into the world economy. They have led to an accumulation of huge Chinese claims on the rest of the world economy which outweighs the large claims that foreign investors have made in China at the same time. But, aA 2022 has demonstrated, a current account surplus can also go hand in hand with uncoupling, as foreign claims on the Chinese economy are unwound.

Of course this is sustainable only so long as there are foreign claims to unwind. But since foreign holdings of Chinese bonds and equities run to over $1.2 trillion, unwinding that pile of commitments may take some time.

****

I love putting out Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

August 5, 2022

Ones & Tooze: Is A Strong US Dollar A Good Thing?

In this episode Cameron and Adam discuss how the US dollar has reached near parity with the Euro and is the strongest it’s been in nearly two decades. The two review what that means for exports and imports and what it says about the overall strength of the US economy. Plus a look at how some Americans are finding it cheaper to buy homes in Europe rather than the US and what that says about the housing markets at home and abroad.

Find more episodes and subscribe at Foreign Policy

August 3, 2022

Chartbook #140: China-Taiwan-Pelosi special

Crashing Weibo

US House Speaker Nancy Pelosi’s visit to Taiwan briefly crashed Weibo, the Chinese equivalent of Twitter, as millions in the country discussed and debated her Asia trip. The microblogging platform apologized for a half-hour outage of its mobile app in the period immediately before Pelosi’s landing at 10:40 p.m. on Tuesday, when countless messages tracking her plane flooded social media.

Source: Bloomberg

Why is Pelosi going to Taiwan?

I found these three pieces particularly illuminating as background.

BBC on Pelosi’s long history of clashes with Beijing.

28 years ago, we traveled to Tiananmen Square to honor the courage & sacrifice of the students, workers & ordinary citizens who stood for the dignity & human rights that all people deserve. To this day, we remain committed to sharing their story with the world. #Tiananmen30 pic.twitter.com/7UqiJVRS3t

— Nancy Pelosi (@SpeakerPelosi) June 4, 2019

Andrew Desiderio at Politico on the making of a progressive hawk.

The FT added a constitutional angle:

“She has a long record of not bowing to Chinese pressure and feels passionately about upholding the principle of Congress being a co-equal branch of government,” Hass said.

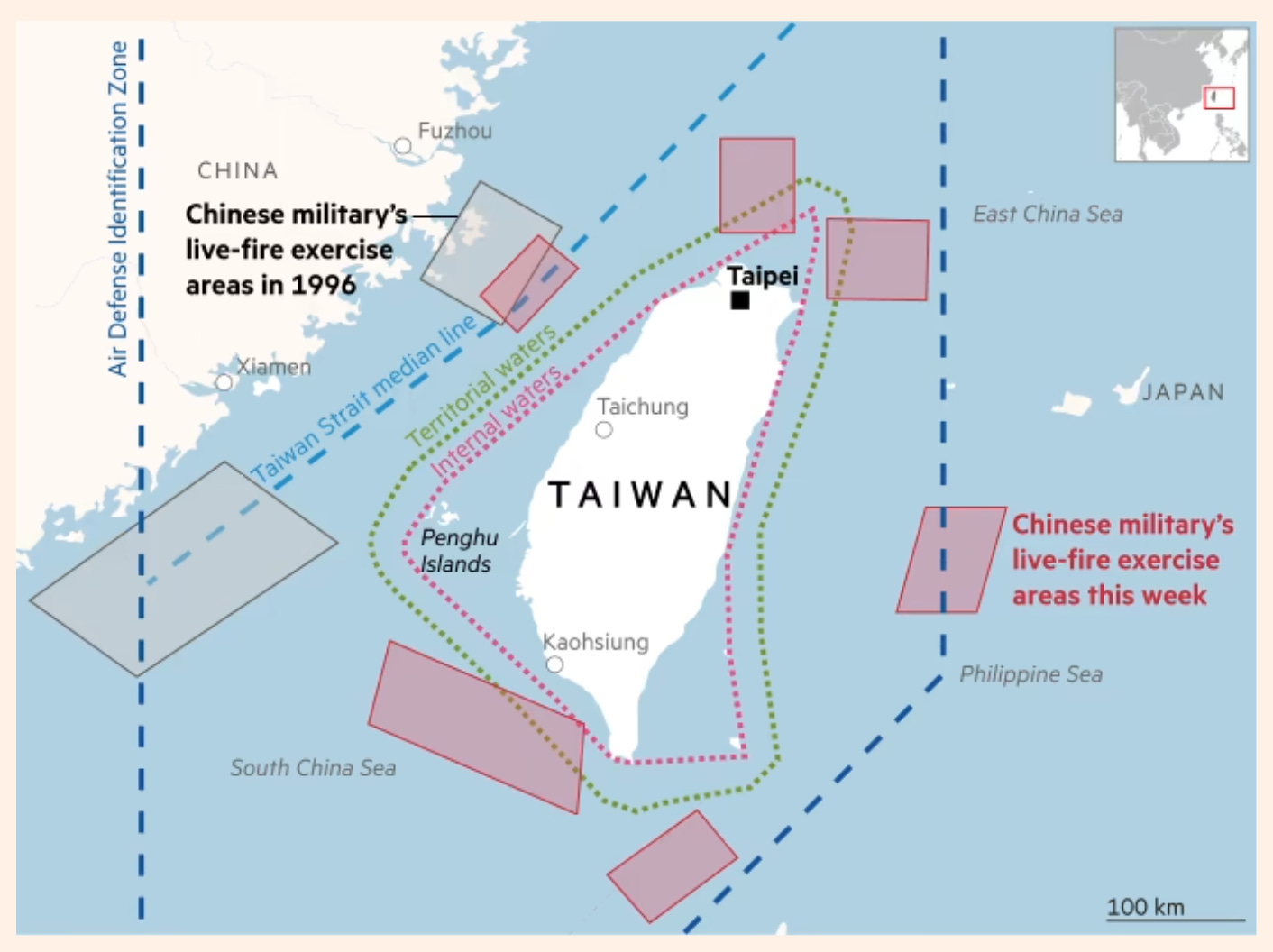

Extent of China’s military exercises around Taiwan has massively expanded since 1996.

Source: FT

Economic Fall Out

Hal Brands wrote in June that the economic fallout from a Taiwan invasion would make Ukraine’s ructions feel like a ride on Taylor Swift’s jet in comparison.

That seems about right!

Waterways

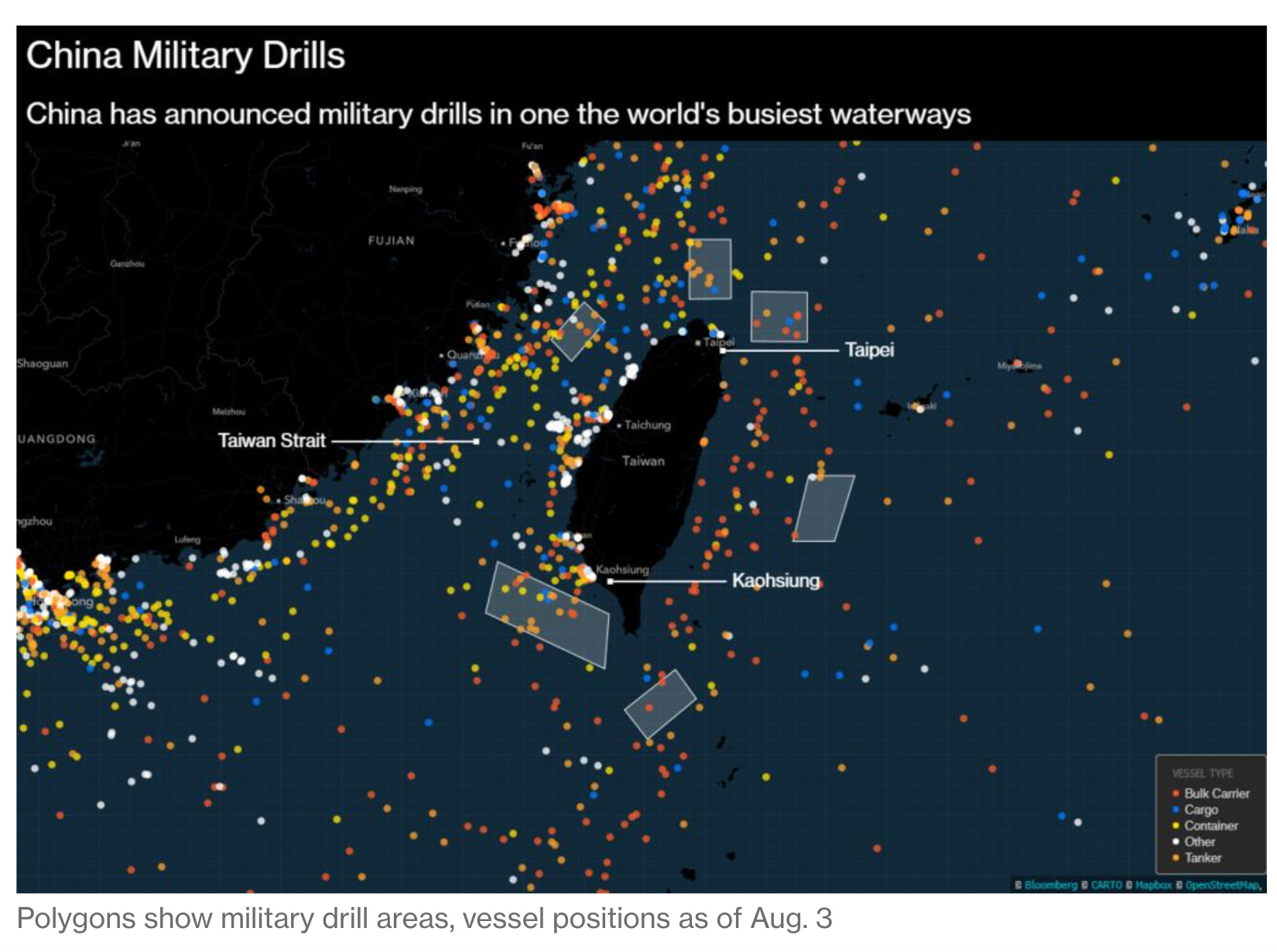

China’s military drills are not just far more expansive than in the 1990s, they are taking place in some of the world’s busiest seaways.

US Bond market ricochet

John Authers at Bloomberg, as ever excellent

Yields have dropped precipitously in recent weeks, despite the lack of any clarity that inflation is over. And that led to an extraordinary trading session Tuesday as they boomeranged back upward. House Speaker Nancy Pelosi can claim a starring role with her fraught visit to Taiwan. Barring only the two worst days of the first Covid shutdown, and the Monday in June when the Fed leaked its intention to hike by 75 basis points at its next meeting, this was the biggest daily gain for 10-year yields in five years:

China’s stock markets

Despite the nationalist outbursts on weibo, the Chinese stock markets have not enjoyed the war scare.

Source: Daily Shot

China’s sliding into recession?

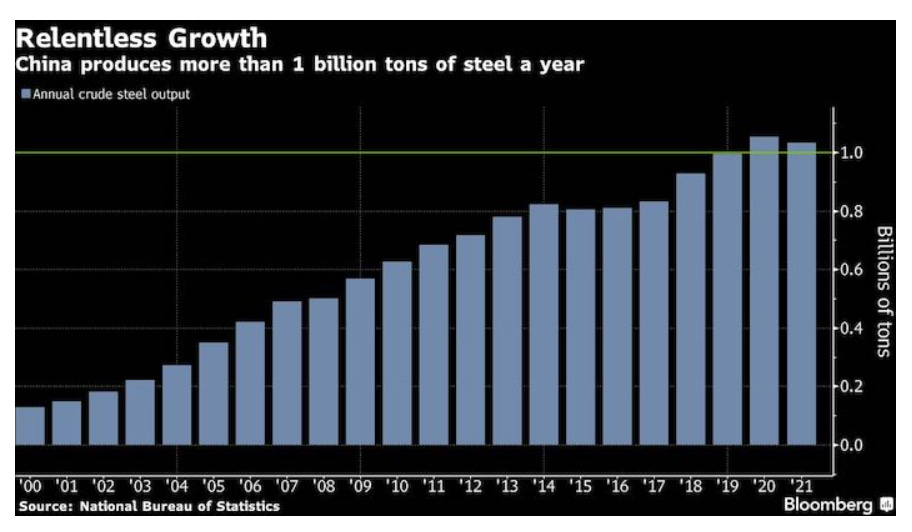

Beyond the Taiwan scare, the outlook for the Chinese economy is increasingly grim.

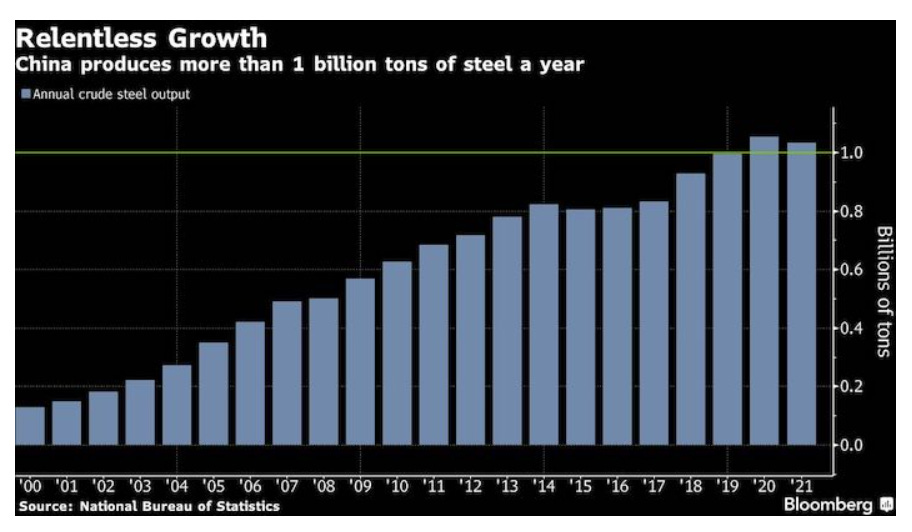

As the real estate sector goes into crisis, one of the principal industrial victims is the steel industry. The growth in the sector from the 2000s was a spectacular industrial revolution. Now the sector is in deep trouble.

As Caixin reports:

China’s steel industry is entering a precarious new era as a worsening property crisis imperils demand and Beijing’s construction-led growth model looks increasingly untenable. Almost a third of China’s steel mills could go into bankruptcy in a squeeze that’s likely to last five years, Li Ganpo, founder and chairman of Hebei Jingye Steel Group, warned in June at a private company meeting. “The whole sector is losing money and I can’t see a turning point for now,” he said, according to a transcript of the gathering seen by Bloomberg News.

Taiwan’s robust growth

If real estate & steel are the critical domestic policy issues for Beijing, the main battlefield between China and the US, in which Taiwan is a key are, are microchips

Out of the limelight, as Caixin reports, the Biden administration is progressively tightening the noose on China’s microchip sector by widening the bans on equipment exports to China from 10 nm to the much more prosaic 14 nm generation of chips.

Chip crackdown

Beijing is carrying out a fierce crackdown on executives and bureaucrats tied to the microchip industry. A series of investigations have targeted senior figures associated with Tsinghua Unigroup Co. Ltd.

Caixin: The head of China’s biggest semiconductor investment fund is under investigation in the latest of a series of graft scandals rattling the state-backed fund. Ding Wenwu, president of China Integrated Circuit Industry Investment Fund, has been probed by authorities and remained out of contact, several people with knowledge of the matter told Caixin. The fund, known as the “Big Fund,” is a key part of China’s drive to develop its homegrown integrated circuit industry to reduce reliance on imported technology.

Caixin: Two more senior executives of China’s Tsinghua Unigroup Co. Ltd. face investigations as the debt-laden semiconductor conglomerate wraps up a bankruptcy reorganization.

From shortage to glut

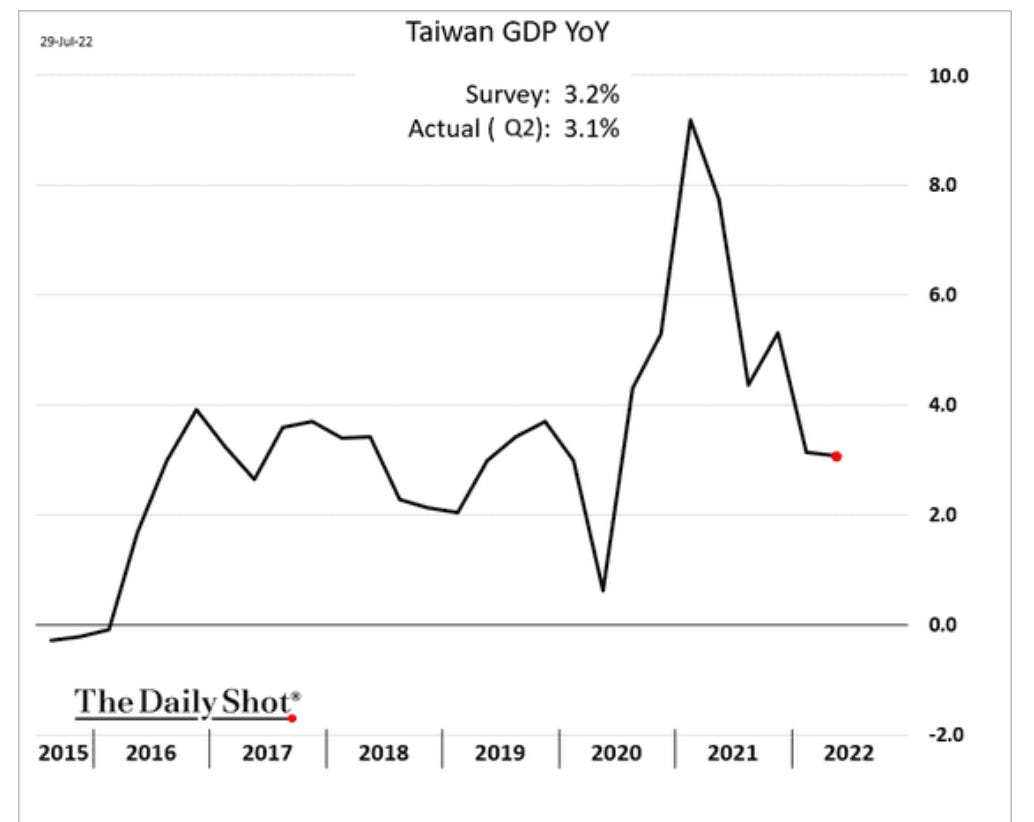

Right now the Taiwanese economy is buoyed by dramatic recovery growth. Though much slower than China’s, growth has remained robust through Q2 2022.

Source: Daily Shot

But, looking forward as the Chinese economy slows, this is very bad news for Taiwan.

The U.S. and the Chinese mainland are Taiwan’s two largest export markets, which combined account for just over half of the island’s overseas shipments. An economic slowdown in the U.S. has sparked recession talk as officials struggle to rein in the highest inflation in 40 years without cratering the economy. The Chinese economy, meanwhile, has been weighed down by ongoing Covid outbreaks and resulting regional lockdowns, leading economists to downgrade their forecasts for growth in 2022 to 3.9% in a recent Bloomberg survey.

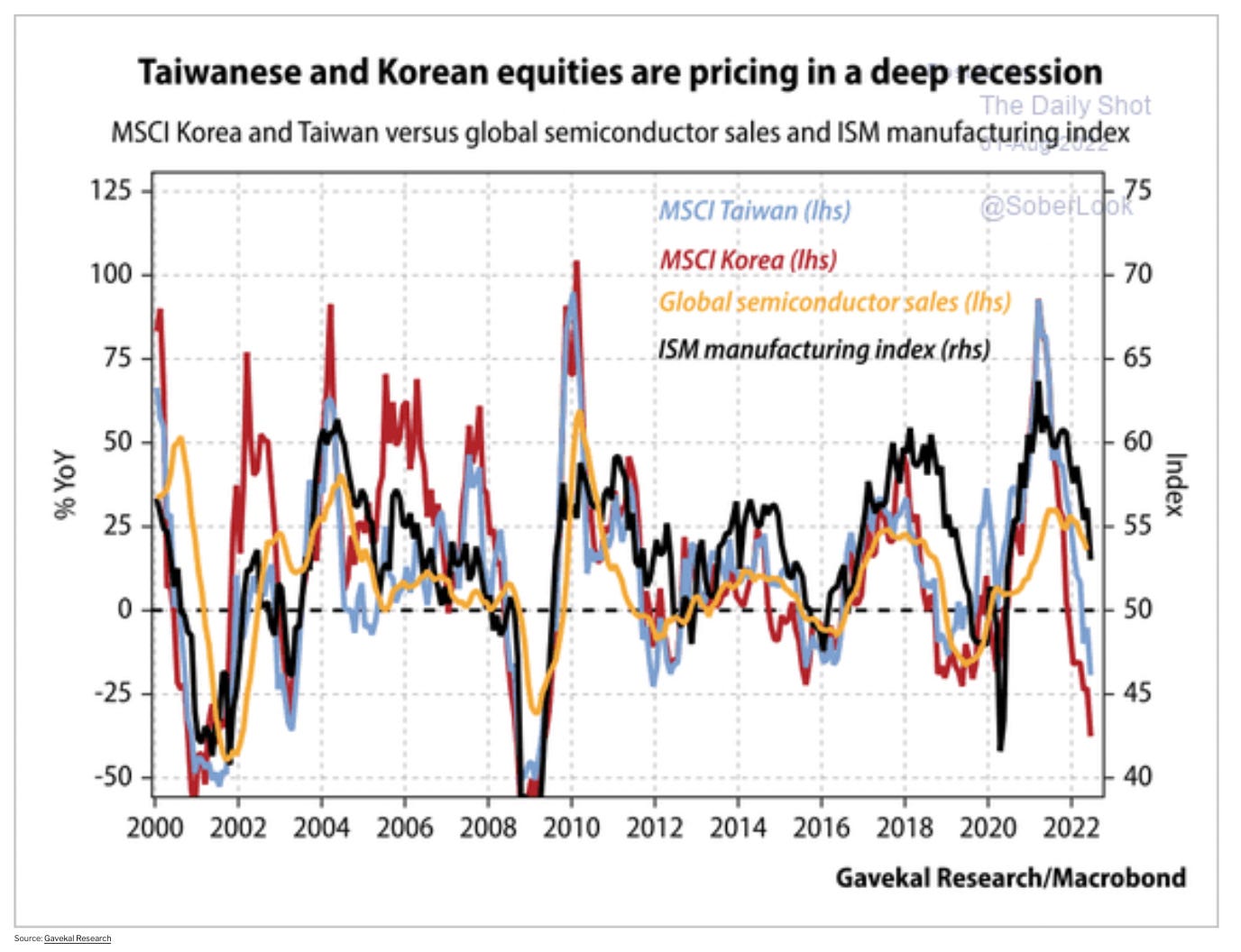

Taiwan’s export-driven growth may be about to come to an end.

Looking ahead, both Taiwanese and Korean equity markets are pricing in a slump in microchip demand to come.

Source: Gavekal via Daily Shot

The economic upshot? In the second half of 2022 we may see both Europe and East Asia struggling with serious recessionary and deflationary pressures.

August 2, 2022

Chartbook #139 The battle for climate legislation in the US: making sense of the Manchin-Schumer compromise

Passing climate legislation in the US is an attritional business. Clinton tried and failed. Obama tried and failed. Until the last week of July it seemed that Biden was doomed to fail too.

The House had signaled its clear support for big legislation last year, including a raft of climate measures in a $1.75 trillion bill. But in the finely balanced situation with the Republicans in dogged opposition it was the Senate that counted and, there, the West Virginia Senator and coal baron Joe Manchin stepped up to play the part of villain.

In an eight month ordeal he forced the scrapping of clean air standards. He also shot down plans for bigger tax credits for consumers who bought union-made electric vehicles, a measure that was opposed by Toyota Motor, which operates a nonunion plant in West Virginia. In December he announced he simply could not vote for a bill of major spending. When he returned to the table, he sliced away at the fee imposed on oil and gas operators for leaks of methane. He rejected an early plan by Democrats to permanently ban oil drilling in the Atlantic and the Pacific. With the Ukraine war raging and energy prices surging, Manchin became ever more adamant in his backing for fossil fuels. Then, finally, within a few feet of the finish line, in mid-July Manchin slammed the door.

On July 13th the US inflation print hit 9.1 percent. The following day Manchin declared that he could not support what was left of the Build Back Better Bill. Amongst wailing, tearing of hair and gnashing of teeth, the Biden administration’s climate policy was declared dead. Several of us wrote obituaries and a mini-debate began about how to understand the failure of the Biden administration.

Then Manchin pivoted once more. On 18 July behind closed doors, secret negotiations resumed between Manchin and Schumer, which on Wednesday 27th produced a remarkable new compromise. Build Back Better was dead. But much of its climate-substance now returned in the form of the Inflation Reduction Act. The announcement came on the day that the Senate also voted through CHIPS act. Whereas ten days earlier the Biden administration had appeared dead in the water, it now seemed possible that the Democrats would pass two major pieces of legislation ahead of the summer recess and the midterms.

The Manchin-Schumer compromise in the draft Inflation Reduction Act includes:

$260 billion in clean-energy tax credits; $80 billion in new rebates for electric vehicles, green energy at home and more; $1.5 billion in rewards for cutting methane emissions; $27 billion ‘green bank’ for a federal green bank to complement the 23 that already exist across the US; support for coal miners with black lung

All told, Democrats estimate the bill will bring in $739 billion in revenue and will invest $433 billion in spending. The result will be to reduce the deficit by in the order of $300 billion. The large-scale pledges on climate spending are flanked by provisions that will force through $288 billion in savings on Medicare expenditure, at the expense of the pharmaceutical industry, a three year $64 billion subsidy to support Obamacare and a $2000 cap on out of pocket costs for seniors on Medicare.

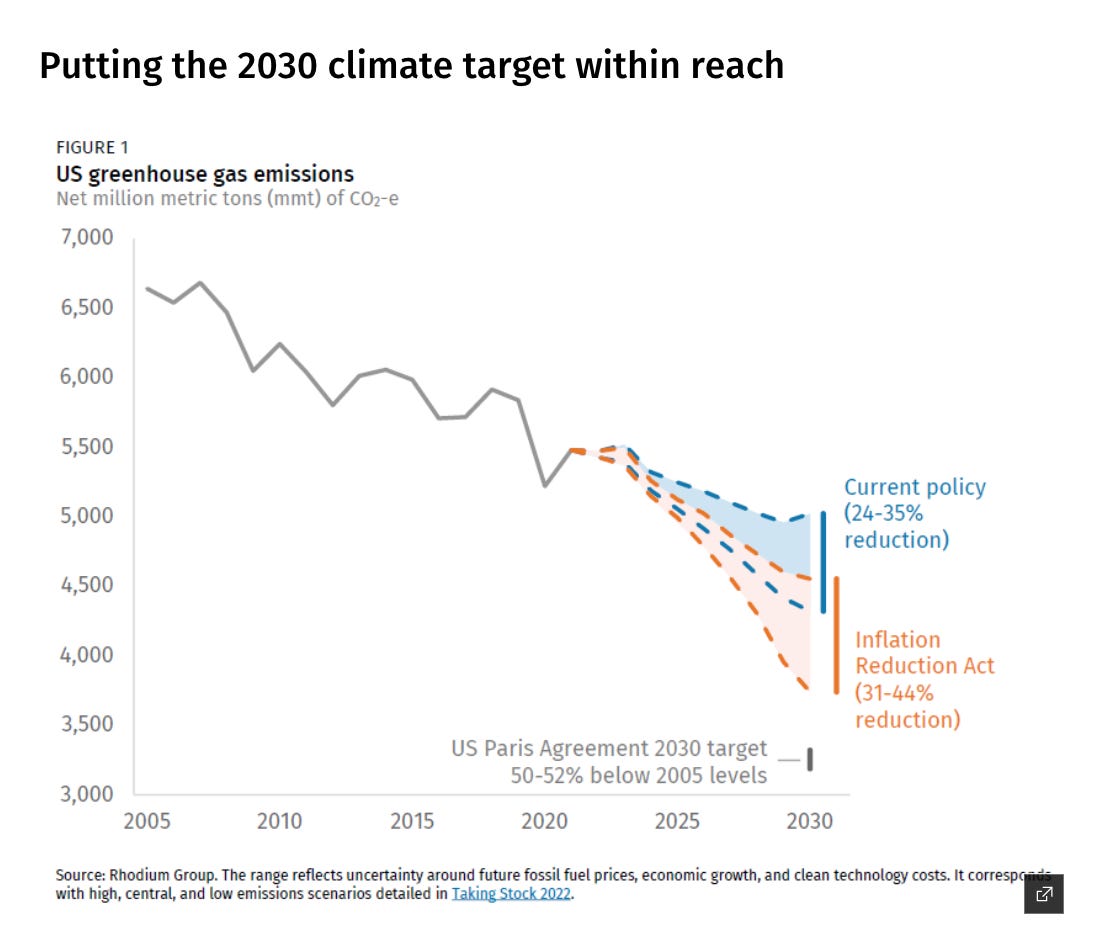

If it passes, the IRA will be the largest piece of climate legislation that Congress has ever approved. As has been true throughout the arduous process of legislative drafting, the impact of the Inflation Reduction Act on emissions was immediately modeled by climate think tanks. In this respect 2021-2022 marks a new era in US economic policy. The Rhodium’s group conclusions are broadly sanguine:

The array of clean energy tax credits has the greatest impact on emissions. Long-term, full value, flexible clean energy tax credits for new clean generation and retention of existing clean generators are roughly in line with the scenarios we examined in prior research. Long-term tax credits for carbon capture, direct air capture, clean hydrogen and clean fuels provide a launch pad for these key technologies to scale and build on the investments of the IIJA hub and demonstration programs. Federal investments have the potential to generate multi-megaton scale natural carbon removal in soils and forests. Long-term electric vehicle (EV) tax credits will accelerate the diversification of passenger vehicles away from their over-reliance on petroleum, though the EV credits included in this bill are scaled back from previous proposals. Manufacturing tax credits and investments will help diversify supply chains, expand domestic capacity to produce the clean technologies the world needs to achieve deep decarbonization, and can help enable the record levels of wind and solar deployment we project in our modeling. Our preliminary assessment of the IRA is that its policies, including the new leasing provisions, reduce net GHG emissions by 31% to 44% below 2005 levels in 2030 (Figure 1). … If Congress passes this package, additional action from executive agencies and subnational actors can put the US’s target of cutting emissions in half by 2030 within reach. … Put simply, the IRA has the potential to be the biggest climate action ever taken by Congress.

****

Quite suddenly, as one House member put, the Democrats are “at the precipice” of actually getting something done.

How did this happen? How did a Presidency that seemed stalled, suddenly recover momentum. Why did commentators, myself included get it wrong? It isn’t fun to revisit bad calls, but honesty demands some kind of reckoning with this disorientating experience. How do we make sense of this switchback?

First thing to say, is that Manchin’s surprises really do seem to be surprises even for those very close to the process. The heartbreak and shock that Manchin engendered twice over, in December 2021 and July 2022, is genuine. Each time his change of heart seems to be last-minute and counter to expectations.

So labyrinthine was the process of negotiations between Manchin and Schumer that some are convinced that it is part of a 5-dimensional chess game that the Democrats have been playing to outwit McConnell and the GOP.

That would be reassuring. It would imply tactical control. If true it would also imply something weird about the US political system: given the GOP roadblock, the best way for the Democrats to pass any legislation is to appear as though they have checkmated themselves, allowing them to attract GOP support for bipartisan bills, before unleashing a partisan ambush to pass the all important reconciliation legislation. The outcome may be pleasing. But this is a crazy way to conduct public affairs.

Pleasing though this theory may be, it also does not chime with the understanding of those closest to the process. Rather than a successful manipulative tactical game, something closer to the reverse seems to have transpired. After Manchin’s veto on July 14th it really did seem as though Biden’s legislative agenda was dead. The realization of that shock, the sense of despair widely shared across the Democratic camp, echoed and amplified by the commentariat, triggered a rally. Biden’s Presidency was in peril. It was time to act.

In the tense negotiations between 13th and 14th of July tempers had frayed. As Manchin tells it, he and Schumer reconnected the following week:

“By Monday we ran into each other again. I (Manchin) said, ‘Are you still upset?’ He (Schumer) said, ‘I’m very discouraged.’ I said, ‘Well, you shouldn’t be. Something positive could be done if we all want to work rationally,’” Manchin said, recounting the key moment. He said their staffs started working together in earnest the next day, July 19. They finally hashed out a deal on Tuesday evening (26th), recognizing they had to announce the package on Wednesday if it had any chance of passing before the scheduled start of a lengthy summer recess on Aug. 6. … It just so happened the timing aligned perfectly with Schumer’s plan to hold a vote on final passage of the chips and science bill at noontime Wednesday. Republicans who voted for tens of billions of dollars for the domestic semiconductor manufacturing industry and the National Science Foundation were outraged and felt betrayed. Sen. John Cornyn (R-Texas), a key player in getting the chips and science bill passed, said he received “assurance privately from some Democrats, including the staff of the Senate majority leader, that the tax and climate provisions were off the table,” which Republicans said would be a precondition for moving the chips bill. Cornyn took to the Senate floor Thursday afternoon to rail against the secret climate and tax deal. “How can we negotiate in good faith, compromise where necessary, and get things done together after the majority leader and the senator from West Virginia pull a stunt like this?” he said with rising exasperation. “To look you in the eye and tell you one thing and to do another is absolutely unforgivable.”

Source: The Hill

Interestingly, both Manchin and Schumer preferred to hold the White House at arms length. They did not wish to repeat the direct negotiations between Manchin and Biden in 2021 which ended in failure and public recriminations after months of fruitless talks.

“President Biden was not involved,” Manchin told West Virginia MetroNews. “I was not going to bring the president in. I didn’t think it was fair to bring him in. This thing could very well have not happened at all,” he said, explaining he didn’t want to involve the president in case talks fell apart again.

What we are witnessing is not a cunning plan but a desperate improvised effort to pull back from the brink. It is the fruit of an effort in crisis-management triggered by the dawning realization of disaster. How was this deal possible?

****

One simple theory is that Manchin remembered that he was a Democrat.

As Manchin described his relationship with Chuck Schumer of New York: “It’s like two brothers from different mothers, I guess. He gets pissed off, I get pissed off, and we’ll go back and forth. He basically put out statements, and the dogs came after me again.” Clearly, Manchin did not want to be blamed for the failure of the Biden Presidency. He has ambitions. He wants to get things done.

Furthermore, at some point, he may have come to the realization that climate measures are actually good politics, even in West Virginia. It is commonly said that American voters do not support climate action, especially with stagflation looming. But that is a claim not strongly supported by evidence. In fact:

Climate action enjoys broad support. Indeed, some climate policies are supported by huge majorities, including Republican voters. A large majority (58 percent) believes the federal government is doing too little to address the problem. As U.C. Santa Barbara political scientist Matto Mildenberger has been pointing out on Twitter, the public favors climate action and rewards it. Furthermore, while Manchin’s West Virginia constituents are more conservative than the national population, polling shows a clear majority of the state’s voters support aggressive clean energy initiatives, and many coal miners supported Build Back Better due to its funding for treatment of black lung disease. So the more plausible explanation for Manchin originally blocking climate action wasn’t because of voters but because he’s a coal baron (coal mine owners opposed Build Back Better). His most recent move—supporting climate legislation and pitching it as an anti-inflation measure—is far closer to a majoritarian position.

Specific policies like a green bank enjoy large majorities even in conservative states.

In Manchin’s homestate of West Virginia, 54 percent of likely voters supported the idea of a national green bank, the survey found, with 31 percent opposing. In Alaska, 68 percent supported the bank and 20 percent opposed. Among oil, gas, and coal workers and their families, support was even higher: 62 percent and 77 percent of them supported a green bank in West Virginia and Alaska, respectively.

And this points to a bigger and broader point. It turns out that though the US may since the 1990s have been the place where climate policy goes to die, the balance may finally be shifting. As Zack Colman, Josh Siegel and Kelsey Tamborrino reported in an important piece in Politico, Manchin’s threat to sink Build Back Better unleashed a furious lobbying effort on behalf of green business opportunities.

When Joe Manchin balked at the clean energy incentives in Democrats’ expansive spending bill two weeks ago, the corporate C-suites and union boardrooms jumped into action. With hundreds of billions of dollars of incentives for manufacturing, electric vehicles, nuclear power and carbon capturing technology hanging in the balance, executives from some of the nation’s biggest companies and labor unions made their case to the Democratic West Virginia senator: The next generation of clean tech needed Washington’s backing to take off. Clean energy manufacturing companies with plans to set up shop in Manchin’s state helped orchestrate the 13-day effort to change his mind …. That push — which two of the people said included a call from Bill Gates, whose venture capital firm has backed a West Virginia-based battery start-up — was taking place alongside a campaign by other senators along with economist and inflation hawk Larry Summers to convince Manchin of the merits of the bill. On Capitol Hill, Democratic Sens. John Hickenlooper of Colorado, Chris Coons of Delaware and Tina Smith of Minnesota continued engaging with Manchin and his staff behind the scenes, …. Duke Energy and Constellation Energy making the case for the clean energy package in the days after Manchin appeared to walk away from the energy and climate measures. A senior executive with a clean power company said his firm communicated with Manchin, Schumer and Senate Finance Chair Ron Wyden (D-Ore.) in the past two weeks “softly reminding them” that “tens of billions of dollars in investment are at stake here.” Ultimately, Summers, the former Treasury secretary under President Bill Clinton, made the case that the climate package would not stoke inflation as Manchin had feared. Economists from the Wharton School at the University of Pennsylvania and deficit reduction advocate Maya MacGuineas, president of the nonpartisan think tank Committee for a Responsible Federal Budget, also briefed Manchin during that period … Jason Walsh, executive director of the BlueGreen Alliance, a coalition of labor and environmental groups, said several West Virginia companies pushed Manchin to back the credits as well — even suggesting failure to pass the bill imperiled their plans to invest in new operations. A senior executive with a utility operating in Appalachia said that his company communicated with Manchin how aspects of the bill such as tax credits to build clean energy manufacturing plants at former coal sites and incentives for developing small nuclear reactors and hydrogen would help West Virginia’s economy. “We know coal plants are ultimately going to close,” the executive said. “What is going to replace them? What are the jobs? What are we transitioning to? … Nucor Corp., the largest U.S. steelmaker, which is building a new plant in West Virginia, also reached out to Manchin’s staff — as did the Carbon Capture Coalition, a cross-sector group that includes labor unions, oil companies and manufacturers, according to a person familiar with the contacts. Form Energy, a battery storage startup backed by Gates’ Breakthrough Energy Ventures and which has plans for a West Virginia manufacturing hub, walked Manchin’s staff through its growth trajectories with and without the proposed suite of legislative incentives, a person directly familiar with the interaction said. … And labor unions also pressed Manchin. The United Mine Workers of America engaged throughout the 13-day period with Manchin’s staff … Brandon Dennison, the CEO of the economic development organization Coalfield Development, pointed to companies like Solar Holler, a West Virginia-based solar installer whose employees are members of the International Brotherhood of Electrical Workers labor union. Dennison said that when he talked to Manchin’s staff in the past two weeks, he made it clear that passing clean energy incentives was about giving West Virginia “a chance to stay an energy state. “If we want to benefit from the investments and the jobs that are going to come with that transition, we need to be part of the proactive solutions and policies rather than constantly playing on defense,” Dennison said. “That’s the case I tried to make.”

What this suggests is that in the future we may look back on Manchin’s pivot in July 2022 as the moment at which the green capitalist coalition in the US had finally gathered sufficient strength to overcome at least the most dogged defense of the energy status quo. As one commentator remarked: “This is a historic climate bill, but it’s also one of — if not the — most significant industrial policy bills of this era”.

Again, West Virginia stands to benefit, as the NYT reports.

West Virginia remains the nation’s second-largest producer of coal, but its mining industry has declined sharply over the past decade as electric utilities have closed hundreds of coal plants nationwide because of competition from inexpensive natural gas and renewable power. Industry leaders said they expected more coal plant closures with the passage of the bill. “Our preliminary estimates indicate that West Virginia would be one of the states with the largest number of coal retirements due to the wind and solar tax credits,” Michelle Bloodworth, chief executive of America’s Power, an industry trade group, said in a statement. But these days, there are more former coal miners in West Virginia than current coal miners, and the bill will undoubtedly help them, said Phil Smith, the top lobbyist for the United Mine Workers of America. He praised the permanent funding for the Black Lung Disability Trust Fund as well as the tax credits for carbon capture, a technology that Mr. Manchin has called “critical” but that has so far struggled to gain traction because of high costs. “If we’re going to have coal industry 15, 20, 30 years from now, it is because we have developed carbon capture and deployed it, that’s just the truth,” Mr. Smith said. “Folks out in the coal fields understand that. And the coal companies understand that.” Mr. Smith said the bill’s $4 billion in tax incentives for renewable energy manufacturers to build their factories in former coal fields would directly help the approximately 45,000 miners nationwide who have lost their jobs in the past decade. … another $5 billion in the package that would allow existing coal-fired power plants to improve their efficiency and adopt environmental controls like scrubbers, which remove pollutants from smokestacks. Those measures to help the coal industry, she noted, come on top of $8.5 billion for carbon capture and storage that Mr. Manchin secured as part of a bipartisan infrastructure bill last year.

But if the Manchin-Schumer bill marks an important shift in America’s political economy, Machin’s interventions have also given that shift a profoundly conservative shape. Most obviously, the Inflation Reduction Act is a fraction of the size originally envisioned for Biden’s legislative initiatives. The Democrats, who once aspired to pass a mammoth $3.5 trillion bill are now cheering a $433 billion package.

The Manchin-Schumer bill is not only shrunken in size. It is conservative in its political framing and larded with concessions to fossil fuel interests. Whereas energy transition was once paired with social radicalism, it is now linked to Manchin’s agenda of energy security, inflation control and deficit reduction.

To claim that the Manchin-Schumer compromise will actually reduce inflation is an overstatement, but according to the influential analysis of the Wharton School it is broadly inflation-neutral.

The analysis, produced by the Penn Wharton Budget Model, finds that the Inflation Reduction Act “would very slightly increase inflation until 2024 and decrease inflation thereafter.” The increase could be as high as 0.05 percentage points in 2024, and could be followed by an estimated 0.25 percentage point fall in the Personal Consumption Expenditures price index by the late 2020s. “These point estimates are statistically indistinguishable from zero, thereby indicating low confidence that the legislation will have any impact on inflation,” write the study’s authors.

The net effect of the bill, according to the Wharton study, will be to reduce the deficit by $248 billion over the budget window.

Included in the bill is a 15 percent corporate minimum tax, which Schumer and Manchin argued will collect $739 billion in government revenue over ten years. Overall, “a decrease in spending on prescription drugs combined with increases in revenues from personal income taxes and business taxes lead to a decrease in government debt will lead to a decline in government debt by 8.4 percent by 2050,” the model says.

Meanwhile, the big news from the fossil fuel industries is that they don’t hate the Manchin-Schumer compromise either.

the legislation contains what some called “Easter eggs” that would benefit oil and gas companies, including access to new swaths of federal waters in Alaska and the Gulf of Mexico. … Those leasing provisions alone would offer a win for oil and gas companies that are feuding with the Biden administration over Interior’s slow pace of fossil fuel lease sales, one lobbyist for the industry said. Meanwhile, the bill’s proposal to charge a fee of up to $1,500 a ton for the petroleum industry’s emissions of methane, a potent greenhouse gas, would be less of an issue for large oil companies already working on reducing them, industry analysts said.

As one lobbyist remarked:

“The Easter eggs that Manchin forced into the bill on leasing, they’re a big deal. If you squint hard enough, you can see this being a bipartisan compromise.” The bill would also make it easier for businesses to use a tax credit for deploying technology that captures and stores planet-warming carbon emissions, which has become big business for companies like Exxon Mobil and Chevron. … “If enacted … this package would provide the most transformative and far-reaching policy support in the world for the economy-wide deployment of carbon management technologies,” Madelyn Morrison, spokesperson for the advocacy group Carbon Capture Coalition, said in a prepared statement. … Oil company BP said the deal offers a lot to like for oil companies that are extending their reach into renewables, carbon capture and other forms of alternative energy. … “We applaud Senate lawmakers for making progress toward a historic climate deal,” BP spokesperson Josh Hicks said in an email. “BP has actively advocated for Congress to pass strong climate legislation, including the full suite of clean-energy and low-carbon tax credits the U.S. House passed in 2021. We will continue engaging constructively with policymakers to advance these measures as we aim to become a net zero company by 2050 or sooner.”

Unsurprisingly, the American Petroleum Institute, the trade group representing the largest oil producers in the country, was more restrained in its initial take. But even EXXON’s CEO commented that the legislation as a step in the right direction.

Environmental groups meanwhile are furious at the compromises forced by Manchin.

Under the terms of the deal, the Department of Interior would be required

over the next decade to offer oil and gas drilling leases on at least 2 million acres of public land as well as 60 million acres offshore in any year the department seeks approval of new renewables projects on federal land or waters. That would hold renewables “hostage” to expanded fossil fuel extraction, said Brett Hartl, CBD’s government affairs director. CBD’s Hartl called the IRA a “devil’s bargain that ignores science and locks us into at least a decade of new oil and gas extraction.” In a CBD, press statement, he said, “This is a climate suicide pact. It’s self-defeating to handcuff renewable energy development to massive new oil and gas extraction. The new leasing required in this bill will fan the flames of the climate disasters torching our country, and it’s a slap in the face to the communities fighting to protect themselves from filthy fossil fuels.”

Erich Pica, president of Friends of the Earth, commented

“The Inflation Reduction Act may be the most Washington can offer right now, but it’s a far cry from what’s actually needed to address the climate crisis. The investments in renewables, energy efficiency and Superfund clean-ups will make a difference, but communities and the climate continue to be sacrificed to Sen. Manchin’s fossil fuel demands.”

All told the terms of the deal will make it impossible for Biden to uphold his campaign promise to end new federal oil and gas leasing.

Overall, the Inflation Reduction Act is a true compromise. On substance, the balance of evidence generated by emissions models strongly suggests that the advantage lies with the energy transition. as Manish Bapna, president of the Natural Resources Defense Council, told the New York Times, “his group’s internal modeling showed that the emissions cuts from the legislation would be as much as 10 times greater than the effects from the support it extends to fossil fuels. He called the fossil fuel provisions “pain points” but said overall the deal was “significantly positive.”

But the balance of political arguments is rather different. If the basic aim of the early Biden administration was to reconfigure American politics with a bold legislative agenda under an overtly progressive brand, then that project has come to grief and the last minute Manchin-Schumer compromise does not change that. The combination of GOP opposition, spoiling by Manchin and Sinema, and the surge in inflation, have fundamentally changed the terms of the discussion and the legislative possibilities. What has emerged in the CHIPS act and the IRA are two pieces of industrial policy legislation that may significantly alter America’s political economy. But they do so under the sign of global geopolitical competition, energy security and fiscal restraint. This is not incompatible with Biden’s message in the spring of 2021, but it recasts that message in distinctly conservative terms.

And, at the time of writing, it still remains unclear whether Manchin-Schumer compromise will fly. Given the last minute nature of the compromise and the Congressional recess on August 6th, the timeline is incredibly tight. The draft bill faces a grueling passage through the Senate.

Manchin’s pivot has unleashed not just the constructive forces of green modernization, but also the lobbyist interests that hitherto have sheltered behind Manchin’s stonewall. As one person close to the process commented to me, the fight will be fought this week.

In a notice reviewed by The New York Times, Democratic floor staff offered some advance advice for senators and their aides as they looked toward the marathon voting session. “Please be patient, stay hydrated, wear comfortable shoes, bring snacks for your hideaway, a blanket for your lap as it usually gets cold in the chamber at night and anything else to make you comfortable as we hunker down and get to work,” it said.

Apart from snacks and hydration, it is political economy that is to the fore. The Democrats still need every vote in the Senate and, as of the time of writing, Kyrsten Sinema of Arizone has been ominously silent on the compromise deal.

She was not party to the conversation between Manchin and Schumer – the “brothers from different mothers”. And there is nothing that Sinema likes to do more than to break liberal hearts over issues like the privileges given to taxation on carried interest.

Talking points that are circulating emphasize private equity’s influence in Arizona’s economy and how taxing the industry could chill job creation. A number being circulated, originating from research by lobby group American Investment Council, is that private equity-backed businesses have employed some 229,000 people in Arizona.

Sinema isn’t expected to oppose all tax changes. But in the past she’s indicated that she doesn’t support eliminating the carried interest break. That tax perk allows private equity and hedge fund managers to pay lower capital gains tax rates, which top out at 23.8%, rather than the 37% income tax rate on a portion of their earnings. The senator hasn’t publicly explained the reasoning for her stance on carried interest.

… Sinema is the main reason the smaller Inflation Reduction Act proposal now on the table doesn’t reverse the Trump-era corporate and individual rate cuts. But it does impose a minimum tax on corporations and eliminates the carried interest break, which has led to heavy pressure from Republicans and industry.

That may be too much for her to stomach. There may also be a rebellion of right-wing low-tax Democrats in the House, if they do not get their way.

Eliminating carried interest is a relatively small change dollar-wise in the context of the $739 billion in tax provisions in the bill. It would only raise about $14 billion additional tax dollars over the course of the decade. If Sinema were to object to repealing carried interest, it could be stripped from the bill without large consequences on other spending priorities, but it could be politically difficult for other Democrats to hand a win to hedge funds and private equity firms.

The result of the Congressional battle this week remain to be seen. Whatever transpires – surprise victory or oft-predicted defeat – the basic and most general point is that this entire process is unbelievably contingent. The balance of forces in US political economy as refracted through the structures of American politics are, in the current moment, finely balance. The Democratic coalition, though it can draw on support of progressive elements of American business, is internally riven. What is clear is that the progressive impetus of 2021 has been decisively broken. The CHIPS and IRA Acts may be effective, but they are not pieces of legislation that will transform American society. They work with the grain of its political economy. And given the dismal poll numbers that still dog the Democrats, they may have come too late, and be too overshadowed by the issue of inflation, to secure what the Democrats and American democracy most urgently need – something less than total disaster in the mid-terms. The progressive side of the Biden team has been worn down, whether the political obituaries for the Biden administration as a whole were written prematurely still remains to be seen.

*****

I love putting out Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

July 29, 2022

Ones & Tooze: Stagflation Nation?

On this episode, Adam and Cameron discuss stagflation—possibly the most ominous portmanteau in the English language. It’s the double whammy of inflation combined with zero or negative economic growth. How can the two coexist? And what does stagflation mean for the world economy?

Later on the show, they talk about dinosaur bones and the economics of Jurassic Park—if it could actually exist.

Find more episodes and subscribe at Foreign Policy

Adam Tooze's Blog

- Adam Tooze's profile

- 767 followers

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}