Adam Tooze's Blog, page 16

July 22, 2022

Ones & Tooze: Why do Italian Governments Collapse so Often?

With the latest political turmoil in Italy, Adam and Cameron consider a bewildering data point: The country has had 67 governments in the past 75 years. Why are Italian politics are so chronically unstable and what does the economy have to do with it?

Later in the show: The economics of food insecurity.

Find more episodes and subscribe at Foreign Policy

July 20, 2022

Chartbook #138: Build Back Better, Dead Again

On Thursday last week, the Build Back Better package that was to define the first term of the Biden presidency with a combination of climate funding, health care measures and progressive taxation, was declared dead, for the second time. The last rites had first been pronounced in December last year. It was then revived. Now it seems to have a stake planted squarely in its heart.

As reported by the NYT, the mood in Washington was desperate:

Privately, Senate Democratic staff members seethed and sobbed on Thursday night, after more than a year of working nights and weekends to scale back, water down, trim and tailor the climate legislation … only to have it rejected inches from the finish line. “Rage keeps me from tears,” Senator Edward J. Markey, Democrat of Massachusetts and a longtime advocate for climate legislation, wrote on Twitter late Thursday.

As David Dayan put it in the American Prospect:

What was once a transformative, multitrillion-dollar agenda to face numerous long-standing crises in domestic policy has narrowed to an exceptionally narrow drug price reform, the main part of which—price negotiation in Medicare—doesn’t kick in until 2026, two years after the next presidential election, and a two-year extension on ACA subsidies that were set to expire at the end of the year. Eighteen months of fruitless negotiation has come down to that.

The health part may still pass. There is some talk that climate bits might be brought back in the autumn. But no one really believes that. In November the betting is that the Democrats will lose control of Congress, which means that for progressive politics a historic window of opportunity has slammed shut. The US is now unlikely to meet the ambitious emissions targets – a 50-52 percent cut in CO2 emissions relative to 2005 – that the Biden administration announced to the world in the spring of 2021.

As Jonathan Chait put it in New York Magazine’s Intelligencer:

Joe Biden once dreamed of an FDR-size domestic-reform agenda. But the collapse of negotiations in Congress … will ensure he achieves nothing of the sort — not Roosevelt-size, not Obama-size, nor even Clinton-size. (Bill Clinton managed to increase taxes on the rich, expand the Earned Income Tax Credit, and create a health-care benefit for poor children.) In addition to losing its chance to address any domestic social need in an enduring way, the administration is also having imperiled its global leadership on climate change and a global corporate minimum tax, two measures that hinged on Biden getting his own country’s house in order.

The death of Build Back Better is yet another failure of the American political class to respond to the multiple global crises of our current moment – climate, pandemic, immigration, financial instability, global inequality and economic risk – that I’ve been calling the polycrisis. As the world swelters under extreme heat, Washington – in certain respects still the command center of global power – has declared that it has other, more pressing concerns to attend to, such as inflation – as though there were any meaningful trade off – or passing a gargantuan defense bill.

The House just passed a bill authorizing $840 billion for the Pentagon. More Republicans voted against it than Democrats. pic.twitter.com/3TRwgFXoeH

— Stephen Semler (@stephensemler) July 14, 2022

Whilst the Pentagon arms for a confrontation with America’s enemies abroad – notably China and Russia – as John Podesta, formerly senior counselor to President Barack Obama and founder of the Center for American Progress, put it in rather melodramatic terms: the failure of Build Back Better has “doomed humanity”.

And this Washington drama has a villain: Joe Manchin. The Senator from West Virginia is single-handedly responsible for crippling Biden’s key proposal not once, but two times over.

Throughout the tortuous process of negotiation that began in the summer of 2021, the administration and Congressional leaders worked closely with Manchin in the hope of persuading him to back some combination of Biden’s infrastructure, welfare, taxation and climate proposals. In the process, Biden’s ambitious agenda was subject to salami slicing.

First the Congressional centrists sliced off the infrastructure component, and the Democratic leadership went along. For David Dayen at the American Prospect.

The defining moment might have been when Democratic leadership decided to back the bipartisan infrastructure bill and take centrists and Republicans at their word that they would vote for anything else in exchange.

Then there was the package of $300 billion to be spent on tax credits for producers and consumers of wind and solar power and buyers of electric vehicles. As the NYT reports:

It would be the single largest expenditure by the United States to fight climate change. (Senator) Mr. Wyden sought Mr. Manchin’s input to shape the tax package in such a way that the West Virginian would support it. Mr. Manchin obliged: He told Mr. Wyden to rewrite the package according to his specifications, so that the tax credits could also be used for nuclear energy and for carbon capture and sequestration, a nascent technology that has so far not proved commercially viable but that could theoretically allow power plants that burn coal, oil or gas to continue to operate without climate-warming emissions.

The $300 billion subsidy package was flanked by regulatory measures

At the same time, other Democrats were crafting an even more ambitious climate provision for the bill, known as a clean energy standard, that would have paid electric utilities to replace coal- and gas-fired power plants and penalized those that didn’t. In a private memo signed last summer with Senator Chuck Schumer of New York, the majority leader, Mr. Manchin, the chairman of the Senate energy and natural resources committee, secured control over the design of the program. But by October, Mr. Manchin had backed out of the clean energy standard, saying he could not support any version. Democrats deleted the entire proposal.

Then in December, Mr. Manchin pulled out of negotiations altogether, saying he could not vote for the overall spending package. Talks were dead for months.

At this point, Build Back Better died its first death.

But the administration and Congressional Democrats had not given up. In the spring of 2022 talks resumed, but now Manchin’s position was stronger than ever. The administration was becoming increasingly desperate to pass legislation of some kind and the war in Ukraine sent petrol and gas prices soaring, strengthening the hand of those who demanded a voice for fossil fuels.

“Russia’s invasion of Ukraine gave Manchin a huge new bargaining authority, as did record inflation,” said Paul Bledsoe, a strategic adviser at the Progressive Policy Institute. That, he said, “changed the dynamic.”

Every time Manchin hacked away at the bill, the climate policy community scrambled to come up with solutions and exception. By last week Manchin appeared to have everything he wanted. Build Back Better had become as much a short-term promotion package for fossil fuel production, as a long-term renewable energy program. As late as Wednesday night it seemed that a deal had been clinched. But then, Manchin walked away. In the end he did not even attempt to make a case, simply waving at reporters and pointing to inflation. So nonchalant was his dismissal that it left commentators wondering whether a deal had ever been there for the taking.

Manchin makes a villain straight out of central casting. He took more campaign donations from the oil and gas industry than any other Senator and owed his personal fortune to dealing in the coal business. He is vain and extremely sensitive. But explaining how he is able to exercise the leverage he is, is a more subtle question than simply tracing his personal finances. It is not good enough at this moment of disillusionment simply to blame one bad apple.

As Kate Aronoff put it in the New Republic:

Manchin is as good a person as any to heap blame onto. He has blood on his hands. It’s comforting to have a single person to focus rage on. But his power to make or break climate policy was years, maybe centuries in the making. Until the real causes are snuffed out—from an undemocratic Constitution to a political system beholden to corporate profits—they’ll just keep boiling us.

America is both one of the birth places of modern climate politics and the place where climate politics has gone to die, not once but over and over again. Biden’s is now the third democratic administration in succession to try to pass major climate legislation and to fail. Clinton tried with a carbon tax. Obama tried with cap and trade carbon pricing. Both efforts collapsed.

The 2021-2022 Build Back Better package was the product of a learning process. It started from the assumption that carbon pricing was impossible in modern America. Instead, the Biden administration would focus on a combination of regulations – clean air – and subsidies for electric vehicle adoption. These were not vague gestures. The scenarios were carefully calibrated by the leading climate modeling teams. Never before had economic policy plans been so closely harnessed to emissions modeling. At least until the winter of 2021-2 there was still optimism that the compromise packages would allow America to meet its 2030 objectives. But even the most sophisticated modeling and dedicated campaigning were not enough to overcome Manchin’s cynical maneuvering.

Manchin is a figure who draws the eye. But he only has the sway that he does because the Democratic majority is as slim as it is. You could blame that on the failings of the Democratic party. Anguished postmortems will fill the summer and autumn, even more so if the Democrats do as badly in the midterms as is to be expected.

But was there really a strategy by which the Democrats might have won thumping majorities in 2020 in both houses of Congress enabling them to pass major legislation in the face of the filibuster rules and the anti-majoritarian procedures of Capitol Hill? One must surely doubt. For decades, neither the Democrats nor the Republicans have commanded the kind of huge majorities that enabled the New Deal of the 1930s and 1940s. America a profoundly divided society that does not easily yield large majorities for ambitious legislation from either side. Already in the 1990s, neoliberalism, though hegemonic in the political elite, lacked large majority support. Carter, Reagan and Clinton all had to maneuver carefully.

Nor is America peculiar in this regard. Bruno Amable has made a similar case for contemporary France. With the break-up of traditional left and right social blocs, modern societies are fragmented without a clear alignment of political parties and projects with familiar social coalitions. Opinion pollsters generally find that the public in Europe and the US can be divided into five or six distinct social, political and cultural segments. The obvious way to organize power, therefore, is through some kind of moderated proportional representation model and a multi-tier coalition system of the type that operates in Germany. By contrast, the two party, first past the post systems in US as in the UK create a highly unpredictable political scene, in which the two main parties span interests and sub-groups that have hugely divergent interests and politics and the head to head off run off is hard to call, unless it is stabilized through gerrymandering of constituencies.

Invoking the German example is not meant to imply a simple solution either to the constitution of effective governance or the hegemony of green modernization in particular. In Germany too, the substance of climate policy remains disputed. But there is little or no scope for outright denial or obliviousness to the issue. What Joe Manchin along with the entire GOP has just done to the Biden administration, which is to put in question the priority of the entire climate agenda, would be unthinkable.

It is tempting to say that ultimately the problem in the US is that climate is just not popular enough. But that begs the question. Climate is not an issue that asserts itself simply through the force of facts. It is not the same as pollution or a war. Climate is abstract. To join the dots, to make it salient requires political work. Activists, scientists, the media, a few key politicians have, in fact, done that work in the US and the evidence is that they are gaining ground.

A poll conducted in early May by the Pew Research Center found a majority of Americans, 58 percent, think the federal government is doing too little to reduce the effects of global warming while 22 percent said it is doing the right amount and 18 percent said it is doing too much. In the same survey, 71 percent said their community had been hit by extreme weather in the past year and a majority linked it to climate change.

As Matto Mildenberger a leading political scientist in the field of climate policy remarks, the narrative that climate was of declining salience to the public simply does not stand up.

Been reading more and more takes that climate bill failed because of shifting public opinion: e.g. the NYT "reported" this week (without empirical evidence!) that the public has soured on climate as the economy weakened. Nonsense. A short

— Matto Mildenberger (@mmildenberger) July 19, 20221/https://t.co/LP1HiH9Zy8

Even in West Virginia, Manchin was criticized by the coal miners union for his efforts to block Build Back Better.

The problem with climate politics in the US is not that you could not find a popular majority for a suitably designed program, but that the GOP and centrist Democrats have no interest in proposing or agreeing to such a policy. Beyond the individual figure of Manchin, this is where lobbying by fossil fuel industry matters. The influence of oil, gas and coal lobbyists and their associated industries works not on the broad mass of the public, but on the political class, to ensure that they dissuade, moderate and ultimately kill off proposals like Build Back Better.

Of course lobby groups play a key part here. Manchin is clearly in their pocket. But that by itself is not an adequate answer either. The fossil fuel industries, even in West Virginia, does not account for a dominant share of regional, let alone national economic activity. And there are, after all, major interests who stand to gain from the low cost energy that the renewable energy transition promises. So, this is the other key role for fossil lobbying. Not only do they seek to persuade the political class to oppose measures like Build Back Better they dissuade other business groupings from forming the kinds of coalitions for green modernization that are beginning to set the tone in Europe.

Another way of putting the same point is to ask why Build Back Better did not have more powerful friends? How could a giant national program come to depend on the vote of a single Senator who represents a state with a population smaller than that of Brooklyn. On this score, it is worth listening more closely to Manchin and the justifications he offers. His arguments are illogical but nevertheless telling. As reported by the New York Times

At the start of this week, Mr. Manchin said his top concern was the price at the pump and the need for more fossil fuels. “How do we bring down the price of gasoline?” he said. “From the energy thing, but you can’t do it unless you produce more. If there’s people that don’t want to produce more fossil, then you got a problem. That’s just reality. You got to do it.”

On Wednesday, after data was released showing the nation’s inflation rate at 9.1 percent, the highest in a year, Mr. Manchin said in a statement, “No matter what spending aspirations some in Congress may have, it is clear to anyone who visits a grocery store or a gas station that we cannot add any more fuel to this inflation fire.”

As one of his spokespersons went on to elaborate:

“Senator Manchin, believes it’s time for leaders to put political agendas aside, reevaluate and adjust to the economic realities the country faces to avoid taking steps that add fuel to the inflation fire.”

In comments to TV news crews widely circulated by Fox, Manchin gestured to a supposed connection between inflation and debt. To fight inflation you have to “get the debt under control” he declared. This was not a moment for a big spending package like Build Back Better. Of course, the proposed legislation included taxation too, but on that too Manchin was a skeptic. He doesn’t want to squeeze American business.

What this suggests is that it may be a mistake to view the failure of Build Back Better primarily through lens of climate. It may, in fact, be better thought of as part of a more comprehensive effort on part of centrist Democrats, for whom Manchin makes a convenient frontman, to stall the reformist energies that were briefly unleashed on the left-wing of the Democratic Party in 2021.

The theory of change that informed the effort to pass Build Back Better was itself broad-based. Loosely derived from Green New Deal vision, Biden’s Jobs and Families Plans linked climate to a wider agenda of progressive policies. The gamble was that you could thus build a powerful electoral coalition. By the same token, however, you also multiplied your enemies. As Chait describes it in American Prospect:

In the final weeks (AT: June/July 2022), Manchin returned to the bargaining table with a deal that still would have counted as a substantial achievement. The plan would have raised taxes on the ultrarich and allowed the federal government to save money by negotiating the cost of some prescription drugs. The proceeds from these measures — likely around a trillion dollars — would have been split between deficit reduction, energy investments (short-term fossil-fuel production, and long-term green-energy investment), and enhanced support for tax credits to help people buy health insurance. A key faction of Democrats in the House, along with Senator Kyrsten Sinema, blanched at the tax hikes. Moderates have been privately coordinating their opposition, and it seems very likely that Manchin’s sudden opposition to raising taxes on the rich comes not from him, but from them — he sometimes takes the heat for fellow Democratic moderates. In this case, he is likely channeling their concerns and passing them off as his own.

Not only did opposition in the House led by Josh Gottheimer of New Jersey rally around opposition on taxes on the richest Americans, another issue was corporate taxation. In the progressive agenda of the early Biden administration, a key plank was the effort led by Janet Yellen at Treasury to create a global coalition around a 15 percent minimum corporation tax. The provision was due to be included in the reconciliation bill, which under the arcane procedures of the Senate, would bundle together all the key policy proposals to be voted through by the Democrats wafer thin majority. But as Brian Faler reported at Politico, Manchin raised objections to this too.

Sen. Joe Manchin on Friday rejected the idea of imposing a 15 percent global minimum tax on U.S. companies, blowing a big hole in the Biden administration’s campaign to remake the international tax system. Speaking with West Virginia radio host Hoppy Kercheval, Manchin (D-W.Va.) said he doesn’t support the administration’s plan because other countries have yet to adopt the tax, and he doesn’t want to put American companies at a competitive disadvantage. “We’re not going to go down that path overseas right now,” said Manchin. “Because the rest of the countries won’t follow, and we’ll put all of our international companies in jeopardy, which harms the American economy.” “Can’t do that, so we took that off the table,” said Manchin, referring to his closed-door talks with Senate Majority Leader.

What, you might ask, have climate measures got to do with global taxation? The link are so called “pay fors”, a legacy of the move spearheaded by Nancy Pelosi and supported by Janet Yellen’s Treasury in 2021 to ensure that the second wave of Biden administration measures did not add considerably to the national debt. That meant that climate and other spending would have to be funded through taxes. That went some way towards allaying the fears of fiscal conservatives, but it also widened the coalition against enacting any legislation at all.

The unintended side effect of Biden’s failed mega-pack of progressive measures is that Donald Trump’s $3 trillion December 2017 tax cuts that overwhelmingly favor the richest Americans are now likely by default to become permanent. As Chait comments:

Donald Trump was able to unite his party behind an unpopular tax cut for the rich. Biden was unable to unite his party behind a popular reversal of that bill, or even a partial reversal. Political scientists have an explanation for both these things: The wealthy hold a disproportionate influence on both the elite in parties, pulling Democrats to the left of their voters on social issues, and Republicans to the right of their voters on economic issues.

As David Dayen points out in American Prospect, this is an astonishing reversal. Trump’s December 2017 tax measures were wildly unpopular. Reversing them and restoring the tax code of 2017 ought to provide all the funding the Democrats need. And yet instead, thanks to the Democrats themselves, Trump’s tax regime will make it unscathed through the Biden Presidency.

within months of Biden taking office, a pro-Trump tax cuts caucus took shape. Suddenly, the likes of Sinema, Gottheimer and Schrader and others were uninterested in raising taxes on corporations, capital gains, inheritances, pass-through businesses, wealthy households, or really anything or anyone else. The Biden administration and Senate leaders kept bargaining for other ideas. If the pro-tax cut caucus didn’t like raising marginal rates, how about a tax just on billionaires? If they didn’t like new corporate rates, how about a global minimum tax for large corporations, negotiated with the entire world, that would prevent evasion? How about just beefing up IRS enforcement so that the taxes actually owed under the current structure are actually collected? One by one, the pro-Trump tax cuts caucus rejected these. The only part of the Trump tax cuts they really wanted to change was to reverse the repeal of the state and local tax deduction, practically the only non-giveaway to the rich in the whole package. Manchin finally became a full-fledged member of the pro-Trump tax cuts caucus last week, when he rejected any tax increases in reconciliation. The entire premise of Democratic policy for the last two years—use the rollbacks of the most unpopular (the only unpopular?) tax cut maybe in history to offset a new round of deeply needed public investment—was dead. … The Trump tax cuts are going to be made permanent, signed by whoever is president in 2025, if not by Biden before that. Despite lofty promises, not a single dollar of the uniquely unpopular policy, courtesy of the president maybe more reviled by Democrats than any other, will be touched. ….

This is the full measure of the failure of the early Biden administration. It allowed innovative long-term spending plans to be burdened with short-term funding requirements. Those could largely have been met by reversing Trump’s 2017 cuts. And yet today it stands empty handed. Not only is Build Back Better dead, but Trump’s tax cuts live on and that double loss has been inflicted on Biden by the Centrists within his own party.

As David Dayen comments:

(w)hy are the Trump tax cuts still standing? Is it something to do with tax policy in particular, and the Democratic allergy to tax increases? Is it a function of bare Congressional majorities, ridiculous legislative rules like the filibuster, and too-dramatic goals overlaid onto them? I think it goes deeper, and signals how Democrats have just forgotten what constitutes governing. The way they create policy ideas, form political coalitions, and work to pass measures through Congress is just impossibly broken. If you have unanimous opposition to a bad policy with no real political proponents and then can’t get a single thing done about it in the space of five years, it speaks to an essential malfunctioning at every level of the party and the process. Nobody should get a pass for it. It’s nothing short of an embarrassment.

Having failed comprehensively in Congress, the Biden administration now insists that it will double down on administrative regulations as a way to push forward the climate fight.

“Action on climate change and clean energy remains more urgent than ever,” Mr. Biden said. “So let me be clear: if the Senate will not move to tackle the climate crisis and strengthen our domestic clean energy industry, I will take strong executive action to meet this moment.”

But so far the administrative actions taken by the administration have in fact pointed in the opposite direction, aiming to appease the likes of Manchin and accelerate oil and gas development.

the Interior Department offered the possibility of 11 new offshore oil and gas lease sales in the Gulf of Mexico and Alaska — despite Mr. Biden’s campaign promise to end new drilling in federal waters … The White House also was weighing whether to allow a path for other fossil fuel projects, like a gas pipeline in West Virginia, in order to gain Mr. Manchin’s vote. …. The administration delayed federal rules to address methane, mercury and other pollutants from oil and gas facilities so as not to anger Mr. Manchin during negotiations, according to several administration officials. That’s two years lost time in a regulatory process that can be lengthy.

Meanwhile, the entire viability of the regulatory route has been put in question by the Supreme Court where the conservative majority recently voted to limit the Environmental Protection Agency’s ability to regulate carbon emissions from power plants. The EPA can continue to regulate greenhouse gases, but it has effectively lost the power to force the closure of the most polluting coal-fired plants, or compel utilities to switch to renewables.

****

Eighteen months on from the inauguration of January 2021, the Biden administration faces the shipwreck of its domestic policy agenda. Dayan sums up the mood on the left well

Most important, stopping the will-they-or-won’t-they is an absolute political imperative. The party is exhausted by failure, and won’t hold out for another couple months of wishes and hopes. Eighteen months of Joe Manchin being America’s most well-known Democrat is enough. Just put (AT: what remains of) the bill on the floor and get this over with. Get something completed, and spend the August recess thinking about how we got here.

The future as far as American progressives are concerned looks grim.

For two years in Washington the Republicans, hunkered down in iron clad opposition, were a sideshow. The politics that mattered were within the Democratic party, between the left, centrists and right-wing. Now, with the midterms looming, we are about to embark on a new, darker chapter dominated by the efforts of a resurgent GOP to crush the remaining life out of the Biden White House and to prepare the ground for the Presidential elections in 2024.

This gear shift in Washington will affect the entire world.

When Biden’s climate agenda was announced in the spring of 2021 it was not merely a national event. The White House hosted a global climate summit ahead of COP26 in Glasgow. The point was to demonstrate that America was “back”. Both Biden’s climate and tax agenda were designed with global deals in mind. On both fronts US credibility is now cut to shreds.

This is, no doubt, very bad news. Reading the commentary on Manchin’s sabotage of Build Back Better you would be forgiven for thinking that it implied a death warrant for the world. But such exaggerations reflect the shock of the moment rather than clear-headed analysis of America’s actual influence on world affairs in 2022.

There may once have been a moment, in the 1990s perhaps, where global climate politics really did revolve around the battles in Washington DC. But today that is a deeply anachronistic view. America’s share of global emissions is less than 14 percent, half that of China, and its share is falling year by year.

Of course, a world with a cooperative, United States committed to the energy transition would be a better world. Trump showed how the US can anchor an anti climate coalition. But even with an obstructive United States, the energy transition in Europe and large parts of Asia has a momentum that will carry it forward regardless. Fundamentally, what impels this logic is the difference between energy exporters and energy importers and the increasingly compelling cost advantages of renewable energy.

As far as the world is concerned it merely confirms the fact that the US is an unreliable partner in the energy transition and has an in-built and profound structural bias towards fossil fuels.

The collapse of Build Back Better is bad news, above all, for America itself.

What it means is that the US energy transition will be slowed down. It will proceed without support and at a considerable disadvantage. It places Detroit, for instance, in an invidious position. The risk is that in the not too distant future the US becomes collateral damage as eurasian transition proceeds. That is bad news for US capital. American business misses out on the profits to be made from green modernization. Whilst carbon pricing is creating an entirely new asset class in Europe, America cannot even get to first base.

American capitalism will no doubt survive. What is more in question is the future of American society and the political system built on it. Above all the failure of the Biden administration’s domestic agenda is terrible news for “ordinary” Americans. It is one more sign of the refusal of the American political class to devise coherent and future-orientated solutions for American society as a whole. Instead of charting the off-ramp towards a greener future, the Biden Presidency is mounting a sustained campaign to hustle America’s oil and gas producers to maximize production and humbling itself before Saudi Arabia. The autopsies on Biden’s Build Back Better package may give Joe Manchin as the cause of death. But America’s problems with the energy transition go far deeper than that.

****

I love putting out Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

July 15, 2022

Ones & Tooze: The State of the Saudi Arabian Economy

As U.S. President Joe Biden visits Saudi Arabia, where he hopes to get more oil, Adam Tooze and Cameron Abadi look at the broader state of the economy in Saudi Arabia. Then, Adam and Cam answer a first batch of listener-recorded questions. Expect a lot more soon.

Find more episodes and subscribe at Foreign Policy

Chartbook #137: The regime at risk – macroprudentialism faces the test of inflation

With the fight against inflation taking center stage, the talk now is of the risks involved in slowing an economy hard. It is a test not just of particular policies and policy-makers but of a policy regime. Ahead of the surge of prices in the second half of 2021, were central bankers focused on the right things? Did they underestimate the risks? Do they actually understand the economy?

The most common accusation is that the slow reaction to the build-up of inflationary pressure in 2021 will now require such a serious hike in interest rates that it will precipitate a “hard-landing” and severe economic pain. In his latest column for the FT, Mohamed El-Erian indicts the Fed for being too slow and warns of the tough times ahead for, “the most vulnerable segments of the population and the most fragile developing countries”.

Let us name this scenario for the ghost of Paul Volcker, the Fed chair who in 1979 ended the “great inflation” of the 1970s with a brutal interest rate hike and a savage recession, helping to precipitate a global debt crisis.

As I’ve argued in a recent Foreign Policy piece, the question is whether the next few years will finally lay that ghost to rest. If inflation does peak in the next few months – as is still widely expected – and then come down with no more than a short and mild recession, perhaps it will be possible in, due course, to stand back and recognize the rollercoaster of 2020-2022 for what it is, not a disastrous failure of policy, but a story of difficult policy-making under conditions of huge uncertainty in the wake of the unprecedented COVID shock.

On the prospects for a hard-landing, it is worth remembering the BIS analysis of the Annual Economic Review, which puts things in perspective. In the worst-case scenario it expects a shock to real estate prices far less dramatic than 2008 and a GDP shock of moderate proportions relative to a scenario in which the ultra-loose monetary policy prevailed.

Source: BIS Annual Economic Report

If some scenario of this kind transpires, then on balance, allowing for the dramatic recovery in labour markets and a resumption of growth in latter half of 2023, what will be the judgement on the economic policy mix in 2021? I think the jury remains out.

Of course, there are other risks that could further complicate the situation.

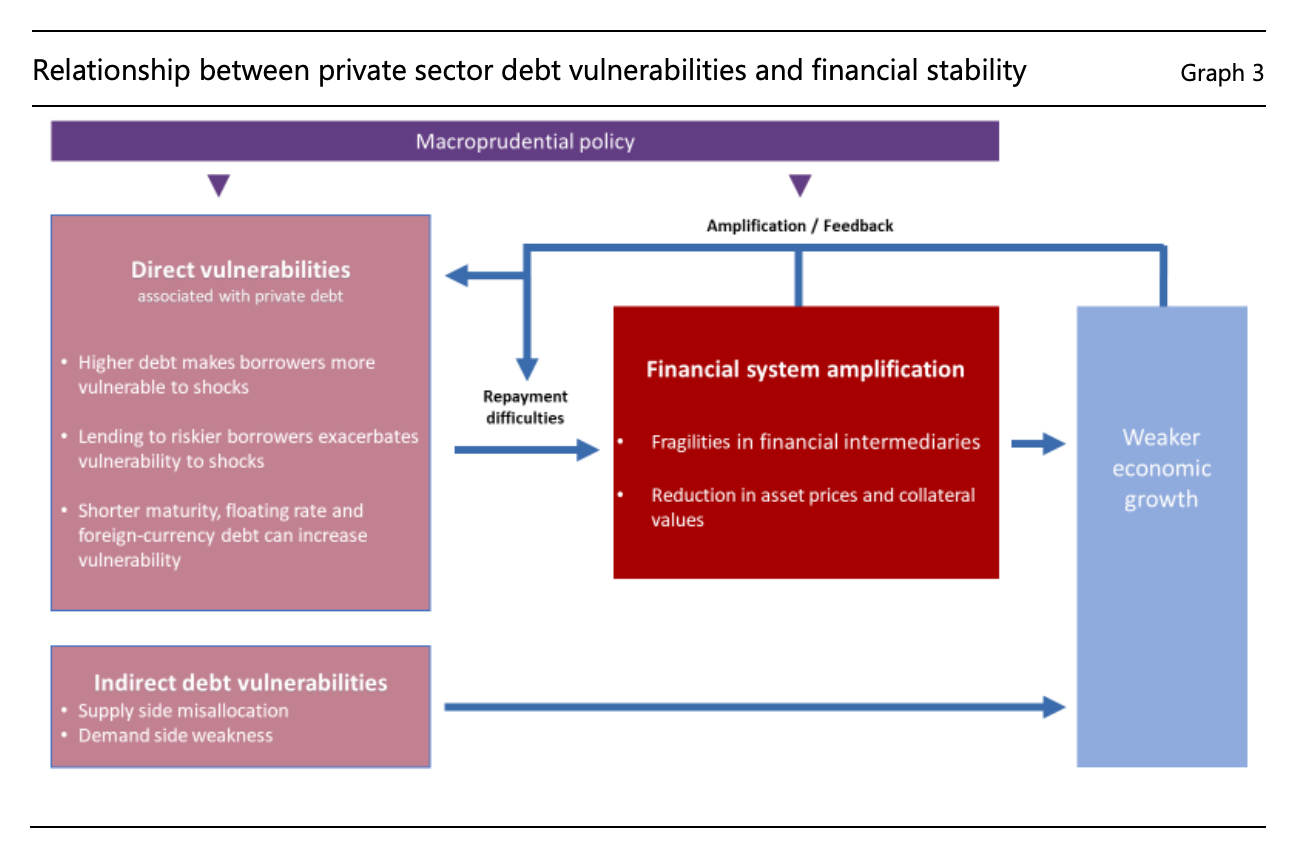

The most urgent concern is that in the course of the tightening of interest rate policy something breaks in the financial system – call this the financial crisis scenario. Another risk is, that as a result of the accumulation of debt service obligations, the 2020-2022 switchback in interest rates triggers a sustained fall in investment, spending and growth – call this the zombification scenario.

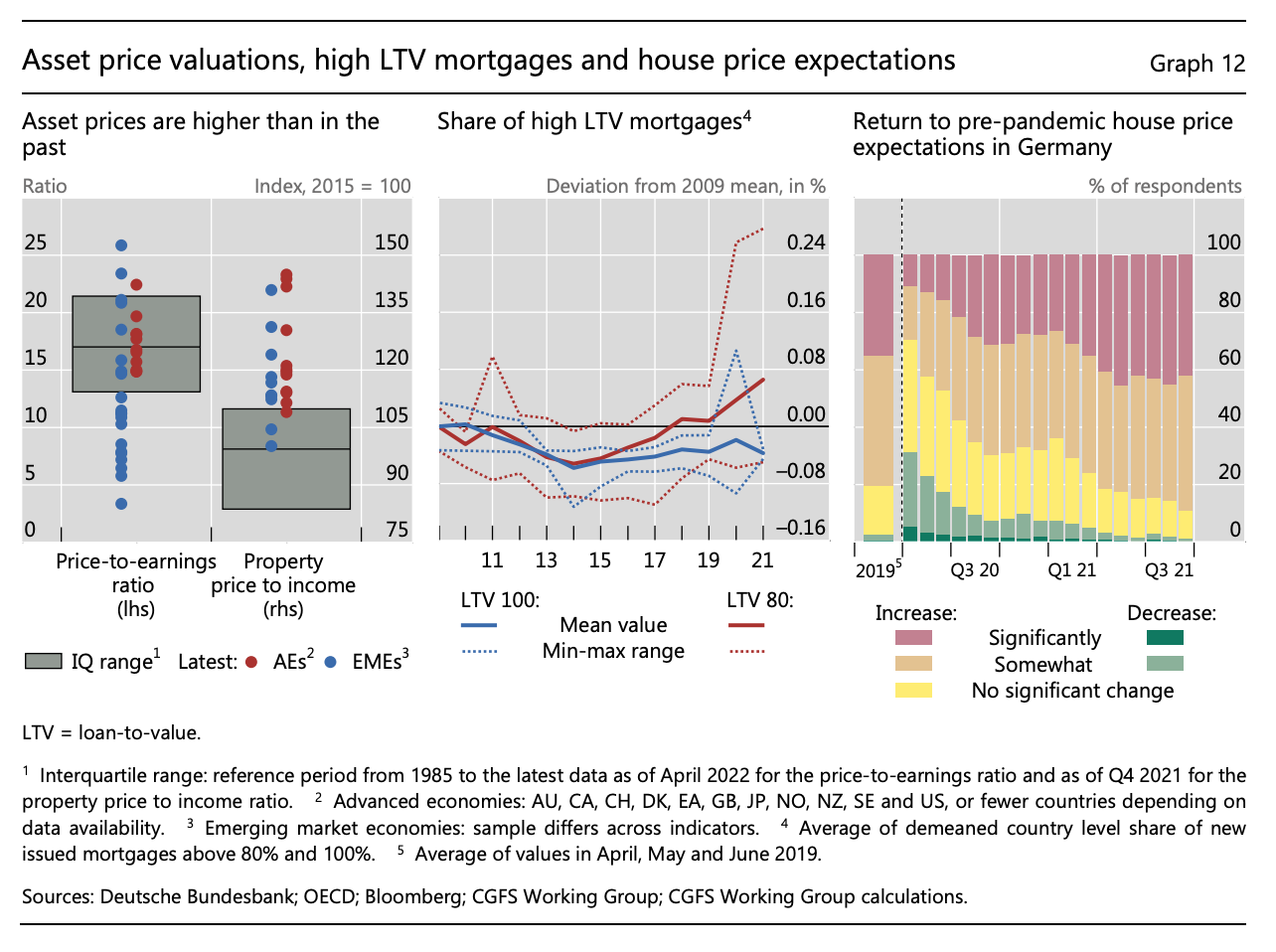

Gillian Tett in a recent piece in the FT drew attention to more work out of BIS – this time by a working group of the Committee on the Global Financial System (CGFS), co-chaired by Roong Mallikamas (Bank of Thailand) and Benjamin Weigert (Deutsche Bundesbank) – which assesses the risk of these latter two effects.

Tett cites the CGFS in minatory terms. Her title and subtitle warn:

“We should be worrying about debt as well as inflation. Pundits have long ignored the issue because declining interest rates kept borrowers’ servicing costs low.”

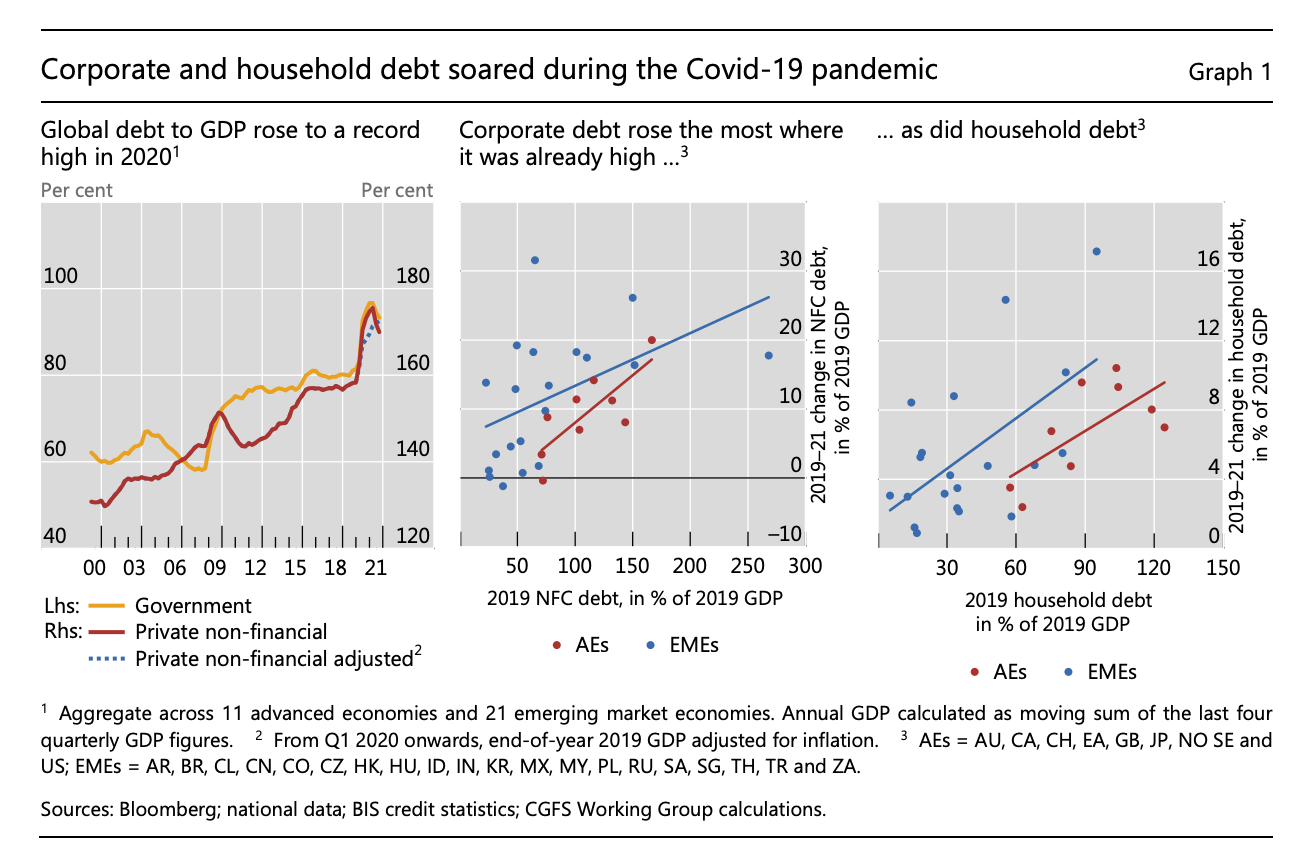

Drumroll! But how worried should we be? As Tett notes, the message from CGFS Working Group is, in fact, mixed. The starting point is the global rise in debt and, in particular, the surge in debt following the COVID shock in 2020. This increase was substantial and, strikingly, it seems that debt rose most where households and corporations were already highly indebted.

These levels of debt mean that if interest rates rise, debt service costs will become a heavier and heavier drag on the balance sheets of businesses and households. As the Working Group notes

A 100-basis point increase in borrowing costs would raise the aggregate household debt servicing cost by around 1 percentage point of income in the average economy (Graph 6, right-hand panel, red triangles). However, due to the non-linear relationship, a 300-basis point rise would increase debt service by around 4 percentage points of income (blue triangles). Although such an increase in debt service costs is still modest, vulnerabilities could be amplified if rising interest rates have negative effects on collateral and asset prices which in turn result in debt rollover difficulties for borrowers.

What worries the Working Group are less the national averages than the tail risks. In particular it notes that amongst firms, it was loss-making firms and small and medium-sized enterprises that borrowed most during the COVID crisis. They do not have the strongest balance sheets with which to withstand the current tightening.

Beyond the weak tail of the corporate sector, the authors of the Working Group report are particularly worried about household debt and in particular mortgages that make up 75 percent of household debt. Households often take on far greater risks in housing markets than they realize, especially if they are suddenly faced with falling rather than rising house prices.

The empirical evidence shows a strong association between mortgage credit and recession severity, with both higher levels and faster growth of household debt associated with larger consumption decreases during downturns and more severe recessions (Dynan (2012), Anderson et al (2016), Bunn and Rostom (2015), Kovacs et al (2018)). Jorda et al (2014) find that, although mortgage lending booms were only loosely associated with financial crises before the Second World War, mortgage lending was a significant predictor of financial crises in the second half of the 20th century.

Currently, as the Working Group notes, property prices appear particularly stretched in many economies around the world.

The big worry, on the model of 2008, is that a vicious circle could be set up between increasingly unsustainable debts owed by households and firms and the financial system itself. Defaulting borrowers would put the banks at risk, further crippling economic growth and adding to the woes of the indebted firms and households.

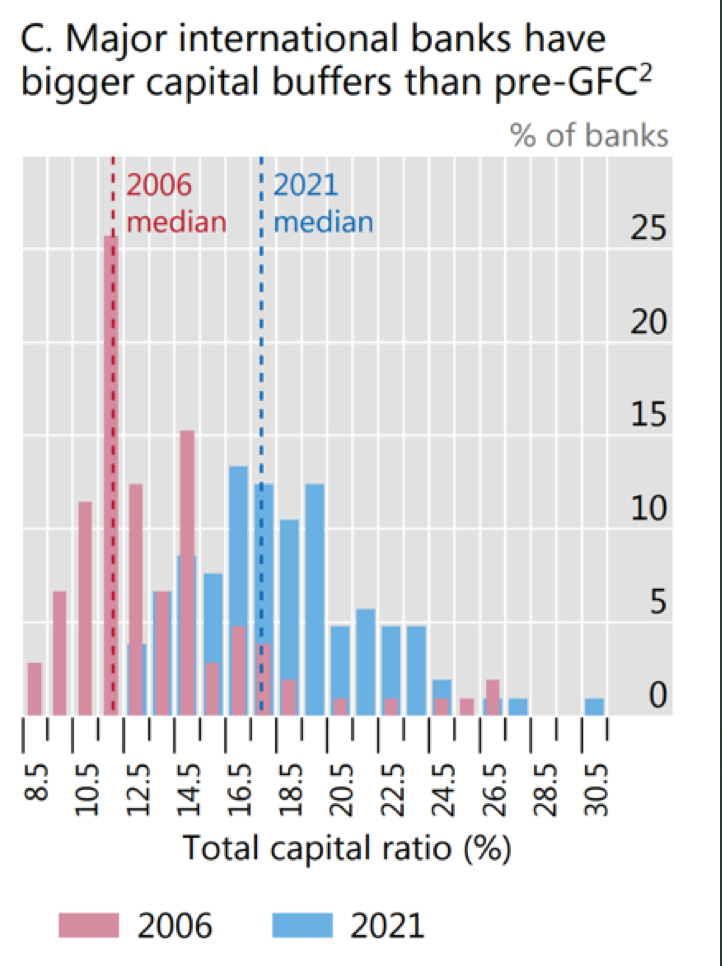

But how serious is this risk? To produce the 2008 crisis required not just an overstretched housing market and a dangerous system of mortgage finance, it also needed a banking system whose funding structure was fundamentally unsound and whose balance sheets were dangerously over-expanded. As has often been noted, there was no radical overhaul of the system of financial capitalism after 2008. The big banks are, in in some cases at least, bigger than ever. But what is also undeniable is that the mega- banks are more robust. The median capital buffers of international banks were, in 2021, at least fifty percent more substantial than they were in 2006.

This returns us to the basic conclusion of the BIS’s scenario analysis for a hard landing. Even in the worst case model it seems unlikely that the core institutions of the financial system will suffer the kind of shock that debilitated them in 2008 and the threw the entire economy off course.

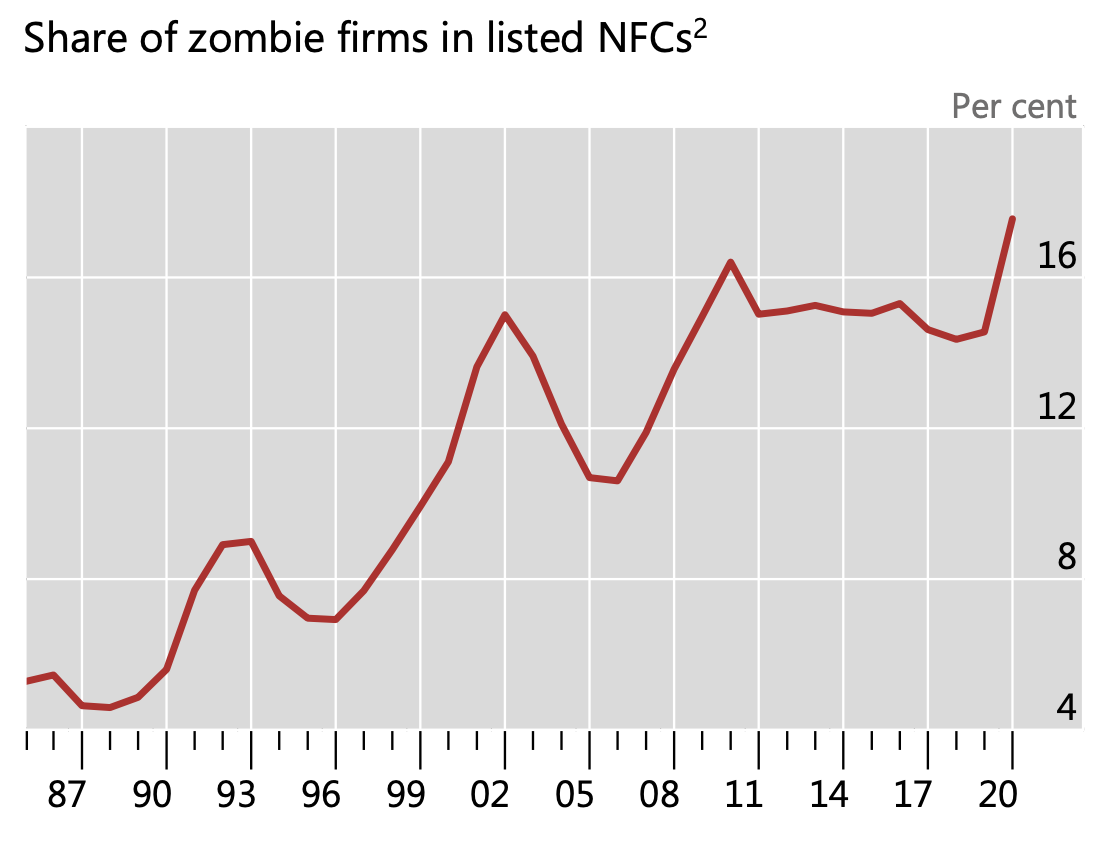

What then of the third concern attendant on the rise of debt in a world of higher interests rates, zombification? Zombie firms are firms that do not generate enough profit to pay down their debts. They are able to pay interest and service their liabilities, thus avoiding bankruptcy and liquidation, but they subsist in a state of suspended animation. According to the analysis of the Working Group team, 17 percent of companies in the advanced economies fell into the zombie category in 2020. That is a new record and it was set before interest rates began to increase substantially in early 2022.

If the situation is deteriorating, one has to ask why we face this deterioration in the condition of global business. The diagnosis of zombification was originally intended as an indictment of a policy regime that lowered interest rates to the point where they no longer exercised much selection pressure on weaker firms. The undead survived. But ahead of the COVID shock the ranks of zombie firms were, in fact, gradually thinning. The sudden surge in 2020 is due, not to policy choices but the unprecedented and, from the point of view of corporate finance, exogenous shock of COVID. Perhaps it would be fairer to label the recent additions to the ranks of ailing businesses not as zombies but simply as casualties. The difference in labeling matters. To be put out of their misery, zombies have to be blown to pieces. Casualties should be nursed back to health.

As Tett points out, one of the important conclusions of the Working Group is that the true scale of financial risks can be assessed only in detail.

Aggregate debt statistics can be misleading because they might mask underlying debt vulnerabilities. For example, a stable aggregate debt-to-income ratio might mask an accumulation of debt among households or firms with lower incomes. Moreover, as highlighted in Section 2, lending to riskier borrowers exacerbates the vulnerability of the economy to shocks. Thus, data on the distribution of debt vulnerabilities can provide useful information on debt vulnerabilities among borrowers at most risk of experiencing repayment difficulties. Analysis of distributions requires micro data, which are often not available from public sources. The Working Group collected data from central banks to analyse the distribution of debt vulnerabilities.

And the Working Group report is indeed a monument to the extraordinary wealth of data now collected by central banks on the balance sheets not just of the banks, but of the entire economy. This reflects the expansive power/knowledge logic of the contemporary policy regime.

What is known as the regime of macroprudential regulation – the monitoring of macroeconomic risks to the financial system, and impacts from the financial system on the macroeconomy – is centered on the systemically important banks. But, the health of the banks depends on their clients – households and firms – who make up the broader economy. “Stress testing” the center piece of the modern system of macroprudential regulation, gauges the health of bank balance sheets against more or less extreme macroeconomic scenarios. To make those models more comprehensive and accurate, central banks need to monitor not just aggregate numbers, but the balance sheets of the entire economy. How extensive and adequate, the Working Group asks, is the extent of this central bank monitoring?

To answer this question the Working Group polled 23 central banks in both advanced economies and emerging markets on their practices of debt surveillance. The results are fascinating for what they reveal about the extension of the macroprudential monitoring system from the banks to the rest of the economy.

All 23 central banks polled monitored a basic indicator like household credit to GDP. In addition,

Almost all central banks report monitoring the evolution of house prices indicators in order to detect overheating, with the most common indicators being price-to-rent and price-to-income ratios. Some countries use econometric models to compare house prices to values predicted by fundamentals. Fewer central banks monitor other indicators of overvaluations such as indicators of speculative activity, such as flipping trades

But when it comes to the problematic tail of borrowers, the coverage is more scanty:

Only eleven countries monitor at least two of the following indicators: net debt to income; net worth to liabilities; liquid assets to liabilities; or gross interest payments to disposable income. Six central banks monitor none of these indicators. More than half of central banks nevertheless indicate that they monitor vulnerable households, using indicators such as debt to income or debt service to income to define this group. A few central banks also monitor the share of riskier households and loans.

As the Working Group notes

In this regard, greater use of granular household debt data has been a major development since the GFC, helping to shine light on those vulnerabilities most associated with macroeconomic stability. Central banks have been innovative in sourcing such data, collecting it from credit bureaus and banks as well as data collected in the course of other central bank operations (see Appendix C). However, there are often specific challenges related to gathering such data, not least with respect to cost and privacy.

Not only have central banks pioneered the mobilization of new types of data for monitoring and supervision. They have also devised new methods for aggregating the data to inform the policy-making process.

More than three quarters of central bank respondents report the use of indicator dashboards. These dashboards bring together multiple indicators (often between 50 and 100) covering several specific sectors or types of risk, with the aim of providing an overview of the main vulnerabilities in the financial system.

…. While dashboards and composite indicators allow information from several potential areas to be combined, it is important to assess the degree to which identified vulnerabilities translate into systemic risks. In this respect, thresholds for composite indicators or individual dashboard indicators are often used to signal areas of emerging or increasing risk. Growth-at-risk models provide estimates of the severity of potential systemic risk in terms of downside risks to GDP growth.

Setting thresholds is a way of guiding policy-makers’ attention towards emerging critical risks.

Virtually all central banks that use dashboards establish thresholds for indicator categories in the dashboards. The thresholds are used to assign colour codes to indicators or groups of indicators within the dashboard in order to signal areas of vulnerability. The colour codes may derive from thresholds defined either at the level of individual indicators or at the level of indicator groups or categories. … One statistical method is based on crisis prediction models where the indicators and corresponding thresholds are chosen to minimise the risk of false positives or false negatives when predicting historical banking crises. Another method combines statistical methods with expert judgment by utilising graphical analysis to identify points of non-linearity at which debt vulnerabilities often turn into actual debt distress.

A more elaborate type of risk analysis known as growth-at-risk models links financial indicators directly to macroeconomic metrics

Growth-at-risk (GaR) is a statistical method to measure systemic risk. It is used by two-thirds of the responding central banks. GaR models use macroeconomic and financial variables to estimate a probability distribution of future real GDP growth. One important advantage is that GaR models map the effects of different vulnerabilities into one easy-to-understand measure: potential GDP losses. GaR models can also illustrate how current debt vulnerabilities affect downside GDP growth risk at various horizons. … Most central banks tend to focus on both the near term (one month or one quarter) and medium-to-long term (one to three years) GDP risks. Medium-to-long horizon models may be more useful to guide policy actions to manage the build-up of debt vulnerabilities.

Finally, closing the loop back to bank regulation, central banks use statistical models to guide their decisions with regard to the counter-cyclical capital buffers that big banks are required to hold. When there is a risk of severe recession, bank lending can be released. In the current moment, one would expect those buffers to be tightened.

Beyond debt monitoring frameworks, central banks also use statistical methods in the context of the CCyB framework. The methods include: quantile regressions that provide estimates of future NPLs; statistical filters to identify excessive credit growth; stress tests to review the adequacy of the CCyB; and models measuring the long-term trade-off between efficiency and stability.

For obvious reasons, in the current debate about central bank policy and inflation, it is the classic macroeconomic questions of a hard landing that hog the headlines. How much unemployment may be necessary to bring inflation down to the desired level? This is the question first formulated by the Phillips curve in 1958 and reformulated with the expectations augmented Phillips curve in the 1970s. It is – now as then – a hugely important trade off. But we should not mistake the era that we are in. What is being put to the test in the current moment is the entire regime of policy instruments, tools and priorities that has emerged since the financial crisis of 2008. That regime was created under the sign of low inflation and low interest rates. The question now is how well it will function as central banks wage a struggle to bring inflation down from close to ten percent and interest rates rise as they have not done since the early 2000s.

****

I love putting out Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

July 8, 2022

Ones & Tooze: What Fluctuating Oil and Gas Prices Mean for the World.

Adam and Cameron look at dropping prices for crude oil and forecast what that might mean for the global economy. And they take a broader look at energy consumption and what can be done to curb it in times of crisis. In the second segment the two take a deep dive into playgrounds and the history of how they’ve been valued.

Find more episodes and subscribe at Foreign Policy

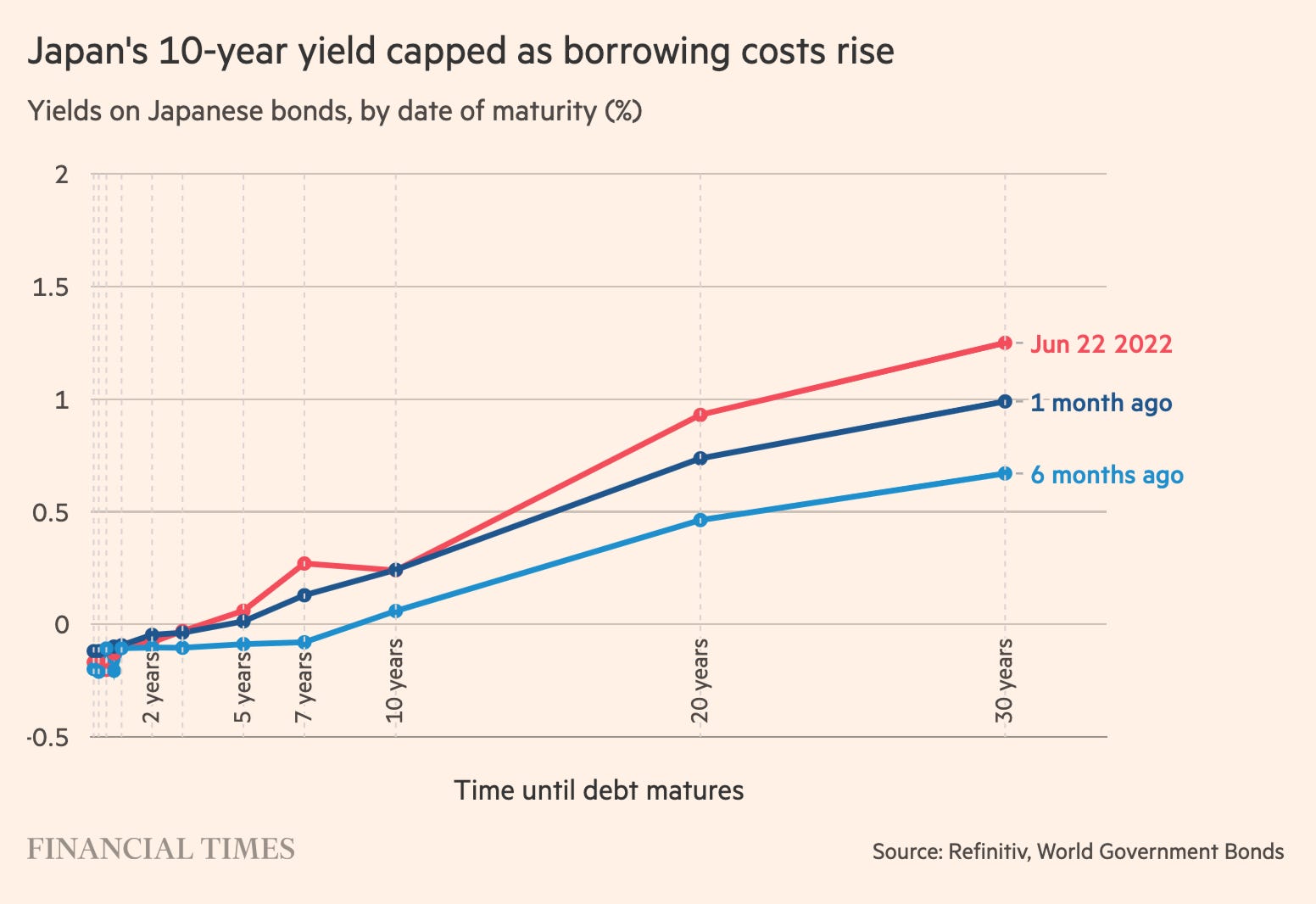

Chartbook #136: The legacy of Shinzō Abe, yield curve control & the “widow-maker” trade.

The assassination of Shinzō Abe looks to have been the act of a crazed loner. But the circumstances were not merely fortuitous.

When he was shot, Abe was on the stump campaigning on two issues that defined his legacy for contemporary Japan.

Abe was an unabashed nationalist and historical apologist. He is also being celebrated today as the champion of a new realism in East Asian foreign policy. Abe saw Russia’s aggression against Ukraine and mounting Sino-US tension as vindication for his calls for a new Japanese security policy that broke with the postwar taboos. Under the influence of “pivot to Asia”-stalwarts like Kurt Campbell, the Biden administration has re-embraced the alliance with Japan. To many analysts, Abe looks like a prophet of Indo-Pacific containment policy.

On the stump on the day of his death, Abe’s other great talking point was Japan’s economic situation. Here, Abe was on the defensive. His killing comes at a moment when his economic policy legacy is under threat. As the world’s central banks turn to tightening, the question has become ever more pressing whether the Bank of Japan can remain the odd central bank out.

Abe was elected in 2012 with a mandate to adopt an economic policy – soon dubbed Abenomics – based on “three arrows”: flexible fiscal policy, monetary expansion, and structural economic reform.

Abe was out of power during the 2008 financial crisis, which hit Japan hard. Compared to the US or Europe, Japan’s banks survived the crisis in relatively good shape, but Japanese exports were dealt a severe blow. This compounded the recessionary and deflationary pressure evident since the 1990s. In the worst months of 2009, Japan recorded an alarming deflation of more than 2 percent.

Japan Inflation

Source: Trading Economics

Falling prices are so dangerous because they form a downward spiral of self-fulfilling recessionary expectations. Falling prices punish those who borrow to fund investment. Abe’s goal was to push Japan above 2 percent inflation and thereby to restore investment and growth.

On the three prongs of Abe’s ambitious agenda, the verdict is mixed.

Abe’s structural reform agenda was a partial success at best.

To address Japan’s declining labour force, Abe favored women’s labour market participation. And during his administration Japanese women did enter the labour market as never before. The fact that a significantly larger percentage of Japanese women are in paid employment than in the United States is a remarkable historical turnaround.

In structural terms, however, gender relations were little changed. Japan remained profoundly patriarchal.

Along with Abe’s avowed nationalism, on structural reform his administration presented the picture of an ambiguous experiment in modernization.

By contrast with his agenda of structural change, Abe’s fiscal policy started boldly. In 2013 Abe introduced a stimulus package worth ¥10.3 trillion (equivalent to $116 billion) in government spending. But at the crucial moment in 2014, as the momentum of the early years was stalling, Abe allowed a hike in the consumption tax, legislated by the government of his predecessor, to go ahead.

The retreat from fiscal stimulus left policy walking effectively on one leg. The one side of Japanese economic policy that cannot be accused of half-heartedness is monetary policy.

In February 2013 to flank his expansive agenda, Abe nominated Haruhiko Kuroda to the governorship of the Bank of Japan. He had long been an advocate of looser monetary policy in Japan. Kuroda’s appointment was reinforced by the choice of Kikuo Iwata – another critic of the BoJ’s policies to date – and Hiroshi Nakaso, a senior BOJ official in charge of international affairs, as his deputies.

Kuroda and his team immediately adopted a policy of aggressive monetary stimulus, doubling down in 2014. When this was not enough in January 2016 the BoJ resorted to a policy of negative interest rates followed in September 2016 by the adoption of yield-curve control, centered on the Japanese 10 year bond. The Bank of Japan effectively committed to buying bonds in sufficient quantity to ensure that 10-year JGB yield remains around 0 percent and deposit rates remain at -0.1 percent .

The 2016 shift was driven by domestic factors but also by global forces. 2015 was an extremely nervous year for the world economy. China suffered a major sell-off in stock markets and the economic growth miracle wobbled. Europe’s situation prompted EU Commission President Jean-Claude Juncker to first use the term poly-crisis. Ukraine, the Syrian refugee crisis, Greece’s debt crisis all came together. The ECB feared the worst. Inflationary expectations were slumping into deflationary territory. Would the Eurozone under the weight of inadequate investment and too much austerity slump into Japanese territory? In March 2015 the ECB responded by launching QE on an unprecedented scale.Previously, the ECB had bought bonds only to stabilize specific markets. Now it did so wholesale.

The Fed may be the undisputed leader amongst global central banks and Ben Bernanke led the charge in 2008. But, together, the scale of the ECB and the BoJ’s program bond buying after 2015 dwarfed anything the US had previously attempted.

This convergence of policy between Japan and Europe was not simply a matter of politics. Both Japan and Europe were suffering from chronic surpluses of savings, above all in the corporate sectors. The former champions of industrialization and export-driven growth were no longer investing enough at home. Sustained public investment i.e. fiscal policy, was the advice given by most economic experts. But given the obstacles to that in both Japan and Europe, central bank policy was the “only game in town”.

In 2015-6, the world avoided recession, but it was now profoundly imbalanced. The Fed under Janet Yellen was tightening. The ECB and BoJ were fully expansionary. The result was that the euro and the yen depreciated against the dollar, triggering a mini-recession in US manufacturing in 2016. Tough times in the rustbelt helped to set the stage for the victory of Donald Trump in November 2016, a nationalist populist with whom Shinzō Abe got along far better than most other world leaders.

In his effort to Make America Great Again, Trump adopted his own version of Abenomics, focusing on big tax cuts. Initially, this put him at odds with America’s central bank. The Fed first under Yellen and then Jerome Powell continued to attempt to “normalize” policy. In 2019 this produced mounting political and financial market tension in the US with former Fed officials openly taking positions against the Trump administration. After some months of jitters, culminating in the nasty incident in the US repo market in September 2019, it was the Fed that gave way. Jerome Powell abandoned his effort at tightening monetary policy. Mario Draghi, in his final months in office in Frankfurt, did the same. The ECB resumed bond buying.

As 2020 began, before news of COVID spread, it seemed that the Japanese model had won. More than a decade on from 2008, there was no alternative to continuing unorthodox monetary policy. The shock of COVID only reinforced this impression. Every central bank did it differently, but everyone intervened and did so on a massive scale. In Japan, to counter COVID, Abe’s administration adopted a giant fiscal and monetary stimulus – rated at 20 percent of GDP.

As Abe was force out of office by ill-health in September 2020, it seemed that at least as far as monetary policy was concerned the whole world had “gone Japanese”.

In 2020 the RBA in Australia adopted yield curve control in explicit imitation of the Bank of Japan, with whose economy Australia is closely connected. The ECB was not targeting the yield curve but it was hard to deny that it had an eye on spreads, which are the yields that matter as far as the eurozone is concerned. In 2021, both the ECB and Fed adjusted their policy framework for a world in which the Japanese problem of secular stagnation and ultra-low inflation was assumed to be the backdrop.

And then the poly-crisis took another unexpected turn. Rather than stagnating, first the price of energy, then commodities and then the price of many other things began to surge. Even in Japan, inflation ticked up. In Europe and the US the shock was dramatic.

This faced the central banks and bond markets with an unexpected dilemma. It was clear that central banks would have to reposition themselves. And by the autumn of 2021 this was causing deep anxiety in global bond markets.

As bonds sold off hard, promises to prop up prices and keep yields down lacked credibility. In November 2021 as markets became disorderly the Reserve Bank of Australia was forced to abandon its version of the the Japanese policy of yield curve control. The RBA was no longer willing to muster the fire power necessary to peg rates. Yields surged out of control.

Australia is a relatively small player. Though the RBA’s about-face added to uncertainty, it did not destabilize global markets. It was indicative, however, of a broader shift. Many emerging market central banks around the world, led by Brazil, were already raising rates. By early 2022, both the Fed and the ECB were clearly indicating the end of QE and the move to tightening. This has left the Bank of Japan isolated.

Fumio Kishida, as Abe’s successor, had promised to honor the legacy of his predecessor’s economic policies. And in November 2021 he made good on that promise with a giant fiscal stimulus. Meanwhile, at the BoJ there is continuity of leadership and commitment. On the day of Abe’s assassination, his monetary policy legacy remains intact. But the question is how long this can continue.

With other central banks raising interest rates around the world, to peg Japanese rates at low levels, the BoJ has had to buy bonds at a dramatically accelerated rate. Even by the standards of its long history of experimentation, the current policy stance is extreme.

As the FT reports, global investors are increasingly betting that this cannot continue. They are positioning themselves to take advantage of a BoJ move to follow Australia and release yields. If you short Japanese bonds, you may be in a position to take advantage of a Bank of Japan exit from the market, falling bond prices and rising yields.

This is not a new trade. Indeed, it has been attempted so many times without success that it is known in the financial markets as the “widow-maker”. But might this time be the moment in history when the Bank of Japan reverses direction? Pressure is clearly building.

Aside from the 10-year yield, which is pinned by the BoJ’s policy, shorter and longer-term borrowing costs have been pulled upwards as global interest rates rise. Japan’s yield curve — the graph of its yields across increasing maturities — would usually be a smooth upward-sloping line. But it has developed a distinct kink around the 10-year point.

The uncapped yields on 7-year debt, are now above those on 10-year, which the Bank of Japan is targeting. This gives a clear indication of how the curve would adjust if the Bank of Japan removed its support.

Domestic Japanese investors continue to maintain faith in the Abe-Kuroda formula. Too much political capital has been invested over the last decade in the BoJ’s adventurous program. Publicly, the BoJ too remains completely committed to its stance.

At last week’s policy meeting, the Japanese central bank renewed its pledge to buy as much government debt as it takes to keep 10-year borrowing costs below 0.25 per cent.

The Bank of Japan has more than reputation invested in the continuity of policy. If it loses control of yields and bond prices plunge it could face a paper loss of as much as $200 billion on its huge bond portfolio.

There is determination, therefore, to continue. On the other hand, those shorting the trade insist that this veneer of continuity cannot be taken at face value. If the BoJ is to have any chance of managing the exit from its strategy in an orderly way, it must remain in charge of the narrative. That means that it must give no advanced warning to the markets of a potential change in position. The change must come as a complete surprise.

If the Bank of Japan maintains its policy, on the other hand, the pressure will show up not only in the bond markets. The Japanese currency is really feeling the pressure of continuous monetary expansion and low interest rates.

In a period of dollar strength, the yen has devalued dramatically against the US currency, falling to a 24-year low. This adds to the competitiveness of exports and raises the cost of imports, which helps to counter any deflationary tendency. But the sheer speed of the devaluation also spreads uncertainty to Japanese investors. Would they be better off investing abroad? How long can the devaluation continue for?

Compared to this scenario of mounting pressure in bond markets and a serious devaluation, many think the Bank of Japan would be better advised to bite the bullet and initiate a policy shift. After all, it is in a position, somewhat unexpectedly, to declare victory. Inflation in Japan has for the first time since 2015, exceeded the level of 2 percent that Abe’s government initially set as its objective.

If the Bank of Japan does decide to change direction, how it does so will be crucial. Australia’s exit from yield curve control, was, as the Bank’s own analysis now admits, a bit of a shambles. The Bank of Japan unlike the Reserve Bank of Australis is a whale. If it attempts an exit from unconventional policy and it goes wrong, it could send shockwaves through bond markets worldwide. It might also imperil the forward momentum of the Japanese economy. In any case, it would be the end of an era that will, forever, be associated with Shinzō Abe.

***

I love writing Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

July 6, 2022

Chartbook #135: A Chartbook sampler

It is a delight to welcome new readers to Chartbook.

Many have come by way of the very generous profile in The Atlantic by Annie Lowery.

Both for new readers and those who have been following Chartbook for a while, it may be of interest to take a tour of some of the older posts.

Much of the material in the newsletter is by its nature ephemeral but some of the posts cover issues that have a longer sell by date.

For the first anniversary of the newsletter in the fall of 2021 I put together an index.

Here are some particular recommendations. Back in the fall of 2021 I did two pieces to accompany the release of my COVID book Shutdown, which still rattle around in my mind.

On Keynes and why we can afford anything we can actually do.

And on writing in media res, which my friend Nick Mulder suggested to me might actually be a great alternative title for the Newsletter.

I am in the Abacos right now, and two pieces I wrote here last year come to mind.

Chartbook #20 on The Caribbean, Central America and the “Brazilianization” thesis, which was a response to a fascinating article by Alex Hochuli.

The other, Chartbook #21, was an essay about Vasily Grossman’s Stalingrad novels.

I wrote it in the weeks following my father’s unexpected death and the essay carries some of the emotion of that moment.

Then there is Chartbook #45 on the Mariel boatlift to Miami and the award of the Nobel prize in economics to David Card, “or the history of a natural experiment”.

Chartbook #45: Of Scarface & the Nobel – The Double Life of Mariel

Chartbook #37 on how to write the economic history of China, the Soviet Union and Eurasia’s great divergence is one I regularly come back to.

Chartbook #44 on William Jennings Bryan, populism, the gold standard, and the “cross of gold” speech.

Chartbook #44: The Cross of Gold – populism, democratic iterations and the politics of money

Chartbook #82: The rise of asset manager capitalism and the financial crisis of 2008

More recently I’ve done a mini-series on the ideological tropes that have emerged from the war in Ukraine.

Chartbook #119: Lend-Lease & Escalation

Chartbook #120: St Javelin, Lockheed & the arsenal of democracy

Chartbook #123: The war in Ukraine and the triumph of the all-American anti-tank gizmo

But perhaps the newsletter that has meant most to me is an appreciation of Stuart Hall’s autobiography.

Chartbook #125: Familiar Stranger – Stuart Hall on diasporic thought

In any case, this is an invitation to browse the archive and enjoy.

And if you find stuff you enjoy and have not yet hit the subscription button, please do consider giving your support to the enterprise.

July 4, 2022

Chartbook #134: Inflation as an emergent macroeconomic phenomenon

The current situation of unexpected and rapid price increases, has forced us to define more clearly what is inflation. In a nominalist vein you could say simply that inflation is whatever the CPI or some other index says it is. And for everyday purposes it is almost perverse to refuse this simple answer.

But from an economic point view, as the BIS puts it, in a remarkable section of its recent Annual Economic Review, we need to make a crucial distinction:

The distinction between relative price changes and underlying inflation is critical. Relative price changes reflect those in individual items, all else equal. This may or may not be related to underlying inflation, ie a broader-based and largely synchronous increase in the prices of goods and services that erodes the value of money and devalues the “unit of account” over time.

There is a lot to unpack in this crucial passage. We are in a state of inflation when all prices – both those for goods and labour (i.e. wages) – are going up, broadly speaking in parallel. If that happens, since all prices are moving, the only fixed point from which to measure the change is that offered by the unit of account, i.e. the unit of money. This is the deeper meaning behind Friedman’s famous comment that inflation is always and everywhere a monetary phenomenon.

Price movements can do many things and have many meanings and effects. But those price movements that qualify as properly inflationary are those which collectively shift the ratio in which “all goods and services” exchange with the unit of account.

What the BIS shows in its remarkable chapter on inflation in the latest Annual Economic Review is that in this strict sense, in the decades since the 1990s when price indices were growing at very low rates, often well below 2 percent and in Japan even declining, not only was “inflation” low, but in a strict sense, price movements no longer qualified as inflation at all (fast or slow). Price movements were increasingly uncorrelated with each other and crucial connections e.g. between energy prices and the general index became much less significant in statistical terms.

Inflation – the movement in the general price level – was not just low. It would be better to say that inflation had attenuated to the point of irrelevance. It was no longer a reference point. Indeed, successive Fed chairs, Paul Volcker and Alan Greenspan adopted defined price stability precisely in these terms:

“a situation in which expectations of generally rising (or falling) prices over a considerable period are not a pervasive influence on economic and financial behavior.”

The macroeconomic dimension of prices and money “in general” was no longer relevant. The price changes that were observed were interpreted in microeconomic terms i.e. as shifting relativities between goods and services rather than being indicative of the general state of the economy or society. The general price level, one of the basic macroeconomic variables, was no longer a relevant reference point.

By contrast, an inflationary period is one in which issue of the general price level, as captured by an index, or perhaps the exchange rate, comes to dominate all other considerations. What matters, in the first instance, are not relativities, but keeping up with the overall level. In this state, the macroeconomy emerges from irrelevance, to be the dominant, overriding concern for all decision makers.

When prices rise faster, we miss the point if we simply say that inflation is higher. Reading the BIS report between the lines, it would be better to say that as rate of price increases increases, “inflation happens”. We enter an inflationary state.

To survive, investors have to shift from being stock pickers, to macro bond investors.

What is remarkable about the BIS’s recent report is that is able to show in extraordinarily rich empirical detail how the emergence and then disappearance of inflation as a macroeconomic phenomenon played out over the last half century.

One crucial index of this process is simply how far price changes begin to resemble each other. In an non-inflationary situation price changes are idiosyncratic, driven by supply factors, particular business decision or bargaining strategies by trade unions. As inflation takes over, that changes:

the degree to which the general price level becomes relevant for individual decisions increases with the level of inflation. When inflation rises, price changes become more similar

This effect can be achieved through explicit social agreements and contracts e.g. price indexation. But the BIS’s data analysis allows them to show this effect in operation across price-setting more generally. In Advanced Economies, once inflation rises to around 5 percent, the similarity of price-setting surges. For emerging market economies, with inflation experiences that go as a high as 25 percent, the effect is even more pronounced.

As inflation becomes the dominant concern, what we see is the emergence of key prices that help actors to orientate themselves in an increasingly confusing scene. Energy prices and exchange rates, for example, have a far larger influence on the general price index in high inflationary regimes than in low inflation regimes.

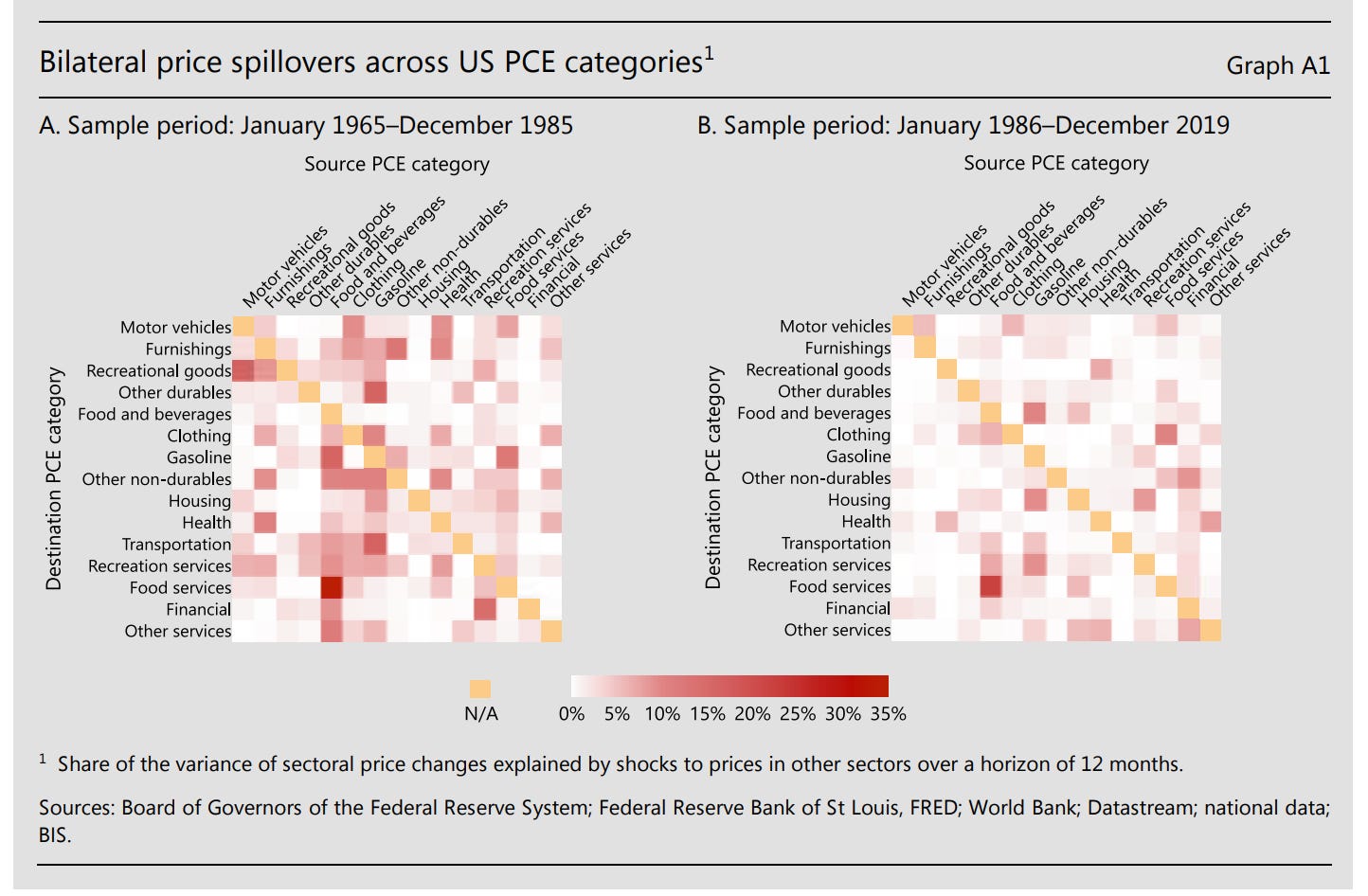

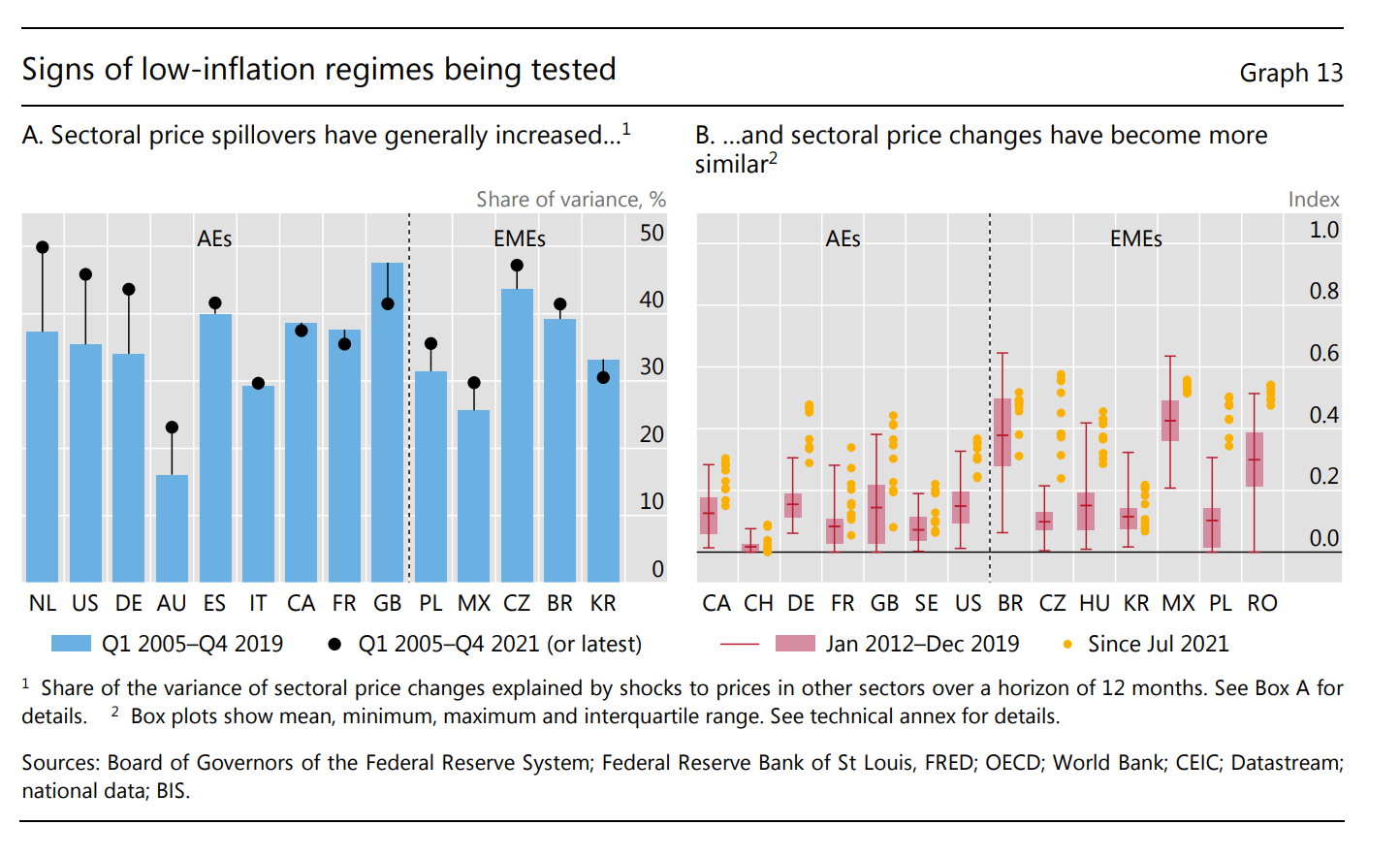

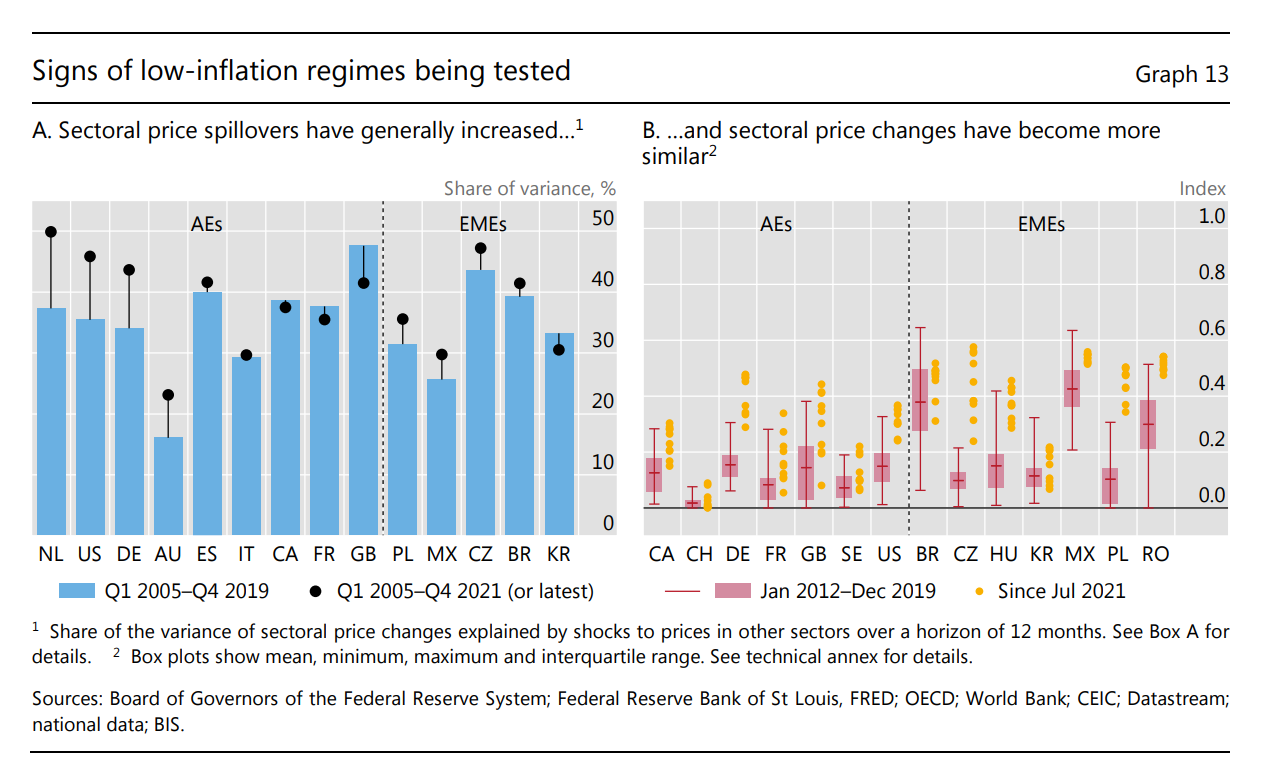

But one does not have to confine oneself to examining just the headline numbers like oil and the dollar exchange rate. What the BIS has constructed is a general measure of the degree to which shocks in the price of one sector affect the rest of the economy.

Examining how shocks to prices in certain sectors transmit and propagate to others can help shed light on how individual price changes are able to morph into broad-based inflation. One relatively simple way to do this is to look at how shocks affecting certain sectoral price indices affect the variability of prices in other sectors within a certain horizon.

The key ingredient for the construction of the spillover indices is the generalised forecast error variance decomposition (GFEVD) matrix.2 This measures the share of the variance of each PCE sector (the rows) explained by shocks to each of the sectors (the columns).

Apart from the fascinating sectoral details, what the comparison of the matrices from the high-inflation period (on the left) and the low-inflation period (on the right) shows is how inter-sectoral price linkages become attenuated as inflation falls. The matrix on the left has fewer dark-red cells.

Higher inflation per force constitutes “an economy” that moves as an articulated organism, with ripple effects running from one sector to the other. As inflation fell from the late 1980s onwards, those connections became progressively attenuated.

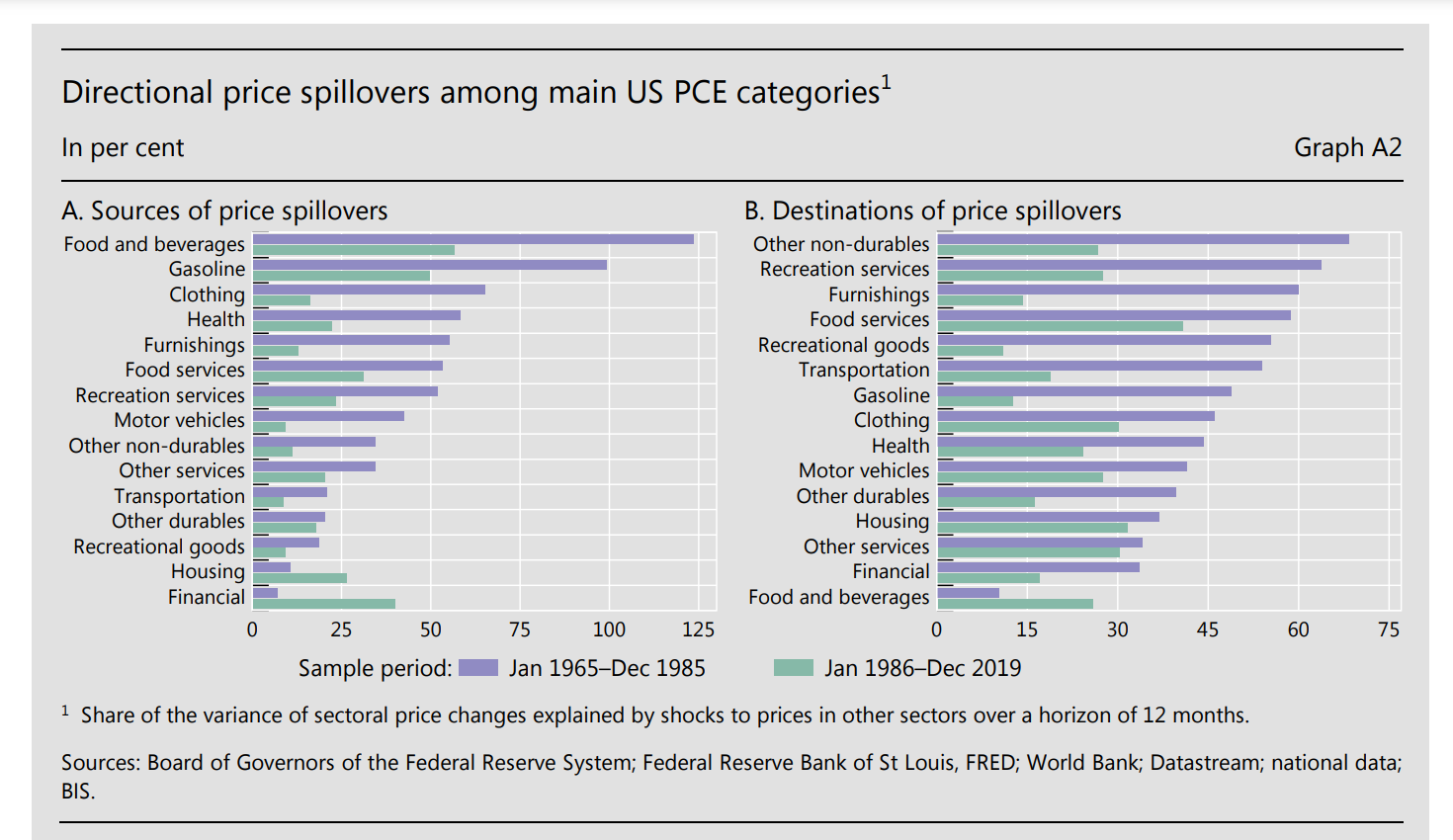

For ease of reference this result can also be broken down by particular index components. In the period 1986-2019 the key sectors no longer delivered the kind of shocks that they did in the 1965 to 1985 period, the period of the “great inflation”. Conversely, price movements which before 1986 were heavily influenced by shocks in other sectors, became less and less susceptible.

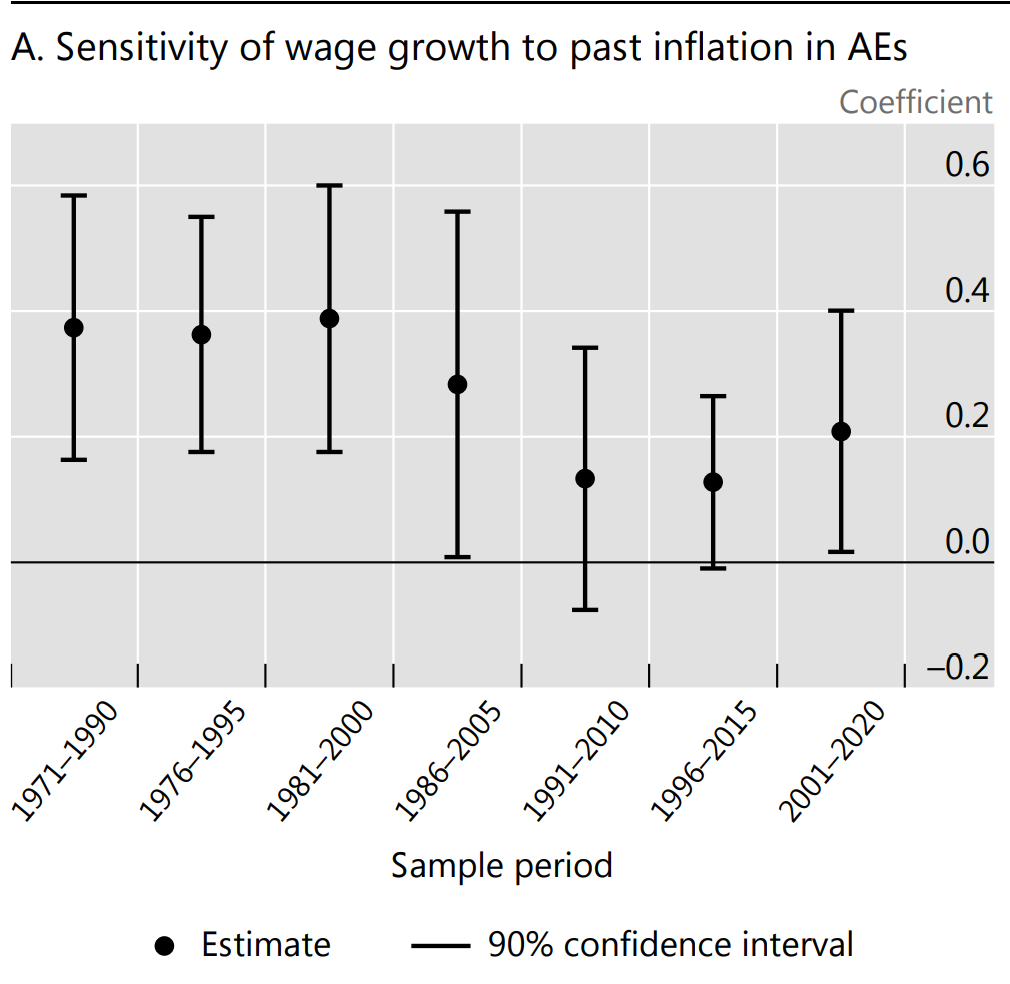

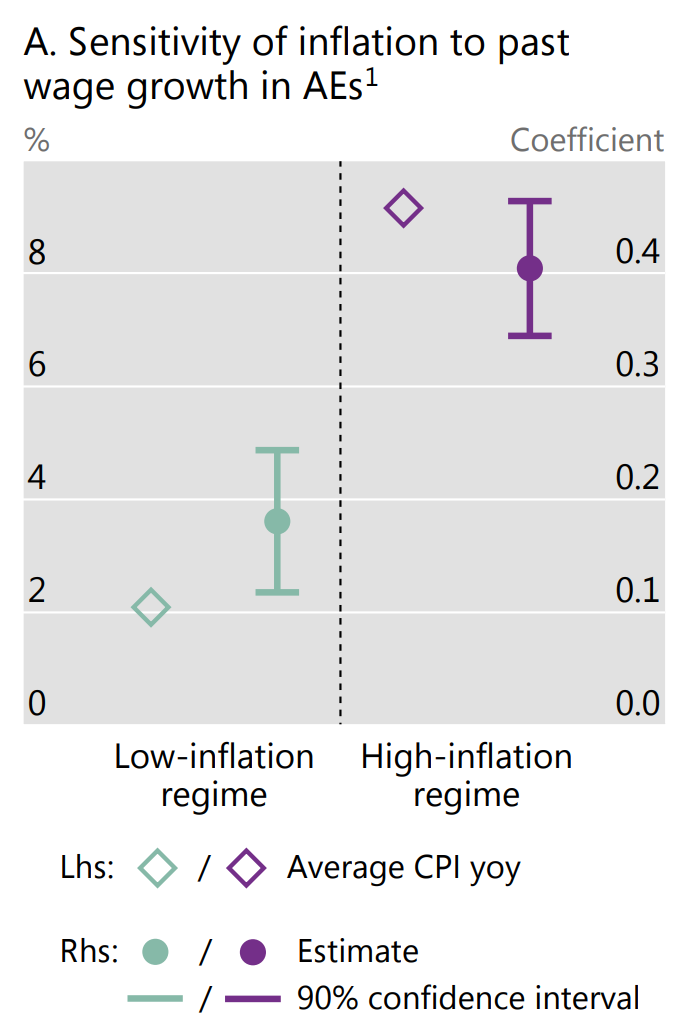

Though the BIS does not apply a political economy lens to these numbers, it would be possible to do so. The question is who has price-setting power and who does not. Who are price-takers. Because the matrices are based on the PCE price index they do not include wages, but, as I discussed in Chartbook #133, the BIS has shown how in an inflationary regime, wages are more responsible to prices and conversely prices are more responsive to wage pressure.

What worries the BIS right now is that even in the short space of time since the summer of 2021, as prices have surged, there are signs that what we are witnessing is something akin to a true inflationary process of correlated, spillover-driven, imitative price changes.

On an alarmist reading, the point is not simply that prices are rising, but thatt inflation (in the general macroeconomic, Friedmanite sense) is baaaaaaaaaack.

This may indeed be alarmist. Crucially, the signs of a wage-price spiral which, as the BIS acknowledges, is crucial to any truly general inflationary process, are weak at best.

Furthermore, the report adds an interesting consideration about policy.

Monetary policy – as in central bank interest rate setting – operates most powerfully on the common, general component of price increases.

In the low-inflation environment of recent decades it was not for nothing that central banks had to resort to unconventional measures. Their instruments have little bite in a world of microeconomic price movements.

As of early 2022 this has clearly changed.

The contention of those who refused to be panicked by inflation and still are not panicked, has always been that, if inflation were actually to occur, policy-makers had the tools to deal with it. That contention is now going to be put to the test.

*******

I love writing Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

July 3, 2022

Chartbook #133 Under the hood of the power dynamics of inflation

In 2021-2022 we are living through something very unusual – a historic break, a sudden shift from a low inflation regime, that had persisted for several decades, to a moment of much higher inflation.

Amongst those who fear inflation, it is raising deep and concerning questions. Might we be entering a new era, a new regime of higher inflation? What, previously, anchored the regime of low inflation that we have for so many decades taken for granted? Looking back, the last time we overcome rapid inflation – in the late 1970s and early 1980s – how was it that the new regime of lower inflation was institutionalized?

What is fascinating is that in answering these questions, even at a technical level in reports by an agency like the Bank of International Settlements, the underlying regime of power is thematized. In a remarkably unselfconscious way, the managers of the system articulate their preference for a particular configuration, or non-configuration of social forces.

An inflation regime, as the BIS defines it, is one of sustained and general price increases. This cannot be a one-round affair. It requires successive price and wage adjustment. It can only happen if you have a wage-price spiral, with both price and wage setters driving up their demands.

Sustained inflation ultimately involves a self-reinforcing feedback between price and wage increases – so-called wage-price spirals. Changes in individual prices can broaden into aggregate inflation. And they can also erode real wages and profit margins for very long spells. But, ultimately, they cannot be self-sustaining without feedback between prices and wages: profit margins and real wages cannot fall indefinitely. So, beyond the important impact of aggregate demand conditions on wage- and price-setting, a key question is how changes in relative prices that pass through to the aggregate price index (“first-round effects”) can trigger feedback between price and wage increases (“second-round effects”).

If this is what defines inflation, what anchors a low-inflation regime is a situation in which that reciprocal action cannot take hold. Either, neither price-setters (corporate capital) or workers have the power to set prices, or only one side does, so that you can have a first round price shock, but no second-round reaction.