Adam Tooze's Blog, page 14

September 10, 2022

Chartbook #149: Success on the battlefield whilst the pressure mounts on Ukraine’s home front.

Though the news from the frontline may be good for Ukraine. As the summer comes to a close, its economic situation is increasingly alarming. The Russian invasion dealt a devastating blow to Ukraine’s economy, its public finances are in free fall, inflation is surging and millions are threatened with misery and deprivation. Unless Ukraine’s allies step up their financial assistance, there is every reason to fear both a social and a political a crisis on the home front, which will massively compound Kyiv’s difficulties in continuing the war regardless of its progress on the battlefield.

This bleak news is driven home by a joint report compiled by the government of Ukraine, the World Bank and European Commission.

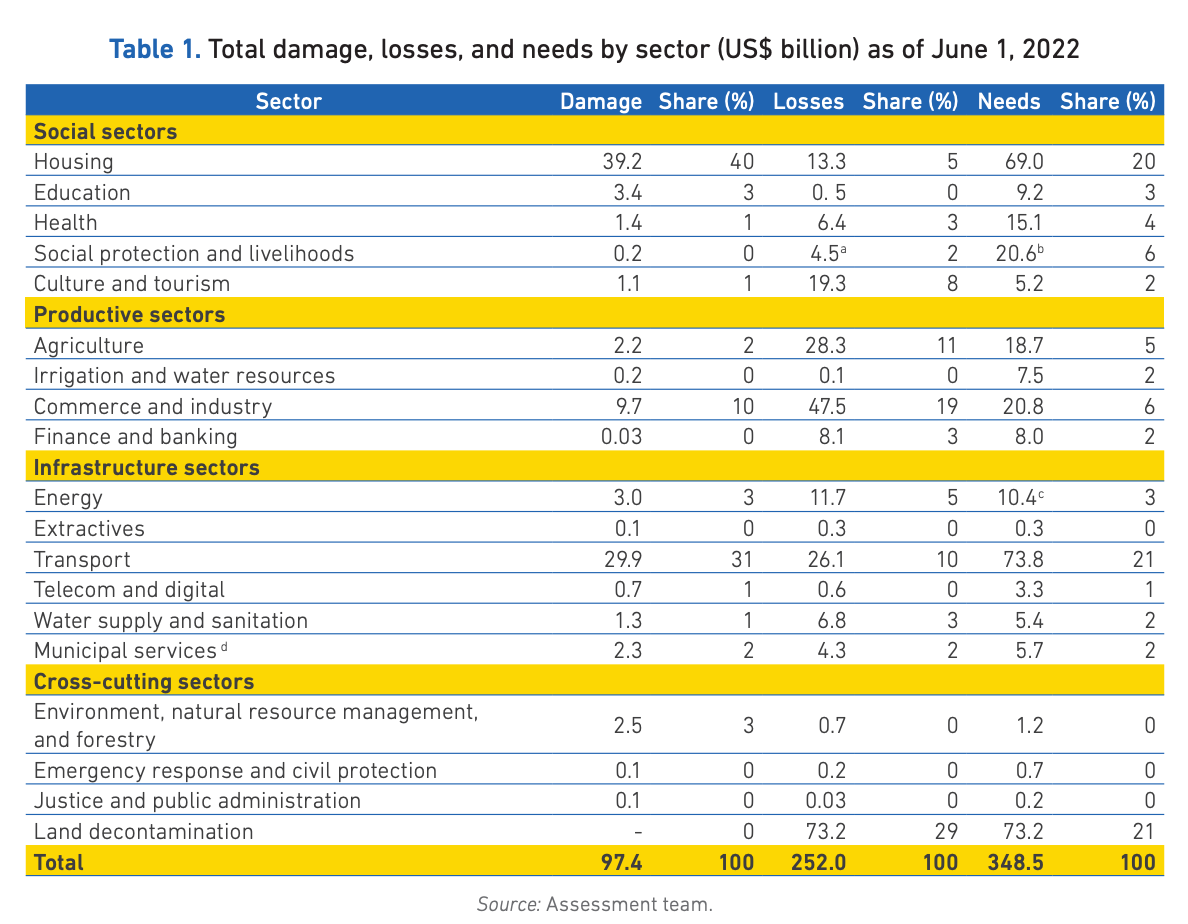

The main purpose of the Rapid Damage and Needs Assessment report is to document the financial needs of long-term reconstruction. To this end the report contains an impressive compilation of tables showing damage to housing, infrastructure and the need for decontamination.

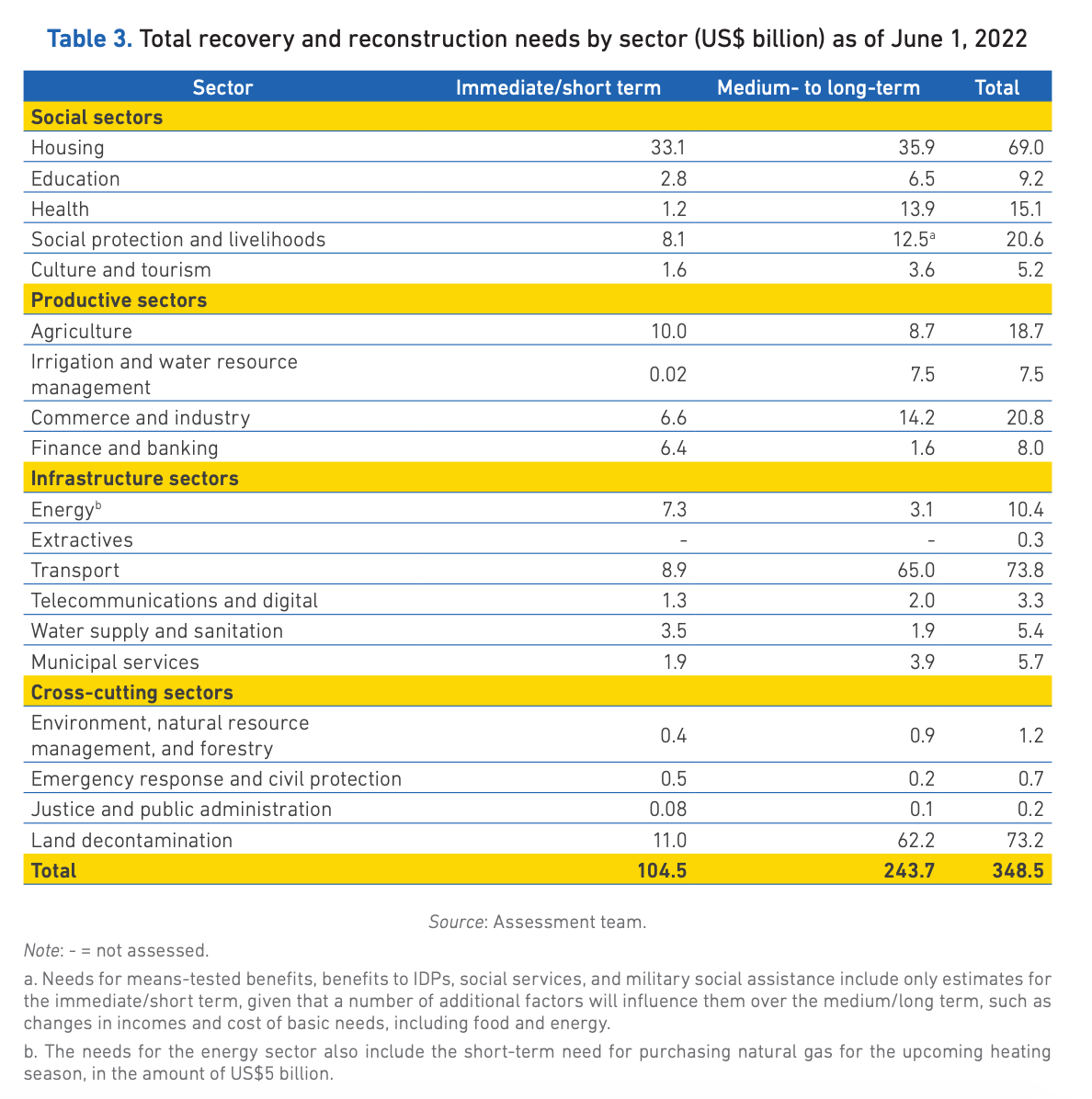

All told the bill for recovery and reconstruction comes to $104 bn in immediate and short-term spending and $243 bn over the longer term.

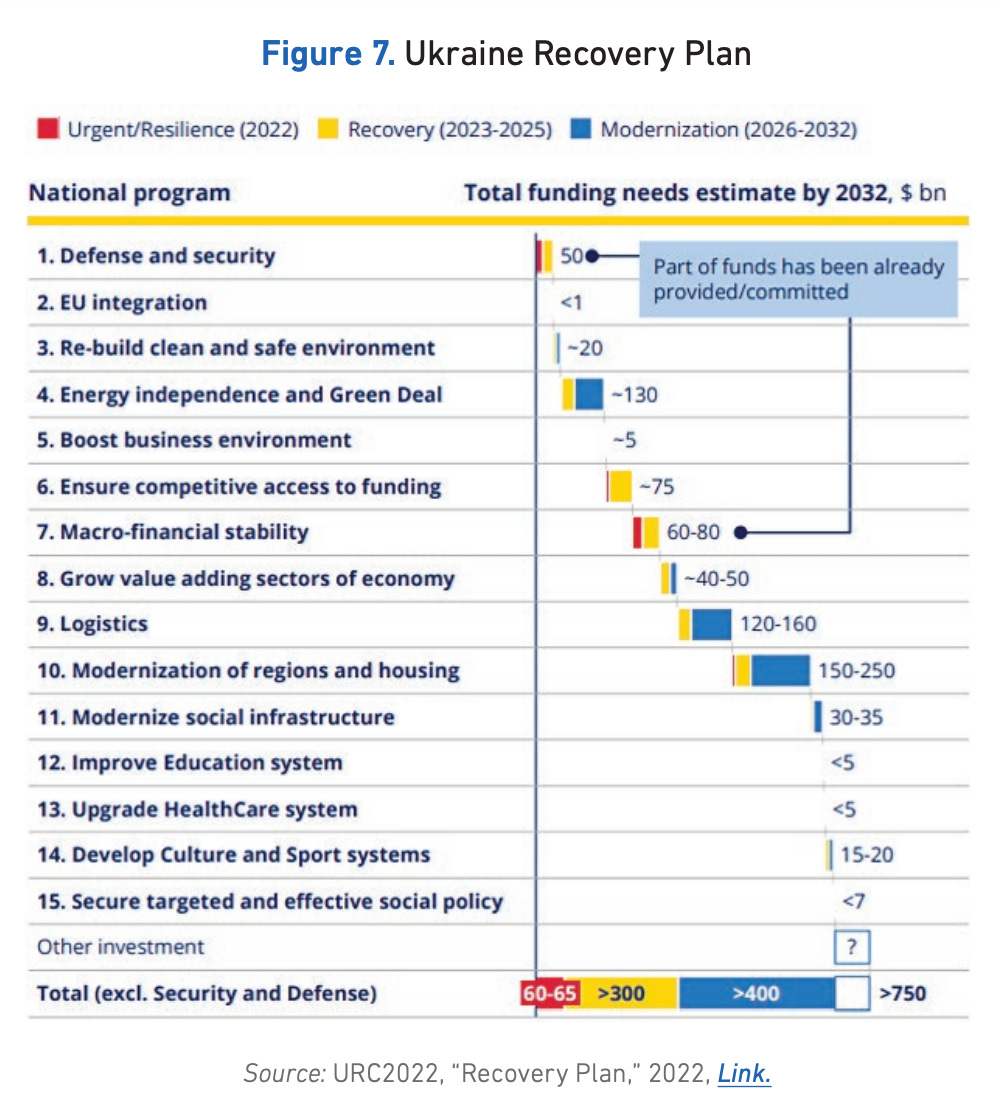

As laid out at the Lugano reconstruction conference in July, Kyiv has a recovery plan that stretches to 2032 and involves spending on reconstruction and modernization totaling $750 billion.

All of this long-term planning, however, has a ghostly aspect given the desperate economic and social situation facing Ukraine, not by 2032, or 2025, but over the coming weeks and months.

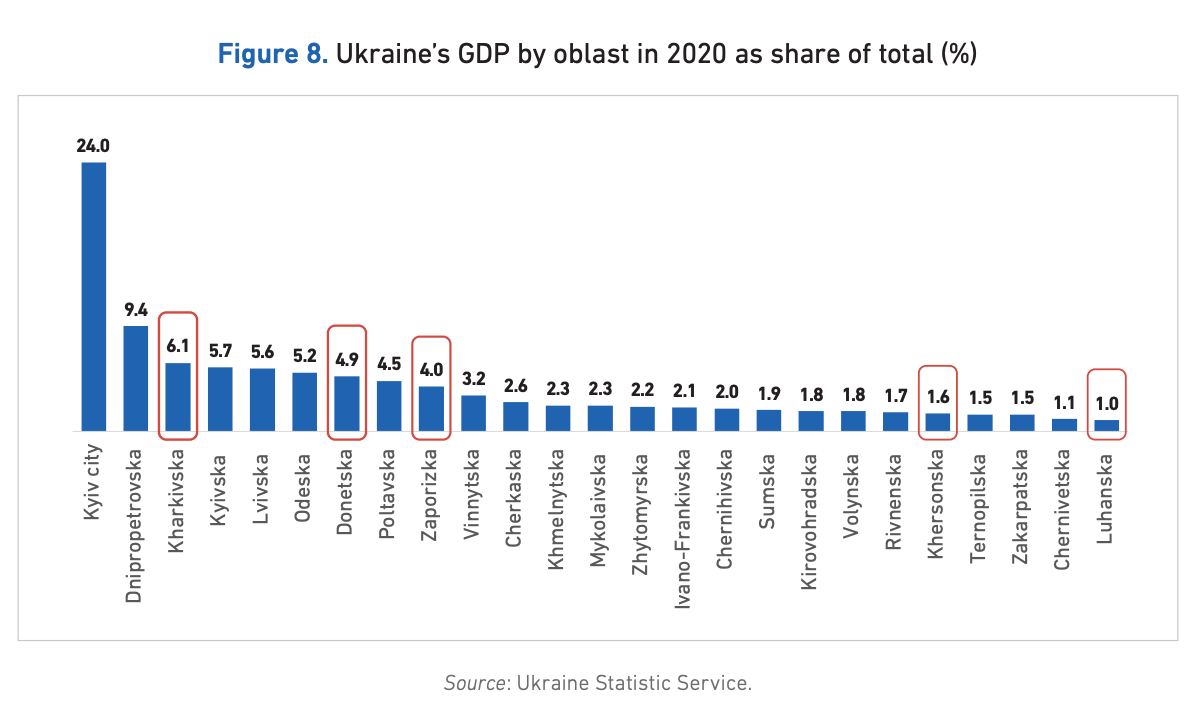

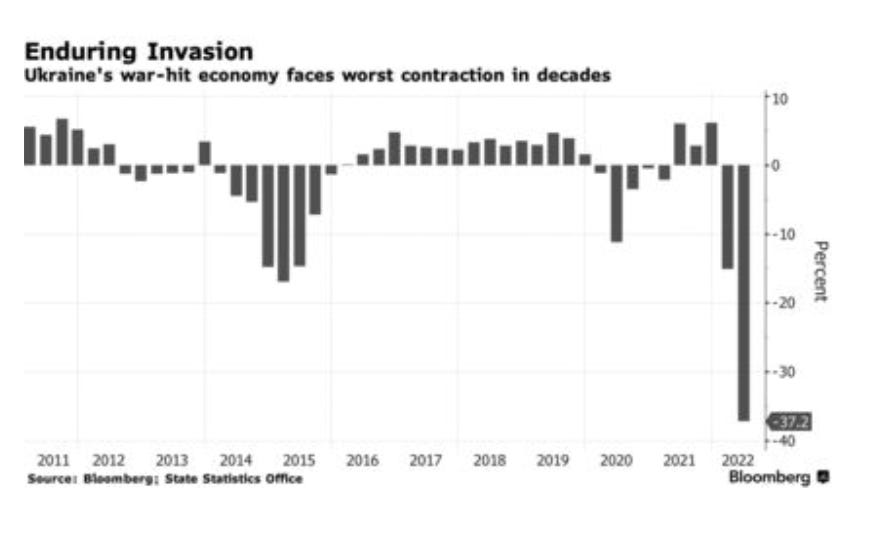

The hit to Ukraine’s economy in the spring was devastating. In March, the Russian attack engulfed 10 oblasts and the city of Kyiv, which together account for more than 55% of prewar GDP. Today, the fighting continues in regions which account for c. 30% of prewar GDP.

Under the immediate impact of Russia’s assault, in the first quarter of 2022 Ukraine’s GDP shrank by 15.1 percent year over year (YoY), wtih a gigantic 45 percent fall in March. In the second quarter, the contraction on an annualized basis was measured at 37 percent. This is far worse than the shock suffered by Ukraine in 2014-2015. With some signs of recovery in August, Kyiv is now guestimating that the contraction for the year as a whole will be in the order of 33 percent.

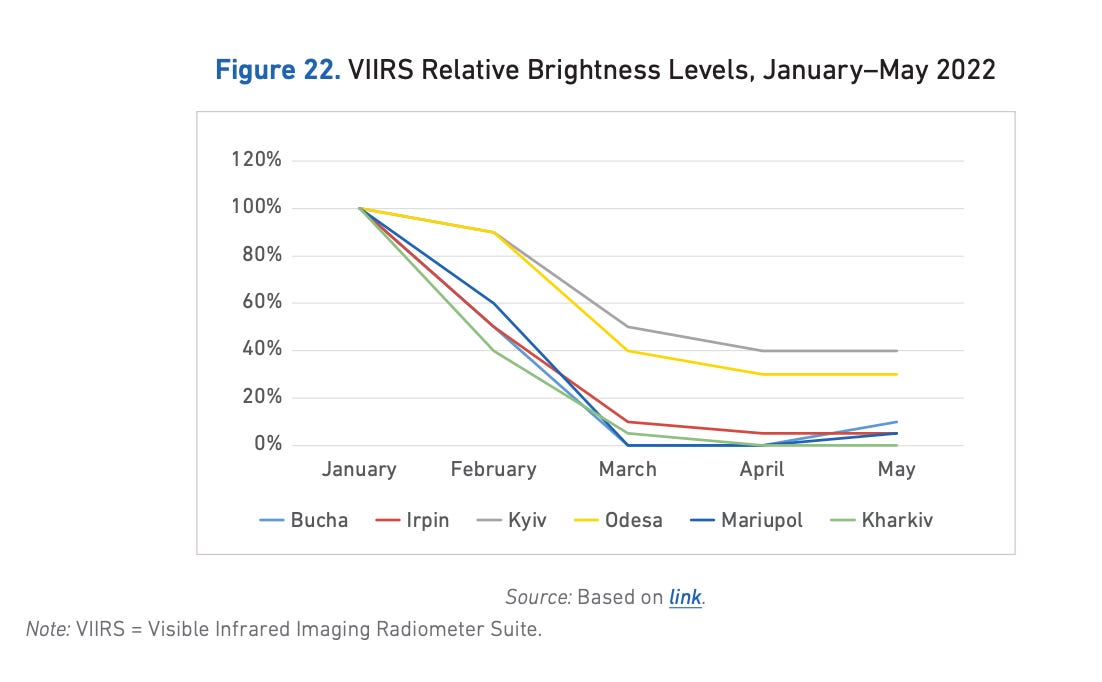

These GDP figures are dramatic. But they are also rather abstract. A more concrete way to track the level of economic activity is to monitor night-time illumination. All over Ukraine in the spring of 2022 the lights went out.

This is normally an excellent indicator of the overall level of economic activity. But as the RDNA report notes, there are things to bear in mind when monitoring illumination in wartime.

While in this case nightlight brightness is not a direct indicator of access to electricity services (since many citizens hide in their basements at night), in some cities it remains an indication of the loss of access to electricity. As shown in Figure 22, streetlights completely disappeared in most of Bucha and Irpin during March and April. In Kyiv, the decline was more gradual and has remained stable after the end April.

Another way to bring home the significance of the GDP numbers, is to examine levels of poverty.

Prewar, Ukraine was a middle-income country with a poor track record of growth. But it was also a post-Soviet society with an unusually large welfare network. In Ukraine, a quarter of the population receives old-age pensions, which are a key safety net.

As a result of this extensive welfare network, severe poverty below US$5.5 per person per day was rare. Under the impact of the war, the share of Ukrainians falling below that poverty line is expected to increase tenfold and reach at least 21 percent in 2022; war-affected regions are expected to experience much higher poverty rates. In Khersonska oblast, which is currently at the heart of fighting, food prices have surged by 62 percent resulting in a spiking poverty rate.

For a large part of Ukraine’s population of 44 million, the war has upended normal life:

One-third of Ukrainians have been displaced by the war. Over 6.8 million Ukrainian residents have left the country, a large majority of them women and children.4 An estimated 6.6 million people are internally displaced—fewer than in the previous month5 —with many individuals displaced more than once since leaving their homes of origin.6 According to the UN Office for the Coordination of Humanitarian Affairs (OCHA), the humanitarian situation is deteriorating rapidly, as access to critical services such as clean water, food, sanitation, and electricity declines, and 17.7 million people are left in need of humanitarian assistance

The social crisis is so severe, because of the inability of the majority of the internally displaced refugees to support themselves.

To address this crisis, Ukraine’s needs a capable government apparatus. It has a dense network of social provision. But those agencies, networks and institutions need funding and that is in jeopardy.

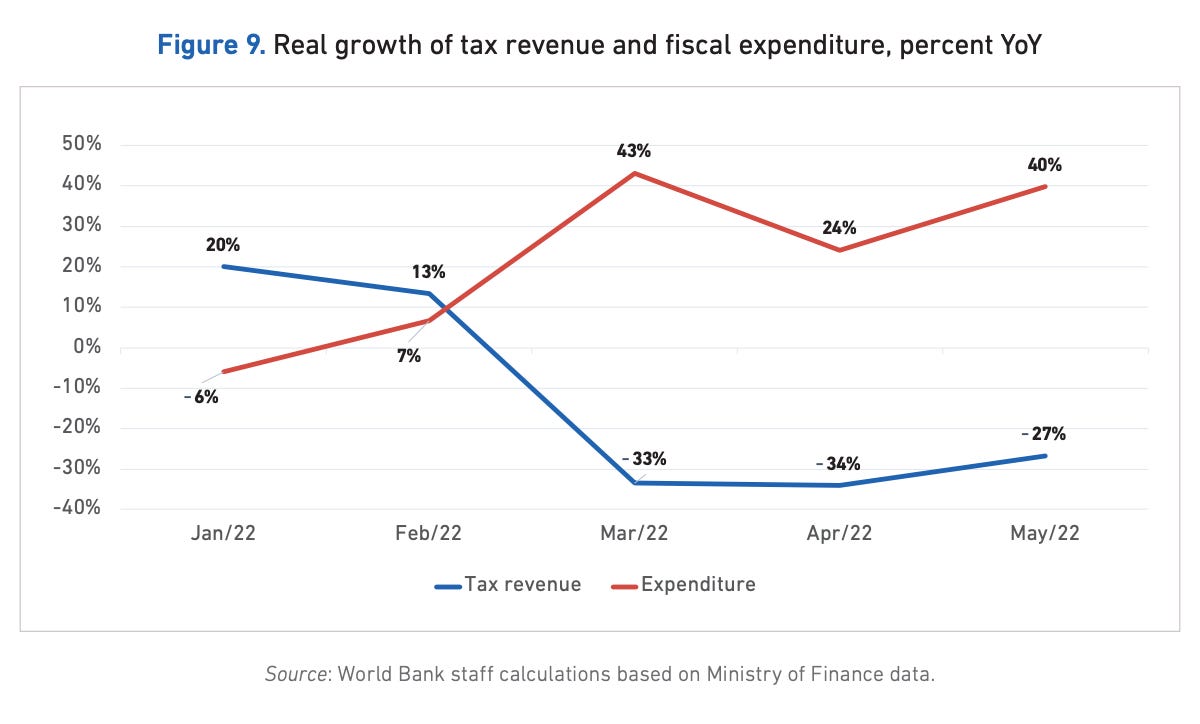

Since the beginning of the war, tax revenue collection has deteriorated significantly, while public expenditure has increased sharply.

Since the beginning of the war, as military spending surged by 4.5 times, Kyiv has struggled to slash non-military spending.

Non-essential current expenditures have been cut 78 percent YoY. Far from engaging in large-scale reconstruction, capital spending has been cut back by 61 percent YoY. But there is a limit to how far austerity can be carried in wartime. Between March and May, Ukraine’s public spending on wages and salaries surged, including for emergency medical personnel and first responders. Transfers and social protection spending increased, as did procurement of goods and services, to pay for basic recovery work. All told – despite the cuts in non-priority areas – surging spending and falling tax revenues have opened a nonmilitary fiscal need of over US$15 billion for the second half of 2022. This figure takes account of Kyiv’s efforts to reduce its debt service by rolling over domestic debt and a two-year deferral on external debt amortization. Allowing for military spending and current recovery needs, Ukraine’s total fiscal financing needs may reach US$28.8 billion in the second half of 2022 (around US$4.8 billion per month).

To cover some of this funding shortfall, the National Bank has stepped in to monetize the deficit. As of the end of June the National Bank had monetized over US$7.7 billion in fiscal needs.

That paid the bills but it also helped to stoke a surge in inflation. In August inflation in Ukraine reached 23 percent year on year, more than double the rate in February. By the end of the year, the central bank warns that inflation may reach 30 percent.

If this continues the outlook is disastrous.

In a scenario of continued deficit monetization, the poverty rate is expected to climb to 34 percent by the end of 2022—a level not seen since the early 2000s—as rising inflation erodes the purchasing power of low- and middle-income households. Going forward, if the extent of monetization is limited to avoid excessive inflation, sweeping expenditure cuts will be needed and will affect the most vulnerable segments of Ukrainian society. Under this scenario of austerity, poverty rates are projected to further increase to over 40 percent in 2022 and 58 percent by 2023. In this worst-case scenario, an additional 18 million Ukrainians would fall below the poverty line.

The National Bank is struggling to control inflation. It has raised interest rates to 25 percent. It would like ideally to absorb as much purchasing power as possible into stable, government war debt. That puts pressure on the government to offer attractive interest rates. But, for fear of further burdening the budget, Zelensky’s government is resisting an increase in bond coupon. If interest rates on war bonds are too low, however, they will not attract buyers, which in turn forces the central bank to finance the war effort itself.

Given the scale of the financial pressure it is under, it is hardly surprising that Kyiv is appealing for help from outside. Last week it asked for an immediate package of international financial support totaling $17 billion.

So far the international community has been providing c. $1.5bn a month to support Ukraine’s budgetary needs, which is significant, but far short of Kyiv’s needs. Pledges to date extend no further than the end of 2022, with no firm commitments for 2023. The EU signed up to a notional total of €9bn in budgetary support in May, but only about €1bn has been disbursed. With Kyiv running deficits of $5bn a month Von der Leyen said on Friday that €5bn from the EU was “in the pipeline”.

The urgency of those funding needs is compounded by the seasonal outlook. With the summer having drawn to a close, Ukraine now faces falling temperatures. As the FT reports, “average temperatures in Ukraine typically fall from 20C in summer to minus 3C in winter, with an average of minus 7C in some regions, according to the Climatic Research Unit at the University of East Anglia.” As Arup Banerji, the World Bank’s regional director for eastern Europe, noted:

the bank was “terribly concerned” about the arrival of winter. “The damage that Ukraine has suffered has been just staggering,” said Banerji. “Ukraine’s winter season starts on October 15 and can be really harsh. This could be quite devastating given that many houses have windows and doors missing and there are so many internally displaced people.”

A population of millions, facing a freezing winter with windows and doors blown out, is a grim prospect indeed. Without a dramatic step up in international financial assistance, Ukraine will face a tragic choice between continuing the war at full intensity and risking a social and economic crisis that will destabilize the home front. If Kyiv finds itself in that impasse, the risk is that the highly technical tensions that are currently visible over interest rate policy between the central bank and the national government will widen into deeper political divides over the management of the war effort. That would put in jeopardy the political consolidation that has been one of Ukraine’s most remarkable achievements in this terrible ordeal.

September 9, 2022

Ones & Tooze: Is China’s Economy in Trouble?

China’s economy is projected to grow by four percent this year, a rate that many countries would envy. But with China’s track record, that number could actually be a harbinger of bad news. On today’s show, Adam and Cameron discuss the mechanics of the Chinese economy and why it’s unlike any other in the world.

Also on the show: Golf has been described as a game of strenuous idleness. How did it become an $84 billion industry in the United States?

And… Adam and Cameron will be doing a live taping of the show in New York City on October 25th! This is the podcast’s first-ever live show, at an intimate venue on the Lower East Side. Seating is limited! Follow the link for tickets (livestream available as well). https://www.caveat.nyc/events/ones-and-tooze-live-10-25-2022

Find more episodes and subscribe at Foreign Policy

September 2, 2022

Chartbook #148: Life, liberty and the pursuit of happiness? How China, Cuba and Albania came to have higher life expectancy than the USA.

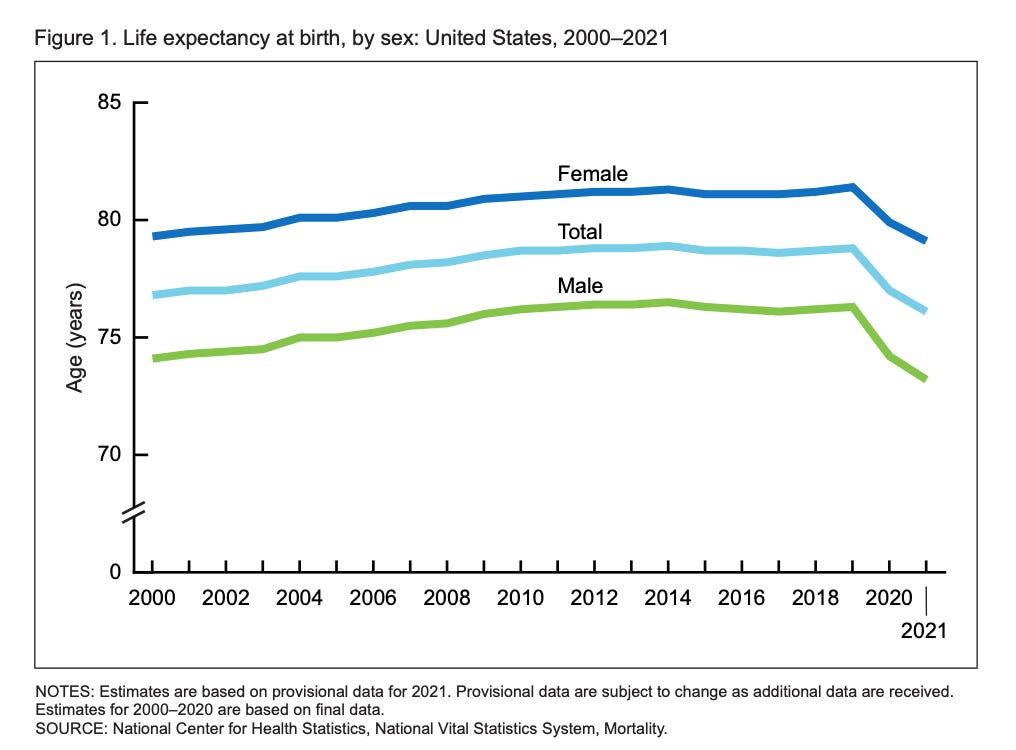

In August America’s Center for Disease Control (CDC) published a set of data that ought to have brought political, economic and social debate to a standstill. If there is one question that should surely dominate public policy debate, it is the question of life and death. What did the Declaration of Independence promise, after all, if not “life, liberty and the pursuit of happiness”. But on that score the CDC in 2022 delivered alarming news. In the last three years, life expectancy in the United States has plunged in a way not seen at any point in recent history.

Source: CDC

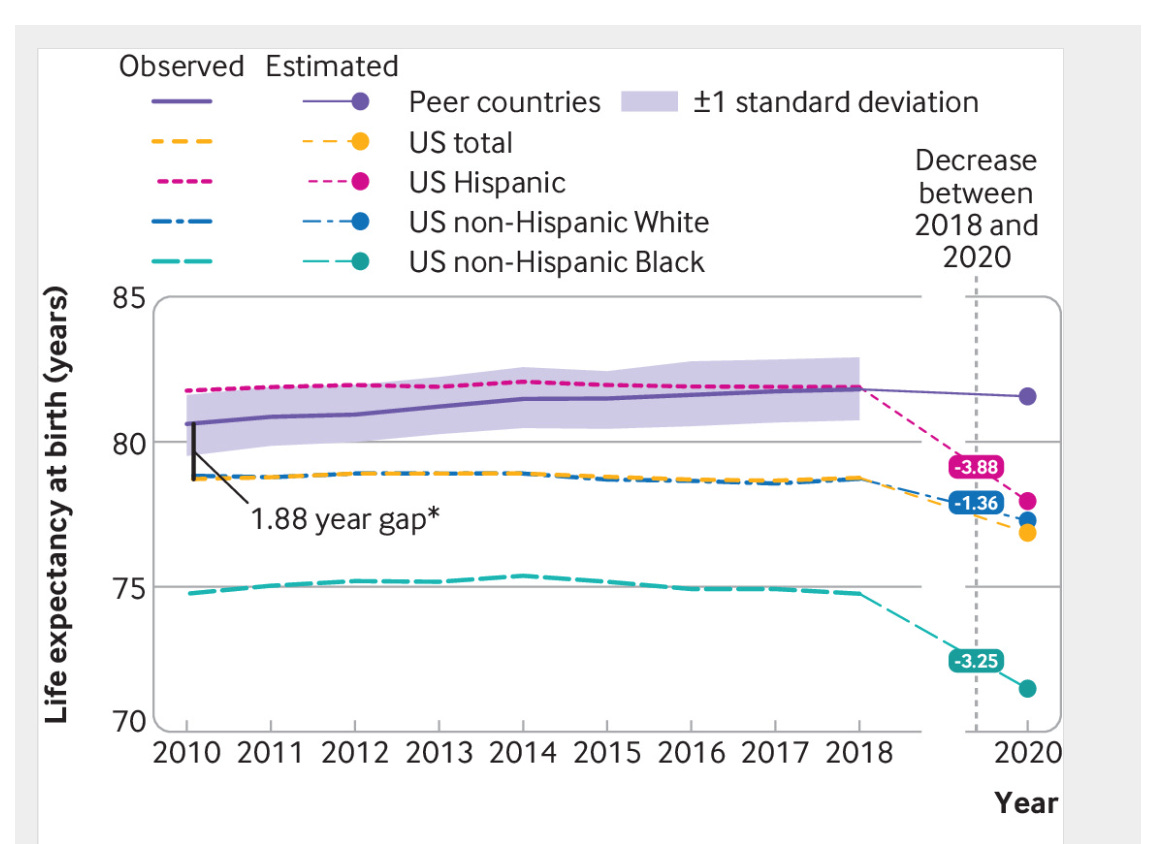

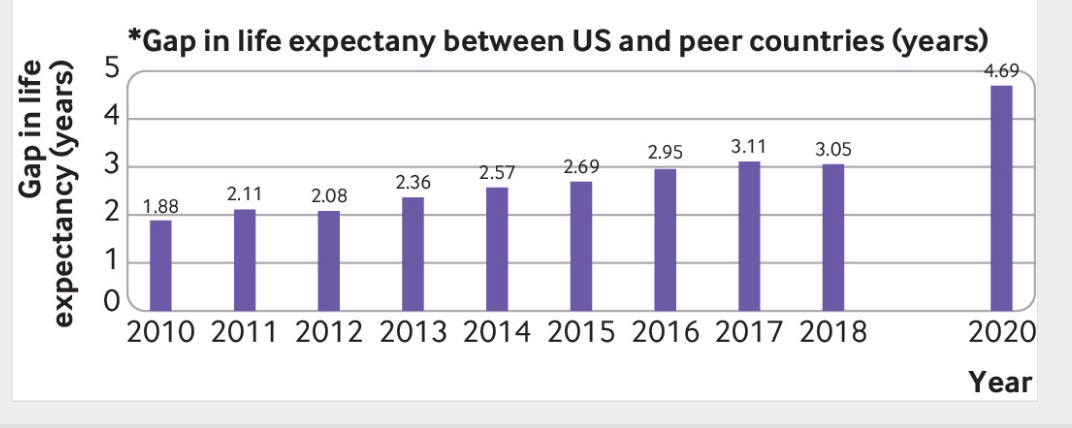

America is inured to bad news about its health. Life expectancy in the United States has stagnated since 2011, a trend which separates the United States not just from rich peer countries but from most other countries in the world, rich or poor.

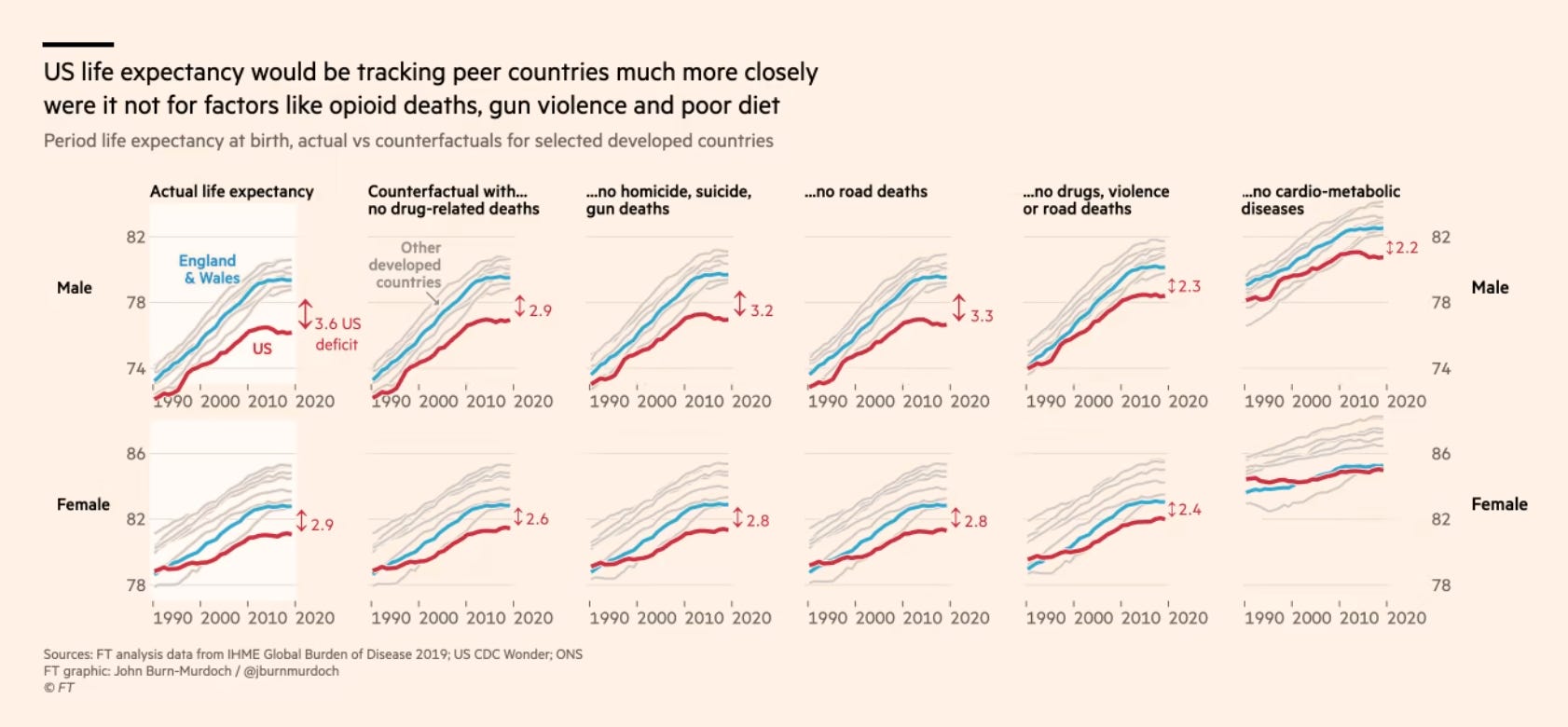

Given economic growth and advances in medicine for life expectancy to stagnate requires serious headwinds. In the United States those headwinds include, homicides and suicides, the opioid epidemic (so-called deaths of despair) car accidents and obesity. As John Burn-Murdoch shows in the FT, without those factors the US would have tracked its peer societies much more closely.

Source: FT

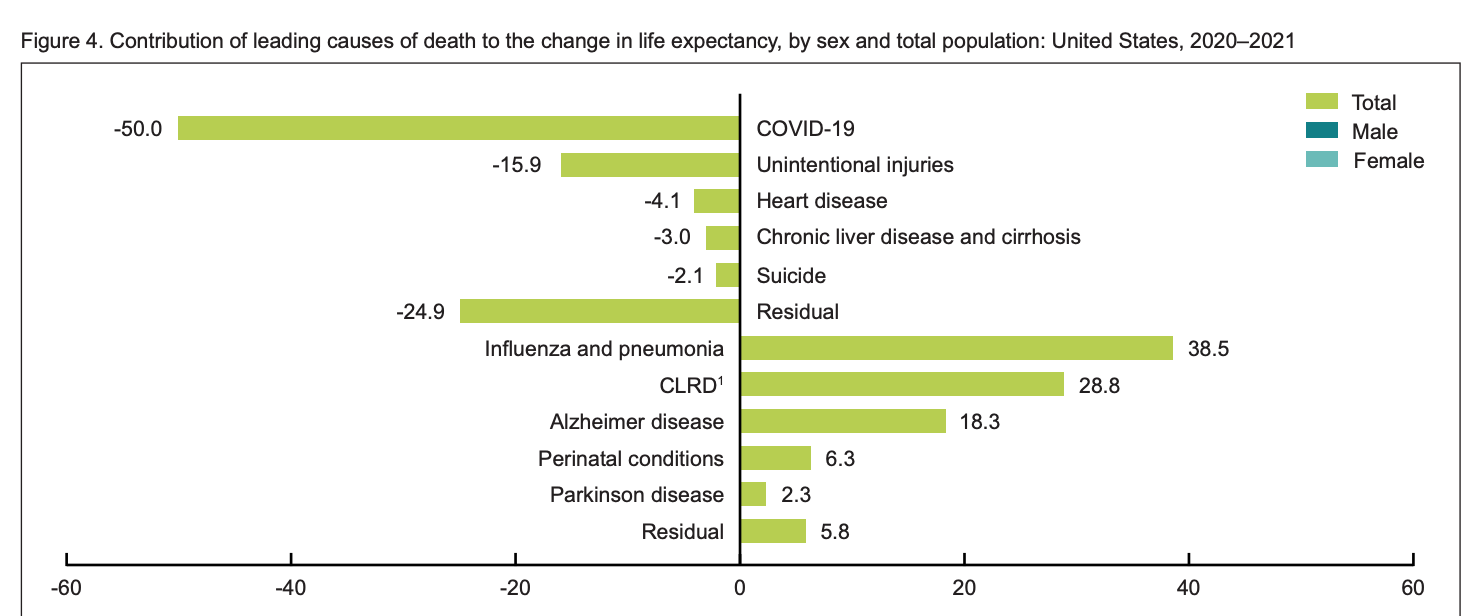

But stagnation is one thing, the collapse since 2019 is a phenomenon of a different quality. It is a full measure of the disaster that was the COVID pandemic in the United States. Over a million Americans died of COVID, one of the worst outcomes on the planet.

According to the CDC, half the disastrous fall in life expectancy is attributable to COVID with the opioid epidemic being a second significant factor.

Source: CDC

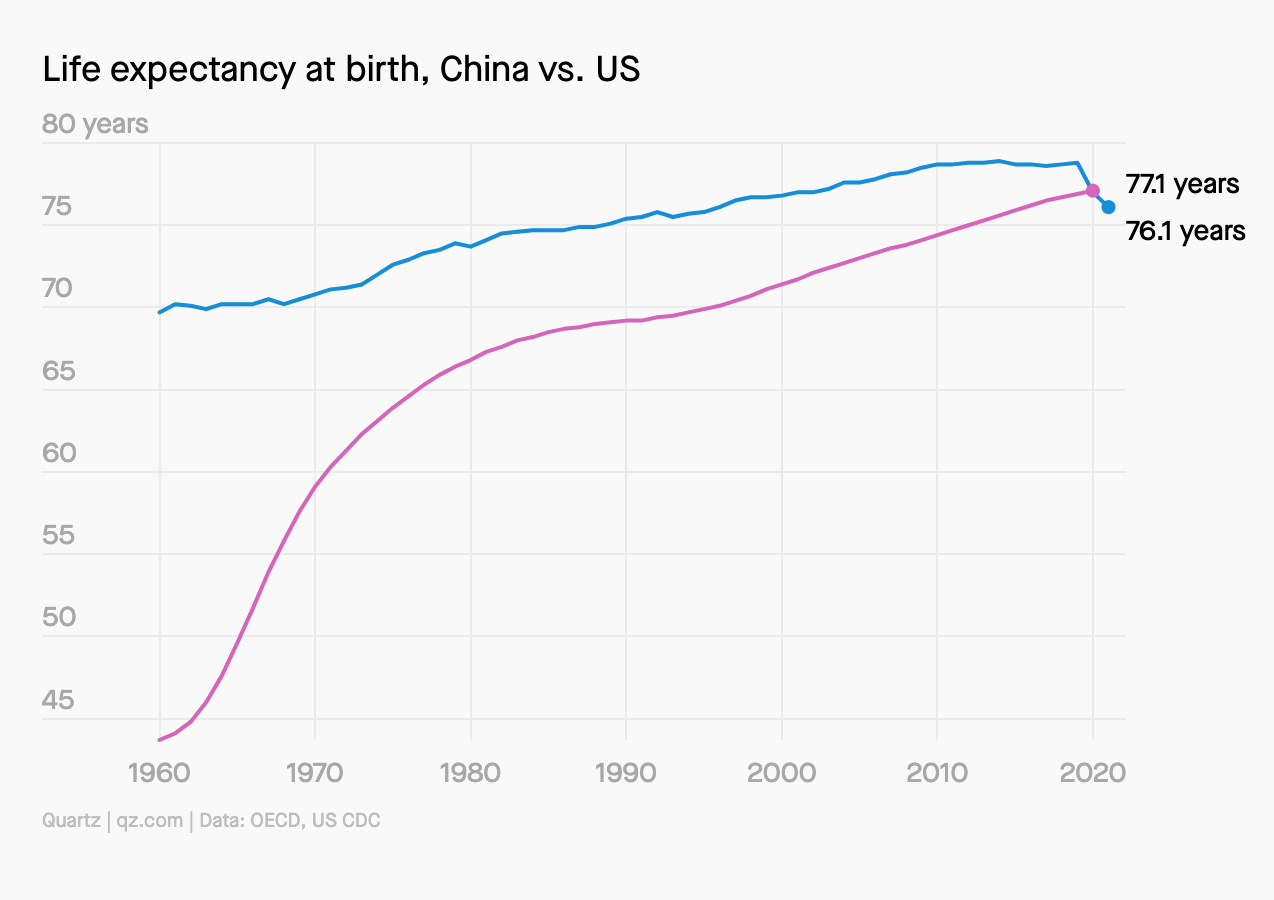

The data are eye-catching in their own right. But when you put them together with global figures, you find that 2021 marked the moment in which American life expectancy was overtaken by that of China. This is a historic transition in some ways even more telling than the more commonly cited GDP figures.

In living memory China’s life expectancy languished at levels prevailing in the West a hundred years ago. By the 1980s, thanks to the provision of basic sanitation, a minimum standard of living and health care, Communist China had surged ahead of most other developing countries. Chartbook Newsletter #28 showcased the reports of the World Bank on this startling fact. China’s dramatic economic growth since the 1980s propelled further steady increases.

In terms of healthy years of life, China overtook the United States already in 2018. At the time the United States was one of only five countries – the others being Somalia, Afghanistan, Georgia and Saint Vincent and the Grenadines – that were experiencing a fall in healthy life expectancy at birth. Extrapolating those trends, China was expected to overtake the United States in absolute life expectancy by the mid 2020s. The divergence in the handling of the COVID pandemic has brought that moment forward to 2021.

Zero COVID is now a strategy much criticized in the West. The cost to China in GDP terms in 2022 will be great. The megacity of Chengdu is the latest to be shutdown. As of this week, its 21 million inhabitants are confined to their homes. That will involve a nightmarish restriction of day to day freedoms. But Beijing operates under the assumption that given its current rate of vaccination, a Western-style epidemic would cost 1.5 million deaths nationwide and it is not willing to pay that price. The consequences of that painful choice show in the data. In 2020, unlike in most other countries, life expectancy in China actually increased and will likely increase again in 2021. The contrast to the United States is stark.

It is worth pausing at this point to briefly explain what “life expectancy” measures. As the BMJ explains:

Life expectancy is a widely used statistic for summarizing a population’s mortality rates at a given time.2 It reflects how long a group of people can expect to live were they to experience at each age the prevailing age specific mortality rates of that year.3 Estimates of life expectancy are sometimes misunderstood. We cannot know the future age specific mortality rates for people born or living today, but we do know the current rates. Computing life expectancy (at birth, or at ages 25 or 65) based on these rates is valuable for understanding and comparing a country’s mortality profile over time or across places at a given point in time. Estimates of life expectancy during the covid-19 pandemic, such as those reported here, can help clarify which people or places were most affected, but they do not predict how long a group of people will live. This study estimated life expectancy for 2020. Life expectancy for 2021 and subsequent years, and how quickly life expectancy will rebound, cannot be calculated until data for these years become available.

Source: BMJ

Rather than life expectancy, it might be better to refer to the measure as something akin to mortality profile.

In any case, it is not only China that has overtaken the United States based on this metric. In 2021 Cuba has a higher life expectancy than the US. So does Albania.

In a society marked by inequality as deep as modern America’s, to speak in terms of national averages is not very meaningful. The circumstances of life and health outcomes are vastly different.

COVID impacted the minority populations of the United States with particular force, and Hispanics and Hispanic men in particular. In 2020 life expectancy of Hispanics fell by almost 4 years.

Source: BMJ

Hispanics entered the pandemic with life expectancy substantially above the national average. The opposite is the case for Black Americans.

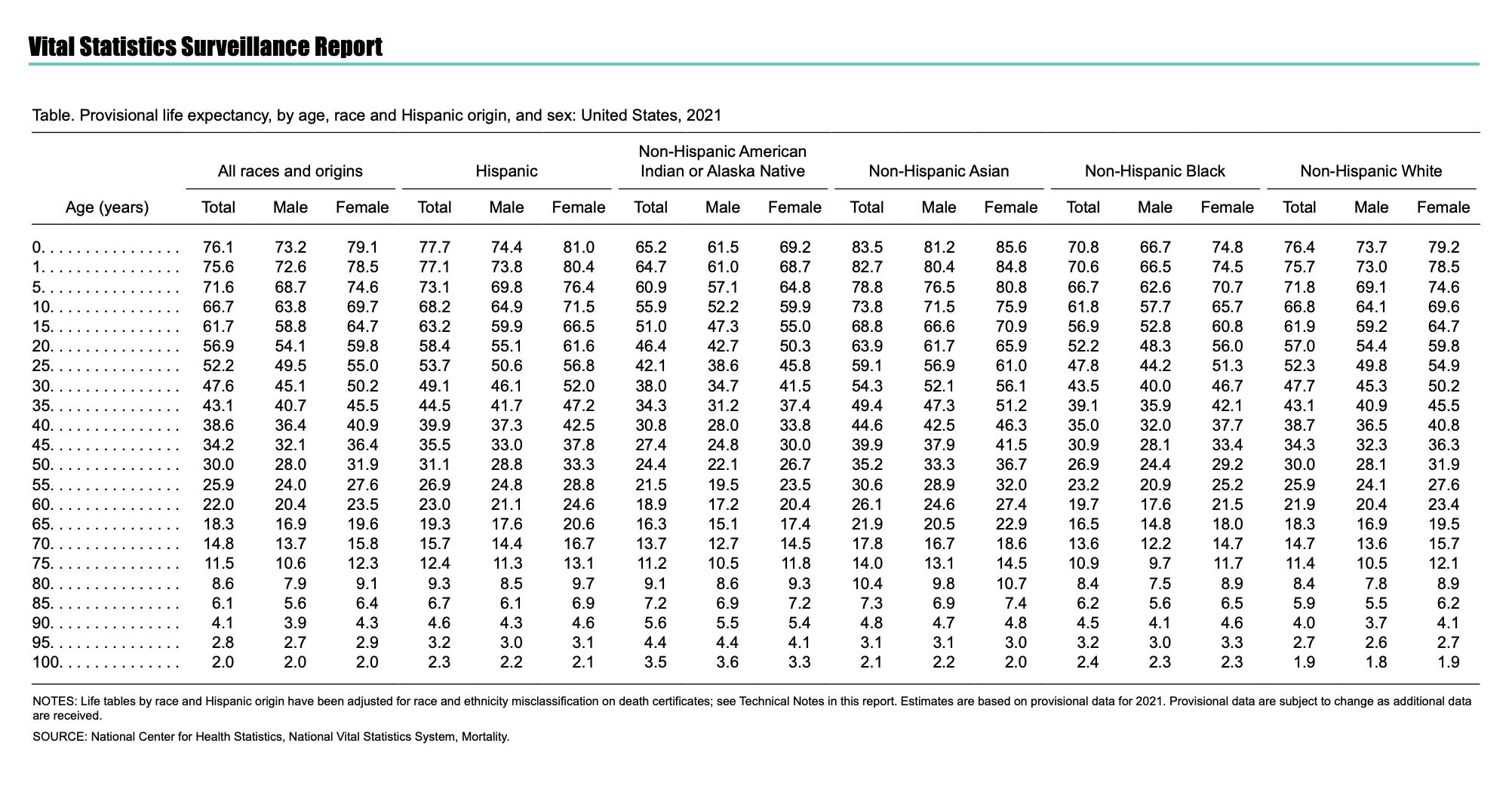

In 2021, according to the CDC, the life expectancy of Black American men at birth was 66.7 years, as compared to 73.7 for Non-Hispanic Whites.

Source: CDC

A life expectancy of 66.7 means that Black men in the United States have, at birth, the same life expectancy as men in Pakistan, a country which ranks #150 out of 193 on the global list. In 2021, a boy born in an African success story like Rwanda has a longer life expectancy than a Black boy born in the United States. Men in India, Laos and North Korea have a higher life expectancy than Black men in America.

The most disadvantaged populations of all are Native Americans. In 2021, according to the CDC, Native American men have a life expectancy that puts them on a par with low-income Sub-Saharan African countries such as Togo or Burkina Faso, some of the poorest countries in the world.

One might think that faced with these stark facts all other subjects of political debate would pale into insignificance. Whatever else a society should do, whatever else a political system promises, it should ensure that its citizens have a healthy life expectancy commensurate with their nation’s overall level of economic development. An ambitious society should aim to do more, as Japan does for instance. Judged by this basic metric, the contemporary United States fails and for a substantial minority of its population, it fails spectacularly. And yet that extraordinary and shameful fact barely registers in political debate, a silence that is both symptom and cause.

****

I love putting out the newsletter for free to thousands of readers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options.

Several times per week, paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

There are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.Ones & Tooze: The Cost of Space Exploration

As NASA prepares for new missions Adam and Cameron look at the cost of space exploration and how America views its return investing in the space program. The two also discuss what a possible lunar economy might look like. In the second segment Adam answers listener questions on everything from how to get the rich to pay their fair share to the economics of union organizing.

Find more episodes and subscribe at Foreign Policy.

August 27, 2022

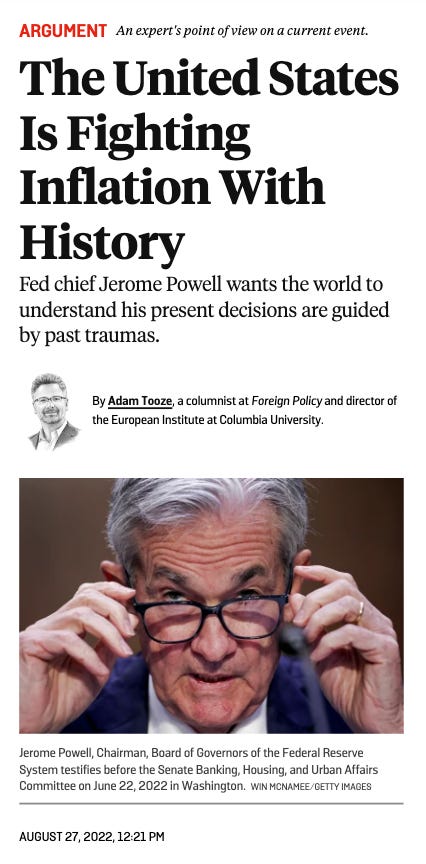

The United States Is Fighting Inflation With History

At the annual gathering of central bankers and economists in Jackson Hole, Wyoming, this year, all eyes were on U.S. Federal Reserve Chair Jerome Powell. Last year at the Jackson Hole conference, Powell had announced a new era in economic policy. This was premised on the assumption that we were in an era of low inflation. The Fed would, in the future, target average inflation, offsetting periods of low inflation below 2 percent per year with periods of more rapid price increase. Today, that world seems very remote. Inflation in the United States is running at more than 8 percent, the most rapid rate since the 1970s. Given this extraordinary turnaround, Powell needed to signal that the Fed was serious about stopping inflation.

How to make the case? Jackson Hole is a meeting of central bankers and economists. But in making his stand, Powell invoked neither economic theory nor econometrics. Instead, he summoned history.

He gave a speech laced with references to the 1970s and 1980s and paid his respects to three of his predecessors—Paul Volcker, Alan Greenspan, and Ben Bernanke. His aim was to signal that though we may no longer be in the era that Bernanke once dubbed the “great moderation,” that does not mean that we are going backward to the future. We are not heading back to the 1970s. The Fed will meet the challenge of inflation promptly and head-on. This time will be different.

In the fall of 2021, Powell still spoke of inflation as transitory. And it remains true that a large part of the price surge has been induced by supply-side issues, such as supply chain bottlenecks and surging oil prices. There is every reason to expect those pressures to ebb in the coming months. But to overemphasize this point would not help Powell make his case. So, instead, he placed emphasis on the inflationary momentum that has built up on the demand side. Investment and consumption are running ahead of capacity. Wage growth has accelerated significantly. To damp this down, the Fed is raising rates, squeezing credit, and encouraging saving. The result, as Powell acknowledged, will likely be a period of “below-trend growth” and some “softening of labor market conditions.” This is central-banker-speak for a recession.

Read the full article at Foreign Policy.

Chartbook #147: Jackson Hole 2022 – the 18th Brumaire of Jerome Powell

It is the weekend of the eagerly anticipated Jackson Hole monetary policy conference. You can see the agenda, the papers and notes on the discussion here. Since the conference became a focal point of global monetary policy discussion, in 1982, it has not met under conditions as complex as they are today.

To mark the occasion Cameron Abadi and I did a podcast segment about the Jackson Hole conference for Ones and Tooze.

The Jackson Hole conference is different. It isn’t a jamboree like Davos, or a giant global gathering like the IMF/World Bank meetings in DC. Jackson Hole is an exclusive wonkfest attended by barely more than 100 central bankers, regulators, economists and handpicked journalists. The conversation is dominated by central bankers and the über-elite of academic economists who engage in friendly sparring over academic papers.

To get an idea of the crowd check out the roster of folks who attended the last in-person event prior to COVID in 2019.

How a conference of the world’s leading monetary policy thinkers and policy-makers ended up meeting in a mountainous resort in Wyoming, is an entertaining story nicely recounted in a short history put out by the Kansas City Reserve Board.

The fact that this world famous conference emerged in the late 1970s from a regional meeting on global agriculture, reinforces the point that the Kansas City Reserve Board is an idiosyncratic but fascinating vantage point from which to view world economic history. This was a point ably made by Leonard’s biographical study of Tom Hoenig, an obscure local economist who rose to be President of the Kansas City Reserve Bank and a major sparring partner of Ben Bernanke after 2008. I discussed Leonard’s book in Chartbook #85 earlier in the year.

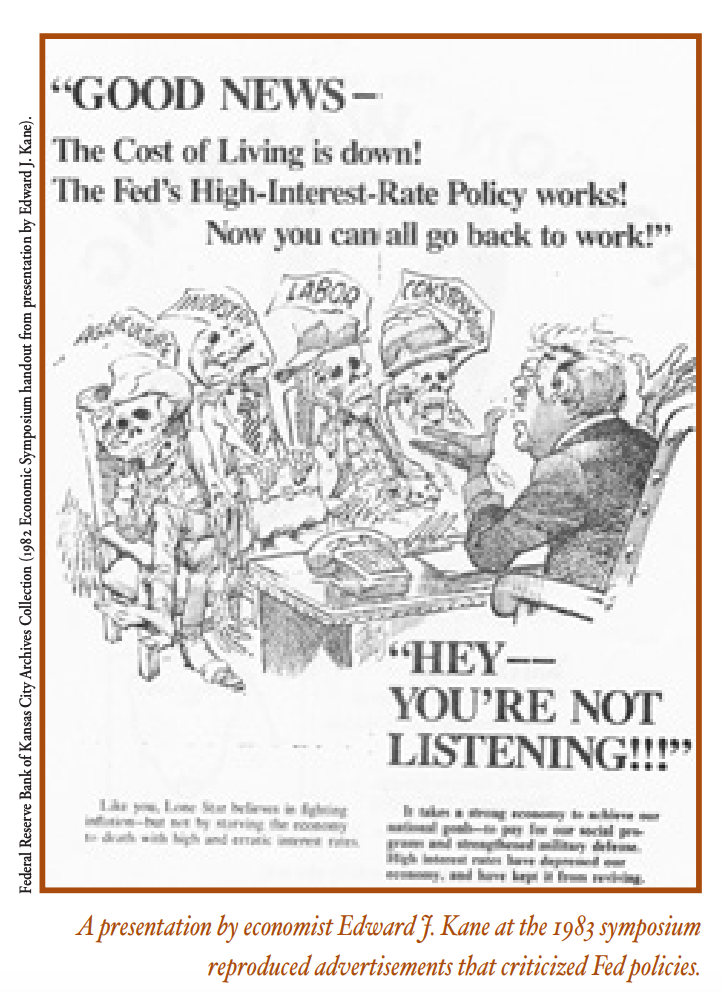

The first meeting attended by a Fed chair was in 1982, when Paul Volcker, lured to Jackson Hole by the fly-fishing, clashed with his Keynesian critics. Economist Edward Kane delivered a blistering critique of Fed policy backed up by amusing adverts being run at the time by America’s banks.

As the conference history goes on to note:

Although attendees would later note Kane’s presentation as being especially brutal and unfair towards both Volcker and the Fed, he was certainly not the only Fed critic in the room. James Tobin, a Nobel Prize-winning economist from Yale University, said during one of the symposium’s discussions that the Fed should have less autonomy. Monetary policy goals, he said, should be set in coordination with the government’s fiscal policy decisions. “After all, monetary policy decisions are the most momentous economic decisions the federal government makes,” Tobin said.4 “It seems anomalous to me that when the budget is planned and eventually voted, the process is completely detached from the gentle and amateurish surveillance the Congress exercises over monetary policy.” In case there was any question about Tobin’s views, the following Sunday, The Washington Post published a lengthy article by Tobin titled “Stop Volcker from Killing the Economy.”5

By the mid 1980s the Jackson Hole conference had firmly established itself on the circuit and journalists armed with the first generation of “laptop” computers were in eager attendance.

In doing research for the podcast perhaps the most remarkable piece I came across was an article by Brian Cheung on the community of Jackson Wyoming itself.

‘The weirdest place in the world’: What the Fed missed in Jackson Hole

Brian Cheung·Anchor/Reporter

August 28, 2019

As Cheung reported:

The Jackson Hole valley is home to the most unequal metropolitan area in the United States. As measured by the Economic Policy Institute in 2015, the top 1% of residents earned an average of $16.2 million, more than 132 times the average income of the bottom 99% of families.

It is a community divided between, on the one hand, the multi-million mansions of America’s elite, drawn to Wyoming by the scenery, the seclusion, and the great tax incentives, and, on the other, the service class of working people that struggles to find accommodation in the overpriced resort town. According to one resident, Jackson Wyoming is the “weirdest town” in America because you can always find work. You always earn well. But you always struggle to make ends meet.

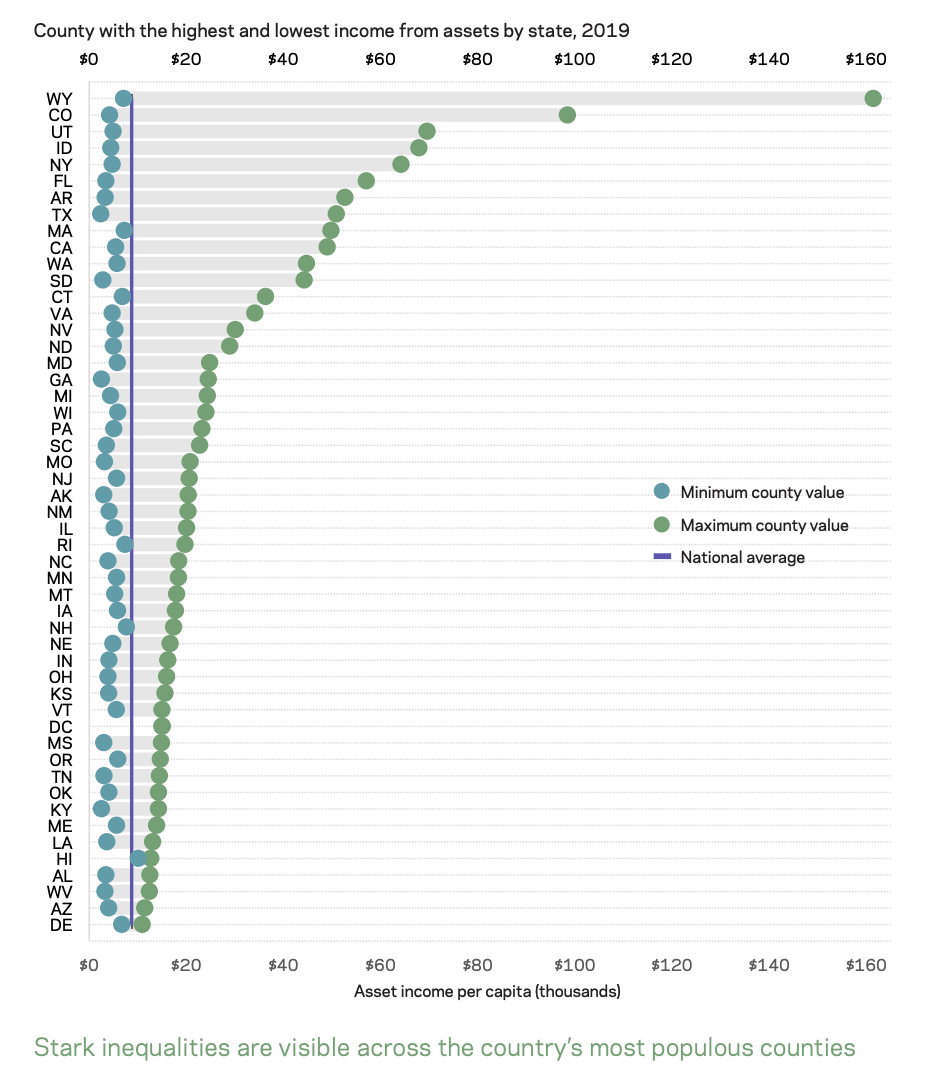

And these impressions were confirmed in 2021 by a study from the Economic Innovation Group which found that within Wyoming,

Teton County (Jackson Hole) is a preferred domicile of the super-rich and has the highest income from assets per capita in the country at $161,400, while Uinta County has just $7,100 per capita. As substantial as this gap is, Uinta is not far from the national average.

In 2022 all eyes were on Fed chair Jerome Powell as he struggled to define a new agenda for the Fed in the face of surging inflation. I did a piece for Foreign Policy in which I discuss Powell’s rather fascinating use of history in his speech to the Jackson Hole conference.

In my rather jaundiced take, Powell’s performance has about it an “18th Brumaire” feel – as in Karl Marx’s The Eighteenth Brumaire of Louis Bonaparte – in which we go through the motions of reenacting Volcker’s 1979 interest rate shock, whilst being actually aware that conditions are radically different.

In his speech Powell’s use of history seems to have been quite self-conscious. In a piece by Colby Smith and Eric Platt one portfolio manager remarks:

“The theory of a dovish pivot has been squashed,” said Brian Kennedy, a portfolio manager with Loomis Sayles. “Powell is a creature of history and to me this is further confirmation that the Fed does not believe inflation is rolling over and going back to 2 per cent.”

As the FT spotted, Powell’s speech was studded with knowing references to the past.

Fed watchers noted that “Keeping At It” — a phrase Powell used twice in his speech — is the title of Volcker’s 2018 memoir, which was published just over a year before he died.

Meanwhile, as if to make my point, Bloomberg regales its readers with an entire battery of sensationalizing historical analogies.

The reality of 2022 is rather less dramatic than photos of the 1930s suggest. The Fed may be risking a recession as it tightens policy, but what kind of recession is it?

Economists also expect the US unemployment rate to rise beyond the 4.1 per cent broadly anticipated by Federal Open Market Committee members and regional bank presidents in June. The unemployment rate, a bright spot as the economic picture darkens, hovers at a multi-decade low of 3.5 per cent.

As is often the case, the smartest critical take on Powell’s dilemmas came from Mohamed El-Erian. Strikingly, El-Erian too framed his analysis in terms of temporality, in his case in terms of the past, present and the future. El-Erian was pleased with Powell’s message that rates will continue to rise and will do so for some time to come. But he regretted Powell’s failure to come to terms with the past and to more clearly map the future.

In El-Erian’s view, Powell has a fivefold problem.

(1) Powell’s 2021 speech premised on low inflation gave hostages to fortune and, with hindsight, was in El-Erian’s view a refletion of a fourfold failure of “bad forecasts, poor communication and belated policy responses”.

(2) In 2021, the Fed missed the chance for a soft-landing (by acting earlier) and now needs to show a determination to act since otherwise it will become a “mistake that builds on itself, aggravating problems of low growth, high inflation, worsening inequality and future financial instability”.

(3) The Fed’s forecasts and guidance have lost credibility. “Its quarterly (inflation) forecasts have been repeatedly dismissed as fantasy and its communication is seen as lacking the consistency needed for effective policy guidance.” This matters, according to El-Erian because it means the Fed will have a harder time persuading markets to believe its tougher stance.

(4) The Fed needs to address the fact that the “new policy framework” it first began developing in 2020 to deal with a world of low inflation, looks out of step with reality.

(5) Powell needs to “take responsibility for the last 18 months of Fed errors, including the mis-characterisation of economic and policy issues in last year’s speech”.

In El-Erian’s judgement, Powell’s unusually short 2022 speech: “dealt well with the present, but left out important past and future issues. I suspect that we will look back on this year’s Jackson Hole speech as a missed opportunity for the Fed to regain control over its policy narrative, as well as to outline what is needed to overcome the considerable policy challenge facing the world’s most powerful and systemically important central bank.”

This is perhaps the most substantive and extensive articulation of the critical position. It will be interesting to see how the Fed moves forward from this moment.

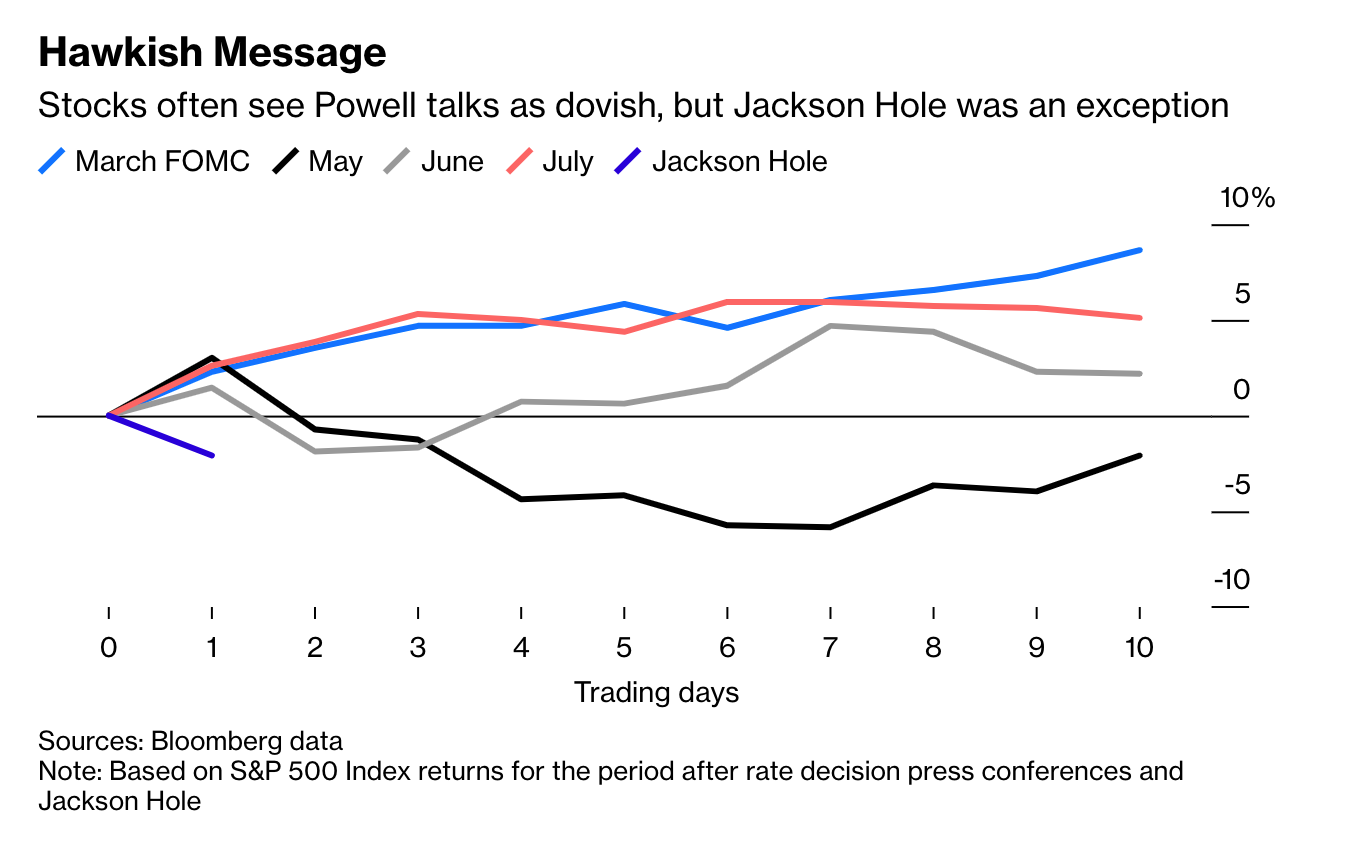

Not everyone agrees with El-Erian’s scathing critique. As Karl W. Smith notes at Bloomberg, the Fed has in fact pivoted to a far tougher line since March. Part of the problem is that after an initial selloff, markets have been slow to get the message. Over the summer the rebound helped to ease credit conditions at least somewhat.

On this occasion the markets seem to have taken the point.. Rather than rallying as they have done after Powell’s more upbeat press conferences, the reaction to his toughly worded speech at Jackson Hole was a significant sell off.

Meanwhile, Raghuram Rajan, formerly the governor of India’s central bank, is kinder to Powell.

Clearly the Fed’s shift in August 2021 to a more accommodating framework of average inflation targeting was ill-timed.

This was the right framework for an era of structurally low demand and weak inflation, but exactly the wrong one to espouse just as inflation was about to take off and every price increase fuelled another. But who knew the times were a-changing? Even with perfect foresight — and in reality they are no better informed than capable market players — central bankers may still have been behind the curve. This is understandable. A central bank cools inflation by slowing economic growth. No matter how independent it is, its policies have to be seen as reasonable, or else it loses its independence. With governments having spent trillions to support their economies, employment just recovered from terrible lows and inflation barely noticeable for over a decade, only a foolhardy central banker would have raised rates to disrupt growth if the public did not yet see inflation as a danger. Put differently, pre-emptive rate rises that slowed growth would have lacked public legitimacy — especially if they were successful and inflation did not rise subsequently. Central banks needed the public to see higher inflation to be able to take strong measures against it.

The real question is what happens next.

This is not a time for postmortems to assess central bank functioning.

Instead central banks in Rajan’s view should concentrate on inflation fighting and they should do so without fear of deflation.

Of course, when central banks succeed in bringing inflation down, we will probably return to a low-growth world. It is hard to see what would offset the headwinds of ageing populations, a slowing China and a suspicious, militarising, deglobalising world. … What if inflation is too low? Perhaps like the virus, we should learn to live with it.

Rajan’s worry is that if they go beyond this limited but cruciual mandate, they risk a larger cycle of exaggerated expectations, disillusionment and delegitimization.

As central bankers meet in Jackson Hole, they must wonder how far they have fallen in the public’s eyes. A short while ago, they were heroes, supporting feeble growth with unconventional monetary policies, promoting the hiring of minorities by allowing the labour market to run a little hot, and even trying to hold back climate change, all the while berating paralysed legislatures to do more. Now they stand accused of flubbing their most important task, keeping inflation low and stable. Politicians, sniffing blood and mistrustful of the power of unelected officials, want to re-examine central bank mandates.

It is a dramatic scenario, of which Rajan has some experience in the Indian context. And no one should underestimate the threats to the institutional fabric in America today. But here too one must surely ask, when the talk turns to “sniffing blood”, are we talking about reality, or are we enacting a pantomime political economy?

****

I love putting out the newseletter for free to thousands of readers around the world. But what sustains the effort are voluntary subscriptions from paying supporters. If you are enjoying the newsletter and would like to join the group of supporters, press this button and pick one of the three options.

Several times per week, paying subscribers to the Newsletter receive the full Top Links email with great links, reading and images.

There are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.August 26, 2022

Ones & Tooze: Why the World’s Top Economists are Going to Jackson Hole

Hosts Adam Tooze and Cameron Abadi look at the Jackson Hole Economic Symposium taking place this week and talk about its history and its significance in influencing world economics. And in the second segment the two discuss the massive teacher shortage occuring in the United States this year and how teacher salaries have failed to keep pace with the salaries of similarly educated professionals.

Find more episodes and subscribe at Foreign Policy.

August 24, 2022

Chartbook #146 The Russia-Ukraine War At Six Months: symbolic anniversary or economic and military turning point?

It is six months since Russia launched its attack on Ukraine.

Amongst the anniversary coverage two long reads by the Washington Post are in a league of their own. One, by Shane Harris, Karen deYoung, Isabelle Khurshudvan, Ashley Parker and Liz Slycovers, covers the build-up to war. The other by Paul Sonne, Isabelle Khurshudvan, Sehiy Morgunov and Kostiantyn Khudov reconstructs the battle for Kyiv. Both are highly recommended.

On the six-month anniversary, the celebrations of Ukraine’s national day serves as a counterpoint to the increasingly sober reporting of the war and uncertainty about the longer-term outlook.

For much of the summer the talk was of an imminent Ukrainian counterattack, which was expected to be launched in the South around Kherson. The hope was that this might break the stalemate and perhaps create conditions under which a ceasefire could be negotiated on terms favorable to Kyiv. By early August it was clear that a large-scale counteroffensive by the Ukrainian military was, in fact, unlikely. Acute observers like Shashank Joshi, Defense Editor of The Economist noted a significant slippage in messaging by both Kyiv and its backers in the West.

Indeed, there was anxiety in some circles that the drumbeat of expectation was putting unreasonable pressure on Kyiv to launch an attack prematurely. This thread by C.M. Dougherty is excellent on this score.

3/22 This pressure may be pushing UKR may to launch an offensive, despite lacking the military means to do so effectively, as laid out brilliantly by @KofmanMichael & @EvansRyan202 in this @WarOnTheRocks podcast: https://t.co/GnMvdl7hNx

— Christopher M. Dougherty (@C_M_Dougherty) August 9, 2022

On the ground there are few illusions about the balance of forces. As the FT quoted Andriy Zagorodnyuk, a former defence minister of Ukraine.

“The US gives us enough to stop the Russians from advancing, to reverse some gains, to shape the operational direction, but absolutely, clearly, not enough for a major counteroffensive,”

This is a far cry from gung-ho talk earlier in the year about driving Russia back to the border. On Washington the turning point may have come in early July, as captured by a piece by Peter Baker and David Sanger in the NYT which flagged up growing unease in the Biden administration about the strategic rationale for US aid for Ukraine (h/t Ted Fertik). Baker and Sanger offered a startling insight into the complex, not to say confused, messaging from Washington:

Some officials, including Mr. Biden, cringed when Defense Secretary Lloyd J. Austin III said in April that “we want to see Russia weakened to the degree that it can’t do the kinds of things that it has done in invading Ukraine.” The president called Mr. Austin to remonstrate him for the comment, then directed his staff to leak the fact that he had done so. But officials acknowledged that was indeed the long-term strategy, even if Mr. Biden did not want to publicly provoke Mr. Putin into escalation.

On the basis of such muddled communication what, frankly, are either Kyiv or Moscow to think? Does Washington want to wear down Russian power or does it not?

What is more clear cut are the force ratios on the ground. Fro an offensive against prepared defensive positions, the attackers needs to have an advantages of 3:1 to have much prospect of success. If accumulating such an advantage was ever plausible for Ukraine in the Kherson sector, by mid-August that opportunity had slipped away. As Shashank Joshi, reported

Konrad Muzyka of Rochan Consulting, a firm which tracks the war, thinks there were 13 Russian battalion tactical groups (btgs) in the province in late July (a btg usually has several hundred troops). Now there may be 25 to 30. “We believe that this window of opportunity has passed,” says Mr Muzyka. “Ukrainians do not possess enough manpower to match Russian numbers.”

As Joshi found to his cost, this was not a popular view. The comments on this twitter feed make for enlightening reading.

My piece on the “counter-offensive”: Ukraine is squeezing Kherson city, but its army may not be ready for a big offensive. Ukraine’s political imperatives—the need to demonstrate progress to Western backers—might be in tension with military considerations. https://t.co/JEYm8rUSVE

— Shashank Joshi (@shashj) August 14, 2022

But as other sources, such as The Guardian, reported, Joshi’s downbeat view is, in fact, widely held.

Ukrainian commanders … concede that a big push in Kherson is some way off. “We have more weapons. Not enough to do an offensive now and to beat the enemy. It is enough to defend our territory,” said Roman Kostenko, a pro-European deputy who heads the parliamentary defence and security committee.

Often the debate about Western support to Ukraine is concretized in the form of weapons systems. First there were the Javelins. Then there were the Himars rocket launchers. Now the talk is of ATACMS.

Ukraine’s Himars rockets have a range of about 50 miles (80km). … So far the Biden administration is refusing to supply Kyiv with Army Tactical Missile System (ATACMS) rockets, which can be used in Himars systems and have a 185-mile range. Its reasoning is that Ukraine could use them to strike Russia itself, an act the US fears may lead to a third world war. Zelenskiy dismisses this scenario and has pledged not to attack Russian territory. Negotiations continue, as the Pentagon reviews the situation.

The focus on equipment makes for good headlines, but it deflects from the broader operational and strategic picture and the longer-term question of how the war can be continued and for what purpose.

Dara Massicot in Foreign Affairs defines the objective in more limited terms. The aim is not so much a decisive breakthrough, as to foil Russian efforts to annex Ukrainian territory and to drain their military power, eventually forcing Putin to give up. To achieve this more limited goal, what may suffice is simply attrition.

If Ukraine can create a highly contested frontline—just as it did outside Kyiv and Kharkiv—with attacks on command-and-control points, high rates of equipment losses, and large Russian casualties, it may again convince Moscow to withdraw. But for such a Ukrainian strategy to have the best chance of success, it must be in progress before Russia attempts to annex the territory it holds; that way, Ukrainian attacks can deny Russia a foothold in an area like Kherson. And even if Russia does annex Ukrainian territory and tries to force an operational pause, Kyiv and its Western supporters don’t have to comply.

On the question of a “highly contested frontline” and the attrition of Russian strength, one of the fixed points in Western analysis of the war, is the evidence that the Russians are suffering much higher casualties than the Ukrainian side. But how accurate are our casualty figures and how are they estimated?

On this grim subject The Economist provides excellent analysis. It turns out that estimates of Russian casualties depend on a macabre parameter known as the “wounded-to-killed ratio”. This is a ratio that reflects the intensity of fighting, the sort of weapons used (shrapnel v. machine-guns) and the availability of rapid battlefield medical care. In the 20th-century a ratio of 3 or 4:1 was normal. But in recent conflicts thanks to rapid medevac the United States has been able to push the ratio as high as 10:1 – of eleven of its soldiers who are hit by enemy fire, one dies and 10 survive their wounds. Ironically, in the case of the Russo-Ukraine conflict, since we know the number of killed Russians with relative accuracy, a higher “wounded-to-killed ratio” would be bad news for Moscow, since it would imply a greater number of overall casualties. The consensus seems to be that the ratio probably hovers at an unremarkable 3.5:1, which implies an estimate of Russian casualties in the order of 70,000 killed and wounded.

If the West is increasingly counting on attrition, that shifting outlook has not been lost on the Russians. An interesting view from the other side is provided by a piece in Kommersant by Russian think tank director Andrey Kortunov. As he remarks:

… Western historians today recall the “miracle on the Vistula” a century ago, when in the summer of 1920 the Polish state managed to stop the Red Army’s advance on Warsaw and push it far to the east. A hundred years later, in the United States and Europe, they started talking about the coming “miracle on the Dnieper”. It seems that one more effort, one more strain, one more week or a month – and the Russian military machine will start to falter, rolling back to Donetsk and Lugansk, and even to Rostov and Belgorod. But week after week, month after month passes, and the dates of the expected “miracle on the Dnieper” are shifting further into the future, like an elusive horizon line. The growing supply of Western weapons strengthens the Ukrainian army, but still is not able to change the overall picture of what is happening. Russian forces, albeit cautiously and without spectacular breakthroughs, continue their stubborn advance in a westerly direction. The situation on the battlefield, albeit slowly, is changing in favor of Moscow, which, in turn, is tightening Russian conditions for future political agreements. Is the West able to reverse this trend? Such an all-in game would involve a sharp increase in the scale of military support for Kyiv. But in this case, it is likely that NATO would be directly involved in the Ukrainian conflict, after which the twenty-year Afghan saga would most likely seem like a cakewalk. It is clear that any decision on a truce, and even more so on a peaceful settlement, should be made in Kyiv. However, a lot depends on the position of the West. If “Plan A”, that is, the victory of Ukraine, looks less and less realistic, then the West should, apparently, already now think about a “Plan B”, which involves achieving at least a temporary compromise not only between Moscow and Kyiv, but also between Russia and the West.

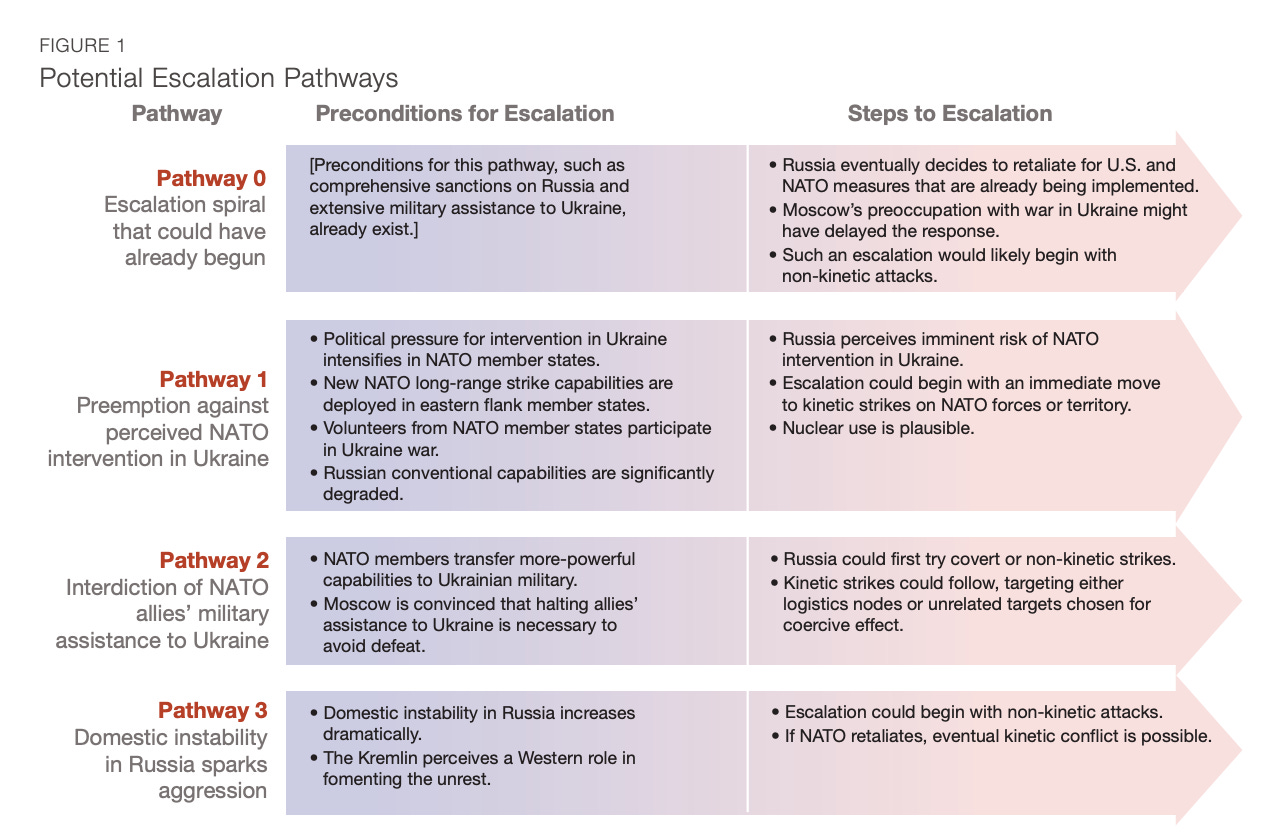

What hangs over the entire discussion, on both sides, is the risk of escalation. In February and March, as the war began, as the West surged its support for Ukraine and ramped up its sanctions against Russia, as Putin responded with nuclear saber-rattling, talk of escalation was everywhere. Since then, fears have calmed somewhat. For a cool-headed assessment of the risk of escalation as of July 2022, a report by a RAND team is worth reading. The punchline is this:

although escalation risks stemming from the Ukraine war are real and significant, the preceding analysis helps to bound those concerns: A Russia-NATO war is far from an inevitable outcome of the current conflict. U.S. and allied policymakers should be concerned with specific pathways and potential triggers, but they need not operate under the assumption that every action will entail acute escalation risks.

The great hope of Western governments was that Western economic sanctions would have a material effect on Russia’s ability and willingness to sustain the war against Ukraine. Battlefield attrition and economic attrition would combine to force Moscow to sue for peace. This, of course, depends on actually making a serious dent on the Russian economy. Six months into the conflict, how far that has been achieved is hotly contested.

As Nick Mulder pointed out in his very timely history of The Economic Weapon, already during the Allied blockade of the central powers in World War I, sanctions were the incubators of economic expertise. And that has been true with regard to Russia in 2022 as well. A lot of people have learned a lot, very fast about Russia’s economy. But, as was true in previous episodes of economic warfare, this collective learning process has not let to consensus.

Over the last month starkly contrasting analyses have been offered on the state of the Russian economy and its likely future development.

At Yale a group pulled together by Jeffrey Sonnenfeld of the Yale SOM have published a sprawling analysis of an impending economic catastrophe in Russia. Their conclusion is that Russia faces not just a long-term deterioration of its position as a commodity exporter, but the prospect of immediate disaster. Their conclusion is that:

Looking ahead, there is no path out of economic oblivion for Russia as long as the allied countries remain unified in maintaining and increasing sanctions pressure against Russia.

The Sonnenfeld report, has elicited numerous replies. Ben Aris has provided one detailed response. Another has come from Elina Ribakova, at the IIF – the think tank and lobby of the international financial industry – who has published in-depth analysis, which is far more skeptical of the weakening of the Russian economy and the extent of the pullback by Western firms.

1/ Sanctions on Russia are proving to be porous not only in energy. While self-sanctioning has been an important contributor to sanctions impact, many companies are still sitting it out. @SelfSanctions @JeffSonnenfeld pic.twitter.com/X3SeroBXgw

— Elina Ribakova(@elinaribakova) August 18, 2022

At the macroeconomic level, opinions are similarly divided. Forensic analysis of trade data by Matt Klein at the Overshoot newsletter suggests that Russia is suffering a ruinous squeeze on its imports. But a broader assessment of the Russian situation, again by Elina Ribakova, or by The Economist magazine suggests that the Russian economy is, in fact, in stronger shape than many imagine. Amongst other indictors, imports to Russia, as captured in the export data of its major trading partners, may be down on their prewar peak, but are currently recovering to their pre-COVID level.

Of course, no one disputes that the war and sanctions will be terrible for Russian growth in the long term. The loss of investment and human capital and reputation is irreparable. But, any prospect of an imminent squeeze serious enough to force a change in policy in Moscow seems remote.

The same cannot be said for Ukraine. By contrast with the serious disagreement about Russia’s economic position, there is little doubt that Ukraine is living on borrowed time. To put it simply, Ukraine cannot afford the war it is fighting. The aid it is receiving, though substantial, is an order of magnitude smaller than Russia’s fossil fuel earnings and is entirely inadequate to cover the running costs of the war. As a result, Kyiv is resorting to financing the war by printing money. It can only be a matter of months before Kyiv faces crippling choices between continuing to fight the war and upholding any semblance of normal economic life on the home front.

As Maria Repko deputy executive director of the Centre for Economic Strategy in Ukraine described the situation in the pages of Foreign Policy magazine.

Scarce foreign funding is forcing the National Bank of Ukraine to buy government bonds (effectively printing hryvnia) to cover the enormous budget deficit, which reached $4 billion in May and almost $6 billion in June. In March to May 2022, the government’s own revenues covered just about 40 percent of the expenditures needed to run the country and pay the bills. Another 40 percent was covered by the National Bank of Ukraine. The rest is funded by grants (about 7 percent of expenditures during three months of the full-scale war), foreign loans, and local bond issues. … on July 20 Ukraine asked Eurobond holders for a standstill, because the commercial debt servicing becomes too much of a burden for the budget, as well as from the balance of payments prospective.

That standstill was granted by the bondholders. It buys Kyiv $5.9 billion in relief over the next two years. But that only covers a small part of the financial shortfall. In the mean time,

The National Bank of Ukraine (NBU) was selling up to $1 billion per week to keep up with the pace of foreign currency demand and to defend the exchange rate peg. On July 20, the decision was made to shift the peg upwards, to 36.60 hryvnias to a dollar from 29.25 hryvnias to a dollar. Ukraine’s foreign currency reserves stood at $23 billion as of the end of June. The current pace of losses means that Ukraine will be shortly on the verge of financial collapse if aid inflows are not sped up.

Ukraine’s situation is made worse by the disruption of its economy due to the war, the dislocation of its foreign trade by the Black Sea blockade and by the economic activity of its citizens who are now refugees spread out across Europe. Of the 5 million Ukrainian refugees many are working remotely. All of them are spending money from their Ukrainian bank accounts. The result is a monthly drain of c. $1.5 billion at the expense of Ukraine’s foreign exchange reserves.

The basic point, as Oleg Churiy former deputy governor of the National Bank of Ukraine spelled out in the pages of the FT, is that Ukraine must come to terms with the long war it now faces not just in military terms, but in economic policy as well.

A longer duration of the conflict alters not only the military strategy but the macroeconomic calculus. In the war’s early days, Ukraine’s macroeconomic policies aimed to control expectations and avoid panics. These policies were based on controlling prices — for example, the hryvnia-dollar exchange rate was fixed at the prewar level — and providing stop-gap measures to support businesses and households, such as suspending import duties. These responses were appropriate to address the initial shock. But as the war grinds on, they need to be adjusted or Ukraine will run into an economic catastrophe.

As Churiy sees it there is no alternative to putting Ukraine’s domestic finances on a sounder footing. That means raising taxes and slashing all “non-essential” spending. But that is hard to do in wartime and is already producing conflict between the central bank, for which Churiy speaks, and the politicians who run the government. As the WSJ pointed out in its portrait of Ukraine’s finance minister Sergii Marchenko there is a simmering dispute between the bankers and the government over stabilization. Marchenko, of course, recognizes that this has become a war of attrition, but his priorities are clear.

“Sometimes we have a different point of view from the National Bank,” said Mr. Marchenko. “We have to worry about winning the war. It is better to risk high inflation than not to pay soldiers’ salaries.”

In a country at war, the implication that the central bank has other priorities than national defense, is dramatic indeed. An independent central bank is ill suited to the needs of total war…

The only way to relieve this conflict is to look for more support from outside. So far, Ukraine has received external support to the amount of c. $2.5bn-$3bn a month. For the second half of 2022 it is expecting $18bn all told. But it needs more. It needs $4bn-$5bn per month immediately.

A lot has been pledge. But frustratingly little has so far been disbursed. Most flagrant of all is the EU, which has pledged €9 billion but delivered only €1 billion on account of internal disputes about the modality of funding. As the WSJ reports:

Germany, which sent Ukraine a separate bilateral grant of €1 billion in June, objected to the commission’s plan to offer low-interest loans backed by guarantees from EU member states (Germany favors grants). Discussion about whether to offer grants or loans, and how to share the burden, has dragged on all summer.

With a new proposal being tabled in early August. As Politco reports: “While there’s no timeline yet, the Commission is aiming to obtain approval by the European Parliament and EU countries in September so that disbursement can start in October, one official said. “

Zelensky’s reponse was merciless: “Every day and in various ways, I remind some leaders of the European Union that Ukrainian pensioners, our displaced persons, our teachers and other people who depend on budget payments cannot be held hostage to their indecision or bureaucracy. Such an artificial delay of macro-financial assistance to our state is either a crime or a mistake, and it is difficult to say which is worse in such conditions of a full-scale war”.

As Zelensky knows, the stakes could not be higher. If, at the six-month mark, Ukraine now faces a long war, then stability is crucial. And that stability must be secured, not just on the frontlines, but on the home front as well, which is “highly contested too”. Otherwise, when Kyiv comes to mark the 12-month anniversary and the 18th-month anniversaries in 2023, the narrative may be less up beat than it is today.

August 23, 2022

Chartbook #145: China on the tightrope

The headwinds acting on the Chinese economy right now are formidable, on top of collapsing housing markets and the risks of Xi’s Zero-Covid policy, add one more anthropocenic shock, extreme heat. As far as economic policy is concerned, Beijing is walking a tightrope in a storm.

The heatwave affecting large parts of China is, by most metrics, the worst ever recorded.

China is experiencing the worst heatwave ever recorded in global history.

— Colin McCarthy (@US_Stormwatch) August 23, 2022

The combined intensity, duration, scale, and impact of this heatwave is unlike anything humans have ever recorded.

Over 260 locations have seen their hottest days ever during this 70+ day heatwave. pic.twitter.com/TCKvR37Em3

In Wuhan the Yangtze river is running so dry that local residents are taking walks on the river bed itself.

Wuhan river bank, Yangtze River water receded to the centre

— 自由情意#6376 (@sdcltrc) August 21, 2022

Following Chongqing's Jialing River, Wuhan's famous river banks are also drying up, with the Yangtze River water receding to its centre. Wuhan people say: never seen such a sighthttps://t.co/ObXD2L5gnh

It is not just an environmental disaster. It has an immediate impact on the economy.

As Caixin Global reports the six areas suffering the extreme heat and drought — Sichuan, Chongqing, Hubei, Henan, Jiangxi and Anhui — accounted for almost half of China’s rice output in 2021. Global Times reports that the Chinese Minister of Agriculture and Rural Affairs Tang Renjian has called for “all-out battle” against high temperatures and drought to secure autumn harvest.

Sichuan is heavily dependent on hydro power and the low water levels have forced power cuts. That directly affects the production of lithium, polysilicon, aluminium and copper. But, more importantly, it places the entire regional power grid under pressure. Major cities, including Shanghai, are making efforts to economize on power usage. The legendary Bund skyline was not illuminated for two days this week. As the FT reports: “Toyota and Apple supplier Foxconn are among the companies that have suspended plant operations in south-west China as the region is buffeted by hydropower shortages caused by droughts and heatwaves.”

As always, on all things China energy policy Lauri Myllyvirta is a key Western voice to follow. This fantastic thread delves deep into the latest China energy crisis.

This is taking into account that reportedly half of the hydropower capacity has been knocked out by the drought.https://t.co/iSQPIX9cgB

— Lauri Myllyvirta (@laurimyllyvirta) August 23, 2022

The power situation would be even more strained if China’s economy were running at full throttle.

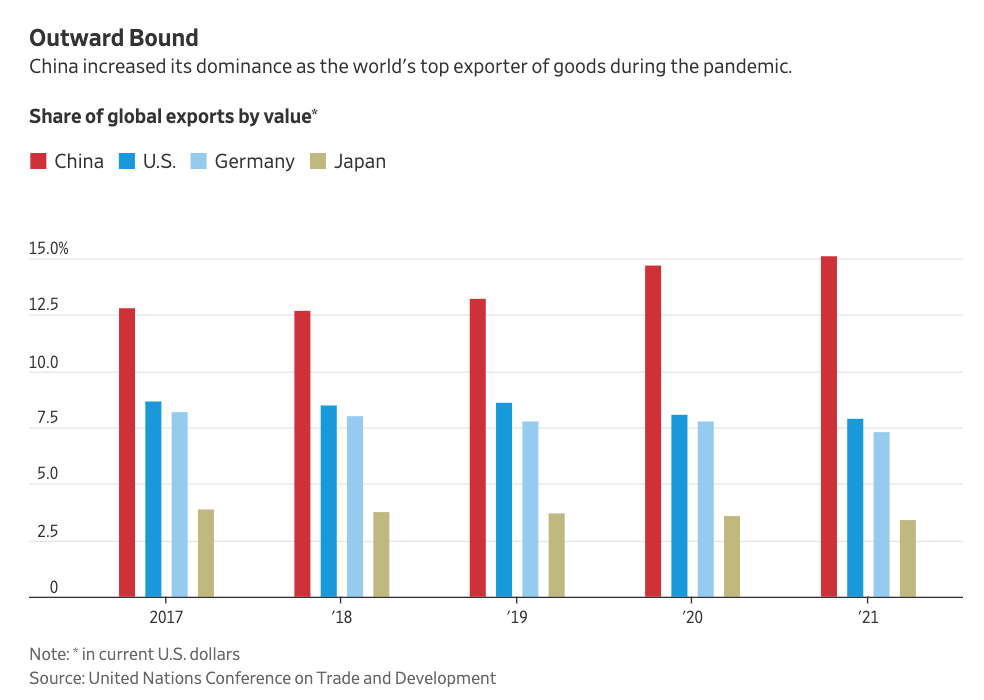

Some bits of the Chinese economy are running hot. In particular, as the WSJ reports China’s exports are booming.

China’s share of global goods exports by value increased over the course of the pandemic, to 15% by the end of 2021 from 13% in 2019, according to data from the United Nations Conference on Trade and Development, which tracks global trade. Major competitors’ share of global exports shrank over the same period, suggesting China’s gains came at the expense of others. Germany’s share of global exports fell to 7.3% in 2021 from 7.8% in 2019; Japan’s share declined to 3.4% from 3.7%; and the U.S.’s share slipped to 7.9% from 8.6%.

But China’s export boom is driven in part by the hunt for markets, which are missing at home. As Paul Krugman argues in a NYT piece, echoing points long made by Michael Pettis and Matt Klein, China’s trade surplus is as much the result of domestic doldrums as overseas success.

The heart of the China’s domestic slowdown is the real estate sector, which since September-October 2021 has been experiencing a slow-motion crisis.

As Matt Klein notes in the FT:

The downturn in the housing market began last summer in response to government restrictions on mortgage borrowing and developer leverage. Homebuilders sold an average of 156mn sq m a month of residential floor space from April to June 2021. This year in the same period, Chinese developers have sold just 106mn sq m a month. The plunge in demand has flowed through to new building, with the amount of “residential floor space started” in April-June 2022 down by nearly half compared to last year. The pace of homebuilding has not been this slow since 2009.

As Michale Pettis outlines in a brilliant blogpost for the Carnegie Endowment, a downturn in property prices risks unraveling the entire housing finance system. In the nightmares of the Chinese leadership the mortgage strikes that swept Henan province in July would be a harbinger of things to come.

The ramifications of the sudden stop in the housing market are being felt across China’s economy. Consumer confidence has fallen off a cliff.

The unemployment rate amongst young Chinese, aged 16-24 hit an alarming 19.9 per cent in July.

Source: SCMP

Hoping to revive the housing market, the Peoples Bank of China has responded by cutting interest rates. And, in recent days, a variety of non-conventional have begun to take shape. The National Association of Financial Market Institutional Investors (NAFMII), the interbank bond market self-regulatory body under the central bank, is discussing potential credit guarantees with a handpicked group of six developers. Bloomberg reports that to address the delays in project completions that triggered the wave of mortgage strikes, the Housing Ministry is offering 200 billion yuan ($29.3 billion) in special loans to ensure stalled housing projects are delivered as quickly as possible.

But as Bill Bishop at Sinocism remarks:

The fact that the policymakers appear to have been surprised by the mortgage strikes and unfinished building mess may be another sign that they have a weak grasp of the hidden risks in the economy, and especially around real estate. The latest moves – rate cuts and loan support for some developers – do not seem like nearly enough to change sentiment, but I am not sure anything will do that until we get past dynamic zero-Covid.

Short of a U-turn on zero-COVID, which is not likely before the Party Congress in October, the one thing that might conceivably reverse the downswing would be really large-scale stimulus. This would have to focus on reviving both the housing market and boosting infrastructure. As Gavekal points out, infrastructure spending by itself, however lavish, has never been enough to turn the Chinese business-cycle.

Recent statements by outgoing Premier Li Keqiang make clear that some in China’s leadership grasp the seriousness of the situation. It looks worse today than it did in 2020. So far, however, though Beijing has rolled our dozens of policy measures, their scale has been modest.

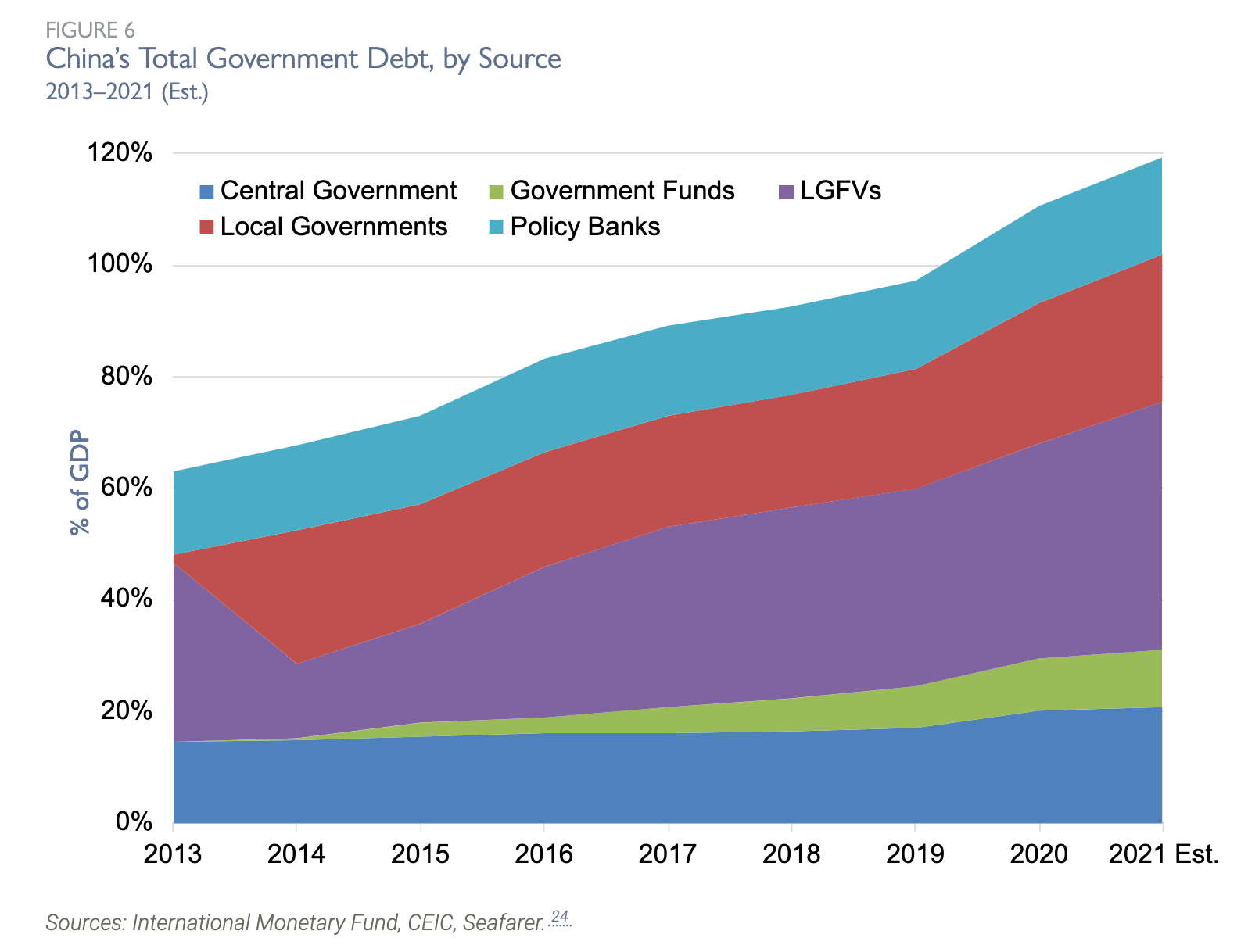

Seafarer Funds, in an insightful analysis, attributes the relatively small scale of the action so far, to the hidden balance sheet constraints on China’s public sector. China’s national debt level may appear modest on paper, but the hidden liabilities of China’s public sector are substantial. Though they continue to receive inflows of funding, local government and local government financing vehicles are financially stretched.

As Seafarer continues:

Recognition that the current system is approaching its breaking point appears to be growing in Beijing, where reforms to the fiscal transfer system that would better balance revenues and expenditures for local governments are under discussion.30 If these reforms involve a net shift in financial resources to local governments, the central government will run a high budget deficit going forward unless it increases taxes. The longer-term solution to China’s current dilemma is getting economic growth back on track. First and foremost, China needs to find the right balance between controlling the pandemic and preserving the economy. Second, it needs to reprioritize economic reform. China’s best path forward is to raise the economic growth rate and grow its way out of debt. Doing so will require a recommitment to economic growth – a goal recently usurped by concerns over national security and control.

Whichever way you look at it, Beijing is walking a tightrope. And the scale of the risks is unprecedented not just for China but also for the wider world. Matt Klein may be right in his recent FT piece to argue that from the point of view of inflation-fighting, the deflationary effect of China’s slowdown is welcome at this current moment. But to take the next step to argue that “China’s troubles may be just what the rest of the world needs”, is surely to push a good point too far. It may be true that “China’s healthy exports and weak imports” were previously a “drag on the global economy, depriving workers elsewhere of the incomes they would have earned selling goods and services to Chinese customers.” But that is a counterfactual argument. A better world is, indeed, imaginable in which China’s current account since the late 1990s was more balanced. Fair enough. Meanwhile, in the actually existing world economy, there are plenty of workers and businesses around the globe who depend heavily on exports to China. None of them will be celebrating bad news from China as good news, especially in light of the pressure also being exercised by a strong dollar and Fed tightening.

****

I love putting out Chartbook and I am particularly pleased that it goes out free to thousands of readers all over the world. But it takes a lot of work and what sustains the effort is the support of paying subscribers. If you appreciate the newsletter and can afford a subscription, please hit the button and pick one of the three options.

There are three subscription models:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.August 21, 2022

Chartbook #144: The Energy Shock and the Southern Cone – Is Argentina the weakest link?

As the combination of the energy price shock and the strong dollar ripple around the world they are putting consumers and governments everywhere under pressure.

In Sri Lanka, acute petrol and diesel shortages helped to bring down the government. But it is not just oil that is tight. In 2022 gas is in even shorter supply relative to demand. And for gas, because of the difficulty of transport, market are much thinner. LNG is the only truly fungible global gas supply and it requires complex and expensive facilities. With Europe and rich East Asian consumers competing for cargos, the price of LNG is spiraling. Poor energy importers like Pakistan are struggling to secure the supplies they need.

As Helen Thompson remarked in the FT:

Across the world, politicians are ever more desperately looking to contain the explosive consequences of the energy crisis. In those parts of Asia, the Middle East and Africa already mired in multiple economic and political difficulties, the crisis is proving catastrophic. Those who import liquid natural gas must now compete with European latecomers to the LNG market seeking an alternative to pipelined Russian gas. … In poor countries, a large proportion of the state’s resources go on subsidising energy consumption. At prevailing prices, some cannot: earlier this month, the Sri Lankan Electricity Board imposed a 264 per cent increase on the country’s poorest energy users. In Europe, governments want to alleviate the dire pressures on households as well as energy-intensive and small businesses, while letting spiralling prices, pleas to consume less and fear about the coming winter drive down demand. Fiscally, this means state funding to reduce rising energy bills by subsidising distributors, as in France, or transferring money to citizens to pay those bills, as in the UK. What is not available anywhere is a quick means for increasing the physical supply of energy.

State funding or transfers presume that there is “fiscal space” to offer this kind of support. In countries already under financial pressure in the aftermath of COVID and now facing rising interest rates, fiscal accommodation is painful.

In her global overview, Thompson mentions Asia, the Middle East and Africa, but Latin America too is feeling the shock. As The Economist remarks

It is not hard to see why governments (in Latin America) are so sensitive to the price of fuel. Latin America is a region of long distances in which roads are paramount in the movement of both goods and people.

As in North America, in South America too, fossil fuel culture runs deep. Indeed, there are parallels in the politics of fossil energy that connect settler-colonial societies around the globe from the Amazon basin to North America, Eurasia and Australia.

Country after country in the region has come under pressure.

In June 2022 after weeks of protests in which three people were killed, Ecuador’s notionally pro-market government was forced to offer subsidies for fuel and fertilizer worth c. 0.8 percent of GDP. In July, fuel price protests brought ordinary life in Panama to a halt and extracted a government promise to cut petrol prices by more than a third.

Since the start of 20222, the governments of Peru, the Dominican Republic, Chile and Colombia have all taken steps to moderate fuel price increases, often under pressure of protests and at considerable cost.

In Brazil – the giant that dominates the continent – Jair Bolsonaro, owed his election in 2018 to the support he gained by breaking ranks with the establishment and backing a disruptive truckers’ strike against the phasing out of fuel subsidies.

And then there is Argentina.

Any mention of Argentina in the context of a global economic crisis is likely to be met with an eye-roll. After Brazil, Argentina with 44 million inhabitants is still South America’s second largest economy. But over the last half century it has racked up an unequalled track record of boom-to-bust and financial crises.

Right now Argentina is again perched on the brink. Inflation is heading towards 90 percent. Protestors throng the streets of Buenos Aires. The government is divided and will struggle to meet the terms of yet another IMF program.

Argentina’s track record is so extreme that it is tempting, in explaining its current difficulties, to point to idiosyncratic national factors. As Simon Kuznets, the legendary growth economist, is said to have remarked, there are “four sorts of countries: developed, underdeveloped, Japan (exceptional for its sustained and rapid growth,AT), and Argentina.”

But, even the most extreme “national case” can never be understood in isolation. Argentina’s history of economic crisis, as particular as it may be, is inextricably intertwined with the history of its region and the world conjuncture. It is the combination of the two – domestic and global forces – that drives its history. It is in this regard an archetypal case of uneven and combined development.

***

One place to start the recent economic history of Argentina would be in the 1970s when Argentina was swept by the tidal waves of the petrodollar lending-boom, before crashing into Paul Volcker’s 1979 interest rate shock.

After stabilizing in the early 1990s by means of a fully convertible currency pegged at one-to-one against the dollar, Argentina became once more a favored destination for foreign investment. And then, by the same logic, it also became the victim of the successive “EM shocks” that rippled around the world – starting in Mexico in 1995, Asia in 1997, Russia in 1998 and Brazil in 1999. By the turn of the millennium Argentina’s position was untenable. The monetary corset that had provided stability in the 1990s had become a noose.

As the dollar rose against all competitor currencies, taking the Argentine currency with it, its real economy was squeezed mercilessly. Argentina desperately needed to devalue, but it could not break the dollar peg without risking a full-blown financial panic. In 2001 a catastrophic crisis ensued. The banking system was shut. Unemployment soared. More than half the Argentine population were pushed below. the poverty line. The currency devalued by two thirds.

The 2001 crisis shocked Argentina politics and society. It revived the fortunes of the left-wing of Peronism, bringing first Nestor Kirchner and then his wife Cristina to power.

For an English-language overview of their period in power I found this survey by Marcela Lopez Levy very handy.

Until they lost power in 2015, the Kirchnerites pursued what might be described as a triple strategy. Economic growth was boosted by the commodity super cycle that made Argentina into a champion exporter of soy beans. At the same time, the left Peronists took a tough but pragmatic approach to negotiations with Argentina’s international creditors, refusing to deal with the vulture funds. That shut off market access, but also had the effect of channeling the money that did flow towards productive investment in FDI. At the same time the Peronists sought to spread the benefits of growth through an expanded welfare state. In this they were not alone. The pink tide that swept Latin America in the early 2000s saw a welcome expansion of welfare, poverty reduction and health care across the continent.

Though frowned upon by many economic experts, Argentina’s strategy had both a degree of consistency and of success. Growth accelerated. Inequality and poverty were reduced. And the formula also saw Argentina through the Global Financial Crisis, perhaps the only global shock to which Argentina has shown a degree of immunity. In November 2008 in Washington DC, at the founding meeting of the G20 leadership meeting, Cristina Fernandez Kirchner (known as CFK) found herself in the unwonted position of lecturing George W. Bush on the perils of unfettered financialized capitalism.

But from 2011 onwards, when CFK won a landslide second term, Argentina’s latest success story began to unravel. The fiscal balance deteriorated sharply. Political rhetoric heated up on both sides. And in 2015 CFK was ousted in a humiliating defeat by the conservative pro-market Mauricio Macri.

Macri promised a classic liberal package of retrenchment and opening up. He delivered privatization and slashing cuts to welfare. Meanwhile, he came to terms with the creditors and opened Argentina up to foreign capital flow, which resulted in a dramatic influx of money and a destabilizing crisis. For this most recent crisis, the article Old Cycles and New Vulnerabilities: Financial Deregulation and the Argentine Crisis by Pablo Gabriel Bortz,Nicole Toftum,Nicolás Hernán Zeolla in Development and Change May 2021 is essential and timely reading.

In May 2018 a sudden loss of financial confidence triggered a dramatic peso devaluation. As inflation surged, real wages plunged, bringing about a recession. And the IMF worsened the situation both by adding new debts to those that Argentina could already not afford to pay and insisting on severe budget cuts – a halving of the deficit from 2.7 to 1.3 percent of GDP between 2018 and 2019 – that helped to depress demand.

The resulting crisis was nowhere near as severe as 2001, but it was one of the most savage switchbacks on record and it forced a default not only on foreign debts but also on Argentina’s domestic peso-denominated obligations, a highly unusual occurrence, which puts Argentina’s status as a monetary sovereign into question.

Against this backdrop, the government of Alberto Fernandez that took office in December 2019 struggled to find a new balance that would reconcile debt service with growth, foreign account sustainability and a viable domestic social bargain. It also has to square a political bargain between different wings of the Personist-Kirchnerite movement, that ranges from the centerists around the President to the populist left-wing headed by CFK.

In 2020, in the midst of the devastating COVID shock, Argentina reached a settlement with private creditors and in March 2022 agreed a deal with the IMF. But almost before the ink was dry, that deal has begun to unravel. The question now is whether Argentina can make it through to the end of 2022 without a further savage devaluation, inflation soaring well above 100 percent and a serious recession.

The permutations of Peronist politics, the repeated defaults, the sheer scale of the action, the dizzying inflation rates and tens of billions in defaulted debts, are all elements of the Argentinian drama. But the inner mechanics of these repeated crises are familiar from other settings. Capital flows are driven by global forces. The ideological currents that Argentina navigates are a blend of its national traditions and international opinion. And there are strong structural similarities in the kind of policy instruments that Argentina, like other states of similar income-level, deploys.

As elsewhere in the middle income world, energy subsidies are at the heart of the argument in Argentina over the balance between socio-political imperatives, fiscal deficits, the foreign account and debt service. For most of the last decade, eliminating energy subsidies would have closed most of the fiscal deficit which has been at the center of so much attention in debt negotiations. But that is easier said than done.

****