Adam Tooze's Blog, page 28

December 19, 2021

Chartbook #61 RIP: A climate revolution in fiscal policy?

NB: As you will see from the below, this newsletter was being edited literally as Joe Manchin was killing Build Back Better on Fox TV. Gutted. Trying to figure out what comes next. Pinwheel for now …. pinwheel in the darkest colors.

Back in November, a good friend from the climate community (you know who you are) sat me down and explained how he saw the negotiations over Biden’s Build Back Better infrastructure and welfare package working. Out of that came the slow-cooked piece that appeared in the New Statesman last week.

In the New Statesman I attempt a broader assessment at what is at stake in Build Back Better. I want to focus here on the climate part which was the original motivation for the piece.

In the foreground was the haggling with the centrist Democrats Joe Manchin and Kirsten Sinema. With them it was a matter of pork, of “pay-fors”, of fiscal evaluation by the Congressional Budget Office – conventional fiscal politics in other words. It was tortuous and demoralizing to see Biden’s undersized investment program being further whittled down.

To address climate, the dereliction of infrastructure and America’s many social ills, let alone the “China challenge”, the investment program would have needed to have been hundreds of billions more per annum. For a country of America’s resources, the railway and EV-charger components are laughable. Defense spending in excess of $760 billion per annum puts everything else. This is what America is capable of if its political class actually agrees.

But for all the gloom, there was a glint of enthusiasm in my friend’s eye. Behind the scenes the people pushing Build Back Better had a secret weapon – the modeling teams working the numbers for CO2-emissions.

There were several of these teams. Another interlocutor named three that were particularly influential: Rhodium, Energy Innovation and the Princeton Net Zero project. WRI and E3 have also been working on the problem. There is talk of a group of staffers around Senator Chuck Schumer. When Schumer refers to “the best available data from a wide range of organizations that specialize in policy analysis”, he is, presumably, referring to this network.

If there are other key groups involved that I have not mentioned, I apologize. I would love to hear about their work and to assemble a map of this complex of modeling and analytic project. A project for 2022.

I am sure there is a lot more one could say about the different models they use and their implications. But I want to focus here on the political implications.

What they have been doing, through all the Congressional haggling, is to score each of the revised versions of the bill, as they come down from Capitol Hill, with a view to keeping the overall package in line with the climate objectives of the Biden administration. Above all this has involved replacing sticks with carrots. When Manchin strikes a penalty you add in an inducement to speed up the EV-transition.

The upshot, as the WRI has most recently confirmed, is that so long as the basic provisions of Build Back Better make it through the Senate, there is enough there to give the Biden administration a fighting chance of keeping the US on course for a 50 percent emissions reduction relative to 2005 by 2030.

Energy and CO2 emissions modeling have helped to guide the rearguard action. In the context of the broader discussions about the emergence of a new paradigm in economic policy in 2021, this seems to me to be a significant point.

Often the tendency is to assume that new concepts and ideas in economic policy take the stage when a progressive policy program is on the front foot. That, I think, was the tone of the discussion earlier in the year that accompanied the inauguration of the Biden administration. Indeed, the hope was that with new ideas one might actually gain political momentum. Novelty and innovation build energy and momentum. Its a caricature, perhaps, but I think that was the vibe around the association between MMT and the Green New Deal.

What we are seeing in the context of the “Build Back Better”-fight is a different theory of change. New types of knowledge are being brought to bear on the policy-process, but as part of a rearguard action, to save what can be saved.

The scoring of fiscal policy on the basis of CO2 emissions rather than votes in Congress, impact on the Federal deficit, output gaps or GDP, strikes me as a remarkable innovation.

The idea of doing a green stimulus has been around at least since 2007 and the birth of the first Green New Deal. A lot of modeling has been done on the energy transition. But this is something different: blow by blow negotiation of fiscal policy guided by CO2 scoring with a view to achieving a particular target for emissions reductions within a given timeframe. This is much closer to output gap calculations, or conventional fiscal rules, but with CO2 rather than percentages of GDP as the basic metric.

I’m going to call this a historic first.

I think the idea came to me because I had been teaching a segment in my “Capitalism and Democracy” class on the so-called “Keynesian revolution in government” during the 1940s. One of the key issues in that debate about British and American government is: when does fiscal policy become subordinated to a clearly macroeconomic logic?

The historiography is quite technical and seems to have died down on the UK side about thirty years ago. One good summary for the UK side is by Rollings (1988). For the US William J. Barber’s Design within Disorder is a useful overview.

It is parochial in its focus on the Anglosphere. Planners in Goering’s Four Year Plan were doing output gap estimates at the latest by 1938.

It should not be confused with the broader debate about the “invention of the economy” as an object of government, which to my mind predates the “Keynesian revolution in government” by at least two decades.

But there is no doubt, that as far as fiscal policy in the US and the UK is concerned, the 1940s brought major institutional and conceptual changes. And what is striking, is that the Keynesian revolution in government, particularly in the UK, was innovation on the defensive.

One might think that a Keynesian revolution in government, one in which Keynes himself participated, would have been all about full employment and fiscal stimulus. In fact, in the 1940s it was all about how best to achieve to inflation control.

In the UK, the 1941 budget, marked the first attempt to estimate and manage aggregate demand in order to reduce inflationary pressure. In 1947 the UK Labour government used Keynesian analysis to justify its austerity budget to control inflation. The Economic Section headed by the Keynesian James Meade, argued that price subsidies should be cut. In the short-run that might result in price increases but by reducing macroeconomic imbalance it would help to reduce inflationary pressure in the medium-term.

So strong was the emphasis on inflation-control that if you take the true message of Keynesianism to be the argument for budget deficits to stimulate aggregate demand for the sake of ensuring full employment, you might ask in the British case, whether the Keynesian revolution ever happened. That was Jim Tomlinson’s skeptical view.

In climate terms, how would we feel, if we were using energy and CO2 models to gauge the impact of investing in a large fleet of coal-fired power stations? That is the situation of climate activists when it comes to India or China, not the US or the EU.

Of course, you could take the view that Build Back Better is billed as a climate measure, so it is unsurprising that it is scored in climate terms. We will have to see whether the CO2 approach will generalize to other policy domains, assuming, of course, that the Biden administration gets to pass any further legislation.

It will be interesting to see, also, whether the kind of CO2 analysis of fiscal policy put into action in the US begins to operate in Europe as well.

It is an interesting test of how far the climate governance framework is truly becoming hegemonic. Will CO2 metrics become as omnipresent as GDP currently is?

In the mean time, the general point stands. When we are looking for innovation in economic policy, hard-fought rearguard actions should be as interesting as the moments when history appears to lurch forward.

After all, when do you have to think most carefully about how to get what you want? When you have a big blank canvas and and unlimited budget? Or when you are trying to dance in a phone booth?

***

I love putting out Chartbook for free to a wide and diverse range of subscribers from all over the world. It is a pleasure to write and a great place to pull ideas together. It is also, however, a lot of work. If you feel moved to support the project, there are three subscription options:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.

December 17, 2021

Ones & Tooze: The Pentagon vs. Walmart

Season 1, Ep. 13

Congress has approved a $768 billion defense budget for 2022. If the Pentagon were a private company, would it be bigger than Amazon? Walmart?

Also, can $859 billion buy you love? Or at least domestic goodwill? That’s the amount of money Americans will spend on themselves and their loved ones ahead of the Christmas holiday.

We want to hear from you! To fill out our 2021 listener survey, go to survey.fan/foreignpolicy.com

Chartbook #60: Books we read in International and Global History HistGR8930

Over the last few months I’ve had the pleasure of teaching the introductory course on “Approaches to International and Global History” for the MA program that Columbia jointly runs with the LSE. It wasn’t a course I had taught before. But this is one of the fun things about teaching – the impulses you don’t expect.

I picked a list of books and articles that I wanted to read and I thought would drive an interesting methodological conversation. NB: This is not an introduction to International and Global History, but an introduction to “approaches” to such a history. Nevertheless, I wanted a broadly chronological spine.

To my mind, the course really worked. I was very lucky to have a great group of smart and highly engaged students who drove a fascinating discussion.

Week 1 I started with a Brief History of Commercial Capitalism by Jairus Banaji because for the first week I wanted a text that was short, but “high concept” and challenging.

#2 was a long selection from Geoffrey Parker. Global Crisis: War, Climate Change and Catastrophe in the Seventeenth Century (2013) – to address climate and the early modern global crisis from every angle.

#3 The Great Divergence: Pomeranz and his critics. Not just because it addresses the economy, but because it raises such interesting questions about causation, historical method, politics etc.

A pairing with Prasannan Parthasarathi is always stimulating.

#4 Anthropology and history: Sidney Mintz

Sweetness and Power is obligatory reading on courses like this. For good reason. It is a classic, but …

As several students remarked, it is far more interesting if read, not in isolation, or as a foundational text for “consumption studies” etc. but against backdrop of Mintz’s anthropological work that goes back to the mid century and focused not on production in the “global North” but on plantation production in Puerto Rico and the Caribbean. This essay by Mintz on the Caribbean is simply brilliant. And this essay on Columbia anthropology in the Cold War is highly illuminating.

#5 Family life and Empire: Emma Rothschild, The Inner Life of Empires. Princeton University Press, 2011.

Love this book by my old friend and mentor from Cambridge. Subtle, twisty, reading 18th century through 18th-century concepts. Very smart.

#6 Revolution in global context: Haiti and the French Revolution

At the suggestion of one of the students we read Michel-Rolph Trouillot’s memorable essay: “An Unthinkable History: The Haitian Revolution as a Non-event”. Highly recommended.

#7 Global nations.

We revisited Benedict Anderson, Imagined Communities: Reflections on the Origin and Spread of Nationalism, 2nd ed. (Verso, 1991). First time I had reread it in more than a decade. Quite a trip down memory lane. His trio of functionalist determinations: how do societies anchor power, truth, time, proved generative for the entire rest of term. We paired it with Duara, Prasenjit. Rescuing history from the nation. University of Chicago Press, 1996 which I found impressive and Rebecca Karl’s Staging the World. Chinese Nationalism at the Turn of the Twentieth Century (2002). The idea of staging the world became a bit of a theme in the following weeks.

#8 On Global Time

We read Vanessa Ogle, The Global Transformation of Time, 1870-1950. The chapter I particularly recommend is the one on debates about time in the Islamic world. Mindblowing.

#9 Color Line.

We paired Mae Ngai, The Chinese Question (2021) with Marilyn Lake and Henry Reynolds. Drawing the global colour line: White men’s countries and the question of racial equality. (2008). It makes for a great “bottom-up”, “top-down” contrast. Ngai’s book has really grown on me. What is particularly impressive, is the arc from a cosmopolitan Pacific in the 1840s and 1850s to the closure of the American nation and finally the devastating conclusion in the forced-labour mines of South Africa. For me it evoked shades of the Third Reich. Lake and Reynolds is a book I come back to again and again. Can’t think of many history books that have more dramatically reorientated my thinking about the 20th century.

#10 The strange histories of Realism

We paired Robert Vitalis’s history of race and the making of international relations between Britain and the US, White World Order, Black Power Politics. Cornell University Press, 2016 with Matthew Specter’s fascinating book, The Atlantic Realists, which traces the origins of postwar realism to the US-German connection. Specter’s book will be out in (2022). His forensic demolition of Schmitt’s postwar self-exculpation is devastating.

#11 Postcolonial worldmaking in a neocolonial world

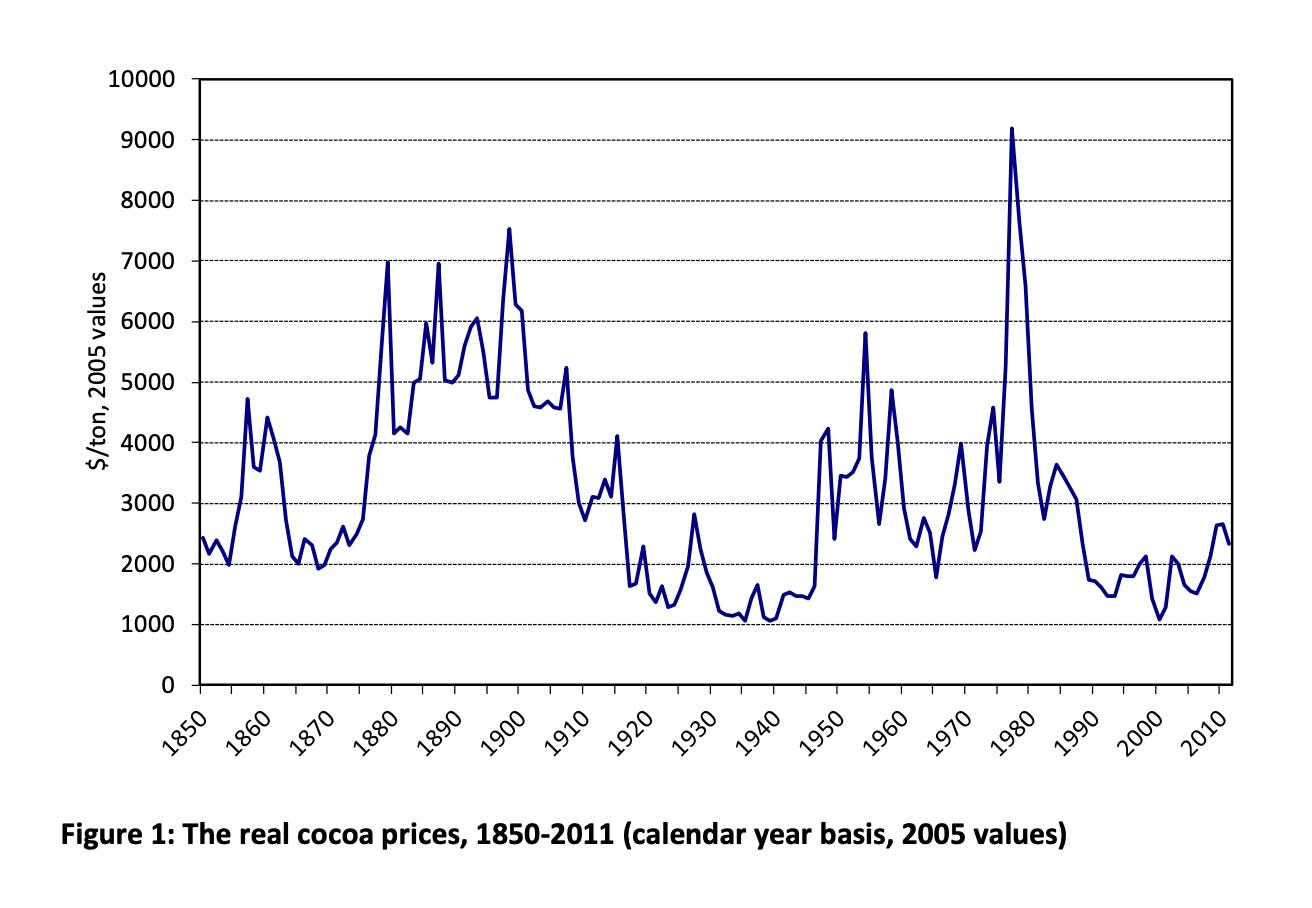

Great to read Adom Getachew, Worldmaking after Empire. Princeton University Press, 2019. I remember Getachew’s PhD taking shape at Yale back in the day. Fascinating to read the finished product. Her compelling argument about the shipwreck of the postcolonial project leaves me more convinced than ever, that an intellectual history of cocoa prices after 1945 would yield major dividends. Before the oil price shock of 1973 a lot hinges on the disappointing development of cocoa prices following Ghana’s independence in 1957.

#12 Sinews of War and Trade

Really enjoyed Laleh Khalili’s Sinews of War and Trade Shipping and Capitalism in the Arabian Peninsula.

Khalili’s wonderfully exploratory method and her engaging writing, encouraged a debate about storytelling, assemblages, the 1970s and declensionist narratives, as well as business history, taking rides on container ships and the links between management consultancy and anthropology. It formed a great bridge to …

#13 Modern ruins

Anna Lowenhaupt Tsing, The Mushroom at the End of the World. Princeton University Press, 2015.

To my mind, this is a truly fascinating book. A micro-study, a macro-history a methodological toolkit a philosophy of history all in one. More on Tsing in a later newsletter over the holiday season.

Conclusion?

Too many to draw out here. Plus, what happens in seminar stays in seminar. But, it was an intellectual trip. Delighted with the way that the texts caused us to reflect on our own positions as “intellectual and global historians”. Delighted also that there are so many other texts that we could and should have included. I will certainly volunteer to do this again in future.

Subscribe

I’m delighted that Chartbook goes out free by email to folks across the world in all walks of life. I enjoy putting it together. But if I’m honest with myself, it takes a lot of work. If you enjoy the feed and can afford to support the mission, why not take up one of the paying options. There are three:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.Subscribe nowAnd since it is holiday season, why not give Chartbook as a gift:Give a gift subscriptionAll very best, ATDecember 13, 2021

Chartbook #58: More reading on WWI

Yesterday’s post about World War I has triggered a remarkable crop of suggestions from readers. They are so good I thought I would pass them on.

It is holiday season after all. Perhaps there are one or two things here that folks might consider for xmas stockings etc.

From Michael Pettis (with many thanks):

“I just read your excellent Urkatastrophe piece, Adam, and it occurred to me that you ought to read, if you haven’t, Charles Arthur Conant’s “The United States in the Orient: the nature of the economic problem” (1900). Conant was a well-known and highly influential (at the time) American economist, and along with Kemerrer the most famous of the “money doctors” of the late 19th and early 20th centuries. I often include him with JA Hobson as the leading proponent of the “excess savings”/imperialism thesis, except that while Hobson opposed imperialism, Conant embraced it. I mention his book because he discusses Russia and the Russian economy a great deal in the book, and his Russia isn’t a decrepit Russian on the edge of revolution but rather one of the most dynamic economies in the world and the only serious rival to US/UK dominance. There is a lot of other very interesting stuff in his book, but as I read your piece it was the comments on Russia that most made me think of Conant.”

You can read it here, for free.

From Policy Tensor a typical hard-hitting riposte, which I in fact largely agree with. With more head space I would have expanded this point.

Wonder why @adam_tooze ignores high racialism as a structuring force in 1890-1914, which was on par with Liberal ideology, if indeed not even more important. World history by conceived by contemporaries as racial history, world politics as the struggle between the races. 1/

— Policy Tensor (@policytensor) December 13, 2021

The book this immediately brings to mind is this wonderful analysis of the global color line by Lake and Reynolds.

A lovely reading list of World War I classic by J. Van Wyck

Worth reading @adam_tooze's latest post on WWI below. The WWI scholarship is vast but I do think the best path is still: Hobson -> Lenin -> Albertini -> Fischer -> Joll -> Clarke. Gives you contours of debate. 'The Deluge' is also vital & provocative. https://t.co/K5JL0Ifi21 pic.twitter.com/4zmgpyx9OA

— J. Van Wyck (@TheRealJVanWyck) December 13, 2021

I agree with Erik Grimmer-Solem that I should have included his brilliant new book amongst the references of the blogpost. It really is highly recommended.

Imperial mindscapes—imagined geographies of upward mobility, prosperity, and security—are crucial for understanding globalization in the age of empire and its breakdown in 1914, esp. for Germany. Have a look at my Learning Empire (CUP 2019)

— Erik Grimmer-Solem (@grimmer_solem) December 13, 2021

It is part of a crop of relatively recent books about Germany and globalization that have finally shown the way out of the dead end that was the Sonderweg (special path) debate.

Top of the list would be Dirk Bonker’s Militarism in a Global Age, a brilliant and eye-opening comparison of German and American navalism in the moment of high imperialism.

From the economic side, Cornelius Torp’s work is crucial:

From the side of cultural and political history, Sebastian Conrad blazed a trail.

Andrew Zimmerman’s Alabama in Africa: Booker T. Washington, the German Empire, and the Globalization of the New South saw connections where no one had seen them.

Chris Manjapra connected imperial Germany to India

GREAT reading all of these. And there are no doubt many more one could add.

I am delighted that Chartbook goes out free to a long list of email subscribers. If you would like to support the effort, why not consider subscribing here.

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.December 12, 2021

Chartbook #57: 1914, the Urkatastrophe of the 20th century

WWI is clearly the “Urkatastrophe” – the original catastrophe – of the 20th century. Not just of the short twentieth century, from 1914 to 1991, but of the long twentieth century too.

1914 is in the news again today as a way of understanding the mounting tension between China and the United States. In this historical analogy, the United States, the incumbent, is allotted the role of the British Empire, seeking to resist the challenger, China, which is placed in the position of the Kaiser’s Germany. (Btw: Apart from the weirdness of this analogy, it also assumes a pretty strong and contentious thesis on what actually happened in 1914. More on this another time.)

The line you take on the outbreak of the war in 1914 colors your entire vision of European and world history. One way of describing the situation is simple. In the words of my good friend Alexander Zevin, as quoted by Perry Anderson: ‘The structural reality is that the First World War took place over empires, for empires and between empires’.

A clash of Empires, for sure. How could it have been anything else? After all, all the great powers at the time were one or other type of empire. To add any value we need to be more precise in defining the historical conjuncture. 1914 was not simply a clash of Empires. The war was a product of a distinct conjuncture, well-labeled as the ‘age of imperialism’ . This conjuncture was defined not simply by empires butting up against each other, as they had for centuries. It was a new epoch defined by a new blend of expansive geopolitical claims, empires dynamized by nation-state mobilization at their core and the imbrication of those states with the interests of the latest generation of capitalist accumulation. All of this took place against the backdrop of a vision of history and global geography that was both grand and claustrophobic. The global frontier closed in the 1890s. The stage was set for the great play of world history to begin in earnest.

Nor was this lost on contemporaries. The wide currency of imperialism theories dates to the moment of the Spanish-American war and the US invasion of the Philippines (1898-1899), the Boxer intervention (1899-1900) and the Boer War (1899-1902). The notion comes in different shades, ranging between J.A. Hobson’s liberal version to Lenin’s Bolshevik classic.

Lenin’s analysis, like that of Rosa Luxemburg before him, is more holistic and deterministic than that of Hobson. They have in common that they described the current moment of imperialism as something new.

The age of imperialism was clearly the final stage in a Western drive to expansion that began in the 15th century. It also continued the history global competition, which in the case of Britain and France went back to the 18th century. But in the late nineteenth century, this took on a radical new expansiveness and violence. Crucially, because it was now conceived of as taking place within a finite sphere. The frontier was closed and because the pressure of historical time and drama speeded up. The German phrase, Torschlusspanik, is apt.

In this remarkable interview, the South African artist William Kentridge defines it as:

The panic of closing doors. The fear of opening one door rather than another, and hearing it slam behind you, once you have made your decision; but maybe that decision is the wrong one, so you would rather stand paralysed in front of three doors to avoid making it. Torschlusspanik.

William Kentridge in interview with Peter Asden, “The art of war” for The Financial Times, 7/8 July 2018.

In 1959 the publication of William Appleman Williams’s Tragedy of American Diplomacy, and in 1961 Fritz Fischer’s Griff nach der Weltmacht, gave imperialism theory a new lease on life in the historical profession.

Amidst the general resurgence of imperialism-talk in the context of Vietnam and Third World struggle, Fritz Fischer’s Germano-centric account of 1914 produced an extraordinary éclat. But as far as the July crisis of 1914 was concerned this was also the last great hurrah of imperialism theory. The critical onslaught against Fischer’s interpretation of the outbreak of the war helped to discredit models of imperialism more generally. It did not help that Fischer’s take on German responsibility got caught up with crude Sonderweg models that tried to identify the supposed abnormalities of Germany’s modernization. This involved tying undeniable and important differences in political organization, military command chain and strategic outlook to subtle and much harder-to-define national social-structural differences. It was an intellectual dead end. What got lost in the process was any awareness of the broader development both of global capitalism and imperialist competition.

By the 1990s, whether or not historians have ascribed responsibility for the July crisis to Germany, the focus has shifted away from a broad-based analysis of imperialism (and the Sonderweg) to one based on politics, diplomacy, the arms race and military culture. Often this is associated with a stress on the July crisis as an event determined by the continental logic of Central Europe rather than the wider forces of global struggle – the scramble for Africa or imperial tension in Asia – that seemed to be implied by references to imperialism.

Economic forces continue to play a key role in any plausible interpretation of World War I – in the form of Russia’s looming development and the costs of the arms race between the major power. But whereas under the sign of imperialism theory the link from geopolitical ambition to economic interests was made scandalously explicit, in more recent work the underlying economic dynamics are no longer foregrounded . The tight connection between the outbreak of war, imperial expansionism and capitalist competition has unravelled.

If conventional historiography displaced imperialism and the discussion of capitalism from the center of the discussion, economists and economic historians were only too happy to concur. British economic historians of empire were in the vanguard of the academic attack on the first generation of imperialism theories. They never liked Lenin.

The body of work on the 19th-century world economy that emerged in the 1990s, notably that jointly authored by Kevin O’Rourke and Jeffrey Williamson, treated the period before 1914 under the rubric of globalization, rather than imperialism. Theirs was not a panglossian history of globalization. Loosely following the model offered by Karl Polanyi’s classic The Great Transformation (1944) they focused on social tensions unleashed by mass migration and the grain invasion in Europe, which collapsed commodity prices and hurt the rural interest. But war lay outside their purview. 1914 was exogenous. Sarajevo appears as a nasty accident.

In 2007 the Communications Director of the IMF remarked ruefully: “Alas a sniper’s bullet on June 28, 1914, triggered a chain of events that reversed globalization.” Indeed, pushed to the limit, the neo-Polanyian school of economic history could be read as arguing that to understand the crises of globalization that arose in the early 20th century, you did not need the exogenous shock of World War I at all. Counterfactually, the “interwar crises” might well have happened even without the wars.

It is strong stuff!

Crucially, monopolies and militarism were not seen as constitutive of globalization, as imperialism theory à la J.A. Hobson would have it, but as antithetical to globalization. As Williamson and O’ Rourke put it with characteristic frankness, in their calculations of market integration they assume that ‘(i)n the absence of transport costs, monopolies, wars, pirates, and other trade barriers, world commodity markets would be perfectly integrated’. Globalisation, by their measure, would thus be complete if only power and politics did not get in the way. The fact that imperial rivalry actually led to major investments in transport infrastructure and enabled globalization is excluded by assumption. Likewise, there is little room for acknowledging the way that large-scale foreign lending – on the basis of an increasingly integrated capital market – supercharged the imperialist aggression of a rising power like Japan. Whilst “domestic” socio-economic stresses are admitted, economics and geopolitics are held at arms length.

An economics squeamish about the question of power converged with an anti-Leninist historiography to squeeze out the question of imperialism and 1914.

Whatever one thinks of the political and intellectual lineage of imperialism theory, this is obviously problematic. A useful theory of globalization must account for global conflict as endogenous to the process of global growth, rather than exogenous.

My book Deluge sought to capture one element of that shift – the dramatic rise of the United States. For that reason it started, provocatively, in 1916.

But, conscious of the need to face the “1914 question”, I addressed the question of the politics and economics of the war in a trio of essays that appeared at the same time as the book.

An essay with Ted Fertik queried whether WWI was really a break in the trajectory of globalization or could instead be seen as a phase in which globalization was rearticulated in violent ways.

Another, argued not that WWI was a war of democracy v. autocracy, as Entente propaganda had it, but a war fought under democratic conditions over what democratization might turn out to be in the 20th century.

I will come back to both those arguments in later posts.

Most pertinently, I contributed an essay to a volume edited by Alex Anievas explicitly on the question of “Capitalist Peace or Capitalist War? The July Crisis Revisited”. A full draft can be downloaded here. – Read now

You can find at least some of the footnotes necessary to support the following sketch argument in that pdf.

Even within the sphere of mainstream academic social science, it is striking that compared to history or economics, political science has been far bolder and more interesting in advancing ways of explicitly connecting economics, politics and war. In arguments over the theories of “capitalist peace”, “democratic peace” and bargaining theories of war, economic development, or the lack of it, is tied to 1914. The PDF article discusses some of those debates as they stood around the anniversary in 2014.

In this newsletter I want to make a more streamlined version of that argument.

The key points are as follows:

The firewall drawn between “1914” and the story of the first globalization is ideological. But it is also a weak form of ideology – a silence rather than a strong thesis. Mainstream historical accounts of the July crisis in 1914 are, in fact, based, more often than not, on a modernization theory that dare not speak its name. Accounts such as Chris Clark’s Sleepwalkers rank Western European Empires and the scrappy Balkan protagonists in developmental terms. Meanwhile, economic accounts of the late 19th century that give a civilian-socio-economic analysis of the stresses of globalization and treat 1914 as exogenous, result not just in a whitewashing of global economic development, but in strange and counterfactual history of the early twentieth century.

Uncoupling geopolitics from socio-economic development is a problem not just for our understanding of 1914, but for the interwar period that follows. Not only is 1914 exogenized but you end up, for instance in Barry Eichengreen’s work, with an account of the interwar period to which the war itself is causally incidental. As I will argue in a future note, this points to a broader problem of articulating global power politics with international economic history in the early 20th century.

In light of all this evasiveness, we should bring the concept of an age of imperialism back.

In a remarkable article published in 2007, Paul Schroeder the doyen of European diplomatic history, asked how are we to characterise the sea-change that had clearly come over the international system in the generation before 1914. The world that the modern political science literature takes for granted, of multi-dimensional, full spectrum international competition was not a state of nature. It had taken on a new comprehensive form in the late nineteenth century. There is still no better concept, Schroeder insists to grasp this competition that embraced every dimension of state power –GDP growth, taxation, foreign loans – that made the constitution of Russia itself endogenous to grand strategic competition, than the concept of an ‘age of imperialism’. Schroeder is not, of course, appealing for a return to Lenin. But what Schroeder wishes to highlight is what it was that Lenin, Kautsky and other theorists of the 2nd international were trying to analyse and rationalise; namely the widely shared awareness that great power competition had become radicalised, expanded in scope, and had taken on a new logic of life and death.

In this view of the age of imperialism the driver is not the competition of individual capitalists, harnessing nation states for their purposes, with Krupp or Vickers Armstrong, or Cecil Rhodes in the driving seat. The notion of imperialism that Schroeder invokes and I would subscribe to, is more general and ultimately framed by state power and politics. As far as the economy is concerned the key is the global balance of (geoeconomic) power, both as a specific construct – number of guns etc – and as a frame for thinking about the world. This links to my early work on the history of statistics. It is against the backdrop of the age of imperialism that both the concept of national economy and, as Quinn Slobodian has shown, the idea of the “Weltwirtschaft” take shape. We enter, in short, the world of mental mapping that we still inhabit today, the mapping that causes us to ask: when China will overtake the United States as the world’s largest economy?

The basic point to be made about global economic growth before 1914 in connection with the outbreak of the war, is that it was uneven. Some national economies grew faster than others. This uneven economic development threatened to shift the military balance of power, by way of manpower, tax revenue and technological capacity as well as strategic assets like railways. And it was that which was a prime driver of the tensions and calculations that lead to war in 1914.

Furthermore, this competition should not be understood merely in objectivist terms – the numbers of troops and speed of railways etc. If we want to understand decision-making we also need to grasp the way in which those differences were made sense of. How they fitted into visions of the present and the future. How they were framed as part of the great drama of world history.

The logic of rivalrous uneven development played out in distinct force fields.

The one most commonly invoked for purposes of historical analogy is Imperial Germany’s rivalry with Britain. This was no doubt serious. It could, at various points have lead to conflict. But, as far as the war that actually broke out in 1914 was concerned, it was an indirect contributor. By 1914, Britain had clearly won the naval arms race. It had sone so, not through superior industrial performance, but through strategic focus, determined technological development and the success of the Liberal government in forcing through a constitutional and a fiscal revolution. Britain had the tax base to compete.

The military-industrial race that directly impelled the outbreak of war in 1914 was not naval but continental and it was not, in fact, one race, but two.

The decisive axis was France-Germany-Russia. This revolved around the relative mobilization of national resources by France and Germany and the sporadic and unpredictable development of Russia. Russia was truly the swing variable.

Russia was defeated by Japan in 1905 and had been shaken by revolution. On the other hand its huge size and enormous potential made it a looming threat as far as Germany and Austria were concerned. The Tsar and his ministers had huge freedom of action. It had a neutered parliamentary system. In Russia’s governing circles politicised nationalist protectionism was rampant. Added to which, with ample funding from France, Russia’s power was growing by the year and its expanding railway network was speeding its pace of mobilization. In the summer of 1912 Jules Cambon of France noted after a conversation with Germany’s Chancellor Bethmann-Hollweg that regarding Russia’s recent advances,

the Chancellor expressed a feeling of admiration and astonishment so profound that it affects his policy. The grandeur of the country, its extent, its agricultural wealth, as much as the vigour of the population … he compared the youth of Russia to that of America, and it seems to him that whereas (the youth) of Russia is saturated with futurity, America appears not to be adding any new element to the common patrimony of humanity.

The French themselves were extremely optimistic about Russia’s prospects. A year later French foreign minister Pichon received from Moscow a report commenting that

there is something truly fantastic in preparation, …. I have the very clear impression that in the next thirty years, we are going to see in Russia a prodigious economic growth which will equal – if it does not surpass it – the colossal movement that took place in the United States during the last quarter of the 19th century.

Was Russia a bankrupt? Or was it a steamroller?

In 1913 the Kaiser’s government finally persuaded the Reichstag to agree to raise the size of peacetime army from 736,000 to 890,000. But the immediate response was to triggers the passage of the French three year conscription law and the promulgation of Russia’s ‘Great Programme’, which raised its peacetime strength by 800,000 by 1917. By 1914 Russia’s army strength was double that of Germany and 300,000 more than that of Germany and Austria combined with a target by 1916 of 2 million. Against this backdrop the Germans were convinced that by 1916–1917 they would have lost whatever military advantage they still enjoyed. This implied to them two things. First, Russia would be unlikely to risk a war until it reached something closer to its full strength. So Germany could risk an aggressive punitive policy in Serbia. If this containment were to fail, then 1914 would be a better moment to fight a major war than 1916 or 1917.

But, no more than Anglo-German competition, was it a direct confrontation between France, Germany and Russia that triggered war in 1914. The stakes were too high for an open clash to happen there.

What launched the war was a clash between their allies in a third zone of competition – the shatter-zone of the Habsburg and Ottoman Empires. The basic question that dominated the rivalry between the Balkan powers and their great power backers was the question of backwardness. This was in part political and military but it was also, crucially, economic. These were the poorest parts of the European economy. Could they catch up? Did any of them, the Bulgarian, Serbians, Austrians or the Tsarist Empire, actually have a place in the 20th century?

In a very general sense this three-sphere model: Anglo-German, Franco-German-Russian, Habsburg-Serb-Russian can clearly be ranked in terms of economic and political development.

But that neat hierarchy is muddled by the fact that the logic of alliances dictated not separation of hierarchical levels but interconnection. For progressives in France and Britain, those who believed most firmly in the logic of progress, it was profoundly disturbing to find themselves from the 1890s onwards, drifting towards a strategic alliance with Tsarist Russia.

On grounds of liberal political ethics an alliance between the French republic and the autocratic and anti-semitic regime of Tsarist Russia was clearly to be regarded as odious. But furthermore, if as liberals insisted, the domestic constitution of a society was predictive of its likely international behavior and its future prospects, then an alliance between a republic and an autocracy was questionable not merely on normative liberal, but on realist grounds. For a convinced liberal placing a wager on the survival of the Tsarist regime was a dubious bet at best. Tsarism’s army was huge and it was convenient to be able to count on the Russian steamroller. But could Tsarism really be relied upon as an ally? Might Tsarism not at some point seek a conservative accommodation with Imperial Germany? Furthermore, given liberals understanding of history, was the Tsar’s regime not doomed by its brittle political constitution and lack of internal sources of legitimacy?

Following the defeat at the hands of the Japanese and the abortive revolution in Russia in 1905, Georges Clemenceau, an iconic figure of French radicalism before his entry into government in 1906 was particularly prominent in demanding that France should not bankroll the collapsing Tsarist autocracy. From Russia itself came pleas from liberals calling on France to boycott the loan to the Tsar. Poincaré typically cast the problem in legal terms. How was Russia to reestablish its bona fides as a debtor after the crisis of 1905? If Russia was to receive any further credits it must provide guarantees of their legal basis. That would require a constitution, precisely what the Tsar was so unwilling to concede. Meanwhile, France’s own democracy suffered damage as Russian-financed propaganda swilled through the dirty channels of the French press. The most toxic product of this multi-sided argument were the notoriously anti-semitic Protocols of the Elders of Zion a forgery generated by reactionary Russian political policemen stationed in Paris, who were desperate to persuade the Tsar that the French-financed capitalist modernisation of Russia was, indeed, a Jewish plot to subvert his autocratic regime.

But the demands from French Republicans and Russian radicals were, in fact, to no avail. The international system had its own compulsive logic that might be modified but could not so easily be overridden by political considerations, however important they might be. The consequences of Bismarck’s revolution of 1866–1871 could not be so easily escaped. By the 1890s the triumphant consolidation of the German nation-state had created enormous pressure for the formation of a balancing power bloc anchored by France and Russia. This type of peace time military bloc might be a novelty in international relations. It might be odious to French radicals. But Tsarism knew it was indispensable. By 1905, Russia was too important both as a debtor and as an ally to be amenable to pressure. With the French demanding that foreign borrowing be put on a secure legal basis and the Duma parliament uncooperative, the Tsar’s regime simply responded by decree powers arrogating to itself the right to enter into foreign loans.

Desperate to escape this dependence on Russia, French radicals looked to the Entente with liberal Britain. Clemenceau indeed risked his entire political career in the early 1890s through his adventurous advocacy of an Anglo-French alliance, laying himself open to allegations that he was a hireling of British intelligence. And certainly some British liberals, Lloyd George notable amongst them, understood the 1904 Entente with France as a way of ensuring that there would be no war between the two ‘progressive powers’ in Europe. But Britain’s own concern for its imperial security was to pressing for it to be able to ignore the appeal of a détente with Russia. It was the hesitancy of the British commitment to France that combined with the Russian revival to push Paris back in the direction of Moscow. By 1912 the French republic was committing itself wholeheartedly not to regime change in Russia but to maximising its firepower.

The appeal of the ‘liberal’ British option was not confined to France. In Germany too the idea of a cross-channel détente with Britain was attractive to those on the progressive wing of Wilhelmine politics. Amongst reformist social democrats there were even those who toyed with the idea of a Western democratic alliance against Russia, including both France and Britain. Bernstein reported that when he discussed the possibility of a Franco-German rapprochement with Jaures, the Frenchman had exclaimed that in that case France would lose all interest in the alliance with Russia and the ‘foundations would have been layed for a truly democratic foreign policy’. Beyond the ranks of the SPD, ‘Liberal imperialists’ speculated publicly about the possibility of satisfying Germany’s desire for a presence on the world stage, without antagonising the British. But in practice the Kaiser and his entourage, no doubt backed by a large segment of public opinion, could never reconcile themselves to the reality that they would forever play the role of a junior partner to the British Empire. Antagonism with Britain, however, implied an alliance system that bound Germany to the Habsburg Empire as its main ally. And this commitment was reaffirmed in 1908 by Bülow’s support for Austria’s abrupt annexation of Bosnia-Herzegovina. This in the eyes of many liberal imperialists in Berlin was to prove a tragic mistake. Richard von Kühlmann, a leading advocate of détente with Britain, who would serve as Germany’s foreign secretary during World War I and was driven out of office in the summer of 1918 as a result of clashes with Ludendorff and Hindenburg, would describe Berlin’s dependence on Vienna as the true tragedy of German power. From the vantage point of a liberal view of history, the true logic of World War I was a struggle over the inevitable dismantling of the Ottoman and Habsburg Empires. For a German liberal such as Kuehlmann for Berlin to have tied itself to the Habsburg Empire, a structure condemned by the nationality principle to historical oblivion, was a disaster. A true realism involved not sentimentality or blank cynicism but an understanding of history’s inner logic. A new Bismarck would, Kühlmann believed, have joined Britain in a partnership to oversee the dismantling of both Habsburg and Ottoman Empires, whose crisis was instead to result in the self-destruction of European power.

Instead, 1914 manifested an utter confusion of hierarchies. And in a historical moment characterized by extreme reflexivity it is hardly surprising that all these theories were anticipated and incorporated such that all sides derived justifications for their actions. Both the rally by German social democracy to national defense and Lenin’s defeatism were justified in terms of hierarchical notions of historical development. For both the pivot of the argument was Tsarist Russia.

At the time of the 1848 revolution and after both Marx and Engels had preached the need for a revolutionary war against reactionary Russia. Since the 1912 election the SPD had emerged as the largest party in the Reichstag. As a socialist party it was committed to a Marxist interpretation of history and thus to the cause both of progress and internationalism. It was also, of course, a mass party enrolling millions of voters many of whom were proud German patriots, who saw in August 1914 a patriotic struggle and an occasion for national cross class unity. Famously the party like virtually all its other European counterparts voted for war credits. But despite the abuse hurled at them by more radical internationalists, for the SPD as for other European socialists, it was not naked patriotism that triumphed in 1914. What overrode their internationalism was their determination to defend a vision of progress cast within a national developmental frame. World War I was a progressive war for German social democracy in that it was through the war that domestic reform would be won. It was not by coincidence that it was during the war that the Weimar coalition between the SPD, progressive liberals and Christian Democrats was forged. It was that coalition that delivered the progressive constitution of the Weimar Republic. This was a democratic expression of the spirit of August 1914. It was the first incarnation of Volksgemeinschaft in democratic form. It was defensive in inspiration. An Anglophile like Bernstein deeply regretted the war in the West, but there was no question where he stood in August 1914. The cause of progress in Germany would not be helped by surrendering to the rapacious demands of the worst elements of Anglo-French imperialism. If the Tsar’s brutal hordes were to march through Berlin, the setback to progress would be world historic. But it was not merely a revisionist like Bernstein who took this view. Hugo Haase, the later founder of the USPD, justified his support for the war on 4 August in strictly anti-Russian terms: ‘The victory of Russian despotism, sullied with the blood of the best of its own people, would jeopardise much, if not everything, for our people and their future freedom. It is our duty to repel this danger and to safeguard the culture and independence of our country’.

Lenin himself employed a similar logic in developing his position on the war in 1914. In his September 1914 manifesto Lenin declared the defeat of Tsarism the ‘lesser evil”. Nor did Lenin shrink from making comparisons. In his letter to Shlyapnikov of 17 October, he wrote: “for us Russians, from the point of view of the interests of the working masses and the working class of Russia, there cannot be the smallest doubt, absolutely any doubt, that the lesser evil would be now, at once the defeat of tsarism in this war. For tsarism is a hundred times worse than Kaiserism.” Early in 1915 this line was reiterated in a resolution proposed to the conference of the exiled Bolshevik party that echoed Marx and Engels in 1848. All revolutionaries should work for the overthrow of their governments and none should shrink from the prospect of national defeat in war. But for Russian revolutionaries this was essential, because a “victory for Russia will bring in its train a strengthening of reaction, both throughout the world and within the country, and will be accompanied by the complete enslavement of the peoples living in areas already seized. In view of this, we consider the defeat of Russia the lesser evil in all conditions.”

Lenin, of course, was at pains to distance himself from the logic of national defense that would seem to follow from his comment for German social democracy. Instead, he called on revolutionaries to raise the stakes by launching a civil war. But, given the difficulties that Lenin had in formulating his own position, it is hardly surprising that the SPD chose a more obvious path. A German defeat at the hands of the Russian army would be a disaster. So long as the main aim was defense against the Tsarist menace they could be won for a defensive war. And this was well understood on the part of the Reich’s leadership who by 1914 were convinced that they needed to bring the opposition party onside. To secure the solidity of the German home front it was absolutely crucial from the point of view of Bethmann Hollweg’s grand strategy during the July crisis that Russia must be seen to be the aggressor. Throughout the desperate final days of July Berlin waited for the Tsar’s order to mobilise before unleashing the Schlieffen Plan. As Bethmann Hollweg well understood, whatever Germany’s own entanglements with Vienna, only if the expectations of a modernist vision of history were confirmed by a first move on the Tsar’s part could the Kaiser’s regime count on the support of the Social Democrats, who were in their vast majority devoted adherents of a stage view of history that placed Russia far behind Imperial Germany. It was Russia’s mobilisation on 30 July 1914 that served as a crucial justification for a defensive war, which by 1915 had become a war to liberate the oppressed nationalities from the Tsarist knout, first the Baltics and Poland then Ukraine and the Caucasus.

The logic of the imperialist age was at work here in multiple layers of determination. In the threat of being locked in life and death competition with Russia. In the significance of Russia’s railway development and the scale of its military mobilization. But also in assumptions about the aggression that such a regime would surely manifest and what the appropriate reaction of a progressive Empire like Germany should be.

Most fundamentally what were at stake were conceptions of history. This subtle point is explicated by Schroeder himself in the telling image he chooses to illustrate the difference between the classical game of great power politics and the age of imperialism.

The classical game of great power politics, Schroeder suggests, was like a poker game played by highly armed powers but with a sense of common commitment to upholding the game. It was thus eventful, but repetitive, highly structured and to a degree timeless. There was no closure. Win or lose, the players remained the same. Imperialism, by contrast, was more like the brutal and notoriously ill-defined game of Monopoly. Under the new dispensation the players’ sole aim was accumulation up to and including the out-right elimination of the competition through bankruptcy. As Eric Hobsbawm also pointed out, one of the novelties of the situation before 1914 was that great power status and economic standing had come to be identified and the terrifying aspect of capital accumulation was that it had not natural limit.

The difference with regard to temporal dynamics is striking. Unlike an endlessly repeated poker round, as the game of Monopoly progresses, the piling up of resources and the elimination of players marks out an irreversible, ‘historical’ trajectory. Unselfconsciously Schroeder thus introduces into the discussion one of the most fundamental ideas suggested by Hannah Arendt in the critique of imperialism and capitalist modernity that she first developed in The Origins of Totalitarianism. What she described was precisely the colonisation of the world of politics by the limitless voracious appetites of capital accumulation. And for her too this brought with it a new and fetishistic relationship to history.

If global capitalist development was tied up in a very deep way with dynamic that drove the powers to war in 1914, so too was its guiding ideology of liberalism. Liberalism is not imperialism’s other, as by 1918 would be suggested by Woodrow Wilson’s reworked version of liberal ideology. Nor, on the other hand, is it reducible to, or identical with imperialism, as some critics would allege. They undeniably existed within the same space and in the early 20th century constituted each other.

Liberalism could justify violent escalation – “the war to end all wars” etc. But that violent dialectic was only one possibility. The moment also gave rise to a new crop of theories of world order order and “ultra-imperialism” as advanced, for instance by Karl Kautsky and J.A. Hobson.

The problem of finding a new global order in the early twentieth century, the idea that came to such prominence in the wake of World War I, is not best understood in terms of “idealism” or the soft tissue of a disempowered international civil society. As I argued in Deluge, the project of world order, is best understood, as a power-political project.

And this is where the question of hegemony enters in.

With the plausibility of empire as a means of global ordering having reached its limit, hegemony is a convenient term for a global ordering of power amongst the powerful. The concept is indispensable. But it is also a snare.

In the wake of the interwar crisis, analysts, taking inspiration from cyclical models of the development of capitalism, posited that hegemony was, if not a universal tendency, then certainly a recurring imperative of modern capitalism. To function well, the system needs a hegemon. Always!

This was the thesis both of Kindleberger and Arrighi.

The interwar crisis was the latest to result from a phase of hegemonic transition. In this case the baton dropped as it passed from the British Empire to the US.

There can be little doubt that a baton dropped. But what was at stake was not some ancient scepter of hegemonic power passed down from the Genoese to the Dutch, from them to the British and from there to the United States – the phrase is translatio imperii.

That is of course an attractive idea for empire-builders, but its significance is as a piece of ideology rather than as an explanation. British power in the 19th century constituted the global condition, in Geyer and Bright’s terms, but it had precious little to do with hegemony as the US exercised it after 1945 – as instantiated in organizations like NATO and the European Community. Those were tools of order suited for an age of extremes. The problem of order is defined by the forces in play. The transhistoric notion of a hegemonic imperative fails to do justice to the explosive force of accumulation and state-formation unleashed from the middle of the nineteenth century i.e. the age of imperialism. To corral those forces, hegemony of a far more robust and intrusive kind was required.

The British Empire did attempt to raise its game to match the challenges of the era. I take this to be the point of John Darwin’s indispensable Empire Project. But that radical new British ambition, to hold the global ring not at a distance, but through direct engagement of all the key players, suffered shipwreck in 1922 at Genoa. That was the moment, especially in comparison with the remarkable deal brokered at the naval conference in Washington, that America’s indispensability – in this conjuncture, at this moment – became undeniable. More on this to follow.

Three subscription options

I am delighted that Chartbook goes out free to a long list of email subscribers. If you would like to support the effort, why not consider subscribing here.

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.Or gift the newsletter to a friend, for the holidays.

PS. And, yup. This is part #2 of my slow-moving reply to Anderson. Steady as she goes!

December 10, 2021

Ones and Tooze: Is Democracy Better for the Economy?

Season 1, Ep. 12

With President Joe Biden’s Democracy Summit underway, Adam and Cameron discuss whether democratic principles help or hinder economies. The answer is more complicated than you might think. Also, if you have an old Ford Escort or other classic car, hang onto it. You might get rich.

Subscribe wherever you get your podcasts or learn more at Foreign Policy.

December 4, 2021

Chartbook #56: The West Asian Polycrisis – From Afghanistan to Lebanon

In the recovery from the COVID shock of 2020 there is a stark gap between the rapid rebound of rich countries and the slower recovery of middle-income and low-income economies. It is important to recognize this stark difference and how 2020 differs in this respect from the 2008 crisis. But dividing the world in this dualistic way, between rich and poor, sacrifices any geographical detail. We lose sight of the way the problems afflicting economies and societies in a region can compound each other.

I wrote in Chartbook 20 about the Caribbean and Central America. In commentary of late, South America has been singled out as a possible zone of interlocking crises.“Three shocks unsettle business confidence across Latin America”, warned a recent FT headline.

Regions of polycrisis might be defined succinctly as zones in which the collective trouble is worse than the sum of its parts. Think of a region where climate change brings drought or a historic hurricane that crosses borders, creating misery and refugee flows, with no safe place to go. Think of regions wracked by geopolitical tensions and local rivalries.

Alongside Latin America, another region that might be thought of in these terms, is the region that Fred Halliday once dubbed Western Asia, a region that stretches by way of Pakistan and Afghanistan, to Iran, Iraq, Syria, Lebanon and Turkey (figures refer to population estimates).

The aggregation population of these countries is 491 million, comparable to that of the EU (445 m) or Canada-USA-Mexico (497 m).

State borders in this region are some of the most arbitrary in the world. The Kurdish population of 40 million stretches across Turkey, Syria, Iraq and Iran. Millions of displaced people from Afghanistan, Syria and Iraq lived in improvised camps. The economies are interconnected through the use of multiple currencies, trade and infrastructure connections, particularly for energy. Climate change has inflicted simultaneous drought on Iraq, Iran and Afghanistan. Altogether, the region presents a landscape of crisis more intense than anywhere else in the world.

At the Eastern end of the region, following the Western withdrawal and the Taliban takeover, Afghanistan is on the edge of catastrophe. The UNDP and the IMF are predicting that the Afghan economy may contract by 20-30 percent in a single year, an unprecedented collapse. “Nine out of 10 Afghans are expected to fall below the poverty line by next year. More than half of the 39m population require food assistance.” The G20 meeting in October agreed to take action to address the humanitarian crisis. But despite UN appeals, the foreign assets of Afghanistan to the tune of $9.6 billion remain frozen.

Today is international #GISDay. #GIS plays a critical role in all that we do.

— The Integrated Food Security Phase Classification (@theIPCinfo) November 17, 2021

Behind this map of #Afghanistan, there is the work of 51 analysts, 45 analysis areas, and the #foodinsecurity status of over 41 million people. #GIS helps us get information to those who can help. pic.twitter.com/d2HAEQmYVu

All eyes were on Afghanistan at the moment of Western withdrawal, we should not avert them now that tens of millions of people have to suffer the consequences.

Afghanistan’s immediate neighbors will have no option. Refugees are already beginning to flood into Pakistan and Iran. These are the latest IMF estimates.

Source: IMF

Pakistan is in no position to provide much support to the Taliban regime or to Afghan refugees. As the FT recently said:

“Pakistan’s more than 220m people were spared the worst of the coronavirus pandemic’s initial economic shock, thanks in part to the government’s policy of shorter, looser lockdowns. But they are now facing a new crisis: inflation has surged to the worst level in years, with an index tracking everyday essentials such as fuel, food and soap last week rising above 18 per cent year on year. The rupee has also tumbled to all-time lows, losing 15 per cent of its value against the dollar in six months. Officials fear a surging import bill will deplete foreign currency reserves and further destabilise the economy.”

This poses a major challenge to PM Imran Khan. He came to power in 2018 promising to end “the country’s cycles of economic instability, where high debt and low foreign currency reserves forced repeated bailouts from institutions such as the IMF. But Khan has found himself trapped in this same vicious rhythm ….”.

Since December 2017 the Pakistani rupee has devalued by half. Under Khan’s premiership the devaluation has been 30 percent.

The Taliban victory was celebrated as a victory also for Pakistan, but without strong US backing it is unclear whether Pakistan has the platform to really take advantage. China is Pakistan’s main strategic ally, but on that front too there are mounting difficulties. BRI programs, once loudly hailed, are making disappointing progress.

Apart from Pakistan, Iran is the immediate destination for most people fleeing Afghanistan. In the last few weeks it is reported that some 5,000 Afghans are entering Iran every day. Iran has the resources to cope, but it too will suffer as a result of the Afghan implosion. Since 2018 when Iran faced a dramatic intensification of US sanctions, Afghanistan has served Iran as a conduit for $5billion per annum in cash. Both the US and Iranian currencies were in widespread use in Afghanistan. “… the Iranian rial has been broadly used in western border provinces, such as Herat, Farah and Nimroz. … the Herat governor tried to ban the use of the rial in 2019, arguing that Iranian currency was entering the Afghan economy to essentially drain US dollars. However, usage of the rial has broader driving factors too. There has been extensive drug smuggling originating from Afghanistan, boosting financial exchanges between the two neighbors. Moreover, numerous Afghan border communities purchase many of their supplies inside Iran, hence the demand for the rial.” Now the Taliban have issue a ban on foreign currencies. That may help to explain why the Iranian currency, the rial, weakened as the Taliban consolidated their grip.

Severe as the spillover from Afghanistan to Iran may be, one should not imagine that they are in the same boat. Whereas Pakistan and Afghanistan are stuck at low levels of income. Iran is a middle-income country with a large and highly diversified economy. It is far less agrarian than Pakistan and far less dependent on oil than Iraq. A chart of PPP-adjusted GDP per capita divides Western Asia into three regions.

Given its sophistication and population of 80 million, Iran has the potential to be an economy on the scale of Turkey or Saudi Arabia, both of which are members of the G20. That it is not, is a matter of politics, geopolitics and political economy – the state-run political economy of the Islamic Republic and the dramatic pressure of sanctions. If you bring Iran’s economic development over the last decade into close up, the impact of sanctions is clear. In the summer of 2010, the Obama administration and the EU moved towards an aggressive tightening of sanctions. Within a year you can see the impact in Iran’s GDP per capita figures. The nuclear deal of 2015 brought some relief, but with the maximum pressure policy of the Trump administration from 2018 onwards the decline resumed.

Cameron and I discussed Iran’s situation on Ones and Tooze. In that discussion I made a mistake. I claimed that Iran’s population growth was rapid. It is not. It is weird. Population growth surged in the 1980s, producing a youth bulge, but it is now as low as 1 percent per annum. That bulge accounts for the chronic problem of unemployment.

The latest round of sanctions initiated by Trump have delivered a severe blow. Over the winter of 2017 the news of Trump’s new stance, combined with domestic resentment over price increases to trigger something like a comprehensive crisis of the regime. There was a shock devaluation and inflation surged. Today, at 40 percent, inflation remains the most acute economic problem facing Teheran.

As a backgrounder on the current Iranian economic situation I found this videoed conference interesting. As the speakers in this session make clear, the impact of sanctions is severe, but Iran does not face immediate collapse. Oil is an important part of the Iranian economy, it drives exports and investment and tax revenue. But even when oil prices are high, it accounts for not more than 10% of GDP. Furthermore, under the pressure of sanctions Iran has moved up the value chain. It can now export not just crude but petroleum and diesel, which gives it considerable leverage with its cash-strapped neighbors.

Iran, in short, is not Iraq, which is a caricature petrostate with a vastly overgrown public sector that serves as the fiefdom of rival factions, many of which also command powerful armed militias. The combination of COVID and the collapse in global oil prices triggered a moment of existential crisis in Iraq in 2020. The failed development of the last decade was cruelly exposed. The upshot was an apocalyptic assessment by a team of experts delivered in October 2020 in the form of a White paper report.

Non-oil tax revenues in Iraq amount to a laughable 1.4% of GDP, compared, for instance, to 27.8 or 30.%% in Angola or Algeria. Other than oil, Iraq has no exports to speak of. Crude oil exports account for 95 % of Iraq’s exports, compared to c. 60% for Saudi Arabia and Iran. Iraq’s labour productivity record over the last half century is one of the more shocking graphs you are ever likely to see.

A panel on Iraq’s economic situation posted to youtube in January 2021 by Chatham House delivered a remarkable sense of urgency. It is also, however, a historic document. The reform demands of the White Paper were always exorbitant and since then the immediate pressure has been lifted by the resurgence of oil revenues. The upshot of a more recent LSE panel chaired by the excellent Chloe Cornish of the FT in September 2021, was that so long as the oil revenues continue to flow, so will Iraq’s lopsided political economy limp along.

Iraq remains a disaster waiting to happen. Where this has registered most recently on Western radars is in the appalling scenes on the Belarus and Poland border. Of the 16-17000 people stuck between the two East European countries, between 7,500 to 8,000 are from the Kurdistan region of Iraq, thousands of miles to the South.

The Kurdish region of Northern Iraq (KRI) under its own government (KRG) was once a safe haven. Of its 6 million inhabitants one million are refugees mainly from other parts of Iraq but also Syria. But in recent years the KRG has faced deteriorating economic conditions forcing salary cuts for its one million civil servants and austerity. This in turn is a spillover from the national financial crisis in Baghdad, brought on in 2014 by the collapse of oil prices. This produced a 90% drop in financial transfers from the central government to the KRG. The simultaneous upsurge of ISIS and the collapse of oil prices in 2014 was a perfect storm. Added to which, KRI politics is dominated by brutal and increasingly repressive infighting between two parties: the Barzani family-led Kurdistan Democratic Party (KDP) and the Talabani family-led Patriotic Union of Kurdistan (PUK). Meanwhile, the SIS threat remains acute, particularly in the “disputed areas” between Erbil and Baghdad, …. According to a KRI spokesperson, most of the Kurdish migrants fleeing to Belarus hail from the “disputed areas” as well as Duhok Governorate, where conflict between Turkey and the Kurdistan Workers’ Party (PKK) continues.” Recent Turkish offensives against the PKK in the region have caused damage in over 800 villages in the KRI.“

The struggles across the Kurdish region of Iraq are one example of the pattern that repeats in Syria and Lebanon. Powerful external players – notably Iran and Turkey – maneuver violently for influence in zones of failed or fragile states.

Lebanon was once a safe haven in the region, but since 2018 it has been dragged down by disaster. It is hard to overstate the scale of this collapse. In the spring of 2021 the World Bank reported that: “The Lebanon financial and economic crisis is likely to rank in the top 10, possibly top three, most severe crises episodes globally since the mid-nineteenth century … Lebanon’s GDP plummeted from close to US$ 55 billion in 2018 to an estimated US$ 33 billion in 2020, with US$ GDP/ capita falling by around 40 percent. Such a brutal and rapid contraction is usually associated with conflicts or wars.”

Financial incontinence on an epic scale, corruption, factional infighting, macroeconomic imbalances suspended in mid air, Lebanon’s economy, borders on the surreal. But the effects on the ground are devastating. A society once fabled for its wealth and cosmopolitan culture has been reduced to hunger and acute shortages of essentials. And the situation is getting worse by the week.

In November, the near total collapse of the electricity supply have forced the US and the World Bank to stitch together an emergency program to supply Lebanon, once the financial and cultural powerhouse of the region, with gas from Egypt and electricity from Jordan.

The embarrassment for Washington is that to build a rescue platform for Lebanon it is hard to avoid going through Syria, itself in ruins following a decade of brutal armed struggle. Since 2018 the fighting in Syria has calmed, but the economic situation is disastrous. It reached a peak of intensity in 2020 when the announcement of a new wave of Congressionally-backed sanctions – “the summer of Ceasar” – triggered a panicked devaluation of the Syrian currency. The impact of the new wave of sanctions is unclear, but the collapse of the currency, on top of the COVID shock dramatically increased the pressure on the Syrian population. It was, as one particularly compelling report put it, a perfect storm.

As the Assad regime tightens its grip, the battle for influence continues. Iran spent between $20 and $30 billion backing his regime during the decade of armed conflict and would like to see a return on its investment. But Iran is hobbled by sanctions and lacks the cash to compete with Assad’s new friends in the Gulf. As Amwaj comments: “UAE’s entry as a regional economic giant into the Syrian market will push Iran further to the sideline, considering actions like Abu Dhabi’s promise to build a solar plant near Damascus”.

In Syria, the last remaining resistance stronghold is the starving and freezing enclave in Idlib, home to about 4.4 million people, about half of them refugees. About 75 percent of Idlib province residents are in need of humanitarian assistance. Their one land-connection to the outside world is the Bab al-Hawa border crossing to Turkey, effectively controlled by the Islamist HTS.”

In 2019 as the Lebanese economic crisis escalated, the Syrian pound began to collapse, destablizing Idlib’s precarious economy. In the summer 2020, in search of a financial lifebelt, the Islamists introduced the Turkish lira as the new currency throughout Idlib province. They did so just in time to avoid the precipitate collapse of the Syrian currency following the US sanctions announcement. As a result, prices in Idlib province did stabilize for eighteen months, only for disaster to strike again, this time from across the border to the North.

In 2021 Erdogan, Turkey’s capricious President embarked on his latest confrontation with the financial markets and Idlib’s Turkish currency anchor was torn loose. When the Turkish lira was introduced as a means of payment in Idlib in 2020, the exchange rate was 6.8 lira for one US dollar. As of December 1 2021 it had crashed to 12.9 lira. The result was a savage spike in living costs as the price of imported fuel surged.

Turkey’s rollercoaster financial ride through 2021 is the clincher in the crisis narrative of Western Asia. Turkey is a major geopolitical player (in Libya, Syria, Iraq, Azerbaijan-Georgia). It is a contender in Eastern mediterranean energy politics. It is the key to one of Europe’s refugee crises. It is a major regional power. Its destabilization would have huge regional implications.

But amidst all the crisis talk we also have to put Turkey’s situation in perspective. Since its last major financial crisis in 2001, Turkey’s per capita income, in PPP adjusted terms, has tripled. That remarkable growth is the foundation for Erdogan’s legitimacy. It is also that track record that has given Turkey’s its financial staying power. Seemingly, no matter what Erdogan does, the investors ultimately come back. Since 2018 Erdogan has been flirting with disaster. The question for the months ahead is whether this time Erdogan has gone too far. Inflation in Turkey is accelerating. There has been a huge shock to imports that will generate a current account surplus but also inflict pain on the population. Can Erdogan survive once again?

***

I am acutely aware that a survey like this cannot really do justice to the complexity and drama of the terrain it surveys. The drama and complexity of this region is mind-blowing. In the mean time, a scrapbook may be helpful in orientating ourselves in the flow of daily events. It provides a framework for thinking about the interconnectedness that defines major world regions. It may help to focus our attention on the extraordinarily acute crises facing the populations of Afghanistan and Lebanon, the responsibility of the United States and its sanctions policies in Syria and Iran, and the responsibility more generally of richer and more capable states to act where necessary to relieve humanitarian disaster.

December 3, 2021

Ones and Tooze – How Sanctions Work (and Why They Often Don’t)

Representatives of Iran, the United States, and European countries met this week in Vienna for more talks on reviving the 2015 Iran nuclear deal, but all sides seemed doubtful that an agreement could be reached.

On Ones and Tooze this week, Adam Tooze and Cameron Abadi discuss the toll U.S.-led sanctions have had on Iranians for much of the past decade—devastating the country’s economy but failing to curb its nuclear program.

Also on the show: The travel and tourism industries accounted for a whopping 10.4 percent of GDP worldwide. Then COVID-19 came along.