Adam Tooze's Blog, page 30

November 3, 2021

Chartbook #49: Global bond market turmoil 2021 – an explainer.

In 2020 COVID unleashed a gigantic financial and economic shock. Shutdown chronicled the desperate struggle to manage the implosion in financial markets and put workers and businesses on life-support. As the uneven economic recovery from the COVID shock continues, the headlines have been dominated by supply-chain issues and price increases. The energy crisis has bubbled up. There are fears that what were once seen as transitory price adjustments may become a self-sustaining inflation. Will we face a comprehensive cost-of-living shock? Might that spill over – Gilets-Jaunes-style – into politics and society? On top of those concerns it has become clear in recent weeks that we must now reckon with a further line of pressure – mounting stress in the financial markets. The bond markets are back to haunt us.

In the last days of October, as attention was focused on the run up to COP26, trouble at Evergrande, or the battle to clinch a deal on Capitol Hill, bond markets had one of their “wildest weeks in decades”.

In markets around the world, bonds have sold off. As prices fall and yields rise, this inflicts losses especially on holders of longer-term bonds. Meanwhile a fall in short-term rates puts pressure on the yield curve.

The yield curve (which maps the way yields vary between short and long-term bonds) normally slopes upwards from short to the long end. A sharp sell-off at the short end flattens the yield curve. Indeed, some exotic parts of the US yield curve – 20 v. 30 year Treasuries for instance – have actually inverted. You get more money lending to the US government over 20 years than if you lend over 30. This is the opposite of what many speculators were reckoning with. Many funds that were gambling on the yield curve to steepen booked substantial losses, adding to painful sense of uncertainty. There have been ominous signs of liquidity drying up.

The headlines are graphic: “Bond rout”; a Nixon moment;

The Bond Market Is a Powder Keg

********

Bonds are less attention-grabbing than brand-name equities, which over the same period have surged to record levels. But the government bond market is vast. $87 trillion as of September 2020.

Source: ICMA Group

The attractiveness of government bonds is dictated not by industry trends or corporate strategies but by general macroeconomic conditions – inflation, currencies, growth etc. The fate of public debt is tied directly to government finance and thus explicitly political. The bond markets are also preeminently the domain of central bank intervention.

When intense selling pressure built up in bond markets in March 2020, the Fed and other central banks stepped, buying trillions of dollars-worth, to stabilize prices and interest rates. This was crucial because bonds are not just the means to raise funds for the government, they are the basis for trillions of dollars of private speculation.

Having stepped in to catch a falling economy, the question in 2021 is how long the central banks can continue their interventions. Since June 2020, the Fed has been buying $80 billion of Treasury securities and $40 billion of agency mortgage-backed securities (MBS) each month. With the economy recovering strongly and prices rising, the question is, when will the major central banks reduce their purchases?

With prices set correctly, the market can live with any inflation and policy scenario. But the question is what to expect.

Inflation is a particular threat to fixed-income assets that pay a fixed interest coupon not dividends. All else being equal, the expectation of higher inflation makes bonds less attractive. Furthermore, central bank interventions have since the spring of 2020 been dominating market movements. Every morning at shortly after 10 am in New York, large purchases begin, setting the direction for the day. Markets could be confident of a large bloc of demand for bonds. But, if inflation surges, central banks will find it impossible to continue with purchases. Price stability remains a key priority for central banks. If they are no longer buying on the same scale, bond prices will fall and yields rise.

There are thus two different motives for a selloff. One driven directly by the investors’ calculations of the likely rate of return. The other driven by investors’ expectations about the likely behavior of the central bank.

Until recently, the expectation of the markets following dovish communications from the central banks, had been that the Fed and its colleagues would be slow to respond to inflation. A degree of overheating is acceptable within the new central banking policy framework of average inflation targeting. A major factor driving the turmoil of recent weeks has been a reevaluation not just of inflation, but of the likely reaction of central banks to the price increases. The central banks seemed to be moving in a more hawkish direction, suggesting they would end bond purchases sooner and there might even be rate rises on the horizon. That would make it less attractive to hold short bonds (on account of higher inflation expectations) and more attractive to hold long bonds (on account of lower inflation in future) thus flattening rather than steepening the yield curve.

The central bank, for its part, must take price stability seriously, but it must also reckon with the bond markets. It will not want to be seen to be dragging its feet. On the other hand central bank action to withdraw support just as bond investors are selling and driving yields up, risks strangling the recovery.

**********

What is playing out in the markets right now is a hugely delicate rebalancing towards the expectation that current inflation is more serious and more long-lasting and that central banks will likely respond more vigorously and hawkishly than expected.

As John Authers sums up the situation: “it was in October that financial markets switched from nonchalance about inflation to instead try to pressure central banks toward raising rates.”

The focus of attention is on the Fed. The US Treasury market is the anchor of the whole system and the Fed the most important central bank. Today, (Wednesday 3 November) all eyes will be on the FOMC as it concludes its meeting to discuss the future course of policy.

But the logic of bond markets ties much of the world into an interconnected system. It is telling that signs of bond market stress did not start in US, but in the emerging markets (EM). IIF @IIFNEW: Capital Flows Tracker for August data sees flows slow to a trickle, with portfolio flows to EM standing at $4.3 billion in August. Full report: ow.ly/Cgsc50G74Rz

September 9th 20212 Retweets3 Likes

All year, the EM have been living under the shadow of an anticipated tightening in monetary policy by the advanced economy central banks. If the Fed tilts strongly in a hawkish direction money will flow back to the US to take advantage of the better yields. For several months, bond markets around the EM have seen lower prices and rising yields.

The core-periphery relationship is powerful. But it is also one-way. The EM import pressure from the AE. They do not transmit it to the same degree.

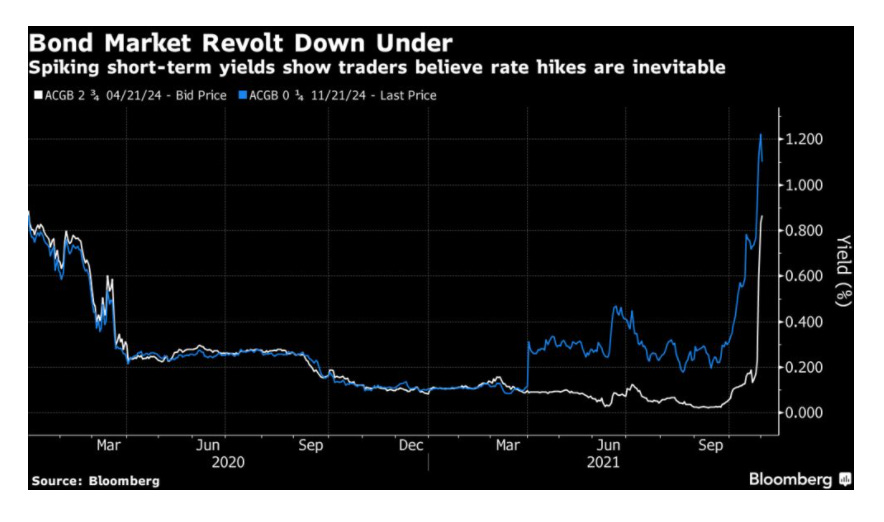

In the last few weeks what we have seen is another dynamic playing out. In rather an unusual pattern, selling pressure in Canada, Australia and the UK has set the pace. This in turn is blowing back on the US.

Canada, Australia and the UK are not “peripheral” to the global financial system in the sense, for instance, that South Africa is. What they have in common is that they are medium-sized advanced economy monetary sovereigns. They have the confidence and authority of advanced economy monetary and fiscal actors, but they are exposed to a full set of inflation, interest rate and exchange rate risks. They are small-scale analogues, you might say, for the US.

Last week, Canada abruptly stopped it QE program. Australia abandoned the defense of a low interest rate.

As Authers describes it:

Most spectacularly last week, traders bet that the Reserve Bank of Australia, which has long targeted keeping three-year bonds, due in April 2024, to a yield of only 0.1%, would have to abandon a policy in place since March last year. On Friday, the bank gave up intervening to keep the yield close to its target, with dramatic results:

The Bank of England has also been sending strongly hawkish signals.

The news from the Anglosphere sent shockwaves through bond markets globally. So far, the Eurozone has remained reasonably calm. Inflation rates for the eurozone as a whole are relatively muted, as is the recovery. If there is a central bank that seems credibly committed to not tightening too soon it is the ECB. Nevertheless, in the last week, pressure has begun to mount on Italy and Spain.

But the question that comes to a head at 2 pm Eastern Time today (November 3) is how the Fed will declare. The expectation is that it will announce a taper path for its bond purchases but will refuse to commit to rate rises. As chair, Jerome Powell has invested considerable capital in the idea that inflation was transitory. The evidence continues to support that view. What has changed is that the period of price adjustments appears to be more protracted than expected. In the face of market pressure, the Fed is expected to make a staged retreat.

This will be a delicate operation. If the Fed tightens too hard, too fast, it will exert painful pressure on the EM. This was the taper tantrum scenario of 2013. But what will matter more in 2021 are concerns for the health of US equity markets.

Bond market and equities are currently in different worlds. Whilst the bond markets are in turmoil, shares are going from record high to record high. VIX the equity volatility index is at record lows, even as volatility in bond market surges.

If the central banks push too hard, will they bring the house down?

As Robert Armstrong remarks, the fear among many big players in the market is that the central banks will act prematurely. For fear of inflation they will kill the recovery.

With China also applying the brakes, that would imply a major shift in policy stance across the world economy.

As Armstrong sums it up with admirable brevity:

Are the central banks about to do what they have frequently done before, which is to stifle a recovery prematurely?

If one believes that the problems are mainly issues of supply-side bottlenecks and logistical difficulties, using a tightening of monetary policy is a crude way to deal with the problem. Neo-Keynesians like Skanda Amarnath and Employ America are full of smart ideas about how to curb inflationary pressures short of using interest rates to cosh aggregate demand.

Meanwhile, stalking the markets is the fear of something even worse than a premature tightening or spillovers to equities and the EM. The most pressing question is, can the Treasury market take the strain?

**********

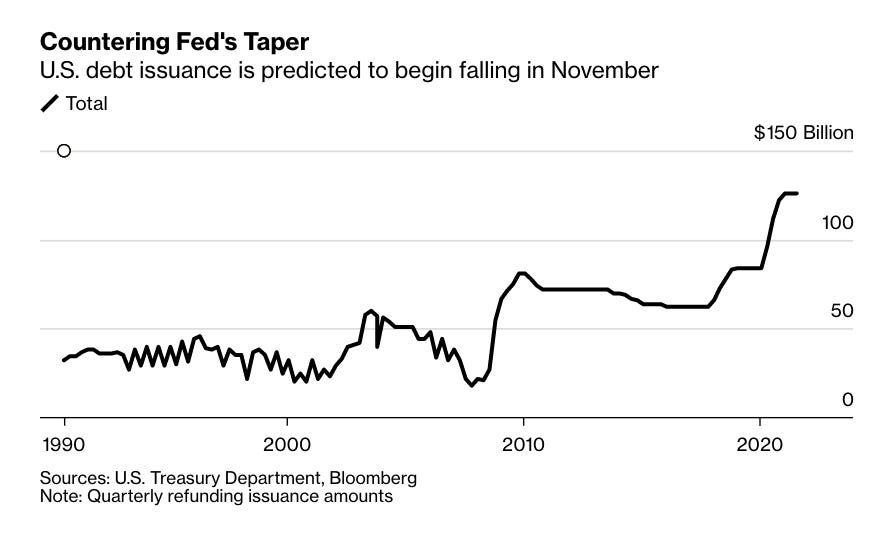

The US market is by far the largest in the world. It is the true hub of the global financial system. When we talk about the dominance of the dollar, what we really mean is the dominance of dollar-denominated Treasuries as reserve assets.

The volume of US Treasuries in the portfolios of private investors is huge and rapidly growing as the US authorities issue more and more debt.

Source: Bloomberg

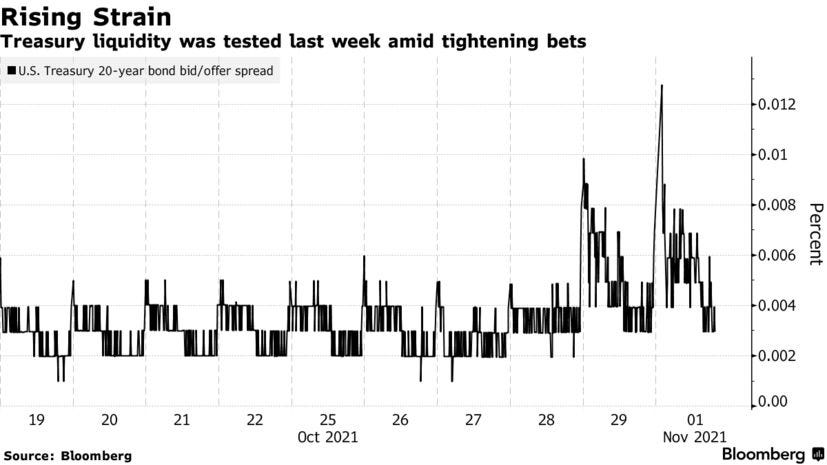

Huge it may be, but the disconcerting realization of the last two years has been that the US Treasury market is also prone to breakdown. Some of the turmoil of recent weeks was due not simply to a shift in macroeconomic and policy outlook. Some of it had to do with malfunctioning of the market. At the short-end liquidity tightened and pricing became erratic.

Nor is this the first time. In September 2019 there was the repo crisis. In March 2020 the market came close to failing. In February 2021 there were a rash of worries as demand for Treasury issuance briefly dried up. And now, in recent weeks we have again seen symptoms of market stress and malfunction.

In the last days of October, big selling pressure did not meet with adequate demand, leading to an alarming surge in the bid/offer spread, an index of market stickiness.

Source: Bloomberg

The mismatch between demand and supply seems to have had two sets of causes.

The sudden and unexpected flattening of the yield curve triggered losses in hedge funds which were betting on steepening. That in turn triggered sell-offs, which put the the market under pressure.

On the demand side there is a suspicion that the so-called primary dealers – the 24 financial firms that are charged by the Fed with providing buy and sell prices for Treasuries – were less than willing to absorb the selling pressure. I have not yet, so far, seen any specific data on this for October. But data for Feb 2021 and March 2020 do show a reluctance on the part of the primary dealers to expand their balance sheets. This is commonly blamed on the Dodd-Frank regulations in the wake of the 2008 financial crisis which force banks to set aside more capital to back their holdings of debt.

Primary dealers are less willing to put huge balance sheets in play to make the repo market work.

Source: FT

As you would expect this is a prime area for industry lobbying:

“The banks never were there to catch the falling knife but they certainly did act as a pretty huge liquidity buffer to the marketplace in a way that they can’t or won’t today,” said Kevin McPartland, head of market structure and technology research at Coalition Greenwich. The Securities Industry and Financial Markets Association, an industry lobbying firm representing big lenders, wrote earlier this year that changing bank balance sheet rules would ensure smooth market functioning. “Some modest loosening of primary dealer balance sheets would likely help reduce these more frequent bouts of volatility, and we would still have a much safer system” than before the financial crisis, said Tyler Wellensiek, global head of rates market structure at Barclays.

The argument against any such loosening is strong. At least in the current situation we do not have to deal with a dangerously unstable and oversized bank balance sheet. As the Financial Times explains:

As primary dealers have stepped back from their market-making role, hedge funds and high-frequency traders including Citadel Securities, Virtu Financial and Jump Trading have moved into their place. But when markets become volatile, high-frequency trading funds also can pull out. Data from Coalition Greenwich show that order-book volume — a large portion of which is made up of high-frequency trader activity — has shrunk during recent liquidity glitches. In March last year, average daily order book volume on a relative basis compared to other execution methods dropped to the lowest level since 2014 and has not fully recovered since.

Source: FT

The system as a whole looks highly unstable. The Treasury market, “is primed so that high-frequency traders and primary dealers pull back when there are problems”, said Yesha Yadav, a professor at Vanderbilt Law School in Nashville who studies Treasury market structure and regulation. “The way this is set up is designed to fail. It is exceptionally fragile,” Yadav said.

Yadav has just put out a Columbia Law Review article on Treasury market structure and its fragilities which I highly recommend. The picture she paints is alarming:

The asymmetric distribution of regulatory burdens between primary dealers on the one hand and high-speed securities firms on the other limits opportunities for private cooperation and mutually reinforces risk-taking behavior by both sets of players. Unwieldy public monitoring, combined with a light-touch rulebook, allows all firms to take risks or trade opportunistically with little chance of detection and discipline. Traders can also cheaply exit the market if something goes wrong, limiting how fully they must internalize the costs of their risky behavior. For the less-regulated, nonprimary dealer firms, the regulatory constraints are even weaker, further increasing their financial incentive to seek risk in Treasury markets. Faced with diminishing profits and a less lucrative franchise, primary dealers are also incentivized to take risks and shirk self-discipline. So, not only is the task of private oversight logistically harder as the number of traders proliferates and diversifies, but it is also problematic when self-policing would result in primary dealers imposing added costs on themselves in a period of fierce competition and lower profits. The consequences of this regulatory neglect in Treasury markets were apparent even prior to the March 2020 COVID-19 crisis, as a number of disruptions over the years pointed to unaddressed fragilities at the heart of this supposedly failure-proof market.

Regulators have discussed making changes to bolster Treasury market liquidity. There have been recommendations also from the G30.

But progress has been slow and the lack of a centralised Treasury market regulator can cause confusion.

Yadev’s first proposal for stabilization would be a binding Memorandum of Understanding between the regulators themselves to create a clearer division of labour between them.

Her second proposal takes up the suggestion from Darrel Duffie for a centralized Treasury clearing house model that would ensure that all major players had skin in the game in ensuring that the market continued to function even at moments of stress.

Others go even further. In the view of Bank of America analysts: “Treasury market size “has outgrown dealer ability to effectively intermediate risk.” This then requires an “official-sector role as dealer of last resort.””

********

What the repeated shocks to the Treasury market have revealed since 2019 is the instability and incoherence of the market mechanisms which govern the trading and pricing of the world’s most important safe asset. Since the liquidity of Treasuries – the fact that you can turn them into ready cash very easily – is part of what makes them into the global safe asset, the fragility of the market is a fundamental challenge.

The current turmoil drives that lesson home.

Advocates of the MMT position will no doubt be moved to remind us that our reliance on government issues IOUs is a matter of choice. There are other ways of funding government. We choose to issue interest-bearing IOUs and to allow a market for them to exist.

This is, indeed, a crucial insight. Unfortunately, it does not follow that ending the system and replacing it with something radically different is plausible politics. But it forces the question of how we organize this market and how we distribute the profits and the risks.

After the series of shocks we have witnessed in recent years, we should do so proactively, before we are forced to do by an even more serious crisis. The market can no longer claim to be autonomous. It moves with speculation about Fed interventions and the slightest word from the central bank. Since the Treasury market is already a creature of policy. Let us tame it. Whatever policy stance and whatever policy mix we choose, if we are going to have a market-based public debt system at the heart of the global financial system, let us make it a solid platform.

October 31, 2021

Chartbook #48: The first climate Kalecki moment – the politics of energy crisis talk

As the G20 and COP26 convene in Europe, there is crisis talk everywhere.

The climate crisis is front and center, of course.

But, in the weeks before the summits convened, another crisis surged to the top of global attention.

We are – we are told – living in the midst of an “energy crisis”.

Oil has surged above $ 80 per barrel, its highest price since 2014. Gas prices in Asia have spiked at the equivalent of over $ 300 per barrel. In the UK, a dozen retail gas suppliers failed, leaving 2 million households in limbo, uncertain who would be supplying their homes.

Since hitting peak anxiety in late September to early October, the panic has eased somewhat. But, last week President Macron warned of an energy crisis. And, at the G20, Bloomberg quoted Amos Hochstein, Biden’s top energy diplomat, as saying, “we found ourselves in an energy crisis”. According to Bloomberg, this is a“broadly held view by big oil consuming nations”. In the context of the G20 that means Japan and India. In a thirty-minute State Department briefing on October 25, Hochstein used the word “crisis”, 11 times.

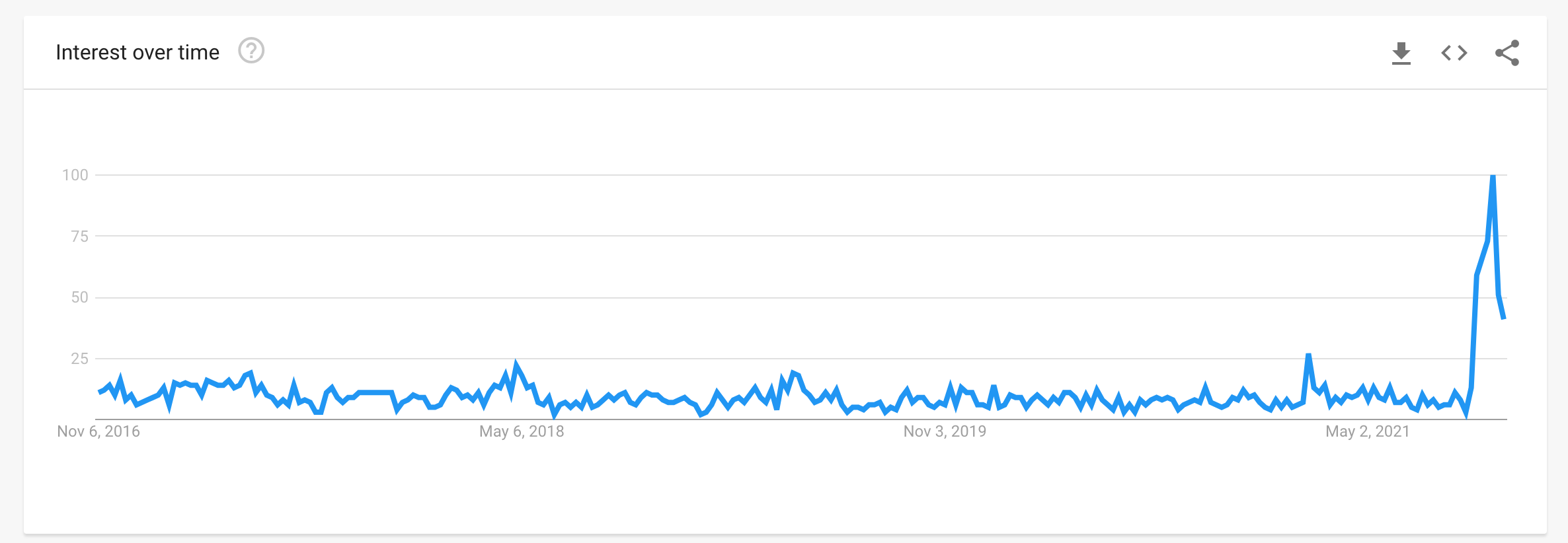

Meanwhile, google searches of “energy crisis” are at a five-year high. And stagflation is one of the hot memes on the terminals.

Source: Google Trends

The point of emphasis is different depending on where you are in the world. In the US, as ever, the main preoccupation is petrol prices. In the UK and Europe the main worry is gas. At the G20, the US apparently ganged up with Japan and India to pressure Saudi and Russia to raise oil production.

But, how seriously should we take this talk of “energy crisis”?

************

The evidence for an interconnected energy crunch of a structural kind is not strong. Columbia’s energy policy unit headed by Jason Bordoff, ex of the Obama administration, has published several reports pouring cold water on the idea of a general squeeze. So has the CER.

What is particularly contentious is the idea that this price-surge has anything to do with a big push to net zero.

The argument goes as follows. Net zero ambition has shaken confidence in the fossil fuel sector. Investors who lack confidence in the future of their industry don’t invest. Lack of investment means that we don’t have the capacity to deal with surges in demand. Behind the energy price volatility, on this very contentious reading, lies an investment strike. The implication is obvious. To avoid further spikes in energy prices, we thus need to back away from radical net zero policies and build some extra gas capacity, as a transitional solution.

How dangerous this kind of argument is, how little we can afford to make any concessions to the gas lobby right now, is brought out by the recent batch of graphics showing the vertiginous path of decarbonization to which we have condemned ourselves.

Source: Carbon Brief via Open Democracy

For good reason, this transparently self-serving idea has been attacked on Bloomberg, the Washington Post, by the IEA and indeed by Hochstein of the Biden administration who insisted that his talk about an energy crisis should not be misread. It has nothing to do with a push to net zero.

As Hochstein puts it:

“there is this notion out there that – I would say a false notion that ties the current crisis to the energy transition. And I want to be very clear. There is – the energy transition is not what caused this crisis. There are a number of contributing factors. But some of the leading factors – not all of them, but some of the leading factors have to do with global weather patterns that have significantly affected the energy system. We had a drought in China and a drought in Brazil that affected hydropower in a fairly significant way. We had hurricanes in the Gulf of Mexico that affected deliveries into Europe, two of them in fact back to back. We’ve had fires. So the weather pattern – the climate is changing. We are in a climate crisis. And in fact, if I learn anything from this crisis that we are facing – and I think it’s a real crisis, right, because oil prices are extremely high, coal prices are high, natural gas prices are high; this is having an impact of a chain event on other metals production where prices of metals are going up; those are inputs into renewable energy.”

***********

So what is going on? In the New Statesman this week I argued that we are facing a new kind of crisis – a political crisis of the energy transition. The real effects of the energy transition are as yet modest, but the politics are already live. The fightback by the gas lobby is in full swing. It will be one of the big struggles of the next decade.

In making the case, I invoked the left-wing Polish Keynesian Michał Kalecki to argue that crisis-talk is being instrumentalized for the defense of business interests.

In 1943, just as Keynesian thinking began to take hold in government in both the UK and the US, Kalecki made the prescient argument that faced with the new government activism, the business lobby would retreat to a defensive position. At the depths of a cyclical downturn they would welcome state intervention to rescue the economy. But as government spending built up, labour markets tightened and employer control both over their factories and the agenda of economic policy was challenged, the same business lobby would resort to arguing that excessive government spending and big deficits were bad for confidence. Lack of confidence in turn impeded investment and growth. Talk about “confidence” would thus become the battleground for an effort to preserve an “equilibrium” of unemployment. Confidence I take to be the flipside of crisis-talk in our current moment.

Kalecki with his Marxist background realized that even as the technocratic vision of a government-managed economy emerged, it would face powerful opposition. Full employment, as promised by Keynesians, would never be achieved. The world would remain in Kalecki’s words in an “artificial restoration of the position as it existed in nineteenth-century capitalism”.

The analogy to climate change is not perfect. The climate crisis is not generated by cyclical swings, but by the growth process itself. But Kalecki’s analysis of the confidence game played by business lobbyists is prescient. And the vision of being trapped in an “artificial 20th century of fossil-fuel-dependence” by the rearguard action of business, is haunting.

For those reasons I think we should dub 2021 the first “climate Kalecki” moment. It should go alongside the “climate Minsky” moments we have been learning to analyze in the sphere of macrofinance. This may be our first but I wager that it will not be our last climate Kalecki moment.

Clearly, diagnosing the situation in 2021 is important. But the broader issue at stake here is how technocratic strategies of economic management – whether with regard to employment energy transition – can actually be brought to bear in a political economy riven with contradictions and conflicting interests. And in particular what role the diagnosis of crisis plays in such a setting.

The argument in the New Statesman article is directed against business lobbyists and their claque. But it also marks a point of difference to some folks on the left who are trying to make sense of the current conjuncture.

*********

One of the left intellectuals I most consistently enjoy reading is Richard Seymour. For anyone who enjoys a blend of Marxism and psychoanalysis, his Patreon account is highly recommended. Seymour is also one of the leading lights at Salvage magazine.

Seymour has done two interconnected newsletters on the current moment. One of the energy crisis. One for the opening of COP26.

Contrary to the line that I have adopted in the New Statesman, Seymour argues that though the symptoms of stress in energy markets may be dispersed, the crisis is fundamentally deep and real. As he says, crises often take this form.

“One problem. This is how structural crises always manifest themselves: as moments of intense overdetermination, gatherings of apparently unrelated shocks.”

The key reference here is to Althusser’s 1962 essay on overdetermination. (NB this is a TRULY dense work. Not for the fainthearted.)

Nor, in Seymour’s view, is the reemergence of a real crisis to be regretted, because it is at such moments that elite consensus come apart, the climate movement gains real purchase and can force a change in agenda. This is a classic Marxian idea, that out of crisis, moments of emancipation emerge.

Or as Seymour puts, it: “As a moment of intense overdetermination, this situation is also a moment for political intervention … it is in the nature of crises that the ruling class doesn’t have to get everything its own way.” “Like all successful movements, they have exploited and collaterally benefited from crises that are not directly related to their issue. The strategic and sectional divisions within the ruling class can usually be prised open by militant movements”

As Seymour argues, the current moment in climate policy may disappoint the movement, but against the backdrop of what is to be expected, it has to be understood as a triumph:

“the problem to be explained is not ‘failure’. Failure would be the default, the normal state of affairs. The odds are stacked heavily against human survival. What needs to be explained, particularly if we want to know what to do about COP26, is success. For, as I’ve said, despite the forces arrayed against us, the legal and consensual parameters of climate action have shifted. Three big waves of environmental action –– the movements of the late 1980s, the action around COP15 and after, and the upsurge of school strikes and direct action since 2018 –– have combined with improving climate science, the growing economic costs of climate change, and alarming droughts, wildfires and extreme weather events, to force the environment up the agenda. ….

Climate protest has forced the fossil industry to junk its overt denialist apparatuses and pretend to be green. Most big businesses crave association with the rising ecological consciousness …

Capitalist states overwhelmingly accept ‘the science’ and, with the use of increasingly efficient renewable energy sources and the ‘transitional’ fossil energy of natural gas, some overdeveloped states have begun to cut emissions.

In the last decade, the Green New Deal has gone from being a marginal concern of some economists and ecologists to being a globally mainstream policy idea. The Biden administration has embraced some of the policies of the Left ….”.

All of this is true and I agree, it is utterly surprising. But what about the current moment? What about the relationship between the energy crisis and this struggle between social movements and power.

In this regard Seymour remarks:

“A far-sighted ruling-class response”, to the current energy crisis, “will probably be to accelerate the transition to renewables and more energy-efficient buildings, transport and supply chains. There may even be competition over who transitions fastest, and trade wars over rare metals. But the point will be to continue to expand, in perpetuity, the extraction of human labour and the metabolisation of the natural environment.”

The problem that Seymour sees is not in the energy crisis as such, but in the successful realization of green-washed coping strategies. These new growth model will be badged green and sustainable. But they will, in fact, “accelerate the ecological crisis eroding even the material infrastructure of capitalism.”

It is here that we differ. Remarkably, if I read him correctly, Seymour is more sanguine than I am. He seems to be suggesting that thanks to the pressure on its flanks, green modernization is now mainstream and so the energy transition, despite all the current crisis talk, is unstoppable. I am more worried.

This you might say is simply a judgement call. We may differ in how we assess the vigor of the fossil-fuel rearguard. It may be a matter of a European and an American perspective. But I actually think it opens up a bigger issue, which is how we think crisis and its impact on the balance of political forces.

In Seymour’s analysis, crisis is an opening. I am not so sure.

In the recent political economy of both the US and Europe, crisis has all too often been a generator of compulsive and highly conservative logics. Think of “too big to fail”, or the threat of bond market vigilantes, invoked to impose austerity. Or the meltdown that we saw in financial markets in 2020.

Out of a diagnosis of crisis, threat, insecurity, slippery slopes, tipping points, a powerful case for conservatism has been fashioned. Is this not what is happening in 2021 too? An attempt is being made to declare the fossil fuel energy system too big to fail. If you let us go, then the supply of gas and electricity to main street will either fail or become exorbitantly expensive. That is the threat that we have to face down.

*********

I’m a self-confessed liberal Keynesian. My kind of politics, focused on present-minded crisis-fighting no doubt predisposes one to downplay the structural elements in a moment of tension like the one we are currently living through. (Yes I can hear the echoes of Anderson’) It predisposes one to focus on the contingent factors and to seek to disaggregate different lines of causation that are in play so that they can be addressed in a targeted way. That is what I am advocating in the New Statesman article. But, I would insist, my skeptical debunking approach to energy-crisis-talk is not picked out of thin air. It is based in a strategic assessment and a structural diagnosis of the challenge we face. It is based, by way of Kalecki, in a structural reading of the interests that crisis-discourse serves and the need to resist the confidence tricks with cool heads and sharp analysis. Above all it is orientated towards the dynamic, constantly evolving challenge of the energy transition.

Given the drama of this graph, there is no need to exaggerate our difficulties.

Source: Carbon Brief via Open Democracy

*********

If you would like to support the Chartbook project, there are three subscription options:

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.October 30, 2021

Ones and Tooze: the COP edition

This week on Ones and Tooze, Cameron and I give you a run down of COP26.

Get the podcast here:

Next week marks the start of COP26 in Glasgow

— Ones and Tooze (@OnesandToozePod) October 29, 2021Listen to today's episode of #OnesandTooze to hear why @adam_tooze is optimistic ahead of the climate summit:https://t.co/yX1kFSGCIC

One factoid I wish I had known ahead of time is COP26’s own carbon footprint:

Apparently, of COP26’s estimated 53,374 tons of carbon footprint, 45k are for air travel. Source: FT

The second segment in the podcast is on global food prices.

I covered this story in Chartbook last week.

This morning I read in the FT that the ripple effect is spreading through the food chain. The FT has compiled a “cost of breakfast”-index consisting of futures prices for coffee, milk, oats, orange juice and wheat, it has surged 60 percent since its low in the spring of 2020.

On top of the harvest failures in Brazil, we have other climate issues to deal with:

”Oat prices, meanwhile, have doubled this year after a severe drought in Canada wiped out almost half of its crop. As the world’s largest oat producer and exporter, Canada’s oat production drives global trade, and this year its crop shrank 44 per cent, according to Gro.” Oats are at an index value of 240 relative to 100 in the summer of 2020.

October 27, 2021

Why the so-called “energy crisis” is both a threat and an opportunity

When it comes to the politics of energy and the climate it can seem as though we are living inside a kaleidoscope. In April 2020 Covid-19 sent oil futures tumbling into negative territory. In May this year, global oil companies were on the run, as ExxonMobil’s diehard management were humiliated by activist shareholders when they demanded that the company take action on climate change. Now, only a few months later, the oil price is more than $80 per barrel for the first time since 2014. With gas and coal also in short supply, the talk is of a “global energy crisis”.

In the UK the sense of panic is particularly acute. Brexit amplifies the uncertainty. But tensions are rising worldwide. In Beijing and Delhi, Brussels and Washington, DC, surging prices for coal, oil, gas and carbon permits are causing alarm in governments and chancelleries. A ripple effect is running through the global economy. As the prices for oil, gas and coal increase, so do the prices of everything that is made out of them, such as fertiliser. That, ultimately, adds to the price of food. Before long, an energy crisis may become something more comprehensive and more politically dangerous – a cost of living crisis.

Fear of stagflation – a combination of low growth and high inflation – haunts the terminals. On this telling, the world is facing a historic rerun of a 1970s-style “energy shock”. Except this time the crisis is not blamed on the Organisation of the Petroleum Exporting Countries (Opec) but on a premature and ill planned push for decarbonisation.

Thanks to crowd-pleasing green policies, so the narrative goes, we are being starved of gas. To some conservatively inclined commentators, the pursuit of net zero appears as a new totalitarian ideology, a “religious-like” cult of state-planning that will impel societies towards global hunger and mass death. According to the head of one influential energy advisory firm, “as with so many previous, state-led utopian revolutions in the 20th century, the road to a promised utopia [in this case ‘net zero carbon’] is littered with the likely reality of a dystopian nightmare”. Apparently, the spectre of Stalin’s famine in 1930s Ukraine is lurking on the horizon.

Read full article at The New Statesman.

“It Would Be a Mistake to Grant Him His Wish”

From the coalition negotiations in Berlin so far, two things are clear: The Traffic Light coalition – so named because of the colors associated with the parties involved – is the government Germany needs right now. The three parties – the center-left Social Democrats (red), the business-friendly Free Democrats (yellow) and the Green Party – balance reassurance and innovation. They can readily agree on a new language on language, on immigration, on rights. But, as many feared, the common denominator of the three parties is low. On climate, the message in the paper that emerged from the initial exploratory talks is alarmingly weak. The same goes for the promises on the digital backbone. The language on European policy is not promising either.

The risk is that, though the Traffic Light coalition seems doomed to succeed, it will be a weak government that struggles to meet the challenges of the moment. This means that who gets the top jobs matters. Strong ministers with good staff can make a big difference. The best demonstration of that is Olaf Scholz himself, who has served as German finance minister since 2017.

Under Scholz, who will end up in the Chancellery if the current coalition negotiations find success, the Finance Ministry went from being a brake block to being a driver of change. It delivered a substantial surge in public investment, beginning to make up for the deficits of recent decades. It opened the purse strings at the critical moment in 2020, enabling German society and the economy to get through the shock delivered by the coronavirus crisis. Scholz and his team should care about their legacy at the ministry. They made a huge difference. As the Greens must realize, there can be no serious climate policy without control of the Finance Ministry. It is the number 2 job in the government. As the number 2 party, the Greens should hold it. With Green party co-leader Robert Habeck as finance minister and his party ally Sven Giegold as parliamentary secretary of state in the Finance Ministry, they would have a plausible leadership team.

Read the full article at Zeit Online.

October 24, 2021

Chartbook #47: Crisis Talk – Global Food Prices

The economic news right now is filled with talk of inflation, energy price hikes and shortages. There is even a mini strike wave. “Striketober” is a thing!

References to the 1970s are everywhere. Stagflation – the combination of low growth and inflation characteristics of the 1970s -has become one of the most searched terms on news terminals.

Personally, I invoke crises a lot. In my new book, Shutdown, “polycrisis” is a key term. But I’m skeptical about this current crisis discourse. Perhaps it is an effect of having recently taught Michał Kalecki’s classic 1943 essay on the manipulative politics of confidence discourse. As Kalecki explains, in economic policy debate, talk of confidence is not innocent. It is a way for business leaders and their spokespeople to set the agenda in economic policy. Who after all is to judge whether business has lost confidence or not. Crisis talk is often the flip side of “confidence” talk. And in the current moment talk of inflation linked to talk of an energy crisis is being wielded against at least two progressive agendas: the Biden infrastructure push and the global push for net zero. It will no doubt soon rear its head in Eurozone fiscal policy debate as well.

I’m going to be coming back to this issue in future newsletters. It is at the heart of a new piece forthcoming in the New Statesman.

I want to focus in today’s newsletter on a particularly urgent issue: food prices

Generally, when we think about the 1970s and early 1980s we think about OPEC, lines at petrol stations, inflation and labour unrest in the US and Europe. Perhaps we might think of the tensions in Eastern Europe that culminated in the declaration of martial law in Poland in 1981. Or, the beginning of the era of Latin American debt crisis.

But from a global point of view, one of the most severe symptoms of crisis in the early 1970s was the spike in food prices, coinciding with starvation and famine conditions in some of the poorest countries in the world.

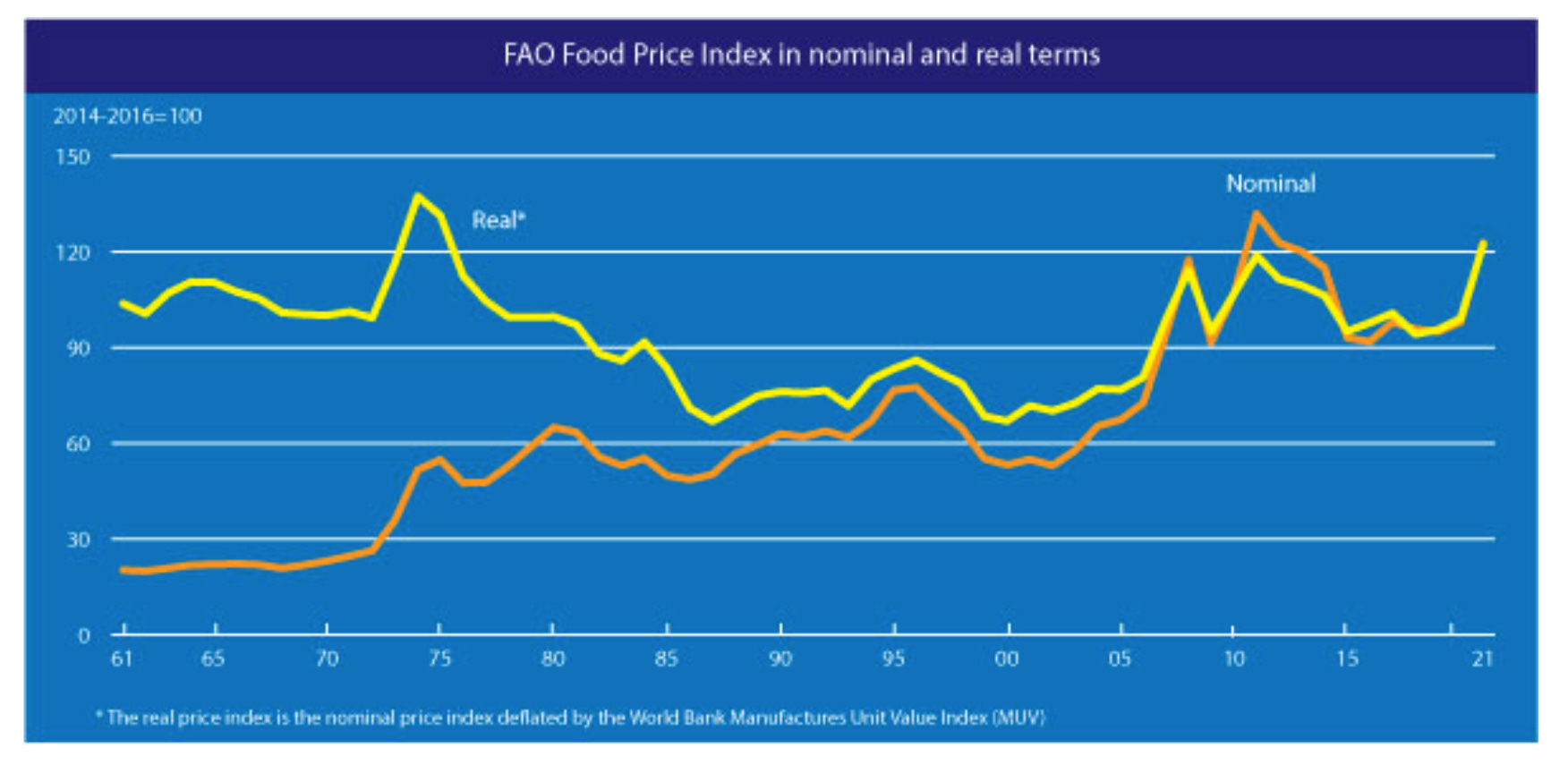

Source: FAO

Over the following decades, from their peaks in the early 1970s, world food prices fell by almost 50 percent in real terms. They did not begin to rise again sharply until the early 2000s, reaching a new peak in 2008 and then again in 2011, just ahead of the Arab spring protests. Increases in global food prices put particularly heavy pressure on food importers. The countries of the Middle East and North Africa are the most dependent on food imports in the world.

Against this backdrop, it was big news in the last couple of weeks when the FAO sounded the alarm. The FAO’s Food Price index indicates that world food prices have surged above their 2011 level and are now at a level, in real terms, not seen since the 1970s.

Source: FAO

“Real terms”, in this context refers to the price of food benchmarked against the price of other goods.

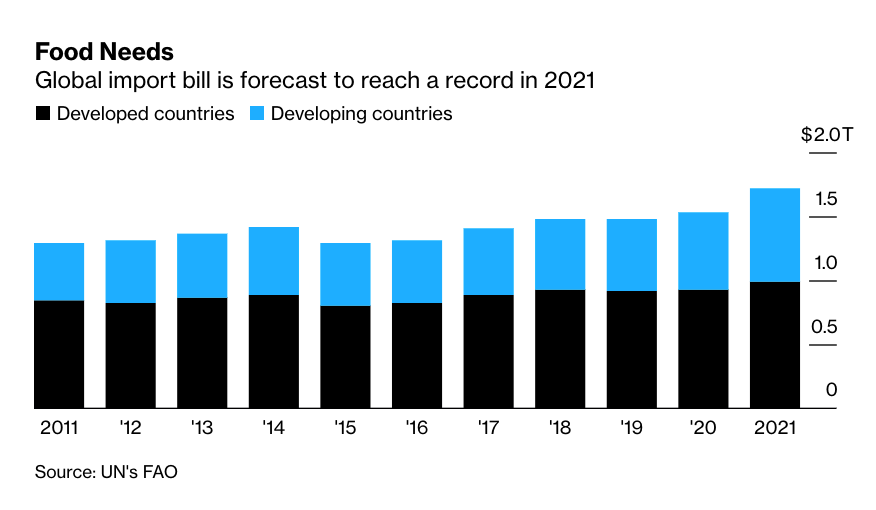

There is no doubt that this is bad very news for poor countries. It will be a matter of urgent concerns for UN agencies. A food price squeeze will compound the devastating impact of 2020 on the world’s poorest. 768 million people — nearly 1 in 10 globally — were undernourished in 2020, up 118 million from 2019.

In a vast redistribution of income, hundreds of billions of dollars will be transferred from low-income and middle-income food importers to agricultural exporting countries. As the FAO reports, developing countries face a 21% jump in the total import bill for food, compared with a 6% increase for the richest ones.

It is a serious situation. And it can appear even more so, if one combines it with the other crisis du jour – the energy crisis.

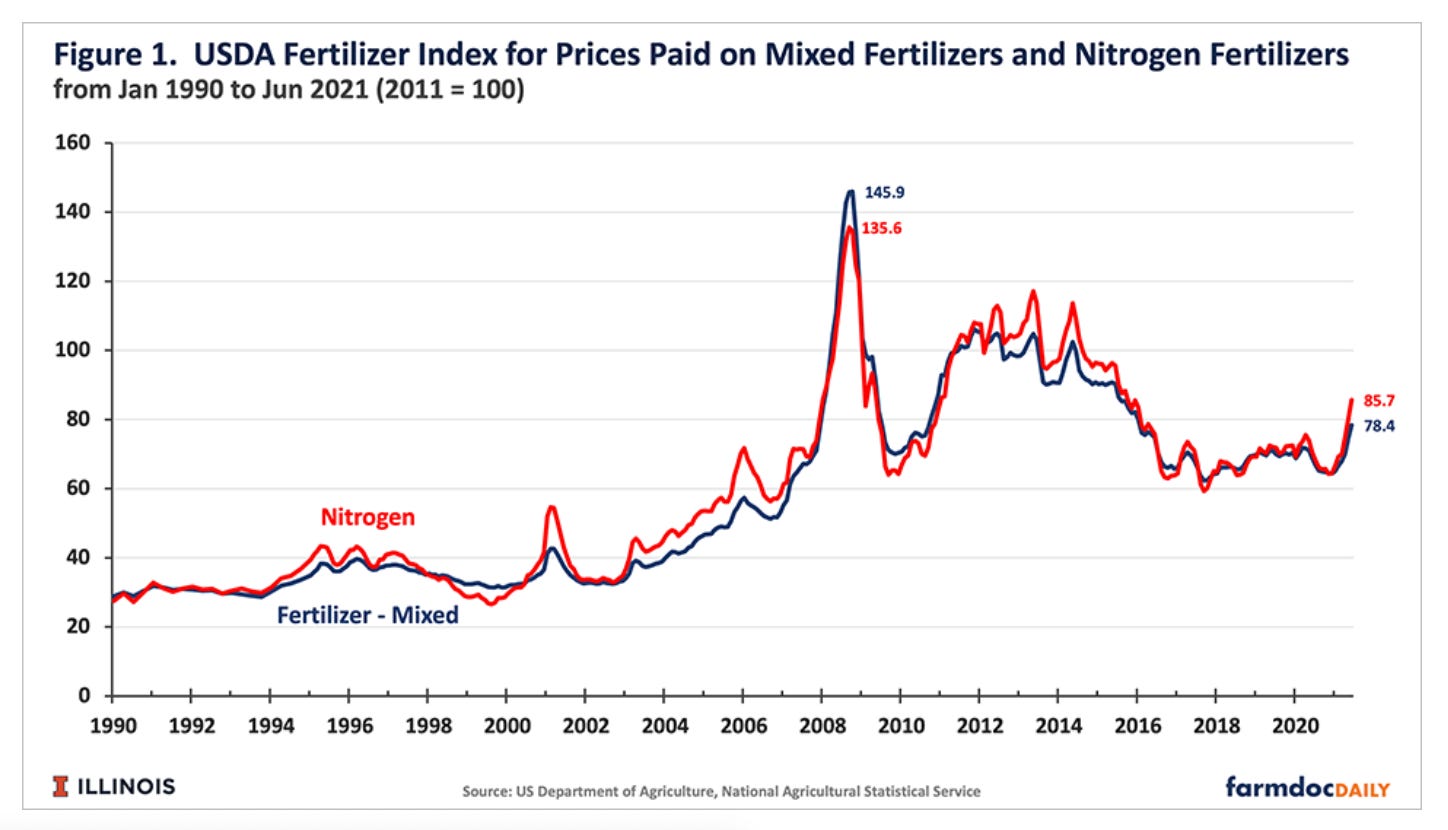

As the saying goes, modern agriculture is a mechanism for turning fossil fuels into food. Not just through mechanized farm machinery but, crucially, through artificial fertilizers. Natural gas is the feedstock for 95 percent of the production of ammonia, which in turn is the key ingredient for the production of nitrogen-based fertilizers. So, rising global gas prices, will feed into rising fertilizer prices, which will feed into higher farmgate prices for food.

As the Nobel Institute explains:

“Manufacturing 1 ton of anhydrous ammonia fertilizer requires 33,500 cubic feet of natural gas. This cost represents most of the costs associated with manufacturing anhydrous ammonia. When natural gas prices are $2.50 per thousand cubic feet, the natural gas used to manufacture 1 ton of anhydrous ammonia fertilizer costs $83.75. If the price rises to $7.00 per thousand cubic feet of natural gas, the cost of natural gas used in manufacturing that ton of anhydrous ammonia rises to $234.50, an increase to the manufacturer of $150.75.”

In Asia in October gas prices briefly touched a peak of in excess of $34 per thousand cubic feet. The price since then have eased, but the implications are clearly serious.

In Europe, the surge in gas prices has been most extreme in the UK. Ten small firms supplying almost 2 million households have failed, leaving open the question of continuity of supply. Brexit-induced supply chain difficulties and the absence of East European harvest labour have meant that supermarket shelves have sometimes been empty. Taken together, the UK seems, to some observers at least, to be facing a new “winter of discontent”.

The UK is also the home base of a particularly influential financial newspaper, which may account for some of inflamed tone of the commentary on this coincidence of rising energy prices and nagging supply chain issues. At times, a famine like that in 1930s Ukraine, has not seemed far away. And the panic – cue handwaving – has something to do with climate activists, state interventionism and net zero.

This is a discursive knot that desperately needs untangling.

I want to focus here on the global food price issue.

The rise in global food prices is a HUGE deal that demands urgent attention at the UN level. It is crucial that the budgets of all relevant aid agencies be adequately funded so that food supplies can be maintained. Importing countries must have the foreign exchange they need.

The World Food Programme has sounded the alarm:

“High food prices are hunger’s new best friend. We already have conflict, climate and COVID-19 working together to push more people into hunger and misery. Now food prices have joined the deadly trio,” said WFP Chief Economist Arif Husain. “If you’re a family that already spends two thirds of your income on food, hikes in the price of food already spell trouble. Imagine what they mean if you’ve already lost part or all of your income because of COVID-19.”

…..

A record 270 million people are estimated to be acutely food insecure or at high risk in 2021 – a 74% jump from 2020, driven by conflict, economic shocks, natural disasters, the socio-economic fallout from COVID-19, and now food price hikes. In 2021, WFP is undertaking the biggest operation in its history, targeting 139 million people worldwide.

It is also true that there is more and more evidence to suggest that climate change is impacting global food supplies. To name just two examples, both the US and Brazil are suffering from serious drought.

It is more than likely that high energy prices will, in due course, feed through to farm gate prices, by way of fertilizer costs. But, it is very unlikely that energy is a major driver of the escalation of food prices we have seen so far. The timing is just not right. The escalation in key commodity prices began months before the surge in fertilizer prices began to make itself felt.

The serious implications are for prices in 2022 not in 2021.

Finally, it is altogether implausible to attribute any of these price increases, either those we have seen so far, or those that are likely to be in the pipeline, to climate policy. Climate change, yes. But climate policy, no.

Net zero may be a slogan to be heard everywhere, but, regrettably, it has had far too little real impact so far.

As for the analogies to the 1970s, if they serve a purpose in alerting the authorities to the need to take urgent action to avoid a food crisis, so be it. But in looking more closely at the data, I have run into some real puzzles.

I may be barking up the wrong tree with the following thoughts. So, take the above as read and let me put the following in a separate section, which comes with a health warning.

*********

The FAO food price index, which appears to show that in “real terms” food prices are now close to their 1970s levels, is a complicated beast.

Its make up is explained well in this useful FAO slide deck.

It is clearly a mistake to read this index as a food price index. It is not an index of what consumers actually pay. It is really a commodity price index. More relevant for producers than for consumers.

But, what is puzzling me, is the way it is adjusted to reflect relative price movements i.e. the way we move from a nominal food price index to a thing we call a “real price index”. This is the adjustment which generates the remarkable conclusion that food prices today are as high today as they were in the crisis period of the early 1970s.

My worry about this claim, arises from the simultaneous publication of another report on the world food situation. This too was authored by the FAO. But this one is published in collaboration with the OECD.

The OECD-FAO report also contains a table on the long-run development of real food prices. And it this graph which is causing me the headaches. It shows the 1970s price spike. It shows the 2008 and 2011 spikes, but the current spike is really not showing up.

https://www.fao.org/3/cb5332en/cb5332...

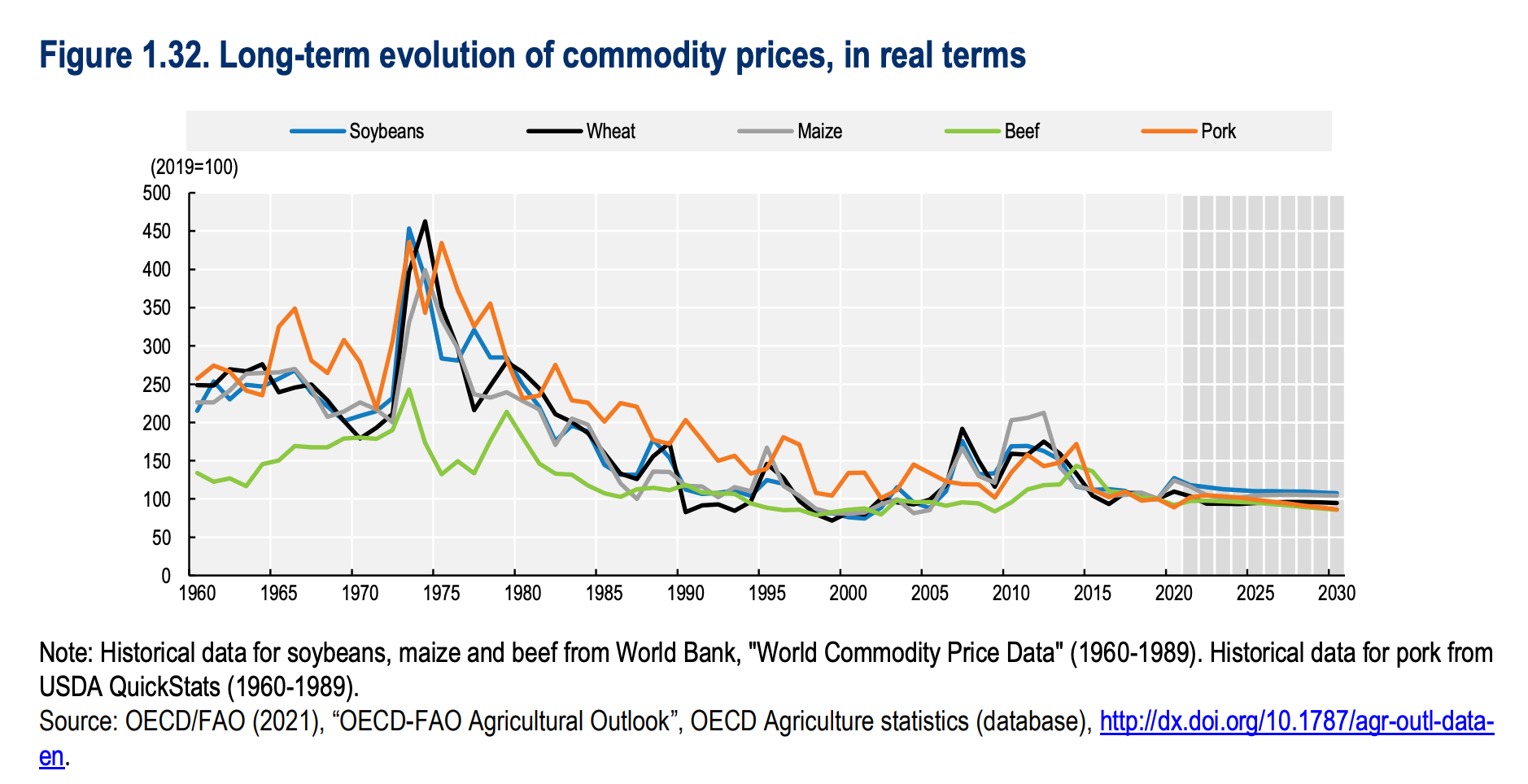

https://www.fao.org/3/cb5332en/cb5332...Rather than a composite index, the OECD-FAO graph shows the price of soybeans, wheat, maize, beef and pork separately. Together they make up a substantial part of the FAO food price index and according to the OECD-FAO calculations, in real terms they are up slightly relative to 2020, but they remain very far below their 1970s peaks.

To reiterate, these are separate price series for particular commodities. But these are very important commodities. Given their weight in the FAO food index, it is hard to see statistically how one can reconcile the two charts. Indeed, it is hard to see economically how it could be true that if the real prices of these commodities are this low, the prices for other commodities in the FAOs index could be at 1970s levels in real terms. For traders there would be gigantic opportunities for arbitrage between crops. And why would any farmer continue to produce wheat if all wheat commands are the kind of prices being shown in the OECD-FAO numbers, whilst other commodities are commanding the kind of staggering prices implied by the FAO food price series.

There is something wrong here. The discrepancy is huge and it is not recent. What is going on? I cannot be the first person to notice this. I must be missing something!

My first thought was that the problem is not in the commodity prices, but in the price for other goods to which they are being compared. The widely quoted FAO Food Price is deflated by the Manufactures Unit Value Index of the World Bank, whereas the OECD-FAO table uses the US GDP deflator. As the OECD-FAO report notes, that may create a different.

For a description of the index and its components please refer to the special features on the FFPI in (FAO, 2013[37]) and (FAO, 2020[36]). The Outlook uses the US GDP deflator (2014-2016=1) to obtain the index in real terms. As a result, the real FFPI in the Outlook is different from what is published in (FAO, 2020

Reading that footnote came as a relief. The OECD-FAO analysts see the discrepancy too and attribute it to the deflator. That was the hypothesis that Cameron Abadi and I discussed on Ones and Toozes.

It is an intuitively plausible idea. If the World Bank price index used by the FAO to do the deflation is measuring “Manufactures Unit Value” it might well exhibit a strong downward tendency. After all, we have become very, very efficient at making manufactured goods. It would not be implausible to suggest that a bushel of wheat buys you far more computer or cellphone in 2021 than it did in 1973. That is what it means to say that the real price is as high now as it was in the early 1970s.

To be make sure, I thought I would email the official at the FAO responsible for the index. They responded, pointing out that the FAO index has far more components that the few commodities listed by the OECD-FAO, but broadly agreeing with my hunch that the action was probably in the deflators i.e. the prices series to which the food prices were compared.

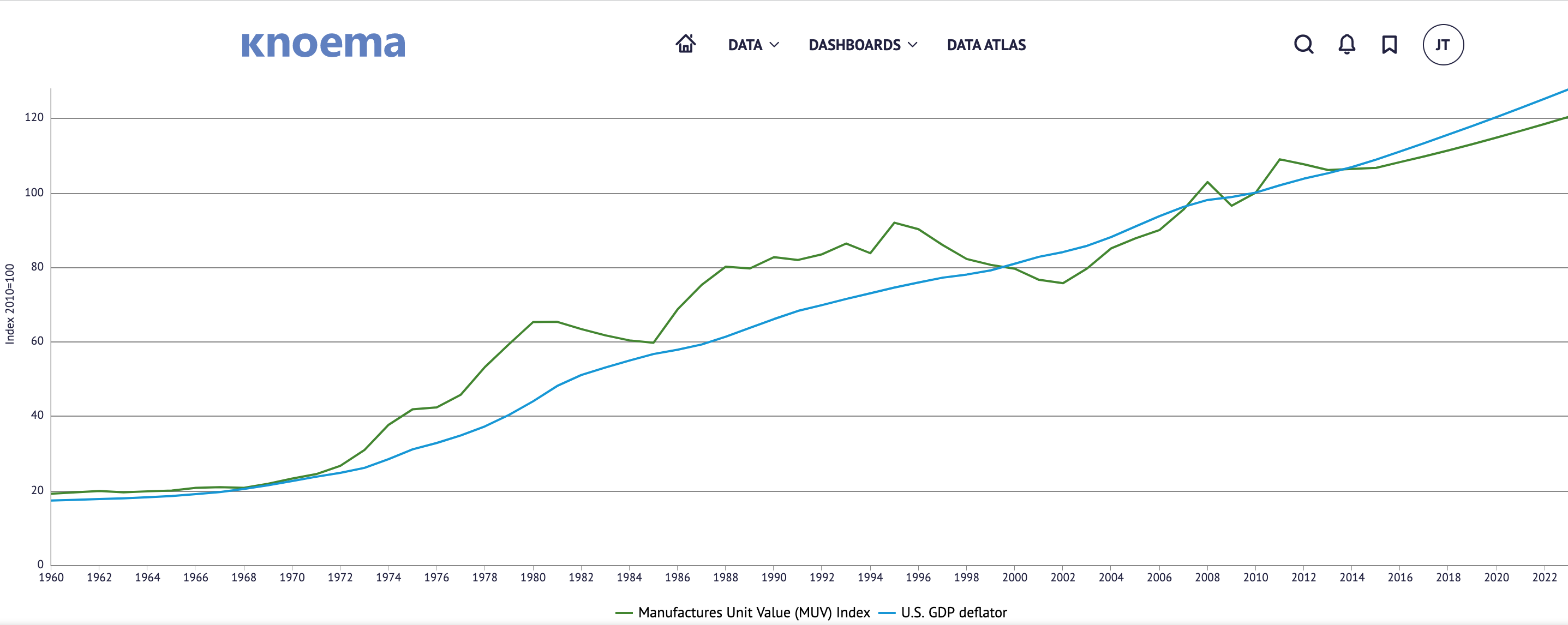

But could the discrepancy really be large enough? I decided I really ought to check the underlying price indices themselves. Did the World Bank’s Manufactures Unit Value index (used by the FAO to produce the headline about the 1970s) diverge as strongly from the US GDP deflator (used in the far less dramatic OECD-FAO) numbers as I supposed? To offer a satisfactory explanation, the MUV would need to plunges below the GDP deflator.

So, it was a bit of a shock to discover this.

The two deflators really don’t diverge at all.

Admittedly, the World Bank MUV index is rather obscure. I may have got hold of the wrong index. But this is the kind of thing that makes you go … hmmmm.

I’m a bit stumped. I’ve fired off more emails to the person at the FAO. Maybe they can help.

Right now, amidst all the talk of stagflation and energy crisis, I’m worried that we have the story about food wrong too. Not only is the link to energy being seriously overplayed and for bad reasons. But the idea that we are back to 1970s in real terms, may be quite misleading. I hope I may simply be misreading the numbers somehow. If anyone can resolve the puzzle I would be very grateful.

Watch this space ….

I love putting together this newsletter and I love the fact that it goes out free to many readers. If you are enjoying the read and can afford to support the project, please consider signing up for one of the three subscription options.

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.October 21, 2021

Ones and Tooze: Inflation, pasta and Maultaschen

This week Cameron and I discuss inflation and why Germans love Italian pasta and what it means!

Sign up at Apple

Or from many other podcast providers at the Foreign Policy website.

Apparently the best derivation of Maultaschen is

Maul = animal mouth

Taschen = pouch

→ Ravioli = feed pouch.

Kinda makes sense!

Why do you need to know this? Listen to the latest Ones and Tooze to find out.

In the mean time, to subscribe to chartbook, click here:

October 20, 2021

The future of Europe is at stake in the fight for Germany’s finance ministry

The result of the German election was known within minutes of the polls closing on 26 September. But the kind of government that will emerge is being decided now, behind closed doors, in intense three-way coalition negotiations. With the Christian Democratic Union (CDU)/Christian Social Union (CSU) humiliated by a defeat of unprecedented magnitude, Olaf Scholz of the Social Democratic party (SPD) is the clear favourite to succeed Angela Merkel at the chancellery.

The real question is the balance of power between the SPD’s two coalition partners, the Greens and the Free Democratic party (FDP). A key issue in those negotiations is who gets the job at the Finance Ministry. The politicians concerned may be unknown outside of Germany, and the battle over who controls the purse strings may not seem glamorous. But it will, in fact, decide the prospects not just of Germany’s next government, but of Europe.

Both the FDP and the Greens want the finance ministry job. Indeed, in the course of the campaign, FDP leader Christian Lindner made it into a headline issue, warning voters that the choice was between him and Robert Habeck, the Green party chairman and chief architect of the traffic-light coalition.

The FDP and Greens are, in some ways, similar. They are the two parties that contend for young people’s votes. Both take a strong line on civil liberties and have little time for accommodation with Russia and China. Both want to modernise Germany’s creaking infrastructure, especially when it comes to tech. But on climate, the Greens are far more serious than the FDP. The two parties also differ on social and economic policy – and they differ, too, on Europe.

Read the full article at The Guardian.

October 17, 2021

Chartbook #46: West Virginia – the historic roadblock to US climate policy.

The New York Times headline on Saturday morning screamed:

Key to Biden’s Climate Agenda Likely to Be Cut Because of Manchin Opposition

The West Virginia Democrat told the White House he is firmly against a clean electricity program that is the muscle behind the president’s plan to battle climate change.

This is the nightmare many advocates of a progressive US climate policy have long been haunted by.

The clean electricity program that Senator Joe Manchin (WV) has turned against is the cornerstone of the Biden climate program. Driving first coal and then gas out of the US electricity system, combined with a big push on EV, were the twin mechanisms through which the administration hoped to meet its objective of cutting greenhouse-gas emissions by 50-52 relative to 2005 levels by 2030. It was always feared that Manchin might dig in on gas. It now seems that his position has hardened to one of outright opposition to any form of clean energy provision in the spending package. Without the clean electricity program it is hard to see how the United States can make good on its climate promises. Unless Manchin flips, America will go to the global climate talks at COP26 at Glasgow with nothing to offer.

Manchin is the senior senator for West Virginia, commonly described as “coal country”. He is a Democrat in a massively Trump-voting state. As the NYT reported, West Virginia’s other senator, the Republican Shelley Moore Capito, “said she was “vehemently opposed” to the clean electricity program because it is “designed to ultimately eliminate coal and natural gas from our electricity mix, and would be absolutely devastating for my state.””

The power that West Virginia’s two Senators wield is astonishing considering that the state has a total population of 1.79 million – as compared, for instance, with the New York borough of Brooklyn which numbers 2.89 million inhabitants. West Virginia’s swing votes in the Senate are another demonstration of the warped constitution that the 21st-century United States has inherited from the eighteenth century.

By way of their influence in Washington, West Virginian politicians have repeatedly stymied not just American, but global climate policy. As Lee Harris reminds us in a timely piece in American Prospect, in 1997 it was West Virginian Democrat Robert Byrd who, along with Chuck Hagel, blocked American ratification of the Kyoto climate protocol negotiated by the Clinton administration.

West Virginia’s identity is deeply tied up with coal. So too is Joe Manchin’s personal fortune. See this Guardian investigation and this hard-hitting piece in The Intercept.

But, how deep is the state’s economic dependence on fossil fuel extraction? Is Capito right? Would decarbonization be devastating for West Virginia?

Back in September Paul Krugman announced in the Times: “Dear Joe Manchin: Coal Isn’t Your State’s Future”

“It’s actually startling how small a role coal plays in modern West Virginia’s economy. Before the pandemic, the coal mining industry employed only around 13,000 workers, less than 2 percent of the state’s work force. Even attempts to make the number look bigger by counting jobs indirectly supported by coal suggest a state that has overwhelmingly moved on from mining. So what does the state do for a living? These days West Virginia’s biggest industry is health care, which employs more than 100,000 people (and offers many middle-class jobs).”

As Krugman points out, what has run down coal in West Virginia are not liberal environmental regulations, but market forces. Meanwhile, health care as a growth industry shows the benign face of big government at work.

“Federally subsidized health care is particularly important in West Virginia, where Medicare beneficiaries are a quarter of the population, compared with only 18 percent of the nation as a whole; the state also experienced a very rapid decline in the number of uninsured after the implementation of the Affordable Care Act.”

It is easy to agree with Krugman that coal is not West Virginia’s future. But, if the matter were as simple as Krugman presents it as being, it would be truly puzzling that West Virginian politicians are as dogged in their defense of the status quo as they are.

Is the energy interest really as trivial as Krugman suggests? In trying to answer this question one descends into a bewildering mesh of politics, theory and empirics. This is itself significant. The fossil fuel lobby in West Virginia is well-defended in ideological terms. It is not a matter simply of denial. It continues to offer an entire vision of the local economy, which is inextricably tied up with fossil fuels.

The West Virginia news site that Krugman cited in support of his contention that coal was irrelevant, was actually making the opposite case. It was quoting a report commissioned by the West Virginia Coal Association from West Virginia University’s Bureau for Business and Economic Research (BBER).

I would love to learn more about the history of the BBER. The website says that it traces its history back to the 1940s. Does anyone know more? How did this regional hub of expertise get established in coal country?

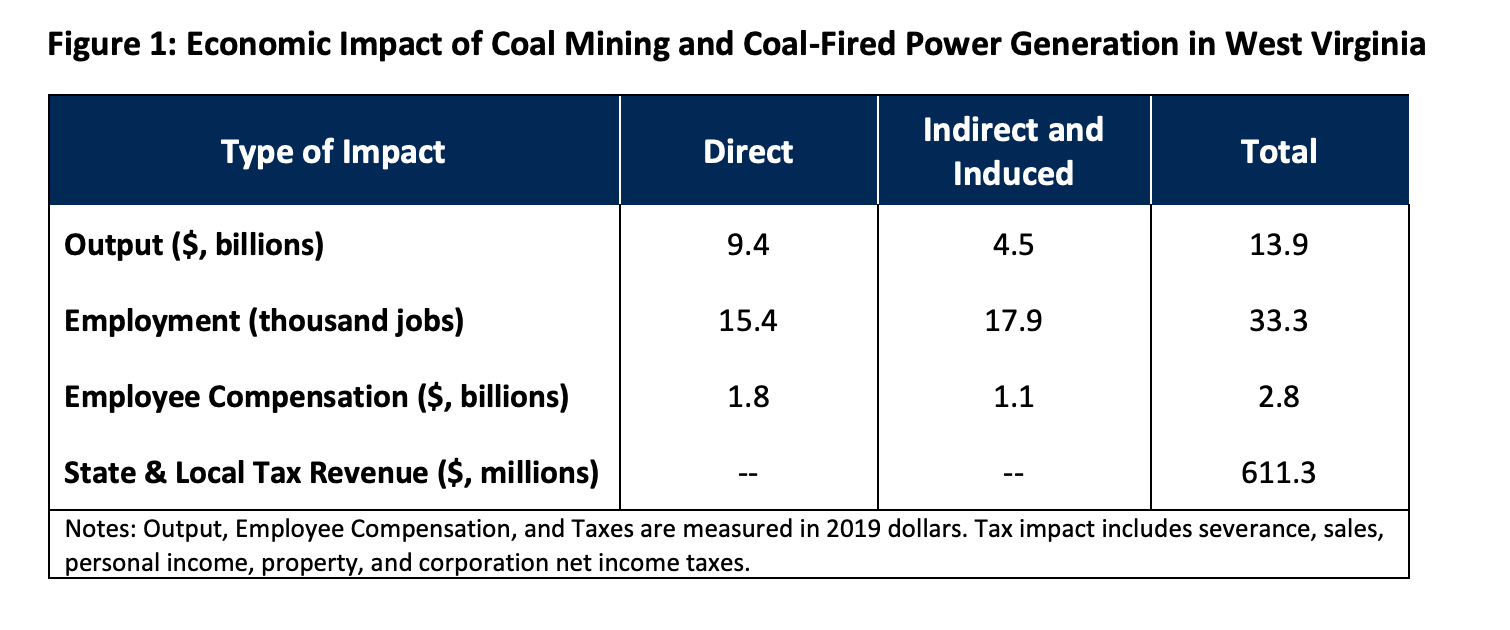

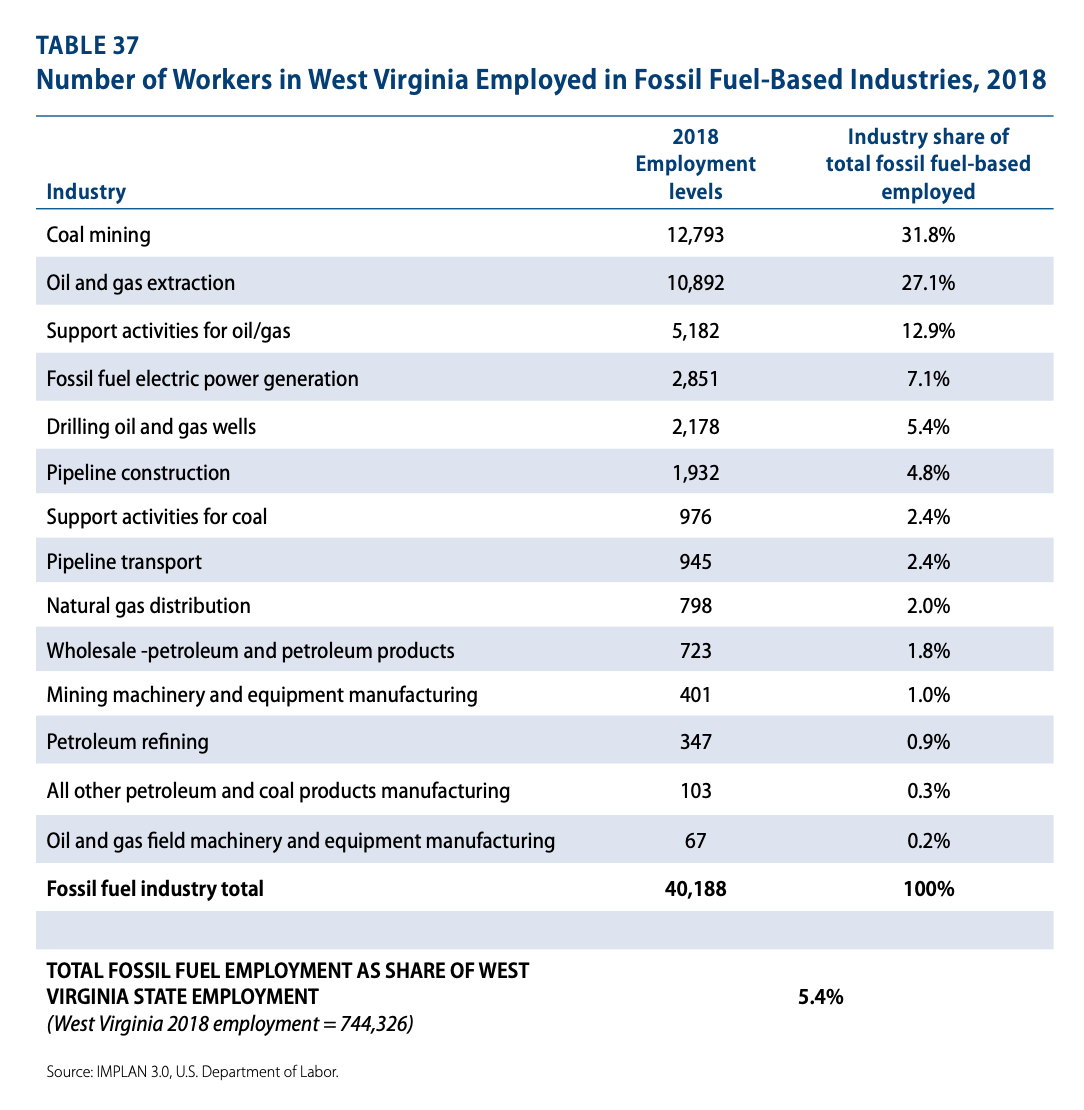

The BBER’s latest report on the coal industry’s significance for West Virginia claims “that the mining industry alone spends more than $2.1 billion on wages and coal operators generated approximately $9.1 billion in economic activity in 2019, far more than the entire general revenue budget of state government.” All told, the “combined economic impact of coal mining and coal-fired electric power generation was approximately $13.9 billion, meaning the industries supported 17 percent of the state’s total economic output or one out of every six dollars generated.”

The BBER’s commissioned report can be accessed here. The key table is the one below:

The definition of output used in this table is somewhat unclear. As Krugman suggests, the “multiplier” methodology, in which an industry is credited with supporting thousands of other jobs through its purchases of inputs from other sectors, can easily be used to generated inflated numbers. The more conservative route would simply be to compare value added in coal-mining and ancillary services with state-level GDP of $78.86 billion. Alternatively one could weigh employment and the wage bill.

But even the simple question of how many workers are employed in coal-mining and related services is not uncontentious. Krugman cites a figure of only 13,000. From the following compilation put together by PERI UMass it is apparent that this does not include contractor or ancillary workers.

Source: PERI UMASS

The coal experts at the BBER count a total of 33,000 workers in coal mining and coal-fired power generation. Hard-core advocates of the coal industry go further. They cite data from the West Virginia Office of Miners Health, Safety and Training (WVOMHST) which “reports 15,440 direct coal mining jobs and 37,463 contractors, for a total of 52,903 coal industry jobs in the state”.

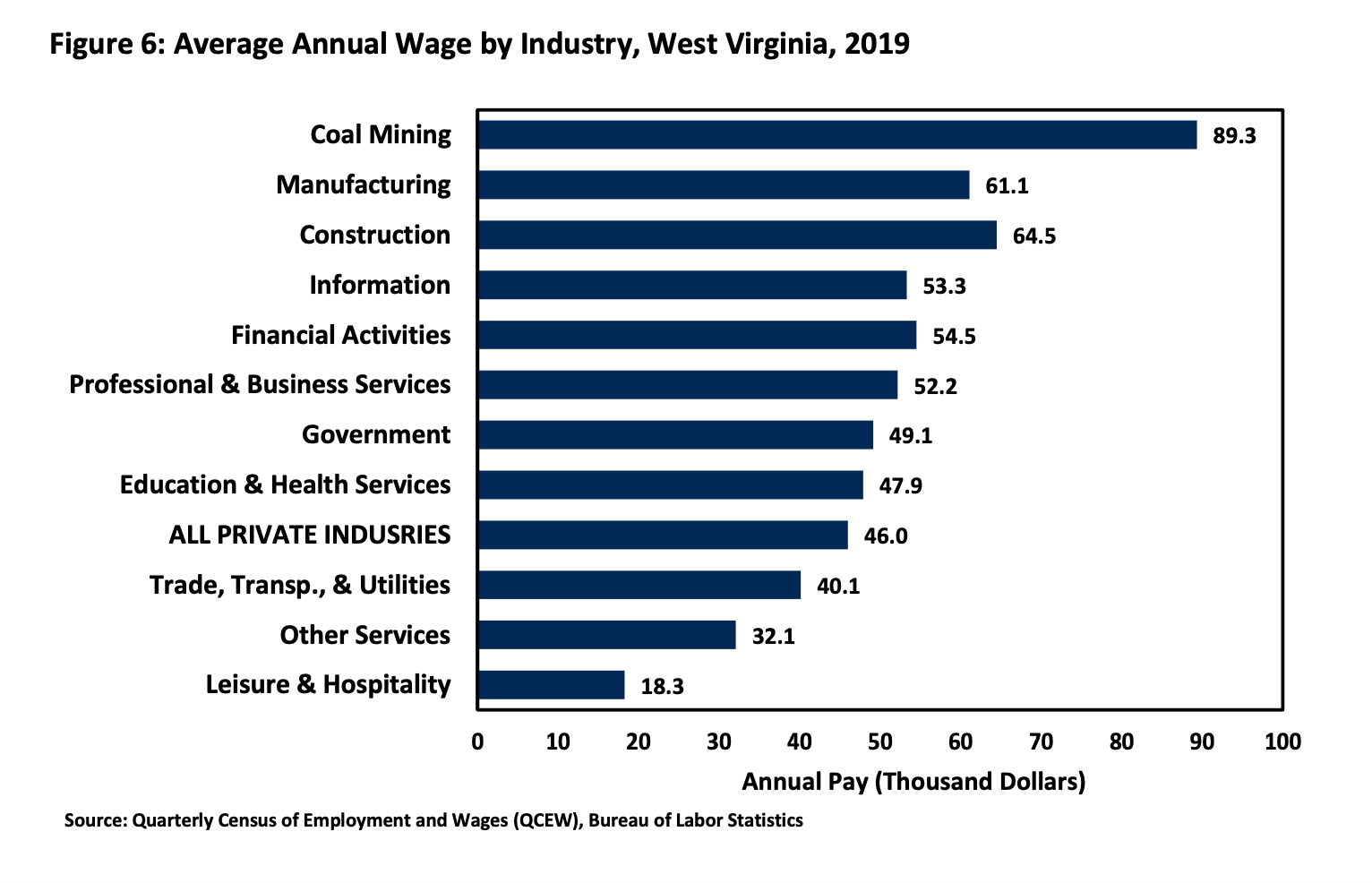

Relative to West Virginia’s pre-COVID non-farm employment of 720,000 that would imply a share of employment somewhere between 2 and 7.3 percent. That is a long way form the 17% share of output claimed by the BBER. Admittedly, the significance of the coal workforce is multiplied by the fact that they earn significantly higher wages. Again the figures vary. According to the BBER report, annual average wages in West Virginia ranged as follows.

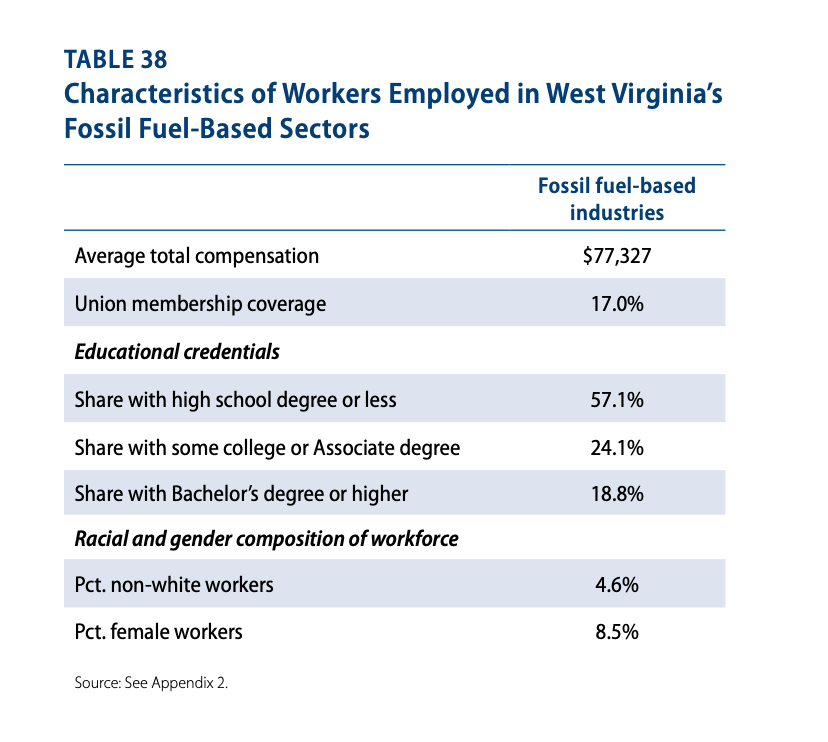

Applying these pay differentials to the range of employment figures would imply a coal share in the wage bill of between 4 and 14.3 percent. But once again one must ask, are these extremely high numbers of coal-industry wages really plausible? The UMass report on the West Virginia fossil fuel sector gives a figure for earnings of $77k.

Four things, at least, are clear. The coal sector has declined and will likely continue to decline, despite occasional upswings as in 2018-9, whether Joe Manchin wins his rearguard action or not. Secondly, the battle over coal is over more than 2 percent of the West Virginia economy. The high-side estimates would come close to one in six jobs in the state. Thirdly, it is not just coal that is at issue. Gas is no less crucial. According to the UMass study, more than half the fossil-fuel sector jobs at stake are in gas and oil. Estimates by the BBER suggest that gas adds almost as much to West Virginian gross state product as does coal. According to its somewhat opaque methodology, nearly one-third of state GDP in 2019 can be attributed to fossil fuels. This is the kind of vision of West Virginia’s economy that makes decarbonization a mortal threat.

The other thing that is clear is that though the health care sector that Krugman champions is large. It promise for the future of West Virginia is ambiguous. For one thing, it pays significantly less than the energy sector jobs that are at risk. I worry that lumping education with health care workers may be a ploy on the part of the BEER. In any case, wages in that sector are barely half those in coal.

Krugman is right that health care is a larger and more dynamic employer. But one has to ask why. In the analysis of the BBER economists, the growth of the health care sector is less a bright promise of the future than a symptom of West Virginia’s economic and social distress. The large medical sector is servicing a population that is not just aging, but wracked by ill-health and an epidemic of “deaths of despair”.

As the BBER notes:

“According to the Centers for Disease Control (CDC), West Virginia’s age-adjusted mortality rate is the second highest among all states and also ranks among the tier of states with high incidences of heart disease, cancer and diabetes. Furthermore, behavioral or lifestyle factors that contribute to poor health outcomes such as physical activity during leisure time are among the lowest in the nation and rates of cigarette smoking and smokeless tobacco use among the adult population are among the highest nationally. Another source of the state’s poor health outcome trends over the past decade or so has been the skyrocketing use and death from opioid overdoses. Indeed, crude mortality rates among young men – particularly those between the ages of 25 and 34 – have risen significantly. For example, even as the 25 to 34 population has shrunk by roughly 3 percent since 2012, deaths among residents in this age group has increased by nearly 17 percent ….”

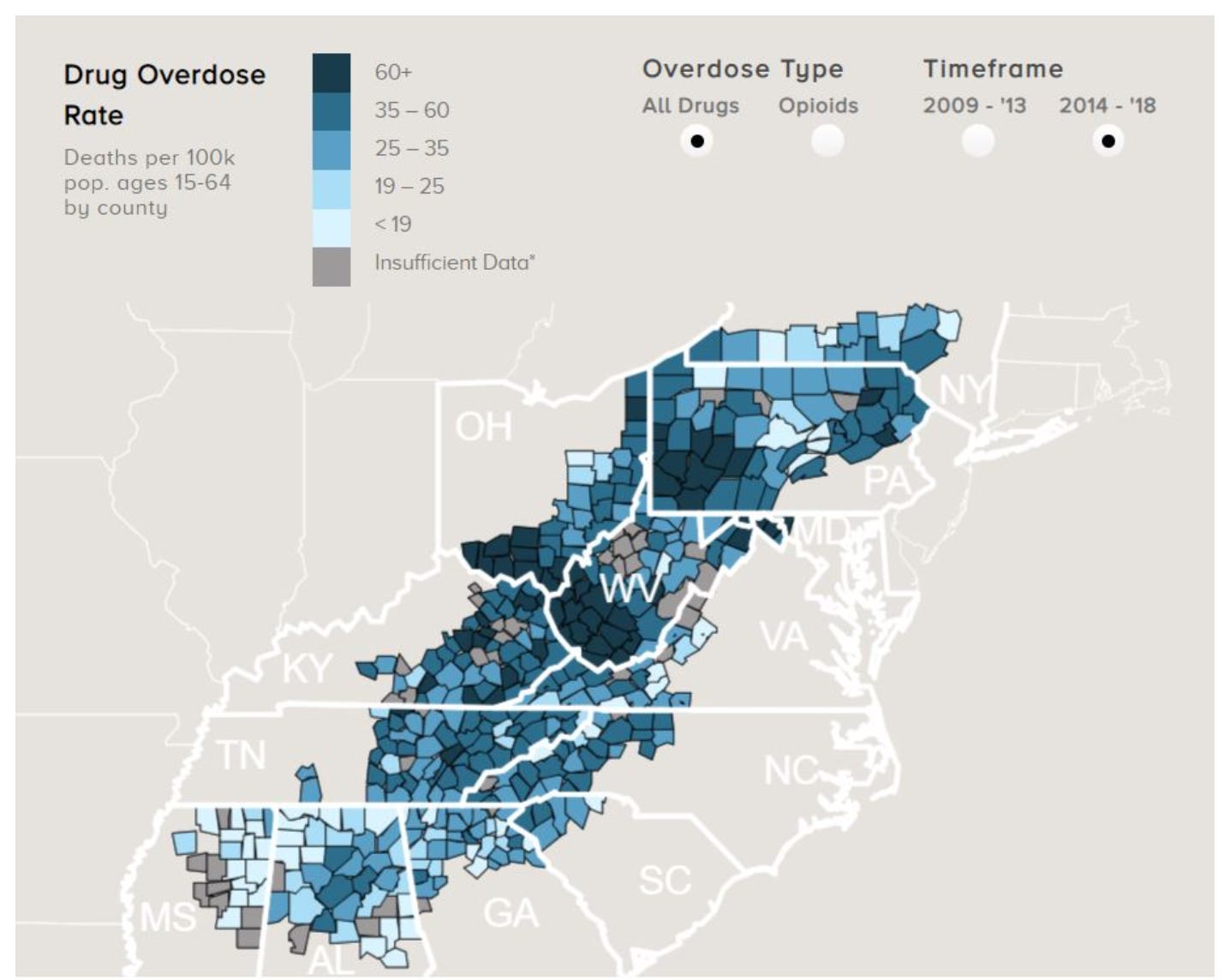

West Virginia is at the heart of an epidemic that has swept Appalachia.

Source: ARC

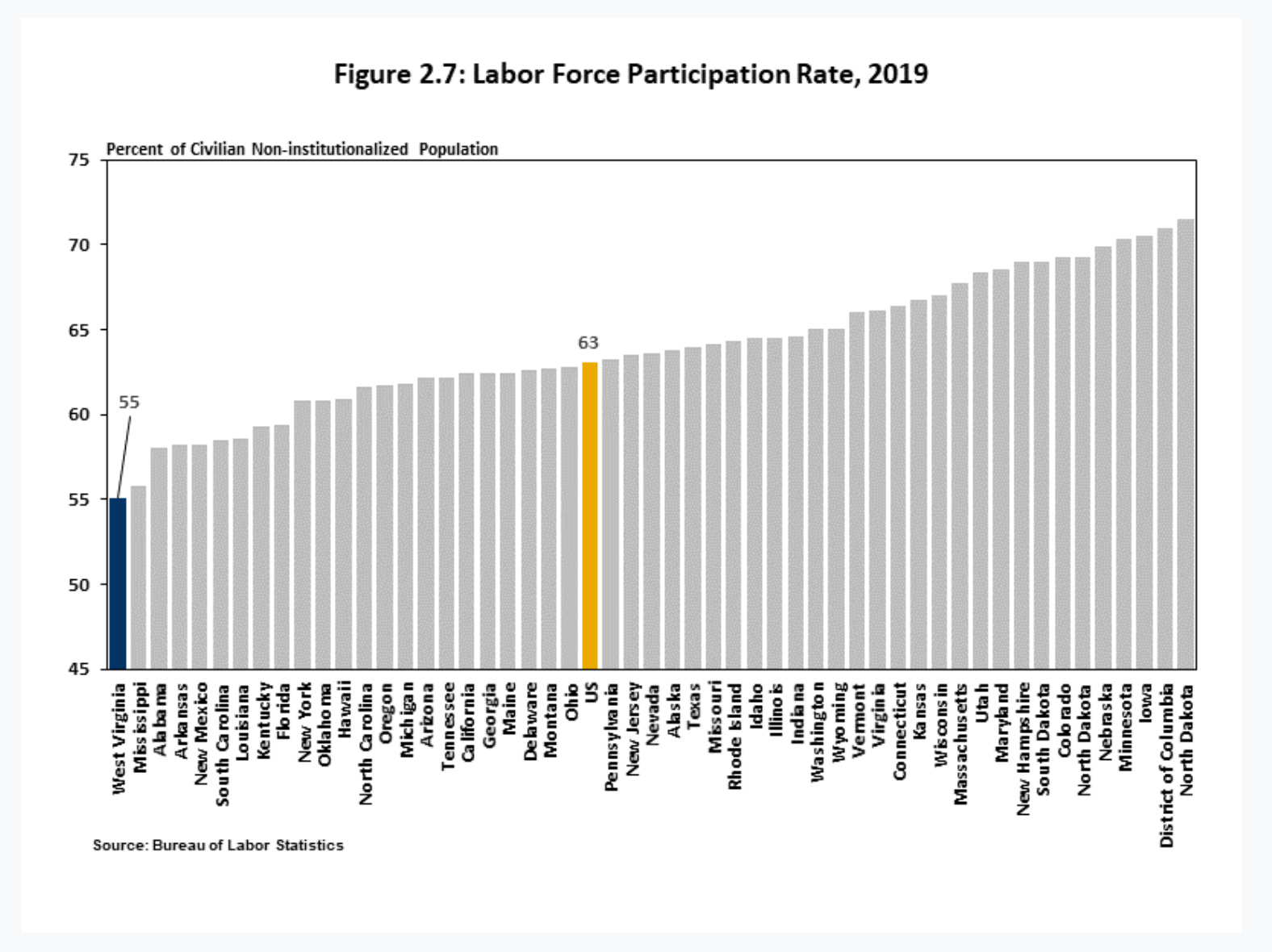

It is not by accident that West Virginia has a labour force participation rate of 55%, the lowest in the United States.

No doubt this was not Paul Krugman’s intention, but against this backdrop it can seem almost cynical to advocate health care as the future for West Virginia’s economy.

It is good news, therefore, that a variety of coalitions have been at work trying to develop blueprints for an economic future for West Virginia that goes beyond tending to its own ailing population.

One plan has been developed by Robert Pollin at PERI UMass Amherst. It maps how an annual investment of $2-2.5 billion in renewable energy and land management sectors, would enable a gradual wind down of the West Virginia fossil fuel sector, whilst fully protecting the retirement rights of the existing workforce. The full program is here. Robert Kuttner interviewed Pollin about the plan for American Prospect.

But it is not just out of state experts who can see a different future for West Virginia. A grouping called the Appalachia Coalition has developed a blueprint for a sustainable future for the entire region from Southwestern Pennsylvania, Kentucky, Ohio and Kentucky.

Earlier in the year 100 members of Congress endorsed the so-called THRIVE resolution (Transform, Heal, and Renew by Investing in a Vibrant Economy). Under this version of the Democrat’s investment planning, West Virginia would get about four and a half billion per year, easily enough to fund a just transition in this small state.

Whereas the economists attached to the business school of West Virginia University repeatedly underscore the huge footprint of fossil fuels in the state, at the Law School the Center for Energy and Sustainable Development has worked out a glossy plan for decarbonization.

As David Roberts has outlined in an extremely helpful compilation on his Volts substack, Joe Manchin, in fact, has his own plan, the American Jobs in Energy Manufacturing Act. If he so chose, could be rolled into the larger Biden agenda, releasing tens of billions in federal spending that could be mobilized for West Virginia.

The polling evidence suggests that West Virginia voters are concerned principally not about coal, but about jobs and their long-term future. The Biden billions could secure that future, not by clinging to the old, but by investing in new jobs.

The claim that West Virginia’s economy depends on protecting coal and gas, is thus not a self-evident fact, but a strategic political and economic choice. It is a choice to double-down on a status quo which may be deeply entrenched but whose prospects are, by common consent, dwindling. It is a choice to reject the option of restructuring and new investment. Given the funds on offer, the reason that Manchin makes that choice is not so much economic, as tactical and political.

Manchin lives dangerously as a Democrat in a deeply red state, where to be tarred with the brush of woke liberalism is a political death sentence.

Manchin’s strategy of running as a Democrat but tacking away from the liberal agenda seems like a textbook demonstration of the kind of “popularist” tactics advocated by controversial political advisor David Shor.

For smart introductions to the popularist debate check out this by Eric Levitz and this excellent piece by Ezra Klein.

Shor argues that Democrats make a fatal mistake in taking on policy choices that appeal to liberal educated voters at the expense of working-class voters. As Klein reports:

Shor showed me, as an example, a set of environmental talking points he’d tested, in which the ones that mentioned climate change performed worst. “Very liberal white people care way more about climate change than anyone else,” he said. “So when you talk about climate change, you sound like a weird, very liberal white person. This is why policy issues matter more than people realize. It’s not that voters have these very specific policy preferences. It’s that the policies you choose to talk about paints a picture of what kind of person you are.”

True or not, this certainly is the lens through which much of the New York Times coverage frames the Manchin story. This, for instance, is how Nate Cohn describes Manchin’s political position:

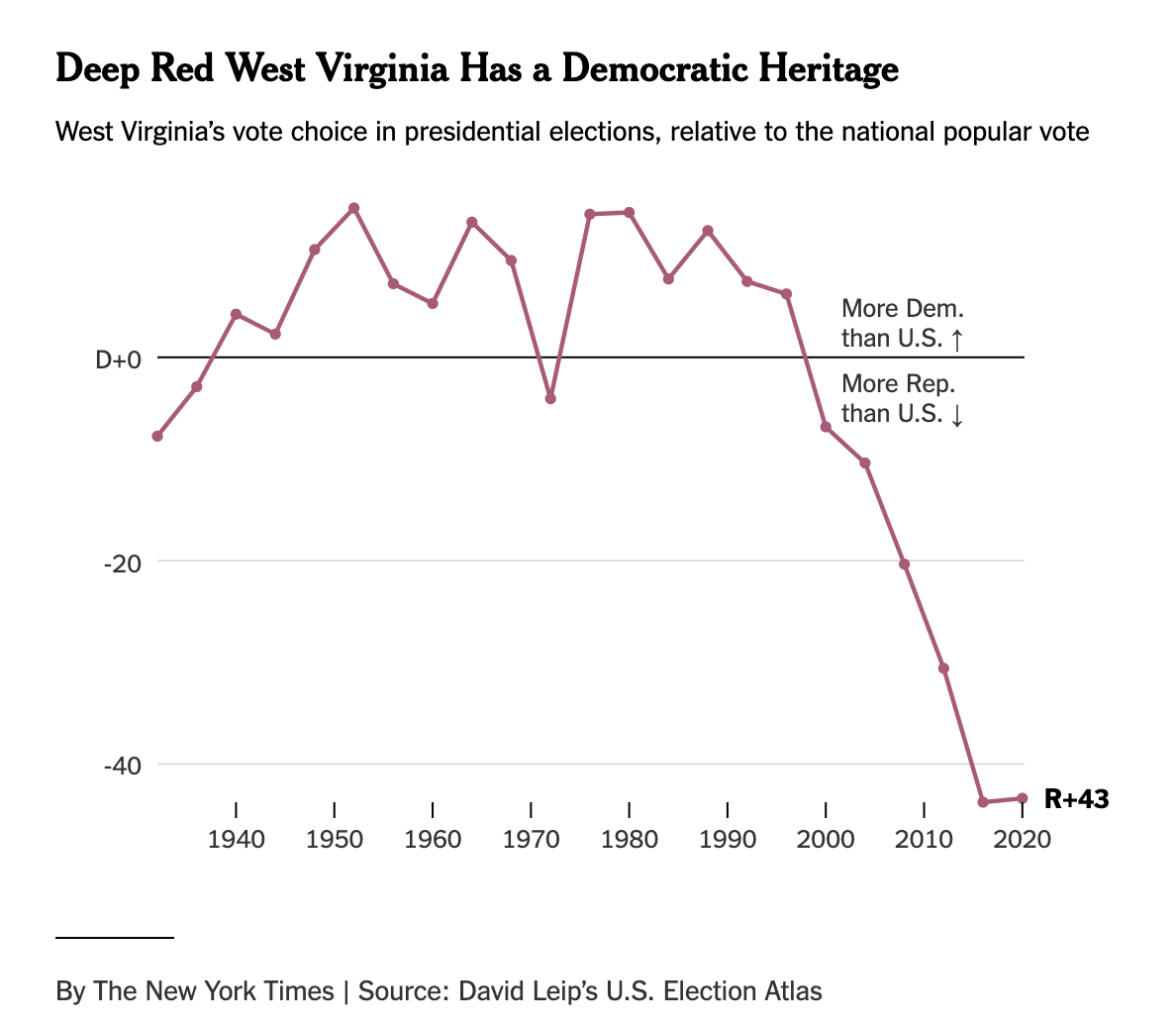

Yet Mr. Manchin’s unique ability to survive in West Virginia is the last vestige of the state’s once-reliable New Deal Democratic tradition, dating to old industrial-era fights over workers’ wages, rights and safety. It was one of the most reliably Democratic states of the second half of the 20th century, voting in defeat for Adlai Stevenson in 1952, Hubert Humphrey, Jimmy Carter in 1980 and Michael Dukakis. The so-called Republican “Southern strategy” yielded no inroads there.

But Democrats began to lose their grip on the state during the 1990s, at least at the presidential level. In a way, West Virginia voters have been thwarting progressive hopes ever since. The promise of a new progressive, governing majority always rested on the assumption that the Democrats would retain enough support among white, working-class voters, especially in the places where New Deal labor liberalism ran the strongest. They did not.

By the late 1990s, the old New Deal labor Democrats no longer defined the party nationally. And when in conflict, the party’s growing left-liberal wing prevailed over working-class interests: New environmental regulations hurt West Virginia’s already faltering coal industry; new gun control laws put Democrat at odds with an electorate where most voting households own a gun (in the 2018 exit polls, 78 percent of voters said someone in their household owned a gun).

So, on this telling, what is at stake in Manchin’s stand, is less the economics of fossil fuels or the costs and benefits of decarbonization for West Virginia, but the trajectory of party political and class realignment. It is that history that persuades Manchin to cling to the totems of coal and gas, whilst rejecting billions in investment. As the senior representative of one of the poorest states in the Union, he declares himself to be the last bastion against a new culture of entitlement. As Jamelle Bouie concludes it is a “dispute over values as much as — or even more than — a dispute over policy.” Ironically, what an enquiry into the West Virginia roadblock exposes is less the defining importance of actual producer interests – insofar as we can measure them – than the perverse grip of conservative “producerist” ideology over American politics.

October 15, 2021

The Economics Revolution and the Nobel Prize

This week, Cameron Abadi and Adam Tooze talk about the economists who won the Nobel Prize—for helping to make the science of economics … more scientific.

Also: Whatever happened to cap and trade? The strategy for stemming climate change is largely dead in the United States but surging in Europe.

Find more episodes or subscribe to Ones and Tooze at Foreign Policy.

Adam Tooze's Blog

- Adam Tooze's profile

- 767 followers