Adam Tooze's Blog, page 29

November 21, 2021

Chartbook #53 The history of the Havanese – Accompanying Ones and Tooze

Ones and Tooze this week is about JOLTS, the great resignation and about pets and pet food.

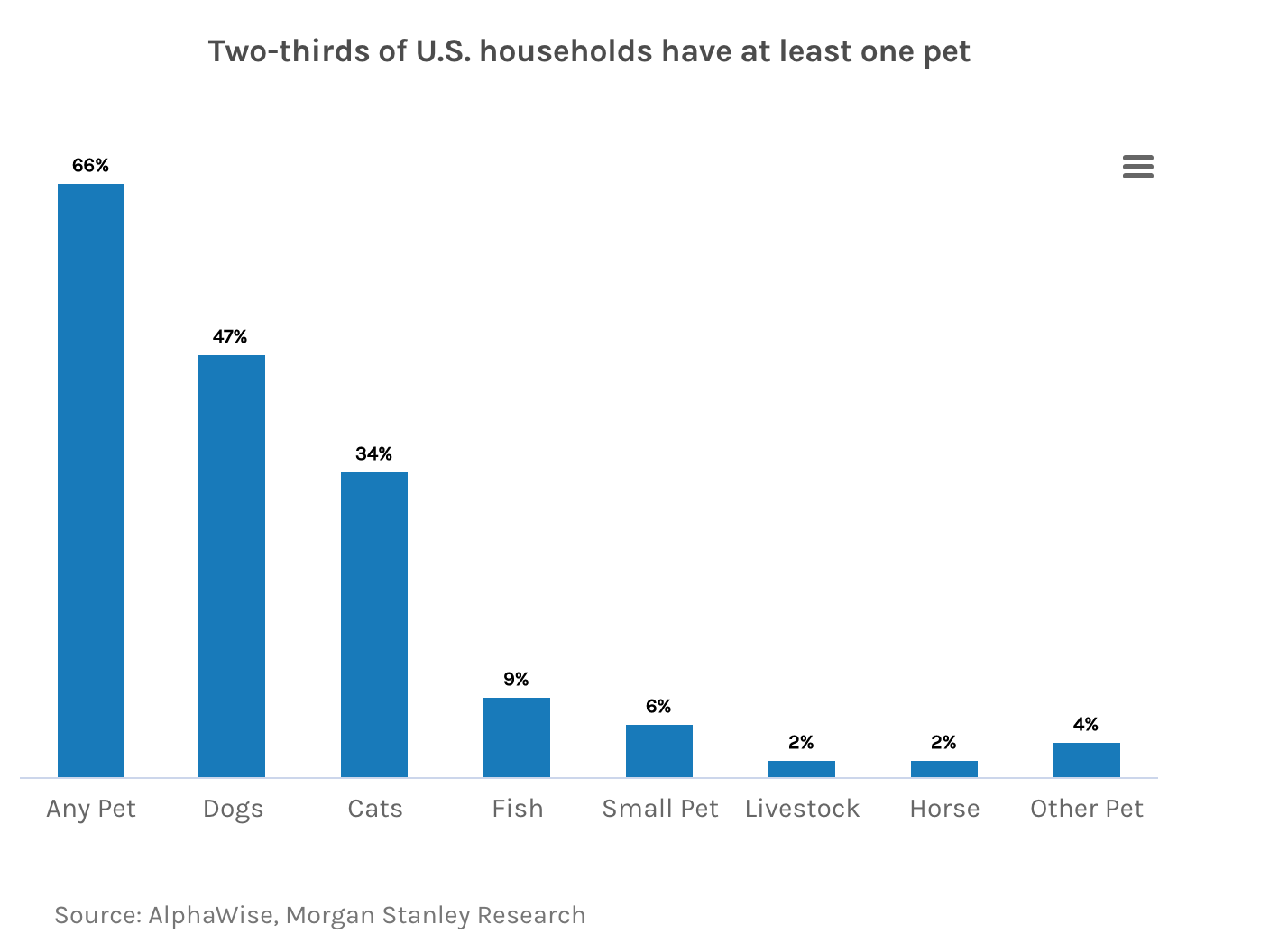

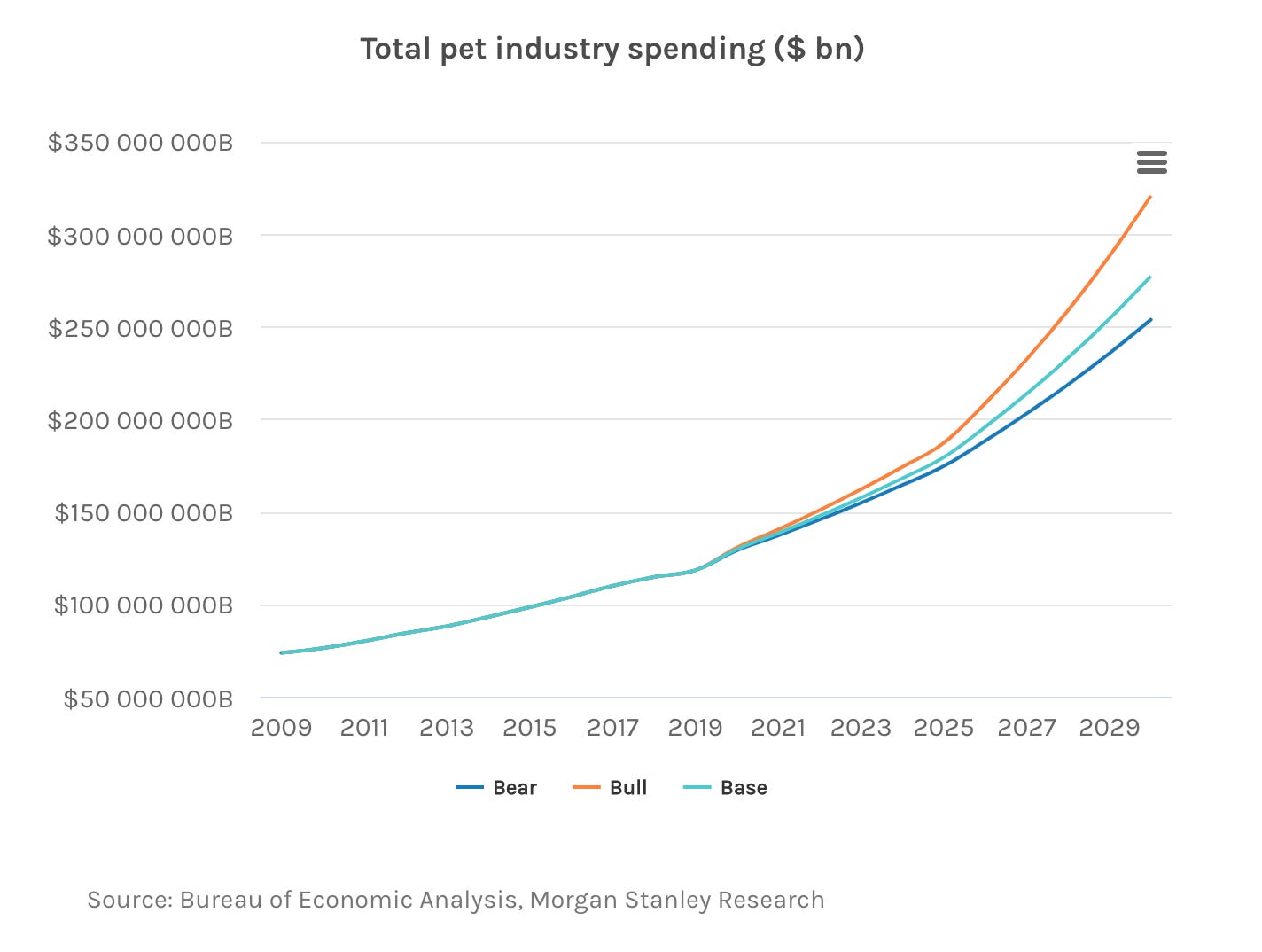

Its a huge industry. $100 billion per annum in spending in the US. And pet spending is highly income elastic. What drives it, is our deep attachment to companion animals.

As Cameron and I discuss living with a pet, particularly a human-centered dog can be a transformative experience – intimacy with a being that is not human.

In large part as a result of caring for Ruby, our Havanese, I’ve given up eating meat. As I would freely acknowledge, given the carnivorous appetites of dogs, this is not a straightforwardly logical response.

I’ve also acquired a new appreciation for the kind of animism that sees animals as the bearers of a peculiar spirit. That’s a rather highfalutin way of saying that the apartment in New York feels dead when Ruby the dog is not at home.

But I’ve also acquired an appreciation for the history of the human-canine relationship. The Havanese breed, it turns out, has a rather remarkable history, intertwined with Empire.

A constituency of amateur historians has dedicated themselves to unravelling a complicated narrative. Their work is a gift to anyone interested in canine history.

Havanese are one of the branches of the large family of bichon.

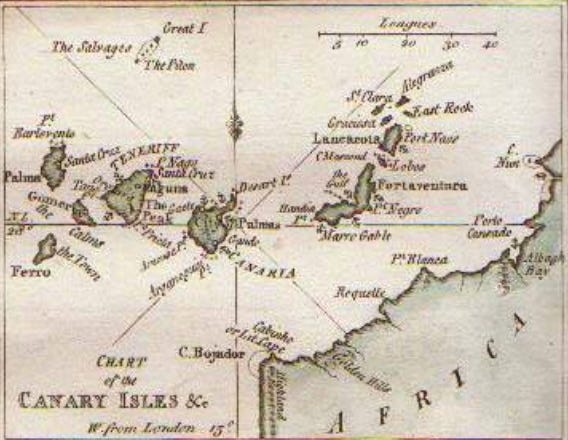

The family originated in the Mediterranean, where we find the Maltese and Bologenese breeds. In the 15th century they became entangled in a complex circulation of power and biology history within the Spanish empire, a circulation that runs by way of the Canary Islands.

The Canary Islands were first settled by humans and their livestock around 900 BC from north Africa. The romans gave them their name, Insular Canaria, not for birds – canaries – but for dogs (canaria).

After the fall of Rome, the Canary islands disappear from maps for many centuries, forming an isolated cultural, political and biological system.

In 1150 an Arab geographer wrote about them. In 1312 the Portuguese established a Catholic mission on Lanzarote (part of the Canary Islands). Traveling with Spanish and Italian sailors, small bichon dogs most likely arrived on the islands in the 1300s.

As a key launching pad for Atlantic exploration, the Canary Islands did not long escape the interest of the expanding Spanish empire. The Castilian ‘Reyes Catolicos’ (Catholic Kings) conquest of the Canary Islands began in early 1400’s and preceded through years of bloody struggle. Only in 1479 did the ruler of the Canaries recognize Spanish sovereignty, with Tenerife being the last island to surrender in 1496.

The great environmental historian Alfred W. Crosby offers a remarkable, “Ecohistory of the Canary Islands: A Precursor of European Colonialization in the New World and Australasia” in Environmental Review 1984.

In 1492, Columbus came to the islands to restock his western bound ship. It was by way of the Canary Islands the sugar cane most likely reached the Caribbean. And it was also from the Canary Islands that the ancestors of the Havanese dog arrived in Cuba.

In the mean time however, in a pattern that would repeat, the bichon dogs originally brought to the Canarys from Europe were reimported to Europe, and were given the name Tenerife dogs. They were a fashionable accessory in Renaissance court society, notably at the royal court of Francis I of France (1515-1547).

In this era they appeared in paintings by Titian.

Portrait of Federico II Gonzaga of Mantua (c. 1529) is a painting by Titian, who signed it Ticianus f. with his faithful Maltese.

Britain’s Queen Anne (1665-1714), a greater lover of dogs, acquiring two bichon after she saw them performing in a circus.

Anne, circa 1684, painted by Willem Wissing and Jan van der Vaardt

Goya (1746-1828) matched the Duchess of Alba or the White Duchess, with the fur of a bichon or a “white Havanese”.

Source: Wikipedia.

In Cuba, the Havanese bichon were the lap dogs of the local aristocracy.

Cuba was one of the richest islands in the Caribbean attracted many visitors. Havanese circulated as tourist trophies. They were not just lap dogs. They were gift dogs, presented as tokens to distinguished guests.

As one particularly rich history notes:

Cuban author and founder of the cuban Habanero Club, Zoila Portuendo Guerra brings forth perhaps the most logical theory in her book titled “Bichon Havanese”. Her extensive research has attempted to sort through the lore, fact and fiction and presents a plausible progression that incorporates facets of the many other theories. She is adamant that there have been two Cuban breeds.

According to her, the first of these, was the now extinct “Blankito de la Havana” developed on the island in the 16th and 17th centuries during the days of Spanish colonization. This breed would have been a refinement of small bichons and lap dogs brought over directly from Spain or smuggled in illicitly by pirates and sea merchants. During these times, in Europe, tiny immaculate white dogs were the height of fashion as companions to the ladies of high society. The Cubans emulated this fashion in the development of the Blankito. He would have been a very small dog, weighing just 3-6 pounds, pure white, with a very silky, perhaps curly long coat. This original Cuban dog, the Blankito would have been the breed that returned to the continent in the early 18th century to be recognised with much fanfare. Much of the confusion surrounding the breed may come from the fact that in Cuba it was erroneously referred to as the “Maltese” while in Britain it was acclaimed as the “White Cuban”. It was known throughout the rest of Europe as the “Havanese” because it came from Havana or later as the “Havana Silk Dog” because of the profuse soft coats. Mrs Guerra maintains that the Blankito would have remained a tiny white charmer till the early 19th century.

In the early 1800’s many immigrants from Continental Europe settled on the island bringing with them their own little lap dogs, most notably small coloured poodles from France, Belgium and Germany. These new dogs were bred with the Blankito and a new breed subsequently evolved, a little bit larger and with a coat of many colours. The author portends that this second native of Cuba, created on the island during the 19th century is the Havanese breed as we know it today. Is this finally the actual account of our breed’s history and development? Perhaps one of these accounts is true, but who can say for sure?

England’s first dog show, ‘The Sporting Dog Show’, was held in Newcastle-on-Tyne in 1859. Non-sporting dogs were shown in Birmingham also in 1859. Havanese made their appearance on the show circuit in 1863 at The National Dog Show held in Chelsea.

Amongst the celebrity owners were Charles Dickens and Hemingway.

To speak in rather grand terms, the Havanese were a product of empire and its class structure. And the breed almost died with it.

The Cuban revolution of 1959 shook the social foundations of the island’s famous lap dog breed. And, at this point, the histories written by breed aficionados become contentious. The story of the Havanese becomes an anti-Communist morality tale.

According to the research of enthusiasts, in Cuba the breed collapsed. Many dogs were left behind as the defeated upper class abandoned the island. Only two families, the Perez and Fantasio, are known to have escaped Cuba with their dogs. “Their dogs are remembered as the first Havanese in America. Later it was learned Senor Ezekiel Barba had been able to escape to Costa Rica with his dogs.”

Some Havanese were also adopted and taken to the Communist bloc by Soviet and other East European advisors. They became known as the Iron Curtain Havanese.

In the US in the 1970s the cause of the breed was taken up by a dog-breeding couple Dorothy L. Goodale and her husband, Bert. Placing adverts in the Spanish language press in Miami they managed to collect enough dogs to form four distinct bloodlines. From that small group of dogs, all of the thousands of pedigree Havanese in the United States today are descended.

As one website notes:

“Not till 1991 was anyone sure that the Havanese still existed in Cuba. The Bichon Habanero Club was established to study the island’s remaining indigenous dogs to ascertain their purebred status. After careful study and consideration, a closely supervised breeding program was put into place using a foundation stock of approximately 15 dogs.”

So this is the genealogy of Ruby our beloved housemate and companion. She is, not to put to finer point on it, a running dog of planter capitalism. I had previously known that phrase only as a classic of Maoist denunciation. Now I find myself with one as a member of my family, the descendant of a line that runs back perhaps 700 years.

Oh and here are some charts on the pet industry from Morgan Stanley.

November 19, 2021

Ones and Tooze – Do We Need to Worry About the Great Resignation?

On this episode of Ones and Tooze, we talk about 10.4 million—that’s the number of jobs that are currently unfilled in the U.S. economy as of September, according to the latest data from the Bureau of Labor Statistics. That’s not much different than the record high of 10.9 million openings that were recorded back in July. As COVID-19 vaccinations have increased and the economy has continued to open up, employers have been finding it incredibly difficult to find workers to fill jobs.

Economists are calling it the “Great Resignation”—this phenomenon of people exiting the labor force in droves and employers struggling to fill their openings. Adam Tooze and Cameron Abadi examine the Great Resignation and what it may portend for the economy.

Then, the two hosts discuss the billions of dollars Americans spend each year in the growing market for pet food. Is this consumerism run amok, or does the connection between humans and pets tell a different story about the value of animal companionship?

For more information visit the podcast website at Foreign Policy

November 16, 2021

The Cop26 message? We are trusting big business, not states, to fix the climate crisis

Cop26 delivered no big climate deal. Nor, in truth, was there any reason to expect one. The drastic measures that might – at a stroke – open a path to climate stability are not viable in political or diplomatic terms. Like climate breakdown itself, this is a fact to be reckoned with, a fact not just about “politicians”, but about the polities of which we are all, like it or not, a part. The step from the scientific recognition of a climate emergency to societal agreement on radical action is still too great. All that the negotiators at Cop26 could manage was makeshift.

When it comes to climate finance, the gap between what is needed and what is on the table is dizzying. The talk at the conference was all about the annual $100bn (£75bn) that rich countries had promised to poorer nations back in 2009. The rich countries have now apologised for falling short. The new resolution is to make up the difference by 2022 and then negotiate a new framework. It is symbolically important and of some practical help. But, as everyone knows, it falls laughably short of what is necessary. John Kerry, America’s chief negotiator, said so himself in a speech to the CBI. It isn’t billions we need, it is trillions. Somewhere between $2.6tn and $4.6tn every year in funding for low-income countries to mitigate and adapt to the crisis. Those are figures, Kerry went on to say, no government in the world is going to match. Not America. Not China.

We should take the hint. There isn’t going to be a big green Marshall plan. Nor are Europe or Japan going to come up with trillions in government money either. The solution, if there is to be one, is not going to come from rich governments shouldering the global burden on national balance sheets.After the failure of Cop26, there’s only one last hope for our survivalGeorge Monbiot

So, how does Kerry propose to close the gap? As far as he is concerned, the solution is private business. Hence the excitement about the $130tn that Mark Carney claims to have rallied in the Glasgow Financial Alliance for Net Zero, a coalition of banks, asset managers, pension and insurance funds.

Lending by that group will not be concessional. The trillions, Kerry insisted to his Glasgow audience, will earn a proper rate of return. But how then will they flow to low-income countries? After all, if there was a decent chance of making profit by wiring west Africa for solar power, the trillions would already be at work. For that, Larry Fink of BlackRock, the world’s largest fund manager, has a ready answer. He can direct trillions towards the energy transition in low-income countries, if the International Monetary Fund and the World Bank are there to “derisk” the lending, by absorbing the first loss on projects in Africa, Latin America and Asia. Even more money will flow if there is a carbon price that gives clean energy a competitive advantage.

Read the full article at The Guardian.

November 15, 2021

Ecological Leninism

The carbon clock is ticking. Governments and official agencies assure us that all will be well, that they can balance the risks. Some insist that technology will save us. We have achieved the impossible before, we will do it again. But why believe them? Progress towards decarbonisation has been limited. Fossil fuel interests remain stitched into global networks of power directly descended from the age of imperialism. Their political outriders may be cynical hacks, but public support for the fossil fuel status quo is all too real. The carbon coalition seems death-driven, defiant of expert advice. Centrist liberals are loud in expressing outrage, but shrink away when push comes to shove. There are periodic waves of protest. Children boycott school. There are demands for a new social contract and a just transition. A minority, tiny as yet, calls for rebellion.

With only minor alterations, this could be the portrait of a nation sliding towards defeat in a major war: relentless time pressure; limited resources rapidly running down; over-confident technocrats; promises of wonder weapons; pro and anti-war factions at loggerheads; desperate young people calling for a halt to the madness. War remains a crucial way of thinking about collective peril and about agency in the face of that peril; in climate politics, the rhetoric of war and wartime mobilisation is commonplace. American advocates of the Green New Deal called for a repeat of the staggering industrial production achieved during the Second World War. In the UK, memories of the postwar welfare state persist. There is talk of the Marshall Plan.

But isn’t this all rather too convenient? A ‘good war’, fought by democracies, ending in spectacular victory and inaugurating a golden age of economic growth and the advent of the welfare state. One way of reading the recent burst of publications – three books in the space of a year – from the historian and climate activist Andreas Malm is as a sustained challenge to this complacent historical framing of our present condition. The historical analogy he prefers to draw is with the First World War and its aftermath, a world defined by the upheaval of revolution and the violence of fascism – the beginning, not the end of an age of crisis.

To have in mind the Second World War and the birth of the modern interventionist welfare state is to take your bearings from such thinkers as Maynard Keynes, with his promise that ‘anything we can actually do, we can afford.’ The First World War and the years after it evoke a different cast of characters. Malm’s own political background is in Trotskyism, and he now declares himself an ecological Leninist. His co-authors in White Skin, Black Fuel named themselves the Zetkin Collective after the German communist and feminist Clara Zetkin, whose interpretation of fascism they draw on and whose ashes were interred in 1933 beside the Kremlin Wall.

Some will accuse Malm of cosplaying revolution while the planet burns. But his position is actually one of tragic realism. As he and his colleagues argue in White Skin, Black Fuel, the defining fact about climate change is that it is ‘a revolutionary problem without a revolutionary subject’. The environmental movement may have aligned itself with social justice activism, but it hasn’t been ‘able to challenge capitalism with anything like the power once evinced by the Third International or the national liberation movements, or even the social democratic parties of the Second International; a lame successor, it won no Vietnam War and built no equivalent of the welfare state.’

Read the full article at London Review of Books.

November 14, 2021

Chartbook’s 1st Birthday 2020-2021

This weekend Chartbook celebrates its first birthday. It has been a great year.

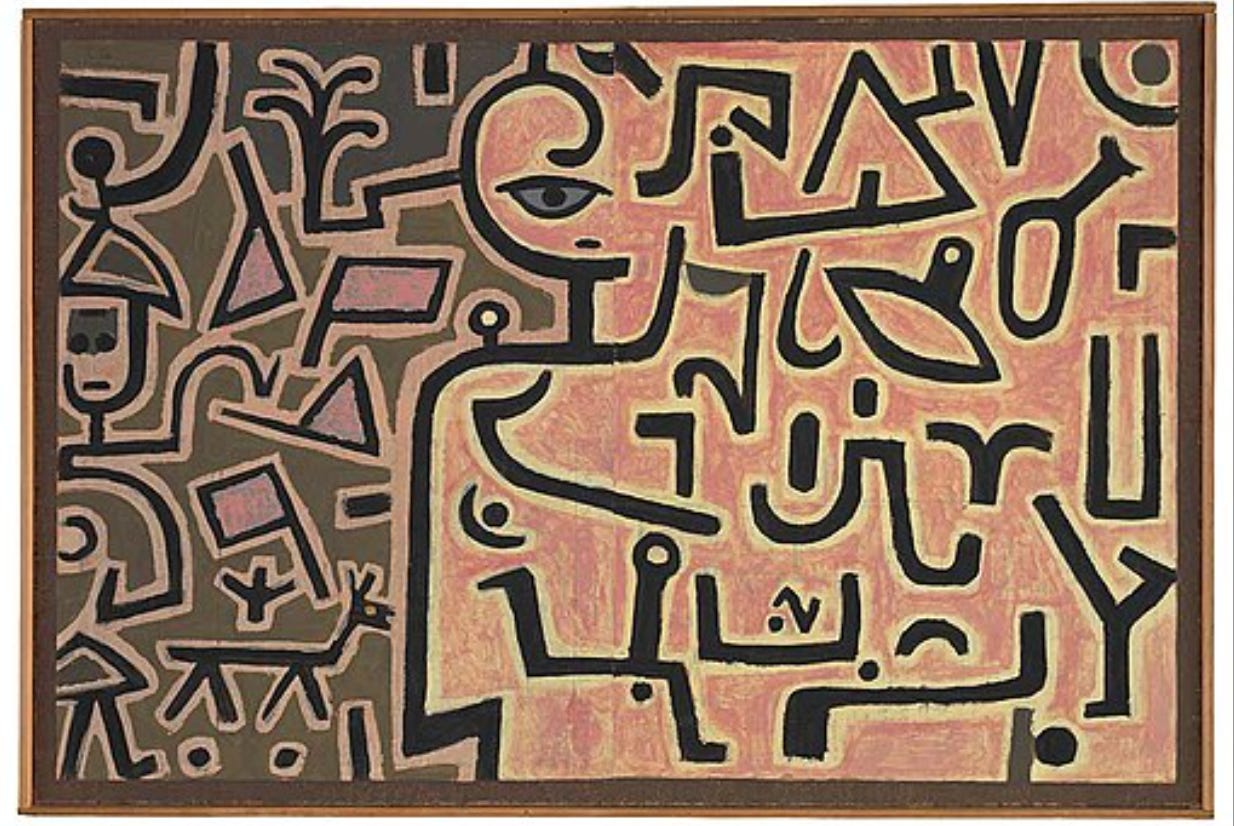

When, six years ago, I was first getting into social media (yes, as recently as that), I chose as my facebook banner this image by Paul Klee.

Paul Klee, Vorhaben, 1938. Source: Wikimedia

Klee’s title is Vorhaben, a compound German noun made up of the prefix “Vor” i.e. in front or before, and “haben” i.e. to have. Vorhaben is the thing you “have “in front of you”, the project or undertaking. That’s the spirit of Chartbook: projects, plans, things ahead of us, stuff to figure out, more to come ….

To mark the occasion and take stock, I thought it would be nice to make a compilation of the 52 Chartbook newsletters to date. My friend and trusty assistant Graham Weaver – without whom finishing Shutdown would have been a complete nightmare – put together this index. Thank you, Graham!

Afghanistan

Chartbook 29: Afghanistan’s Economy on the Eve of the American Exit

Chartbook 30: Back to Afghanistan – the Horror of the 1980s and the Long Recovery

Chartbook 33: From Afghanistan to Haiti

Chartbook 35: It’s Not the Fall that Kills You… Afghanistan’s Looming Triple Crisis

Chartbook 36: After Afghanistan – No Post-American World

Africa

Chartbook 10: Nigeria at a Crossroads?

Arts & Culture

Chartbook 21: Reading Grossman’s Stalingrad and Life and Fate

Britain

Chartbook 6: Britain on the Brexit Brink

China

Chartbook 9: Reading China’s State Capitalism

Chartbook 23: Biden’s China Strategy: A Chronology

Chartbook 26: China’s Hyperinflation

Chartbook 28: China in 1983, a Miracle Waiting to Happen?

Climate Political Economy

Chartbook 17: Realism & Net-Zero: The EU Case

Chartbook 24: Climate, Carbon, and Class

Chartbook 27: Gilet Jaunes (A Spector Haunting Europe)

Chartbook 31: The Mirage of Carbon Markets

Chartbook 32: Biden’s Foreign Policy for the Middle Class, Climate, and OPEC

Chartbook 46: West Virginia – the Historical Roadblock to US Climate Policy

Chartbook 48: The First Climate Kalecki Moment – the Politics of Energy Crisis Talk

Chartbook 50: Andreas Malm and Ecological Leninism

Chartbook 51: Explaining the Energy Dilemma of 2021 – the 2014 Shock and the Global Energy Business

COVID/Vaccines

Chartbook 1: All the Best Charts and Links

Chartbook 2: RECP, the Mounting Pandemic & the Business of Sport

Central Banks

Chartbook 3: Battles over Fiscal Policy, Central Banks and Global Debt Relief

Chartbook 4: Financial Stability Three Ways

Chartbook 12: No Room for Complacency in the Euro Area in 2021

Chartbook 13: Europe Needs to Step on the Gas

Cryptocurrency

Chartbook 15: Talking (and Reading) about Bitcoin

Debt Politics

Chartbook 3: Battles over Fiscal Policy, Central Banks and Global Debt Relief

Chartbook 18: Mario Draghi and Italy’s Years of Crisis

Chartbook 41: The Interlocking Crises that Will Shape the Future of Biden Presidency

Chartbook 49: Global Bond Market Turmoil 2021 – An Explainer

Europe

Chartbook 3: Battles over Fiscal Policy, Central Banks and Global Debt Relief

Chartbook 6: Britain on the Brexit Brink

Chartbook 12: No Room for Complacency in the Euro Area in 2021

Chartbook 13: Europe Needs to Step on the Gas

Chartbook 17: Realism & Net-Zero: The EU Case

Chartbook 18: Mario Draghi and Italy’s Years of Crisis

Chartbook 27: Gilet Jaunes (A Spector Haunting Europe)

Chartbook 40: Newsflash: German Election Beyond the Headlines

Germany

Chartbook 22: How Do You Count Inflation? Tracking Weimar’s Hyperinflation

Chartbook 25: Economic History of World War II and the 18th Brumaire

Chartbook 40: Newsflash: German Election Beyond the Headlines

Global Economy

Chartbook 3: Battles over Fiscal Policy, Central Banks and Global Debt Relief

Chartbook 4: Financial Stability Three Ways

Chartbook 7: Revisiting the Role of Hedge Funds in the March 2020 Treasury Market Turmoil

Chartbook 20: The Caribbean, Central America, and the “Brazilianization” Thesis

Chartbook 43: An IMF-Crisis Made in America

Chartbook 47: Crisis Talk – Global Food Prices

Chartbook 49: Global Bond Market Turmoil 2021 – An Explainer

History

Chartbook 22: How Do You Count Inflation? Tracking Weimar’s Hyperinflation

Chartbook 25: Economic History of World War II and the 18th Brumaire

Chartbook 28: China in 1983, a Miracle Waiting to Happen?

Chartbook 30: Back to Afghanistan – the Horror of the 1980s and the Long Recovery

Chartbook 34: How We Paid for the War on Terror

Chartbook 44: The Cross of Gold – Populism, Democratic Iterations and the Politics of Money

Chartbook 45: Of Scarface & the Nobel: The Double Life of Mariel

Inflation

Chartbook 22: How Do You Count Inflation? Tracking Weimar’s Hyperinflation

Chartbook 26: China’s Hyperinflation

Chartbook 42: The Great Inflation Debate

Chartbook 47: Crisis Talk – Global Food Prices

USA

Chartbook 3: Battles over Fiscal Policy, Central Banks and Global Debt Relief

Chartbook 5: What Happened in the US Treasury Market in March 2020?

Chartbook 14: Are Bond Vigilantes Real? The Strange Case of the 1994 Bond Market Massacre

Chartbook 16: Treasury Markets and the SLR Exemption. When the Financial Plumbing Gets Political

Chartbook 19: American Family Values and Biden’s Families Plan

Chartbook 23: Biden’s China Strategy: A Chronology

Chartbook 32: Biden’s Foreign Policy for the Middle Class, Climate, and OPEC

Chartbook 34: How We Paid for the War on Terror

Chartbook 36: After Afghanistan – No Post-American World

Chartbook 41: The Interlocking Crises that Will Shape the Future of Biden Presidency

Chartbook 42: The Great Inflation Debate

Chartbook 43: An IMF-Crisis Made in America

Chartbook 44: The Cross of Gold – Populism, Democratic Iterations and the Politics of Money

Chartbook 46: West Virginia – the Historical Roadblock to US Climate Policy

US Treasury Market

Chartbook 5: What Happened in the US Treasury Market in March 2020?

Chartbook 7: Revisiting the Role of Hedge Funds in the March 2020 Treasury Market Turmoil

Chartbook 14: Are Bond Vigilantes Real? The Strange Case of the 1994 Bond Market Massacre

Chartbook 16: Treasury Markets and the SLR Exemption. When the Financial Plumbing Gets Political

**********

I enjoy putting out Chartbook and I’m delighted that it goes out free to many readers. If you can afford to support the effort, if you’ve enjoyed a year of great newsletters, why not consider signing up for a paying subscription

The annual subscription: $50 annuallyThe standard monthly subscription: $5 monthly – which gives you a bit more flexibility.Founders club:$ 120 annually, or another amount at your discretion – for those who really love Chartbook Newsletter, or read it in a professional setting in which you regularly pay for subscriptions, please consider signing up for the Founders Club.And if you know someone who might enjoy Chartbook, the holidays are coming up. Why not gift a subscription.

November 12, 2021

Ones & Tooze: electric vehicle charging and the economics of death.

New Ones and Tooze just dropped.

Cameron and I talk about electric vehicles, chargers, the US and China …. and then Cameron takes us down a really wild and dark path about the economics of death, end of life care, COVID, the pandemic and trauma.

Going to come back to this with a post tomorrow filling out the details on the economics of dying. But this is a taster.

You can get it from the Foreign Policy website

November 10, 2021

Chartbook #51: Explaining the energy dilemma of 2021- the 2014 shock and the global energy business.

In 2021 energy prices around the world surged triggering talk of an “energy crisis”.

Why did the supply of coal, oil and gas fall so far short of demand? After an article in the New Statesman and exchange with Richard Seymour I return to the question again not only because the energy industry is complicated and fascinating, but because the answer we give is crucial to locating where we stand in the battle for the energy transition.

The canard that continues to circulate is that the supply shortfall is directly connected to climate policy. Too much talk about net zero has discouraged fossil fuel investors, resulting in lower investment, restricted supply and vulnerability to demand shocks. This idea has an obvious attraction for fossil-fuel lobbyists, who can use it to argue that the energy transition should be postponed. But it also has traction on the left, as argued most recently and explicitly in Cédric Durand in an essay entitled “energy dilemma” on the New Left Review blog. In New Left Review he writes:

“capitalism has already experienced the first major economic shock related to the transition beyond carbon. The surge in energy prices is due to several factors, including a disorderly rebound from the pandemic, poorly designed energy markets in the UK and EU which exacerbate price volatility, and Russia’s willingness to secure its long-term energy incomes. However, at a more structural level, the impact of first efforts made to restrict the use of fossil fuels cannot be overlooked. Due to government limits on coal burning, plus shareholders’ growing reluctance to commit to projects that could be largely obsolete in thirty years, investment in fossil fuel has been falling. Although this contraction of the supply is not enough to save the climate, it is still proving too much for capitalist growth.”

The attraction of this kind of argument for a crisis-theorist of a Marxist bent is obvious. It has about it the ring of a contradiction from which one could then derive a general crisis model. It has also had a surprising amount of currency in the pages of the FT. It is, after all, a plausible-seeming scenario. But, as an account of the 2021 energy crisis it is fundamentally misleading. It attributes far too much influence to climate policy and mistakes the basic dynamics of investment in the sector.

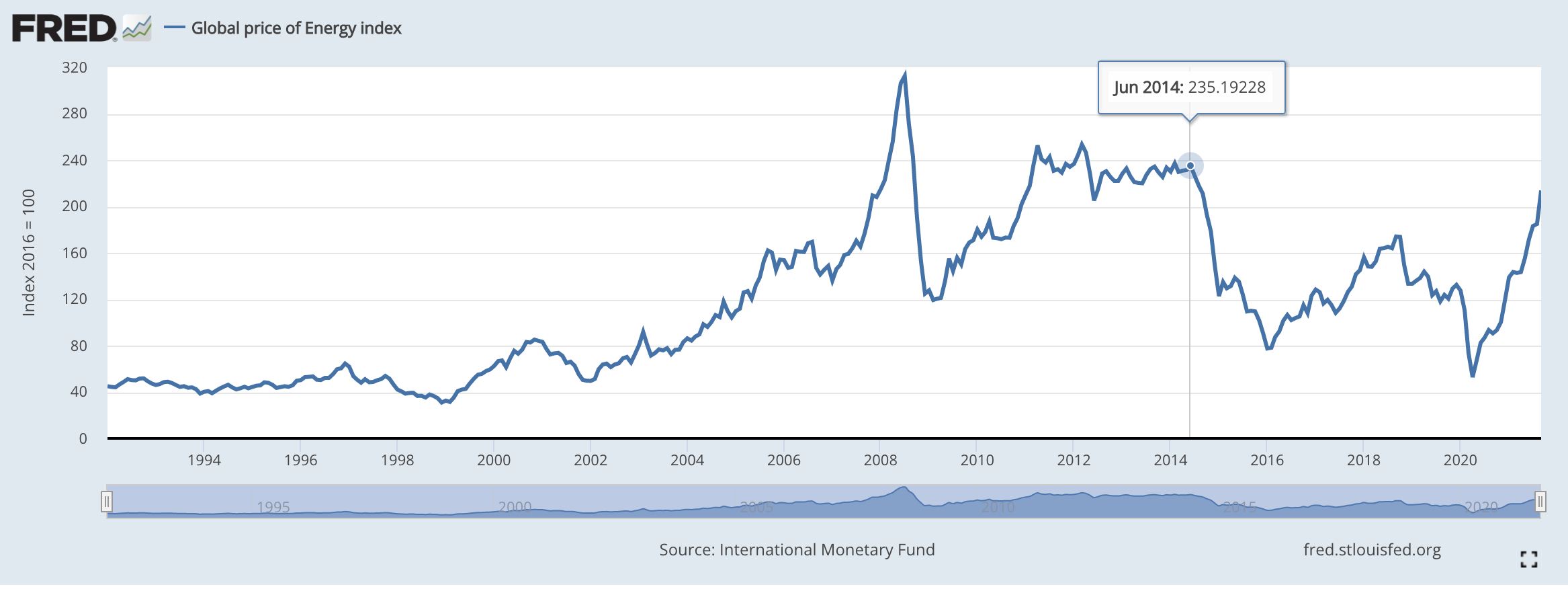

Rather than the political trajectory of climate policy, the starting point for an analysis of developments in the energy sector in recent years should be the energy market price shock of the summer of 2014, when, between the summer of 2014 and 2016, an aggregate index of energy prices fell by two thirds.

Source: FRED

It is this collapse of global energy prices that has dictated both the patterns of investment in the global energy industry, and the balance between fuel types in electricity generation, not only in EU but in the US. Both of these developments have framed the new era of ambition in climate policy, but the causation originates in the energy price shock.

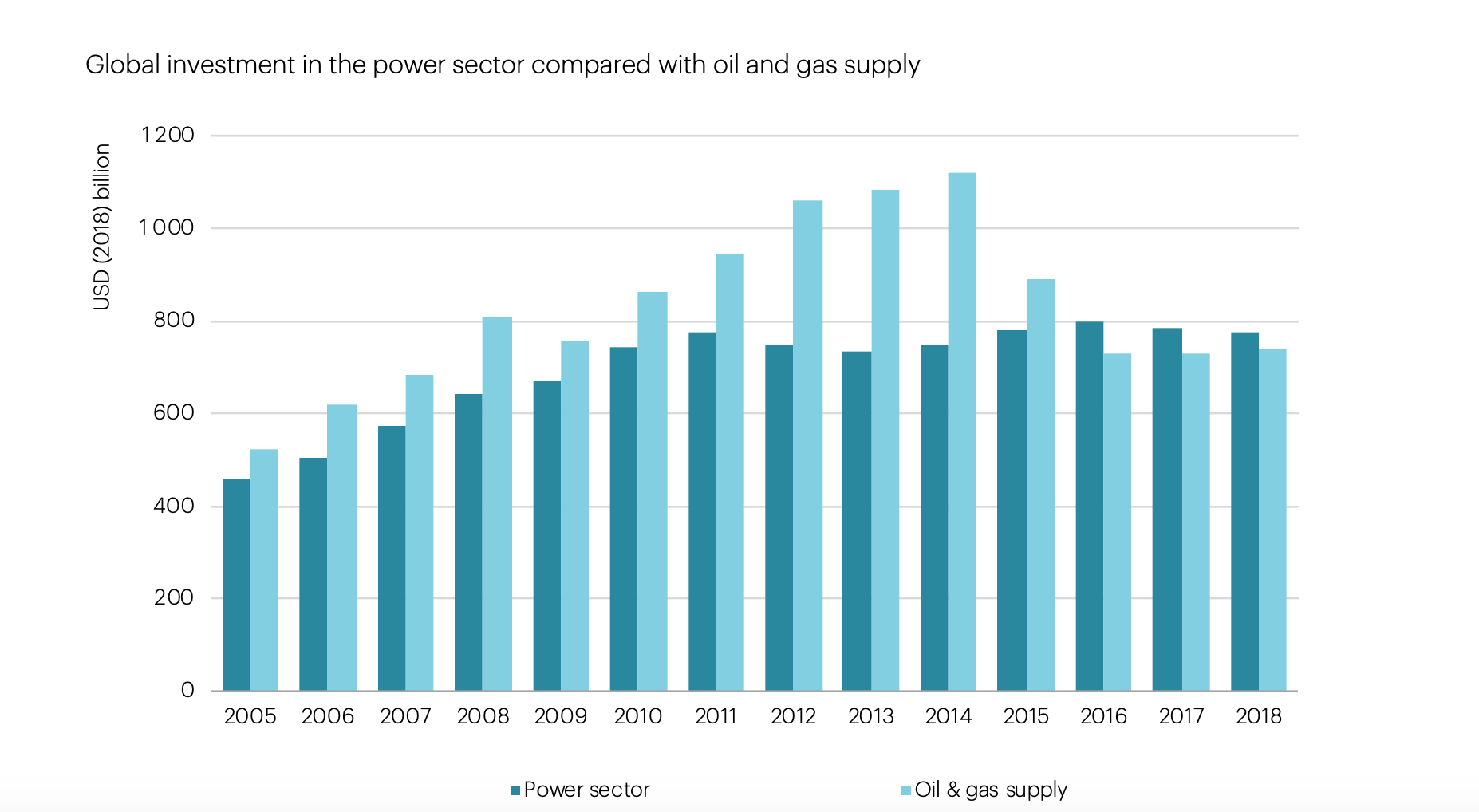

After the 2015 Paris accords, the ramping up of climate ambition did coincide with a slump in gas and oil investment. But, it was not the former that caused the latter. A decline in fossil fuel investment attributable to an increasingly credible commitment to net zero, would likely take place in a gradual way. After 2014 investment plunged.

Source: IEA 2019

The huge shock to energy prices also led to an adjustment in the pattern of energy use. If gas could be bought at rock bottom prices, thanks in part due to the abundance created by the American shale revolution, then flexible gas-fired power plants could replace coal-fired electricity generation. After 2014 the “dash for gas” was key to driving coal out of the power-chain. Even with Trump in the White House the effect continued to operate. Coal was simply uncompetitive relative to gas. Thus, coal dies in Europe and the US in the years after the Paris conference of 2015. But the causal effect runs through the energy market. Both in the US and the EU, climate policy was not just a secondary factor. It was politically enabled by the historic depression in energy prices.

The fossil fuel sector did not so much retreat after 2014 as regroup. The collapse in investment after 2014 was sudden and severe. But, even off their peak levels, investment in fossil fuels continued on a par with the level in 2007-8, just prior to the financial crisis. And costs were lower, so you got more bang for your buck. In the US, the Obama administration, threw its weight foresquare behind America’s new, shale-based oil and gas industry. Literally days after signing the Paris climate accord in 2015, Obama signed off on Congressional legislation authorizing American oil exports for the first time since 1975. For the Obama administration there was no energy dilemma. Pushing climate policy in the Paris-mode was fully compatible with continuing to invest in America’s future as a fossil-fuel superpower. Only blind climate denying GOP ideologues and hired hands of the coal industry would mistake the Obama administration as having been hostile to fossil fuels. For America’s allies, American gas was made of “freedom molecules”, displacing oil and gas sourced from authoritarian regimes. Conventional international carbon accounting does nothing to constrain this logic. Fossil fuel exports are not counted towards national carbon targets. Hence, Saudi Arabia can promise to achieve carbon neutrality by 2050, by powering its own economy with solar, whilst continuing to invest on a massive scale in Saudi Aramco’s export capacity.

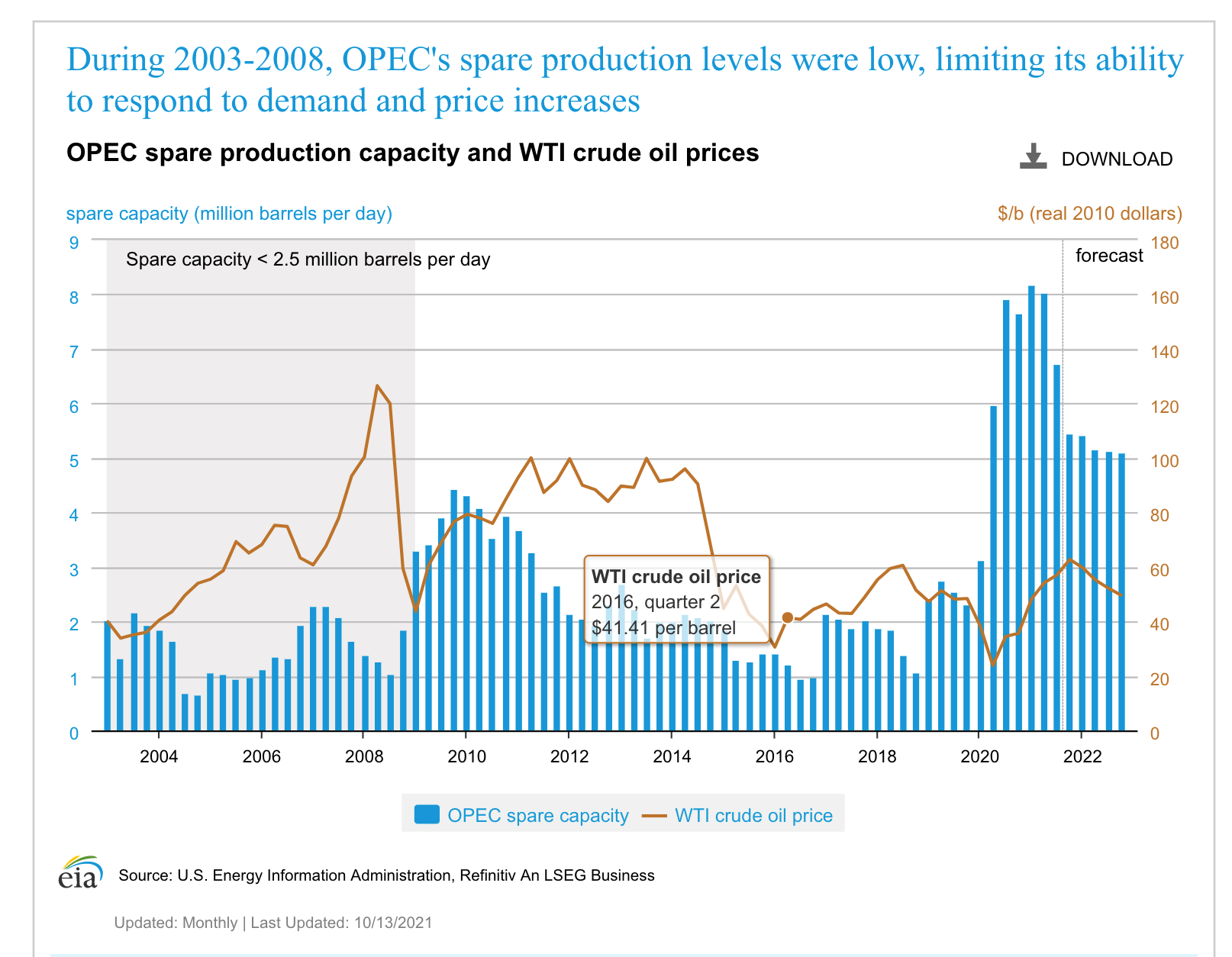

Certainly, the cutback in the rate of new investments suffered by the oil industry after 2014 was not enough to induce any shortage of capacity. In the second and third quarters of 2021, when the surge in oil prices began, America’s EIA estimated that OPEC had the capacity to pump at least 7-8 m extra barrels per day, compared to global demand of c. 100 m barrels per day.

If Saudi Arabia and Russia have recently had problems in surging production, as analysts like Josh Young of Bison Investments observe, it is to do with “logistical hurdles, political turbulence and U.S. sanctions”. Likewise, if there is a force holding back new investment in America’s shale industry today, it is not government climate policy, but the insistence by Wall Street that the shale industry actually pay out dividends rather than plowing back its earnings into new drilling.

You might think that the arrival of electric vehicles would weigh in the balance, darkening the horizon for the oil producers. But Exxon and co imagine a future for themselves as suppliers of feedstock to the global chemicals industry. And as far as Saudi Arabia and the Gulf producers are concerned, given their ultra-low cost base, they know that they will be the global suppliers of last resort. They may, in fact, have an interest in investing in new capacity so as to be able to conduct a fully fledged price war with a view to knocking out their higher-cost competitors.

As far as oil is concerned, in 2021 the energy dilemma is a non-factor. The current surge in oil prices is the result of a deliberate policy decision by OPEC and Russia to throttle production and allow prices to rise. The producers want to take profits to restore their cash balances and reward their investors for their patience since the shock of 2014.

Likewise, though overall gas investment was off its peaks after 2014/5, one can hardly speak of an investment strike in the gas sector. The outlook across the industry globally was buoyant. Worldwide, gas has consolidated its share of electricity generation at c. 23 percent. Given global growth that created considerable need for new investment. Interest was particularly strong in the LNG field – the part of the global gas supply that is traded by long-range carrier rather than by pipeline. Net zero talk has had no obvious impact on a dramatic curve of liquefaction capacity over the last thirty years. America’s ambition to become a major LNG exporter adds a further layer of capacity growth projected to the mid 2020s.

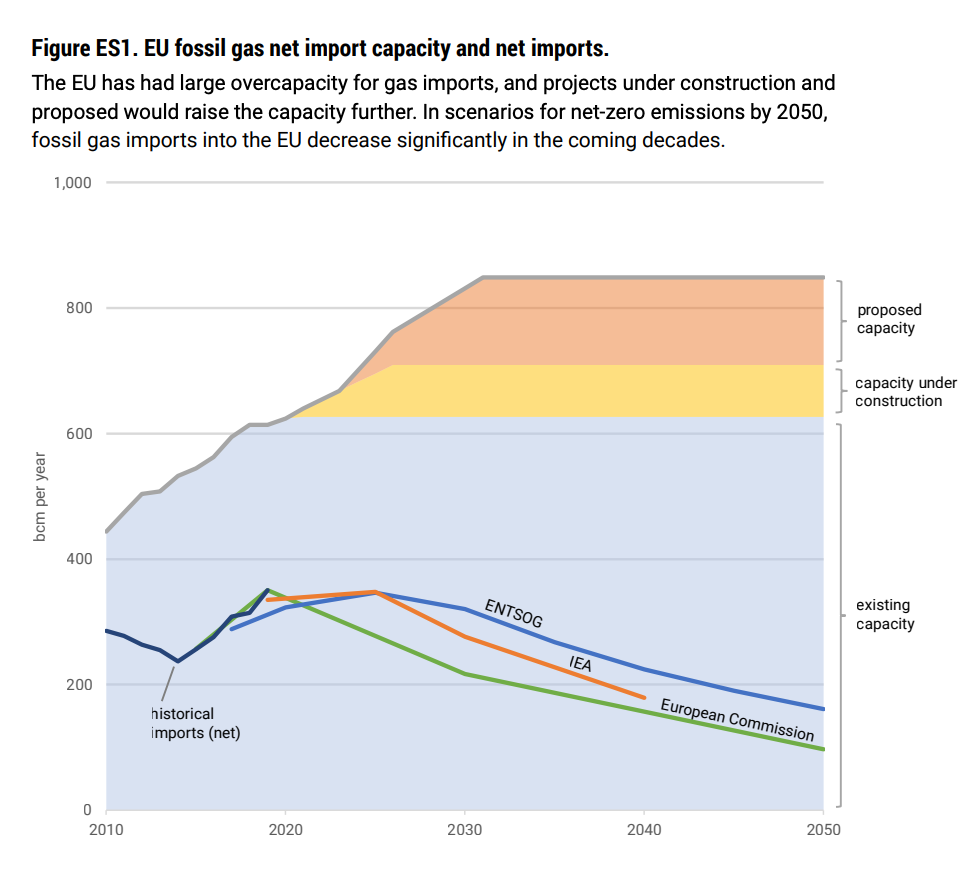

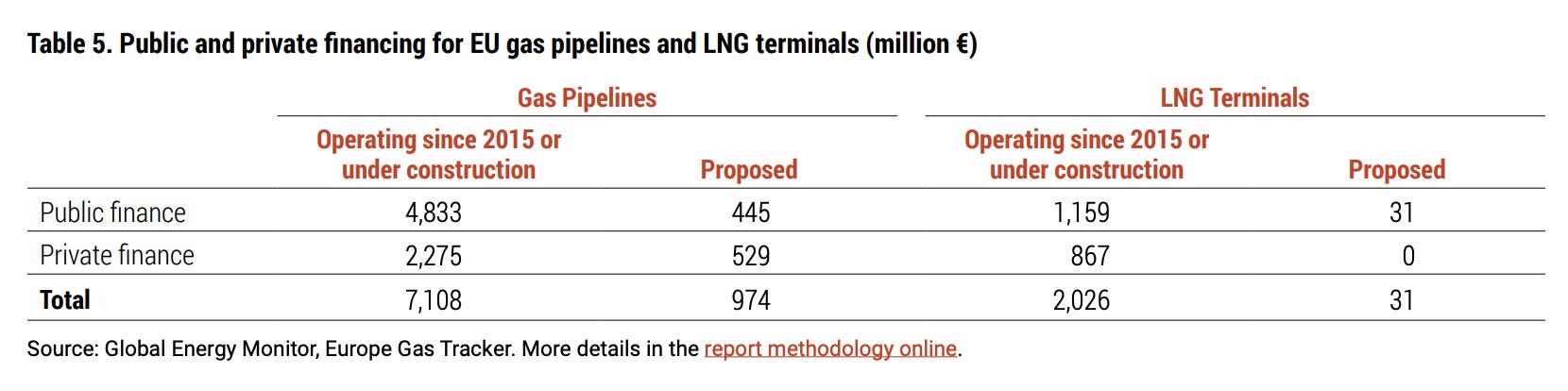

Does the constraint perhaps operate from the demand side? In light of its fulsome commitments to climate policy it would seem obvious that Europe must be seeking to reduce its reliance on both foreign and domestic gas. Along with coal, Europe will in the foreseeable future have to give up on gas too. You might imagine that it would be shrinking its gas transport capacity to a bare minimum. That would then expose it to sudden demand shocks like that in 2021. This is the scenario of the “energy dilemma”. Unfortunately, the reality of Europe’s gas supply situation is almost precisely the opposite. Much as wind and solar have grown in importance, their share of electricity generation was matched in 2020 by that of gas, which since 2014, on the back of ultra-low prices, has seen a dramatic comeback. As Europe’s domestic gas production has fallen sharply in recent years, to fill the gap, Europe has relied on imports. To transport those supplies the EU already in 2010 had pipeline and LNG terminal capacities far in excess of its needs. But rather than treating that as a reason to minimize further investment, it has doubled down. Nord Stream 2 is just the most notorious of a suite of pipeline and LNG terminal projects.

Source: Global Energy Monitor

To reiterate, this investment to the tune of c. 10 billion euros has taken place since the Paris agreement was signed in 2015 and despite huge existing over-capacity. Furthermore, far from public policy squeezing private investment, public money has been thrown into Europe’s gas infrastructure.

Source: Global Energy Monitor

In 2021, that situation is changing. Public funding is being withdrawn. But these long-overdue decisions cannot be made responsible for the gas market imbalance of 2021.

The idea of a secular retreat of fossil fuel investment under the sign of an “energy dilemma” simply misses the mark. Over the last fifteen years, whilst it was trumpeting its commitment first to the Kyoto climate protocol and then to the Paris agreements, the EU made a substantial physical and financial investment in integrating its system of gas supply with global energy markets. Since the early 2000s, the aim of EU gas policy has to been to create a “liberalised” gas market, that amongst other things would reduce its cold war-era dependence on supply and pricing through contracts with Russia. Furthermore, the EU has moved to pricing gas not on the basis of long-term supply contracts but by way of the spot market. Seen from this point of view, the huge capacity of pipelines and LNG terminals is not redundant. It is the physical infrastructure that has enabled Europe to play the global gas markets.

Gas is less polluting than coal, but this strategy was not driven by the desire to minimize CO2 emissions, but to minimize energy costs and achieve energy security. This is a crucial point to emphasize. Shifting back to gas after 2014 played a key part in Europe’s climate policy in the years immediately following Paris. And it is through gas that the global energy shock of 2021 has arrived in Europe. But gas was not adopted by Europe’s electricity generators to minimize CO2 emissions. Until recently, the cost of emitting a ton of CO2 was so low that electricity generators in Europe had little reason to consider the climate implications of whatever fuel they were using. It was not until August 2018 that the price of emitting one ton of CO2 for a European power plant rose above 20 Euros. The aim of investing in gas import capacity was to take advantage of low fossil fuel price world. Thanks to ultra low global gas prices, since 2014, according to IEA estimates, the EU’s strategy of relying on global markets saved $ 70 bn. But by the same token it was also exposed to the shock suffered by the global energy economy in 2020. It is above all through the gas market that Europe and Asia were interconnected as arenas in the “global energy crisis”.

**********

In 2021 the serious electricity shortages in both China and India were an essential part of the energy crisis narrative. By mid October 2021, India’s coal supply situation was critical. “17 thermal power plants had zero days of coal stocks as of October 10, with production and despatches from coal mines falling short of demand. Another 26 plants had stocks for one day. … that’s about 31% of the power from coal-fired thermal power plants.” But the operative term here is coal. Unlike in Europe and the US, China and India’s main source of electricity supply is burning coal. Between the two of them, they entirely dominate the global coal market. They also, however, rely for the most part on domestic sources of coal. In India’s case, domestic production covers 95 percent of power needs. How then was this part of a global energy crisis?

In the case of India, it really wasn’t. The shock of rising global prices would not, by itself have propelled a crisis in India. The Indian crisis that did occur could have occurred without any outside forces involved. Furthermore, in the course of 2021 India uncoupled from the global energy system. So, its local difficulties in fact relieved pressure on global markets. The reason that India does belong as part of the global narrative is that its national crisis resulted from the common experience of uneven and haphazard recovery from the COVID crisis. As India’s recovery began in earnest in 2nd quarter of 2021, India’s largely national electricity system came under huge pressure. It was, in effect, an intense, local supply-chain crisis.

India can certainly be described as facing an “energy dilemma”, but net zero is not the issue. The question is how to organize the supply of power to hundreds of millions of low-income consumers. Who in the supply chain should bear the costs and risks? Coal India the giant mining conglomerate sells coal to generators, who burn it and sell power to distributors who supply power to business and retail customers at rates, set by regional governments, that are amongst the lowest in the world. The fixed prices squeeze the finances of distributors. They, in turn, often fail to pay generators, leaving them unable to pay Coal India. Coal India retaliates by restricting the generators to delivery-against-payment, limiting their ability to build adequate stocks of coal. The dramatic reduction in coal stocks at the generators was less a symptom of coal shortages than shortages of cash.

The surge in global energy prices did no more than exacerbate this domestic squeeze. Given fixed local power prices, the surge in world prices caused coastal generators that normally use imported fuel to shut down, shifting load to inland producers, or to shift demand to Coal India, increasing pressure on limited supplies. The effect, as Reuters reported was actually to cut India’s demand for global coal, relieving pressure on global markets.

Could more coal have been supplied? Perhaps. But if so, the shortfall was not due to environmental concerns. Critics accuse the Modi government of milking Coal India’s balance sheet to help cover government deficits. Production has stagnated. As the economist M.K. Venu points out in The Wire, in 2016 the Modi government had sought to bring big private players into coal production. But the promised 130-150 m tonnes of production had not materialized. Why not?

The private sector was complacent because global prices of coal were consistently low, incentivising imports over investment in domestic capacity. Typically, private miners invest when global prices are high. As the private sector delayed coal production, the Centre also took its eye off the ball and did not give follow-up clearances for exploiting new coal blocks.

In any case, when the crunch came in 2021, Coal India was able to surge production considerably above 2019 levels. Production and deliveries were higher in September 2021 than in 2019. The immediate problem was not so much inadequate coal production, but the parlous financial state of distributors and generators.

********

If India’s energy crisis was part of the global crisis more in the way of sharing a common experience than in being causally interconnected, the reverse was true for China. The causes of its energy supply difficulties in early 2021 were highly idiosyncratic. But the causal ramifications for the rest of the world were dramatic.

The precise causes of China energy’s crunch are complex. There is no doubt that deliberate decisions by Beijing to regulate coal-fired electricity generation played a key part. In this sense this is where the energy dilemma narrative really bites. But the dilemma in question is once again rather different than the one commonly invoked. It is driven by a deliberate national policy to throttle coal use rather than any indirect effect on private investment and it plays out transnationally and by way of the spillover of Chinese supply constraints both from coal and low-carbon sources, to global LNG markets.

As one leading LNG expert commented in June 2021: “Rising electricity consumption has been in the spotlight since the start of 2021, driven by China’s economic recovery.” Normally this would be met by coal and renewables. But, “In the first four months of this year, gas-fired power generation jumped 14% year-on-year. Strong electricity demand has been a key driver for increased LNG imports in southern China in particular, as gas provides the critical peak-shaving supply into that market. With hydro generation in southwest China curtailed by lower rainfall and solar power output below expectation, Guangdong province has experienced a shortage of electricity imports. Tightening power supply options in China’s industrial heartland have come as power demand continues to rise on the back of solid export-led industrial growth and the early arrival of higher summer temperatures.”

China was not hitherto the leader in the global LNG market, or even the East Asian LNG market. “For as long as most can remember, Japan has been the world’s largest LNG market.” Unlike China or Europe, Japan had no other practicable way of accessing gas. “The country’s utilities and trading houses underpinned decades of LNG supply growth, signing long-term contracts that formed the bedrock of the industry.” Now in early 2021, China overtook Japan as the largest importer of LNG. It was that historic shift that triggered the remarkable escalation of East Asian spot prices for gas in the autumn of 2021. In Asia, however, the impact of those recored spot prices is easily exaggerated. Only around 35 percent of Asian gas is priced at spot prices. In Europe the situation was far more serious. There, 80 percent of gas pricing was on a spot basis. That is how the energy crisis spread to Europe.

*********

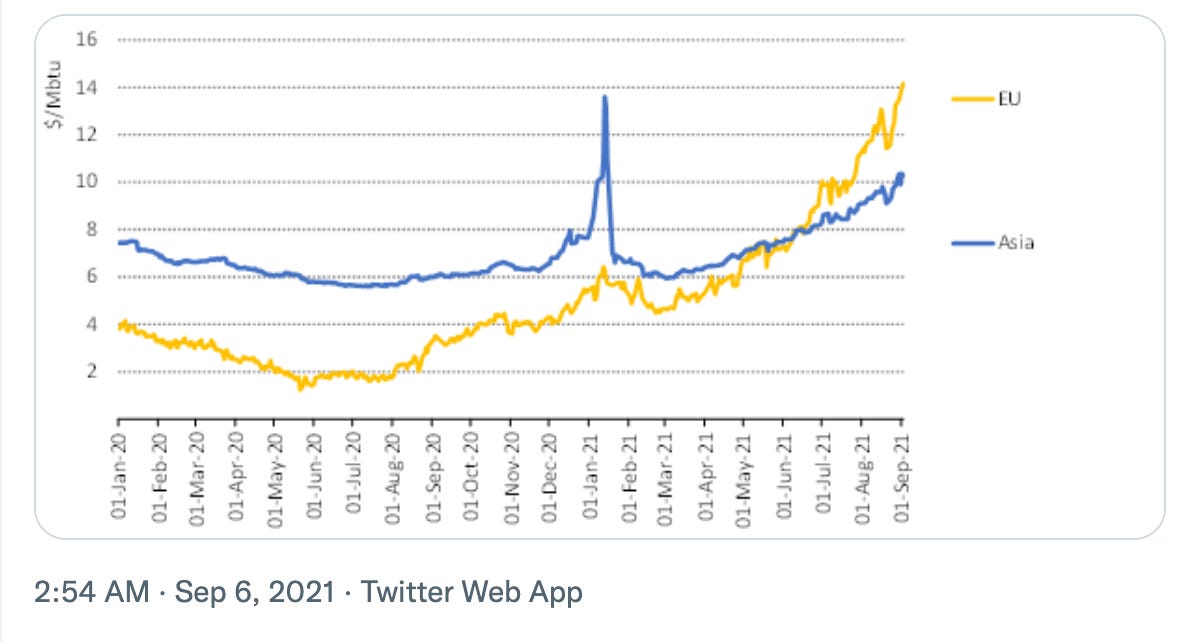

In the good times of low gas prices since 2014, Europe bought the cheapest gas on offer and diversified away from Russia. But when markets got tight, the boot was on the other foot. In 2021 Europe was competing with Asia for its gas and it was paying the price. This very illuminating graph shows the average prices paid by European and Asian consumers, weighted for the share that was price at spot rates.

Source: Peter Zeniewski

Ordinarily, to escape the squeeze on gas, Europe might have switched back to generating electricity from coal. But coal prices were elevated by the bottlenecks in China and India and by a surge in the price of emissions permits in the EU-ETS. This is how the green factor finally does enter the European story. The EU-ETS had long been a dead letter. But in early 2014 it had been subject to tough reforms. They tightened the supply dramatically. The full effect had not been noticeable at first because energy prices collapsed. Then in 2018 prices in the EU-ETS began to rise, hitting 60 euros per ton in 2021. At that point there was no switching back to coal.

Source: Trading Economics

*******

So the issue is not that post-Paris climate ambition depressed investment, narrowed margin of supply and created conditions for spike. That entirely exaggerates significance of green policy. What 2021 exposes is that the green push since 2015 has been enacted against the backdrop of a regime of low energy prices set by the price collapse in 2014. On both sides of the Atlantic, the extremely low price for gas delivered a series of easy wins for climate policy. Emissions in the US power sector went down even under And then the switchback of 2020 hit, China’s gas demand surged and everyone was found out. The lesson is not that the EU has been pushing green too hard, too fast. The lesson is that if China and the rest of Asia embark on a huge dash for gas, Europe’s investment in market-based gas import model is very high risk. The logic of diversifying away from Russia was good, until you ran into China. The solution is not less commitment to the energy transition but more. But here too, the 2014 price shock has had its effects. Though seen from the side of power generation, the shift to wind and solar has continued, viewed from side of finance, investment in renewables in Europe has been flat since 2015. In 2019 it actually fell sharply. This was less catastrophic than it seemed because of the fall in the cost of solar panels. But it was far from the dramatic acceleration that might have ben hoped for in light of rhetoric.

November 7, 2021

Chartbook #50: Andreas Malm and ecological Leninism

In recent weeks I’ve taken a deep dive into the writing of historian and activist Andreas Malm. A long review just appeared in the LRB.

Malm is, simply put, one of the most productive and provocative historical thinkers on the left right now.

Malm can be read in many ways. In my essay I deliberately foreground his interventions as acts of historical interpretation. In particular, in the LRB essay I argue that his most recent writings are efforts to read our current crisis by way of the history of WWI, Russian Revolution and civil war, as compared to the far more comfortable 1940s analogy offered by the Green New Deal.

I was no doubt predisposed to read Malm this way because of my own skepticism about the Green New Deal’s historical references. On this, see my Foreign Policy essay from January 2020.

But this framing of the LRB essay also helped me to distinguish the latest phase of Malm’s work – dated broadly to 2019-2021 – both from his own earlier interventions and other work in Marxist ecology.

**********

Ecological Marxism is a large and multi-stranded school. At its heart is the critique of loose talk about the Anthropocene. The idea of putting humans (Anthropos) at the heart of the story made sense in a natural scientific context. It captures the fact that humans now stand alongside glaciers as movers of the earth’s surface. But when transferred from the natural sciences to a more general description of reality, the notion of the anthropocene induces a profound misconception. Though it is true that climate change is human-induced, it is not true that humans in general have that impact. It is the economic system and those who manage and profit from it who do. The epoch of crisis that we are in should really be called the capitalocene.

In the work of many writers in this school, for instance Jason Moore, the notion of the capitalocene takes you back to the early modern period. Malm’s historical work to date is distinctive for its focus squarely in the classic Marxian period of the 19th century. His first book Fossil Capital is a directly on the terrain of Kapital volume 1 and Marx’s Grundrisse.

In many environmental histories of capitalism the arrival of the dark satanic mills of 19th-century industrialism is the telos towards the which the whole story develops. It is the place that we know we are going to end up. Malm’s pivotal contribution in Fossil Capital lies in throwing open the question of obviousness and delivering a scorching critique of the most familiar explanations for the world-historic shift in the energy system.

In the mainstream that Malm is criticizing there are three predominant views of the coming of the steam-powered factory. Malthusian economic historians (most prominently Tony Wrigley and Ken Pomeranz) argue that by the late 18th century, the European economy was running out of fuel and found an answer to this functional imperative in the form of coal. For other writers, the mastery of steam power is simply the development of humanity’s long coevolution with combustion. Managing fire is part of what makes us human. Finally, one can see the advent of steam as first and foremost a technological achievement born out of the scientific revolution and the logic of discovery and enquiry.

Each of these narratives, in its own way, aligns fossil fuel revolution with necessity. For the Malthusians the industrial revolution follows from the imperative need to find ways of overcoming the scarcity of firewood and food. For others it follows from human nature and our drive to mastery. Or, finally, it follows the necessary logic of scientific development.

The problem, according to Malm, is that none of these plausible theories is actually empirically persuasive. Malm argues that through to the mid-nineteenth century, water power was a fully viable economic alternative – both abundant and cheap. To understand what is going on we have to go inside the factory to see how fossil fuels enter as the essential but hitherto unacknowledged complement to the struggle between capital and labour. What was ultimately decisive in Malm’s view was the question of control, or in Marxist terms real rather than formal subsumption. Ultimately, what shaped the technological choices of the British industrialists was the class struggle.

Mobilizing the stock of fossil energy layered under the ground was the weapon with which British capitalists fought back against the upsurge in unionism and Chartism in the 1830s and 1840s. Water was cheap and abundant, but unlike the power unleashed from coal, it could not be controlled. As Malm remarks, “If the autonomy of the working class is to be fought by a regiment of machinery, the prime mover – the field commander – had better be reliable.”[1]

Autonomy is the key word here. Though the basic insight of the role of coal is to be found in Marx’s Grundrisse, it was Italian Marxists of the so-called autonomist school, struggling in the 1960s and 1970s to make sense of the new abundance of Fordist mass production, who insisted on the fact that technology and class struggle were not separable. As Toni Negri, one of their leaders put it, the basic challenge facing the employer was to subjugate the autonomous potential or Potenza of human labour. The machine was the means for doing so. The classic separation of forces and relations of production was false. In fact the relations of production (as in class struggle) were inside the machinery itself. What Malm adds is the recognition that the driving force of that coercive synthesis is the mobilization of fossil fuels.

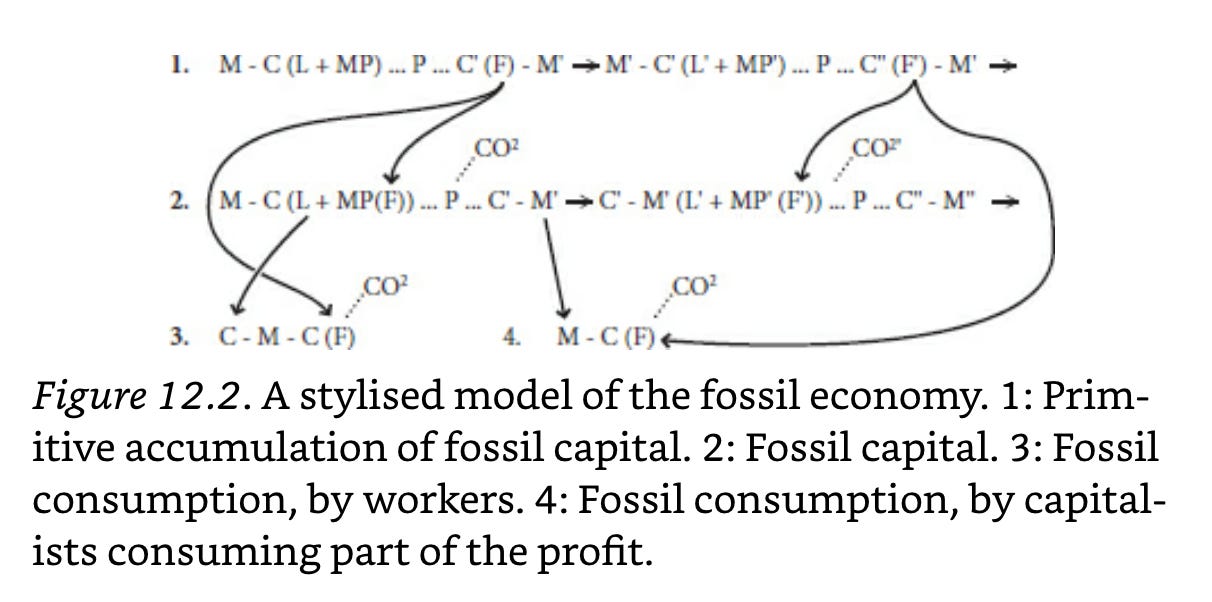

Source: Fossil Capital

This isn’t just an imaginative theoretical and historical move. It grounds Malm’s skepticism towards the possibilities of reform today. If the relationship between non-renewable one-way exploitation of stocks of energy and the birth of capitalism is not accidental, if it is entangled in the most basic logic of surplus-value-generation, it will be far harder than is commonly imagined to dissociate capitalism from fossil fuels.

Ultimately, a system reliant on the unpredictable flows of natural energy, does not permit the same kind of comprehensive subordination enabled by the unlocking of stocks of coal, oil and gas. It is naïve to imagine that you can simply change the technology and leave the old relations of power and economy in place. In the limit, this would be imply that only comprehensive revolution or a truly coercive state apparatus can impose the energy transition we need.

*******

If Fossil Capital was Malm’s opening statement on political economy, the Progress of the Storm begins his turn to the present. It is withering overview of our current intellectual condition. The “storm” of the title is the climate emergency viewed also through the lens of Walter Benjamin’s famous meditations in the philosophy of history. And what the angel looks back on is not just the wreckage left by fossil-fueled progress, but a disordered and disorientated intellectual landscape.

The idea that the continued destruction of the environment is enabled by a fog of doubt and confusion is of course all too familiar. Corporate-backed climate denial is perhaps the favorite target of liberal climate activists. Refusal of the logic of climate science is the cardinal sin. But Malm’s target here is not simply climate denial, what he identifies is a far more comprehensive loss of intellectual bearings. In the manner of a Marxist cultural critic like György Lukács or a Frederic Jameson, Malm diagnoses an intellectual derangement that affects much of what passes for critical thinking too.

If postmodernity is a malaise of amnesia and displacement – as though time and nature had in fact disappeared – we might think of the warming condition as a realisation, in the dual sense of the term, of a more fundamental illness or wrongness in the world.

Malm, Andreas. The Progress of This Storm . Verso Books. Kindle Edition.

In what is his most aggressive work to date, Malm lays waste to the contemporary intellectual scene. It is an intellectual bloodbath worthy of a Bolshevik bull session. The stakes are far too high for muddy thinking. Malm is there to put things back on their feet.

********

Climate, Corona and Chronic Emergency and White Skin, Black Fuel are historically bookended by these two earlier interventions.

Between Fossil Capital on the classic Marxian terrain of the 19th century and The Progress of This Storm on our current intellectual scene, Malm now inserts Climate, Corona and Chronic Emergency on war communism and White Skin, Black Fuel on the fascist period.

As Barnaby Raine pointed out to me, the “war communism” theme is one that Malm shares with the group of Marxist authors known as the Salvage Collective. Their recent manifesto The Tragedy of the Worker. Towards the Proletarocene begins with the classic lines from the Communist Manifesto:

“Workers of the world unite, you have nothing to lose but your chains. You have a world to win.

But then continues:

What if the world is already lost? This is the question that vexed us as we set out to write The Tragedy of the Worker. From the vantage point of the present, the history of capitalist development is, as Marx expected, the history of the development of a global working class, the proletarianisation of the majority of the world’s population. But the very same process of that development has brought us to the precipice of climate disaster. Our position, position, to recall Trotsky’s rationalisation of War Communism in 1920, is in the highest degree tragic.

It is now clear that we will pass what scientists have long warned will be a tipping point of global warming, accelerating the already catastrophic consequences of capitalist emissions. How do we imagine emancipation on an at best partially habitable planet? Where once communists imagined seizing the means of production, taking the unprecedented capacities of capitalist infrastructures and using them to build a world of plenty, what must we imagine after the apocalypse has befallen us? What does it mean that as capitalism has become truly global, the gravediggers it has created dig not only capitalism’s grave, but also that of much organic life on earth?”

One of the issues at stake here is clearly the need for radical thinking to turn away from the kind of cornucopian promise that was crucial to 19th-century Marxism and has recently been revived by Aaron Bastani in his Fully-Automated Luxury Communism.

For all his visions of communist austerity Malm is anything but a technophobe. He insists that the left must overcome any hang ups about large-scale technology including both nuclear and large-scale carbon capture. On this score, check out:

Has It Come to This? The Promises and Perils of Geoengineering on the Brink.

What is left more open-ended is how far Malm believes that capitalism as such can adjust to a new technological basis.

In light of the foundational analysis in Fossil Capital, it is hard to see how capital accumulation in the form that we know it today can continue without the large-scale harnessing of non-renewable stocks of fossil fuels to the labour process. That, after all, is for Malm, the foundation of profit.

But, if Malm cleaves to this position, it rules out any real compromise with the Green New Deal and reformist camp. In White Skin, Black Fuel, as I indicate in the LRB review, he seems to open the door to compromise. He does so by recognizing a distinction between extractive fossil fuel capitalism i.e. coal, oil and gas extraction, which will have to be wound up, and other forms of business, which may be able to make the energy transition. That would seem to open the door at least to a tactical compromise with those advocating for a Big Green State.

*********

Compared to such subtle shifts in emphasis, the break between How to Blow up a Pipeline and Malm’s earlier work is far more sharp. He is as provocative as ever and as imaginative in the use of historical arguments for current political purposes, but what has gone is the direct reference to the Marxist tradition. This was ruled out constructing a review for the LRB that covered all of Malm’s work to date. I couldnt see a way of bridging the gap and resorted to the historical framing instead.

The intellectual inspiration for the How to Blow Up would seem to be Fanon. In this respect there is a continuity to White Skin. Black Fuel.

But what is missing from How to Blow Up is any reference to Lenin.

It would be tempting to suggest that this is due to Lenin’s disapproval of terrorism. But that is in fact simplistic. As recent scholarship on Lenin has show, though Lenin did not favor individual terrorism, he was far from dismissive of “mass violence” as a revolutionary strategy.

The more obvious reason for Malm’s downplaying of ecological Leninism as a theme in How to Blow Up is the context in which he is intervening. Malm is writing for a specific contemporary context in which extensive references to Lenin would be far from helpful to his cause.

In the LRB piece I frame Malm’s provocative stance in How to Blow Up a Pipeline against the very specific historical situation of the German climate movement between the anti-coal mobilization of Ende Gelände and Fridays for Future. James Butler in his essay on Malm in the same issue adds an excellent panorama of further mobilizations.

For a sense of what was at stake in the German debates, this remarkable dialogue between Malm and Tadzio Müller, one of the organizers of Ende Gelände, is both entertaining and highly instructive.

What is nevertheless striking is the fact that Malm does not engage more systematically with the full range of experience of movements that have sought to combine violent direct action with other forms of political protest. Of course, there are some instances in which this was successful. But there are many others in which this combination of tactics ended in division, isolation and disaster.

Toni Negri who was one of the inspirations for Malm’s early work, paid the price for the disaster of radical militancy in Italy. He spent years in jail and emerged from the “years of lead” scarred and profoundly disillusioned with that form of tactics. In later writing he would diagnose the turn to terrorism as misguided.

Ulrike Meinhof, in fact, does make an appearance in How to Blow up a Pipeline, but only buried in the footnotes. In the text itself she is coyly referred to as “a German journalist” reporting the views of a black radical activist visiting from the US.

Malm no doubt agrees with Negri’s analysis, but he does not give us a more elaborated analysis of what the precise conditions are under which he favors escalation. And, as James Butler suggests, the question must be asked too about the Ende Gelände model that is for Malm the touchstone. It too, after all, ended in failure.

*******

As Malm makes clear in How to Blow up a Pipeline, he refuses to accept historical success and failure as the ultimate criterion of judgement or meaning. After all to do so would write much of the radical tradition out of history. Malm advocates direct action in part as a tonic to the demoralization that results from living in the cognitive dissonance of climate capitalism. And he recommends it on the basis of personal experience. As he describes his involvement in the 2016 Ende Gelände action:

“If destroying fences was an act of violence, it was violence of the sweetest kind. I was high for weeks afterwards. All the despair that climate breakdown generates on a daily basis was out of my system, if only temporarily: I had had an injection of collective empowerment. There is a famous line in Wretched of the Earth where Frantz fanon writes of violence as a “cleansing force”. It frees the native “from his despair and inaction; it makes him fearless and restores his self-respect.” … there has been a time for Gandhian climate movement; perhaps there might come a time for a Fanonian one.”

In How to Blow up a Pipeline the ultimate touchstone of significance for Malm is, at least on my reading, the heroic resistance of Jewish fighters against Nazi extermination policy. This takes up several dramatic paragraphs in the book.

It struck me this way no doubt in part because I am particularly sensitized to historical references to World War II and the Third Reich. I had written about Vasily Grossman’s definition of freedom in relation to death only a few months earlier, in Chartbook #21.

And I emphasizes Malm’s references to the Jewish resistance Nazism, also as a way to anchor How to Blow up a Pipeline in the same historical conjuncture as War Communism and fascism. Ultimately, on the reading offered in my LRB essay, it is that shared historical imaginary that links Malm’s three most recent interventions as a single unit and counterposes them against the more optimistic Anglo-American Green New Deal framing. Historical imagination bridges the theoretical discontinuities to Malm’s earlier work.

There is, however, also another anchor for Malm’s vision of historically meaningful, if unavailing struggle and that is the ongoing Palestinian resistance. Malm spells out the connection in a remarkable essay for Salvage in 2017.

Not only is Palestinian history an allegory for the kind of displacement that much of the world’s population may suffer over the next century, if the climate crisis is not contained. There is also an interconnected material history of power, colonialism and fossil fuels, by way of the history of fossil-fueled Western power in the region, Middle East oil and the pipelines that channel it to Western markets.

*******

Malm’s work is instructive, brilliant and unsettling.

His historical imagination is fascinating and inspiring.

His arguments pose a serious intellectual challenge to complacent reformism.

The extent to which they become an actual political challenge will depend on the degree of reformism’s success in delivering real progress on the energy transition.

That is the historical test that can no longer be dodged.

November 6, 2021

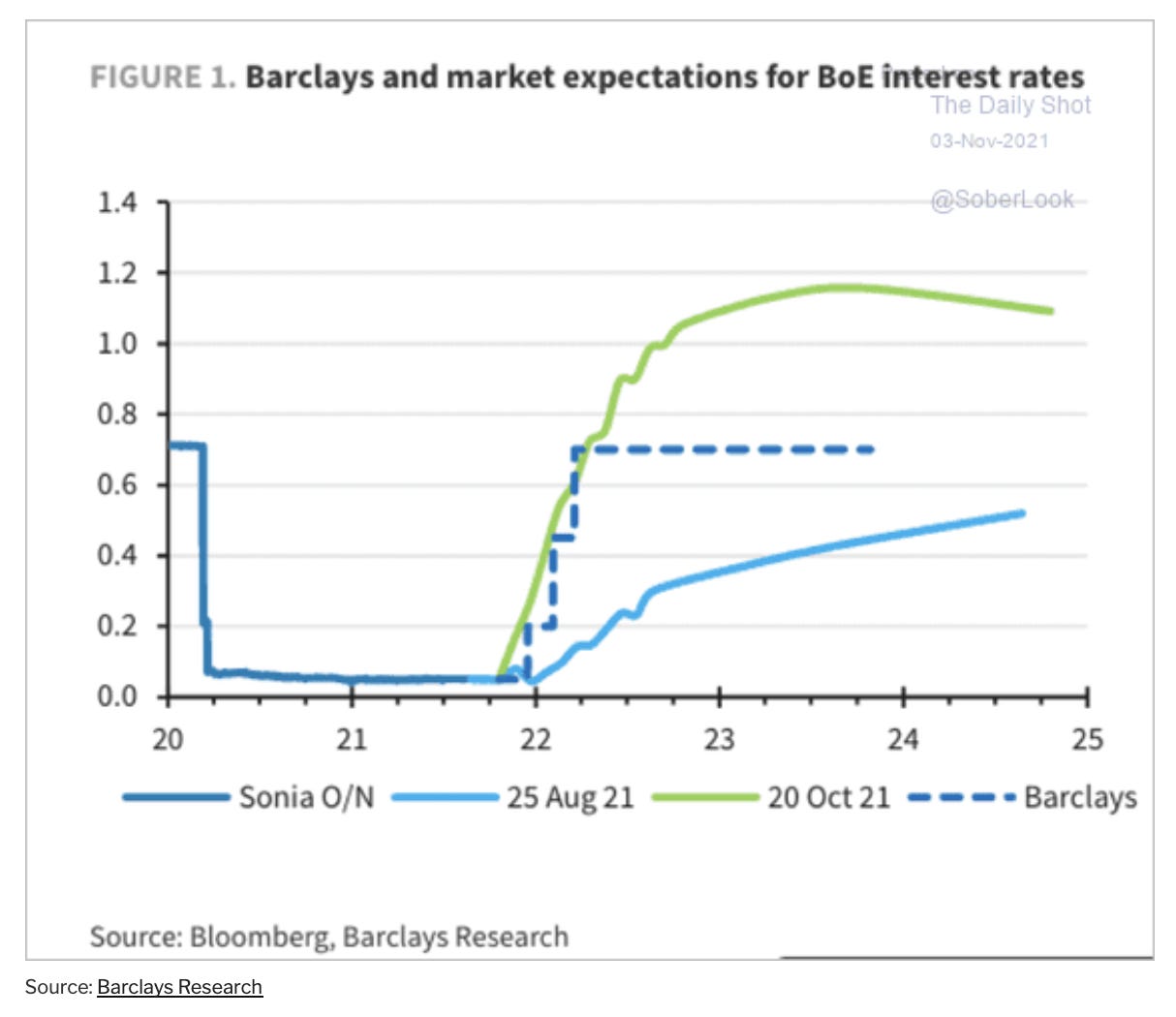

Ones and Tooze on the bond market turmoil and Carney’s trillions

The latest Ones and Tooze posted Friday. Recorded from Lisbon, Cameron and I talk bond markets, central banks and big money at COP26.

Listen below or subscribe via the Foreign Policy website, here.

Since we recorded the episode even the Bank of England, seemingly the most hawkish of the Anglosphere central banks has declined to raise rates.

Markets adjusted their expectations for rate rises, and the pound sold off.

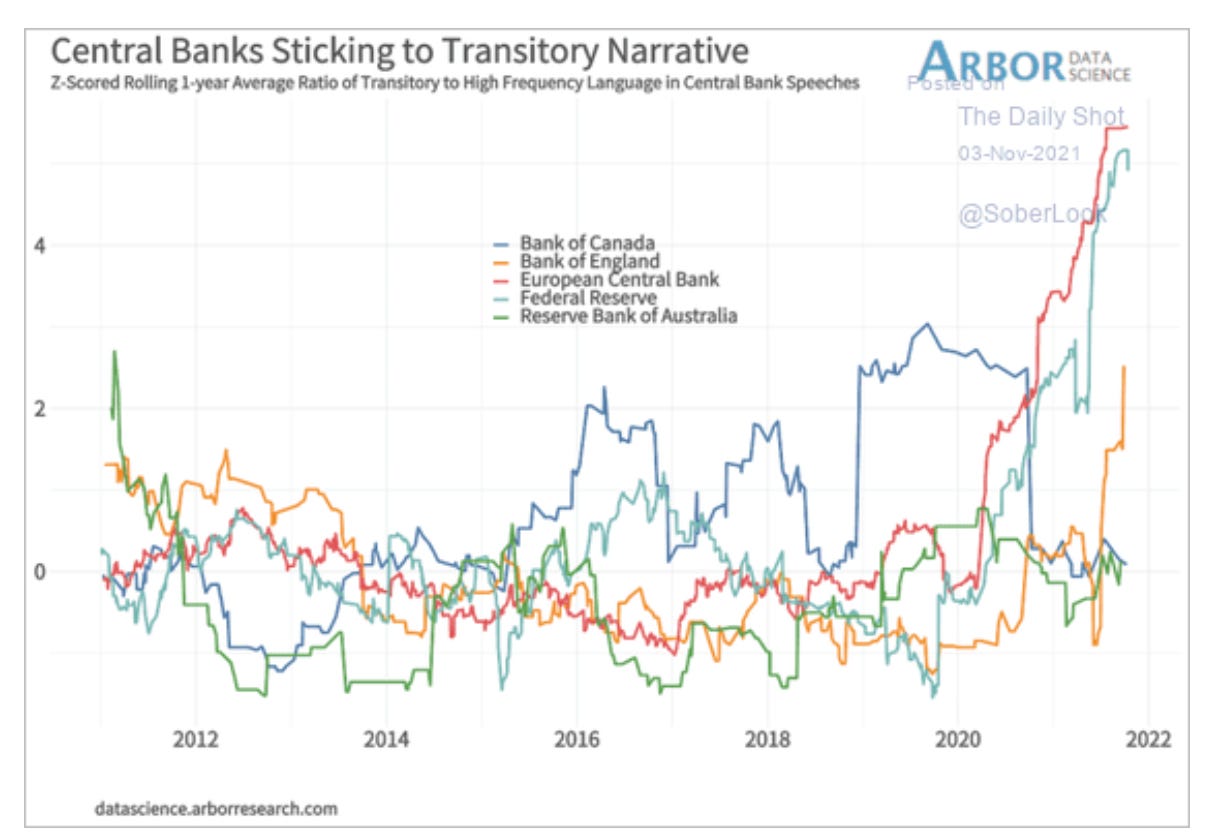

The “inflation is transitory”-narrative remains the main game in town, anchored both by the ECB and the Fed.

To get all the chartbook bells and whistles regularly to your email inbox, sign up here:

November 5, 2021

Ones and Tooze: Jerome Powell vs. The Bond Markets

On this episode, Adam Tooze and Cameron Abadi discuss the moves and countermoves of the bond market and the Federal Reserve Chairman in response to inflation.

Also: A new alliance of banks and investment funds is committing $130 trillion to carbon neutral projects in the next 30 years. Green altruism or green washing?

Learn more or subscribe on the platform of your choice at Foreign Policy.

Adam Tooze's Blog

- Adam Tooze's profile

- 767 followers

{kind=link}

{kind=link}

_by_Paul_Klee,_1938.jpg){kind=link}