Bec Wilson's Blog, page 8

June 8, 2024

Letter: Frustrations from the workplace and 'should I really be avoiding the pension at all cost?'

This letter is a two-in-one

Hi Bec, Thanks for including me on your mailout. Very interesting reading. I am curious about the attitude toward receiving a pension and what constitutes a sustainable super balance.

I have done some reading on retirement and spoken to financial advisers. It seems that most literature and advice is around avoiding the pension at all costs. I am unsure whether this is just a financial advisor scare tactic to make people think their advice is needed, or whether there is truth in pursuing the goal of being self funded in retirement.

As far as I am aware most people will not be able to accumulate over the pension cut off amount of just over a million dollars in assets. As such, most people will have to receive some pension. (Is this true? Are there any numbers on this?) But if you see a financial advisor, or read any book on retirement, the advice seems to be to work as hard as possible and pile as much into super to avoid the government and the risk of running out of funds.

To me this is insanity. Most people hate working, or hate doing what they have to do. The goal of retiring is mostly about being in a position to stop working but also to be able to do what you want. If that means being able to stop when you reach a condition of release and retire early by accessing your super then so be it. The subsequent top up in your income from a pension is just a bonus.

We all recently experienced going through COVID. One thing that I realized in that period was how little you actually need to live on. For the first time in my life the government sent me money because my business could not earn anything. In that period I also realised I reached an age to notionally retire, and I had a reasonable balance in my super account, so I did. I have only worked sporadically for the past three years. I might add that I hate my job. I hate the people and I hate doing anything for the sector I work in. I would like to keep working at something else but just don’t know what.

The upshot is that I am all but retired several years before being entitled to the pension. I am living off the interest and some of the balance of my super. It is a bit dull at times but I rationalise it as being far better than working at something I hate.

So, I am curious, whether most people aim for self funded retirement and, if so, why? Why is the pension so stigmatized by financial advisors and media? How much superannuation do most people accumulate and can there be that many people with over a million in super? Regards, Rob

Hi Rob,

What an interesting letter. I have to suggest that you read my book to better understand the age pension, and also to explore your own happiness and fulfilment. I offer a number of model financial scenarios that show how people can achieve a comfortable or a modest retirement, explaining a little more about how the pensions plays into it, and what capital is conceptually required.

Let’s start with my views on the pension. I absolutely believe you should, if you’re an ordinary Australian with an average-ish super balance (~$150-500k), learn to balance and layer multiple income streams, one of which is the age pension. It is nothing to be afraid of. In fact it’s a marvellous system, supporting the income of more than 62 percent of Australians over the age of 67. So whatever you’re being told to the contrary should be re-explored. And, if you don’t qualify today, and you are currently self-funded, with around $1M in assets other than your home, you might well qualify in the future, depending on how much you spend and how your investments perform in the years ahead. You should take the time to develop an understanding of the assets and income tests, which I explain in the book and explore whether getting the age pension is something you want to aim for or fall back on. You should also explore the Commonwealth Seniors Health Card - as you will likely qualify for some good health benefits if you are ineligible for the pension. Its income test thresholds are quite high, and the assets test doesn’t apply. Note, if you do access the age pension, you can still earn $11,800 per calendar year from working, without your pension reducing. It’s called the Work Bonus. It’s another way the government encourages layering of income, and for many people, that $11,800 can be the difference between living in comfort and living modestly.

I should warn you - I’m not a financial adviser. So, your own financial situation is not something I can speak directly to, and I do believe good financial advice is valuable. Maybe you just haven’t found an adviser you can trust and rely on, who understands your goals and objectives - an important part of the process of getting advice - also covered in my book.

Next let’s address your frustrations from work: I feel for you. Working on something you enjoy can be so fulfilling that it can even lengthen your life, but working on things you don’t enjoy, with people who you don’t relate to is stifling.

I encourage you to do some self examination - to explore what it is that you’re passionate about, and to develop work (or charitable acitivites) in areas where your interests lie. Here’s a little table I suggest people use to do a bit of self enquiry to explore where their skills and passions collide - often a great place to start looking for work. And the upside - people who are passionate about similar things, often find things in common - and may even get on quite well, adding to the social rewards of working. I hope this helps. Remember, ‘work’ doesnt have to be paid! It can be charitable too.

INSTRUCTIONS:

Just take out a piece of paper like this and create four columns, or print this out.

Write down all the skills that you have, and the things that you do in life rather naturally and with joy. They may be skills you have fallen out of the habit of using, or they may be skills you use regularly.

Then, consider your passions - the issues, concerns or things in the world that you feel a passion about - and that you get a high sense of accomplishment from.

And then think about your values and beliefs - and write them down - your anchor points in right and wrong.

Now, imagine what you can do that brings all three together - this is where you should start looking, exploring for opportunities.

Six financial foundations you need in place (long) before retiring

This Article was first published in The Age, The Sydney Morning Herald, WA Today and the Brisbane Times.

Life’s changing fast. People are living longer, rethinking retirement, and aiming for a future filled with choices. But to live it up in our later years, we need to lay down some solid financial groundwork earlier in life.

It’s about saving smart, making savvy choices, and understanding how systems can back us up. No matter our dreams for the future, setting these foundations in place sooner rather than later is key.

When you look at people facing retirement today it’s easy to see what the important foundations are. Those who know how to budget, save and invest, own their own homes outright, have learnt to understand and use their superannuation, and only spend money they can afford on luxuries are the ones headed into retirement feeling financially secure.

So let’s spread the word about these vital basics and help everyone grasp them. With these pillars in place, we can all make the most of our longer lives and enjoy every moment.

1. Maintaining a household budgetBudgeting might seem boring to many, but those who commit to it regularly reap significant rewards.

By tracking our cost of living, trimming unnecessary expenses, and striving to create a surplus in our day-to-day lives we can invest and use our funds to achieve our lifestyle goals.

Most people learn to budget properly when they decide to save for their first mortgage. But over the years after, as salaries rise and hopefully housing values too, the need to budget tightly and diligently wanes for some, and they may not exercise these important skills again until the years before retirement.

Or they might fall out of the pattern of driving a surplus during the middle years under financial stress and resist re-evaluating their position. And we as a community don’t like to discuss the ‘boring act of budgeting’. But we should, and then we should get on and do it, updating it regularly.

2. Setting lifestyle goals within our meansEveryone lives the ‘good bits’ of their lives differently. It’s easy to covet thy neighbours’ ways of living well, wishing for fancy holidays and nice new furniture we can’t afford. In these modern easy credit times, it’s pretty easy to spend like that neighbour, even if we can’t afford to.

But fundamental to good financial management is knowing when we can afford to spend up on life’s little luxuries and when we need to buckle down and save up before we can have them. In an era of buy now, pay later, this important lesson can get lost.

So my suggestion is that we each create a lifestyle budget that is separate from our cost-of-living budgets, so we can see the difference between our needs and our wants.

Plan up to three years ahead for the one-off or regular lifestyle purchases and epic experiences you want to do, and put a price tag on each in today’s money. Work out how much you need to save for each to be viable, and only do things you can afford to.

3. Understanding compound investing and managing riskUnderstanding compound interest is a game changer for financial success. Yet, this fundamental concept often gets overlooked.

Many people don’t realise that money invested over the long term at a 7 per cent compound return will double every 10 years, and money invested at a 10 per cent return will double every seven years.

Teaching this concept also underscores the need for risk management. It’s not always about chasing the highest returns but diversifying investments, considering insurance to protect against losses, and building an emergency fund.

4. Buying a home and paying it offBuying a home isn’t just about having a place to live. It’s a cornerstone of financial stability. But with the current housing affordability crisis, owning a home seems out of reach for many.

Paying off a home offers a few unparalleled benefits: we get financial security, and we get a lower cost of living every year for the rest of our lives – because we don’t have to have the cash flow for rent.

The other thing we get, as our house grows in value over time, is a growth in our asset value that can be used to fund our lives in retirement.

Many people downsize from their family homes that are paid off later in life, and contribute some of the funds into superannuation, providing them with income generating assets for the years they need it. Others choose to stay in their homes and access their equity through a reverse mortgage.

5. Understanding and leveraging taxation benefitsUnderstanding the ins and outs of the tax system early in life offers numerous benefits. (More)

You can read the rest of this article here in today’s The Age, and the Sydney Morning Herald today. It is not behind their paywall, but you may need to sign into their website to read it.

Letter: Is owning your own home really important in retirement?

Hi Bec,

Thanks for your work! All the best retirement advice says you must own your own home. We want to sell our huge family house (mortgage fully paid off). We do not want to live in a house again and want the ease and ‘lock up and leave’ lifestyle of apartment living. However we do not want to buy an apartment as we don’t want to get involved in a strata title. In fact, during these discussions we have realised we don’t want the responsibility of owning at all and would love to just rent an apartment.

So our question is, what are the pros and cons of investing the $$$ and renting?

Thanks Lisa

Wow! Lisa! That’s a big can of worms. I’ll do my best in a short answer but on this, I URGE YOU to get advice. Your situation can differ wildly depending on YOUR assets and income sources.

As you can read in my book, and in other things I write, I see owning your own home outright as you head into retirement as a fundamental pillar that supports financial confidence and financial certainty. And I know not everyone has the benefit of owning outright, but that’s a different conversation. Here’s why I think it’s important:

It makes your housing costs predictable: Owning a home (with a paid-off mortgage) eliminates the risk of rent increases and provides a predictable housing cost in retirement. This can be particularly important for those on a fixed income - which, let’s face it, is most people

Housing investments can still appreciate: Historically, property values have appreciated over time, potentially increasing your net worth and providing a source of equity for emergencies or additional income.

There’s psychological security in owning your own home: For many, homeownership provides a sense of stability, security, and control over their living environment. This can be particularly valuable in later years.

You get to leverage the systems of retirement in Australia: Your principal place of residence is exempt from the assets test for the age pension in Australia. So, if you will be eligible to receive an age pension at any point and will be leaning on the assets test to do so, this is an important consideration as you can own a palace in Byron bay and potentially still get the age pension. If your income in retirement is what throws you out - it’s a totally different discussion.

You have a protected asset for future financial needs: And, if you need access to capital later in life, it can be an important tool, allowing you to downsize OR sell it to fund an aged care bond.

Now, my opinion is not necessarily right for everyone. You really need to think about your own situation and get advice.

It’s also important to point out that just because I think housing is an important pillar of financial certainty in older age, I am also very aware that this is not as straightforward a discussion as it once was. There's no denying that homeownership can offer some financial benefits, but it's not the only path to security. In fact, for some retirees, renting and investing, or renting, with a guaranteed income stream like a defined benefit pension or annuity can be an advantageous option.

Here’s the other side of the argument:

By selling a ‘HUGE’ house, you should unlock a significant amount of capital. Investing this wisely can generate passive income and potentially grow your wealth over time. Renting frees you from the financial burdens of rates, building insurance, and unexpected maintenance costs.

Renting gives you the flexibility to easily change your living situation. You can move closer to family, downsize if your needs change, or even try out different locations without being tied to a property.

Say goodbye to mowing lawns, fixing leaky roofs, and dealing with strata concerns. Renting allows you to enjoy a low-maintenance lifestyle, freeing up your time for travel, hobbies, and relaxation.

Investing your capital allows you to spread your risk across different asset classes. This may, if invested well, lead to higher returns and greater financial security compared to having all your wealth tied up in one property.

But there’s also a hefty list of cons…

You won't build equity in a property or have a tangible asset to pass on. For some, the emotional and psychological benefits of homeownership are important.

While you'll avoid unexpected maintenance costs, rent can increase over time, potentially impacting your budget. It's important to factor this into your long-term financial planning.

As a renter, you're subject to the landlord's rules and regulations. You may have less control over renovations, modifications, or even pet ownership.

Investments come with inherent risks. Market fluctuations can affect the value of your portfolio and your overall financial security. So, if you go down this path, please seek professional financial advice to develop a sound investment strategy.

Obviously, this discussion is tricky.

There’s one other type of housing people who want the benefits of renting but the long term stability of ownership might consider - and that’s land lease otherwise known as lifestyle communities. This type of living is particularly interesting to those who can access rent assistance which happens if you are eligible for the age pension - but many people who live in them do so without rent assistance,

Land lease and lifestyle communities offer an alternative option for retirees seeking a low-maintenance, community-oriented lifestyle without the burdens of traditional homeownership. You own the dwelling but lease the land, which can result in lower upfront costs and ongoing fees compared to buying a house or apartment outright. These communities often provide amenities like swimming pools, clubhouses, and organised activities, fostering social connections and a sense of belonging.

But, just like in all other property moves, and perhaps more so here, it's important to understand the terms of the lease agreement, potential annual compounding fee increases, and any restrictions on selling or bequeathing the property.

That WAS a big can of worms - hope I did it justice. Make it epic Lisa and please, get some advice.

There are four types of modern retirees. Which one are you?

There’s just one massive newsletter each week now, so sit back and have a Sunday read!

Letters: Is owning your own home really important in retirement?

From Bec’s Desk: Without a hitch

In today’s Newspapers: There are four types of modern retirees. Which one are you?

Prime Time podcast: The nine golden rules of investment with Jamie Nemstas

First, our wonderful sponsor, Viking Cruises, has built a cool eguide for Primetimers and Epic Retirees who want to learn about river cruising. It’s got me tempted! Take a look…

Everything you need to know about river cruising

Everything you need to know about river cruisingImagine waking up in a new destination every day, feeling rested, refreshed and ready to explore. This is the beauty of a river voyage: like a floating hotel, your ship allows you to visit multiple countries with ease.

At Viking, our ships dock right in the heart of the grandest cities and quaintest towns, where our local guides will immerse you in enriching experiences that fascinate. Simply unpack once and let our dedicated crew take care of the rest.

To learn about life on the rivers, download our free guide that outlines everything you need to know about river cruising.

Download the Viking River Cruise Guide

Hi Bec,

Thanks for your work! All the best retirement advice says you must own your own home. We want to sell our huge family house (mortgage fully paid off). We do not want to live in a house again and want the ease and ‘lock up and leave’ lifestyle of apartment living. However we do not want to buy an apartment as we don’t want to get involved in a strata title. In fact, during these discussions we have realised we don’t want the responsibility of owning at all and would love to just rent an apartment.

So our question is, what are the pros and cons of investing the $$$ and renting?

Thanks Lisa

Wow! Lisa! That’s a big can of worms. I’ll do my best in a short answer but on this, I URGE YOU to get advice. Your situation can differ wildly depending on YOUR assets and income sources.

As you can read in my book, and in other things I write, I see owning your own home outright as you head into retirement as a fundamental pillar that supports financial confidence and financial certainty. And I know not everyone has the benefit of owning outright, but that’s a different conversation. Here’s why I think it’s important:

It makes your housing costs predictable: Owning a home (with a paid-off mortgage) eliminates the risk of rent increases and provides a predictable housing cost in retirement. This can be particularly important for those on a fixed income - which, let’s face it, is most people

Housing investments can still appreciate: Historically, property values have appreciated over time, potentially increasing your net worth and providing a source of equity for emergencies or additional income.

There’s psychological security in owning your own home: For many, homeownership provides a sense of stability, security, and control over their living environment. This can be particularly valuable in later years.

You get to leverage the systems of retirement in Australia: Your principal place of residence is exempt from the assets test for the age pension in Australia. So, if you will be eligible to receive an age pension at any point and will be leaning on the assets test to do so, this is an important consideration as you can own a palace in Byron bay and potentially still get the age pension. If your income in retirement is what throws you out - it’s a totally different discussion.

You have a protected asset for future financial needs: And, if you need access to capital later in life, it can be an important tool, allowing you to downsize OR sell it to fund an aged care bond.

Now, my opinion is not necessarily right for everyone. You really need to think about your own situation and get advice.

It’s also important to point out that just because I think housing is an important pillar of financial certainty in older age, I am also very aware that this is not as straightforward a discussion as it once was. There's no denying that homeownership can offer some financial benefits, but it's not the only path to security. In fact, for some retirees, renting and investing, or renting, with a guaranteed income stream like a defined benefit pension or annuity can be an advantageous option.

Here’s the other side of the argument:

By selling a ‘HUGE’ house, you should unlock a significant amount of capital. Investing this wisely can generate passive income and potentially grow your wealth over time. Renting frees you from the financial burdens of rates, building insurance, and unexpected maintenance costs.

Renting gives you the flexibility to easily change your living situation. You can move closer to family, downsize if your needs change, or even try out different locations without being tied to a property.

Say goodbye to mowing lawns, fixing leaky roofs, and dealing with strata concerns. Renting allows you to enjoy a low-maintenance lifestyle, freeing up your time for travel, hobbies, and relaxation.

Investing your capital allows you to spread your risk across different asset classes. This may, if invested well, lead to higher returns and greater financial security compared to having all your wealth tied up in one property.

But there’s also a hefty list of cons…

You won't build equity in a property or have a tangible asset to pass on. For some, the emotional and psychological benefits of homeownership are important.

While you'll avoid unexpected maintenance costs, rent can increase over time, potentially impacting your budget. It's important to factor this into your long-term financial planning.

As a renter, you're subject to the landlord's rules and regulations. You may have less control over renovations, modifications, or even pet ownership.

Investments come with inherent risks. Market fluctuations can affect the value of your portfolio and your overall financial security. So, if you go down this path, please seek professional financial advice to develop a sound investment strategy.

Obviously, this discussion is tricky.

There’s one other type of housing people who want the benefits of renting but the long term stability of ownership might consider - and that’s land lease otherwise known as lifestyle communities. This type of living is particularly interesting to those who can access rent assistance which happens if you are eligible for the age pension - but many people who live in them do so without rent assistance,

Land lease and lifestyle communities offer an alternative option for retirees seeking a low-maintenance, community-oriented lifestyle without the burdens of traditional homeownership. You own the dwelling but lease the land, which can result in lower upfront costs and ongoing fees compared to buying a house or apartment outright. These communities often provide amenities like swimming pools, clubhouses, and organised activities, fostering social connections and a sense of belonging.

But, just like in all other property moves, and perhaps more so here, it's important to understand the terms of the lease agreement, potential annual compounding fee increases, and any restrictions on selling or bequeathing the property.

That WAS a big can of worms - hope I did it justice. Make it epic Lisa and please, get some advice.

Well! This week was not without eventful activities!

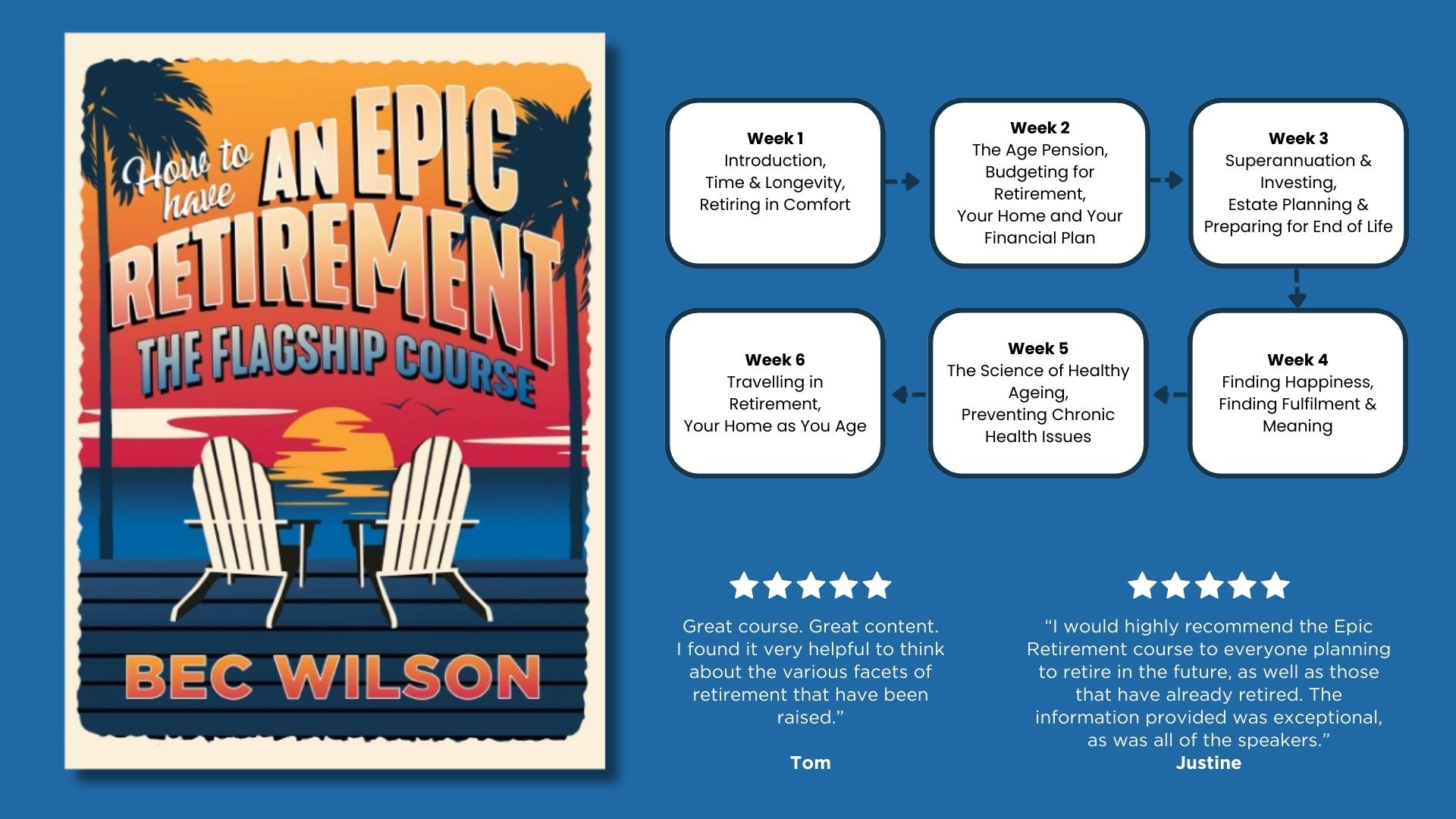

The Winter Edition of the How to Have an Epic Retirement Flagship Course is now underway - and it happened without a hitch! It’s so much fun to be inside the learning portal with hundreds of new students chatting away about their excitement and trepidation at the years ahead. Each week of the program, they get to attend live Q&As with some of Australia’s true technical leaders of retirement too, which I think adds a lot of opportunity to learn that simply isn’t available elsewhere. If you missed this one, the next program is our Spring Edition, launching in August - more here.

And, also this week just gone, the members of Care Super were treated to a 90 minute How to Have an Epic Retirement education session by their fund this week. A real thrill to present to hundreds of their members. Such a buzz when, after talking non-stop for an hour, the questions start rolling in thick and fast. Big thanks to the Care Super team for inviting me along for the event.

Next week is a busy one. I’m hopping down the east coast to present at the Association of Superannuation Funds Victorian Conference - presenting a case study of our retirement education! I’ll also be speaking in the offices of Colliers in Brisbane, Sydney and Melbourne to retirement housing developers about what retirees said they want and need more of in our recent housing survey (and I’ll share the insights with you very soon). It’s such a joy to be able to elevate the needs and wants of today’s modern retirees in the industries that support you.

Our podcast this week was super-interesting session with Jamie Nemstas, a premium financial adviser and the author of The Golden Years. He shared his nine golden rules of investment - which you can listen to wherever you get your pods.

And The Epic Retirement Club Facebook Group continues on strong! You just won’t believe how much it is growing peoples’ confidence to have other retirees to relate with.

Finally, don’t forget to send me your letters. I really want to help people with the big questions. And using your letters to guide my conversations can be super-fun.

Until next week… make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

There are four types of modern retirees. Which one are you?

There are four types of modern retirees. Which one are you?This Article was first published in The Age, The Sydney Morning Herald, WA Today and the Brisbane Times.

Retirement is a funny word. When you look it up in the dictionary, it means leaving your job and ceasing to work. But we all know that’s an outdated definition, one that is actually untrue for many of today’s retirees.

Retirement age and the concept of retirement in Australia is changing dramatically. For some, it’s the age they can access their super. For others, it’s the age they can access the age pension. And for some, it’s never.

The recently released 2022-23 Australian Bureau of Statistics retirement intentions survey shows the average retirement age in Australia last year was 64.8 (66.9 for men and 63.2 for women). Interestingly, the average age people intended to retire was 65.4. When you dig deeper into the real reasons people left their final role, the picture gets even more interesting.

One-fifth of people lost their last job or closed their business for economic reasons, and never re-entered the workforce, 12.8 per cent left because of their own sickness, injury or disability, 3.4 per cent left to care for an ill, disabled or elderly person, and 31.8 per cent retired because they reached retirement age, or became eligible for superannuation or the age pension.

When you look at the sources of income people are dependent on in retirement, the real picture of what’s driving our retirement definition becomes even clearer.

In 2022-23, the age pension remains the single most important income source for most Australians in retirement. More people than ever before are retiring with a superannuation balance that will provide them with the ability to use it as a source of income, but the era of superannuation being the primary source of income for most retirees in Australia is still quite a long way off.

For each type of retiree, the opportunities and desires to work differ.

The latest data shows that 31.8 per cent of Australians are completely dependent on the age pension in retirement today and 17.6 per cent are partly self-funded, still drawing a part-pension. That’s at least 49.4 per cent of retired Australians relying on the pension for income. Alongside this, 37.1 per cent are fully self funded, a growing cohort.

The data shows that the number one factor influencing someone’s decision to retire is their financial security. No surprises there.

So the fact that IT, mining industry and financial services workers intend to retire earlier than nurses, administrative staff and agriculture workers again will be no surprise. Maybe the latter feel more passion for their jobs, but I suspect it’s the financial security that’s key.

When you get to know today’s retirees like I do, you see four distinct retirement definitions and each do retirement strategy completely differently:

Retirement age = superannuation age. These folks have healthy super balances and can afford to self-fund their early and middle retirement years (maybe even their later years too) without much help from the age pension. For these people the target window for retirement is often 60, the earliest age most can access their superannuation if they stop working.

Retirement age = age pension age. This group pairs a modest super balance with the age pension to create a passive income they can scrape by on without working full-time.

With the age pension qualification age at 67, this is the critical layer of income that enables them to give up full-time work and formally begin to access both the age pension and their superannuation.

Retirement? What retirement? These people love their jobs and don’t want to retire. They stay in the workforce longer and may choose to access their superannuation from the age of 65, without ever uttering the word “retirement”. Age is just a number to these people, and why shouldn’t it be?

The sweet spot strategists. This one is the person who is well-planned, understands how to use both superannuation and the age pension systems together. Having done their homework, they know they have enough superannuation to retire a couple of years before pension age.

You can read the rest of this article here in today’s The Age, and the Sydney Morning Herald today. It is not behind their paywall, but you may need to sign into their website to read it.

The nine golden rules of investment with Jamie Nemstas

The nine golden rules of investment with Jamie NemstasGetting ready for retirement and wondering how to make your investments work harder? Today I’m talking with financial adviser, Jamie Nemstas, one of the two authors behind the book The Golden Years: How to plan a happy and secure retirement.

If you're nearing retirement, have capital to invest and are wondering how to make your money work as hard as you did, Jamie's got nine golden rules of investment he thinks everyone should know and understand. Buckle up for a ride through the do's, don'ts, and golden nuggets of retirement investing from a guy who does it for people with much larger super balances than average.

LISTEN HERE:

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

June 1, 2024

When will the Age Pension be axed?

There’s just one massive newsletter each week now, so I’ve crammed heaps in…

Letters: When will the Age Pension be axed?

From Bec’s Desk: On the road with the funds; extra last minute course deal

In today’s Newspapers: Six financial foundations you need in place (long) before retiring

Prime Time podcast: Tales from a truly Epic Retiree - Mike Chesworth

But first, I am thrilled to welcome Viking Cruises as a sponsor of the Epic Retirement newsletter, and thank them for their support. (And check out their amazing deal for Prime Timers and Epic Retirees!). If you’re planning a trip, they offer both ocean and river cruises and they’re all about meaningful experiences!

Explore the world in comfort with Viking - Voyages for the curious minded

Explore the world in comfort with Viking - Voyages for the curious mindedAs an award-winning small ship cruise line, we have developed a deep understanding of our guests' unique, inquisitive nature. We take you closer to the unique art, heritage, traditions, architecture and people that define each destination and focus our energy on creating meaningful experiences that linger long in the mind after you’ve returned home.

With no kids, no casinos, fewer sea days and more time in port, every day on a Viking voyage is an opportunity to discover more.

Book your next voyage before 31 July 2024 to save $4,600 per couple and experience 'The Viking Difference'.*

When will the Age Pension be axed? “Hi Bec, I heard the age pension is not available to those born from 1965. Is that correct? For clarity I understand pension is not paid till age 67. But many years ago the govt announced the age pension would cease for those born after 1965. Is there an alternative pension income? - Katrina”

I get asked questions like this all the time on radio, at events and in our Facebook Group, so you’re not alone in fearing the end of the age pension. And I’m pleased to report that it’s all an urban myth. The government has not announced any plans to completely eliminate the age pension for those born after 1965 and I highly doubt we will see that happen in our lifetimes. If there were any such significant policy changes, they would be widely publicised and involve substantial public debate and extensive legislative process. And, with about 30% of the population over 55 years of age, I think it would be political suicide. And then it would be overturned later.

If you’ve read my book, you’ll see that over the next two decades, as the number of people who’ve contributed super at higher compulsory contribution percentages throughout their lives grows, the number of people who are eligible for for the age pension will decline. This is simply because more people will be in excess of the assets and income tests. They will be able to self-fund their retirement. And, over time, the country’s dependence on the age pension will dramatically decrease. I don’t believe any government will ‘take it away’, nor will it be a significant rising cost or risk to the nation. We are in an excellent position, likely very close to ‘peak number of age pensioners’ with superannuation contributions now climbing to compulsory 11.5% of salary in July 2024. Instead, policy efforts all look to be focussed on ensuring the sustainability of the pension system while encouraging greater self-sufficiency through superannuation. That’s a win for all I think.

Here's a summary of the current age pension eligibility:

Born before July 1, 1952: Eligible at 65 years

Born between July 1, 1952, and December 31, 1953: Eligible between 65.5 and 66 years

Born between January 1, 1954, and June 30, 1955: Eligible at 66 years

Born between July 1, 1955, and December 31, 1956: Eligible between 66 and 67 years

Born from January 1, 1957, onwards: Eligible at 67 years

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

It was a big week! We successfully closed the early bird deal on the upcoming Epic Retirement Course on Monday, and on Tuesday I jetted off to speak at a super fund event series in Melbourne, Sydney and Brisbane, held by the Funds Executive Association of Australia (FEAL).

I spoke about ‘How funds can make retirements more epic!’ and I am delighted with the interest from funds. Basically, I shared what an epic retirement is (the six pillars you know well) and dove deep into the insights and lessons for funds gathered from the Retirement Planning survey we did a couple of months ago with you.

The rooms were frankly packed to the gills! The people were interested and it was really fun to talk about what you need to retire well with all the right people in super-funds to see action. The team at Allianz Retire+ sponsored all the events and the research, so I am very grateful to them for helping to give us a very loud voice among the funds sector! I’ll do a longer piece on the research for you in weeks to come.

The Epic Retirement Flagship Course Workbooks have arrived! Mailbags are packed and sent, and the course kicks off on 6th June (this Thursday). I can’t wait.

******If you haven’t yet booked your place, I have dropped a special coupon code that will be available to our community until 3pm Sunday giving you 25% off RRP with the code WINTER25. Click here to book with the code. After that, we’re done on discounts. There’s hundreds of people booked so you’ll be part of a great cohort learning together! ******

And the other highlight this week is The Epic Retirement Club Facebook Group which has been growing like topsy and is packed with so much joy of retirement. Many thanks to our new moderators, David, Jillian, Yvonne, Jane and Colleen. If you have a hankering for a like-minded community - this is pumping with it.

Meanwhile, How to Have an Epic Retirement, the book, has been holding court on Amazon’s top 100 books for a few weeks now. This week it’s at #68. Amazon just got heaps more stock if you’re keen for a copy. Order it here.

And the Prime Time podcast is just such a dream to make. This week I chatted with a truly epic retiree… it was a real thrill to hear and share his stories. I hope you enjoy it as much as I did. Links below.

Until next week… make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Six financial foundations you need in place (long) before retiring

This Article was first published in The Age, The Sydney Morning Herald, WA Today and the Brisbane Times.

Life’s changing fast. People are living longer, rethinking retirement, and aiming for a future filled with choices. But to live it up in our later years, we need to lay down some solid financial groundwork earlier in life.

It’s about saving smart, making savvy choices, and understanding how systems can back us up. No matter our dreams for the future, setting these foundations in place sooner rather than later is key.

When you look at people facing retirement today it’s easy to see what the important foundations are. Those who know how to budget, save and invest, own their own homes outright, have learnt to understand and use their superannuation, and only spend money they can afford on luxuries are the ones headed into retirement feeling financially secure.

So let’s spread the word about these vital basics and help everyone grasp them. With these pillars in place, we can all make the most of our longer lives and enjoy every moment.

1. Maintaining a household budgetBudgeting might seem boring to many, but those who commit to it regularly reap significant rewards.

By tracking our cost of living, trimming unnecessary expenses, and striving to create a surplus in our day-to-day lives we can invest and use our funds to achieve our lifestyle goals.

Most people learn to budget properly when they decide to save for their first mortgage. But over the years after, as salaries rise and hopefully housing values too, the need to budget tightly and diligently wanes for some, and they may not exercise these important skills again until the years before retirement.

Or they might fall out of the pattern of driving a surplus during the middle years under financial stress and resist re-evaluating their position. And we as a community don’t like to discuss the ‘boring act of budgeting’. But we should, and then we should get on and do it, updating it regularly.

2. Setting lifestyle goals within our meansEveryone lives the ‘good bits’ of their lives differently. It’s easy to covet thy neighbours’ ways of living well, wishing for fancy holidays and nice new furniture we can’t afford. In these modern easy credit times, it’s pretty easy to spend like that neighbour, even if we can’t afford to.

But fundamental to good financial management is knowing when we can afford to spend up on life’s little luxuries and when we need to buckle down and save up before we can have them. In an era of buy now, pay later, this important lesson can get lost.

So my suggestion is that we each create a lifestyle budget that is separate from our cost-of-living budgets, so we can see the difference between our needs and our wants.

Plan up to three years ahead for the one-off or regular lifestyle purchases and epic experiences you want to do, and put a price tag on each in today’s money. Work out how much you need to save for each to be viable, and only do things you can afford to.

3. Understanding compound investing and managing riskUnderstanding compound interest is a game changer for financial success. Yet, this fundamental concept often gets overlooked.

Many people don’t realise that money invested over the long term at a 7 per cent compound return will double every 10 years, and money invested at a 10 per cent return will double every seven years.

Teaching this concept also underscores the need for risk management. It’s not always about chasing the highest returns but diversifying investments, considering insurance to protect against losses, and building an emergency fund.

4. Buying a home and paying it offBuying a home isn’t just about having a place to live. It’s a cornerstone of financial stability. But with the current housing affordability crisis, owning a home seems out of reach for many.

Paying off a home offers a few unparalleled benefits: we get financial security, and we get a lower cost of living every year for the rest of our lives – because we don’t have to have the cash flow for rent.

The other thing we get, as our house grows in value over time, is a growth in our asset value that can be used to fund our lives in retirement.

Many people downsize from their family homes that are paid off later in life, and contribute some of the funds into superannuation, providing them with income generating assets for the years they need it. Others choose to stay in their homes and access their equity through a reverse mortgage.

5. Understanding and leveraging taxation benefitsUnderstanding the ins and outs of the tax system early in life offers numerous benefits. (More)

You can read the rest of this article here in today’s The Age, and the Sydney Morning Herald today. It is not behind their paywall, but you may need to sign into their website to read it.

Tales from a truly epic retireeThis episode really is a doozy. I don’t know anyone as proactive about living their retirement well as Mike Chesworth. He’s a truly epic retiree. Seven years into a retirement that he chose to kick off fairly young, Mike has plenty to say on how he’s shifted away from his big career as the former GM of Financial Planning and Advice for Westpac and BT into a new life packed with things he loves doing.

LISTEN HERE:

He has gone from being “the guy from financial services” to “Mike the bike guy” in his neighbourhood and he embraces that. In fact he’s thrilled with the transformation and listening to him talk about the joy in his life is exciting.

So today Mike and I chat through tales from his retirement so far. There’s stories about his transition, stories about his sense of purpose, stories about his really meaningful passions and stories about travelling to places that are packed with culture and experience.

I hope everyone can take away some inspiration and some lessons from Mike’s attitude to getting out there and living life well.

May 25, 2024

You’ll probably live longer than you think, so start planning now

It’s a bumper edition - everything epic in one newsletter a week from now on. Enjoy! My Sunday Herald/ Sunday Age money section article, a bonus extension to that article about living our longer lives well, this week’s Prime Time podcast and a ‘from Bec’s Desk’ too.

This article was first published on The Sydney Morning Herald, The Age, WA Today or the Brisbane Times here.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

It’s interesting to contemplate how long we might live as we head through our midlife and plan for retirement. Not just as a passing thought – but to really think about it. When you do, you might find you’re underestimating the years you have ahead and how much you can do with them.

Life lengths have been changing rapidly. Back in 1970, the average Aussie life expectancy was 71 years. Today, the average life expectancy is 83. If you are approaching midlife and retirement in good health today, that’s likely to improve significantly. But how much longer is the question we all want to answer.

There are some big things to think about when you consider your life length, and use it to set goals and plans for your life ahead. Firstly, which type of life expectancy data will you use to project how long you might live? Secondly, are you likely to live longer than 50 per cent of the population?

The most common numbers we see on life expectancy are those from the Australian Bureau of Statistics’ Life Tables, based on historical data. They tell us the average age people are expected to live based on past experience in the population.

These numbers are interesting, and heavily quoted by the retirement industry, but the reality is, they don’t consider future changes in health and wellbeing, and they don’t consider whether you’ll be one of the lucky ones.

The ABS Life Tables historical data tells us that a 65-year-old man today might live to the age of 85.2 and a woman to about 88.

We need to plan for a longer retirement, both financially and functionally.

As a nation, our health is improving quickly. So, there’s better data to look at if you want to understand how your own life might turn out, particularly if you’re healthier and/or wealthier than average today.

There’s also data publicly available that is adjusted for mortality improvements, that is, they are adjusted to take in potential improvements to our health and wellbeing, given the upward trends in age-of-death rates in the past 25 years.

There’s more… but I can’t fit it all in the email!

Read the whole article here on the Sydney Morning Herald or The Age and find out your adjusted life expectancy for both 65 and 42 year olds. It’s not behind their paywall - but you may have to sign up to view it. It’s also in the print edition today.

So what can you do to make those longer lives better?

So what can you do to make those longer lives better? If you've read my article in The Age and The Sydney Morning Herald today, you might be wondering what changes could we make to improve our longer lives and make sure we get to live them well? Let’s contemplate it seriously. Here’s my list. Can you add any?

We would clearly look after our bodies better. Exercise, diet, hearing, eyesight, gut health, and brain health will impact how we age physically and mentally, likely improving our quality of life.

Taking proactive steps to prolong our mobility becomes essential. We can replace knees, hips, and shoulders, allowing us to maintain our mobility much later in life. This choice requires an investment of time, effort, and sometimes money, to ensure proper rehabilitation.

Regular healthcare and preventive measures become more critical. Regular check-ups, vaccinations, screenings, and early interventions can help manage chronic conditions and prevent potential health issues.

Mental and emotional health needs more attention. Staying socially active, engaging in intellectually stimulating activities, and seeking help for mental health issues can significantly impact our well-being.

Altering the way we invest, save, and spend our money becomes crucial. A longer life means more years to enjoy leisure activities, as well as more years of general expenses. Budgeting for both might become a higher priority if we believe it's possible.

Lifelong learning and adaptability gain importance. Staying open to new experiences and continuously learning can help us navigate changes and improve our quality of life.

Community and social engagement play a vital role. Being involved in community activities and maintaining a strong social network can provide a sense of purpose and connection.

Financial planning for our ageing years and frailty later in life becomes essential. Having a financial cushion to cover our ageing health and care needs can provide peace of mind.

Valuing our family and friends takes on much greater significance. If we believe our family and true friends will be our anchor in our later years, bringing us joy, we might spend more effort appreciating them now, before we need their company.

Let’s face it, thinking about how long we might live can be confronting or quite exciting, knowing that, to some extent, we have the power to influence our own longevity.

I started this week in Melbourne, speaking at the Boroondara Library to a packed house of 80 people on the coldest night I’ve felt in a long time. Thanks to everyone who came along! There truly wasn’t a spare seat.

Then, it was onto the Australian Shareholders Association (ASA) conference in Melbourne the next day for a really fun panel discussion about modern retirement.

And, then on Wednesday I did a prepared online education session about how to live out longer lives better for the staff at the Australian Prudential Regulation Authority (APRA) the government organisation that regulates our super funds and life insurers. 350 people came along for that one frm all ages - rather a buzz.

Then Thursday we dropped that awesome podcast with Financial Planner Paul Benson - our EOFY Checklist.

And I started finishing off my next speeches as I’m hitting the road down the east coast next week to present for the Fund Executives Association of Australia. Yep! They want to know more about what you want from your funds as you head into retirement. And I’m thrilled to share it so hopefully, they get the retirement phase right for you.

And, throughout the week, our Epic Retirement Club Facebook Group has been going rather nuts!

All this busy-ness has driven me to change the epic retirement emailing schedule. I’m going to do just one, long, valuable weekend emailer for a little while and include everything I do in that one newsletter. And then I’ll see what you think. You’ll still receive the Prime Time podcast newsletter on Thursdays too. Every now and then if something important happens or I get a doozy of a letter, I’ll email midweek, but not every week - only as a special treat.

I’m conscious that the How to Have an Epic Retirement Flagship Course kicks off in just 13 days and that gets all my priority. Our Earlybird 25% off deal closes on the 27th May (MONDAY) at 12 noon, so book now if you want a great deal. I’ll put a more detailed overview of the course below.

And I am gradually chipping away at writing my next book too. A girl can only do so much!

Until next week… make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Epic Retirement Course Earlybird Deal Ends Monday

Epic Retirement Course Earlybird Deal Ends MondayThe Epic Retirement Flagship Course is booking up beautifully. We have an awesome cohort in the hundreds, booked to kick off on the 6th June. And our guests are ready and raring to go too.

The course includes 8.5 hours of epic retirement education, a signed copy of the book, as well as a new 150 page professionally printed workbook for you too.

We’ve got some amazing live Q&As with some of Australia’s most respected retirement experts, from big companies and small. They include Mark Lapedus from Allianz Retire +, Jen Harding from HESTA, Andrew Lowe from Challenger and David Lane from Ord Minnett. We’ve also go an amazing life coach joining us, Rowena Millward and the amazing travel guru Fiona Dalton too.

So, get your booking in. This is the last chance for these prices for our Winter program. Want to learn more or download a brochure? - you can do that on our website.

Book now for our Winter Course

The end of financial year is just around the corner, and for those approaching retirement, it can be quite an important time to think about your superannuation contributions and how to maximise your tax savings. This year is also pretty special, because on 1 July we get an uplift in the concessional and non-concessional superannuation caps, an increase in the contribution rate as well as the stage three tax cuts.

LISTEN ON APPLE - LISTEN ON SPOTIFY

So this week I’m chatting with Paul Benson. He’s a Financial Adviser, and a fellow columnist for The Age and The Sydney Morning Herald finance section. And we’re talking through the end of financial year checklist we should all be thinking about before June 30 comes around.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

May 18, 2024

Could grandparents be our biggest financial influencers?

It’s Sunday! And I’m on the road in Melbourne enjoying the crisp, sunny, cold weather. I’ll be seeing a few of you at an event in the library at Boroondara in Melbourne on Monday night. It’s completely booked out though so more can’t come I’m sorry!

I’ll also be at the Australians Shareholders Association conference on Tuesday. If you’re there, come and say hi! I love to meet our Primetimers and Epic Retirees in real life.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

If you missed our awesome Prime Time podcast with Jo Peck on her experience of becoming “Suddenly Single at Sixty” make sure you have a listen. 🎧 Listen on apple podcasts here. Or you can search for ‘Prime time with Bec Wilson’ wherever you get your podcasts.

Finally - the countdown is on to the next six week How to Have an Epic Retirement Flagship Course. The early bird 25% off discount closes ten days before kickoff on the 27th May. So lock in your place so I can send out your book and workbook as soon as they arrive from the publisher. 🎓 Find out more and book your place here.

And that’s it for today. I’m off to be a tourist in this beautiful city of food.

Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Could grandparents be our biggest financial influencers?

Could grandparents be our biggest financial influencers?

This article was first published on The Sydney Morning Herald, The Age, WA Today or the Brisbane Times here.

Grandparents play an enormous role in securing their grandkids’ financial future. Plenty of them take their role very seriously too, seeing it as their guiding role to teach their grandkids how money works, and contributing to savings and investments for their grandchildren that can make an enormous difference later in their lives.

My own grandparents were key in shaping my financial literacy, teaching me how to do jobs in their yard and home, making me negotiate a rate for each job, and paying me with little piles of 20 cent and 50 cent pieces that I had to count out and take to the bank.

Using that cash, they taught me about savings, interest, and compounding too. They also taught me how to spend, encouraging me to spend a little of my pocket money, carefully, at the local lolly shop, but not to go overboard.

And they showed me how to be frugal, or careful with money, like they were, by modelling sensible behaviours like shopping for gifts at the sales and tucking them away months before Christmas.

I know now, but I didn’t know then, that in the times when my parents faced financial strain, they quietly supported my education helping my parents juggle those difficult middle years too.

It’s a role more and more grandparents want to play, especially if they’ve got a little more financial certainty than their adult children, but it’s not as easy as it used to be.

With the decline of cash, the ability to make money tangible is harder. Investing on behalf of your grandkids can cause tax issues and grandparents, frankly, aren’t all living frugal lives like mine had to in their generation, so they’re not always modelling the behaviour kids can learn from any more.

So this week, I’ve got some suggestions and lessons for playing that role in your grandchildren’s lives in a much more cashless world.

Teaching kids early in lifeAs the use of cash declines we’re going to have to get more creative in how we make money tangible for kids early in life.

The fundamentals stay the same – you can help your kids open their first bank account, even become a supervisor on their account alongside their parents, and teach them to use it, the same way my grandparents taught me to use my bank book.

As a supervisor, you can allocate limits for spending and approve money for use. Then, once you have your banking and digital currency tools set up, you can set them jobs they can do, negotiate the rate of payment, teaching them to seek a fair amount, and then pay them diligently once the role has been performed.

Then, you can together set up goals for the savings, allowing a small portion for spending on little joys, and a larger portion for a more strategic goal. You could even be clever, and make one of the rewards an outing to purchase a strategic item together or a trip they need spending money for – a true bonding moment for grandparent and grandchild.

Help build a nest eggBack in the ’70s, when most grandparents were getting on the property ladder, an average annual wage was about $6300 and the average house price in Sydney was $18,700 – a multiple of about 2.9 times.

The price to wage ratio is now up to 12 times a person’s salary with the average house price in our capital cities now $1,145,000 and the average wage about $90,000 per annum. That means the multiple for a capital city dwelling is something in the league of 12.7 times.

By being a guiding hand with financial literacy, you’re investing in their own future happiness.

Owning your own home is one of the principles of financial security later in life. So, it makes sense that we do whatever we can to help kids to get there as early as possible. The power of compound investing in Australian property has rewarded many and disappointed few. But it’s hard to get started.

Grandparents play an enormous role in securing their grandkids’ financial future. Plenty of them take their role very seriously too, seeing it as their guiding role to teach their grandkids how money works, and contributing to savings and investments for their grandchildren that can make an enormous difference later in their lives.

My own grandparents were key in shaping my financial literacy, teaching me how to do jobs in their yard and home, making me negotiate a rate for each job, and paying me with little piles of 20 cent and 50 cent pieces that I had to count out and take to the bank.

Using that cash, they taught me about savings, interest, and compounding too. They also taught me how to spend, encouraging me to spend a little of my pocket money, carefully, at the local lolly shop, but not to go overboard.

And they showed me how to be frugal, or careful with money, like they were, by modelling sensible behaviours like shopping for gifts at the sales and tucking them away months before Christmas.

I know now, but I didn’t know then, that in the times when my parents faced financial strain, they quietly supported my education helping my parents juggle those difficult middle years too.

It’s a role more and more grandparents want to play, especially if they’ve got a little more financial certainty than their adult children, but it’s not as easy as it used to be.

With the decline of cash, the ability to make money tangible is harder. Investing on behalf of your grandkids can cause tax issues and grandparents, frankly, aren’t all living frugal lives like mine had to in their generation, so they’re not always modelling the behaviour kids can learn from any more.

So this week, I’ve got some suggestions and lessons for playing that role in your grandchildren’s lives in a much more cashless world.

Teaching kids early in lifeAs the use of cash declines we’re going to have to get more creative in how we make money tangible for kids early in life.

The fundamentals stay the same – you can help your kids open their first bank account, even become a supervisor on their account alongside their parents, and teach them to use it, the same way my grandparents taught me to use my bank book.

As a supervisor, you can allocate limits for spending and approve money for use. Then, once you have your banking and digital currency tools set up, you can set them jobs they can do, negotiate the rate of payment, teaching them to seek a fair amount, and then pay them diligently once the role has been performed.

Then, you can together set up goals for the savings, allowing a small portion for spending on little joys, and a larger portion for a more strategic goal. You could even be clever, and make one of the rewards an outing to purchase a strategic item together or a trip they need spending money for – a true bonding moment for grandparent and grandchild.

Help build a nest eggBack in the ’70s, when most grandparents were getting on the property ladder, an average annual wage was about $6300 and the average house price in Sydney was $18,700 – a multiple of about 2.9 times.

The price to wage ratio is now up to 12 times a person’s salary with the average house price in our capital cities now $1,145,000 and the average wage about $90,000 per annum. That means the multiple for a capital city dwelling is something in the league of 12.7 times.

By being a guiding hand with financial literacy, you’re investing in their own future happiness.

Owning your own home is one of the principles of financial security later in life. So, it makes sense that we do whatever we can to help kids to get there as early as possible. The power of compound investing in Australian property has rewarded many and disappointed few. But it’s hard to get started.

Some sources say it can take a young couple or a single person today between six and 12 years to save the deposit for their first home if they are saving about 25 per cent of their income a month to aim for a target of a 20 per cent home deposit.

This is where grandparents are playing a powerful role, setting up carefully constructed investment assets and contributing to them early in a child’s life. The objective is to make an investment that can, over the 20-30 years before a child matures and wants their own home, really be left untouched to grow or added to over time, and can offer them a valuable start in life.

However, grandparents who are saving for their grandchildren under 18 years of age need to be aware of the tax implications which can be complicated depending on your personal circumstance and the child’s.

You may find, after talking to an accountant, that it’s better to consider a growth asset than an income strategy, as income tax laws are designed to limit the amount of money a minor can earn from dividends and interest and other passive sources to avoid adults diverting income to their children’s accounts.

And, if setting up a bank account, you’ll also want to get a tax file number in the child’s name to avoid the bank withholding tax unnecessarily, something that is often forgotten or overlooked.

Teaching kids how to spend moneyThis is a really tough one for many of today’s retirees who are in the midst of the best years of their lives, spending with a greater sense of excitement than the silent generation ever did.

This article continues. Read it on the Sydney Morning Herald, The Age, WA Today or the Brisbane Times here.

Read my article from last weekend that went a little crazy: Cash is dead. Why are we still pretending it isn’t?

This week we’ve dropped two episodes at the same time. A ripper of a podcast with author Jo Peck and in a bonus edition of the podcast, a very focussed and rapid-fire update on what’s in the 2024 Federal Budget for Prime Timers. All the info is below. Have a listen and leave us a rating and a review.

Suddenly Single at Sixty with Jo Peck

Suddenly Single at Sixty with Jo PeckIn this episode, I speak with Jo Peck, author of the candid memoir, 'Suddenly Single at Sixty'. It’s a ripper of a conversation and a true story.

Not long after Jo's 60th birthday, her husband drops a bombshell—he’s leaving her for a (much) younger woman. Jo is shocked and heartbroken that the life she’d worked towards, has gone up in smoke. All those dreams of growing old with the person she loved … destroyed.

In this interview, Jo details the journey of personal growth which led to her rebuilding her life, making it clear that life does NOT end at 60.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

May 14, 2024

Budget 2024: what really matters for those approaching and in retirement

In this week’s edition:

From Bec’s Desk: A big can of worms and a lot of letters

Feature story: Budget 2024: what really matters for those approaching and in retirement

Prime Time: The BIG retirement mistakes people make and how to avoid making them

The Course Countdown: It’s on…

First, a big thanks! How to Have an Epic Retirement, the book, hit #10 on the Amazon bestseller list this week! Number Ten! We didn’t even get that high in the first weeks of book sales. I’m excited. Normally retirement books are hidden at the back of the store on the bottom shelf. Not this one. 🏝️ Thanks for telling your friends. That’s clearly how a book gets this far ten months after publishing. 🥰

In case you haven’t got a copy yet - you can buy How to Have an Epic Retirement, the book on Amazon and Booktopia and in many of the major bookstores. It did sell out in a few places this week - but more is on its way!

Cash is still dying… even if you’re angry about it.No doubt you saw the giant can of worms I opened with my very well-meaning and factually correct article on Sunday in The Age and The Sydney Morning Herald. I used my column to encourage retirees to learn about and use online banking and digital wallets before cash becomes obsolete in about 7 years time.

I GOT SMASHED with feedback.

Even the Daily Mail wrote an article about the extraordinary furore my article caused! “Woman sparks outrage after claiming cash is already dead”. 😵

Yep! Hard core smashed. My inbox resembles everyone’s worst nightmare, but they’re raising legitemate concerns. So I won’t leave you out of the story. Here’s some insights into the feedback and some reasonable questions they raise for me and for others.

A picture of my print column in the Sunday Age on 12th May 2024

A picture of my print column in the Sunday Age on 12th May 2024Are bank fees for transactions evil? Or are they paying your dividends?

Many don’t want to pay fees to banks. I don’t like paying fees either. But that doesn’t mean I won’t learn how to use a system and use it when it suits me. I personally recognise that I used to pay retailers a margin that included their handling, banking and processing of cash. Now, I probably don’t pay that to retailers as they bank my money at the time of payment without having to count tills, drive to the bank and such. And banks are not going to provide that service for free, no matter how loud people cry. So, if I want the convenience, and the business wants the efficiency, there will be a cost. Either the retailer pays it and hides it in your margin. Or you pay it. It’s a bit like postage on an online purchase.

A little aside, but a worthy thought - How many of you have bank shares that pay you dividends, or have a holding in a bank via a major super fund? Surely many are benefitting from the banks earning money too? Retirees are some of the largest holders of bank shares after all. And banks are some of the biggest payers of dividends. It’s a circular world we live in.

Some have loves ones who simply can’t cope with the technology.

This is awful and I have deep empathy. Cash will probably be around a while still, and while it is, I hope someone finds ways to limit digital technology so they dont get scammed and can use it in a simple manner. Maybe some clever entrepreneur or social enterprise can come up with a limited account that can have capped risk and supervision. Some banks already offer accounts with a second account holder in a supervisory function for dementia sufferers. It might be worth asking your bank. Some have dedicated teams for dementia and disability support too.

Scammers and fraud

Cyber crime sucks. I agree with all of you. So when we teach people how to use digital technology, we also have to teach them what to look out for. There’s nothing we can do here but teach, and reinforce and teach again I don’t think.

Connectivity issues

This is an argument I get. When there’s no internet - there can be no internet banking. So it can’t happen until internet coverage improves and we have options. But this is improving over time. Sure, in regional Australia it sounds like we might be able to hold off the death of cash simply because of the delays to connectivity. But that can only happen if we can find trucks to deliver cash and ATM owners and supermarkets that want to provide it! Let’s be realistic, the concerns about Armaguard going into administration in March and April of this year are real. Moving cash around this country is expensive and noone is putting their hand up to lose money doing it - so that’s a watching space.

“I don’t wanna”

That is frankly your choice. This issue may well be a silent one. No politician or bank is going to take a public stance and rally the end of cash, because it’s a politicians worst nightmare to anger older Australians in the prelude to an election. It’s my suspicion that they will just let it disappear organically. And the losers will be those who don’t want to learn. It’s a tough message to hear. But, just like with retirement, you have to learn to become wise. I want you to be wise and capable.

Issues with charities and kids

I have had a lot of letters about the death of donations and the disaster of children’s financial literacy. There is alternatives here, and the organisations that embrace digital tools can find them. I went to an Australian Independent Retirees event the other day who sold their raffle tickets using a square reader that takes digital payments. Anyone who wanted to pay with digital funds could and did. Similarly at charity auctions, they provide a QR code and people bid with ease. At my son’s school the whole tuckshop and uniform shop has been digitised with amazing tools that integrate parent approvals into spending. Its happening, and I know it’s not the world I grew up in where I did learn by counting coins, taking them to the teller and having my bank book stamped, but they can’t do that anymore anyway. So let’s teach them in the language of the world they will live in. Change sucks sometimes, but Boomers have been the masters of it so I have faith you’ll get there.

Ultimately though, I can’t change the trajectory. I can only point to it and educate. And I’m still pointing to the death of cash in LESS THAN seven years. So, if I managed to reach a whole lot of older Australians and got them to start to consider the reality that they will need to learn about digital transacting, then I’m kicking the goals I aimed for. What my article didn’t say because I only get 800 words of printed column space to play with, is that if you choose only to use digital transacting for some things, because you don’t like paying bank fees - then that’s perfectly ok too. My rallying call is to encourage people to learn and become capable and confident in digital transacting. Then you have the CHOICE.

I know most of you here actually know how to use digital technology, but you might not yet have leapt into digital wallets. So, I’ll point you back to the Sydney Morning Herald article to read my three steps.

Start with web-based online banking

Next, learn to use your bank’s mobile app

Then, start using the digital wallet on your devices

Always know I mean to look after your best interests. I’m just one annoying, opinionated person who is really on ‘team retiree’!

The upcoming Epic Retirement 6 week courseThe early bird discount on the How to Have an Epic Retirement Flagship Course closes on the 27th May. So it’s time to get your bookings locked in. Book for Winter here. Or, simply find out more on the website here.

I released the first video of the course, freeI thought it might be nice for you to watch the first, foundational lesson of the How to Have an Epic Retirement Flagship Course, so I released it for free yesterday. The video teaches you the six pillars of an epic retirement. Watch it here.

Until next week! Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Budget 2024: what really matters for those approaching and in retirement

Budget 2024: what really matters for those approaching and in retirementThe winners are, pretty much anyone who still pays tax - which is our pre-retirees - who will get a handsome stage 3 tax cut. Another smaller win will be felt by anyone living in a home paying an electricity bill as they get a $300 rebate on electricity costs.

Pensioners will get a couple of wins. The first is that the cost of medicines at $7.70 for 60 days under the PBS will not go up for five years. The second, if they pay rent, is through another 10% increase to the Commonwealth Rent Assistance program.

And the freeze in the deeming rate on financial assets for the Age Pension income test is another little win, but won’t affect too many people.

But let’s take a deeper look at the budget for Prime Timers and Epic Retirees!

A freeze on Pharmaceutical Benefits Scheme pricesThere will be a freeze on the price of medicines under the PBS for people over the medicare safety net for 1 year. And, for age pensioners for FIVE years. Those who are eligible can get 60 days of medicines for $7.70 under the PBS.

Chalmers said in the telecast that this would mean “no pensioner or concession cardholder will pay more than $7.70 for the medicine they need”.

The Medicare Levy thresholds have gone upThe low-income thresholds for the medicare levy have increased. This is helping them to keep up with inflation basically, so it’s not a big move.

For single seniors and pensioners, the threshold has increased from $38,365 to $41,089

The family threshold for seniors and pensioners has increased from $53,406 to $57,198

Cost of living electricity rebateA $300 cash rebate for every household provided as a reduction to power bills. This is not means tested. Every Australian household will qualify. This will come on top of the rebates offered by the state governments in QLD and WA.

Stage 3 tax cuts for workers arrive 1 JulyThe stage 3 tax cuts have arrived. These were announced earlier this year. For those in the highest tax bracket, these tax cuts will result in annual savings of $4,529. On average, taxpayers will save $1,888 each year. If you’re approaching retirement this little windfall could be used to lift your super balance.

A 10% bump to Commonwealth Rent AssistanceWe know renters are really feeling pain. So a 10% increase in the Commonwealth Rent Assistance payments will be well-received. This comes in addition to the 15 per cent announced last September. Every dollar helps.

Carer payments changeStarting March 20, 2025, there's a small change happening for people who receive Carer Payment.

Before, they were allowed to spend up to 25 hours per week on certain activities like work, study, volunteering, and travel combined. Now, they can spend up to 100 hours over four weeks, but this limit only applies to work, not study, volunteering, or travel.

If someone goes over this limit or uses up all their temporary breaks from caring duties, their payments will be stopped for up to six months instead of being completely cancelled. They can also use single-day breaks instead of having to take at least a whole week off if they go over the limit.

So, it's a change in the rules to give carers a bit more flexibility without losing their payments entirely.

A freeze on deeming rates for the Age Pension and Commonwealth Seniors Health Card income testThe government has frozen deeming rates for one more year.