Bec Wilson's Blog, page 10

March 25, 2024

Retiring by choice - something only one third of people today do

Feature article: Retiring by choice - something only 33% of people today do

Prime Time podcast: The feelings of invisibility in midlife with Jane Tara

From Bec’s Desk: My big milestone

Your letters: A ripper from Peter about safe spending numbers

I invite you to take the Epic ‘Retirement Planning’ Survey. This is a detailed survey that dives into how you feel about the process of ‘retirement planning,’ what tools you are using and how you are progressing. It also gives me a read on how confident you feel, and what you might need to help you.

It’s all multi-choice so it should be quick and easy. I’ll be using the results to produce a report (which I’ll share with you) and educate the industry - guest speaking for financial advisers, super funds and other companies who really want to do right by you, the modern pre-retirees. I’ve added a little prize too… Three people who complete the survey in full, including the competition at the end, will win a $100 VISA card (conditions apply).

Retiring by choice - something only 33% of people today do

Retiring by choice - something only 33% of people today do

We all talk about retirement as a time of life when you get to choose what you do with your time and hopefully, really get to enjoy yourself. And, if you have planned for it and are prepared, both financially and functionally when the time comes, there is no reason why it shouldn't be epic.

I make a lot of noise about getting yourself ready for retirement and pacing yourself into that stage of life slowly when the time feels right for you. The fact is, you don’t always get to choose when you retire. In fact, the team at Colonial First State sent me some research this week that showed that only about one in three Australians actually retire because they want to. The rest were kind of pushed into it by stuff they couldn’t control.

It’s confronting when you stop and think about it.

According to their survey, 33% of retirees they surveyed retired by choice but about 28% of retirees had to leave work because of health problems. And, 7% had to retire because their partner was dealing with health issues.

Then there was 11% who got laid off, 4% who felt like they weren't wanted at work anymore, and another 18% who had different reasons for retiring. I’m quite sure some of them would have stepped out of the workforce to care for their ageing parents, which the ABS Census says 4% of retirees do.

Now, why does this matter? Well, it means planning for retirement by choice isn't something you should put off unless you want to arrive in the position where you are forced into it at a time that is not of your choosing. You have got to start thinking about it early and with some pragmatism, knowing you have a plan, but also recognising that things might not all go to that plan.

So, what steps can you take if you’re worried about being one of those people forced to retire early? For a start, you can use those worries to fuel you to work on your preparation and understand your best case plan, and a less optimal but sensible plan too. If retirement comes early you’ll then know where you might be able to adapt your retirement planning, and be clearer on the steps you need to take versus the ones you can choose to take. Here’s some sensible steps to think about:

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Craft a Plan A and Plan BLife has a way of throwing unwelcome curveballs, so it's wise to have exciting goals and an understanding of your backup plan. While you may have a dream retirement scenario (Plan A), it's also worthwhile outlining a contingency plan (Plan B) in case things don't go as expected. This means thinking about how you can adjust your retirement goals and vision to adapt to a scaled back version in case there’s unexpected or expected changes to your circumstances. Maybe your Plan B reduces your ambitions to align your post retirement income with your pre-retirement income; or allows you the budget and time out of active retirement to care for a loved one before resuming your travel and lifestyle ambitions a little later in life. Or, it might see you downsizing to tip more funds into superannuation earlier so you have enough to live a modest or comfortable retirement rather than working a couple more years.

Remember, some flexibility is key when it comes to retirement planning for tricky situations. By preparing for different scenarios, you'll be better equipped to navigate whatever challenges may come your way.

Become acutely aware of your budgetIf you build and understand your retirement budget based on your goals, you’ll have the perfect tool to use to recalculate your costs of living should things change.

You’ll want to separate your budget for your cost of living, required one-off expenses you need, and your epic retirement experiences. When you separate them you will find it easier to build the budget, but also to de-construct it if you need to cut your costs of living or axe some leisure costs. You can learn how to build your budget in the How to Have an Epic Retirement 6 week program.

Explore ways you can start to diversify your income in the lead up to retirementRelying solely on one source of exertion-based income as you loom toward retirement can leave you vulnerable to shocks. Basically, you can be laid off at any time, and that risk gets higher with age and ageism in the workplace sadly. To mitigate this risk, many people consider diversifying their income streams in pre-retirement, especially if they want to play an ongoing role in the workplace and start to enjoy a part time retirement alongside it. It’s something many people call building their ‘portfolio career’. This could involve exploring part-time work or consulting opportunities or even building a portfolio career, renting out property, or investing in dividend-paying stocks or bonds. By diversifying your sources of income, you'll create a more resilient financial foundation that can better withstand unexpected changes in your retirement plans. Plus, you should have greater flexibility to adapt your income strategy if early retirement in a key role becomes a reality.

Remember, being proactive and prepared for your dream situation, but also your Plan B is key to making sure you make your retirement as epic as it can be, even if the planning doesn’t quite go to plan.

This week I am talking with Jane Tara, the author of Tilda is Visible, one of the hottest bestsellers on the women’s fiction list right now.

Tilda is visible is a very relatable story for women in modern midlife. It’s about a woman in her 50s who wakes up one morning and her little finger and her ear are missing. She’s diagnosed with invisibility by her doctor. The story is a comedic fiction book about her journey to see herself again. It’s an easy read, and I love that there’s a juicy love interest, and a few really powerful self-help lessons woven together into the book. It tackles a time of life that isn’t written about in this way very often. We don’t talk enough about the feelings of invisibility in midlife.

The book is resonating because it talks about a very relatable stage of midlife that may not be commonly spoken about.

Listen nowLISTEN HERE - LATEST EDITION (E17) - OMNY

or listen on APPLE PODCASTS

Exciting moment yesterday! I received my first royalty cheque as an author. And last week we charged through more than 10,000 books sold via retailers and even more through audiobooks, ebooks and industry orders.

For those unfamiliar with the writing world (which I was previously), apparently 10,000 printed non-fiction books sold in 9 months through retailers is a very healthy number for a purely Australian focussed book. And receiving royalties as an author isn't always guaranteed or even common, making this moment even more special.

It is a wonderful feeling to know your little passion is well-read. I'm all for cherishing the journey and the little moments. Thank you to everyone who has supported me along the way and to everyone who has bought the book and told their friends about it – your encouragement and support for Epic Retirement means the world to me!

In case you haven’t got a copy yet - you can buy How to Have an Epic Retirement, the book on Amazon and Booktopia and in many bookstores. It’s in reprint again! Keeps running out of stock in stores 😎.

—

Last week I attended a conference packed with academics, actuaries and superannuation product specialists in Sydney about the ‘future of the retirement phase of superannuation’ and the conversation was all about longevity. It was all about how we’re going to be able to make peoples’ (your) money last with greater confidence in retirement.

The industry is deeply focussed on this right now, trying to work out what ‘financial products’ they can and should offer pre-retirees and retirees to try to give them more certainty about their retirement income, especially if they think they’ll outlive life expectancies.

There was no conversation about improving pre-retirement education in this room at all. I guess you’ll just have to keep asking your funds about that.

But, if you’d been a fly on the wall, you’d have felt very pleased at how much attention building products for those approaching retirement are getting in the industry right now. Everyone is trying to work out what products they can offer you so you can simply relax and have an epic retirement. Most products will take months or years to enter the public domain. I’m going to dive deeper into this as they show their hands, to better explain the whole concept of retirement financial products. But not until it’s clear what features the industry is prioritising and for whom each is targeted. So hang around, I’m watching this space.

—

The How to Have an Epic Retirement Flagship Course is up to week 3, and the 250+ people doing it are continuing to rave about their experience. Last week we covered retirement budgeting which I received many complements for. This week it’s all about superannuation, financial advice and estate planning. If you’d like to come to our next 6 week program, we’re taking expressions of interest for a May/June/July program. I’ll release more details after Easter.

Express your interest for the course

And finally, thanks, there has been a huge response to the Epic ‘Retirement Planning’ Survey. I am absolutely delighted at the insights you’ve shared into how you feel about retirement planning. We’ll start on the report very soon, which I’ll share with you when it’s released at industry events coming up.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

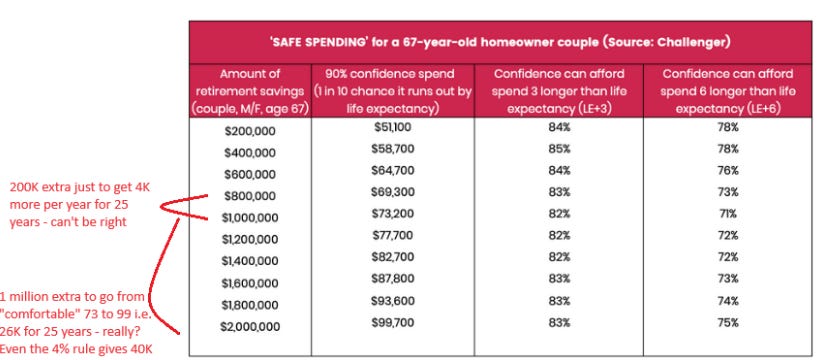

I got this excellent email from Peter today. Such a great question that I had to share it with you. I wish everyone would read things this closely! Thanks Peter.

Don’t hesitate to send me your questions… I love to answer them so long as they aren’t personal financial advice. Email Bec@epicretirement.net

Hi Bec,

I recommend that you have a closer look at the Challenger table featured in your recent podcast notes and Sydney Morning Herald article about safe spending as I can't see how it can be right.

Cheers, Peter.

Hi Peter

It’s interesting. You’ve just discovered the ’sweet spot’ between where someone gets income from the age pension and where they have to fund that gap without access to the pension at all. 😉

There’s this strange little anomaly in our retirement system that’s truly worth understanding. It’s the fact that people with less superannuation can actually end up earning more retirement income - just by knowing how to use the systems of retirement well in Australia.

It’s called the “sweet spot”, and it’s where both singles and couples with a lower superannuation balance leverage the age pension alongside their superannuation income stream to earn more in retirement income than someone with a far larger superannuation balance can at the same drawdown rates.

I have written about the sweet spot here in the Sydney Morning Herald a few months ago. https://www.smh.com.au/money/super-and-retirement/the-sweet-spot-how-to-earn-more-while-having-less-in-retirement-20231124-p5emjw.html

Admittedly, the Challenger projections are designed for ‘safe spending’ too, so don’t expect them to be aggressive. Have a great day! Make it epic!

Cheers Bec

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

March 23, 2024

How much can you safely spend in retirement? We crunched the numbers

As you read this I’ll be enjoying a whole hour on 3AW Melbourne with the legendary radio host, Darren James (DJ) on Sunday Breakfast at 9am this morning. If you’re in Melbourne, have a listen and tell me if you hear me!

This is the easy-read Sunday edition of my newsletter designed to bring you my column in The Age, The Sydney Morning Herald, Brisbane Times and WA Today on Sundays. This week it is all about how much you can afford to spend in retirement when you look at your super balance going in. We crunched the numbers, contemplating how your superannuation pairs up with the age pension and how much you might be able to ‘safely spend’ over an average lifetime, and a longer than average lifetime.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

There’s two other things I’d love to bring to your attention today, before you dive into the article below.

The Epic ‘Retirement Planning’ Survey is roaring. If you haven’t responded yet - please consider doing it today.

It’s an important survey that will allow me to better understand you and guide the industry to give you more of what you need. It dives into how you feel about the process of ‘retirement planning,’ what tools you are using and how you are progressing. It also gives me a read on how confident you feel, and what you might need to help you.

It’s all multi-choice so it should be quick and easy. And, you might find some of the questions really get you thinking about the process of retiring, and what you could be doing vs what you are doing. So dive in and help me out - please.

The Epic Retirement Course is going so well I am ready to plan the next one.

I am taking expressions of interest for the next Epic Retirement 6 week program which is being set up for May/June. We’re up to week 3 of the Mar/April program and so far it’s going swimmingly! We’ve had feedback this week like:

“I am learning a lot and finding the course enjoyable,”

“The course is really informative and presented well and the content is exactly what I was looking for,” and

“Loving the course so far, getting a lot out of it - thank you!”

So if you want to get in on our next one, sign up for the information here. There will be limited earlybird-priced spots this time.

Express your interest for the course

I had a ripper of a week in Sydney this week. I’ll tell you all about it on Tuesday in the big epic newsletter.

Have a lovely Sunday and Melbournites don’t forget to listen in to Breakfast on 3AW. Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

How much can you safely spend in retirement? We crunched the numbers

How much can you safely spend in retirement? We crunched the numbers

Most people, whether individuals or a couple, set a savings target for retirement, something similar to “I want to have $200,000, $400,000, $800,000 or $1,000,000, or perhaps even more available as a lump sum to fund my retirement when I get there.”

Even when you have a healthy lump sum, it’s pretty hard to work out how much money that will allow you to safely spend each year without running out of money. So this week, I’m exploring how much you can afford to spend if you want your money to last a lifetime, and what level of income that will support when you take in the age pension too.

But before we get to the big numbers, we need to understand a couple of key concepts that go into working this out.

First there’s how much do we need to live comfortably in retirement. This forms the baseline for spending on everyday living. The Association of Superannuation Funds of Australia (ASFA) says that a retired couple aged 65-84 needs $72,148 per year, and a single person needs $51,278 to live in ‘comfort’. If they’re living a more modest lifestyle, a couple needs $46,994 and a single person needs $32,665.

This assumes that you own your own home outright, and can access a part-aged pension. These amounts alone won’t give you an epic retirement per se, but it will provide us a number to compare with when we explore how much we can spend and how much we need to spend on costs of living.

The second important concept is the age pension, which 62 per cent of Australians use. For those people, the maximum amount they can take is $43,752 for a couple and $29,023 for a single person, and in addition to this, they become eligible for rent assistance which could be up to $177.20 per fortnight for couples or $188.20 per fortnight for single people.

The third important concept is how you want to budget for your own spending in retirement and in what type of spending pattern. At the core, when we talk about safe spending, we talk about safely planning for your needs, or your cost of living first, then building an additional budget for your wants, or your one-off costs and retirement experiences.

Fourth, a key ingredient of safe spending is considering how long you might live. Life expectancy for an average Australian over 65 right now is 85.3 for men and 88 for women. Any planning for safe spending really has to consider the possibility of living longer than the median life expectancy, which is more possible than ever with modern health standards.And finally, the concept of ‘safe spending’ itself, which means to have confidence to spend your retirement savings and have a 9 out of 10 chance that you will have enough money to reach your life expectancy, or perhaps even three or six years beyond it.

So let’s talk safe spending amounts, starting with a 67-year-old homeowner couple with a variety of different joint superannuation balances as they reach retirement. In the below table you’ll see that the team from Challenger have plotted how much a retired couple could draw down with a 90 per cent degree of confidence their money could last to life expectancy.

There’s lots more in this article including two really powerful tables. It has been published in full in print and digital in the Sydney Morning Herald, The Age, The Brisbane Times and WA Today Money section today. You can read it here (without a paywall).

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

March 18, 2024

The 15 minute retirement plan

Take our Epic ‘Retirement Planning’ Survey

Feature Story: The 15 minute retirement plan

From Bec’s Desk

Your letters: Starting over pension thresholds

Take our Epic ‘Retirement Planning’ Survey

Today we’re kicking off the first of two really important surveys that will allow me to better understand you and guide the industry to give you more of what you need.

The first is the Epic ‘Retirement Planning’ Survey. This is a detailed survey that dives into how you feel about the process of ‘retirement planning,’ what tools you are using and how you are progressing. It also gives me a read on how confident you feel, and what you might need to help you.

It’s all multi-choice so it should be quick and easy. And, you might find some of the questions really get you thinking about the process of retiring, and what you could be doing vs what you are doing. So dive in and help me out - please.

I’ll be using the results to produce a report (which I’ll share with you) and educate the industry - guest speaking for financial advisers, super funds and other companies who really want to do right by you, the modern pre-retirees!

I’ve added a little prize too… Three people who complete the survey in full, including the competition at the end, will win a $100 VISA card (conditions apply). Complete it now.

The 15 minute retirement plan

I saw an advertisement for a ‘15 minute retirement plan’ promoted this week and I couldn’t resist clicking on it. I clicked, then I went down a rabbit hole trying to find out what they were promising in their amazing plan that could purportedly make a process I teach in 8.5 hours with 6 hours of expert Q&A so darned slick and simple.

The ad led me to a web form requesting personal details - name, email, address, phone number, and exactly how wealthy I am before I could get access to the elusive guide. I used a pseudonym to access it. Then, when I did download it, it sure as sugar didn’t provide me with a guide on how to do it all in 15 minutes, or even how to do it at all. Instead it told me how hard and complex investing is, and how I could never do it without their professional advice. Essentially, the guide prescribed a single solution: enlist the services of their investment company and allocate the remaining 14 minutes to prayer. This felt like clickbait for retirement planning.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

The lesson… I’m quite sure that there will be a few companies who will have a go at sucking you in over the years ahead with these types of things. So, I want to make sure you’re smarter than that!

I want you to know that there’s no shortcut to planning for your retirement yourself. Sorry! Even engaging an experienced and capable adviser won’t take away the need to shape your own plan using their advice. Learning about it yourself IS key.

I want you to recognise that it’s perfectly normal to feel doubt, uncertainty and fear at this stage of life, and to use that to LEARN, not let it lead you to buy ‘quick fix solutions’. Embracing this truth allows you to sit back and take a more sensible approach to the years and journey ahead.

The transition into retirement really is best taken slowly with patience and a fair dose of introspection. As tempting as it is to seek a ‘get retirement quick’ approach, you must remember that you can’t rush real progress. (Gosh I’m full of cliches today aren’t I!)

Instead, tell yourself that you have to invest your time into the process of learning how to retire well, and take that time to consider what you want your retirement to look like. Then, once you are able to start to contemplate a picture, it’s time to work through the simple but time-consuming process of learning about retirement and how it works. That knowledge which you should seek from multiple sources - financial advisers, your super fund and other experts (of which I am just one) - will allow you to feel more confident as you move towards and into retirement, ideally more slowly than it used to be prescribed.

Of course I think there’s some important lessons from this ‘get retirement quick’ approach - and they are basically ‘do the opposite’. 😉

Build your own vision of retirement, don’t buy someone else'sEvery single person I speak to has a different vision of what retirement means for them. And that’s OK. The proactive ones take ideas and inspiration from everywhere, watching their friends, reading books, watching movies and documentaries, and keeping up with media stories too. Then they sit back and contemplate how they can combine them to form their own picture. That’s the beauty of being older and wiser. We don’t all want to do the ‘same thing’ as everyone else like we did when we were young. And we know we don’t have to be wealthy to have an epic retirement.

A retirement plan is no longer a prepackaged wealth solution sold by a financial institution. It is now about embracing a learning journey that incorporates sound advice, education and a willingness to find what’s right for you in the next stage of life.

Understand your financial landscape early onMoney is important, but there’s many facets to your retirement finances. You need to work through the creation of your own financial balance sheet, budget and investments and then really understand how your money is meant to work in the next stage of life. It might be a process that you abhor or even fear, but it’s also one of the most critical parts of retirement planning. Remember the difference between a vision and a plan, is that a plan is realistic and practical. It needs to work when put into practice. This is a big job. There’s saving for retirement using tax-effective concessions, budgeting your cost of living, investing your hard earned superannuation over the long term and monitoring it. Then there’s understanding the systems of retirement like superannuation and the age pension and how they fit around you and learning how you will create a layered income from all these sources that will last a lifetime. And finally, there’s working out how much you can afford to spend, without running out of money.

Consider this: you're embarking on a new chapter of life that could span 30 or 35 years. Will you rely solely on advisers to handle everything, or will you take the time to understand the ropes yourself and seek their guidance as needed?

I simply want you to know how to ask the right questions and feel calm because you know what’s quite likely to be ahead of you.

Go looking for your sense of purpose in the next stage of lifeWe all fear irrelevance. Whether we’ve worked in a hospital, cared for a family all our lives, or climbed up a corporate career, we all get to a point where change is inevitably going to lead to a shift in our daily activities. So rather than let it take you by surprise, take that bull by the horns and go looking for ways you can be more fulfilled from your days. Look for new activities, new social communities, and new organisations you can contribute to. Or lean into some you’ve been trying out and enjoy. That way as you head into retirement, you’ll feel invigorated as you move towards something, rather than afraid as you step away from something.

Take control of your healthYou’ve heard me say it many times before - you can’t have an epic retirement without your health. So what are you going to do about it? We all need to do 150 minutes of zone 2 cardiovascular exercise each week, and 2 sessions of muscle mass exercise too. We also need to work on our balance, ideally 3 times per week. That’s the most sensible way to manage ageing. No vitamin, supplement or potion will do a better job than good old exercise. Every retirement plan should have a commitment to looking after your health, if you want to enjoy your life that is. So what’s yours?

Think about ageing in placeWe all need to more actively strive to steer clear of aged care, both for the cost and for the unpleasant experiences involved. There’s one way we can possibly try to do so, and that is by really putting more thought into where we live as we get older. If we want to try to prepare ourselves better than the generations before us, choose a home with no stairs, and equipped with the modifications and nearby homecare services that support growing old in the home. If you didn’t read my article last weekend, go back and have a look.

Resolve to spend on the good bitsThe government is very worried that the current generation of retirees, most of whom have been saving for retirement for 32 years, are now too afraid to spend their money on the good bits of life. So don’t forget to plan for this part. This is what I call your ‘epic retirement experiences’. You can see this as travel, family moments, passions, and things that bring you a sense of purpose. Just don’t forget to invest a little of your hard-earned money in the things you’ve always wanted to do. You can plan for it in your financial plan, and dream about it in your vision setting, just don’t forget to live it!

Feeling inspired to take control? It really is important to resist the temptation of quick fixes in retirement planning. The really good bits come from taking the time to understand your wants, fears, and dreams, learning how the systems or superannuation and the pension work, investing for the long term, and seeking really trust worthy financial advice. This gradual process leads to a future that you shape yourself with a combination of careful preparation and personal growth, not rushed decisions and quick fixes.

PS. If you need a financial adviser please don’t select them based on downloadable clickbait. Please ask the most financially secure and sensible friends you have who they use, and evaluate from there.

I’m buzzing! The first 6 week How to Have an Epic Retirement flagship course is more than a week in to the program, and it’s going swimmingly! The lessons are being voraciously consumed by the hundreds of participants. The Community Zone is a hotbed of conversation and the live Q&A last Thursday was terrific. Everyone got into the question-asking, and the wonderful Mark Lapedus from Allianz Retire Plus did a great job of answering them. Many thanks Mark!

I’ve resolved to launch another 6 week program in May (Dates TBC) for completion in May-June. You can express your interest here for the earlybird price release and download a brochure.

As you might have seen, last week we did a deep-dive into the recommendations of the Aged Care Taskforce last week on the Prime Time podcast, learning from William Burkitt the CEO of Care & Living with Mercer about how the cost of aged care and home care might change. It’s clear we are all going to have to plan for the cost of aged care and home care when we plan for retirement. But there’s one other thing I want you to know - and that’s how you can minimise your risk or time spent in aged care by making better housing decisions. Have a listen and a read.

PODCAST: “The real cost of care and how it might change with William Burkitt”

ARTICLE IN THE SYDNEY MORNING HERALD/THE AGE: “Why you must now plan for aged care during retirement”

Don’t forget, this week I’m off to the Central Coast of NSW for an event for the 2024 Seniors Festival Community Book Talk. It’s on Friday 22nd March 2024 10.30-12 at Brentwood Village. More info and register to attend here. If you’re in the region, come along. We’ve got Bookface there selling books too - so I can sign them!

Now please, get on over and do the survey, if you haven’t already! I’ll be really grateful.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

In case you haven’t got a copy yet - you can buy How to Have an Epic Retirement, the book on Amazon and Booktopia and in many of the major bookstores.

Hi Bec,

Thank you for your wonderful book. I purchased it following your interview with Virginia Trioli on radio Melbourne last year. I have since recommended it to everyone I know over 50 !

I have a question regarding a point in your book. On page 33, you mention that a single person requires $595,000 in savings for a comfortable retirement, along with additional funds for one-off purchases and epic endeavors, totaling $675,000. However, I'm concerned that having $675,000 in savings would exclude me from receiving a part pension. Am I correct in this understanding?

I am interested in attending your epic retirement course; however I work Monday evenings. Are the sessions recorded for later viewing?

Many thanks Bec, love your work and your passion

Kind regards, Trish

Hi Trish

Lovely to hear you are so interested in your own retirement situation. And thanks for recommending my book 😊. While I can't offer personal financial advice as I'm not a financial advisor, I can provide general insights into how the age pension works.

As you can see on Services Australia’s website here the assets test for the pension has a cutoff of $667,500 for a part pension. https://www.servicesaustralia.gov.au/assets-test-for-age-pension?context=22526

The average person with assets of about $675,000 spending $51,000 per year which is what ASFA deems is a comfortable retirement, may be eligible to access the pension in the first or second year of retirement, provided they fall below the assets test threshold and do not go over the income test triggers. Over time, people evaluating how to navigate the age pension and income from superannuation might like to explore finding the ‘sweet spot’ where the age pension and income from your superannuation are more carefully balanced. Ask your super fund or financial advisers to help you understand your own personal situation better. These strategy decisions are important to understand and get advice on, and take time to consider the impacts of on your financial circumstances throughout your years ahead.

Regarding the course. It kicked off last Monday - but the actual program is watched in your own time. It is all pre-recorded. The only activities that you need to do together are the live Q&As which in this program are being held on Thursday nights at 6pm Sydney time. It’s really flexible.

There will be another one in a few months - it will kickoff in May/June. You can register to find out more here.

Hope that helps! Have a lovely week. Cheers Bec

Now for a poll… I know you love them!

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

March 16, 2024

Why you now must plan for aged care when you plan for retirement

This is the short Sunday email, designed to bring you today’s article from The Sydney Morning Herald, The Age, WA Today and Brisbane Times. And today I’m digging deep into how to plan for homecare and aged care when you plan for retirement.

I’ve also included the cracker of an interview I did with William Burkitt from Care & Living with Mercer this week on the Prime Time Podcast about “The real cost of care and how it might change with William Burkitt”.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

We’re headed into week 2 of the 6 week Epic Retirement Flagship Course this week and the feedback is SUPERB 😊. We have hundreds of people working hard to learn how to make their retirements truly epic. Their signed copies of How to Have an Epic Retirement - the book are all packed and ready to leave first thing Monday! Boy was that a big job!

If you missed this release - we’ll look to do another 6 week course event in May/June. You can express your interest here to be notified of our earlybird release when it happens.

Don’t forget, this week I’m off to the Central Coast of NSW for an event next week for the 2024 Seniors Festival Community Book Talk. It’s on Friday 22nd March 2024 10.30-12 at Brentwood Village. More info here. If you’re in the region, come along. We’ve got Bookface there selling books too - so I can sign them!

And I’ll be in Sydney for a big retirement industry conference too! That should give me lots to write about next week!

Have a lovely Sunday. Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Why you now must plan for aged care when you plan for retirement

Aged care and home care used to be something that you could worry about later in life, or, frankly, leave for your kids to worry about for you. But the recommendations delivered in the final report of the Aged Care Taskforce this week leaves us in no doubt: aged care and home care services are about to become something you need to plan for at retirement.

There were three big takeaways for me in the report for everyday people. The first is that people should be planning for their care needs when they plan for their retirement. The second is that we should expect to pay for the standards of accommodation and services that we want to have in our later years of life, and only look to the government to support our care needs.

And third, if we don’t want to pay for aged care accommodation by the day for long periods of time, that we really should look hard at where we are planning to live in our later years in life, and prepare for ageing better.

This will be a big shake-up for the aged care system. Some might see the suggestions as positive, others will feel like they might lose out. And we won’t know which recommendations the government will adopt or how they’ll implement it until the budget leaks start.

There’s no question that the government will continue to help those who cannot afford to pay for care. But for everyone who owns their own home and has a healthy super balance, you need to take this seriously. Here are three things we all should understand.

How home care services work and how to budget for themThe government offers four levels of home care packages, each of which give people a level of in-home clinical care, and access to a range of other more basic care and support services. The consumer can drive how this is spent to suit their needs, within the list of approved services.

We can get angry, shake our fists at change, or we can get on with it and plan for our futures.

There are no obvious plans to change this. In fact, the taskforce supports this continuing, possibly only with a decrease in focus on non-clinical services.

To put this in perspective, the highest level of in-home-care funding available today amounts to around $59,000 of home care funding per year, which equates to 10 to 13 hours of care services in the home per week.

So if you see yourself needing to supplement this, just like you may have in your working life, by paying for carers, cleaners, gardeners or other support, you will need to budget for it, with care priced upward from $100-$120 per hour on weekdays.

This is a much longer article packed with helpful insights. Read the rest of this article, on The Age, The Sydney Morning Herald, Brisbane TImes and WA Today. It is not paywalled.

The real cost of care and how it might change with William Burkitt

The real cost of care and how it might change with William BurkittAged care and home care have become a bit of a political football. But here's why you should be paying attention to it. It’s about to impact your retirement plans more directly than ever.

The Federal Government's Taskforce into Aged Care has just handed down its final report, and there's A LOT of noise around it. Two of the biggest takeaways from this report are firstly, the suggestion that people should be planning for their aged care and home care needs when they plan for retirement. And secondly, that we should expect to pay for the standards of accommodation and services that we want in our later years, and only expect the government to support our care needs.

This will be a big shake up for the aged care system. Some might see them as positive, others will feel like they might lose out. And we won’t know which recommendations the government will adopt or how they’ll implement it until the budget leaks start.

So today I chat with William Burkitt the CEO and Founder of Care and Living with Mercer about how we should plan for our aged care, home care and options for ageing in place when we retire. His business provides families with support in navigating the aged care and homecare systems.

We start by diving into the fundamentals on care that we all need to know. Then we dig into the taskforce’s final report and what lies ahead.

Listen nowLISTEN HERE - LATEST EDITION (E16) - OMNY

or listen on APPLE PODCASTS

Interested in joining an upcoming Epic Retirement Education Program?We’re currently taking expressions of interest for another 6 Week Epic Retirement Education Program in May/June. If you’re curious and want to make sure you get our best earlybird pricing, you can register your interest and find out more here. You can also download a brochure and we’ll send you the list of handpicked Live Q&A guests in coming weeks.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

March 11, 2024

The power of deciding for yourself what retirement means

In this edition

Feature story: The power of deciding for yourself what retirement means

Juicy titbit: Keep an eye on the Aged Care Taskforce report and what happens next - it might impact you more than you realise.

From Bec’s Desk

Your letters

Prime Time Podcast

The power of deciding for yourself what retirement meansWe all have different preconceived notions of what retiring means. And we forget that to each of us, it means something different. Our own definition is built from our personal influences, experiences and judgements. Think about it.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

For some, the image of retirement is coloured by people who have parents who worked well into their late 60s or 70s. For them the question then arises: was this a positive or negative for their lives?

In contrast, others have experienced the untimely loss of parents, partners or friends who never had the chance to embrace the joys of retirement. This might serve as a powerful reminder that life is fleeting and you must seize the moment, seeking it out sooner than later.

And for others retirement is something they associate with growing old and beige, having watched their parents or grandparents live less fulfilling and quite sedentary lives than are common in 2024.

One of the big challenges we face is the stigma associated with the term ‘retirement’. To some it feels like a label that implies the time when you withdraw from life, and step back from the vibrant and active existence they once knew into the shadows and slink into a recliner to pass the time. If this is you, I think it’s worthwhile taking a deeper look at your inner thoughts and reframing them.

In the freshly launched Epic Retirement Flagship Course, one of the first challenges for people is to share when they think they might want to retire. This week, Kathy in the cohort pointed out that some people might say she is retired now, simply because she isn’t earning a wage at the moment after a career change that didn’t quite work out the way she’d planned. But she doesn’t ‘feel retired’ so she’s decided that she isn’t retired yet. During the course she’s keen to define what being retired means to her, not let other people define the meaning of retirement for her and badge her with it before she is ready. I really appreciate this perspective. I know a few friends in their 50s who don’t work, but equally they don’t want to call themselves ‘retired’.

Over the last year I’ve looked the word ‘retirement’ up in a few dictionaries to get some perspective on why we think this word is so negative. It seems dictionaries are not ‘up with the times’ that I roll in. They haven’t caught on to the Epic movement.

In the Oxford Dictionary ‘retirement’ is defined as ‘the action or fact of leaving one's job and ceasing to work’.

In the Merriam-Webster Dictionary, it’s “withdrawal from one's position or occupation or from active working life.”

And in the Cambridge Dictionary it’s “the act of leaving your job and stopping working, usually because you are old”.

I’ve written a new definition, far more suited to people approaching retirement today in my opinion.

To me, retirement is simply defined as “the stage of life where you move from living off your own exertion, to sourcing your income from pensions, investments and work you really enjoy and choosing what you do with your time”.

It is not a statement of ‘ceasing to work’ or ‘withdrawing’. It is not even about our sense of identity. It is simply a statement that acknowledges retirement is a phase where we draw our income from passive sources not active sources. That’s it. Then you get on with living life however you want. You can sit back in a recliner and rest, or you can get out there and make it epic.

This might seem like a lot of fuss over a definition, but anyone facing retirement head on and trying to work out what this stage of life means for their identity will understand what I’m talking about.

People define you with this word once you no longer have a title. When we are asked “What do you do?” during our working lives, giving the answer is fairly easy. We are judged based on on our level of social or commercial hierarchy. But if you respond with “I am retired,” the next part of the conversation is left hanging because so much of our identity is unclear after that. I’ve found the key is to respond with passion, to break the stereotype and to give people a new-word picture. I’m retired, and loving it…. Then tell them about the things you feel a sense of purpose or higher meaning in.

Remember always, that retirement is not an identity. It is only a statement of how you draw your income in the next stage of life. You decide your identity and what you do with your time, and yes, it can be epic!

JUICY TITBIT: Keep an eye on the Aged Care Taskforce report and what happens next - it impacts youDon’t skim past this. It might not seem relevant but if you have ageing parents it could well be important.

The Aged Care Taskforce has dropped its big report this morning, a really important report for all of us that will form the basis for political discussion in the next few weeks. Keep your eyes out for this one. Some say the next political moves could be to tie the funding of aged and home care to superannuation balances - but that could be just media hot air. Let’s wait to see how it pans out.

This report talks about our parents and calls out a variety of changes they say are needed to the aged care and home care systems to make them fairer and more sustainable. Let’s watch this space. I think the recommendations on the report are interesting and seem quite fair. It will be anyone’s guess where politics takes it.

Quotes like this will leave us wondering:

“Generally, older people are expected to be wealthier than their predecessors, largely due to the maturing superannuation system. As a result, the proportion of people over 65 years of age accessing the Age Pension or other income supports will decline by around 15 percentage points by 2062–63. Of those receiving a pension, fewer will be full-rate pensioners and more will receive a part-rate pension due to increased accumulation of income and assets. Over the next 20 years, the number of people with superannuation balances at age 85 will grow considerably, with a greater proportion of people having significant funds available.

The Taskforce notes the superannuation system supports Australians to save for retirement. The government’s proposed objective for superannuation is: ‘to preserve savings to deliver income for a dignified retirement, alongside government support, in an equitable and sustainable way’. Income from superannuation should be drawn down in retirement to cover health, lifestyle, other living expenses and aged care costs. These superannuation trends, combined with high asset wealth through the family home and other investments, mean increasingly people still have accumulated wealth and income streams when they need to access aged care services. As a result, there is more scope for older people to contribute to their aged care costs by using their accumulated wealth than in previous generations.”

Just an important area to be across - particularly if you have ageing parents or are trying to budget for your own costs of ageing in the future.

Back in the real world, without politics. Another juicy week. It was all about women last week, with my Prime Time Podcast interview with Mary Delahunty from the Association of Superannuation Funds of Australia hitting just before International Women’s Day when the government announced they would finally pay superannuation on maternity leave. It was an awesome conversation.

Here’s a fun clip. The podcast is called ‘Practical ways women can fill the superannuation gap: With Mary Delahunty’ and it’s a ripper. If you haven’t signed up for the podcast newsletter you can do that here at primetimers.net.

Too little too late for today’s retirees though, so in the Sydney Morning Herald and The Age on the weekend I did a written feature on ‘the practical ways older women can fill their superannuation gap’.

The How to Have an Epic Retirement Flagship Course launched on Monday and now I get to soak in the stories and experiences of hundreds of pre-retirees who are building their picture of the next stage of their lives for the next six weeks. I could not be more in my happy place than in our private Community Zone hearing the stories of hope, excitement and fear and offering robust education on the things people really need to know. If you’ve missed this start date, you can sign up for the next course event which will probably be in May/June. Express your interest for the earlybird release here.

I’m off to the Central Coast of NSW for an event next week for the 2024 Seniors Festival Community Book Talk. It’s on Friday 22nd March 2024 10.30-12 at Brentwood Village. More info here. If you’re in the region, come along.

Finally, last week I celebrated International Womens’ Day with the wonderful team at Services Australia (Brisbane), who put on a really cool panel event. Thanks for the invite team.

Wishing you a wonderful week! Make it Epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

In case you haven’t got a copy yet - you can buy How to Have an Epic Retirement, the book on Amazon and Booktopia and in many of the major bookstores.

One juicy letter today, from Bron.

Hi.

I am slowly reading your book and taking notes as I really want and need that epic retirement. I have two questions.

I’m 57 and have just over $350,000 in my super. I only earn about $76,000 gross but I salary sacrifice $200 per fortnight. I also save about $350 per fortnight. My husband and I paid our house off years ago. But after that we got a $75,000 house loan to do a couple of renovations. It’s now down to about $20,000.

I keep hearing you should pay your mortgage off but then I hear you shouldn’t because a bank will not loan you money over a certain age. So is it a yes or a no? And what’s all the fuss about credit cards? We don’t have one.

My other question is a bit of a request for help. I am trying to work out how much super I would need for a retirement that would include road trips, perhaps a new car, and 2-3 overseas trips before I’m 80?

Cheers Bron

Hi Bron,

I am afraid that I simply cannot answer these personal financial questions as I am not legally able to give financial advice. I do think they are something that your superannuation fund’s financial advice team should find easy to help you with.

The things I can comment on are the items of fact! So let’s talk about paying down your mortgage and what people mean when they say this… and about credit cards and budgeting for retirement. I hope you have a copy of my book. It covers all this! You can order a copy here.

Anyone can hold their mortgage at $1 for many years if they are within the term of their loan - paying down all but that last dollar - so it stays open, but the interest payments are all but gone. And that way people still have access to that wonderful redraw facility if needed. Whilst it is nice to get your mortgage papers back from the bank - the popular opinion is that the access to cash if you need it might be worth any annual fees required to keep the mortgage open if interest payments are nil. It’s something your should consider personally.

Now, credit cards - just be aware that after you no longer have a pay cheque it might be very difficult to get one. Banks don’t take ‘retirement income streams’ as an income source at this time. They can be handy for travel, even if you don’t use them at home all the time. It’s a really personal decision though.

And, to work out how much super you need, the best step is to take control as I talk about in the book, and set up a detailed post-retirement budget so you know how much you need. This is a really personal answer I’m afraid so you need to work through the process, plus, you’ll be much more confident if you do. You can read all about how, then download the excel template and build your cost of living, your one off purchases and your epic retirement goals, budget them out and then you will have a clearer picture. Here’s where you can access the excel budget: https://www.epicretirement.com.au/resources-and-tools

Hope this helps… make it epic! Bec

Got a letter for me? Email me at bec@epicretirement.com.au.

Prime TimePractical ways women can fill the superannuation gap with Mary Delahunty It’s International Women’s Day this week so we need to talk about the place where disparity is most felt by women in the second half of life, and that’s your superannuation. Too many women only figure out that they have been heavily disadvantaged over their lifetime as they approach retirement. The system isn’t set up fairly and it’s time we talked abo…Read more5 days ago · 5 likes · Bec Wilson

Prime TimePractical ways women can fill the superannuation gap with Mary Delahunty It’s International Women’s Day this week so we need to talk about the place where disparity is most felt by women in the second half of life, and that’s your superannuation. Too many women only figure out that they have been heavily disadvantaged over their lifetime as they approach retirement. The system isn’t set up fairly and it’s time we talked abo…Read more5 days ago · 5 likes · Bec Wilson

March 9, 2024

Practical ways for older women to fill their superannuation gap

This is the short Sunday email, designed to bring you today’s article from The Sydney Morning Herald, The Age, WA Today and Brisbane Times. And today it’s all about women!

I’ve also included the terrific interview I did with Mary Delahunty, the CEO of the Association of Superannuation Funds Australia (ASFA) giving more mature women practical steps about how to fill their super gap.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Don’t forget my Epic Retirement Course kicks off MONDAY! (More info below!)

Have a lovely Sunday. Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

There’s a stark reality all of us must face: most women today have super balances up to 25 per cent lower at retirement than men, even when we have comparable roles in the workplace.

This hits hard for women looking at retirement in the next 10 to 15 years, putting them at a severe disadvantage. Any policy change, which will be gratefully received by our daughters, is unlikely to touch the sides for today’s pre-retirees. We look at your options for filling your super gap later in life, or, if you can’t, helping you look into the gap head-on and deal with the fear.

There’s no beating around the bush here – the disadvantage imposed on women by the last three decades of the superannuation system is just plain unfair. And it’s today’s pre-retirees who bear the brunt of it.

Often, women who have dedicated their careers to crucial yet frequently underpaid sectors such as healthcare, education and hospitality find themselves at the greatest disadvantage as they approach retirement. And there are three big reasons why.

The first is the gender pay gap. Many women, even today, and certainly over previous decades, are paid less than their male colleagues, so their superannuation contributions are lower over their lifetime. As a result, their compound investment returns are also lower.

The second is the time we spend not working and not contributing to super. Many women take time out of the workplace to raise their children and care for ageing parents. This is a crucial role that we need people to play in society, and women shouldn’t be disadvantaged for doing so.

And the third is the lack of superannuation attached to maternity leave allowances, which the government has taken steps this week to tackle, announcing that superannuation would be paid on maternity leave provisions from July 1, 2025. It’s a good move, but it doesn’t help women staring at an existing gap.

So what can you do if you are an older woman facing retirement with a lower super balance?

Confront any fear and open your super fund statement. It might seem simple to say this. But many women with lower super balances admit feeling so hopeless about their super that they ignore looking at their statements and super fund’s emails and, as a result, they miss the opportunity to put themselves on a better path.

Mary Delahunty, chief executive of the Association of Superannuation Funds of Australia, said this is the first and possibly the most important step most women can take. “Don’t think that you are alone in the alarming numbers you may see. Take a deep breath … and face into it together with your super fund,” she says.

Read the rest of this article, on The Age, The Sydney Morning Herald, Brisbane TImes and WA Today.

Practical ways women can fill the superannuation gap with Mary Delahunty

The fight to help women level their superannuation up with their male counterparts requires a strong stance on two fronts. Practical help for today's retiring women and a battle for tomorrow's too.

In episode 15 of Prime Time we talk with the CEO of the Association of Superannuation Funds Australia (ASFA) Mary Delahunty about the practical ways that women with lower super balances can navigate their pre-retirement and retirement years, and optimise their position to achieve the best possible standards of living despite their disadvantaged super funds.

We also talk about the very important systemic changes needed in superannuation to prevent this problem in the future. Mary has some terrific ideas that policy advisers and governments might listen more to if the women’s voices around it were louder.

Mary Delahunty is a passionate advocate for women, fighting for the equal opportunity to build super fairly, and spends a huge amount of time campaigning the government to the challenges women face, more seriously.

In her role at ASFA, Mary Delahunty is one of the women who can really make a difference. So it’s a refreshing and entertaining conversation, perfectly timed for women’s day.

Listen nowLISTEN HERE - LATEST EDITION (E15) - OMNY

or listen on APPLE PODCASTS

FINAL CHANCEThe How to Have an Epic Retirement Flagship Course kicks off on Monday (11th March)!Hundreds of people have booked for the upcoming How to Have an Epic Retirement Flagship Course. Launching TOMORROW 11th March, the course offers 8.5 hours of online lessons, and a practical 85 page workbook, dripped over 6 weeks; weekly live Q&As with some of the retirement industry’s most respected leaders, a community of people approaching retirement to learn with… and me - Bec Wilson, as your educator and coach! You also get a signed copy of the 2024 edition of the book! Find out more or register here. You can use the discount code EPIC25 to get 25% off the price this week.

Use the discount code EPIC25 to get 25% off this week.

Use the discount code EPIC25 to get 25% off this week.Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

March 5, 2024

Want to live longer? Some lessons in longevity from Iris Apfel | Another age pension payrise coming | Epic letters

Feature article: Want to live longer? Here's how you can, according to the science of longevity

Titbit: Pension payrise coming

Prime Time Podcast: 'How much can you really afford to spend each year in retirement?' with Aaron Minney

Letters: Just one letter today, on super and insurance

From Bec’s Desk: Last week was pretty epic!

Before we start - a little ad for our upcoming course …

The How to Have an Epic Retirement Flagship Course kicks off on Monday 11th March!Hundreds of people have booked for the upcoming How to Have an Epic Retirement Flagship Course. Launching on the 11th March, the course offers 8.5 hours of online lessons, and a practical 85 page workbook, dripped over 6 weeks; weekly live Q&As with some of the retirement industry’s most respected leaders, a community of people approaching retirement to learn with… and me - Bec Wilson, as your educator and coach! You also get a signed copy of the 2024 edition of the book! Find out more or register here. You can use the discount code EPIC25 to get 25% off the price this week.

Use the discount code EPIC25 to get 25% off this week.

Lessons in longevity from Iris Apfel

Source: Iris Apfel Instagram

Source: Iris Apfel InstagramIris Apfel, a woman we all got to watch age in the public eye, died over the weekend at the age of 102 and a half. Most people only knew her for her very bold outfits, big round black glasses, and wild combinations of accessories. What you may not know is that this woman had a passionate unwillingness to retire, having worked, mostly running her own businesses and creative pursuits, and influencing popular designs, for more than 80 years.

She famously told the American TV show, Today shortly after she turned 100, “I think retiring at any age is a fate worse than death. Just because a number comes up doesn’t mean you have to stop.”

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

She was irreverant. She was colourful. She broke every stereotype of ageing and retirement. But most of all she stayed engaged all the way through her life - engaged with her passions, curiosity and creativity through her work.

Iris admitted back in her 100th year in an interview with People that she felt that there were three things that contributed to her longevity. She looked after her diet, having eaten well all her life and avoided junk food. She exercised periodically, for her health too. And, she acknowledged that her attitude was probably an important part.

“Attitude can significantly impact how old you actually feel,” she said in the interview.

“It’s a matter of the way you look at things. I know 30-year-old people who are old and 90-year-old people who are young,” she said. “Everything is your attitude. When you think about things a certain way, you look at them a certain way.”

Her husband Carl Apfel died in 2015 at the age of 101. They had been married 67 years in what she called a ‘beautiful marriage’. Another thing we know from the Harvard Study of Adult Development can contribute to longevity and happiness in later life.

Vale Iris Apfel. Now let’s dive into the lessons on longevity we can all take away.

Don’t stop dreaming, and don’t live a small lifeIris Apfel's life was a testament to the idea that living boldly and passionately contributes to longevity. "I think you have to have a dream. I couldn't get through life without a dream," she said.

I want all of us to latch onto the concept that we don’t have to stop dreaming in midlife or to start living small. In this new age of longer life, we can set and fulfil our dreams, goals and ambitions all the way through life, trying things, and building out a portfolio of activities we enjoy and do regularly and semi-regularly. We just have to get up and be proactive and curious enough to do so.

Seek eudaimonic well-beingIt’s important to seek out eudaimonic wellbeing as a priority in later life. But if we want to seek what’s otherwise known as ‘a purposeful life’ which Iris certainly lived for, we need to go beyond the pursuit of mere happiness and pleasure in the everyday. We need to look for ways to bring greater meaning and more passion into our lives, in all stages. The science of positive psychology says that engaging in activities aligned with your passions can enhance your sense of purpose, contributing to a holistic well-being that can extend your life expectancy.

Cultivate curiosityApfel famously said, "You have to be interested. If you're not interested, you can't be interesting." Iris Apfel had a keen interest in art, fashion, and culture right up to her very last days. She was interested in them, read widely and considered developing her own views on subjects important.

We can all take a leaf out of this book. Curiosity is crucial! Cultivate a curious mind, stay open to learning, and explore a variety of interests throughout your life. And anytime you find your curiosity waning, give yourself a kick, and go looking for fresh interests or renewed energy.

With purpose often comes communityPurpose-driven activities often lead you to participate in communities and social networks. Connecting with others who share similar passions not only deepens the joy of shared experiences but also reinforces the importance of social connections. We know from the research conducted in the Blue Zones that community is an enormous and powerful driver of longevity.

And finally, be alive, not old.My favourite quote from Apfel is "I don't have time to be old. I'm too busy being alive." That says it all. And I leave you with the question - what did you do today that made you feel alive? And what will you do tomorrow?

An age pension payriseThe Age Pension indexation for 20 March 2024 has been announced, with full age pensions set to rise by $19.60 a fortnight for singles and $29.40 a fortnight for couples combined. Including Pension Supplement and Energy Supplement, the maximum rate of pension will be increased to a total of $1,116.30 a fortnight for singles, and $1,682.80 a fortnight for couples. Commonwealth rent assistance will also be indexed. This is the twice-yearly indexation of the pension that occurs in March and September each year.

'How much can you really afford to spend each year in retirement?' with Aaron MinneyIn episode 14 of the Prime Time podcast we're talking about spending in retirement, covering two topics. We talk about ‘safe spending’ or how you calculate the amount you can afford to spend, based on your super balance at retirement if you want your super to last to your life expectancy or a little beyond. We also talk about spending patterns in retirement, and the various different ways that people plan their annual spending budget to work over their lifetime. To talk about these tricky and interesting topics, we have Aaron Minney, the Head of Retirement Income for Challenger, who for 12 years has been researching ways to generate income from investments in retirement.

This is a topic that anyone approaching or in retirement with a fear of running out of money will really enjoy.

And on the Prime Time newsletter which accompanies our podcast we provide you with a really helpful and detailed ‘safe spending’ analysis, thanks to the team at Challenger who have done the calculations.

Listen nowLISTEN HERE - LATEST EDITION (E14) - OMNY

or listen on APPLE PODCASTS

Hi Bec,

I am currently reading and loving your book 📕 🙏🏼

Loving the podcast too - keep up the great work! Wish I had found you 20 years ago!

I am 60. Taking the deep dive on my super funds to try and sort out which one to keep (I have two).

One (with UniSuper has a low balance) has insurance the other (with North which holds the bulk of my super) doesn’t have insurance. My husband has retired (he is 65) and I am currently working 3 days a week.

Following your advice in the book, on page 96, about trying to review the fees can I please ask if insurance premiums are to be included as a fee when trying to work out the fees as a percentage? Hopefully once I can work this out it will be possible to make a more informed choice.

I must admit that I am finding navigating retirement/superannuation all very complicated and overwhelming and my husband has no desire to try and understand (numbers are not his thing but he has many talents in other areas) but trying my best to understand it as much as I can.

I would sincerely appreciate your help with this question 🙏🏼

Many thanks, Kathy

Hi Kathy

This stuff is not easy to navigate on your own. It can get incredibly complex! So let’s start with some simple rules of thumb. Always remember - I'm not a financial adviser so I can only explain ‘how’ people do things in a general sense - not tell you ‘what to do’.

If you want to compare superfund apples with apples, you need to leave the insurance out of the fund comparison. Just compare the funds first. And you do this by reviewing the superannuation fund’s core investment returns and their fees for providing that service, which are best considered in line with the balance. Anyone can use the instructions on page 96 of the book for this.

Then, separately, compare each fund’s insurance offering, if both funds have them, or simply reassess and re-quote for insurance that suits your next stage. If you review, you’ll need to understand whether you hold a basic low cost group insurance policy or an individual policy with customised features and benefits. Again, so you compare apples with apples. At times of change in life it’s often worth taking the time to think about your needs for insurance, and doing a full review with an adviser.

I’ll be honest, I use a financial adviser for the insurance part because insuring yourself against not being able to work in the years you need to is important to get right. Each fund should give you access to some sort of advice to help you review your insurances. That’s usually free to members. They won’t do the comparisons of your funds unless they’re a personal adviser, but you can drill them with questions about the fund they manage. Then, if it’s still unclear you can get some personal advice.

It really can be tricky to navigate the intricate details of insurance on your own.

Thanks for the letter. Hope you enjoy the book! Bec Xx

Got a letter for me? Email me at bec@epicretirement.com.au.

Wowsers! What a week just gone.

You might remember we launched the How to Have an Epic Retirement Flagship Course just over a week ago! Well, it now has HUNDREDS of people booked for our flagship launch on 11th March! I’m still pinching myself. Really though, it’s an incredible course and I’m delighted you can see the value packed into the 6 week program. You can learn more about it here. And if you still want to book for this one, you can use the discount code EPIC25 to get 25% off the price this week.

Last week I flew to Adelaide to speak at two terrific pre- and post retirement events for the superannuation fund Hostplus. It was a buzz. So many really interested members, devouring information to help them navigate retirement. There was hundreds of people in each of the two different sessions and thousands of people online. I even met a few epic retirement community members at the event who brought their books with them. (Gosh how much do I love that! 😊). The vibe was terrific and left me in no doubt that people want more education on how to approach retirement. Thanks for the invite Hostplus. I really hope to do more of this with funds. It’s definitely where I find my own eudaimonic happiness (sense of purpose).

While I was in Adelaide I stopped in on a long time female entrepreneur friend Tania Jolley (a Prime Timer) who is building an ethical business in mascara that could change the way we can use and buy mascara with her beautiful brand Lashes of Change… The mascara formula is divine, designed to be low irritant on our more sensitive eye skin as we get older. The stylish canister is refillable, and you can choose your brush type so the experience of mascara can be right for you. My pick for my long lashes is the brush called Eliza. As a breast cancer survivor, she donates a portion of her profits to breast cancer! Take a look. She’s offered all Epic Retirement subscribers free shipping with the code EPIC. This gal is up for South Australian business woman of the year this year 🥰. I’m just a proud friend and think you should know about this fairly new product. And I love the mascara.

I hope you’ve had time to read up on my big safe spending feature last week. Both the Prime Time podcast and my article in the Sydney Morning Herald and The Age faced into the subject of how we spend in retirement and what we can learn to build our confidence on spending. I’m hoping it helped!

And that’s it. The week ahead is all about women! Speaking, writing and podcasting on womens’ issues knowing that we still have a lot of equality to fight for. And there’s some really practical information we can offer women approaching retirement today with a superannuation gap. Keep an eye out ladies.

Wishing you a wonderful week! Make it Epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

In case you haven’t got a copy yet - you can buy How to Have an Epic Retirement, the book on Book Epic Retirement">Amazon and Booktopia and in many of the major bookstores.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

March 2, 2024

How much do people really spend at each stage of retirement?

This is the short Sunday email, designed to bring you today’s article from The Sydney Morning Herald, The Age, WA Today and Brisbane Times.

This week’s article is timed super-well with a podcast we released with Aaron Minney - Challenger’s head of Retirement Income, talking about how to predict and plan for your spending in retirement. I’ll put more info on it below.

I have thrown in a doozy of a letter too… because you love them so much! (Send me more please!!)

And don’t forget - the Early Bird pricing of 50% off our How to Have an Epic Retirement Flagship Course ends on the 4th of March at midnight. No exceptions. So please take advantage of the good deal. I ordered 12 cases of the new edition of the book for our already-booked attendees on Friday. That’s how epic it’s going to be! I can’t wait. 8 days to go til kickoff! Download a brochure and book your place here.

Have a lovely Sunday. Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

How much do people really spend at each stage of retirement?As people head into retirement, most start to dream about the exciting years ahead and the years that they will age through then try to put it into a financial plan. Rarely, if ever, does anyone reflect on their plan to see if their strategy was correct.

They simply live out their lives and adapt to the circumstances that present themselves. But for those who are planning how their money might work, a discussion on retirement spending and whether it still works the way history tells us is worthwhile.

The financial planning framework most people use was defined back in the 1960s, and it suggests that we should plan to spend smoothly across our lifespan. Bengen’s 4 per cent rule, released in 1994 and still widely used in planning, recommends that people will want to spend 4 per cent per year of their initial wealth at retirement and that this will need to be increased with inflation each year to live a comfortable retirement.

The second and perhaps more interesting theory was released in 2014 in the US by Blanchett. It suggests people actually spend more in the first years of active retirement; then spending tapers off as we become settled in a phase they call passive retirement; then again as we become more frail.

And, when you apply this framework to Australia, the latter two phases usually have lower costs simply because the majority of medical and care costs can be covered by the government.

Seems logical right?

Well, some smart researchers from Challenger have taken a deep dive into the actual spending data of Australians captured by various government surveys over their retirement, and they pose a different approach to planning your spending off the back of it.

It drives you to really think about what you want to spend over your retirement years and how you think your pattern of spending will work, rather than going off historical assumptions.

They’ve combined the data from a number of key sources, to look at real household spending data across 60-80 year olds in retirement. And they think that people are actually spending fairly consistently over their whole retirement, similar to Bengen’s recommendation, and that Blanchett’s theory is playing out simply because of a generational spending gap.

They believe the cause of lowering spending data in older people could be simply that older generations have traditionally spent less than more modern generations, skewing older age data. And they point out that current generations are seeing their expenditure maintain or even increase as they age – a contrast with Blanchett’s conclusion.

It’s in the discretionary items – or the “wants” – where the differences in spending are seen over retirement.

According to the head of research at Challenger, Aaron Minney, it all comes back to needs and wants in retirement – and you need to think about both separately.

Your needs being the everyday expenses that allow you to reach your minimum desired standard of living. And your wants being the goods, services and experiences that are not consumed every day, and can be forgone if you choose, to lower your costs.

Their data on household spending shows that people spend fairly consistently over their lifetime on regular essentials or their needs. Their data points out that there is a cohort of more recent retirees spending more on living expenses and that based on previous cohort spending insights, they are likely to maintain that lifestyle spending throughout their lifetime.

Minney points out that when you look at people of different age groups, you are, in fact, comparing younger retirees with an older cohort that locked in much more modest lifestyle expectations earlier in their retirement, and carried that spending behaviour all the way through.

They did not spend more on their needs earlier in life. But younger retirees are starting retirement with more financial resources and higher expectations of everyday living.