Bec Wilson's Blog, page 2

June 14, 2025

Forget what you knew: your Prime Time plays by new rules

Feature: Forget what you knew: Prime Time plays by new rules

Newspapers: Seven steps to boost your super this tax time

Podcast: 37 years in one business...and then what?

From Bec’s Desk: Warmth in the cold

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

Forget what you knew: your Prime Time plays by new rules

Forget what you knew: your Prime Time plays by new rulesIf you’ve followed my writing or read my books, you’ve heard me talk about the six pillars of an Epic Retirement more times than you can count. It’s the framework I use to help people build the retirement they want - and the order matters. I always start with “time”: helping people picture their lifespan, their healthspan, and what they might do with the years ahead. Then comes financial confidence — how money works, and how to make it work for you. Only after that do we talk about health, happiness, travel, and finally, housing — and how to live somewhere you can age well.

If I had to write How to Have an Epic Retirement all over again (and yes, I will be soon), I wouldn’t change that structure. It works. It’s clear, and it gives people a roadmap.

But when I sat down to write my new book - Prime Time: 27 Lessons for Midlife - I needed a whole new framework. One for people in their late 40s, 50s and 60s who aren’t just waiting for retirement. They’re building something now. And for many of them, an “epic retirement” is not the goal - or at least, not yet. They want a bigger, better life before retirement. They want more fun, more flexibility, and to do more of what matters while they’re still working. This is a different generation, and their money story is different too.

Why Gen X is in a different positionUnlike the Boomers who are now retiring, today’s 50-somethings have had superannuation for longer and at higher rates. They’re likely to reach retirement with more in their super - but only if they learn how it works and make some smart moves in these powerful midlife years. And that’s the real opportunity: if we help people understand their money and choices earlier, they can do so much more with their lives now and later.

That’s where the idea of Prime Time comes in. It’s the chapter before your epic retirement - and it might just be the best one yet.

The six pillars of Prime Time

The six pillars of Prime TimeHere’s a sneak peek at the new framework I built for Prime Time - a guide to making the most of these midlife years.

1. Power

For the first time in a long time, you might actually have some power - over your time, your work, your money, your future. But to use it well, you need to recognise it. That means updating your mental models, letting go of outdated decision-making templates, and learning how longer lives, more super, and more options change the game. It’s about becoming a little more selfish - in the best ways - and giving yourself permission to enjoy this next stage of life.

2. Money

Midlife is your financial pivot point. The decisions you make now can change everything - for your future and for your freedom. This is the time to stop being passive about super, investments, spending and saving. Learn the foundations of financial confidence, and then build the new midlife money lessons on top. You’ve got time, you’ve got options - and it’s time to use both.

3. Work, purpose and happiness

This isn’t about giving up work. It’s about reshaping it to serve the life you actually want. It might mean working less, learning something new, or finding more meaningful work that gives you energy instead of draining it. This is the moment to redefine success on your own terms - not promotions and pay rises, but purpose, autonomy, and joy.

4. Health

This is the non-negotiable one. You need your body and mind to carry you through the decades ahead. Use the science of modern ageing, take a preventive approach, and stay strong, flexible and energised. Longevity isn’t just about years - it’s about quality of life.

5. Family and community

Many Prime Timers are the meat in the sandwich - supporting ageing parents, raising or launching kids, and trying to protect their own relationships and sanity in the middle of it all. This is the time to rebalance. Nurture your adult relationships with your kids. Give your parents a good final chapter. And show up for your partner - or rediscover what brought you together in the first place.

6. Adventure

Don’t let life go beige in the middle. Say yes to the trips, the movement, the unknown. These are your best active years - so ski, hike, climb, backpack, caravan, road trip, motorbike, explore. Travel now in ways you might not want to (or be able to) later.

Prime Time is the stage before retirement - but it’s not a warm-up. It’s a life stage in its own right. If you do it well, it can be just as good as retirement, maybe even better. Because you’ve still got energy, opportunity, and power - and now you’ve got permission too.

I’m so excited to share this new framework and everything that comes with it. And today marks 45 days until the book is released.

Stay tuned.

It’s back! The Epic Retirement Flagship Course kicks off this August — and Earlybird is officially ON 🔥

It’s back! The Epic Retirement Flagship Course kicks off this August — and Earlybird is officially ON 🔥If you’ve been thinking about getting serious (but not boring-serious) about your next chapter, now’s the time. My 6-week How to Have an Epic Retirement Flagship Course has already helped thousands of Aussies set themselves up for a retirement that’s smart, secure, and actually fun - with real strategies for money, time, health, happiness, travel, and how to age well in your own home.

🎟️ Earlybird spots are now open - and they’re 25% off.

They won’t last long, and once they’re gone, they’re gone. So if this is your season, jump in now and lock it in at the best price.

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

Warmth in the cold

Warmth in the coldThis weekend I spoke at the Open Day for Lifestyle Woodlea - in Melbourne. In fact, I’m writing this on the plane home, high on adrenaline after what turned into a big, beautiful event. I was meant to speak for 45 minutes… but in true Bec style, I ended up going for an hour and a quarter. Oops. But I promise - the room was buzzing! Sparkling eyes, great questions, real engagement. I can talk about this stuff for hours and never get tired.

Now that the dopamine is wearing off and I’m headed home in time for Saturday night dinner (phew!), I want to tell you some of my exciting news. Because honestly, I love sharing things with you — this community feels like my team. Being an author can be lonely sometimes, and it means a lot to have you along for the ride.

We’re off to a flying startMy publisher called me on Friday with some amazing news: the response to Prime Time has been incredible. Pre-orders are tracking well above expectations — and there’s still 45 days to go before it hits shelves! Apparently, Australians don’t usually pre-order in big numbers, but you’ve completely turned that idea on its head. There are already a huge number of pre-orders, and there’s still 45 days until the book is officially out. How exciting is that?!

Because the buzz is catching on, you can now pre-order from a few different places:

Amazon ($24) – Order here

Booktopia ($28.50) – I’ll be signing all Booktopia pre-orders! Order here

Big W ($24) – Order here

And here’s a small favour to ask… if you get an early copy, would you consider leaving a quick review on Amazon or Goodreads once you get it and have a flick? A few honest, personal reviews can go a long way in spreading the word — and I’d love it if you became my “buzz club”. (Yep, that’s a real thing. Authors in other categories have them!) We already have the Epic Retirement Club… now we can have buzz too.

Big milestone: the UK edition is done!This week I hit a huge behind-the-scenes milestone: I sent off the finished manuscript for the UK edition of How to Have an Epic Retirement.

Yes - I’ve been rewriting it under the radar for months! The whole book has been adapted completely for UK readers, and I’m thrilled to say that Hachette’s UK team has officially said yes, we want it. Now we’re just waiting on the publication date so we can get it into stores and start spreading the word.

Let me tell you - I’ve learned SO much about the UK State Pension system (and yes, we Aussies really should be thankful for 33 years of compulsory super…).

Audiobook done. Podcast recorded. Buzz building.I’ve also finished the final pickups on the Prime Time audiobook - the last bits where I had to re-record the occasional fluffed line or mispronunciation. It’s officially in the can. Whoohoo!

And I’ve recorded a full preview podcast series about Prime Time too - so keep an ear out for that coming very soon.

A little breather (and a lot of deep gratitude)I’m prepping to take a few weeks off before Prime Time hits shelves at the end of July. I’ll be a little quieter through late June and early July - just stepping back to rest, recharge, and live my own version of Prime Time. (My shoulders are still recovering from all the time hunched over a mic and laptop!)

If I skip a newsletter or two, I hope you’ll understand. They’ll be back on track soon - and when the book comes out on 30 July, I’ll be back at full speed.

Until then, you can follow along on Instagram or Facebook for a few photos of me thoroughly enjoying my Prime Time.

Puppy updateAnd for those who’ve been following I realised I forgot to tell you that my 12-year-old dog has made a FULL recovery! It took 3-4 months to go from completely flaccid paralysis to walking, but he’s following me everywhere again! He can’t do stairs yet but I think even they might be in his future.

So, on that note — have a lovely weekend!

Bec x

If you’ve been thinking about joining the Spring Edition of the course, now’s the time. 👉 All the details are here. There’s a downloadable brochure and you can book your place here too.

Until next week, make it epic!

Bec

Got thoughts this week — send an email to bec@epciretirement.net. I read every one.

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Seven tips to boost your super this tax time

Seven tips to boost your super this tax timeExtract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 15 June 2025.

Most people don’t think about their super until something shifts. A milestone birthday. A serious conversation about retiring. A market wobble that makes them nervous.

But with the end of the financial year fast approaching – and the super guarantee about to rise to 12 per cent – this is the perfect time to take a closer look. Think about the tax you’re paying, the income you’re building, and whether your super is really set up to support your next chapter.

You don’t need to overhaul your whole retirement plan. But a few smart tweaks before June 30 could save you tax, grow your future income, and make sure your super is actually working for your life, not stuck in the settings you picked 20 years ago.

So whether you’re in your 50s, 60s or already retired, here’s what’s worth reviewing now.

(READ ON… my articles are never paywalled for Aussies in The Age, The Sydney Morning Herald. )

In this energising episode, I sit down with the ever-curious and inspiring Mike Chesworth, who spent 37 years at Westpac-finishing his career as Head of Financial Advice-before stepping boldly into a new life chapter, his epic retirement. Since then? Banjo lessons, photojournalism, bike-building for kids with disabilities, gravel cycling adventures, and a big dose of bush travel.

We talk about planning early, resisting the identity trap of corporate life, and why curiosity and nimbleness might just be the two most important skills in retirement. It’s honest, wise, and a whole lot of fun.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

June 7, 2025

What does a good day look like?

Feature: What does a good day look like?

Newspapers: Retiring without $1 million? Don’t worry, so is everyone else

Podcast: How to have the hard conversations with your parents with Jean Kittson

From Bec’s Desk: A wild week

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

What does a good day look like? Have you ever stopped to think about what a good day in retirement will look like for you?

Forget bucket lists for a moment. I’m not talking about the dream trip to Tuscany or walking the Camino. I’m talking about a regular Tuesday. One of the 10,000 ordinary days you’ll live in retirement.

What does a good one look like?

Not extraordinary. Not packed with big plans. Just a solid, satisfying day in this new season of life.

It’s a question we don’t ask often enough. Retirement planning usually circles around the big stuff - super balances, travel goals, downsizing, whether to keep private health insurance. But I think the real power is in the day-to-day. Because that’s what your life is now. Days. One after the other.

So try this:

Close your eyes and picture a really good Tuesday, ten years from now. You’re healthy. You’re not working full-time. The urgent pace of midlife has eased. What does your morning look like? What gets you out of bed? Who do you talk to? What pulls your attention? How does the day move? When do you feel most you?

Because here’s the secret: most people overestimate how much they want freedom - and underestimate how much they still need structure, connection and purpose. We’re wired for momentum, in our Prime Time and even in retirement. We just want to be the ones choosing where we direct it.

For some people, a good day might include a coffee with a mate, a bushwalk, a bit of volunteering, an hour in the garden, and a late afternoon lie-down with a book. For others, it might be walking the dog in the morning then building something, mentoring someone, or helping care for grandkids. You don’t have to be productive - but it helps to feel useful.

Retirement isn’t a holiday. It’s a new kind of Tuesday. And the better we get at designing those, the better this whole phase of life turns out to be.

So, what does your good Tuesday look like?

Your turn: design your good TuesdayGrab a pen, or open a blank note on your phone. Picture yourself ten years from now, on a regular Tuesday. You’re not working full-time. You’re in decent health. Life is yours to shape.

Now answer these:

What time do you wake up?

Is it early and peaceful, or a slow, luxurious sleep-in?

What’s your morning rhythm?

Coffee? Exercise? Reading? Walking the dog? What sets the tone?

Who do you spend time with today?

Friends, family, partner, or no one at all?

What gives your day purpose?

Is there something useful or meaningful you do today - paid, unpaid, creative, caregiving, community-based?

When do you feel most energised?

What moment in the day gives you that sense of "this is what I love"?

What does rest look like?

Is there a moment where you pause and take it all in? What gives you that grounded, content feeling?

What’s one small joy that would make the day feel complete?

A good meal? A perfect playlist? That feeling after a swim? A text from your grandkid?

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!This 6-week program has helped thousands of Aussies get retirement-ready - with smart strategies for money, time, health, happiness and purpose, travel and your home as you age.

🎟️ The 25% off early bird spots are now open and they’re filling up quickly. So get in and lock down your place at this price.

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

A wild week (and a quick update)It’s been a big one.

I kicked off Monday morning as a special guest on Life Matters for their Good Retirement series, chatting about “Living the high life on a low budget.” You can listen in [here]. Then it was onto ABC Melbourne radio that afternoon with Brigitte Duclos, unpacking Denmark’s decision to lift the retirement age and what that might mean for us.

Each night this week I’ve been in the recording studio, reading Prime Time aloud for the audiobook — five hours a night. My voice nearly gave up on me on the very last night … but it’s done. Tick!

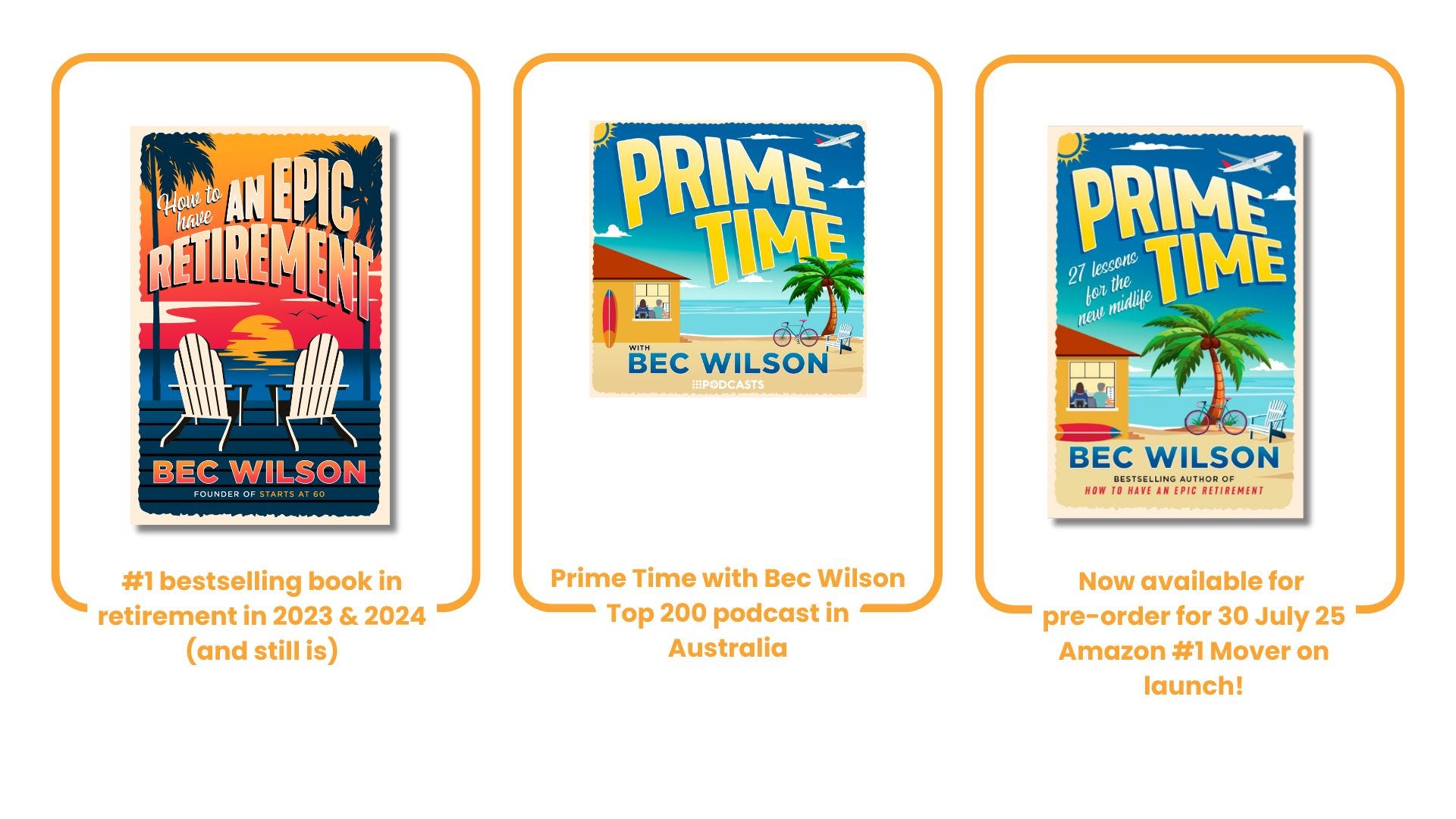

And then on Wednesday: we went to print. Prime Time: 27 Lessons for the New Midlife is now officially on its way. It’ll be in stores on 30 July too.

You can pre-order a copy on [Amazon] or [Booktopia]—and if you go through Booktopia, I’ll be signing all their pre-orders in person before launch.

On Thursday, Amazon released a feature on Prime Time, Epic Retirement (and me!) that sent both books flying up the bestseller lists—and into the Movers and Shakers list too. That was a lovely surprise.

And I interviewed the incredible and entertaining Jean Kittson for the Prime Time podcast, talking about how to have the hard conversations with your ageing parents. She’s been doing it for years… so a wise and experienced guide.

In the background, I’ve also been working on not one but three secret projects I’ll be sharing soon. I’m terrible at keeping secrets… but trust me, you’re going to love what’s coming.

Next week, my big focus is our Epic Retirement Flagship Course. It kicks off on 28 August, and we already have over 100 people booked in. I’d love to get that to 200 before the week’s out — but when we reach 200, the Earlybird offer will end and the price will rise from $374 to $499. So get in and book your place if you want the discount.

If you’ve been thinking about joining the Spring Edition of the course, now’s the time. 👉 All the details are here. There’s a downloadable brochure and you can book your place here too.

Until next week, make it epic!

Bec

Got thoughts this week — send an email to bec@epciretirement.net. I read every one.

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Retiring without $1 million? Don’t worry, so is everyone else

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 7 June 2025.

For years people planning for retirement have been haunted by a single goal: reaching $1 million in super before they retire. Apparently, that’s what we’re all supposed to have neatly tucked away before we even think about retiring. A million bucks. In one account. By 65.

No pressure, right?

But new research from AustralianSuper has just blown a hole in that myth – and it’s about bloody time.

It shows 94 per cent of recent retirees didn’t retire with $1 million in super. Most didn’t even come close. And yet ... they retired and many of them are living in comfort. Without fanfare. Without financial collapse. Without eating two-minute noodles in a cardigan for the next 30 years.

Take Warren Morrison – he retired at 64 with $350,000 in super, and a plan. He’d figured out how much he’d need to spend to have a good life. Now he officiates weddings, runs trivia nights, and judges roller-skating competitions (as you do). His secret? Not being rich. Just being smart about the life he actually wanted.

So maybe the real question isn’t “how much do I need?” or “can I get to a million dollars in super before I retire?” Maybe it’s “what kind of life do I want?”

(READ ON… my articles are never paywalled for Aussies in The Age, The Sydney Morning Herald. )

How to have the hard conversations with your parents with Jean Kittson

How to have the hard conversations with your parents with Jean KittsonIn this episode of Prime Time, I sit down with the incredible Jean Kittson AM — performer, writer, comedian, and author of the bestselling book We Need to Talk About Mum and Dad. Jean opens up about the decade she spent caring for her parents, Elaine and Roy, and the many lessons she learned along the way — about family, love, aged care, and what it really takes to help our parents through their final chapter.

We talk about the emotional weight of being part of the sandwich generation, the complexity of the aged care system, and the importance of early conversations — the hard ones that help everyone make better choices. Jean is generous, wise and deeply real about what it means to be a carer, and this conversation is one I think every midlifer should hear — whether you’re just starting to notice your parents slowing down, or you’re right in the thick of it.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

May 31, 2025

Retirement isn't a product or a service, it's a project

Feature: Retirement isn't a product or a service, it's a project

Newspapers: Retirement at 70? It’s coming, whether we like it or not

Podcast: Finding your new rhythm

From Bec’s Desk: In a little dark room

Retirement isn’t a product or a service. It’s a project.For a long time, retirement was treated like a product - something you bought into, something delivered neatly at a set age (often by your financial adviser or a super fund). You handed over your paperwork, drew out a lump sum, set up your account based pension, and quietly exited the stage.

But that idea doesn’t fit anymore. Not for this generation.

Retirement today isn’t something that happens to you, or you can be ‘told how to do it’. It’s something you build. And that takes time, thought, and learning - because there’s no one-size-fits-all pathway anymore.

We don’t talk about this enough: entering retirement is stepping through a transition into a whole new stage of life, not an end point. And just like any big life change, it deserves space, curiosity, and creativity.

Some people approach it like a second or third stage of their career. Others use it to explore parts of themselves they’ve put on hold for years or have never really taken time for. Many are still working out what they want it to look like - and that’s okay.

Because the truth is, the best retirements aren’t scripted. They’re shaped.

That’s why I think we need a new way of thinking about this chapter. Not just as the winding-down years - but as a phase with depth, with decisions, and with potential.

Retirement isn’t a product to buy or a process you have have an adviser do for you. It’s a project to shape. And the best years of your life might just be the ones you haven’t lived yet.

Think of retirement not as a finish line, but as a design project.

Then ask yourself three questions:

What do I want my days to look like?

What do I want to keep doing - and what am I ready to let go of?

What will give me a sense of meaning, challenge, or bring me personal joy in this next chapter?

You don’t need all the answers. You just need to start asking the important questions.

Because once you shift from “retiring from” to “retiring into,” the whole thing opens up. That’s where the magic starts! Make it epic!

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!This 6-week program has helped thousands of Aussies get retirement-ready - with smart strategies for money, time, health, happiness and purpose, travel and your home as you age.

🎟️ The 25% off early bird spots are now open and they’re filling up quickly. So get in and lock down your place at this price.

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

Well, I’ve spent most of this week in a little dark room (a professional studio), reading Prime Time aloud into a microphone for the audiobook. It’s slow going (and a bit of a vocal marathon), but I secretly love the shift in pace. I’ll be doing that every night this week—four to five hours of reading out loud a day is more than enough, thank you very much.

The book itself—the one that never seemed to stop being edited—is finally locked and off to print. I saw the final cover this week, complete with the back-cover blurb. Very exciting. We’re counting down now to launch day: 30 July. Just two months to go.

You can pre-order your copy on Amazon here or Booktopia here, and I’d be so grateful if you did—it genuinely helps the retailers get behind the book. I’ll be dropping into Booktopia in Sydney the week before release to sign all their pre-orders, so if you want a signed one, that’s the way to go.

Meanwhile, our Facebook Group—The Epic Retirement Club—is absolutely booming. It’s on track to hit 400,000 worldwide members this weekend. We’ve got an incredible team of 19 volunteer moderators around the world keeping the conversation thoughtful, kind, and high quality.

There’s no financial advice flying around in there—just real people sharing real stories about how they’re navigating their Prime Time and Epic Retirement years. It’s the most honest, inspiring window into what retirement really looks like. I’m constantly blown away by the generosity and wisdom in the group. If you haven’t joined yet, come take a look.

And if you’re thinking about joining us for the next course — which I’m really excited for — The Spring Edition of the How to Have an Epic Retirement Flagship Course- don’t wait too long. The 25% Earlybird Deal is booking up fast, and the course kicks off on 28 August. 👉 More info here

Until next week, from the small dark room

Bec

Got thoughts this week — send an email to bec@epciretirement.net. I read every one.

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Retirement at 70? It’s coming, whether we like it or not

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 1 June 2025.

This week, Denmark did something bold, and frankly, confronting. It locked in a plan to lift its state pension age to 70 by 2040. Not a proposal. Not a think tank idea. Actual law.

Seventy. Let that sink in.

It’s the kind of move that makes people everywhere shift in their seats. Because if Denmark can do it, so can we. And whether we like it or not, the ripple effect is coming.

In Denmark, “retirement age” means the age you can access the state pension, their version of our age pension. It’s currently 67. It’ll rise to 68 by 2030, and then 70 by 2040, when today’s 55-year-olds hit that milestone. It’s been legislated in line with life expectancy – so as people live longer, the pension age just rises. Automatically – no political debate required, and no elections lost to the shift.

The message is clear: you’ll still get support, but not until much later in life. Want to retire earlier? That’s on you. You’ll need your own savings to bridge the gap.

That’s precisely what many Danes are preparing for – because while the state pension won’t kick in until 70, many private and workplace pensions can still be accessed from around age 60 or 62.

Expect more pressure to plan your own income, not less. Denmark had the guts to say it out loud. I’m not sure Australia’s ready to.

People who want to stop working earlier can do so, but they’ll need to rely on their own savings for a longer period before the state support begins. Bridging that gap is now a personal responsibility.

The Danish system looks generous, but it’s designed to be fair, not cushy - though many Australian pensioners might think otherwise. If you’ve lived in Denmark for 40 years between age 15 and retirement, you’re entitled to the full public pension. Less than that, and you receive a proportional amount. And it’s no small sum.

The full Danish folkepension pays around AUD $57,000 a year, but after tax, most retirees take home between roughly AUD $40,000 and $42,000. That includes a base pension, which everyone gets, and a supplement, which is means-tested. About half the payment is universal; the rest tapers off if you have higher income from savings or investments.

(READ ON… my articles are never paywalled for Aussies in The Age, The Sydney Morning Herald. )

In this soul-stirring episode of Prime Time, I am joined by retirement coach John Glass from 64 Plus for a powerful, heartfelt conversation about the emotional shifts and lifestyle reinvention that come with retirement. We explore how to build a meaningful, purpose-driven life after work—one that’s full of connection, curiosity, and clarity.

Together, we unpack the emotional roadblocks many people face when the structure of full-time work disappears—from loss of identity to fear of irrelevance—and how to replace them with daily rhythms that support wellbeing, purpose, and joy. From cartooning and language learning to rose gardening and gym rituals, Bec and John reveal what it really means to craft a “portfolio life” in retirement.

Plus, I chat with Kat McPhee from Aware Super about what to do when life throws a financial curveball your way. Whether you're forced to retire early, navigating Centrelink, or just trying to feel financially confident, this segment is full of reassuring, practical advice.

This episode is a must-listen for anyone wondering: What’s next? And How do I make it count?

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

May 24, 2025

The spending myth that might not hold up in your retirement

Feature: The spending myth that might not hold up in your retirement

Newspapers: The advice gap: Why are we abandoning middle-class retirees?

Podcast: Getting retirement advice shouldn’t be this hard

From Bec’s Desk: The Chant West Pension Fund of the Year is…

The spending myth that might not hold up in your retirement

The spending myth that might not hold up in your retirement(Spoiler: spending doesn’t always drop as you age)

There’s this persistent little myth that floats around whenever people start planning for retirement:

“You’ll spend less as you get older.”

Sounds logical, doesn’t it? No more commuting to the office. No more work wardrobe. No more takeaway coffees at morning tea, afternoon tea, and Friday lunch. If the mortgage is gone and the kids have moved out (or at least slowed down their wallet-draining efforts), surely your costs will go down too?

Except… that’s not how it works for most people I meet. And interestingly, retirement researchers don’t all agree on what’s coming for future generations either.

Retirement spending: past trends vs what’s aheadWhen we look back at earlier generations, we see a clear trend:

Each new generation of retirees starts retirement spending more than the last—and they finish retirement spending more too.

But here’s where it gets tricky. The curve of spending across life appears as a gentle downward slope. Why? Because the data is often comparing different cohorts at different stages: one generation in its 80s and another just entering retirement. So yes, the chart drops. But that doesn’t mean your own personal spending will.

In fact, for most people, the shape of spending over retirement is relatively flat. What changes is what you’re spending on.

The real rhythm of retirement spendingIn the early years, it’s all go-go-go.

Travel, activities, entertainment, leisure—all those things you finally have time for.

Then, in the middle years, spending on your home, your health, and your family might creep up.

And in later life, aged care, in-home services, and health support can start taking bigger bites out of the budget.

Meanwhile, essentials like housing, insurance, and utilities often stay steady—not really helping that “spending goes down” narrative.

The truth? You might spend moreEspecially in the first 5 to 10 years after leaving full-time work. Why?

Because you’ve finally got time - and a long list of things you’ve been waiting to do.

This is your Epic Retirement. You’re healthy, energetic, and ready to say yes to the good stuff:

Big holidays

Club memberships

Home upgrades

Hobbies that mysteriously require lots of gear

Trips to see the grandkids (who are somehow always interstate or overseas)

I’ve looked at hundreds of retirement budgets. And honestly? Most people spend more in the early years - not less.

And yes, spending can drop later… kind ofSpending might ease off in your 80s, depending on your health, lifestyle, and support needs. But even then—it’s not guaranteed. If you need extra help at home, care services, or residential aged care, those costs can ramp right back up.

That classic image of spending gently tapering off as you age? Too simplistic. Real life’s not that neat.

So what does this mean for your plan?It means you need to:

Budget properly for your epic retirement years

Build in flexibility, because life doesn’t follow a straight line

Give yourself permission to enjoy the early years, guilt-free

Retirement isn’t a financial dead zone. It’s not about shrinking into a smaller life.

It’s about choosing how you want to spend your time—and yes, your money.

Don’t short-change your Epic Retirement. You’ve earned it.

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!This 6-week program has helped thousands of Aussies get retirement-ready - with smart strategies for money, time, health, happiness and purpose, travel and your home as you age.

🎟️ The 25% off early bird spots are now open and they’re filling up quickly. So get in and lock down your place at this price.

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

The weeks are flying by at the moment.

This week we wrapped up our How to Have an Epic Retirement Flagship Course for Winter. We finished on a high with the wonderful Fiona Dalton, travel guru and fountain of practical inspiration, joining us for a live Q&A on the secrets of the travel sector. It ran 15 minutes over time because people were having such a great time. Always a good sign.

A few radio shows about the $3M tax too — apparently a lot of people have feelings on it that they didn’t express in the election.

I then popped down to Sydney for the Chant West Super Fund of the Year Awards—and what a brilliant night it was. A proper celebration of all the hard work happening across the super industry.

A huge congratulations to the team at Aware Super, who took out Best Pension (Retirement Phase) Fund, and to Unisuper, who won Best Super (Accumulation Phase) Fund. These awards are hotly contested, and both funds should be super proud (pun absolutely intended).

The rest of the week? Books, courses, articles... it’s a full plate and I wouldn’t have it any other way.

I sat down with Mary Delahunty to talk about the real issue holding up financial advice reform - and why it’s slowing progress on making advice more accessible and affordable. See the podcast below.

If you’ve been following along, you’ll know my 12-year-old pup has had a tough time with paralysis for about 3-4 months - but this week, he stood up on his own. We’re now counting down to the next big milestone: his first steps.

And for me? The week ahead is all about recording the audiobook for Prime Time. Twelve long days in the studio start now. Wish me luck (and a strong voice)! The men in my household all have man-flu right now so I’m headed for quarantine.

Our 25% off Earlybird Deal is booking up so incredibly well for the Spring Edition of the How to Have an Epic Retirement Flagship Course, which kicks off on 28 August 👉🏻 More info here 👉🏻

Got thoughts this week — send an email to bec@epciretirement.net. I read every one.

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

The advice gap: Why are we abandoning middle-class retirees?

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 25th May 2025.

There’s a big problem with financial advice in Australia, and it’s been dragging on for years: most people heading toward retirement can’t get the help they need to understand their money and structure it for their retirement.

Super funds want to offer advice. Financial advisers want to protect their role as the go-to experts and don’t want funds in their category. And the government? Well, they’ve been reviewing it all for years and doing very little.

While the government stalls and industry bodies argue over who should do what, the people who actually need advice are still missing out. The system, as it stands, is failing those who need help the most. And it’s time we stomped our feet.

If you’re an everyday Australian with up to $500,000 in super and a family home, chances are you’re not getting personal financial advice at all. You probably can’t justify spending $3000 to $5000 or more, on a full financial plan.

But you’re precisely the kind of person who needs one-off personal guidance on how to combine your super with the age pension, whether downsizing might be worth considering, how to make your money last, and when you can afford to pull the pin on work.

These are the real-life questions people are asking. But answers are difficult to come by because the current system doesn’t serve people like you.

The truth is, advice in Australia isn’t designed for the majority any more. There’s less than 16,000 financial advisers left, and insiders say perhaps only half are actively seeing clients.

The rest are behind the scenes writing plans and handling compliance. Most advisers focus on wealthier households because that’s what makes the business model viable.

Super funds are well-positionedYour super fund probably knows you’re getting close to retirement. They’ve got tools, calculators, and people on staff who want to help (and they’re ready to charge a fee for that help too, albeit a smaller one than most comprehensive advisers).

But here’s the catch: they’re legally restricted from giving you personal financial advice unless they jump through costly and complex hoops, like acquiring or establishing a licensed advice business and running it separately on a fee-for-service basis, just like a traditional financial planning firm.

(READ ON… in The Age, The Sydney Morning Herald. )

We’ve built a colossal $4.2 trillion super system, but we’ve failed at the one thing people need most: guidance and advice for everyday people.

Most Australians hit their 50s or 60s with savings in super, fear in their gut, and no idea what to do next. And when they go looking for advice, they hit a brick wall. Financial advisers are expensive, often full-service only, and in short supply. Super funds? Most are legally restricted from giving personalised help. The result? Confused, stressed-out pre-retirees stuck in limbo.

This is Australia’s retirement blind spot—and we’re long overdue to fix it. Getting advice on your retirement shouldn’t be this hard!

In this episode, I sit down with Mary Delahunty, CEO of the Association of Superannuation Funds of Australia (ASFA), to unpack the long-awaited reforms that aim to close the advice gap. Reforms that seem to be moving very slowly!.

We talk about the politics, the pain points, and the promise of a new class of advice that could finally meet people where they are—with the right help, at the right price, when they actually need it. If you’ve ever asked, “What should I do with my super?” or “How do I navigate retirement” and been met with silence, rules, or fees—you’ll want to hear this.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

May 17, 2025

Time for your own retirement reality check

Feature: Time for your own retirement reality check

Newspapers: Who cares about a tax on $3 million super balances? Maybe you should

Podcast: How scammers scam even the most tech savvy

From Bec’s Desk: 😁

Time for your own retirement reality check

Time for your own retirement reality checkI’ve been running our flagship course for a year and a half now (I know—hard to believe, isn’t it?). Over that time, we’ve gotten better at surveying and understanding the people who join us when they arrive: where they’re at, what they’re wrestling with, and what they’re hoping to figure out. Then, we survey them at the end, and learn what’s changed.

Most come in wanting to understand how retirement really works, and to build confidence in their own finances and choices for the years ahead. They also want to understand themselves better — and how they might find purpose, fulfilment and happiness. More than half of them arrive thinking retirement is still three to five years away. Some feel behind. Others feel stuck. And some feel financially able, but afraid. But almost everyone is making time, often for the first time, to sit down and take a proper look at the whole picture — what they’ve got, what they want, and how the retirement income system actually fits together and supports them.

By the end of the course, something incredible happens.

They realise they might be able to retire within one to three years. And many make the choice to reconsider their plans.

It’s not because they won the lottery. Or inherited a windfall.

It’s because clarity changes everything.

When you actually sit down and look, really look, at what you have, what you need, and what kind of life you want to live next… you start to realise retirement might not be some distant dream long off in the future. It could be your next chapter. A version of it, at least. And it could be exciting, fulfilling and … possible to choose your path into it.

And when that clicks, something else unlocks too: confidence.

Not blind optimism - real confidence.

The kind that comes from understanding your numbers, seeing your options, and knowing what levers you can pull to shape your future.

I want everyone to have a taste of their retirement reality today — so this week I’m giving you a challenge.

I want to give you a simple formula to help you take an hour and give yourself a little reality check.

Ask yourself:

– What does my next chapter actually look like?

– How do I want to spend my time, energy and freedom in this phase of life?

– What income do I actually need to support that?

– How close am I to being able to fund that income - through super, the age pension, savings, or part-time work?

– And if I brought forward my retirement timeline by a few years, or started to ease into retirement via my Prime Time… what would that look like?

Even if the answer is “not yet,” you’ll walk away with something powerful: a clearer sense of what needs to happen next.

And that’s how retirement shifts - from a vague vision to possible and achievable. Make yours epic!

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!This 6-week program has helped thousands of Aussies get retirement-ready—with smart strategies for money, time, health, happiness and purpose, travel and your home as you age.

🎟️ The 25% off early bird spots are now open and they’re filling up quickly. So get in and lock down your place at this price.

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

A short but sweet update this week (or maybe not?). I’ve got a book to read—and I may have accidentally left this email to Sunday morning (eek!). I’ve been deep in the final stages of writing and editing all weekend and almost forgot! (Almost. I’d never actually forget you ☺️)

I’m currently doing the final read of Prime Time before it heads to print. It’s exciting—yes—but it’s also a huge process, and I’m more than ready to wrap it up and move on to the next phase. There’s a real sense of relief when a book reaches the finish line.

In the papers this weekend, I did a deep dive on the proposed $3 million super tax. It’s a long, meaty article—my word count was supposed to be 800, but I submitted 1800, and my editor barely cut a thing for the digital version (he had to trim for print, of course). I tried to be balanced across politics but focused on making the implications clear for everyday people. Honestly, I’m surprised more Australians aren’t engaging with this. But then again, that’s superannuation—most people don’t pay it much attention until retirement is right in front of them. (Not you though. You’re one of the proactive ones.)

In the Course we held our "‘Finding your Purpose week” with Sue West from Flourishing After Fifty as a guest, then I facilitated a session where everyone on the course jumped in and chatted about their own journey to finding their purpose. This could be one of my favourite live sessions of the program. It’s so validating, so personal!

This week my daughter is coming home from Canada (hopefully for uni this time). I’m a bit excited. Then I’m heading to Sydney for the Chant West industry awards, which celebrate excellence across financial services. Always fun to put on a frock and cheer on the best in the business.

And on the home front, something very special: my 12-year-old pup is about to walk again—after nearly 16 weeks of rehab from flaccid paralysis. He and I are beside ourselves with excitement. We’ve worked so hard.

Thank you, as always, for your letters this week. Sometimes I wish this email was longer so I could share more of them with you—they’re that good. Your stories, questions, and insights genuinely shape where I take things next, so please keep them coming.

Our 25% off Earlybird Deal is bringing in a wave of bookings for the Spring Edition of the How to Have an Epic Retirement Flagship Course, which kicks off on 28 August 👉🏻 More info here 👉🏻

Got thoughts this week — send an email to bec@epciretirement.net. I read every one.

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Who cares about a tax on $3 million super balances? Maybe you should

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 18th May 2025.

Who cares about a tax on people with $3 million in super? They are Australia’s rich people, after all. The top half a per cent. They have accountants, investment properties and franking credits coming out their ears. Most of us will never get near that kind of money in our lifetime.

So why should we care?

Well, let’s dig a little deeper. Because we, the everyday people who go to work and pay our tax the right way, actually have a lot more riding on this change than it first appears. It is time we all stood up and gave this policy a bit more thought before it gets rushed through parliament.

The government now has a free pass to legislate this tax in the first sitting of the new Senate season. And, so far, Treasurer Jim Chalmers is showing no sign of backing down.

He’s also provided very limited insight into how it will work practically, so we might end up with a tax we don’t properly understand, and one that no one wants to speak out about except the wealthy, who we all shrug and roll our eyes at.

So before we all move on, let’s take a closer look at what this tax might actually do, and why it might – one day – affect far more Australians than we think.

This isn’t a tweak – it’s a turning pointSuperannuation has been one of the great Australian policy successes. For more than three decades it has helped millions of ordinary workers build wealth over time, with tax incentives, long-term growth and compounding returns on their side.

It has turned everyday Australians into investors on the global stage. It has reduced pressure on the pension, as well as alleviated our fear of ageing impoverished. It has given people choice, dignity and financial independence in retirement.

But this tax marks a clear change in approach. It hits people for building wealth inside the system that was designed to help them do exactly that. It tells every smart investor that if your super grows too much, you will be penalised. Not when you realise the gains but while it is still just sitting there, growing on paper.

This is a sign that the government is stepping back from protecting super as our most effective long-term wealth-building tool.

It makes super harder to manage, more expensive to comply with and less attractive to contribute to, beyond the compulsory 12 per cent. And that weakens the system for everyone.

Maybe that’s actually what the government is trying to do, to slow down the use of super as a more extreme wealth creation tool and start to shape the system into an ordinary person’s retirement fund.

(READ ON… in The Age, The Sydney Morning Herald. )

My article in the weekend’s newspapers about a hoax article pretending that superannuation rules would change on 1 June was incredibly well-read and discussed. And it made me want to go deeper into the issue of hacks and scams.

So this week on Prime Time, I sat down with one of the world’s most experienced scam investigators, Ken Gamble. Ken has been tracking down fraudsters and exposing global scam syndicates since the 1980s - and his insights are jaw-dropping.

We went deep on how scammers operate, why midlife and older Australians are prime targets, and what you can do to protect yourself. From fake bond offers to crypto cons, and even cloned Facebook groups (yep, including fake ones pretending to be me), this episode is a must-listen if you, or anyone you care about, uses the internet (which let’s face it — is all of us!)

Ken doesn’t just talk theory - he’s lived it. He’s tracked criminals across continents, infiltrated call centres, and helped put scammers behind bars. This one’s packed with red flags, insider tips, and some genuinely shocking stories.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

May 10, 2025

Retirement doesn't give you purpose - you have to bring it with you

Feature: Retirement doesn’t deliver purpose. You have to bring it with you.

Newspapers: Sweeping new super changes in June? Don’t fall for it

Podcast: Stop working, keep earning

From Bec’s Desk: Happy Mothers Day!

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!

The

How to Have an Epic Retirement Flagship Course

is back for August kickoff! And the Earlybird 25% off won’t last!This 6-week program has helped thousands of Aussies get retirement-ready—with smart strategies for money, time, health, happiness and purpose, travel and your home as you age.

🎟️ The 25% off early bird spots are now open—get in before they fill up!

👉 Check it out here and download the new brochure for Spring 2025

Let’s make your retirement epic.

Retirement doesn’t deliver purpose. You have to bring it with you.There’s a quiet panic that hits a lot of people in their late 50s or 60s. It goes a little like this: ‘I’m nearly done with work… but what am I actually retiring to? Who am I going to be when work ends? What’s my purpose?’

We spend decades working, raising families, juggling… everything. And when the noise settles, what’s left that’s still there when the kids leave and we leave work? Plenty if you get it right. Or a gaping hole if you don’t.

This is where looking for and identifying what fires your sense of purpose becomes important—and it needs to be built before you walk out the door for the last time.

One of the world’s most thoughtful voices on this is American expert Richard Leider, who has spent decades studying the concept of “life’s purpose.” He boils it down to this:

“Growing and giving.”

That’s it. That’s what purpose is. And it doesn’t stop at 60 or 65.

Think about it. If you stop growing and you stop giving you find yourself living a pretty small life.

And it’s worth chasing, because according to research from both Stanford’s Center on Longevity and the Modern Elder Academy, people with a strong sense of purpose:

Stay healthier and live longer

Transition more smoothly into retirement

Are less likely to experience depression or cognitive decline

And the big message I want you to hear is, the earlier you start building that purpose outside work, the better. Remember, growing and giving!

So if you're in your 50s or early 60s, ask yourself:

What makes you feel most alive?

What could you keep doing or learning even if no one paid you?

Where are you still growing?

Where could you start (or continue) giving?

It doesn’t need to be grand. Teaching your grandkids to cook counts. Volunteering at the community garden counts. Mentoring, painting, writing, hiking, joining a men’s shed—it all counts. Think about things that give you a sense of belonging, a feeling of wanting to get up and go, and the rush when time whooshes by.

This sense of purpose is yours to shape—and you’ve got more freedom than ever to do it your way. Make it epic!

Mothers Day! Warm hugs to all the mothers out there today! I’m going to soak in my kids making me breakfast, my husband doing the shopping and people brainstorming fun adventures for my day. And then, in just 7 days time, my biggest baby (now 21) returns from more than a year in Canada — could be the best Mothers’ Day gift of all.

And, if you’ve been following along, my 12-year old pup is nearly back to standing after his full paralysis this year. It’s been a lot of healing, rehab and encouragement — but he’s a joy and thankfully I work from home.

This week in retirement education was another doozy in the rear-view.

Our How to Have an Epic Retirement Flagship Course for Winter kicked into Week 5, and we all enjoyed our live Q&A event with Jen Harding, the General Manager of Education, Engagement and Advice at HESTA who explained to everyone how advice works inside funds, and answered a record number of questions.

This week I spoke at a large online live event for Care Super Members on the 6 pillars of an Epic Retirement — what a thrill that so many came and enjoyed it! Hundreds and hundreds of people came along for 1.5 hours of education and Q&A — and it was in the evening so great for pre-retirees!

And we released another really enjoyable podcast to record where we talked about how money works when you retire. And this one was mainly me explaining layering — and how income works, with some great help from Katrina McPhee at Aware Super who explained the superannuation parts too.

Our 25% off Earlybird Deal is live for our Spring Edition of the How to Have an Epic Retirement Flagship Course. The course kicks off on the 28th August. 👉🏻 More information here 👉🏻 And we’re already blown away with bookings! 😁

Got thoughts this week — hit reply to email me or leave a comment.

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Sweeping new super changes in June? Don’t fall for it

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 11th May 2025.

I was on a superannuation fund livestream this week doing a Q&A when a woman asked me what I thought about the major new super rules coming in on June 1.

I did a double-take. She continued – what did I think of the new phased withdrawal limits that would be imposed on people in the pension phase? And the limits to lump sums that we could withdraw?

“There’s no new super rules coming in on June 1, unless Albo brings parliament back early and passes the $3 million rule,” I said, pretty confident I hadn’t missed something. The fund’s financial adviser also agreed with me. And I didn’t give it a second thought – until the next day.

That was when I received an email from a lady asking me what I thought about the new super withdrawal rules coming into effect on June 1. She’d forwarded on an article in the email – which I categorically refused to open.

I sent it back to her with the note: “You’ve been scammed. You should never click on a link in an email that you don’t know the source of.”

The scam article doing the rounds currently.

The scam article doing the rounds currently.She persevered, sending me screenshots of an article that is clearly doing the rounds online among imminent retirees, driving fear into their souls. Eventually, I opened it on my iPad on incognito mode.

It was slick. It was confidently written. And it was utterly made up.

The article includes a table claiming to list so-called “changes” coming to Australian super rules on June 1, 2025. Among the fake claims is a shift in the preservation age, increasing it from 60 to 70 by 2030.

It also claims that lump-sum withdrawals will be capped at 50 per cent of a person’s balance, rather than being fully accessible as they are now. Another claim is that phased withdrawals in pension phase will become mandatory – something that is already the case under current rules, making the statement clearly incorrect.

The article goes on to mention a so-called “deferred access bonus” of 3 per cent per year up to age 75, which actually applies to age pension systems in the US and UK, not Australia. Finally, it states that early access to super will be subject to tighter eligibility criteria and capped withdrawal amounts.

Right now, the only thing changing on June 1 is the temperature.

Not a single one of these things has been proposed by the Australian government or Treasury. None are in legislation. None are real.

(READ ON… in The Age, The Sydney Morning Herald. )

Welcome back to Prime Time! In this episode, Emelia and I are diving into one of the most common questions we get: Can I stop working… but still keep the income flowing? The answer? Absolutely—but it's probably not in the way you think.

We’re unpacking the magic of layering your income in retirement—how money keeps flowing in after the paychecks stop, and why understanding your income layers is one of the most powerful financial shifts you can make as you transition into retirement.

We also bust some myths about passive income, talk about how super actually works once you hit retirement, and explain why your home is already one of your biggest investments. Whether you're planning to downshift, semi-retire, or hang up your boots entirely, this episode gives you a clear, calm way to start thinking about your future cash flow.

And we’re joined by Kat McPhee from our sponsor Aware Super to talk about how a retirement income account works and why it might be the easiest “passive income” play you didn’t know you had access to.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

May 3, 2025

The most important number in your retirement plan isn't your super balance

Feature: The most important number in your retirement plan isn't your super balance

Newspapers: Retirement is powerful and freeing. It’s time we treated it that way

Podcast: Fighting the grey stigma

From Bec’s Desk: Highlights!

The most important number in your retirement plan isn’t your super balance(It’s how much life actually costs.)If you’ve been quietly stressing about your super balance, you’re not alone. It’s become the headline number — the one everyone watches, measures, and compares. But here’s the thing: it’s not the number that matters most.

The real number — the one that can make or break your retirement — is your annual spending.

Because retirement isn’t just about how much you have saved. It’s about how much you need.

Let’s say you’ve got $600,000 in super.If your lifestyle only costs $45,000 a year, then you’ve got options. You might be able to retire earlier than expected, or work part-time and stretch it out. If you’re eligible for the Age Pension down the track, even better — that reduces the pressure on your nest egg.

But if your lifestyle quietly costs $90,000 a year — and you’ve never really tracked it? That same super balance suddenly looks fragile. You could burn through it in 10 years and still have decades of retirement to fund.

Most people don’t know what they’re spendingI’m not talking about budgets here. I’m talking about awareness.

In your working years, you often live on autopilot. Income comes in, bills go out. But once you stop earning a full wage, the equation flips. You need to know: What does my lifestyle actually cost me every year?

This is your “burn rate.” And once you know it, you can build your plan around it.

Retirement is just cash flowWhen you strip everything back, retirement isn’t a date or a dollar figure. It’s a cash flow puzzle.

If your income from super, investments, the Age Pension, and part-time work adds up to more than your spending? You’re good. If it doesn’t? You’ve got time to adjust.

That’s why this number — your annual spending — is so powerful. It gives you control. It helps you answer the real question: Can I afford the life I want?

So before you panic about your super balance, take 20 minutes to figure out your real number. Not the one you think it should be — the one it is.

You can use the budgeting chapter in How to Have an Epic Retirement to guide you, and the template available to everyone who’s bought the book.

Because once you know what life costs, you can shape your retirement around reality — not fear.

Another long weekend — for Queenslanders anyway! This time I am not editing the manuscript for Prime Time — it’s done!

But I’ll be coming back early for our Week 4 Live Q&A for the How to Have an Epic Retirement Flagship Course with Jen Harding head of Education, Engagement and Advice from HESTA. It’s a great opportunity for people to find out how superannuation and investing really works from an insider.

This week was a whirlwind. The highlight was definitely presenting at Hostplus’s Retirement events in Melbourne. Thousands of people tuned in and showed up for Hostplus’s biggest round of retirement events ever! A real thrill to be MC and the keynote speaker for their pre-retirement event too!

In the week ahead there’s more excitement! I’m presenting online for Care Super Members on the 6 pillars of an Epic Retirement this Thursday evening (8th May), in “a high-energy, eye-opening live webinar on the six key pillars to building a rewarding and meaningful life after work.” Should be terrific fun. More here.

We’ve had two great podcasts in the week just gone. The first one was with Catherine Greer, author and champion for midlife women about her journey to ditch the dye and let her grey shine through (and her new book!).

And with the election looming, on Friday we grabbed a last-minute conversation with our go-to guru for making sense of things that span economics and politics, Shane Wright, Senior Economics Correspondent at The Age and The Sydney Morning Herald.

Our 25% off Earlybird Deal is live for our Spring Edition of the How to Have an Epic Retirement Flagship Course. The course kicks off on the 28th August. 👉🏻 More information here 👉🏻

Got thoughts this week — hit reply to email me or leave a comment.

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Retirement is powerful and freeing. It’s time we treated it that way

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 4th May 2025.

In your working years, there’s structure. A job to show up to. Bills to pay. A mortgage to chip away at. School runs, packed calendars, the occasional holiday, a few career steps to climb.

Life is shaped by outside forces – deadlines, obligations, the steady rhythm of earning and spending. You can stay busy in that rhythm for decades. Never look too far ahead. Never open your super statement. Never stop to ask what happens next.

But then one day, the structure starts to loosen. The kids leave home. The career ladder stops looking so appealing – or maybe you’ve climbed as far as you care to. And for the first time, the idea of retirement starts to feel real. Not theoretical. Not distant. Just … there. On the horizon.

And suddenly, there’s no clear next step.

There’s no manager giving you a new title. No family schedule running your days. Just questions. Can I afford to stop working? Do I even want to stop? How do I turn my super into income? What will my life actually look like when it’s not ruled by routine?

This is the moment that catches many people off guard. Retirement has been sold to us as a finish line, a reward. But in reality, it’s a blank canvas. There’s no script. No formula. Even financial planners, when asked what to do next, often throw the question back: Well, what are your goals? (READ ON… in The Age, The Sydney Morning Herald. )

In this episode of Prime Time, I’m joined by the wonderful Catherine Greer — an Australian-Canadian author, copywriter, baker, and mother — to talk about something so many of us are thinking about in midlife: going grey.

Catherine shares her honest journey of choosing to ditch the dye before it became trendy, how it felt to let her natural silver hair come through, and what it taught her about ageing, authenticity, and freedom. We talk about why going grey can feel like an act of rebellion, how the pressure to stay young is still stitched into our culture, and why midlife is actually the vibrant middle — not the end — of our lives.

We also dive into Catherine’s new novel, The Bittersweet Bakery Cafe, a beautiful celebration of resilience, creativity, and starting over in the middle of life. If you’re feeling the pull toward authenticity, creativity, or just a little tired of the endless salon visits, you’ll love this conversation.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

April 26, 2025

Three big questions I get asked all the time (and my answers)

Feature: Three big questions I get asked all the time (and my real answers)

Newspapers: Not ready to retire yet? This could be the strategy for you

Podcast: Dipping your toe into retirement

From Bec’s Desk: This week is going to be fun!

Three big questions I get asked all the time (and my answers)Do you ever wonder what I get asked all the time? Well, I’ve been making a note of the questions and I’m going to start using them as inspiration for this newsletter. Here’s three of the best this week. Got one you want me to answer? — Send it in.

1. What if I’m not ready to stop working—but I don’t want to keep going like this?Welcome to your Prime Time. This isn’t about pushing through until the finish line—it’s about redesigning work so it actually works for you so you do want to keep doing it — if that’s a priority for you. The good news is, the world has changed and there are now more flexible ways to stay engaged with work while freeing up time and energy for the rest of your life — I promise.

For employees aged 55+, Australia’s Fair Work Act gives you the legal right to request flexible working arrangements, including reduced hours or days. Your employer has to respond within 21 days. While they’re not legally required to approve it, many workplaces are becoming more open to part-time and remote roles—especially since COVID shifted how we think about productivity.

And if you’re self-employed or freelance and unhappy with how things are working, this is your moment to reshape your schedule and set some lifestyle boundaries. Or consider building a portfolio career—where your work includes a mix of paid gigs, passion projects, volunteering, and maybe even sabbaticals.

Think of this not as winding down, but changing gears. The goal is energy, purpose, and time freedom—not burnout followed by a sudden retirement then relevance deprivation.

2. How do I know if I have ‘enough’ to retire?The big ‘enough’ question isn’t really about hitting a magic number (athough there’s plenty of benchmarks on how much is enough)—it’s about knowing three things about yourself and your lifestyle:

What your cost of living and lifestyle will cost across all phases of retirement

What income streams you’ll have to fund it (at each stage)

How to draw down those assets and income sources tax-efficiently, without running out before you die

Technically speaking, you’ll want to map out:

Your annual income needs (don’t forget fun and travel, not just bills)

Your superannuation balance and whether it’s in accumulation or pension phase (where earnings and withdrawals are tax-free)

Any non-super assets like shares, savings, or property that might be able to generate an income or be sold/repurposed to do so at some point

Your eligibility for the Age Pension and any other income-tested benefits (like the CSHC)

A drawdown plan that takes into account sequencing risk, investment returns, and how long you really might live (ignore those simple estimates that say 85 and 88 — they are under-estimating your real longevity if you’re healthy and proactive).

Retirement doesn’t have to mean your spending stops. It means shifting from earning your income from exertion to having more passive income sources. The more confident you are in that plan, the freer you’ll feel.

3. Is it too late to make a difference with my super if I’m over 50 (or 60) now?Not even close. The decade before retirement is often the most powerful time to grow your super. You can double your money in super every 7-10 years simply through good compound investing at returns of 7-10% per year, and generate even more if you keep contributing to your super!

Here’s some things anyone can do to make a decent difference in years not decades.

Salary sacrifice up to the concessional cap ($30,000 from 1 July 2024)

Make catch-up concessional contributions using unused caps from the last 5 years (if your balance is under $500,000)

Review your investment mix and evaluate how you can keep a healthy portion in growth investments for the longer term —many people shift too much into conservative investments when they don’t need that money for 10-20 years and it could keep growing. (Be sure to understand where your shorter term income will come from to avoid sequencing risk)

Consolidate old superannuation accounts to reduce duplicate fees and insurance premiums

Consider spouse contributions or co-contributions if you’re in a couple with uneven balances

Think about whether you’re in the position to downsize and make use of the downsizer concession, which allows you to contribute up to $300,000 into super tax free from the sale of your home. It requires you to have owned it for 10 years and lived in it as a principal residence.

And remember: super continues to grow during retirement. In the retirement phase, it’s tax-free and can still be invested in a solid portion of growth investments. So the changes you make now can compound for decades - really!

Another long weekend! It would be nice if it wasn’t raining and they hadn’t sent back my manuscript for another ‘quick review’. It’s never quick reading 400+ pages of your own writing! 😮💨 I will be thrilled when this book finally goes to print!

The week ahead is looking fun!

On Monday evening we have our Live Q&A for the How to Have an Epic Retirement Flagship Course for Winter 2025 and David Lane, the QLD State Manager of Ord Minnett, also a Senior Financial Adviser is our guest. We’re talking all about investing, financial advice and superannuation.

Then, I’m heading to Melbourne for a few days to MC and speak at the Hostplus Retire Ready event — and you’re invited to tune in online or join us in person.

I’ll be sharing ideas on Embracing an Epic Retirement at this big pre-retirement event, held at the Clarendon Auditorium in the Melbourne Convention Centre on Tuesday evening. Doors open for registration from 5.30pm, and the live broadcast kicks off at 6pm. And it’s not just me you’ll hear from — some brilliant financial planners will be diving into the tools and strategies to help you get retirement-ready.

👉 REGISTER HERE to attend or book in to watch online. Hope to see you there!

This week’s podcast really seemed to strike a chord. It’s all about ‘dipping your toe into retirement’ — and some wonderful letters came in afterwards that really made me smile (THANK YOU!).

I’m always a little surprised when the episodes I record with my producer Emilia get so much feedback — mostly because I’m far more comfortable interviewing others than sitting in the expert chair myself. But it turns out, you seem to like those ones much more than I like listening to myself! 😊 Should we do more of these ‘Bec as the expert’ sessions on the podcast? I’d love to know what resonated — hit reply and tell me what you’d like us to dig into next.

I’ve quietly put the 25% off Earlybird Deal live for our Spring Edition of the How to Have an Epic Retirement Flagship Course this week too, knowing a few of you want to get in and get organised early for this one because you’re going away beforehand. So it’s live and you can book. The course kicks off on the 28th August. 👉🏻 More information here 👉🏻

Now, I’m off to read that manuscript AGAIN!

Have a lovely long weekend. Lest we forget our ANZACs.

Got thoughts this week — hit reply to email me or leave a comment.

Cheers, Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Not ready to retire yet? This could be the strategy for you

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 27th April 2025.

What if retirement wasn’t a line you crossed, but a lifestyle you eased into – deliberately and on your own terms?

For decades, retirement has been treated like a finish line. A date we count down to. One day you’re working, the next, you’re not. But as we live longer, work more flexibly and expect more from life, that abrupt model is starting to feel outdated.

In its place is a more thoughtful approach I call dipping your toe into retirement. It’s about gradually stepping into life after full-time work – giving yourself time to figure things out rather than making all the decisions at once.

Retirement is better seen as a continuum: a slow shift involving financial preparation, emotional readiness and a reworking of your lifestyle to suit what’s next.

Some of the most fulfilled retirees I’ve met didn’t retire in the traditional sense. They began easing in five or 10 years before they fully stepped away from work, gradually shaping a life they genuinely wanted to live.

Often, that meant reducing their hours, trialling new routines, taking career breaks or volunteering. They rebalanced their priorities and made small changes to explore what brought them joy and meaning, while also planning how to fund it.

Start smallA simple way to dip your toe in is to shift to a four-day week. That one extra day creates space – for health, family, hobbies, or simply catching up on life. It gives you the chance to try a different rhythm while still enjoying the structure and financial benefits of work.

One Prime Time podcast listener described it as “a way to practise living life better, before I have to do it every day”. That mindset is powerful. It lets you experiment, reflect and adjust, long before you retire for real.

Then, when that day becomes purposefully used, and you’ve built up some financial confidence in what you can afford, you might step down another day to three days a week. Each step, taken carefully, can allow you more time to be sure about your approach to your future retirement.

How to fund the shiftYou don’t need to stop working completely to access your super. If you’re over 60, a Transition to Retirement income stream may allow you to draw a modest income while continuing to work part-time. Your super stays invested and working for you, and if you’re still contributing, you could even reduce your overall tax bill. (READ ON… in The Age, The Sydney Morning Herald. )

Dipping your toe into retirement

Dipping your toe into retirementRetirement doesn’t have to be a finish line you stumble across one day—it can be a gentle, joyful transition that you design on your terms. In this episode of Prime Time, I’m cracking open a key theme from my new book Prime Time and chatting with my producer Emelia Fuller about how to try retirement before you buy it.

From negotiating one less day of work to planning a sabbatical or exploring a "portfolio lifestyle", I’m exploring how to gradually step into the next phase of life with more freedom, more choice—and less fear.