Bec Wilson's Blog, page 6

September 8, 2024

An Epic Challenge: The Three Capes Walk in Tasmania

Feature: The Three Capes Walk in Tasmania: An epic challenge

From Bec’s Desk: I’m back!

In today’s SMH & The Age: Three of the biggest retirement myths, busted

Prime Time: How healthy relationships are built (and broken) in midlife with Nahum Kozak

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

The Three Capes Walk in Tasmania: An epic challenge

The Three Capes Walk in Tasmania: An epic challenge[This article is a newsletter version without the picture galleries - I urge you to visit the website edition and enjoy all the photos here.]

“You have nothing to do over the next four days but walk and eat. So put your phones on airplane mode and really enjoy the opportunity to disconnect.”

These were the words of our guide Dandy, as we packed our handful of clothes, water and rain jackets into backpacks to head off on one of Australia’s and possibly the world’s most iconic walks, The Three Capes Signature Walk, hosted by the Tasmanian Walking Company. Our four-day hike was a luxury experience, staying in stunning remote lodges, eating chef-prepared three course meals and sipping local Tasmanian wines. But it was more than that. It was rustic, outdoorsy, and challenging.

I’ve never been on a multi-day hiking trip before so the whole concept of this trip was new. I’m no fitness fanatic. Sure, I go to the gym 3-4 times a week and walk the dog on other days. But I really only started training for this hike 6 weeks ago, walking up Brisbane’s Mt Cootha and Mt Gravatt one or twice weekly to prepare my legs and lungs. I’m certainly glad I did, as the hike was every bit the physical challenge I’d hoped. And yet it was also achievable for an ordinary, not super-fit person like me.

I’m calling this trip the first of my “Prime Time (or Epic) Challenges” – things I want to challenge myself to do in midlife – hard things, wild and interesting experiences that keep me learning and push me out of my comfort zone in midlife.

So, onto the trip.

We started on Wednesday in a room in Hobart. 14 strangers, two guides and a pile of backpacks. Into our backpack, which we had to carry for three of the four days, went our carefully planned clothes, toiletries, sheets and water bladder, raincoats and lunchboxes. If you wanted to wear more, you had to carry more. Mine weighed about 12-13kg when we departed. My husband’s less–he teased me. The weather was cold, grey and gusty — but we were optimists – this was going to be special. It was the first walk for the 2024-25 season. Spring was peeking through, or so our guides promised.

Then it was off to Stewarts Bay near Port Arthur where we boarded a small boat, and cruised around looking at the sights on our way to Denmans Cove, a small deserted white beach where the hike begins. We had to strip off our shoes and pants and jump into the water carrying our packs to kick things off. The water was freezing so there was lots of squeals and giggling–a terrrific way to start our easy contact with the elements which for me was one of the ongoing highlights of the trip.

Day one was a polite opener to the days ahead. We hiked 7.5km – about 3km of which was firmly uphill. The trees and the undergrowth change in Tassie as you climb. So every kilometre brings something new to look at, distracting you from the stairs you’re climbing and the screaming of your legs and lungs. New mosses and ferns, wild flowers, different shaped trees, each interesting in their own ways.

Views over Tasman Island from The Blade, The coast along Munro Bight, Standing on The Blade, Dining together in Cape Pillar Lodge, and Munro Bight from a different angle.

Views over Tasman Island from The Blade, The coast along Munro Bight, Standing on The Blade, Dining together in Cape Pillar Lodge, and Munro Bight from a different angle. We’ve arrived in the beautiful Crescent Bay lodge before sunset to a hot cuppa, fresh homemade cake and a magnificent views across to Cape Raoul! We found our rooms for the first time, appreciating their simple, rustic beauty, comfy beds and warm doonas.

Then, we gathered for wine and dinner. Both lodges on the hike are designed of wall-to-wall glass, wrapped by captivating ocean views, soft Tasmanian timber floors, warmed with roaring fireplaces and including a big sitting area, a large dining table, and an open kitchen where the guides and chef worked to prepare our meals.

We exchanged stories. On our tour were two groups of four women in their fifties travelling together, leaving their hubbys and kids at home; one couple in their forties; one recently retired couple and us… all Prime Timers it seemed, chasing a physical challenge and an escape. All but 4 were first-timer multi-day walkers.

Day two arrived we packed up our things, revelled in a hot breakfast then we were off to climb Arthurs Peak for a magnificent view across to Caspe Raoul and across to Bruny Island. Our guides came into their own today, boiling tea on the track, telling us stories of the conflicts between indigenous Australians and early settlers, explaining the history of the lands we walked on and helping us really appreciate the landscape and changes in nature.

We ate our healthy packed lunches overlooking Haines Bight with views towards Black Head. Then we walked through Tornado Flat to Munro before climbing the big entry-hill to the magnificent Cape Pillar Lodge… where hot tea and warm cake were waiting for us again.

The Gondwana forest at the top of Mt Fortescue was amazing, and the views superb. Finally we reached Fortescue Bay beach after a long descent on day 4.

The Gondwana forest at the top of Mt Fortescue was amazing, and the views superb. Finally we reached Fortescue Bay beach after a long descent on day 4.The Cape Pillar Lodge has a spa treatment room and masseuse who was booked-solid by the 14 people on the trip over the two days we stayed there. Her skill–working knots out of every corner of your body, and making 30 minutes feel like an hour–bliss.

Then a joyous three course dinner with our new friends, a Tasmanian wine or two, a briefing about what we’d done that day, and what lay ahead tomorrow, and early to bed.

Day three of this hike is the day the postcard-like photos come from. We left the lodge with a belly full of gourmet porridge carrying only day-packs, a welcome relief, knowing we were returning to the same lodge that night.

Whilst the winds were gusting at up to 90 km/hr, and the rain was threatening, we felt every bit of the joy of the Tasmanian outdoors, putting on raincoats, taking off raincoats, then putting them on again. In the morning we hiked through Corruption Gully where the plants which would normally be tall trees are shrubbed or ‘bonsai’d’ by the winds. Then, on through Hurricane Heath, along a 2km climbing boardwalk up to Resolution Point. We looked out over Tasman Island at the lighthouse and its three homesteads–absolutely spectacular scenery. Then we climbed the very steep and very narrow, The Blade, a hair raising five minutes at the very top of this rocky outcrop, with the winds threatening to push us off the rocks as we took pictures of our bravery. Finally, we walked around to Cape Pillar for another healthy packed lunch! Lots of stairs, hills and stunning views. After lunch and some storytelling we walked the 6 or so kilometres back to the lodge at our own pace where a hot cuppa and warm cake was waiting!

In keeping with the Tasmanian natural vibe, dinner on day three was Wallaby Tagine, a gamey-flavoured meat worth trying. Then board games, storytelling with our guides and another briefing of the day ahead.

On day four we set off early, with our large packs, to the top of Mt Fortescue, 480m above sea level–a challenging and beautiful climb that took about 45 minutes. That was the hardest stretch of the trip given the weight of our large packs! Our guides had mentally prepared us, telling us to predict how far we had left to climb based on three chairs - one chair at the bottom - one chair a third of the way – and a third chair two thirds of the way and our guide with a hot brew waiting at the top. It wasn’t until we’d made it to the top they realised the first chair had been removed during winter - so all of us had reached the top, exhausted, thinking we had only made it about two thirds of the way!

The Gondwana Forest as we got closer to top was a sight to behold with amazing ancient tree ferns and stunning mosses and ferns, dwarfed by towering eucalypts, some of the tallest in Tasmania – stuff out of fairytales really. We had lunch and caught our breath looking back over Munro Bight and Cape Pillar - and The Blade we climbed yesterday.

Our group then split into two, with the uber-fit tackling a 3km round trip to Cape Huay– down 600 stairs, up 200 stairs, then, in return up 600 stairs and down 200 stairs. The rest of us felt confident that reaching our intended 19.6km today would be enough of a challenge and started the gradual, tough and seemingly never ending descent back down to sea level to the squeaky white sands of Fortescue Bay.

With aching feet and a few blisters we stripped our shoes and went into the ice cold 12.5 degree water. Some even went for a swim (not me!).

Then, the bus ride back to base for a celebratory champagne with our fellow travellers and our two guides. We walked about 54kms in four days and it was magical! The highlight – the challenge of the walk, eating healthy and delicious food I didn’t have to prepare, the stories and lessons from our guides, taking time to really enjoy my surroundings, and the rugged, chilly, spectacular beauty of the Tasmanian outdoors.

I’m a convert - more hiking trips ahead for me. Tasmanian Walking Company – our hosts – run 8 different walks in Australia, five of which are in Tasmania. And they also offer a range of international walks too. They’re the only company that offers private hut accommodation on the Three Capes Lodge Walk. TWC’s collection of walks also includes The Overland Track, Bay of Fires Lodge Walk, Bruny Island Long Weekend and Wineglass Bay Sail Walk. And if you’re keen to try the Three Capes for yourself, I’m told that there’s still a couple of spots available later in the year.

I couldn’t fit the photo galleries on this newsletter - so I’ve made a special article on the site here and published all the photos from this epic challenge. You can see it here.

I took a week away from writing, and did some hiking, as you read above. And I’ve bragged enough about that. But it’s back to cooking my own food, running our awesome course and writing my book this week. (And replying to emails I promise 😁).

—

Our Spring Edition of the Flagship Course is in week 5. To kick off the week we’ve got our ‘Finding your purpose’ session in the Epic Retirement Course, with Rowena Millward on Monday night. Then our interactive session, where everyone jumps on-screen and talks about the process of finding their purpose together.

—

I’ll be launching our next How to Have an Epic Retirement Flagship Course - the Summer Edition, for earlybird bookings this week. The initial discount will be 25% off the RRP to the first-in (which means you’ll get it at $359). The next course will kick off on the 10th October - not long now! I can’t wait. Keep an eye out as the earlybird deal will be for those who are first in. Register your interest here. This is my last course for 2024.

—

If you’re part of a couple and you haven’t yet listened to this week’s Prime Time Podcast, with Nahum Kozak, do yourself a favour and turn it on. I learnt a lot speaking with him, and it pointed me to things we should all be thinking about that maybe we don’t discuss much because of how personal and intimate they are. So much insight into our relationships and how they change as we get older in this one- and so many sensible tips for things we can and should do!!

And a big thanks to HESTA who’ve joined us as a sponsor of the Prime Time podcast for the next quarter!

And that’s the week’s update, done. You can always email me at bec@epicretirement.com.au. I love getting your letters. Until next week… make it epic!

How healthy relationships are built (and broken) in midlife with Nahum Kozak

How healthy relationships are built (and broken) in midlife with Nahum KozakIn this edition of Prime Time we explore how our most important relationships change in midlife and how we can connect better with our partner as these shifts occur. I’m talking with Senior Psychologist Nahum Kozak from Lighthouse Relationships who has so much wisdom, empathy and expertise in this area, it’s boggling.

This episode unpacks the shifts and changes that relationships undergo as we transition from working life to retirement. Nahum offers deep insights into how these changes can impact our identity and intimacy, and shares practical strategies for strengthening connections and navigating conflicts. Whether you're looking to deepen your relationship or understand the complexities of love in your Prime Time and retirement, this conversation is packed with valuable advice and real-world solutions.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Three of the biggest retirement myths, busted

Three of the biggest retirement myths, bustedExtract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 8th September 2024.

There are a few retirement myths that seem to persistently buzz around, no matter how much we try to swat them away. Today, I’m tackling three of the biggest ones that keep cropping up in my retirement courses and events. It’s time to lay these myths to rest once and for all.

Myth 1: You need a million dollars to retire in comfortFor ages, there’s been this overwhelming notion that a million-dollar superannuation is the ticket to a comfy retirement. But let’s set the record straight – this isn’t necessary for most people. Data shows that the median super balance for Australians between ages 65 and 69 is far less than a million. In fact, as of the last report in 2021, it was $213,986 for men and $201,233 for women.

The Association of Superannuation Funds of Australia says that the average Australian couple needs $690,000 in superannuation as they enter retirement, to be able to reach the level of income they declare will provide for a comfortable retirement of $73,337 a year. And a single person will need $595,000 in super for a comfortable retirement, allowing them to rely on an income of $52,085. These numbers assume that you retire at 67, own your own home outright, and you can access a part age pension and the pension concessions to help manage your cost of living. If you are ineligible for the pension, or you don’t own your own home, you’ll need to budget more.

But everyone’s idea of a comfortable retirement varies. For some, it means travelling the world and enjoying life’s greatest luxuries, while for others, it’s about simplicity, spending time with grandchildren, indulging in hobbies, or spending time on passions and purposeful volunteering. Your retirement goals are at the core of knowing how much you actually need for the comfortable retirement – and you need to spend some time working on them.

The best way to assess how much you need is to take those goals, then build a detailed budget, incorporating the amount you want to spend on everyday living, the amount you want for one-off expenses and big ticket items; and the amount you want to put towards your epic retirement experiences. Then, get onto a retirement calculator, such as the one on the moneysmart website, and see whether your current superannuation balance can support the budget you’ve built over your projected lifespan.

Myth 2: You should move all your investments to conservative assetsWhen people shift into retirement, they can feel gripped by the financial realities of never earning a pay cheque again, with many people becoming quite concerned about protecting their capital. Some even consider shifting their entire portfolio to conservative assets. However, completely turning your back on growth assets might not be the smartest move. The reasons are twofold. First, life expectancy has risen dramatically. For many, retirement could now span 25 to 30 years, or even longer. This extended timeframe means you need to maintain some exposure to growth assets to maintain your capital pool over and above inflation. If you shift all your investments to conservative, they might struggle to keep pace.

This article continues. Read the rest of the article here.

Hey! Two last things.If you aren’t an Aussie and you don’t want to read all this guff about “Superannuation”, sign up for my Epic Retirement International newsletter here… international.epicretirement.net.

And, if you haven’t got yourself a copy of the book, How to Have an Epic Retirement, you can order it on Amazon here.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

The Three Capes Walk in Tasmania: An epic challenge

“You have nothing to do over the next four days but walk and eat. So put your phones on airplane mode and really enjoy the opportunity to disconnect.”

These were the words of our guide Dandy, as we packed our handful of clothes, water and rain jackets into backpacks to head off on one of Australia’s and possibly the world’s most iconic walks, The Three Capes Signature Walk, hosted by the Tasmanian Walking Company. Our four-day hike was a luxury experience, staying in stunning remote lodges, eating chef-prepared three course meals and sipping local Tasmanian wines. But it was more than that. It was rustic, outdoorsy, and challenging.

Standing on The Blade, views over The Blade and Tasman Island and the coastline along Munro Bight

Standing on The Blade, views over The Blade and Tasman Island and the coastline along Munro BightI’ve never been on a multi-day hiking trip before so the whole concept of this trip was new. I’m no fitness fanatic. Sure, I go to the gym 3-4 times a week and walk the dog on other days. But I really only started training for this hike 6 weeks ago, walking up Brisbane’s Mt Cootha and Mt Gravatt one or twice weekly to prepare my legs and lungs. I’m certainly glad I did, as the hike was every bit the physical challenge I’d hoped. And yet it was also achievable for an ordinary, not super-fit person like me.

I’m calling this trip the first of my “Prime Time Challenges” – things I want to challenge myself to do in midlife – hard things, wild and interesting experiences that keep me learning and push me out of my comfort zone in midlife.

So, onto the trip.

We started on Wednesday in a room in Hobart. 14 strangers, two guides and a pile of backpacks. Into our backpack, which we had to carry for three of the four days, went our carefully planned clothes, toiletries, sheets and water bladder, raincoats and lunchboxes. If you wanted to wear more, you had to carry more. Mine weighed about 12-13kg when we departed. My husband’s less–he teased me. The weather was cold, grey and gusty — but we were optimists – this was going to be special. It was the first walk for the 2024-25 season. Spring was peeking through, or so our guides promised.

Then it was off to Stewarts Bay near Port Arthur where we boarded a small boat, and cruised around looking at the sights on our way to Denmans Cove, a small deserted white beach where the hike begins. We had to strip off our shoes and pants and jump into the water carrying our packs to kick things off. The water was freezing so there was lots of squeals and giggling–a terrrific way to start our easy contact with the elements which for me was one of the ongoing highlights of the trip.

Day one was a polite opener to the days ahead. We hiked 7.5km – about 3km of which was firmly uphill. The trees and the undergrowth change in Tassie as you climb. So every kilometre brings something new to look at, distracting you from the stairs you’re climbing and the screaming of your legs and lungs. New mosses and ferns, wild flowers, different shaped trees, each interesting in their own ways.

We’ve arrived in the beautiful Crescent Bay lodge before sunset to a hot cuppa, fresh homemade cake and a magnificent views across to Cape Raoul! We found our rooms for the first time, appreciating their simple, rustic beauty, comfy beds and warm doonas.

Then, we gathered for wine and dinner. Both lodges on the hike are designed of wall-to-wall glass, wrapped by captivating ocean views, soft Tasmanian timber floors, warmed with roaring fireplaces and including a big sitting area, a large dining table, and an open kitchen where the guides and chef worked to prepare our meals.

We exchanged stories. On our tour were two groups of four women in their fifties travelling together, leaving their hubbys and kids at home; one couple in their forties; one recently retired couple and us… all Prime Timers it seemed, chasing a physical challenge and an escape. All but 4 were first-timer multi-day walkers.

Day two arrived we packed up our things, revelled in a hot breakfast then we were off to climb Arthurs Peak for a magnificent view across to Caspe Raoul and across to Bruny Island. Our guides came into their own today, boiling tea on the track, telling us stories of the conflicts between indigenous Australians and early settlers, explaining the history of the lands we walked on and helping us really appreciate the landscape and changes in nature.

We ate our healthy packed lunches overlooking Haines Bight with views towards Black Head. Then we walked through Tornado Flat to Munro before climbing the big entry-hill to the magnificent Cape Pillar Lodge… where hot tea and warm cake were waiting for us again.

The Cape Pillar Lodge has a spa treatment room and masseuse who was booked-solid by the 14 people on the trip over the two days we stayed there. Her skill–working knots out of every corner of your body, and making 30 minutes feel like an hour–bliss.

Then a joyous three course dinner with our new friends, a Tasmanian wine or two, a briefing about what we’d done that day, and what lay ahead tomorrow, and early to bed.

Day three of this hike is the day the postcard-like photos come from. We left the lodge with a belly full of gourmet porridge carrying only day-packs, a welcome relief, knowing we were returning to the same lodge that night.

Whilst the winds were gusting at up to 90 km/hr, and the rain was threatening, we felt every bit of the joy of the Tasmanian outdoors, putting on raincoats, taking off raincoats, then putting them on again. In the morning we hiked through Corruption Gully where the plants which would normally be tall trees are shrubbed or ‘bonsai’d’ by the winds. Then, on through Hurricane Heath, along a 2km climbing boardwalk up to Resolution Point. We looked out over Tasman Island at the lighthouse and its three homesteads–absolutely spectacular scenery. Then we climbed the very steep and very narrow, The Blade, a hair raising five minutes at the very top of this rocky outcrop, with the winds threatening to push us off the rocks as we took pictures of our bravery. Finally, we walked around to Cape Pillar for another healthy packed lunch! Lots of stairs, hills and stunning views. After lunch and some storytelling we walked the 6 or so kilometres back to the lodge at our own pace where a hot cuppa and warm cake was waiting!

In keeping with the Tasmanian natural vibe, dinner on day three was Wallaby Tagine, a gamey-flavoured meat worth trying. Then board games, storytelling with our guides and another briefing of the day ahead.

On day four we set off early, with our large packs, to the top of Mt Fortescue, 480m above sea level–a challenging and beautiful climb that took about 45 minutes. That was the hardest stretch of the trip given the weight of our large packs! Our guides had mentally prepared us, telling us to predict how far we had left to climb based on three chairs - one chair at the bottom - one chair a third of the way – and a third chair two thirds of the way and our guide with a hot brew waiting at the top. It wasn’t until we’d made it to the top they realised the first chair had been removed during winter - so all of us had reached the top, exhausted, thinking we had only made it about two thirds of the way!

The Gondwana Forest as we got closer to top was a sight to behold with amazing ancient tree ferns and stunning mosses and ferns, dwarfed by towering eucalypts, some of the tallest in Tasmania – stuff out of fairytales really. We had lunch and caught our breath looking back over Munro Bight and Cape Pillar - and The Blade we climbed yesterday.

Our group then split into two, with the uber-fit tackling a 3km round trip to Cape Hauy– down 600 stairs, up 200 stairs, then, in return up 600 stairs and down 200 stairs. The rest of us felt confident that reaching our intended 19.6km today would be enough of a challenge and started the gradual, tough and seemingly never ending descent back down to sea level to the squeaky white sands of Fortescue Bay.

With aching feet and a few blisters we stripped our shoes and went into the ice cold 12.5 degree water. Some even went for a swim (not me!).

Then, the bus ride back to base for a celebratory champagne with our fellow travellers and our two guides. We walked about 54kms in four days and it was magical! The highlight – the challenge of the walk, eating healthy and delicious food I didn’t have to prepare, the stories and lessons from our guides, taking time to really enjoy my surroundings, and the rugged, chilly, spectacular beauty of the Tasmanian outdoors.

I’m a convert - more hiking trips ahead for me, and an ongoing committment to walking more in nature, regularly. Tasmanian Walking Company (TWC) – our hosts – run 8 different walks in Australia, five of which are in Tasmania. And they also offer a range of international walks too. They’re the only company that offers private hut accommodation on the Three Capes Walk. TWC’s collection of walks also includes The Overland Track, Bay of Fires Lodge Walk, Bruny Island Long Weekend and Wineglass Bay Sail Walk. And if you’re keen to try the Three Capes for yourself, I’m told that there’s still a couple of spots available later in the year.

August 31, 2024

Hitting preservation age: 'Should I retire then pick up part time work?'

In this edition

Feature: Hitting preservation age: 'Should I retire then pick up part time work?'

From Bec’s Desk: wild weather ahead

SMH/The Age: Four tough truths about renting and retirement (seriously… read the digital edition of this story in full - some 💔 stories)

Prime Time podcast: The do's and don'ts of a South East Asian sabbatical

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

Hitting preservation age: 'Should I retire then pick up part time work?'

Hitting preservation age: 'Should I retire then pick up part time work?'

A popular nurse retiring after many years of long shift work - image by Dall-e

A popular nurse retiring after many years of long shift work - image by Dall-eHi Bec. I have a question for you. I reach my retirement preservation age of 60 next week. Yay! Cutting back days in my 60-70 hour week isn’t an option, however I do have offers for part time work elsewhere.

I’ve read a little about tax implications if it is deemed I have not actually retired.

I would like to retire, pay off my mortgage, and then pick up another job 2-3 days per week, probably within 3 months. Is that within the regulations around retirement and super? — Sue E.

Hey Sue! Congrats on hitting your retirement preservation age—exciting times ahead! Let’s dive straight into your question because it’s a really good one!

When you reach your preservation age (which is 60 for everyone in Australia now), you can access your superannuation if you meet a ‘condition of release’. One of the most common conditions of release is ‘retirement’. For the tax office and your super fund to consider you officially ‘retired,’ you generally need to genuinely finish up your employment and not have any agreement in place to work afterwards. Then, you can complete the form with your superfund to transfer your superannuation from the accumulation phase into a retirement phase account. There’s a cap of $1.9M (called the transfer balance cap) on how much you can transfer to retirement phase during your lifetime. If you do this, you can access your super as a lump sum or start drawing down from it from the age of 60.

There’s a few important things to be aware of:

Taking up another job: You can retire, legitemately, access your super and then decide afterwards that retirement isn’t for you and pick up some work - part time or full time. Funds tell me the important thing is not to have agreements in place prior to going through the process of retiring with your fund. The process itself is pretty simple— a form with a tick box that asks you if you’re retiring. But ultimately, you’re reporting your status to the ATO, which is important to do correctly and with integrity. Just talk to the financial adviser at your fund. They’re pretty keen to help people get the transition from accumulation to retirement right.

What happens if you’re not retired? If you don’t meet the retirement condition when you complete the form with your superfund, your super could be deemed "not preserved," meaning any withdrawals might be subject to tax penalties. Again - funds really know how to help you navigate this — and it sounds like you are actually legitemately retiring — so ask them to guide you through.

Transition to retirement (TTR): If you’re not sure about fully retiring, consider starting a TTR income stream. This lets you draw down from your super, up to 10% of your balance each year—while still working part-time. It’s tax-effective and could give you the flexibility you need. Ultimately though, if you want to be able to make a lump sum drawdown to pay off your mortgage, you can’t with a TTR account.

Compulsory drawdowns: Remember, once you kick off a retirement phase account you need to withdraw the mandatory drawdown from your super fund every year. This is an amount that starts at 4% from age 60-64 and goes up as you get older. For most people accessing this drawdown is actually the goal, but for some feeling forced to draw down their retirement savings to a required level is a surprise.

I hope that insight helps— it really is a great question. When I chat with the superfund financial advisers - they’re eager to help people navigate this step without fear, and do it correctly. So don’t hesitate to book a call in with your fund’s general advice team and ask about it.

Cheers, congratulations on hitting preservation age - now get out there and make it epic! Bec Xx

So many wonderful things are happening. I feel blessed this week.

The Epic Retirement Flagship Course is up to week 4. Last week we had David Lane the QLD State Manager and Senior Adviser from Ord Minnett for our Live Q&A event - and we ran over the hour because we had SO MANY QUESTIONS! I love it when it rains questions in a live event! In the week ahead for our live event we have Jen Harding, the GM of Advice, Development and Growth at HESTA to answer questions about super and the help people can expect from their super funds.

If you’d like to do the course, we will only be holding one more 6 week program this year — in October/November. It will launch in the next few weeks and the first-booked will get the best prices. Register your interest here.

—

This week I spoke at the Nillumbik Seniors Housing Forum in Eltham, Victoria. It was a hoot. 130 people all hungry for very current insights on how to navigate downsizing, when to downsize and what their options really are. And I got halfway through a new speech before the crazy Melbourne weather came in, blew out the power and made me rest on my knowledge and present without slides. I actually think we all had an even better time learning from that point on - without the formality of the slide show and with the intimacy of working through each lesson together! And we got real with on-the-fly questions and answers too!

—

This week I’ve done a story in The Age and The Sydney Morning Herald that I’ve been mulling for weeks or even months. People have asked me to address renting and retirement and I didn’t want to do so unless what I wrote could help — and it’s not an easy thing to do. So have a read. It certainly taught me a few things immersing myself in the issues, choices and stories of the people who rent today, thinking about what they can and can’t do tomorrow! — [Even if you get the paper in print, read the digital edition on this one -shared below — it’s longer and has more real life stories].

—

I’ve done it - I’ve kicked off a new Epic Retirement International newsletter. It went out for the first time on Friday. So if you’re an international person, lurking here to find out what an Epic Retirement is all about, you can now join a dedicated newsletter that’s completely separate with 23,000+ other people who’ve been asking for it (yes! really). The first piece is foundational - ‘There’s six pillars of an Epic Retirement’. Read it here and sign up free. (And it’s ok to choose to get just one newsletter - the Aussie or the International). The international won’t be as frequent as my Aussie one!

—

QBD have this quarter included How to Have an Epic Retirement in their local author celebration and campaign. That means I’ll be dropping into QBD bookstores all over the place to say ‘hi’, and signing copies of the book as I go. So keep an eye out. Such a thrill to see the book being supported, read and enjoyed. You can find plenty of copies in QBD stores and online here too.

—

And finally - I’m taking a few days later this week away from the desk to go on a four-day hike along the Three Capes in Tassie with the Tasmanian Walking Company. The weather is really going to make this fun. The current weather report is calling for Spring sleet, snow and extraordinary winds over the week ahead. So my husband and I are excited, not just for the 50kms of hiking, the beautiful cabins and local cuisine, dotted through some of the most picturesque countryside in Australia. We’re also really looking forward to the crisp, wild experience of the outdoors that lies ahead. I’ll post pics on my public Facebook profile if you want to follow along. Hiking in snow is a first for me.

And alongside all this, I’m writing furiously, aiming for that book deadline like there’s no tomorrow.

Have a great week ahead. You can always email me at bec@epicretirement.com.au. I love getting your letters. Until next week… make it epic!

Many thanks! Bec Wilson

Author, podcaster, guest speaker, retirement educator … Visit my website for more info about me, here.

Four tough truths about renting and retirement

Four tough truths about renting and retirementExtract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 1st September 2024.

A key goal for a comfortable retirement is owning your own home outright when you get there. Many renters nearing retirement write to me looking for advice, and it’s difficult to respond given the ongoing housing crisis, a problem without an easy fix. In my view, renting is a bad investment, often a necessity, driven by circumstance rather than desire.

But this week, I decided to dive deeper and asked some people who rent, why they do it. Some of their stories are sad, while others show the tradeoffs people are making. The truth is, renting can teach you some pretty hard lessons. Here are four of the biggest ones.

Lesson 1: Renting has no finish lineLet’s be honest: renting sucks. There’s no end in sight, no moment where you can sit back and say, “I’ve made it.“ Every year or two, when your lease comes up, you get that knot in your stomach, wondering if the rent will go up or if the landlord will decide to sell. It’s a never-ending cycle of uncertainty. And it’s worse when you’re older.

Take Susan, who’s 70 and living on Melbourne’s northern fringe. She’s widowed, broke, and relying on the single age pension after her husband’s business went under during COVID, and he died of a heart attack not long after.

She had to sell everything they owned. Now, she’s moved out of the city, away from her friends and community to be able to find a place to rent for $370 per week, which she affords thanks to some help from rent assistance.

It took her a year of lining up at rental inspections and submitting applications to find a place because landlords took one at her application as a single woman on the full age pension and offered it to someone younger or more affluent. She lives in constant fear that her lease won’t be renewed.

Lesson 2: Home ownership remains the best way to build wealthOwning a home used to be the great Australian dream, but the data points out that buying a home in the inner circles of our capital cities is unreachable for average young people in Australia right now.

They can’t scrabble together the scale of deposit a bank wants them to have to underpin a large loan. They can’t afford the enormous mortgage with six per cent interest rates on their average salaries.

And yet, despite this mess, owning a property could be the single greatest way of creating wealth ever in our economy. There are three simple reasons why: every dollar of capital growth you make on your home is capital gains tax-free for your entire life, and the amount of leverage you can take on your family home is higher than the leverage available in any other asset class, so when it grows, your wealth grows –fast quickly.

If you’re middle-aged and mortgage-free or close to it, count your blessings.

Paying a principal and interest mortgage is the most diligent long-term savings regime most people enter into voluntarily.

Over the last 30 years residential property has grown by an average of 5.2 per cent per year. And remember, all of that growth, if made in your principal place of residence is capital gains tax-free.

Jen, 28 and Greg, 29, are renting in inner Melbourne and have given up hope on buying a home for now. They’re young and working hard with a household income of $130,000 between them after tax and their rent is $42,000 per year.

They’ve grown up in Richmond, and lived all their lives in the surrounding suburbs of inner Melbourne, so that’s where their roots are and where they’d want to buy.

If they took out a mortgage on a small apartment they’d expect to be paying closer to $60,000 in repayments a year, and then they’d have to pay body corporate fees too. They’re afraid of getting themselves into financial hot water they can’t deal with.

They feel sick about not-buying, but they need to recognise that they still have time and choice – time to save up a deposit, to rethink their inner-city ambitions and move a bit further out of the inner city to a more affordable suburb if they’re brave enough.

Or, they might even consider getting themselves on the housing ladder earlier by buying an investment property in a suburb with good rental returns.

Lesson 3: Renting can be a financial and lifestyle choice – reallyThis article continues.

Read the rest of this article here in The Age, The Sydney Morning Herald, Brisbane Times, WA Today. It also appears in the print editions.

The do’s and don’ts of a South East Asian sabbatical

The do’s and don’ts of a South East Asian sabbaticalThis week on Prime Time, we dive into the art of taking a midlife sabbatical with Mel Pike. At 53, Mel took extended leave from her public service role and spent five months living near Kata Beach in Thailand, using the time to decompress and rediscover what she wanted from the next stage of her life. We’ll explore her entire journey—from how she saved for it to what she did during her stay—and share plenty of insights along the way. It’s an inspiring story with lessons we can all take to heart.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

August 24, 2024

How much do you need to retire in comfort in Australia? It just increased.

Feature Story: How much do you need to retire in comfort in Australia? It just increased.

From Bec’s Desk: An exciting launch of the retirement planning survey insights

SMH/The Age: The truth about why we’re working longer in retirement

Prime Time: Longevity: separating fact from fiction with Dr Nick Coatsworth

How much do you need to retire in comfort in Australia? It just increased.

Woman retiring in comfort with Australian income - Dall-e

Woman retiring in comfort with Australian income - Dall-eIf you've ever wondered how much income you’ll need in retirement to live in comfort, then today’s article is for you. The latest benchmarks from the Association of Superannuation Funds of Australia (ASFA) have just been updated to reflect the cost of living for the June 2024 quarter.

ASFA’s data shows retirees are feeling the pinch, with the cost of a comfortable retirement rising by 3.7% over the last 12 months, slightly under pacing the CPI at 3.8%. The June quarter alone saw notable hikes in home and vehicle insurance, along with private health insurance premiums, pushing up budgets by 0.9% for both singles and couples.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

So, what does that mean for you? If you’re around 65, couples now need to expect a cost of living of $73,337 per year for a comfortable retirement, while singles require $52,085.

The ‘ASFA comfortable’ lifestyle budget assumes that retirees own their own home outright and are eligible for a part-aged pension, and have access to pension concessions. The ‘ASFA modest’ lifestyle budget assumes retirees receive a full age pension and again, own their own home outright. There’s no benchmarks that can help renters to navigate.

ASFA also updated the amounts you should expect to need if you are planning to live a more modest lifestyle, which see’s retirees in this category live a lot more frugally, with a budget of $47,731 for a couple and $33,134 for a single person.

ASFA also calculates the superannuation balances they believe people will require at retirement to be able to comfortably meet these levels of income over their lifetime. These are unchanged. A couple will still need $690,000 and a single person $595,000 in superannuation to generate this level of income from their assets. And someone seeking a modest income needs to have $100,000 in superannuation, whether a couple or a single person.

Where's the financial strain hitting hardest this year?

Insurance Costs: Insurance premiums have surged, jumping 3.1% in the June quarter and a whopping 14.0% over the past year. This spike is largely due to higher reinsurance costs, the impact of natural disasters, and increased claims.

Private Health Insurance: From April 1, private health insurance premiums rose by an average of 3.03%, marking the biggest increase since the pandemic started.

Electricity Prices: Electricity costs climbed 2.1% in the June quarter and 6.0% over the past year. The Energy Bill Relief Fund helped, but without those rebates, electricity prices would have soared by 14.6% over the 12 months to June 2024.

Food Costs: Annual food inflation eased slightly to 3.3% in the June quarter, down from 3.8% in March. However, essentials like fruits and vegetables are still 3.7% more expensive than a year ago, impacting retirees' grocery bills.

Clothing and Footwear: Prices for clothing and footwear rose by 3.1% this quarter, driven by new season stock and the end of sales promotions.

Fuel Prices: Automotive fuel prices edged up 1.7% in the June quarter, adding to the ongoing fuel cost fluctuations that retirees have to navigate.

Travel and Accommodation: Domestic travel costs remained stable, but international travel and accommodation expenses shot up by 8.1%.

If you want to dive into how to budget for retirement, how much you need to retire, and how the age pension interacts with superannuation, get your copy of How to Have an Epic Retirement. It’s available online at Amazon here and in all Big W stores.

An exciting launch of the retirement planning survey insights and some new projectsFirst, the new projects…

I’ve got two new projects in coming weeks… and I’d love you to get involved.

1) an international newsletter for our growing international followers who don’t really want to read about Australian pension and superannuation issues but do want to learn how to have an epic retirement (sign up here) and,

2) I’ve been contemplating launching an exclusive private online community (like a facebook group but off-facebook and privately managed with a small fee) for Australians. Preregister your interest here so I know if you’re keen to participate.

—

The Epic Retirement Flagship Course is now in week 3 and flying by! Everyone is learning the finer details of superannuation and investing this week - some of the hardest material in the course to learn but also some of the most important to grasp. And we have David Lane, the State Manager and a Senior Financial Adviser from Ord Minnett joining us on Monday evening for a Live Q&A event. The reviews and feedback from those doing the program have again been amazing (thank you so much everyone!).

We’ll only be holding one more program this year, in October/November. I’ll be releasing it in coming weeks. You can sign up for the Expression of Interest List here. Earlybird offers will be a bit different next time - designed to reward people who book first with better discounts.

—

This week was a big week, a project I have been working on for months came into the public eye… You might remember a few months ago I ran a Retirement Planning Survey here, asking you to share what you need help with. Well, you might be pleased to see that the data from this survey has been put to extraordinarily good use.

I’ve worked with the wonderful people at Allianz Retire+ to produce a detailed paper for the financial services industry. The paper talks about what today’s retirees need and want, and is designed to give financial advisers and super funds some insight into how they can make your retirements more epic! The report is seriously called “How do we make retirements more epic?”

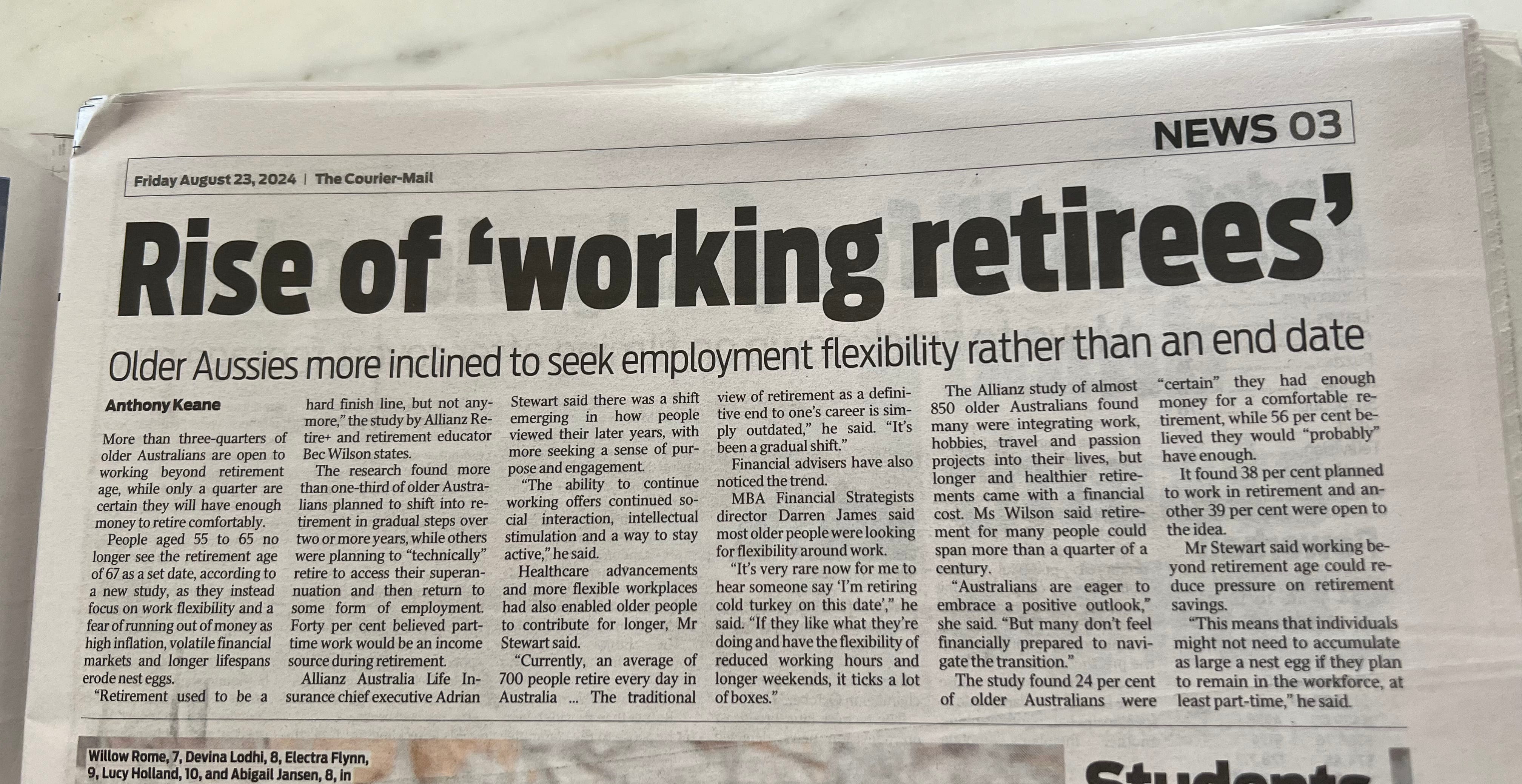

Some of the insights from the report have been featured in the nation’s newspapers this week. It started a big discussion on this insight that many of you want to work AFTER you retire! Including this piece in The Australian “Why working in retirement is set to boom’, and articles in the Daily Telegraph, The Courier Mail (pictured), NT News and plenty of others.

Article on page 3 of Friday’s Courier Mail about insights from the report.

Article on page 3 of Friday’s Courier Mail about insights from the report. I’ve also written a detailed article about the report and insights in this weekend’s Nine Newspapers. (see it below)

And, if you want to have a look at the wider report, ‘Unlocking the secrets to an Epic Retirement’ and see what a wonderful resource we’ve created — you can. Download the report here. (Remember it’s for the industry - not designed for consumers). See if you agree with the insights and conclusions - I welcome your feedback.

—

I’m counting down… 10 days until my big 50km hike over 4 days of the Three Capes in Tasmania. And 22 days until my daughter comes home from Canada for her 21st birthday! I’m counting.

I’m hitting the road this week, off to Melbourne to keynote the Nilumbik Seniors Housing Forum, and then catching up with some of the funds, recording some podcasts too and trying to squeeze in some writing in-between.

Have a great week ahead. You can always email me at bec@epicretirement.com.au. I love getting your letters. Until next week… make it epic!

Many thanks! Bec Wilson

Author, podcaster, guest speaker, retirement educator … Visit my website for more info about me, here.

The truth about why we’re working longer in retirementExtract of article published in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 25th August 2024.

Retirement doesn’t really mean ‘stopping’ work anymore. For most people approaching this phase of life, the plan isn’t to clock out for good; it’s to keep working even after they start tapping into their superannuation.

But we have to ask: Is this because they genuinely want to keep working, or is it driven by the fear of running out of money and scraping by on the age pension, which barely keeps you above the breadline in Australia?

The Allianz Retire+ ‘How do we make retirements more epic?’ survey, just released this week, sheds some light on this. We surveyed 850 people approaching and in early retirement across Australia to explore their retirement planning needs, and the message is clear – the traditional templates for retirement are outdated. Today’s retirees, the Baby Boomers, and Gen Xers coming up behind them are having to forge new paths.

We’re all living longer. According to Australian government actuaries, the median life expectancy for today’s 65-year-olds is between 91 and 95, considering ongoing improvements in health and wealth. This longevity has snuck up on us during our lifetimes, catching many pre-retirees off guard.

The reality of retirement today is sobering. A whopping 82 per cent of those surveyed agreed that the age pension simply isn’t enough for a comfortable retirement. And that reality bites.

What’s more, 67 per cent want to front-load their spending in retirement, enjoying the fruits of their labour while they’re still relatively young and healthy.

Retirement is no longer about stopping work; it’s about managing and balancing your money, health and happiness in a way that suits you.

As we approach retirement, the sudden realisation that we need to plan for a much longer life leaves us juggling four key strategies:

Cutting costs – trimming your lifestyle to fit a smaller budget.

Building the nest egg – often by downsizing the family home to free up cash.

Smarter investing – putting your money into income-producing assets that can last a lifetime.

Working longer – slowing down the drawdown of your superannuation.

And if you’re already nearing retirement and don’t have time to build up more savings than planned, your options narrow to just three: be savvy with your budget, invest in assets that will last your lifetime, or keep working longer.

The data speaks volumes. Only 24 per cent of Australians surveyed feel confident they have enough to provide them with a comfortable retirement, while a significant 49 per cent actively fear running out of money during their retirement years.

Interestingly, around 50 per cent of people admit they have only a basic understanding of how retirement finances work. Most of those who do feel confident say they gained their knowledge through self-directed research – whether through books, newspapers, or their super fund’s website.

Read the rest of this article here in The Age, The Sydney Morning Herald, Brisbane Times, WA Today. It also appears in the print editions.

This week on Prime Time, I’m joined by Dr. Nick Coatsworth—an infectious disease and respiratory physician, former Deputy Chief Medical Officer, and the host of the hit TV show Do You Want to Live Forever?. We’re diving into the science and medical advancements in ageing and longevity, and exploring what we can all do to make the most of our prime time years.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

August 17, 2024

How do you help yourself?

Article: How do you ‘help yourself‘?

SMH/The Age: Nervous about retiring? You might be better off than you think

Prime Time: A practical guide to living alone and loving it

From Bec’s Desk: Hiking and writing!

How do you ‘help yourself‘? I got a phonecall from a financial adviser I didn’t know last week who said to me “I’ve just had a new client sign on with me — the best client I’ve had in years! She understood retirement really well and what might be ahead of her and she was excited about it. She’d set her budget, written down her goals and was ready for advice when she walked through the door. She asked all the right questions - and when she got advice from us, she acted on it. She was really proactive,” he said.

The punchline — this woman had just completed the Winter Edition of the Epic Retirement Flagship Course. And the adviser wants all his clients to do it.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

I was surprised that he was surprised! Why woudn’t you want to be proactive about shifting gears into retirement? I talked to a few superfunds about it during the week and they confirmed this advisers’ thoughts. Many funds have divided their members up into the ‘proactive people’, the ‘reactive people’, and the ‘inactive people’ as they traverse retirement. And they’re trying to work out how to help each group if they can.

I’m assuming most people reading this are ‘proactive people’, but I do think, in every group, there’s also a lurking group of people who are reactive, curiously watching on, not taking action. And I have no doubt, among your friends, you know some inactive people. You know the ones - those people who don’t make decisions actively and wait for life to happen to them, then wonder at how you achieved so much as a proactive person.

So today I want to talk about helping yourself in retirement. I think it’s a critical skill. It’s the self-helpers I meet that are doing modern retirement the best! They help themselves to information on how to navigate their finances, to ideas on looking after their health, and ways of living their lives well and they research them. Whether they are rich or not-so-rich financially, the self-helpers go out of their way to keep learning, finding ideas, testing them out and implementing them. And that is something I think we need to talk about more.

During our working lives, we’re constantly reminded of the importance of staying ‘up with it’. We know that staying relevant takes self-driven effort. What noone tells us is that, once we’ve left behind our formal years of education we’ve often got to take a ‘self help’ approach — reading, going to events, talking to smart people and then, developing our own views of what decisions and choices are right for us in the next stage.

As we move into this new phase, the need for learning is more crucial than ever. Why? Because without staying sharp, we risk missing out on great opportunities, getting hoodwinked by bad advice or locking ourselves into services that frankly aren’t right for us. We risk taking someone’s advice on social media at face-value instead of developing our own thoughts and knowledge too.

Let’s be real—things are changing faster than ever, and the best source of knowledge is a combination of well-trusted experts and advisers and our own well-developed nose for the truth.

Because the people we trust don’t always have the answers we need. Product companies want to sell you something, whether it’s right for you or not. Doctors are often too pressed for time to give you the deep dive you might need, and let’s not forget the shortage of financial advisers, leaving many unable (or unwilling) to afford advice. And to be honest—the world is evolving at such a speed that many busy professionals are struggling to keep up.

So, how do you take the same proactive approach you’ve used all your life and apply it to the years ahead to make the right decisions?

I’m a firm believer that we need to be more self-help-oriented at this stage of life. We’ve got to step up to the plate and gather information ourselves and make active judgements on what is ‘good’ information and what is information with a deeply vested interest. I see a huge difference between the financial circumstances and life satisfaction of those who are proactive self-helpers and those who are reactive (or heaven’s forbid, inactive), just waiting for things to happen to them to drive their decision making. And you know I’m always going to push you to be proactive!

So, if you feel like you’re not doing enough ‘self-help’ today, here’s how you can start:

1. Deliberately embrace a more active, learning mindset: Decide what you are going to learn about and be interested in, just as you did during your working years. Continue seeking out knowledge, but shift your focus to areas that will impact your retirement quality. This could be learning about new financial strategies, understanding the latest in health and wellness, or even picking up new hobbies that keep your mind sharp.

2. Embrace and leverage technology: The internet is a treasure trove of current information, but you need to be discerning. Start to work out which experts you want to follow, and where you can follow them. Look for reputable newsletters, leaders, online courses, and communities that align with your interests and needs. Consider using the calculators from your superfund or a reputable site like Moneysmart to help you better understand your money, before you get advice. Make sure you know a little about what you’re asking, before you ask an expert, in case they dont know what they should.

3. Network with peers and experts: Find people who are navigating the same transition. Whether through local groups, online forums, or even social media, connecting with others can provide insights into how they’re adapting and what’s working for them. (The Epic Retirement Club is a great place to start). It’s such a powerful thing to be able to ask someone ‘how they’re doing it’.

4. Stay skeptical of ‘Old Wisdom’: While it’s important to respect experience - really important! Don’t be afraid to question whether the advice you’re getting is still relevant, and moving with the current trends. The world is changing quickly, and what worked 10 or even 5 years ago may not be the most appropriate approach today given changes to longevity data, health advice, changing financial legislation and a world that has fundamentally shifted. You need to have your wits about you when people ‘guide you’ or ‘advise you’ using their own self-help insights - because often times, they come from good intentions, but they are incorrect.

5. And finally, and most importantly, accept you must be wise enough to be your own advocate: Whether it’s in health, finance, or lifestyle choices, you need to know enough about what lies ahead so you know what ‘good’ is and fight for it. Don’t rely solely on professionals who may not have the time or up-to-date knowledge to guide you fully. Instead, do your own research, ask questions, and seek second opinions and look for advisers and guides who stay as current as you need them to be.

Moving towards and into your epic retirement doesn’t mean you stop growing and rely on others to instruct you —it’s about shifting your focus and driving your ability to self-help into better shape for the challenges and opportunities ahead.

I’m almost half-way into writing my next book (called Prime Time) and I am pretty happy with how it’s coming together! A rainy week this week has kept me indoors and focussed all week so far. The finance section is almost done - a huge weight will be lifted when I get there. Just the examples to go - which is why I felt inspired for this week’s newspaper article below. The examples, when you calculate them out, for people in their 50s today are pretty inspiring (especially if you’re a proactive person). I wish we could get to everyone earlier to help them plan for retirement, and excite them about their prime time of life. When you see how disciplined retirement savings work, you see it really is worth planning for.

The Epic Retirement Flagship Course for Spring is underway and our week one has been dazzling with excited newbies and week two content has now dropped into the portal! Many thanks to Mark Lapedus who joined us for this week’s live Q&A event. Terrific insights on longevity. I love the first week of the course. Everyone is so hungry to learn everything all at once. There will only be one more course this year - our Summer edition starting in October. We’re taking expressions of interest on the website, and we’ll drop the dates and details out soonish so you can book a place! Register now for more info - it’s obligation-free to do so.

The Epic Retirement Club Facebook Group is certainly keeping us busy! It has blasted through 95,000 people in it all of a sudden, from all over the western world - which is great for all our curiosity on living life well. And our moderation team has expanded too. Many thanks to everyone who has been an active part of the conversation, helping people to navigate their pre-retirement and retirement experiences. And huge thanks to the mods! You all rock!

I’ve been training for my trek of the Three Capes in Tasmania in less than three weeks. 50kms in four days! Like a good first-time hiker, I’ve got new hiking boots and I’ve been walking Mt Cootha in Brisbane a few times a week - probably not a scratch on the four days of hiking ahead. But it’s getting me excited. Thanks for all your letters about what I’ve signed on for.

Have a great week ahead. You can always email me at bec@epicretirement.com.au. I love getting your letters. Until next week… make it epic!

Many thanks! Bec Wilson

Author, podcaster, guest speaker, retirement educator … Visit my website for more info about me, here.

Nervous about retiring? You might be better off than you think

Nervous about retiring? You might be better off than you thinkExtract of article published in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 18th August 2024.

The above-average Australian approaching retirement is doing quite well, yet many don’t consider themselves wealthy, and they certainly don’t feel confident about how they’ll pay for their retirement.

If you’re in your midlife, heading towards retirement and feeling a bit nervous, you’re not alone. Even if you’ve done everything right – built up a solid super balance, paid off your home and kept your financial ducks in a row – it’s easy to feel uncertain about what the future holds.

The reality is, there’s a whole raft of pre-retirees and midlifers in Australia who are above average in the wealth stakes, yet still don’t feel as secure as they should.

Let’s take a look at some numbers to help you build your confidence. Currently, the average super balance for a 55-year-old male is $359,100, and for a 55-year-old woman, it’s $233,200. Those figures are the highest they’ve ever been for people at this age.

If you’re one of the 70 per cent of Australians who live as a couple, that gives you a combined super balance of around $592,100. Not too shabby, right? What you may not realise is that your best growth years are probably ahead of you, and if you keep working, that number can really only go up.

Retirement income is calculated as household income, so couples naturally have more to play with. Singles, on the other hand, may feel the pinch a bit more. But even then, they’re often better off than they think when they understand how money really works after retirement.

One of the biggest misconceptions about superannuation is that it stops growing once you retire.

There’s another reason you might be wealthier than you feel: nearly 80 per cent of 55-year-olds in Australia today own their own homes outright or with a minimal mortgage: usually between 0.6-0.12 of the property’s value at this age.

Considering the average Australian family home is closing in on $1 million, that’s a pretty significant asset under your belt. In addition, more than 1 million over-50s own rental properties. They’re the largest group of landlords in the country.

In my experience, there are three things most above-average but not wealthy people discount that, if they understood better, might ease their minds.

Read the rest of this article here in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 18th August 2024. It also appears in the print editions today.

A practical guide to living alone and loving it

A practical guide to living alone and loving itIn this episode, I sit down with Jane Mathews—author, advocate for solo living, and proud single woman—to chat about her book, Living Alone and Loving It. We dive into the perks and pitfalls of living solo in your Prime Time, and let me tell you, nothing’s off the table in this conversation! While the book might have been published a few years back, its insights are just as relevant for today’s Prime Timers.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

August 10, 2024

Special edition: The top performing super funds in the retirement phase 2024

In this edition:

Article: The highest performing superfunds in retirement phase

SMH/The Age: The best superfunds for when you retire

Prime Time: A podcast discussing the best superfunds for when you retire with Ian Fryer

From Bec’s Desk: No space!

Special edition: The top performing super funds in the retirement phase Aussie retirees can't use public benchmarking to compare their retirement phase super fund's cost or performance. There’s simply no data in the public domain that benchmarks the performance of retirement phase funds investment returns or fees.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Today, I have a special edition of the Epic Retirement Newsletter for you. We're featuring exclusive data from research house Chant West on the performance of Australia's retirement-phase superannuation funds over both 10 years and 1 year for the financial year ending June 2024. This will help you review how your fund is performing in the retirement phase and assess whether you need to take action.

The terrific news is that retirement phase funds are outperforming accumulation phase funds handsomely. These key data points from Chant West tell the story.

Performance of growth funds over 1 year:

Median 1 year performance of the top 10 growth funds in accumulation phase (61-80% growth assets): 9.1%

Median 1 year performance of the top 10 growth funds in the retirement phase (61-80% growth assets): 10%

Performance of growth funds over ten years:

Median 10 year performance of the top ten growth funds in accumulation phase(61-80% growth assets): 7.2%

Median 10 year performance of the top ten growth funds in retirement phase (61-80% growth assets): 5.8%

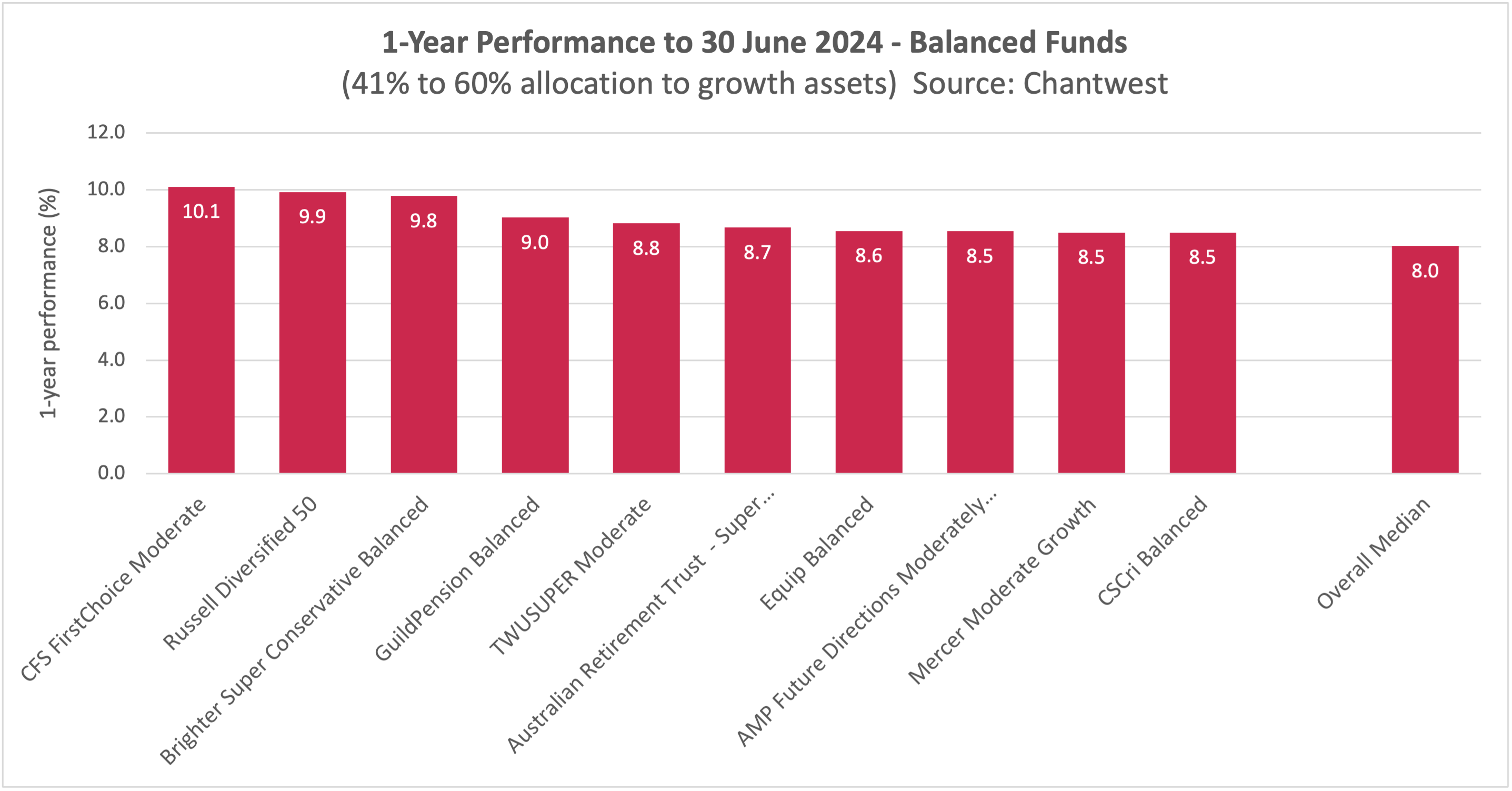

Performance of balanced funds over 1 year:

Median 1 year performance of the top 10 balanced funds in accumulation phase (41-60% growth assets): 7.4%

Median 1 year performance of the top 10 growth funds in the retirement phase (41-60% growth assets): 8%

Performance of balanced funds over ten years:

Median 10 year performance of the top ten balanced funds in accumulation phase(41-60% growth assets): 8%

Median 10 year performance of the top ten balanced funds in retirement phase (41-60% growth assets): 6.4%

But there’s a lot more to talk about than the medians.

In the accumulation phase, the government offers a national benchmarking system called the YourSuper comparison tool - which is accessed via the ATO website. On this website you can compare the annual and long-term returns for ‘default’ (or standardised) superannuation products offered by all the superfunds.

In retirement phase, there’s simply no government benchmarks for assessing performance and fees. This makes it challenging for retirees to evaluate their retirement phase funds.

Most people don’t realise this. In fact, many people simply don’t understand how the retirement phase of super works at all.

What is the retirement phase of superannuation?It might surprise you but there’s only 1.3 million people in Australia who have elected to join the retirement phase of superannuation, even though there’s more than 4.2 million people who call themselves retired in the census today. That means millions of people are electing not to draw down their superannuation as a tax-free income stream. Many of these people simply don’t understand how it works. Some have decided that it’s not right for them.

The retirement phase of superannuation is something you have to kick off with your superannuation fund by filling out a form, and opening a retirement phase account. To qualify for the retirement phase, you need to meet the conditions of release, and there’s two to consider, depending on your age.

You can access your super once you reach the ‘preservation age’ (now 60 for all Australians) and retire from your job. (Note - you can commence other work after).

Or, you can access your super and keep working unconditionally from the age of 65.

Once you enter the retirement phase, your superannuation is income tax and capital gains tax free, saving most people about 15% in tax in comparison to the accumulation phase. This is then seen in the performance metrics of superannuation funds, which have a like-for-like higher performance in the retirement phase, simply due to the tax free status of the members.

How do you define good performance?Superannuation is a long term investment. It is a system designed to encourage you to save money in the accumulation phase, invest it well in good long term investment options, with low fees and watch your money grow through compound investing. Then, when you retire, you move it into the retirement phase, re-evaluate your risk profile now that you rely on it for income, and start to draw down. You can draw down in three core ways - using an account based pension (income stream); an annuity; or a lump sum.

Once you enter the retirement phase, you have to drawdown a percentage of your balance every year, based on your age.

Most people only change superannuation funds a couple of times in their lifetime, and only if their fund is not achieving their goals. When we evaluate funds we need to look at the things that really impact us:

The investment performance of the fund: When we consider the investment performance of our fund, we need to ensure we are comparing apples with apples. We need to know whether we are in a growth or a balanced fund, and how that specific investment is performing versus the competition over the long term - a ten year window is a good benchmark to consider. You can also look at the one year numbers - chiefly for entertainment to see who has done well in the year just gone, but always remember that a fund can strike it lucky in one year, but holding consistent, long term returns is what we are all here for.

The fees you are paying: The fees you are paying your fund are fundamental to consider, and they are often difficult to benchmark because there is so many different line items on a statement and so many differences to the way they are charged. When you look closely, a fund usually divides their fees out into two categories: administration fees and investment fees. We need to look at the total of both to benchmark our funds properly. Always exclude insurance when considering your fees as these are specific to your policy choices. You’ll also need to be cognisant of comparing your fees on the same sized balances as fees are usually lower on higher balances as there is usually a fixed component for administration and a variable component for investment costs that scales with the balance.

We have benchmarked the fees this year for the growth option, so you can see the administration fees, the investment fees and the total fees on the top ten performers - for a bit of insight.

So, to understand whether your fund is performing, you need to look at the long term performance, the fees they are charging as a percentage of your balance. You also need to consider the services they offer you as a member in my opinion.

Now let’s talk about the performance of funds this year, and over the last ten years, and explore who the real high-performers are.

We’ve gathered the data on the two most popular asset allocations:

GROWTH - which represents funds with a 61-80% allocation to growth assets; and

BALANCED - which represents funds with a 41-60% alloocation to growth assets.

The data on performance shows performance below shows net of investment fees over 10 years and 1 year at 30 June 2024.

One year investment horizonIn 2023/24 there’s been a real changing of the guard in which funds are outperforming on a one-year basis. This time last year eight of the top ten growth funds on the 1 year performance chart were industry funds. This year there’s just two industry funds in the top ten.

Growth

Balanced

Ten year investment horizon

Ten year investment horizonThe ten year performance metrics tell a very different story to the one-year. The top ten performing funds over the last ten years has not changed much in the twelve month. Our highest performing super funds over the longer term have continued to hold onto their top positions as best performing funds, with just a little bit of movement between positions.

Growth

Balanced

Fees

Fees Super funds usually report their performance and charges annually on your statement. They are required to publicly report the fees on their default accumulation funds on the YourSuper website.

The most important lesson on fees that I can give you in the retirement phase is to evaluate your fund’s investment returns net of the investment fees - that is, remove them from the total returns. If your fund is charging a big fee to manage the investments but getting you a great return on your investment net of fees - what do you care? Applaud them.

The fee you really need to keep an eye on and benchmark is the administration fees. To work this out I recommend you add together all administrative fees from your fund and calculate the percentage fee relative to your account balance. By doing so, you can gauge how your fees compare to the norm.

Many funds impose fees as a fixed dollar amount, regardless of your account's size. Generally, as your account balance increases, your fee as a percentage of the total balance should decrease.

Chant West have provided the data on the fees as a percentage of the balance for growth funds with a balance of $250,000, the median balance for Australians at retirement today.

Thinking about your risk appetite in retirement

Thinking about your risk appetite in retirementAs shown in the data above, I've provided two levels of risk in the benchmarks. This is because, as we enter retirement, many people's risk appetites change. They often shift from being eager to embrace risk and reward to being more cautious about market downside risk. Take some time as you head into retirement to consider whether you want to remain heavily exposed to growth assets or adopt a more balanced approach. There’s no right answer—only your answer. Consulting with a financial planner can also provide valuable insights.

Knowing the performance of funds, what actions should you take?If you want to take a deeper dive into your retirement phase superannuation’s performance and fees, here are three essential steps:

Review your own superannuation statement:

Compare your fund's returns against the ten-year returns for balanced funds if your fund has 41-60% growth assets, or growth funds if your fund has 61-80% growth assets.

Look harder at the fees:

The fees that really matter if you’re watching them are the administration fees. Most funds have these under control these days - but keep an eye on them for good measure. Compare these fees with those charged by the top ten companies with similar account balances to see if yours is on par, lower, or much higher.

Assess your risk appetite:

Consider whether your current risk appetite is suitable for your life stage and goals. Adjust your investment strategy if necessary.

If you're uncertain, seek financial advice from your super fund or an independent financial adviser.

The best superfunds for when you retire

The best superfunds for when you retireExtract of article published in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 11th August 2024.

The data is in on the best performing superfunds for the year ending 30 June 2024. We know, from widespread media reports, that the top ten accumulation phase funds holding 61-80% in growth assets saw a median one year performance of 9.1% and the top ten funds holding 41-60% in growth assets, called balanced funds, saw an average of 7.4% returns in the accumulation phase. And that over 10 years, the top ten growth funds in the accumulation phase averaged 7.2% and the top ten balanced funds averaged 5.8%.

But what noone is talking about is how retirement phase funds performed over the same period and over the longer term. It’s like retirees don’t exist in the superannuation conversation. But they do. There’s nearly 5 million people at retirement age in Australia, so, talking about how their super funds are performing and what good looks like is quite an important conversation. Today the analysts at Chant West, one of Australia’s superfund analysts have helped me to take a deeper look at the performance of retirement phase funds. And the numbers are exciting.

This article continues…

Read the rest of this article in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 11th August 2024. It also appears in the print editions today.

The best superfunds for when you retire with Ian Fryer