Bec Wilson's Blog, page 7

July 13, 2024

Are you guilty of these five midlife money myths

Feature: Letter: Making the most of your retirement while caring for ageing parents

The Age/SMH: Are you guilty of supporting these five midlife money myths

From Bec’s Desk: A quick one

Prime Time: How to get your hands on a Retirement CASH Bonus

But first, a little promo for our upcoming Epic Retirement course…

The six week How to Have an Epic Retirement Flagship Course - Spring Edition is now open for earlybird booking. Our six-week get-ready-to-retire program, hosted and run by Bec Wilson kicks off on the 8th August.

You can download a detailed brochure here. Or, click here to book your place.

Find out more about the course

Hi Bec. I love the podcasts and get a lot out of it. However as a 66 year old retiree , I like many of my friends spend my time caring for my ageing parent and parent in law who wish to live at home , "independently" . This is not the epic retirement I envision but one I may be left with for many years to come. Could you do an episode on how to make the most of this situation as I feel it would be very useful to a lot of people who I know for sure are in exactly the same boat.

Thanks, Lorraine

A great letter Lorraine. Indeed I think many people struggle with this. So I’ve done a longer feature on it.

Letter: Making the most of your retirement while caring for ageing parentsWe all dream of a retirement jam packed with leisure, travel, and long-awaited free time to pursue some passions. But the reality of long lives also means our parents are living longer, and at some point they can become quite a responsibility. While it might not be your vision of an epic retirement it really can be a precious gift to be able give a caring parent a good old-age. The key is to find the ways you can make the most of your situation, ensuring your wellbeing is still a priority, and you properly set yourselves and your loved ones up with some balance, if you can.

There’s a few points to consider, even if you planned for this.

Get your head around the new normalAll-too-often we recognise the decline in health of our loved ones a little too late to get them into suitable housing or access to care packages that will support them in an ongoing manner, leaving them dependent on us for their final years.

Whether your caring role was planned or unplanned, it can be tough to work through the animosity you feel for the caring process interrupting what were meant to be your best retirement years. But reframe it. It really can be a precious time, caring for those who have cared for you all your life. And there are ways to get some of your dreams in too. You just might have to delay or reframe them.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Prioritise self-carePlease put your own physical and mental health first. Ensure you maintain regular exercise, eat a healthy and balanced diet, and ensure you get adequate sleep. Your body’s health is paramount. You don’t want to blame these months or years for it going down hill and resenting that later.

Then, really take action on things that are good for your mental health like reading, gardening or spending time with your friends. Don’t hesitate to seek out a counsellor or support group to help you navigate the caregiving role which at times can feel overwhelming and lonely.

Create a support networkThere’s a few steps to this one. First, getting other members of your family to take on some of the responsibility. Balance it equally if you can. And second, to put in place professional support so you can get a break.

a) Involve others in the family: Be purposeful in engaging other members of the family in the caregiving process. This allows your load to be lighter, and it’s also good for the whole family, strengthening the bonds. It can be tempting to martyr yourself if your siblings are not as engaged with the caring process, but this will just make it much harder for you to achieve balance in your life, so please resist it.

b) Seek paid support and respite care: Look around for appropriate professional caregivers who can come to the home; as well as respite care options so they can go and stay on-site under professional care for short periods. This can allow you to plan for short breaks to recharge, or even to take a 1-2 week holiday if your loved one's health is manageable.

Foster some independenceEncourage your parents to maintain their independence as much as possible. This not only benefits their mental health but can also reduce your caregiving burden. Small adaptations to their home can make a significant difference, such as installing grab bars, improving lighting, and ensuring easy access to frequently used items. Embrace care in the home, meals that are home-delivered, and even get discuss with the idea of visiting respite care for a period of time if you are unable to come and help. (I know, it’s often not that easy - but try).

Stay actively connectedAll too often we retreat from our social circles during difficult times. But I urge you not to. Maintaining social connections is crucial for both you and your parents. Encourage them to stay engaged with their friends and community and support them to do so. For yourself, continue to nurture your social life. Regular interaction with your friends can give you something to look forward to and can provide a much-needed break and emotional support.

“You could even set yourself a little challenge, setting yourself a future goal to travel to a foreign-speaking country you’ve always wanted to learn the language of, and using the time you are caregiving to take language lessons.”

Create and cherish the moments/ consider a collaborative projectI love this. One of our Epic Retirement community members said he spent some of the latter years of his father’s life tracing his family history, sharing his discoveries with his dad as he did it. They would talk, pore over photographs and news clippings and capture old memories. And not long before his father died, he published it into a printed book. He treasures that time spent together now.

While caregiving can be challenging, it’s also an opportunity to create lasting memories with your parents. Cherish the small moments of joy and connection. Whether it’s a shared meal, a walk in the park, or simply reminiscing about the past, these moments can be incredibly rewarding.

Seek out types of fulfillment you can achieve nowAdjust your expectations of retirement for now. Your parents or loved ones won’t need caring forever, and if they do, you’ll eventually find more permanent solutions. So while you are in this phase, make some new, temporary plans and seek fulfillment in new ways. This might include learning a new skill, take up a weekly volunteering gig doing something you’re passionate about, or starting a small project. You could even set yourself a little challenge, setting yourself a future goal to travel to a foreign-speaking country you’ve always wanted to learn the language of, and using the time you are caregiving to take language lessons. You can do this on an app like Duo Lingo at home, or join a local language school and make friends with others doing the same. Whatever you do, make an effort, in the same way you would chase your epic retirement, to find activities that you can integrate into your caregiving routine, allowing you to pursue your passions without compromising your responsibilities.

It’s not going to be easy, but it won’t be forever, so make some temporary plans and keep on working towards that epic retirement. It’s just going to take a different course to the way you originally envisioned it.

Add to the comments some of the lessons you’ve learned if you’ve been trying to balance your epic retirement dreams with caring for a loved one. This article was published as a separate piece before being included in the newsletter, comment here.

Are you guilty of these five midlife money myths?

Are you guilty of these five midlife money myths?This article was published in today’s The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

Midlife can be a challenging period when everything seems to weigh heavily on us. Most people in this stage are at the top of their game and under pressure to keep rising. They’re earning the biggest bucks they’ll ever earn.

But they’re also likely saddled with the tail end of the largest mortgage and the most financial responsibilities they’ll ever carry.

They’ve got teenagers or young adults in their home, ageing parents looking for support, a partner they barely find time for and a career they have to keep looking invested in. And they feel the pressure of planning for retirement, too. No wonder so many of us end up in midlife crisis.

To put some light in the tunnel, while running on that wheel, many midlifers take shortcuts and avoid having to do the hard work required to be financially successful into the next stage of life.

There’s lots to choose from – taking on risky investments, hoping for high returns without understanding the market; operating without a budget and spending on ‘whatever we need’; using credit cards to cover shortfalls in income. Then there’s my favourite: putting off retirement saving to free up cash flow in the short term.

But these quick grabs rarely lead to financial stability. And they certainly don’t help you set yourself up for the future.

Instead of falling for these myths, let’s bust them wide open and focus on what truly works for a healthier, wealthier and wiser second half of life.

Myth #1: I don’t have time to focus on my moneyMost people in midlife face a common challenge: they don’t prioritise making time to focus on their finances. This lack of attention costs them. They miss the opportunities to understand how financial systems work in the second half of life, set goals for their future and consistently practise the right things to build their wealth.

Yet the changes we need to make, if made at this time of our lives, can make us truly wealthy, even if we have no wealth today to speak of.

What should you prioritise learning about? Superannuation is the big one. As you get closer to retirement age, this system can really bolster your financial security. Investing is also important, as is managing your cash flow sensibly, with a set of financial goals firmly in focus.

Myth #2: I don’t need a budgetI’m not suggesting you should be overly conservative in midlife. But choose the risks carefully and be smart.

Many people in midlife spend as they need and want to, often covering any shortfall with credit cards. In today’s challenging economy this has become more common than we might admit, leading many to find their finances spiralling out of control.

I hate to break it to you: if you want to plan for the future you need a budget. Your budget is the framework that tells you the truth about your spending habits – how much you spend on your cost of living, how much you spend on discretionary items and how much you spend on your lifestyle.

Once you have a budget in place you need to work out how much you have as surplus in that budget every month, after paying your mortgage and your other debts. And finally you need to look hard at the numbers and evaluate whether you should reset the way you spend and save money.

It’s really tough to do when things cost so much. But, as you’ll see below, saving is important in midlife.

Myth #3: Everyone has a new car and drinks fancy wine – I should, tooIf you live in the suburbs of a big city it might feel like everyone around you has a new car, a selection of stunning, posh-brand jeans and a passion for fancy wine. I have one message for you: it’s a trap that can delay your retirement one day.

And it’s a common trap in middle-class Australia, where we want to look like we have more than we really do to please people we aspire to be connected with or want to maintain connection with.

Sadly, many people use their credit cards and debt to do this. We buy a new outfit – on credit card or, even worse, Afterpay, to look good “because they saw my blue dress at the last event” or “my jeans are so last year”.

We buy a new car because “everyone’s doing it” and we bring fancy wine to dinner to look good, or worse, we go out and eat fancy when we really can’t afford to.

It’s a hard trap to unwind ourselves from, and you need good friends to be able to do it.

A few years ago our friends got together and agreed on four principles:

There’s more to this article… You can read the rest of this article here in today’s Sydney Morning Herald. It is not behind their paywall, but you may need to sign into their website to read it.

Another week went by, and I spent it planted firmly at my desk, writing, much to my publisher’s delight. It’s been really invigorating to get back to researching new material and creating new ways of explaining things.

Week 6 of the Winter Course has kicked off - the last week - and it will all be over in a flash. That means nearly 500 people have taken the Epic Retirement Course now. I’m delighted! And the reviews and feedback are terrific, which is very humbling. If you are thinking about doing it, our Spring program is on sale. More information can be found on my website here.

On the 25th July I’ll be popping down to Sydney to speak at a half-day retirement event hosted by Financial Advisors, Wattle Partners. It’s called “Making the most of your Golden Years”. My topic is “The six pillars of an Epic Retirement”. And I’m speaking alongside a selection of very interesting people - I’m looking forward to hearing each of them. The Wattle Partners team has been kind enough to offer our Epic Retirement community free admission to the event if it interests you to come along. Here’s a link to the event website where you can register. The coupon code to use for your free pass is EPIC. Might see you there!

If you’re a radio-listener, keep an ear out. I’ve been doing lots of little radio shows throughout Australia. This week I did spots on ABC Brisbane, ABC Hobart and 3AW Melbourne too! I love it, (and I’m no longer nervous!). It’s always a hoot when we get lots of callers weighing in too.

And, in case you haven’t got a copy yet - the book, How to Have an Epic Retirement is still a bestseller on Amazon Australia. 🎉 Buy it here.

Finally, don’t forget to send me your letters. You can always email me at bec@epicretirement.com.au. Until next week… make it epic!

Many thanks! Bec Wilson

Author, podcaster, guest speaker, retirement educator … Visit my website for more info about me, here.

Today we’re talking about retirement bonuses — the one-off and quite large payments offered by an increasing number of superannuation funds to their members at retirement that almost no one seems to know about.

Last week, I covered them extensively in my Epic Retirement newsletter, and in The Age and The Sydney Morning Herald and lots of people wanted me to explain them in person.

It’s complex stuff, so I’ve invited Anne Fuchs, Executive General Manager of Advice, Guidance and Education Australian Retirement Trust, one of Australia’s largest superannuation funds, to chat with me about how they calculate theirs and how it really works.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Making the most of your retirement while caring for ageing parents

Hi Bec. I love the podcasts and get a lot out of it. However as a 66 year old retiree , I like many of my friends spend my time caring for my ageing parent and parent in law who wish to live at home , "independently" . This is not the epic retirement I envision but one I may be left with for many years to come. Could you do an episode on how to make the most of this situation as I feel it would be very useful to a lot of people who I know for sure are in exactly the same boat.

Thanks, Lorraine

A great letter Lorraine. Indeed I think many people struggle with this. So I’ve done a longer feature on it.

Making the most of your retirement while caring for ageing parentsWe all dream of a retirement jam packed with leisure, travel, and long-awaited free time to pursue some passions. But the reality of long lives also means our parents are living longer, and at some point they can become quite a responsibility. While it might not be your vision of an epic retirement it really can be a precious gift to be able give a caring parent a good old-age. The key is to find the ways you can make the most of your situation, ensuring your wellbeing is still a priority, and you properly set yourselves and your loved ones up with some balance, if you can.

There’s a few points to consider, even if you planned for this.

Get your head around the new normalAll-too-often we recognise the decline in health of our loved ones a little too late to get them into suitable housing or access to care packages that will support them in an ongoing manner, leaving them dependent on us for their final years.

Whether your caring role was planned or unplanned, it can be tough to work through the animosity you feel for the caring process interrupting what were meant to be your best retirement years. But reframe it. It really can be a precious time, caring for those who have cared for you all your life. And there are ways to get some of your dreams in too. You just might have to delay or reframe them.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Prioritise self-carePlease put your own physical and mental health first. Ensure you maintain regular exercise, eat a healthy and balanced diet, and ensure you get adequate sleep. Your body’s health is paramount. You don’t want to blame these months or years for it going down hill and resenting that later.

Then, really take action on things that are good for your mental health like reading, gardening or spending time with your friends. Don’t hesitate to seek out a counsellor or support group to help you navigate the caregiving role which at times can feel overwhelming and lonely.

Create a support networkThere’s a few steps to this one. First, getting other members of your family to take on some of the responsibility. Balance it equally if you can. And second, to put in place professional support so you can get a break.

a) Involve others in the family: Be purposeful in engaging other members of the family in the caregiving process. This allows your load to be lighter, and it’s also good for the whole family, strengthening the bonds. It can be tempting to martyr yourself if your siblings are not as engaged with the caring process, but this will just make it much harder for you to achieve balance in your life, so please resist it.

b) Seek paid support and respite care: Look around for appropriate professional caregivers who can come to the home; as well as respite care options so they can go and stay on-site under professional care for short periods. This can allow you to plan for short breaks to recharge, or even to take a 1-2 week holiday if your loved one's health is manageable.

Foster some independenceEncourage your parents to maintain their independence as much as possible. This not only benefits their mental health but can also reduce your caregiving burden. Small adaptations to their home can make a significant difference, such as installing grab bars, improving lighting, and ensuring easy access to frequently used items. Embrace care in the home, meals that are home-delivered, and even get discuss with the idea of visiting respite care for a period of time if you are unable to come and help. (I know, it’s often not that easy - but try).

Stay actively connectedAll too often we retreat from our social circles during difficult times. But I urge you not to. Maintaining social connections is crucial for both you and your parents. Encourage them to stay engaged with their friends and community and support them to do so. For yourself, continue to nurture your social life. Regular interaction with your friends can give you something to look forward to and can provide a much-needed break and emotional support.

“You could even set yourself a little challenge, setting yourself a future goal to travel to a foreign-speaking country you’ve always wanted to learn the language of, and using the time you are caregiving to take language lessons.”

Create and cherish the moments/ consider a collaborative projectI love this. One of our Epic Retirement community members said he spent some of the latter years of his father’s life tracing his family history, sharing his discoveries with his dad as he did it. They would talk, pore over photographs and news clippings and capture old memories. And not long before his father died, he published it into a printed book. He treasures that time spent together now.

While caregiving can be challenging, it’s also an opportunity to create lasting memories with your parents. Cherish the small moments of joy and connection. Whether it’s a shared meal, a walk in the park, or simply reminiscing about the past, these moments can be incredibly rewarding.

Seek out types of fulfillment you can achieve nowAdjust your expectations of retirement for now. Your parents or loved ones won’t need caring forever, and if they do, you’ll eventually find more permanent solutions. So while you are in this phase, make some new, temporary plans and seek fulfillment in new ways. This might include learning a new skill, take up a weekly volunteering gig doing something you’re passionate about, or starting a small project. You could even set yourself a little challenge, setting yourself a future goal to travel to a foreign-speaking country you’ve always wanted to learn the language of, and using the time you are caregiving to take language lessons. You can do this on an app like Duo Lingo at home, or join a local language school and make friends with others doing the same. Whatever you do, make an effort, in the same way you would chase your epic retirement, to find activities that you can integrate into your caregiving routine, allowing you to pursue your passions without compromising your responsibilities.

It’s not going to be easy, but it won’t be forever, so make some temporary plans and keep on working towards that epic retirement. It’s just going to take a different course to the way you originally envisioned it.

Add to the comments some of the lessons you’ve learned if you’ve been trying to balance your epic retirement dreams with caring for a loved one.

July 6, 2024

Could you get a retirement bonus?

Feature: Could you score a retirement bonus?

In this weekend’s newspapers: Have you heard of retirement bonuses? Here’s how to get one

The Course: The new Spring Edition now open for booking

From Bec’s Desk: By stealth

Prime Time: The outlook for investments, interest rates and inflation in the year ahead with Shane Oliver

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Could you score a retirement bonus?Are they really as cool as they sound?

Could you score a retirement bonus?Are they really as cool as they sound? The concept of receiving a retirement bonus from your superannuation fund sounds cool, doesn't it? It's a lump sum payment that lands in your account as you transition from the accumulation phase to the retirement phase. Today I want you to understand them, and I want you to be able to explore whether they are really as cool as they sound.

About 40 percent of Aussie superfunds are giving cash bonuses to their members as they move from an accumulation account or a transition to retirement account (TTR) in an effort to ‘do what’s right’ for their members. But not many people know about them, or understand how they’re calculated; and not all funds are doing them, and they’re certainly not all doing them the same way.

So this week I spoke with a few funds and dove deep into the different ways they are promoting, calculating and providing retirement bonuses, and now, I’m breaking them open in an effort to make them a little easier to understand.

As you approach and enter the retirement phase of superannuation you move from paying 15% tax on the income your superannuation fund generates in the accumulation phase, and discounted Capital Gains Tax on growth, to paying no tax at all in the retirement phase. None! Zip! Zero! Zilch! No income tax, no CGT on assets held over the long or short term. Nothing.

Superannuation funds that are invested in assets in the accumulation phase put aside money to pay those taxes. It’s called ‘provisioning’ - an accounting term. And they can build up quite a healthy tax provisioning account. But, when you move from accumulation to retirement phase, that tax is no longer required to be paid and it certainly no longer needs to be provisioned by your fund. So, the fund can either absorb the amounts they have provisioned on your behalf into that that year’s returns, and put it back into the pool to benefit all members; or they can pay that amount that has been provisioned on your behalf back to you as a lump sum or ‘bonus’ when you retire.

As I said above, about 40 percent of funds are choosing to pay it back to members from what I can tell, at the moment, the others are absorbing the provisioning back into their pooled funds to benefit all members. I expect the bonus will become more common as the retirement phase offerings of superannuation get juiced up in what is gradually becoming a competitive market, knowing many people are reviewing their superannuation fund’s offering in pre-retirement, comparing them and switching.

Many of the funds that are choosing to pay it back to you as a lump sum have cleverly turned it into a marketing opportunity, branding it up as a rather sexy sounding ‘retirement bonus, booster or reward’ or similar and hanging their topline amounts, if they can, up in lights – and good on them! They’re doing something good for you - they should be able to promote it. It’s up to you to work out whether your fund’s approach is worthy of applause.

Retirement bonuses are more tricky to understand than a simple cash handout. They’re also difficult to compare because different funds are doing them differently. And, if you look harder at them, you’ll realise that one cash windfall as you retire is not the be-all and end-all if your fund is outperforming in investments and keeping their fees down over the long term. It’s just one thing to consider in the bigger picture of what your fund delivers. Let me explain why.

How are funds calculating retirement bonuses?

Retirement bonuses are being calculated and offered in two very different ways.

Type 1: Pooled provisions

One way of doing it is by pooling all the provisioned capital gains and income tax amounts for the people who have retired during that year and, once the final tax is calculated, defining how much is in the provisioning account. Then carving that up equally to all the people who have retired during that period calculated as a percentage on the balance they move into their new, freshly opened, retirement phase account.

This is the easiest type of retirement bonus to explain and advertise - because it is offered to a member as a percentage of their balance at retirement and everyone who opens a retirement income stream gets the same percentage. The percentage amounts are revised annually. If a fund has had strong capital growth and provisioned for that tax, when lots of members roll into the retirement phase, it can leave a healthy pool. This is the approach being taken by Australian Retirement Trust, MLC and Brighter Super among others. In some ways it sounds ‘fairer’ but in reality, the people who were in high growth funds would have had more tax provisioned for them in the accumulation phase than the people who were in bonds and cash investments. So, it is not technically fair to each individual member to pay all members equally. Many funds get around this by restricting access to the bonus to only people invested in growth assets - and leave cash investors out of the opportunity to get a bonus. But, some pay all members the same, regardless of their investment types.

The percentages being offered, quite publicly by these three funds are appealing - with MLC releasing a 1.25% bonus for their 2023/4 financial year, Brighter Super offering 0.8% and ART offering 0.5%.

Type 2: Individual provisions

The other way to do it is by calculating the bonus based on each individual’s unique fund position, using a set of criteria. This is being done by industry funds like HESTA and Australian Super, taking into account which options each member is invested in at the point where they shift into retirement, how long they have been invested in their current investment options, their balance history in each investment option, how much they transfer into their new retirement income stream, and, alongside this, just like the above, considering the Fund’s tax position at the time they transfer into a retirement income stream. This sounds much harder to understand, but, in all reality, it probably allows the people who have been invested in growth assets for a long time and therefore provisioned at a higher level to receive a benefit that is larger than the person who has been more conservatively invested or only been with the fund for a short time, not building as significant CGT provisions.

In both cases the money is paid to your super account automatically, when you move from an accumulation or TTR account, and it is paid outside your concessional contributions. But there’s a few watchouts. Sensible ones I think, designed to stop people from ‘gaming’ the retirement bonus, or switching to try and get one then leaving.

All funds have a caveat that if there’s a period with negative performance, in which they won't be provisioning for income tax or CGT, they won’t pay a retirement bonus - so don’t count your chickens before they hatch. Most funds only implemented their bonuses in the last five years, so we’re yet to see this play out publicly.

They also all have an eligibility period, that is, they won’t pay someone who joined their fund in the last six or 12 months. Some funds require you to be invested in ‘growth assets’ in the 12 months prior to retirement, with many disqualifying the amounts in your account that are held in cash, and sometimes government bonds as the provisioning is minimal on these. Most funds only offer a bonus once, even if you transfer more money from your accumulation account to retirement phase later, because they are about ‘provisioned tax’ not incentivising deposits. But this is not the case for all funds with some choosing to offer a bonus as a percentage each time you roll an amount into your retirement income stream account. And finally, some funds say they will claw back the bonus if you leave within twelve months, others see this as too hard.

So what happens to the money if your fund doesn’t pay a retirement bonus? Does it mean you’re missing out?

If a fund has elected not to pay a bonus, but rather, to absorb the tax that has been provisioned for you and not paid, back into their member investment account, that’s not necessarily a bad thing. Invested well, those millions of dollars that could have been paid out to people at retirement but weren’t, should impact fund performance to the upside for all members and, over a long term period you should see the benefit of this every year in your investment returns in accumulation. This is especially relevant to understand if you have a few years ahead of you before you retire where you are really leaning on your funds performance for growth. I would expect funds without a bonus, if they have an average or above average number of people retiring in their member base, to have strong ongoing topline investment returns because they’re absorbing the benefits of tax provisions.

You won’t see this unless you take the time to review the one, five and ten year returns of your fund against the returns of funds that offer a retirement bonus into future years; and that relies on your fund being a top-performer anyway. Quite possibly, with the number of people retiring as a percentage of fund’s member bases still quite small, the impact will not be significant yet - but with massive waves of people approaching retirement in the next five years, the impact of absorbing the provisioned tax back in might be more visible.

The real consideration

The average superfund balance between the ages of 65-69, which is when most people retire, is $453,075. That would yield a retirement bonus at the highest advertised rate I can find of 1.25 percent from MLC’s Master Trust of $5663. At 0.8 percent, Brighter Super’s 2024 rate, that’s $3,625, and at ART’s advertised rate of 0.5% that’s $2265. HESTA, which calculates bonuses individually, reports an average payment of over $2,100 while Australian Super reported their average at $2,600. When asked about their top bonus payment for 2023/24, MLC reported a top payment of more than $22,800, Brighter Super said theirs was over $15,200, ART’s was $9,500, and HESTA says their largest payment exceeded $18,000.

On a real basis though, if your fund has been returning an annual return each year that is 0.25 percent higher than the funds paying a bonus; or their fees have been 0.25 percent lower - then you could be winning if you compound those returns or savings on fees in balanced or growth assets over the long term. So don’t forget to look further than the advertising. If you can get good long term growth, low fees AND a retirement bonus - then you’re really winning.

This week, my weekend newspaper column is a shorter article about retirement bonuses, limited simply by the reality that the newspaper can’t fit more than 1000 words in to it! You can read it in The Sydney Morning Herald, The Age, The Brisbane Times and WA Today here. I decided to feature a much longer version on this newsletter so you didn’t miss out on the good information I found in my research.

Have a read of the column here in The Age and The Sydney Morning Herald.

Our Winter Edition has just over one more week left. It’s gone by so fast. Gosh I love hosting it.

So this week I kick off the marketing of our next six week course - The How to Have an Epic Retirement Flagship Course - Spring Edition. It starts on the 8th August 2024. I can’t wait for the next six week program to begin. I have boxes and boxes of books and workbooks waiting to be signed and sent to our next cohort. Will you be in it?

Our earlybird pricing is now available at 25% off, but not for long. If you’re curious, you can download a brochure on the website here and read all about it. And, you can book your place so I can get your books and workbooks out as early as possible.

By stealth

By stealthWe’re creeping up the Amazon bestseller list, almost by stealth. This week we’re at #27 on the overall Amazon Bestseller list - the highest I can remember seeing it at ever! Only nineteen days until my little book turns 1 year old! Thanks for spreading the word. If you haven’t already, you can order it on Amazon here.

Another fun statistic this week. The book popped up on a list as the ten most borrowed non-fiction library books in Wagga Wagga City Council Libraries. Cool huh! I am told some people buy the book because the library list is 50+ people deep. Should be worth it I think!

I spoke virtually for a professional development session to room full of financial advisers in Newcastle, about how to make retirements more epic - thanks to the team at Allianz Retire+ for inviting me to be part of their event.

I also made great headway on the writing of my next book, called ‘Prime Time’. It’s coming out in 2025 so watch this space.

On the Prime Time podcast, I interviewed the economist I have most looked up to over my investing lifetime, Shane Oliver, the Chief Economist for AMP. We looked into his very-well-respected crystal ball at what 2024/25 holds for pre- and post retirees that are dependent on markets for their passive income sources. He had some interesting views of which geopolitical issues to watch for, and which ones matter less. And, he’s calling Australian equities positively for the year ahead with some interesting insights into where the winners and losers will be.

Finally, The Epic Retirement Club is giving me excitement chills. I feel like the people in there know more about how to have an Epic Retirement than I had ever dreamed possible. And they’re guiding and supporting each other. If you havent joined yet - don’t delay. And, if you have, invite your friends. It certainly seems like the more the merrier. Visit it here.

On top of all those wonderful work things, I had a houseful of school holiday extended family visitors keeping my kitchen busy. And, I hosted several gatherings for my husbands birthday as his week-long celebration rolled through. So, I’m feeling like my cup is full.

Now off you go and make your Sunday epic. Until next week…

Many thanks! Bec Wilson

Author, podcaster, guest speaker, retirement educator … Visit my website for more info about me, here.

The outlook for investments, interest rates and inflation in the year ahead with Shane OliverWe look into Shane Oliver's crystal ball for the year ahead.

The outlook for investments, interest rates and inflation in the year ahead with Shane OliverWe look into Shane Oliver's crystal ball for the year ahead.When a new financial year ticks around, you find that the super funds start to crow (or cry) about their annual returns. And really, what we all want to know is, ‘what is next year going to be like?’ This week on Prime Time, we delve into that pressing question. We’ve brought in Shane Oliver, the Head of Investment Strategy at AMP Financial Services and their Chief Economist, one of Australia’s most well-known and well-respected economists, to help us navigate the financial landscape.

We explore the surprising positives from the past financial year and the key areas to watch. Shane offered insights on Australian equities, inflation, and interest rates, guiding you on how to protect your savings and investments. We also dive into the impacts of geopolitics, the evolving housing market, and his view on the best asset classes for balancing income and growth in the year ahead.

Whether you're living your Prime Time, approaching retirement or already there, understanding these trends is crucial. Shane’s predictions for the next year will help you make informed decisions to maximise your financial health.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

June 29, 2024

Finding financial advice in your fifties

Letter: Finding financial advice in your fifties

In today’s Newspapers: How to retire happy and still leave your kids an inheritance

From Bec’s Desk: Still holding firm at #89

Prime Time podcast: Balancing kids' inheritance expectations with your goals of an epic retirement with Brian Herd

Finding financial advice in your fifties

Finding financial advice in your fifties

Dear Bec,

I've just found you through the Age and wanted some advice. I expect you may have been asked this before, but I wasn't sure where to look. I am a 49-year-old female with a 50-year-old husband and two kids (15 and 17). We are looking at setting up our finances for an early retirement between ages 55 and 60 if possible. We need to find someone to help us make a plan, but I have trouble knowing who to trust.

Can you offer some advice on how to find a financial adviser that specialises in retirement? I am worried that if I look to my super fund for help, they will have a bias towards their options and not be impartial.

Many thanks, Natty

Hi Natty,

Thank you for reaching out. It’s amazing how many letters I get about this. I wish there were an easy solution, but vested interests are everywhere, both among funds and advisers. Your best protection is to start yourself off with a good basic education in financial and retirement literacy and then take a step-by-step approach, validating each step along the way. If you’re looking to retire in your fifties, you’ll be expecting to self-fund a significant portion of your retirement before age pension age even arises. So financial literacy and a good base of investments is going to be crucial. Consider seeking advice from both superfund advisers and independent advisers, really learning from the process and becoming your own best judge. You’ll be looking for an advice relationship that helps you really achieve your (rather ambitious) goals.

I honestly do believe advice is critical. It’s important to know what type of advice is right for you and to think about your end goals before seeing an independent adviser. Different situations and needs require different types of advisers, who can have very different approaches to ongoing and upfront fees. I like people to consider working through it rather than rushing it. Consider my two-step approach.

Step 1: Consider using your super fund’s advice to educate yourself, evaluate what they say, then assess if you need more.

Funds usually offer intrafund advice ‘at no extra cost,’ which really means it’s included in your member fees. It’s worth using this to learn more about your superannuation and become savvy and street smart. Then use that knowledge to determine whether/when you need to see an independent adviser and what specific help you need to pay more for. Think of it as a a stepping stone in your education. In addition, you’ll get a better look at what your fund really does offer and whether you want to push to keep them in the mix in your future.

Your super fund can give you advice on your risk appetite, superannuation investments, how super aligns with the age pension at retirement, and they can review your insurances inside super. However, if you and your partner need comprehensive advice on the bigger picture or insurance outside super, and how to fund your retirement before you can access super, you’ll need to find an independent adviser.

Step 2: Understand the right type of independent advice for you.

Before you walk in, consider whether you want to be ‘switched out’ of your superannuation fund into a managed portfolio of investments, or if you want to maintain your super fund, and build investments outside super; or you just want a strategic plan that revs up your approach to saving and puts your superannuation into the right risk level for maximising compound returns. Anyone planning to retire before 60 needs to think about where they’ll invest for the years before they can access their super and how they want to structure those investments - if they plan to live off passive income before the age of 60.

While I don’t actively recommend specific advisers, as everyone’s needs are unique, I suggest a very specific approach to finding one. Start by looking within your local community to find one that is reputable. Identify the most successful people you know who share your values and ethos, and ask them who their adviser is. Seek recommendations from two or three people you respect and know personally in your area.

In my opinion, this is the best way to find someone who has ethically built their business providing financial advice up with a good reputation over time. Resist the temptation to seek advisers in Facebook groups or take advice from people who haven't invested the time and effort to establish their credibility in their community. (you’ll note everyone on the internet has ‘a mate’ that does this that they’d love to introduce you to - be very wary! Plenty of people pay ‘mates’ online for leads).

You should meet with at least two to three advisers in person when considering your options. Most, if not all, will offer a free initial appointment. Keep in mind that they won’t be able to provide you with proper advice on your situation until AFTER you’ve completed a fact find and they’ve prepared a statement of advice. This is usually when you’ll receive a quote for their services, outlining both the upfront and ongoing costs. Nothing will be done until you pay them for their upfront services. All the good learnings and advice come after that. But you have to make a choice BEFORE you pay.

One interesting thing to point out is that most, if not all advisers are tied to a dealer group, the company that provides their investment services, defines their preferred product list, and sets the standards and procedures they follow. This affiliation can influence the products and services the adviser recommends to you and the way they do business. Be aware of who this dealer group is and how that relationship works and what the limitations of their preferred product list are; and contrast that with your investment and advice objectives. Advisers, their approach, and their skills can vary greatly so some of these things help to guide you!

Here’s a much longer article I wrote about financial advice, and I even got some adviser friends to read it to see if they agreed - they did! What to expect when you go looking for a Financial Adviser. And of course, there’s a section in my book too.

Cheers, and let me know how you go! It’s a great question to ask!

Bec

Got a letter? Send it to me at bec@epicretirement.com.au.

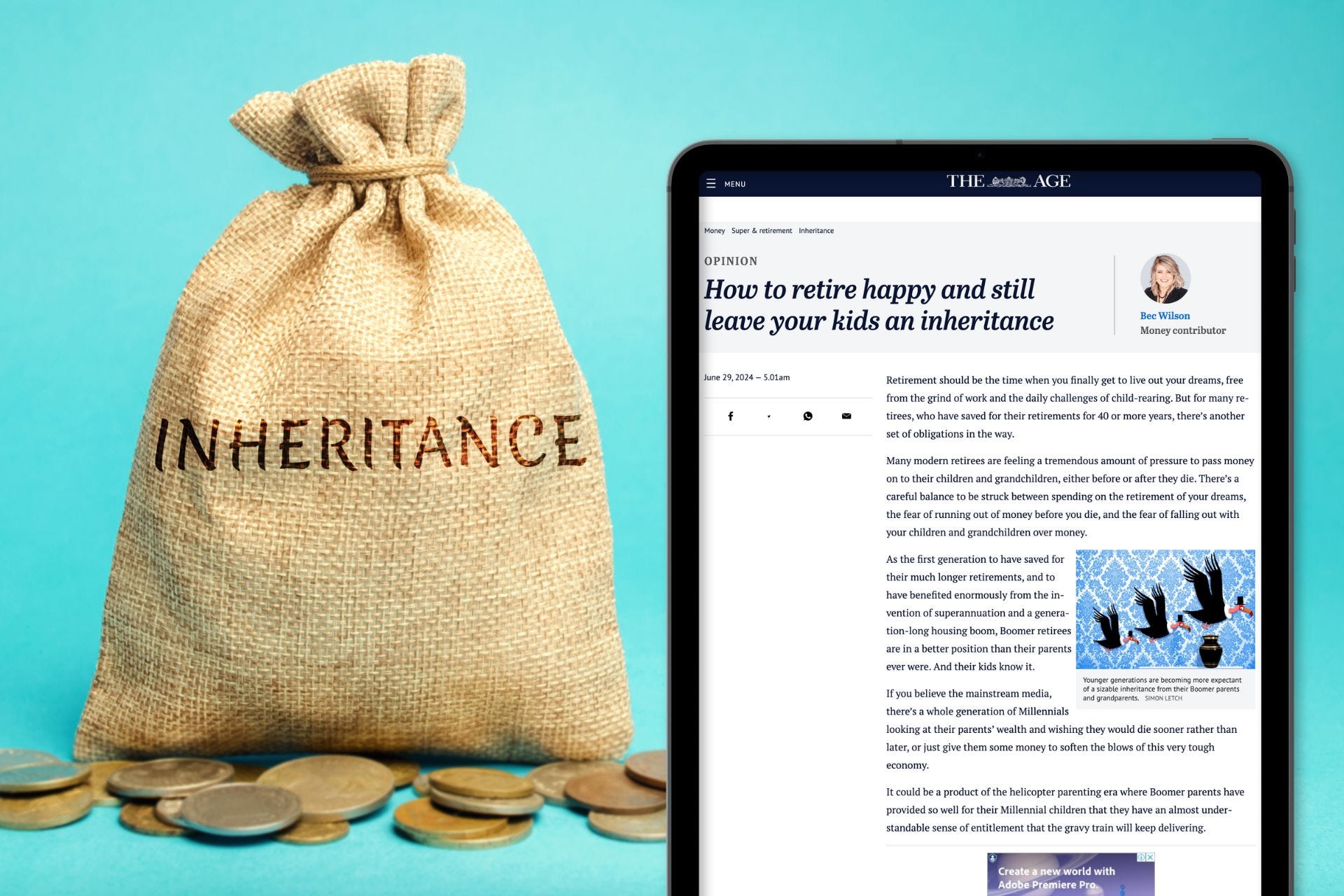

How to retire happy and still leave your kids an inheritance

How to retire happy and still leave your kids an inheritance

This article was first pubished in The Age and The Sydney Morning Herald, the Brisbane Times and WA Today, in both print and digital.

Retirement should be the time when you finally get to live out your dreams, free from the grind of work and the daily challenges of child-rearing. But for many retirees, who have saved for their retirements for 40 or more years, there’s another set of obligations in the way.

Many modern retirees are feeling a tremendous amount of pressure to pass money on to their children and grandchildren, either before or after they die. There’s a careful balance to be struck between spending on the retirement of your dreams, the fear of running out of money before you die, and the fear of falling out with your children and grandchildren over money.

As the first generation to have saved for their much longer retirements, and to have benefited enormously from the invention of superannuation and a generation-long housing boom, Boomer retirees are in a better position than their parents ever were. And their kids know it.

If you believe the mainstream media, there’s a whole generation of Millennials looking at their parents’ wealth and wishing they would die sooner rather than later, or just give them some money to soften the blows of this very tough economy.

It could be a product of the helicopter parenting era where Boomer parents have provided so well for their Millennial children that they have an almost understandable sense of entitlement that the gravy train will keep delivering.

The reality no one is pointing out is that our growing life expectancies mean most Millennials won’t receive any inheritance from the death of their parents until they are well into their late 50 or in their 60s, which is really too late to help them onto the housing ladder. So it leaves the decisions in the hands of today’s retirees.

People looking into retirement are faced with a conundrum. Do they use their hard-earned and saved money to live out the retirements of their dreams, throwing caution to the wind and expecting to spend their latter years of life dependent on the age pension and their darling children who they didn’t offer generosity to?

Do they sacrifice some of those savings, trade down some of their wilder dreams and help their kids and grandkids financially? And if it’s the latter, do they help them financially today, while they (the retirees) are alive, or do they make them wait until they die?

This week on the Prime Time podcast, I chatted with HopgoodGanim Lawyers estates and succession partner Brian Herd about how the current generation of retirees should navigate these issues. Our conversation pointed to seven big and meaningful lessons.

Find the right balanceFinding the appropriate balance between living your retirement dreams and providing some assistance to your children is difficult. This is the first reconciliation most people have to do, and in essence, it is deciding your financial philosophy.

The real legacy of your life is the relationships you leave behind and the love for one another that you have.

I suggest that people consider their own goals and happiness first, contemplating what they really want their second half of life to look like, and how much money they’ll need to achieve it, before understanding what that leaves for their children.

Not everyone has the money to choose this, but those who do should be careful with their prioritisation. You might have a long life ahead.

Throw tradition to the windIf you don’t have a lot of money and you want to live your retirement well, consider that maybe it’s time to throw some of those money-sucking traditions to the wind.

It used to be that a parent was expected to pay for the wedding, which can extend well into six figures today, a sizable portion of average retirees’ retirement budget. But we must remember that we don’t have to live life by tradition any more. No other generation does.

Acknowledge FOMO and FOFOMany parents will find themselves juggling a fear of missing out (FOMO) on their own retirement dreams and yet, alongside that, they have an immense fear of falling out (FOFO) with their children if they don’t provide financial support when it’s demanded (and demands are increasing, rather than requests, Herd says).

You’ll feel the swings of judgment and worry, but if you’re making an active choice, and you really believe in the reasons why, then it will be a lot easier to communicate.

Communicate with your familyPrevious generations got old after midlife, so we’re unaccustomed to talking about ‘goals’ for our second half. That’s something we have to get past. The only way that goals, dreams and expectations can be managed within families is through good communication.

All generations deserve to have some goals and some expectations. You might consider writing out your philosophy and retirement goals first, so you and they can be clear before discussing them with your children openly about your goals and intended actions.

My ultimate hope for you is that open discussion will set up realistic expectations and remove some of the risks of FOFO in your life.

Remember the importance of fairnessAs you look at how you dole out money to your children in life or death, remember how important it can be to offer all children fairness. The best way to do this is with transparency.

This article continues on The Age and The Sydney Morning Herald here.

Still holding firm at #89A nice warm mid winter week up in Queensland this week. Plenty of sunshine, outdoors and fresh air in between writing, teaching the Epic Retirement Flagship Course and preparing for the speeches and programs ahead.

The How to have an Epic Retirement Flagship Course has now had week four kickoff, again, very smoothly. Our live event last week for week three was with the State Manager for Queensland and Senior Financial Adviser at Ord Minnett, David Lane who answered droves of questions about SMSF investing, superannuation and financial advice. Coming up this week we have the wonderful Jon Standen from HESTA to teach us about superfunds financial advice and answer the myriad of questions on super.

Our next program kicks off on the 8th August. You can find out more and book your place here. The 25% off earlybird pricing is on now.

Here’s a bit of incidental feedback written on the wall of the course community chat this week… both of which made me smile. Thanks ladies!

“Am truly enjoying this course and recommending it to many friends and colleagues … best money spent this year!!” Claire

(in reply) “I agree. I currently have my daughter visiting from interstate. She has been nearby when I have been listening to this weeks modules and at the end there has been a lot of discussion and interest shown in the information presented coupled with quite a few "I didnt know that" comments. I have gained knowledge that I can now discuss and pass onto my children so that they can educate themselves further with courses such as this and then pass/instill those evolving lessons onto their children as they grow,” Karen.

I wrote another midweek feature for The Age, The Sydney Morning Herald, The Brisbane Times and WA Today this week. A really long and useful one. “How do you actually spend your super. Here’s all you need to know”. Find a comfortable spot and a cuppa and have a read. It’s one of those long, educational ones.

And this week’s podcast really hit the spot. I got so many emails and messages from people about it! It’s a straight-to-the-point chat with succession and estates lawyer, Partner of Hopgood Ganim, Brian Herd, about ‘balancing kids' inheritance expectations with your goals of an epic retirement’. More on this one below.

11 months went by this week since the release of How to Have an Epic Retirement and it’s still holding firm at #89 on Amazon Australia’s bestseller list! Hundreds and hundreds of books are still selling each week all over the country which is a blessing! You can buy one here on Amazon - a new batch has just arrived in warehouses. If I could ask you a favour. If you have bought it on Amazon - please leave a review. It helps for people to hear real, honest insights from people like them! And, tell your friends.

Got a letter? Email me on bec@epicretirement.com.au. And don’t forget to join the conversation in The Epic Retirement Club facebook group. It’s constantly pumping!

And that’s enough for this weekend. Have a lovely Sunday. Until next week - make it epic.

Many thanks! Bec Wilson

Author, podcaster, guest speaker, retirement educator … Visit my website for more info about me, here.

In this norm-challenging episode of the Prime Time podcast, we tackle the delicate balance between living out your goals for an epic retirement and managing your children's expectations of inheritance. This is a hot topic in the media, as many pre-retirees and retirees today face the challenge of living well while having to navigate sometimes hefty expectations of being a (significant) contributer to the financial futures of their adult children and their grandchildren.

To talk about it I’m joined by Brian Herd, Partner of the Estates and Succession team at HopgoodGanim Lawyers and author of the book, The Ageing Parent Trap. Brian’s helped thousands of families set their family plans, wills and living wills in his time. He’s also spent many years untangling family disputes over money and inheritances and managing expectations within families. So he’s got lots of valuable lessons for all of us.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

June 22, 2024

Practical advice for pre-retirees - from those already retired

It’s Sunday again and this weekend, the bumper epic newsletter includes:

Feature article: Practical advice for pre-retirees - from those already retired

In today’s Newspapers: How can super funds help us retire happy? Here are eight ideas

From Bec’s Desk: It felt quieter this week

Prime Time podcast: Explaining ETFs: How retirees use them to invest for income and growth with David Lane

First, our terrific sponsor, Viking Cruises, has got a really good deal for our Primetimers and Epic Retirees on their OCEAN CRUISES! Worth a good look.

Explore the world in comfort with no kids, no casinos and award-winning ships.

If no kids, no casinos, fewer sea days and more time in port sounds like your ideal way to cruise, then a Viking Ocean voyage is your perfect opportunity to discover more.

We take you closer to the unique art, heritage, traditions, architecture and people that define each destination and focus our energy on creating meaningful experiences that linger long in the mind after you’ve returned home.

With voyages ranging from 8 to 180 days and 2024-2026 sailings now available, now is the time to book your next ocean voyage and save up to $3,600 per couple. * T&C's apply.

Practical advice for pre-retirees - from those already retired

Practical advice for pre-retirees - from those already retiredThis article was first published on our website here.

This week, in The Epic Retirement Club (Facebook Group) there was a wonderful discussion led by our epic retirees. They were offering open and honest advice to our pre-retirees about the things they wish they’d known and acted on before they retired. There was some really terrific advice shared on the post, which was packed with long, well-thought out responses. In fact, there was so much good stuff that I thought I should turn it into a long, valuable article so it doesn’t get lost in the annals of social media. It almost makes me redundant - knowing there’s such good advice out there in our community! I’m delighted to see it matches up to lots of the things in my book too. So, here’s 20 of the best pieces of advice. Enjoy. Leave your own as comments on the newsletter too.

Think about what you’ll do once the honeymoon is over

Before retirement (I retired at 56), I thought it was a maths problem and therefore all my pre retirement planning was financial. I had a great financial plan but did not have a ‘what am I going to do plan’. After the initial honeymoon period of around 12 months, which was awesome, I fell into a bit of a heap. Even travel was not quite so enjoyable as I had not earned the holiday, unlike taking a break from work. I eventually found a great little casual part time job where I am connected with people doing something I really enjoy. And they are OK with me going away for long periods at a time. I wish I had thought more about what life would be like after the first 12 months of retirement, planned in advance, and set up a part time role. I did not appreciate that for me, working is actually an important part of a well rounded enjoyable retirement! Advice from Barry Wyatt

You retire from WORK not LIFE.

Don't be afraid to try new things even though they may be out of your comfort zone. You may surprise yourself. Advice from Robert Silvestrini

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Be aware - it’s hard to get or up the balance on a credit card once you aren’t working anymore

Increase your credit card amount as it’s impossible to do when self funded living off your super., get a interest free card to buy furniture etc - just in case. Advice from Kathryn Davis

Don’t put off the good stuff, you might not stay healthy forever

Travel lots as you never know what’s around the corner health wise, enjoy new things/people. Advice from Jean Shephard

Think about putting some structure into your days and weeks

Have an idea of how you will structure your time. From having a few regular weekly activities to having travel plans to look forward to. Advice from Jan Smith

Be proactive about keeping in touch with people from your working life

If you work in a large organisation, get the numbers of the people you respect and like the most. Stay in touch with the real people you like being around. Advice from Brendan Winduss

Be kind to each other in adjusting to retirement.

You'll most likely spend more time in daily life with your partner. Do fun things together and also maintain your own activities and friendships. Grow together and also individually as a person. Advice from Jan Smith

Have a complete health check up.

Your body is important. Advice from Lyndal Meredith

Get money into super every which way that you can

Get as much money into super as possible as it’s all tax free coming out. Advice from Robert Relph

Use your leave before you retire, rather than getting it paid out

Take all annual/long service lease as leave - super is paid on it. Super is NOT paid on lump sum payouts. Advice from Scott Malpass

Declutter

Declutter everything - the house, your finances, your super, your insurances … Advice from Lyndal Meredith

Replace things that need replacing before you retire

My brother retired at 60 but wished he had replaced things in the house. Like oven, carpets, fridge, paint inside etc. before he finished work. They cost $$$ after retirement. Advice from Astrid Thompson

Be lifestyle-ready as well as financially ready

By that I mean give serious thought to how you will fill your days when you no longer have work and you’ve been on the big trip. What will get you up in the morning and genuinely excited about the day ahead? What are your passions? Dig deep - this is the chance to find out who you are outside of work and live the real you. Have a go at some of the things you identify before you finish work to help with the transition from work to your retired life. Advice from Giulio Cerasani

Celebrate

Enjoy the fact you made it to retirement age as not all do. And, take up activities you enjoy that also keep you fit active and connected to society and try not to over think everything. Advice from Bob Dyer

Make sure you have a purpose

Retirement without a purpose has been found to reduce your life expectancy. Advice from Steve Weir

I can’t fit them all on the newsletter - so read more on a longer article on this website here.

How can super funds help us retire happy? Here are eight ideas

How can super funds help us retire happy? Here are eight ideasNever before has Australia had so many people interested in retiring simultaneously. There are over 4.2 million retirees in Australia, but only about 1.3 million have shifted their superannuation into the retirement phase.

This means most super funds are not yet accustomed to managing the needs of retirees and the outflow of funds via pensions in large volumes. They also haven’t felt the pressure to educate people about spending their money in retirement. However, the winds of change are gathering.

Seven hundred thousand Australians are projected to retire in the next five years. While this number might not seem overwhelming, when combined with the 2.9 million retirees not technically in the retirement phase who may start using their super funds as intended, the industry faces a significant shift in demand for retirement products and services.

The government has been nudging the superannuation system and funds of all kinds to prepare for this shift. In 2018, they legislated for the introduction of retirement income products to help consumers manage their money over longer lifespans.

They also required funds to have a retirement income strategy by July 2022, aiming for improved retirement outcomes for consumers. By July 2023, they reviewed the pace at which funds were implementing their strategies and pointed out that most weren’t moving fast enough.

But what does that really mean for us everyday people? According to the 2024 Allianz Retire+ Epic Retirement Planning Survey, 57 per cent of retirees said they were happy with their fund’s support of the retirement process. That number isn’t high enough.

Proactive funds are the ones actively building retirement income products, financial advice, education, and tools suited to their members.

Frankly, the government can only push funds so far. After that, it’s up to us, the everyday people who want good products and services at retirement, to take action and vote with our feet. We need to know how to identify a good super fund at the retirement phase from a less effective or even lazy one. Today, I’m going to teach you what I look for.

Here are eight things that we, as ordinary people looking to use our superannuation fund’s services in pre-retirement and retirement, should understand and watch for as our funds improve in the retirement phase. These services might not all be available now, but you’ll be able to tell if they’re making progress.

1. Investment options with competitive returns. Your fund has probably already mastered getting good investment returns in the accumulation phase. If they have, then your returns in the retirement phase at the same risk level should be higher because it’s a CGT and income tax-free phase.

You should monitor your fund’s performance by benchmarking it against the top 10 performers in the retirement phase at the same risk level every year. Finding this data can be tricky as there are no government benchmarks.

I published a report here on last year’s top performers to help. For instance, the top ‘growth’ fund in the retirement phase in 2022/23 was Brighter Super’s Optimiser Multi-Manager, Growth, with a 14 per cent return. Over 10 years – a far more important benchmark – CSCi Aggressive and Hostplus Balanced Growth both topped with 10 per cent returns, according to Chantwest.

2. Fair fees. Fees eat away at your returns and slow down the compounding of your money, but benchmarking fees in the retirement phase is difficult due to the lack of public data.

For now, you can calculate your fees as a percentage of your balance and compare them with accumulation phase fees at the same risk level using resources like the YourSuper comparison website. If they’re high, ask yourself why. Ask your fund too.

3. Retirement phase products. Most superannuation funds offer retirement phase products, the most popular being account-based pensions. Some are starting to build ‘lifetime income’ products to sit alongside these, into which you can invest a portion of your retirement savings and get a guaranteed income for the whole of your life, even if you live much longer than you expect.

It’s like having life insurance for a long life, rather than a short life. Many funds also offer term annuities and term deposits, though these are not always heavily promoted. This is likely to change as the number of retirees increases.

4. Education. One of the fundamental tenets of the retirement income covenant was ‘fit for purpose’ assistance for members approaching, and in, retirement. Education is one place where funds can really do right by their members.

When members understand what happens in the retirement phase, how money works, what decisions need to be made and how the systems of retirement support them, they can feel a lot more confident about using their money in retirement.

I project that they also make better long-term decisions because they won’t be as easily tricked by slick operators. So look twice at the education offered by your fund. Is there any? Are you using it? Does it help you navigate retirement?

5. Financial advice. Superannuation funds are waiting on government legislation to offer better quality advice to members approaching retirement. As the rules change, you’ll have access to various types of advice from your fund – some free and some paid – all of which must be in your best interest.

There’s more to this article…

You can read the rest of this article here in today’s The Age, and the Sydney Morning Herald. It is not behind their paywall, but you may need to sign into their website to read it.

Was it a quieter week? It felt like it. This week I’ve been gloriously back in my home office, focussed on hosting the 6 week Epic Retirement Flagship Course - Winter Edition which is up to week 3 already! And it’s going swimmingly. Our live event this week with Andrew Lowe from Challenger ran overtime people had so many questions about spending in retirement and safe spending levels, always a wonderful problem!

A massive delivery of Epic Retirement books has just arrived, ready for our Spring Edition of the course which kicks off on the 8th August. So if you want to lock in your place at the earlybird rates, you can now book here. There will only be one more program this year after that one… I’m going to run these just four times a year from here as a lot of effort goes in from myself and our guests. We’ll take a longer break after the Spring program before launching one for Summer.

This week I did a new national live education session for the Life-X team at Suncorp (Gen X and boomers employees), who organise their chosen staff training as a peer-group and keep asking me back (thanks guys!). This topic, by special request was ‘Travelling in your Prime Time: The travel hacks and tips every over 50 wants to know’ - such fun to deliver! And everyone wanted to know how to get great deals and amazing experiences!

And, also this week I was asked to produce a special feature for The Sydney Morning Herald, The Age, Brisbane Times and WA Today - for their midweek edition. This piece answered the big questions that most people need to understand about their superannuation. “How do I get my super when I retire? And how much will I need?” was the topic. It’s a long, practical piece. Read it here.

Finally, on the Prime Time podcast, it was all about ETFs - a popular type of investment for retirees and pre-retirees. I had one of my favourite people on the show - Senior Financial Adviser and the QLD State Manager of Ord Minnett, David Lane, who helped me with the How to Have an Epic Retirement book. The topic of the show was ‘Explaining ETFs: How retirees use them to invest for income and growth’, and that we did! He also talked about which ETFs he’s watching right now.

All in all, it felt like a quieter week - maybe because I didn’t fly anywhere - but plenty to show for it. Next week is a book-writing week. Gotta get my next one finished. It’s planned, mapped and underway (and I am rather optimistic that it’s pretty cool). This cold weather provides the perfect indoor-time.

A new claim this week - one I never thought of achieving - my book is now #1 most gifted book on Amazon in the categories of Accounting Specialties, Pensions and more - and it’s not even gifting season. And, it’s bestseller #90 on the Amazon top 100 for ALL books in all categories! You can order it on Amazon here and it’s just $22 in Australia right now.

And if you’ve already bought it via Amazon (which I know thousands of you have) - do a girl a favour and please, leave a review!

Finally, don’t forget to send me your letters. You can always email me at bec@epicretirement.com.au. Until next week… make it epic!

Many thanks! Bec Wilson

Author, podcaster, guest speaker, retirement educator … Visit my website for more info about me, here.

Explaining ETFs: How retirees use them to invest for income and growth

Today we’re talking about the very hot investment topic - ETFs or exchange traded funds. We’re going to dive into what they are but also how all generations, and most particularly, modern retirees are using them to invest for income and growth.

So this week I’m chatting with Senior Financial Adviser and State Manager for Queensland of investment firm, Ord Minnett, David Lane. And we’re truly demystifying ETFs.

LISTEN HERE:

Hey there! A quick and important noteThe content in this newsletter and this podcast is for your general information only. It’s not financial, legal, or professional advice. I do my best to keep things accurate, but there’s no guarantees. Before making any big money moves, please chat with a qualified and experienced advisor. I can't take the blame for any mishaps from relying on this information - nor can Epic Retirement, or other related companies. Stay savvy and always do your homework!

Practical advice for pre-retirees - from those already retired

This week, in The Epic Retirement Club (Facebook Group) there was a wonderful discussion led by our epic retirees. They were offering open and honest advice to our pre-retirees about the things they wish they’d known and acted on before they retired. There was some really terrific advice shared on the post, which was packed with long, well-thought out responses. In fact, there was so much good stuff that I thought I should turn it into a long, valuable article so it doesn’t get lost in the annals of social media. It almost makes me redundant - knowing there’s such good advice out there in our community! I’m delighted to see it matches up to lots of the things in my book too. So, here’s 20 of the best pieces of advice. Enjoy. Leave your own as comments on the newsletter too.

Think about what you’ll do once the honeymoon is over

Before retirement (I retired at 56), I thought it was a maths problem and therefore all my pre retirement planning was financial. I had a great financial plan but did not have a ‘what am I going to do plan’. After the initial honeymoon period of around 12 months, which was awesome, I fell into a bit of a heap. Even travel was not quite so enjoyable as I had not earned the holiday, unlike taking a break from work. I eventually found a great little casual part time job where I am connected with people doing something I really enjoy. And they are OK with me going away for long periods at a time. I wish I had thought more about what life would be like after the first 12 months of retirement, planned in advance, and set up a part time role. I did not appreciate that for me, working is actually an important part of a well rounded enjoyable retirement! Advice from Barry Wyatt

You retire from WORK not LIFE.

Don't be afraid to try new things even though they may be out of your comfort zone. You may surprise yourself. Advice from Robert Silvestrini

Be aware - it’s hard to get or up the balance on a credit card once you aren’t working anymore

Increase your credit card amount as it’s impossible to do when self funded living off your super., get a interest free card to buy furniture etc - just in case. Advice from Kathryn Davis

Don’t put off the good stuff, you might not stay healthy forever

Travel lots as you never know what’s around the corner health wise, enjoy new things/people. Advice from Jean Shephard

Think about putting some structure into your days and weeks

Have an idea of how you will structure your time. From having a few regular weekly activities to having travel plans to look forward to. Advice from Jan Smith

Be proactive about keeping in touch with people from your working life

If you work in a large organisation, get the numbers of the people you respect and like the most. Stay in touch with the real people you like being around. Advice from Brendan Winduss

Be kind to each other in adjusting to retirement.

You'll most likely spend more time in daily life with your partner. Do fun things together and also maintain your own activities and friendships. Grow together and also individually as a person. Advice from Jan Smith

Have a complete health check up.

Your body is important. Advice from Lyndal Meredith

Get money into super every which way that you can

Get as much money into super as possible as it’s all tax free coming out. Advice from Robert Relph

Use your leave before you retire, rather than getting it paid out

Take all annual/long service lease as leave - super is paid on it. Super is NOT paid on lump sum payouts. Advice from Scott Malpass

Declutter

Declutter everything - the house, your finances, your super, your insurances … Advice from Lyndal Meredith

Replace things that need replacing before you retire

My brother retired at 60 but wished he had replaced things in the house. Like oven, carpets, fridge, paint inside etc. before he finished work. They cost $$$ after retirement. Advice from Astrid Thompson

Be lifestyle-ready as well as financially ready

By that I mean give serious thought to how you will fill your days when you no longer have work and you’ve been on the big trip. What will get you up in the morning and genuinely excited about the day ahead? What are your passions? Dig deep - this is the chance to find out who you are outside of work and live the real you. Have a go at some of the things you identify before you finish work to help with the transition from work to your retired life. Advice from Giulio Cerasani

Celebrate

Enjoy the fact you made it to retirement age as not all do. And, take up activities you enjoy that also keep you fit active and connected to society and try not to over think everything. Advice from Bob Dyer

Make sure you have a purpose

Retirement without a purpose has been found to reduce your life expectancy. Advice from Steve Weir

Feel the tension dissipate

Learn to stand up straight and lose the tension in your neck. shoulders, and upper back from years of desk work. Developing a simple routine for flexibility and exercise while still working will make it more likely you will succeed and keep it up, or expand it in retirement. "A flexible spine is the key to eternal youth." If you think you are standing upright already, find a wall or doorway with no floor moldings and try to stand with your heels, butt, shoulders, and back of your head against the wall, looking straight ahead. Advice from Pat Entwisle

Let go of your working ego

To younger working people your work experience quickly becomes irrelevant, be ready to just let this go. Your working life becomes a conversation with other retirees. Advice from Geoff Smith

Get advice and have a financial plan

See a financial advisor and formulate a plan, without that there will inevitably be financial stress. When you are working out your budget make sure you allow for whatever travel and activities you want to enjoy in your retirement. Advice from Andy Will

Enjoy the small things and resist getting FOMO

You are not missing out because your priorities are different to other people’s and remember, not every moment needs to be productive - find joy in small things as it’s these smaller things that often have the biggest impacts. Advice from Glenda Rosie

Volunteer and make a difference; and keep learning

It is not too late to study and, it is a great time to get involved in political activism Advice from Eva Meland