Bec Wilson's Blog, page 9

May 4, 2024

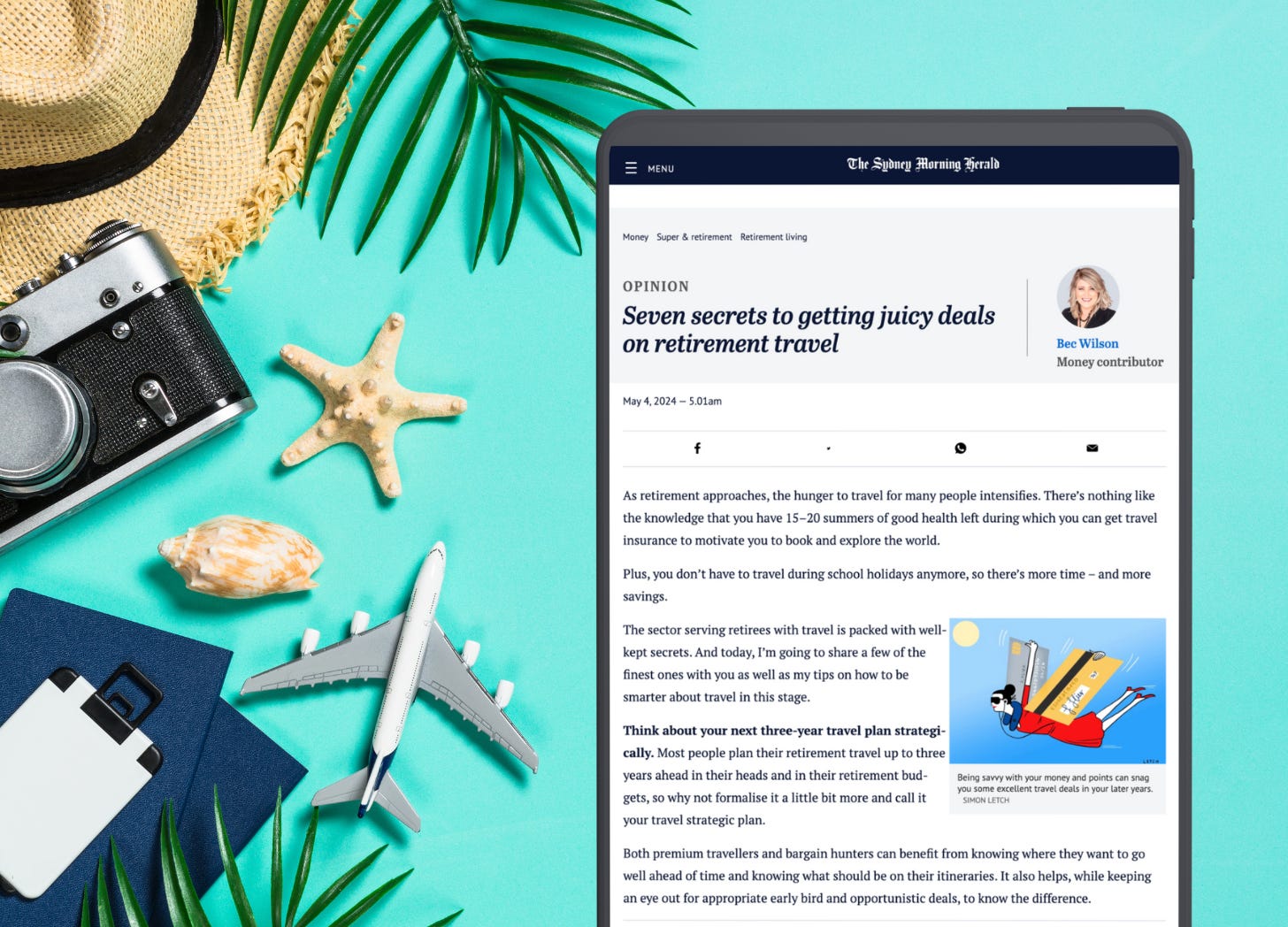

Seven secrets to getting juicy deals on retirement travel

Happy Sunday!

This week is a big week for talking about travel. The Prime Time podcast features a really interesting chat with travel industry insider, Fiona Dalton, who taught us a stack of lessons about retirement and pre-retirement travel. They’re things she’s learned as one of the true leaders in travel for prime timers and retirees over her career of more than 30 years. If you love travel and plan to book more trips, you’ll really benefit from listening.

And, this week in my column in The Sunday Age and The Sun Herald I dove in to seven juiciest secrets on how to get great retirement travel deals, and have amazing experiences at the same time.

Before you have a read and a listen, I have two little titbits:

Our Epic Retirement Housing Survey needs your input: If you haven’t taken our survey yet, please take a moment this weekend. This survey is all about your housing preferences in the second half of life. I want to bridge the gap between what you desire and what the housing and community markets offer. So, spill the beans on the kind of living spaces you envision for your future years. Many thanks to those who have already!

The next ‘How to Have an Epic Retirement Flagship Course’ is now a month til kickoff 🏝️: So get your bookings in and lock in your diary for our awesome live Q&As each week. I’m excited to show you the cover of the new workbook I sent to print on Friday… yes you heard right. We decided to offer the 150+ page workbook in print for future course participants - and they’ll be ready for the kickoff in June. The next course begins on the 6th June, and our 25% off earlybird pricing is still available (for a limited time). You can find out more about the 6 week education program, download a brochure and book your place on the website here.

Lots of people are already booked! It’s going to be awesome - just like last time! But don’t ask me… listen to the people who’ve done it before. 🥰

“I would recommend the course to anyone who has ever wondered whether they really know what a truly fulfilling retirement looks like, or could be. Thanks to what I learned over the six weeks I'm now looking forward to my own retirement with confidence and a sense of excitement that simply wasn't there pre-course.” Maryanne

“If you want to prepare for an epic retirement this is the course to explore all your options. It gets you thinking and planning on your different stages of your prime time in an extremely informative way. It makes you think about the fun stuff as well as the tough stuff in a positive way. I highly recommend this course and am now primed and looking forward to my epic retirement.” Sarah

“I found the course invaluable, the overall content was excellent covering many relevant topics for the new stage in our life to be truly epic! We have the tools and so much more knowledge which combined with your book we're on our way to the fantastic years ahead. I would highly recommend both the course and the book.” Leigh

“Great course. Great content. I found it very helpful to think about the various facets of retirement that have been raised.” Tom

Now get on and learn about how to really amp up your travel. Have a great Sunday - and for us Queenslanders, a great long weekend! Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

This article was first published in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

Seven secrets to getting juicy deals on retirement travel

As retirement approaches, the hunger to travel for many people intensifies. There’s nothing like the knowledge that you have 15–20 summers of good health left during which you can get travel insurance to motivate you to book and explore the world.

Plus, you don’t have to travel during school holidays anymore, so there’s more time – and more savings.

The sector serving retirees with travel is packed with well-kept secrets. And today, I’m going to share a few of the finest ones with you as well as my tips on how to be smarter about travel in this stage.

Think about your next three-year travel plan strategically. Most people plan their retirement travel up to three years ahead in their heads and in their retirement budgets, so why not formalise it a little bit more and call it your travel strategic plan.

Both premium travellers and bargain hunters can benefit from knowing where they want to go well ahead of time and knowing what should be on their itineraries. It also helps, while keeping an eye out for appropriate early bird and opportunistic deals, to know the difference.

It’s easy to get tricked if you haven’t done the strategic research on what’s included in offers by the major companies and what a good deal needs to be really good.

Learn the early bird booking windows. If you dream of a trip to Europe during peak season, it’s quite likely you will have to pay peak season prices. If that’s the case, the best pricing you might be able to get is the early bird pricing released by travel operators and airlines, usually nine to 11 months ahead of departure.

These early bird fares are usually released with limited capacity and a limited window for booking. Once they’re gone, the prices rise with demand.

Consider travelling in shoulder seasons to save. The one thing most retirees have is the luxury of time. It allows two things – to travel outside school holidays in the shoulder seasons either side of peak season, when prices are almost always lower, but the experience is similar. You can either pocket the savings or use that time to travel slower, really taking in the destinations of your dreams.

Know the companies that serve solo travellers well and look out for “no solo supplement” deals. More than 25 per cent of over 50s tell me they will be travelling solo. And this can be tricky when you recognise that the travel industry is built on selling rooms with two-person beds for two people to share the cost of.

Solo travellers can avoid the dreaded solo supplement by looking for the few bold companies that offer dedicated solo rooms or tours and booking early. These rooms book very quickly when released.

Several of the major cruise companies offer smaller but well-designed single cabins and some even organise collaborative dining. Some luxury hotels are offering beautiful yet smaller single rooms.

My favourite tip for solo travellers is to sign up to the email lists for tour, river cruise and cruise companies and look out for “no solo supplement” package deals. Many offer these as tours and cruises get closer to departures as a way of discounting or filling up their vacancies without dropping their in-market standard prices.

If you’re smart and opportunistic, you can snag a much better price than the standard solo supplement might offer you. Do your homework.

Understand your alternatives to “flying flat”. Everyone wants to fly business class in retirement on long-haul flights, but not everyone can afford or justify it. There are other alternatives you can consider such as booking an economy fare that gets you to Europe over a two to three-day period and includes a stopover in one of the major hubs, allowing you to rest, do a little touring and arrive in Europe without swollen legs, a crooked neck and terrible jet lag.

These packages are often some of their best fares, and if you’ve got time on your side, you can really enjoy it. Or, you might want to consider a round-the-world ticket flying you through Europe and America, allowing you a stopover on each leg for a similar price to flying to Europe alone.

Learn how to use airline currencies. There are two major currencies that airlines offer – points and status.

THIS ARTICLE CONTINUES …

Read the rest of this article on the Sydney Morning Herald or The Age.

Now let’s have some fun… poll time.

Travel is something on almost every retirement bucket list, and everyone wants to know the secrets to travelling well, getting great deals and having amazing, life changing experiences, don’t they.

Today I chat with travel expert and industry insider Fiona Dalton for her top tips, tricks and secrets for travelling in our Prime Time.

Fiona Dalton has over 30 years of travel and tourism experience running some of the largest tour operators, river cruise brands and retailers in travel in Australia. She understands the travel industry inside out, and over the years, the prime timers have been her main customers, so she going to tell us the secrets.

Fiona has just stepped into her own Prime Time, kicking off a travelling ‘gap year’ so she’s got plenty of information to share.

And please, give us a review, and make sure you download and subscribe on Apple Podcasts, or wherever you get your pods!

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

April 30, 2024

The tension of shared couple goals and individual goals at retirement - age gap included

This week’s newsletter is a little late. It’s been a big week. An awesome podcast on Prime Time will follow hot on its heels tomorrow morning too - apologies in advance for the back-to-back emails.

In this week’s edition we cover:

Feature: Letter time + The tension of shared couple goals and individual goals at retirement - age gap included

The upcoming 6 week Epic Retirement Course

From Bec’s Desk: Lots goin’ on

Prime Time: Life lessons from Australia’s most trusted GP: Dr Kerryn Phelps

Letter time!

Letter time!Hi Bec, I've really been enjoying your podcasts and all the guest speakers, you all have great knowledge and wisdom to impart.

Most information about retirement is for either singles or couples retiring within a couple of years from each other.

My question is if there's a large age gap for instance 15 years, how do we go about our epic retirement?

Hoping you can shed some light on this. Kind regards and keep up the good work.

Sheryl

Hey Sheryl. This is an awesome question. And today I’ve written a whole article about couple goals, individual goals and how these work in an age gap to get you thinking. I hope it helps! Bec Xx

The tension of shared couple goals and individual goals at retirement - age gap included

Before I dive into talking about life with an age gap, I think I should talk about the bigger picture for couple-goals in retirement, and frankly in pre-retirement too. Navigating shared goals is something all couples have to do, and it’s a really personal process and one we don’t talk about much.

Retiring as a part of a couple means a few things to me. These may differ for you.

The opportunity to do life together, sharing the experiences, hardships, joys and adaptations that makes life what it is. We share the happiness and we share the tough times too, working together to make the best of things. We share sickness and we share health - remember.

The opportunity to share the costs with someone, which, let’s face it, is a pretty good thing. We know it is easier financially to be a part of a couple in retirement, simply because so many of the costs of life are household costs. And, when we share costs, we also share assets and income, drawing on our collective savings to retire.

The opportunity to help each other fulfil your individual goals, as well as live out your shared goals. This is possibly the most tricky of the three because it relies on honest, open communication about our individual goals, and it also relies on you having a picture of yourself as an individual. It also relies on you having enough in common to build shared goals.

Knowing this, there’s a few things to work through for any couple looking ahead into retirement.

You need to think about the things you want from the years ahead.

You need to understand the things your partner wants from the years ahead too.

And, alongside this, you need to discuss and build shared visions of what you both want together.

There will be the need to compromise or agree to do things independently, if you both want different things and can’t find common ground. And, at all points, finances have to factor into the logic too.

I’m no psychologist, but years of researching your prime time and retirement years points to this time as a time of life where many people do want to ‘find themselves’ as individuals, especially if they lost themselves in the parenting and working process. And they need to individually figure out how to do this, as well as be an active part of a couple. It can cause tension.

As a part of a couple, we either figure these things out as two individuals, putting our independent selves first, or we put our couple-identity first and trade off some of the individual goals. There’s no right answer. But, I come back to each of the three points above and ask you to look at each, and how to try to achieve all three, for both of you.

It’s very much going to depend on how strong you are as individuals, how well you communicate and how fairly you compromise as to how each of you navigates this to the other one’s satisfaction and, importantly, to your own satisfaction too.

Addressing an age gap

Now let’s look at how it might impact you with a larger age gap, without emotion.

With an age gap, you may find yourselves hitting the prime time of your lives at different times. You may also hit post-euphoria or ‘passive retirement’ at different times too.

Equally, depending on the attitudes and behaviours of each person, you might not too. I know plenty of couples with a large age gap that are doing it really well. In fact, their relationships feel more active and more energetic than other people at the age of the older partner because their vibe is simply younger. But, the biology of ageing eventually happens to all of us. So, while I hate to generalise, I think you need to be aware of each of the following points, talk about them and make your decisions with them in mind:

Think about both your life expectancies, and get perspective.

Contemplate how many years each of you has in good health and when your ‘best years’ will be (your active years and your partners’ active years).

Write down what you each want as individuals in the years ahead - and what the priority for these things is (career, specific travel goals, family, other priorities).

Talk about what you want to do together, and when these things would be ‘best timed’ in life given the risks of health decline for one of you will come sooner than the other (of higher propensity would be the older person, but not always).

Maybe break those best years down into a couple of different phases you want to live out and put some timelines on each if you need to shape a more collective plan with compromises.

Then I want you to talk about what happens if one of you declines in health - will that limit both of you?

I know I’m not handing you the answer - because there is no right answer. Life’s simply what you make of it.

The Epic Retirement Six Week Course

The Epic Retirement Six Week CourseIt’s full steam ahead for our How to Have an Epic Retirement Flagship Course which is booking up super well! My publisher and I have been hard at work on the new high quality workbook which is exclusive to course attendees - and it’s ended up 150+ pages in the final typeset manuscript now it’s all laid out and almost ready. So many helpful exercises to do!

The Winter Edition kicks off on the 6th of June. It goes for six weeks. And during the six weeks you’ll get:

✔️ 8.5 hours of high quality online video education - where I deliver 14 modules of content in 100 short bite-sized videos. (People who’ve done the course say they love the bite-sized videos as they are easy to consume). This is dripped in an organised manner over 6 weeks.

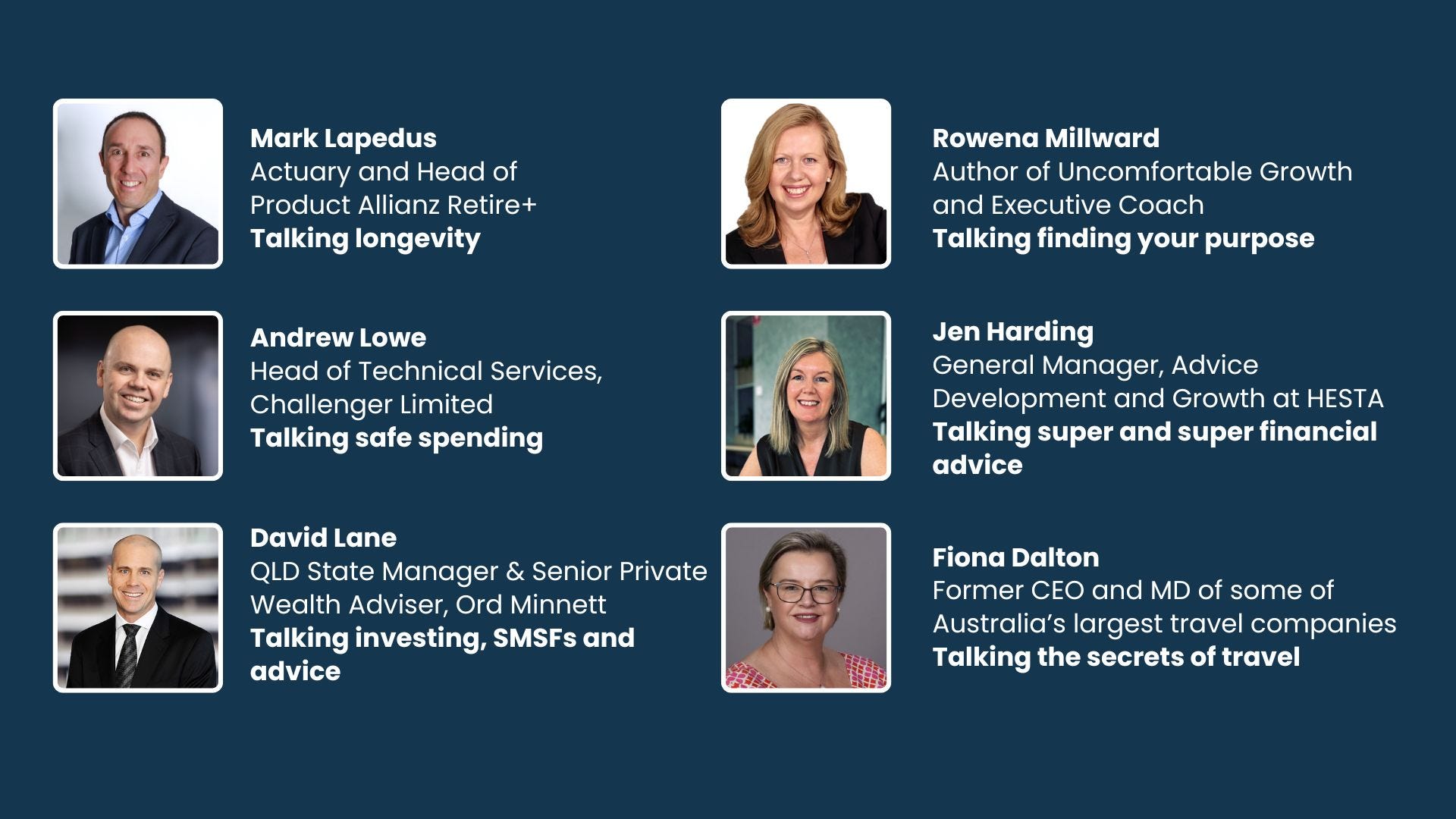

✔️ 6 live Q&As with some of the most respected experts in the areas of retirement finances, longevity, fulfilment, and travel. I know our last course attendees really revelled in these sessions, being able to ask all their questions in a peer environment and learn from other people’s questions too.

✔️ A new, exclusive 150+ page workbook.

✔️ A community zone where you can chat with others in the program.

✔️ A group online session led by Bec Wilson on finding your sense of purpose.

✔️ Plus, a signed copy of How to Have an Epic Retirement delivered to you by Australia Post too.

Our live Q&A guests are pictured here. Awesome people to chat with and learn from.

There’s lots more included…. You can download the brochure and book your place here. I am ordering books for our course attendees this week from the publisher, so get your bookings in.

There’s a 25% early bird discount for a limited time.

DOWNLOAD A BROCHURE AND BOOK HERE

Booking links:

WINTER EDITION - 6th June - 17th July 2024 - BOOK NOW

SPRING EDITION - 8th August - 18th September 2024 - BOOK NOW

Hope I see you in the course!

There’s lots of cool stuff going on. I coach a cohort of female entrepreneurs at UQ and they graduated from the female founders program last night. So I will soon have more time - which I plan to use to finish off my next book. Yes! It’s coming.

Our Facebook Group, now re-titled “The Epic Retirement Club” is growing like TOPSY! And everyone is talking! As a long-time community gal - I’m in my happy place there. Come along and have a chat - there’s so many conversations to join in on. From today I’ve promised we’re going to have a 66 day health kick because according to the European Journal of Social Psychology it takes on average 66 days to form a new habit. (Or at the very least, everyone there is going to keep me accountable 😁) It’s day-1 today! What are we doing?

1 hour of exercise a day. Ideally, some indoors and some outdoors, and, if you can use the guidelines in my book - incorporating 2 weights sessions a week and 3 balance sessions plus 150 minutes of cardio.

Nutritious healthy eating (we’re going to share ideas). I’m monitoring nutrition using a great free app called Cronometer which breaks down the protein and nutrient content.

And no booze. I don’t drink much these days but it’s all going on hold.

And come July, I think we’ll all be feeling fabulous.

I’ve also been busy writing industry papers on how the financial sector can help people have more epic retirements, which I’ll be presenting later this month. And, we’re preparing a similar view for the housing sector too… so please help me with this survey.

🏡 Take ‘The Epic Retirement Housing Survey’ 🏡We kicked off a new survey last week. And I ask you all to get in and tell us what you really want from your homes in the second half of life.

It’s a detailed survey designed to help me better understand where you want to live so I can represent that to the property sector better. This industry really wants to know what you want in the next stages of life. They have to build it after all! So dive in and help me out - please.

I’ve added a little prize too… Two people who complete the survey in full, including the competition at the end, will win a $100 VISA card (conditions apply). Complete it now.

🚗 I’m hittin’ the road 🚗I’m hitting the road for a few different epic retirement education sessions - most are open to people to come along - and when they are, I’ll share them!

I’m on Sydney ABC Radio at 2pm tomorrow talking about how to have an epic retirement. Come have a listen!

I’m speaking at the Association of Independent Retirees event in Noosa in Queensland next Saturday. Bookings are here!

And, I’m headed to Melbourne in two weeks to speak at two events:

The Australian Shareholders Association (ASA) Conference in Melbourne on the 21st May where I’ll be joining a panel for an active discussion about retirement. They’ve got a great deal for the conference + new membership for those who want to attend… check it out!

On the same trip I’m speaking at the Boorondarra library in Melbourne on the 20th May about ‘How to Have an Epic Retirement’… check it out!

So, if you’re in the region, come along. I’m also doing a few corporate presentations to ‘prime time’ staff, as a part of HR, company and industry education programs and there’s a few super fund events coming too. I love doing the speaking and educating on how to have an epic retirement - so if you have somewhere I can make some magic happen, please reach out.

Until next week! Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

In case you haven’t got a copy yet - you can buy How to Have an Epic Retirement, the book on Amazon and Booktopia and in many of the major bookstores.

Life lessons from Australia’s most trusted GP: Dr Kerryn Phelps

Life lessons from Australia’s most trusted GP: Dr Kerryn PhelpsThis week I chat with Dr Kerryn Phelps AM, one of Australia's most well-known GP's and health communicators. She's spent her life educating people about health, but she's so much more than a doctor.

Today we’re talking about how we can maintain and optimise our wellbeing in our midlife and retirement. Dr Phelps just released her new book, The Power of Balance this month. And it leads us into a really interesting conversation about how health and health advice has changed, and what’s really important today, as well as a more personal conversation about her own career in health and what she’s learned along the way.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

April 27, 2024

Why is retirement so hard?

This week, in addition to bringing you my weekly Sunday newspaper column, I’ve got a couple of things to draw your eye to so come on in…

The Epic Retirement Housing Survey is now liveFirstly, today I invite you to dive in and take our next survey: The Epic Retirement Housing Survey. I’m asking you all to get in and tell me what you really want from your homes in the second half of life.

It’s a detailed survey designed to help me better understand where you want to live so I can represent that to the property sector better. They want to know what sorts of housing you want for the years ahead.

It’s quick and easy - and you might find some of the questions really get you thinking about your home needs and wants over the years ahead. So dive in and help me out - please.

The Epic Retirement Flagship Course is back!After a really successful Autumn program, we’ve released our next dates for the How to Have an Epic Retirement Flagship Course. There’s two six week course events scheduled for coming months. And, I’m offering a 25% early bird discount for a limited time, because I want everyone to come!

WINTER EDITION - 6th June - 17th July 2024

SPRING EDITION - 8th August - 18th September 2024

I made a little video to get you excited.

What’s included in each program? Hop on over to our website to have a look.

DOWNLOAD A BROCHURE AND BOOK HERE

And finally, a quick heads up for a couple of events I’m doing in May in Melbourne which are now booking up!I’m headed to the Australian Shareholders Association (ASA) Conference in Melbourne on the 21st May where I’ll be joining a panel for an active discussion about retirement. They’ve got a great deal for the conference + new membership for those who want to attend… check it out!

And on the same trip I’m speaking at the Boorondarra library in Melbourne on the 20th May about ‘How to Have an Epic Retirement’… check it out!

So if you’re in Melbourne, come along to one of these events - and make sure you register early to get a place.

Have a lovely Sunday! Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

This article was first published in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

Retirement is really hard to navigate. But what is it exactly that makes it so difficult?

For most of our working lives, once we make life decisions, the following impacts to our superannuation and our income are automatic or even quite passive. We get a job, our employer pays us a salary that we spend on living costs and takes 11 per cent super out. We never really miss it.

It goes into a super fund which we can choose, or they’ll choose one for us, and we actively, or passively invest that superannuation to drive compound growth for our future retirement. If we don’t specify our investment preferences, our fund is obligated to invest that into a default fund which, quite frankly, has offered strong returns over the long term.

The accumulation system of superannuation has generally served all of us well. The retirement phase of superannuation presents an entirely different situation.

It’s hard to understand because none of the decisions are made for us by the system. Suddenly, each of our big life decisions demands us to pay attention and take actions ourselves. And, what makes it harder is that there’s no easy way to predict what the later-life impacts of our decisions will be without trying to use a crystal ball. So let’s look at the decisions that feel difficult.

When and how to step away from work. The decision to stop work usually drives a waterfall of other choices around superannuation. Think of this as a two-part process.

For many retirees, this is the first time they’ve managed multiple layers of passive income from a couple of different sources.

The first part is considering when to step back from full-time work, into a more part-time capacity. The second is contemplating when to give up work altogether. Each choice rolls you into a series of other choices as a result.

Whether to use a transition to retirement account in pre-retirement. Once you decide you want to slow down your work a little, you might then contemplate where to draw some top-up income from.

You might look at whether it’s smart to use a transition to retirement account (TTR) to draw from your superannuation while you continue to work while you also contribute into your accumulation account. It can be a tax-effective move for some.

When (or if) to move into the retirement phase. One of the most difficult choices is when to move your funds into the retirement phase account and start an account-based pension.

A retirement phase account is available to you after you meet the conditions of release, reaching preservation age which is now 60, and giving up work. Or you can keep working and access your super after the age of 65.

It requires you to reapply to your superannuation fund for a whole new account structure, quite a lengthy process. But on the other side, you then transfer up to the transfer balance cap of $1.9 million per person, from the accumulation phase where you pay 15 per cent tax on earnings into the retirement phase where earnings up to $3 million are tax-free.

You will be forced to draw down a percentage of your funds each year, which is 4 per cent from 60-64, and 5 per cent from 65-74 and rises with your age. If you keep it in accumulation phase, you pay more tax, but you can draw down any time and are not forced to draw down a minimum amount each year. It’s your choice.

How your superannuation is invested in retirement phase. Once you flip over into the retirement phase you need to contemplate how your retirement phase funds are invested because there is no such thing as a ‘default fund’ in retirement phase.

And there’s no way to benchmark how your funds are performing other than to get in there and look around for yourself at how the one and ten year returns and fees stack up.

How much you need – or want – to spend each year in retirement. As you approach retirement or a few years before, you’ll find yourself wondering at how much you need to live on if you were to never work again.

You’ll probably ask yourself how much of your current cost of living is essential, and how much is for things you choose to do that you might change in the next phase of life?

To answer these questions, you’ll need to build a retirement budget and a bucket list budget and test different scenarios. See what impact changes to the budget will have on your longer-term finances.

Where the layers of your income will come from in retirement. For many retirees, this is the first time they’ve managed multiple layers of passive income from a couple of different sources.

Many in retirement today will layer account-based pensions and annuities, an age pension if you’re eligible anywhere from the age of 67, and income from any rental properties or investments outside superannuation. And, many retirees still work in a part-time, casual or contract capacity adding another layer.

In addition, it’s worth pointing out that some choose to simply stay in accumulation phase and pay more tax, drawing down lump sums to fund their living expenses. So many choices!

This article continues, read the whole article on The Age, The Sydney Morning Herald, Brisbane Times and WA Today. It is not behind a paywall, but you may have to sign in.

The life lessons from Australia’s most trusted GP: Dr.Kerryn Phelps AM

This week I chat with Dr Kerryn Phelps AM, one of Australia's most well-known GP's and health communicators. She's spent her life educating people about health, but she's so much more than a doctor.

Today we’re talking about how we can maintain and optimise our wellbeing in our midlife and retirement. Dr Phelps just released her new book, The Power of Balance this month. And it leads us into a really interesting conversation about how health and health advice has changed, and what’s really important today, as well as a more personal conversation about her own career in health and what she’s learned along the way.

April 22, 2024

What to expect when you go looking for financial advice

In this edition - it’s a big one so take your time!

Survey - Take ‘The Epic Retirement Housing Survey’

Feature - What to expect when you go looking for financial advice

From Bec’s Desk - Our new course dates have been released.

The Prime Time podcast - The ESSENTIALS of a modern retirement plan

🏡 Take ‘The Epic Retirement Housing Survey’ 🏡We’re kicking off a new survey today. And I ask you all to get in and tell us what you really want from your homes in the second half of life.

It’s a detailed survey designed to help me better understand where you want to live so I can represent that to the property sector better. This industry really wants to know what you want in the next stages of life. They have to build it after all!

It’s all multi-choice so it should be quick and easy. And, you might find some of the questions really get you thinking about your home needs and wants over the years ahead. So dive in and help me out - please.

I’ve added a little prize too… Two people who complete the survey in full, including the competition at the end, will win a $100 VISA card (conditions apply). Complete it now.

What to expect when you go looking for financial adviceI got this distressing letter this week from Sally. It’s probably about the tenth letter this month that I have received about financial advice and financial advisers. So today I’m going to dive in and start a conversation about what to expect from financial advice right now. Last year I said I was going to write an eguide on the topic of getting financial advice, then the government announced one week later that they were going to change the whole structure of the financial advice sector, so that’s on hold for now. I will write one, but only once the dust settles on the new regime, which is still stuck on the path through parliament. In the meantime, I’m going to take it one topic at a time.

But first, the letter behind today’s newsletter…

Hi Bec,

Is it weird for me to think that you are my friend and you don't even know me? It's just that you and I spend a lot of time driving around chatting.. admittedly I don't tend to say much and I let you do all the talking.

Jokes aside, I wanted to drop you a note to say that I love your Prime Time podcast -- discovered after reading How to Have an Epic Retirement. I'm in my mid 50s and your book has really changed my perspective on my future from one of "aiyahhh, I can't keep up with the current pace, but I've still got a lot to do and give" to one of "springiness" (I know there's no such word - but it feels right). I'm even considering more study at my age AND realising that it is NOT a waste. When I hear folks like Bernard Salt explain the ageing demographics and Spencer Howsen open up about his financial goals for retirement, it's like a secret is out and there's a running track that will guide me to the so-called finish line.

I'm only about half way through the podcasts, but I'd love to get some thoughts from experts on how to select a financial advisor. I'm in the muck of finding one right now. One recommended firm has not been able to articulate what I will get in return for their fees. And, at $5500 for fees, that feels like I'm gambling rather than investing.

What's the average one should pay for such advice? Do you go for one-off fee? On-going annual fee? etc… When I go to my accountant and pay funds, I get a tax return done in return. When I go to a doctor, she solves a health problem. What do I get here? It's so unchartered for me. Would love some ideas.

best, Sally

This week, I want to talk about what to expect when you go looking for financial advice.

You are oh so right Sally! It’s confusing and difficult to work out what is going on in the financial advice sector and where to go, and what service you’ll get. And that’s because it is going through an extraordinary transformation right now, from being a ‘product selling’ service, which got shut down with the Hayne enquiry when they could no longer take commissions on financial products, to becoming a professional service, which ultimately usually charges for the expertise and time of the people providing it. And that’s a bloody hard transition to make as an industry.

When you go to the doctor, you go with one or two specific complaints, and you get 15 minutes of their time for about eighty bucks, and hopefully, in that time they offer you some type of solution to one problem. If you have two problems, they make you take a ‘long appointment’ and they charge you 180 bucks for 30 minutes. Then, you leave, pay for the time used, and the doctor moves onto their next patient. It’s a predictable business model that we’ve all learned how to access over a very long time. It’s transactional but your doctor ultimately builds up knowledge of you too.

Accounting is a little more complicated, but if you have an accountant, you know how much you are willing to spend to get your tax return done based on the number of hours they provide services for, or the amount of pain they take away for you. You know to call an accountant to set up a company, or a trust, to guide you on ‘tax strategy’, help with your BAS too, and you know ultimately you’ll save or make money by doing so. And if they get too expensive, you switch.

Financial advisers are on the back foot, because we don’t know how to buy what they are offering right now, and no one is taking a clear lead in telling us what to ask for or making the pricing very transparent. So it looks scary to many people. Not all advisers are good at explaining their value in simple terms either. Today I’m going to try to make it clearer. Advisers basically provide three different services, in a whole lot of different ways.

Super fund financial advice

This is the type of advice that your superannuation fund provides to review how your superannuation is invested. You can usually make an appointment with their advisers to evaluate your risk appetite and re-consider where your superannuation is invested.

Most superannuation funds will also provide you with retirement planning services, projecting how your superannuation could grow over the years ahead for each investment type suggested. If you don’t want them to dive into assets outside super in much detail, they can also help you plan for retirement and how you could use the age pension and your superannuation to generate income, and how much you can expect to safely draw down from each. The scope of superfund advice is under review. We all expect super funds to be able to offer more comprehensive advice in the years to come, but they can’t YET.

Single issue financial advice

Single issue advice is where you approach an independent financial adviser with a very specific issue, looking for one off independent advice on how to navigate it. (Super fund advice can be single issue but it often can’t take in your wider financial situation). It might be that you are about to receive an inheritance, and want to understand the most effective way to utilise it in building your future financial security; or you might want to have someone review how your household’s superannuation is invested.

Quite frankly, not all independent financial advisers like to provide single issue based advice and there’s a big reason why. They basically have to do just as much work as they would to provide you with comprehensive advice but you only pay them for a one-off hit of information. And you want to pay less, despite the amount of work involved. They figure their time is best spent getting to know clients who want to work with them, over a longer period of time.

The reality is that the legislation currently requires that advisers conduct a thorough and detailed discovery called a ‘know your client assessment” or KYC before they provide any kind of advice. And they have to document the advice process too, including their information gathering, your objectives, the advisers’ recommendations and the rationale behind them.

As I mentioned, the government is currently in the process of changing the legislation to enable banks, superfunds and financial advisors to provide single issue advice without the burdensome detailed discovery process. And, they are proposing a new tier of financial adviser be legislated into the system to provide this. So watch this space.

Comprehensive financial advice

This is where a financial adviser takes a holistic approach to your financial situation. They delve deep into your current financial position in great detail, and get to know your financial goals, circumstances, and risk tolerance to develop a tailored financial plan that helps you get where you want to go.

And the hardest part for most people is knowing what their financial goals are when they walk in the door. Because we aren’t actually taught much about this stuff and don’t know what to ask for.

We all need to bear in mind that every person approaching an adviser likely has different needs and wants. Sure, they might be built on the same basic foundations, much like seeing a GP is, but the problems you need solved are unique to you, and you need to take in the varying levels of financial hygiene people operate in before they get advice.

So when you walk in the door you might have some idea of what you want, but you might want to get clearer before you walk in on why you’re going, too.

Common reasons people see an adviser are usually one of a few things:

They want an adviser to help them focus on retirement at a point of time in the future, teaching them how they can save and invest for this window of life and usually they want to set the timer on when it will be possible. As a part of this process they want someone to understand their current financial position and draw projections on how to get them to an ideal future state, which, let’s face it, has to be mapped and agreed together if it’s going to be achieved. Then they want a view of what their ‘retirement income’ might look like when they get there too - more projections. Then, they want advice on investments too… see below.

Something happens in your life that changes everything and you need to reconsider your situation - your debt, your investments, your home and your income needs. This could be a death in the family, an inheritance, a divorce, the purchase of a new home (downsizing or upsizing), or another significant life event. And you see an adviser to help you navigate the things you should do, and guide you through the big decisions ahead. This is bigger than single issue advice, simply because many of these issues change EVERYTHING.

They want an adviser to look at their current financial situation and tell them how to get ‘on track’ for good financial health - regardless of their future retirement goals or timing. That usually means they want the adviser to help them learn to save more, use the right tax structures, and guide them on risk appropriate debt and investment strategies to have that money compound effectively over the long term.

They want someone to get to know their goals and ‘manage’ their investments so they don’t have to be hands-on. This is a tactical and ongoing process where the adviser, after developing a strategy with the client as mentioned above, then makes recommendations on where to invest, and places and manages those investments, reviewing them periodically to determine whether they are the best investments for the economic times ahead. They may also provide the investment platform and managed investing services in addition to their advice, from their company or a related company.

They want to manage the risks in their life and put themselves on a path for success. Early in our working lives, usually when we take on our first mortgage, and have a few kids that rely on us, we head off to a financial adviser to understand whether we have enough life insurance, total and permanent disablement insurance and trauma insurance. We fear something happening to us that will leave our families unable to manage, so we insure for it. As our salaries get bigger, our mortgages get smaller, and our children become independent, the amount of risk we carry might change, causing us to review our insurance needs.

We’re going to discuss the cost of advice in a minute. But before we do, I want you to think about some of the things an adviser has to work through before they can provide you with meaningful advice:

They need to understand how much you earn, and what tax you pay, what you have in assets and liabilities.

They need to understand what you spend every year, and whether that is generating any savings or surplus that can be put to use in building wealth. And, they might be able to guide you to have a better understanding of your spending and how you could generate savings more effectively.

They need to contemplate where those savings will best be deployed, considering whether to pay down debt or build up assets, and in doing this they consider the most tax effective ways of saving.

They evaluate your risk profile, and review where and how your money is invested, and whether it is getting a satisfactory return based on your own personal goals and ambitions, when compared to other options.

They need to explore what you want in the future, even if you can’t quite see it yet and try to set some markers with you of what success looks like so they can build a plan you can understand.

And, they need to understand your appetite for protecting yourself - AKA, how much you want to be insured for your death, or how much you could get in the case of your worst nightmare - that you could never work again and needed long term healthcare.

And only then, can they start building the plan and the actions you need to take to implement it. Then, once the plan is written, there’s a whole new job to be done in holding your hand on the road ahead as you implement it yourself, or managing your assets and ongoing strategy for you as the world twists and turns around you. It’s worth appreciating that a good adviser can guide you on ways to make clever tax savings, tax structuring and tax effective investment. They can help you understand how the age pension fits into your picture, and support you in making choices you might not even know exist. The value of that differs for everyone.

How do financial advisers charge and what do you get for your money?

First up I want to point out that the superannuation advice option is provided by funds as a part of your ongoing fees. That makes it look like it’s free. In reality, it is part of what you are paying 0.6-1.5% in superannuation management fees for. So if you aren’t using it regularly, you’re missing out on something you already pay for. Most funds don’t limit the number of times you can access it either, so don’t be afraid. They may charge for specific retirement services. Ask - they’ll tell you.

Next, let’s talk about the cost of independent advice. This is a lot harder to explain.

Every single financial adviser I know offers the first meeting for free. That meeting allows them to do a fact find, understanding what your problems are, and what you are trying to achieve. Then, the adviser will provide you with a proposal. They CAN’T give you advice until after you sign that proposal. When you read this proposal I want you to look for two things:

The advice fee - which is the upfront cost you are expected to pay for the deep dive into your financial situation, and the preparation of a detailed statement of advice. This is usually built out based on how the company classifies your complexity, that is, the company will have an internal classification system something like this:

Simple advice - This is some kind of single issue advice or advice on a not-very-complex financial situation that needs mapping out. You could expect to pay $1,500-$3,000 for this type of advice upfront.

Complex advice - This is the most common type of advice for people who have a significant life event and need to reconsider the impacts, if they don’t have complex investments and structures. This advice would usually cost between $3,000 and $5,000.

Comprehensive advice - This is deeply comprehensive advice that dives right into all facets of your more complex finances, your goals and your future timing. And you should expect to pay $5000-$10,000 depending on the complexity of advice and the expertise of your adviser.

Some advisers, not all, will offer the upfront advice for free if you take up an ongoing advice service, which, as you’ll see below, could end up costing you somewhere between 1.5% to 3.5% of funds under management.

Ongoing or future costs - You need to consider the reality that taking independent advice usually means you are looking to undertake independently guided investing and if you do, there will be ongoing costs. Ongoing costs are usually broken down into three areas:

Ongoing advice fees - where the adviser manages and oversees your investments, monitoring your situation and adjusting your strategy over time. Bear in mind that this doesn’t always include investment management fees. This fee could be expected to be somewhere around 1-1.5% of funds under management.

Platform fees - the cost of the platform you are investing through, which might be platforms like HUB24, AMP North, BT Panorama or Macquarie Wrap. This fee can often be in the league of 0.5% of funds under management.

Funds management fees - the costs being charged for the management of funds invested into ‘managed investments’ by an internal or external funds management team, if that is how your chosen advice firm does things. This could be in the league of 1-1.5% of funds under management at the extreme end, depending on how they do things. These costs should be detailed in your initial proposal, and will be in your statement of advice, but they might not be in very large print and you might not know what they mean. There are ways of minimising these costs, by looking for the types of advisers that guide your investment into lower-cost investment options like ETFs. However you need to be aware of, have an appetite for, and ask about this.

So how do you choose an adviser? That’s for another day. One thing I will say is you need to know why you’re getting advice before you rock up at the door, so you appreciate and get the value you are paying for.

I will declare openly - My husband and I get financial advice on an ongoing basis. Our adviser waived the upfront fee when we signed up for that service. We invest quite simply for the long term with advice in low cost ETFs and equities through a platform. There’s plenty of good advisers out there. It’s up to you to find them and work out the value they can offer you.

Sally, I hope that helps!

I have really BIG NEWS. The ‘How to Have an Epic Retirement Six Week Flagship Course’ is back! We have two new course dates that have just launched for the months ahead. And 25% off one early bird discount - for a limited time!

WINTER EDITION - 6th June - 17th July 2024

SPRING EDITION - 8th August - 18th September 2024

Both programs are identical. So it’s just the dates that differ. They include:

8.5 hours of education delivered in 14 modules (100 short punchy videos that are easy to absorb)

A NEW exclusive 100+ page digital workbook, which my publisher Hachette is preparing with me right now - ready for these new programs.

6 Live Q&A sessions with some of the industry’s most esteemed leaders. These experts got RAVE reviews last time. (See more in our brochure)

One community group coaching session to work through finding our purpose with others facing it alongside you with Bec Wilson as your guide.

An online community and the ability to do the program with a synchronous cohort, so you can learn from their questions as well as your own.

A signed copy of How to Have an Epic Retirement - the book

And, I’m offering a 25% early bird discount for a limited time, because I want everyone to come! Also, it helps me to know how many books to order - so help a girl out and book early! 😆

Our Autumn edition was a RAGING success. I’ve included a couple of testimonials below. They bring tears to my eyes. There’s more in the brochure!

You can download a brochure and book your place here.

“I would recommend the course to anyone who has ever wondered whether they really know what a truly fulfilling retirement looks like, or could be. Thanks to what I learned over the six weeks I'm now looking forward to my own retirement with confidence and a sense of excitement that simply wasn't there pre-course.” Maryanne

“If you want to prepare for an epic retirement this is the course to explore all your options. It gets you thinking and planning on your different stages of your prime time in an extremely informative way. It makes you think about the fun stuff as well as the tough stuff in a positive way. I highly recommend this course and am now primed and looking forward to my epic retirement.” Sarah

“I found the course invaluable, the overall content was excellent covering many relevant topics for the new stage in our life to be truly epic! We have the tools and so much more knowledge which combined with your book we're on our way to the fantastic years ahead. I would highly recommend both the course and the book.” Leigh

“Great course. Great content. I found it very helpful to think about the various facets of retirement that have been raised.” Tom

“I would highly recommend the Epic Retirement course to everyone planning to retire in the future, as well as those that have already retired. The information provided was exceptional, as was all of the speakers.” Susan

“It has been absolutely brilliant. I was hesitant to sign up - no clue why - but I am so glad I did.” Sue

That’s humbling huh! Huge thanks to our special guests in the AUTUMN EDITION which is now finished; and to the more than 250+ people who attended too!

I can’t wait to host the next ones. I’ve found my true sense of purpose in this! Have a great week - make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

In case you haven’t got a copy yet - you can buy How to Have an Epic Retirement, the book on Amazon and Booktopia and in many of the major bookstores.

When you think about what goes into your retirement plan, you might start with a long list of financial items, and stop at your superannuation. But there’s so much more to think about than that if you want to have an EPIC retirement.

This week, I’m joined by Peter "Grubby" Stubbs, a seasoned radio personality and a vibrant advocate for living life to the fullest. Together, we're diving into the essentials of a modern retirement plan, breaking down everything from when to retire, how to plan for your desired lifestyle, managing your finances effectively, and why it's never too early to start preparing. And boy does Grubby make it a fun and relatable conversation.

April 20, 2024

What a modern retirement plan should look like

Happy Sunday! It’s a rainy weekend in Brisvegas - so I got busy finalising our next course! And… ta daaa! It’s here.

In this short weekend edition, I’m bringing you two things:

My column which is printed in today’s Sun Herald, Sunday Age and syndicated across the Nine News network, into the Brisbane Time and WA Today.

The ripper of a Prime Time podcast I did on a very similar topic with radio legend, Peter “Grubby” Stubbs. Talking with Grubby is certainly the way to make finance topics more fun to listen to! (Well I think so - you tell me!)

And finally, as I mentioned, I’m launching the Six Week How to Have an Epic Retirement Flagship Course again, bigger and even better! We ran the Autumn Edition as a pilot for more than 250 people, and now those six weeks are done, I’m thrilled to say - people loved it. (You can read their rave reviews in the brochure and on the website!) So, we’ve tweaked, improved and updated it and developed a NEW and improved digital workbook with the help of my publisher, Hachette. And it’s back!

There’s two programs to choose from in coming months:

THE WINTER EDITION: from the 6th June to the 17th July 2024 - BOOK HERE

THE SPRING EDITION: from the 8th August to the 18th September 2024 - BOOK HERE

You can read all about the programs here, and download a brochure and book your spot now.

And, I’m offering a 25% off earlybird discount for a limited time because I want everyone to come along and learn. So don’t delay!

Now, onto your letters. I got some doozies of letters this week thank you. I am going to use them on Tuesday in a big email! I would love to keep a steady flow of them coming on the weekly newsletters. If you have a letter, email me at bec@epicretirement.com.au.

And, get on over to our Facebook group if you’re bored. I renamed it “The Epic Retirement Club” and it’s positively popping with activity this week.

Have a lovely Sunday! Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

This article was first published in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

My column in this weekend’s The Sun Herald and the Sunday Age. Also published in digital, and in WA Today and Brisbane Times.

My column in this weekend’s The Sun Herald and the Sunday Age. Also published in digital, and in WA Today and Brisbane Times. Anyone approaching retirement knows it ain’t what it used to be. Modern retirement has gone from being a time when we stepped back into the shadows to being potentially one of the most exciting phases of our lives.

But whatever it becomes that is really up to us, and how we plan for, prepare for and live it. So, today, let’s look at what, I think, should be in your modern retirement plan.

Think about your longevity firstWe’re all living longer, but most of us are still coded to picture ourselves living much shorter lives. To get our planning under way, we need to explore how long we might live first, then start to build a vision of what the years ahead of us could look like.

Smart actuaries say that today’s 50-year-olds have a good chance of living into their mid 90s, and those younger could easily get to 100 years. That says to me that we need to paint a very different picture of modern retirement in our own minds.

Build your financial confidence as well as your financial planOnce you know how long you expect to live, and of that, how long you want to spend living off more passive income streams in retirement, you should find yourself quite motivated to build your financial plan. That financial plan could have up to 11 moving parts. And I think everyone should make the effort to understand this stuff, rather than outsource it completely.

There’s building your budget for the period before you retire to nail down your cost of living, planning how much you can save. Usually people try to juggle paying down their mortgage, and trying to contribute more actively to their super as early as they can, leveraging the superannuation tax concessions available, then investing those funds appropriately to drive compound investment growth before retirement.

Then there’s thinking about your income from working and contemplating how that might change over time.

Next, you should build a budget for your retirement years, so you understand your real cost of living after retirement. Please don’t just pluck a number out of thin air. After that, you should spend some time dreaming up a list of the holidays you want to do and allocate a budget to them that you can layer on top of your cost of living budget. And finally, you need to think about your retirement income layers.

I think everyone approaching retirement should start to build a ‘dream trip list’, and talk about these trips more actively.

Contemplate whether you’ll be eligible for the age pension and really think about how much you would like to draw down from superannuation in the early part of retirement and whether that differs from the later parts.

You might also want to think about the opportunity to use the transition to retirement accounts offered by superannuation funds if you think you might want to work part-time and draw some money from super while continuing to contribute using employer contributions in the run-up years.

Finally, you must consider the way your money is invested in retirement, knowing more than 50 per cent of the money you make passively from superannuation in your lifetime is usually generated during your retirement years. Most people don’t realise this – it’s the real magic of superannuation.

Act on your healthIf you’ve got the goals and the financial plan to live well into your 90s, then you’re going to have to start thinking about the body you want in your 70s, 80s and 90s, too.

Use that vision to start working on your health much earlier in life. It’s the things you do every day that make all the difference, according to the science of healthy ageing. Be alert to creating a combination of cardiovascular, muscle mass and balance exercises to make your body strong.

Seek out a sense of purpose beyond your workplaceThis is a big and important part of planning for retirement. And it’s even more important today when you consider how many healthy years we spend living on a more passive income thanks to superannuation.

So take some time, ideally long before you retire, to explore more deeply what you are passionate about, and what your natural skills are. Then, think about how you might be able to use these in the next phase of your life, and build some social communities outside your workplace as well as inside.

This article continues, read the whole article on The Age, The Sydney Morning Herald, Brisbane Times and WA Today. It is not behind a paywall, but you may have to sign in.

When you think about what goes into your retirement plan, you might start with a long list of financial items, and stop at your superannuation. But there’s so much more to think about than that if you want to have an EPIC retirement.

Today, I’m joined by Peter "Grubby" Stubbs, a seasoned radio personality and a vibrant advocate for living life to the fullest. Together, we're diving into the essentials of a modern retirement plan, breaking down everything from when to retire, how to plan for your desired lifestyle, managing your finances effectively, and why it's never too early to start preparing. And boy does Grubby make it a fun and relatable conversation.

Whether it's continuing work in some capacity, embracing new hobbies, or planning for future financial security, this episode is packed with practical advice and insights that will inspire you to rethink the traditional concept of retirement, ensuring your future is filled with passion, purpose, and plenty of adventures.

Got something to say? Leave a comment or come over to the Facebook Group and start a discussion…

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

April 15, 2024

Letter: Tell me about 'the sweet spot'

Feature article: Letter - Tell me about 'the sweet spot'

Prime Time: We’re all going to live a lot longer, and that changes everything with Dr Andrew J. Scott

From Bec’s Desk

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

This week let’s focus on one really cool letter I received from Janet. It’s a doozy!

Hi Bec, I enjoy your column and podcast - lots of useful stuff.

I am scaling down to retirement - currently working part time - and am 62.

I had dismissed the chance that I would qualify for even a part pension in due course (at least until some of my super is spent) but I hear about 'the sweet spot'.

This seems to imply that for those of us just over the pension threshold there are options to better arrange our affairs. But is this really the case and is it worth it? I don't want to spend money just for the sake of it to qualify for not a lot...

Help - please explain the theory here.

Janet

Hi Janet, as you know I can’t give you personal advice, but I can present you with the facts on ‘the sweet spot’ and point you to where you can get more free information before you pay for professional advice if you feel you’re ready. So let’s dive in…

Where is the sweet spot between the age pension and superannuation drawdowns?This week, let’s delve into a pressing topic that many approaching retirement ask me about: the elusive "sweet spot" between the age pension and superannuation drawdowns.

Everyone with an average superannuation balance in Australia could benefit from learning about how our superannuation and age pension systems work together to create a real sweet spot.

The sweet spot represents the tipping point where people with moderate superannuation balances, and eligibility for the age pension can potentially earn more annual retirement income than those who are fully self-funded with a much larger super balance. To understand it you need a comprehensive understanding of the Australian retirement system, and how you use the age pension and superannuation together most effectively.

To understand what the sweet spot is, you need to learn about a couple of key things:

You need to understand how the eligibility for the age pension works, and how you’ll perform on both the assets test and the income test.

If the assets test is the one that is biting you, then the sweet spot discussion is an important one to learn more about. I cover both tests in the book.

You then need to understand what the taper rate is, and how it impacts age pension payments.

The taper rate is the rate that the age pension is tapered for people who trigger the full pension assets test threshold. In basic terms, when you trigger the assets test cap, which is currently $301,750 in personal and investment assets for singles and $450,500 for couples, the fortnightly full age pension rate is ‘tapered’ by $3 for every additional $1000 in personal and financial assets beyond the threshold. (Remember your family home is exempt from the assets test.)

Then, you need to work out how you might be affected.

The current full pension rates as at April 2024 are $43,752.80 for couples, including supplements, and $29,023.80 for single people. So that’s the baseline you’re reducing from.

A person or couple on the cusp of the full pension assets test cap, where the taper rate kicks in, will effectively lose $78 per year (26 weeks * $3) in aged pension for every $1000 in personal and financial assets they have over the thresholds.

A person or couple who are ineligible for the age pension would need to earn approximately 7.8% in income from their funds to achieve the same financial outcome as someone receiving the full pension, considering the tapering effect between the part-pension's limits.

People who are marginally over the assets test threshold and do not trigger the income test because their core incomes come from their superannuation or other ‘financial assets’ that are deemed, may see benefit in planning around these assets test windows.

Let’s do some sums together to show you how it works.Maya and Sunil, both 67 years old, have combined assets of $451,500 in superannuation and own their family home outright worth over $1M dollars. They are drawing down only the mandatory 5 per cent superannuation drawdown rate, which amounts to $22,575 income from super. (Remember that the income test handles superannuation as a deemed asset not actual income).

Additionally, because they are at the threshold, they would be able to receive a total of $43,752.80 from the age pension, including supplements. In this scenario, their combined annual retirement income stands at $66,327.80, closely aligning with the amount deemed comfortable for retirement which is now $72,148. They could also afford to earn an additional $11,800 from working without affecting their pension income at all. If they earn more from work, they’ll need to pay greater attention to the income test thresholds too.

In contrast, Melanie and Will, who are 67, have a home worth $1.5M that they own outright, $1.2M in their joint superannuation fund, and are ineligible for the age pension. They too are drawing the standard 5 per cent drawdown rate, and, if they do this, their superannuation drawdown is $60,000. They can work, pay tax and put money into superannuation by the standard rules, as they don’t have to worry about triggering an age pension cap. They can also choose to draw down more from their fund.

There’s a much bigger debate to be had here about the returns you can get from money if you are a partially self-managed retiree accessing a part age pension. Effectively, you would need to be getting a return of more than 7.8% on your funds over the pension thresholds to be outstripping the benefits of minimising your balance to these levels. Boggling when you really think about it.

It's crucial to carefully consider investment returns and pension thresholds before making decisions about retirement finances. And you really do have to think about it. I don’t think people should make the decision to ‘burn down’ their financial assets lightly to access more pension income. And I do think that getting advice, if you are on the cusp is really important.

Where can you get advice?If your money is in one of the major superannuation funds, my first suggestion is to use their online calculators and tap into the free advice they offer you as a part of your annual member fees. Most have ‘superannuation financial advisers’ and/or ‘retirement advice’ that can help you make informed decisions tailored to your own financial circumstances. This advice is usually free, as I said. Some might charge you a nominal amount.

The other thing to know is that independent financial advisers who specialise in retirement advice, are usually expert at this stuff. As Janet pointed out, getting personal financial advice could be expensive, but if you are on the cusp, the advice and support in making decisions about saving versus spending your superannuation more quickly are important to make very carefully.

I recognise that people who are planning to be entirely self-funded might feel annoyed by this sweet spot, but the extra flexibility to draw down more in the early more active phases of retirement may mean they could also end up in the sweet spot over time. I’m of the view that if the systemic capability is there, people may as well learn more about it. Then, they have the power to seek more advice on their own situation and make educated choices.

People who can’t get the pension at all may also benefit from exploring their eligibility for the Commonwealth Seniors Health Card, which relies on the income test only and has very high caps.

Love this? Forward it to a friend and suggest they sign up!

We’re all going to live a lot longer, and that changes everything with Dr Andrew J. Scott“We have an opportunity to improve our lives significantly, simply by recognising that longevity is not about older people, it’s about how we adapt to living longer lives.”

We’re all going to live a lot longer, and that changes everything with Dr Andrew J. Scott“We have an opportunity to improve our lives significantly, simply by recognising that longevity is not about older people, it’s about how we adapt to living longer lives.”Our life expectancies are growing, and it's likely we'll all live much longer. This means we need to make changes to the way we live long before we reach old age so we can enjoy a better quality of life.

This week, I had a chat with Dr. Andrew J. Scott, one of the world’s foremost authorities on longevity and the author of The 100-Year Life. He's just released a new book, The Longevity Imperative, which will be hitting Australian bookstores on April 23rd.

He is a professor of economics at London Business School and he has previously taught at both Oxford and Harvard Universities. And his perspective on longevity is simple, logical and sensible.

“We have an opportunity to improve our lives significantly, simply by recognising that longevity is not about older people, it’s about how we adapt to living longer lives,” he said.

I really enjoyed this conversation, weaving our way through all the impacts of longer lives, and hearing his very esteemed opinions on what we should do to make the most of them.

Listen nowLISTEN HERE - LATEST EDITION (E20)

Visit the show on APPLE PODCASTS

It’s Tuesday of the last week of the How to Have an Epic Retirement six week flagship course, and it has been truly a joy to run and host. Last week we enoyed a Live Q&A with the amazing Jim Kilkenny who many of you will have heard in the book, and on my podcast talking about relevance deprivation. We also hosted a live coaching session which absolutely blew me away! Our course attendee community openly talked about their feelings about their sense of purpose, and together walked through what they were doing as individuals to tackle it, with honesty and curiosity. I provided the framework and the facilitation, but they were the total focal point, each taking turns to put up their hands and talk on camera. We’re going to do more of these sessions in our next program.

I know I’ve been promising the launch of the next online course program for a few weeks, but we’ve been making some improvements, so I have to wait until I know they are ready.

Last week we filmed our updates, and the video-editors are hard at work on new lessons to go into the program in time for our next release. And, my amazing publisher has agreed with some excitement to create a high quality workbook exclusively to accompany the program! Yippee! So my nose is down, working on this beautiful addition. So the next dates will depend on the editors, typesetters and when it can arrive. They promise it will be fast. I should have dates by next week. The experts are all ready-to-go too!

You can register your interest here. There will be limits on earlybird spots next time so I recommend getting in fast. But we will be able to accomodate a much larger number of attendees as this is not a pilot anymore!

Register your interest for the course

In other things, I’ve spent a lot of the week on radio stations and recording podcasts! So - much - fun! You might have heard me on ABC stations in Queensland, Tasmania, NSW and Victoria talking about how the age people are actually retiring at is rising, and the reality that some people really want to work longer, with balance in their lives of course.

This week we have a doozy of a Prime Time podcast coming out. Make sure you’ve set yourself to subscribe and download Prime Time in your podcast player so you get it when it drops. And thanks to Aware Super for becoming our super sponsor from last week!

And, I’ve been preparing some guest speeches for the weeks ahead. I’ll be heading to Melbourne, Sydney and Brisbane for a few corporate and superfund events in May and June. I love the guest speaking and educating in person part of my work. It offers a direct contrast to sitting behind this computer educating in writing that gives the perfect balance. Want me to speak somewhere? Email me.

And don’t forget to send me your letters! I love them. Please, send them to bec@epicretirement.com.au.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

April 13, 2024

How to live better now we’re living longer

A quick note today - saving the juicy stuff for Tuesday’s big newsletter!

This weekend’s article in The Age, The Sydney Morning Herald, Brisbane Times and WA Today is below, and it’s all about living our longer lives better and practically, what I think we all need to be concerned with.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

It pairs up with a wonderful interview I did on the Prime Time podcast this week with Dr Andrew J Scott, one of the world leaders in longevity and a professor of economics at London Business School. Totally worth a listen.

SPECIAL REQUEST: Please send me your letters. I would love to keep a steady flow of them coming on the weekly newsletters. If you have a letter, email me at bec@epicretirement.com.au.

Have a lovely Sunday! Make it epic!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

How to live better now we’re living longer

How to live better now we’re living longer

This article was first published in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

Longevity has become a buzzword that’s almost as hot as sustainability and AI in some circles – and it’s not just about old age.

Our life expectancies are growing. It’s likely we’ll all live much longer, and we want those years to be good years. This means we need to change the way we live long before we reach old age so we can enjoy a better quality of life.

The science of modern ageing already tells us that we can slow the march of time simply by looking after our bodies, minds and communities better. And then, if we do that, we have to look after our money, our work, our sense of purpose and our relationships better too. Because living longer is only worthwhile if we can enjoy it.

This week, I did a podcast with Dr Andrew J. Scott, international bestselling author of The 100-Year Life and his new book, The Longevity Imperative. He says today’s over-50s should expect to live well into their nineties, possibly even to 100, and young people could see a life as long as 120 years.

The question then becomes, how do we make these years good quality years? None of us want to live the last 20 or 30 years of life lonely, in poor health and without a sense of purpose.

There are a few things we have to start working on more actively if we want longevity. We have to push society’s norms too. But what should we do first?

Think about future-youThe very first thing you can do is start to think about your longer life. Imagine the person you want to be in your 50s, 60s, 70s, 80s and 90s and reverse out the things you’ll need to do today to become that.

Thanks to the media’s dislike of ageing, we haven’t got enough mature, dynamic role models, so we have to use our imaginations to think about the physicality we hope our bodies will have, the financial security we want, and the sense of purpose and belonging we will enjoy.

Then, we have to take responsibility. Stop telling yourself that the medical system, health insurers, superannuation, and retirement companies will look after you. You have to look after yourself in a world where we live longer than ever before!

They’re just the service providers you’ll pay along the way. I hate to say it, but it’s your responsibility to learn about how to do longer life well.

Take compound investing and superannuation much more seriouslyThe government created the compulsory superannuation system 32 years ago, but it’s up to each individual to really reap its power or even to turbocharge it. It’s designed to encourage you (and force you) to save money for your future and allow it to grow over a lifetime if invested well.

And, if you really grasp and embrace the power of compound investing via superannuation early, or even in midlife, while you can still work, save and invest actively, I can almost guarantee you that you won’t have to worry about money later in life, even if you live to 100 or 120.

To achieve that, you need to open your superannuation dashboard, learn how it works and make sure you use its powers. Be selfish about your own financial future.

Recognise the changing role of work in the second half of your lifeThe end game is not ‘retirement’ any more. It’s reaching the point of choice. Think about getting yourself to the critical tipping point of financial freedom that allows you to choose what types of “work” or leisure you do.