Bec Wilson's Blog, page 13

November 18, 2023

How comfortable can you afford to be in retirement?

It’s Sunday again. And this week I’m bringing a big voice to a big issue across my major newpaper column in the Nine Newspapers, and on my podcast, Prime Time (with Bec Wilson).

So it’s a simple newsletter today with one big message. Most people planning well in advance of retirement can budget for ways to live in comfort - you just need to understand the process of planning for retirement effectively. So in both the column and the podcast, I do a deeper dive. A comfortable retirement is something I wish everyone could have.

In this editionToday’s SMH/Age article: How much do we really need to retire in comfort

Prime Time Podcast: How much do you really need to retire in comfort and making sense of your super

Order your signed copy of How to Have an Epic Retirement, the book - in time for a Christmas gift

Budgeting tool: Access to our free, updated excel budgeting tool, discussed at length in the podcast and the book.

#Ad 🌟 Maximize your brand's impact: Epic Retirement sponsorship opportunity! 🚀Join us in shaping epic retirements! Become a sponsor or partner for 2024.

Reach over 25,000 people (and growing) who are passionate about preparing for and living their best retirement each week. Elevate your brand in our exclusive email sponsor position. Your support fuels our commitment to providing valuable info, education, and resources. Connect with engaged pre and post retirees, showcase your brand in our weekly emails, and make a lasting impact. Act now - contact us at bec@epicretirement.com.au. Be part of the journey to empower retirees to live their best lives!

How much do you really need to live in comfort?Every Sunday I write a column that is published in the money section of The Age, The Sydney Morning Herald, Brisbane Times and WA Today. And our community asked that I send it out the day it goes to print. So, this week’s column can be read in full here.

As you look forward to full-time or part-time retirement in your future, there’s a massive question most people need answered to build up their confidence to set a retirement date: how much money do you really need to retire in comfort? It seems like such a simple question, surely it has a simple answer. Well, it does – sort of.

The Association of Superfunds Australia (ASFA) releases their retirement cost of living benchmarking quarterly. The latest numbers say that single people who will be eligible for the age pension, and own their own home outright will need an annual income of $50,207, while couples will need $70,806 to afford a comfortable retirement.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Assuming a lifespan of 88, they say that single people need to have a superannuation balance of $595,000 and couples will have to have a balance of $690,000 when they retire.

These comfortable retirement budgets assume a certain standard of living that most people want to be able to afford, but certainly not everyone will be able to. It expects that you’ll have a lifestyle that includes the purchase of comprehensive health insurance, owning your own reasonable quality car, and can afford to buy fashionable clothing and footwear fairly regularly.

It also assumes that you will want to run air conditioning for heating and cooling. It budgets for you to take one domestic holiday to visit family per year and a simple international holiday every seven years. And it affords enough for you to participate actively in leisure activities like going to the club or the movies.

It does not offer you enough money to take regular holidays, undertake sizable home renovations or maintain and upgrade a fancy new car, allowing only for modest renovations every 20 years. And it certainly does not allow for rent payments, although if you are eligible for a part-pension you will also be able to qualify for rent assistance which will offer some support. Nor does it accommodate the payment of significant body corporate fees.

This article continues on the Sydney Morning Herald website here. It’s usually free to access the article - you may need to register.

Podcast: How much do you really need to retire in comfort and making sense of your super

Podcast: How much do you really need to retire in comfort and making sense of your superIf you're heading toward the next phase of your life, you've probably asked yourself this big question: How much money do I really need to retire comfortably? Today I tackle it head on. Is there a magic number? Will I ever be able to quit my job or start stepping back from full time work? How do I work it all out for myself?

This week I have invited radio personality and weekends presenter at 4BC 882, Spencer Howson back onto the show to chat about money with me, and help me break down this big and important topic. With Spencer’s help I take a deep dive into how to plan for your retirement and build your own set of numbers, explaining how to build a vision for your retirement years and then calculate your numbers against that vision. He’s a blessing in disguise, making this tough topic much more relatable.

Listen nowLISTEN HERE - LATEST EDITION (S1E5) - OMNY

or listen on APPLE PODCASTS

Highlights:

Understand how much money you need to spend each year on living expenses to have a comfortable retirement, based on the benchmarks, so you can start to explore your own needs and wants, and understand what you can afford to dream about.

Consider how much you need to have in your superannuation account before you retire to generate a comfortable retirement income.

Learn the fundamentals of how your superannuation works, and what you need to be paying attention to to maximise your compound investment goals over the years before retirement, and in the years after it.

Find out the formula to help us build out our own budgets.

Explore the things that can change or impact our retirement planning in the economy that we don’t have much control over, and how we can manage them.

Understand when you might want to get the help of a financial adviser.

This is one of those topics where there’s no ‘right answer’ only your answer, so I feel it’s important to give you the formulas and tools so you can take the time to work through it yourself.

Many thanks to Spencer for being such a great friend of the show and helping us navigate the tricky topics in a friendly and relatable way. I hope you enjoy his company as much as I do!

So, go now and have a listen! And please, consider leaving us a rating and a review - and sharing the podcast with your friends! ★★★★★ It’s hard to believe but our Prime Time podcast has been making it into Apple’s top 100 each week so far - and that’s because of you, our wonderful community! Thanks for getting behind it.

Buy an inscribed copy of Epic Retirement for a Christmas gift (or for yourself)

Buy an inscribed copy of Epic Retirement for a Christmas gift (or for yourself)This is the ultimate guidebook for a modern retirement, and if you love it, surely your friends will too. At popular request, we’ve set up an online store so you can order a signed, personally inscribed copy as a gift. Check it out here and get in while stocks last.

The book walks you (or your loved one or friend) through the six key pillars that matter most as you approach retirement, the biggest life change you’ve every navigated so far. It is designed to provide structure, build confidence, and ignite excitement across each of the six areas: time, money, health, happiness & fulfilment, travel and your home.

Or, you can buy the book at all major booksellers and heaps and heaps of smaller bookstores. Stockists are here. Or just buy it now on Booktopia.

Access to our free Epic Retirement excel budgeting template

Access to our free Epic Retirement excel budgeting templateIt is very hard to work out how much you need to retire in comfort without doing a comprehensive cost of living budget. I have built this powerful little budgeting spreadsheet (recently updated), the use of which is explained in-depth in How to Have an Epic Retirement - the book, and discussed in this week’s edition of the Prime Time Podcast.

You can download the template here. It’s worth about $169 in real money - but I am giving it to you for free - please use it to prepare to make your retirement as comfortable as you can: https://epicretirement.com.au/budget/

Repay me by telling someone about Epic Retirement. Forward this email to your friends. Let’s help more people make it epic!

THE IMPORTANT STUFF: The information provided in this article, newsletter and podcast about pre-retirement and retirement is intended to be general advice and for educational purposes only. It is not personalised financial, investment, or legal advice and Bec Wilson is not a financial adviser. The content presented is based on facts, research and our understanding of current laws and regulations, which may change over time. We recommend consulting with a qualified financial advisor, accountant, or legal professional before making any financial or retirement-related decisions. We make no representations or warranties of any kind, express or implied, regarding the accuracy, completeness, reliability, or suitability of the information shared. Listeners are solely responsible for their own actions and decisions based on the information provided in this podcast.

November 11, 2023

Your changing roles, portfolio life and your wardrobe and grooming

I admit it, I didn’t manage to get a midweek newsletter out this week, so I’m making up for it today by bringing you both an Epic Retirement Feature and my column from The Sydney Morning Herald and the Age. I’ve also included a link to the latest edition of the Prime Time podcast too. In this edition:

Epic Retirement Feature: Your changing roles, portfolio life and your wardrobe

From Bec’s Desk: A short update

Today’s SMH/Age Article: Why some people are quietly cheering higher interest rates

Prime Time Podcast: The science behind the modern Mediterranean diet, and wisdom from the 'Blue Zones'

Your changing roles, portfolio life and your wardrobe and grooming

Your changing roles, portfolio life and your wardrobe and grooming

Many people head towards a modern retirement by moving into a more ‘portfolio life’. Or a life where they go from doing one main job, and coming home at the end of each nine to five day; to performing a selection of different roles, some very different to the things they used to do. This in turn changes the way they dress and the sense of style they invest in what they do. But how conscious and aware are you of the intertwining of grooming and self-pride in your next stage? What role does the portfolio life play for you in defining your next stage wardrobe or leveraging your wardrobe differently?

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

The essence of a portfolio life lies in being deliberate with your choices, curating a collection of roles that contribute to the richness of your life in pre and post retirement. It might involve a blend of part-time work, freelance projects, volunteering, and epic pursuits that collectively make up your portfolio. You may also find healthy living activities and family time is better able to fit into your portfolio life, adding even greater diversity.

Some actively pursue a portfolio life, while others prefer to live life spontaneously, and no matter which way you look at it, for most people, a portfolio life or a spontaneous lifestyle, requires a very different wardrobe and possibly shifts your sense of style for the first time in a very long time.

When I was writing How to Have an Epic Retirement I sat with a dear friend who has been navigating both his shift into portfolio life, and a divorce at the same time. He spoke of his own lessons about style, saying he deliberately and consciously stepped up his game recently, conscious that many people do not, and that he finds great pride in dressing for the roles he now has, and knowing what to wear with each hat he wears. He spoke of how important he finds it to get up, exercise, groom, and dress in well-ironed and appropriate clothes suited to the role he was performing that day, to feel good in his semi-retired portfolio life. I remember sitting back from it and wondering how much people really speak about this.

After all, when we’re young, style and fashion and grooming is everywhere. And so we attach our self-pride to dressing well for work, like the old adage says “dress for the job you want, not the job you’ve got”. Some people do this, some don’t and the world keeps spinning.

But what happens when you don’t have a job or the jobs you do are different each day? I guess you need to decide if that adage should still apply to you. Should you dress for the roles in life that you perform, or want to perform?

I’m not a particularly vain person, so you wont find me judging people or telling them how to dress. But talking to people who have lived through this stage and who do pride themselves on their presentation, many say that their sense of style changes and adapts, with different outfits and style for the jobs they have. And some say they revelled in actively shifting their wardrobe to suit.

Some even talk of taking time out to do a little wardrobe audit, with help from Pinterest, to see how they can adapt their looks (without a whole lot of spending) to better fit the different roles in their lives. That way they still feel pride in dressing for ‘success’!

Have you been through a wardrobe audit? Leave me a comment today.

From Bec’s DeskBusy busy busy! The Epic Retirement course is coming together! I’ve been speaking at some wonderful corporate and community events. My second daughter has finished year twelve exams and Christmas really is coming. The Prime Time podcast is getting more and more downloads each week. I’m quite sure we’ve cracked 15,000+ downloads already! And, people just keep buying the book - thank you I feel blessed!

I’m toying with setting up an online store where you can buy a personally signed and inscribed copy of How to Have an Epic Retirement for your loved ones for Christmas or a Kris Kringle gift for someone you know. Tell me if you think it might interest you and I’ll set it up in the week ahead so we can get shipping to you in time for Christmas. I’ve never written a book that might make a good gift before… and I do think it would.

If you’re impatient, you can just order your copy of How to Have an Epic Retirement online from Booktopia here.

Until next week- Make it epic!

Many thanks! Bec Wilson

Author, columnist, retirement educator, and keynote speaker

Why some people are quietly cheering higher interest ratesEvery Sunday I write a column that is published in the money section of The Age, The Sydney Morning Herald, Brisbane Times and WA Today. And our community asked that I send it out the day it goes to print. So, this week’s column can be read in full here.

Interest rates hit a 12-year high this week with RBA governor Michelle Bullock announcing our 13th consecutive rate rise since we hit all-time lows of 0.1 per cent in November 2020.

The cash rate now sits at 4.35 per cent, and while many mortgage-holders are feeling the pinch and the media are screaming about the agony, there’s a huge population in Australia that is quietly rejoicing in the higher interest rate environment. And it’s time we talked about them a little more.

The number of people approaching and in retirement, who live on the income generated from their savings, are almost as sizable as the home owners paying mortgages in this country right now. And they have the power to cause some significant abnormal shifts to economic patterns.

Thirty-five per cent of Australian homes are owned with a mortgage, according to the most recent census. And 31 per cent of homes are owned outright without a mortgage, many of these owned by people over the age of 50.

For people who own their own homes outright, and have then diligently saved and built up a comfortable cash reserve, rising interest rates are usually good news. Those people, if they have any money invested in cash, have enjoyed a 1.5 per cent pay rise over the twelve months and quite possibly, a positive bump to their consumer confidence.

This article continues on the Sydney Morning Herald website here. It’s usually free to access the article - you may need to register.

The science behind the modern Mediterranean diet, and wisdom from the 'Blue Zones'

This week, our fourth episode of Prime Time is a doozy (if I do say so myself!). It is all about the Mediterranean diet which has been lauded by scientists for its ability to help people live longer, healthier lives.

We’ve invited Professor Catherine Itsiopoulos, Australia’s leader in this remarkable diet to talk about it in detail, explaining the principles of this way of life and how you can integrate it into your days in a modern and achievable way.

The Mediterranean diet has been shown to offer so many benefits in addition to longevity, including reducing the risk of heart disease and the effects of inflammation in the body, decreasing the risk of cognitive decline, and helping people control their blood sugar more effectively.

Prof. Catherine Itsiopolous is Dean of Health Sciences at RMIT University and she's spent her career studying the benefits of the Mediterranean Diet scientifically. She’s also lived the benefits, as a passionate Greek Australian, who has grown up with a deep enthusiasm for family cooking.

She's dedicated to adapting the secrets of the 'Blue Zones' to a busy modern lifestyle, through her new book 'The Modern Mediterranean Diet', her fifth book on healthy living.

Listen nowLISTEN HERE - LATEST EDITION (S1E4) - OMNY

or listen on APPLE PODCASTS

And that’s it! Have a great week!

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

Why some people are quietly cheering higher interest rates

Every Sunday I write a column that is published in the money section of The Age, The Sydney Morning Herald, Brisbane Times and WA Today. And our community asked that I send it out the day it goes to print. So, this week’s column can be read in full here.

Interest rates hit a 12-year high this week with RBA governor Michelle Bullock announcing our 13th consecutive rate rise since we hit all-time lows of 0.1 per cent in November 2020.

The cash rate now sits at 4.35 per cent, and while many mortgage-holders are feeling the pinch and the media are screaming about the agony, there’s a huge population in Australia that is quietly rejoicing in the higher interest rate environment. And it’s time we talked about them a little more.

The number of people approaching and in retirement, who live on the income generated from their savings, are almost as sizable as the home owners paying mortgages in this country right now. And they have the power to cause some significant abnormal shifts to economic patterns.

Thirty-five per cent of Australian homes are owned with a mortgage, according to the most recent census. And 31 per cent of homes are owned outright without a mortgage, many of these owned by people over the age of 50.

For people who own their own homes outright, and have then diligently saved and built up a comfortable cash reserve, rising interest rates are usually good news. Those people, if they have any money invested in cash, have enjoyed a 1.5 per cent pay rise over the twelve months and quite possibly, a positive bump to their consumer confidence.

This article continues on the Sydney Morning Herald website here. It’s usually free to access the article - you may need to register.

November 4, 2023

More joy, less stress: Why you should rethink your work before you retire

Every Sunday I write a column that is published in the money section of The Age, The Sydney Morning Herald, Brisbane Times and WA Today. And our community asked that I send it out the day it goes to print. So, this week’s column can be read in full here.

My full weekly Epic Retirement newsletter comes out on Tuesday; and the Prime Time podcast comes out on Thursdays at www.primetimers.net.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

So enjoy this week’s article which is in print in the Nine Newspapers today and have a lovely Sunday. Take a moment if you have one to listen to this week’s podcast. We talked about all the insider secrets to downsizing, with Dr Nicola Powell, the Chief of Research and Economics at Domain. (more info below)

Bec Wilson XX

More joy, less stress: Why you should rethink your work before you retire

In the grand narrative of work and workforce choices, it’s often the young and ambitious who are credited with driving change. For decades, they have spearheaded revolutions in the way we work, challenging traditional structures and seeking more flexibility in their careers.

But, there’s a quieter, yet equally profound, revolution under way, led by the Baby Boomers and Generation X – or the Prime Timers as I call us – who can now glimpse retirement on the horizon and want the best of both worlds sooner.

This revolution has gained momentum in the post-pandemic workforce shortage, and it’s all about shifting from high-pressure career work to work that aligns with your lifestyle and flexibility goals. We could aptly call it the “life-flex movement”.

The life-flex movement marks a pivotal moment in the lives of those closing in on the end of their formal careers. It’s when people start to reassess the role of work in their lives and explore different ways to get the most out of it.

While the younger generations have been at the forefront of the gig economy, remote work, quiet quitting and work-life balance discussions, it’s our older generations who are now embracing the concept of more flexible work to support their desired lifestyles.

And it’s a conversation for both those in pre-retirement and post-retirement years. Because retirement doesn’t mean completely giving up work any more. It means knowing more about your choices.

It has become obvious that the traditional work model is no longer sustainable or fulfilling for a significant portion of the workforce.

A report released this week by Amazon, Lonergan Research and demographer Bernard Salt got me excited. It provided real data on the shift I have observed occurring in pre-retirees, pointing out that the way we work has fundamentally changed for Australians across all demographics, but especially for those aged 55 to 69 years.

“The old model of 50-somethings continuing to work at a job that ‘takes’ more than it ‘gives’ after waving goodbye to the kids as they leave the family home has been reimagined. Workers over 55 are seeking out additional income, social engagement, improved workplace camaraderie and maybe even ‘meaning’ in their later working years,” the report said.

For many people, the need to keep earning money is still there throughout this phase, right up to the pension age of 67, especially in the generation approaching retirement. And beyond that, many still need work to supplement their pensions.

For those in pre-retirement now, most people know their superannuation is only going to be just enough, or not quite enough to fund a comfortable retirement from 67 to their life expectancy of 85-88 or longer.

But, the events of the past few years have driven an attitude change. The post-pandemic world has brought into sharp focus the fragility of life, urging many to rethink their priorities.

The workforce shortage, ageism and the desire to live better, and longer, have made it more obvious that the traditional work model is no longer sustainable or fulfilling for a significant portion of the workforce.

And for the new generations of pre-retirees, the new concept of retirement isn’t a simple binary choice between work and leisure. Instead, we are embracing the idea of more flexible and rewarding work during pre-retirement and incorporating work into our picture in our post-retirement years.

This movement isn’t about working until the last possible moment but rather at some point after midlife, actively choosing work that aligns with personal interests and allows for a more relaxed, flexible, and enjoyable lifestyle.

This article continues here on The Sydney Morning Herald and includes tips for those considering changing up their work. It’s free to access the article - you may need to register.

Have you changed up your work life for more flexibility or to better suit your pre-retirement and retirement goals? Tell us about it in the comments here - you might just give someone else the insight or feedback they need!

Prime Time Podcast: The insider secrets to downsizing your home

The third episode of Prime Time with Bec Wilson is all about your home and downsizing and how that could be changing the great Australian dream for the generation that created it. I chat with Dr. Nicola Powell, the Chief of Research and Economics at Domain, Australia’s leading property marketplace, about how downsizer trends are changing.

The dynamics of the housing market are clearly shifting as the new generation of downsizers are entering the market. And it makes for a terrific conversation, about where people want to live in the next stages of life, what they want from their homes, and how the quarter acre block that used to be the Australian Dream might in fact be ready for change.

Listen nowLISTEN HERE - LATEST EDITION (S1E3) - OMNY

or listen on APPLE PODCASTS

Here’s some highlights:One of the two key drivers of our housing markets in the years to come is the changing demographics. How the Baby Boomer’s desires are shifting away from the quarter acre block in the inner or middle ring suburbs.

Housing rich, cash poor - the median prices that are driving the prime opportunity for downsizers.

The behaviour we are seeing from downsizers is changing to be more local to the areas they’ve lived in for years, but the downsizing stock isn’t necessarily available in their preferred areas.

Why people are continuing to live in homes that don’t suit their needs. Is there a role for government in densifying our cities to accommodate the changing demand.

The downsizer contribution, an incentive to drive people to consider downsizing, and how it works.

A favour?

Thousands and thousands of you have been working your way through How to Have an Epic Retirement making good use of the research and insights. And now I have a favour to ask. Would you consider leaving a review for it on Good Reads here?

It has been in bookstores for four months, and the reception has been rather terrific. It can officially be called a bestseller, and is currently ranked #1 on Booktopia’s Bestseller list in Retirement.

If you haven’t read it yet, you can order your copy from Booktopia here, or it is available for sale in almost all booksellers. Look for it in stores like Big W, Dymocks, Harry Harthogs, David Jones, Target and many of the more boutique bookstores too.

October 31, 2023

Do you really understand your options for getting financial advice and help with retirement planning?

Article: Do you really understand the financial advice landscape in Australia?

Prime Time Podcast: Exercise for longevity: How muscle mass improves your lifespan

From Bec’s Desk: This week in Epic Retirement

How to Have an Epic Retirement: The Book

There was a big discussion this week in the Epic Retirement Facebook Group about what type of financial adviser is ‘the right’ type of financial adviser for guiding your journey into retirement. And it raised more questions than answers for most people in the group. So today I’m going to take a deeper look into the financial advice sector and the different types of financial advice that you should expect to come across out there in the market right now. And in coming days I’m going to release an eguide into the area of getting financial advice - which you can sign up to receive here. I’ll include a lot of valuable insights into the different services on offer, from both super funds and independent financial advisers and I’ll give you a list of questions to consider and ask too. Sign up here to get your copy by email when it’s released.

This image of wise owls generated using AI tool, Dall-e

This image of wise owls generated using AI tool, Dall-eTo write this article, and the eguide that will follow in coming days I spoke with several superannuation funds, spanning industry and retail sectors; the Financial Advisers Association (FAAA) and several independent advisers, some specialist and some more generalist in nature. So I gathered a lot of individual insights - too many to share today. One thing I’m clear on - the industry is working hard to help people navigate retirement. And it wants you to be less afraid of asking for help and advice, and know the difference between general advice and personal advice. They serve different roles.

You see, financial advice has fundamentally changed in the last five years, since the Banking Royal Commission in 2019. It used to be all about guiding investment into financial products and ‘growing wealth’, with most advisers incentivised by trailing or lump sum commissions from financial product companies, even independent advisers. But all this has changed when the Royal Commission put an end to trailing commissions.

So let’s boil down the types of advice you can get today, and how you might be able to use each to grow your confidence in the preparation for retirement. They all have a role to play in my opinion. You definitely might consider using more than one type!

General advice - it’s really accessible ‘help’ and educationGeneral advice is typically the provision of factual information, not personalised to your specific financial situation. General advice is commonly provided by superannuation call centres and visiting workplace superannuation advisers and provides information and guidance on topics purely related to your individual superannuation. You might prefer to call it ‘useful help’ that will explain how things work. It is a great way to start learning and exploring about the contributions you can make; your investment options; the age pension and how people can layer their income in retirement. The people who provide this advice are usually expected to have a qualification in financial product advice, called an RG146, and may have a diploma of financial advice too. But remember - this is facts and general information. If what you are doing has any complexity, or you need any insights into your personal situation they cannot assist. But it’s a great place to start asking questions and learning how things work.

Intra fund advice - free advice available via most super fundsThis is personalised financial advice provided by fully qualified superannuation fund advisers but their scope is usually limited to advising on superannuation, hence the name - intra fund. Some funds allow their advisers to provide advice for the individual member that expands wider than their superannuation, while others keep the scope limited. Intra fund advice commonly addresses your investment choices within your superannuation fund, insurances held within superannuation, contributions advice to grow your funds in super, transition to retirement advice and retirement income stream advice.

Most funds I spoke to offer intra-fund advice for free to their members, funded by their member administration fees. Some charge a small fee to guide the member through the retirement process of setting up the retirement phase accounts, while for others this process is completely free.

It is important to point out that the limitations to intra fund advice differ across funds. Some will provide advice on your wider assets, while others will only provide advice on your superannuation.

Intra fund advisers cannot provide advice across a couple unless both people are with the same fund. And if you require advice that pertains to the couple on joint superannuation strategies, investing and insurances held outside super, you will need to seek independent advice. All the funds I spoke to had preferred independent advisers to which they refer you if you ask. Or you might consider finding someone through your own networks.

Personal financial advice - comprehensive financial planning and investmentPersonal financial advice is provided by fully qualified financial advisers, who are licensed and registered under the regulation of ASIC. All independent financial advisers are required to gather the client’s information properly, produce a statement of advice and comply with the regulatory requirements of the sector that have been imposed to protect consumers.

Financial advisers will usually walk you right through your big financial picture in your first meeting or two, understanding where you are now, and where you want to be. They understand your goals, your cash flow, your balance sheet, your structures, your current risk profile, your responsibilities now and into the future and the stage of life you are at.

They then take in all your information and build you a strategy that takes in your accumulation goals, retirement goals and setup. Then, they’ll guide your structuring needs setting up appropriate tax structures and accounts within your super to maximise your returns or retirement income depending on your goals. Each year they’ll re-evaluate your insurance needs too, which usually decrease as you approach retirement rather than increase. And if they’re a good adviser, they’ll explain to you why this strategy will deliver to your goals and build your confidence through a better understanding of your big financial picture.

Then, they’ll define an asset allocation for investing and roll out that investment strategy on your behalf if you want them to. Advisers can only invest in investment products from their approved product lists which are built through high quality research and under the careful eye of an investment committee. It’s worth asking how they select investments, and how diverse their approved product lists are, to see if that meets your needs. Different companies have very different approaches to try to manage compliance and risk.

There’s a few very specific things you need from your adviser when approaching retirement, they are looking for:

a more detailed review of their accumulation strategies,

the support of the shift into the retirement phase

the layering of retirement income, through a combination of the age pension and investment income streams.

These are the big areas most financial advisers are adept at, but it never hurts to ask them to explain their experience with the pension, superannuation and retirement phase advice to you.

Specialist financial advisers - for those with special needs or wantsAs the financial advice industry has evolved over many many decades, some advisers have chosen to specialise in either types of investment, or types of clients. It’s worth being aware that specialist advisers exist, and that they specialise for a reason, to be able to more deeply invest in a specific and perceived higher value way of delivering their service. All specialist financial advisers have to comply by the same rules as personal financial advisers as they are in effect the same thing. You may just find that some have crafted their process and offerings to better suit a specific client group or a client need or want.

There are a few types of specialisation you will come across. Most lead their offering with any combination of:

Stockbroking or specialised investing

Funds management

Family office style wealth advice

Some firms set themselves up to offer services to higher net worth families and individuals so they can focus on managing larger portfolios only.

Each of these businesses are held to the same legislative requirements, and while they invest in individual stocks and investment products on your behalf, they will do so from the basis of robust research and economic insights, done with the oversight and governance of an investment committee; and extensive compliance obligations. All of this you should expect from any financial adviser.

Calculators and tools - test your theories at homeAs you look around at advice offerings, the other things to be aware of are the powerful calculators, tools and digital advice offerings that are starting to emerge. Many superannuation funds are offering their members a robust set of retirement planning calculators and tools which you can use to project your own calculations, and test out ideas. It’s a great way to start learning about your money, and how it works in the lead up to retirement. Some super funds encourage you to play with their tools, then ring their general advice call centres for more help, as the first port of call to start learning progressively about superannuation.

Digital Advice platforms and robo advice - DIY your financial planningIn the new world of advice is a selection of platforms that for a fee, will provide you with very detailed financial advice. These powerful tools, which I’ll explain more about in our eguide, are designed to give you a set of tools that collect your information, stage of life and goals and allow you to see clear recommendations based on your circumstances or individual needs. I’ve tried a few - they’re getting really powerful. They are usually offered by independent digital advice companies operating under their own license, who are focussed on advancing the technology available to help consumers with common issues and needs.

And now for the big question…

How much should you pay for advice?Well, that really depends on what you need advice for. According to the Financial Advice Association of Australia, the average price of advice right now is somewhere around $4000 for a financial plan produced by an independent financial adviser. Ongoing services cost more.

Intra-fund advice from your superannuation fund is usually offered for free, with some services like the transition to retirement and incurring a fee with some funds in the league of $300.

There’s quite a lot to consider when you are contemplating getting a financial advisor or changing advisers. And for each person, that consideration will be different.

If you want to read more about financial advice and how the industry is changing to serve your needs in pre retirement and retirement, register for our eguide on Professional Financial Advice and I’ll send it through as soon as it’s all ready to go.

NEW PODCAST: SERIES 1, EPISODE 2 Exercise for longevity: How muscle mass improves your lifespanAn interview with exercise physiologist and exercise for longevity expert, Jonathan Freeman. There's so much helpful health advice packed into this one episode.

Exercise for longevity: How muscle mass improves your lifespanAn interview with exercise physiologist and exercise for longevity expert, Jonathan Freeman. There's so much helpful health advice packed into this one episode.This week on the second episode of Prime Time with Bec Wilson, we learn all about how exercise, muscle mass and protein intake can help us age better. And more importantly, what types of exercise and how often.

I chat with Jonathan Freeman, a widely respected exercise physiologist and founder of Australia’s largest active over 50’s gym group, Club Active. He's a Professional Fellow with Southern Cross University and presents guest lectures in Functional Anatomy at numerous universities throughout Australia... AND he's worked with the likes of Chris Hemsworth and Kelly Slater, so he knows what he's talking about.

I learned so much about exercise, protein and muscle mass from this conversation and I’ve already adopted some of his lessons into my everyday behaviours.

Listen now:LISTEN HERE - LATEST EDITION (S1E2) - OMNY

or listen on APPLE PODCASTS

Here’s some highlights:According to Jonathan, only 1 in 10 Australians over the age of 50 do enough exercise to keep their hearts healthy and improve longevity. And he says physical inactivity is the biggest killer…

The three most important things you can do for your body as you age: Build your muscle mass, improve your V02 max and work on your joint longevity

He explains the way we can look at our body’s functional age, rather than our chronological age.

How people 50s-65s are looking to slow down the onset of ageing, and pointing out that our generation didn’t grow up with the gym, nor with the information and education on health and exercise that younger generations did, so we approach it differently.

The impact that our local community can have on our longevity, and considering how we can be supported to change the way we age.

Muscle mass and the muscle index score - how we measure it and how we improve it.

People over 50 who don’t currently go to a gym, need to understand structured exercise programs and their role in growing our muscle and strength - which contributes to longevity.

Cardiovascular health and your VO2 max - how we improve it, and how the various zones of cardiovascular exercise work, and where we get optimal results.

The critical role protein plays in our bodies and how much protein we should think about consuming to maintain our muscle mass

From Bec’s DeskWell hello! It has been a busy few weeks here at Epic Retirement and I can’t wait to tell you all about it.

The Prime Time podcast is going from strength to strength. Thousands and thousands of people have tuned into our first two episodes so far. I really enjoy getting to ask the questions of some rather amazing experts at the very forefront of how we can live longer, better quality lives. Be sure to find us on your favourite podcasting platform (links above), and give it a listen. And don’t forget to subscribe! The podcast drops every Thursday and we email out the highlights if you sign up for the Prime Time Newsletter at www.primetimers.net.

The Epic Retirement education program is now ‘in the can’ with more than four days of filming now finished. We are now working to build it into an online education program we can launch for you in the coming months. Be sure to jump on our waitlist for the release if you want to be one of the first participants.

I’ve taken up a regular slot on ABC Darwin and the NT, in a new segment with Alex Steer’s Tuesday morning program every other week that they’re calling ‘Retire Like a Rockstar!’ - what a hoot that is. If you’re anywhere in the Northern Territory be sure to listen out!

And then, there was last week’s column in the Nine Newspapers, The Sydney Morning Herald, The Age, The Brisbane Times and WA Today - How much super do we really have at retirement? Less than you think.

It’s keeping me busy. I have been planning for 2024, and am preparing some in-person full-day retirement seminars for Brisbane, Sydney and Melbourne, and some of the regions too. I wanted to get your feedback on coming along to an event where you can learn alongside up to 80 people at the same or similar stage of life, interactively!

I look forward to your honest feedback. Thanks for being curious! Pop in and like this post and leave me a comment about your financial advice experiences here on the article…

Many thanks! Bec Wilson

Author, columnist, retirement educator, and keynote speaker

About me

How to Have an Epic Retirement is the ultimate guidebook for modern retirees. It is grounded in my own widespread research on modern retirement, and draws on my prior ten years as the CEO of Starts at 60 and Travel at 60 (before I stepped away to pursue my next career in retirement education). It also draws on the work of the leading thinkers in the longevity, health, happiness, purpose and modern ageing spaces and incorporates many interviews with people who have navigated the sometimes challenging path into retirement.

I am incredibly proud of the response to the book so far. It has sold out online in Amazon and Booktopia several times and run the warehouse out completely. It has also reached #4 on Booktopia’s National Bestseller list, #8 on Dymocks Business & Finance Books list and #1 on Amazon Australia in the category of ‘Retirement’.

And it’s Booktopia’s #1 Retirement Bestseller right now! See for yourself here!

October 28, 2023

How much super do we really have at retirement? Less than you think

Every Sunday I write a column that is published in the money section of The Age, The Sydney Morning Herald, Brisbane Times and WA Today. And our community asked that I send it out the day it goes to print. So, this week’s column can be read in full here.

My full weekly Epic Retirement newsletter comes out on Tuesday; and the Prime Time podcast comes out on Thursdays at www.primetimers.net.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

So enjoy this week’s article from the Nine Newspapers below and have a lovely Sunday. I’ve linked the podcast below too. It was a ripper this week!

Bec Wilson XX

How much super do we really have at retirement? Less than you thinkEveryone talks about how much we need to retire in comfort in Australia. But rarely do we stop and discuss the reality of how much or how little money people really have in their superannuation fund at retirement age.

How much we each have tucked away isn’t a topic of polite conversation at barbecues, especially if we feel like it might not be enough. So today I take a deep dive into the average superannuation balances of those between 55 and 69 right now.

It’s an important set of numbers for us all to see a bit more publicly. They reveal that for the current generation of soon-to-be retirees and retirees, there’s not quite enough in most people’s accounts to be comfortable, and women are definitely in a less advantageous situation.

As we know, the Association of Superfunds of Australia (ASFA) suggests that to be comfortable Australian retirees need to have $590,000 in super if they are single when they retire, or $690,000 if they are a couple. And that’s if they have paid off their home and able to rely on a part-pension.

Yet, the Australian Tax Office’s latest superannuation statistics for the 2020/21 year show that the average superannuation balance for people aged between 55 and 59 is $277,327. For those aged 60-64 it sits at $361,539, 65-69 it is $428,738.

The difference between men and women is noticeable, with the average super balance for men aged between 55 and 59 sitting at $316,457 while for women the average, is $236,530. A gap of nearly $80,000. For those aged between 60 and 64, the average for men is $402,838 while for women it sits at $318,203 with a gap of close to $85,000. And for those between 65 and 69 years of age, the average balance for men is $453,075 whereas for women it is $403,038, with a smaller gap of $50,000.

Many people can use the last ten years before retirement to significantly improve their super balance

The average age of retirement in Australia is between 64.5 years for women and 65.3 for men right now. But preservation age, or the age you can actually start drawing down from your superannuation fund either through a transition to retirement or retirement pension, depending on your work status, is now 60 years of age. And pension age is firmly planted at 67 years, meaning many people will have to stay in the workforce until then, in the current generation.

If you are feeling pretty “average” knowing your superannuation fund is below the comfortable threshold, which, quite frankly, is the case for most Australians, there are still things you can do to try and improve your situation. Think about a few of these:

This article continues on the Sydney Morning Herald website here. It’s free to access the article - you may need to register.

Exercise for longevity: How muscle mass improves your lifespanPRIME TIME WITH BEC WILSON PODCAST An interview with exercise physiologist and exercise for longevity expert, Jonathan Freeman. There's so much helpful health advice packed into this one episode.

This week on the second episode of Prime Time with Bec Wilson, we learn all about how exercise, muscle mass and protein intake can help us age better. And more importantly, what types of exercise and how often.

I chat with Jonathan Freeman, a widely respected exercise physiologist and founder of Australia’s largest active over 50’s gym group, Club Active. He's a Professional Fellow with Southern Cross University and presents guest lectures in Functional Anatomy at numerous universities throughout Australia... AND he's worked with the likes of Chris Hemsworth and Kelly Slater, so he knows what he's talking about.

I learned so much about exercise, protein and muscle mass from this conversation and I’ve already adopted some of his lessons into my everyday behaviours.

Listen now:LISTEN HERE - LATEST EDITION (S1E2) - OMNY

or listen on APPLE PODCASTS

Here’s some highlights:According to Jonathan, only 1 in 10 Australians over the age of 50 do enough exercise to keep their hearts healthy and improve longevity. And he says physical inactivity is the biggest killer…

The three most important things you can do for your body as you age: Build your muscle mass, improve your V02 max and work on your joint longevity

He explains the way we can look at our body’s functional age, rather than our chronological age.

How people 50s-65s are looking to slow down the onset of ageing, and pointing out that our generation didn’t grow up with the gym, nor with the information and education on health and exercise that younger generations did, so we approach it differently.

The impact that our local community can have on our longevity, and considering how we can be supported to change the way we age.

Muscle mass and the muscle index score - how we measure it and how we improve it.

People over 50 who don’t currently go to a gym, need to understand structured exercise programs and their role in growing our muscle and strength - which contributes to longevity.

Cardiovascular health and your VO2 max - how we improve it, and how the various zones of cardiovascular exercise work, and where we get optimal results.

How to look after your joint mobility - and where we should focus to maintain joint function and joint longevity as we get older.

The critical role protein plays in our bodies and how much protein we should think about consuming to maintain our muscle mass

What we can learn from the Blue Zones abot incidental exercise and community

There so much information to absorb in this edition of Prime Time that I couldn’t possibly detail it all here. So have a listen, and subscribe, wherever you get your podcasts.

Enjoy and catch you with a more detailed newsletter on Thursday!

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

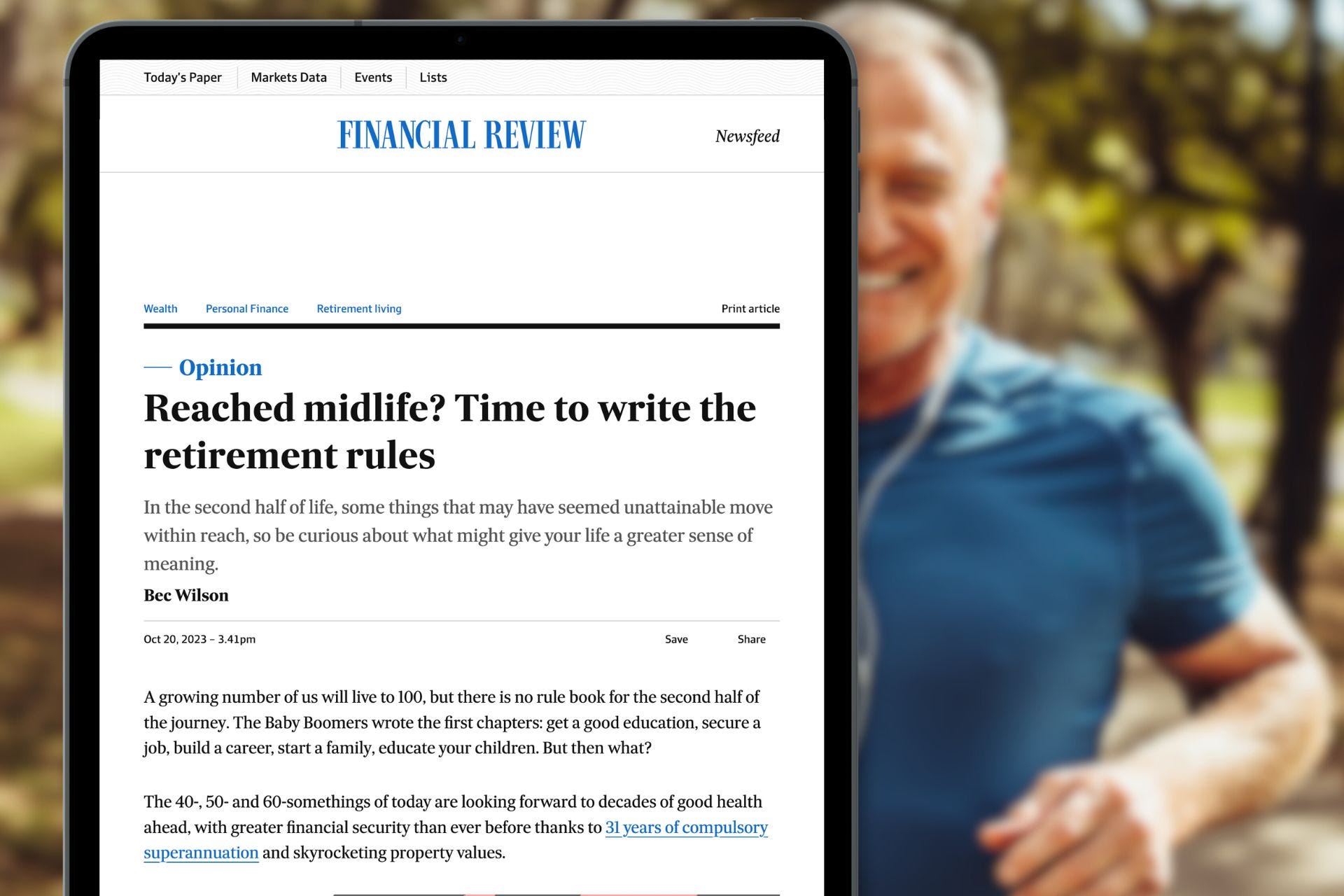

Reached midlife? Time to write the retirement rules

I wrote a feature article for The Australian Financial Review, ‘Reached midlife? Time to write the retirement rules’ which you can read here.

“A growing number of us will live to 100, but there is no rule book for the second half of the journey. The Baby Boomers wrote the first chapters: get a good education, secure a job, build a career, start a family, educate your children. But then what?”

I break down my own view of what I think those rules should be! Let me know your thoughts on the rules in the comments here.

October 21, 2023

Seven things you should think about long before you retire

This newsletter is a bit of a 2-for-1. I didn’t manage to get a newsletter out earlier in the week, so this is a bit of a combo of everything that happened this week…

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

My SMH/Age article in print today

From Bec’s Desk

Prime Time with Bec Wilson - Series 1 Episode 1 (which made it to Apple’s top 50 this week)

Get your copy of Epic Retirement

Seven things you should think about long before you retireEvery Sunday I write a column that is published in the money section of The Age, The Sydney Morning Herald, Brisbane Times and WA Today. And our community asked that I send it out the day it goes to print. So, this week’s column can be read in full here.

We all know retirement has changed fundamentally as current generations tackle it. It’s not a time to stop and sit back anymore, or a time to be put out to pasture by your employer. Modern retirement and the ten or so years leading up to it could, in fact, be the best years of our lives, if we approach them with curiosity and intent. But what do we need to be intentional about?

I launched my new podcast this week with the Nine network, called Prime Time with Bec Wilson. The first episode was a terrific conversation about the seven things I think everyone should know and do before they start changing their life for retirement. These are the most important things to think about before you get to the point where you even start to wind back your workload or shift your way of life.

1. Know how long you really might live. This is a big question. The government says that people who are 65 right now will likely live to the ripe old age of 85 for men and 88 for women. And the intergenerational report takes it one step further, saying today’s 40 and 50-year-olds might live to 89 for men and 91 for women. And those are just the medians – 50 per cent of people will live longer.

It leans heavily back on how you’ve looked after your body so far, and how you intend to look after it in the future. If you plan to look after yourself well, you might want to consider that in your self-picture, so you set the right goals, ambitions and curiosity in place to keep yourself fulfilled over your long life.

2. Decide on some goals. We all have goals in our first half of life but we often overlook setting them for the second half, other than our holiday goals (we’re all pretty good at them). I think it’s a remnant from when we lived shorter lives. But goals are crucial. They move us forward, giving us things to aim for and they set the framework for our budgets, which frankly, we can’t do without.

If you go into retirement without goals you might find yourself rudderless, lost and even ageing unnecessarily fast. So consider at least putting in place some guiding principles for how you want to live your life, and some short and medium term ambitions you aim to achieve and drive yourself forward.

Read the rest of the article here on The Sydney Morning Herald. It’s free to access the article - you may need to register.

From Bec’s DeskAnother week has gone by. And I want to get a bit more personal today. I’m conscious we don’t talk enough about our epic pursuits here, so today I’m going to tell you about one of mine. Pop on over to this post in our Private Epic Retirement Facebook Group and tell me one of yours - in detail. Here’s my post…

I am a bit of a gardener, (or maybe I pretend to be). But my garden is a tale of two zones, in the zone where I pay it attention it’s wonderful, and in other corners where I don’t manage to water, it’s sad. Spring shoots are everywhere on my beloved rose and succulent gardens, into which I pour litres of water each week guiltily, and layer them dutifully with seamungus. And the reward is that the roses are already in their second round of blooms since winter ended and the succulents are throwing off little baby succulents with joy that I can plant out in other spots. I’ve re-constructed my herb garden this week, after it died back in winter. But within days the possums have arrived and shaved all the leaves off my basil and parsley seedlings. I’m trying a natural poultice of chilli and garlic sprayed on them. Anyone got any better tips?

Now, onto the happenings of the week. IT WAS HUGE.

We launched the Prime Time podcast. I’m working with the wonderful team at 9Podcasts on this - and have a listen - it’s top quality stuff. It’s officially called ‘Prime Time with Bec Wilson’ and you can find it and listen to it on any podcast platform. I’ll bang on more about this a bit further down on this email! It actually made it into Apple’s top 50 podcasts on the podcast rankings within 24 hours. What a buzz!

I also had a full video crew takeover my office and turn it into a filming set, for the recording of the How to Have an Epic Retirement online course. We spent two days recording the high quality lessons that will make up the education program. If you want to hear more about it, register here for our expressions of interest, and I’ll send you more details as they unfold.

I wrote a feature article for The Australian Financial Review, ‘Reached midlife? Time to write the retirement rules’ which you can read here.

“A growing number of us will live to 100, but there is no rule book for the second half of the journey. The Baby Boomers wrote the first chapters: get a good education, secure a job, build a career, start a family, educate your children. But then what?”

I break down my own view of what I think those rules should be! Let me know your thoughts on the rules in the comments here.

I’ve absolutely loved doing a few radio shows too - dropping in to chat with Jacqui Felgate on 3AW in Melbourne Thursday afternoon, and Spencer Howson in Brisbane’s 4BC 882 on Saturday for The Sizzle, a ripper of a talkback show too.

I hope you’ve had a lovely weekend! Don’t forget to subscribe for my new podcast, Prime Time with Bec Wilson at www.primetimers.net. It drops every Thursday.

Many thanks! Bec Wilson

Author, columnist, retirement educator, and keynote speaker

Prime Time Episode 1: Seven things you NEED to know before retiringI’m thrilled to invite you to listen to the first episode of the new podcast called Prime Time with Bec Wilson. The podcast has bee created with you in mind. It is designed for everyone who is in the second half of life, which frankly has no rules, because we’ve never lived this long or wanted this much from life before. It is produced in partnership with 9 Podcasts, who do audio really well.

And this is just the first episode! There’s so many more wonderful episodes to come - and they will get better and better! So have a listen and email me with your thoughts on bec@primetimers.net. And be sure to subscribe to the podcast wherever you get your podcasts.

CLICK HERE TO LISTEN ON ALL PLATFORMS

Of go to Apple Podcasts

Or Spotify

Prime TimeSeven things you NEED to know before retiringWelcome to the very first edition of Prime Time with Bec Wilson, the podcast designed to help you live long, live well and squeeze more out of the second half of life! LISTEN HERE Each week I’m going to bring you the very best advice from the leading minds in, well, everything - finance, health, psychology, sex, diet, relationships, travel, superannuatio…Read more3 days ago · 3 likes · Bec Wilson

Prime TimeSeven things you NEED to know before retiringWelcome to the very first edition of Prime Time with Bec Wilson, the podcast designed to help you live long, live well and squeeze more out of the second half of life! LISTEN HERE Each week I’m going to bring you the very best advice from the leading minds in, well, everything - finance, health, psychology, sex, diet, relationships, travel, superannuatio…Read more3 days ago · 3 likes · Bec Wilson

I’m the author of bestselling book, How to Have an Epic Retirement

And that’s it for today. Have a wonderful Sunday. I’ll be back with a full newsletter during the week. I’m still trying to figure out how to get everything timed well for you.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

October 14, 2023

Why it’s time to redefine how we think about retirement

Every Sunday I write a column that is published in the money section of The Age, The Sydney Morning Herald, Brisbane Times and WA Today. This week’s column can be read in full here.

Retirement could be the ultimate financial and personal goal for anyone over the age of 50. But I think it’s time we redefined the word.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

It’s stereotyped as the perfect time of life, when you stop working and can live your life to the fullest, taking long holidays, spending time in the garden and resting. But as we live longer and longer lives, is it practical or sensible to stop working completely? Or should we contemplate a different way of thinking about retirement, one that sees us retire more gradually and enjoy the period before retirement as much as the period after it?

My suggestion is that we all start to think about retiring as a stepped process that gradually moves us along a retirement continuum, slowly and incrementally morphing our way of living, and our income into a retired state over many years, if we can. That would allow us to enjoy the benefits of work, like social engagement and pursuit of meaning, which have been shown to positively impact our health and wellbeing.

At the heart of this continuum is the definition of modern retirement. I define modern retirement as the time in life when we can afford to live off various sources of passive income and choose what we do with our time. That choice should, where possible, include staying in the workforce if we like, both for financial and personal reasons.

But it would be a choice at that point, not an obligation or need. And for it to be a choice we need to have a level of financial confidence and security, which most people establish over time, as they learn to live on their combined income from the age pension, superannuation account-based pension and investment incomes.

Think about how the continuum really could work for you. At the beginning of the continuum you might still be engaged in traditional full-time work, but you know you can start to draw some income from more passive sources. You might start by dropping a day a week of work to spend with a grandchild or participating in community activities you really enjoy and build confidence in living on that smaller passive income while still earning a wage for four days.

Full and structured retirement might not actually be the ultimate goal for incoming generations - but living a life of choice can be.

Then, months or years later, you might drop a second day, or even a third, picking up hobbies you love, spending more time on your health, or in your community. Maybe you even start a small business.

As you move down the retirement continuum, you can pursue less and less formal work, but you don’t necessarily have to stop working. There are plenty of options for part-time work, flexible work arrangements, and reduced hours allowing you to take longer sabbaticals too. The key is that you don’t have to put yourself into full retirement to have balance and leisure time in your life.

There are two small problems with this under the current rules. The first is that the government currently requires a rather rigid shift into retirement to move your superannuation into retirement phase. But, the reality is that you only have to meet the conditions of release once in your life to move your superannuation into a state where it can provide that income. And before that, you could consider a transition to retirement pension.

The second is that once you reach pension qualification age at 67, your pension income will decrease after you earn more than $11,800. To me, this just becomes an important time for a cost-benefit analysis that takes in how you value work in your life, both financially and from a fulfilment perspective.

This article continues. Read it here on the Sydney Morning Herald. It’s free to access the article - you may need to register.

And just in case you missed it, here’s a link to this week’s Epic Retirement Newsletter.

Epic RetirementWelcome to your Prime Time 🌞 Do you know what your real purpose is? In this week’s edition: A big announcement: the launch of Prime Time with Bec Wilson 🥳 Article: Do you know what your purpose is? Join Prime Time with Bec Wilson on social Book: A titbit…Read more3 days ago · 1 like · Bec Wilson

Epic RetirementWelcome to your Prime Time 🌞 Do you know what your real purpose is? In this week’s edition: A big announcement: the launch of Prime Time with Bec Wilson 🥳 Article: Do you know what your purpose is? Join Prime Time with Bec Wilson on social Book: A titbit…Read more3 days ago · 1 like · Bec WilsonI hope you’ve had a lovely weekend! Don’t forget to subscribe for my new podcast, Prime Time with Bec Wilson at www.primetimers.net. It launches Thurdsday!

Many thanks! Bec Wilson

Author, columnist, retirement educator, and keynote speaker

Introducing our new podcast: Prime Time with Bec Wilson

Introducing our new podcast: Prime Time with Bec WilsonOur late forties, fifties, sixties and even early seventies are our Prime Time! These are our best years. Grab them with both hands! Understand how money, meaning, health and happiness works so you get the best out of them. Join me weekly! It's free

How to Have an Epic Retirement is the ultimate guidebook for modern retirees. It is grounded in my own widespread research on modern retirement, and draws on my prior ten years as the CEO of Starts at 60 and Travel at 60 (before I stepped away to pursue my next career in retirement education). It also draws on the work of the leading thinkers in the longevity, health, happiness, purpose and modern ageing spaces and incorporates many interviews with people who have navigated the sometimes challenging path into retirement.

How to Have an Epic Retirement is officially a bestseller in Australia! You can buy it at all major booksellers. Or get your copies at one of the largest online booksellers below.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

October 11, 2023

Welcome to your Prime Time 🌞 Do you know what your real purpose is?

A big announcement: the launch of Prime Time with Bec Wilson 🥳

Article: Do you know what your purpose is?

Join Prime Time with Bec Wilson on social

Book: A titbit

A big announcement: the launch of Prime Time with Bec WilsonThe moment is finally here. I am thrilled to announce a BIG new project, the launch of the podcast called Prime Time with Bec Wilson. But before I tell you all about it, I want to explain where it comes from. (Humour me!)

My world has been undergoing a delightful transformation, and maybe yours has too. As my kids started spreading their wings and becoming more independent, I found myself with a sense of nervous freedom. And I’m calling it. I’m a few months past 47.5 right now and I think this is the beginning of the best bits of life, the start of what I’m calling affectionately my Prime Time. Almost all of you here are already in yours.

Now don’t get me wrong, I love my kids. I don't even want an empty nest at this time - I love them popping in and out, ignoring my requests to tell me if they don’t want dinner.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.

I know from watching all of you in your 50s, 60s and 70s planning for and living out your epic retirements, that the years ahead can be the best years of our lives, if we get out of our own way and live them to the fullest.

But, here's a nugget of wisdom I've gathered from watching you: we need to start discussing the steps we should take to lead a longer, healthier, and higher quality life way before the typical "retirement age." We need to extend the concept of our "best years" to encompass the 10-15 years BEFORE retirement, when we have more financial flexibility to shape our lives into this exciting next stage.

So, as I mentioned, I'm giving this stage of life a new name. I'm calling it our PRIME TIME of life. For me, it begins at the powerful age of 47.5 and stretches all the way through and well into to our EPIC RETIREMENT. And there's solid science backing this up.

Research involving more than a million people in the western world says that 47.5 is the bottom of the U-curve of happiness. (Which you can read about in the book).

It's around this age that many people start realising that the career climb, even if they scaled to the top, might not be the ultimate goal. They begin to understand that their work and the reasons they wake up each morning can be more meaningful if they choose.

Around the same time, many of us start seeking more from life than just "more stuff" and "more career achievements." We yearn for meaning, purpose, relationships, and above all, health. And wouldn't you know it, these are the very things that research shows lead to longer, happier lives! Of course, we can only do that if we have financial confidence, so we have to have that too.

And, if we start talking about this stuff from 47.5, and we keep talking about it we naturally arrive in our epic retirement with plenty of fuel in the tank. We get there healthier, more financially secure, more fulfilled by our work, and more secure in what we want from our relationships. And that places us in the enviable position of choosing how we spend our time—perhaps embarking on longer trips, working part-time, and gradually easing into retirement at our own pace. Sounds like a much better way to approach the second half of life, doesn't it?

So, today is the big reveal. Today I’m introducing PRIME TIME, a high-quality podcast that I've had the joy of producing in partnership with the Nine Network. This podcast is for all of us in the second half of life who want to live long, live well, and thoroughly enjoy it.

I get to ask ALL the questions. I want to dive deep into what will make this phase of life absolutely fantastic, with insights from experts and pioneers. After all, there are no set rules for navigating this second half for our generations. Just 50 years ago, we expected to live till around 70. Today, we could live well into our 90s! We're the first generations with such long lives and such grand expectations for the second half.

Let's figure out how to live the SECOND HALF of our lives well. So, come with me and let’s explore what our Prime Time can look like, together.

I invite you to listen to the trailer here: It’s just launched. The first full edition will be released NEXT THURSDAY the 19th OCTOBER 2023.

LISTEN TO THE PRIME TIME PODCAST TRAILER HERE

Make sure you FOLLOW or SUBSCRIBE on your chosen podcast platform.

Now, for some logisticsNext week I’ll be launching a NEW weekly newsletter called PRIME TIME that is just for the podcast (you can click through and visit it at primetimers.net anytime), and you’ll all receive it. It will go out on Thursdays. Please, share it with your friends!

That means, Epic Retirement’s weekly newsletter will flip to being released in the first half of the week - probably Mondays or Tuesdays as time and juicy topics allow!

And I’ll send you my syndicated national newspaper column which is featured on the Sydney Morning Herald, The Age, Brisbane Times and WA Today over the weekend in a simpler Epic Retirement email too, so you get it while it’s hot.

Read on, I’ve got a helpful little titbit for you this week on the power of finding your purpose.

If you love the concept of the Prime Time podcast, or have thoughts on your ‘purpose’ drop me an email at bec@epicretirement.net.

Please, have a wonderful week and make it epic!

Many thanks! Bec Wilson

Author, columnist, retirement educator, and keynote speaker

Do you know what your real purpose is?It sounds awfully profound to ask you this question. But for some people it’s a really easy question to answer. They feel a true sense of who they are and why they are here. For others it feels like ethereal bullshit.

So I’ll ask a simpler question. “Why do you get up in the morning?” or even “What drives you to do things each day?”.

In the working years of our lives this identity and sense of purpose is often tied up in going to work, and meeting your expectation-led family and career goals. But when you leave your job, or start reaching toward retirement this can disappear, or seem much less important. So I want you to look deeper.

Your true purpose and values can’t be stripped away by leaving your job. It’s built around what you find real meaning in.

According to the gurus of purpose, having a clearly understood purpose can add years to your life. It can also add a buzz, or a sense of momentum. But how do you know what yours is?

Many people in the middle of life or at a point of significant transition like retirement often wonder what their purpose is, and plenty wonder at whether they have actually found their purpose earlier in life at all. They ask themselves questions like:

Do I know what I want or need to feel happy on the inside?

Have I missed my calling in life? Can I find it now?

Is this all there is to my life? Surely there’s meant to be more?

If this is you, there’s a couple of helpful steps that Victor Frankl, a holocaust survivor and popssibly the world’s most recognised leader in finding life’s meaning, says could help you explore your own purpose.

“We can discover this meaning in life in three different ways”, he said:

(1) “by creating a work or doing a deed”;

(2) “by experiencing something or encountering someone”; and

(3) “by the attitude we take toward unavoidable suffering" and that "everything can be taken from a man but one thing: the last of the human freedoms – to choose one's attitude in any given set of circumstances"

Think about this in the context of your own life and how you have managed to find a sense of meaning and value in other phases.

“Doing a deed or creating a work” is said to be achieved by doing deed or creating work which moves us emotionally, and this can be in our family, community or within an organisation we are passionate about. The important thing to note is that the deed doesn’t need to be noticed by others to be worthy of a sense of purpose and value. In fact, if we are doing it to be noticed, that may show a lack of real purpose behind it.

Ask youself - is there a deed or a work that seems important or needed to you?

“By experiencing something or encountering someone”. Another way of saying this is having a relationship with something or someone. It is centred around our sense of real relationships with family and community. We know how important it is to feel like we belong, and to love and be loved in our lives. And this is one of the pivotal ways we can achieve a sense of purpose.

Who do you treasure and want to spend time with in your life? Which people and which communities?

And finally, “by the attitude we take to unavoidable suffering”. This can be said another way as how we find courage during difficult times. So how do you respond to suffering? As Frankl said, “even the helpless victim of a hopeless situation, facing a fate he cannot change, may rise above himself, may grow beyond himself, and by so doing change himself.”

Sometimes suffering can cause us to revisit our own stories - the stories we tell ourselves about what matters to us, and sometimes it can drive us to reconstruct our stories. Sometimes it is necessary to reconsider what’s important so we can move forward.

Follow Prime Time with Bec Wilson on socialThe Prime Time with Bec Wilson podcast will have some new social handles, and we’d love to play with you on social media.

Pop on over to our very new and fresh Instagram and Facebook pages and be a part of it all. Our little excerpts and lessons will be posted here from next week.

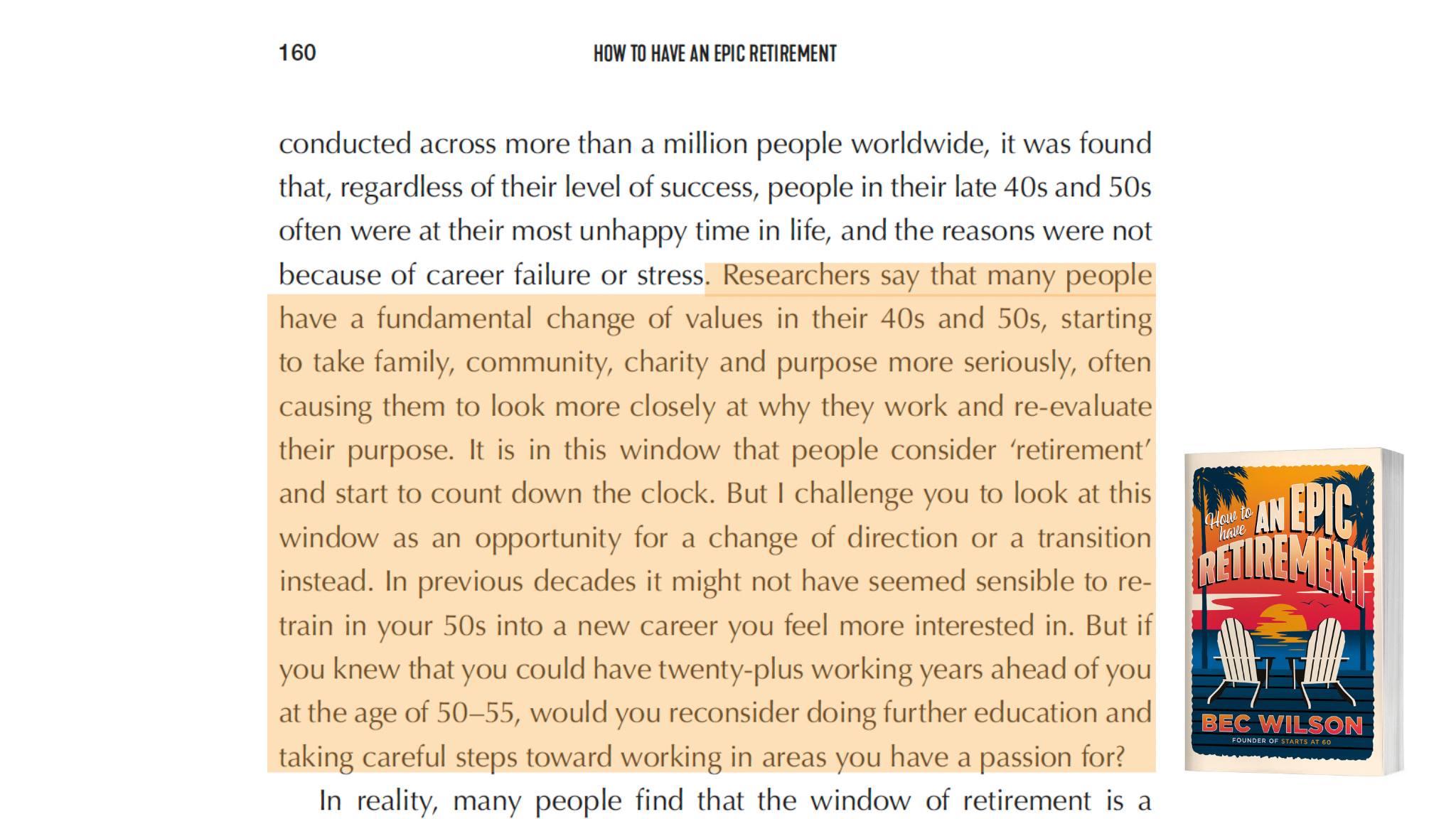

How to Have an Epic Retirement: a helpful titbitFrom page 160: Happiness and Fulfilment

Given our topic today on purpose, this short challenge from the book seemed a good one to leave with you today. Enjoy Xx

“Researchers say that many people have a fundamental change of values in their 40s and 50s, starting to take family, community, charity and purpose more seriously, often causing them to look more closely at why they work and re-evaluate their purpose. It is in this window that people consider ‘retirement’ and start to count down the clock. But I challenge you to look at this window as an opportunity for a change of direction or a transition instead. In previous decades it might not have seemed sensible to retrain in your 50s into a new career you feel more interested in. But if you knew that you could have twenty‑plus working years ahead of you at the age of 50–55, would you reconsider doing further education and taking careful steps toward working in areas you have a passion for?”

About the book

How to Have an Epic Retirement is the ultimate guidebook for modern retirees. It is grounded in my own widespread research on modern retirement, and draws on my prior ten years as the CEO of Starts at 60 and Travel at 60 (before I stepped away to pursue my next career in retirement education). It also draws on the work of the leading thinkers in the longevity, health, happiness, purpose and modern ageing spaces and incorporates many interviews with people who have navigated the sometimes challenging path into retirement.

How to Have an Epic Retirement is officially a bestseller in Australia! You can buy it at all major booksellers. Or get your copies at one of the largest online booksellers below.

Thank you for reading Epic Retirement. This post is public so feel free to share it.

Thanks for reading Epic Retirement! Subscribe for free to receive new posts and support my work.