Bec Wilson's Blog, page 3

April 5, 2025

Retirement panic? Here’s how to stay steady when the news gets noisy

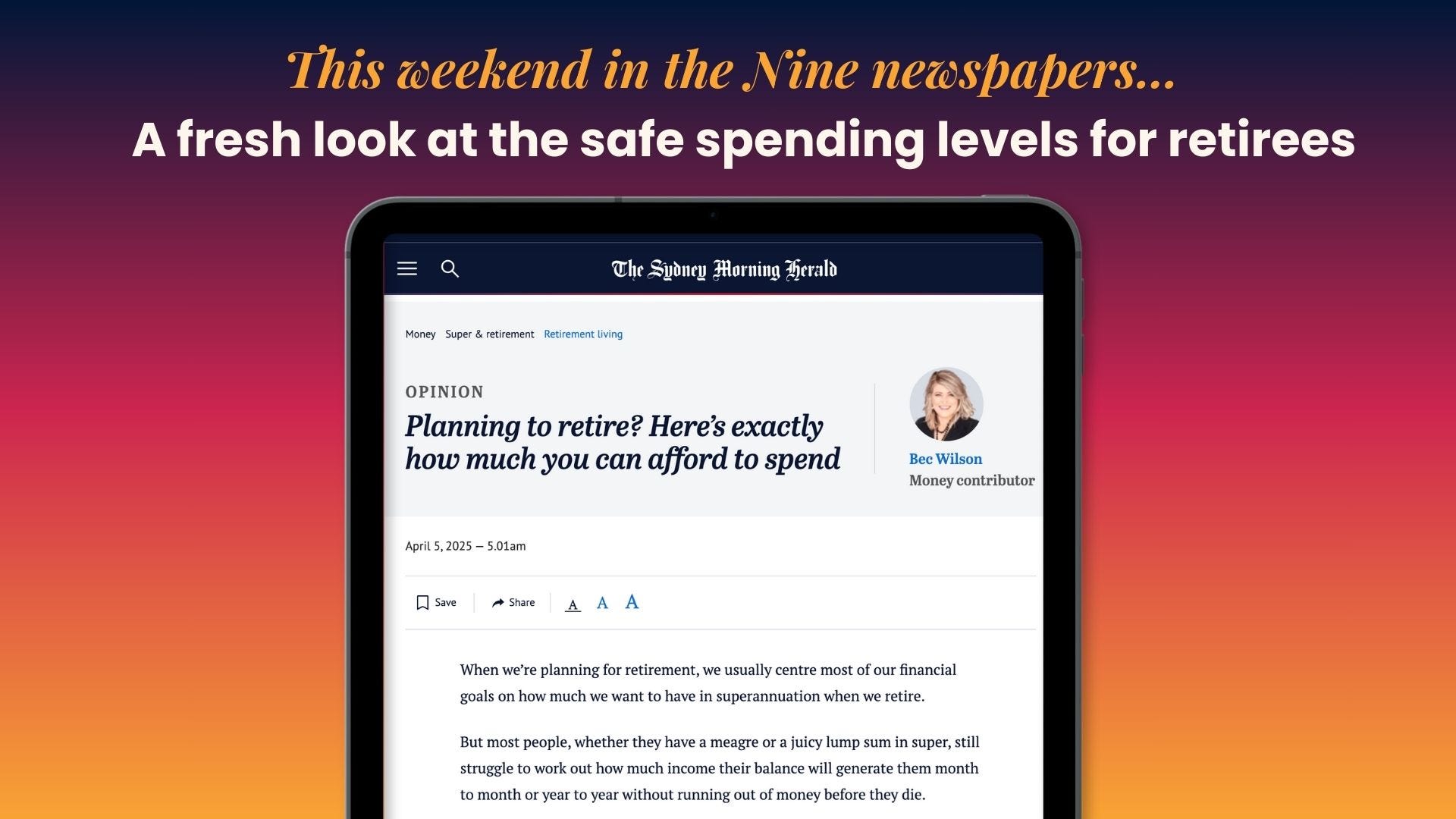

Newspapers: Planning to retire? Here’s exactly how much you can afford to spend

Feature: Retirement panic? Here’s how to stay steady when the news gets noisy

Podcast: Do you want to retire early?

From Bec’s Desk: A wild wild week!

Now, an important promotion for Winter course!

We’re getting ready to kick off – are you in?

The How to Have an Epic Retirement Flagship Course kicks off on the 10th April, and we’re sending out the welcome packs this week to everyone who's coming along. It’s six weeks of practical, engaging, real-life retirement planning—designed to help you feel more confident, more in control, and ready to shape your next chapter.

Here’s what’s included:

Six weeks of well-structured online learning, delivered across 14 modules

Six live Q&A events with some of Australia’s top retirement experts (mostly Monday nights, with a break for Easter)

A professionally published, 150-page workbook—exclusive to participants

A signed copy of How to Have an Epic Retirement

And a few surprises along the way

This course gets rave reviews. In fact, 100% of participants in the most recent intake said they’d recommend it to a friend—and they told us their retirement confidence had significantly improved thanks to the program.

📥 Download the brochure here

📅 Book your place here

I’ve got a coupon code that will give Epic Retirement Newsletter subscribers 15% off the RRP if you missed the earlybird deal: LASTCALLW25

Here’s a fresh new testimonial from our Autumn program that only wrapped up last week! 😎

“I found this course to be a breath of fresh air in the retirement space. Bec and her team provide you with a holistic experience that doesn't just cover th financial aspects of retirement. It delves into budgeting (and provides some fantastic resources in this area), retirement planning, mental wellbeing, health and ageing and travel. In the process she enlists the help of experts in these various fields. the workbook she provides is very professional and extremely helpful. After completing the course I have a much better idea of what my epic retirement will look like AND what I need to do to make sure it happens. Thank you so much Bec and all the other experts we spoke to in our course. You guys are making a real difference for pre-retirees and retirees.”

Retirement panic? Here’s how to stay steady when the news gets noisy

Retirement panic? Here’s how to stay steady when the news gets noisyPeople approaching retirement in Australia are feeling a little bruised and nervous this week – or most of them awake at the wheel are anyway. Liberation Day in the USA where Trump implemented the biggest changes to tariffs in a long time has left markets in freefall and the (somewhat unnecessary) media storm around a co-ordinated cyberattack on our superfunds and subsequent rush to login to super websites to check balances and bank details has seen them falling over for members for nearly two days.

So today I’m going to focus on the calm steps you can take if you’re feeling rattled, to reclaim a bit of control, protect what you’ve built, and remind yourself that short-term chaos doesn’t have to derail your medium and long-term retirement plans.

Here’s what to focus on:

1. Don’t make panic movesThis is the golden rule. When markets tumble, it’s tempting to jump online and switch your super to cash — but that often just locks in losses and leaves you on the sidelines when the rebound comes (and it usually comes quicker than expected).

Instead, pause. Your fight-or-flight response is real — but so is the mountain of evidence showing long-term investors come out ahead. Let the adrenaline fade. Give your amygdala a moment to stand down, and let your prefrontal cortex take the wheel — that’s the part of your brain that handles logic, planning and clear-headed decisions – but it takes longer to kick in when there’s panic.

2. Check your mix, not your balanceIt’s natural to be afraid to peek at your super balance after a rough market week — but you must remember, the number alone doesn’t tell the full story. What matters more is how your money is allocated. If you’re within a few years of retirement, it might be time to start thinking in buckets.

A bucket strategy breaks your super into two or three parts and allocates them to a suitable risk level for the horizon they will be needed. Here’s an example. But get some advice as this differs depending on your situation.

Short-term bucket for the next 2–3 years of income (usually in cash or lower-risk assets)

Medium-term bucket for the next 3–7 years (in stable, income-generating investments)

Long-term bucket for money you won’t need for a decade or more (still in growth assets like shares)

If you’ve already got a mix like this, great — you can ride out the storm with more confidence. If you don’t, your next step might be as simple as making sure you’ve got the next 1–2 years’ worth of spending tucked away in cash. That breathing space gives your long-term investments time to recover, without you needing to sell at the worst possible moment.

3. Remember: the super system is robust — but your passwords matter tooThis week’s headlines made it sound like hackers were swarming the gates of every super fund and balances were vanishing into thin air. The reality? According to the funds, only four people lost money — and even then, it was through targeted breaches, not mass theft.

Super funds have strong, multi-layered cyber protections. The so-called “co-ordinated attack” turned out to be more disruption than destruction — with websites crashing under the weight of concerned members all rushing to check their balances and personal info. Frustrating, yes. But not a sign your money was missing.

If you’re worried, the best action you can take isn’t to panic-refresh your balance — it’s to update your login / password details. Strong, unique passwords (not the same one you use for everything!) and two-factor authentication are your best defences – they really are. Super funds are holding up their end of the bargain — we just need to do the same on ours.

4. Stay focused on your planIf you’ve got a plan — whether it’s retiring at 65, downsizing at 70, or drawing down slowly over 30 years — a few rough weeks on the market doesn’t undo it. Your strategy was never meant to hinge on a single news cycle. That’s the whole point of having a plan: it gives you something solid to stand on when everything else feels a bit shaky.

If you don’t yet have a clear plan? This is your sign to make one. Knowing where your income will come from, how you’ll use your super, and how much you actually need to live well in retirement makes a huge difference — especially when the headlines are screaming.

And a plan doesn’t have to be complicated. It can start with three simple questions:

What will I live on in the first 5–10 years of retirement?

How will I draw from my super over time?

Do I have a buffer to ride out the bumps?

When you can answer those — even roughly — you’re already in a better place than most. The goal isn’t to time the market perfectly. It’s to move forward with confidence, knowing your plan can handle a few speed bumps along the way.

5. Talk to someone (real, not just to people on social media where the drama is high)Your cousin on Facebook might be shouting about moving everything to gold or crypto — please don’t follow the herd (or even listen to them). If you’re feeling unsure, it’s a great time to book a chat with your super fund’s advice team (make an appointment when their website is back online ideally) or to speak to a licensed financial adviser. Many funds offer free advice on your investment options. Others offer a first appointment free on your retirement planning. Ask them what’s available to get you started.

It was a wild wild week (in markets, funds and real life). Mine started in Byron Bay, presenting to the Sales Team Conference for Ingenia Lifestyle Communities about how they can make retirements epic. Then, back to Brissy to prepare for our Epic Retirement Winter course launch this week. All the workbooks have been mailed — and we’re ready to launch the course content on Thursday at noon.

I’ve recorded a few fun podcasts this week — the first of which came out on Thursday with Drew Meredith, from Wattle Partners. A really pragmatic chat about the things you need to know if you’re thinking about retiring early. Have a listen (details below).

I’ve done a huge article for The Age and The Sydney Morning Herald — on safe spending levels, with help from the Challenger team who are known for their great data on this.

And finally — I bumped out a last minute newsletter on Friday afternoon all about the Cyberattack on Australian Super Funds because so many people were worriedly posting pictures of their superfunds’ websites ‘down’ on Friday. I investigated — chatting with the affected funds and they were keen to make sure the message got out about how website traffic was the problem not ongoing attacks.

In the week ahead we’re going to be unveiling the book cover for Prime Time, my next book, so watch this space… it drops on Wednesday I believe. I am a little excited to hear your thoughts!

Got some thoughts about the topics this week — leave a comment or write me an email. I love to hear from you!

You can always email me at bec@epicretirement.com.au.

BTW — my puppy is improving — slowly slowly. Still running a dog-care centre as I write!

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Planning to retire? Here’s exactly how much you can afford to spend

Planning to retire? Here’s exactly how much you can afford to spend

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 6th April 2025.

When we’re planning for retirement, we usually centre most of our financial goals on how much we want to have in superannuation when we retire.

But most people, whether they have a meagre or a juicy lump sum in super, still struggle to work out how much income their balance will generate them month to month or year to year without running out of money before they die.

You’re not alone if you look at your super balance and think, “I wonder what that amount actually means for me year to year?”

Well, today I’m going to answer that, and the short answer is … it depends. It depends on how long you live. It depends on how your investments perform. It depends on whether you’ll be eligible for the age pension and, if so, how much. And it depends on how your spending patterns change over your lifetime – as you move from your epic retirement years into ageing and frailty.

None of us know the answers to these questions with certainty, but we can lay out a reasonable plan and project a sustainable amount that would be appropriate to spend year to year using solid assumptions, realistic simulations and a bit of planning discipline.

The financial services industry quite commonly uses what’s called a safe spending rate – basically, the amount you can withdraw from your super each year, with a high probability that your money will last as long as you do.

A couple with a starting balance of $600,000 in account-based pensions could spend $65,300 per year.

This isn’t about squeezing every last dollar out. It’s about setting a pace of spending that supports a great lifestyle and reduces the chance of running short in your later years.

A good safe spending calculation should take in a conservative view of your life expectancy in case you live a long time. It will build in inflation adjustments to your spending, so your income keeps pace with rising prices, and it will have an expectation that the performance of markets will vary over the years. (READ ON… here in The Age, The Sydney Morning Herald. )

Do you want to retire early?

Do you want to retire early?Thinking about pulling the pin early on work? This episode of Prime Time dives deep into what it really takes to retire before 60 — and why it’s not just about scrimping and living on two-minute noodles. Bec is joined by wealth expert Drew Meredith from Wattle Partners to unpack what financial independence truly means, who early retirement suits, and how to actually fund those golden years (and silver ones, and legacy ones too).

Whether you're aiming to leave your job in your 50s or just want more lifestyle freedom, this episode is packed with practical guidance, honest perspectives, and a few laughs about budgets, buckets, and breaking free from the grind.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:Last of all, if you haven’t read the book, you can order your copy from Amazon online. Or pick up a copy at your local Big W, Dymocks, or QBD stores. And if your bookstore doesn’t have it - ask them to get it in. It’s still regularly in the Amazon Top 200.

I have a little online store where you can purchase signed copies too.

Before you quit your job and sell the house... read this!Everything I share here is general information, not personal financial, legal or tax advice. It hasn’t been tailored to your specific life, goals, money situation, or brilliant retirement plans—so before making any big decisions, please chat to a licensed financial adviser or relevant professional who can look at your individual circumstances.

I do my best to keep things accurate and current, but I can’t guarantee it (rules change, governments shuffle things around, and I’m only human). Any figures or examples are just that—examples—to help explain things, and they might not reflect the latest laws or your actual numbers.

Use this as a helpful guide, not gospel.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

April 3, 2025

Super fund cyberattack: Things you should know

At around 1:45pm today, several Australian superannuation funds confirmed they had been targeted by what appears to be a co-ordinated cyberattack. Media alerts lit up across the country — and understandably, members are concerned. Many are rushing to check their super balances, including many who are logging in for the very first time.

While the timing of the announcements might suggest a recent incident, conversations with media representatives from the funds reveal the attacks have been occurring over several weeks, not just in the last day or two.

Which funds are affected?Media reports and direct confirmations indicate that AustralianSuper, Insignia, REST, Hostplus, and ART (Australian Retirement Trust) have all been affected.

Each of these funds is urging members to log in and check their superannuation accounts, including:

Verifying account balances

Reviewing linked bank accounts

Confirming that no account details have been changed

Important note: this is creating massive traffic and massive delays on websites and web infrastructure.

‼️ Massive traffic, massive delays ‼️This advice has created a wave of pressure on super fund websites across the country. Many funds rely on shared secure infrastructure, and the volume of concerned members trying to access their online portals has been overwhelming.

Thousands of members are now reporting:

Inability to log in

Error messages or zero balances showing (which is an issue when the front end and back end of the website struggle to connect)

Login pages timing out completely

I contacted several funds directly, and the consistent message is this: the traffic from concerned members is crashing servers, not the cyberattack itself. Funds are asking members to remain patient, and to understand that website outages are largely due to volume, not system compromise.

Who is most at risk?Importantly, the only members currently at risk of money being withdrawn are retirees or those who have unrestricted access to their super accounts. For most members—especially those still working—there’s no facility in place for lump sum withdrawals, which means the risk of actual funds being stolen is very low.

What are the funds saying?From what I’ve been told by two of Australia’s largest funds, the scale of the attack is limited, and they believe it has been largely contained. We are still awaiting public statements from some of the other funds. ART says they have contacts ALL members affected.

Here’s what we know so far:

AUSTRALIAN SUPERAround 500 accounts have had details changed

Only 4 accounts have reported actual financial losses

The total value of funds withdrawn: around $500,000

ART (Australian Retirement Trust)Two waves of attempted attacks

Up to 8,000 accounts were targeted

No money has been withdrawn

ART has emphasised that their security systems triggered early and effectively stopped funds from being accessed.

HOSTPLUS“We are actively investigating the situation to determine the facts and the extent of any impact to Hostplus. Whilst the investigation remains ongoing, we can confirm that no Hostplus member losses have occurred.”

What should you do?If you're a member of one of the affected funds:

Try logging in when website traffic is lower (outside peak hours)

Check your account details and linked bank accounts

Contact your fund directly if you see anything unusual

Above all—stay calm. The situation is being monitored closely, and the funds are working hard to keep accounts secure. For most members, the risk remains low.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

March 29, 2025

Why spending in retirement doesn’t drop the way some expect

Newspapers: As we head to an election, does either party care about retirees?

Feature: Why spending in retirement doesn’t drop the way some expect

Podcast: April 1st is coming - time to check in on your health insurance

From Bec’s Desk: A week of travelling

Now, an important promotion for the upcoming course …

The next How to Have an Epic Retirement 6 week flagship course kicks off on the 10th April. And if you want the 25% off earlybird price then you’ll need to book in the next 48 hours. BOOK HERE | DOWNLOAD A BROCHURE

Our last course has just finished — look at some of the feedback coming in:

Thank you for your positive and vibrant delivery of your modules within this course. Clear, concise and to the point, that is not easy to do when you need to cover so much information to a wide audience at different levels of their Epic Retirement. Well Done and Thank you. Your passion to help inform people on all the important topics have been invaluable and the knowledge I have learnt will certainly prepare me for my Epic Retirement.

The course is amazing. Well structured, great content, Bec is very clear and it is easy to understand her message. There is so much to take in, very happy that we also have the workbook and paperback version to take and make notes as we go.

Great course. Bec you are really offering an amazing service. Thank you. I love your entrepreneurial bent is also providing such a helpful service.

The course is interesting and well designed and the concepts clearly articulated. Picked up interesting facts from Q&A sessions too.

Why spending in retirement doesn’t drop the way some expectAnd why that’s not necessarily a bad thing

One of the biggest myths in retirement planning is that your spending will magically drop the moment you stop working.

Some in the retirement industry will even tell you that your expenses should fall to 80% of your pre-retirement budget almost overnight. But today I want to give you a different perspective—especially if you’re part of the new generation of retirees who want more from retirement.

There’s a long-held idea that once the mortgage is paid, the kids have left home, and the office clothes are packed away for good, your cost of living will shrink dramatically.

And sure, for some people, that happens. But here’s the truth that doesn’t get talked about enough: for many others, spending doesn’t drop—it just shifts. And often, what it shifts toward is a whole lot more epic.

I call it your epic experiences budget. It’s the part of retirement spending that isn’t about your basic needs—it’s about living well. And if you don’t factor it into your planning, you might find yourself short on fun, not just funds.

Retirement doesn’t shrink your spending. It shifts it.There are plenty of things you stop spending on when you leave work. The daily commute. Takeaway lunches at your desk. Expensive work clothes. The Friday night drinks you were too tired to enjoy anyway.

But once you have more time and more freedom, you start spending in new ways. And those ways often bring more joy, connection, and meaning. Here’s what we often see:

Travel spending takes off.

The first 5 to 10 years of retirement are often the most active. People start ticking off wish lists—walking the Camino, seeing the Kimberley, caravanning around Australia, or taking that long-awaited Europe trip. Even smaller, regular adventures—weekend getaways or visits to the grandkids—can add up quickly.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

More spare time = more discretionary spending.

When you’ve got time, you say yes to things you enjoy. You might join a wine club, take up a hobby, go to concerts or festivals, or do that $1,000 course you've always been curious about. Time creates space for spontaneity—and that can come with a price tag.

Helping loved ones becomes a new priority (if you can afford it).

Many people in their 60s and 70s choose to support their families—helping with school fees, gifting cash for a home deposit, or paying for a family holiday. It’s not expected, but it’s part of the way some people want to spend their money: generously.

Comfort, convenience, and quality of life start to matter more.

You might decide to pay for a cleaner, upgrade appliances, or renovate instead of downsizing. For those who can afford it, spending isn’t about indulgence—it’s about easing into this new chapter with more comfort and less stress.

Of course, not everyone can afford all of these things.

But that’s exactly why it’s worth talking about—because even if you can’t do everything, you might still want to do something. And planning for joy, at whatever scale is realistic, helps you avoid being caught off guard.

So why are we still planning as if we’ll spend less?The idea that retirement equals frugality is outdated. It’s based on a different era—when people worked until 65, lived until 75, and moved through a single, slower retirement phase. And most people back then were dependent on the age pension.

But today? Retirement is more like a series of life stages.

You’ve got your prime time years, often before you fully retire. Then come your epic retirement years—the active, energetic phase when travel and fun take centre stage. After that come the ageing years, where things slow down a little, followed by the frailty phase, where support becomes the priority.

Each stage has its own spending pattern. And that’s why a flat, fixed number doesn’t make much sense anymore.

Here’s how to plan for your epic goals:Be honest with yourself about your lifestyle goals.

Retirement isn’t about cutting back—it’s about living well on your own terms, (and living within your means). Start with your vision, not a generic budget spreadsheet.

Model your spending in stages.

Think of your retirement in 5- to 10-year blocks. Your travel budget at 65 will likely look very different from your needs at 80.

Build flexibility into your retirement income.

Whether it’s super drawdown, investments outside of super, or part-time work, the more flexible your income, the easier it is to say yes to the moments that matter.

Stop guilt-tripping yourself for spending on joy.

This is exactly what you saved for. Joy isn’t a luxury—it’s part of a life well lived.

Your epic retirement isn’t about spending recklessly—it’s about spending intentionally, on the things that bring you joy and connection.

Plan for the kind of retirement that reflects you—not the version someone else predicted you’d need.

I kicked off the week with our final live Q&A for the Autumn Edition of the How to Have an Epic Retirement Flagship Course on Monday night. It was an absolute ripper—an energising session all about travel and getting amazing value on your adventures, featuring the fabulous Fiona Dalton.

After that, my week was mostly spent in Melbourne, filming course content and then making podcasts in the Nine studios. A joy to do!

My little 12-year old puppy continues to make progress — so we’re hopeful he’ll get his mobility back soon.

And now, in the week ahead I’m packing our welcome packs for the How to Have an Epic Retirement Flagship Course for Winter — which kicks off on the 10th April. Not long now! And off to Byron Bay for a corporate event too. The earlybird 25% off ends Monday. Make sure you lock in your place. More information here:

Download our new brochure here

And don’t forget — you can book for a couple with just one ticket and just buy an extra workbook on the way through so you can each still work through your dreams as individuals, alongside each other.

This week on the Prime Time podcast we focussed on health insurance — given everyone’s premiums are due for a price rise on 1st April; and depending on your policy, the increase could be even higher. So I sat down with Sally Tindall from Canstar for a discussion to explain health insurance and what you need in this phase of life.

Got some thoughts about the topics this week — leave a comment or write me an email. I love to hear from you!

You can always email me at bec@epicretirement.com.au.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

As we head to an election, does either party care about retirees?

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 30th March 2025.

If you really understand how money works in retirement, you might be wondering – does anyone in Canberra even know retirees and pre-retirees exist?

This year’s budget and budget reply were clearly targeted at families and younger workers, with little more than crumbs offered to midlife and older Australians.

Despite making up more than 50 per cent of the voting public, older Australians once again got treated like a bolted-on voting bloc. Taken for granted. Overlooked. Politically invisible.

Let’s unpack what’s on the table, what’s missing, and whether either side has really shown up for the generations who built the economy and are now trying to retire with dignity. And let’s remember – with the election only announced this week – there’s still time for the major parties to step up and serve older generations better. It could be the difference required to gain the balance of power.

1. Tax cuts: nice headline, but most retirees won’t see a centThere’s a lot of talk about “everyone” getting a tax cut in the Labor budget and legislation subsequently rushed through. But here’s the truth: You only benefit if you’re paying tax. And most retirees don’t.

As always, if you’re trying to retire with dignity and independence, you’re expected to just figure it out.

In practice, many self-funded retirees, and most full-rate (and many part-rate) pensioners pay no tax at all. That’s thanks to the tax-free nature of retirement income streams from superannuation, and the tax-free threshold plus offsets like the Seniors and Pensioners Tax Offset (SAPTO) and the Low Income Tax Offset (LITO), which lift the effective tax-free thresholds to above the age pension.

And let me tell you – that doesn’t mean ‘they’re loaded’ or don’t feel the pinch from the cost of living rising.

So unless you’re earning additional taxable income – from part-time work, rent, or super in accumulation phase – you won’t benefit from tax cuts Labor has promised for 2026 and 2027 at all. For many retirees, this is just another headline that sounds good but means nothing in reality.

2. Deeming rate freeze: one quiet win (for now)Labor’s decision to freeze deeming rates until 30 June 2025 is a meaningful win for pensioners with financial assets. Deeming is how Centrelink guesses the return you’re earning on your savings, and it affects how much pension you get if you’re assessed using the income test.

The rates are still artificially low (0.25 per cent and 2.25 per cent) – so retirees with term deposits and shares are being assessed as earning far less than they actually are. And that keeps more of their pension intact. This move helps around 450,000 pensioners.

The concern? The Coalition hasn’t yet said if they’ll match it. In an environment where retirees are already stretched, letting deeming rates rise could quietly strip away hundreds – or thousands – of dollars a year from people who’ve done the right thing and saved to fund their own retirements – that would be a tough break and one I’m sure many would like to know about before the election.

3. Fuel excise: short-term sugar hit, not real reformPeter Dutton’s promise to halve the fuel excise for 12 months sounds appealing – it could save around $750 a year for single-car households, and up to $1500 for those with two vehicles. But it’s a blunt instrument.

Many older Australians drive less as they age, or they’ve already downsized to hybrid or electric vehicles, and if that’s the case, they won’t benefit at all.

Again, this sounds nice in theory, but in practice, it risks feeling like yet another hip pocket headline grab aimed at families, while they’re once again sidelined when it comes to direct benefits for their own cost-of-living pressures.

4. Medicare and medicines: small wins, but the system is still strainingThe government boosted bulk billing incentives and reduced the cost of common PBS medications – which is helpful, especially for those managing chronic health conditions. And the opposition offered to match it. (READ ON… here)

Read on — this article continues in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

April 1st is coming - time to check in on your health insuranceIn this episode, I sit down with Sally Tindall, Director of Data and Insights at Canstar, to unpack what the premium hikes mean and explore your options as you head into this next chapter of life.

This week on the show, we’re putting health insurance under the microscope for Prime Timers. From 1 April, premiums are set to rise by an average of 3.73%, but depending on your policy, the increase could be even higher.

To help make sense of it all, I’m joined by Sally Tindall, Director of Data and Insights at Canstar. We unpack what these increases really mean, how the pricing system works, and what your options are—especially if you’re heading into retirement or already there.

We also cover how to figure out if you're still getting value from your cover, what to watch out for in your policy, and tips to reduce costs without losing the benefits that matter most.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:Last of all, if you haven’t read the book, you can order your copy from Amazon online. Or pick up a copy at your local Big W, Dymocks, or QBD stores. And if your bookstore doesn’t have it - ask them to get it in. It’s still regularly in the Amazon Top 200.

I have a little online store where you can purchase signed copies too.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

March 22, 2025

When the kids don't lift off: How can you start your epic retirement?

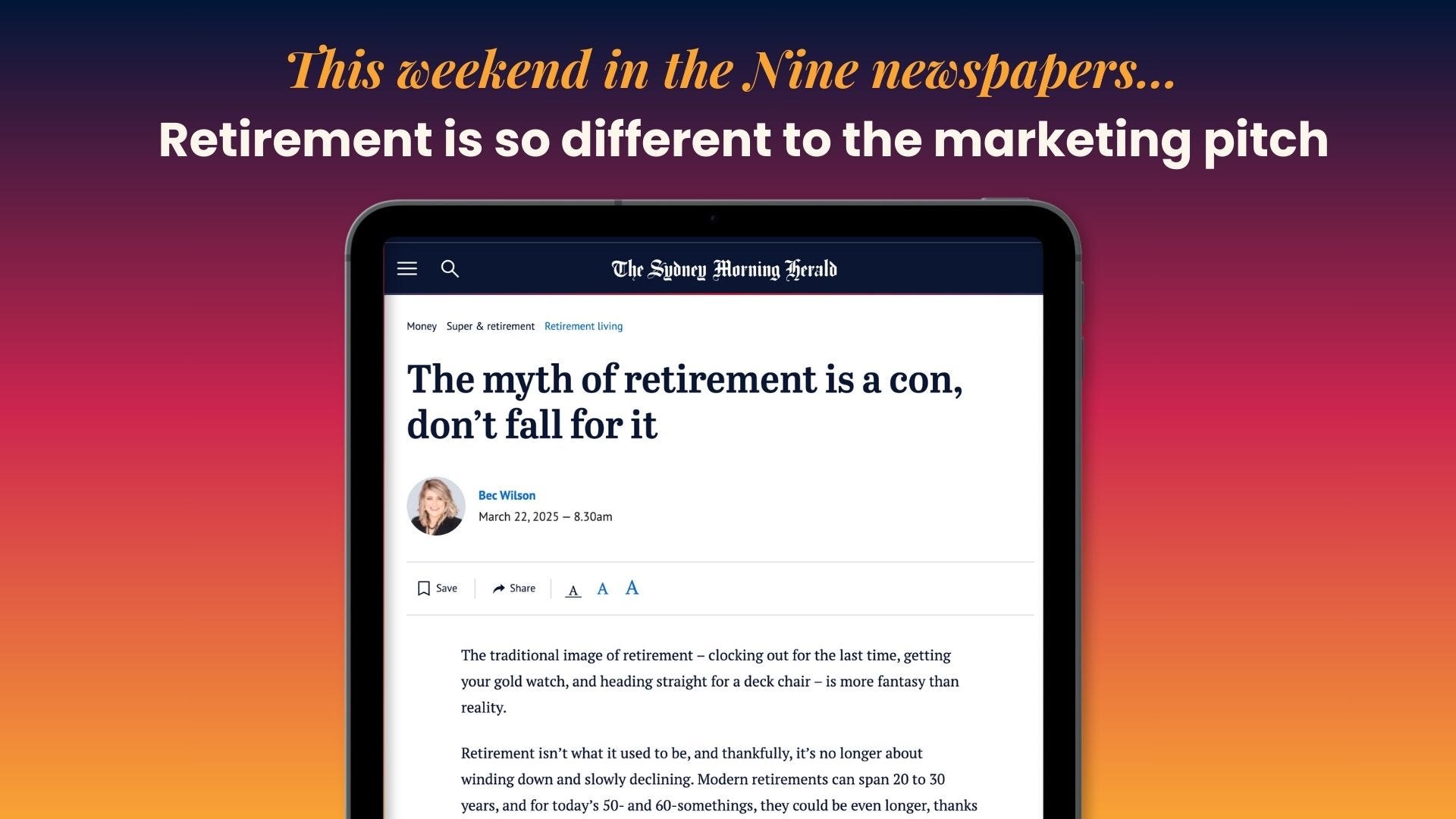

Newspapers: The myth of retirement is a con, don’t fall for it

Feature: When the kids don't lift off: How can you start your epic retirement?

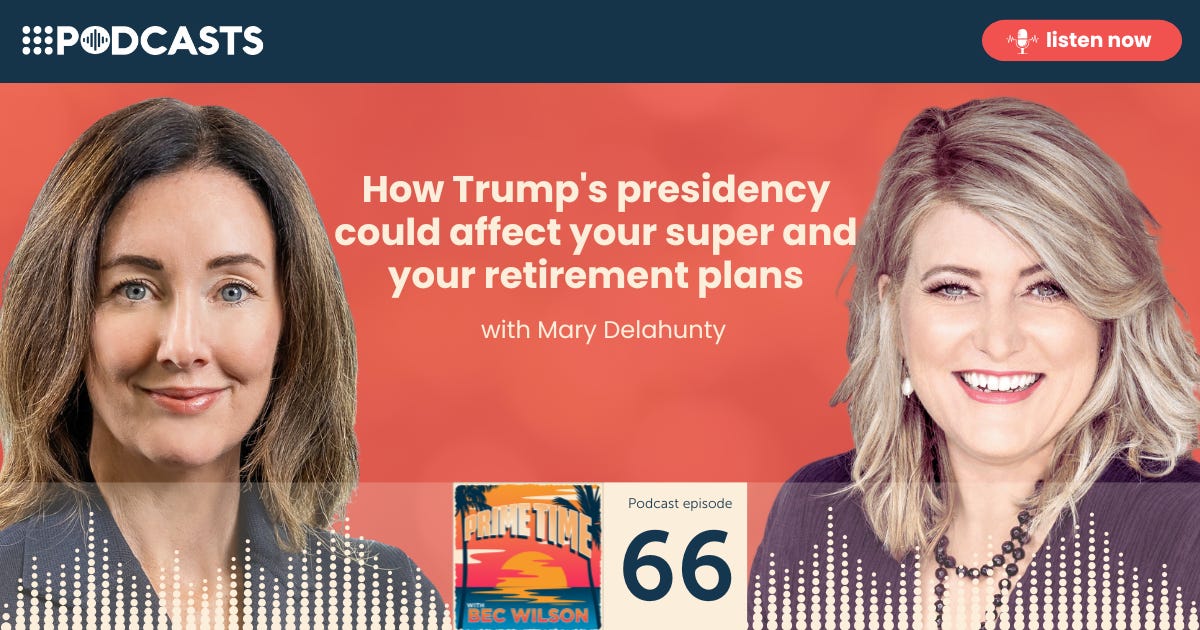

Podcast: How Trump's presidency and market volatility could affect YOUR super and your retirement with Mary Delahunty from ASFA

From Bec’s Desk: Did you hear the news?

Before we get started though… a promotion for our upcoming How to Have an Epic Retirement Flagship Course.

The next How to Have an Epic Retirement 6 week flagship course kicks off on the 10th April. And if you want the 25% off earlybird price then you’ll need to book in the next few days. BOOK HERE | DOWNLOAD A BROCHURE

Our last course (Autumn 25) is just wrapping up — look at some of the feedback coming in:

Thank you for your positive and vibrant delivery of your modules within this course. Clear, concise and to the point, that is not easy to do when you need to cover so much information to a wide audience at different levels of their Epic Retirement. Well Done and Thank you. Your passion to help inform people on all the important topics have been invaluable and the knowledge I have learnt will certainly prepare me for my Epic Retirement.

The course is amazing. Well structured, great content, Bec is very clear and it is easy to understand her message. There is so much to take in, very happy that we also have the workbook and paperback version to take and make notes as we go.

Great course. Bec you are really offering an amazing service. Thank you. I love your entrepreneurial bent is also providing such a helpful service.

The course is interesting and well designed and the concepts clearly articulated. Picked up interesting facts from Q&A sessions too.

When the kids don’t lift offHow can you have an epic retirement when they still need you?Many of those entering retirement imagined it a little differently, didn’t you?

Did you imagine retirement would be a bit different? Image: Canva

Did you imagine retirement would be a bit different? Image: CanvaRetirement was supposed to be the time when things would ease off a bit. You’d raise your kids, help them through school or uni, maybe lend a hand with a house deposit, and then — eventually — they’d launch. You’d get your lounge room back. You’d stop being an unpaid Uber driver or personal loan provider. You could finally turn the page to your next chapter. Prime Time. Epic Retirement. You time.

But for many people, that chapter is being delayed. Or rewritten entirely.

Because many kids haven’t lifted off.

They’re still at home. Or they’ve come back. Or they’ve got real problems — financial, mental health, work-related, relationship breakdowns — and they need you more now than they did when they were little. And you love them. Of course you do. You want to help. But you also wonder: when is it my turn?

This is one of the hardest parts of modern retirement. Not the money. Not the super system. Not even the health stuff. It’s this grey zone of expectations and love and guilt and survival.

And no one really talks about it. Let’s talk about it.

Why it’s happeningThere are a bunch of reasons this is happening more now than ever:

Housing costs are astronomical – especially for under-35s trying to live in cities and make ends meet.

The job market is unstable – casual work, layoffs, career shifts, or automation are hitting young adults hard. And they’ll probably be even more impactful in the years ahead.

Mental health issues are rising – and you’re often the emotional (and financial) backstop for neurodivergent kids who need extra support and kids with mental health issues alike.

Cultural norms have shifted – launching isn’t just moving out. It’s becoming self-sufficient in a very expensive world. That’s harder now than it used to be.

And while most parents are happy to support their kids when times are tough, what’s often unspoken is the toll it takes — emotionally and financially — especially when you're at the point where you're trying to wind down, not gear up.

It can feel like emotional whiplashYou’ve probably spent decades planning, saving, imagining. You finally get to the age where you can start dreaming big again — travel, new hobbies, more time together, downsizing, volunteering, a slower pace. And then life says: “Hang on. Not yet.” One child or even two whiplash back into your home.

It can be disorienting. It can feel selfish to even say, “I want this next phase of my life.” But it’s not selfish. It’s valid. And it matters.

We need to make space for both truths:

Your adult kids may genuinely need your support right now.

You still deserve to design and live a meaningful, enjoyable second half of life.

So what can you do?There’s no one-size-fits-all answer here. But here’s what I’m seeing work for people:

Have a grown-up family conversation.

Be honest about your timeline, your plans, and your boundaries. It doesn’t have to be a confrontation — but don’t let your own needs get lost in the chaos. Kids are often more understanding than we give them credit for, especially if you frame it as “I want us all to thrive.”

Redefine the dream.

Maybe your Epic Retirement doesn’t start with caravanning or overseas adventures. Maybe it starts small — one weekend a month where you take time for you. One day a week that’s not about caregiving or crisis-managing. You don’t have to go big to go epic. Remember — Epic is about meaning, passions and purpose too.

Set financial boundaries.

This one’s tough, but important. Supporting adult kids can’t come at the cost of your own long-term wellbeing. If you drain your super or keep postponing your transition out of full-time work, it’s not just your retirement at risk — it’s your ability to be there for them in the long run.

Explore options beyond you.

If your child has health, housing, or job challenges, see what services or support systems exist beyond your household. You don’t have to shoulder it all alone.

Reclaim a piece of yourself.

Whether it’s a creative pursuit, a walking group, a course, or just coffee with friends — keep that part of you alive. You’re not just someone else’s parent or safety net. You’re still you. And you matter.

And remember — this is a generation-defining challenge that is new to the retirement phase. More and more people in their 50s, 60s, even 70s are helping their adult kids navigate a rougher world than we expected. It’s not easy. It’s not fair. But it’s real.

The goal isn’t to walk away from your family. It’s to walk into this next season of life with clear eyes, open hearts, and a plan that honours everyone — including yourself.

Because your Prime Time hasn’t disappeared. It might just look different than you thought. And that’s okay.

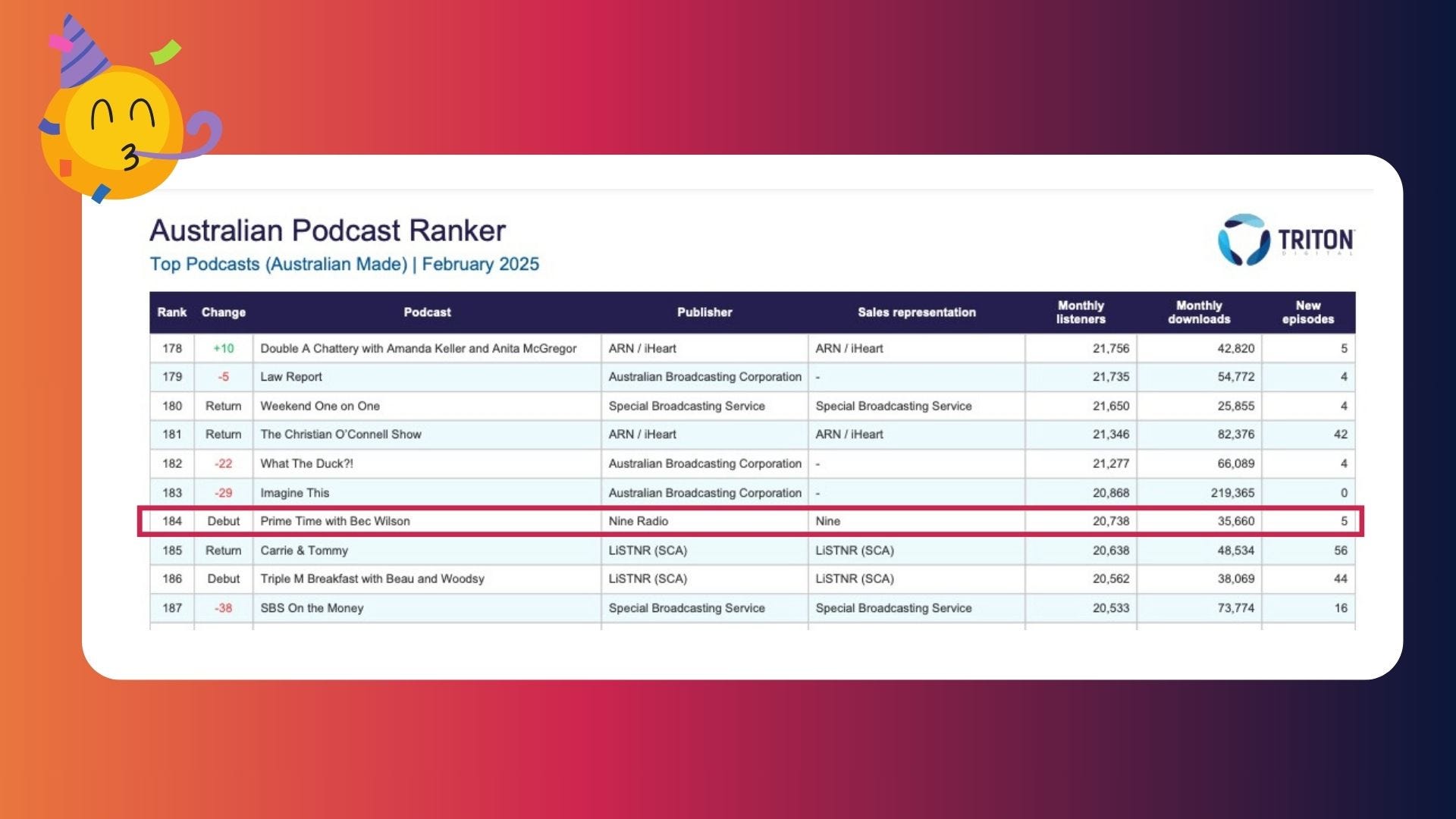

Hey — did you hear the news? I snuck it into this week’s Prime Time newsletter, but I’m so excited I have to put it in here too. The Prime Time podcast this week debuted on the Triton Australian Podcast Ranker which lists the top 200 podcasts in the country. And we came in at #184 for the first time on the ranker since we launched just over a year ago. It’s an amazing thrill to know that the help and support we’re bringing to life are resonating and that you’re coming back time and time again.

Take a look for yourself. I’m a bit stoked. Big thanks must go to the team at Nine who do all the production and sales on it!

Head down - bum up — that’s my last week. Deadlines everywhere. That’s what it felt like. But we’re almost through them…

My little 12-year-old puppy is battling the paralysis in a good way and we’re optimistic of a slow recovery. And he’s a joy to spend my days caring for while writing scripts, running courses and making podcasts. He’s swimming with me and has learnt how to use his bark again (it disappeared for a few weeks) which can be challenging during a call when he wants attention 😉.

The Epic Retirement Flagship Course for Autumn is almost over. Week 6 six lessons have dropped, and we have our last live Q&A this week. This one with Fiona Dalton a real travel guru about the secrets of the travel industry and how to get amazing deals. It’s a ripper… I can’t wait for Monday night.

And our next course (Our Winter Edition) kicks off on the 10th of April. We have heaps of people booked for it already — so the earlybird 25% off won’t last too much longer. Make sure you lock in your place as I’m packing welcome packs and sending them off next week. More information here:

Download our new brochure here

And don’t forget — you can book for a couple with just one ticket and just buy an extra workbook on the way through so you can each still work through your dreams as individuals, alongside each other.

This week on the Prime Time podcast I had the enigmatic Mary Delahunty, the CEO of the Association of Superannnuation Funds of Australia to talk to us about the volatility in the market and the things to think about when panick starts to strike. People are really enjoying this one leaving comments all over social. Make sure you have a listen.

Got some thoughts about the topics this week — leave a comment or write me an email. I love to hear from you!

You can always email me at bec@epicretirement.com.au.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

The traditional view of retirement is a con, don’t fall for itExtract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 23rd March 2025.

The traditional image of retirement – clocking out for the last time, getting your gold watch, and heading straight for a deck chair – is more fantasy than reality.

Retirement isn’t what it used to be, and thankfully, it’s no longer about winding down and slowly declining. Modern retirements can span 20 to 30 years, and for today’s 50- and 60-somethings, they could be even longer, thanks to superannuation and longer life expectancies.

A modern retirement is about embracing a new phase where we don’t have to work for income (or work much unless we want to), we still have our health, and we seek relevance, purpose, and belonging. But does that fit the word “retirement” any more?

Whether you’ve built up a solid superannuation balance or are still working on it, everyone can turn this phase into something that works for them. For some, it’s about securing enough passive income to feel financially free, then letting life unfold less actively. For most, it’s about getting their finances in order, then focusing on what’s next – finding purpose and building a new community.

Sure, the idea of sitting on a beach sounds nice for a few days (or maybe a couple of weeks), but after that? Most people crave more than just doing nothing. Modern retirement is about the freedom to pursue a second career, creative projects, or hobbies that didn’t fit into the work schedule.

This freedom comes from planning ahead – figuring out your finances early so that your choices align with your values and health. It’s about building a foundation that lets you live your best life, whatever that looks like.

And here’s the kicker: this new type of retirement is available to everyone, regardless of how much money you have. Yes, it’s tougher on a full pension, but whether you have ‘enough’ or ‘plenty,’ anyone can fall into the trap of being passive and waiting for a good retirement to come to them – but it doesn’t.

And financial freedom doesn’t automatically bring fulfilment. Even those with more than enough can struggle to find meaning and purpose in retirement.

So, if you’re craving retirement, acknowledge that the idyllic version is a myth. It’s a new phase that offers freedom, flexibility, and the chance to find joy and purpose – if you plan for it and act on your plans. With that in mind, here’s how you can make the most of this new chapter, proactively: (READ ON… here)

Read on — this article continues in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

How Trump's presidency and market volatility could affect YOUR super and your retirement planswith Mary Delahunty, CEO of the Association of Superannuation Funds (ASFA)

If you've been watching the markets lately and thinking about your retirement, you're probably not alone in feeling a little uneasy. I’ve been getting loads of emails from people wondering whether Trump’s latest moves will ruin their retirement and asking if it's time to move to lower-risk investments, or even to the sidelines with their super.

And i want you to stop, look and listen before you react.

In this episode of Prime Time, I sit down with Mary Delahunty, CEO of the Association of Superannuation Funds of Australia (ASFA). We unpack what’s really going on with your superannuation in the midst of this downturn and how to take a considered approach to the current volatility in the market, especially if you’re thinking about retirement.

And, we talk about what your super fund is doing to support you during these unpredictable times, and how you can tap into advice and guidance to help navigate the uncertainty.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:Last of all, if you haven’t read the book, you can order your copy from Amazon online. Or pick up a copy at your local Big W, Dymocks, or QBD stores. And if your bookstore doesn’t have it - ask them to get it in. It’s still regularly in the Amazon Top 200.

I have a little online store where you can purchase signed copies too.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

March 15, 2025

Breaking free from old midlife and retirement templates

Feature: Breaking free from old midlife and retirement templates

From Bec’s Desk: On the road again

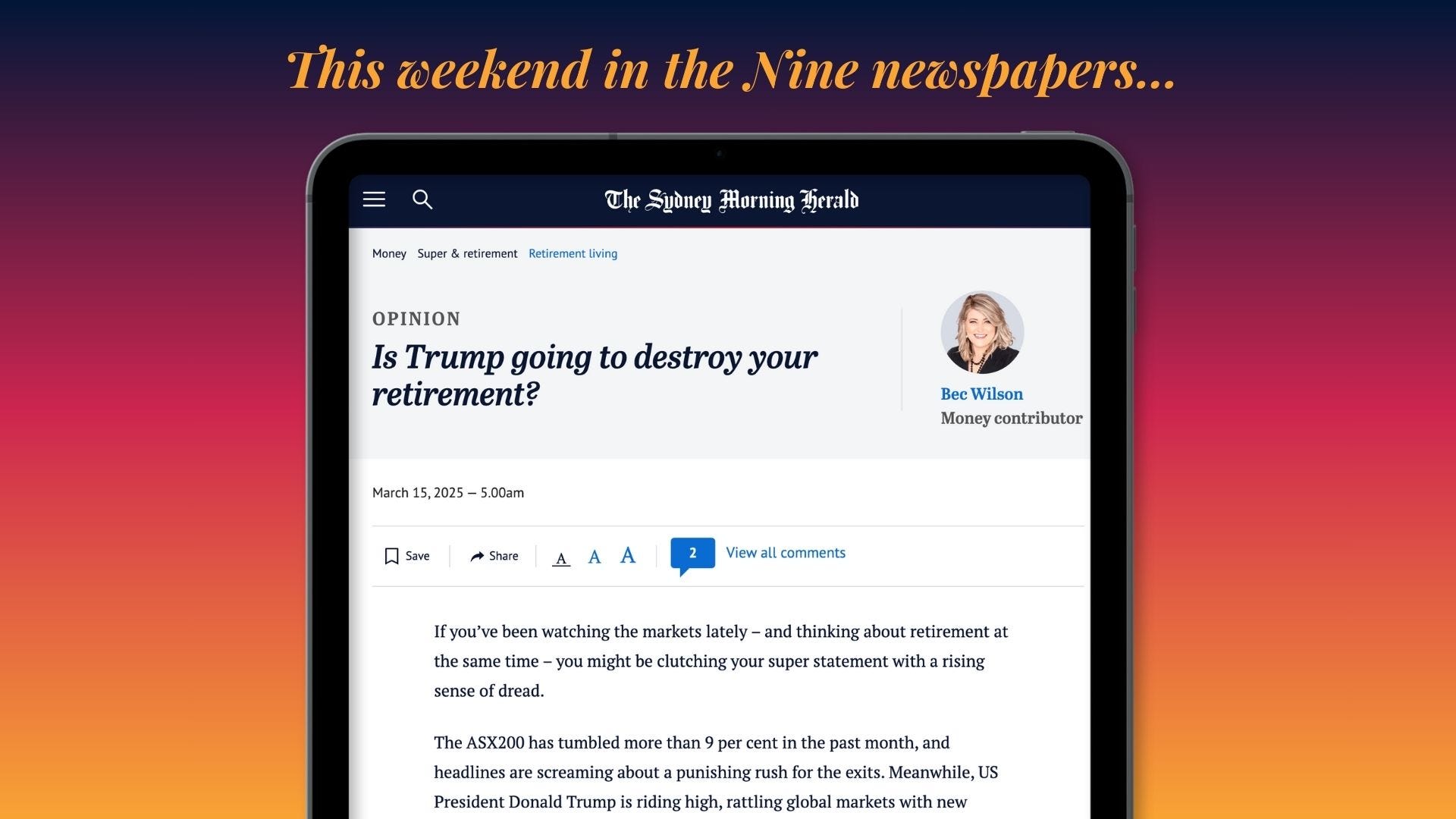

SMH/TheAge: Is Trump going to destroy your retirement?

Prime Time: All the key election issues that matter to Primetimers—broken down and analysed just for you!

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

Before we start — a big thanks to our newsletter sponsor this week, Viking

New 2025-2027 Viking River Cruise Brochure Now Available.

New 2025-2027 Viking River Cruise Brochure Now Available. Viking’s latest river cruise brochure is now available to order with complimentary delivery to your home. Covering 8 to 23-day voyages in Europe, Egypt, Vietnam and the USA across 2025, 2026 and 2027, this is your ultimate travel planning companion.

With no kids, award-winning ships and everything you need included, Viking offer a relaxed atmosphere and destination focused experiences, designed to help you explore the world in comfort.

Book your next river voyage by 31 March 2025 and enjoy free return flights, valued up to AU$2,400 per person.*

Request your new brochure today

*Terms and conditions. Promotion ends at 11.59pm (AEDT) on 31 March 2025.

Breaking free from old midlife and retirement templatesFor decades, we’ve all been following outdated life templates that shape how we think about ageing. These old scripts told our parents and grandparents that life followed a set track—education in your early years, working hard through your ‘prime,’ then stepping into retirement as if it were the official start of ‘old age’ and the beginning of a slow decline. But here’s the truth: those templates belong to another era, and clinging to them is making many of us act older than we actually are.

This week, I was speaking to rooms full of people approaching retirement, and you could see the lightbulbs going off. They nodded furiously, recognising that they’d been subconsciously holding themselves back because of these outdated assumptions.

So let’s crack this wide open. The idea that midlife is the start of decline isn’t just outdated—it’s actively harmful. It leads to self-directed ageism, where we shrink our ambitions, stop learning new things, and convince ourselves that certain opportunities are ‘for younger people.’ And the worst part? By believing it, we actually speed up the very decline we fear.

The new realityModern science, longer life expectancy, and shifting social norms have redefined what it means to be "middle-aged" or "older." If you’re in your 50s or even your 60s today, you’re likely to have decades of good health, career potential, and personal growth ahead of you—if you choose to embrace them.

Consider this: most people in their 50s today have a longer average life expectancy than a 40-year-old did in 1950. The idea that we’re “too old” for change, learning, or reinvention at this stage is simply outdated. Yet, many of us don’t realise we’re still running on an old, broken script about what midlife and beyond should look like.

Overcoming self-directed ageismThe first step to overcoming self-directed ageism is recognising it. Ask yourself:

Have I ever assumed I’m too old to start something new?

Have I invested in learning some new skills and knowledge lately? (It might be for a pursuit you’re keen to become better at or for your working life)

Do I hesitate to learn new skills because I think younger people will do it better?

The antidote? Intentional learning and action. People who continue learning, staying curious, and setting new challenges for themselves not only maintain their cognitive and physical abilities but actually enhance them as they age.

Rewire your approachIf you want to feel younger, stay sharper, and avoid falling into outdated thinking, you need to actively challenge those old narratives – noticing them when they pop into your head and knocking them out. Here’s a few ways you can try:

Promise yourself you’ll learn something new every year. Whether it’s a new language, a digital skill, or even a hobby that challenges your brain in different ways, the act of learning rewires your mindset.

Look for ways to expand your social circles beyond your age group. Intergenerational friendships and work collaborations keep you adaptable and engaged. They can make you feel vibrant, interesting and capable too.

Reframe your expectations. Instead of seeing midlife and retirement as a winding down period, start seeing it as the best bits of life—a phase where your experience, wisdom, and time freedom give you a unique advantage. (They do!)

Challenge your own biases about ageing. When you catch yourself thinking, I’m too old for that, stop and ask, Am I really? Or is this just an old belief I’ve absorbed?

Stay physically and mentally engaged. Exercise, brain training, and social activities aren’t just good for you—they’re essential for keeping you feeling younger.

You are not “old” just because a decades-old life template told you that you should be. The biggest risk to your vitality and potential isn’t ageing—it’s accepting an outdated mindset about what ageing looks like.

If you shift your thinking, challenge self-directed ageism, and actively build a life that prioritises learning, growth, and engagement, you might just find that your best years aren’t behind you—they’re still ahead.

I spent a lot of the last week on the road. First it was off to Sydney for the Inner West Council’s SeniorsFest events. Two terrific education sessions for rooms packed with people are the West Ashfield Leagues Club. I was thrilled to meet so many of our community there — thanks for coming up and saying hello!

Then it was off to Port Stephens to speak at the open day for Ingenia Natura — a stunning new lifestyle community.

It’s certainly terrific to be out and about hearing everyone’s tales of retirement in-person — and share how to have an epic retirement in person too. It’s my favourite thing to do.

Meanwhile, our Epic Retirement Flagship Course for Autumn has reached week 5 already! And this has been a fantastic cohort. All our Live Q&As are flooded with questions, as everyone makes the most of our terrific guest experts! And they come away feeling like they’ve got plenty of learning done. This week we’re learning about finding your sense of purpose, and Sue West joins us from Flourish After Fifty to talk about the transition process.

Our Winter Edition of the How to Have an Epic Retirement Flagship Course has launched for Earlybirds this week. The program will kick off on the 10th April. There’s a new brochure on the website packed with all the event details. Our next event after this one won’t start until very late in August. You can book your place here.

And finally, on the Prime Time podcast this week I had a ripper of a conversation with Shane Wright the Senior Economics Correspondent for The Age and The Sydney Morning Herald all about the election — and the big issues that matter to midlifers and retirees.

Don’t forget, you can always email me at bec@epicretirement.com.au. I love it when you tip me off on things that I can help with or reply with insights.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Is Trump going to destroy your retirement? (with practical steps inside)Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 16th March 2025.

If you’ve been watching the markets lately – and thinking about retirement at the same time – you might be clutching your super statement with a rising sense of dread.

The ASX200 has tumbled more than 9 per cent in the past month, and headlines are screaming about a punishing rush for the exits. Meanwhile, US President Donald Trump is riding high, rattling global markets with new nationalist tariffs and rhetoric that sounds a lot like a return to trade wars. For retirees and pre-retirees, it’s a nerve-wracking time.

I’ve been flooded with messages from people who are either planning for retirement or in the early days of what should be the most exciting time of their lives – only to find themselves gripped with fear that we’re staring down four years of turbulent, unpredictable financial markets.

The questions keep rolling in: “Should I drop my investments back to more conservative levels?” ,“Should I pull my super out and put it all in cash?” and “Is this going to be another GFC-style hit to my retirement?“

So, is Trump about to wreck your retirement? Or is this just another case of markets overreacting to uncertainty?

Read on — this article continues in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

All the key election issues that matter to Primetimers—broken down and analysed just for you!With Shane Wright the Senior Economics Correspondent for The Age and The Sydney Morning Herald.

It’s time to talk about the upcoming federal election. While we’re all still waiting for it to be officially called, once it happens, things will move fast. In this episode, we break down the big issues that matter to midlifers and retirees—because with around 50% of voters over 50, older Australians are going to be important voters.

Joining me is Shane Wright, the Senior Economics Correspondent for The Age and The Sydney Morning Herald. He’s got a deep understanding of both the historical and current political landscape, and he doesn’t hold back when it comes to calling things as he sees them. We didn’t always see eye to eye in this discussion—which makes for a much more interesting conversation for you!

LISTEN TO THIS EPISODE OF THE PODCAST HERE:Last of all, if you haven’t read the book, you can order your copy from Amazon online. Or pick up a copy at your local Dymocks, or QBD stores. And if your bookstore doesn’t have it - ask them to get it in.

I have a little online store where you can purchase signed copies too.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

March 8, 2025

Retirement phase: the good, the bad and the must-know

Feature: Retirement phase: the good, the bad and the must-know

From Bec’s Desk: A windy week

SMH/TheAge: Women must act now if they want to save their retirement. Here’s how

Prime Time: How to get the right financial advice for you

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

Before we start — a big thanks to our newsletter sponsor this week, Viking

Don’t Miss Out On Free Flights With 2025-2027 Voyages.* Offers End 31 March 2025

Viking’s Explorer Sale is ending soon, so make sure you don’t miss out on the opportunity to travel further for less.

Sail with us to extraordinary shores where you can immerse yourself in new destinations and unique experiences. Whether by river or ocean, you can choose from over 160 unforgettable journeys across all seven continents and explore more of the world.

Book your 2025-2027 cruise by 31 March 2025 and enjoy free flight offers with Viking’s river, ocean or expedition voyages, valued up to AU$2,400 per person.* Plus receive AU$500 shipboard credit with any ocean and expedition booking.

Terms and Conditions

*Terms and conditions apply. Ocean offer terms and conditions, River offer terms and conditions, Expedition offer terms and conditions. Promotion ends at 11.59pm (AEDT) on 31 March 2025.

Retirement phase: the good, the bad and the must-knowSo, you’ve hit that point where you can start drawing an income from your super or you can see it coming. That means you’re officially ready for the retirement phase—or as it’s more technically known, pension phase. Sounds great, right? No more 15% tax on your super earnings, regular payments landing in your bank account, and total financial freedom? Well, mostly. But, as always, there’s things people need to understand.

About 4.2 million Australians count themselves as retired in Australia today, but only 1.4 million are drawing down on their superannuation using a tax-free account based pension. ‘Why?’ I hear you ask. Well, it’s a bit of a mystery really. Some people don’t understand the benefits, or don’t realise they can shift their super to tax-free status. While others are using super as a safety net savings account — and ignoring it until later in life. So I thought it might be useful to explain the retirement phase tax benefits today — the good and the bad.

The good✅ No more tax on investment earnings – While your super is in accumulation, earnings get taxed at 15%. In retirement phase, that drops to 0% on both capital gains tax and income tax. That’s a big deal.

✅ Regular income payments – Instead of watching your super balance go up and down, you’ll get a set income stream that you define. Most superfunds will pay it into your account fortnightly or monthly if you choose. This can feel like a paycheck and helps with budgeting, taking the guesswork out of managing your cash flow.

✅ Flexibility to draw down – You can withdraw as much as you want, whenever you want (as long as you adhere to the a minimum drawdown rate). If you want to take out a lump sum for travel or a big expense, you can.

✅ Estate planning benefits – Pension accounts can be more tax-friendly for passing on wealth, depending on your beneficiaries. And you can work on a recontribution strategy to maximise the tax effectiveness to your estate up to the age of 75.

The bad (or the things to consider)❌ You must withdraw a minimum amount each year – The government makes you start drawing down your super. If you’re aged 60-65 you must withdraw at least 4% of your balance each year. From 65-74, you must withdraw 5% of your balance and it increases as you get older.

❌ Super in accumulation still gets taxed – If you keep some money in accumulation, earnings on that portion are still taxed at 15%. Only money moved into retirement phase gets the tax-free treatment.

❌ Centrelink counts all your super after 67 – If you're under 67, super in accumulation phase isn’t counted in Centrelink’s Age Pension assets test. If you have a younger partner, their super in accumulation phase remains exempt from the assets test until they turn 67. This can be an advantage if one partner is eligible for the Age Pension while the other’s super stays unassessed. However, any super moved into pension phase is counted immediately, regardless of age.

❌ No going back – Once you move money into pension phase, you generally can’t move it back into accumulation unless you commute the pension and transfer the balance back to accumulation. However, if you want to add more money to super later, you’ll need to make new contributions (usually by opening a new accumulation account in parrallel with your retirement phase account) and you’ll need to stay within the contribution caps.

You also need to be aware of the transfer balance cap (TBC), which is currently $1.9 million (2024-25) and set to move to $2.0M at 1 July 2025. Once you have used part of your cap, any future amounts commuted then moved into pension phase will count against your TBC again. Even if you commute (move money back into accumulation), your used TBC amount does not reset—so you can’t start a new pension with more than your remaining cap.

Of course, you can withdraw funds and recontribute to super using any remaining caps. If you end up with an accumulation account and a pension account (which many do who decide to do some part-time work, you’ll probably end up paying two sets of fees — worth being aware).

So, what’s the best move?If you want to stop paying tax on your super’s investment earnings, moving to pension phase makes sense—because super in pension mode is tax-free.

If you don’t need the income yet, you could keep some money in accumulation (where you’re not forced to withdraw a percentage each year) and move the rest into pension phase for the tax-free benefits.

The big advantage of pension phase is saving tax—but once you move money into pension mode, you must start drawing it down. If you’re happy with that, it’s usually the better option. 🚀

Cyclone Alfred disrupted my week — but those of us in Brisbane are feeling lucky today that the wind did not arrive in the worst case scenario. I wish everyone good luck over the days ahead and with the clean up.

For those following along for news of my 12-year old dog. He’s improving a little — can hold his head up, is eating well but still arms and legs are paralysed. Still crossing our fingers for incremental (or speedy🙏) improvements. He’s in great spirits, if a little frustrated.

This week I’m all ready and raring to go for the two events I am doing in Sydney on Tuesday the 11th March. They’re being held at the West Ashfield Leagues Club. Both are free, hosted by Inner West Council.

12.00- 1.30pm — The 12 Secrets of an Epic Retirement. More info/ https://events.humanitix.com/how-to-p...

6-7.30pm — How to prepare for an Epic Retirement. More info/RSVP https://events.humanitix.com/12-secre...

This week the Autumn Epic Retirement Course is in Week 4, with Jen Harding from HESTA joining us for our live Q&A about how superannuation funds work and the advice on offer. This cohort is rather amazing — with so many questions asked they’re running over time each week. It’s keeping me and our guests on our toes!

And our Winter How to Have an Epic Retirement Flagship Course is opening for booking this week and will kick off on the 10 April 2025. — you can register your interest for our earlybird deal here.

I’ve just submitted the next edit of Prime Time — it’s the last time I can really change it much. Exciting times. The cover reveal is coming very soon.

And finally, on this week’s podcast I took my conversation on financial advice further and deeper, talking to David Lane about how we can all recognise good financial advice when we see it. A tough conversation but an important one.

Don’t forget, you can always email me at bec@epicretirement.com.au. I love it when you tip me off on things that I can help with or reply with insights.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Women must act now if they want to save their retirement. Here’s howExtract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 8th March 2025.

I’m a woman approaching 50, and I’ve learned a few things the hard way. If I could go back and give my younger self advice – or offer lessons to other women in the workforce – I wouldn’t be talking about skincare, wardrobe or career hacks.

I’d be telling her to take her financial future seriously. Because here’s the thing: by the time you reach my age, the gender pay gap isn’t just an abstract issue or a talking point in a boardroom. It’s the reason so many women over 50 are staring down an inferior retirement compared to men, with fewer options and a lot more stress.

And if you’ve ignored the problem for decades, it’s damn hard to fix.

As we mark International Women’s Day, let me be blunt: the financial security of women approaching retirement today is in crisis. The numbers don’t lie. The average super balance for women aged 55-64 is $246,300, compared to $326,200 for men of the same age, according to the ABS Household Income and Wealth Survey (2019-20).

Nearly two-thirds of women believe they won’t achieve a comfortable retirement, according to the Brighter Super & Investment Trends Report (2024), and they’re not wrong to worry. The average woman expects to fall short of what she needs to live comfortably by about $1500 per month.

With less money comes fear, pessimism, and disengagement from her super. I see it all the time – women who don’t even want to check their balances because they already know the numbers won’t be in their favour. Then, because they don’t look, they don’t do anything to improve it. It’s a dead spiral we need to stop.

The gender pay gap might be real, but you don’t have to let it define your retirement.

We must acknowledge three key problems if we want women to have fairer super balances at retirement – and if we want to fix things for the next generation of women – those who haven’t reached retirement yet. If that’s you – stand back and take notice.

The first is that the gender pay gap is alive and well. In 2025, Australian women are still earning, on average, $28,425 less than men per year. That’s 78¢ for every dollar a man earns. And when you break it down, about one-third of the pay gap comes from incentives, bonuses, and superannuation contributions – which companies are still getting away with not offering fairly.

The second is that women spend fewer years in full-time work. Many of us take on caregiving roles – stepping out of the workforce for months or even years to raise children, and later, to care for ageing relatives.

I know I did – and working part-time or not at all for years has certainly affected my super significantly. What no one tells us is that every time we do, we sacrifice super contributions, career momentum, and financial security.

And thirdly, women leave the workforce earlier too.

This article continues — Read on, in The Age, The Sydney Morning Herald, Brisbane Times and WA Today.

How to get the right financial advice

for you

An Epic Retirement community member reached out last week with a frustrating experience about getting financial advice. They were referred to an adviser for guidance on preparing for retirement and had a great first meeting. Everything seemed promising—until they received a 70-page Statement of Advice that lacked a clear retirement strategy or any meaningful projections. Instead, the main recommendation was to roll their high-performing super fund into a wrap platform—a move that hadn’t even been discussed in their initial meeting. They were disappointed, especially since they were with one of Australia’s top-ranked super funds and had no plans to leave.

I wrote about it in the weekend’s Nine newspapers, and in my Epic Retirement newsletter too. But this topic deserves a more detailed conversation that you can draw some lessons from. Because I’m a big supporter of financial advice — if you get the right type of advice for your needs. But to get the right advice, you need to know the different types of advice available and ask the right questions going in.

So in this episode I sit down with David Lane, the Queensland State Manager and Senior Advisor at Ord Minnett, and one of Australia’s award-winning advisers, to demystify the financial advice market. Together we break down the different types of financial advice, explore how to ask the right questions, and talk about what a good advice relationship should look like. We also unpack the real reasons some advisors recommend wraps and platforms, and help you consider whether you need ongoing investment management at all or can seek out an adviser for one-off strategic advice instead.

LISTEN TO THIS EPISODE OF THE PODCAST HERE:Last of all, if you haven’t read the book, you can order your copy from Amazon online. Or pick up a copy at your local Dymocks, or QBD stores. And if your bookstore doesn’t have it - ask them to get it in.

I have a little online store where you can purchase signed copies too.

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

March 1, 2025

Seven questions to ask at your first financial advice appointment

Feature: Seven questions to ask at your first financial advice appointment

From Bec’s Desk: Looking up

SMH/TheAge: Thinking about financial advice? Don’t make this costly mistake

Prime Time: How to start planning your epic caravan adventure

Thanks for reading Epic Retirement Australia! Subscribe for free to receive new posts and support my work.

Seven questions to ask at your first financial advice appointmentAs I wrote in my article in this weekend’s national newspapers, I recently heard from an Epic Retirement Community member about their experience with a financial adviser. And I don’t want their story to scare you off getting financial advice—I want it to empower you to ASK THE RIGHT QUESTIONS upfront so you walk away with the advice you actually need.

In preparation for retirement, they paid for independent financial advice, expecting guidance on managing their household super and investment property, along with projections to help them plan their income in retirement. Instead, their adviser recommended moving all their super into a wrap account—something that hadn’t been discussed in their first meeting.

They were already invested in one of Australia’s highest-performing super funds, so they didn’t understand why switching was the best option. In hindsight, they realised they probably didn’t ask the right questions upfront or clearly communicate that they wanted retirement planning guidance—not a recommendation to change funds. Now, instead of having a clear roadmap, they’ve walked away with more questions than answers:

❓ Should they really be moving from a high-performing super fund to a wrap?It depends on their goals, investment preferences, and whether the extra costs of a wrap account would provide real value. Wraps can offer greater flexibility and personalised investment choices, but they also come with higher fees and complexity and usually a need for ongoing advice. Advisers like them because they allow them to provide you with an ongoing investment management service. But, the real question this couple wanted to ask was ‘If their current super fund is already performing well, why move to a wrap?” Will it actually improve their long-term outcome or just add unnecessary costs and a need to use an adviser on an ongoing basis? And do they want this?

A key question they may not have thought to ask is: "What are the tax implications of moving our super before retirement?" Their existing fund may have incurred capital gains tax on earnings just to transition into the adviser’s recommended structure—an important cost to consider before making any changes.

❓ What even is a wrap, and how does it compare?Most people don’t walk into an adviser’s office asking for a wrap account, yet they’re often recommended. A wrap account is an investment platform that allows an adviser to manage multiple assets under one structure. Instead of keeping your super in an industry or retail fund, your super is rolled into a wrap, where investments are selected and managed for you.

Wrap accounts can provide flexibility and access to a wide range of investments, but they also come with additional fees and complexity. For some people—particularly those who want more control over their investments—they can make sense. But for others, especially those already in a well-performing super fund, a key question is whether switching to a wrap genuinely improves their financial position. A good adviser should be able to explain that clearly.

❓ And why didn’t they get the projections they needed to plan their future?This is the real issue. Retirement planning should start with strategy, not just product recommendations — unless you have just come for investment advice. The adviser should have provided projections on how their super, investments, and property decisions would affect their income in retirement—before suggesting any changes.

The key takeaway?A good adviser should help you understand your full financial picture before making recommendations. And if they don’t? That’s when it’s time to ask more questions.

How to avoid this mistake— Seven questions to ask your adviser at your first appointment1️⃣ Do you offer full retirement strategy and projections, or just investment management? (Make sure their focus aligns with what you need—there’s no wrong answer, just the right fit for you.)

2️⃣ Does your firm have a preferred product list or specific way of investing? (Ask them to explain how it works, so you can decide if it suits you.)

3️⃣ If I move to a wrap account, will I have to leave my current super fund? (Find out how this impacts your fees, performance, tax and insurance.)

4️⃣ Can you model different retirement scenarios for me? (For example: keeping vs. selling an investment property, staying with my current super vs. switching, different drawdown strategies, and tax implications.)

5️⃣ Do I need ongoing advice, or is this a one-time plan? (Clarify the costs and whether ongoing fees are necessary for your situation.)

6️⃣ If I want to keep my super where it is, can you still help me with retirement planning? (Some advisers only work with clients who move investments—ask upfront.)

7️⃣ What are all the fees involved? (Request a direct comparison to your current setup to see if the recommendations truly add value.)

Tell ‘em I sent you! Good advisers are thrilled to have well-prepared clients who are right for them and keen to learn!

Let’s talk about it in the comments.

Thanks for your lovely messages about my 12-year-old pup. After another week of nursing his paralysed body, he’s showing some positive signs of improvement… so keep your fingers crossed for me that this is the beginning of his recovery.

This week I’ve been preparing for the two events I am doing in Sydney on the 11th March. They’re being held at the West Ashfield Leagues Club. And there’s two events that are open to the public to attend. Both are free, hosted by Inner West Council.

12.30-2pm — The 12 Secrets of an Epic Retirement. More info/ RSVP https://events.humanitix.com/12-secre...

6-7.30pm — How to prepare for an Epic Retirement. More info/RSVP https://events.humanitix.com/how-to-p...

This week the Epic Retirement Course is in Week 3, with out third Live Q&A being held. These events are an absolute ripper — the last two weeks we’ve squeezed more than 50 questions into each event and run over time! This week’s is with David Lane the Queensland State Manager of Ord Minnett (and Senior Financial Adviser), and we’re talking Superannuation, Investing, Platforms and SMSFs.

I’m gradually working my way through the laid up edit of Prime Time - my next book. And preparing for the launch later next week of our April education program - which has a huge waitlist already! 😁 (You can waitlist yourself for the earlybird deal here).

And, we’re having huge fun on the podcast, with a great conversation about caravanning — something I’m really keen to do in the years ahead and clearly many of you are too.

Don’t forget, you can always email me at bec@epicretirement.com.au. I love it when you tip me off on things that I can help with or reply with insights.

Many thanks! Bec Wilson

Author, podcast host, columnist, retirement educator, and guest speaker

Thinking about financial advice? Don’t make this costly mistake

Extract of article published in print in The Age, The Sydney Morning Herald, Brisbane Times, WA Today on Sunday 2nd March 2025.

If I received a gut-wrenching letter the other day from a pre-retiree who had just seen a financial adviser – and walked away deeply disappointed.

She and her partner had been diligent savers, carefully building their retirement nest egg in one of Australia’s largest super funds. They weren’t looking for magic solutions – just solid, independent advice to help them map out their retirement strategy.

They wanted to understand their options for their investment property, make informed decisions about their super, and see projections of how their retirement income might play out under different scenarios before making the shift into retirement.

Their first appointment started with the usual – filling out a stack of forms before they even stepped into the room. Then came what felt like a pleasant, productive chat with an adviser personally recommended by a dear friend.

But when they received their Statement of Advice (SOA), reality hit hard. The document was 70 pages long, packed with complex jargon, and the primary recommendation? Take their super out of a high-performing fund, open a wrap account, and invest in a model portfolio.

Looking back, they admit they didn’t understand the advice process or ask the right questions – and they didn’t tell the adviser this upfront, which might have helped simplify things. They also didn’t realise they had to explicitly state they were happy with their existing super fund, a consistent top performer.