Nick Reichert's Blog, page 21

May 3, 2019

Investing in Yourself

There is an ongoing debate within the FIRE movement about whether it's okay to enjoy your work / career or simply focus on working at a job (doesn't matter what it is as long as it pays), living below your means and saving aggressively in order to retire early. Many of these folks don't like what they do, so they simply endure their job to achieve FIRE. Then there are are others who actually love what they do, while they still have the objective of retiring early. Part of that debate also centers around quality of life. Is it okay to spend some money on living a little (maybe a nice dinner once in a while or a trip), or is it better to be extremely frugal in order to accelerate savings?

There is an ongoing debate within the FIRE movement about whether it's okay to enjoy your work / career or simply focus on working at a job (doesn't matter what it is as long as it pays), living below your means and saving aggressively in order to retire early. Many of these folks don't like what they do, so they simply endure their job to achieve FIRE. Then there are are others who actually love what they do, while they still have the objective of retiring early. Part of that debate also centers around quality of life. Is it okay to spend some money on living a little (maybe a nice dinner once in a while or a trip), or is it better to be extremely frugal in order to accelerate savings?All of this discussion centers on working, which provides the means of survival and saving up for retirement, whether you like the job or not. If you have chosen your career wisely, I would argue that your job could be your best investment. This is true especially if you do what you love, since you tend to excel when you are in that situation.

“Choose a job you love, and you will never have to work a day in your life.”For those who are lucky enough to have found meaningful work, a stable company and a great team that is high-performing and fun to be around, it's a sort of nirvana. This can lead to a virtuous cycle of progressive opportunities, promotions and of course raises and bonuses, which can help accelerate your savings. This "top line" growth can perhaps be more effective than cutting down on living expenses in order to accelerate savings. Once your savings builds up enough, you can begin Building a Financial Fortress to help ensure that you can protect and grow your hard-earned wealth.

I would argue that investing in yourself, by improving your skills on the job through training opportunities and seeking out new challenges, is often under-appreciated. In fact, I would say today with so many people talking about having one or more "side hustles," there's even less focus on your primary job. Honestly, the time spent on side hustles often simply doesn't pay off like investing in your career. If you can create the time and space at work to think and plan ahead strategically, you can further accelerate that investment through preparation, whether that's for an important meeting or for getting your team ready for change. If can master your day job, and if you still have the energy, you can come home after a full and satisfying day at work and spend your spare time in the evening working on your side hustle.

Here are a few other thoughts on investing in yourself:

You might need to take things to the next level with an MBA (maybe your company even reimburses for it), leadership training, or technical training. Ideally you should have a mentor that can help you figure out what's best for you to maximize your investment in yourself Leaving your job for another opportunity may seem tempting, but consider whether your opportunity is as good or better where you are - sometimes your best opportunity is right in front of youIf you are interested in other investing ideas, please check out my books here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.

April 28, 2019

Irrational Exuberance?

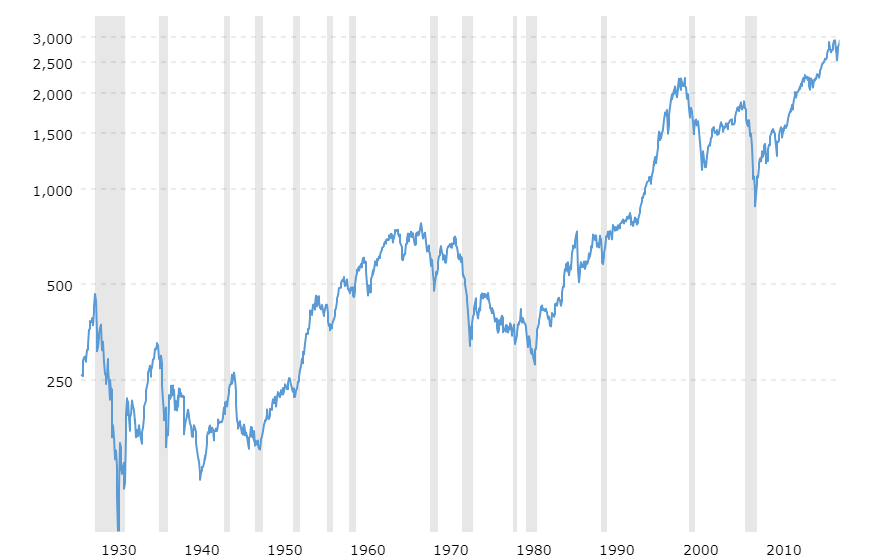

S&P 500

S&P 500"Clearly, sustained low inflation implies less uncertainty about the future, and lower risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past. But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade? And how do we factor that assessment into monetary policy? We as central bankers need not be concerned if a collapsing financial asset bubble does not threaten to impair the real economy, its production, jobs, and price stability. Indeed, the sharp stock market break of 1987 had few negative consequences for the economy. But we should not underestimate or become complacent about the complexity of the interactions of asset markets and the economy. Thus, evaluating shifts in balance sheets generally, and in asset prices particularly, must be an integral part of the development of monetary policy."

Alan Greenspan, December 1996As we enter a new period of prosperity, Alan Greenspan's comments almost 23 years ago are starting to resonate again. The stock market continues to climb to new highs. How much higher can the market go? Is everyone talking about their stock investments at cocktail parties? Should I be worried when my 18 year old opens up a RobinHood account for day trading? Have we reached a state of irrational exuberance? Should we be worried and put some cash on the sidelines or stay should we stay fully invested in the stock market? Here's a look at both sides of the story.

The Bull Case:

Historically low interest rates are likely to continue for some time (see chart below), keeping cost of borrowing low and favoring leverage and higher-yielding investments (i.e., margin accounts invested in stocks)Recent tax cuts have largely run their course, but have materially enhanced corporate income statements, fueling stock buybacks and dividend increases; the lower corporate tax rate tailwind effect is likely to continueLow and declining unemployment rate more likely than not to continue as economy chugs alongRecord corporate earnings - Q4 2018 67% of Companies reporting beat their earnings projectionsFear and Greed Index showing Greed - if you're a momentum investor, that's good and you go with the flowBanks are in good shape and real estate lending is relatively conservative these days

Federal Funds Rate

Federal Funds RateThe Bear Case:

Companies going public that don't make money, at least not yet (i.e., Uber, Lyft, etc.) - a sure sign of irrational exuberance, right?Oil price spikes, which are pretty reliable predictors of recessions and stock market correctionsChina trade war and economy concernsEurope slowdown concerns and threat of new trade war frontWeekly ETF / Mutual Funds Flows show a lot of movement into bonds from stocks recently, indicating investors are taking a more defensive stanceUnemployment may be worse than reported (see chart below with alternative stats)Fear and Greed Index shows Greed - if you're a contrarian that's bad and means it's time to head for the hills

Estimated Fund Flows

Millions of dollars4/17/20194/10/20194/3/20193/27/20193/20/2019Equity4,5425,811-7,496-11,085-2,145Domestic3,9936,210-7,465-10,8961,474World549-400-31-190-3,619Hybrid-976-122-3,575-199-636Bond8,8097,81311,2757,88410,552Taxable7,5596,6759,7835,5288,660Municipal1,2501,1381,4922,3561,892Commodity-101-286-983141393Total12,27313,216-778-3,2598,163

Unemployment may actually be a lot worse than reported, since the official measure has changed over the years:

Ultimately you need to decide how much risk you can tolerate in your portfolio and your investment strategy should follow suit. Following a broad diversification strategy, especially when markets are volatile, is a good approach. The goal should be to make money in any market environment and most importantly, to sleep well at night knowing your strategy matches up with your risk tolerance.

If you are interested in other investing ideas, please check out my books here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.

April 20, 2019

College Math

After completing (hopefully) our last college tour today, I was reflecting on the process for planning and saving for college for my son, who will be attending in the Fall. The process is definitely not simple or easy - SAT preparation courses / tutors, taking the SAT multiple times (including subject matter tests), filling-out applications for multiple schools and then the angst of waiting to see where you get in. Then there is the depression of rejection, the uncertainty of "waitlist," and the struggle of choosing between the schools that accepted you. It's a roller coaster of emotions, for sure. For your child, it can be the first time in their life where they truly have difficult choices to make.

After completing (hopefully) our last college tour today, I was reflecting on the process for planning and saving for college for my son, who will be attending in the Fall. The process is definitely not simple or easy - SAT preparation courses / tutors, taking the SAT multiple times (including subject matter tests), filling-out applications for multiple schools and then the angst of waiting to see where you get in. Then there is the depression of rejection, the uncertainty of "waitlist," and the struggle of choosing between the schools that accepted you. It's a roller coaster of emotions, for sure. For your child, it can be the first time in their life where they truly have difficult choices to make. Walking through the dorms today really brought back memories of my own college experience - both good times (like the parties) and bad times (like doing your laundry in the basement with a hangover and not having enough quarters). There were academic highs and lows too, but for me college was about the people I met and the life skills I learned as much as the classroom work. I would have to say even to this day that my college experience was awesome and I'm really excited for my son to start that journey soon. College was also a relative bargain back when I attended. I went to a state school and had in-state tuition. I calculated that the entire cost of my education over 4.5 years was roughly equivalent to one year today.

The cost of college today is simply staggering. Just the preparation, testing and applications was $3K for us and we did most of it ourselves. But the real sticker shock is the cost to attend. A typical school in the University of California system will set you back about $19K for "cheap" in-state tuition/fees/books and another $16K for room and board - a total of $35K/year. Oh and that's assuming you get in, which turns out is really hard, even for the best California students. Many wind up going out of state. That's about $140K for one child for four years of college, assuming no scholarships or loans are available to help fund their education. The number could easily be double that for out of state / private schools.

Turning back the clock and using our handy compound interest calculator, you would have had to start saving $400 per month when your child was born 18 years ago and earn an average rate of return of 5% in order to have $140K today ($139,680.81 to be precise). If you only earn 2%, your contribution goes up to $550 per month to achieve substantially the same result. For most people, that's the equivalent of a car payment and also makes saving for retirement, or anything else for that matter, at the same time a real challenge. Conventional wisdom is that you should always save for retirement first before saving for college. With inflation, the amount you would have to save in the future could easily be double that of today. Using the calculator again, $140K at a 3% annual inflation rate will be $240K in 18 years. That's the power of compounding working against you.

Fortunately, there are plenty of scholarships and grants available and also student loans to help pay for the cost of education. I believe in the wake of the college admission scandal, there will also be more opportunities generally for kids who work hard themselves to get into college. I also see more opportunities for legitimate athletes to attend college over the next few years and possibly more scholarship money available for them. Even if you aren't able to save the full amount for college, having some money saved is better than nothing.

If you are interested in other investing ideas, please check out my books here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.

April 13, 2019

And Now the UBER IPO...

Similar to Lyft, which I reviewed in a post about a month ago, UBER is losing lots of money in order to grow their business rapidly. Also, as has been well publicized, Lyft is down more than 20% from it's first day valuation. It's Deja Vu all over again to the dot.com days as far as I'm concerned.

Similar to Lyft, which I reviewed in a post about a month ago, UBER is losing lots of money in order to grow their business rapidly. Also, as has been well publicized, Lyft is down more than 20% from it's first day valuation. It's Deja Vu all over again to the dot.com days as far as I'm concerned. Here is a quick analysis of UBER, which recently filed its IPO registration statement. I won't spend a lot of time talking about the business because everyone is pretty familiar with it. The company is global and has several lines of business, including personal mobility (cars, bikes, scooters), meal delivery, freight handling and an autonomous vehicle strategy.

A few highlights from the registration statement worth noting:

Impressive revenue growth - from $3.8B in 2016 to $11.3B in 2018 - 293%Consistent LOSS from operations of between $3B and $4BProfitable in 2018, but only because of one time gains from investmentsHere's a snapshot of the Company's debt and other contractual obligations. Not much coming due in the next year, but almost $13B in total outstanding, half of which comes due in the next five years which is a little concerning.

Here are a few notes on UBER's cash flow situation, which shows that the Company burned through $2.2B in 2018 ($1.5B in operations and $0.7B in investing activities).

"We currently anticipate that our available cash and cash equivalents and revolving credit facility will be sufficient to meet our operational cash needs for at least the next 12 months. We may need to raise additional capital or incur additional indebtedness to continue to fund our operations in the future or to fund our needs for merger and acquisition activity or other strategic initiatives. Our future capital requirements will depend on many factors including our growth rate, headcount, sales and marketing activities, research and development efforts, capital expenditures, the introduction of new products and offerings, and potential merger and acquisition activity, or other strategic initiatives. Additionally, as our business has grown, our restricted cash balance has increased primarily due to increasing insurance reserves for potential future liabilities, thereby reducing the amount of unrestricted available cash we have to fund our operations."

While this company is very large and growing significantly, my main concern is the path to profitability. I'm not sure it's sustainable for very long, especially if we see a global economic downturn in the next year or two and the debt / equity financing necessary to sustain the business becomes harder to obtain. I think investors have already figured that out in the case of Lyft.

If you are interested in other investing ideas, please check out my books here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.

April 5, 2019

Having A Wealth Mindset

If you want to improve your financial situation and build your Financial Fortress now, it starts with having a "wealth mindset."

If you want to improve your financial situation and build your Financial Fortress now, it starts with having a "wealth mindset."First and foremost, you need to have a positive outlook on life. If you find yourself saying "I can't do that" or "I can never get ahead," you are creating negative energy that will naturally inhibit you from reaching your wealth-building goals. On the other hand, if you surround yourself with positive people, thoughts and messages and always think in a positive way, you can change the conversation in your mind to "HOW can I do that?" or "HOW can I get ahead?"

The second element to a wealth mindset is having financial discipline. This means developing a reasonable monthly budget, sticking to it and paying yourself first. The easiest way to pay yourself first is to contribute to your 401(k) at work so you never even see the money. Keeping to a budget helps you stay focused on your spending and allows you to make choices. Even if you may have plenty of money or credit, you will want to force yourself to choose when it's time to spend money on something. The more the item costs, the more thought needs to be put into whether it is needed or not and how much you really want to spend on it. Will a used car be good enough versus getting a new car? Do you have to buy the nicest house or rent the nicest apartment or is something more modest adequate? Do you have to eat at the finest restaurants and wear designer clothes or can you get by with family style dining and sweats?

The third element to a wealth mindset is reflection. I often find by thinking about things before going to bed or taking long walks and mulling things over can help me develop new ideas and strategies to overcome obstacles and achieve my goals. It also helps me prioritize things and solidify my financial plan. Having quiet time to yourself is also very important to help you focus and let your own natural creativity help you. For example, I wanted to invest in real estate during the Great Recession, but I didn't have any cash. By putting my mind to it, I realized I could tap into my IRA to get started investing and I did just that.

The fourth element to a wealth mindset is persistence. When I was trying to buy properties during the Great Recession, it was very competitive and I had to be relentless with offers in order to get deals. Many times my offers were rejected. There were many setbacks, but eventually I was able to purchase four properties in all. Life will often deal you setbacks, but that's also where having a persistent mindset is important. Sometimes all it takes is a little more effort, one last push and you can overcome the obstacles you face and you can succeed. Failure is simply a learning experience and should never be allowed to define what you have set out to do.

By combining these four elements together, you can develop a wealth mindset that can ultimately help you successfully Build Your Financial Fortress.

If you are interested in other investing ideas, please check out my books here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.

March 30, 2019

10 Things to Do With Your Tax Refund

It's almost April 15 and tax day. If you file your taxes and have a refund due to you, after you adjust your withholding so you don't have as much of a refund next year, here are some ideas for what to do with the refund (other than spending it):

It's almost April 15 and tax day. If you file your taxes and have a refund due to you, after you adjust your withholding so you don't have as much of a refund next year, here are some ideas for what to do with the refund (other than spending it):Pay off high interest rate credit cards - this is an easy way to make a great 18% - 25% return on your money with no risk Pay down your car loan - paying off your car loan early gets rid of a car payment and helps you save more money for other things Pay down student loans - same as car loan, but lower priority since interest rate is likely the lowest of the three Contribute to your IRA for 2019 - start up a new IRA if you don't already have one or contribute for next year early and grow your money tax deferred (or tax free with a Roth)! Open up a high interest savings account - put the money to work earning interest Apply to your 2019 estimated tax payment - if you have to make an estimated tax payment for the first quarter, this is an easy way to do it Buy music royalties - get some nice yields from your favorite artists Buy some gold or silver coins - a nice way to hedge against inflation Buy reliable dividend stocks - earn a yield that is tax-efficient and use the dividends to reinvest and buy more shares to compound your investment Donate to charity - give something back to the community!

If you are interested in other investing ideas, please check out my books here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.

March 23, 2019

10 Steps to Positive Personal Cash Flow

The key to being able to save and invest is having positive personal cash flow. The best approach is to have multiple sources of positive cash flow, not just your paycheck. This is often called "making money while you sleep" and it really is possible! You just have to start small, be disciplined and patient and don't get discouraged! Each one source individually might not amount to much - maybe only $50 to $100 per month, but when you add them all up it can be a lot of money and can help supplement what you bring home on your paycheck. If you're really successful, it can ultimately replace your paycheck and you can become Financially Independent and Retire Early (FIRE). What is the best way to accomplish this? Here are several simple steps that you can take to help get to that goal.

The key to being able to save and invest is having positive personal cash flow. The best approach is to have multiple sources of positive cash flow, not just your paycheck. This is often called "making money while you sleep" and it really is possible! You just have to start small, be disciplined and patient and don't get discouraged! Each one source individually might not amount to much - maybe only $50 to $100 per month, but when you add them all up it can be a lot of money and can help supplement what you bring home on your paycheck. If you're really successful, it can ultimately replace your paycheck and you can become Financially Independent and Retire Early (FIRE). What is the best way to accomplish this? Here are several simple steps that you can take to help get to that goal.Start with a household budget - when budgeting your expenses, make sure to "pay yourself first" and set aside money for savingsMake sure you have a plan to pay off high interest credit cards, then car loans, then student loansEnsure you have an emergency fund of 3 to 6 months of living expenses set asideFirst focus on retirement planning and maximize your 401(k) contributions, then make sure you are fully funding a Roth IRAInvest in residential real estate that generates a positive monthly cash flow (at least $100-$200 per month)Put cash in high interest yielding savings accounts (at least 2%)Invest in music royalties that yield at least 10%Invest in consistent dividend paying stocks (target a 3% to 6% yield) - these also have great tax advantages since qualified dividends are taxed at a lower rate than ordinary incomeDevelop other passive income sources that require you to invest some personal time up front but then minimal time thereafter in areas where you have a passion and expertise, such as writing and self-publishing books and online courses, blogging, starting a YouTube channel, etc.As the cash flow builds, continue to invest the extra cash in the same areas to compound growthRemember the rule of 72 (if you divide 72 by the interest rate you receive, you'll know how much time it will take for your investment to double in value). I was just reminded of the power of compounding recently when I cashed in a EE US Savings bond that I received as a gift for my son when he was born (he's now 18 and ready for college); it was purchased for $500 and is now worth a little over $1,000! Best part is if I use the money for college I don't have to pay tax on the interest!

If you are interested in other investing ideas, please check out my books here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.

March 16, 2019

Emergency Fund or Pay off Credit Cards?

Should I pay off my credit cards or build an emergency fund? How much of an emergency fund should I have? What should I invest my emergency fund in? These are very common questions, especially for people who are early in their careers, just out of college or starting out fresh after a major life event. The general rule is that because credit card interest is very high (much higher than what you can earn on a savings account), it's better to pay off credit cards than to save. However, if an emergency does arise (car breaks down, an unexpected home repair, or medical payment), you will need to use the credit card to cover the emergency expense, which can put you back in the same place. Also, your home equity is not an emergency fund, as I have written about before - see my related post. As soon as credit cards are paid off, then it's a good idea to build an emergency fund. The amount of your emergency fund should be at least three months of living expenses and ideally six to nine months of living expenses. So, for example, if your monthly living expenses (including rent, car payment, food, utilities, etc.) are $5,000 then you should start to build a $15,000 emergency fund and then increase it to $30,000 and then $45,000. Emergency funds should be invested very safely, preferably in an FDIC insured bank account or my favorite, which is US Treasury Bills that you can buy directly from the US government with a TreasuryDirect account. There are many savings account options to choose from - see this post on best savings account rates for some ideas. Once you have built your emergency fund, the next steps would be to fully-fund your retirement accounts (401(k) at work or Individual Retirement Account, preferably a Roth), then build your taxable accounts. If you're interested in investing ideas for your taxable accounts, check out my books on Amazon. Then you are well on your way to Building a Financial Fortress!

Should I pay off my credit cards or build an emergency fund? How much of an emergency fund should I have? What should I invest my emergency fund in? These are very common questions, especially for people who are early in their careers, just out of college or starting out fresh after a major life event. The general rule is that because credit card interest is very high (much higher than what you can earn on a savings account), it's better to pay off credit cards than to save. However, if an emergency does arise (car breaks down, an unexpected home repair, or medical payment), you will need to use the credit card to cover the emergency expense, which can put you back in the same place. Also, your home equity is not an emergency fund, as I have written about before - see my related post. As soon as credit cards are paid off, then it's a good idea to build an emergency fund. The amount of your emergency fund should be at least three months of living expenses and ideally six to nine months of living expenses. So, for example, if your monthly living expenses (including rent, car payment, food, utilities, etc.) are $5,000 then you should start to build a $15,000 emergency fund and then increase it to $30,000 and then $45,000. Emergency funds should be invested very safely, preferably in an FDIC insured bank account or my favorite, which is US Treasury Bills that you can buy directly from the US government with a TreasuryDirect account. There are many savings account options to choose from - see this post on best savings account rates for some ideas. Once you have built your emergency fund, the next steps would be to fully-fund your retirement accounts (401(k) at work or Individual Retirement Account, preferably a Roth), then build your taxable accounts. If you're interested in investing ideas for your taxable accounts, check out my books on Amazon. Then you are well on your way to Building a Financial Fortress!

March 8, 2019

Saving For College

Many people recommend you save for college using 529 Plans. Here's some information on these programs and my own experience with them.

Many people recommend you save for college using 529 Plans. Here's some information on these programs and my own experience with them.Among the biggest advantages of 529 plans over other college savings options are the tax advantages they offer. Earnings grow tax-deferred and withdrawals are tax-free when used for qualified education expenses.

Although the IRS typically allows you to give no more than $15,000 a year (for tax year 2019) to another person without a federal gift tax, you can contribute up to $75,000 to a 529 plan in one year. A special tax law allows you to aggregate five years of the allowable $15,000 annual gift-tax exclusion to jump-start a 529 plan. While you will be precluded from making any further gifts for five years, compounding will make your earnings grow faster than if you invested $15,000 in each of the five years. Also, anyone can contribute to a 529 plan. Unlike education savings accounts (ESAs) and saving bonds, there are no income limitations. For most wealthy families, 529 plans are one of the few available tax-advantaged college savings options.The assets of one 529 plan can be transferred tax-free to another 529 plan of another beneficiary, as long as the new beneficiary is a "family member" of the beneficiary of the 529 plan from which the transfer was made. "Family members" include, among others, the beneficiary's spouse, son, daughter, grandchild, niece, nephew and first cousin.If your child decides not to go to college or you over-fund a 529 plan, you may pay a penalty in addition to any taxes you owe on earnings. If you withdraw money from a 529 plan that is not used for qualified education expenses, you are generally required to pay income tax and an additional 10-percent penalty on earnings.There are a number of exceptions to this penalty. The penalty may be waived if your child gets a scholarship or is disabled. You also can avoid the taxes and penalties by transferring the 529 plan to another beneficiary who will use the funds for qualified education expenses. My own experience with 529 plans is that the investment options in these state-sponsored plans are not very good. We setup one plan initially for my son and it lost money, then we moved the funds to another plan and it didn't do much better. Also, since you can only use the money for educational expenses, this limits the flexibility if for some reason you don't need the money for education.

For these reasons, I decided a few years ago to close the 529 and move the money into a Uniform Transfers to Minors Act (UTMA) account for my son. I also set up similar accounts for my other children. You have more flexibility over investment choices, which is great and you also have flexibility in the use of the money for just about anything as long as your child who owns the account is the beneficiary of the funds. A portion of the child's income earned by the investments is tax free and a portion is taxable at the child's rate or parent's rate, depending on age. If not needed for college, your child will have the money to help them get started living on their own after they graduate (they get access to the money at age 18 or 21, depending on the state). We invested in some growth stocks for early years and then as each child gets closer to college age, we move the money into safe money market investments, while continuing monthly contributions. So far, this has worked out well.

If you're interested in other investing ideas, you may want to check out one of my books, click here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.

March 2, 2019

Lyft IPO Summary

Year Ended

December 31, 201620172018 (in thousands, except for pershare amounts)Revenue $343,298$1,059,881$2,156,616

Costs and expenses(1) Cost of revenue 279,011659,5331,243,400Operations and support 97,880183,513338,402Research and development 64,704136,646300,836Sales and marketing 434,344567,015803,751General and administrative 159,962221,446447,938

Total costs and expenses 1,035,9011,768,1533,134,327

Loss from operations (692,603) (708,272) (977,711) Interest income, net 6,96420,24366,462Other income, net 3,246284652

Loss before income taxes (682,393) (687,745) (910,597) Provision for income taxes 401556738

Net loss $(682,794) $(688,301) $(911,335)

Net loss per share attributable to common stockholders, basic and diluted(2) $(37.08) $(35.53) $(43.04)

While Lyft is showing impressive revenue growth, expenses are very high and are driving huge losses. In 2018, the company spent 21% of its revenue on General and Administrative expenses, which is a red flag for me as is the 37% of revenue spent on Sales and Marketing.

The risk factors in the registration statement include most notably competition, including the much larger Uber as well as a host of other startups. The development of autonomous driving technology and how Lyft is able to leverage that in their business is also a fairly significant risk. They also face risks associated with insurance of their drivers' vehicles. This is an interesting read. My concern here is that reinsurance is a complicated business and is not really core to a ride sharing platform.

From the time a driver becomes available to accept rides in the Lyft Driver app until the rider is dropped off at their destination, we, through our wholly-owned insurance subsidiary and deductibles, bear substantially all of the financial risk with respect to auto-related incidents, including bodily injury, property damage and uninsured and underinsured motorist liability. To comply with certain state insurance regulatory requirements for auto-related risks, we procure a number of third-party insurance policies which provide the required coverage in such states. Our insurance subsidiary reinsures the auto-related risk from such third-party insurance providers. In connection with our reinsurance and deductible arrangements, we deposit funds into trust accounts with a third-party financial institution from which such third-party insurance providers are reimbursed for claims payments. Our restricted reinsurance trust investments as of December 31, 2016, 2017 and 2018 were $118.3 million, $360.9 million and $863.7 million, respectively.The Company also has two classes of stock and the founders will continue to control the majority of the voting through the shares they own (not being sold in the IPO). This raises corporate governance issues in my mind.

Lyft may indeed some day be a very successful company or it could end up like Groupon. Either way, it's best to proceed with caution and if you do decide to buy shares in the IPO, keep it small.

If you're interested in other investing ideas, you may want to check out one of my books, click here.

Disclaimer: I use affiliate links where I get paid a small amount if you buy the service or product. This helps support my blog.