Harlan Vaughn's Blog, page 21

October 2, 2018

Free Money: Why Even Frugal Folks Should Have a Credit Card

Just got back from FinCon. Of course I told everyone how I like to travel using credit card points & miles. Within the personal finance/FI/RE community, I was shocked how many people still don’t have credit cards.

And these are people who delight in number-crunching!

I understand the concerns about mismanagement, overspending, or accidentally missing a payment. But fact is, credit cards are part of adulting because your credit score is part of adulting.

Responsibly using credit is a sign to lenders that you qualify for lower rates and higher lines of credit. You can’t even rent an apartment without a credit check these days.

I’ve literally earned $1000s for free with no annual fee credit cards – everyone should!

And if you’re counting every penny, you definitely want a credit card. Because you can get back 2% of everything you spend. For completely free. Why wouldn’t anyone want that?

No annual fee credit cards are a no-brainer

Link: No annual fee credit cards

Link: Cashback credit cards

My generation graduated college into a nonexistent job market because of the 2008 recession. I worked retail jobs, served tables, and poured drinks until I eventually found a staff job after months of sending job applications into the black hole of the internet.

For a long time, I innately distrusted money. After months of piecing together rent payments, there was no way I could afford a single misstep. One mistake would mean $100s of dollars in late fees – and I didn’t have it to throw away.

I knew credit cards, with their late payment fees, interest rates, and generational reputation, were prime evil. When I got my first one, I treated it like an animal that would turn on me at any second. I was terrified to mess it up.

Ah, but a small sample of the 30+ cards I currently hold

Over the years, my attitude changed. I enjoy being in touch with my finances. My credit score hovers around 800.

I got a great rate on my first mortgage, and on an auto loan last year. My credit limits are high and utilization low. I pass every credit check with flying colors.

I’m not afraid of credit cards any more. Now, I make them work for me.

1. You need credit

If you ever want to:

Own a home

Rent your own place

Buy or lease a car

Get high-level jobs

Refinance student loans

Open a personal loan

Cosign for your kids or family…

Then you need a credit score. That’s only built by using credit lines responsibly. Opening a card with no annual fee is the easiest way to start building credit, even if you only charge something small and set up automatic payments every month.

Sooner or later, you’re going to need a good credit score. The earlier you begin, the better.

2. They offer protection

For consumer purchases, you get way more protection with a credit card than you do with a debit card. Some credit cards even offer price protection and extended warranties. If there’s fraud on your account, you’re NOT liable for the damages.

Debit cards are a direct link to your bank account. The second you swipe them, the money comes out. Credit cards offer a buffer should your card number fall into the wrong hands.

3. Better cash flow

Link: Turn Your Credit Card Into a Debit Card (And Earn Rewards!) With This Website and App

When your credit card statement closes, you legally have a 28-day grace period to pay everything back in full. If you get paid every couple of weeks, there might be a few days per month when things get tight. Having a credit card – THAT YOU KNOW YOU WILL REPAY IN FULL – can give you better control of your finances.

I personally have internet, phone, Netflix, Spotify, insurance, electricity, and a couple of other services set to autopay. If those were randomly coming out of my checking account all month, I’d be a nervous wreck if my balance got low.

I much prefer to watch it roll in so I can strategize about when checks are coming in and when I can repay. If you can’t handle the payment cycles, try a service like Debitize that turns your credit card into a debit card.

4. FREE MONEY

Seriously! Imagine if you got 2% cashback on everything you spent. $2 back every time you spent $100. Over the course of a year. With a card that’s free to get and keep. It all adds up!

I’ve gotten $1,000+ back from my Discover It card this year!

I wrote about my adventures maximizing cashback with Discover It cards.

The first year, I got $2,368 back

The second year, I got $2,226 back

And this year, the third, I’m getting $1,043 back

Just for using the card regularly in the bonus categories, I’ve earned $5,600+ and never paid a single dime of interest or a fee to have the cards.

I’ve gotten $100s in free Roth IRA contributions with my Fidelity Visa, which earns 2% cashback on every purchase and has no annual fee.

And my Chase Freedom card has been a never-ending source of valuable Chase Ultimate Rewards points thanks to 5% cashback categories that change each quarter.

Chase Freedom15,000 Chase Ultimate Rewards points

• $0 annual fee• $500 on purchases in the first 3 months from account opening

• A great first Chase card• Compare it here

Not using a free credit card to earn cash rewards is literally leaving free money on the table. Even if you don’t earn a lot, why say no to free money?

Money is a tool – and you can use it to make more

I love managing my money. I love looking at my balances, moving it around, and making it work for me. Multiple accounts at different banks don’t phase me.

Why? Because money is a tool.

It’s true

Money exists to bring you things that make you happy. And like any tool, it’s neither inherently good or bad. But the more skilled you are, the more finely you can sculpt your life, your reality, your future.

Some peeps think “money” is a dirty word. They don’t like watching it flow in and out. And they make careless mistakes that end up costing them… more money.

But you can NOT live without money. You have to pay for where you live, exchange dollars for food, and find a way to get to work.

And while, yes, credit card companies prey on carelessness, when you pay attention, you reap the benefits of a credit score, free cash rewards, consumer protections, and better financial control.

If you want to know anyone’s true passion, look where they spend their money. That will tell you exactly what they value. The sooner you get comfortable with money, the sooner you can start earning free cash. Even – and especially – if you’re frugal!

Bottom line

Link: No annual fee credit cards

Link: Cashback credit cards

This subject is near and dear to my heart. And it pains me to watch people paying with debit cards. I understand the “evils” of credit cards. But why say no to free money? If anything, use it as encouragement to manage your finances better.

Once you get comfortable earning rewards on one card and with your higher credit score, you’ll find things begin to flow more easily.

If you have to spend money anyway – which everyone does – get rewarded for it! Here are cards with no annual fee and others with cashback rewards. After a few months, you might be surprised at how much cashback you accumulate. Getting comfortable with credit is one of the best – and most rewarding – things you can do for your future.

Also see: How I Got Started With Points & Miles 6 Years Ago

October 1, 2018

Allbirds Alternative for Guys: Try These Stylish Travel Shoes for Only $40

Last year, I championed Allbirds shoes because they look great, last a long time, and feel like walking on a cloud. I wore them every time I traveled – and walked 100s of miles in them.

For $95 a pair, that’s a great price for shoes you’ll have for up to a year. I wore them until the grip on the soles wore off and little holes appeared in the bottom. I’m rough on my shoes, and get a certain amount of pride from putting them through the wringer. I need my shoes to carry me from place to place – and I am not kind to them when I’m on the go.

So when I found a similar shoe for $40, I decided to give it a go. Urban Fox shoes are just as comfy, stylish, and simple as Allbirds. And I dare say – even more comfortable.

These are NOT Allbirds. They’re $40 and even more comfy. Why pay $95 for the same look?

After walking around FinCon for a solid week in these bad boys, I can confidently say they’re the real deal. And while I like the sustainability/green choice factor with Allbirds, I also like paying $40 instead of $95 for a similar product.

Are Urban Fox shoes the best Allbirds alternative?

Link: Urban Fox Parker shoe on Amazon

The company that makes these shoes, Urban Fox, only creates men’s products.

After my Allbirds bit the dust, I wore my old New Balance shoes until those, too, eventually died. I thought about getting another pair of Allbirds, but decided to research before committing. I’m glad I did, because it led me to these Urban Fox wool sneakers.

I think these are my new “one pair” when I travel

I want a shoe I can take when I travel. Something simple – no flashy logos – that’s easy to slip on and off, has great support, and can dress up or down. Essentially, I want to take one pair of shoes when I travel and have those shoes be neutral and versatile enough for any environment.

Like Allbirds, the Urban Fox Parker shoes have a wool top, thick padded bottom, and removable insole.

You’ll also notice they’re similar colors, shape, and overall design.

These are Allbirds – can you tell the difference?

There are only ~20 reviews online, but 80% of them are 5 stars. Peeps love how lightweight they are, the comfort, and the wool material used for the top.

They also come in gray/white and black/black

After absorbing the reviews and seeing they were only $40, I decided to give them a shot. And took them as my only pair to FinCon, where I knew I’d be walking a lot.

The black/black variety look very sleek

After raving about them at FinCon, a friend ordered a pair to try – and he loves them as much as I do, so far.

Urban Fox Vs Allbirds

The dark gray color I got is nearly identical to my old Allbirds. So is the bottom, and general look.

One thing I like much more on the Urban Fox shoes is the support. Whereas Allbirds got a “crinkle” in the heel area, the Urban Fox Parker is stacked solid. It is thick and cushy and bouncy all at the same time. It really feels like walking on air. I cannot overstate how good the support feels.

As far as other elements, the wool top feels just like Allbirds. The laces are the same. The bottom actually has a little more grip than Allbirds. It feels more solid, like it can stand a lot more impact – which is awesome.

I like the traction on these puppies

The bottoms have a wavy design imprinted whereas Allbirds are completely smooth. But it’s not a dealbreaker at all.

The final difference is invisible. Allbirds are all about sustainability and being kind to nature. I don’t know where Urban Fox stands on those issues. In fact, I’d never even heard of the brand and can’t find an official website for them. So I don’t really know where they come from or what their corporate posturing is on that.

Buck for buck, these shoes are comfy as heck

But I do understand the difference between $40 and $95 for similar items. After trying them, they’re good enough to challenge the title of “world’s most comfortable shoe.”

Bottom line

Link: Urban Fox Parker shoe on Amazon

Allbirds were the only show in town for a while there. So I’m glad to see competition in the wool top/travel shoe arena. There are lots more out there. But when I saw these Urban Fox Parker shoes for $40 on Amazon with free shipping, I couldn’t resist trying them out.

If you’re looking for a comfy shoe to wear pretty much anywhere with incredible support, I definitely recommend them. The price is almost too good to believe. And I like them more from a support perspective, which is important to me.

Be sure to check out my original Allbirds review and 6-month followup for more comparison. I’m looking forward to 6+ months of roaming in these shoes!

Guys, would you consider these instead of Allbirds? Let me know if you snag a pair, or another alternative!

Sinemia Review: How It Works & How to Get the Most From It ($10 for 3 Movies a Month!)

So we all know MoviePass is dead as a doornail by now. Other programs have (or will) pop up, like AMC’s A-List and Alamo’s upcoming season pass (get on the waitlist now if you’re interested).

I used the ever-loving crap out of MoviePass, so losing it stung hard. But I’ve had Sinemia for a couple of weeks now and I gotta say – I like it even better than MoviePass.

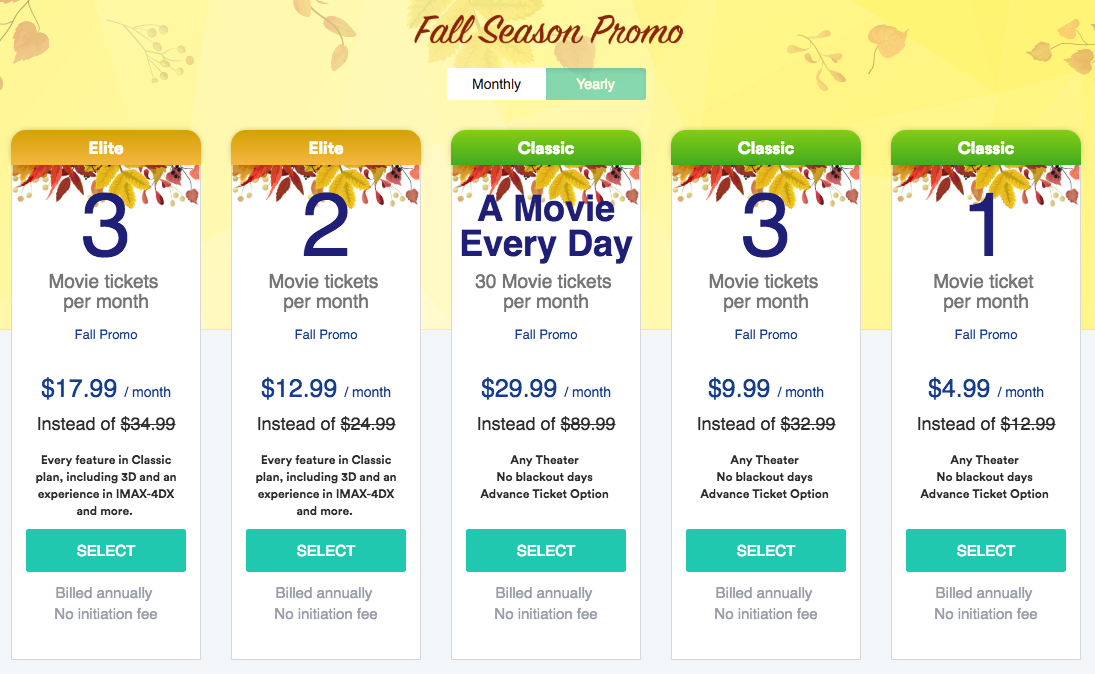

Right now, they have a fall promotion to see a movie:

Every day for $30 a month

3 times a month for $10 a month

1 time a month for $5 a month

Considering the average movie ticket is $10+, that’s a great deal. But with MoviePass in the can, it begs the question: how long will this one last?

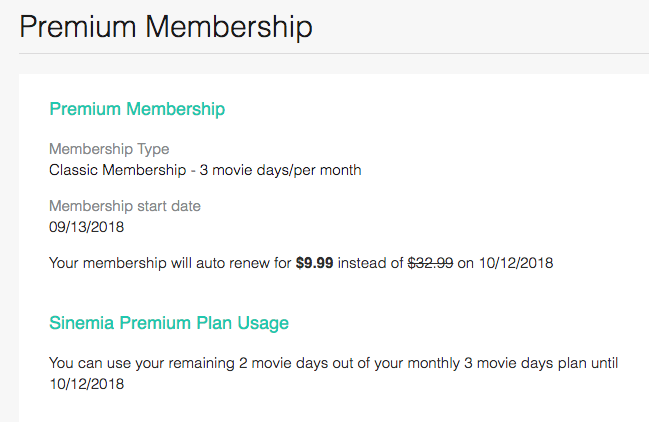

I opted for the $10 plan to see 3 movies a month

So far, so good, though. I like that you can buy tickets in advance. And there are a couple more ways to get an even better deal out of the membership.

My Sinemia Review

Key Link: Join Sinemia

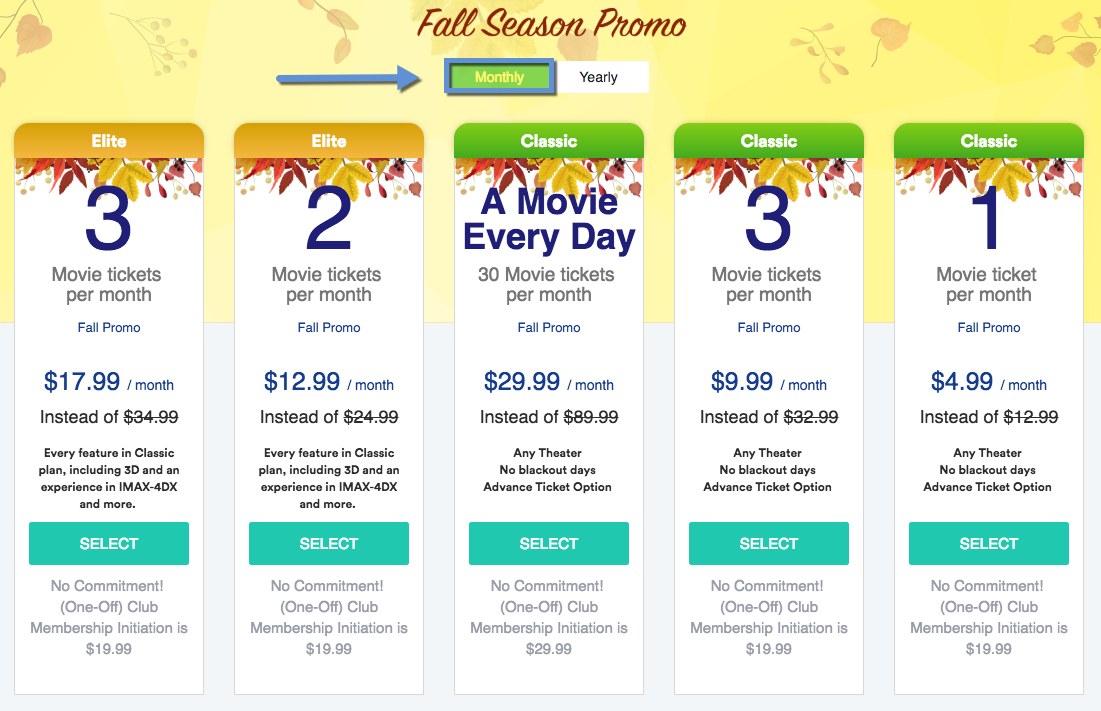

First, let’s look at the elephant in this room. Yes, the prices above are real but – HUGE CAVEAT ALERT – you have to pay annually to get them.

So $10 a month is really $120 for the year. You have to be willing to sink $120 into the enterprise to secure the rate.

Or!

You can pay monthly with an initiation fee.

Monthly options + initiation fees

I personally went this route to have the option to cancel any time. For the $10 a month plan, you’ll pay $20 straight away. Which means your first month is actually $30, then $10 a month afterward.

I will definitely see 3 movies a month for $10

And after you sign up, you can’t use the service right away. You have to wait ~2 weeks for them to “activate” your cardless payment option. Or, how convenient, you can pay $10 more to activate it instantly.

I was actually packing for a move, and then went to FinCon for a week, so I was happy to wait. But I was a little bummed there was one more “gotcha” before I could start watching movies. I mention it here to set expectations. When your card is active, that’s when your membership month begins.

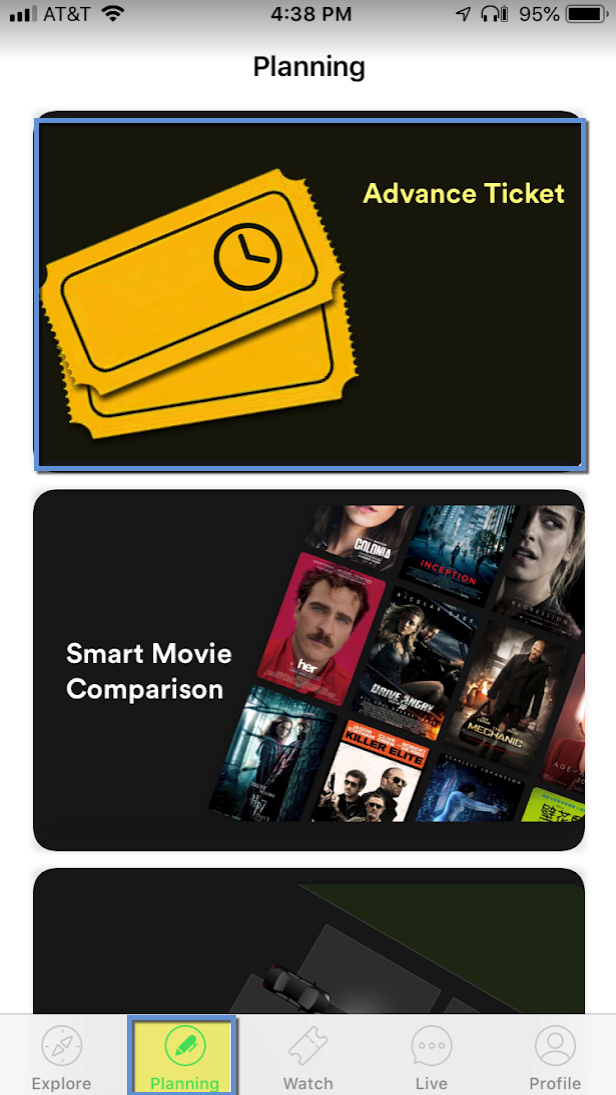

How Sinemia Works

It’s all in the app. To buy a ticket, load the app and click the “Planning” tab, then “Advance Ticket” – even if you are seeing a movie that same day.

Tap “Planning” then “Advance Ticket” to start the process

It’ll ask you which theater you’re going to, and the date and time. This is awesome because you can buy a ticket in advance – something you could never do with MoviePass.

I bought a ticket for “A Star Is Born” 2 days from now. So I don’t have to worry about it selling out day of. This puts Sinemia far above the competition.

September 17, 2018

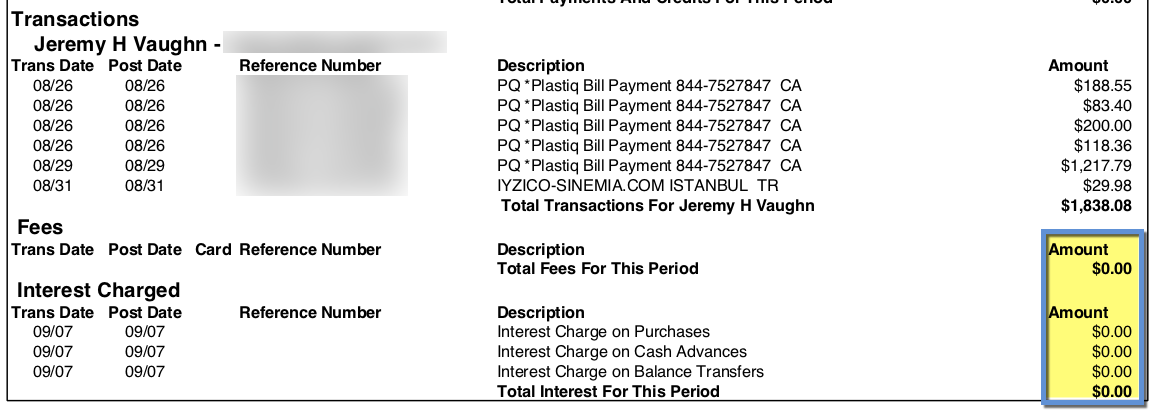

USAA Cards Not Earning Reward Points (Cashback) for Plastiq Payments

I opened a new USAA card to take advantage of a 0% APR rate until February 2020 (but gosh how I wish the Limitless card with 2.5% cashback everywhere would come back). I previously got a new card to make a student loan payment.

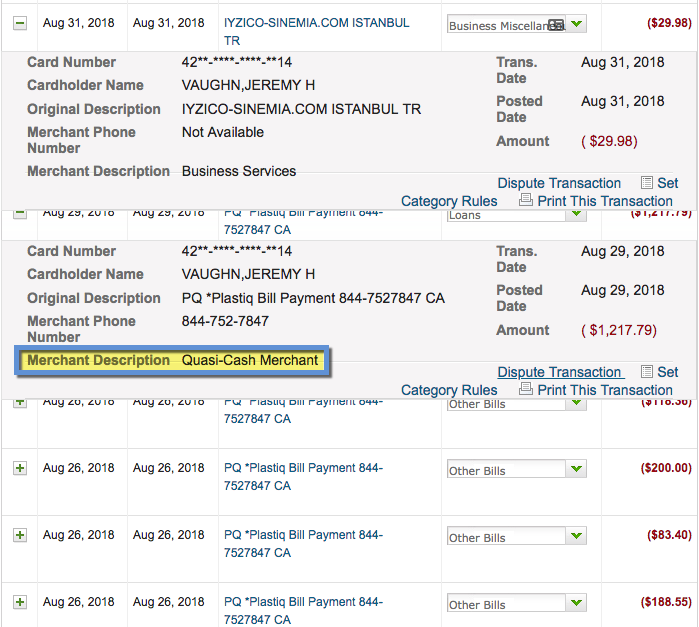

So the USAA Preferred Cash Rewards card earns 1.5% cashback on purchases. I was hoping Plastiq payments would code as “miscellaneous services” (or similar), but nope, they post as a “quasi-cash merchant” and do not earn any reward points.

So don’t use your USAA card with Plastiq!

More importantly, I hope this doesn’t signal a trend of Plastiq coding as cash-like purchases.

Don’t mix USAA cards with Plastiq payments, cuz you won’t earn rewards

Even still, I was not charged a cash advance fee per Plastiq’s advising.

Tread carefully with USAA Plastiq payments

Link: Blue Business Plus Amex – learn more here

Link: Blue Business Plus Amex: New Card for Plastiq Payments?

Currently, the best cards to use for Plastiq payments are:

MasterCards for mortgage payments

Discover cards for mortgage payments

Amex cards for rent, utilities, student loans, and most others

Visa small business cards

Within this framework, there aren’t many worthwhile cards left. That’s why I recommend the Blue Business Plus Amex (learn more here) for most payments, though the jury’s still out regarding mortgage payments.

If you go the Visa personal card route, you’ll get a cash advance fee on cards except those issued by:

Capital One

Navy Federal Credit Union

Alliant Credit Union

USAA

Wells Fargo

So when I saw USAA on the list, I thought, yay I can make payments without fees and get caught up on some bills.

I still did that but…

USAA cards don’t earn rewards for cash-like transactions

And Plastiq codes as a “quasi-cash merchant.” I hoped it would code differently.

USAA coding as cash-like

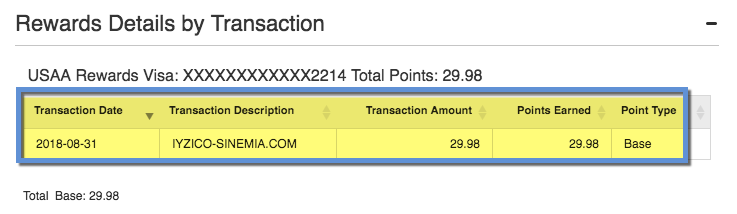

The only rewards I earned for this billing cycle were for my Sinemia membership (I’m using it the first time this week – review coming!). I earned nothing for $1,000+ of Plastiq payments.

Only earned ~30 measly points

That said, I did NOT incur cash advance fees (whew!) – so that is still a net positive.

No fees for any of the charges though

But it stung a little to lose/not earn all that cashback. Which would’ve been awesome, but alas.

Bottom line

The bit about USAA cards not earning rewards for Plastiq payments is niche because not everyone can get a USAA card. But the bigger issue is how Plastiq codes – and how it continues to shift.

In a general sense, I hope this doesn’t mean a shift toward no rewards with any cards because these payments will eventually code as cash-like instruments. If that ever happens, Plastiq will be useless.

For now, I’m still earning points and cashback with other cards. And, touch wood, I hope USAA is alone in how they’re processing payments for a long time.

Just wanted to put it out there in case you’re in the same boat.

September 7, 2018

7 Tricks to Save EVERY Time You Shop at Costco

Dear light of heaven, I love Costco. Whereas to some it can seem like a gigantic warehouse with narrow aisles stacked to the ceiling with pallets, to me it’s a veritable wonderland.

I love a good deal, and the best deals are often buying in bulk. When I mention I’m a Costco member, I’ve gotten scoffs and “Yeah but I don’t need 25 rolls of paper towels and 8 dozen eggs [or some other exaggeration]. Plus, where would I put it all?”

Ummmm… Costco was the cheapest place to shop in New York City, honey. If I can find space in a tiny Brooklyn apartment to store extra items and save some cash, you can too. And that’s what it’s all about: saving cash.

In my element

Admittedly, Costco isn’t always the best deal. Sometimes they try to pull one over on ya and slip in some regular-priced stuff. But I don’t blame ’em for trying to make profit. Because when the deals are good, hoooo boy are they stellar (find me a cheaper avocado and I’ll eat my hat, and bananas cheaper than Trader Joe’s). That’s what keeps me shopping at Costco year after year: THE DEALS.

On top of already great prices, I’ve found ways to push them even further by making sure I always get a discount. 2% off, 5% back, even 10% rebates in some cases when I’m in the mood to plan a big shopping trip.

Here’s how I save every time I shop at Costco.

Stack these offers to build your own discounts at Costco

Y’all know I love a good stack (that means combining a bunch of small discounts that add up to BIG discounts). The more you stack, the more you save.

You got this! Save that money!

You’ll be happy to know a lot of these offers are completely automated after you set them up just once.

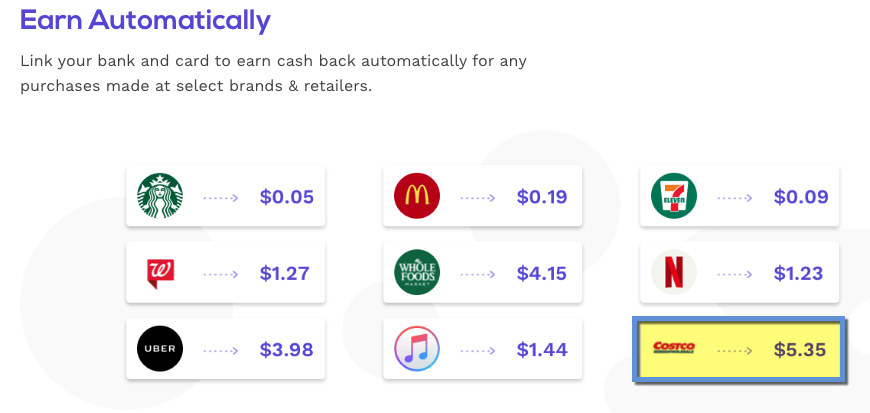

1. Save 1% with the Spent app

Link: Download Spent

Y’all prolly think I just sit around with a ton of apps on my phone cuz I’m always recommending them. But free money for downloading something? I’ll never turn that down.

You can get 1% back at many popular retailers, including Costco

With the Spent app, you need to plug-in your banking information one time. It will track your transactions and add 1% cashback when you activate offers on the app for popular merchants, including Starbucks, Uber, Whole Foods, Netflix, and Costco.

(I also have 1% cashback at Kroger, Shell, Chick-fil-A, and Home Depot in my offers.)

Be sure to activate the offer in-app

You can withdraw your earnings when you hit $20. At a 1% earn rate, you’ll need to spend $2,000 to get $20 back.

But:

It all adds up

It’s free money

You only need to set it up one time

If you spend a lot at Costco, getting a 1% rebate on every shopping trip is pretty sweet. Plus, with all the other cashback retailers, you can sit back and count your $20s as they roll in.

September 4, 2018

Mississippi on My Mind Tonight… #Gordon

I’m from Mississippi. I was born and raised in the Mississippi Delta (“The Most Southern Place on Earth” as in, characteristically Deep South) and went to one of the best public high schools in the US in Columbus before heading to Vermont for college (I went to Bennington, for the record).

The state is constantly glossed over in so many ways. I get it has a low population, little industry, and is stuck in 1950. But as another hurricane comes to shore (Gordon), I’m thinking about my home state tonight.

I grew up in Clarksdale

Just wanted to share a few thoughts.

The Mississippi weather I know

Total flyover state. It’s one of (if not the) poorest and least educated states and leads for most obese, with high rates of heart disease and diabetes. So… a bunch of poor, fat, uneducated people – which of course, is the stereotype anyway.

It’s also been getting scraped with violent weather as Tornado Alley shifts east (some people call it Dixie Alley) and more hurricanes pulverize its shores to literal shreds.

I was in Memphis on the night Katrina hit. And didn’t sleep at all because the air felt so sickeningly bad – just stayed up watching The Weather Channel. Then watched all the images filter in.

Everyone focused on New Orleans, of course. But the storm actually made landfall in Mississippi. And the physical damage along the Mississippi coast was far worse than what happened in New Orleans.

I’ll never forget driving through the state during the weeks after – so many trees turned over and roads blocked for repairs. Things that were there one day were gone the next – homes, businesses, land formations. It was chaos.

The south has its own sort of strange beauty

I also remember the sky turning literally purple a couple of times – and hearing the dead calm give way to train whistle sounds as tornados formed. Nothing will freeze your blood faster (well, except maybe hearing a rattlesnake and then seeing your foot next to it).

One summer, a couple of my high school’s buildings were simply swept away. There one minute, and then completely gone, right down to the studs in the ground.

A new hurricane, but old problems

I tend to watch the weather there because all of my family lives scattered around the area. So of course, with a new hurricane making landfall tonight, I’m hyper aware of what’s going on.

We rarely get national coverage.

Um… you mean the entire Gulf Coast of Mississippi?!?

Dallas Meetup 9/14 – And Any Interest for AUSTIN Meetups?

Out and Out is hosting another Out for Miles frequent flyer meetup in Dallas, this time at Komali on Fitzhugh and Cole, right off Highway 75.

This one will be next Friday, September 14th, at 5:30pm – just in time for a fantastic happy hour! I made this one on Friday evening per a few requests. If you’re in the Dallas area, feel free to join!

See you next Friday at Komali for the next Out for Miles meetup

I also want to gauge interest for a potential Austin meetup. I was thinking of having one in early or mid-October. If this sounds fun, please leave a quick comment. I’ll try to organize it as soon as I’m done with FinCon!

Out for Miles event details

Link: Join Out for Miles

Link: RSVP here

We’ll be at the big table in front of the bar – you’ll see it right when you walk in. Grab a marg or glass of cold sangria and let’s discuss:

Recent best-ever card offers like 60,000 points with Citi ThankYou Premier or that new Capital One Savor card and if it’s worth it

Your summer travels and where you’re going this fall

The final fallout of the Marriott/Starwood merger

Chase’s further moves into being the worst bank for points collectors

Anything else about travel, points, or miles

Feel free to RSVP via the links or simply show up!

What: Out for Miles – Dallas Meetup

When: Friday, September 14th, from 5:30 to 7:30pm

Where: Komali, 4152 Cole Ave, Dallas, TX – Google Maps directions and location

Links: Join the group and RSVP on Meetup or RSVP on Facebook

The happy hour is until 7pm with:

$5 house margaritas

$5 sangria

$5 beers

1/2 off all appetizers

Here’s the full menu. Parking is directly in front of the restaurant and there’s a big lot attached, too.

Feel free to bring friends or plus ones!

(If you can’t make this one, join the official group to get updates on future events!)

Austin travel meetup???

I’ll also be between Austin and Dallas for the next little bit and thought it would be fun to expand Out for Miles into Central Texas.

Buy a Coin for $1,400 – Earn Points + $50 Cash!

Yay! I’m opted-in to this deal which happens at exactly 12pm Eastern Time on Thursday, September 6th, 2018.

It’s through PFS Buyers Club, which I’ve written about before.

The Palladium coin costs $1,387.50 + $4.95 shipping – so your total will be $1,392.45. PFS Buyers Club will pay you $1,443 once you complete the deal, for a profit of $50.55 – on top of the points you earn.

If you’re looking to meet minimum spending on a card, this is a simple way to do it!

Get ready to buy this coin and make $50 on Thursday

This one is going to go quick, so hurry if you can do it!

Buy through PFS Buyers Club and make $50

Key Link: PFS Buyers Club

There are a few conditions. First, you must opt into the deal. To do that, you need to make sure you can purchase the coin on Thursday, September 6th, 2018 at exactly 12pm Eastern Time.

The coins will sell out fast and you need to click the “Buy” button as soon as you can. Also, lots of people will opt-in and there are limited slots open.

To facilitate this day-of, I recommend creating an account in advance with the US Mint so you’re not having to create a new login and all that day of. This will be the order page.

That way, you can log in, do your thing, and get the points/cash ASAP.

Is it legit?

Yes. I have many many friends that have purchased deals through PFS Buyers Club with no issues whatsoever (myself included!).

More tips

If you have an upgrade offer on a card, this is an easy way to start knocking it out (I’m thinking Amex cards here)

If you get a retention offer from Citi to spend $X in X months, this will earn you more bonus points/miles. (This is how I’m going to use the deal – you might want to call and see if you have any. I got 5,000 AA miles for spending $1,000 in 3 months, so this deal knocks that out completely!)

If you just got a new credit card, you can use this to knock out all or some of your minimum spending requirements

Or, if you just want $50 and some points, that’s reason enough!

Bottom line

Key Link: PFS Buyers Club

Sign-up for an account via this link and click “Current Deal” to opt-in. Be sure you read through all the terms very carefully.

Also, don’t opt-in if you can’t make the purchase in the 10 minutes following 12pm Eastern Time this Thursday – you’ll be taking someone else’s slot who could actually use this deal.

Finally, this the order page you’ll need on Thursday.

Hurry! This is going to go FAST. Opt-in NOW if you can do the deal and are interested. Set a timer/reminder/alarm/email alert/whatever so you don’t forget!

Ultimately, you get $50 plus at least 1,400 points or miles for a few minutes of your time. So this is definitely worth it.

August 25, 2018

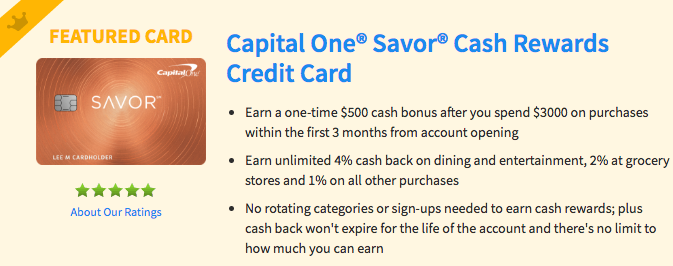

Get 4% Cashback for Sporting Events, Theme Parks, & More With This Card’s Unusual Category Bonus

Let’s talk about this new Capital One Savor card. It has:

A $500 cash sign-up bonus after meeting spending requirements

4% cashback on dining and entertainment

2% cashback at grocery stores

1% cashback everywhere else

Learn more here

I dug into that entertainment category and realized how surprisingly broad it really is. It includes:

Buying tickets to a movie, play, concert, sporting event, tourist attraction, theme park, aquarium, zoo, dance club, pool hall or bowling alley. Also, making purchases at record store and video rental locations.

Some of those things are pricey! And saving 4% could add up quick.

I freaking love Sleigh Bells (look them up!). You can earn 4% on a HUGE number of activities with Capital One Savor

The dining category is wide, too – it includes nearly any place you can get a meal, snack, or drink. But I’ll keep my Chase Sapphire Reserve for those purchases.

If you’re LOL/24, looking for a nice sign-up offer, or spend a lot on entertainment the card easily pays for itself. And could be worth keeping long-term.

Let’s look at some numbers.

Capital One Savor review

Key Link: Capital One Savor card – learn more here

To start, there aren’t many cards with “entertainment” as a category bonus. The only 2 that come to mind are Citi Prestige and Citi ThankYou Premier – both earn 2X for entertainment.

So not only does the Capital One Savor earn more for entertainment (4% cashback), it’s also not a Citi card (obvi).

You’ll earn $500 cashback after spending $3,000 on purchases within the first 3 months of account opening.

Deets of the Capital One Savor card

There’s a $95 annual fee, waived the first year. So you have a full 12 months to see how much you’ll earn with the card. And the sign-up bonus alone is worth it.

Keep in mind, Capital One pulls from all 3 credit bureaus when you apply for their cards. And they won’t give you more than 1 personal card every 6 months.

What’s entertainment include with Capital One Savor?

Here’s how I think of it: basically anything you do for fun outside your house. That would include things like:

Season passes for sporting events

August 15, 2018

GIVEAWAY: Enter to Win a Basic Pass to FinCon 2018 Next Month (Worth $600+)!

Join me at FinCon 2018 next month!

For my birthday weekend next week, I’m giving away a Basic Pass to the event which is September 26th through 29th, 2018, in Orlando!

The entries begin today at 5pm Central Time and end on August 22nd, 2018, at midnight Central Time!