Joe Withrow's Blog, page 9

December 6, 2023

What to do when trust is broken…

“Your dollar is a promise, a pact of trust,” President Nixon once assured the nation. “It will hold its value, come what may.”

The date was August 15, 1971. The day the world’s financial landscape was forever altered.

Nixon had just closed the “gold window”, a system that allowed foreign countries to exchange their US dollars for physical gold. This had been a cornerstone of the global monetary system for nearly 30 years.

The essence of this system was trust. But not in the US dollar. In gold.

If the United States started to print money excessively, the rest of the world could exchange their dollars for gold. That’s what the gold window was for.

The narrative behind Nixon’s “gold shock” is complex, but the aftermath is starkly clear…

Since Nixon’s decision, the US has created over $8 trillion out of thin air. This naturally diluted the purchasing power of each circulating dollar.

This is evident in the rising consumer prices we are all grappling with today.

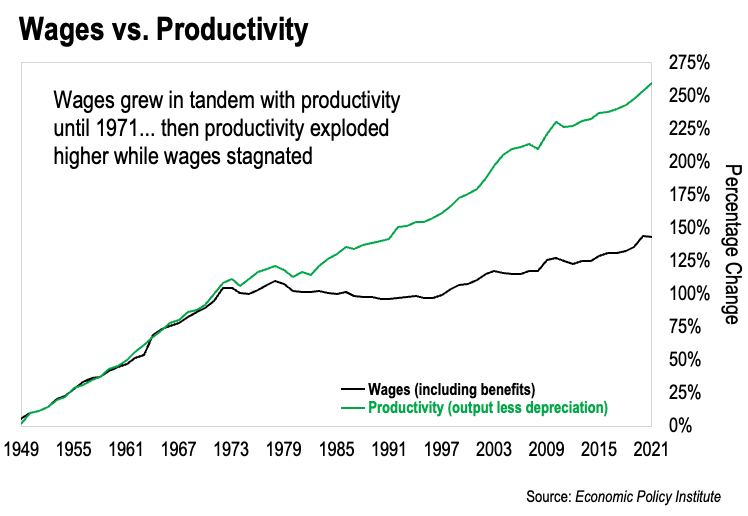

But there’s another, less visible story unfolding. This chart reveals the truth:

The chart compares the growth in median US wages, adjusted for inflation, against total American productivity. The data spans from the late 1940s to the present day.

It’s clear that wages and productivity were in sync until 1971. The average person’s salary increased proportionally with America’s output of goods and services. Just as it should.

But look at what’s happened since. Our productivity powered forward… but our inflation-adjusted wages went stagnant.

Why?

The trillions of dollars created from nothing siphoned purchasing power from everyone in the economy. And remember, this data is measuring the real purchasing power of wages adjusted for inflation.

In other words, nominal wages have gone up. In dollar terms, the median salary is higher than it’s ever been.

The problem is, those dollars buy just a fraction of what they once did. Because their purchasing power was stolen.

And where does this stolen purchasing power end up?

In the hands of those who get to use the newly created money first.

Creating new dollars out of thin air effectively funnels most of America’s productivity gains to Washington, DC and Wall Street. We can see that clearly in the chart above.

This dynamic is why it’s become more and more difficult to get ahead. If we follow the traditional success path, that is.

My friends, it’s time to shift our focus to a new approach—one designed for the times we find ourselves in today. If we do, true financial security is more available to us than ever before.

Stay tuned for a major announcement on that next week.

The post What to do when trust is broken… first appeared on Zenconomics.

The post What to do when trust is broken… appeared first on Zenconomics.

December 5, 2023

The Fed Can’t Outrun This Economic Law

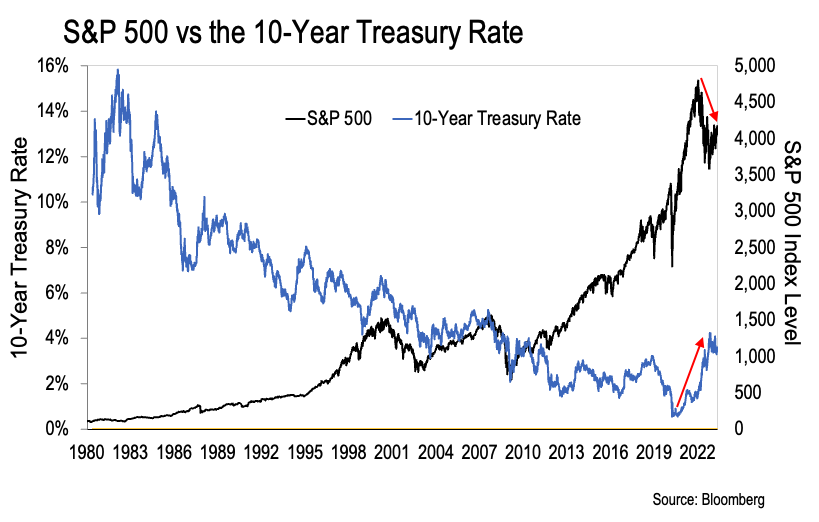

As regular readers know, my thesis is simple. The Age of Paper Wealth is over. This chart tells the story:

Here we can see the S&P 500 and the 10-year Treasury rate going back to 1980. The S&P 500 is the black line. And the 10-year Treasury rate is the blue line.

We’re using the S&P 500 as a proxy for US stock prices. And we’re using the 10-year Treasury as a proxy for interest rates. This chart makes it perfectly clear that the two are inversely correlated.

Interest rates started falling in 1982, and they fell consistently for the next 40 years. Meanwhile, US stocks consistently went up in value over that same time period.

But everything reversed in 2022. Rates started going up, and stock prices started to fall. We can see those moves clearly marked by the red arrows on the chart above.

So the period from 1982 to 2022 will go down in history as the Age of Paper Wealth.

And here’s the thing—what happened from 1982 to 2022 was not normal. Nor was it organic.

Instead, it was all driven by the debasement of our money.

The US government and the Federal Reserve (the Fed) worked hand-in-hand to create over $8 trillion dollars from thin air during this time period. We can verify that $8 trillion because it hit their balance sheet.

There’s also strong evidence that the Fed collaborated with other major central banks to create over $20 trillion off balance sheet in the wake of the 2008 financial crisis.

This activity drove interest rates down and stocks up.

As we discussed yesterday the Fed has a vested interest in reversing course. It needs to normalize interest rates to save the legacy financial system.

But some readers want to know – what if this thesis is wrong? What’s to say the Fed can’t get right back to their same antics?

It all comes down to the law of diminishing marginal utility.

The law of diminishing marginal utility states that as consumption increases, the utility derived from each additional unit declines. In the context of the Fed Put, this principle suggests that each additional round of stimulus has a smaller impact than the last.

The Fed Put began in 1987 under Fed Chairman Alan Greenspan.

In response to the Dow Jones Industrial Average falling over 22%, Greenspan cut interest rates to inject liquidity into the financial system. That set the precedent.

Going forward the Fed cut rates every time the stock market began to correct. In total it cut rates 47 times from 1990 through December 2008. When it was done, the Fed’s target rate was at zero.

What happened next illustrates the law of diminishing marginal utility very clearly.

In 2008 the Fed pumped $1.3 trillion into the financial system to effectively bail out the banks. That’s what it took to liquify the system and stop the stock market from plummeting.

But then when Covid-hysteria ramped up and the stock market crashed in 2020, the Fed had to pump over $3 trillion into the system to stop the bleeding. It took more than twice the amount of “stimulus” to back-stop the markets.

That’s the law of diminishing marginal utility at work. And there’s another nuance to it all that makes it finite.

Today our money comes from debt. By that I mean every new dollar created also creates an associated debt obligation.

When the Fed wants to pump money into the financial system, it does so by purchasing US Treasury bonds. And that means the US government must make interest payments to the Fed.

Sure, the Fed returns a portion of those interest payments back to the Treasury each year after it pays its own operating expenses.

But that doesn’t change the dynamic. The more money the Fed prints, the higher the US debt goes—driving up the Treasury’s annual debt service costs.

And that impacts the US government’s credit rating.

This is important because it influences real market actors. The more shaky the US credit rating is, the less foreign central banks and institutional investors will want to buy its bonds.

So at the end of the day it’s all a confidence game.

The Fed and the US Treasury have gotten away with creating trillions of dollars from nothing thus far. But that doesn’t mean they can do this forever.

The market will set limits… and Jerome Powell knows this.

That’s why he made a conscious decision to kill the Fed Put. It’s all about shoring up confidence in the system—a system in which the Fed and the New York banks benefit from tremendously.

-Joe Withrow

P.S. Stay tuned for a major announcement next week. I’ll be unveiling an opportunity that will help you navigate these complex financial waters. Don’t miss out on this chance to gain a deeper understanding of the economic landscape and learn how to protect and grow your money in these uncertain times.

The post The Fed Can’t Outrun This Economic Law first appeared on Zenconomics.

The post The Fed Can’t Outrun This Economic Law appeared first on Zenconomics.

December 4, 2023

Why the Fed Put Is Dead

Everything’s been on a tear this year.

Bitcoin’s up about 153% year to date. The S&P 500 is up roughly 20%. And gold has gained 13%. It’s now trading at all-time highs in all currencies.

These moves all occurred as the 10-year Treasury rate rose nearly 70 basis points – from 3.53% to start the year to 4.22% today.

This doesn’t make a lot of sense according to what’s become conventional wisdom over the past few decades. The market has come to expect assets like Bitcoin, stocks, and gold to fall in value when rates rise. So what gives?

Well, there’s been a lot of speculation that the Federal Reserve (the Fed) is going to turn around and begin easing again next year. In fact, the futures market is projecting a 45% chance that Fed Chairman Jerome Powell will cut the Fed’s target interest rate at his March 2024 meeting.

It’s not going to happen.

Clearly a large portion of the market still hasn’t accepted the core thesis that I’ve been presenting in these pages. The Age of Paper Wealth is over.

There were two primary trends from 1982 to 2022. Interest rates went down. Stocks went up.

And each time those trends threatened to reverse, the Fed stepped in to cut rates and push stocks higher again. That became known as the “Fed Put”.

This began in 1987 under Chairman Alan Greenspan. Then Ben Bernanke and Janet Yellen kept the Fed Put going as his successors at the Fed. We came to see it almost as a cosmic fixture.

But then Jerome Powell put his foot down last year.

Powell executed the most aggressive rate-hiking campaign in the history of central banking in America. And he made it clear to all who would listen that the jig was up.

I suspect those whose understanding of economics is informed by superficial mainstream sources missed the memo. They simply don’t have any historical context to compare it to. And the concept of malinvestment isn’t on their radar.

For those of us well-versed in Austrian economics—Powell’s actions are still hard to accept.

After all, the Fed is the enemy of free markets. It’s the institution that, more so than any other, has enabled Big Government to metastasize and distort so many areas of our economy – hollowing out the middle class in the process.

So we figured the Fed would do everything it could to keep rates at zero. That’s what’s necessary to monetize trillions in government debt and support all these uneconomical government programs.

We were wrong.

It’s become clear that the Fed isn’t blindly loyal to the US government. Its allegiance is to the interests underpinning the New York banking scene.

This is a faction unto itself. And its power and wealth reside here in America. As such, it needs a strong American economy and a robust commercial banking system.

That’s why the Fed Put is dead.

The Fed Put “financialized” everything. It created a world where we associated market health and economic health with numbers going up.

The stock market… gross domestic product (GDP) – as long as those numbers went up, we thought everything was fine. And when those numbers went down, we expected the Fed to rush in and save the day.

This directed trillions of dollars and countless man-hours to the financial industry.

Wall Street created roughly 71,492 mutual funds from 2009 to 2022. And while we don’t have exact data for exchange-traded funds and index funds, we can be sure that they created tens of thousands of those in this same time period as well.

None of this drives real economic activity. It simply herds capital into the financial markets where fund managers can siphon off big fees year after year.

Meanwhile, the fiat monetary system divorced American wage growth from economic productivity… which obliterated the American middle class.

Now our system of industrial capitalism is teetering. And if it falls, the legacy financial system falls with it. That would be very bad for the Fed and the New York banks.

That’s why they reversed course.

Tomorrow we’ll look at how a fundamental law of economics ensures that the Fed’s days of backstopping the stock market are over for good.

-Joe Withrow

P.S. It’s also a misconception that normalizing interest rates will eradicate consumer price inflation. With nearly $34 trillion in sovereign debt and a $2 trillion budget deficit, inflation is baked into the cake.

The bad news is that many are falling into the trap of thinking that the Fed’s rate hikes are about beating inflation. That’s not it. The good news is that if you understand what’s really happening, you’ll know exactly what financial moves to make.

I’ll have a big announcement for you on that front next week.

The post Why the Fed Put Is Dead first appeared on Zenconomics.

The post Why the Fed Put Is Dead appeared first on Zenconomics.

November 30, 2023

Ancient Secrets and Black Friday

I’ve got a bone to pick with Black Friday. And Cyber Monday. And Giving Tuesday…

I spent this past week wading through all the marketing emails that hit my inbox. I bet you did too.

Black Friday early sales… day-of sales… last chance sales… I lost count of how many there were. Then there was Cyber Monday. And all the emails for something called Giving Tuesday. I hadn’t even heard of that one before.

Of course, I don’t have any problem with these emails. I understand. I send out four emails every week myself.

But here’s the thing – the whole concept underlying Black Friday is a problem. That’s because it perpetuates the most common misconception we have around money.

It’s the consumerist view. The idea that the whole point of making money is to spend it on stuff. And then if we can make “good money”, we can buy even nicer stuff.

So many people view money in this way.

And as a result, they live their life on a treadmill. Constantly working for money… buying stuff… and working for more money.

I think it’s time we flipped the script.

I propose that the whole point of making money is to acquire assets that make their own money. Then when we have enough assets, they will produce all the money we need. We can get off the treadmill.

This is the key lesson in the timeless board game Monopoly. I think we would all be wise to heed it.

Of course, this raises the question – what assets should we buy?

That’s the question we answer in The Phoenician League.

Don’t you think it’s time we get off the treadmill? Isn’t it time we make the money we’ve worked so hard for work for us?

It turns out that building an asset portfolio isn’t quite as simple as buying some index funds online. Not if we want to make it bulletproof, anyway.

Then if we want to make sure that our assets produce income for us also – well, that takes a little more thought and planning.

The good news is that building a bulletproof asset portfolio that will also produce thousands of dollars for us in extra income each month isn’t difficult.

At The Phoenician League, we’ve got it down to a science. And we provide our members with a step-by-step approach that provides information and implementation.

That is to say, we walk everybody through the process and provide ongoing support. Nobody ever has to wonder what to do next.

And here’s the best part…

We leverage an ancient secret that’s been hidden in plain sight for thousands of years. It’s a simple thing… but it makes all the difference in the world when it comes to financial independence.

Ready to learn more?

Don’t let another day pass in uncertainty. Check out our story and our solutions right here.

-Joe Withrow

P.S. If you’re interested in giving The Phoenician League a look, please do so soon. We offer to do extensive onboarding with all our new members, so we can only bring in so many new folks at one time.

Our doors are currently open to you… but we’ll be closing them again on Sunday, December 3rd at midnight Eastern. Just click the link below for more information on how to join:

Achieve Financial Independence Using an Ancient Investing Secret

The post Ancient Secrets and Black Friday first appeared on Zenconomics.

The post Ancient Secrets and Black Friday appeared first on Zenconomics.

November 29, 2023

Why it’s gotten tough out there…

“Your dollar will be worth just as much tomorrow as it is today,” President Nixon proclaimed on television with a straight face.

“The effect of this action, in other words, will be to stabilize the dollar.”

The date was August 15, 1971. President Nixon just announced that he was closing what was known as the “gold window”. This was the system through which foreign countries could redeem US dollars for physical gold upon demand.

The gold window was a fixture of the Bretton Woods System of 1944. That was the international agreement which established the US dollar as the world’s reserve currency.

What we’re talking about here is trust. The idea was that if the United States started printing too much money, the rest of the world could trade their dollars in for gold.

After all, nobody wants to hold a currency that somebody else can create from nothing anytime they want.

The story behind Nixon’s “gold shock” is very nuanced. But what followed isn’t…

According to the Federal Reserve’s data, the US created over $8 trillion dollars from nothing since Nixon closed the gold window in 1971.

Naturally, this reduced the purchasing power of each dollar in circulation. That’s just basic supply and demand economics.

We see this very clearly in the form of rising consumer prices. But there’s a hidden story at work here also. This chart spills the beans:

This data comes from a study done by the Economic Policy Institute. Researchers there measured the growth in median US wages, adjusted for inflation, against total productivity – the output of goods and services. This data goes back to the late 1940s.

And we can see very clearly that wages moved in lockstep with overall productivity up until 1971. That means the average guy’s salary went up in proportion to America’s output of goods and services. As it should be.

We can also see very clearly that our productivity has continued to explode higher. But our wages, adjusted for inflation, have been mostly flat since 1971.

The reason?

Those trillions of dollars created from nothing stole purchasing power from everybody in the economy. And where does that purchasing power go?

To the people who get to use the newly created money first.

Ever wonder how the US government can spend trillions of dollars on every kind of program imaginable… and still run trillion-dollar deficits?

This chart explains it.

The act of creating new dollars from thin air effectively transfers all American productivity gains to Washington, DC. That’s been happening since the early 70s.

This dynamic is why it’s so hard to get ahead these days. And it is why we need to rethink financial planning 101.

Fortunately, there is a solution.

There is one tried-and-true investment that puts inflation to work for us, rather than against us. What’s more, this investment also creates passive income streams for us.

Passive income is critical. It’s how we fill in the gaps caused by stagnating wages. And with the right system, our passive income can quickly grow to meet and exceed our annual salary.

That’s what we focus on in The Phoenician League.

We have a step-by-step approach to bulletproofing our money and building extra monthly income. That’s how we mitigate inflation and keep up with rising costs of living.

With our system, anybody can work up to having $2,000 or $3,000 a month in passive income in just a few years. No previous knowledge or experience necessary.

From there, getting to $10,000 a month or more in extra income is just a matter of accelerating the process.

And here’s the thing – this can be done with no more thirty minutes worth of work each week. That’s the beauty of having the process and the networks already in place.

So we’re not talking about a side hustle here. We aren’t talking about an online business where we have to work nights and weekends to get the extra income.

Our approach is far more turn-key.

Look, it’s getting tough out there. The rules of money have changed.

But that doesn’t mean we need to fall victim to the circumstances. Quite the opposite.

I’m reminded of an old saying I heard years ago. It goes: Either you happen to the world or the world happens to you.

Let’s be the kind of people that happen to the world. That’s what The Phoenician League is all about.

If you’re interested in learning more about our membership, our doors are currently open. You can find more information right here:

Achieve Financial Independence Using an Ancient Investing Secret

-Joe Withrow

The post Why it’s gotten tough out there… first appeared on Zenconomics.

The post Why it’s gotten tough out there… appeared first on Zenconomics.

November 28, 2023

The Rules of Money Changed

The rules of money and finance changed last year.

If we look at a chart of the S&P 500 going back to the early 80s, the picture is clear as day—stocks only went up over time.

Sure there were plenty of “dips”. But from 1982 on, we could buy a simple mutual fund or index fund and two years later we would have made money. Fifteen years later we would have made a lot of money.

Meanwhile, if we were to overlay a chart of the 10-year Treasury rate – the opposite is true. Interest rates only went down over time.

That dynamic – stocks go up, rates go down – was largely thanks to the Federal Reserve (the Fed). It had a hand in both via “loose” monetary policy.

But the game’s over.

The Fed pivoted in 2022. And Fed Chair Jerome Powell made it abundantly clear that he will no longer push interest rates lower to support the stock market.

And that means The Age of Paper Wealth is over.

We’re in uncharted waters here. Nobody under the age of 60 has been an adult in a world in which the Fed didn’t push stocks up and rates down.

So to me, the big takeaway is that we have to rethink financial planning 101. And I’m talking about the entire “nest egg” approach to retirement.

By that I mean the idea that we need to pour our savings into financial assets trying to get to this mythical retirement number.

What’s Your Number? I remember old commercials promoting this slogan.

The nest egg model puts our assets and our income on a see-saw.

When we’re working, we focus on building up assets. Then when we retire we sell off those assets to create income.

It’s always a choice between assets and income.

When our assets are going up, we don’t have the income. Then when we want the income, our assets have to come down.

Why put ourselves in this position? Why not get assets and income on the same side of the equation?

Well, that’s exactly what we do inside The Phoenician League.

Are you skeptical of traditional retirement plans? Seeking a more dynamic way to secure your financial future? Welcome to The Phoenician League – a unique investment membership designed for those who dare to think differently.

We throw the entire idea of retirement out the window. Because instead of fixating upon a certain age, we focus on building both assets and passive income streams.

Then, once our income streams can cover our expenses… we’re good. We can stop working any time we want. But our income will keep coming in, month after month.

Why The Phoenician League?

Expert Guidance: We don’t just provide information. We walk you through each step of building your passive income streams.Community Support: Join a network of like-minded individuals, all focused on financial growth and independence.Real Success Stories: Our members speak for us. Brian M. discovered a “fantastic way to increase wealth,” while Nate J. started earning monthly passive income in just one month. Mike W. built more monthly income than he ever thought possible.Curious to learn more?

Click here to explore how The Phoenician League can revolutionize your approach to money, investing, and passive income.

Don’t just plan for the future. Actively shape it with us…

-Joe Withrow

The post The Rules of Money Changed first appeared on Zenconomics.

The post The Rules of Money Changed appeared first on Zenconomics.

November 27, 2023

The Beginning is Near

We’re at an inflection point in history right now. Things aren’t going back to how they used to be.

I don’t think the financial media understands this yet. But the bread crumbs have been in plain sight for over a year now.

It comes down to an arcane change at the core of our financial system.

Last year something called the Secured Overnight Financing Rate (SOFR) went live across the board.

I bet very few people out there even know what this is. And of those who do, I doubt many understood SOFR’s significance.

SOFR is a benchmark interest rate for dollar-denominated loans and derivatives.

We don’t need to go down a deep rabbit hole on this. What’s important to understand is that the interest rates for all loans in the U.S. are now influenced by SOFR.

The London Interbank Offered Rate (LIBOR) used to hold that privilege. Before this year those who influenced LIBOR could also influence interest rates in the U.S.

And that means the Fed did not previously have full control over U.S. monetary policy.

SOFR changed that.

That’s why the Fed raised interest rates so aggressively last year. It was all about planting the flag and letting the world know that the days of coordinated monetary policy were over. Globalism hit its peak.

That means the days of the Fed propping up the stock market are over. The Fed Put is dead.

And this aggressive monetary policy will force some dramatic changes with how U.S. Treasury debt is handled. I think we may even see gold partially remonetized as a means of offsetting higher rates.

As such, we need to completely rethink financial planning 101. The old ways aren’t going to work anymore.

And that’s where The Phoenician League comes in.

Imagine a future where you’re not just surviving, but thriving. A future where you’re not just keeping up with inflation, but outpacing it. A future where you’re not just preserving your money, but growing it.

This is the future The Phoenician League can help you build.

The Phoenician League is an investment membership program that leverages an ancient investing “secret” to help you bulletproof your money and build passive income streams. In as little as 30 days, you could start receiving passive income checks that show up every month, right on time.

But The Phoenician League is more than just a source of passive income. It’s a network.

And our network is a shield against the uncertainties of the future. As the world changes and The Age of Paper Wealth fades away, our professional network will be right here—adapting to the times.

Imagine it’s five or ten years from now. The world is a radically different place. And millions of people who trusted their fortunes to paper wealth are struggling to live out their retirement with dignity.

But not you.

Your real assets have protected you from inflation. And your passive income empire is still growing. That’s the vision.

And we built our membership around that vision. It’s all about information, connections, and mutual support.

Join The Phoenician League today and start building your future. Because financial independence isn’t just about weathering the storm. It’s about living a purpose-driven life.

Please note that we do extensive onboarding for all new members. We make sure everybody knows exactly how our network and resources can work for their situation.

As such, we can only accept a limited number of new members at any given time. Just go right here for more information on how to join the membership while our doors are open.

-Joe Withrow

The post The Beginning is Near first appeared on Zenconomics.

The post The Beginning is Near appeared first on Zenconomics.

November 20, 2023

Thankful 2023

Hey friends,

In the spirit of the upcoming holiday, I felt compelled to share a quick note of appreciation with you today. No markets, economics, investments, or theories today… just thankfulness.

We talk a lot about becoming a good steward of civilization inside our investment membership The Phoenician League. What that means is a little different to each of us… but it’s tangible. And practical.

If we look around our world today, there’s something that’s blatantly obvious – yet none of us recognize it for what it is. We have conquered scarcity.

This statement is considered blasphemous in certain circles, but it’s true. It’s evident.

If a person who died prior to 1940 were to somehow magically appear in our world today, this is the very first thing they would realize. Humans conquered scarcity. That fact would smack them right in the face… because they didn’t think it was possible.

What I mean is this…

Nobody goes hungry in the developed world today. Quite the opposite. Even the “poorest” among us have the means to consume far more calories than they need.

And that’s because we – humanity – now have the ability to produce food in abundance. And we do just that. It’s estimated that we throw away roughly 133 billion pounds of food every single year… because we don’t need it.

Often when I mention this, somebody will point out that there are still people in developing countries who do sometimes go hungry. Countries in Africa and Latin America are often mentioned.

And that may be true. But it’s not because food is scarce.

It’s because their corrupt governments, bureaucracies, and power factions enforce artificial scarcity. They siphon off the hundreds of billions of dollars in humanitarian aid for themselves. And they prevent modern markets and logistical infrastructure from forming—despite the fact that those institutions are what would enable their people to lift themselves out of poverty.

Some folks like to argue that last point too. But I don’t think it can be refuted logically.

Poverty is the default position. For most of human history nearly everybody alive lived in poverty. Humans were always one bad harvest away from food shortages.

Our recent ancestors changed that. And they did so through hard work, innovation, and human ingenuity over time. And that’s the key. The innovations built upon themselves. They accreted.

And of course it’s not just food.

Today we have big houses, comfortable furniture, central heating and air conditioning… flat screen TVs, smartphones, fast cars, air travel – you name it. All of this would look like magic to those who came before us.

When I think about it all, I can’t help but feel a direct link to the past. And I am thankful. I’m thankful for all the hard work our ancestors did to create a world of abundance for us to enjoy.

So when I think about being a good steward, it’s about doing my part to pass on this world of abundance to my children and grandchildren… and maybe upgrading it ever-so-slightly.

With that mindset in place, I see all kinds of opportunities. Just in my local area.

Lots of little things would make an impact if someone made the effort to do them. And little things add up to big things. That’s especially true when there are lots of people out there doing little things that matter.

That’s the world I want to pass on to my kids. A world of abundance and thoughtful stewards.

And guess what? We don’t need elections or laws to build that world. We just need to act with purpose.

My friends, we are the ones we’ve been waiting for. That’s why I’m also thankful for you.

Happy Thanksgiving.

Joe

P.S. The Mrs. and I are taking the kids to visit their cousins for Thanksgiving. We’ll be out of town the next several days… and I doubt the environment will be conducive to writing. So this will be my only original e-letter this week.

I won’t leave you empty-handed though. I’m going to pick out a few excerpts from my monthly newsletter The Phoenician to share with you tomorrow, Wednesday, and Thursday at our normal publishing time.

The post Thankful 2023 first appeared on Zenconomics.

The post Thankful 2023 appeared first on Zenconomics.

November 16, 2023

What to do about uncertain times…

People who are in or approaching retirement today face immense challenges that those who retired in the years before them did not.

Simply put, we’ve been living in a bubble world since the 1980s, but the bubble popped in 2022.

I think most of us know this to be true. We can feel it. But this next chart tells the story quite well:

Here we can see the S&P 500 and the 10-year Treasury rate going back to 1980. The S&P 500 is the black line. And the 10-year Treasury rate is the blue line.

We’re using the S&P 500 as a proxy for US stock prices. And we’re using the 10-year Treasury as a proxy for interest rates. This chart makes it perfectly clear that the two are inversely correlated.

Interest rates started falling in 1982, and they fell consistently for the next 40 years. Meanwhile, US stocks consistently went up in value over that same time period.

But everything reversed in 2022. Rates started going up, and stock prices started to fall. We can see those moves clearly marked by the red arrows on the chart above.

I keep coming back to this image because I want to hammer the message home. The Age of Paper Wealth is over.

The question is – what comes next?

We’ve talked all week about the secret war between the globalist power structure and the New York Banking Cartel. It’s all about answering this question. They know the game is up… and each faction wants to control what comes next.

Of course, this raises an important question for us. What do we do about it?

We’ve worked so hard to build up some wealth and plan for what we hope to be an enjoyable, meaningful retirement. But how do we plan strategically amidst all the uncertainties we see out there today?

To me, it comes down to four pillars. They are:

Asset AllocationPortfolio ConstructionCash FlowAlternative InvestmentsLet’s hit each of these briefly today.

Asset Allocation

Asset allocation is about spreading our money—our capital—across several different asset classes. I find it’s best to do this according to a personalized model. The purpose here is true diversification.

I suspect many of us hear the word diversification and CNBC’s definition comes to mind. You know, buy stocks in all kinds of different industries so that we have a diversified portfolio.

I don’t believe that.

Whenever we see market crashes or bear markets, they typically take all stocks down. Maybe utility stocks go down less than early-stage biotech stocks… but they go down all the same.

Asset allocation is about true diversification. Stocks are just one piece of the model.

So here’s what this looks like. An antifragile asset allocation model will consist of:

10–20% Cash5–10% Gold10–50% Real Estate10–30% Stocks0–10% Bonds5–20% Bitcoin0–5% Early-Stage InvestmentsKeep in mind this model is just a suggestion.

We should each tailor our allocation percentages according to our own circumstances. And we should adjust it over time as the macroeconomic conditions change.

Personally, I have a running spreadsheet I use to keep track of my own asset allocation model. It’s similar to a personal financial statement, but it compares my actual allocation in each asset class to my target allocation at all times.

Portfolio Construction

Portfolio construction refers to how we build our stock portfolio.

This is something we didn’t have to worry much about during The Age of Paper Wealth. We could just buy some growth stocks and let the market take them higher for years.

Today it’s a whole different game.

We need a bulletproof portfolio – one that can weather “higher for longer” interest rates and the coming recession. To get that, we need to focus on four specific buckets. They are:

World-Class InsuranceEnergy StocksGold EquitiesTop-Tier Consumer GoodsWe dedicated an entire email series to each of these, so I’ll just hit the highlights here.

World-Class Insurance refers to the world’s best property and casualty insurers. These companies sell policies that enterprises and consumers need to have—it’s not a choice.

Then the insurance companies invest the premiums they receive before they have to pay any claims. That’s where the magic happens.

This creates another revenue stream. And because these companies invest primarily in bonds and mortgages, their investment returns will grow significantly now that interest rates have risen.

For energy stocks – we should focus on both the oil & gas sector as well as uranium for nuclear power.

As we’ve discussed, solar and wind simply aren’t going to power our grid… because the power they produce isn’t constant – it’s intermittent. Yet we’ve poured trillions of dollars into companies working on solar and wind power.

That’s created a dynamic where we will see energy shortages… which will drive the price of oil, natural gas, and uranium higher. Let’s get ahead of it.

I also expect we’ll see the price of gold rise in the years to come.

We’re in a world where national governments are drenched in debt, alliances are shifting, trust is fading, and wars have broken out in eastern Europe and the Levant.

That’s a world in which gold should trade at a premium. The right gold stocks will add some pop to an otherwise conservative portfolio.

That leaves us with top-tier consumer goods companies.

These are well-managed companies who sell products that the American consumer will buy regardless of what happens with the economy.

Dollar General, Domino’s, Hershey, and Home Depot come to mind. They can serve as inflation hedges for us if we buy these stocks when they’re trading at attractive valuations.

That said, I don’t mean to suggest that we should only own stocks in these four buckets. But these four areas are likely to outperform the market over the next few years.

Cash Flow

Having multiple income streams will be even more important in the new climate we find ourselves in. As they say in real estate – cash flow is king.

And it just so happens that investment real estate is a great way to build cash flow.

Of course, real estate represented an amazing opportunity when we could lock in 30-year mortgages at 3.5%. But there are still markets today where investment properties will throw off 10-16% a year cash-on-cash returns – even with mortgage rates in the 7% range. Those opportunities are mostly in boring markets where home prices tend to be stable over time.

What I love about real estate is that there’s no guessing what our return on investment (ROI) will be.

That’s because the ROI for any property depends upon its monthly rent, purchase price, insurance costs, property taxes, management fees, and HOA dues (if any). We know each of these numbers up front.

So when we run the numbers and find that a property wouldn’t produce adequate cash flow for us, we don’t buy it. Simple.

And if we focus exclusively on cash flow like this, it doesn’t matter much whether real estate goes up or down in value. That’s key.

We’ll get our capital appreciation with stocks, Bitcoin, and our early stage investments. Let real estate be our tool to generate extra monthly income.

With that approach, investing in real estate becomes straightforward.

And just to quantify this, if we focus on rental properties that produce $500 a month in cash flow, we only need ten properties to create $5,000 a month in extra income.

That’s within the realm of possibility for anyone who has built a little retirement nest egg over their working years.

Alternative Investments

Alternative investments exist outside of our asset allocation model, but may prove immensely valuable in the years to come.

Of course, any kind of collection could fall into this category. Numismatic coins… classic cars… baseball cards… stamps – I know people who are fanatics about these things.

But I’m not. So to me, alternative investments are largely about home resiliency.

Home resiliency refers to the ability to be self-sufficient for at least six months within our home. That means we have all the food, water, and provisions we need to get by and maybe even live comfortably—even if we can’t leave our house or receive any deliveries.

It used to be that you were looked at as a crazy doomsday prepper if you talked about this concept. But then COVID-19 happened and we got lockdowns, travel restrictions, and all kinds of supply chain disruptions. Suddenly home resiliency seemed like a wise strategy.

When you’re just getting started, building six months of resiliency seems like a daunting task. But it’s not hard to achieve. And it doesn’t cost that much.

Home resiliency consists of four parts—food, water, energy, and provisions.

Let’s start with food…

The easiest way to build a food reserve is to buy pre-packaged food with a long shelf life. There are numerous companies out there that offer suitable products.

Mountain House, Wise Company, Augason Farms, Legacy Food Storage, My Patriot Supply, Thrive Life, and ReadWise each offer various food storage packages.

Keep in mind this is food specifically designed to have a long shelf life. It may not taste the best, and it may not be the most nutritious, but it’ll get us by in a pinch.

In addition, I like to keep some extra canned goods, rice, and peanut butter in the pantry as well. Just in case. We also keep our meat freezer stocked at all times.

Next up is water.

Water’s a bit more difficult to store because you don’t want it sitting in direct light for too long. Plus it takes up a fair amount of space. But I’ve got a pretty good solution here.

Water.com offers monthly and bi-weekly water delivery services. We can set up a subscription to receive five-gallon jugs of water from that site. Then a service representative will come out to our house every two weeks to bring us new jugs.

I started by buying 15 five-gallon jugs of water. Typically we go through three jugs every two weeks. Then when the service rep comes out, he simply replaces our empty jugs. Or he leaves us extra jugs if we ask him to.

As such, we have anywhere from 55 to 75 gallons of water on hand at all times. We just drink it as we go and replenish our stash every two weeks. Then we supplement that with bottled water.

The key here is to store the water out of direct sunlight and to be diligent with a rotation system, to ensure that your water never stagnates.

The next thing we need to think about is energy. We need something that provides heat and enables us to cook in case the power’s out during an emergency.

The easiest thing here is to buy a propane grill or two. I have a large one and one of the small portable grills. And I keep a few extra propane tanks on hand at all times. Easy and simple.

The other thing I highly recommend are solar-compatible batteries. We keep a few of these around the house, fully charged at all times.

These are batteries that can be charged by plugging them into the wall or hooking them into the solar panel they come with. The Jackery brand is probably the most popular of these products. The batteries are equipped with power outlets that work the same as our wall outlets. Thus, we can plug anything into them to get power.

They would be good for powering any electronic device for a limited period of time in a power outage. And if we drain the battery, we can always recharge it with the solar panel. See – solar’s good for something.

The larger expense to consider is a whole-home generator. I consider this a must if you want to keep a meat freezer stocked up. Just call Home Depot or Lowe’s and they’ll give you a quote.

And that brings us to provisions.

The big thing here is just to keep an extra supply of all of the items we use regularly: contacts, saline, paper towels, toilet paper, soap, toothpaste, flashlights, batteries, first-aid kits… whatever else.

We can buy these things in bulk and replace them as we go. That way we always have plenty of everything on hand.

So those are the four pillars: asset allocation, portfolio construction, cash flow, and alternative investments.

Put it all together and suddenly your money is bulletproof and your home is your castle. That’s a comforting feeling during uncertain times – come what may.

-Joe Withrow

P.S. For a deeper dive on each of these issues, please see my book Beyond the Nest Egg. You can find it on Amazon right here:Beyond the Nest Egg – How to Be Financially Independent Outside of a Broken System

The post What to do about uncertain times… first appeared on Zenconomics.

The post What to do about uncertain times… appeared first on Zenconomics.

November 15, 2023

The Fed, the Treasury, and the future

We’ve been talking all week about how the Federal Reserve (the Fed) and the New York banks have broken ranks from the globalist power structure.

The two factions now appear to be in direct conflict with one another. They are fighting a secret financial war for the future of our economic system.

This is something that’s hard for those of us schooled in Austrian economics to accept. We tend to lump all these people into the same Deep State category. But the signs of the current power struggle are everywhere…

When the Fed switched the US interest rate benchmark from the London Interbank Offered Rate (LIBOR) to the Secured Overnight Financing Rate (SOFR) last year—that was directly against the globalists’ interests.

Then when the Fed proceeded to raise rates farther and faster than ever before in history – exceeding even the pace of Fed Chair Paul Volker from 1979 to 1981, and even as the United Nations (UN) screamed at them to stop from across the pond—that was a shot across the bow. The war was on.

And Powell made it clear that he wasn’t going to back down. He even told the media over the summer that his Fed would not finance out-of-control government spending. Here’s that dialogue:

EDWARD LAWRENCE, FOX BUSINESS: So I want to go back to comments you made about, in the past, about unsustainable fiscal path. The Congressional Budget Office (CBO) projects the federal deficit to be $2.8 trillion in 10 years. The CBO also says that federal debt will be $52 trillion by 2033.

At what point do you talk more firmly with lawmakers about fiscal responsibility? Because—assuming monetary policy cannot handle alone the inflation or keep that inflation in check with the higher-level spending.

JEROME POWELL: I don’t do that. That’s really not my job… I will say, and many of my predecessors have said that we’re on an unsustainable fiscal path, and that needs to be addressed over time.

EDWARD LAWRENCE: Is there any conversation then about the Federal Reserve financing some of that debt that we’re seeing coming down the pike?

JEROME POWELL: No. Under no circumstances.

That was another line in the sand. Powell said he wasn’t going to finance government spending anymore.

This puts the US Treasury in a bind. And Treasury Secretary Janet Yellen knows it.

The Treasury Picks a Side

The US Treasury is tasked with managing the federal government’s finances. This includes collecting taxes, paying the government’s bills, and managing the national debt.

As I write, the Treasury presides over $33 trillion in debt… and the CBO expects the government to run deficits great than $1 trillion each year going out to 2030.

Whenever there’s a deficit, the Treasury must issue more debt to pay for it. It does this by selling Treasury bonds at auction. To understand why Powell’s comments above are so important, we have to understand the nuances within this process.

The largest competitive participants in Treasury auctions are institutional investors and primary dealers.

Institutional investors consist of insurance companies, pension funds, and mutual funds. And the primary dealers are large financial institutions who have approval to sell Treasury bonds directly to the Federal Reserve.

These participants bid for Treasuries at auction, and those bids determine the interest rate for the bonds.

Now, the Fed was actively buying Treasury bonds up until June of this year. But the Fed doesn’t participate in Treasury auctions. It must buy from the primary dealers who do.

So when the Fed was buying Treasuries, the primary dealers knew they had built-in demand for the bonds they bid on. They could turn around and sell those bonds to the Fed.

Naturally this created additional demand for Treasuries… which helped finance the government’s debt. But that changed in June.

The Fed is no longer buying Treasury bonds. And Powell’s strong words suggest this won’t change. His comments about not financing government deficits means the Fed is not going to start buying Treasury bonds again.

So the US Treasury won’t have the same built-in demand at its auctions going forward. And it’s already happening.

On November 9, the Treasury’s auction for 30-year bonds nearly failed. The big banks had to step up and buy 18% of the entire auction to account for weak demand. Typically the banks don’t account for any more than 11% of a Treasury auction.

The message is clear. If the Fed isn’t going to buy bonds going forward, one of two things must happen.

Either the US government must cut back on its spending dramatically… or the Treasury must figure out how to manage the ballooning debt without its buyer of last resort.

Well, Yellen made her choice. Financial news titan Bloomberg broke the story.

Per this announcement, the Treasury plans to start “regularly purchasing” U.S. Treasuries next year. They claim this will add liquidity and make the Treasury bond market more “resilient”.

Make no mistake about it, this is about what’s called yield curve control (YCC). It’s a tool to account for dwindling demand for Treasury bonds.

YCC is where an entity – typically a central bank – aggressively buys as many sovereign bonds as it needs in order to keep interest rates from rising above a certain level.

What we’re talking about here is akin to Operation Twist all over again.

Operation Twist was what the Fed called its yield curve control program back in 2011. Ben Bernanke chaired the Fed at the time.

Per the program, Bernanke bought long-term Treasury bonds while simultaneously selling short-term Treasuries in great quantities. This served to push long-term interest rates lower than they otherwise would be.

So here we have Yellen prepared to embark upon a similar program – just with a different name. But there’s a problem…

The US Treasury cannot create money from thin air like the Fed can. The only thing it can do is issue new bonds to finance its spending… but it needs willing parties to step up and buy those bonds.

This is why it’s the central bank that typically engages in yield curve control. The central bank doesn’t need to worry about selling bonds to investors because it can simply ‘print’ the money it needs.

This raises the question – why is it Janet Yellen and the US Treasury that’s engaging in this program rather than the Fed?

To me the answer is obvious. The Fed and the Treasury are now on different teams.

The Fed is in league with the New York banking interests. They are normalizing interest rates and forcing some degree of fiscal responsibility upon the system again. They have to if they want to save the financial system as it currently exists.

Yellen and the Treasury are in league with the globalists. They want to push unlimited government spending to bring about their “Great Reset” initiative. We talked about that yesterday.

Obviously these are two very different agendas. And only one of them can come to fruition.

Which one that is will have a dramatic impact on everything going forward.

-Joe Withrow

P.S. Tomorrow we’ll talk about what it all means for money, markets, and investing in the years ahead.

The post The Fed, the Treasury, and the future first appeared on Zenconomics.

The post The Fed, the Treasury, and the future appeared first on Zenconomics.