Joe Withrow's Blog, page 5

February 19, 2024

The End of ESG

Energy is the master economic resource.

We take it for granted… but nothing happens without energy. Everything we see in our modern world today – and everything we use on a daily basis – is only possible because of energy.

It’s a simple thing. But if we truly ponder this, it changes our perspective.

Last week we talked about building a robust asset portfolio for financial security. The concept is called asset allocation. The idea is to spread our savings across a range of asset classes in a strategic way.

As we discussed, a tactical stock portfolio is a key piece of the puzzle here. And this is where we can leverage energy as the master economic resource…

My philosophy when it comes to portfolio construction is this: I want a portion of my portfolio to have exposure to energy. And I want to own that energy in the most advantageous way I can. If we start there, all we need to do is figure out what form that energy should take.

The Environmental, Social, and Governance (ESG) movement would have us believe that we should own energy in the form of solar and windmills.

They told us that we’re rapidly moving towards a “carbon-neutral”, “net-zero emission” world. And in that world, we would reduce our dependance on fossil fuels—namely oil, natural gas, and coal.

Countless “clean energy” exchange traded funds (ETFs) popped up in recent years to support this theme. ESG investing became a hot trend. And Larry Fink, CEO of investment management giant BlackRock, paraded around in media appearances proclaiming the gospel of ESG for a few years.

But reality has finally set in.

The world is quickly realizing that it is impossible to run our power grid on renewable energy sources like solar and wind power. And Fink no longer wants to use the term “ESG”. He’s now distancing himself from it.

We’re also waking up to the fact that these forms of energy are not nearly as “clean” as we were told they are. But that’s a topic for another day…

When it comes to energy production, energy density is everything. Energy density simply measures the amount of energy stored in a given fuel source per unit volume or mass.

Uranium (for nuclear power), oil, natural gas, and coal are incredibly dense fuel sources. I listed them in order of most dense to least dense.

When it comes to solar and wind power – we can’t measure their energy density. Because they aren’t fuels. Their power output depends on whether the sun is shining and the wind is blowing.

That means their power production is intermittent. It’s not constant.

As best I can tell, this is a problem that simply cannot be solved when it comes to solar and wind.

No matter how efficient solar panels become – and no matter how much battery technology improves – solar’s power production will always be intermittent. No sun, no power.

The same dynamic holds true for windmills. No matter how much the tech improves – wind power will always be intermittent. No wind, no power. And we just can’t run a modern civilization on intermittent power.

Yet, nearly $2.2 trillion worth of investment dollars have poured into the development of renewable energy since 2016. That’s according to financial media giant Bloomberg.

That’s what we call “malinvestment”.

Sure, renewable energy can be useful on a smaller scale. Especially in rural areas where the power grid infrastructure is limited.

But those use cases do not warrant trillions in investment. So we’re going to see a large portion of annual energy investment flow back into traditional energy sources in the years to come.

Indeed, we’re seeing signs that this is big shift is already underway. And that presents us with some great investment opportunities within our tactical stock portfolio.

More on that tomorrow…

-Joe Withrow

The post The End of ESG appeared first on Zenconomics.

February 15, 2024

Beyond Retirement

Yesterday we examined the three weaknesses in the traditional retirement planning model.

In short, that approach pits us against the tax code… is vulnerable to inflation… and it forces us to choose between having assets or having income.

Today let’s talk about a more comprehensive approach – one that mitigates each of these weaknesses.

My philosophy is simple: Financial security first. Then financial independence.

I define financial security as the ability to weather any sudden change or emergency for an extended period of time in relative comfort.

It’s a simple concept. In mainstream circles, they would say it’s about “having money”.

That way if we were to lose our primary source of income or incur an unexpected large expense – we’re good. We have the resources we need to handle the issue without it disrupting our life.

But here’s the thing – we don’t want to have money. They are printing money by the trillions. It’s guaranteed to lose purchasing power year after year. Instead, we want to have assets.

For true financial security, we need to build a portfolio comprised of several distinct assets. They are: cash (strategically warehoused), gold, Bitcoin, a tactical stock portfolio, and alternative investments (including the items we need for home resiliency).

Each asset class serves a different purpose for us. But collectively they mitigate any risks we may face. And if we are strategic about this, our asset portfolio will grow in value over time – regardless of what happens with the economy, inflation, interest rates, or the stock market.

Here’s how it works…

If we want to attain financial security, we must first assess our personal situation. Are we married? Do we have dependents? Do we own our home or do we rent? What does our cost of living look like relative to our income? How stable is our income? Are there any immediate risks we face that could disrupt our life?

Based on this assessment, we then come up with a number. How much money would we need to have available to us in order to pay our bills, support those who depend on us, and maintain a comfortable lifestyle without worry for an extended period of time?

I would say that’s six months at the bare minimum. But a year or more would be better.

That number will be different for each of us. Whatever it is, we then create an asset allocation model custom-tailored for our own situation. That model tells us exactly how much money we need to put into each asset class.

For example, let’s say our financial security number is $100,000 – just for easy calculations. And let’s say we determine our ideal asset allocation model is the following:

Cash: 30%Gold: 10%Bitcoin: 30%Stocks: 25%Alternative Investments: 5%This tells us that we need to have $30,000 in cash and Bitcoin… $10,000 in gold… $25,000 in stocks… and $5,000 in alternative investments. That’s how we spread out the $100,000 to achieve true financial security.

[Side note: there are much better ways to warehouse cash than simple checking accounts.]

Now the next question is: do we already have $100,000?

If so, it’s just a matter of repositioning it. If not, we need to save as much of our income as possible and use it to gradually build out our model over time.

Simple, right?

So once we have a robust asset portfolio in place equal to our personal financial security number – $100,000 in this example – then what?

Then it’s time to create financial independence.

This is all about building streams of monthly cash flow. That is to say, we need to create passive income for ourselves. The goal is to work up to the point where our passive income exceeds our cost of living.

Believe it or not, there are all kinds of ways to do this. Rental properties… mortgage notes… private lending… royalties… passive businesses – there’s plenty of opportunity out there.

It’s just that these items get very little exposure in mainstream investment circles. They all take a backseat to the stock market… because our financial institutions command gargantuan advertising budgets and get all the media attention.

Inside our investment membership The Phoenician League,we talk at length about creating a cash flow wealth strategy. That strategy lays forth our investment criteria and helps us determine which passive income investments we’re willing to consider.

With our financial security portfolio solidified and our cash flow wealth strategy in place, we’re now free to focus our time and resources on building passive income via our chosen method.

The beauty of this approach is that in order to grow our monthly cash flow, we must go out and acquire high quality assets. That means as our income goes up, so does our asset base. We aren’t forced to choose between the two.

Then, once our passive income comfortably exceeds our expenses – we’re there. We’ve achieved financial independence.

And guess what?

We never have to sell off our assets in order to fund our retirement. Instead, our assets will keep throwing off income for us month after month, year after year.

Then if we do proper estate planning, we can pass our cash flow empire down to the next generation in a responsible, tax-efficient way.

And then maybe – just maybe – humanity can finally get off the hamster wheel.

-Joe Withrow

P.S. For more on this approach to personal finance, please see our urgent financial training for 2024. You can find it right here: https://financeforfreedomcourse.com/training

The post Beyond Retirement appeared first on Zenconomics.

February 14, 2024

The Three Weaknesses in Retirement Planning

The rules of money changed in 2022.

To illustrate this from a different angle, let’s assess how the “traditional” retirement planning model came to be…

Modern retirement planning has its roots in the Employee Retirement Income Security Act (ERISA) of 1974. That legislation created the Individual Retirement Account (IRA). Then supplemental legislation created the 401(k) and the SEP IRA for self-employed individuals in 1978.

ERISA marked a monumental change in the US.

Prior to this legislation, it was common for employers to provide employees with a lifetime pension plan. Companies would invest in this plan on behalf of their employees. Then they would make lifetime payments to each employee after they retired.

As such, the burden of retirement planning fell to corporations.

This gave rise to the “three-legged stool” principle. It said that a sound retirement consisted of three things:

Social Security benefitsCorporate pension paymentsPersonal savingsERISA changed everything. It shifted the responsibility for retirement planning from employers to employees.

This gave companies the green light to phase out their pension plans. It had become clear that lifetime pensions weren’t sustainable anyway.

That eliminated one of those three legs on the retirement planning stool. It also set in motion what was almost certainly an unforeseen chain of events.

Suddenly millions of people became responsible for their own retirement planning. And they were sold on using the 401(k) and the IRA as their primary savings vehicles. This created millions of new customers for Wall Street – almost overnight.

When they realized this, financial institutions created scores of investment funds designed to go into retirement accounts. First it was mutual funds. Then index funds. And then exchange-traded funds (ETFs).

Fast forward to today and there are over 15,000 different investment funds out there for people to choose from. And every single one of these funds comes with its own fee structure. These fees ensure that the fund managers get paid no matter how their investments perform.

Thus, retirement planning became a massive industry… and Retirement Inc. was born.

Then clever marketers crafted slogans like “What’s your retirement number?” and “Stocks only go up over time”.

The industry pushed the idea that we should all plan for retirement the same way – by funneling a small portion of our savings into diversified funds held within qualified retirement accounts.

We do this for 30 or 40 years to work up to as big of a “retirement number” as we can. Then when we retire, we start selling off our funds to create income for ourselves. And we hope that we don’t outlive our money.

Wall Street and guys like Dave Ramsey made an absolute fortune pitching this method of retirement planning. And I suppose it worked okay during the Age of Paper Wealth from 1982 to 2022.

But this approach is riddled with holes. In fact, there are three fundamental weaknesses that Retirement Inc. completely ignores.

For starters, planning for retirement this way pits us against the tax code.

Any withdrawals we make from a 401(k), IRA, or SEP IRA are subjected to ordinary income taxes. That means the “retirement number” we worked up to isn’t our actual number. Because a portion of it will be taxed away from us.

Today, the average income tax bracket for American retirees is 12%. At that tax rate we only receive $88,000 for every $100,000 we withdraw from a qualified retirement plan. The other $12,000 gets taxed away.

And here’s the kicker – tax rates today are lower than they’ve ever been. Yet the national debt is over $34 trillion and Congress is running trillion-dollar deficits each year.

This begs the question – what happens if tax rates go up?

It certainly seems likely that they will at some point. And then retirees will have an even greater portion of their nest egg taxed away from them when they go to access their money.

The second weakness to this approach is that it leaves us vulnerable to inflation.

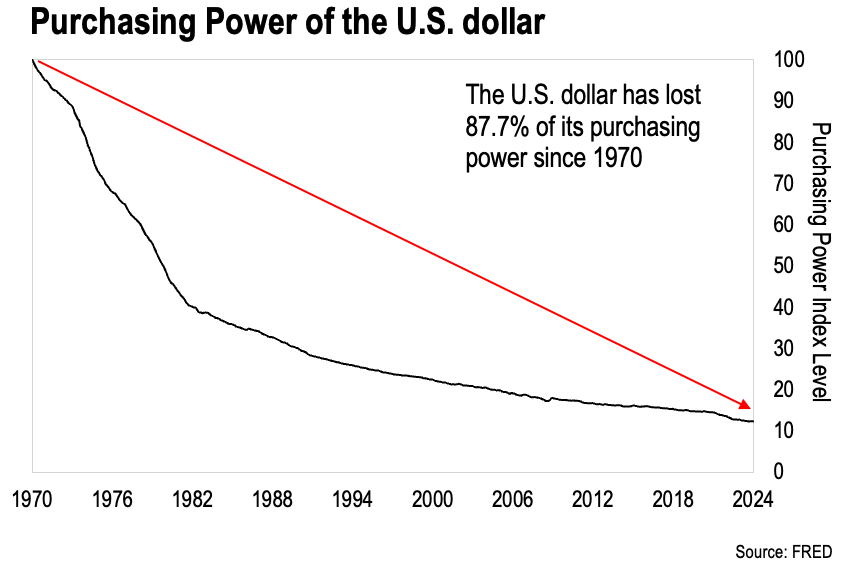

We saw yesterday how the US dollar has lost nearly 88% of its purchasing power since 1970. That means an investment portfolio worth $100,000 in 1970 would need to be worth $833,333 today just to have the same purchasing power.

In other words, inflation is constantly eating away at our investments – so we need to generate a rate of return that outpaces inflation to get ahead. Our nominal rate of return doesn’t tell the full story.

To be fair, a properly constructed equity portfolio does stand a good chance of beating inflation over time. But most of the smorgasbord of funds out there are far too diluted with poor investments. I wouldn’t trust them to beat inflation going forward.

The third major weakness of Retirement Inc’s approach to financial planning is that it puts us on a see-saw.

When we’re working, we use our income to build up financial assets inside of retirement plans. Then when we retire, we sell off those assets we spent our life working for.

So during our working years, our assets are going up… but we’re not getting any income from our investments. Then in retirement we do get some income – but we deplete our asset base in the process.

That’s the see-saw. It’s a constant choice between assets and income.

This strikes me as silly.

Why would we make such a choice? And why would we work so hard for 30 or 40 years only to sell off everything we worked for later in life?

Wouldn’t it be nicer to instead build a legacy that will live on long after we’re gone?

I bet most people agree with this sentiment. It’s just that Retirement Inc. convinced us that their way is the only way… And they control the financial media and massive advertising budgets.

Tomorrow we’ll flip the script and envision a better approach.

-Joe Withrow

P.S. I mentioned that a properly constructed equity portfolio should outpace inflation over time. We demonstrate exactly what that looks like in a special report available on our new author site: https://joewithrow.com/

Just scroll down to the bottom of that page to get the report.

The post The Three Weaknesses in Retirement Planning appeared first on Zenconomics.

February 13, 2024

The state of the American middle class

When we left off yesterday, we were examining the idea that the Age of Paper Wealth had a devastating impact on traditional American society.

As a reminder, the US government cut the dollar’s final link to gold in 1971. This removed all restrictions on creating new dollars at will.

It took most governments about a decade to realize this… but they’ve been printing money in greater and greater quantities since 1982. This drove interest rates down to zero… and it propelled the US stock market to all-time highs.

I call this period from 1982 to 2022 the Age of Paper Wealth. It certainly seemed like a prosperous period in American history – and for some it was. But the combination of artificially low interest rates and printed money financialized the American economy.

That is to say – we emphasized financial markets, financial institutions, and financial activity to the detriment of hands-on knowledge, skilled labor, the middle class, and traditional American values.

Today, very few people seem to know how to do anything with their hands. Myself included. Finance is all I’ve known. But I am making an effort to get better about this.

And look at what’s happened to our dollar…

This data comes directly from the Federal Reserve. Their own data shows that the US dollar has lost nearly 88% of its purchasing power since 1970. This is why nearly everything has increased in price dramatically.

And what’s the result of this?

The once robust American middle class has been hollowed out. Because the purchasing power they work so hard for is constantly stolen from them – but in a subtle way.

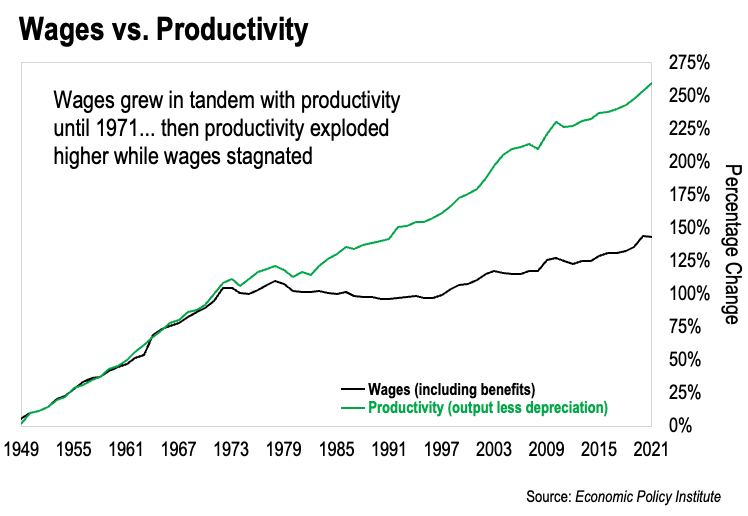

I have one more chart for you today to tell that story. Here it is:

This chart compares the growth in median US wages, adjusted for inflation, against total American productivity. The data spans from the late 1940s to the present day.

It’s clear that wages and productivity were in sync until 1971. The average person’s salary increased proportionally with America’s output of goods and services. Just as it should.

But look at what’s happened since. Our productivity powered forward… but our inflation-adjusted wages went stagnant.

Why?

Those trillions of dollars created from nothing siphoned purchasing power from everyone in the economy.

Remember, this data is measuring the real purchasing power of wages adjusted for inflation. If we look at nominal wages – they have gone up. In dollar terms, the median salary is higher than it’s ever been.

The problem is, those dollars buy just a fraction of what they once did. Because their purchasing power was stolen. That’s why we have to adjust for inflation.

And where does this stolen purchasing power end up?

In the hands of those who get to use the newly created money first.

Creating new dollars out of thin air effectively funnels most of America’s productivity gains to Washington, DC and Wall Street. That’s been happening for decades now.

This dynamic is why it has become so difficult to get ahead.

If we look at the data, the median price of a new car today is over $48,000. That’s what the median home cost back in 1980.

Think about that… today a regular new car costs just as much as what a nice single family home cost just forty years ago.

Then if we look at the median home price today – it’s over $430,000. Just for a nice single family home.

Of course, that number is skewed by real estate prices in the large cities. But at the same time, most young people live in the cities.

This begs the question – how can they afford a middle class lifestyle? And what does that say about the American dream today?

Then if we look at those approaching retirement – how do they grapple with the fact that our cost of living is streaking higher?

To me, it’s clear that the rules of money have changed. When it comes to personal finance, what worked so well in the past is not going to work terribly well going forward.

We need a new vision and a new approach to navigate the choppy waters we find ourselves in. And that will be our topic for tomorrow…

Stay tuned.

-Joe Withrow

P.S. Don’t forget we’re currently offering two in-depth special reports on money and investing. You can get more details at the bottom of our brand-new author page right here: https://joewithrow.com/

The post The state of the American middle class appeared first on Zenconomics.

February 12, 2024

What happened to our money?

Last week we looked at the strange de-banking trend and the history of our money.

In our brief history lesson, we noted how the dollar was not only backed by precious metals for most of its history – it was in fact defined as a specific amount of silver and later gold.

But everything changed in 1971. That’s when President Nixon cut the dollar’s last link to gold.

This thrust the world on a purely fiat monetary system controlled entirely by governments and central banks. Fiat is the Latin word for “let it be done”.

This is what gave rise to the Age of Paper Wealth I highlighted in my book Beyond the Nest Egg. Because the fiat system removed all restrictions on printing money.

It took most governments about a decade to realize this. But once they did, they didn’t look back.

From 1982 to 2022, most nations printed their currency excessively to finance all kinds of government programs. As part of this, central banks used newly created money to buy sovereign (government) bonds… which dropped interest rates to zero around the world.

This fueled a massive stock market boom that lasted for four decades. That’s what gave rise to the idea that stocks only go up over time. Much of our mainstream personal finance advice is based on this premise.

The reality is, what happened from 1982 to 2022 was not normal. Instead, it destroyed our monetary system and the value of our dollar.

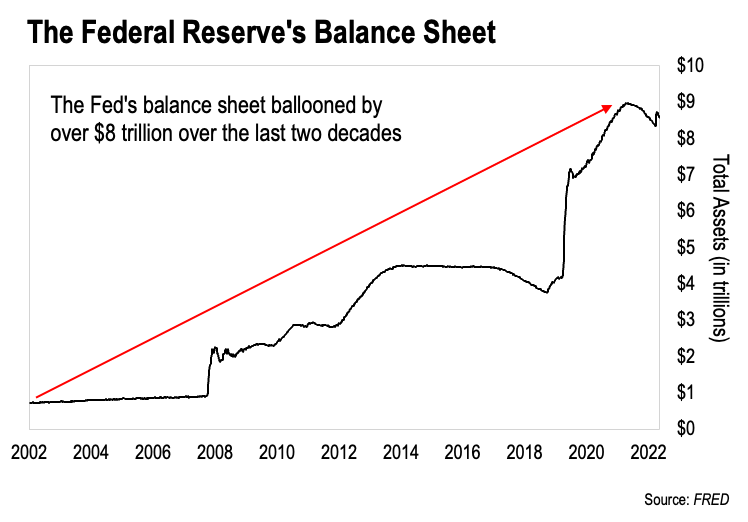

The Fed and the US Treasury worked hand-in-hand to create over $8 trillion dollars from thin air over this time period. We can verify that $8 trillion because it hit their balance sheet.

Here’s the chart:

This is a chart of the assets held on the Federal Reserve’s balance sheet going back to 2002. When we see that black line going up, that’s the Fed buying assets. These are mostly US Treasury bonds and to a lesser extent mortgage-backed securities.

As we can see, the Fed owned less than $1 trillion worth of assets in 2002. But over the next 20 years it bought over $8 trillion worth of bonds.

And where did the Fed get the money it needed to buy these assets?

As we noted, it created those dollars from nothing. Then that liquidity worked its way into the financial system, driving the US stock market higher and higher.

This enriched two sets of people – those in Washington, DC who got to use the newly created money first for all manner of government programs. And those on Wall Street who benefitted the most from the massive bull market in US equities.

But this also had a subtle, devastating impact on American society. We’ll examine that tomorrow.

-Joe Withrow

P.S. In other news, we just launched our official author page to keep you updated on all our latest projects and insights. And to celebrate, we’re offering exclusive access to two in-depth special reports on money and investing for those interested.

You can claim your reports at https://joewithrow.com/. Just scroll down to the bottom of the page for more details.

The post What happened to our money? appeared first on Zenconomics.

February 7, 2024

The History of Our Money

Yesterday we talked about the nature of money… and we noted that we haven’t had sound money for quite some time now.

So today let’s look at a brief monetary history to see how that came to be. This is something that nearly every University in the western world has either ignored or swept under the rug to keep us ignorant – so let’s take a minute to briefly pull the curtain back today.

We’ll look at the history of money from an American perspective. But only because the dollar has served as the world’s reserve currency since 1944.

And we have to start with this – what is a “dollar”?

In 1792 the United States Coinage Act defined the US dollar as 371.25 grains of pure silver. If this seems strangely specific, there’s a reason why.

The primary currency used at the time was the Spanish silver dollar. It was a coin that contained exactly 371.25 grains of silver.

The Coinage Act based the US dollar on the Spanish dollar since it already circulated widely in America. It also pegged the ratio of silver to gold at 15:1.

From there, the same Act created the US Mint. It’s job was to make gold and silver coins based on this precise measurement.

The US also experimented with a central bank and a national banking system in the century following the US Coinage Act. There were plenty of nuances and tons of intrigue involved here… but we’ll keep it simple today.

During this period US banks would issue paper notes (private currency) backed by the common coins in circulation. Their promise was that if somebody came into the bank with one of their notes, that person could redeem the paper for gold and silver.

But some of these banks created more paper than they had gold and silver backing for. Given the competitive nature of the system, those banks would inevitably go under for inflating their paper currency after everybody found out about it.

Whenever a bank went bust like this, it wiped out innocent people holding that bank’s notes. The propagandists emphasized this when they later set out to establish the Federal Reserve Cartel. We’ll talk about that in just a minute. But the key here is that all bank notes were once backed by gold and silver.

Fast forward to 1900 and the US officially went on the classical gold standard. The Gold Standard Act defined the US dollar as 25.8 grains of gold nine/tenths fine.

This was a purposeful shift away from silver. Per the classical gold standard, most transactions were settled in gold coins and private bank notes backed by gold.

That is, until the Federal Reserve came to be in 1913.

G. Edward Griffin’s The Creature From Jekyll Island provides fantastic insight into the back-room dealings the brought the Fed into existence. It was very much a sleight-of-hand play. Case in point – it’s not federal and there are no reserves.

We don’t have the space to go into those details today. But I highly recommend that book for anyone interested in this subject.

They key here is that the Federal Reserve Act prohibited private banks from issuing their own bank notes. In their place, the Fed began issuing “Federal Reserve Notes”. They were paper currency 100% redeemable in gold… at first.

But twenty years later, in 1933, President Franklin Roosevelt issued an executive order that made private gold ownership illegal. At that point Federal Reserve Notes were no longer redeemable in gold.

And per FDR’s order, all Americans were required by law to deliver all their gold coins, gold bullion, and gold certificates to the Fed or a member bank. The exchange rate was $20.67 paper dollars per ounce of gold.

And the executive order had teeth. The penalty for failing to turn in gold would result in fines and imprisonment.

This effectively removed gold from the domestic economy. But foreign central banks could still redeem their Federal Reserve Notes for gold bullion through what was called the gold window.

Meanwhile, the world wars forced nations to abandon the classical gold standard around the world. That’s because the combatant nations printed money to pay for the wars. As a result, each nation’s currency fell dramatically in relation to gold.

This left a major vacuum. Absent the gold standard, what would the international financial order look like?

In 1944, representatives from 44 nations of the world met in Bretton Woods, New Hampshire to discuss just that subject. They agreed to what was called “The Bretton Woods System”. It established the US dollar as the international reserve currency.

Per this agreement, the US dollar replaced gold as the medium for international trade settlement. That meant all international goods would be bought and sold in US dollars no matter which nations were doing the buying and selling.

The new system pegged the dollar to gold at $35 per ounce. Then foreign entities could redeem their dollars for gold through the ‘gold window’ at that rate.

Bretton Woods bestowed an enormous privilege upon the United States as it created a global demand for dollars. Suddenly all nations needed to hold dollars to purchase foreign goods.

This created a situation where the US government could borrow money very cheaply to increase its spending. That’s because there was now a massive global market for U.S. Treasury bonds – which are nothing more than a loan to the US government.

The US used this dynamic to finance President Lyndon Johnson’s “Great Society” programs. That was the beginning of the Welfare State in America.

The US also ramped up military spending to finance the wars in Korea and Vietnam. That gave rise to what President Eisenhower called the “military-industrial complex”.

To finance this increased spending, the US government issued debt and ran trade deficits. Under the classical gold standard, this would have required the US Treasury to pay its creditors in gold. But under Bretton Woods, the US government could simply print new dollars and ship them overseas to make its payments.

That worked for a little while. But eventually other nations began to fear that the US government’s excessive spending would lead to a revaluation of the dollar to gold.

Think about it this way…

They pegged the dollar to gold at $35 per ounce, but the US government kept creating more and more new dollars from nothing. This prompted foreign nations to increasingly exchange their dollars for gold through the gold window.

As a result, gold began to flow out of the US Treasury. And this led President Johnson to sign the Gold Reserve Requirements Elimination Act in 1968. This legislation eliminated the requirement that 25% of all Federal Reserve Notes be backed by gold in reserves.

That was a precursor to what happened in 1971.

On August 15, 1971, President Richard Nixon closed the international gold window. Nixon assured the world that this was just a temporary measure. And he took to the television in an attempt to maintain confidence in the US dollar.

“Your dollar will be worth just as much tomorrow as it is today.” Nixon proclaimed on television with a straight face. “The effect of this action, in other words, will be to stabilize the dollar.”

Of course, nothing Nixon said was true. The gold window never reopened – and that thrust the world onto a 100% fiat monetary system. The word fiat is Latin for “let it be done”.

In other words, our dollar became something that was only money because the government said it should be.

Tomorrow we’ll look at the consequences of this…

-Joe Withrow

P.S. My book Beyond the Nest Egg takes a deep dive into how the perversion of our money impacts our approach to financial planning. If you’re interested, you can find it on Amazon right here: https://www.amazon.com/Beyond-Nest-Egg-Financially-Independent-ebook/dp/B0CG7VYRV7/

The post The History of Our Money appeared first on Zenconomics.

February 6, 2024

The Nature of Money

Yesterday we talked about a strange case of someone getting de-banked… and I asked the question – what’s going on here? Is this a trend?

I suppose time will tell. But I can’t help but think that this is a signal we need to be paying attention to. And it’s a good opportunity to tune in to what’s happening in the world of money and finance.

So today, let’s talk about the nature of money.

Now, I know that may sound a little strange. We all use money every day. We’re familiar with it. But have we really thought about it?

Where does money come from? Why is it valuable?

The short answer is that money is a unit of account that serves as a medium of exchange. But this is an incomplete view.

In order to be viable over long periods of time, money must contain several definitive characteristics. Money must be:

PortableDivisibleFungibleDurableLet’s examine each of these characteristics in more detail.

Money must be divisible. This one’s easy – we need to be able to make change out of our money. It should break down into consistent smaller units that add back up to consistent larger units.

Next, money must be fungible. This is a fancy way of saying that money should be interchangeable. That is to say, it should be uniform.

A dollar in my pocket should be the same as a dollar in your pocket. A Euro in my bank account should be the same as a Euro in your bank account. A one ounce gold coin in my safe should be the same as a one ounce gold coin in your safe. A bitcoin in my wallet should be the same as a bitcoin in your wallet. You get the point…

And last, money must be durable.

To be viable over long periods of time, money needs to serve as a store of value for us. We should be able to save our money and come back to it in a year… in 10 years… in 50 years and still be able to buy things with it.

In other words, good money should maintain its purchasing power over long periods of time.

This one’s a little tricky to analyze because value is subjective. Humans assign value to everything – something’s only worth what someone else is willing to pay for it. There’s really no such thing as intrinsic value.

So a big piece of the durability puzzle is that money must be relatively scarce. Otherwise people would not want to trade goods and services for it. This is why rocks and sea shells don’t work as money. It’s just basic supply and demand economics.

So these are the characteristics inherent in sound money. Sound money is money that will last for long periods of time.

Of course, we don’t have sound money today. The powers that be gradually eliminated sound money in America and thus the world.

To understand this, we have to understand our own monetary history. And that will be our topic for tomorrow…

-Joe Withrow

P.S. The rules of money changed in 2022. That’s both good news and bad news.

The bad news is that under the new rules now in place, traditional retirement planning just isn’t going to work very well. The good news is that we can leverage these rules into a far more robust financial strategy.

For all the details, see my book Beyond the Nest Egg. You can find it on Amazon at: https://www.amazon.com/Beyond-Nest-Egg-Financially-Independent-ebook/dp/B0CG7VYRV7/

The post The Nature of Money appeared first on Zenconomics.

February 5, 2024

How to get de-banked

“Well, I just got de-banked.”

I received a call from a gentleman I’ve known a long time over the weekend. He was chuckling as he shared with me his dealings with Wells Fargo last week. He maintained one of his business checking accounts at the bank.

Wells Fargo had sent him a letter back in January. The letter advised him that the bank didn’t believe his mailing address to be legitimate. Then it demanded that he update his mailing address… or else the bank would close his account.

The thing is – the mailing address is legitimate. So he read the letter. Then he updated his address.

But since it happened to be the right address, he simply moved the mailbox number from line two to line one. He figured this would signal to them that they did indeed have the correct address for him – and he thought nothing more of it.

Until last week, that is. He received an email from Wells Fargo alerting him to the fact that they closed his business checking account. Naturally he called the bank’s customer service right away…

The customer service representative advised him of what had happened – he failed to update his address per the bank’s demand in January, so they closed his account. He interjected…

Gentleman: “Hold on – I did in fact update my address after I read that letter.”

Customer Service: “But you just input the same address. You didn’t change it…”

Gentleman: “Doesn’t that indicate to you that it’s the right address? I mean, you sent the letter to that address… I received it… then I acted upon it.”

Customer Service: “I’m sorry, but I don’t have any additional insight. I’m just telling you what it says in the system here.”

Gentleman: “Okay, but what about my money? What is Wells Fargo doing with the funds that were in that account?”

Customer Service: “Oh, don’t worry! We are mailing those funds to you via a certified check.”

Gentleman: “Mailing me… to what address?”

Customer Service: “The address you have on file.”

Gentleman: “Umm, the one you closed my account over because you don’t think it’s real? Doesn’t this seem a little off to you…?”

Customer Service: “Um… well… I’m sorry, sir, I’m just telling you what’s in the system here.”

I couldn’t help but laugh as he was telling me this story. I mean, Wells Fargo’s stated reasoning is completely illogical… and that’s immediately obvious.

But this does raise a serious question – what’s really going on here?

I mean, we’ve seen some recognizable figures get de-banked in recent years over what the mainstream narrative considered to be controversial statements. But that’s not what’s happening here. This gentleman isn’t in the public sphere.

So what’s going on here? And is this the start of a larger trend?

I don’t know. But I think it’s a good time to make sure we’re up to speed on what’s happening in the world of money and finance…

More to come tomorrow.

-Joe Withrow

P.S. Several prominent macroeconomic trends are colliding as we speak. I’m not sure where this de-banking instance fits in – or if it does. But we take a dive down the rabbit hole of what’s happening on the global stage in my book Beyond the Nest Egg. You can find it on Amazon right here.

The post How to get de-banked appeared first on Zenconomics.

February 1, 2024

The Bitcoin Vision

Yesterday I suggested that we should avoid the new Bitcoin ETFs… because they are antithetical to the big picture underlying Bitcoin.

That big picture is harder to describe. It took me a full year of reading and thinking about Bitcoin before I could see it.

Today I’ll do my best to share it with you. And it starts with this…

We all use space-age technology every single day and think nothing of it.

Text messages fly across the country. We send 2.4 billion emails every single second. Satellites bounce data all across the globe.

Now we can do video chats with each other – just like the old Jetsons cartoon envisioned. We all walk around with a device in our pockets that can access the entire store of accumulated human knowledge instantly, from pretty much anywhere.

And this device can do almost anything we ask it to. It can give us navigational directions. It can send money to a friend. It can play music and movies. There’s an app for almost everything.

If that weren’t enough, we can now buy virtually any item made anywhere in the world online, including food, and it will show up in a box at our door step in short order.

All of this would look like magic to my grandfather who died in 1994.

Yet our core civic institutions are stuck in the Bronze Age. Governments… banks… all of them. They are dinosaurs.

And all of these institutions have developed massive bureaucracies of middlemen. Their primary job is to collect as much data on everybody and then funnel as much money as possible to the institution.

They aren’t there to serve you. They don’t give a rip about what’s good for you. They only care about power, control, data surveillance, and monetization.

It’s the “skim” economy.

We now have entire agencies and industries set-up specifically to spy on us and skim money from our transactions, our investments, and our business endeavors.

Then if we factor in taxes at all levels (federal, state, local, sales tax, etc.), governments confiscate at least 50% of many people’s income year after year.

And what do we get for it?

A bunch of wars and a bunch of entitlements that make people dependent. And now we even see them pushing programs that undermine our culture and indeed civilized society itself.

Think about this – less than 5% of total government spending in the U.S. goes to useful civil service functions. By that I mean the things most people consider necessary. Courts… police… schools… roads… trash collection – those types of things.

Less than 5%. And they aren’t even good at most of these items…

Here’s what I want you to understand – the skim economy we have today creates artificial scarcity.

As a civilization, at least half of our productivity is wasted. The skim economy takes half of our income from us and blows it. Every year. And as part of this it redirects labor and precious resources towards uneconomical programs and projects.

Imagine what your life would look like if your income doubled over night. Imagine how much easier everything would be.

And imagine what our communities would look like if everybody’s income doubled as well. We’re talking about a new renaissance here.

Well guess what… we don’t need our income to double. We just need to get the government and the parasitic institutions out of our pockets.

Right now we all have to squeeze every single dollar we earn because so much is taken from us. And that’s true of small businesses too.

Unproductive middlemen are currently sucking trillions of dollars out of the economy every single year. Trillions.

That money could be used to start or expand businesses and improve infrastructure. It could finance research and development. And it could be directed towards mutual aid and constructive charitable work.

But right now it is being wasted on uneconomical and destructive programs. Our civilization is much poorer because of this… and so many people are struggling to pay the bills each month.

That’s where Bitcoin comes in.

Bitcoin gives us the ability to disintermediate the middlemen and transact with one another directly. It also allows us to store the fruits of our labor in an asset that cannot be inflated, manipulated, or controlled by any third party.

Thus, Bitcoin gives us the ability to create robust, circular economies at the local level.

That is to say, we can create ecosystems where people can pay for desired goods and services using Bitcoin. Then those ecosystems can sync up to form even larger networks.

The larger these networks get, the more practical it becomes for enterprising individuals to create alternatives to the core civil services provided inefficiently by the skim economy.

Then we can begin to disintermediate those institutions that create artificial scarcity… and that’s when we can build a civilization truly fit for humanity.

That’s the big picture.

Jesus of Nazareth was fond of saying: Behold – the Kingdom of Heaven is at hand.

And he would talk at length about the need for people to adopt a new morality and a new lifestyle – based on the Golden Rule.

Well, Bitcoin empowers us to move in that direction. Because it gives us the ability to create ecosystems based on voluntary transactions – transactions based on mutual benefit to all parties. Force and coercion have no place within the Bitcoin network.

And please note that all we’re talking about here is what America was supposed to be – and perhaps was for a little while. A land of free people conducting their lives and running their communities as they saw fit. This is the modern version of Thomas Jefferson’s vision.

Of course, those institutions who thrive on force and coercion aren’t just going to go away. And we can’t escape them entirely in the current climate. All we can do is mitigate their impact on our lives.

Bitcoin gives us a path forward to this end.

It is a tool with which we can build a world of abundance and respect for human ingenuity. But we are the ones who must do the building…

That’s the big picture of Bitcoin. I hope that I did it justice.

And with that, I’ll leave you with a quote from the late architect, inventor, and systems theorist Buckminster Fuller. Here’s Bucky:

“You never change things by fighting the existing reality. To change something, build a new model that makes the existing model obsolete.”

That’s the Bitcoin vision.

-Joe Withrow

P.S. One way to mitigate the impact that those institutions who thrive on data surveillance have over us is to up our game when it comes to privacy and cybersecurity technology. There are quite a few simple changes we can implement to shield our sensitive data and prevent them from building robust data profiles on us.

For this, there’s no better resource than Privacy Action Plan. The program is jam-packed with actionable suggestions that you can implement easily – no technology background necessary. I went through the program recently and learned all kinds of stuff I didn’t even know that I should know.

If you’re interested, you can learn more right here: Privacy Action Plan

The post The Bitcoin Vision appeared first on Zenconomics.

January 31, 2024

Why we should avoid the Bitcoin ETFs…

We’ve been talking this week about why the new Bitcoin ETFs are a misdirection play.

The Securities and Exchange Commission (SEC) approved them with two ulterior motives in place:

Funnel people into the ETFs so that they don’t buy and self-custody any bitcoins themselves.Gain more influence over the dollar price of Bitcoin.Sure, the ETFs will give investors upside exposure to Bitcoin.

If Bitcoin increases in value relative to dollars over time – which I’m quite sure it will – those who own a Bitcoin ETF will make money in dollar terms. They will find themselves with more dollars than they had before.

But the ETFs convey no ownership in the underlying asset – Bitcoin. They are nothing more than a paper claim to Bitcoin’s value priced in dollars.

Now let’s think about this for a minute…

As we discussed yesterday, I see Bitcoin as both a reserve asset and as sound money. It holds enormous utility.

Bitcoin is both a payment network and a currency wrapped into one. That makes it unique. To my knowledge there has never in history been a payment network that also supplied its own independent currency.

Instead – outside of in-person cash transactions – we’ve always relied on intermediaries to facilitate monetary transactions for us.

Whether its banks, credit card companies, or financial technology (fintech) companies like PayPal and Stripe – we’ve always needed third parties to move money for us. That introduces friction. And it exposes us to several risks.

What if the third-party engages in fraud? What if it gets hacked?

And what if it decides that it doesn’t like us or the entity we’re transacting with… so it chooses to freeze our funds? Sadly, that kind of thing has been happening quite a bit in recent years.

Bitcoin eliminates those risks. Because as long as we hold our bitcoins in self-custody, we can always send any amount of value to anyone else at any time and for any reason over the Bitcoin network.

That’s why Bitcoin’s true value is in the independent network.

And as a reminder, nobody owns or controls the Bitcoin network. It’s powered by independent mining rigs operating in relative secret all over the world. They run 24 hours a day and 7 days a week. We talked about that on Monday.

So Bitcoin gives us true monetary independence.

If we own bitcoins in self-custody, we’ll always have economic energy available to us within this new system. And that’s exactly what the power structure behind the SEC does not want. Liberty and independence are dirty words to these people.

This is why we should avoid the Bitcoin ETFs.

Let’s not sacrifice our independence for just a paper claim on Bitcoin’s dollar value. Instead, let’s accumulate bitcoins and learn how to use them.

Because it’s the big picture that truly matters… not the size of our brokerage accounts. And that will be our topic for tomorrow.

Stay tuned…

-Joe Withrow

P.S. My friends at Bitcoin Bay are putting the big picture into practice right now. One step at a time.

They are doing this by educating local farmers and small businesses in the Tampa Bay area on Bitcoin – what it is and how to use it. In so doing, they are building a directory of local businesses that accept Bitcoin as payment for goods and services.

Ranchers… berry farmers… contractors… auto mechanics – they even have an accounting firm signed on to the project. This is creating a circular economy where people in Tampa can deal with one another exclusively in Bitcoin – without needing to move back and forth into dollars.

This is a localized solution to all the fiscal irresponsibility and coming turmoil we see in Washington DC. The more self-reliant our local communities are, the less exposed we are to bad economic policy.

If you’re curious, you can see Bitcoin Bay’s business directory right here.

The post Why we should avoid the Bitcoin ETFs… appeared first on Zenconomics.