Joe Withrow's Blog, page 7

January 16, 2024

What’s coming next for the financial system?

The snow continued to fall throughout the night up here in the Virginia highlands. It was a fine, sticky snow that clings to everything, creating a winter wonderland.

Here’s a shot from this morning:

And speaking of frozen…

Between March and May of last year, the United States saw the 2nd and 3rd largest bank failures in its history.

At the time I was in touch with a tech entrepreneur who had recently launched a new company. She had $2 million parked at Silicon Valley Bank (SVB) – one of the banks that collapsed. Those funds were her company’s start-up capital.

The bank’s management told her on a Friday that they would let her know by Monday how much of her money she could withdraw – if any. She was left to spend the weekend wondering if her company was about to be bankrupt.

It turns out that JP Morgan was allowed to buy SVB’s assets for pennies on the dollar, and my tech entrepreneur’s company was saved. But this highlights something critically important in the world of finance… confidence.

The financial news made it sound like SVB magically collapsed without warning. But that’s not the case.

SVB simply got caught with what’s called a duration mismatch in the banking world. The bank had a large portion of its reserves in long-term U.S. Treasury bonds and mortgage-backed securities.

Now, the market value of a bond moves inverse to interest rates. When rates go up, bond values go down.

And that’s what triggered an old-fashioned bank run at SVB. The value of its bond portfolio declined dramatically… which raised questions about its financial health.

What’s interesting though is that SVB planned to hold those bonds to maturity. And when a bond matures, investors get their original investment back. No matter what.

So the fact that SVB’s bond portfolio declined in value shouldn’t have been such a big deal. It was largely just a paper loss.

But SVB’s customers caught wind of the large paper loss and they scrambled to withdraw their money from the bank. That is to say, they lost confidence.

That’s the problem with confidence. It can blow away like leaves in a gale.

And this same dynamic applies to the US dollar as it pertains to the global financial system…

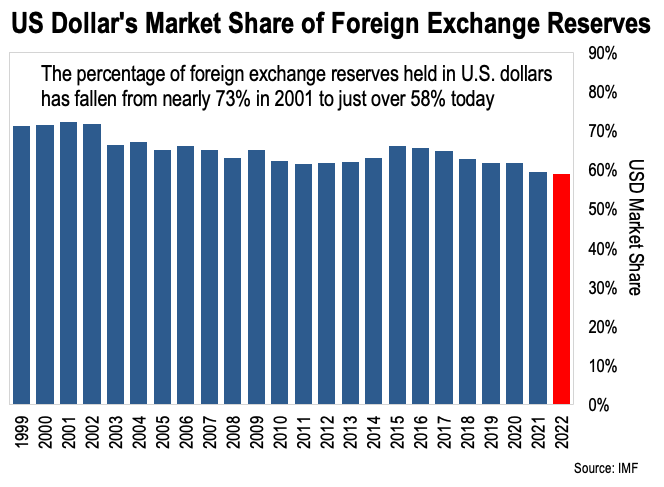

The US dollar has been the world’s reserve currency since 1933. But the BRICS alliance seeks to change that.

BRICS refers to an economic alliance originally forged between Brazil, Russia, India, China, and South Africa. Several other countries have since joined the bloc.

The BRICS countries now represent 42% of the world’s population and 36% of global gross domestic product (GDP).

And this trading bloc is working furiously to build an alternative payment system so they can ditch the US dollar.

Slowly but surely, the dollar is losing market share.

This shows us that global demand for US dollars and dollar-denominated assets has fallen.

You don’t need a degree in international relations… or a deep understanding of geopolitics to know why this is a big threat to asset prices in the US.

As more nations figure out how to avoid it, demand for US dollars will continue to decline. And that means fewer foreign countries and corporations will be investing in US stocks and bonds.

This is the second factor creating what I call, “the new rules of money.”

The old rules – where the Fed would bail out everyone every time something went wrong… well, those days are behind us. Because the Fed can’t afford to bail anyone out going forward.

It’s going to be too busy trying to defend the dollar and delay the inevitable for as long as possible….

So the financial landscape is changing… and it’s changing fast. We would be wise to change our approach to money and retirement planning accordingly.

More to come on that front tomorrow…

-Joe Withrow

The post What’s coming next for the financial system? appeared first on Zenconomics.

January 15, 2024

The truth about stock prices

After 20 years in finance, I’ve learned that so much of it has to do with your perspective and your attitude. There’s an old saying that sums it up nicely: “If you know what’s happening, you’ll know what to do”.

Of course, the challenge is to know what’s happening.

We’ll come back to that in just a minute. But first I’d like to share a photo with you:

I snapped this one from behind my home office this morning. I never tire of seeing the majestic barefaced cliffs in the background covered in snow.

Getting back to finance…

One of the primary themes I’ve been tracking in these pages is a major paradigm shift in the financial markets.

From 1982 to 2022, interest rates went down consistently while US stock prices moved higher. That made financial planning simple. Buy a few funds that track US equities and then sit tight…

But the trend reversed in 2022. Rates rose rapidly while stock prices fell.

This signaled that it was time to rethink financial planning 101 – which prompted me to write a book about it.

For a while my thesis played out perfectly for all to see. But then the “Fed pivot” craze kicked back into gear and US equities went on a tear to end 2023.

According to the financial news, the US stock market just made a new all-time high in December. And in nominal terms, that’s true. So it seems like the Age of Paper Wealth is alive and well, right?

Not so fast my friend….

Remember, a price is just a measurement of value. So when they say stocks hit all-time highs that means they are worth the most they’ve ever been when priced in dollars.

Now let’s look at what’s really going on.

When we measure stocks in terms of something that cannot be inflated like gold, the picture is much different. This chart tells the story:

As we can see, the S&P 500 did not make new all-time highs last month when we price the index in terms of gold. Instead, pricing the S&P 500 in gold reveals a declining trend in the stock market.

So what’s the discrepancy here?

Inflation.

The Federal Reserve (the Fed) created nearly $6 trillion from nothing in 2020 and 2021. And the US Treasury pumped another $814 billion into the economy via its fiscal “stimulus” programs in 2021.

This created a tidal wave of liquidity in a very short period of time… and that liquidity drove up prices for virtually everything.

Measuring stocks in dollar terms is like using an elastic ruler. It’s not accurate because the ruler (the dollar) is being “stretched” by massive supply increases.

The more dollars they print, the more prices rise. This includes stock prices. But that is not the same as saying stocks are worth more.

When you measure them in gold – the most “inelastic” ruler of the last 5,000 years – you see that stocks are actually falling in value.

Technically, your stocks are worth less than they were in 2021 – even though the price (measured in dollars) says they went up.

And that brings me to one of the most important new rules of money:

The way you protect and grow your money as the dollar decreases in value is to own real assets.

You want to own assets that:

Don’t depend on the Fed’s ability to keep interest rates artificially low (they won’t be able to)…Go up if the Fed (or the Treasury) create dollars from nothing…And most of all, you want a portion of your asset portfolio to give you an income stream…More on that tomorrow…

-Joe Withrow

The post The truth about stock prices appeared first on Zenconomics.

January 11, 2024

Destroying What’s Left of Capitalism

“The competitive market process promotes the efficient allocation of resources, leading to the highest possible standard of living for consumers.” -Ludwig von Mises

That’s Austrian economist Ludwig von Mises writing about the true benefit of a market-based system – the efficient allocation of resources. Mises went on to suggest that the market process is the only method of economic calculation that can be used in a world of scarcity and uncertainty.

The fact is, we must allow competitive markets to allocate resources if we want to enjoy a high standard of living. Anyone who doubts this can simply look at the difference between life in the United States and life in Sub-Saharan Africa.

In the US we enjoy comforts that the richest person alive 150 years ago could never fathom.

We live in homes that are the perfect temperature year-round. Weather is now just a talking point.

We take running water and indoor plumbing for granted. We have supermarkets overflowing with food just down the street. And we have all kinds of screens that offer us endless entertainment.

In Sub-Saharan Africa, nearly half of the population lives without electricity and running water. The local markets offer only a small amount of goods from the capital city. And many families still live as subsistence farmers.

I know this first-hand. Our foundation just drilled a new solar-powered well in rural Uganda. Previously the villagers were walking up to a mile twice a day to collect clean water from a natural spring.

It’s not about money. It all comes down to the allocation of resources.

According to the Organisation for Economic Co-operation and Development (OECD), western governments have been sending an average of $36 billion a year in foreign aid to Sub-Saharan Africa. That’s since the year 2000.

We don’t have clean records – foreign aid is shady business. But according to this estimate, Sub-Saharan Africa has received nearly $1 trillion in foreign aid over the last two decades.

So why haven’t those countries seen much progress? Why is the infrastructure still lacking?

It’s all because the foreign aid gets sucked up by corrupt governments. They use it for their own gains. The money doesn’t flow into a market-based system where companies can bid for it and build out modern infrastructure.

Competitive markets, when free from distortions, direct resources towards their highest and best use. And that brings us back to the central bank digital currency (CBDC) story from yesterday.

As we discussed, the CBDC push is an attack on the commercial banking system. It would take deposits out of the independent banks and move them to the central bank. Afterwards the banks would no longer be free to finance the companies and projects they saw as most economical.

That’s the true purpose of the CBDC.

It’s a pillar of the World Economic Forum’s (WEF’s) globalist master plan they call the “Great Reset”. And it’s how they intend to co-opt full control over money and finance. Why?

To get rid of competition in banking… so they can finance their uneconomical projects.

Renewable energy (that can’t power our grids)… electric vehicles (that we won’t be able to charge without traditional energy production)… 15-minute cities (with total surveillance)… carbon-free farms (that produce fake food)…

These are among the stated goals of the Great Reset. But none of them will come to fruition in a world of competitive markets and banking. Because they aren’t economical. Any commercial bank financing these endeavors would lose money and risk collapse.

So the true goal behind the CBDC push is to destroy what’s left of capitalism.

That’s why they have been working so hard to convince people that capitalism is evil and corporations are greedy. The globalists want us to see their plan as friendly and selfless. But it’s the exact opposite.

To bring it all home, this is why the Federal Reserve (the Fed) raised rates so aggressively in 2022.

As we laid out yesterday, the Fed is owned by the iconic New York banks on Wall Street. They aren’t going to simply roll over and give up their independence.

By raising rates, the Fed made financing anything much more expensive. As such, it’s now even harder for its proponents to implement the Great Reset.

We can see this very clearly as the Environmental, Social, and Governance (ESG) narrative is being swept away right now.

Globalist cheerleader and CEO of BlackRock Larry Fink recently went on TV and said he didn’t want to use the phrase anymore. And new legislation in France proposes to scrap most of the country’s hard “green energy” commitments in favor of nuclear energy.

It we look at it this way, it’s a fascinating game of chess playing out on the global stage.

But it’s a game with serious consequences. And it sure looks like 2024 will be a pivotal year…

More to come next week.

-Joe Withrow

P.S. For those who find economics and little-known historical events interesting, I would highly recommend Tom Woods’ Liberty Classroom.

Tom’s program provides a world-class education on both subjects. And it does so in a compelling and entertaining way. No kidding – I’ve learned far more from Liberty Classroom than I ever did in seventeen years of public education.

If you would like to review Liberty Classroom’s course listings, just go right here: Tom Woods Liberty Classroom Course Listing

The post Destroying What’s Left of Capitalism appeared first on Zenconomics.

January 10, 2024

There’s more to the CBDC story…

A central bank digital currency (CBDC) is a digital form of a country’s fiat currency, regulated by its central bank. It is a liability of the central bank and is widely available to the general public.

This is the definition of a central bank digital currency according to Perplexity.ai. And it spells out exactly why the Federal Reserve (the Fed) has a direct incentive to oppose the CBDC push.

We’ve been diving into the macro talk this week.

On Monday we explored the idea that the “Great Taking” already happened. And yesterday we talked about how Keynesian economics has been dead-wrong on pretty much everything – including its view that recessions are bad.

As we explored, there’s a school of thought that says the Fed raised rates aggressively to cause a financial collapse and usher in a CBDC. I think the opposite is true…

The Fed’s rate-hiking campaign was about defending the dollar and slowing capital-flight out of the US financial markets. The Fed’s incentive is to save the commercial banking system as it currently exists.

This seems ironic on the surface. If the Fed would be in charge of the American CBDC, wouldn’t that mean it gets more power and control? And wouldn’t the Fed want that power?

Well, under previous Chairs Ben Bernanke and Janet Yellen it certainly would.

Under their leadership the Fed coordinated its monetary policy with the European Central Bank (ECB) and catered directly to globalist interests. And the CBDC push is a big part of the globalist “Great Reset”, as spelled out by the World Economic Forum (WEF).

But a silent coup took place within the Federal Reserve system in 2018.

That’s when Jerome Powell took over as Fed Chairman… and he began laying the groundwork for the Fed to break ranks with the globalists.

Powell is a Wall Street guy. He’s deeply connected within New York’s banking cartel. Their power, wealth, and influence depend on a robust commercial banking system here in the US.

And this is where the Fed’s unique structure comes into play.

The Bank of England (BOE) is wholly owned by the British government. The European Central Bank (ECB) is owned by the central banks of the 27 EU member states.

By comparison, the Federal Reserve is composed of 12 regional banks. Those banks are private corporations. And those corporations are owned by commercial “member banks” – not the government.

And those who understand the Federal Reserve System well know that it’s the New York Fed that holds all the power. Its member banks are the iconic New York banks on Wall Street. That’s who Jerome Powell works for.

With that in mind, let’s look at the definition of a CBDC again:

A central bank digital currency (CBDC) is a digital form of a country’s fiat currency, regulated by its central bank. It is a liability of the central bank and is widely available to the general public.

I bolded the most important piece of the puzzle here.

In the commercial banking system today, deposits are the liability of the bank. Loans, securities, and reserves are its primary assets… but the bank can only make loans and invest in securities if it has deposits.

A CBDC would take those deposits away from the commercial banks and house them at the central bank. That’s what the language above in bold is telling us.

So if we take deposits out of the commercial banks… what’s left?

This is why the Fed has a direct incentive to oppose a CBDC. It would gut the commercial banking system and transfer immense power, wealth, and influence away from the big New York banks that dominate American finance today.

Sure, maybe a CBDC would allow the New York banks to continue operating as proxies. But they would not have full decision-making authority if they didn’t have their own deposits to lend against.

And neither would the Fed. Because if we’re going to have an American CBDC, it would require legislative and regulatory approval from the US government.

So there’s more to the CBDC story than meets the eye…

It’s not just a power grab by the insiders to exert more control over the rest of us. It’s a direct attack on the commercial banking system itself. Tomorrow we’ll look at why…

-Joe Withrow

P.S. For a deeper dive on the whole saga, see Beyond the Nest Egg: How to Be Financially Independent Outside of a Broken System. It’s up on Amazon right here.

The post There’s more to the CBDC story… appeared first on Zenconomics.

January 9, 2024

The Recession is Part of the Cure

Yesterday we talked about how the “Great Taking” isn’t in the future… it already happened.

I’m referring here to a popular book and documentary making the rounds in the alternative finance space. It posits that the global bankers are going to set off a great depression and legally steal everyone’s wealth. Afterwards, they will force a central bank digital currency (CBDC) on us.

The book seems to suggest that the Federal Reserve’s (the Fed’s) aggressive rate-hiking campaign was part of that plan. Higher interest rates are what will trigger the crash.

I don’t see it that way.

For one, I don’t see the incentive for bankers to execute such a plan. With the fractional reserve banking system and fiat money, they control and influence the vast majority of the world’s wealth already.

What’s more, I believe the powerful New York banks are actively opposed to a retail CBDC. They have a very big incentive to do so. We can talk about that more tomorrow.

The idea I’d like to explore today is that recessions are healthy. They are necessary.

Keynesian economists have dominated Academia and American politics since the 1960s. They conditioned us to believe recessions were bad. And in their arrogance, they told us that their policies could stop them from happening.

That’s why they used the central banks to drop interest rates to zero in response to the financial crisis of 2008. The world’s central banks colluded to execute what they called zero interest-rate policy (ZIRP).

That made borrowing money effectively free – for those closest to the money spigots. And here in the US they proceeded to inject trillions of new dollars (created from nothing) into the financial system. From there some of those new dollars trickled into the real economy.

They said this funny money would work as stimulus. And in a sense it did.

ZIRP and funny money fueled all kinds of malinvestment. That is to say, the free money funded countless companies and projects that simply aren’t economical with normal interest rates. That includes the electric vehicle (EV) “revolution” and all these “green energy” initiatives they pushed on us.

The onslaught of liquidity also sent asset prices soaring. Real estate… stocks… bonds – everything skyrocketed in price.

As we noted yesterday, those closest to the free money got to buy up these assets first. They are the ones who bid up asset prices. That made it harder for regular folks in Main Street America to play the game.

But their “stimulus” didn’t drive sustainable economic growth. It warped the economy and redirected precious resources (capital/natural resources/labor) to uneconomical endeavors. We call that malinvestment.

Because these uneconomical companies and projects can’t pay for themselves, they constantly need new injections of liquidity to survive.

That’s why the great Austrian economists always warned against Keynesian theory. They pointed out that this kind of “stimulus” creates a quagmire.

Here’s how Ludwig Von Mises put it in his great work Human Action: A Treatise on Economics:

There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.

What Mises was saying is this…

Once you go down the path of manipulating interest rates lower and printing new money from thin air, you necessarily sow the seeds of a future crisis.

Yes, you may successfully push asset prices higher in the short-run. But you’ll drive consumer price inflation and make the economy quite fragile in the process. Then you’ll need to print more and more money just to keep the game going.

If you keep this up for too long, you’ll destroy the currency and wreck the economy beyond all recognition. That’s the worst-case scenario.

But if you recognize that these policies are unsustainable, you can make the decision to reverse course.

Doing so will result in a painful economic contraction as all the malinvestment you enabled is liquidated. The uneconomical projects will be scrapped. The zombie companies will go bankrupt… and all associated debt will be written off.

That’s what the necessary recession does. It clears out the bad debt and gets rid of unproductive companies.

It’s not pleasant. But this process will free up resources for better use – so long as it’s accompanied by normal interest rates.

So I don’t see the Fed’s aggressive rate-hiking campaign as a devious plot for destruction. Quite the opposite.

Normalized interest rates are going to cause a much-needed recession. It will get rid of all the malinvestment that’s accumulated over the last sixteen years. That is, if we let market forces work without intervention.

Higher rates and a recession will also force some degree of fiscal restraint on governments once again. The days of running trillion dollar deficits will have to end one way or another.

This is exactly what needs to happen if we want to salvage whatever’s left of the American dream.

It’s also what needs to happen if we ever hope to restore sound money to this country. That would quickly resurrect the middle class and reverse the Great Taking.

Of course, there are powerful forces out there who don’t want America to save itself. That’s what makes 2024 such a pivotal year.

The battle lines are drawn. The question is – how will it play out?

-Joe Withrow

P.S. Ironically, I believe the Fed needs a recession and higher rates to defend the dollar and save the commercial banking system as well. If I’m right about this, the Fed’s incentives are directly opposed to those of the globalist faction and its “Great Reset” with CBDCs.

We’ll talk more about this dynamic tomorrow. And if you would like a deeper dive, you can get it in my book Beyond the Nest Egg right here.

The post The Recession is Part of the Cure appeared first on Zenconomics.

January 8, 2024

The Great Taking already happened…

One of the books making waves in the finance space right now is David Webb’s The Great Taking. It posits that the global elite have reworked the legal system such that they are now the secured creditors for all financial assets and all the underlying property held by publicly-traded corporations.

According to Webb, the global banking cabal plans to set off another great depression – similar to what happened in the 1930s. This will cause a financial collapse and allow the elites to legally transfer all wealth to themselves.

Afterwards, we’ll wake up to find that we don’t actually own the stocks and funds held in our retirement and brokerage accounts. The middle class will be wiped out. Then, if we want to get back into the new financial system, we’ll have to consent to using a programmable central bank digital currency (CBDC).

The book suggests that the Federal Reserve’s (the Fed’s) aggressive rate-hiking campaign of 2022 was part of this plan. It was the trigger. Higher interest rates are what will cause the collapse and set the plan into motion.

It’s an entertaining story. But I don’t think it correctly identifies the incentives.

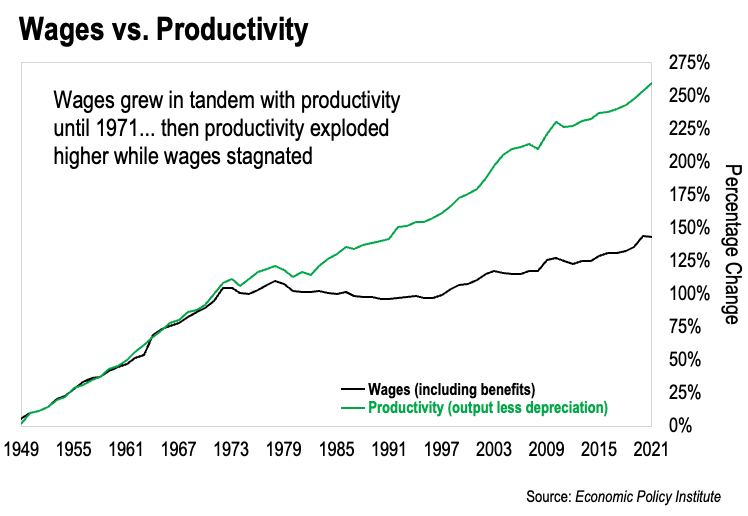

If we look at the numbers, the great taking already happened.

It started in 1971 when President Nixon cut the dollar’s final link to gold. That thrust the world onto a fiat monetary standard.

This allowed governments to create currency units from thin air… which effectively transfers purchasing power from market participants to those who get to use the newly created currency first – the insiders in each country.

That’s just basic supply and demand economics. The more currency units created from nothing, the less purchasing power each unit holds. We see this in the form of rising prices across the board.

This chart tells the story for America:

This depicts inflation-adjusted wage levels compared to annual productivity in the US. Wages are the black line – we can think of this as a proxy for the American middle class.

And we can see very clearly that wages rose in lock-step with productivity every year until 1971. Then productivity kept marching higher… but wages stagnated when adjusted for inflation.

That’s the great taking at work.

The fiat monetary system transferred all productivity gains to the US government and its favored institutions. This effectively eradicated the middle class. But it did so in such a way that nobody realized what was happening.

It was a gradual taking that took place over decades.

But then it accelerated in 2008. That’s when the world’s central banks colluded to cut interest rates to zero.

And make no mistake about it – that was coordinated. Only by working together could central banks enact their zero interest rate policy (ZIRP).

And ZIRP set off what the great Austrian economist Ludwig von Mises referred to as a “crack-up boom”. Free money created from nothing hollowed out the real economy, financialized everything, and sent asset prices (real estate/stocks/bonds) skyrocketing.

Those who got to use the newly-created money first bought these assets before they shot up in price. But the rest of us didn’t get that luxury. And we had to grapple with a rising cost of living at the same time.

The result is that it became harder and harder for regular folks to save money and accumulate assets.

The Fed conducted an “economic well-being” study in 2022. It showed that 37% of American households can’t afford any unexpected expenses greater than $400.

That means a large percentage of the population lives month-to-month.

And today, even people earning “six figures” (over $100,000 a year) struggle to come up with a down payment for a home. Because in many cities a nice home costs well over half a million dollars.

So fiat money and ZIRP are what executed the great taking. They are the disease that wiped out the middle class.

Normalizing interest rates is the cure.

Don’t get me wrong – I’m no fan of the Fed. Central banking is a blight upon the world. But it’s clear to me that the Fed broke ranks under Jerome Powell. Powell made a conscious decision to normalize interest rates.

That’s what the Fed’s aggressive rate-hiking campaign in 2022 was about.

Powell threw ZIRP into the garbage where it belongs. And he powered forward with rate hikes even with everybody yelling at him to stop.

If we remember, the United Nations (UN) issued a statement in October 2022. That statement was directed at the Fed. It called on all central banks to stop raising rates. This signaled that the globalists did not want to end the age of coordinated monetary policy.

Powell ignored them completely.

Now, the Fed’s rate-hiking campaign guarantees that we’ll have a recession. I have no doubt about that. But a recession is exactly what we need. It is part of the cure.

More on that tomorrow…

-Joe Withrow

P.S. I spent quite a bit of time trying to connect the dots when the Fed first began hiking rates. At the time, most analysts were saying it wouldn’t last, and that the Fed would “pivot” at the first sign of trouble.

But my research revealed that the Fed wasn’t just raising rates to fight inflation. It’s aim is much bigger. And I found that the Fed has clear incentives to normalize interest rates and oppose the globalists.

If you’re into this kind of thing, I laid it all out in my book Beyond the Nest Egg. You can find it on Amazon right here.

The post The Great Taking already happened… appeared first on Zenconomics.

January 6, 2024

The Fractures in Global Shipping and What It Means

Global shipping is fracturing and the new year is off to a chaotic start.

On New Year’s Eve a rebel group from Yemen known as the Houthis attacked a Maersk container ship in the Red Sea. In response, the US destroyer USS Gravely intervened and engaged several Houthi small boats in naval combat.

This event was an escalation of previous skirmishes in the Red Sea. The Houthis have been attacking ships they believe to be in route to Israel since last November. They made it clear that any cargo ships traversing the sea are at risk.

This has already impacted global shipping tremendously. To understand why, we have to look at the geography:

The Red Sea is that narrow strip of water separating Africa from the Middle East. It also connects to the Suez Canal, which provides direct access to the Mediterranean Sea.

So the Red Sea is critically important when it comes to global trade. Roughly 15% of all trade moves through it. And around 10% of the world’s oil and liquefied natural gas (LNG) moved by ship flows through the Red Sea – most of that heading for Europe.

At least it did previously.

With the Houthis disrupting shipping routes in the Red Sea, Maersk suspended all cargo movements through the Suez Canal until further notice. And 262 container ships have already rerouted around the Cape of Good Hope, which is located at the southern tip of Africa.

So all those shipments into Europe that previously entered the Mediterranean through the Suez Canal must now sail all the way around Africa to get to their final location.

That’s added enormous expense – up to $1 million in extra fuel costs for every round trip. And of course it’s causing dramatic delays as well.

No surprise, rates for shipping containers have skyrocketed. The cost to ship from China to Europe is up 80% just this week. And if the disruptions continue, we’ll almost certainly see oil prices spike as well.

But there’s a less tangible effect at work here also…

Trust is collapsing around the world. We’re seeing signs that the established order of the last several decades is splintering.

That means major changes are coming fast… and they will impact everything about money, investing, and retirement planning.

Are you positioned for what’s to come?

Get a jump on 2024 with our new financial training. We’re calling it Mistakes, Misconceptions, and Malinvestment.

You can find the broadcast right here.

-Joe Withrow

The post The Fractures in Global Shipping and What It Means appeared first on Zenconomics.

January 3, 2024

Mistakes, Misconceptions, and Malinvestment

Urgent Financial Training for 2024

I Want to bulletproof my moneyTech Support Note: Our back-end system isn’t playing nice with certain VPN server connections right now. This is causing a “Forbidden” error message for some when navigating to our membership portal.

For now the solution is simply to disconnect the VPN or change servers until the button works. If you have any issues after clicking the “I Want to Bulletproof My Money” button, please reach out to admin@gammacapital.tech for immediate support. Just put “Finance for Freedom Tech Support” in the subject line.

The post Mistakes, Misconceptions, and Malinvestment appeared first on Zenconomics.

January 2, 2024

The Death of Financialization

The Age of Paper Wealth is over. And that means the era of hyper-financialization is going to fade away.

I see this as good news.

Financialization refers to the increasing emphasis we’ve placed on financial markets, financial institutions, and financial activity over the last several decades.

All of these items may be important… but they should not dominate our economic activity. Especially not from within a fiat monetary system where all new currency is issued with debt attached (loaned or monetized into existence).

The growing emphasis we’ve placed on finance has come to the detriment of hands-on knowledge, skilled labor, the middle class, and traditional American values.

That is to say – nobody seems to know how to do anything anymore. Myself included. Finance is all I’ve known.

I’ve talked with small business owners all over the US in recent years. They all say the same thing – finding and keeping good employees is nearly impossible. Across the board this is the #1 challenge for a small business.

And it’s all because those who would be good employees just aren’t interested in small business. It’s not glamorous. And it doesn’t pay terribly well. At least not at first.

I can’t help but reflect on this dynamic…

When I was a kid, adults often suggested that we needed to get good grades so one day we could become a doctor or a lawyer. It was understood that those professions paid well.

At some point that must have changed. Today it seems that becoming an investment banker or hedge fund manager is painted as the ideal. They’re the ones making the big bucks.

I see that as folly.

For much of our history the primary means of professional education was the apprenticeship model. A young person would go to work at an older person’s business for at least a few years just to learn the ropes.

Once that young person had fully learned the trade, they became a “journeyman”. Sometimes they would remain in the same place and help their master expand the business – in exchange for much greater pay. And sometimes they would go off and do their own thing.

I see a tremendous opportunity inherent in a modern version of this model today.

We’ve shipped our kids off to college for decades now. Many of them then integrate into corporate America and never return.

That’s created a situation where the people who own small businesses all over this country are now around retirement age. I’m sure many of them would love to sell their business… but who are they going to sell it to?

That’s the opportunity.

Small business may not be glamorous, but it can be lucrative. HVAC technicians, roofers, plumbers, electricians, commercial florists – even the local pizza restaurant can make over a million dollars a year. Those operators with business savvy can even push their annual revenue into the eight figure range.

And that’s all possible in small town America where the cost of living is low, traffic is non-existent, and quality of life is high. What’s not to like?

Hyper-financialization taught us to ignore small business. But it’s the backbone of middle America.

And with a renewed focus on small business, we could put an end to the rat race. I think this will become more evident as we move past the Age of Paper Wealth in the years to come.

Of course, we still have to get our personal finances right. And we have to do so in a very difficult economic climate.

That’s what our event tomorrow is all about. We’re calling it Mistakes, Misconceptions, and Malinvestment. The initial broadcast will go out at 1:00 pm Eastern tomorrow afternoon.

We’re going to talk about why the traditional model for retirement planning just won’t cut it going forward. Then we’re going to talk about a new approach that can create true financial security.

My promise to you is that we’ll keep the entire production under an hour. And I’ll share some stories and insight that I haven’t shared anywhere else. I’m confident it will be well worth your time.

So please be on the look-out for an email invitation tomorrow just before 1:00 pm Eastern. It will contain the link you need to access the event.

See you there.

-Joe Withrow

The post The Death of Financialization appeared first on Zenconomics.

January 1, 2024

What’s Coming in 2024

Happy New Year!

I hope you and yours had a great Christmas season. It’s such a magical time of year.

Each year I take a day or two the week after Christmas just to sit in my office and reflect. I reflect on the previous year… and then I think about my goals for the year to come.

You know, this is the first time that I’m not excited about the new year. I’m uneasy about what 2024 will bring.

Don’t get me wrong – I’m an eternal optimist. But something is in the air. We can feel it.

A core theme I’ve been tracking in these pages is the covert macroeconomic battle between the New York banking cartel, the West’s globalist faction, and the expanded BRICS bloc.

These factions are each jockeying for position on the world’s stage. And their weapons of choice are politics, media, and global finance.

That’s why I’m particularly concerned about what the globalists will do as we approach next year’s presidential election in the United States.

Last time they pushed lockdowns and “peaceful protests” in some big cities… and it just so happens that the same protesters showed up in city after city. It’s almost like they were paid to be there.

And then when those professional protesters arrived at the scene, they conveniently found big stacks of bricks laying around nearby. It’s almost like somebody put those bricks there specifically to be thrown through windows.

I know the media played these things off as a coincidence – if they paid them any attention at all. But it sure looks to me like it was all part of a globalist operation. They needed a puppet in the White House who could be trusted to carry their agenda forward.

So I have to ask – what’s it going to be this time?

And I can’t help but notice that we’re starting to get hints of a pending calamity from various angles.

The Obamas just produced a movie about a grid-down scenario and civilizational collapse in America. Since when are they movie producers? There’s a similar movie coming out in April titled Civil War.

And just last week a CBS News reporter predicted that we’ll see a “national security event with high impact” in 2024. Meanwhile, Tucker Carlson is suggesting that the 2024 election will be like nothing we’ve ever seen before.

That’s a lot of smoke that I can’t ignore.

So I’m uneasy about what’s coming in 2024. But I’m not worried.

I’ve planned my finances and my affairs such that my family will be fine no matter what happens. I’ve also invested in the four alternative assets that provide true security.

The contrarian in me suspects that perhaps these not-so-subtle warnings are a lot to do about nothing. There’s a decent chance 2024 will come and go without any major calamities.

But I still can’t shake that feeling in my gut. It’s telling me that it’s time to be careful. Danger is near.

So we’re ready for whatever at my household. And I’m putting together an urgent financial training to help others get ready for a volatile 2024 too. I’m calling the production Mistakes, Misconceptions, and Malinvestment.

We’ll broadcast the event at 1:00 pm Eastern on Wednesday, January 3rd.

As the title implies, we’re going to talk about the common financial mistakes people make when it comes to personal finance.

Then we’ll talk about the big misconceptions out there right now. Understanding these will provide clarity around what we should be doing to get ready for 2024.

And we’ll also cover the malinvestment that’s shaped our economy in recent years… and what it means going forward.

My promise to you is that we’ll keep the event under an hour long. I think we can even cover everything in 40 minutes or less. I won’t waste your time with any fat, fluff, or ceremony.

So please keep an eye out for your invitation to join us for this urgent financial training on Wednesday at 1:00 pm Eastern. I’ll email you directly with an access link.

-Joe Withrow

The post What’s Coming in 2024 first appeared on Zenconomics.

The post What’s Coming in 2024 appeared first on Zenconomics.