Joe Withrow's Blog, page 10

November 14, 2023

The Fed and Warring Factions

It’s a big club and you ain’t in it.

The late great comedian George Carlin loved spitting this quote in his skits. He would talk about how the political power structure and the media always seem to march to the same beat… regardless of which political party happened to be in power.

What Carlin was talking about is often called the Deep State today. It refers to what appears to be a shadowy coalition of people behind the scenes who drive government policy.

Donald Trump catapulted Deep State into popular vernacular. But to be fair, Bill Bonner was using the term years ahead of Trump. Let’s give credit where it’s due.

But the question is… does this view of the power structure explain the macroeconomic events we are seeing play out today?

To be sure, the Deep State view can explain why nothing much seems to change regardless of which political party is in power. But it cannot explain the break between the Federal Reserve (the Fed) and the international power structure—the globalists.

As we discussed yesterday, the Fed coordinated monetary policy with the world’s central banks in the wake of the 2008 financial crisis. It certainly looked like there was a big club at work.

But the globalists did not want the Fed to raise interest rates aggressively last year. The Fed powered forward anyway… and fired the first shot in what’s become a secret financial war.

So what gives? Isn’t the Fed supposed to be part of the Deep State also?

If we want the real answer, we must look at the factions at work… and their incentives.

An Attack on Capitalism

In June 2020, an international organization called the World Economic Forum (WEF) announced what it calls the “Great Reset”. The WEF pitched it as an economic recovery plan in response to COVID-19… but that was just the cover story.

The WEF is a globalist organization that engages with government and corporate leaders from around the world. It designed the Great Reset in collaboration with many of these “leaders”.

The core idea is to shift from what they call ‘short-term shareholder capitalism’ to ‘long-term stakeholder capitalism’ with a focus on environmental, social, and governance (ESG) issues.

In other words, the Great Reset is about replacing the current economic system – with its focus on private property and competition – with a system where stakeholders collaborate on key economic and social issues.

It’s supposed to sound like a friendlier version of capitalism. But is it?

If we want to analyze the Great Reset and stakeholder capitalism, the most obvious place to start is this: Who are the stakeholders?

Well, it’s them. In their vision, their globalist organizations control everything.

In fact, these people were arrogant enough to make a commercial that pitches the slogan, “You’ll own nothing and be happy”. That’s what they think of everyone not in their circle.

The WEF outlined five pillars for their Great Reset. They are:

JusticeSustainabilityDigitalizationNew Social ContractShift in CapitalismLet’s break these down…

When they talk about justice, they say we need to reduce inequalities and promote social inclusion. What they mean is that we need to get rid of competition and merit-based economic mobility.

When they say sustainability, it’s all about replacing traditional energy production with what they call “green energy”. This is the push for solar and wind power.

Of course, it isn’t economical. Solar and wind cannot generate enough baseload power to run our economy. We talked about that earlier this month.

And this is why they need to eliminate competition with that first pillar. Their green energy revolution simply will not happen within the current system.

The Great Reset’s next pillar is digitalization. This is about central bank digital currencies (CBDCs) and 15-minute smart cities.

We’ll talk about CBDCs is a minute—they are a big reason why the Fed is at war with the globalists. As for smart cities – they are all about herding people into small living areas where they can be subjected to total surveillance.

The fourth pillar is “new social contract”. They say this is about fostering social inclusion and reducing inequality between countries. Really, it’s about eliminating national sovereignty in everything but name. That’s the globalist fantasy.

And the last pillar is “shift in capitalism”. This is about replacing the current economic system with their model… which isn’t capitalism at all. It strikes me as a modern version of feudalism. It’s a system where the peasants can be kept subservient to their overlords.

I know this sounds like a giant conspiracy theory… except the WEF has talked openly about all of it. And they even set a timeline for implementation—2030. They wanted to get it all done within this decade.

And for a few years it looked like they just might pull it off. The Covid hysteria – with its lockdowns, travel restrictions, and contact tracing gave them a great head start in 2020 and 2021.

But then the Fed made its move in 2022.

I know this sounds backwards. The Fed is America’s central bank. Doesn’t it want to take on additional power and control with CBDCs?

Jerome Powell has indeed talked positively about a “wholesale” CBDC. But that’s just a back-end settlement system for use between the Fed and the commercial banks.

As for a “retail” CBDC – something meant for the American public – Powell said that would require the authorization of Congress.

He’s not interested in pushing a retail CBDC himself. One Fed insider even said that there will be a retail CBDC “over Powell’s dead body”.

To understand why, the Fed is at odds with the globalists over retail CBDCs and the rest of the Great Reset, we must understand what CBDCs are really about. Then we’ll realize that a powerful faction stands to lose out big time if they become a reality in this country.

The Real Threat of CBDCs

To implement the Great Reset’s five pillars, the globalists need to make central banks the ultimate arbiter of everything related to money and credit. That’s what CBDCs are all about.

With retail CBDCs, our bank accounts would reside at the central bank. This is true both for individuals and corporations. That would give the central bank full control over our money and our transactions.

Then, when we need a loan, they are the folks we would have to go to.

That’s huge. Especially when we consider that it’s not just individuals who would have to go to them for loans. It would be everybody, including large companies. They would have to go to the globalist power structure to get financing for their business and key projects.

That means the globalist faction would suddenly have direct control over which projects and activities could get financing and which couldn’t. This alone would give these people almost total control over the western world.

And the key is this – there would be no competition in their “stakeholder” model. It’s all about being able to finance uneconomical projects like green energy.

To accomplish this, they need to neuter the commercial banking system and eliminate the banks who don’t play along.

That’s because there’s fierce competition in the banking world. Competition ensures that each bank strives to make good credit decisions. The better their loans perform, the more money, power, and influence they accumulate.

And on the flip side, those banks who finance uneconomical projects struggle. And if they finance too many uneconomical projects, they collapse.

This dynamic creates built-in incentives that encourage wise resource allocation and economic growth.

Stakeholder capitalism is about tearing down those incentives and emasculating the banks. That’s the only way the Great Reset could come to fruition.

The New York Banking Cartel Woke Up

The American banking scene has an illustrious history. Not all of that history is noble and honest… but it’s illustrious nonetheless.

Of course, American banking revolves around Wall Street. And the top Wall Street banks trace their history back over a century.

The people running these banks are wealthy and well-connected throughout the American power structure. That makes them a faction unto themselves. We can call it the New York Banking Cartel.

At some point over the last several years the New York Banking Cartel realized that the Great Reset was a direct attack on their commercial banking system. And they said nope, that’s not happening here.

This is why Jamie Dimon is suddenly calling himself a red-blooded, patriotic free-market capitalist. He wrote that verbatim in his annual letter to shareholders this year. These are all dirty words according to the globalist rhetoric.

And notice how Dimon has also ditched the ESG meme. He’s now talking up the need for more oil and gas investment. Again, that’s a no-no from the globalist perspective.

This shift in rhetoric is just more proof that there’s a power struggle happening right now. It’s the globalists vs. the New York Banking Cartel.

And guess what?

Jerome Powell is a Wall Street guy. He’s deeply connected within the New York banking scene.

That’s why the Fed broke ranks. Powell and the Fed stand with the New York banks… in opposition to the international power structure.

It’s all about saving the current system.

And the only way to do that is to get back to having “normal” interest rates set by market forces. That’s where the Fed comes in.

Jerome Powell didn’t raise rates so aggressively last year just to fight inflation. He did so to save American capitalism and the commercial banking system as currently constructed.

Normalized interest rates will stop the massive misallocation of resources that’s occurred since 2008. Higher rates also curtail the globalists’ ability to leverage Eurodollars to finance programs they favor, as we discussed yesterday.

Of course, normalized interest rates also guarantee that we’ll have a recession. The media will raise a fuss about it… but it’s a good thing.

The coming recession will clear out all the bad debt and malinvestment that have clogged the arteries of our economy. This must happen if we want to get back to having an environment that favors capital formation, small business, and the middle class.

And here’s the key to it all – the New York banks need just that environment to stay alive.

It strikes me as ironic, but the Fed and Wall Street are fighting against further centralization right now. Yet nobody even realizes it’s happening.

And the story got even more interesting when the US Treasury threw its hat into the ring. More on that tomorrow…

-Joe Withrow

P.S. I know this kind of macroeconomic analysis isn’t everyone’s cup of tea. But if you would like to dive into the story in even more detail, check out my book Beyond the Nest Egg. You can find it right here.

The post The Fed and Warring Factions first appeared on Zenconomics.

The post The Fed and Warring Factions appeared first on Zenconomics.

November 13, 2023

Powell closed the door on the globalists

Jerome Powell wasn’t having it.

“Just close the %!@?! door”, he instructed his security team as they rushed him off the stage.

Powell was speaking at the International Monetary Fund’s (IMF’s) annual research conference in Washington, D.C. last week. The event lasted two days – last Thursday and Friday. Powell’s speech was the headliner.

The Fed Chair took the stage to talk about the Federal Reserve’s (the Fed’s) outlook on inflation, interest rates, and the US economy. But about a minute into his talk, a group of “climate activists” rushed the stage to heckle him.

They shouted angrily about “fossil finance” and held up a big sign in front of the audience and the cameras. It read, “Business As Usual Is a Climate Disaster”.

Of course, the media dismissed it as a random event. It’s just those feisty climate activists wanting to be heard.

But let’s think about this for a minute…

I’ve been to plenty of conferences across the country over the years. The process for getting in has always been the same—you buy a ticket online and present it at the check-in station upon arriving at the event.

They scan the bar code to validate the ticket. Then they give you a badge to wear. It signals to security that you are supposed to be at the venue.

And there’s always security. These conferences are expensive to put on. The organizers and sponsors take them very seriously.

Now, if we look at the audience gathered at the IMF’s conference last week, the majority of the crowd sported bald heads or gray hair. And they all wore business suits. The audience consisted mostly of older professionals.

Then if we look at the climate protesters, they each appeared to be in their 20’s or 30’s… with the exception of one token old guy. They weren’t particularly well-dressed. And they carried with them a massive sign that took six people to hold.

How did they get through security?

Even if we assume they each bought tickets and checked in, there’s no way security at an IMF event in Washington, D.C. would allow a rag-tag group of young people to carry a giant sign into an event featuring the Federal Reserve Chair.

That is, unless it was staged. And that’s exactly what it was.

A Secret Financial War is Raging

As we discussed last week, very few analysts expected the Fed to raise interest rates so aggressively last year. Many touted the same tired message. They said the Fed was only raising in the present to “pivot” and cut rates later in the year.

Why did so many analysts get that one wrong?

Well, it’s obvious that a large portion of the international power structure did not want higher interest rates. By power structure, I’m referring to national governments and the international institutions that have influence on policy. This includes the United Nations (UN), the IMF, the World Bank, and numerous others.

In fact, the UN proclaimed that all central banks needed to stop raising rates back on October 3rd of last year. Then the World Bank published a fear-based report saying that interest rate increases would trigger a global recession.

The mistake so many analysts made was in thinking that the Fed was aligned with those institutions. That’s why so many thought the Fed would “pivot”. They assumed the Fed was on the same team as the globalists.

And why wouldn’t they be?

The Fed collaborated with these international institutions to coordinate monetary policy when Ben Bernanke (2006-2014) and Janet Yellen (2014-2018) ran the show as Fed Chair. We didn’t have reason to believe the game would change when Jerome Powell took over.

But change it did…

The Silent Coup of 2018

Under Powell, the Fed began publishing something called the Secured Overnight Financing Rate (SOFR) in April 2018.

I doubt many people have ever heard of SOFR. Of those that have, I suspect very few know what it is, or why it’s so significant.

SOFR is a benchmark interest rate for dollar-denominated loans and derivatives. It’s based exclusively on transactions in the US Treasury repurchase (repo) market—which the Fed is directly involved in.

We don’t need to go down a deep rabbit hole on this to get the big picture.

What’s important to understand is that the Fed first began publishing SOFR in 2018. Then it gradually integrated SOFR into the financial system over the next four years.

By January 2022, SOFR became the dominant interest rate benchmark in the US. The interest rate for all loans in the US have been influenced directly by SOFR ever since then.

To understand why this is important, we must know what SOFR just replaced.

Previously, the London Interbank Offered Rate (LIBOR) was the interest-rate benchmark for dollar-denominated loans and derivatives. That means those who could influence LIBOR could also influence interest rates in the US.

And who could heavily influence LIBOR? Among others, the Bank of England (BoE) and the European Central Bank (ECB) can have an impact on LIBOR through their own policy initiatives.

What this means is that the Fed did not have full control over US monetary policy prior to 2022. That’s why Powell couldn’t raise interest rates aggressively sooner.

He used SOFR to decouple US monetary policy from the international power structure first. If he hadn’t, the ECB would have been able to keep a lid on interest rate increases by manipulating LIBOR lower.

It was all calculated.

The Fed Landed the First Blow

By raising interest rates in the US, the Fed very quickly drained the Eurodollar market of liquidity. That, in turn, limited what the ECB could do with its own monetary policy. In fact, it forced the ECB and the rest of the world to follow suit and raise their own domestic interest rates.

Now, Eurodollars are simply US dollar-denominated deposits held at foreign banks, mostly European.

The Eurodollar market exists outside the US regulatory system. And it provides liquidity to European financial institutions and ultimately European governments. They can leverage Eurodollars to support spending programs that they favor.

By draining the Eurodollar market, the Fed effectively hamstrung the ECB’s ability to drive its own agenda forward.

Which of course raises the obvious question: why?

As we noted earlier, the Fed seemed to be aligned with the ECB for years… maybe decades. On many occasions it appeared their policies were coordinated. The response to the 2008 financial crisis is a great example.

So why did the Fed break ranks?

Understanding this is the key to understanding what’s playing out on the world stage right now… and why the IMF allowed those protesters to heckle Powell.

More to come tomorrow.

-Joe Withrow

P.S. The World Bank is right – Powell’s aggressive rate hikes will cause a recession. The World Bank sees that as a bad thing… but it’s not.

Recessions are a necessary part of the economic cycle. They are healthy.

Further, I submit to you that allowing a massive recession to occur over the next 12-36 months is the only thing that can save American capitalism and the commercial banking system. More on that this week…

And for a deeper dive into everything we’re discussing, check out my book Beyond the Nest Egg. You can find it right here.

The post Powell closed the door on the globalists first appeared on Zenconomics.

The post Powell closed the door on the globalists appeared first on Zenconomics.

November 9, 2023

America is at a crossroads…

For the last two generations, the success plan was clear.

Go to school —> get good grades —> go to college —> get a good job. If you followed that plan and had a good work ethic, a successful middle-class lifestyle would come easy to you.

And for those more ambitious, there were very few roadblocks to starting a business. Opportunity was everywhere.

That was the American dream. It’s what inspired countless immigrants to leave their homeland to create a new life in this country.

But that dream is fading.

The traditional success plan – go to school, get good grades, get a job – it no longer guarantees success. Colleges today load students up with debt and fill their heads with all kinds of useless claptrap.

Meanwhile, the Administrative State peppers small businesses with all kinds of regulatory burdens. Those small business success stories from a generation ago would be hard-pressed to recreate the same success if they had to start today.

And to top it off, reckless government spending has driven up everybody’s cost of living dramatically in recent decades. They finance this spending with printed money, and that creates consumer price inflation. It’s wiping out the middle class.

And that’s not just an opinion. It’s all in the data. Today I’ve got two tables for you that spell it all out, clear as day.

Here’s the first:

This table tracks the median price of a new car, ten gallons of gas to put in that car, and five pounds of ground beef going back to 1940.

As we can see, it’s not a pretty picture. Costs have risen dramatically over every ten year period in modern history.

That said, we have to compare these costs to the median income to get a better feel for the story. And that’s what this next table does:

Here we’re tracking the median home price compared to median annual incomes going back to 1940.

And again, we can see that home prices have risen significantly over every ten year period. But incomes have too… so it’s that third line we need to focus on. It shows us exactly what percentage of the median home the average guy’s salary can cover.

The median home costs $430,300 today. The median annual income is $74,580. That means the average person’s salary can only cover 17% of the median home price.

We can see just how dramatic this is by looking at past data.

If we go back to the turn of the century, the median income could cover 33% of the median home price. That’s nearly twice as much.

Then if we go back to 1970—the median salary could cover more than half of the median home price. If that were the case today, the average person would be making $232,362 a year.

What these numbers illustrate is that it has become harder and harder to live a comfortable middle class life in the US. And it’s all because inflation has eroded the value of our dollar… thus, costs have risen far faster than incomes.

We can’t do much to change this dynamic. But we can protect ourselves from it with strategic investments.

Consumer Goods Inflation Hedges

Inflation has eroded the average American family’s disposable income.

We see this in the charts above. And we see it if we look at the data for average savings rate and credit card debt. Savings has plummeted while credit card debt has ballooned.

This doesn’t bode well for companies selling higher-end goods. Luxury cruises… high-end cars… overpriced fashion brands – these businesses and many like them are going to struggle in the years to come.

At the same time, there are certain goods the American consumer will always buy – regardless of how tight the monthly budget is.

For example, people will still go to the supermarket regularly. They’ll buy their food, soda, snacks, candy, personal care products, and household cleaners… just like they always have.

Many families will still go out to eat regularly as well. The convenience is hard to beat.

Except instead of going to a nice restaurant, many will choose fast food because it’s cheaper. There’s a reason why certain fast food chains are among the world’s best businesses.

Given Americans’ addiction to coffee and sweet drinks, Starbucks and other coffee shops are likely to remain popular in the years to come as well – even as the middle class continues to shrink.

And what about discount stores like Walmart and Dollar General?

They will continue to offer consumers every-day goods at low prices. These “lower end” stores will likely gain new customers as inflation wreaks havoc on disposable income.

The point is, the American consumer isn’t going away. But his spending habits are likely to shift to lower-price alternatives.

So, there are at least a handful of publicly-traded companies that will benefit from this shift in consumer spending. Their stocks are our consumer goods inflation hedges.

And here’s the thing – some of these companies are fantastic businesses. They are capital-efficient and shareholder friendly. That’s exactly what we’re looking for in a great investment.

The key is – as with our other market-based investment “buckets” – we must buy these companies when they trade at a reasonable valuation.

If we’re patient enough, we’ll be able to add these inflation hedges to our portfolio at an incredible price. Then we can reinvest the dividends to compound our investment for years to come.

-Joe Withrow

P.S. We talk about asset allocation and specific investment suggestions inside our investment membership The Phoenician League.

Our goal is to help all our members bulletproof their money, just as we’ve been discussing. From there we create a cash flow wealth strategy. It’s all about building additional income streams to make our financial situation far more robust.

If you’d like more information on our program, just go here.

The post America is at a crossroads… first appeared on Zenconomics.

The post America is at a crossroads… appeared first on Zenconomics.

November 8, 2023

Gold Never Left

Gold served as base money for thousands of years prior to 1933.

In other words, gold served as the foundation of our monetary system. It was the monetary reserve upon which the financial system operated. Even when gold coins were not used to settle transactions in the private sector, the banks would redeem the paper currency in circulation for gold upon demand.

That all stopped in 1933. That’s when the United States and other countries transitioned to fiat currency not redeemable for gold. By the way, the word fiat is Latin for “let it be done”.

This transition paved the way for The Age of Paper Wealth. It lasted forty years from 1982 to 2022. During that time the world’s central banks created trillions of dollars out of thin air to drive interest rates down and stock prices up.

But that era is over now. The Fed’s aggressive rate-hiking campaign last year marked the end of it.

So if The Age of Paper Wealth is over… what do we think that means for gold going forward?

I think it’s wildly bullish.

We aren’t going back to the days of using gold as base money. But we can’t ignore the fact that the US government still owns 8,133.5 tons of gold. That’s worth over half a trillion dollars at current prices.

And official records suggest that the world’s central banks hold 26,866.5 tons of gold. That’s worth over $1.7 trillion today.

These numbers aren’t large in the big scheme of things with gold priced around $2,000 an ounce. But they could become significant if the price of gold roared higher.

This shows that the world’s central banks never abandoned gold… even as they worked hard to convince people that gold was a “barbarous relic”, as famed economist John Maynard Keynes put it.

Why is that?

Why did the central banks hold onto their gold for all these years? And why have some central banks actively bought more gold recently?

Central banks around the world bought over 1,100 tons of gold last year. That’s the largest annual buying spree on record.

Here’s the story nobody else is talking about…

Gold Is About to Be Re-Monetized

Yesterday we talked about how the Fed is dead-set on normalizing interest rates. They have to if they want to save the legacy financial system and the American economy.

So the Fed isn’t raising now just to cut rates significantly later. And this presents the US Treasury with a major problem.

Today, the average interest rate on the US government’s outstanding debt is just under three percent. But roughly 40% of that debt is coming due over the next three years. That’s somewhere around $13 trillion.

Obviously the US government cannot afford to pay this debt off outright. It’s set to run annual deficits well in excess of $1 trillion over the next ten years.

That means the debt coming due will need to be rolled over. The Treasury will need to issue new debt at today’s higher rates just to pay off the old debt.

This sets the stage for a massive budget crisis.

The Congressional Budget Office (CBO) projects that the US government’s debt service costs will hit $745 billion by the end of next year… and then rise to $1.4 trillion by 2033. That would make debt service the second largest line-item in the federal budget—second only to Social Security and Medicare payments.

So if I’m right that the Fed is dead-set on normalizing interest rates, the US government will have to reduce its spending dramatically in other areas to satisfy debt service costs.

That is, unless the Treasury can figure out a way to roll over that $13 trillion at a much lower interest rate… even if the Fed doesn’t cut.

How could it do that? By re-monetizing America’s gold hoard.

Remember those 8,133.5 tons of gold we talked about earlier? Suppose the US Treasury agreed to settle a portion of its maturing debt with this gold. Meaning, when the Treasury paid off a bond coming due, it paid out a portion of the balance in gold.

That’s gold re-monetization.

This could lend itself to a tiered system of sorts. The Treasury could sell bonds with various degrees of gold backing at corresponding rates. For example, a 1% gold-backed bond would carry a higher rate than a 5% gold-backed bond. But both would pay lower rates than a standard U.S. Treasury bond with no gold backing.

See how this works?

Gold re-monetization would allow the Treasury to sell bonds at a lower rate than it otherwise could. In turn, this could allow the government to manage debt service costs even with higher rates.

This would also make Treasury bonds attractive again to foreign countries and central banks. That’s big.

The Treasury will need to sell around $13 trillion worth of new bonds just in the next three years. If the Fed stands pat on its resolve to normalize rates, it can’t be the buyer of last resort anymore.

So the Treasury will need to drum up significant demand for its bonds among the world’s major financial institutions and central banks. Yet, the US government’s creditworthiness is not trusted as much as it once was.

In fact, Fitch Ratings just downgraded the United States’ sovereign credit rating in August. Fitch cited “expected fiscal deterioration over the next three years” as the key driver behind its decision.

It’s no secret—the US Treasury is in a tight spot.

Gold is the solution. Gold re-monetization is how it can attract the foreign investment it needs in the years to come.

And make no mistake about it – foreign central banks remember what JP Morgan said in 1912. Gold is money, everything else is credit.

The Big Opportunity

If we find ourself in that world – a world where the US is re-monetizing its gold stash – what do we think would happen to the price of gold?

It would go much higher. Especially if the US government cracked down on naked short selling in the paper gold markets…

Naked short selling occurs when an entity shorts gold futures contracts without actually owning the physical metal required for delivery. This can serve to artificially suppress the spot price of gold.

It’s not entirely clear how prevalent this practice is, but JP Morgan did pay $920 million in fines in 2020 for manipulating the gold futures market. We know it happens to some degree. Suddenly the US government would have an incentive to put a stop to it. Because it would want a higher gold price to support its re-monetization program.

So, the stage is set for a roaring bull market in gold over the next several years.

We need to understand that these macroeconomic conditions are now in the driver’s seat when it comes to gold’s price. Gold will not trade inverse to interest rates going forward.

And that means it’s time to build exposure to the best gold equities on the market.

We discussed the need to own physical gold when we talked about reserve assets last week. Moving 5-8% of our portfolio into gold equities as well can add some real pop to our gold holdings.

I’m most partial to the best gold royalty companies right now. These are firms that provide creative financing solutions to the mining companies in exchange for royalty and streaming rights to the total production of mining operations.

Royalty companies have far fewer operating costs than the gold miners. And they build diversified portfolios of royalty and streaming rights.

That makes their income far more stable… which allows them to pay consistent dividends. We can reinvest those dividends to put the power of compound interest to work for us.

So we want to anchor our gold equities allocation with the best royalty companies.

Then we can take some shots on a few gold mining stocks when it becomes clear that the price of gold is about to kick. They are far more speculative. But the returns can be outstanding if you get the timing right.

-Joe Withrow

P.S. We’ll talk about consumer goods inflation hedges tomorrow. That’s our fifth investment “bucket”. Then next week we’ll get into the break between the Fed and the US Treasury… which I alluded to today.

And if you would like more comprehensive guidance on how to implement these investment themes, and then begin building passive income on top of them, check out The Phoenician League. All the info is right here.

The post Gold Never Left first appeared on Zenconomics.

The post Gold Never Left appeared first on Zenconomics.

November 7, 2023

What the “normies” are missing…

The world as we know it changed last year.

From 1982 to 2022, the Federal Reserve (the Fed) created over $8 trillion from nothing to flood the financial system with liquidity. This drove interest rates consistently lower while pushing stock prices higher for forty years.

Nobody under the age of 60 has known anything else in their adult life.

In that era, stock prices tended to move in tandem. When an index like the S&P 500 or the Nasdaq was going up, most stocks in that index would go up also.

So being in the best stocks wasn’t as important as just being in the market. Nearly 1,000 “passive investing” exchange traded funds (ETFs) formed since 2008 to capitalize on this dynamic.

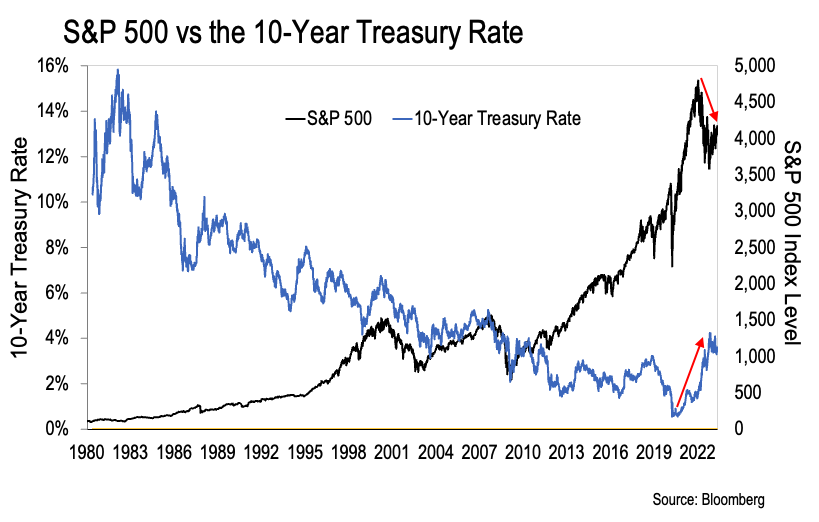

But the game’s over. This chart paints the picture:

In March of last year the Fed embarked on the most aggressive rate-hiking campaign in its 110 year history. That reversed the two primary trends.

Interest rates screamed higher—that’s the blue line in the chart above. And stocks began to march lower, as illustrated by the black line.

The red arrows make it clear… The Age of Paper Wealth is over.

But wait—Fed Chair Jerome Powell just declined to hike rates again for the second meeting in a row. Some analysts are now saying that the Fed is done raising rates.

And the S&P 500 is up over 6% in just the last week and a half in response. The same analysts say that’s evidence that stocks are about to go on a tear and the game is back on.

Here’s what they are missing…

The Story is Far More Complex

The “normie” understanding is that the Fed is raising interest rates to fight consumer price inflation. Then, when inflation comes back down, the Fed will cut rates again to juice the markets – just like it has for the last forty years.

This view sees inflation as a mysterious boogieman that rears its head every now and then. And it sees the Fed as a reactionary institution stepping up to fight it.

I submit to you that this is an overly simplistic view. And it ignores our current economic situation completely.

The fact is, we’ve lived in a “number go up” world for the last forty years. That is to say, we’ve been conditioned to think growth is perpetual and stock prices should always go up over time.

But none of it was natural.

To keep the numbers going up, the people pulling the strings of monetary and fiscal policy had to push interest rates ever-lower and constantly pump more and more printed money into the system. They called it stimulus.

The problem is, rates can only go so low. And the lower they go, the more malinvestment forms within the economy.

Malinvestment refers to projects and companies that just aren’t economical. They don’t produce enough value to pay for themselves.

And that makes them a mistake. They misallocate scarce resources that could have gone to something that would provide greater value to the market and to society.

This is nothing more than Adam Smith’s Invisible Hand principle at work. It comes from his masterpiece The Wealth of Nations.

Smith’s principle points out that the free market has incentives built-in to ensure that resources are allocated in an optimal way. At least most of the time. And when resources are misallocated, the market quickly purges the malinvestment to correct those mistakes.

We’ve known this for 247 years now. Smith’s book published in 1776. But we’ve ignored it… and we’ve made a lot of mistakes recently. Then we didn’t allow the market to correct those mistakes.

The Fed and the world’s central banks collaborated to drop interest rates to zero in 2008. They said it was necessary to save the financial system.

Whether that’s true or not doesn’t matter at this point. What matters is that their actions allowed an enormous amount of malinvestment to form.

Goldman Sachs estimates that 13% of all publicly traded companies in the US are zombie companies. The Fed puts its estimate at 10%.

Zombie companies are companies that can’t generate enough revenues to cover their debt-service costs. So they must consistently borrow more and more money to stay alive.

In a free market, these companies would be forced into bankruptcy very quickly. Nobody would lend them the money they needed to survive.

But in our “number go up” world of zero interest rates, these companies have been able to borrow money cheaply for over a decade now.

And that’s because the central banks fought tooth-and-nail to keep rates near zero. They haven’t allowed a correction to occur.

Until now.

What the Fed is Really Up To

The Fed is acting to save the financial system and the American economy. That’s what this is all about. Consumer price inflation is just a small part of the picture.

It’s almost like Mr. Powell has been studying up on his Austrian free market economics recently.

Those of us well-versed in Austrian economics know very well that zero-bound interest rates and fiscal “stimulus” are not sustainable.

Ludwig Von Mises spelled out the dilemma very clearly in his great work Human Action: A Treatise on Economics. Here’s Mises:

There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.

What Mises was saying is this…

Once you go down the path of manipulating interest rates lower and printing new money from thin air, you necessarily sow the seeds of a future crisis.

If you keep going down that same path for too long, you’ll destroy the currency and wreck the economy beyond all recognition. This is the worst-case scenario.

But if you recognize that your current trajectory is unsustainable, you can make the decision to reverse course.

This will result in a painful economic contraction. Artificially low interest rates and funny money fuel all kinds of malinvestment… and that malinvestment must be liquidated.

That’s what the necessary recession does. It clears out the bad debt and gets rid of unproductive companies.

It’s not fun to go through. But it’s far preferable to destroying the currency and the entire economy.

Most of us in the alternative financial space assumed the Fed would never reverse course. But it did. The Fed chose Mises’ voluntary abandonment option when it set out on its rate-hiking campaign last year.

Now, this doesn’t mean the Fed is “good”. Let’s be clear about that. It is simply acting in its own best interest.

What we need to understand is that the Fed is normalizing interest rates. It wants to get back to what it calls the “terminal level”. That’s the rate at which the Fed sees as neutral. It’s neither stimulative nor restrictive to the economy.

When the Fed gets to that level, it will stop raising rates. But that doesn’t mean it will turn around and cut rates aggressively after. The game has changed.

Powell needs normalized interest rates to force fiscal responsibility upon the system again. That’s the only hope we have of getting back to a healthy economy.

And that means we’re going to endure a massive recession in the coming years. It’s unavoidable.

This is why we need a whole new approach to building our portfolio.

The Age of Paper Wealth is over. It’s not coming back. We need to bulletproof our money… before it’s too late.

To do so, we must focus on five core investment themes. They are:

Reserve AssetsWorld-Class InsuranceEnergy RenaissanceGold EquitiesConsumer Goods Inflation HedgesWe talked about reserve assets and world-class insurance last week. I see both as foundational.

We also discussed the coming energy renaissance… and how to get out in front of it yesterday. Doing so all comes down to learning the secret of energy royalties.

We’ll cover gold equities and consumer goods inflation hedges the next few days. Then we’ll talk about the obvious break between the Fed and the US Treasury. I haven’t seen this discussed anywhere else yet…

Stay tuned.

-Joe Withrow

P.S. The Age of Paper Wealth may be over… but that doesn’t mean doom is upon us.

The Phoenician League investment membership is where we put it all together to create a comprehensive plan for financial independence. You can find more information at:

Achieve Financial Independence Using an Ancient Investing Secret

The post What the “normies” are missing… first appeared on Zenconomics.

The post What the “normies” are missing… appeared first on Zenconomics.

November 6, 2023

The Secret of Energy Royalties

Crude oil prices are going back to $100 and then $120 per barrel.

That’s what the portfolio manager of Smead Capital Management told Bloomberg recently. And I think he’s right.

It’s easy to forget that oil hit a 10-year high above $130 a barrel back in March of last year. But economic weakness and recession fears helped walk oil back down from that high.

And then the US government jumped in.

The Biden administration drained the Strategic Petroleum Reserve (SPR) to dump 180 million barrels of oil on the market. This was the largest SPR release in history.

The SPR is simply the US government’s emergency stockpile of crude oil. Congress established it back in 1975 in response to the Arab Oil Embargo which led to shortages across the US.

The current administration drained the SPR to push the price of oil lower. They got it back down into the $70s and $80s. That’s where oil’s traded for most of the year.

But here’s the thing… the rubber band always snaps back. When you push something in a direction it wouldn’t otherwise go in, sooner or later it’s going to come back.

And that’s especially true of oil when you have wars in Eastern Europe and in the Levant… and you have crazy people trying their darndest to escalate those wars into something bigger.

Meanwhile, the Environmental, Social, Governance (ESG) movement shifted nearly $2.2 trillion in investment into renewable energy development. All in just the last seven years.

The problem is, those projects aren’t economical. As we discussed last week, solar and wind cannot produce enough energy to power our grid.

So that money should have gone towards traditional energy production (oil, natural gas, and nuclear power). Instead, annual investment in oil & gas plummeted.

Oil investment here in the US peaked at $205 billion in 2014. Investment has floated between $83 and $124 billion each year since.

The story for nuclear is even worse. We’ve only invested $6-8 billion a year for maintenance and minor upgrades over the last seven years.

So we’ve been underinvesting in traditional energy production thanks to the false promises of ESG.

At some point we’ll admit that was a mistake. And then we’ll see a tidal wave of investment dollars pour back into oil, gas, and nuclear.

That means we are going to experience an energy renaissance in this country and around the world. It’s inevitable if we want to maintain our current standard of living.

So let’s get out ahead of what’s coming…

Simple Moves to Make Today

The easiest way to get exposure to oil and gas is to buy the SPDR S&P Oil & Gas ETF (XOP). It’s an exchange traded fund (ETF) that tracks nearly 60 stocks in the oil & gas industry.

And the easiest way to gain exposure to nuclear is to buy the Sprott Physical Uranium Trust (SRUUF). It’s an investment fund that buys and stores physical uranium—the fuel that powers nuclear reactors.

As I write, SRUUF owns over 62 million pounds of uranium. That stockpile is worth nearly $4.7 billion at current prices.

This gives SRUUF a net asset value of $18.42 per unit. Yet we can buy it today at $17.59. That’s a 4.5% discount. That means SRUUF is on sale right now.

I suggest allocating some money to both XOP and SRUUF at current prices. But please know they aren’t going to go straight up. We should plan to hold these investments for several years as the energy renaissance plays out.

Then if we want to super-charge our energy investments, we need to know the secret of master limited partnerships (MLPs). These are often called “energy royalty” companies.

The Most Efficient Energy Investments

A gentleman by the name of T. Boone Pickens created the first publicly traded MLP back in 1979.

If his name sounds familiar, Pickens is an absolute legend in the energy space. He’s also well respected out in Oklahoma. Oklahoma State University’s football stadium is named Boone Pickens Stadium in his honor.

Boone, as his friends called him, had a brilliant insight. He realized that if he could move the income from his oil & gas production sites to a separate entity, his company Mesa Petroleum wouldn’t have to pay corporate taxes on that money going forward.

So Boone took the assets of his company’s huge oil and gas fields in Colorado, Kansas, New Mexico, and Wyoming and spun them off into a new entity called Mesa Royalty Trust.

But he didn’t set up Mesa Royalty as a new corporation. He structured it as a master limited partnership.

Doing this gave Boone the ability to manufacture stable, predictable cash flows in what has always been a highly volatile industry. I’ll explain…

Oil and gas production sites can cost billions of dollars to develop. Then once they are up and running, it typically costs between $5 and $20 per barrel of oil equivalent (boe) to maintain these sites.

Those expenses are relatively stable year after year. That makes them predictable.

The problem is that an oil & gas development company’s income is not predictable. Because it is tied to the market price of the underlying commodities.

When the price of oil and gas goes up, these companies make a killing. But revenue falls dramatically when commodity prices drop.

And as we know, many political and geopolitical factors impact the price of oil. These are factors completely outside of the industry’s control.

So Boone identified two problems back in the 1970s. Both are true of all oil & gas development companies…

Boone realized that if he left the income in Mesa Petroleum, he would be on the hook for massive corporate tax bills. Especially during commodity booms.

And when commodity prices fell, Mesa Petroleum’s cash flows would plummet. That would make it hard to pay out consistently high dividends. Thus, the market would likely punish the stock price.

The master limited partnership structure solves both of these problems.

MLPs are pass-through entities. They aren’t subject to corporate taxes.

And if an oil & gas development company transfers its logistical infrastructure to a MLP – it’s pipelines, storage, and processing facilities – it can shift as much of its revenue to the MLP as it wants.

The development companies do this by paying the MLP fixed fees for transporting and storing their oil & gas. This reduces the development company’s net income, thus bypassing corporate taxes. And it creates consistent, predictable, tax-advantaged income for the MLP.

That allows the MLP to pay higher distributions (similar to dividends) to investors. And the best MLPs can raise their distributions over time thanks to their stable income. The market loves that.

And here’s the kicker – the oil & gas development companies often maintain a controlling ownership interest in the MLPs they create.

This ensures the two entities are aligned on operational matters. It also aligns the company’s interest with that of investors… because they are large investors in the MLP as well.

It’s brilliant. Everybody wins.

And for investors, owning the best MLPs allows us to build exposure to the coming energy renaissance and collect massive distributions at the same time. We can reinvest these distributions right back into the MLP to put the power of compounding interest on our side.

The key is, we only want to own the best MLPs. Not all are created equal.

To identify the cream of the crop, we need to analyze five key metrics. They are:

Free Cash Flow (FCF) MarginReturn on Equity (ROE)Return on Invested Capital (ROIC)Price to Distributable Cash Flow (P/DCF)Enterprise Value to EBITDAThese metrics allow us to assess a MLP’s performance relative to others in the industry.

They also inform our valuation analysis. As with any investment, we must buy at the right price if we want to make money.

Friends, the energy renaissance is coming.

Funds like XOP and SRUUF are simple ways we can get ahead of it today. Then we can use energy legend Boone Pickens’ great MLP innovation to kick our energy returns into hyperdrive in the years to come.

-Joe Withrow

P.S. We are actively tracking these themes inside our investment membership The Phoenician League. We take this insight and help members build a robust investment portfolio with specific suggestions.

If you’d like to learn more about what we’re doing and why we’re doing it, you can get more information at: https://phoenicianleague.com/secret

The post The Secret of Energy Royalties first appeared on Zenconomics.

The post The Secret of Energy Royalties appeared first on Zenconomics.

November 2, 2023

Your only two choices

You have two choices when it comes to investing. You can own currency. Or you can own energy.

If you don’t trust the currency, you better own energy. But how you choose to own that energy is what will determine your success or failure in the markets.

This old-world wisdom comes from an investing legend. I chatted with this gentleman at an investment mastermind back in the summer… and I think we arrived at a fundamental truth.

Energy is the master economic resource.

Think about it… nothing happens without energy. Everything we see in our modern world today – and everything we use on a daily basis – is only possible because of energy.

It’s a simple thing. But if we truly ponder it, it changes our perspective.

My investment philosophy is this: I want to own energy in the most advantageous way I can. If we start there, all we need to do is figure out what form that energy should take.

The ESG Revolution

Of course, the Environmental, Social, and Governance (ESG) movement would have us believe that we should own energy in the form of solar and windmills.

They told us that we’re rapidly moving towards a “carbon-neutral”, “net-zero emission” world. And in that world, we would reduce our dependance on fossil fuels—namely oil, natural gas, and coal.

Countless “clean energy” exchange traded funds (ETFs) popped up in recent years to support this theme. ESG investing became a hot trend.

And Larry Fink, CEO of investment management giant BlackRock, paraded around in media appearances proclaiming the gospel of ESG.

But then reality set in.

When it comes to energy production, energy density is everything. Energy density simply measures the amount of energy stored in a given fuel source per unit volume or mass.

Uranium (for nuclear power), oil, natural gas, and coal are incredibly dense fuel sources. I listed them in order of most dense to least dense.

When it comes to solar and wind power – we can’t measure their energy density. Because they aren’t fuels. Their power output depends on whether the sun is shining and the wind is blowing.

That means their power production is intermittent. It’s not constant. And even at peak production solar and wind produce far less power than our traditional fuel sources.

So it’s no surprise what happened when countries transitioned a portion of their power production to solar and wind. Energy production plummeted… which caused electricity prices to skyrocket.

In Germany, electricity costs hit an all-time high in August of last year. At the peak, electricity costs had risen by a factor of 10.

And it’s not just Germany. Denmark, Spain, Australia, California, and the United Kingdom (UK) have each seen power costs rise as a result of the ESG push.

The evidence is in.

We just can’t run our economy on solar and wind power. And people don’t like it when their power bill blows through the roof. That’s why we’re finally seeing a backlash against ESG.

The Energy Renaissance Has Begun

This summer Larry Fink had to go on television and walk back his position. He said he was ashamed of being part of the ESG conversation. And now he doesn’t want to use the term anymore.

At the same time, JP Morgan CEO Jamie Dimon is actively calling for greater investment in oil & gas. And we’re seeing a renewed focus on nuclear power as well.

If we’re serious about owning energy in the most advantageous way possible, we need to be paying attention here.

We are at the beginning of an energy renaissance in the western world. And it’s going to be big.

We’ve shifted so much investment towards solar and wind in recent years, and that’s curtailed the production and thus supply of traditional energy sources.

And that’s not an exaggeration.

According to Bloomberg, nearly $2.2 trillion has poured into the development of renewable energy since 2016, with solar and wind power receiving the bulk of that investment.

A large portion of those investment dollars will flood back into traditional energy development in the years ahead. But only after the world realizes that ESG has been a false promise, and the price of oil, natural gas, and uranium each spike.

That’s the renaissance. We need to get ahead of it by building exposure to both the oil & gas industry as well as uranium for nuclear power production.

I’ll share with you the best ways to do so next week.

-Joe Withrow

P.S. For a more detailed look at the geopolitical side of the battle between ESG and traditional energy, check out my new book Beyond the Nest Egg. You can find it on Amazon right here.

The post Your only two choices first appeared on Zenconomics.

The post Your only two choices appeared first on Zenconomics.

November 1, 2023

The Fed’s Best Friend

The Federal Reserve and other central banks risk pushing the global economy into recession followed by prolonged stagnation if they keep raising interest rates.

The United Nations (UN) issued that statement in a report published on October 3, 2022.

The Federal Reserve (the Fed) had already raised its target interest rate five times by then, starting in March. Those hikes pushed the Federal Funds Rate – the rate at which banks lend to each other – from 0.25% to 3.25%.

So the Fed pushed its target rate 13 times higher in the span of less than seven months.

The UN publicly stated that this was an “imprudent gamble”. And many investors joined the chorus. They cursed the Fed up and down because these moves caused the S&P 500 to plunge 15.6%. Many individual stocks fell even harder.

The wailing and gnashing of teeth came from all directions. Except one.

The Fed’s bold moves had one industry smiling profusely. But nobody noticed… because nobody had paid much attention to this industry for years.

Well, it’s time to take notice. This one industry will benefit from the Fed’s rate hikes more than any other.

We’re talking about world-class property and casualty (P&C) insurance.

To understand why P&C companies will do so well in the coming years, we have to understand the business. It sounds boring… but there’s magic hidden within the nuances.

Believe it or not, property and casualty insurance is one of the best businesses in the world. I’ll explain…

P&C is about insuring against property damage and potential casualties. These are uncertain events that may never happen. But if they do, it could be catastrophic for the companies (or individuals) involved.

Therefore, we all buy P&C insurance.

As individuals, this is our homeowners insurance and our car insurance. We buy it and hope we never have to use it.

And the actuarial data shows that we’ll probably get our wish. As tragic as they are, car crashes impact very few people. And it’s even less frequent that somebody’s home burns down.

So the beauty of this business model is that the insurance company gets paid on every policy before it pays any claims. Even better, it may neverhave to pay a claim for a given policy.

If our home doesn’t burn down, the insurance company gets our money without doing anything for us. Same goes if we don’t wreck our car.

This is the exact opposite dynamic from what exists in most other businesses. Most companies need to provide goods and services first. Then they get paid afterwards.

And here’s why this is so powerful…

Insurance companies get to invest the premiums they receive right away. This allows them to constantly grow what’s called “the float”. The float is the difference between premiums collected and the amount of money set aside to satisfy claims.

In other words, the insurance company doesn’t only make money by selling policies. The good companies also make money by investing policy premiums well.

This dynamic is true for all insurance companies. But it’s especially powerful with P&C insurance.

That’s because property and casualty events aren’t frequent. Many policies may never file a claim.

The life insurance industry just doesn’t have the same luxury. Eventually every life insurance policy comes due.

And that’s why blue-chip P&C insurance companies are powerful investment vehicles. They safely compound returns for investors year after year. The best insurance companies essentially print money for their shareholders.

And that’s the key—we only want to invest in the world-class insurance companies. We want to own the best of the best.

That is to say, we are only interested in those companies who underwrite and price their policies well… and have a great track record of growing their float and generating investment income.

Underwriting is the process by which insurance companies evaluate and analyze the risks involved in insuring people and assets. This process determines what an insurance company is willing to insure and at what price.

And they have this down to a science. The top insurance companies know exactly what they are doing.

We have specific analytical metrics we use to determine just how good a company is at underwriting. Looking at these metrics over time paints the picture clear as day – the best companies do a great job at underwriting year after year.

If that’s the case, the other item we need to assess is investment income. How good is a given company at managing its investments and generating additional income?

The better a company is at this, the bigger dividends it can pay investors.

And this is why the P&C industry was beaming when the Fed aggressively raised rates last year. These companies invest primarily in bonds, money market funds, and mortgages—instruments that pay a yield based on interest rates.

So when rates go up, the P&C industry can earn more money on its investments. The higher rates go, the higher the yield. And that means more investment income.

And it’s already happening.

One of my favorite P&C companies just reported its third quarter earnings results. Its net investment income spiked 59.3% year-on-year. And the CEO explicitly said this was due to rising interest rates. Then he added that he expects this trend to continue.

I imagine this CEO thinks pretty highly of the Fed right now. Mr. Powell has at least one friend in the private sector.

And here’s the kicker – the property and casualty industry is largely recession proof.

This industry is resilient… for a simple reason. P&C companies service needs, not wants. Their customers need their products.

Think about it this way – do we cancel our homeowners or car insurance when we want to cut our spending? Nope. Because we can’t.

It’s the same dynamic on the enterprise side.

Large corporations need to insure their buildings, equipment, vehicles, and any other property deemed critical to business operations. They also need liability insurance to protect them from lawsuits. And then US regulations say they must also buy workers’ compensation insurance (workers’ comp) for their employees.

So here we have an industry that’s set to grow its profits and its dividends in the years to come thanks to normalized interest rates… and its products will remain in high demand even during the coming recession. What’s not to love?

The key is to only buy the best companies at the right valuation… and then let them run.

If we do, these world-class insurance companies will print money for us quarter after quarter. Especially if we automatically reinvest our dividends. That’s how we leverage the power of compounding interest.

When it comes to portfolio construction, I think it’s wise to allocate at least 10% of our portfolio into the World-Class Insurance bucket. And I would be comfortable going as high as 15% over time.

There’s a reason why Warren Buffett built his business on the back of world-class insurance. Let’s do the same…

-Joe Withrow

P.S. Are you ready to master your finances and inflation-proof your money? Our Finance for Freedom program will show you how. More information right here.

The post The Fed’s Best Friend first appeared on Zenconomics.

The post The Fed’s Best Friend appeared first on Zenconomics.

October 31, 2023

It’s time

It’s time.

If we want to secure our finances and live a comfortable lifestyle, it’s time to bulletproof our money. We can’t put it off any longer.

As we’ve been discussing, the Age of Paper Wealth is over.

From 1982 to 2022 interest rates always went down and stocks always went up. That made investing easy. All you had to do was buy some growth stocks and come back in five years… your account would be up.

Those days are over.

If we want to make money in the markets today, we must focus on five core investment themes. They are:

Reserve AssetsWorld-Class InsuranceEnergy RenaissanceGold EquitiesConsumer Goods Inflation HedgesWe need to spread our money out across these five asset classes, each for a different reason. But they are complimentary. And together they will make our money bulletproof.

Let’s talk about reserve assets today. Then we’ll dive into the others the rest of this week.

Reserve assets are assets that will maintain their value over long periods of time. These are assets we should routinely accumulate regardless of their spot price… and then never sell.

The two primary reserve assets are physical gold and Bitcoin.

They both serve the same purpose within a properly constructed asset portfolio. But there are some nuances that differentiate the two.

When I talk about physical gold, I’m referring to standardized coins and bars that derive their value from the weight of gold they contain.

Gold is often lumped into the “precious metals” category along with silver. But at this juncture I far prefer gold to silver. That’s because silver has become more of an industrial metal. It’s used widely in every consumer electronics device out there.

Meanwhile, every major central bank in the world holds gold on its balance sheet. And many central banks have been buying gold hand-over-fist in recent years. It’s truly a monetary metal.

The beautiful thing about gold is that it’s one of the few assets that’s not also someone else’s liability. In financial lingo, gold has no counterparty risk. When we own physical gold, we are not reliant on another party to honor its contractual obligations to us.

This is not the case with cash in a bank or securities held at a brokerage.

With those assets, we rely on the bank or the company we’ve invested in to be honest and stay solvent. As people who banked with Silicon Valley Bank (SVB), Signature Bank, and First Republic found out earlier this year – it’s not pleasant wondering if your assets are safe after your bank just failed.

This is why I see gold as the cornerstone of my asset portfolio. With gold I know that I’ll always have a store of value available to me no matter what happens out there.

And make no mistake about it, there is a liquid market for physical gold in the US and every major country on this planet.

Buying and selling physical gold is simple. You just have to know where to find the good gold dealers. Then you build a relationship with them.

As for Bitcoin – it is both a payment network and a currency wrapped into one. Perhaps this doesn’t sound too important on the surface… but let’s think about it a minute.

To my knowledge there has never in history been a payment network that also supplied its own independent currency.

Instead, we’ve seen all kinds of currencies come and go over time. And we’ve also seen many different payment networks arise – especially since the internet came about.

Think about the US dollar. It is the de facto reserve currency of the world… at least for now. But how do you spend dollars?

Well, if you have physical cash, you just hand your dirty paper notes to somebody in exchange for the goods and services you want.

But what about credit card payments? Those require payment networks like those built by Visa, MasterCard, or American Express.

And then there’s online and mobile payments. We’ve got networks like PayPal, Venmo, Square, Stripe, and others.

And what about cross-border transactions? You’ve got to go through something like Western Union or MoneyGram. Or, if you’re a bank or financial institution, you have to use the SWIFT system.

The point is there are all kinds of disparate payment networks designed to get dollars from one person or account to another.

With Bitcoin, it’s much more simple. Bitcoin is the payment network. And bitcoins are the currency.

Notice how I capitalize the ‘B’ in Bitcoin when I refer to the network. And I use the lowercase ‘b’ when I refer to the currency. That’s the proper way of doing it… I don’t care what the Associated Press says.

Here’s the thing – Bitcoin’s real value is in the network.

The Bitcoin network is not owned or controlled by any corporation, government, individual, or group of individuals.

Instead, it’s governed entirely by open source computer code. We know exactly what the code says. That’s the beauty of this.

Thus, we know exactly how many bitcoins are in circulation at any given time. We also know that there will only be 21 million bitcoins ever created. And we know that the very last bitcoin will be mined in the year 2140.

This level of transparency puts everybody on an even playing field. There are no insiders in the world of Bitcoin.

By the way – 19.5 of those 21 million bitcoins are now in circulation. That means 93% of all the bitcoins that will ever exist are already here. We’re going to spend the next 117 years mining the last 7%.

That shows you just how scarce this asset is.

Now think about this – close to 70% of all bitcoins in circulation have not moved in the last twelve months.

Those in the know are accumulating. Because at some point our society will consist of two kinds of people – those who hold bitcoins and those who don’t. That’s how scarce this thing is.

And that’s exactly what we should be doing too—with both gold and Bitcoin. These reserve assets need to be the cornerstone of our asset portfolio.

When it comes to portfolio construction, I think it’s wise to move 5-10% of our assets into gold and 5-20% into Bitcoin. Then we can go into accumulation mode.

For Bitcoin, I buy a little more every Monday morning. Like clockwork.

For gold, I pick up a few more ounces every year around the holidays. I make them a Christmas present to my children, and I attach a nice dated note to the box.

The note says that I love them and I’m excited for them… but they better not sell this friggin’ coin if something happens to me.

Reserve assets are forever.

-Joe Withrow

P.S. If buying and never selling sounds boring—don’t worry. The rest of this week we’ll talk about the asset classes that will do quite well in the years ahead.

And if you’d like a holistic view on how it all fits together, check out my new book Beyond the Nest Egg. You can find it on Amazon right here.

The post It’s time first appeared on Zenconomics.

The post It’s time appeared first on Zenconomics.

October 30, 2023

We’re in for a bumpy ride…

The macroeconomic front is starting to get quite complicated.

Under the surface, there’s a covert financial war raging. It pits the globalist power structure and their “Great Reset” against the New York banking faction who want to save the legacy financial system.

At the same time we have a war in Eastern Europe… and now a war in the Levant. And various factions are trying hard to escalate them into something much bigger.

And if that weren’t chaotic enough, we’re at the very beginning of a massive liquidation of all the malinvestment that’s formed since the world’s top central banks collaborated in 2008 to drop their key interest rates to zero. The economy is about to cleanse itself of the uneconomical projects and zombie companies that produce too little value to be profitable.

Put it all together and there’s only one thing we can conclude for certain. We’re in for a bumpy ride.

We can see evidence of this if we assess the most recent quarterly earnings reports from two of America’s largest banks – JP Morgan and Bank of America.

I found these reports especially interesting because JP Morgan appears to be the de facto leader of the New York banking faction. Meanwhile, Bank of America is firmly in the globalist camp. They now talk about the implementation of “stakeholder capitalism” (the Great Reset) in the bank’s annual reports.

And the way each bank presented its earnings release signals that this is a case of dueling banks. And dueling agendas.

JP Morgan reported revenue growth of 21%. And the bank’s quarterly profit surged 35%. These are huge moves for such a large bank.

And this performance was driven by strong growth in net interest income. This is the difference between how much the bank receives from loans and how much it pays out on deposits—which is every bank’s core business.

As for Bank of America, it declared its best quarterly results in over ten years thanks largely to soaring “stock-trading revenue”. It’s right there in the headline:

This is curious.

At some point we each made a conscious decision regarding who we bank with. When considering our options, did any of us think, “hmm, I wonder which bank is going to trade stocks the best”?

Of course not.

We don’t want our bank trading stocks. That’s how banks get in trouble—being aggressive with the funds they are trusted to custody on behalf of depositors.

So why is Bank of America featuring its trading gains in its quarterly earnings report?

There’s an old saying in the banking industry. Good banks are focused on the 3-6-3 rule. It says if you want to be successful in the business, you pay 3% on deposits, you lend money out at 6%, and then you’re on the golf course by 3 p.m.

That’s sound banking in a nutshell. It’s all about net interest income. Nice and simple.

That is, as long as you manage your other costs.

In the banking world, these are called non-interest expenses. They consist of personnel costs (salaries), occupancy expenses, equipment leases, marketing costs, and professional fees.

Now, if we dig into the numbers buried in Bank of America’s earnings release, it generated $14.4 billion in net interest income—that’s its core business.

So far, so good.

But Bank of America’s non-interest expense was $15.8 billion. That means its operational costs exceeded the income from its core business.

If we compare that to JP Morgan – it generated $22.9 billion in net interest income. And its non-interest expense was just $3.1 billion.

It’s night and day.

JP Morgan’s business is doing great. Bank of America’s is not. That’s why it had to book stock-trading gains to make the bank’s quarterly numbers look okay.

What’s more, Bank of America reported unrealized losses in its bond portfolio of $131 billion. That’s largely because it bought over $200 billion worth of US Treasury bonds in 2020 when the 10-year Treasury rate hit all-time lows below 1%.

For context, the bank only purchased $30.4 billion worth of Treasuries in 2019 – when the yield it could have received was much higher. 10-year Treasuries yielded an average of 2.1% throughout 2019.

Remember, the value of a bond moves inverse to interest rates. When rates go up, bond prices go down.

In 2020, 10-year Treasuries paid an average of 0.89%. Today, the 10-year yields 4.8%.

The temptation here is to subtract one from the other and say that rates are up 3.91%… but that’s not correct. The 10-year Treasury now yields 439% more than it did in 2020. The calculation is: ((4.8%-0.89%)/0.89%).

So Bank of America effectively made one of the worst investments in history.

And why did it buy all those bonds yielding less than 1% in 2020?

Well, Bank of America first started talking up stakeholder capitalism that year. This refers to the system that the “Great Reset” seeks to impose upon us.

At the time, the Covid hysteria gave the globalist plot a tremendous window of opportunity. And the Biden administration here in the US made moves to implement it. That’s what lockdowns, contact tracing, and vaccine passports were all about.

It certainly looks like Bank of America upped its Treasury purchases in 2020 to help support the push for the Great Reset agenda amidst the Covid chaos.

They’ll never admit that, of course. But why else would they increase their Treasury purchases nearly 7x to earn less than 1%? Especially when they could have earned over 2% on the same investments just the year before…?

This is why I call Bank of America “King Globalist” among the US banks. The bank sacrificed its own fiscal health for the sake of the agenda.

The bottom line here is that Bank of America is not in great shape. But they are trying very hard to make the bank look good because they are desperate to maintain appearances.

Bank of America can’t afford to give ground to the top New York banks like JP Morgan. It’s not just bank versus bank. The struggle is really the Great Reset versus saving the legacy financial system.

And notice how the commentary from JP Morgan CEO Jamie Dimon was drastically different from that of Bank of America CEO Brian Moynihan.

Here’s Dimon:

“The war in Ukraine compounded by last week’s attacks on Israel may have far-reaching impacts on energy and food markets, global trade, and geopolitical relationships… This may be the most dangerous time the world has seen in decades. While we hope for the best, we prepare the firm for a broad range of outcomes.”

Meanwhile, Moynihan said that we’re in a “healthy but slowing economy”. No warnings. No caution. Just fluff.

By the way, I worked in Bank of America’s Special Assets Group (SAG) for several years. I didn’t realize it then, but it was all an operation to roll up America’s mid-market regional banks into the behemoth that Bank of America became.

As part of the SAG team, I was on Moynihan’s quarterly strategy calls. I’ve never heard somebody say so many words but convey so little meaning. The guy is a master of deception.

So my takeaway here is that the New York banking faction has the upper hand in its financial battle with the globalists. The Great Reset agenda has taken a major step backwards.

But that doesn’t mean the economy is in the clear.

The current administration in the US made it clear that they are happy to support both the war in the Ukraine and the war in the Middle East. Treasury Secretary Janet Yellen even went on record saying that the US can afford to do so.

Of course, it’s always those of us in the private sector who pay for wars and deficit financing—either through taxes or inflation, or both.

And wars on multiple fronts guarantees that we’ll see oil prices rise… which will put even more of a strain on the middle class and the domestic economy.

So I think it’s time to buckle up.

The next several years will be difficult for a lot of people. But that doesn’t mean we need to liquidate everything and hide in the basement.

If we look at history and read some eye-witness accounts, most people’s daily lives didn’t change too much through times of trouble—even through periods of war and chaos.

Most people got up and went to work each morning just like they always had. The local economies did their best to keep things going. And the financial markets continued to chop along.

I mention that because I don’t want this to be a message of doom and fear.

If we focus our investments in the right places – if we make our money bulletproof – we’re going to do fine in the years to come.

As I mentioned on Thursday, the areas we need to focus on are as follows: