Joe Withrow's Blog, page 11

October 26, 2023

How to Make Your Money Bulletproof

Are you here to make money? Or are you here just to play the game?

This important question comes from Adam Smith’s book The Money Game. It was published in 1967—before The Age of Paper Wealth even began.

The Age of Paper Wealth refers to the time from 1982 to 2022. It was a time when interest rates only went down… and stocks only went up.

As we discussed yesterday, investing was easy in that climate. All you had to do was buy some growth stocks and then forget about them. If you checked back in on your account five or ten years later, it was guaranteed to be up.

Those days are over.

And if you’re here to make money – not simply play the game – there are some important moves you need to make.

Look, investing is simple. If you do it right.

I’ve talked to many people who see the stock market as a casino. Of those, many think it’s a rigged game.

And I agree 100%… if you ignore the factors that determine the outcome of any single investment.

I know plenty of people who buy stocks based on “tips” or “intel”.

They’ve heard that a new law or regulation is coming that will catapult a small company’s shares higher.

Or they’ve heard that a company is about to announce a new product that’s going to be revolutionary, thus now’s the time to get in.

Or they’ve heard that some little company is about to ink a major deal with Apple or another giant company, and that’s going to send the stock soaring.

If that’s your framework, you’re not investing—you’re gambling.

Then there’s the other side of the coin…

I also know plenty of people who simply herd their money into their 401k funds because they are “diversified”. Those same folks might venture out into the world of exchange traded funds (ETFs) as well, for the same reason.

That’s also gambling… because you have no control over what those funds buy, sell, and hold. And the fund managers make their money regardless of what their performance looks like.

So what are the factors that determine the outcome of any stock investment?

Time, compounding, and valuation. That’s all we need to focus on.

When it comes to the first – time – the question we need to answer is this: How long can we safely hold a given stock?

Of course, there’s no simple answer to this question. It requires some deep analysis of the company and the industry it’s in, as well as educated projections regarding macroeconomic trends.

But that’s the business we’re in. That’s our job. And we love doing it.

The second factor is compounding.

Apparently Einstein said that compound interest is the eighth wonder of the world. I don’t know if he actually said that. But the second part of the quote attributed to him is correct:

He who understands it (compound interest), earns it. He who doesn’t… pays it.

Compound interest refers to earning interest on your interest over time. Your money makes money… and then that new money makes more money. And so it goes…

When it comes to stocks, the question we need to ask is: How much can we expect a stock to compound each year over our safe holding period?

Well, it all comes down to the dividend yield.

The key is to anchor our portfolio with stocks that pay a strong dividend – and will continue to pay a strong dividend for years to come. Then we have our broker automatically reinvest those dividends right back into the stock for us. At least for as long as the stock is fairly valued.

This grows the number of shares we own every quarter… which increases our dividends… which grows our share count even faster. That’s how we earn compound interest.

But let’s not forget the third factor. Valuation. It’s the most important.

For every investment we make, we must ask: At what valuation can I safely buy this stock?

Notice I didn’t say price. A stock’s share price is meaningless. It doesn’t convey any useful information to us.

Think of it this way – there are “cheap” stocks priced at over $200 per share today. Those stocks will do well going forward. At the same time, there are “expensive” stocks priced under $10 per share today. They will perform poorly going forward.

Don’t be misled by share price. It’s the valuation that matters.

What’s the stock’s enterprise value relative to the company’s sales? How about its earnings? And how does that valuation compare to the key performance metrics for companies in that industry?

If we build a portfolio of companies that will safely compound for us for years, maybe decades to come… And if we only buy these companies when they are trading at attractive valuations, we’ll wind up with a bulletproof portfolio that increases in value every year—regardless of what else happens in the world.

Simple as that.

But I know I haven’t fulfilled on my promise from yesterday. I said that if you want to make money in the market, you’ll need to overhaul your portfolio. How do you do that?

I’m glad you asked…

Bulletproof Your Money

I’m writing this on October 26, 2023. This isn’t evergreen advice… because those three factors we mentioned earlier are constantly changing.

But as of today, there are five “buckets” you need to move your money into. We can think of these as our investment themes. They are as follows:

Reserve Assets World-Class Insurance Energy Renaissance Gold Equities Consumer Goods Inflation HedgesIf we only invest in these five core themes, our portfolio will do very well in the years to come.

But remember, we must do our homework before investing in any stock. And most importantly, we can only buy at attractive valuations. That’s key.

We’ll break down each of these asset classes next week.

-Joe Withrow

The post How to Make Your Money Bulletproof first appeared on Zenconomics.

The post How to Make Your Money Bulletproof appeared first on Zenconomics.

October 25, 2023

It’s a new era in the markets…

The investing game just changed.

A gentleman writing under the pen name Adam Smith wrote a book called The Money Game back in 1967.

Smith put forth the idea that investing in the stock market is an exercise in mass psychology. He pointed out that most investors have no clue how to value stocks… thus, they are not likely to ever make any money in the market.

But that’s okay. Because according to Smith, they aren’t there to make money. They just want to play the game. If you understand that, you’ll realize that the mood is what drives everything.

And Smith pointed out that greed and fear are the two primary emotions in the market. At any given time one of them is likely to be in the driver’s seat.

It’s a great read. But it concludes rather curiously.

Smith wrapped up the book by talking about the prophets of doom. He called them the Gnomes of Zurich.

These are the people who constantly think the market is about to crash and the game is about to end. Many of the early pioneers in the financial newsletter industry fit that bill.

The problem with the doomsday prophet is that he always imposes his bias upon his forecasts. And he brings morality into the picture.

But just because something is wrong… and just because something can’t last forever… doesn’t mean its end is imminent.

That’s why so many editors in this business got burned trying to call the top at one point or another. They didn’t wait for the signal. They didn’t let the data tell them when the jig was up.

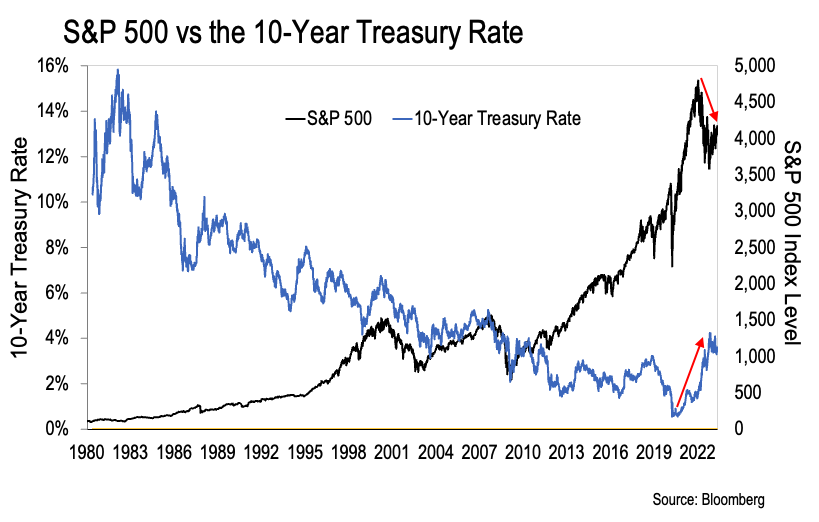

Well, we now have that signal. This chart tells the story:

Here we can see the S&P 500 and the 10-year Treasury rate going back to 1980. The S&P 500 is the black line. And the 10-year Treasury rate is the blue line.

We’re using the S&P 500 as a proxy for US stock prices. And we’re using the 10-year Treasury as a proxy for interest rates. This chart makes it perfectly clear that the two are inversely correlated.

Interest rates started falling in 1982, and they fell consistently for the next 40 years. Meanwhile, US stocks consistently went up in value over that same time period.

But everything reversed in 2022. Rates started going up, and stock prices started to fall. We can see those moves clearly marked by the red arrows on the chart above.

When we zoom out like this, it’s no surprise that stocks fell hard when rates started to rise in 2022. But it sure caught a lot of people by surprise.

In fact, many financial analysts spent months trying to convince themselves and their clients that these moves were temporary. Just wait for the Fed to pivot, they said. Then we’ll get back to normal.

But here’s the thing—what happened from 1982 to 2022 was not normal. Nor was it organic.

Instead, it was all driven by the debasement of our money.

The US government and the Federal Reserve (the Fed) worked hand-in-hand to create over $8 trillion dollars from thin air during this time period. We can verify that $8 trillion because it hit their balance sheet.

There’s also strong evidence that the Fed collaborated with other major central banks to create over $20 trillion off balance sheet in the wake of the 2008 financial crisis. We can’t easily verify this. And at the end of the day it’s not important to do so.

What’s important to understand is what happens next.

End of the Road

Fed Chair Jerome Powell explicitly stated that he intends to kill the “Fed Put”.

This term refers to the fact that the Fed has always stepped in and goosed the markets with cheap money going back to 1987. That cheap money flowed into financial assets, pushing prices higher again.

Those days are over.

That is, if we believe Powell is serious about this.

We can’t ignore the fact that for the last forty years the US government has constantly pressured the Fed to cut interest rates and pump cheap money into the system. And since Paul Volker resigned in 1987, every single Fed Chair has succumbed to this pressure.

Will Powell resist? Danielle DiMartino Booth suggests that he will indeed.

Booth is both a Wall Street veteran and a Fed insider. She began her career on Wall Street, and then she spent nine years at the Federal Reserve Bank of Dallas. There, she served as an advisor to Dallas Fed President Richard Fisher.

Today DiMartino Booth is the founder and CEO of a research firm called Quill Intelligence. And she still has some connections within the Federal Reserve System. Those connections give her a more nuanced understanding of what’s happening behind closed doors at the Eccles Building.

In a recent interview, Booth made it clear that there tends to be a bureaucratic echo chamber at the lower levels of the Fed. Here’s what that means…

We see the Fed Chair when they go on television and when they are quoted in news articles. But what we don’t see is the underlying team of people who feed research and analysis to the Chair. That team tends to consist primarily of academic researchers.

According to Booth, Powell’s comments on inflation being transitory in 2021 were based on the analysis he received from academic researchers within the Fed.

Obviously that analysis was completely wrong. It left Powell with “egg on his face,” as Booth put it in the interview.

She went on to explain that this incident woke Powell up to the fact that there was an academic echo chamber within the Fed. Ever since then Powell has been looking to “outside” data and analysis to guide his decisions.

Booth didn’t elaborate on this point, but I think it’s a safe assumption to say that this “outside” analysis has come from Powell’s network within the upper echelon of the New York banking scene.

Then Booth pointed out the difference between Powell and his predecessors Janet Yellen and Ben Bernanke.

I’m reading between the lines a little bit here, but Booth seemingly suggested that Bernanke was something of an “empty suit” academic. She didn’t use those exact words, of course. But she implied that he simply went along with whatever academic research was popular at the time.

Booth also implied that Yellen, while purely an academic, is also something of an idealogue.

Yellen fancies herself as a globalist progressive. She fervently believes that the global elite know what’s best when it comes to how to manage society and keep the common folk in line. Those are my words, but Booth’s comments seem to support that idea.

Jerome Powell’s different. He’s not an academic. He’s a Wall Street veteran. He has direct experience in the financial markets. And he built a net worth in excess of $100 million.

That also sets him apart from Bernanke and Yellen. They both made their money after becoming Fed Chair.

So, we should ask the important question: what motivates Jerome Powell? What are his incentives?

For Bernanke and Yellen, they knew they would get paid handsomely if they did what the establishment wanted them to do. Book deals… six and seven figure speaking fees… overpriced consultations—there are plenty of ways to reward lackeys for good behavior.

But Powell doesn’t need their money. So, what’s he after here?

Booth offered her opinion directly. She thinks that Powell sees himself as serving his country.

She also explained that Powell was very critical of the Fed’s prolonged zero-bound interest rate policy. He tried to warn Fed officials that the longer they kept rates at zero, the harder it would be to unwind that policy.

If we look at what Powell’s said and what he’s done since 2022 – it all matches up.

Powell is dead set on normalizing interest rates and allowing a massive recession to come. He’s even talked about the need to clear the economy of a decade’s worth of malinvestment. It’s almost like he’s been reading the great Austrian economists recently…

So what’s it mean for investors?

Friends, we’re at the end of the road. We’re entering a new era.

For the last forty years the Fed has forced interest rates lower to juice the markets. Nobody under the age of 60 has been an adult in a world where interest rates didn’t constantly fall.

In that world, all you had to do to make money was buy some growth stocks and let them sit for years, maybe decades.

That’s not the play going forward.

It all comes down to what Adam Smith talked about in his great book. Are you here to make money? Or are you here just to play the game?

If you’re here to play the game, just keep doing what you’re doing. The next few years promise to be exhilarating.

But if you’re here to make money, you’ll need to completely overhaul your portfolio. I’ll tell you how tomorrow…

-Joe Withrow

P.S. For a much deeper dive into what’s playing out in the markets and the economy today, check out my new book. It’s titled Beyond the Nest Egg, How to Be Financially Independent Outside of a Broken System.

You can find it right here.

The post It’s a new era in the markets… first appeared on Zenconomics.

The post It’s a new era in the markets… appeared first on Zenconomics.

October 24, 2023

The three keys to a bulletproof portfolio

Investing in stocks is a simple game.

That was the subject of yesterday’s letter. And the reason is simple. There are only three variables that control the outcome of any stock investment. This is true regardless of the economic climate.

The first variable is time. How long will we be able to safely hold a given stock?

Of course, there’s no simple answer to this question. It requires some deep analysis of the company and the industry it’s in, as well as educated projections regarding macroeconomic trends.

But for certain companies, it’s not that difficult. Take a capital-efficient consumer goods company like Hershey or Domino’s Pizza, for example.

Do you think people will still be buying cheap chocolate loaded with sugar thirty years from now? Do you think they’ll be buying cheap pizzas delivered on time right to their door for decades to come?

I do. Therefore we could safely hold those companies for at least thirty years… if the other two variables line up for us.

And that brings us to the second variable. It relates to compounding.

Apparently Einstein said that compound interest is the eighth wonder of the world. I don’t know if he actually said that. But the second part of the quote attributed to him is correct:

He who understands it (compound interest), earns it. He who doesn’t… pays it.

Compound interest refers to earning interest on your interest over time. Your money makes money… and then that new money makes more money. And so it goes…

When it comes to stocks, the question we need to ask is: How much can we expect a stock to compound each year over our safe holding period?

Well, it all comes down to the dividend yield.

The key is to only invest in stocks that pay a strong dividend – and will continue to pay a strong dividend for years to come. Then we have our broker automatically reinvest those dividends right back into the stock for us.

This grows the number of shares we own every quarter… which increases our dividends… which grows our share count even faster. That’s how we earn compound interest.

But let’s not forget about the third variable. It’s the most important one.

Valuation. At what valuation can I safely buy this stock?

Notice I didn’t say price. A stock’s share price is meaningless. It doesn’t convey any useful information to us.

Think of it this way – there are “cheap” stocks priced at over $200 per share today. Those stocks will do well going forward. At the same time, there are “expensive” stocks priced under $10 per share today. They will perform poorly going forward.

Don’t be misled by share price. It’s the valuation that matters.

What’s the stock’s enterprise value relative to the company’s sales? How about its earnings? And how does that valuation compare to the key performance metrics for companies in that industry?

If we build a portfolio of companies that will safely compound for us for years, maybe decades to come… And if we only buy these companies when they are trading at attractive valuations, we’ll wind up with a bulletproof portfolio that increases in value every year—regardless of what else happens in the world.

Simple as that. More to come tomorrow…

-Joe Withrow

P.S. Speaking of what’s happening in the world… it’s getting interesting out there. And dangerous.

For a breakdown of the key macroeconomic trends playing out right now, and who the major players are, check out my new book Beyond the Nest Egg. It’s starting to gain a little traction on Amazon.

You can find it right here: https://www.amazon.com/Beyond-Nest-Egg-Financially-Independent-ebook/dp/B0CG7VYRV7/

The post The three keys to a bulletproof portfolio first appeared on Zenconomics.

The post The three keys to a bulletproof portfolio appeared first on Zenconomics.

October 23, 2023

Investing is a simple game

We hit peak Fall foliage over the weekend.

Our favorite tree erupted with the most intense shades of red and orange. And the mountains surrounding our humble property lit up into a collage of colors as if someone were playing with the old children’s toy Lite-Brite.

It’s hard to beat Autumn in the mountains.

Shifting gears…

Let’s talk about investing this week. And we’ll start with this – investing is critical for anyone who hopes to achieve financial security and then financial independence.

Of course, there are plenty of asset classes for us to choose from. We cover each (and how to invest in them) in our Finance for Freedom program.

But today I want to talk about stocks… for a few reasons.

Chances are you have exposure to stocks already. Maybe it’s through a 401k. You may also have other investment accounts set up.

I want you to know that investing in stocks is a simple game.

I’ve been immersed in the world of investment research for over ten years now… and I’ve learned that there are only three variables that control the outcome of any stock investment.

And that’s true in any environment.

It doesn’t matter what the overall economy is doing. It doesn’t matter if it’s a messy election year. It doesn’t matter if war breaks out in the Middle East. It just doesn’t matter.

I’ve talked to many people who see the stock market as a casino. Of those, many think it’s a rigged game. And I agree 100%… if you ignore these three variables.

I know plenty of people who buy stocks based on “tips” or “intel”.

They’ve heard that a new law or regulation is coming that will catapult a small company’s shares higher. Or they’ve heard that a company is about to announce a new product that’s going to be revolutionary, thus now’s the time to get in. Or they’ve heard that some little company is about to ink a major deal with Apple or another giant company, and that’s going to send the stock soaring.

If that’s your framework, you’re not investing—you’re gambling.

Then there’s the other side of the coin…

I know plenty of people who simply herd their money into their 401k funds because they are “diversified”. Those same folks might venture out into the world of exchange traded funds (ETFs) as well, for the same reason.

That’s also gambling… because you have no control over what those ETFs buy, sell, and hold within the fund.

Again, it all comes down to understanding the three variables that determine the outcome of any stock investment. Once you do, investing in stocks successfully becomes simple. So simple, you won’t believe it.

We’ll break down the three variables tomorrow.

-Joe Withrow

The post Investing is a simple game first appeared on Zenconomics.

The post Investing is a simple game appeared first on Zenconomics.

October 19, 2023

The Sound Money Solution

We’ve been talking all week about inflation and its devastating impact on civil society. It hollows out the middle class and makes long-term business planning nearly impossible.

And it all starts with a lack of understanding around money.

We are all taught to view money as a medium of exchange and a measurement of value. And sure enough, these functions are critical to civil society.

Money is also a communications system. It allows us to put a price on goods and services in the economy. And those prices communicate valuable information to us about the supply of and demand for scarce resources.

For example, when the price of something goes up, that’s a signal that it has become more scarce relative to consumer demands. This prompts entrepreneurs to devise ways to create more supply or alternatives to the good in high demand.

In just the same way, when the price of something goes down, that’s a signal that the item is relatively abundant compared to consumer demand. And this leads firms to produce less of it. That is, until the price rises again.

This communications system allows an economy to coordinate production across time and space. And it does so according to Adam Smith’s old “invisible hand” principle.

This principle says that individuals making their own decisions based on self-interest drives economic growth. The invisible hand guides firms to produce the highest quality goods at reasonable prices.

It’s all about allocating labor and scarce resources to their highest and best use. Doing so creates a strong economy that benefits all of us.

The problem is, inflation distorts this communications system.

Remember, inflation is the act of creating new money from nothing. It is the act of printing currency. This necessarily reduces the purchasing power of all the currency units in circulation.

The result is that prices for everything priced in that currency adjust higher to account for the greater number of currency units in circulation. That’s just basic supply and demand economics.

But this muddies the water.

Now it’s impossible to determine whether an item rising in price is a scarcity signal or inflation at work. And this leads to what economists call “malinvestment”.

Malinvestment refers to bad investments based on distorted information. It occurs when we allocate labor and resources to the wrong places. That puts a drain on the economy and leads to unemployment.

The bottom line is that inflation wrecks everything. Our grocery bill going up is just one small piece of it.

The only solution to this problem is sound money—money that cannot be created from nothing.

Of course, those who control the printing pressed don’t want sound money. As we saw on Tuesday, they have been using inflation to redirect all economic productivity gains to themselves for fifty years now.

So the only thing we can do is implement sound money at the individual level.

We do this by building a robust portfolio of real assets whose value cannot be inflated away. That’s how we bulletproof our money.

Are you ready to implement the sound money solution? Learn how to do so right here.

-Joe Withrow

The post The Sound Money Solution first appeared on Zenconomics.

The post The Sound Money Solution appeared first on Zenconomics.

October 18, 2023

The middle class is under attack

We’re pulling back the curtain on inflation this week… and it’s getting ugly. The middle class is getting wiped out.

And that’s not just an opinion. It’s all in the data. Today I’ve got two tables for you that spell it all out, clear as day.

This table tracks the median price of a new car, ten gallons of gas to put in that car, and five pounds of ground beef going back to 1940.

As we can see, it’s not a pretty picture. Costs have risen dramatically over every ten year period in modern history.

That said, we have to compare these costs to the median income to get a better feel for the story. And that’s what this next table does:

Here we’re tracking the median home price compared to median annual incomes going back to 1940.

And again, we can see that home prices have risen significantly over every ten year period. But incomes have too… so it’s that third line that we need to focus on. It shows us exactly what percentage of the median home the average guy’s salary can cover.

The median home costs $430,300 today. The median annual income is $74,580. That means the average person’s salary can only cover 17% of the median home price.

We can see just how dramatic this is by looking at past data. If we go back to the turn of the century, the median income could cover 33% of the median home price. That’s nearly twice as much.

Then if we go back to 1970—the median salary could cover more than half of the median home price. If that were the case today, the average person would be making $232,362 a year.

What these numbers illustrate is that it has become harder and harder to live a comfortable middle class life in the US. It’s all because inflation has eroded the value of our dollar… thus, costs have risen far faster than incomes.

And as we saw yesterday, there’s an even darker side to this story.

The American economy hasn’t faltered. We’ve increased productivity and output year after year. But those in charge of our monetary system purposefully redirected those productivity gains away from us and to themselves.

The good news is that there are ways to fight back. There are ways to leverage inflation and put it to work for us, not against us.

Our Finance for Freedom program will show you how. More information right here.

-Joe Withrow

The post The middle class is under attack first appeared on Zenconomics.

The post The middle class is under attack appeared first on Zenconomics.

October 17, 2023

War and the middle class

And it begins.

Yesterday we talked about the real threat of war… especially wars on multiple fronts. Now we have confirmation that it’s happening.

The US just committed troops to the Middle East. And US Treasury Secretary Janet Yellen publicly stated that she believes the US can afford to aid the war efforts in both the Ukraine and Israel. By the way, I pulled back the curtain on Yellen’s motivations and her allegiances in my new book Beyond the Nest Egg.

As we discussed yesterday, governments can only finance wars by printing money.

Technically, that means Yellen is right. The US can afford to support both war efforts. They can just create new dollars out of thin air to do so. But this is going to further erode the dollar’s purchasing power… which will drive our cost of living higher and higher.

So ultimately it’s the average person who must pay for these wars. But we don’t pay for them directly. Inflation is a stealth tax that steals our purchasing power away from us.

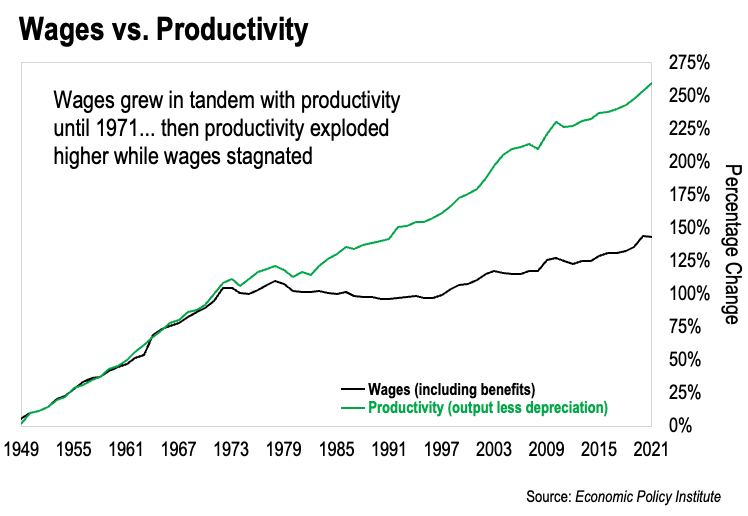

This chart tells the story perfectly:

This comes from the Economic Policy Institute. It tracks the growth of American wages alongside economic productivity increases.

And we can see the two went hand-in-hand up until 1971.

As the economy grew, regular Americans made more money. This is how we created the largest middle class in the history of the world.

But something happened on August 15, 1971 that changed everything. Since then productivity continued to scream higher… but wages stagnated.

That’s inflation at work.

You see, the act of printing dollars steals value from all dollars in circulation. But there’s a trick to it.

Those who get to use the newly printed money first get to do so before consumer prices have adjusted higher for the inflation. In other words, they get to spend new dollars before their purchasing power falls.

This allowed those who control the printing press to redirect nearly all the productivity gains we’ve seen since 1971 to themselves.

So when Yellen talks about financing multiple wars, what she’s really saying is that she is happy to keep this process going. She’s happy to redirect productivity gains away from the middle class to support her agenda.

And that means consumer prices are never coming back down. The days of $30 grocery bills are over. We’ll quantify that tomorrow.

But the key thing we must understand is that inflation undermines civil society. It hollows out the middle class and creates a great economic divide between the haves and the have-nots. This is the real threat of war… and it’s insidious.

The good news is that we can take action at the individual level. There’s an old saying that goes, “if you know what’s happening, you’ll know what to do”.

Well, what’s happening is right there in the open for all to see. What we need to do is mitigate the impact of inflation… and then make it work for us.

I’ll show you exactly how in our Finance for Freedom program. You can find it here: Bulletproof Your Money

-Joe Withrow

P.S. If you want to know what happened on August 15, 1971, just go here.

The post War and the middle class first appeared on Zenconomics.

The post War and the middle class appeared first on Zenconomics.

October 16, 2023

The Real Threat of War

I got very concerned last week.

By now I’m sure you know all about the conflict in the Middle East… and that the US government has gotten involved.

I’m not here to comment on the politics of it all, other than to say that there’s nothing more stupid than war. Like governments and bureaucracy, it’s a relic of the Bronze Age. We’ll need to put it in our past if we wish to build a civilization geared towards human thriving.

That said, war is a major threat to our economy and our finances.

Some of these threats are obvious. Potential supply chain issues and rising oil prices are easy to anticipate.

But the biggest threat is hidden in the shadows… and they will never be honest about it. That threat is inflation.

I know we’ve all had to grapple with consumer price inflation over the last few years.

Homes, rent, cars, groceries, and household goods have all skyrocketed in price. It’s nearly impossible for a family to get out of the grocery store without spending over $100 these days.

As bad as these rising prices are, that’s not what we’re talking about when we talk about inflation. Rising prices are just the symptom. And they mask even deeper structural problems.

Inflation is the act of expanding the money supply. Said more directly, inflation is the act of creating money from thin air. It’s the act of printing money. And this is the only way that governments can pay for wars.

Inflation destroys the purchasing power of the currency unit being inflated—dollars, in this case.

That’s why we see consumer prices rise. It’s not because things are getting more expensive to produce and distribute. They aren’t. Those costs tend to go down over time.

Instead, inflation causes the currency to constantly “leak” value. When our grocery bill goes up, what we’re really seeing is that our dollars buy less than they used to.

And the impact inflation has on our economy and thus civil society is even more insidious than this.

Inflation makes it impossible for individuals and businesses to plan with certainty. I’ll give you a few examples of this…

Let’s suppose somebody named Billy makes $100,000 a year.

Because Billy is wise, he has a robust investment plan in place. Billy is going to save 50% of his income and direct it into specific investments over the next five years. He calculates that this will put him in a bulletproof financial position.

The problem is, Billy is treating his $100,000 annual income as if it is static. As if that $100,000 is a strict measurement of value.

But it’s not. That $100,000 will buy less and less every single year – because the purchasing power of the dollar is being destroyed by inflation.

The dollar is currently losing well over 10% of its value each year. And with the US government seemingly content to support multiple wars on multiple fronts, we can expect the dollar’s fall in value to accelerate. This does two things to Billy…

First, it makes his $100,000 income worth less and less. He’ll see this as his cost of living rises up to consume a greater portion of his income each year. And that will make it harder for him to save his target 50%.

Second, Billy’s investments will need to increase in value equal to the rate at which the dollar is losing purchasing power just for Billy to maintain his current financial position.

Said another way, if Billy’s investments don’t appreciate faster than the inflation rate, he’s actually losing net worth in real terms… even if investments aren’t going down in nominal terms.

Now take this same dynamic and let’s apply it to an enterprise looking to make a strategic investment in the US. It could be anything. Maybe it’s a nuclear power plant. Maybe it’s a semiconductor fab.

Whatever it is, the enterprise must invest a huge sum of money up front to get the new operation going. And to do this, management must be confident that the new operation will make enough money over the next 20 or 30 years to justify the investment.

Well, if the US government ramps up inflation to fight multiple wars, that makes this kind of cost-benefit analysis impossible to do. Because there’s no constant.

Our measuring stick – the dollar – is constantly leaking value. So how can any enterprise possibly know which investments will pay over a 20 to 30 year period and which won’t?

We could explore this dynamic all day long, but I think you get the point.

Inflation destroys the dollar, which in turn hollows out the middle class and reduces the capital investment we need to drive economic activity and maintain our infrastructure. This is the recipe for eroding civil society… and we’re seeing plenty of evidence that it’s all happening right now.

Fortunately, we do have a solution at the individual level. We can structure our finances such that we make inflation work for us, not against us.

And that’s exactly what we do in our Finance for Freedom program. We first identify the threats, then we mitigate them… then we leverage them.

For more information, just go here: Bulletproof Your Money

-Joe Withrow

The post The Real Threat of War first appeared on Zenconomics.

The post The Real Threat of War appeared first on Zenconomics.

October 12, 2023

The Promise of Financial Freedom

All week we’ve explored ways to maximize our after-tax income by leveraging the secrets hidden within the US tax code.

I know some of this may sound tedious—it’s far easier to simply work a W2 job and take the standard deduction. But if you’re willing to do a little bit of tax planning, a whole new world can open up to you. That is the world of financial independence.

Imagine what life would be like without the need to earn employment income. No more commuting to a job you may not find fulfilling. No more answering to bosses and corporate bureaucracies. No more scrambling to pay the bills.

Instead, picture having complete control over your time and schedule. Waking up when you choose. Pursuing creative passions. Volunteering for causes you care about. Traveling the world with family and friends. Simply enjoying each day as you desire.

This is what financial independence looks like. It’s about no longer being dependent on a paycheck to make ends meet. Time freedom. Location freedom. The flexibility to live life on your own terms.

Of course, this doesn’t happen by accident. It requires us to diligently construct multiple income streams and then maximize the after-tax income from each. We’re talking passive income from well-chosen investments.

This is the promise of financial independence. And with the right roadmap, it’s possible to get there sooner than you think.

For a much deeper dive on how it can all come together, check out my new book Beyond the Nest Egg. You can find it on Amazon right here.

See you on Monday.

-Joe Withrow

The post The Promise of Financial Freedom first appeared on Zenconomics.

The post The Promise of Financial Freedom appeared first on Zenconomics.

October 11, 2023

The Deepest Secrets of the US Tax Code

The rich play the game of money very differently. The rich know that the real way to wealth is via cash flow, and if managed properly, cash flow can be both substantial and tax-free. -Robert Kiyosaki

We’re talking smart tax-planning this week. And it all starts with understanding the true nature of the US tax code.

Simply put, the tax code was designed to help entrepreneurs and investors minimize their tax liability. I know that’s not what we’re led to believe in school. But it’s clear as day.

Consider this – the federal tax code consists of over 70,000 pages. Yet, less than five percent of those pages are about paying taxes. The other 95 percent are all about how to avoid paying the taxes that the first five percent says we owe.

This is what Kiyosaki’s quote above speaks to. If we understand the tax code, there are countless ways to reduce our taxable income.

Yesterday we looked at a few ways we can use business entities to write off certain expenses that we would have incurred anyway. We talked about how to make going out to dinner a business meeting. And we discussed how we can make routine home maintenance expenses partially tax-deductible.

As neat as those examples are, they are only scratching the surface of what’s possible.

The US tax code is really about incentives. It provides tremendous tax advantages for those who engage in certain business activities and investments. And the secrets run deep…

This week we’ve looked at how to eliminate taxes on our business income. But what if I told you we could make investments in assets that produce monthly cash flow for us… and write off a material percentage of those assets’ value against all other income sources?

I’ll demonstrate with an example…

Suppose you work a job earning $100,000 a year and you have several investments producing another $50,000 a year for you. Using the methods we discussed yesterday, it’s very easy to reduce your tax liability on that $50,000 to zero. But that still leaves you on the hook for $17,400 in federal income taxes on your W2 income.

But what if you went out and made an investment that allowed you to write off another $60,300 against your W2 income? That would reduce your federal income tax liability to just $4,764. And here’s where the magic happens…

Depending on your withholding selections, you employer likely would have withheld at least $19,000 in federal income taxes… and maybe a fair amount more.

If so, you would be in line for an income tax refund of at least $14,000. Then you can take that money and make a similar investment next year to create a perpetual tax-reduction cycle.

That creates what I call “financial escape velocity”. Doing this automatically maximizes your after-tax income year after year after year. And this will allow you to attain financial independence far faster than most would think possible.

Of course, my example today is just hypothetical and oversimplified for demonstration purposes. And I should point out that it takes advanced tax planning to accomplish this. But the concept is there. People in the know have been using this strategy for a long time.

You know all those times somebody has run for president but didn’t want to release their tax returns? This is why. They are utilizing the deepest secrets of the US tax code—but they don’t want us to know about it.

Tax genius Tom Wheelwright has a saying I very much like. He says when you make more money, you pay more taxes. But when you build more wealth, you pay less taxes.

This speaks to the importance of using our income wisely.

Consumers are crushed by the tax code. Entrepreneurs and investors leverage it to build financial independence.

Tomorrow we’ll look at the big-picture vision…

-Joe Withrow

P.S. If you would like to learn about how to leverage the US tax code in much more detail, it’s all in my new book Beyond the Nest Egg. You can find it on Amazon right here.

The post The Deepest Secrets of the US Tax Code first appeared on Zenconomics.

The post The Deepest Secrets of the US Tax Code appeared first on Zenconomics.