Joe Withrow's Blog, page 8

December 21, 2023

The New Rules of Money for the 2020s and Beyond – Part 2

The world as we know it ended in 2022.

Yet, as we discussed yesterday, our entire approach to retirement planning is based on the world that ended. This new world we’ve entered into comes with new rules of money… and these new rules require a new approach.

I submit to you that we should scrap the nest egg model completely. Because it forces us to choose between assets and income. That’s the core premise within my book Beyond the Nest Egg.

Instead, we should start thinking in terms of “financial security” and then “financial independence”.

Financial security comes first. This is how we make our savings bulletproof.

To achieve financial security, we must assess our current needs and lifestyle relative to our career, income, and family situation.

Based on these things, how much money do we need to save to provide ourselves with reasonable continuity should we lose our job, our income, or suffer a major emergency?

This number is going to be different for each of us.

If we’re young and just getting started, maybe $25,000 is enough. If we’re middle age with a family, maybe we need to accumulate $50,000 or $100,000. And if we’re in or approaching retirement age, we may want our financial security number to be even higher.

But here’s the thing – we don’t simply stuff this money into a savings account or some kind of fund. We build a strategic asset portfolio across a range of asset classes. Each asset serves a different purpose for us.

We need to structure our asset portfolio such that it will be impervious to inflation, market crashes, and economic slowdowns. That’s not hard to do with the right mix of assets.

But at the same time, we can convert these assets back into cash easily if we need to. That’s the key. If we have an emergency, we always have sufficient purchasing power available to handle it.

That’s financial security. Once we have it we can start working on financial independence. This requires us to start building passive income streams.

The idea is to gradually build additional income until our passive income meets and then exceeds our expenses. Once that happens, we are financially independent.

And guess what? Our extra income allows us to also grow our financial security asset portfolio. That’s how we put assets and income on the same team.

So the traditional approach to retirement says that we build up assets and then sell them when we retire to fund our lifestyle. And we hope we don’t outlive our money.

The approach I suggest is radically different. And far more robust.

Let’s build assets and income during our prime working years. That way when we want or need to stop working, our income can fund our lifestyle… and we never need to sell our assets.

Then if we do proper estate planning, we can transfer everything we’ve built to future generations in a tax-efficient manner… and maybe humanity can finally get off the hamster wheel.

The beauty of this approach is that it makes our age irrelevant.

If we start with this approach when we’re young, we can “retire” whenever we’ve achieved financial independence. It doesn’t matter if we’re 45 or 65.

And even if we shift to this approach after we’re older, we can still reposition our nest egg such that it’s far more robust. Then we can still build extra income if we choose to.

In other words. There are no restrictions with this model.

That’s the vision. It just requires us to follow the new rules of money for the 2020s and beyond.

-Joe Withrow

P.S. If you would like a deeper dive on how we go about building our asset portfolio and our passive income streams, check out my book Beyond the Nest Egg. You can get it on Amazon right here.

The post The New Rules of Money for the 2020s and Beyond – Part 2 first appeared on Zenconomics.

The post The New Rules of Money for the 2020s and Beyond – Part 2 appeared first on Zenconomics.

December 20, 2023

The New Rules of Money for the 2020s and Beyond

I have one more image of winter’s first snowfall for you today:

This one truly captures the majesty of the Virginia highlands. But now it’s time for a serious discussion…

The Age of Paper Wealth is over.

That’s the conclusion my research led me to last year. And it’s the core theme I’ve presented in these pages over and over again.

It all comes down to the Federal Reserve (the Fed), interest rates, and the US dollar.

The market has been trained to see the Fed as a reactionary institution. When consumer price inflation rises, the Fed is supposed to raise interest rates to get it back down. Then when inflation slows, the Fed is supposed to cut interest rates to stimulate economic growth.

That’s the Keynesian view. It’s been the dominant economic school of thought in academia and American politics ever since the 1960s. President Nixon even went on television in 1971 and proclaimed, “We’re all Keynesians now”.

Keynesian theory created the Age of Paper Wealth. It lasted from 1982 to 2022.

During this time, the Fed consistently cut interest rates and flooded the financial system with cheap money. This kept borrowing costs abnormally low and sent the stock market soaring for forty years.

But low rates and cheap money fueled a debt binge of epic proportions.

The US government is now $34 trillion in debt. And the American private sector has run up its debt burden to nearly $20 trillion.

At the same time, the policy of creating trillions of dollars from nothing year after year has triggered serious consumer price inflation for the first time in decades.

We see this in the form of rising prices for houses, cars, groceries, and other necessities.

But these items aren’t getting more expensive because they cost more to produce. They are getting more expensive because inflation erodes the value of our dollar.

Meanwhile, the BRICS bloc (Brazil, Russia, India, China, South Africa) now represents 42% of the world’s population and 36% of global gross domestic product (GDP). And this bloc is working furiously to build alternative trade networks and settlement systems to operate outside the US dollar.

This reduces demand for US dollars and dollar-denominated assets – especially US Treasuries.

The problem is, Treasury bonds are the bedrock of the US financial system. American banks, financial institutions, and insurance companies own roughly $12 trillion worth of US Treasuries.

So Wall Street and the Fed can’t afford for Treasury demand to plummet rapidly. That would threaten the entire system.

And if that weren’t enough, the western world’s globalist faction is now pushing for what it calls the “Great Reset”. It’s a plot to overthrow the traditional economic order and make globalist institutions the ultimate arbiter of money and credit.

That’s what central bank digital currencies (CBDCs) are about. They are a threat to the private commercial banking system itself.

To make matters even more complex, a portion of the American power structure (government/corporations/academia) is aligned with the globalist faction. They favor the Great Reset – to the detriment of peace, prosperity, and traditional American values.

This is what the Fed’s aggressive rate-hiking campaign last year was all about.

The financial media tells us that Fed Chair Jerome Powell is trying his best to fight off inflation by raising rates. And the implication is that when inflation slows, he will beat rates back down to where they were.

That’s not it.

Powell is fighting to save the legacy financial system and the US dollar.

He’s not a globalist. Powell’s a Wall Street guy. And Wall Street’s wealth, power, and influence depends on a strong America.

By raising rates so aggressively, Powell has made US Treasuries an attractive investment for global capital again. It has been 15 years since that was the case.

That’s what this is about.

The more global capital the Fed can direct into US Treasury bonds, the better it will be able to thwart the globalist plot and deter the BRICS bloc from abandoning the dollar en masse.

This is why there will be no “Fed pivot”.

As we discussed yesterday, if Powell signs off on any rate cuts next year, they will be miniscule. The narrative that the Fed is going to spend the next two years slashing rates aggressively is based on false premises.

And that means the days of perpetually lower rates and an ever-rising stock market are over. The Age of Paper Wealth met its end in 2022. As did Keynesianism.

This presents us with a major challenge.

Our entire approach to financial planning was crafted in the 1980s. That’s when the “retirement” industry was born – giving rise to retirement accounts and a horde of managed funds to put in them… all laced with fees to line the industry’s pockets.

The retirement industry says that we should work hard and pour our savings into funds within these retirement accounts for decades. Then, around age 65, we are to begin selling our funds year after year to create income for ourselves in retirement.

I suppose that approach worked okay during the Age of Paper Wealth. Falling rates and cheap money constantly pushed the stock market higher – taking most funds along for the ride… no fundamental analysis necessary.

My proposition is that those days are over.

What we consider the traditional approach to financial planning is based on the belief that borrowing costs will always be low and stocks will always go up over time.

That was the world from 1982 to 2022… but we’re in a new world now. And this new world has new rules of money that we need to follow.

More on that tomorrow.

-Joe Withrow

The post The New Rules of Money for the 2020s and Beyond first appeared on Zenconomics.

The post The New Rules of Money for the 2020s and Beyond appeared first on Zenconomics.

December 19, 2023

What comes next…

The first snowfall of the season came last night.

Just a dusting… but the mountains of Virginia sure look magical when they are covered in snow. I snapped a few photos down by the river this morning:

This is the small walking path that winds its way next to the Jackson river.

In the background you can see old Smith’s bridge. It’s a steel bridge that’s just wide enough for a truck to cross the river. It connects what was once Smith’s farm with the Cliffview Inn.

Getting back to finance…

Yesterday we talked about the market’s reaction to the alleged “Fed pivot” last week. The S&P 500 is now up nearly 6% in just the last week and a half on expectations that the Fed is about to cut interest rates.

But we noted that the market is ignoring something very important. The “dot plot” that signals seven rate cuts over the next 24 months doesn’t come from the Chairman nor does it influence monetary policy.

Instead, the dot plot is simply projections from each of the 12 members of the Federal Open Market Committee (FOMC). And if we look at who those members are, four of them are new to the FOMC this year.

Coincidently, the four new members each favor aggressive rate cuts. Meanwhile, the four members they replaced supported Fed Chair Jerome Powell’s aggressive rate-hiking campaign last year.

So this looks to me like the four new members are projecting their desires onto the dot plot… and institutional investors are taking that at face value because they want to get back to the “number go up” days in the stock market.

I think they are in for a rude awakening.

Powell probably will sign off on a small rate cut or two next year. There’s going to be a ton of pressure on him to do so ahead of the 2024 presidential election.

But those rate cuts will likely be 25 basis points (0.25%) each. Given that Powell jacked up the Fed’s benchmark lending rate by over 500 basis points (5%) – do we really expect a few piddly rate cuts to stimulate the financial markets?

I certainly don’t. In fact, the market is more likely to fall on the news because it has already priced in a more aggressive “pivot”.

The thesis that I’ve presented in these pages and in my book Beyond the Nest Egg is that the Age of Paper Wealth is over.

The Fed did not aggressively hike rates last year just to turn around and beat them back down to where they were. Those who are peddling that narrative don’t understand what the Fed is really doing.

The Fed isn’t simply trying to fight inflation. The battle they are fighting is much bigger than that… and the Fed needs to normalize interest rates if it wants to win.

So we’re in a new paradigm now.

And that means we need a new approach to money and finance. More on that tomorrow.

-Joe Withrow

The post What comes next… first appeared on Zenconomics.

The post What comes next… appeared first on Zenconomics.

December 18, 2023

About that pivot…

Suddenly the “Fed pivot” is all the rage… again.

Last Wednesday the Federal Reserve (the Fed) announced that it would not raise its benchmark lending rate again this year. And Fed Chairman Jerome Powell stated that we are “likely at or near the peak rate for this cycle”.

The stock market began ripping higher as those words came out of Powell’s mouth.

As I write, the S&P 500 is now up over 5% in just the last week and a half. That’s a huge move in such a short period of time.

But it wasn’t what Powell said that really kicked the markets into a bullish frenzy. It was the Fed’s quarterly “dot plot”. This is a chart that summarizes the Federal Open Market Committee’s (FOMC’s) collective expectations for interest rates over time.

Now, the FOMC is composed of 12 members. It includes the Federal Reserve Chair, the Board of Governors, president of the New York Fed, and four of the other regional Fed presidents.

The FOMC is technically the Fed’s inner sanctum. It meets eight times a year to discuss monetary policy. The dot plot is supposed to be representative of these insider discussions… which is why the market ripped higher last week.

This quarter’s dot plot shows that FOMC members expect three rate cuts next year and four in 2025. What’s more, the dot plot projects the first rate cut coming in March 2024.

But there’s a nuance here that nobody wants to acknowledge.

Each dot on the chart represents an individual FOMC member’s projection for the federal funds rate over time looking forward. That’s all it is. Each member gets to contribute their own dot.

So the dot plot that sent the markets roaring higher last week didn’t come from Jerome Powell. He gets a dot on the chart just like everybody else… but that’s it. He doesn’t control what the final graph looks like.

That means to analyze the dot plot’s projections, we need to know who is sitting in on those FOMC meetings and placing their dots. And this is where it gets interesting…

Loretta Mester (Cleveland Fed), James Bullard (St. Louis Fed), Susan Collins (Boston Fed), and Esther George (Kansas City Fed) each joined the FOMC earlier this year.

They replaced Lorie Logan (Dallas Fed), Neel Kashkari (Minneapolis Fed), Patrick Harker (Philadelphia Fed), and Christopher Waller (Board of Governors).

If we look at their background and their record within the Federal Reserve system, Mester, Bullard, Collins, and George are each considered to be dovish on monetary policy. That means they favor low interest rates and cheap money.

Then if we look at the records of those they replaced, both Kashkari and Waller have been hawkish. They favored the Fed’s aggressive rate-hiking campaign last year.

And Logan and Harker are both considered centrists. They aren’t as hawkish as Kashkari and Waller, but they do recognize that the Fed can’t permanently keep rates low.

So the four new FOMC members each favor rate cuts. And the four members they replaced did not.

That’s what we’re seeing in this quarter’s dot plot. The dovish members are projecting their own desire to cut rates… and those desires are now largely priced into the stock market.

But here’s the thing – the dot plot has no influence on policy. That’s all Jerome Powell. And he hasn’t said one word about rate cuts. In fact, Powell appears to be the most hawkish member of the FOMC.

So it looks to me like the markets are in for a rude awakening. More on what’s to come tomorrow…

-Joe Withrow

P.S. My new book Beyond the Nest Egg takes a deep dive into what the Federal Reserve’s aggressive rate-hiking campaign last year was really about… and where this is all going.

If you’re interested, you can find the book on Amazon right here. And thanks very much to those who took the time to leave it a review.

The post About that pivot… first appeared on Zenconomics.

The post About that pivot… appeared first on Zenconomics.

December 16, 2023

The best advice I ever got about building wealth…

I spent the last seven years at the largest independent financial research firm in the world. One of my mentors there had a saying he was fond of…

“When your outgo exceeds your income… your upkeep becomes your downfall.”

Wise words. But also simple. So simple…

And that’s what I want you to realize about financial freedom. You do NOT need a fancy degree… You don’t even need a lot of money to start with.

What you need more than anything else is…

A mentor to show you the ropes. Someone who can save you years of expensive mistakes…

And give you the skills and confidence to achieve financial security and then financial freedom.

After working in corporate banking (and hating it)… And seven years at the world’s largest independent publisher of investment research (and loving it)…

I finally decided to go out on my own and bring everything I’ve learned about money and finance to regular people.

And that led me to create the new Finance for Freedom Mastermind.

In it, you will find everything you need – no matter what your level of comfort or experience with money – to deal with the new economic environment we are now in.

Plus, you’ll also get something you won’t find anywhere else – access to a personal mentor who can guide you to adopt sound financial fundamentals for the days ahead.

And you’re going to need it. Because…

The rules of money have changed.

But you CAN change with them. And I can help you.

What has me frightened is… what’s coming next.

For the first time in the last 40 years, the Federal Reserve (the Fed) is not going to bail out investors when trouble hits.

Since 1982, investing has been a one-way bet thanks to endless money printing and lower interest rates.

Those days are over.

Please believe me when I tell you… anyone who doesn’t understand what’s coming is going to pay a hefty price.

Don’t lose your hard-earned retirement savings. Find out how the rules of money have changed so you can navigate this new world successfully.

-Joe Withrow

The post The best advice I ever got about building wealth… first appeared on Zenconomics.

The post The best advice I ever got about building wealth… appeared first on Zenconomics.

December 15, 2023

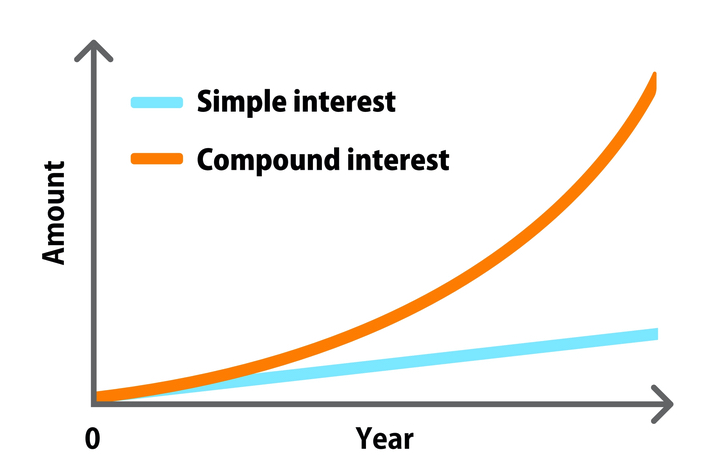

Is this the 8th Wonder of the World?

No lesser mind than the brilliant Albert Einstein thought this feature of money was the “8th Wonder of the World”.

Loosely translated, what he said was…

“Those who don’t understand [it], pay… while those who DO understand [it], earn.

He was talking about compounding – the magic bullet when it comes to investing.

Now, I don’t know if Einstein actually said compound interest was the 8th Wonder of the World. There are questions about that. But you know, it doesn’t matter.

Because the point still applies. If you figure out how to earn a compounding rate of return on your money… you win.

Over time, you not only collect a return on your original investment…

You also collect a return on the money you’ve already earned. That’s how a small stake in the right asset can go like this:

The rules of money are changing dramatically.

If you don’t understand what’s happening, you’ll end up paying a greater and greater amount of your income and savings – just to stay in the same place financially.

Don’t do that.

Join our Finance for Freedom Mastermind right here... and be that orange line in the image above.

-Joe Withrow

The post Is this the 8th Wonder of the World? first appeared on Zenconomics.

The post Is this the 8th Wonder of the World? appeared first on Zenconomics.

December 14, 2023

You’re being robbed RIGHT NOW… [There’s still time to fix this]

In 2022, something big happened to our money… and almost no one has noticed. The Age of Paper Wealth came to an abrupt end.

Interest rates bottomed and started heading up again for the first time in 40 years… all while government and private debt exploded to unpayable levels…

And inflation is now destroying what remains of the American Dream.

If you’ve tried to get a loan to buy a home or car recently, you know what I’m talking about…

Finance charges have more than doubled in the last few years – making it much harder for regular people to secure affordable financing.

Well here’s the truth about the US dollar and where we are headed…

Until 2022, cheap credit was everywhere. Now… it’s gone. And that’s not going to change.

If the Federal Reserve (the Fed) prints a bunch more money and drops rates, it will be the end of the dollar and the financial system as we know it.

If they keep rates high and drain excess liquidity – like they are doing now – we’re guaranteed to go through a recession. And we may even see a full-blown credit crisis if Congress can’t reel in spending.

In this e-letter I’ve made the case that the Fed is NOT going to print money and cut rates like it has in the past.

Which means we are now living in a new world – one we haven’t experienced in over 40 years.

Think about that… No one under age 65 has ever known anything other than easy money and lower rates in their adult life. But those days are over.

The good news is…

You CAN learn to make inflation your friend. You can harness inflation to work in your favor – instead of robbing you blind like the thief it is.

That’s what my new Finance for Freedom Mastermind is all about.

To your financial freedom,

Joe Withrow

P.S. Here’s just a sneak peek at what I share inside the Finance for Freedom Mastermind…

1. Understanding our monetary history… where we are today and how the rules of money are changing.

2. Where are we in the economic cycle today? And what should you do to prepare for what’s coming?

3. “Money consciousness” – how to picture yourself getting wealthy and avoid the big mistakes people make around money.

4. The simple steps to master your finances in 30 days or less…

5. My Finance for Freedom system for building a bulletproof asset portfolio…

6. Five-minute walkthroughs for adding each key asset to your portfolio…

7. How investing wizards Warren Buffett, John Templeton, Ray Dalio, and Paul Tudor Jones view gold, stocks, bonds, Bitcoin, real estate, and private investments – and how you can copy their thinking to grow and protect your money like the biggest names in finance…

8. The four essential alternative investments that create true financial security in a world of central bank insanity…

9. The important mindset shift you need to adopt for building passive monthly income streams…

10. My proprietary spreadsheet downloads to help you quickly organize and implement everything you learn…

The post You’re being robbed RIGHT NOW… [There’s still time to fix this] first appeared on Zenconomics.

The post You’re being robbed RIGHT NOW… [There’s still time to fix this] appeared first on Zenconomics.

December 13, 2023

How I discovered the fast track to financial freedom

When I graduated from Radford University with my degree in finance, I was a fresh-faced lad of 22, ready to take on the world – convinced I would do meaningful work.

Not long after, the 2008 global financial crisis hit and I was right where I felt I needed to be… the Loss Mitigation department at Wells Fargo.

I was in the right place alright. But for all the wrong reasons. Let me explain…

Loss Mitigation is a code word for “we are the guys at the bank whose job it is to modify mortgage paperwork so Wells Fargo could show the government what a fine and noble job they were doing”.

I probably don’t have to tell you this was pure theatre. The only thing being mitigated was reputational damage.

I quickly understood that my real task was to satisfy government bureaucrats at various agencies by fiddling with paperwork to make it look like we were helping…

In reality, all I was doing was making sure my employer would have a profitable quarter… while almost four million families had lost their homes!

Needless to say, that didn’t sit right with me. In fact, I started having real trouble respecting the guy in the mirror. So, I walked.

And then, the most amazing thing happened…

I discovered an investment research publisher where the people all thought like me… cared about telling the truth about our financial system… and didn’t flinch at exposing Wall Street greed for what it is.

Best of all, this publisher took no sponsorship money from Wall Street and could therefore print whatever they wanted without fear of losing revenue.

In fact, the more we told the truth to our readers, the more our readers loved and admired our work. It was a dream come true.

My team and I published a daily financial e-letter that reached two million subscribers at its peak. And then…

Management decided to go in a different direction.

So why am I telling you about my journey?

Because my time inside a Wall Street bank taught me how corporate finance works…

The whole thing is self-serving and unproductive. Wall Street’s investment analysis is lacking. And it is riddled with conflicts of interest.

But my time at the world’s largest independent financial research firm showed it is possible to tell the truth and actually make a difference in people’s financial lives.

This is the work I was born to do.

My name is Joe Withrow. And my unique perspective on personal finance led me to create a group mastermind called Finance for Freedom.

This is not just an online course.

Don’t get me wrong – we have all the financial training modules you need to master your finances and create true financial security.

But the new Finance for Freedom Masterclass takes it one step farther.

We host mastermind calls twice a month where you and I get to speak so you get all your questions about money answered by me and some of the smartest people in finance. And you get to benefit from the questions other people are asking.

Best of all, Finance for Freedom was built from the ground up to help regular people navigate the 2020s – so you can come out on the other side of the chaos with your money intact and your life and family enriched.

The best part?

I’m practically giving it away for a short time. The cost is about 27 cents a day – so anyone who wants to learn the new rules of money can afford to do so.

Go here to find out all that’s included. And don’t wait… because what we are seeing in my network tells me you don’t have much time to get your finances in order.

-Joe Withrow

The post How I discovered the fast track to financial freedom first appeared on Zenconomics.

The post How I discovered the fast track to financial freedom appeared first on Zenconomics.

December 12, 2023

America at the crossroads…

For generations, succeeding in America was simple…

Go to school—> get good grades—> go to college—> get a good job.

If you followed this plan and worked hard, a middle-class lifestyle was easy to achieve.

And those more ambitious could start a business with almost no regulatory obstacles. Opportunity was everywhere.

Not anymore…

Because the American Dream that inspired millions of immigrants to leave their homeland and create a new life in the US… is fading into history.

Today, many colleges load up students with debt and fill their heads with destructive ideas—the kind of ideas that prevent success in the real world.

Meanwhile, the bureaucracy in Washington churns out endless regulations – strangling small business success. Many entrepreneurs from a generation ago would be hard-pressed to recreate their same success today.

And to top it off, reckless government spending and money printing are driving up the cost of living for everyone.

Just look at this data on consumer price inflation:

This table looks at the median price of a new car, ten gallons of gas, and five pounds of ground beef going back to 1940.

Beef is up 2,400%… Gas is up 3,400%… and a new car is 5,500% more expensive. No wonder so many people are struggling! And look at the effects of inflation on the most basic necessity of all – putting a roof over your head

That’s a chart of the median home price compared to median annual incomes going back to 1940.

The third line shows what percentage of the median home is covered by the average person’s salary.

The median home today costs $430,300 – while the median annual income is only $74,580. Today, the average person’s salary can only cover 17% of the median home price.

Back in the 1940s, 50s and 60’s, you could buy a house with only a few years of savings. Today, that dream is almost out of reach.

As recently as the 1970s the median salary could cover more than half of the median home price.

If that were the case today, the average person would be making $232,362 a year.

The numbers don’t lie.

Thanks to inflation, costs are rising much faster than incomes. And the middle class is now on the endangered species list.

After all, the super-rich don’t stop to count the cost of necessities like the middle class. So inflation just isn’t much of an issue to the wealthy elites who drive these destructive policies.

Here’s the thing…

You and I cannot change this dynamic. The politicians will always look for the easiest way to get more money – which is to print it out of thin air.

The good news is…

You CAN protect yourself from inflation if you understand the new rules of money in the 2020s.

Go here to find out about my new Finance for Freedom Mastermind.

This is the fastest way to master your finances by learning the new rules of money for the 2020s and beyond – starting in just 30 days or less.

Imagine how you’ll feel when you no longer have to watch helplessly while your hard-earned money is destroyed by inflation…

Imagine the confidence you’ll have when you know how to make smart financial decisions that safeguard your earnings and ensure a secure future for you and your loved ones…

If you’re intimidated by money or think this topic is overwhelming… you can relax.

I specialize in explaining highly technical concepts quickly and simply.

You and I can even speak personally inside our community mastermind calls – where all your questions about financial freedom will be answered.

And you will get the benefit of hearing other people’s questions and experiences as well. In many counselors there is security, as the late Dr. Gary North used to say.

Are you ready to take control of your financial future? You better be…

Because the changes happening in our financial and monetary system will not wait longer for your decision.

-Joe Withrow

The post America at the crossroads… first appeared on Zenconomics.

The post America at the crossroads… appeared first on Zenconomics.

December 11, 2023

A financial storm is brewing… [Do this to prepare]

What role does money play in society? If you’re like most people, you’ll answer something like:

For transacting commerce. Or… As a means of saving.These are good answers… I give you my money, and you give me a product or service. Or I could save some portion of my money to use later.

Both are vital functions of money in any society. But money plays another role most people have never considered…

Money is also a communications system.

Prices for goods and services act like signals in a massive economy like ours. This price system is the most sophisticated “machine” ever built.

The prices of goods and services communicate information about the supply and demand of scarce resources to billions of individuals in real time all over the world.

When the price of something goes up, that’s a signal that it has become more scarce relative to demand – which prompts entrepreneurs and business owners to create more supply or offer alternatives to meet demand.

When the price of something goes down, that’s a signal that the item is abundant compared to consumer demand – leading firms to produce less of it… until the price rises again.

This price-signaling system allows millions to coordinate their productive efforts across time and space. It’s what Scottish philosopher, Adam Smith, called the “invisible hand”.

This is how individuals can make decisions based on self-interest – driving economic growth for all.

When the price system is left alone, labor and scarce resources can be allocated to their highest and best use.

Why am I telling you this? Because there is a problem…

One group of people have the power, means, and motivation to obliterate the price-signaling system…

I’m talking about those who pull the strings of monetary and fiscal policy. Monetary policy falls to central banks like the Federal Reserve (the Fed). And fiscal policies fall to legislatures and national Treasury departments.

The best way to destroy the valuable information conveyed by prices is to inflate the currency and manipulate interest rates.

When the central bank inflates the money supply and tinkers with interest rates, price signals become confusing. No one knows the real value of goods and services anymore.

And since 2020, the Fed and the US Treasury increased the supply of dollars by nearly 40%.

The US has never before debauched its currency so rapidly.

Inflating the currency by creating new money out of thin air reduces the purchasing power of all currency units in circulation. In other words…

The reason you are paying more at the pump for gas… for your groceries… and for just about everything else right now is because your money is “competing” with lots of other new currency units (dollars) for a limited number of goods and services.

Are the things you need rising in price because they have become scarce? Or is it just inflation doing its evil work?

There is no way to be sure.

This confusion leads to “malinvestment”. That’s where scarce resources get wasted on uneconomical ventures.

The bottom line is this:

Inflation wrecks everything. Your grocery bill is just one small piece of the problem.

But here’s the thing – you don’t have to be a victim of what’s happening.

You have the power to protect yourself and your family from the devastating effects of inflation and economic instability.

Because I created a new Mastermind I call Finance for Freedom.

It’s a unique training series with bi-monthly mastermind calls designed to help you master your finances – starting in just 30 days or less.

You’ll get personal one-on-one time with me and the opportunity to benefit from other people’s questions and comments – along with a series of video lessons to reinforce what you’re learning on the calls.

More importantly, you’ll gain the knowledge and skills to make the right moves so you can come out on top financially in the next decade.

Make no mistake about it… the rules of money are changing. And smart people are changing their thinking and habits to deal with this new reality.

Imagine no longer watching your hard-earned money being destroyed by inflation. Instead, you’ll have the confidence to make smart financial decisions that will safeguard your earnings and ensure a secure future for you and your loved ones.

If this all sounds overwhelming, don’t worry. That’s exactly why I created my Finance for Freedom Mastermind – to give regular people the skills and insights to survive and thrive through the coming financial reset.

I specialize in explaining highly technical concepts quickly and simply. I’ll guide you every step of the way, ensuring that you understand and can apply these strategies effectively.

Are you ready to master your financial future? The answer should be yes, because the changes coming to our financial and monetary systems will be unlike anything we’ve seen in our lifetimes.

Click this link to hear a special message from me and get started on your journey to financial freedom.

-Joe Withrow

The post A financial storm is brewing… [Do this to prepare] first appeared on Zenconomics.

The post A financial storm is brewing… [Do this to prepare] appeared first on Zenconomics.