Menzie David Chinn's Blog, page 33

June 17, 2015

“Answering the TPA Critics Head-On”

Today we are fortunate to have a guest contribution written by Jeffrey Frankel, Harpel Professor of Capital Formation and Growth at Harvard University, and former Member of the Council of Economic Advisers, 1997-99.

In recent op-eds and blog-posts I have argued that prospective trade agreements like the TPP (the Trans Pacific Partnership) would be economically beneficial for reasons similar to past trade agreements and that they would have geopolitical benefits too. I have also opposed adding currency manipulation to the trade negotiations.

I am far from alone. Such support for giving the White House Trade Promotion Authority (TPA) is shared by most economists, including 14 former chairs of the president’s Council of Economic Advisers. But we supporters have not sufficiently responded to the most common arguments of the critics of the TPA process: a perceived abandonment of democracy and transparency.

Despite what one reads, I see no such abandonment, relative to the way that trade negotiations have been pursued by the United States in the past or relative to the way that they are pursued by other countries. Regarding democracy: under Trade Promotion Authority the Congress would vote on the final agreement that the executive branch has negotiated (thumbs up or thumbs down). Regarding transparency: the details of TPP or TTIP that are unknown are details that have not yet been concluded in the international negotiations.

The negotiations could not proceed if Congress were intimately involved every step of the way. That is why it has been done this way in the past. There is nothing different this time around (unless it is the extra degree of exposure that draft texts have received).

It is true that these trade negotiations include more emphasis than many in the past on issues of labor and environment, on the one hand, and intellectual property rights and investor-state dispute settlement on the other hand. And it is true that, to get it right, the details of these issues need fine calibration. But here is the point that everyone seems to have missed, in my view: even if it were somehow logistically possible for international negotiations to proceed while the US Congress were more intimately involved along the way, the outcome would be far more likely to get the details wrong — with big giveaways to special interests – than under the usual procedure of delegating the detailed negotiations to the White House. I know that no commentator is ever supposed to say that any political leader can be trusted. But I do trust President Obama on this, far more than I trust Congress.

This post written by Jeffrey Frankel.

New Gross State Product Figures Reveal…Wisconsin (Still) Lags

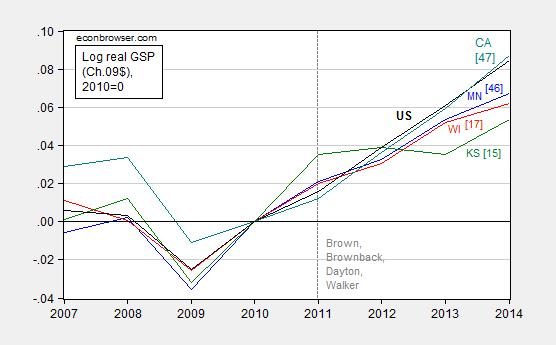

Some individuals have questioned the accuracy of the Philadelphia Fed coincident indices as measures of economic activity. Recently released Gross State Product (GSP) data confirms the pattern previously identified: Wisconsin lags the Nation, and its neighbor Minnesota. Thank goodness for Kansas to make Wisconsin look good!

Figure 1: Log Gross State Product for Minnesota (blue), Wisconsin (red), Kansas (green), California (teal), and United States (black), all normalized to 2010=0. 2014 figures are advance. Numbers in [square brackets] are ALEC-Laffer rankings from Rich States, Poor States, 2014. Vertical dashed line at beginning of Brown, Brownback, Dayton and Walker administrations. Source: BEA, ALEC RSPS 2014, and author’s calculations.

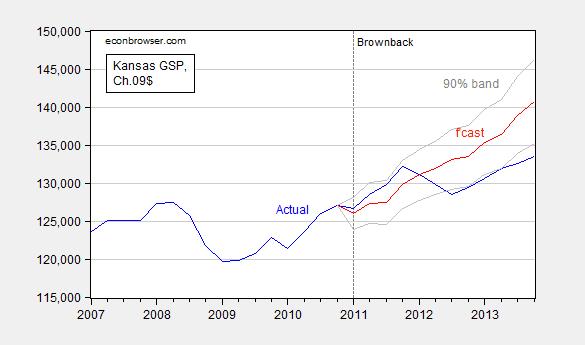

Update, 10pm Pacific: Ironman argues I have committed two offenses: (1) using Philadelphia Fed coincident indices to compare economic activity, and (2) not incorporating weather, for Kansas. On (1), I now use GSP. On (2), I estimate an ECM(1) with the Palmer Drought Severity Index (PDSI) for Kansas in the short run dynamics, using quarterly GSP 2005-11. I then estimate out-of-sample in an ex post simulation.

Even taking into account the drought, Kansas is doing poorly relative to counterfactual (and statistically significantly so).

June 16, 2015

“A Program for Greece: Follow the IMF’s Research”

Today, we are fortunate to present a guest contribution written by Ashoka Mody, Charles and Marie Visiting Professor in International Economic Policy, Woodrow Wilson School, Princeton University. Previously, he was Deputy Director in the International Monetary Fund’s Research and European Departments.

Some had expected that the Greek government would have “blinked” by now. Others believe that by not conceding, the Greeks have bungled the discussions with creditors. And yet others think that the Greeks may turn out to be the better negotiators after all. But the drama of the never-ending exchange is obscuring the principles.

A medical analogy, often used to describe international financial rescues, is useful to frame the issues. When a patient comes into an emergency trauma room, the doctor on the floor typically does not refuse to treat him because the patient has lived an unhealthy life. Nor does the doctor ask him to first run around the block a few times—as proof of good faith—before stemming his blood flow. And certainly no doctor will first increase the hemorrhaging as a warning before treating the patient.

But by threatening to cut off Greek banks from funding and by keeping the Greek economy on a leash, the troika doctors have made the Greek patient worse with the passage of every day. The Greeks, it is argued, could have saved themselves this outcome by agreeing on the very first day to the troika’s conditions. In essence, the troika program stayed with the strategy that has been followed over the past five years:

Borrow more money (this time mainly from the European authorities) to repay one group of creditors (the IMF, to which substantial repayments are due); stay focused on more austerity, steadily increasing the primary surplus (the budget surplus not including interest payments); and undertake “structural reforms”—changes in labor and other markets to improve the Greek economy’s longer-term growth potential.

The Greeks could have agreed to this plan and, eventually, not delivered—just like they have not delivered for the past five years. In part, the Greeks have tried that even in this round. The Greek “agreement” on the primary surpluses is a façade of numbers with little reality behind them. For five years, this has not worked.

To see where things have gone wrong, it is helpful to follow three IMF studies:

Over-indebted countries struggle to grow. In its famous mea culpa for delaying the restructuring of Greek debt, the IMF acknowledged a well-respected academic tradition.

The “debt-overhang,” as economists term it, inhibits new investment and growth. For this reason, it is in the interests of creditors as well as debtors to forgive debt (for an early statement, see Krugman, 1988). The evidence for this proposition is clear, including in an important paper by the University of Chicago economist and former Governor of the United States Federal Reserve Board, Randall Kroszner. Professors Carmen Reinhart and Christoph Trebesch similarly find that growth picks up after debt relief.

Some might say that Greece does not have a debt overhang. With the ultra-low interest rates on its official debt, Greece, it is argued, can repay its debt without sacrificing growth and reasonable social objectives. But even under the troika’s calculations, the conclusion that Greece can comfortably pay back its debts is true only on the assumption that Greece will increase its primary surpluses. The troika’s demands earlier this year were for an extraordinary ramp up in primary surpluses—from a small negative number to over 4 percent of GDP. That demand has been steadily scaled down over the past few months. But even now, the troika requirement is that the surpluses increase by about 1 percentage point of GDP a year for the next three years. To achieve that goal would require a contraction of discretionary spending well above 1 percent of GDP a year. That, by any definition, is significant fiscal austerity, coming on top of an extraordinary austerity over the past five years.

That leads to the second set of IMF analyses.

Austerity in a weak economy is self-defeating. As the budget deficit is reduced, the economy slows down, and the ability to repay debt is undermined. Indeed, austerity can be self-defeating.

Here is how this principle applies today to Greece. Recall, that prices in Greece have been falling for about two years now. Since debt repayment obligations do not change when businesses sell at lower prices or when wages fall, businesses and households struggle to repay their debt in a deflationary environment. Investment and consumption are held back, the government receives less revenue, making its debt repayment harder. If austerity is imposed in this deflationary setting, the weaker demand forces prices and wages down faster, making debt repayment even harder. This is the so-called debt-deflation cycle. Greece is in a debt-deflation cycle.

For this reason, for example, increasing the VAT tax burden now is a terrible idea. Japan—which, despite its troubles, is an infinitely stronger economy than Greece—only recently got its wind knocked out by a premature increase in VAT rates. To be sure, the VAT rates will eventually need to be raised, and pensions and wages will need to be scaled back. But setting a demanding timeline now—before growth is firmly established—will keep Greece trapped in a debt-deflation cycle. The debt-to-GDP ratio, which was about 130 percent of GDP when the Greek crisis began in 2009 has risen to about 180 percent, and will keep rising.

Thus, the third element of the troika strategy: Greece should do structural reforms and spur growth even while it does “growth-friendly” austerity. These are soothing terms. So, consider the third piece of IMF evidence.

Structural reforms have, at best, an uncertain payoff. In Box 3.5 of this recent chapter from the IMF’s World Economic Outlook, the updated finding has a long pedigree: policy measures can possibly create an environment for growth in the long-run, but no immediate payoffs should be expected.

Indeed, where structural reforms are a code phrase for reducing wages and weakening employment contracts—as they are in the Greek context—we circle back to the immediate problem of curtailing demand in an already deflationary environment. But even the long-term growth benefits of these measures are unclear. With lower wages comes lower productivity. Both economic theory and evidence support this concern. And Germany’s much vaunted success came not from suppressing wages but from corporate-labor agreements to outsource labor-intensive tasks to lower-wage economies while German manufacturers upgraded their technology (Dustmann et al., 2014). The IMF’s analysis does find that investing in R&D to raise productivity in the information technology industries may have a long-term pay off. But that will be reaped over decades not in time to extricate Greece from its debt-deflation cycle.

Finally, those calling for throwing Greece out of the euro area must confront Barry Eichengreen’s essay on the costs of breaking up the euro. Professor Eichengreen has recently gone on to warn that a Greek exit could have consequences for the European and global economy that would dwarf the panic following the bankruptcy of Lehman Brothers.

So what should a Greek program look like? The objective should be to return Greece to the financial markets in a phased manner. Following the medical analogy, the objective should be to get Greece out of the Emergency room, work through rehab, and then resume as normal an existence as it can. To that end, the key elements of a Greek program must be:

Forgive Greek debt so that it comes down to 50 percent of GDP payable over 40 years [this is akin to stemming the blood loss].

Scale down the banking system, which has been badly damaged and will continue to create vulnerabilities [this is the surgery].

And agree to a flat 0.5 percent of GDP primary surplus over the next three years, which even Greece can deliver [light yoga in rehab].

With this preparation and its low debt obligations, Greece will be able to tap markets. To those concerned that Greece will return to its bad ways, the new debt should be in the form of sovereign cocos, which will contractually provide for standstills on repayments if debt exceeds 75 percent of GDP. The standstill provision will limit Greek access to markets and raise the costs of borrowing. Greece will learn to live within its means. This would be like Greece training for a 5K race.

If that goes well, then the Greeks can decide if they want to run in a marathon, in which case they will need to change their social contract. How they do that—through reduced pensions, lower wages, increased VAT, or through more effort to rein in Greek oligarchs—is a matter for the Greeks to decide. An international consortium, backed by a hysterical media, cannot micromanage Greece. The Greeks may well choose to let their standard of living gradually decline. That will be their choice.

Staying on the present course will mean that Greece will shuttle between the Emergency room and rehab. In particular, the idea of staggered relief is set to guarantee such an outcome. The debt forgiveness will come in driblets. It will be accompanied by indefinite pain for the Greeks and its creditors.

References

Dustmann, Christian, et al., 2014. “From Sick Man of Europe to Economic Superstar: Germany’s Resurgent Economy,” Journal of Economic Perspectives 28(1): 167-188.

Krugman, Paul, 1988, “Financing vs. Forgiving a Debt Overhang,” Journal of Development Economics 29:253-268.

The post written by Ashoka Mody.

June 13, 2015

The bailouts of 2007-2009

The latest issue of the Journal of Economic Perspectives had a very interesting symposium on the costs and benefits of the various bailouts implemented during the Great Recession.

The first article in the issue is by University of Chicago Professor Austan Goolsbee and Princeton Professor Alan Krueger. Goolsbee served on the President’s Council of Economic Advisers from March 2009 to August 2011, and Krueger spent much of 2009 to 2013 in the Treasury Department and CEA, so one might not expect them to be big critics of the policies. Their review is quite candid in communicating the misgivings that many of those in government had about the measures. Here’s Goolsbee and Krueger’s summary of the bottom line:

The US Treasury recovered a total of $39.7 billion from its investment of $51.0 billion in GM. By the end of 2014, Treasury sold its remaining stake in Ally Financial, recovering $19.6 billion from the original $17.2 billion investment in Ally, for a $2.4 billion gain for taxpayers. In May 2011, Chrysler repaid its outstanding loans from the Troubled Asset Relief Program (TARP) six years ahead of schedule. Chrysler returned $11.2 billion of the $12.5 billion it received through principal repayments, interest, and cancelled commitments, and the Treasury fully exited its connection with Chrysler.

And what did any of the rest of us gain from this?

Since bottoming at 623,300 jobs at the trough of the recession in June 2009, employment in the motor vehicles and parts manufacturing industry has increased by 256,000 jobs (as of July 2014). This is a stark contrast from the previous recovery, when jobs in the industry steadily declined. The increase in the number of jobs in motor vehicles and parts manufacturing accounted for nearly 60 percent of the total rise in manufacturing jobs in the recovery’s first five years. In addition, some 225,000 jobs have been added at motor vehicle and parts dealers. Counting both manufacturers and dealers, auto-related jobs accounted for 6 percent of the total 8.1 million jobs that were added, on net, in the first five years of the recovery—triple the sector’s 2 percent share of total employment.

The authors conclude:

It is fair to say that no one involved in the decision to rescue and restructure General Motors and Chrysler ever wanted to be in the position of bailing out failed companies or having the government own a majority stake in a major private company. We are both thrilled and relieved with the result: the automakers got back on their feet, which helped the recovery of the US economy. Indeed, the auto industry’s outsized contribution to the economic recovery has been one of the unexpected consequences of the government intervention.

The symposium also features an analysis of assistance to financial institutions under the Troubled Asset Relief Program (TARP) by Professord Charles Calomiris and Urooj Khan, both at Columbia. Calomiris is a prominent conservative economist, so one might have expected this review to be somewhat critical of the intervention. But the authors acknowledge the favorable bottom line:

For the most part, the [TARP] transactions with the banks, the focus of this paper, yielded a net cash flow gain. The net cash flow costs were largely from the assistance provided to AIG, the automotive industry, and the programs aimed at avoiding home mortgage foreclosures. The net cash flow gain estimated for the Cash Purchase Program was $16 billion with only $2 billion of preferred stock remaining outstanding. The CBO estimated a net cost of $15 billion to the Treasury for the assistance provided to AIG under the Systemically Significant Failing Institutions program. All of the supplementary support provided to Citigroup and Bank of America through the Targeted Investment Program had been paid back and resulted in a net gain of roughly $4 billion dollars to the federal government. Finally, the loss-sharing agreement with Citigroup through the Asset Guarantee Program yielded a net gain of $3.9 billion.

The authors review evidence for the benefits of these programs and find it difficult to make a definitive statement:

Following the announcement of the Capital Purchase Program on October 14, 2008, the first program of TARP announced in the pre-election phase, there were broad improvements in the credit markets. Between Friday, October 10 and Tuesday, October 14, the Standard and Poor’s 500 rose by 11 percent and the common stock prices of the nine large financial institutions that were the very first participants of TARP increased by 34 percent (Veronesi and Zingales 2010). From October 13, 2008 (before the announcement of the CPP) to September 30, 2009, the LIBOR rate fell by 446 basis points and TED spread fell by 434 basis points. Costs of credit and perceptions of risk declined significantly in corporate debt markets as well. By the end of September 2009, the Baa bond rate and spread had fallen by 263 and 205 basis points, respectively (US GAO 2009, p. 37)….

Using an event study analysis of bank enterprise values, Veronesi and Zingales (2010) analyze the effect of the initial announcement of TARP assistance to the financial sector. They estimate that the October 13, 2008, announcement resulted in a net social benefit to financial intermediaries, after subtracting the cost to taxpayers, of between $86 billion to $109 billion….

[But] Veronesi and Zingales (2010) underestimate the expected costs of TARP as of October 13, 2008. The first round of assistance provided to the big banks effectively committed the government to a “whatever it takes” approach to keep AIG, Citigroup, and Bank of America alive, and therefore, the continuing cost to taxpayers actually experienced in 2008–2012 was predictable, at least to some degree. In other words, if TARP assistance would be forthcoming (and more junior in form over time) in response to worsening bank condition, the recipients effectively possessed a put option from the government to issue equity in addition to the explicitly recognized preferred stock investments made by the government….

With regard to TARP’s gross benefits, a credible evaluation of the impact of TARP assistance to financial institutions remains elusive. First, it is difficult, if not impossible, to isolate the effects of TARP from other initiatives of the Federal Reserve, Federal Deposit Insurance Corporation, and other financial regulators, or from other influences on the economy unrelated to government programs. For example, on October 14, 2008, the Capital Purchase Program was announced jointly with the Fed’s Commercial Paper Funding Facility Program and FDIC’s Temporary Liquidity Guarantee Program. Furthermore, it is hard to know to what extent the financial markets would have stabilized and the economy would have recovered in the absence of an activist government response. Some have argued that government support for financial institutions during the crisis confused and frightened market participants and was itself possibly a net negative for the economy.

The Journal of Economic Perspectives symposium on the bailouts also included an analysis of the federal government assumption of conservatorship of mortgage giants Fannie Mae and Freddie Mac by Scott Frame of the Federal Reserve Bank of Atlanta and Andreas Fuster, Joseph Tracy, and James Vickery of the Federal Reserve Bank of New York. Here again the bottom line so far has been a net financial gain for the government:

As of end-2014, the cumulative Treasury dividend payments by Fannie Mae and Freddie Mac have now exceeded their draws: specifically, Fannie Mae has paid $134.5 billion in dividends in comparison to $116.1 billion in draws, while Freddie Mac has paid $91.0 billion in dividends in comparison to $71.3 billion in draws.

And what did ordinary citizens gain from this?

Was it important to promote mortgage supply during this period given the already high levels of outstanding US mortgage debt? We would argue “yes,” for two reasons. First, mortgage origination was necessary to enable refinancing of existing mortgages…. Second, continued mortgage supply enabled at least some households to make home purchases during a period of extreme weakness in the housing market.

And I have separately examined the Federal Reserve’s participation in emergency lending and concluded that the Fed came out making a profit from its intervention as well.

Like Calomiris and Khan, Frame and coauthors suggest that a positive net cash flow is not the right metric:

As an economic matter, one cannot simply compare nominal cash flows but must also take into account that the Treasury took on enormous risk when rescuing [Fannie and Freddie] in 2008 and should therefore earn a substantial risk premium, similar to what private investors would have required at the time, in addition to the regular required return.

Here I disagree. A key argument for intervention was that private risk premia at the time were too high. Prices of risky assets and the volume of risky lending were depressed by fire sales and a scramble for liquidity and safety, which posed a danger of pushing the economy deeper into crisis. Yes, the government was assuming risk in all these actions, risks that ultimately would have been borne by taxpayers. But taxpayers also faced a very real risk of falling revenues associated with a worsening economic downturn. The contributors of the symposium were all correct in emphasizing the risks the government took in making the bailouts, and I agree with their warnings that we should only enter into such ventures with great reluctance and careful evaluation of the costs and alternatives. But I think an objective observer would conclude that this time, at least, it all turned out well.

June 12, 2015

“The Top Ten Reasons Why Trade Agreements Should Not Cover Currency Manipulation”

Today we are fortunate to have a guest contribution written by Jeffrey Frankel, Harpel Professor of Capital Formation and Growth at Harvard University, and former Member of the Council of Economic Advisers, 1997-99. This post is an extended version of an earlier column at Project Syndicate.

President Obama is still pressing his campaign to obtain Trade Promotion Authority and use it to conclude negotiations across one ocean for the Trans Pacific Partnership (TPP), and then across the other ocean for the Transatlantic Trade and Investment Partnership (TTIP). Many in the Congress, particularly many Democrats, insist that the trade agreements must include mechanisms designed to prevent countries from manipulating their currencies for unfair advantage.

The President is right. The congressmen are wrong. More suitable venues for discussing exchange rate issues with our trading partners include the IMF, the G-20, the G-7, and bilateral negotiations.

Here are the top ten reasons why including currency manipulation language in the trade negotiations would be unwise.

If the US were to insist that “strong and enforceable currency disciplines” be part of trade negotiations, that would kill the negotiations. Other countries would not go along. And yet both the US and its trading partners stand to gain from these deals.

Other countries would not go along with the manipulation language for good reason: It is a bad idea. True, there are times when particular countries’ currencies can be judged undervalued or overvalued and times when their trading partners have a legitimate interest in raising the question with their governments. But even in those cases when the currency misalignment is relatively clear, trade agreements are not the right venue to address it. The undervalued RMB was addressed in bilateral China-US discussions, 2004-11, eventually with success. China allowed the currency to appreciate 35% over time. Today it is well within a normal range.

Most often it is impossible to tell whether a currency is overvalued or undervalued. Manipulation is not like the existence of a tariff or quota that can be verified by independent observers.

A necessary condition for a country to be judged as manipulating its currency is that the authorities are intervening in the foreign exchange market. The People’s Bank of China, for example, bought up a record quantity of dollars in exchange for renminbi from 2004 to 2014, and thereby kept its currency from appreciating as fast as it otherwise would have. But, in the first place, the Chinese aren’t doing that anymore. If anything, they have been selling dollars in exchange for renminbi over the last year, keeping the value the currency higher than it would otherwise be. (Accordingly China’s reserves peaked at $3.99 trillion in July 2014 and then declined to $3.73 trillion by April 2015.) The implication is that US congressmen who say they want China to stop manipulating the currency might be unhappy with the consequences if that happened. Under current conditions, the renminbi would weaken, not strengthen, and American firms would find themselves at more of a competitive disadvantage, not less.

In the second place, there are often legitimate reasons for intervening in the foreign exchange market, including even in cases of intervention to push the currency down. An example would be the overvalued dollar in 1985, when the US joined with Japan, Germany, and other G-7 countries in concerted intervention in the foreign exchange market –- associated with the Plaza Accord — to push the dollar down, bringing it off of a perch that at the time was much higher than where the dollar is today. Certainly intervening to prevent a currency from appreciating, which is what China did over the last decade, is not per se an illegitimate policy. Indeed a heavy majority of countries pursue either fixed exchange rates, exchange rate targets, or managed floating, all of which are legitimate policies that by definition entail buying and selling of foreign exchange to moderate or eliminate fluctuations in the exchange rate.

In the third place, China isn’t even in the TPP, nor in the TTIP, the two sets of trade negotiations in which the US is involved and for which President Obama wants Congress to give him Trade Promotion Authority.

Japan is in the TPP and it is true that the yen has depreciated a lot over the last year. Some US economic interests, particularly the auto industry, accuse Japan of manipulation to keep the yen unfairly undervalued. Many congressional critics cite Japan as the target of their proposals to insist that currency manipulation language be part of the TPP. But the last time the Bank of Japan intervened in the foreign exchange market was 2011. (This was an appropriate move, in the aftermath of its tsunami, to bring the yen down off a perch that was its post-war record high.) In 2013 Japan joined other G-7 countries in agreeing to a proposal from the Obama Treasury to refrain from foreign exchange intervention. The agreement is still in effect.

Similarly with Europe: members of the Eurozone are in the TTIP negotiations; the euro too has depreciated a lot over the last year; and some US trade critics accuse Europe of currency manipulation. But the European Central Bank has not intervened in the foreign exchange market since 2000, and that was to support the euro not depress it. The ECB was party to the 2013 agreement not to intervene as well.

The critics who accuse Japan and other countries of currency manipulation presumably know that they haven’t been intervening in the foreign exchange market in recent years. They generally point instead to recent loosening of monetary policy, such as the quantitative easing, i.e., the purchases of domestic bonds, that the Bank of Japan and the European Central Bank have prominently pursued with the predictable side effect of depreciating their currencies. But countries can hardly be enjoined from easing monetary policy when domestic economic conditions warrant, as was so obviously the case in Japan and Europe.

If monetary expansion does not merit the charge of currency manipulation just because it can be expected to keep the value of the currency lower than it would otherwise be, still less do other sorts of economic policies. Some have argued that even though the People’s Bank of China has stopped buying US and other foreign assets, China’s Sovereign Wealth Funds still do, and that this too counts as manipulation. But for China to put some of its saving abroad is a perfectly sensible and legitimate thing to do. The United States would worry if China and other countries did not want to buy its assets.

Moreover, think of the reductio ad absurdum. Every country makes policy decisions of many sorts every week, many of which can be expected to have an indirect side effect on the exchange rate in one direction or the other direction. (Often stupid policies are the ones that weaken the currency – think of Argentina, Russia, or Venezuela. But not always.) That a particular policy might have the effect of weakening the currency does not mean that the country is a manipulator.

Finally is the point that if legal language were written to include the actions of the major trading partners’ central banks that US congressmen accuse of currency manipulation, then it could also be applied the other direction, against the United States. This would not be a case of misusing a tool – which is common enough among trade remedy cases when interest groups lobby for protection against foreign competition. (An example is the use of Anti-Dumping measures that were originally supposed to address cases of predatory pricing.) Rather it would be a case of using the tool in precisely the way it was written to be used. The Fed adopted quantitative easing in 2008 in response to the weakening US economy, just as trading partners have done recently. It continued to pursue QE up until recently. This had the effect of depreciating the dollar from 2009 to 2011, prompting the same charges of “beggar thy neighbor policies” [allegations of attacks in a supposed currency war] that US congressmen now level against others.

In either direction, whether by the United States or against it, such charges are on shaky ground. Monetary stimulus in one country may even have a beneficial effect on the rest of the world, as its own restored income growth leads to increased imports from its trading partners. But in any case, other countries are free to adopt whatever monetary policy suits their own economic circumstances. Whether one considers charges levelled against the US in 2010, against its trading partners in 2015, or against some unknown defendant in the future, it would be asking for trouble to set up a trade agency or institution to rule on them.

[A shorter version of this column appeared in Project Syndicate.]

June 11, 2015

“Goodbye, Madison”

Josh Marshall of Talking Points Memo, on what he sees as the destruction of a great research university.

The crown jewel of the Wisconsin university system is the University of Wisconsin at Madison. It is one of the top research universities in the country and the world. With this move [ to strip tenure from professors], you will basically kiss that jewel goodbye. To me this is the more salient reality than whether you think academic tenure is a good thing or not in itself.

If this happens, over time, the professors who can will leave. And as the top flight scholars and researchers depart, so will the reputation of the institution. So will graduate students who want to study with them, the best undergrads, money that flows to prestigious scholarship. Don’t get me wrong. Not in a day or a year or even several years. But it will. If you don’t get this, you don’t understand the economy and incentive structure of university life.

In other news, Author of proposal to abolish Legislative Audit Bureau says it’s not a response to scathing WEDC audits. The Legislative Audit Bureau is the Wisconsin equivalent of the Federal government’s Government Accountability Office (GAO).

June 10, 2015

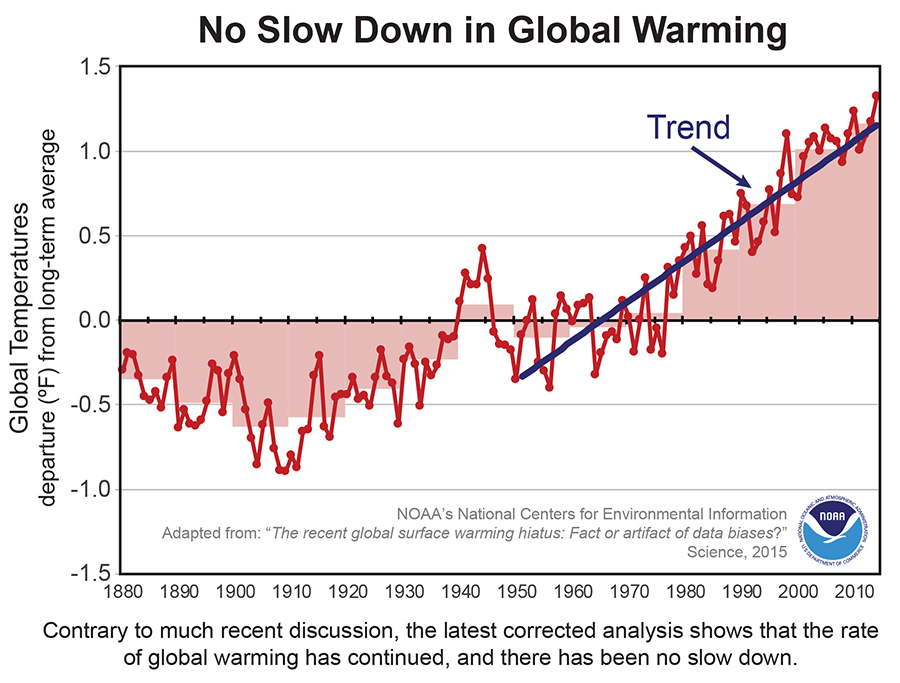

NOAA: “No Slowdown in Global Warming”

From NOAA:

“Adding in the last two years of global surface temperature data and other improvements in the quality of the observed record provide evidence that contradict the notion of a hiatus in recent global warming trends,” said Thomas R. Karl, L.H.D., Director, NOAA’s National Centers for Environmental Information. “Our new analysis suggests that the apparent hiatus may have been largely the result of limitations in past datasets, and that the rate of warming over the first 15 years of this century has, in fact, been as fast or faster than that seen over the last half of the 20th century.”

The report continues:

Since the release of the IPCC report, NOAA scientists have made significant improvements in the calculation of trends and now use a global surface temperature record that includes the most recent two years of data, 2013 and 2014–the hottest year on record. [Emphasis added]

See my previous post on 2014, and many comments disputing the assertion that 2014 is the hottest year measured.

Link to Science article, here.

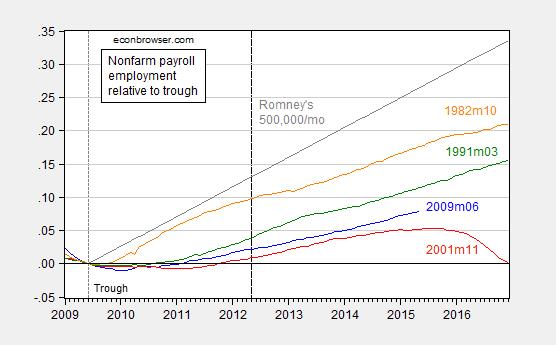

Norms for Employment Growth in Recoveries

Re-visiting Mitt Romney’s “We should be seeing numbers in the 500,000 jobs created per month.” [1]

Well, it’s clear 500,000/month is not the norm. Figure 1 presents employment growth (in logs) relative to trough in the last four recoveries. I have included a trend line implied by the 500,000/mo normalized by nonfarm payroll employment in May 2012 (when Governor Romney made the comment).

Figure 1: Log nonfarm payroll employment relative to 2009M06 trough (blue), to 2001M11 trough (red), to 1991M03 trough (green), 1982M10 trough (orange). Long dashed line at 2012M05 at the time of Governor Romney’s remarks. Source: BLS, May 2015 release, and author’s calculations.

The interesting point is that one has to go back three decades, and three recoveries, to get any numbers that are close to 500,000.

This leaves open the question of what is the expected pace of job creation. That in turn depends upon at the very minimum on (1) the pace economic activity generally, e.g., GDP growth, and (2) the labor intensity of GDP. Since GDP growth lower in the 1991 and 2001 recoveries than the in the preceding, slower employment growth seems a given, even if the employment/GDP ratio were constant (which it isn’t).

Some people will object that the preceding graph does not condition on the depth of the recession. This point is correct, but not a critique per se. The graph also does not condition on the labor intensity of output, nor any of the other determinants of GDP growth, such as financial crisis, or deleveraging. These points have been highlighted by Reinhart and Rogoff (discussed here).

June 9, 2015

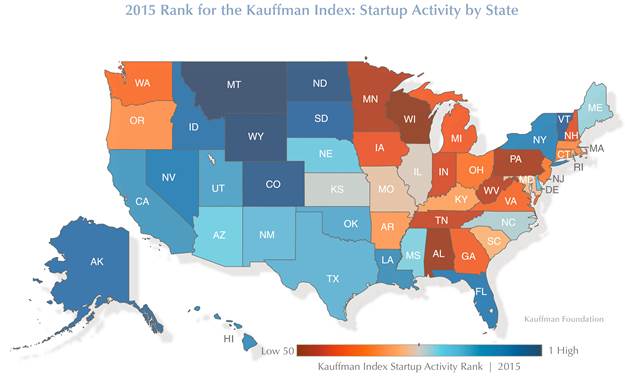

Wisconsin Economic Metrics: Entrepreneurship

From the Wisconsin Economic Development Corporation (WEDC) website:

We’ve [WEDC] put a greater focus on supporting high-growth entrepreneurs in Wisconsin. The Seed Accelerator program is supporting veterans, inner city Milwaukee and water technology businesses; and helping entrepreneurs get their ideas off the ground. …

The Kauffman Foundation’s most recent assessment indicates that progress on the entrepreneurship front is not in line with expectations: in 2015 it ranks Wisconsin at 50 (out of 50 states), falling five slots since the 2014 rankings. Here is a graphical depiction:

Source: Kauffman Foundation, State and Metro Trends.

I don’t take the decline in the rankings from 45th to 50th too seriously — in general rankings are not the ideal way to characterize relative performance. However, the fact that Wisconsin remains two consecutive years in the bottom quintile is suggestive that — at least according the Kauffman metrics — Wisconsin has not enjoyed a renaissance in entrepreneurship in recent years.

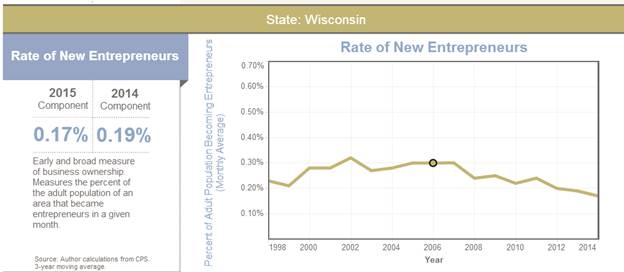

Here is a time series of one of the components, the rate of new entrepreneurs:

Source: Kauffman Foundation.

Notice that this series has been declining since 2011. The opportunity share is lower than 2011, while opportunity density (2012) is essentially flat.

In some ways, this outcome is unsurprising. The agency tasked to improve the entrepreneurial environment — WEDC — is Governor Walker’s flagship innovation to privatize the former Commerce Department. It has received criticism in recent months after writing off a $500,000 loan to a company that was a substantial contributor to Governor Walker’s political campaigns [1], in addition to a long string of bureaucratic problems, as outlined in the Legislative Audit Bureau [2] (Interestingly, two Republican assemblymen have just proposed eliminating the Legislative Audit Bureau [3]).

As an aside, the ALEC-Laffer document Rich States, Poor States 2015 ranks Wisconsin at 13th, rising from its 2011 ranking at 30th (2011 rank pertains to 2010 data). Hence, Wisconsin’s rate of new entrepreneurs seems to be inversely correlated with how highly ranked Wisconsin is, according to RSPS.

June 7, 2015

Ten years of Econbrowser

Last week marked the tenth anniversary of Econbrowser. That gives me an occasion to talk a little about why I started the blog and what we’ve accomplished with it.

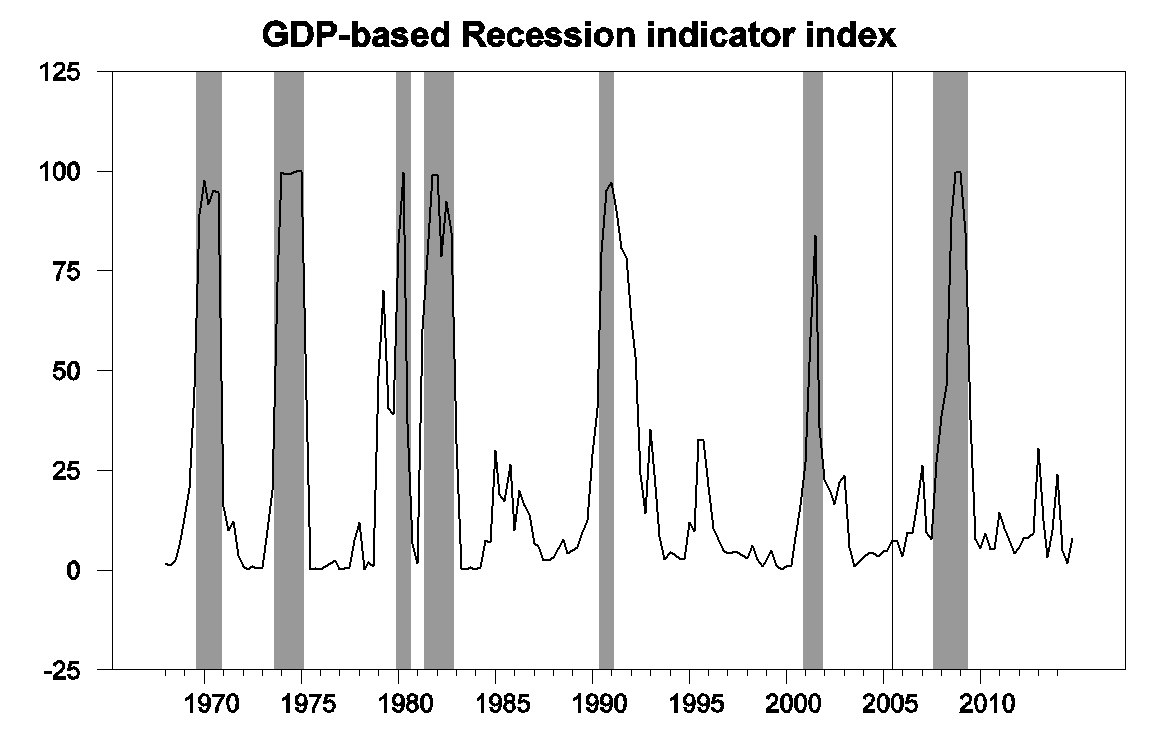

One of my goals was to bring a real-time dimension to academic research. Ten years ago I had just finished a research paper with U.C. Riverside Professor Marcelle Chauvet. We were suggesting a simple pattern-recognition algorithm for dating economic recessions that we thought would work with real-time data. One of the challenges to people making practical business or policy decisions is that the data keep getting revised. Many economists work with the numbers as they’re currently reported when they look for patterns in the data. But for our project we used an approach that was at the time a little unusual, assembling the different data sets as they had actually been reported at each separate quarter and month in history and seeing what the inference of our algorithm would have been at each date, something that’s very easy for anybody today to do using tools like ALFRED. This approach, which I might call “simulated real-time analysis,” suggested that our methods held promise. But it is one thing to look today at historical “real-time” data and say, “here is what I could have concluded at the time.” It is another thing to actually make the calls in real time. That’s one of the things we have been doing at Econbrowser.

The graph below is one example of that. It plots the Recession Indicator Index that we initiated ten years ago. Everything to the left of the vertical line is “simulated real-time analysis,” that is, what the algorithm would have concluded given only data as it had been reported at the time but with the analysis all conducted in 2005. The data the right of the line is what I would call “actual real-time analysis;” every one of those data points was published here at Econbrowser one quarter after the indicated date over a ten-year period.

GDP-based recession indicator index. Values to the right of the vertical line have each been publicly reported exactly one quarter after the indicated date, with 2014:Q4 the last date shown on the graph. Shaded regions represent the NBER’s dates for recessions, which dates were not used in any way in constructing the index, and which were sometimes not reported until two years after the date.

Another one of my goals for the blog was to open better dialog between academic economists, policy makers, and people outside of economics. I was very concerned– and remain so today– about how insular some of my academic colleagues can let themselves become, writing just for other economists using assumptions and conventions shared by other economists. I think it is a very healthy exercise to try to explain from scratch why we think what we do in a way that an intelligent person, who did not share any of the preconceptions or prejudices of academic economists, could follow and evaluate. Such an exercise can often uncover blind spots that the traditional academic protocol can miss. I was fortunate that Menzie Chinn had an interest in joining me in this effort almost from the very beginning, adding his expertise in international and other areas of economics and a passion for covering policy issues.

The blog in this way functions as a personal journal for me, as I try to make sense of what I see and learn from watching the real world unfold, sometimes contrary to my anticipations. Over the last decade we followed the financial strains associated with the housing bubble as they built, snapped, and continue to reverberate today. At the beginning I was definitely underestimating the full implications of what was going on. The biggest reason I was wrong about the bubble early on was a question about incentives– why would financial institutions and investors put hundreds of billions of dollars at risk with fundamentally unsound loans, I asked? Today I think the answer is a combination of misaligned incentives— the actors were often gambling with other people’s money– and a form of groupthink— it’s very hard to be the only person in your institution arguing that the profits everybody is making at the moment are going to come back to bite them very hard.

Another topic I changed my mind about was world oil supplies. I began as a skeptic about peak oil. My views evolved as I watched conventional oil production stagnate over the last decade. But I was surprised also at the success of the unconventional production from U.S. shale oil. It’s a little amusing that one of my posts from 2005 as well as 2015 were on the same topic, namely, what in the world is oil doing at $55/barrel? Though the first was asking why the price was so high, and the second why it was so low.

And it will be interesting to see which force will win out over the decade to come, as well as to gauge the ultimate success of unconventional monetary policy, and see what holds for the future of the U.S., European, and world economies. I’ll be sharing my thoughts on these issues, and listening to yours, right here at Econbowser.

Menzie David Chinn's Blog