Chris Dillow's Blog, page 14

April 14, 2021

Prince Philip & the communist ideal

One unintended and unremarked effect of the eulogies to Prince Philip is that they have reminded us of Marx���s vision of communism.

What I mean is that several of his admirers describe him as a ���renaissance man��� on account of his wide range of interests.

This, however, is an example of a common error ��� of ascribing to agency what is in fact the result of economic forces.

Prince Philip could afford to pursue so many different passions because the day he married the Queen he was freed from what Marx called ���the dull compulsion of economic relations.��� For most of the rest of us, however, this compulsion forces us to specialize, to develop just one skill to the detriment of other interests. Capitalism rests upon the division of labour. But as Adam Smith saw, this can destroy us:

The man whose whole life is spent in performing a few simple operations, of which the effects are perhaps always the same, or very nearly the same, has no occasion to exert his understanding or to exercise his invention in finding out expedients for removing difficulties which never occur. He naturally loses, therefore, the habit of such exertion, and generally becomes as stupid and ignorant as it is possible for a human creature to become. The torpor of his mind renders him not only incapable of relishing or bearing a part in any rational conversation, but of conceiving any generous, noble, or tender sentiment, and consequently of forming any just judgment concerning many even of the ordinary duties of private life. Of the great and extensive interests of his country he is altogether incapable of judging.

A man���s mastery of one skill, said Smith is ���acquired at the expense of his intellectual, social, and martial virtues.��� And there���s plenty of evidence for this. Think of William Shockley, Bobby Fischer, James Watson, Larry Summers, Morrissey, Richard Dawkins���.

In fact, the early history of capitalism was marked by workers��� fierce reluctance to devote long hours to doing just the one thing. Sidney Pollard (pdf) and E.P. Thompson (pdf) have documented how capitalists strove to instil an unnatural work discipline into their employees. As Pollard put it:

Men who were nonaccumulative, non-acquisitive, accustomed to work for subsistence, not for maximization of income, had to be made obedient to the cash stimulus, and obedient in such a way as to react precisely to the stimuli provided.

Of course, working conditions and hours have improved since Smith���s day and many people have internalized the capitalist work ethic. But not all of us. Research by Alex Bryson and George MacKerron has found that even people in good jobs are more miserable whilst at work than they are in any other activity bar being ill in bed. Which is why thousands of those who can afford to do so opt out of the rat race to do what Prince Philip could do ��� pursue a variety of interests. One reason why I���m looking forward to retiring (next year, I hope) is that I want to spend more time reading, gardening, learning music and learning Italian.

Which is where Marx comes in. His vision of communism was one in which the division of labour no longer suppressed our development as Smith thought it did. (Marx, of course, had read Smith much better than have today���s admirers of him):

As soon as the distribution of labour comes into being, each man has a particular, exclusive sphere of activity, which is forced upon him and from which he cannot escape. He is a hunter, a fisherman, a herdsman, or a critical critic, and must remain so if he does not want to lose his means of livelihood; while in communist society, where nobody has one exclusive sphere of activity but each can become accomplished in any branch he wishes, society regulates the general production and thus makes it possible for me to do one thing today and another tomorrow, to hunt in the morning, fish in the afternoon, rear cattle in the evening, criticise after dinner, just as I have a mind, without ever becoming hunter, fisherman, herdsman or critic.

You might object that Marx���s vision was one of a society of (surprisingly bucolic) dilettantes. That misses the point ��� that in communist society you will be able to pursue just one activity if you want: you���ll be free to choose.

Yes, free. Marx���s main beef with capitalism was not so much that it was unfair but that it generated unfreedom by alienating us from our nature. As William Clare Roberts puts it, capital ���bends labour power to an alien and unnatural end.��� Marx, says Clare Roberts, was a theorist of freedom.

Those of us who are rich enough can step away from the alienating and repressive division of labour by retiring early ��� although of course not without damage. But is what���s possible for a privileged few possible for all?

Only in a sufficiently developed economy. Marx thought that a particular level of affluence was necessary for communism, and that whilst capitalism could provide the potential for this affluence, it would not fully realize that potential and that there would come a time when capitalism ceased to develop productive forces but instead held them back. It would, he thought, require communism to allow that potential to be realized for everybody. Aaron Bastani���s ���fully automated luxury communism��� is in this tradition.

Whether this is feasible is of course another matter. The answer lies in the outcome of the race between technical change and diminishing returns and rising rents, and personally I think forecasting the former is a mug���s game.

For my purposes, though, this isn���t the point. I merely want to point to a nice irony ��� that Prince Philip���s eulogists have, perhaps inadvertently, made the case for Marx���s vision of communism.

April 10, 2021

The need for institutional brains

���The trouble with you, son��� said Bill Shankly to a young player ���is that your brains are all in your head.��� I was reminded of this line from the great man by reading Ian Leslie���s Conflicted, on how to have more productive arguments.

His advice is good: define exactly what the disagreement is about; make your interlocutor feel good and secure; acknowledge your own uncertainties; be less tribal; and so on.

In the heat of argument and when the teacups are flying, however, it is easy to forget these principles. We then have what the ancient Greeks called the problem of akrasia, of lack of self-control. Just because we know the right thing to do does not ensure that we���ll actually do it; even self-confessed ���moderates��� are apt to forget their own advice on how to argue well.

This is what Shankly was getting at. He wanted players who were so well-drilled and who had such muscle memory that they did the right things in the heat of battle instinctively, without thinking. Ditto musicians, who must know a piece so well that they can perform it without conscious deliberation.

In such cases, we need our brains not in our heads but in our feet or fingers.

But brains need not and should not be confined to our bodies. They can, and should, and sometimes do, reside elsewhere.

One place is in our habits. I invest into tracker funds by direct debit each month. Most of my investment is done without thinking.

Strictly speaking, this isn���t optimal: stock markets aren���t fully efficient and tracker funds can be beaten by momentum and defensive stocks (pdf) (but, I suspect, not by any other strategy). Implementing such strategies, however, would require me to think. And if I did that I���d fall prey to the gazillion cognitive biases that I warn IC readers against.

My habit, therefore, saves me from error in the same way that Ulysses tied himself to the mast of his ship to save himself from steering it onto the rocks. Government who have made their central banks operationally independent have done a similar thing: in renouncing control of interest rates they have given up the temptation to change them for political rather than economic reasons.

In ways such as these, we protect ourselves from akrasia by taking our brains out of our head and placing them into habits or institutions.

These aren���t the only examples of intelligence being embedded in institutions. No single individual knows how to build a jet plane. But Boeing does. Good companies have brains that no individual has. This is organizational capital. If there is a justification for the high valuations on big tech companies, it lies in this capital. I���d suggest that the Tory party is an example of this. Each individual in the party is cognitively limited. But the party as an organization has a fearsome ability to reinvent itself and win elections.

Companies aren���t the only institutions in which intelligence can exist. Take this observation from P.J. O���Rourke in 1998:

Why do some places prosper and thrive while others just suck? It's not a matter of brains. No part of the earth (with the possible exception of Brentwood) is dumber than Beverly Hills, and the residents are wading in gravy. In Russia, meanwhile, where chess is a spectator sport, they're boiling stones for soup.

The difference, of course, lies in institutions. The people of Beverly Hills have for decades had institutions which make best use of their limited brain-power, not least of these being moderately well-functioning markets. Russians, however, have not enjoyed these. Their tragedy has been (and still is) that their brains were all in their head.

This is why I can���t work up any enthusiasm for the idea that genetic editing could increase our intelligence. What we need is not more brains in our head, but in our institutions ��� ways of making better use of what intellect we have. Without such institutions, high IQ people merely become efficient rent-gatherers, to the detriment of society.

Which brings me back to Leslie. The question is: do we have the institutions which embed the principles he advocates?

I suspect not.

Yes, any well-run company should organize its meetings in a way to embed his ideas ��� and if they are not doing so already they should.

In public discourse, however, such institutions are absent. Any guest on one of the BBC���s many moron-yak shows who followed Leslie���s advice to show humility, introduce novelty or make their interlocutor feel good would probably not be invited back. Unproductive slanging matches are ���good��� TV and radio.

The point generalizes. Our ���marketplace in ideas��� is obviously broken. Not only does it not exclude bad arguments, or ones in bad faith, but it actually favours bare-faced lies and (to paraphrase Burke) the noise of half a dozen grasshoppers over the silence of thousands of great cattle,

What we have in public discourse is not the institutionalized intelligence that has made Beverly Hills or Boeing prosper, but institutionalized stupidity.

It need not be so. We could have institutions (pdf) of deliberative democracy such as citizens��� assemblies and rules about admissible evidence which would embed some of Leslie���s suggestions: ���a set of agreed norms and boundaries that support self-expression���; not trying to control one���s interlocutor; establishing trust; valuing challenges to the consensus; ensuring that you understand your interlocutor; and so on.

But of course, a big reason why we don���t have such institutions is that our current media-political system suits those in power just fine.

And herein lies a problem. What does it mean to have a productive argument? It could be a way of reaching the truth. Or it could be a way of clearing the air so that colleagues and partners can get along better. Leslie���s book is aimed more at the latter: its subtitle is ���Why arguments are tearing us apart and how they can bring us together.���

But there can be a trade-off here. The truth could be that your partner is a lazy lying cheat and you could do better for yourself. Sometimes, we���re better off not being brought together but rather ending toxic relationships ��� yes, cancelling people. I doubt that Leslie wants to have productive arguments with, say, anti-semites or fanatical Islamists.

Which leads me to a cynical thought. In a world of huge inequality of power in which we lack institutions which embed good rules of argument, there���s a danger that Leslie���s call for us to be reasonable merely means us accepting injustice, inefficiency and dishonesty.

March 27, 2021

Complicated motives

This week Boris Johnson claimed that the roll-out of the vaccine was the result of capitalism and greed; Goldman Sachs workers complained about long hours; and I got my jab. There���s a link here. All three episodes shed light on the role of motivations.

Johnson is of course wrong. The Oxford vaccine was discovered by academics and is being produced by AstraZeneca at cost, and the Biontech vaccine was discovered by people who were already billionaires. It���s nearer the truth to say that the vaccines��� discovers were motivated less by greed and more by intellectual curiosity. And this, of course, is only one of countless motives, which include pride, ego, loyalty to colleagues, force of habit, fear of failure, peer pressure, altruism, and so on.

And these non-financial motives are powerful things. The vaccine roll-out has been conducted with impressive efficiency by people who were working either for nothing or for lowish wages. That contrasts with the failure of Test and Trace which has spent millions on expensive consultants. A sense of vocation or of doing good can produce better results than the cash nexus: this is why workers in the public sector are more likely to do unpaid overtime than those in the private sector.

Of course, money matters; it is what gets workers through the door. But whilst it is usually necessary to get a job done, it is not sufficient to get it done well, at least where contracts and worker supervision are incomplete. Instead, it gives us workers who, as Homer Simpson says, go in every day and do it really half-assed. Those Goldman Sachs employees who leave before getting their bonus remind us that we need more than money to induce us to work long hours.

Which brings us to the problem. Trying to motivate people by appealing to their greed can crowd out these many other motives (pdf). Don Revie discovered this in 1974 when he became England manager and proudly announced to the team that he���d raised their appearance money. He immediately lost the respect of players such as Emlyn Hughes who would have paid for the privilege of playing for England.

In the same vein, high-powered bonuses encourage bankers to take on too much risk. Or they encourage managers to focus on what can be measured (such as the next quarter���s earnings) rather than important things that cannot such as innovative activity or a good corporate culture, as Jean Tirole and Roland Benabou have shown (pdf). High CEO pay can incentivize office politics and selfishness as senior bosses jockey for the top job. And as John Kay showed in his book, Obliquity, companies such as ICI and Boeing were more profitable when they focused on making chemicals and planes than when they shifted to focusing on shareholder value.

There are several different mechanisms causing crowding out. One is a selection effect: if you offer big pay you���ll tend to attract people who are motivated by money who might well be more selfish and less moral than others. Also, financial incentives change people���s self-identity. The man who thinks ���I���m a prudent banker��� won���t take reckless risks but the one who thinks ���I could get a big bonus��� will. And then there���s the risk of a loss of reciprocity: if all you are offering is money, workers are less likely to feel respect or loyalty to you, as Emlyn Hughes demonstrated.

All this might explain two big facts. One is the serial failure of government outsourcing. Subcontracting replaces what Julian Le Grand called ���knightly motives��� (pdf) such as public service with the cash nexus. The other is that labour productivity has slumped as neoliberal management has spread, with its emphasis on target and incentives rather than other motives.

But, but, but. The crowding out of intrinsic motives by cash incentives is only part of the story. It���s also the case that financial motives can crowd in these other motives, as Sam Bowles has shown (pdf). This is the message of George Akerlof���s classic paper (pdf), Labour contracts as partial gift exchange. Good pay can sometimes promote reciprocity and hence get workers to put in more effort than necessary. It also allows workers to focus more on their jobs because they are less worried about money. Or financial incentives can serve as signals: a small tax on plastic bags, for example, told us all to use less plastic.

It cuts both ways.

You might think this just shows the weakness of economics. When done properly, it often concludes: ���it all depends.���

But there is a strong message here. It���s that the network of motivations within any organization is a delicate eco-system which is sensitive to context. Any manager who blunders in with faux-cynical theories of human behaviour like Johnson���s risks destroying this system. Sometimes ��� and only sometimes ��� things are more complicated than they seem.

March 18, 2021

The paradox of financial innovation

Back in 1964 Kenneth Arrow showed that, in theory, competitive markets could produce optimal allocations as long as there were state-contingent securities which allowed people to trade risks and so insure against them. The problem is, he said, that:

Many of the economic institutions which would be needed to carry out the competitive allocation in the case of uncertainty are in fact lacking.

Almost thirty years later, Robert Shiller showed that this remained the case. ���The insurance industry has not devised policies that insure against many���causes of fluctuations in incomes��� he wrote in Macro Markets in 1993.

He proposed creating GDP-linked securities which people who were optimistic about economic growth could buy whilst those worried about recession could go short. This would allow ordinary people to buy (via insurance companies (pdf)) insurance against recession. In the same spirit, he showed, securities could be created whose prices were linked to the incomes of specific occupations. These would serve a signalling function, showing young people which jobs to enter and which avoid, and an insurance role, allowing people to hedge the risk of a decline in demand for their skills. And, he added, we could also have house price futures. Young people who fear not being able to get on the "housing ladder" could buy these as insurance against rising prices, whilst people worried about falling prices (such as Buy-to-Let landlords or those planning on downsizing) could go short.

In ways such as these, financial markets could help people spread risk better.

But almost sixty years after Arrow and thirty after Shiller, such markets still don���t exist or do so in still-rudimentary form. Judged by the standard of Arrow���s ideal of complete state-contingent markets, we���ve seen astoundingly little useful financial innovation during my long lifetime. And this is not to mention the other failures of the financial system such as its tendency to generate crises; to commit crime; to mis-sell useless products; and (in the UK at least) fail to finance industry: for every pound that UK banks have lent to non-property SMEs, they have lent ��11 in residential mortgages.

What we have seen in recent years, though, is a lot of innovation of dubious utility such as non-fungible tokens, special purpose acquisition companies, initial coin offerings, platforms to facilitate the mug���s game that is day-trading, and Mintme���s plan for people to issue tokens in themselves. And then there is the fact that it is not obvious what (lawful) need is fulfilled by cryptocurrencies.

Why, then, do we have so little useful innovation and so much useless?

It���s because of a collective action problem. Imagine we had a thriving market in, say, house price futures. Who���d gain? The main beneficiaries would be ordinary people who could trade away their house price risks. Those who devised the securities, however, would get only origination fees, which should in principle be bid down as other firms entered the market.

And markets don���t spring up from nothing. In his excellent An Engine Not a Camera Donald MacKenzie describes how Leo Melamed, head of the CME, encouraged growth of stock index futures, one of the few examples of useful financial innovation. A market, said Melamed, ���is more than a bright idea. It takes planning, calculation, arm-twisting and tenacity to get a market up and going. Even when it���s chugging along, it has to be cranked and pushed.��� In other words, it requires somebody to solve a collective action problem. Markets must be liquid but liquidity is a collective good: it requires many traders to come together.

Financial innovation, therefore, suffers from the problem described by William Nordhaus ��� that producers of new innovations capture only a ���minuscule fraction��� of their social gains. Which means that innovation is under-provided by the market.

What���s not under-provided, however, are forms of innovation in which innovators can extract big rewards. And these come from being able to, in Keynes��� words, ���pass the bad, or depreciating, half-crown to the other fellow.���

What we have here, then, is a simple failure of capitalism ��� the fact that the pursuit of private profit prevents the fulfilment of genuine social need. Mariana Mazzucato���s point that the state can be a source of innovation applies especially to finance. State ownership of financial institutions might be necessary to solve the collective action problem that blocks useful innovation. One could imagine state-owned banks originating GDP or occupation-based securities which the government then gives to everybody as part of people���s QE. When I say state ownership, I mean ownership that forces banks to become providers of public service (and not just in the context of improving financial innovation) rather than the botched nationalizations of 2008 that left the monkeys in charge of the zoo.

You might think this is a Marxian demand. In this context, though, it���s not. There���s a tradition in Marx (which I���m not wholly comfortable with) which sees markets as irrational, alienating and sources of chaos and unfreedom. Advocating more financial markets is therefore unMarxist. What it is, though, is bog-standard orthodox economics. If we really want to achieve the fundamental theorem of general equilibrium economics in which free markets are Pareto-optimal, we need more complete markets ��� and this requires state ownership and control of banks.

Which gives us a delightful paradox ��� that in a sense, conventional economics is more radical than Marxism.

March 10, 2021

On Hans in Luck effects

In the Brothers Grimm fairy tale, Hans in Luck, the protagonist starts with a lump of gold but ends up with nothing after a number of trades each of which seems reasonable on its own. This is a metaphor for a lot of behaviour in politics and economics.

The point is that you cannot always judge an outcome by the individual actions that lead to it. Each action Hans takes is understandable in itself but their cumulative effect is to impoverish him*. Which is an example of the Sorites paradox. If you take a grain of wheat you���ve got next to nothing but if you do so often enough you���ll eventually have a silo full of the stuff.

The fund management business operates on this principle. A modest annual management charge looks like a single grain of wheat, not worth noticing. But if you take it every year it eventually adds up to a silo full. An extra half percentage point a year in fees can easily compound over ten years to a charge of over ��750 on every ��10,000 invested. There���s a reason why fund managers are rich, and it���s not because of their investment skill.

Similar things happen in politics.

For example, any individual tax break might seem reasonable. But their cumulative effect is to produce an overly complex tax system which diverts entrepreneurial effort away from productive activity and towards tax planning and which merely enriches lawyers and accountants.

Ditto other fiscal measures. If a man gets a job with some boondoggle, he���ll feel grateful to the Chancellor for creating it. But if he gets a job because of good macroeconomic conditions he���ll feel less gratitude because it���s harder to link his good fortune to the Chancellor���s actions. In this way, Chancellors are incentivized to come up with gimmicks such as freeports rather than to focus upon proper macroeconomic management. Each individual boondoggle looks reasonable, but the aggregate effect is a political culture which devalues good macro policy and overvalues gimmicks.

Perhaps Brexit fits this pattern too. A bit of extra paperwork is only a small hassle, and who cares about prawn exporters anyway? But a small friction here, a small one there, plus macroeconomically imperceptible year-on-year impacts on productivity and innovation, eventually add up to something significant (pdf).

Yet other examples of Hans in Luck effects might be found in the Labour party. Many on the left have been perplexed by the fact that whilst most Labour economic policies in 2019 were popular on their own, in totality they were not. A similar thing might be true of Starmer���s use of focus groups. In any individual case, it seems reasonable to use such groups. But the total effect could be to alienate voters by giving the impression of somebody who lacks his own ideas or convictions.

Some forms of racism also look like Hans in Luck effects. Victims of racism often speak of a ���drip, drip��� effect. Any individual remark might seem innocuous to a white person: ���why are you so touchy?���. And any single hiring of a white person over one of colour might seem a reasonable marginal decision. But the totality of remarks and marginal decisions and mild stereotyping adds up to something wholly different ��� systematic racism which is experienced as stressful and exhausting.

Which is why I agree with those who have criticized the Society of Editors��� claim that the press is not racist.

Let���s take the now-notorious contrast between the press���s coverage of Meghan and Kate. When Kate touches her pregnancy bump, she ���tenderly cradles��� it whereas when Meghan does so it is a show of ���pride and vanity.��� And so on. If we take each case individually, it seems hard to read racism into it unless you are predisposed to find it. If, however, you look at the totality of editorial judgments a clear pattern of systemic double standards emerges. As in the Hans in Luck story, innocuous individual decisions cumulate to something nasty.

In this context the Society of Editors��� denial of racism perhaps reveals a different kind of media bias ��� a failure to see the wood for the trees. If you look only at stories in isolation, as journalists tend to do, you can miss the pattern. To do that, you need a form of sociological imagination ��� the ability to pan out and see the big picture which is not necessarily the sum of the parts. But journalists are not trained in the sociological imagination. That���s part of their deformation professionnelle. There are therefore limits to what you can learn about society from even good journalism. And that is why we need social science.

* The opposite is also possible. Kyle MacDonald famously traded a paperclip for a house. That could be a metaphor for the story of economic growth.

March 5, 2021

The left after the Budget

Labour���s reaction to this week���s Budget has been widely criticised. James Meadway accuses it of not offering an adequate alternative. He���s right. But there are in fact profound flaws in the Budget which Labour should be pointing out.

One is the failure to address acute poverty. Sunak is planning to cut universal credit payments later this year. That, says (pdf) the Resolution Foundation, will be ���disastrous for family incomes��� and ���bad macroeconomics��� as it is taking cash out of the economy at a time when unemployment is likely to be high. This isn���t an isolated error. In delaying the extension to the furlough scheme last autumn Sunak needlessly destroyed jobs. His failure to ensure adequate sick pay has not only impoverished people but jeopardised their health by compelling Covid-positive people to carry on working. And hundreds of thousands of the self-employed have had no help at all. This government is no friend to the economically insecure.

It is, however, heedful of grifters and cronies. Free ports are a gimmick that���ll only divert jobs from nearby areas whilst encouraging (pdf) money laundering and tax evasion. The towns fund is a giveaway to areas with Tory MPs, and the business people who benefit disproportionately from it will in all likelihood be those well acquainted with those MPs. And super-deductions for capital spending will not only cause Amazon to pay no tax at all but encourage boondoggles in which companies spend government money solely to reduce their tax bill. When added to the PPE contracts handed out to cronies, all this adds up to a pattern. Governments often take their character from the Prime Minister, and Johnson is fundamentally dishonest.

There���s also the failure to respond to climate change. We should read the freezing of fuel duty alongside the PAC���s report that the government has no plan for achieving zero net carbon. There���s a case for shifting taxes from incomes to carbon. The government misses it.

In planning a fiscal tightening for 2023, the government might also be tightening policy prematurely, which Simon says is ���crazy.��� On current forecasts, it will do this whilst official unemployment is over five per cent ��� a figure which grossly under-estimates the slack in the labour market: there are almost two million outside the workforce who want a job and even before the pandemic there were millions of under-employed. The fact that the government feels the need to tighten at a time of mass unemployment is an admission that it believes full employment is either impossible or undesirable.

But there���s something else. The OBR says that by 2025 the share of taxes in GDP will have risen to its highest since the late 60s. But we���ll not have the public services to show for it. The Resolution Foundation says that ���by 2024-25, day to day public service spending per capita in unprotected departments will still be almost one-quarter lower than in 2009-10.��� And even in the NHS, spending probably won���t increase sufficiently to clear the backlog of operations created by the pandemic. We therefore face not only high taxes by a crumbling judicial system, minimal local government services, patchy social care and long NHS waiting lists.

We used to think we had a choice between high taxes and good public services on the one hand or low taxes and poor services on the other. The Tories are delivering the worst of both ��� high taxes and shoddy services.

A big reason for this is simply that the economy isn���t growing fast enough. The OBR forecasts that after 2022���s spurt GDP growth will fall below two per cent, one reason for this being that productivity growth will remain poor (and remember ��� the OBR has consistently been too optimistic about this in the past).

Which tells us that the Tories have failed to address our productivity problem. I���ve recently suggested ways to do this, but I���d highlight two of them.

One is to address the problem of high rents. These depress productivity for example by incentivizing speculation over productive entrepreneurship and by squeezing corporate and personal incomes. One solution to this would be to disincentivize such speculation by a land value tax. If the same tax were levied on an empty building as an occupied one, bargaining power would shift from landlord to tenant. (Of course, attacking rentierism requires more than the tax system: one case for more fiscal loosening is that this would raise interest rates, thereby depressing land prices).

It would be good economics as well as good politics for Labour to drive a wedge between rent-seekers and entrepreneurs, forcing the Tories to show whose side they are on.

A further suite of measures to raise productivity would of course be to democratize the economy; we know that neoliberal managerialism has depressed productivity and that worker coops can raise it. As Joe Guinan and Martin O���Neill have argued, such democratization could have been part of an economic rescue package.

I mention these because they are lines of policy which the Tories, for all their flexibility, are incapable of following. As Phil says, the Tories flexibility is only ���a means of defending the class relations they stand on.��� These class relations, however, lead not only to inadequate support for the insecure and to cronyism, but also to a failure to see both the need and the means to restore economic dynamism. The left should be pointing out that the Tories��� class interests are part of our economic problem and cannot be the solution to it ��� a fact only highlighted by Sunak���s Budget.

March 2, 2021

A defence of maths in economics

What���s the point of maths in economics? I ask because of this:

Much of the mathematics used in economics is simply performance. Despite the sometimes undue attention given to mathematical methods, the actual mathematics economists use often contradicts their economic conclusions. The mathematics in economics is simply a tool to keep out outsiders: economists themselves do not take it that seriously.

I suspect this is sometimes (often?) true. But I want to give a counter-example. It comes from a source some of you don���t like, John Cochrane. It���s this equation (pdf) for predicting long-run returns on assets relative to returns on cash:

ER = RA x SDa x SDbg x corr (a, bg)

Where RA is a coefficient of risk aversion, SDa is the standard deviation of asset returns, SDbg is the volatility of background risk, and corr(a, bg) is the correlation between asset returns and background risk. The intuition here is simple. High expected returns should be compensation for higher risk or for a higher distaste for risk. And the risk that matters isn���t just the volatility of the asset, but its correlation with our background risks ��� the risks to our job or business. An asset that falls when we lose our job or business is much riskier than one that holds up well in bad times, and so must pay us higher returns on average to compensate us.

Now, the derivation of this is quite tricky: see the appendix to Cochrane���s paper. But once something has been derived once, it stays derived. Working through the derivations might be useful for torturing students, but the rest of us can skip them and get to the meat.

We can apply this equation to any asset. I suspect it has done a decent job of explaining long-run returns on UK housing, for example.

Let���s put some numbers on this for equities. The coefficient of risk aversion varies across individuals, across time, and from context to context, but let���s call it three (pdf), where one betokens indifference to risk. The standard deviation of annual equity returns has been 15% (or 0.15) since 1985. The volatility of background risk ��� how likely we are to lose our job or business ��� is hard to measure and varies from person to person, but let���s call it 0.1 for illustrative purposes. Corr (a, bg) also varies from person to person. For most of us, though, it���s positive: we know this because shares fall in recessions. Let���s call it 0.4.

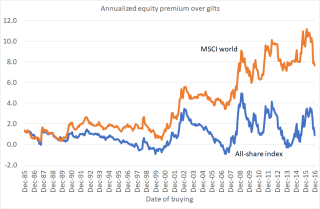

We can then multiply these numbers through: 3 x 0.15 x 0.1 x 0.4 = 0.018. Which tells us we should expect equities to out-perform safe assets by 1.8 percentage points a year on average over the long-term.

My chart shows how this compares to reality. It shows that unless you had bought at the right time (such as after the bursting of the tech bubble or at the low point of the 2009 crisis) you���d have earned an equity premium of less than this on the All-share index. For the MSCI world index, however, the equity premium for pretty much any period in the 90s was very close to this prediction. Thanks to the boom in US equities, though, the premium has been more than this for most of this century.

Which represents a return to history. Back in 1985 Rajnish Mehra and Ed Prescott pointed out ��� based on this sort of thinking ��� that equities had done better (pdf) than they should for much of the 20th century.

Why? Herein lies one virtue of this equation. It is sufficiently clear and parsimonious for us to ask: what does it leave out?

One thing is disaster risk. The (not so small) risk of a catastrophe (pdf) justified higher expected returns on equities for much of the 20th century ��� especially for investors who were loss-averse. Another thing is market imperfections. Roger Farmer has pointed out (pdf) that many of the young are excluded from stock markets by borrowing constraints. That causes shares to be cheaper than they should be and riskier too ��� because such people cannot buy when prices fall. Which justifies higher returns.

I���d highlight several merits of this equation - ones which give us criteria by which to assess when maths is useful in economics.

First, it is simple enough to be useful. If we need Matlab to solve equations, they are too complicated for us to fully understand and manipulate. The maths then becomes ���a tool to keep out outsiders���, and to prevent them following what���s going on.

Secondly, this equation allows reverse engineering. If people expect high returns, we can ask: what terms on the right hand side of the equation justify this? We need high expected returns on Bitcoin, for example, because the thing is so damned volatile and ��� as its fall last March showed ��� correlated with background risk.

Thirdly, maths can be useful without precise numbers - as my illustration showed. As the late Thomas Mayer said, there���s a trade-off between truth and precision. Equations are ways of organizing our thinking. They allow us to ask: what is it that we need to know? What might be missing from this equation? But it is only equations that are simple that allow us to do this.

Finally, this equation is useful for individuals. Economics should not be confined to academia, nor is it a subsidiary of politics. It should instead help people in their everyday life. Which is what this equation does. It draws our attention to an important fact. If you have low background risk ��� say because you���re in a safe job or have retired on a big final salary pension ��� you are better able to take on risks which are correlated with that risk than others. Assets that fall in recessions are less risky for you than they are for people who might lose their jobs in such recessions. You can therefore pick up a risk premium in normal times for taking on a risk that doesn���t bother you. Which means you���re getting something for nothing.

Now, imagine you retire from a job that you could lose in a downturn and take a final salary pension. Your background risk falls. So you���re better placed to take the recession risk which equities carry. Which means that you should own more shares when you are old than when you were younger. For you, the conventional financial advice that people should own fewer shares as they age is flat wrong. Which poses the question: if financial advisers are wrong on this, what else might they be wrong about?

Apparently arid mathematical economics can therefore sometimes undermine orthodoxy and vested interests.

February 25, 2021

Noise, interests & democracy

Tim Fenton writes here about Tracy Ann Oberman���s ���faux victimhood���. I don���t want to get into this particular case, but the concept of faux victimhood is surely a useful one. And it highlights a problem with actually-existing liberal democracy.

The problem is that what gets heard is not necessarily a guide to what really matters.

People with a sense of faux victimhood make a lot of noise. The old saying is true: ���when you're accustomed to privilege, equality feels like oppression." This is why some white people feel victimized by Black Lives Matter, or why some men feel victimized by feminists. And it���s what gives us complaints about people being ���cancelled��� when in fact their only fate is to be reduced to writing for the Telegraph. It���s the stone in the show that gets noticed. And gets complained about. Faux victimhood leads to noisy but unwarranted demands*.

Such noise pushes trivial complaints up the agenda, such as about ���wokeness��� or ���cancel culture��� or how the British Empire is taught. Brexit is perhaps the best example of this: before around 2015 only a tiny minority cared (pdf) much about the EU. But it was a noisy minority.

The flipside of some people making more noise than their grievances justify is that others are too quiet. Amartya Sen has expressed this beautifully:

A person who has had a life of misfortune, with very little opportunity, and rather little hope, may be more easily reconciled to deprivations than others reared in more fortunate and affluent circumstances���The hopeless beggar, the precarious landless labourer, the dominated housewife, the hardened unemployed or the over-exhausted coolie may all take pleasure in small mercies, and manage to suppress intense suffering for the necessity of continuing survival. (On Ethics and Economics, p45).

This juxtaposition means that democratic politics is a poor way of addressing real needs. It attaches too much weight to noisy but trivial complaints and insufficient weight to quiet but genuine suffering. It means that politics becomes not a matter of improving people���s lives but a mere game.

My point here is actually about that basic idea in statistics, sampling bias: what we hear is a biased sample of what there really is, and of what matters. As Edmund Burke said:

Because half a dozen grasshoppers under a fern make the field ring with their importunate chink, whilst thousands of great cattle, reposed beneath the shadow of the British oak, chew the cud and are silent, pray do not imagine that those who make the noise are the only inhabitants of the field.

Anybody who has tried to chair a meeting should know this. Any decent chairman should ensure that all voices are heard. Just because somebody is quiet does not mean they���ve nothing worth saying. And just because they talk a lot does not mean their voice should carry weight.

And yet our political-media institutions do the exact opposite of this. The media amplifies noisy vacuous complaints whilst underplaying genuine ones: columnists are disproportionately higher-rate tax-payers rather than users of foodbanks. And of course there are countless ways in which the noisy rich exercise undue influence over politics ��� for example through funding political parties and lobbying; implicitly threatening to withdraw market confidence; or just plain deference. As Martin Gilens and Benjamin Page (pdf) and Pablo Torija Jimenez have documented, capitalist ���democracy��� serves the interests of elites.

But this is the precise opposite of what we need. A proper democracy ��� in the sense of giving equal weight to each individual ��� would act like a good chairman, ensuring that quiet people���s views and interests were heard as much as noisy ones���. Such a democracy requires institutions that lean against the human tendency to reconcile ourselves to great suffering whilst complaining about trivial slights. Actually-existing democracy, however, does the precise opposite. Which poses the question of whether egalitarian democracy and capitalism are compatible.

* Unwarranted not by my standards but sometimes by their own. For example, the ERG - which had voted for the Brexit deal - now wants to abolish a key part of it. Their demands are incoherent - and yet they are given disproportionate weight.

February 19, 2021

Why Labour should talk about productivity

If you buy a goldfish, you shouldn���t be disappointed that it doesn���t catch mice. It is therefore pointless to criticize Starmer���s speech yesterday for being insufficiently critical of capitalism. There is however one curious but important omission from his speech ��� one which is odd for a technocratic social democrat.

I���m referring to the lack of any discussion of, or remedy for, our productivity problem.

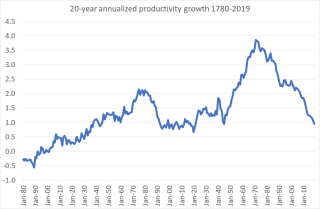

Just before the pandemic, real wages were actually lower than they were in 2007. The average worker has gone 13 years without a pay rise. This is not because capitalists have taken a bigger share of the pie: the share of non-financial profits in GDP was much the same at the start of 2020 as it was in the mid-00s. Instead, it���s because productivity has stagnated: in the 12 years to the start of 2020, output per worker-hour grew only 0.2% per year, compared to 2.2% per year in the previous 30. And in fact in the last 20 years productivity growth has been lower than at any time in the last century.

If workers are to get a pay rise, therefore, we need to raise productivity growth.

Doing so isn���t just a matter of good economics. It���s good politics too. Yes, Starmer���s talk of insecurity and poverty spoke to the jobless and economically marginalized, which is good. But Labour also needs the votes of a wider section of the working class. Talk of raising pay speaks to these. Also, we know that a faster-growing economy fosters more liberal, inclusive sentiments and hence support for the left. Grace is bang right to say:

In the long run, a social democratic model would provide a far better terrain on which to advance class struggle than the current neoliberal one.

And yet Starmer���s speech was astonishingly light on productivity.

But there is much that he could reasonably have said, even within the confines of centre-left Fabian-style thinking.

We could start from the perspective that competition raises productivity - not just by forcing businesses to up their game if they are to survive, but because lots of productivity gains come from new firms entering (pdf) the market.

Some of Labour���s current policies should be presented in this context. Starmer���s proposal for state-backed business loans would encourage start-ups, entry and competition. And we need them because there is a market failure here; banks lend eleven times as much in residential mortgages as they do to all SMEs outside the financial and real estate sector. And Rachel Reeves��� call for more honest procurement should be seen as a way of using the state���s buying power to encourage competition.

We could of course go further. We might call for tougher competition law or a relaxation of restrictive intellectual property laws. And, of course, trade frictions reduce competition and hence productivity, suggesting a need for at least a less stupid type of Brexit.

What's more, Starmer is right to call for more active government. It���s not just investment in transport and better broadband that might raise productivity. Stian Westlake and Sam Bowman, two of the few intelligent centrists, propose direct state funding for innovation. And perhaps simply running the economy hot via looser fiscal policy could also raise productivity: there might be some truth (pdf) in Verdoorn���s law.

Labour could, therefore, talk about productivity without straying much from centre-leftism.

Of course, there���s also a more radical agenda.

One strand of this would be full-on attack on rentiers. It���s no accident that the slowdown in productivity has coincided with the rise of rentierism as splendidly documented by Brett Christophers. Capitalists��� incentives are skewed towards seeking the quiet life of extracting rents rather than the risky entrepreneurialism that raises productivity and living standards. And the extraction of rents suppresses dynamism by squeezing profits and real incomes: if you have to spend half your income on rent, that doesn���t leave much demand for the goods and services that could be produced by entrepreneurs. Ricardo was right: rents are a drag on growth.

Labour has proposed one way to restrain rentierism - bringing the more egregiously rent-seeking government outsourcing back in house. But there are other responses, such as shifting taxes from incomes to land, and for nationalizing monopolies.

Another radical strand starts from the perspective that high inequality depresses growth. One reason for this is that the managerialism unleashed by neoliberalism might have reduced productivity by empowering a ���long tail��� (pdf) of bad bosses and by entrenching vested interests who want to retard creative destruction. As Joel Mokyr has written:

Every society, when left on its own, will be technologically creative for only short periods. Sooner or later the forces of conservatism, the "if-it-ain't-broke-don't-fix-it," the "if-God-had-wanted-us-to-fly-he-would-have-given-us-wings," and the "not-invented-here-so-it-can't-possibly-work" people take over and manage through a variety of legal and institutional channels to slow down and if possible stop technological creativity altogether.

This points to a need for democratic reform of the economy, and empowering workers rather than bosses: we know that democratic workplaces tend to be more productive. But as Phil says, it is on this point that Starmer breaks with Corbynism.

None of this is to suggest that it is easy to raise productivity. As Dietz Vollrath and John Landon-Lane and Peter Robertson have warned us, the opposite is the case.

This, however, is not a reason to give up. Most policies suggested here have little downside; even if they don't raise productivity they'll do little harm (except to those who need harming). There is, therefore, a big potential agenda here for Labour which could be both popular and economically sensible ��� if that is, it could get a fair hearing.

February 17, 2021

It's not the 90s any more

Sir Keir Starmer wants to party like it���s 1999. That seems to be his motive for seeking the advice of Peter Mandelson. There is, however, a big problem with this. It���s not the 1990s any more. There have been huge socio-economic changes since then, which require very different policy responses.

One of these is that the economy is now stagnating. In the 20 years to May 1997 labour productivity grew by an average of 2.3 per cent. In the 12 years before the pandemic, however, it grew by only 0.2 per cent per year. Back in the 90s, therefore, it was reasonable to believe that the economy would grow well if governments could only provide the right framework such as stable macroeconomic policy. Today, though, we know that whilst policy stability might be necessary, it is not sufficient. Capitalism has lost its dynamism. That requires a different ��� perhaps more activist ��� policy response.

A big reason for this stagnation is, of course, the legacy of the financial crisis. Which itself shows another reason to need to break with 1990s thinking. In his 1996 book The Blair Revolution, Mandelson wrote of the need for ���firm macroeconomic policies to avoid any repetition of boom and bust���. ���By far the most important thing��� he wrote ���is to get macroeconomic policy right.��� But we now know that macro policy is not enough to avoid recessions and their aftermath. The banking crisis taught us that the economy is not naturally stable, thrown into recession only by policy error. Instead, crises arise from private sector decisions which cannot be fully corrected by good policy. Mandelson���s claim that ���our understanding of economics has greatly advanced in this century, and in theory enables economic fluctuations to be damped and corrected��� now reads as simple-minded hubris.

Our long stagnation requires another change in thinking from the 90s. ���New Labour emphasizes macroeconomic stability��� wrote Mandelson ���because of principled objections to high inflation and the economic and social havoc it wreaks.���

Today, though, we have the opposite problem. Inflation is too low. A rise in it might actually be a good thing as it would allow us to escape the zero(ish) bound on interest rates. Mandelson wrote of the need for a ���tight new discipline��� in fiscal policy. That might have made sense in an inflation-prone economy where real interest rates were over 4%. But when economies are stagnant and real rates minus 2%? Not so much.

Stagnation also overturns 1990s ideas about inequality. Although Mandelson has disowned his famous remark about being "intensely relaxed about people getting filthy rich as long as they pay their taxes", I���m not sure he appreciates just how wrong it was. A decade and a half of stagnation shows us that inequality is not a minor issue ameliorable by tweaks to the tax system. Instead, it���s plausible that inequality is a big cause of slow growth. It concentrates power within companies into the hands of reckless Stalinists like Fred Goodwin; it incentivizes rent-seeking; it generates perverse incentives; reduces trust, innovation and investment; and so on.

Growth-enhancing policies thus require much more egalitarian actions than we thought in the 90s, therefore.

And the inequality that matters now is very different from that of the 90s. Back then, leftists such as Will Hutton spoke of the 30-30-40 society: ���30 per cent disadvantaged and marginalised; 30 per cent insecure; 40 per cent privileged.��� Today, though, what matters is the wealth and power of the top 1%, or 0.1%. New Labour was largely oblivious to this: in hindsight, one of Gordon Brown���s great failings was his undue deference to bank bosses.

Because the economics has changed since the 90s, so too has the politics. I mean this in two big ways.

One is that the growing wealth of the mega-rich has increased their power over politics. In the 90s, the main opposition to Labour was founded upon businesses��� fears of higher taxes and bad macroeconomic management. The party could then assuage such concerns easily. Today, though, it faces opposition from eccentric billionaires stoking up culture wars. It���s less obvious what to do about this.

Secondly, our long stagnation has strengthened illiberal populist sentiment ��� just as Ben Friedman predicted. In the 90s and 00s the Tories lost elections massively by ���banging on about Europe���. Things have changed since. In the 90s, voters chose technocrats over cranks. They no longer do so. Which gives Labour a dilemma: how far to accommodate itself to populism, and how far to resist it?

In all these ways, the 90s is utterly irrelevant today. What worked then will not work now. Few centrists, however, seem to grasp this. One of their defining features, indeed, is a complete innocence of economic realities and a vacuum where ideas should be.

Which brings us to a paradox. One of the great achievements of Tony Blair was to realize that social democracy had to reinvent itself for the new times of the 1990s. His epigones, however, don���t appreciate that Labour now needs another reinvention for different times, and don���t give John McDonnell credit enough for grasping this fact. The thing about modernizations, though, is that you have to keep doing them.

Chris Dillow's Blog

- Chris Dillow's profile

- 2 followers