Joe Withrow's Blog, page 23

November 22, 2022

Two Ways to Counter Educational Malpractice

“Education is what remains after one has forgotten what one has learned in school.”

That quote comes from Albert Einstein. He also said it’s a miracle that curiosity survives formal schooling.

So the guy who we often associate with brilliance was no fan of school. There’s a good reason for that.

The educational system that’s been in place over the last century isn’t about enlightening and empowering individuals. Quite the opposite.

It’s the factory model here in the U.S. In Germany, they originally referred to it as the gymnasium approach.

The system is designed to produce good soldiers and good workers. People who will be punctual and follow their orders reliably.

This is why the modern education system neglects the subjects of money and finance. It’s also why the history and economics we get is overly simplistic. And these days hyper-politicized.

To me, this is educational malpractice.

Fortunately, there’s a solution. Two solutions, actually.

For adults, it’s Tom Woods’ Liberty Classroom. This is a platform with over thirty online courses – each taught by an expert in the field.

Most of these courses center around history, economics, and classical philosophy. There are also some fascinating courses on mythology, science fiction, and the culture of early America and the American frontier.

I’ve finished seven of these courses so far. They are fantastic. This is the college education I wish I received.

For anyone interested, just go right here for more information:

And for children, the solution to educational malpractice is the Tuttle Twins Series.

This is a set of thirteen illustrated children’s books. Each book focuses on a specific lesson.

The Golden Rule… personal responsibility… basic entrepreneurship… simple economics – the Tuttle Twins series covers it all. And it does so in a way that’s fun. My kids love these books.

And here’s the best part…

The team behind this series is doing a massive Black Friday sale right now. Anyone who purchases this week can get 75% off their bundle options.

Here’s a snapshot of some of the titles.

For more information on the bundles and the individual books, just go here:

The Tuttle Twins Books Collection

Have a wonderful Thanksgiving.

The post Two Ways to Counter Educational Malpractice first appeared on Zenconomics.

The post Two Ways to Counter Educational Malpractice appeared first on Zenconomics.

November 15, 2022

Bitcoin’s Morality is the Killer App

“No man sews a piece of new cloth into an old garment, because that new cloth will pull away from the garment, and the tear will be made worse. Neither do men put new wine into old wine-skins, or else the skins will burst, the wine will be spilled, and the skins will be ruined.

Men put new wine into new wine-skins, and both are preserved.”

That’s a quote from Jesus of Nazareth. He was trying to explain why his proposed system of morality was incompatible with what came before it.

Jesus’ model of morality is the golden rule. On the surface it’s very simple. But there’s a big nuance in there that I suspect a lot of people miss.

That nuance is this: Jesus defined an entirely new way of judging right and wrong.

Previously, laws and commandments from authority figures determined what was right and what wasn’t. With the Jesus model, a person’s actions towards others are what matter.

By treating others in ways that they would not like themselves, people condemn their own actions. And by treating others in a manner that they would like themselves, people justify their actions.

As simple as this model is, it threatened to completely upend the established hierarchy in Jesus’ day. That’s because it was simple, easy to understand, and better. For everybody.

Now I know we may be wondering – what in the world does this have to do with Bitcoin?

The answer is everything.

Bitcoin is the golden rule applied to money. Morality is baked right into the cake.

That’s because Bitcoin is a fully transparent system that cannot be altered or gamed in any way. By anybody.

It starts with the fixed supply. Only 21 million bitcoins will ever exist.

And 19.2 million of them are already here. That’s 91%. Talk about scarce.

Bitcoins are mined into circulation in “blocks” every ten minutes or so. And we know in advance exactly how many new bitcoins will be mined in each block. That’s all governed by an algorithm. Nobody can change it.

This means we can project in advance how many new bitcoins will enter the market month after month, year after year. It’s fully transparent.

What’s more, we can self-custody our bitcoins with just the click of a button. That’s how we take full control of our funds.

When we self-custody, nobody can stop our transactions or freeze our accounts. We have full sovereignty over our money. There are a host of mobile wallets and hardware wallets that empower us to do this.

Compare this with the legacy financial system.

The Federal Reserve (the Fed) has created about $5 trillion out of thin air since September of 2019. We had no say in the matter.

As a result, consumer prices have ballooned this year. We see that very clearly every time we go to the grocery store.

And within the legacy system, we can never take full control of our money.

There’s no option to self-custody the funds in our bank and brokerage accounts. We are always subject to the decisions of a third-party.

Now, that’s no big deal if we trust the third-party. But if we look out at our world today – trust is collapsing.

That’s certainly true here in the U.S. Trust in our core institutions appears to be at an all-time low.

The same dynamic exists on the world stage.

Simply put, the global financial system has fractured. The East (China, Russia, and friends) no longer trust the West (Europe, U.S., and friends).

Yet, the global economy is more interconnected today than ever before.

This is obvious to see when we talk about energy and goods trading hands and crossing borders. But it’s far more nuanced than that.

If we look at any final product sitting on a store shelf, we can bet that it’s composed of materials and parts that were sourced by countless different people across at least a handful of countries.

None of these people know each other. Yet somehow their work finds its way to a central location for manufacturing. Then the final product is shipped around the world for distribution.

And for larger trade deals, there are very complex systems of financing and collateralization that come into play. The modern supply chain is mind-blowing.

But here’s the thing… It only works if people have a standard medium of exchange and store of value that all parties involved can trust. That’s been the U.S. dollar for the last 78 years.

There won’t be a 100th anniversary. The dollar’s reign as the global reserve currency is diminishing right before our eyes.

Right now those countries interested in bypassing the dollar are orchestrating one-off deals using a number of different currencies as their medium of exchange.

That’s fine for now. But it still requires immense trust.

At some point I’m betting the world will want to move to a currency where trust is programmed right in. That currency is Bitcoin.

I was somewhat early to the Bitcoin scene. I got involved back in 2014.

Back then, there was a lot of talk about what Bitcoin’s “killer app” would be. What was the one major feature that would spearhead mass adoption?

My friends, that feature is Bitcoin’s morality.

Bitcoin is new wine in a new wine-skin. And it’s here at just the right moment in history.

That’s why this will be a six-figure asset. Bitcoin will trade north of $100,000 per BTC… likely within the next five years.

Best to buy while it’s cheap.

For more information on how to incorporate Bitcoin into a strategic asset allocation model, just go right here:

-Joe Withrow

The post Bitcoin’s Morality is the Killer App first appeared on Zenconomics.

The post Bitcoin’s Morality is the Killer App appeared first on Zenconomics.

November 14, 2022

How to Profit From the Crypto Bank Run

Old fashioned bank runs are remarkable to behold.

We got a glimpse of one back in 2008. There was all kinds of chaos and excitement for a few days. Iconic investment bank Lehman Brothers even collapsed in a heap.

But then the U.S. Treasury and the Federal Reserve (the Fed) stepped in to bail everybody out. Show over.

Well, last week one of the world’s largest cryptocurrency exchanges, FTX, gave us another show.

To set the stage, FTX was handling billions of dollars in crypto transactions every day. This drove over $1 billion in revenue last year.

And as a company FTX was valued at $32.5 billion at the start of last week. That’s thanks to pulling in nearly $2 billion in venture capital investment since its founding in 2019.

And look at who invested in FTX…

Sequoia Capital… Tiger Global Management… SoftBank… Ontario Teachers’ Pension Plan… Singapore’s sovereign wealth fund… Tom Brady and his former wife… Steph Curry… the list goes on.

These are all people who should have known better.

FTX’s CEO was a thirty-year old kid born with a silver spoon and deep family connections to the Deep State. He was the second largest donor to the 2020 Biden campaign. And he apparently had a favorable relationship with Securities and Exchange Commission (SEC) chair Gary Gensler… who has been openly hostile towards everybody else in the digital asset industry.

Plus, the CEO spent tens of millions sponsoring the Miami Heat’s basketball arena. And he inked another sponsorship deal with Major League Baseball to get the FTX logo on everybody’s uniforms.

So this guy clearly wasn’t focused exclusively on his core business. And he appeared to crave attention and fanfare. What could possibly go wrong?

And here’s the kicker – FTX had its own crypto token called FTT. These are tokens it could create at will.

Now, FTT tokens did not convey equity in the company. Instead, FTX provided reduced trading fees to anyone who held its token. And it would periodically buy back FTT tokens to destroy them. This was done to make FTT seem scarce.

But FTT wasn’t scarce.

In fact, the CEO used FTT to capitalize a quantitative crypto trading firm called Alameda. He also happened to be majority owner of this firm.

Last week we found out that Alameda had $5 billion worth of FTT on its balance sheet. And it was borrowing against that value to finance speculative “investments”. This is the same story we saw play out with the banks in 2008.

Those investments started to go bad in a big way this year. That’s when rumors came out that FTX was seeking billions in emergency financing. And, wisely, people with funds on the exchange began to worry that FTX had used their money to backstop Alameda’s losses.

That prompted the bank run last week. People rushed to get their digital assets off FTX. That is, until FTX stopped withdrawals. Ouch.

The word is that, when the dust settled, FTX was down to just one single bitcoin on its books. I’m not sure if that’s true. But it’s remarkable if so.

At first it looked like the industry would come to the rescue.

Binance, another massive cryptocurrency exchange, initially said it would try to bail out FTX for the good of the industry. But then they looked at the books and said “nope, we can’t touch that”.

So now FTX customers stand to lose everything. We’re talking billions of dollars lost.

And it doesn’t stop there.

We are going to see at least a few companies in the industry go under thanks to FTX. Anyone who lent them money or held assets on their exchange will be impacted. There will be a domino effect.

The good news is that this will likely drive the price of Bitcoin (BTC) lower. I think we could see one more push down to the $11,000 – $12,000 price range. That’s the capitulation moment.

If we want to profit from the crypto bank run, we should be buying Bitcoin on the way down. This will be the last opportunity we have to pick up BTC on the cheap.

And make no mistake about it – Bitcoin is a six-figure asset. It will trade at a price greater than $100,000 per bitcoin within the next five years. We’ll talk about why I’m so confident in that prediction tomorrow.

By the way, we go over all the good practices for allocating to Bitcoin in our newly revamped Finance for Freedom course.

This includes how to buy Bitcoin safely and securely… And how to self-custody using a hardware wallet. That’s how we protect ourselves from hacks and bank runs.

And of course, Bitcoin only makes up one part of a resilient asset allocation model. We talk about all the other pieces in the course as well.

Anyone interested can get more information on it right here:

Finance for Freedom Course Page

The post How to Profit From the Crypto Bank Run first appeared on Zenconomics.

The post How to Profit From the Crypto Bank Run appeared first on Zenconomics.

November 10, 2022

What is Passive Income?

Yesterday we observed how wages, adjusted for inflation, have stagnated since 1971. And we suggested that the answer is to fill in the gap with passive income.

But what exactly does that mean? What is passive income?

Simply put, passive income is money that we make without constantly working for it. That’s it. It’s the holy grail of personal finance.

That said, passive income is a buzz word that’s thrown around everywhere these days. And there are a lot of misconceptions out there.

When we talk about passive income, we’re not talking about a way to make money without effort or investment. That’s impossible… outside of criminal activity and perhaps politics.

Remember, there’s no such thing as a free lunch.

I also don’t consider side hustles to be passive income.

I love the fact that anyone can start an online business today. But it’s a lot of work. There’s nothing passive about it.

So in my experience, old fashioned rental real estate is the single best vehicle for generating passive income. There are a few reasons for this.

First, if we utilize existing systems we can build a robust real estate portfolio with no more than thirty minutes worth of work a month.

The key is having a network of professionals in place already. I call this “infrastructure”.

And this infrastructure provides us with access to the best U.S. rental markets. That means we only invest in places where the cash flow is high and the laws are good.

This also gives us access to a wide range of properties. We can start as small or as big as we want to.

In other words, it’s far easier to break into the game than most people realize. I’m living proof of that.

Finally, real estate provides some tremendous tax advantages to investors. There’s a reason why it’s always been a good old boys game. The tax issue is a big part of that.

My point is this – if we want to build passive income, rental real estate is the way to go.

With the right system in place, anybody can work up to $2,000 to $3,000 a month in passive income in just a few years. That’s $24,000 to $36,000 in extra income a year.

Then that number can grow as big as we want it to. It’s just a matter of systematically following the process.

Which begs the question – what process?

That’s where our Rental Real Estate Accelerator course comes in.

This program tears down the barriers to entry and makes real estate investing simple. It covers the entire process from A to Z.

Developing investment criteria… analyzing properties… strategic financing… LLC structure… advanced tax strategy… asset protection – Rental Real Estate Accelerator covers all of it. Everything one needs to know to get started with real estate, it’s in here.

What’s more, the program walks through the process of buying an investment property step-by-step. We’re talking about a real example. No hypotheticals here.

And if that weren’t enough, we’ll show how anybody can plug in to existing real estate investment networks right now.

This is how we find the best investment properties and trusted professionals – both of which are key to making real estate as passive as possible.

To sum it up, Rental Real Estate Accelerator makes passive income as simple as possible.

In fact, it makes building passive income with real estate almost as easy as buying stocks online. No kidding.

That’s the power of plugging into existing systems.

And the beautiful thing is, anybody can do this. It’s just a matter of knowledge and connections.

Ready to learn more? Just go right here:

Rental Real Estate Accelerator Program

And I should point out that Rental Real Estate Accelerator is incredibly affordable.

We aren’t shilling financial advice for thousands of dollars a year. In fact, we don’t even require a subscription.

Instead, we typically offer our core program at a one-time cost of just $42. That’s it.

But not today.

In honor of the brave new financial world we find ourselves in, we’re offering a 30% discount right now.

That means you can tap into a tried-and-true system this week for less than thirty bucks. Anybody who follows through on what they learn will recoup this and a lot more with their first investment.

To take advantage of your discount today, just enter coupon code “RREA” at the checkout page.

See you inside.

The post What is Passive Income? first appeared on Zenconomics.

The post What is Passive Income? appeared first on Zenconomics.

November 9, 2022

Why Passive Income is Critical

“Your dollar will be worth just as much tomorrow as it is today,” President Nixon proclaimed on television with a straight face.

“The effect of this action, in other words, will be to stabilize the dollar.”

The date was August 15, 1971. President Nixon just announced that he was closing what was known as the “gold window”. This was the system through which foreign countries could redeem U.S. dollars for physical gold upon demand.

The gold window was a fixture of the Bretton Woods System of 1944. That was the international agreement which established the U.S. dollar as the world’s reserve currency.

What we’re talking about here is trust. The idea was that if the U.S. started printing too much money, the rest of the world could trade their dollars in for gold.

Makes sense, right? Nobody wants to hold a currency that can be created from nothing at will.

President Nixon got rid of this restraint on money-printing in 1971. The story behind that move is very nuanced. But what followed isn’t…

According to the Federal Reserve’s data, the U.S. has created trillions of dollars from nothing since then.

Naturally, this reduced the purchasing power of each dollar in circulation. That’s just basic supply and demand economics.

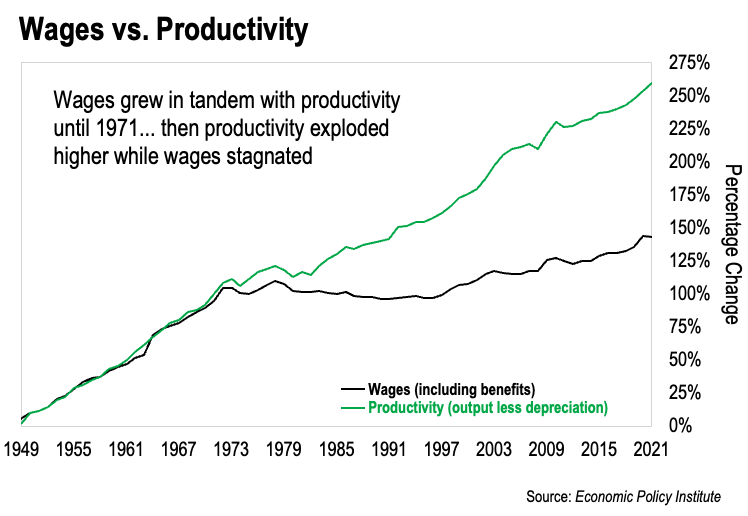

We see this very clearly in the form of rising consumer prices. But there’s a hidden story at work here also. This chart spills the beans:

This data comes from a study done by the Economic Policy Institute. They measured the growth in median U.S. wages, adjusted for inflation, against total productivity – the output of goods and services. This data goes back to the late 1940s.

And we can see very clearly that wages moved in lockstep with overall productivity up until 1971. That means the average guy’s salary went up in proportion to America’s output of goods and services. As it should be.

We can also see very clearly that our productivity has continued to explode higher to this day. But our wages, adjusted for inflation, have been mostly flat since 1971.

The reason?

Those trillions of dollars created from nothing steal purchasing power from everybody. And this happens year after year. That’s why it’s so hard to get ahead these days.

And this is why we need to rethink financial planning 101. We talked about that yesterday.

Fortunately, there is a solution.

There is one tried-and-true investment that puts inflation to work for us, rather than against us. What’s more, this investment also creates passive income streams for us.

Passive income is critical. It’s how we fill in the gaps caused by stagnating wages. And with the right system, our passive income can quickly grow to meet and exceed our annual salary.

That’s what our new Rental Real Estate Accelerator program is all about. It makes building passive income with real estate simple.

With our system, anybody can work up to $2,000 or $3,000 a month in passive income in just a few years. No previous knowledge or experience necessary.

From there, getting to $10,000 a month or more is just a matter of accelerating the process.

And here’s the thing – this can be done with no more thirty minutes worth of work each month. That’s the beauty of having the process and the networks already in place.

So we’re not talking about a side hustle here. We aren’t talking about an online business where we have to work nights and weekends to get the extra income.

Our approach to rental real estate is far more simple.

If you’re ready to get serious about building passive income, please give our program a look. You can find more information right here:

Rental Real Estate Accelerator Program

By the way, we’re running a 30% off special this week. Just use the coupon code “RREA” at the checkout page to take advantage of it.

The post Why Passive Income is Critical first appeared on Zenconomics.

The post Why Passive Income is Critical appeared first on Zenconomics.

November 8, 2022

The Rules of Money Just Changed… Forever

2022 is the year the rules of money and finance changed.

If we look at a chart of the S&P 500 going back to the early 80s, it’s only gone up over time.

Sure there were plenty of dips. But for the last forty years we could buy a simple mutual fund or index fund and two years later we would have made money. Fifteen years later we would have made a lot of money.

Meanwhile, if we were to overlay a chart of the 10-year Treasury rate – which is a proxy for interest rates… It’s only gone down over the last four decades.

This dynamic – stocks going up, rates going down – is largely thanks to the Federal Reserve (the Fed). It’s had a hand in both. Through loose monetary policy.

But the game’s over.

Fed Chair Jerome Powell made that abundantly clear last week. The Fed has aggressively raised interest rates this year… and it will continue. There’s no pivot coming.

And that means stocks will have to stand on their own. The Fed will no longer prop up the market.

We’re in uncharted waters here. Nobody under the age of 60 has lived in a world in which the Fed didn’t push stocks up and rates down.

So to me, the big takeaway is that we have to rethink financial planning 101. And I’m talking about the entire “nest egg” approach to retirement.

By that I mean the idea that we need to pour our savings into financial assets trying to get to this mythical retirement number.

What’s Your Number? I remember old commercials promoting this model.

The idea is that we build financial assets and we hope our returns get us to a big enough number so we can retire. Then we draw-down our assets to create income for ourselves after we quit working.

So it’s always a choice between assets and income.

When our assets are going up, we don’t have the income. Then when we want the income, our assets have to come down.

Why put ourselves in this position? Why not get assets and income on the same side of the equation?

We do this by flipping to a model that focuses on monthly cash flow. On creating extra income streams.

That’s how we put assets and income on the same team.

When our assets go up, so does our income. And when we want more income… we just buy more assets. It’s a far more robust approach.

In fact, with the right vehicle… and the right system in place, anybody can work up to $2,000 or $3,000 a month in extra income in just a few short years.

From there, getting to $10,000 a month in extra income is just a matter of accelerating the process. It’s completely possible to get there in six years. Ten at the most.

And that’s where our new Rental Real Estate Accelerator program comes in.

Our goal with this program is simple. We want to tear down the barriers to entry around real estate investing.

And we do that by providing a step-by-step system for building passive income with real estate. This is something anybody can plug in to right away.

By the way, when I say passive, I mean it. Our program boils real estate investing down to a system.

We aren’t pounding the pavement or taking calls. All we have to do is send a few emails occasionally. That’s it.

Best of all, our course is priced such that anybody can afford it.

We aren’t shilling financial advice for thousands of dollars a year. In fact, we don’t even require a subscription.

Instead, we are offering our core program at a one-time cost of just $42. That’s it. We’re talking about the same price as a decent meal out for two.

And in honor of this brave new financial world we find ourselves in, we’re offering a 30% discount to anybody who checks out our accelerator program this week.

That means you can tap into a tried-and-true system for less than thirty bucks. Anybody who follows through on what they learn will recoup this and a lot more with their first investment.

For a more detailed explanation of our program, just go right here:

Rental Real Estate Accelerator Program

And to take advantage of your discount this week, just enter coupon code “RREA” at the checkout page.

The post The Rules of Money Just Changed… Forever first appeared on Zenconomics.

The post The Rules of Money Just Changed… Forever appeared first on Zenconomics.

October 28, 2022

The Biggest Financial Development Nobody Noticed

We’re at an inflection point in history right now. Things aren’t going back to how they used to be.

I don’t think the financial media understands this yet. But in hindsight, the bread crumbs were right there in plain sight. It comes down to an arcane change at the core of our financial system.

This is the first year in which the Secured Overnight Financing Rate (SOFR) went live across the board.

I bet very few people out there even know what this is. And of those who do, I doubt many understood SOFR’s significance.

SOFR is a benchmark interest rate for dollar-denominated loans and derivatives.

We don’t need to go down a deep rabbit hole on this. What’s important to understand is that the interest rates for all loans in the U.S. are now influenced by SOFR.

The London Interbank Offered Rate (LIBOR) used to hold that privilege. Before this year those who controlled LIBOR could influence interest rates in the U.S.

And that means the Fed did not previously have full control over U.S. monetary policy.

SOFR changed that.

That’s why the Fed’s been raising rates aggressively this year. Even though everybody has been screaming at them to stop.

And it’s why they will keep going. The Fed is playing the long game here. It’s all about self-preservation.

So the days of the Fed propping up the stock market are over. The Fed Put is dead.

And aggressive monetary policy will force some dramatic changes with how Treasury debt is handled. I think we may even see gold partially remonetized as a means of offsetting higher rates.

As such, we need to completely rethink financial planning 101. The old ways aren’t going to work anymore.

And that’s where Finance for Freedom comes in.

This is the only financial course designed to account for the current climate. Our program accounts for the major macroeconomic changes that are playing out right now.

Friends, we’re living history right now. The question is – do we want to be on the right side of it?

Finance for Freedom will show us how. More information right here:

Finance for Freedom Course Portal

And please note, this is the last day to take advantage of our 30% off coupon. Just enter coupon code “ER” at the checkout page to get your discount.

The post The Biggest Financial Development Nobody Noticed first appeared on Zenconomics.

The post The Biggest Financial Development Nobody Noticed appeared first on Zenconomics.

October 27, 2022

What to do as the world burns

Everywhere we look, it seems like the world is falling apart.

The stock market is crashing. Consumer prices are ballooning. Interest rates are on the rise.

It certainly feels like a recession is bearing down upon us. And it’s hard to feel secure about our finances in this environment.

Everywhere we turn there’s another reason to worry. Stuffing money under the mattress now seems like a good idea to many.

The good news is there is a solution.

Our revamped Finance for Freedom program can help you weather the storm.

That’s because it’s designed specifically for times like this. I’m not aware of another finance course out there that can make the same claim.

It all starts with understanding the secrets hidden within the current monetary system. And trust me, they run deep.

Then we cover basic personal finance topics. This helps us optimize our current situation.

From there, we dive into the principles of asset allocation. And we talk about specific investments that are critical in the current climate.

Some of these investments will be familiar. But some won’t. We provide an entire section on alternative investments that provide peace of mind in trying times.

Ready to give it a look? Just go right here.

The post What to do as the world burns first appeared on Zenconomics.

The post What to do as the world burns appeared first on Zenconomics.

October 26, 2022

Getting Banned From the Hospital’s Rehab Unit

Occasionally I sit back and reflect upon my life’s milestones.

Graduation. Marriage. The birth of my daughter… then my son. These were incredibly formative events.

And I just added another milestone to the list. Getting banned from the hospital’s rehab unit.

I was visiting a family member who just had a stroke last week. Upon entering the facility, the person at the front desk informed me that masks were required. And he asked me to take a mask from a box on the counter.

So I did. And then I made my way to the elevator and up to the seventh floor.

It turns out the floor’s nursing station is right there as you get off the elevator. And the director happened to be on duty.

She was talking with somebody as I made my journey towards the room. But she immediately called out as soon as she saw me. Sir, you need to have a mask.

I smiled and called back. “It’s okay – I do!”. Then I held up the mask I was carrying in my hand.

Sir, you must put the mask on! She snapped back.

I repeated that it was okay as I walked around the corner. I figured that would be the end of it.

Wrong.

She pursued me. And she barked at me to put the mask on every step of the way.

I simply repeated to her that it was okay. Then I walked into the proper room and shut the door.

For the first ten minutes of my visit I was thinking that security may barge in any minute. But they didn’t. Though, I don’t think I’ll be welcomed back.

Now, I’m not at all a disagreeable person. I would happily wear a mask if there were truly a medical reason to do so.

But the research is very clear. Masks do not stop the transmission of aerosolized particles.

Two randomized control trials confirm this definitively.

The first trial was conducted in Denmark with about 6,000 participants. That was two years ago. The second was conducted on Paris Island with nearly 2,000 U.S. Marine Corps. recruits.

The data clearly showed that masks did not inhibit the spread of COVID-19. And our real-world experience confirms this.

If masks worked, we would have seen a dramatic drop in cases after mask mandates rolled out. But we didn’t. Cases continued to rise.

So why was this person aggressively trying to coerce me into wearing a mask? They don’t work. And all Covid-related restrictions have long been dropped.

I think the answer is simple. Some people are just like that. Sometimes life just wants to push us around. We all know what that’s like.

But there is an antidote. It’s financial independence.

When we are in a good place financially, we can retain much more control over our lives and our decisions. To me, this is the true purpose of money.

I care nothing for consumerism. I’m not interested in luxuries. What I value is freedom. And that’s what financial independence enables.

This is the driving ethos behind our newly revamped Finance for Freedom course. It drills into the fundamentals of money, finance, asset allocation, and investments.

The goal is simple. The course is designed to help people get a jump on their path to financial independence.

And we’re running a 30% off special this week. That’s in honor of all those times when life tries to push us around.

Just go right here for more information on Finance for Freedom. You can use coupon code “ER” at the checkout page to take 30% off the normal price.

Then let’s stand tall and tell life we refuse to be bullied around.

The post Getting Banned From the Hospital’s Rehab Unit first appeared on Zenconomics.

The post Getting Banned From the Hospital’s Rehab Unit appeared first on Zenconomics.

October 25, 2022

What Strokes Can Teach Us About Life

I spent a lot of time in the hospital last week.

A family member endured a stroke, and my duty was to be there for him. My job was to offer support and encouragement.

I saw this as a one-sided affair at first. But I quickly realized this experience had a critical lesson to teach me. That’s what I want to share with you today.

Strokes strip people of everything they take for granted.

Speech. Eye-hand coordination. Basic motor skills. Autonomy… Strokes reveal just how precious these things are. We can lose them at any time without notice.

Strokes also strip away all those layers of social conditioning that gradually build up on us over time.

We all are conditioned to think and act in certain ways, depending on the situation and the people we are around. That’s our social conditioning. It’s about conforming to preset expectations.

Well, that all fades away when you’re lying in a hospital bed unable to speak or move.

At least that’s my observation. What’s left is purely the human spirit that exists underneath it all. It’s beautiful to behold.

To me, this is a stark reminder of what’s truly important in this life.

Family. Friends. Shared experiences. Integrity of character. I believe these are the things that matter in the end.

But there’s one problem here…

To maximize our time with family and friends – and our ability to create shared experiences – we need a certain degree of financial stability.

That is to say, we need to have some control over our time and our decisions. The more control we have, the better.

And that’s what our newly revamped Finance for Freedom course is all about.

This is the financial education that every high school and college student should have received.

It starts with the secrets of money, and then works up to basic personal finance.

Then we dive into the principles of asset allocation. And we talk about very specific investments.

Lastly, we go over exactly how to develop what I call a “cash flow wealth strategy”.

This is all about building passive income streams. If we can work up to having enough passive income to cover all our needs and our wants, we can be free to pursue those things that truly matter in life. At our leisure and on our terms.

And in honor of what I just learned in the hospital, we’re offering the course at a steep discount this week. Anyone who purchases Finance for Freedom before Saturday at midnight will get 30% off.

That equates to a one-time cost of just $21. These days that’s less than a good meal out for two.

You can check out our course offering right here: https://membership.phoenicianleague.com/courses/finance-for-freedom

Just use coupon code “ER” on the checkout page to get your 30% discount.

My sincere hope is that we can spread the principles of financial independence far and wide so that we all can focus on what truly matters in this life.

The post What Strokes Can Teach Us About Life first appeared on Zenconomics.

The post What Strokes Can Teach Us About Life appeared first on Zenconomics.