Simon Johnson's Blog, page 51

September 28, 2011

Anti-American Bankers

By Simon Johnson. An edited version of this short post appeared today on the NYT.com's Room for Debate: "Are Global Banking Rules Anti-American?"

Jamie Dimon claims that the new rules on bank capital "anti-American" because they somehow discriminate against American banks and American bankers. This framing of the issues is misleading at best.

The term "bank capital" is often poorly explained in the debate on this issue. It is just a synonym for equity – meaning the amount of a bank's activities that are financed with shareholder equity, rather than debt. The advantage of equity is that it is "loss absorbing," meaning that it takes losses and must be wiped out in full before any losses fall on creditors.

More capital means that a bank is safer, both from the perspective of shareholders and for creditors. Bankruptcy has become less likely.

But the real need for capital requirements arises from the social costs that a banking crisis can impose. Switzerland has moved to 20 percent capital requirements because they have two large banks which, if they fail, would cause major damage to the economy. The British are discussing moving in the same direction – the recent Vickers Commission report regards the Basel capital rules as insufficient for safeguarding public interests.

Bankers get lots of guarantees from the government – some explicit, like deposit insurance; and some implicit, like being Too Big To Fail. This is downside protection – but only for bank executives and some employees; everyone else in society still suffers when big banks blow themselves up.

If the evidence from our recent deep recession and slow recovery is not enough, look at Europe today. Big banks have huge debts relative to their equity – Deutsche Bank, for example, has a leverage ratio (assets divided by shareholder equity) around 35 times. Even small losses on sovereign debt in Europe could wipe out shareholder equity – the capital – of those banks.

Requiring higher capital – more equity relative to debt – in US banks is good for everyone. If some bankers complain and work hard to overturn these rules, they are the ones being anti-American.

————————————————

For more reading on what really is bank capital and why we need higher capital requirements, I strongly recommend this paper by Anat Admati of Stanford University and her colleagues: http://www.gsb.stanford.edu/news/research/Admati.etal.html. Send the link to anyone you think may be misusing or misunderstanding the terminology.

September 27, 2011

Should Social Security Be Progressive?

By James Kwak

My earlier rant on the Social Security wage base made me think of a more important question (actually, I was already thinking of it, hence the need to Google the earnings cap): Should Social Security be more progressive than it already is? The most common ways liberals want to make it more progressive are (a) eliminating the cap on taxable earnings altogether and (b) reducing benefits for high earners. For part of my brain the automatic answer is "yes," but I think there is a reasonable argument for leaving things roughly the way they are.

First, there's a straight-up political argument. Social Security is popular because people feel like they earn their benefits. If people thought it was a covert redistribution program, then the high earners would definitely be against it, and most of the middle class probably would be too because of the American allergy to welfare. In fact, there are certainly people who think it is "pure welfare", like the author of the post I criticized last time around. But it isn't:

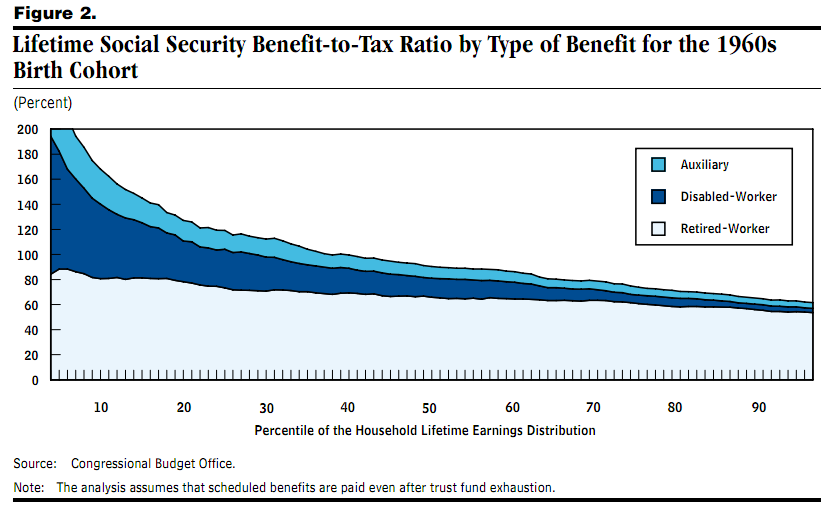

That is from a 2006 CBO analysis of Social Security taxes and benefits, by income level. As you can see, the retirement program on its own is only modestly progressive. The really progressive parts of the program are disability insurance and survivors' benefits. The fact is that there isn't that much redistribution based solely on income level; most of the "redistribution" is based on disability or having your spouse die young, which feels more like insurance than welfare. It turns out that most Americans' instincts are right: Social Security isn't a welfare program. If you make that bottom line steeper, then at some point opinions will change.

That is from a 2006 CBO analysis of Social Security taxes and benefits, by income level. As you can see, the retirement program on its own is only modestly progressive. The really progressive parts of the program are disability insurance and survivors' benefits. The fact is that there isn't that much redistribution based solely on income level; most of the "redistribution" is based on disability or having your spouse die young, which feels more like insurance than welfare. It turns out that most Americans' instincts are right: Social Security isn't a welfare program. If you make that bottom line steeper, then at some point opinions will change.

Now some people will look at that chart and say that Social Security should be more progressive. But I'm not so sure. Conceptually speaking, I think of Social Security as contributory pension system run by the federal government along with an insurance component to protect people against various risks—disability, early death of your working spouse, bad luck that prevents you from saving enough for retirement, living too long, etc. (Disability benefits are a standard feature of private defined benefit pensions, too.) I think of this governmental function as different from the welfare function—the one that ensures that everyone person has the basic means of subsistence. (Wait, we don't have that in this country? Well, we should.) And that's precisely what the founders of Social Security thought; they saw it as an alternative to noncontributory old-age assistance programs, which is what the conservatives preferred. (See Jacob Hacker, The Divided Welfare State, pp. 98–99.)

So to me, it makes the most sense to have (a) a contributory pension/insurance scheme that compensates participants for losses (e.g., disability) but is not mainly about redistribution; (b) a real welfare system for the poor; and (c) a progressive tax system to fund the rest of the government. And I worry that if you make (a) too much like (b) or (c) it will become unpopular and die a slow death. But I'm open to being convinced otherwise.

September 26, 2011

Black Is White

By James Kwak

I wasn't sure what the Social Security wage base was (it's $106,800, by the way), so I Googled "payroll tax cap." The number one hit is a post at a blog modestly called The American Thinker. I wouldn't ordinarily want to bring more attention to it, but it was the #1 hit, and according to Quantcast it has a million unique visitors per month, so nothing I do will affect it one way or another.

Anyway, the thrust of the argument is that we shouldn't eliminate the cap on wages subject to the payroll tax because "America simply can't afford it."

Such plans for expanding an already-huge entitlement are beyond irresponsible, they're frightful. Klein and Weller aren't serious men. When reading their ideas for Social Security expansion in this time of trillion-dollar federal deficits, one realizes that progressives are unconcerned about America's fiscal crisis.

You read that correctly. The argument is that increasing the wage base, which would bring in more revenues and reduce the deficit, is a bad thing—because of our fiscal crisis.

This claim is based on the idea that uncapping the wage base would also mean that benefits would have to be uncapped. That does seem like the sensible way to do it. But the way the benefit formula is written, when you increase the wage base, revenues go up much more than benefits. That's because after the second breakpoint your monthly benefit is only 15 percent of your average indexed monthly earnings. So raising the wage base reduces the deficit, which is a good thing in a "fiscal crisis."

What's more, the author seems to make this very argument later in the post, when he claims that Social Security is almost "pure welfare." The Social Security-as-welfare argument is based (by people who know the facts, at least) on the fact that the benefit formula is progressive, which more than counteracts the regressiveness of the payroll tax. So yes, there is some redistribution. But the thing that causes redistribution is the same thing that causes an increase in the wage base to be deficit-reducing.

Probably everyone who reads this blog knows all this already. But apparently there are plenty of people who think—or will argue—that things are their opposites.

September 25, 2011

Will The IMF Save The World?

By Simon Johnson

The finance ministers and central bank governors of the world gathered this weekend in Washington for the annual meeting of countries that are shareholders in the International Monetary Fund. As financial turmoil continues unabated around the world and with the IMF's newly lowered growth forecasts to concentrate the mind, perhaps this is a good time for the Fund – or someone – to save the world.

There are three problems with this way of thinking. The world does not really need saving, at least in a short-term macroeconomic sense. If the problems do escalate, the IMF does not have enough money to make a difference. And the big dangers are primarily European — the European Union and key eurozone members have to work out some difficult political issues and their delays are hurting the global economy. But, as this weekend's discussions illustrate, there is very little that anyone can do to push them in the right direction.

The world's economy is slowing down, without a doubt. The latest quantification was provided Tuesday of last week in the IMF's World Economic Outlook, which is perhaps the most comprehensive forecast of global growth and its main components (see Table 1.1). (Disclosure: I helped produce and present this view was I was chief economist at the IMF, but I left that position in summer 2008.)

The IMF has reduced its forecasts for both 2011 and 2012, but the latter is a more notable change (we can already see the gloomy 2011 picture all around us). Compared with its view in June, the IMF expects global growth in 2012 to be 0.5 percentage points lower (than previously expected). Part of the pessimism is for the United States – total GDP growth in 2012 is only expected to be 1.8 percent; anemic at best. (Remember that our population typically grows at just under 1 percent per annum, so this level of growth would barely put a dent in unemployment.)

But the really stark message is for Europe. According to the IMF, the eurozone as a whole will expand at only 1.1 percent in 2012 and hopes that troubled countries will grow out their debts seem increasingly like a stretch. Just to take one example, Italy's forecast for 2012 has been marked down to just 0.3 percent – and even in the best case scenario, credit availability there seems likely to get tighter over the coming months, which may further slow growth.

A potential recession in the eurozone and a weak recovery in the United States does not make for a world crisis. Beware people who demand that the world be saved – usually they are making the case for a bailout of some kind.

Don't get me wrong — a serious crisis could still develop. There are plenty of warning signs regarding the situation in Greece and its potentially broader impact. According to the IMF's Fiscal Monitor, also released last week (see p.79) Greece's general gross government debt is now forecast to rise to nearly 190 percent of GDP in 2012, before falling back towards 160 percent by the end of 2016. At this point, Greece needs a global growth miracle – and there is no sign of this on the horizon.

If Greece pays less on its debt than currently expected, this will push down the market value of other sovereign debts in Europe. As The Economist argued recently, the government debt of some large eurozone countries has unambiguously moved from the category of "risk-free" to "risky" in the minds of investors.

The numbers involved are big. Italy, for example, had public debt over 1.84 trillion euros at the end of 2010 (using the latest available Eurostat data, "general government gross debt," annual series). The GDP of Germany is around 2.5 trillion euros and there is no way that German taxpayers would be comfortable in any way guaranteeing a substantial part of Italy's debt. The entire eurozone has a GDP of around 9.5 trillion euros but no one is volunteering to take on debt issued by someone else's government (again, I use end of 2010 data from Eurostat).

To put the scale further in perspective, compare them with the IMF's ability to lend to countries in trouble. The technical term is the fund's "one year forward commitment capacity" which for "Q3 to date" is 246.0 billion SDRs (September 15 update; SDRs are "Special Drawing Rights", which exist only at the IMF.) On September 20, 1 SDR was worth 1.57154 US dollars, so the IMF could lend no more than 386 billion dollars — as one euro is worth about 1.37 US dollars this week, this is about 280 billion euros.

Or you could think of it as 15 percent of Italy's outstanding debt. This is not the only way – and not a precise way – to think about what the IMF could bring to the table, financially speaking. But it makes the right point; the European issue is way above the IMF's pay grade.

Germany, France, Italy and their colleagues need to sort out how to bring the situation under control – to decide who will definitely pay all their debts and who needs some kind of restructuring. About a quarter of the world's economy therefore remains in limbo, beset by repeated waves of uncertainty. And financial market fear can spread to other places, including the United States.

Complaints may be heard this weekend, but there is no one at the IMF meetings who can persuade the key European players to move faster in their decision-making. The politicians will take their own time – prodded periodically, no doubt, by the financial markets.

Do not expect a fast resolution or, therefore, a quick turnaround in the global economy.

An earlier version of this column appeared on the NYT.com Economix blog; it is used here with permission. If you would like to reproduce the entire post, please contact the New York Times.

September 23, 2011

The Price of Gold in the Year 2160

This piece of fun weekend reading is contributed by StatsGuy, an occasional commenter and guest contributor on this blog.

It's become quite popular to talk about the price of gold . . . in blogs, the press, at dinner parties. The latest topic of debate is not about the price of gold as a commodity, but about gold as the one and only king money. The basic argument is that 5,000 years of tradition will overwhelm the tyranny of modern government and the fiat printing press. The barbaric relic will defeat socialism, fascism, Obama-ism, and restore liberty to the world, after a terrible economic collapse in which gold-owning visionaries become fabulously wealthy.

Perhaps they are correct—or perhaps not. I don't know what will happen in 10 years. However, unless civilization utterly collapses (which is what gold hoarders seem to want), the gold bubble will collapse. And I don't mean the 10 year "bubble" . . . I mean the 5,000 year bubble.

This claim might sound crazy, but it's quite easy to defend, for the simple reason that there is too darn much gold. Gold enthusiasts will note that you can't just print gold like fiat paper. They will note that high quality mines are failing, and argue that we've passed "peak gold".

The argument for the collapse has little to do with terrestrial mine quality (although massive amounts of money and new technology are flowing into exploration, long term mine development and extending the life of existing mines). The argument merely requires that gold price ultimately responds to supply.

I can't tell you whether we'll run out of new mines, or Asian jewelry demand will ever be satiated, or global central banks will ever realize that currencies are supposed to serve economies (rather than vice versa). But I do know that in the year 2160 (give or take a century) gold will no longer be viewed as money. Why? For the same reason that all commodity based money systems have collapsed—technology made their production too cheap. Gold bugs like to talk about how every paper based money has failed (or will fail), but they ignore the equally miserable track record of commodity based money systems. For example, the cowry shell, which was used in ancient China and India, a weight of barley (the shekel), copper, cigarettes, or that most insidious of monopolistic money systems—salt.

So how did these money systems fail? Did their cultures implode? Did their governments fail? Quite the contrary, all commodity based money systems were destroyed by one simple factor—technology. At some point, technology enabled low cost production of the commodity, and the currency collapsed.

Very well, but what about gold? Even with technological advances, there just isn't that much easy-to-get gold in the crust of the earth.

True. And the reason gold is so rare in the crust of the earth? Well, that's because it's relatively abundant in the earth's core. When the earth was cooling, most iron-loving minerals sank toward a massive lump of molten iron down near the core. That includes gold and other heavy metallic elements. So where did the gold we currently have come from? Recent evidence suggests it came from smaller asteroid impacts that were not sufficiently large to break through the existing crust of the Earth. Although we've suspected this for a while, news is now hitting the mainstream.

So that means gold is very rare in the crust of the earth, but not so rare in space. In fact, in space, it might be quite common. A detailed study of the moderate sized asteroid Eros over a decade ago indicated it contained over $20 trillion of precious metals—at 1999 prices.

Back then, gold was around $300. Now it's $1,800, and other commodity metals have increased in price too. The nominal value of Eros alone is probably now over $50 trillion. That is a "large" economic incentive to consider exploring that opportunity. But do we really think that technology will be able to rise to the occasion in a mere 140 years? Actually, the real visionaries are already working on it. And technology is rising to the challenge. Already existing technology will drop launch costs from the current $10,000/kg to $500/kg. New propulsion systems are coming online and becoming more dependable. Massive computational resources are now more capable than ever of calculating the acceleration required to alter orbital trajectories to capture asteroids in the earth's orbit. Robotics advance daily, and we're just starting to see truly cost-effective solar power generation.

I don't mean to understate the technological challenges (heavy lift, radiation, anchoring and towing, energy cost of smelting, lack of water, etc.). In all likelihood, the visionaries will fail . . . and fail again . . . and again . . . until, eventually, they succeed.

Then, the greatest economic bubble of all time will end. Unless civilization ends, the only thing that might stop the visionaries is political authority—you know, the folks with the printing press. But that does not mean gold will have no value. Quite the contrary, it makes an excellent roofing material.

September 20, 2011

Confused?

By James Kwak

Some of the headline numbers for President Obama's deficit reduction proposal that you hear are the following:

$3 trillion in deficit reduction over ten years—more than the $1.2–1.5 trillion expected from the Joint Select Committee (JSC)

$4 trillion in deficit reduction, including the discretionary spending caps in the Budget Control Act

$1.5 trillion in tax increases

$1 trillion in deficit reduction by capping spending on Iraq and Afghanistan

This didn't make sense to me for a few reasons, notably that any deal that preserves any of the Bush tax cuts should be scored by the CBO as a tax cut, which increases the deficit. The actual numbers are rather more complicated.

You can download the complete proposal here. Table S-3 (p. 57) shows the administration's view of the world:

Adjusted August baseline deficit of $10.6 trillion (over ten years)

Discretionary spending caps from the Budget Control Act: $0.9 trillion

New Obama proposals, including both the American Jobs Act and the new deficit-reduction proposals: $3.1 trillion

Total reduction: $4.0 trillion

Resulting deficit (over ten years): $6.6 trillion

But the weird thing is that $10.6 trillion number at the top. To see where that comes from, look at Table S-4. What they did is this:

Start with the CBO's current baseline deficit of $4.7 trillion, from the August Budget and Economic Outlook. Note that the $4.7 trillion does not include the $1.2 trillion of deficit reduction that will come either from the JSC or from automatic spending cuts.

Take out the caps on discretionary spending in the Budget Control Act.

(a) Extend the Bush tax cuts and (b) index the AMT for inflation.

Implement the Medicare doc fix (preventing a 30 percent drop in reimbursement rates on January 1).

That gives you a ten-year deficit of $10.6 trillion.

There's nothing underhanded about taking out the discretionary spending caps in Table S-4 and then putting them back in Table S-3; that's just so Table S-3 can show the totals with and without the discretionary spending caps.

There's also nothing particularly nefarious about #3(a) #3(b) and #4, since everyone expects those things to happen. Basically, they are just assuming some of the alternative policies that have been estimated by the CBO.

But there are some issues here. First, if they're including the AMT patch and the doc fix in their adjusted baseline, why aren't they including the cost savings from troop drawdowns in Iraq and Afghanistan? Those fall in the exact same category as the AMT patch and the doc fix: everyone expects them to happen, and they are in the CBO's alternative policies. It looks like the administration is proposing an explicit cap on overseas contingency operations, which would affect CBO forecasts, as opposed to the current situation where the CBO is required to project growth at the inflation rate; this gets them $1 trillion in savings in Table S-3. At first glance, this seems like a pretty naked attempt to get credit for something that was going to happen anyway. If they were starting from the CBO baseline it would be defensible, but I don't see how you justify adjusting the baseline for the AMT and the doc fix but not for overseas contingency operations.

More seriously, it's not clear to me how President Obama's proposal can count as a suggestion for the JSC. The JSC is supposed to reduce the deficit by at least $1.2 trillion relative to the CBO baseline. Obama's bottom line is ten-year deficits of $6.6 trillion, which is higher than the CBO baseline. The biggest reason is that Obama's $1.5 trillion tax "increase" is really a tax cut relative to current law, which includes the expiration of the Bush tax cuts. Anything that sets income tax rates lower than they were in 2000—even if those rates are higher than they are today—count as a deficit-increasing tax cut. According to Mitch McConnell, that was the whole point, since it took the Bush tax cuts off the table. Relative to current law, Obama's proposal reduces taxes by $2.4 trillion, all of which adds to the deficit.

Now, there might be a way around this. As far as I can tell from reading Title IV of the Budget Control Act, the JSC just has to reduce the deficit by $1.2 trillion in whatever bill they come up with (see § 401(b)(5)(D)(ii); they do not have to also offset any other legislation going on in the same session. So Congress could pass one bill to patch the AMT (before or after the JSC bill), one bill to implement the doc fix, and one bill to extend the Bush tax cuts for the "middle class." Then the JSC could reduce the deficit by more than $1.2 trillion just through the cap on overseas contingency operations and the proposed cuts to Medicare and Medicaid. But I don't see how you get $3 trillion in "recommendations to the JSC," since those recommendations include $900 billion from letting the Bush tax cuts expire for the rich—which the CBO can't score as a tax increase.

Just an observation: President Obama has decided to frame his tax proposal as a $1.5 trillion tax increase on the rich (relative to current tax rates), when he could have framed it as a $2.4 trillion tax cut for the middle class (relative to current law). That's a purely political decision, and I'm not sure it's the right one, but his people are the experts, not I.

Finally, by assuming extension of the Bush tax cuts in his adjusted baseline, Obama has moved that item from a contestable policy choice to a fait accompli. It strikes me that no one should be happier about this outcome than President George W. Bush. Obama has basically endorsed making 80 percent of the Bush tax cuts permanent. Sure, the 20 percent for the rich was probably the part that Bush cared about the most. But it means that the core of Bush's domestic agenda—cutting taxes and depriving the federal government of revenue—is now safe. (As far as I can tell, Obama wants to keep the lower tax rates on investment income that were in the 2003 tax cut.) As I've said before, it was bad policy then, and it's bad policy now. But it will be with us for a long time.

September 19, 2011

Happy Constitution Day

By James Kwak

(Actually, it was on Saturday.) I just read Invisible Hands: The Making of the Conservative Movement from the New Deal to Reagan (W.W. Norton, 2009), by Kim Phillips-Fein. It's a history of the resistance from the business community to the New Deal and how it gave birth to at least one major strand of the modern conservative movement. One of Phillips-Fein's major points is that the conservative movement is not just a reaction to the civil rights movement, the 1960s, and the women's liberation movement (and Roe v. Wade). Those trends gave the conservative movement more energy and support, but business leaders had for decades been trying to build an intellectual and political movement that could reverse the New Deal. And while some of them talked about Christian values, what they really cared about were breaking unions and lower taxes.

I think this is relevant because it gets at the question of what the modern conservative movement and the Tea Party are all about. There has been a lot of work on this issue, from a variety of different angles. David Campbell and Robert Putnam looked at longitudinal surveys and found that the best predictors of being a Tea Party supporter are being an activist, conservative Republican and wanting religion to play a larger role in politics—which implies that the Tea Party is just the same foot soldiers who have backed the conservative movement for the past thirty years. Vanessa Williamson, Theda Skocpol, and John Coggin (Chrystia Freeland summary here) studied one local Tea Party movement in depth and found that there is something new about the movement:

"We find that the Tea Party is a new incarnation of longstanding strands in U.S. conservatism. The anger of grassroots Tea Partiers about new federal social programs such as the Affordable Care Act coexists with considerable acceptance, even warmth, toward long-standing federal social programs like Social Security and Medicare, to which Tea Partiers feel legitimately entitled. Opposition is concentrated on resentment of perceived federal government 'handouts' to "undeserving" groups, the definition of which seems heavily influenced by racial and ethnic stereotypes."

Jane Mayer famously described the Tea Party as the creation or the tool of the Koch Brothers and former Gingrich lieutenant Dick Armey. And a number of scholars, including Thomas Ferguson, have argued that political conservatism derives its strength not from a shift in popular attitudes, but from the money provided by businessmen with an anti-regulation, low-tax agenda.

Obviously, as with any complex phenomenon, there are nuances and differences—between elite organizers and grass-roots supporters, and between people who came to the movement for different reasons. I don't have anything particularly original to add here. But I think Phillips-Fein's book strengthens the relative position of the pro-business, anti-union, anti-regulation strand in the genealogy of the conservative movement (as opposed to the family values strand, or the true libertarian strand).

It also contains this gem for anyone who thinks the American people suddenly developed warm and fuzzy feelings about the Constitution in the past two years. Describing the 1934 founding of the American Liberty League—a rabidly anti-Roosevelt, anti-New Deal organization—she writes (p. 10):

"The main topic of discussion was creating a 'propertyholders' association,' as Irénée [DuPont] put it, to disseminate 'information as to the dangers to investors' posed by the New Deal. The group decided that the name of their association should not refer directly to property—it would be better to frame their activities as a broad defense of the Constitution."

September 17, 2011

What Next For Greece And For Europe?

By Peter Boone and Simon Johnson

Uncertainty about potential loan losses in Europe continues to roil markets around the world. For many investors, taxpayers, and ordinary citizens there is no clarity on the exact current situation – let alone a stable view about what could happen next. What should any friends of Europe — the US, G20, IMF, perhaps even China — strongly suggest that they do?

A good start would involve being honest on four points. There is nothing pleasant about the truth in such crisis situations, but continued denial increasingly becomes dangerous to all involved.

Greece is on the front burner. Currently on offer is a debt swap for private sector lenders that, once it goes through, will effectively guarantee 33 cents for every 1 euro in bonds that they currently hold. The downside protection here is attractive to banks – made possible by the fact they will now get hard collateral in the restructured deal (meaning that Greece buys the bonds of safe EU countries, like Germany, and holds these where creditors could get at them).

The first brutal truth is that this is a default by Greece and all attempts to deny this or use another word just muddy the waters.

Greece can probably afford to service debt restructured to this level – although that will depend also on the final terms of EU and IMF funding. But the second truth is that this is a wasted opportunity for Greece. It does not put their debt problems behind them and, most likely, they will be back to ask for further reductions in principal in the future.

The ice has been broken: The EU has agreed that a euro area member can default. Greece should now go all the way – aiming to end up with new bonds that have a 3 year grace period on interest and 10 year grace period on principal.

The third truth – and most difficult for many to stomach – is that, in the context of any such deeper debt restructuring, the Greeks should cut public sector wages across the board and bring down other spending to make their budget deficit much smaller immediately. They and the IMF need to assume another recession in 2012 and no growth for five years. They should aim to balance the primary budget on a cash basis in 2012 (since there would be no interest due, this would also mean they need no cash from any kind of lender). In this scenario, they could collateralize the new bonds with state property.

There is nothing particularly fair or at all just about this set of outcomes. Everyone in Greece is hurt now by the consequences of excessive spending, big deficits, and reckless lending (to the government) in the past.

The issue is: What are the alternatives? If it adopts some version of this deeper debt restructuring approach, Greece can stay in the euro zone and find its way back to growth (assuming the world economy does not go down again sharply). Its private sector will eventually rebound.

In contrast, if Greece were to leave the euro zone, its financial system would cease to operate – at present Greek banks depend to a great extent on support from the European Central Bank (for more background and the available numbers, see our recent Peterson Institute policy brief, Europe on the Brink; http://www.iie.com/publications/pb/pb11-13.pdf). Do not try to run any modern economy on a purely cash basis; the further fall in GDP would be enormous.

And if Greece pays its debts at the currently proposed level (33 cents in the euro), it will struggle to grow. The tax revenue needed to service that debt would burden businesses and households for decades – enterprising and productive people will move their fortunes and their futures elsewhere in the euro area or to the United States.

The fourth and most dangerous truth is that Italy and Germany are not ready for the next stage of the euro crisis.

Any further adverse developments in Greece will precipitate a run on Italy – involving investors selling Italian government debt. The European Central Bank is currently prepared to buy Italian bonds, to keep down interest rates below 6 percent.

The Germans are obviously very worried by this approach – hence the resignation last week of Jurgen Stark, who was the senior German representative in ECB management. He has been replaced by someone who is likely to take an even tougher line on bond buying.

Aside from the politics, the risk is that the euro loses credibility and falls steeply in value. The ECB thinks it can "sterilize" any bond buying by also selling its own bonds into the market – this would mean no net increase in the supply of money (just fewer Italian bonds and more ECB bonds being held by the private sector).

As a technical matter and in the short-term, the ECB may be right. But the ECB is taking on a lot of credit risk – if a big country defaults, the ECB would need to ask member governments to provide it with more capital and this is the kind of transparent fiscal hit that politicians hate.

And if ECB funding seems really unconditional, this just encourages countries not to be careful about their fiscal deficits. "Fiscal dominance" – meaning a central bank always buys up government bonds to keep interest rates down – is a recipe for big inflation.

Expect a great deal of shouting behind the scenes at the highest level in Frankfurt (ECB headquarters) and in European capitals. Instability seems unavoidable. Significant inflation may also follow – although first we will see serious recessions in the troubled European periphery, a ratcheting up of bond buying, and repeated political crises.

An edited version of this post appeared on the NYT.com's Economix blog. It is used here with permission. If you would like to reproduce the entire post, please contact the New York Times.

September 14, 2011

Does Disclosure Help?

By James Kwak

Following up on yesterday's column about corporate spending, I saw that John Coates (Harvard Law School) and Taylor Lincoln (Public Citizen) have published a study of the relationship between voluntary disclosure of political spending and company value (summary here). In short, after applying a bunch of controls, they find that companies with voluntary disclosure policies have price-to-book values that are 7.5 percent higher than companies that don't.

Citing earlier research, they also say, "among the S&P 500 – which accounts for 75 percent of the market capitalization of publicly traded companies in the U.S. – firms active in politics, whether through company-controlled political action committees, registered lobbying, or both, had lower price/book ratios than industry peers that were not politically active."

Of course, the causality could run either way, and Coates and Lincoln are not claiming that voluntary disclosure in itself makes a company more valuable. Disclosure policies make it less likely the CEO will blow company money on her pet political projects, and so it stands to reason that companies that are better governed in general—and hence more valuable—are more likely to have such policies. But it certainly implies that disclosure policies are not going to bankrupt the Great American Corporation.

September 13, 2011

Citizens United and Corporate Political Spending

By James Kwak

Today's Atlantic column is about corporate political spending in the wake of Citizens United and what, if anything, can be done about it. A group of corporate and securities law professors has petitioned the SEC to write rules requiring companies to disclose their political spending, just like they have to disclose their executive compensation today. As usual, I'm not too optimistic about what disclosure can achieve, especially disclosure in SEC filings or proxy statements: who reads those things, anyway? But it's better than nothing, and with the current makeup of the Supreme Court, nothing is just about what we've got now.

Simon Johnson's Blog

- Simon Johnson's profile

- 78 followers

{kind=link}