Simon Johnson's Blog, page 50

October 11, 2011

Bathtubs for Beginners

By James Kwak

In economics life there's a basic conceptual distinction between a flow and a stock. A flow is a something that occurs over some period of time, like water pouring from a faucet into a bathtub. A stock is something that exists at a specific moment of time, like the water in that bathtub. You measure a flow over a period of time (e.g., gallons per minute); you measure a stock at a specific moment in time (e.g., gallons). For a business, the income statement (revenues and costs in a year) measures flows, while the balance sheet (assets and liabilities) measures a stock. That's why the income statement is dated for a year (or a quarter) and the balance sheet is dated for a specific day. Everyone understands this. If you didn't, you would get confused between your salary and your bank account.

But not David Brooks.

In today's self-indulgently contrarian column, Brooks argues that the Occupy Wall Street movement is made up of "small thinkers." Here's his evidence:

"They will have no realistic proposal to reduce the debt or sustain the welfare state. Even if you tax away 50 percent of the income of those making between $1 million and $10 million, you only reduce the national debt by 1 percent, according to the Tax Foundation. If you confiscate all the income of those making more than $10 million, you reduce the debt by 2 percent. You would still be nibbling only meekly around the edges."

This is incoherent to begin with. Tax policy directly affects flows, not stocks, so its impact on the national debt (a stock) is indeterminate unless you specify a length of time for the policy to be in place.

If you look at the Tax Foundation report, it says that those two policies would increase taxes by $306 billion. The Tax Foundation doesn't even say in what year that would happen, but they link to a series that ends in 2009, so let's say they're using 2009 data. In 2009, GDP was $14.1 trillion, so $306 billion is 2.2 percent of GDP.

Now let's apply that to the CBO baseline. Right now, my updated CBO-style baseline shows national debt at 61 percent of GDP in 2021 and 59 percent in 2035. If you add 2.2 percent of GDP to revenues in every year beginning in 2012, those numbers fall to 44 percent in 2021 and 5 percent in 2035 (a reduction in the debt of 54 percentage points, or 92 percent). In other words, the entire long-term deficit problem goes away.

If you prefer to use the CBO alternative scenario (in which, among other things, the Bush tax cuts are made permanent), my updated alternative scenario shows the debt at 80 percent of GDP in 2021 and 142 percent in 2035. Increase revenues by 2.2 percent of GDP and those number become 63 percent and 91 percent. These are big, big differences—a lot more than "1 percent" and "2 percent" and "nibbling meekly around the edges."

Saying these tax changes would reduce the deficit by 3 percent (that's 1 percent + 2 percent, by the way) is a mistake that guts the rest of the column, which is based on the idea that major tax increases on the rich wouldn't matter. It doesn't surprise me that David Brooks can't do basic math, but doesn't he have a fact checker? Or at least an editor?

The people at the Tax Foundation, I assume, are not innumerate. David S. Logan, the person who wrote the analysis that Brooks cites, must have realized that, when you open the tap further, you can't estimate how much the water level in the bathtub will increase without specifying how long the tap will be open.* But their job is to come up with analyses that prove what they want to prove and hope that journalists will take the bait. Every so often one does.

Now, I don't think we should have a 100 percent effective tax rate on people who make more than $10 million. But the idea that increasing taxes on the rich will have a minimal impact on the national debt is pure innumeracy. David Brooks may have something valuable to say about, well, I don't know, but something else. But why is the Times letting someone who doesn't understand arithmetic write about budgetary issues and the national debt?

* At least I assume he knows it. His bio says that he is in a Ph.D. program in business economics at Washington University, a school where they know their math. (When I was in the Math Olympiad Program one of the teaching assistants was a student there.)

October 10, 2011

Too Big To Fail Under Dodd-Frank

By Simon Johnson. This post comprises the first three paragraphs of my latest Bloomberg column; you can read the full column there.

Here we go again. Major shocks potentially threaten the solvency of some of the world's largest financial institutions. Concerns grow over the ability of European leaders to shore up their banks, which are reeling from a sovereign-debt crisis. In the U.S., the shares of some large banks are trading at less than book value, while creditor confidence crumbles.

Private conversations among economists, regulators and fund managers turn naturally to so-called resolution powers — the expanded ability to take over and wind down private financial companies granted to federal regulators by the Dodd-Frank financial reform law. The proponents of these powers, including Tim Geithner and Henry Paulson, the current and former U.S. Treasury secretaries, argue that the absence of such authority in the fall of 2008 contributed to the financial panic. According to this line of thought, if only the Federal Deposit Insurance Corp. had the power to manage the orderly liquidation of big banks and nonbank financial companies, the government could have decided which creditors to protect and on what basis. This would have helped restore confidence, it is argued.

Instead, the government was forced to rely on the bankruptcy process, as in the case of Lehman Brothers Holdings Inc., or complete bailouts for all creditors, as in the case of American International Group. The FDIC already has limited resolution authority, which functioned well over many years for small and medium-sized banks.

To read the rest of this column, please click on this link to Bloomberg: http://www.bloomberg.com/news/2011-10-10/too-big-to-fail-not-fixed-despite-dodd-frank-commentary-by-simon-johnson.html

Straight Out of Antiquity

By James Kwak

In their paper on the Tea Party, Vanessa Williamson, Theda Skocpol, and John Coggin (Chrystia Freeland summary here) argue that one of the central principles of the Tea Party is a division of the world into workers who deserve what they earn (including Medicare and Social Security, which they like) and undeserving "people who don't work"—by which many mean the young, or even their own younger relatives.

We are the 99 Percent, the tumblr associated with Occupy Wall Street, is, among many other things, a kind of response to that worldview. The introduction takes it on directly:

"They say it's because you're lazy. They say it's because you make poor choices. They say it's because you're spoiled. If you'd only apply yourself a little more, worked a little harder, planned a little better, things would go well for you. Why do you need more help? Haven't they helped you enough? They say you have no one to blame but yourself. They say it's all your fault."

Mike Konczal (who, among his other talents, can use perl and python—who knew?) whipped together a quantitative analysis of the 99 Percent tumblr. The tumblr as a whole is depressing (you need to go look at it to know why), but Konczal's analysis adds another level of downer. As his numbers indicate (and my reading of a decent chunk of the pages confirms), there aren't many extravagant ambitions here: no expectations of material consumption, no expectations of self-actualization through work, no 60s-style dreams of peace and community. Instead, as Konczal puts it,

"The demands are broadly health care, education and not to feel exploited at the high-level, and the desire to not live month-to-month on bills, food and rent and under less of the burden of debt at the practical level.

"The people in the tumblr aren't demanding to bring democracy into the workplace via large-scale unionization, much less shorter work days and more pay. They aren't talking the language of mid-twentieth century liberalism, where everyone puts on blindfolds and cuts slices of pie to share. The 99% looks too beaten down to demand anything as grand as 'fairness' in their distribution of the economy. There's no calls for some sort of post-industrial personal fulfillment in their labor—very few even invoke the idea that a job should 'mean something.' It's straight out of antiquity—free us from the bondage of our debts and give us a basic ability to survive."

I'm not saying this is a downer because I think the people sending in photos to We Are the 99 Percent, or the people occupying Zuccotti Park, should have a detailed political program or that they should be mobilizing to overthrow the bourgeoisie.* It's because it shows, in Warren Buffett's words, how far the class warfare has already gone—and how overwhelmingly his class has won. When the primary hope of workers is not to feel so tired anymore, it seems we've regressed back to a time even before the organized labor movement.

Konczal cites David Graeber and Moses Finley for the idea that premodern popular demands focused on canceling debts and redistributing land. A friend of mine brought this up to me a few weeks ago, too. His question at the time was about the Tea Party: when has there been a populist movement that wanted to make money harder? Remember, the Tea Party began with Rick Santelli calling people who were underwater on their houses "losers." In retrospect, it seems like a brilliant preemptive strike by the creditor class.

* Apparently it's been so long since I used the word "bourgeoisie" that I couldn't even remember how to spell it at first. There's a message in there somewhere.

[image error]

[image error]

[image error]

October 9, 2011

Baseline Scenario Goes Glossy

By James Kwak

Simon and I wrote an article for the November issue of Vanity Fair about—well, about a lot of things. It's about the eighteenth-century rivalry between Great Britain and France, the lessons of the American Revolutionary War, the Hamilton-Jefferson debates (again), and the War of 1812. It's also about present-day fiscal policy and budgetary politics. The main question we take up is what the Founding Fathers (from the Constitutional Convention through their involvement in the War of 1812) thought about a strong central government, the national debt, and the taxes necessary to pay for them, and what that means for today. All that in less than 3,000 words, so there isn't a lot of room for all the details.

You can read the article online here.

Wall Street and Silicon Valley

By James Kwak

Whenever someone criticizes "Wall Street," someone else tries to defend Wall Street by saying that without it we wouldn't have Silicon Valley and all of its wonders. Most recently, A.S. at Free Exchange says this:

"What would Silicon Valley have been without venture capital and private equity? Apple's spectacular growth was made possible by the capital it raised in financial markets (it is a public company).

"Much of Apple's initial investment came from an angel investor (a relative or friend who provides the start-up capital). But most new companies rely on formal capital markets. In a 2009 working paper, Alicia Robb and David Robinson investigated the capital structure of start-up firms, and found that 75% primarily relied on external financing from formal capital markets, usually credit cards and bank loans in their first year. They also found that firms that used formal credit were more successful."

As critics of Wall Street go, I probably find this more annoying than most because, well, I worked in Silicon Valley. Most of these comments are obvious, but here goes anyway.

Venture capital has been around for centuries; in its current form, it dates back to the 1950s. Venture capital is one of the most un-innovative forms of finance around: it's equity investment in the form of preferred shares, generally without leverage. The skill it requires is the ability to identify companies that will be successful. Venetian bankers were good at it back before the Renaissance.

(Private equity? What does private equity have to do with HP, Intel, Apple, Oracle, Sun, etc.? There are technology private equity firms such as Silver Lake, but like most private equity firms they focus on mature companies.)

The initial public offering and the secondary public offering (as in "[Apple] is a public company") have been around for centuries. Yes, they involve Wall Street investment banks, but they worked perfectly well before the modern age of financial innovation.

Credit cards have been around since the 1950s. But that's just when the current technology (plastic) was introduced; as a type of finance, there are just unsecured personal lending, which has been around for millennia. You could try to argue that securitization slightly lowered credit card interest rates, but I don't think that's the difference between Google existing and Google not existing.

Ditto for bank loans, except that few if any small business loans are securitized (not homogeneous enough).

Obviously technology startups need capital, but they raise capital in ways that have been around for decades or centuries—not ways that were thought up by former physics Ph.D.s since 1980. Simply saying that capital is good isn't much of a defense of Wall Street, unless you think critics of Wall Street are against capital in all its forms. (A few may be , but many of us are not.) This reminds me of when Ben Bernanke gave a speech praising financial innovation but, as Ryan Avent pointed out, he couldn't come up with an example more recent than the 1970s.

There are certainly ways you can argue that recent financial innovation (custom derivatives, structured finance, the whole works) is good for the economy. But don't try to count Silicon Valley as one of them.

October 6, 2011

The 4 Trillion Euro Fantasy

By Peter Boone and Simon Johnson

Some officials and former officials are taking the view that a large fund of financial support for troubled eurozone nations could be decisive in stabilizing the situation. The headline numbers discussed are up to 2-4 trillion euros – a large amount of money, given that German GDP is only 2.5 trillion euros and the entire eurozone GDP is around 9 trillion euros.

There are some practical difficulties, including the fact that the European Financial Stability Fund (EFSF) as currently designed has only around 240 billion euros available (although this falls if more countries lose their AAA status in the euro area) and the International Monetary Fund – the only ready money at the global level – would be more than stretched to go "all in" at 300 billion euros. Never mind, say the optimists – we'll get some "equity" from the EFSF and then "leverage up" by borrowing from the European Central Bank.

Such a scheme, if it could get political approval, would buy time – in the sense that it would hold down interest rates on Italian government debt relative to their current trajectory. But leaving aside the question of whether the ECB – and the Germans – would ever agree to provide this kind of leverage and ignoring legitimate concerns about the potential impact on inflationary expectations of such measures, could a, for example, 4 trillion euro package really stabilize the situation?

To answer this question, think through the "best case" scenario in which the big package is put in place and, at least initially, believed to be credible. Proponents of this approach argue that in this case the "market would be awed into submission", business as usual would prevail – meaning that Italy and other potentially troubled sovereigns could resume borrowing at low interest rates – and the 4 trillion euro fund would not actually need to be used.

This seems implausible. If the big government money shows up and this pushes down yields on Italian government debt, what will the private sector holders of that debt do? Some of them will sell – taking advantage of what they worry may only be a temporary respite and, for those who bought near the bottom, locking in a capital gain (as interest rates fall, bond prices rise – there is an inverse relationship).

So the European/IMF bailout fund would acquire a significant amount of Italian, Portuguese, Spanish and other debt (including perhaps Greece and Ireland). If the credit utilized from this fund, with its ECB backing, reaches – let's say – 1 trillion euros, how will the Germans feel about the situation? Their worries will only be exacerbated by ongoing budget deficits, exacerbated by recessions, throughout the periphery. Someone will need to finance those deficits, and the stabilization fund is likely to be the financier.

On current form, the Italians will have promised moderate austerity but delivered little. The life styles of rich and famous Italian leaders will start to grate on north European taxpayers. Stories about corruption in Italian public life – perhaps exaggerated but with more than a grain of truth – will become pervasive.

In fall 1997, the IMF – with US and European backing – provided what was then regarded as a substantial package of support to the Suharto government in Indonesia. But then the government refused to close banks as agreed – and after one of President Suharto's sons finally lost one failed bank, he immediately popped up again with another banking license. Stories about Indonesian official corruption and the ruling family were on front pages of major newspapers in the US.

Donor fatigue set in. In January 1998, when the Indonesian government announced a budget that had slightly less austerity than planned, it was roundly castigated by the international community. This set off a further sharp depreciation in the Indonesian rupiah, which worsened the debt problems of the Indonesia corporate sector – which had borrowed heavily and at short maturities in dollars. Panic set in, social unrest became increasingly manifest, and the real economy declined further.

Italy is not Indonesia and Mr. Berlusconi is not President Suharto – who ended up leaving office. But the comparison is still has value. Will the countries backing the enhanced and highly leveraged EFSF be willing to face substantial potential credit losses, i.e., actual and ongoing transfers from their taxpayers to Italians and others?

Lech Walesa famously remarked, it is easier to make fish soup from fish than to do the reverse. So it is with fiscal crises – once fear prevails and markets start to think hard about the stress scenario, it is hard to solve the problem simply with reassuring words or financial support that never needs to be used.

Crisis veterans like to say, quoting former President Ernesto Zedillo of Mexico: When markets overreact, policy needs to overreact in the stabilizing direction. But what really matters is not overreacting; it is making sure you do enough.

In Europe, the first thing peripheral governments need to do is stop accumulating debt, and quickly. Italian fiscal plans to balance the budget in 2012 look implausible as they assume unrealistic growth. The currently planned Greek debt restructuring and increased taxes will not turn that economy around — nor prevent Greece from accumulating even further debt. Despite all the reported austerity, the Irish government is still running a budget deficit near 12% of GNP in 2011 while nominal GNP actually declined in the first half of 2011.

Europe's periphery also needs to recognize that it signed up to a currency union, and that requires a new approach to adjustment. Instead of having massive devaluations like Zedillo's Mexico, or Suharto's Indonesia and Walesa's Poland, Europe's troubled nations need to improve competitiveness through reducing local costs. That must primarily come through wage reductions and more competitive tax systems. In Ireland a pact with the major unions is preventing further wage reductions, while in Greece the government is strangling corporations with taxes in order to avoid deeper wage and spending cuts. The proposed Portuguese "fiscal devaluation" – meaning lower payroll taxes to reduce labor costs and increase VAT to replace the revenue – looks like a weak attempt to avoid talking about the need to much more sharply cut public spending and wages in real, purchasing power terms.

Putting in place a huge financial package is not enough. Policies have to adjust across the troubled eurozone countries so that nations stop accumulating debt, and the periphery moves rapidly from being least competitive nations in the euro area, to the most competitive and this includes lower real wages, even if debts are restructured appropriately. The European leadership is a long way from even recognizing this reality – let alone talking about it in public.

An edited version of this post appeared this morning on the NYT.com's Economix blog; it is used here with permission. If you would like to reproduce the entire post, please contact the New York Times.

October 4, 2011

The Bad Old Days

By James Kwak

There was a time when the main purpose of this blog was to explain just how some government policy or other official action was designed to benefit some large bank under the cover of the public interest. In a bit of nostalgia, I wrote this week's Atlantic column on the Freddie Mac–Bank of America story reported on by Gretchen Morgenson. It's clear that Bank of America got a sweetheart deal from Freddie. The question is why. Did Freddie Mac's people, some of the most knowledgeable people in the country when it comes to mortgages, not realize they were giving away money? (Hint: Probably not.) Did FHFA examiners, some more of the most knowledgeable people in the country when it comes to mortgages, not realize that Freddie was giving money away? (Hint: See above.)

It's amazing that after three full years of our government trying to give Bank of America money at every possible opportunity, it's still a basket case. Now it's charging people $5 per month to use their debit cards. Yes, this is a predictable response to new Federal Reserve regulations limiting debit card fees. But it's easily avoidable: just find another bank. (Neither of mine charges me debit card fees.) Not every bank out there is still trying to pay for the Countrywide acquisition.

October 3, 2011

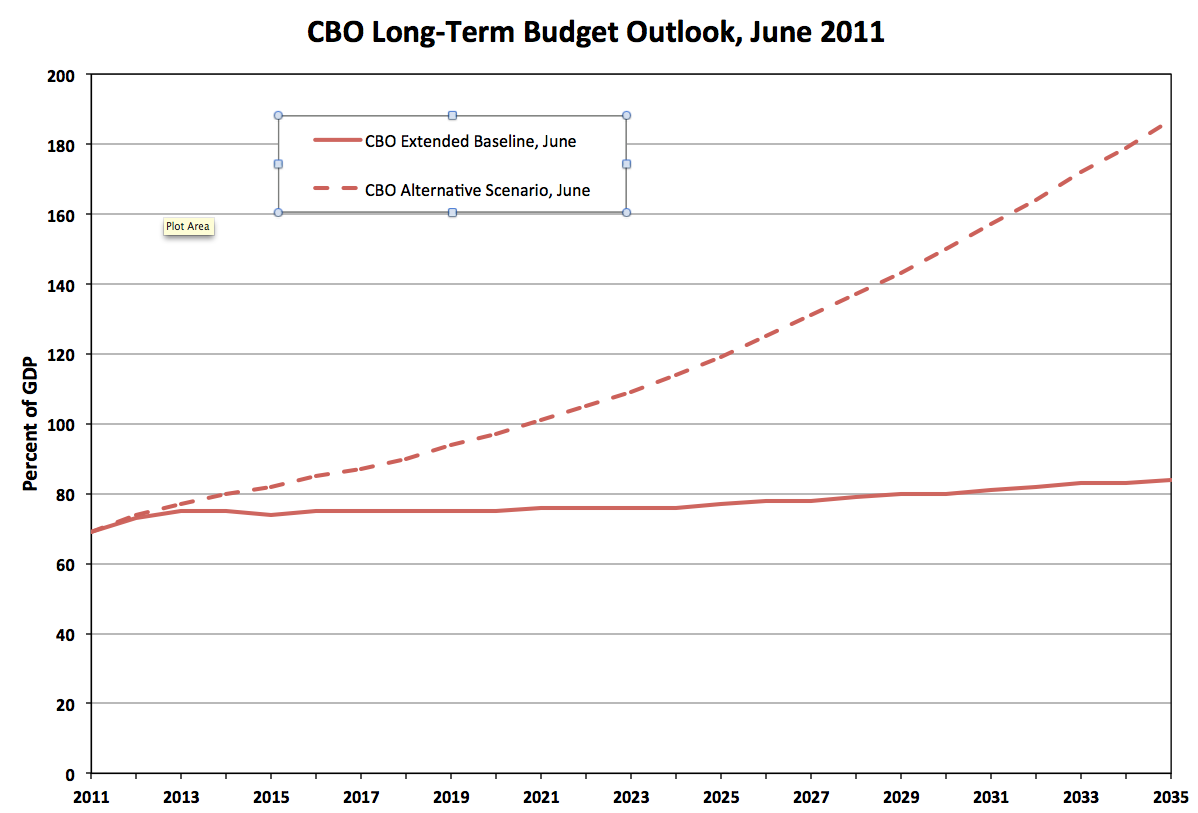

How Big Is the Long-Term Debt Problem?

By James Kwak

Articles about the deficits and the national debt generally talk about unsustainable long-term deficits that will drive the national debt up to a level where scary things happen. Sensible commentators usually acknowledge that our current deficits are a sideshow and the real problems happen in the 2020s and 2030s due to modestly increasing Social Security outlays and rapidly increasing health care spending. I admit that this has generally been my line as well; for example, in a previous post I said that the ten-year deficit problem is entirely a product of extending the Bush tax cuts, but that even if we let them expire things will get worse over the next two decades.

But looking at the numbers, it's not clear that the long-term picture is really that bad. Here I'll lay out the numbers, and then, as they say on Fox News, you can decide. The summary is the chart above; the details are below.

The most common source for long-term national debt scare stories is the CBO's 2011 Long-Term Budget Outlook (LTBO), published in June. That report has two scenarios. In the extended-baseline scenario, which is pretty close to current law, the national debt reaches 76% of GDP in 2021 and 84% in 2035 (Table 1-2, p. 8)—bad, but not that bad. In the alternative fiscal scenario, which is intended to be more realistic (and which everyone cites for dramatic effect), the debt reaches 101% in 2021 and 187% in 2035—the latter being a level that virtually everyone would consider too high.

But things have changed since June, notably because of the Budget Control Act signed in August. In the CBO's Budget and Economic Outlook: An Update (BEO), published in August, the 2021 national debt in the baseline scenario (which the CBO uses as the first part of its long-term extended-baseline scenario) is down from 76% to 61% of GDP (Table 1-2, pp. 4–5). We can also tell what the alternative fiscal scenario's updated 2021 projection would be by reapplying the adjustments included by the CBO in that scenario (extension of all expiring tax cuts, Medicare doc fix, and Iraq/Afghanistan drawdown); in that case, the projected 2021 debt has fallen from 101% of GDP to 80%.* (More on this later.)

So far this is is child's play, since I'm just adding together numbers from different CBO tables. But we're really interested in 2035 for now. The questions I want to answer are: first, what would the CBO's new extended baseline say for 2035? and second, what is a realistic 2035 forecast?

2035 Extended-Baseline Scenario

The task here is to apply the same method used in the LTBO extended-baseline scenario to the new numbers. On the revenue side, revenues grow slowly because of real bracket creep (tax brackets are indexed for inflation, but over time average wages rise faster than inflation) and demographic trends. In the LTBO, the growth rate of revenues as a percentage of GDP from 2021 to 2035 is 0.78 percent per year (calculated from the supplemental data), so I use that in all of my projections. (That's 0.78 percent per year, not 0.78 percentage points per year.) Under that assumption, revenues grow from 20.9% of GDP in 2021 to 23.3% in 2035.

On the spending side, the LTBO breaks spending into four categories: Social Security; Medicare, Medicaid, CHIP, and exchange subsidies (most but not all health care entitlements); other noninterest spending; and net interest. There's no reason to change the June baseline estimates for the first two categories (6.1% and 9.2% for 2035, respectively). For other noninterest spending, the LTBO approach is to assume that this category remains constant as a share of GDP except for a few adjustments that make it fall slightly between 2021 and 2035, from 8.3% to 7.8%. But because of the Budget Control Act, this category has already fallen to 7.7% by 2021, so in my spreadsheet I just leave it at 7.7% through 2035.** Given the 2021 debt, the 2021 budget, a real interest rate of 2.7% (LTBO, p. 17), a real growth rate of 2.1% (LTBO supplemental data), and an inflation rate of 2.5% (LTBO supplemental data), you can project out future budgets. Net interest spending in 2035 turns out to be 3.0% of GDP. Total spending is 26.0% of GDP, the deficit is 2.7%, and the national debt is only 59% of GDP—smaller than it is today (and down from the 84% predicted in June).

2035 Realistic Scenario

Now, everyone knows that the CBO baseline is not realistic, so it's time for the adjustments. First we apply the uncontroversial ones: the AMT patch, the Medicare doc fix, and the more rapid drawdown of troops from Iraq and Afghanistan. As I've pointed out before, these basically cancel out over ten years, and the 2021 national debt stands at 60% of GDP (down from 61% in the baseline). The CBO's alternative fiscal scenario also assumes that discretionary spending grows with GDP before 2021, rather than with inflation as in the baseline scenario. But the Budget Control Act capped discretionary spending growth below the rate of inflation. So if we assume that Congress follows the law it set for itself, then discretionary spending remains low, even in the alternative scenario.

Going out to 2035, revenues are starting at a lower base (20.3% of GDP). Applying the same growth rate as in the LTBO, they grow to 22.7%.

For spending, first I use the same Social Security projection as in the extended baseline. (The LTBO uses the same numbers for both scenarios.) For health care spending, I use the numbers from the LTBO's alternative fiscal scenario—the more pessimistic ones. Other noninterest spending is where things get interesting. In 2021, this category is down to 7.1% of GDP because of the Budget Control Act (which capped discretionary spending growth below the inflation rate) and the Iraq/Afghanistan drawdown. Again, I assume this remains constant as a share of GDP (not falling slightly, as in the LTBO).

With these assumptions, you get 2035 spending of 26.9% of GDP, a deficit of 4.2%, and a national debt at 69% and growing slowly. That's with business as usual for Social Security, Medicare, Medicaid, and the health insurance exchanges. You could make a strong case that this is a problem, especially if you worry (like I do) about things like major financial crises, and the national debt should be lower than 69% of GDP. But it's not obviously, unequivocally a national emergency. And the idea that we have to gut entitlement programs doesn't make sense.

(There are two other reasons this is a conservative (high) estimate. First, I use the CBO's assumption that the Joint Select Committee reduces deficits by a total of $1.2 trillion between now and 2021. But I assume that they do so in a way that does not affect deficits in any year after 2021, which is highly unrealistic. Second, since this realistic scenario has lower debt levels than in the CBO extended baseline, economic growth should be slightly higher on the CBO's theory of the world. (See LTBO, chapter 2.))

Now, there is a big problem in this world: it's that the rest of the government has been crippled by the Budget Control Act. By 2021, discretionary spending will be down to 5.5 percent of GDP—the lowest level since 1931. I'm not saying this is a happy outcome. I'm just saying it's an outcome where the national debt is probably not our biggest problem—it's the fact that we've eliminated almost everything except Social Security and health care programs.

2035 Realistic Scenario with Tax Cuts

Of course, everything gets worse if you assume that the Bush-Obama income and estate tax cuts are made permanent, as the CBO does in its alternative fiscal scenario. In that case, the 2021 national debt is up to 76% of GDP.*** 2021 revenues are only 18.4% of GDP; growing at the same rate as above, they only make it to 20.5% by 2035. Spending is the same as above, except that since deficits are so much bigger every year between now and then, total spending (including interest) is 29.3% of GDP in 2035. The deficit is 8.7% of GDP and the national debt is 117% and growing fast. I think most people would agree that that is a big problem.

2035 Alternative Fiscal Scenario

We can update the CBO's alternative fiscal scenario, too, as I showed two figures above. It's just the previous scenario (realistic with tax cuts), plus extending all other expiring tax cuts (which I think is a dubious assumption for reasons I won't go into here), plus an assumption that tax revenues remain at their 2021 share of GDP indefinitely. (That is, Congress periodically cuts tax rates to compensate for a slowly expanding real tax base.) I think this assumption is gratuitously pessimistic (from a budgetary standpoint). Basically, it is an example of assuming your conclusion: if you want to conclude that we're going to have a huge deficit problem, there's no better trick than assuming that Congress constantly makes sure that tax revenues are too low.

In that scenario, the national debt in 2035 is 142% of GDP and climbing rapidly.

Conclusions

So the bottom line is: If we extend the Bush tax cuts, we have very big deficit problems over the next ten years and the next twenty-five years. If we let them expire, there is no ten-year problem. That's the same as in my earlier post, and I don't think that's controversial to anyone who understands the numbers.

What's more controversial is my claim that if we let the tax cuts expire, there is a twenty-five year problem, but it's not a huge one. Many other people argue that even if we let the tax cuts expire, we still have to cut Social Security and Medicare. On my reading, the problem is a national debt at 69% of GDP and growing steadily. If we have another financial crisis, or we start losing our status as the reserve currency, that could be a serious problem. My opinion is we should do something about it. But it's not necessarily the end of the world.

I've already pointed out a few places where my estimates are conservative, so I should also point out a couple of ways I could be underestimating future deficits (other than the obvious one that the tax cuts will probably be extended). Probably the biggest is that I import the CBO assumption that "other noninterest spending" will be a constant share of GDP after 2021—after it has already been slashed by the Budget Control Act. There is probably a fair chance that Congress will find a way to repeal those caps even before 2021.

Another, smaller issue is that I don't have an allowance for "other means of financing" to increase deficits after 2021. In theory OMF shouldn't systematically increase or decrease the debt (except a little bit, since financing accounts need to grow a little as the economy grows), but maybe there's a practical reason why it usually ends up adding to deficits. If so, can someone let me know?

Of course, the interest rate and growth rate assumptions (from the CBO) could be wrong, but they both look conservative to me, especially a 2.1% real growth rate.

I happen to think we do have a long-term deficit problem. I just think it may be somewhat smaller than the conventional inside-the-Beltway wisdom would have you believe.

For those interested, I've attached my spreadsheet with all of the scenarios discussed above. It includes the CBO spreadsheets that I used as my starting point.

* The BEO provides a 2021 debt estimate of 82 percent of GDP under certain alternative policies (pp. 2–3), but it uses different adjustments than the LTBO. The BEO does not include the Iraq/Afghanistan drawdown, which is included in the LTBO, and it extends fewer tax cuts than the LTBO.

** This is a conservative assumption; if I mimicked the LTBO exactly, it would fall from 7.7% to 7.4% or lower.

*** This is basically the 82% figure on page 3 of the BEO, less the deficit savings from the Iraq/Afghanistan drawdown.

October 2, 2011

What Would It Take To Save Europe?

By Simon Johnson

Last weekend official Washington was gripped by euphoria, at least briefly, as people attending the IMF annual meetings began to talk about how much money it would take to stabilize the situation in Europe. At least one eminence grise suggested that 1.5 trillion euros should do the trick, while others were more inclined to err on the side of caution – 4 trillion euros was the highest estimate I heard.

This is a lot of money: Germany's annual Gross Domestic Product (GDP) is only about 2.5 trillion euros, and the combined GDP of the entire eurozone is about 9.5 trillion euros. The idea is that providing a massive package of financial support would "awe" the markets "into submission" – meaning that people would stop selling their holdings of Italian or Spanish debt and thus stop pushing up interest rates. Ideally, investors would also give Greece and Portugal some time to find their way to back to growth.

But this is the wrong way to think about the problem. The issue is not money in the form of external financial support – provided by the IMF or other countries to parts of the European Union. The real questions are: will Italy get complete and unfettered access to the European Central Bank, and when will we know this?

The big package approach to economic stabilization was most famously demonstrated in the 1994-5 Mexican crisis. With their currency under great pressure, President Ernesto Zedillo and finance minister Guillermo Ortiz arranged a $45 billion loan, a large part of which came from the United States. This may look like a small amount today, but at the time it was seen as a large amount of support. President Zedillo famously remarked that when markets overreact, policy should in turn overreact – meaning, in this context, put more money on the table than is needed. When the financial firepower is overwhelming, as was the Mexican case, it does not have to be used – in fact, the Mexican loan was paid back in about a year.

But this version of Mexican events skips an important detail. It's true that the external financial support helped prevent the complete collapse of the currency, but the Mexican peso did still depreciate significantly. Prior to the crisis, Mexico had a large current account deficit – meaning it was importing more than it was exporting, and the difference was covered by capital inflows (mostly foreigners being willing to lend to the Mexican government.) With the exchange rate depreciation, exporting from Mexico became much more attractive – an export boom of this kind always helps close the current account deficit and also stimulate the economy in a sensible manner.

Important parts of the eurozone, such as Portugal, Greece and perhaps Italy, badly need a reduction in their real costs of production. If their currencies were independent, this could be achieved by a depreciation of the market value of their exchange rate. But this is not an option within the eurozone – and it is within the zone that they need to become more competitive.

These countries could also cut nominal wages – a course of action that is being pursued, for example, in Latvia. But it is unlikely that any government making such a proposal would last long in Western Europe. Latvia is a special case for many reasons, including its desire to become much closer with the eurozone – to which it aspires to join.

Unable to move the exchange rate and unwilling to cut wages, the Portuguese government is embarked on an innovative course of "fiscal devaluation," meaning that they will cut payroll taxes – to reduce the cost of hiring labor – while also increasing VAT (a tax on consumption) as a way to maintain fiscal revenues. Unfortunately, "innovative" in the context of stabilization policies often means "unlikely to succeed" – and the precise implementation of this scheme, with some very complex details, seems fraught with danger.

Europe needs a new fiscal governance mechanism, to be sure. Why would Germany – or anyone else – trust Italy under Silvio Berlusconi with a big loan or unlimited access to credit at the European Central Bank?

Greece and some other countries have serious budget difficulties. But most of the European periphery also faces a current account crisis – something has to be done to increase exports or reduce imports or both. If the exchange rate can't depreciate, wages won't be cut, and "fiscal devaluation" proves unworkable, activity in these economies will need to slow down a great deal in order to reduce imports and bring the current account closer to balance – unless you (or the Germans) are willing to extend them large amounts of unconditional credit for the indefinite future.

And as these economies slow down, their ability to pay their government debts will increasingly be called into question. Last week the IMF cut the growth forecast for Italy in 2012 down to 0.3 percent. With interest rates pushing up towards 6 percent, it is easy to imagine Italy's debt relative to GDP climbing even further than in the still-benign official projections.

If Italy or any other eurozone country is in good shape and can pay its debts, the European Central Bank (ECB) can provide ample short-term support – through buying up bonds to prevent interest rates from reaching unreasonable levels. The euro is a reserve currency – meaning investors around the world hold it as part of their rainy day funds – and all European debt is denominated in euros. In Mexico in 1994, for example, much of their debt was in dollars; in such a situation, a foreign loan can help stabilize a crisis – although even there the right policies have to be put in place.

But if Italy cannot pay its debt, then the ECB has no business lending to it. The Europeans have to decide for themselves: Is Italy's fiscal policy reasonable and responsible? If yes, provide full support as need – from within the eurozone. If not, then find another way forward.

But please get a move on with this decision.

An edited version of this post appeared on the NYT.com's Economix blog; it is used here with permission. If you would like to reproduce the entire post, please contact the New York Times.

September 30, 2011

Edmund Burke and American Conservatism

By James Kwak

It has become a truism that modern American conservatism is revolutionary in the sense that it seeks to overturn the established order rather than to preserve it. "Reagan Revolution," "Tea Party"—the very names for the movement announce that is about more than defending the status quo. In the conservative worldview, America (or "Washington," or the "mainstream media," or some other powerful stratum) is dominated by a liberal-intellectual-academic-bureaucratic-socialist-internationalist (pick two or more) elite that must be overthrown. So in at least a mythical sense, conservatism is about restoration, which is something very different from "conserving" what exists today.

When did this happen? According to one view of the world, to which I have been partial in the past, there was once an ideology called conservatism that really was conservative in the narrow sense: that is, it counseled maintaining existing institutions on the grounds that radical change was dangerous. The Rights of Man and the Citizen may be great, but soon enough you have the Committee of Public Safety and the guillotine. On this reading of history, conservatism became radical sometime after World War Two, when it gave up accommodation with the New Deal in favor of rolling the whole thing back, ideally all the way through the Sixteenth Amendment.

In The Reactionary Mind,* however, Corey Robin has a different take: conservatism, all the way back to Edmund Burke, has always been about counterrevolution, motivated by the success of left-wing radicals and consciously copying their tactics in an attempt to seize power back from them. Conservative thinkers were always conscious of the nature of modern politics, which required mobilization of the masses long before Nixon's silent majority or contemporary Tea Party populism. The challenge is "to make privilege popular, to transform a tottering old regime into a dynamic, ideologically coherent movement of the masses" (p. 43). And the way to do that is to strengthen and defend privilege and hierarchy within all the sub-units of society (master over slave, husband over wife, employer over worker).

Now, the conservative movement in America is what it is; whether Edmund Burke would have blessed it or not is not going to change the number of signatories to the Taxpayer Protection Pledge. But Robin's book should make people skeptical of the occasional claim that there is some "good conservatism" represented by, say, George Will, and some "bad conservatism" represented by, say, Sarah Palin. (I would have said Rick Perry, but these days it seems poor Palin can use all the media mentions she can get, since even Chris Christie is out-trending her.)

Robin also highlights the importance of victimhood in conservatism, going back to Edmund Burke's tears for Marie Antoinette. To restore something, you have to have lost something in the first place. In the 1970s, it was the idea that business was being beaten up by labor that finally got the business community to organize behind the Republican Party (see Hacker and Pierson, Winner-Take-All Politics; Phillips-Fein, Invisible Hands); without that money, conservatism would still be about as powerful as it was in 1964. The idea that ordinary Americans are being trampled on by the liberal-bureaucratic elite, which is so central to the fundraising strategies of the NRA and other lobbying groups, is part and parcel of the whole ideology, not a clever idea thought up by Wayne LaPierre.

Of course, you can always get into an argument about which specific positions can lay claim to the word "conservative" and which can't. To the extent that you feel bound by intellectual history, then I think Robin has a strong argument. To the extent that words are what you make them, I guess everyone has equal claim to the word.

For more, see Robin's guest post at Rortybomb.

* I got a pre-publication copy free from the publisher. I also went to high school with Corey, but haven't seen him in a couple of decades.

Simon Johnson's Blog

- Simon Johnson's profile

- 78 followers