Jonathan Clements's Blog, page 344

December 1, 2019

Imagining the Worst

IF THE NAME Harry Browne doesn���t ring any bells, I���m not entirely surprised. Though he was twice a presidential candidate, he never captured more than 1% of the vote. Still, to my knowledge, Browne is the only financial advisor ever to run for the White House.��

As a Libertarian, some of Browne���s economic proposals were extreme���including, for instance, abolishing income taxes. But one of his ideas has stood the test of time: In his 1981 book,��Inflation-Proofing Your Investments, Browne introduced the concept of the ���permanent portfolio.���

Browne���s permanent portfolio was designed to make an investment mix ���bulletproof,��� able to withstand these four extreme events:

Hyperinflation, like that experienced by Germany after the First World War.

Deflation, along the lines of what Japan has suffered over the past 15 years.

Confiscation of assets, as seen in Venezuela, for example.

Devastation, including war and natural disasters.

How would the permanent portfolio simultaneously protect against all four of these extreme possibilities? Browne���s approach was to identify at least one asset that would survive each calamity. When there���s deflation, for example, cash turns out to be a great investment. When there���s inflation, stocks do well.

Using this logic, Browne was able to construct a portfolio that wasn���t necessarily immune to losses, but would at least be��more immune��than other approaches. Thus was born the permanent portfolio, which was comprised of four asset classes, held in equal amounts: stocks, long-term government bonds, gold and cash.

How has the permanent portfolio done over time? It depends how you look at it. From a performance perspective, it has lagged. Since 2001, the permanent portfolio has grown by a cumulative 170%, while the U.S. stock market has returned 278%. But that ignores risk, which was Browne���s primary concern. On that score, the permanent portfolio was a star performer exactly when investors needed it most. In 2008, when the U.S. stock market lost 37%, the permanent portfolio gave up less than 1%.

Others have followed in Browne���s footsteps. Notably, hedge fund manager Ray Dalio has popularized what he calls an��all-weather portfolio, which is a near carbon copy of Browne���s portfolio. In fact, the concept predates Browne himself. Two thousand years ago, the Babylonian Talmud included this exhortation: ���Let every man divide his money into three parts, and invest a third in land, a third in business and a third in reserve.��� Similar ideas can be found in the writings of King Solomon, Shakespeare and others.

Is this the best way to invest? With the stock market again at all-time highs, it���s a question that many people are asking. As always, the answer is, ���It depends.��� There���s no such thing as the perfect portfolio���one that delivers strong returns with no risk. Everything involves tradeoffs. And in any case, I don���t believe in a one-size-fits-all approach. We���re all different. To help choose the approach that���s best for you, I suggest asking five questions:

1. How much risk can you��afford��to take?��This was Browne���s primary concern. If you���re retired and need money from your portfolio to pay the bills, you can���t afford to lose all of your savings���but you may be able to afford to lose��some. This is a simple mathematical question, and the answer will tell you how much you can afford to put at risk.

2. How much risk do you��need��to take?��If you���re early in your career, you���ll want to invest in stocks to help your savings grow. But if you���ve already saved enough for retirement and your other goals, then you don���t��need to take any risk. You may still��choose to, but it���s important to recognize when risk is optional and when it���s required.

3. How much risk are you��willing��to take?��How much do the regular ups and downs of the market affect you? How much do you worry about the sorts of extreme risks that kept Harry Browne up at night?

4. How much do you care about keeping up with the market?��On any given day, how often do you hear references to the Dow or the S&P 500? These numbers are printed and recited innumerable times in the media every day, so it���s natural to compare your results to these benchmarks.

But here���s where it gets tricky. The more you diversify, the more your results will differ from these commonly cited indexes, and that carries a psychic cost. Sometimes, you���ll do better than the Dow or the S&P and sometimes worse. But however you fare, you can���t do an apples-to-apples comparison with these major indexes, because you can���t quantify the peace of mind that comes with greater diversification.

5. How important is it to accumulate the absolute maximum number of dollars?��If your primary goal is to grow your investments, that���s a very different objective from Harry Browne���s. It���s an entirely valid objective���but it���s going to involve a very different portfolio and will likely involve a far bumpier ride.

Adam M. Grossman���s previous articles��include The Unwanted Payday,��No Comparison��and��A Graceful Exit

. Adam is the founder of��

Mayport Wealth Management

, a fixed-fee financial planning firm in Boston. He���s an advocate of evidence-based investing and is on a mission to lower the cost of investment advice for consumers. Follow Adam on Twitter��

@AdamMGrossman

.

Adam M. Grossman���s previous articles��include The Unwanted Payday,��No Comparison��and��A Graceful Exit

. Adam is the founder of��

Mayport Wealth Management

, a fixed-fee financial planning firm in Boston. He���s an advocate of evidence-based investing and is on a mission to lower the cost of investment advice for consumers. Follow Adam on Twitter��

@AdamMGrossman

.

HumbleDollar makes money in four ways: We accept��donations,��run advertisements served up by Google AdSense, sell merchandise and participate in��Amazon‘s Associates Program, an affiliate marketing program. If you click on this site’s Amazon links and purchase books or other items, you don’t pay anything extra, but we make a little money.

The post Imagining the Worst appeared first on HumbleDollar.

November 30, 2019

Breaking Bad

WE ALL DO things that make us feel good right now, but which aren���t so good for us over the long haul. Yes, even me. Yes, even you.

Some of this behavior stems from hardwired instincts passed down to us from our hunter-gatherer ancestors, like our tendency to consume whenever we can and to focus too much on��today, while giving short shrift to tomorrow. Other damaging behavior is the result of habits we���ve developed, often learned from our parents, that we���re now trying to unlearn.

Fighting our instincts and breaking these bad habits is tough. We could try summoning the necessary willpower. But that can be mentally exhausting. It may even backfire, when we decide the effort just expended deserves a reward���and, the next thing we know, we���re in the drive-through at McDonald���s.

Similarly, knowledge isn���t power. We all know we should exercise regularly, eat more fruits and vegetables, and save 10% to 15% of income. But knowing better doesn���t mean we���ll behave better.

So how do we change our habits and keep our worst instincts at bay? Consider three steps.

First, know yourself. What causes you to spend too much, eat too much or drink excessively? Do these things tend to happen at a particular time of day, or when you���re with certain people, or when you���re at certain places, or if you���ve had a taxing day?

For instance, you might eat too much or eat unhealthily when you go to certain restaurants or if you���ve had a rough time at work. You might drink too much when you���re with certain friends or on Friday evenings. You might shop to feel better if you���re despondent. You might trade more when you have CNBC turned on.

Psychologists have identified five key personality traits: agreeableness, conscientiousness, extraversion, neuroticism and openness. Those who display a strong conscientious streak tend to have good financial and other habits. By contrast, those given to neuroticism���the tendency to respond negatively to events���often have a harder time maintaining good habits. If you���re in the latter camp, you���ll likely find it especially difficult to avoid, say, going on a shopping spree after you���ve had a tough day.

“Anything that slows us down can potentially nix bad behavior, because straying from the straight and narrow might seem like too much effort.”

What to do? That brings us to step No. 2: Make it harder to engage in damaging behavior. Get the potato chips out of the house. Have your regular savings automatically deducted from your paycheck and bank account. Limit the number of times you go to the shopping mall each month. Don���t bookmark retail websites on your computer. Delete food delivery apps from your phone. Use a debit card rather than a credit card, so the money comes straight out of your checking account. Alternatively, spend cash only.

Anything that slows us down can potentially nix bad behavior, because straying from the straight and narrow might seem like too much effort. In addition, it gives time for the contemplative side of our brain to wrestle with the instinctual side, and we might decide we don���t really need another pair of shoes.

It���s also harder to stray if we���ve told others about the changes we���re trying to make. Want to lose 10 pounds or go to the gym three times a week? You might find an ���accountability partner������a friend or family member to whom you confide your goals. In addition, you might look for somebody���perhaps the same person���who also wants to lose weight or exercise more, so you have a companion on your self-improvement journey.

Even as you make it harder to engage in bad behavior, you might make it easier to behave well, by using a strategy called ���habit stacking.��� Find something you do regularly, and then add on or incorporate the desired good behavior. Do you leave the office every lunchtime to buy a sandwich? Find a place that���s 10 minutes��� walk farther away, so you get some exercise at the same time.

With any luck, by making it harder to stray and knowing what���s likely to trigger bad behavior, you can steer yourself onto the right track. Step No. 3: Keep this good behavior going until it becomes second nature.

Have you heard that it takes 21 days to change your habits? Unfortunately, that notion���which has gained widespread currency and is often asserted as fact���is, in truth, just a distorted account of one doctor���s observation. A subsequent academic study found that forming new habits can take anywhere from 18 to 254 days.

The key is to find some way to keep ourselves on the right track for that long. A key ingredient: positive feedback. When our friends tell us that we look like we���re in great shape or they notice we���ve lost weight, we���re encouraged to continue exercising and losing additional pounds.

Similarly, signs of financial progress can encourage us to keep going. I wouldn���t focus on your portfolio���s value, because a bad market could leave you discouraged and perhaps even unnerved. Instead, I���d focus on the dollar amount you save and see if you can increase that sum each month. Similarly, you might track your monthly credit card bills and strive to charge less than the month before.

If you have a mortgage, you might also add a little to your monthly loan payment, and then watch as both the loan balance and the amount of interest you pay go down. I used to love watching my mortgage balance shrink each month���and that encouraged me to make even larger extra-principal payments.

Follow Jonathan on Twitter��

@ClementsMoney

��and on

Facebook

.��His most recent articles include Bullheaded,��Count the Cash��and��Signal Failure

. Jonathan’s

��latest books:��From Here to��Financial��Happiness��and How to Think About Money.

Follow Jonathan on Twitter��

@ClementsMoney

��and on

Facebook

.��His most recent articles include Bullheaded,��Count the Cash��and��Signal Failure

. Jonathan’s

��latest books:��From Here to��Financial��Happiness��and How to Think About Money.

HumbleDollar makes money in four ways: We accept��donations,��run advertisements served up by Google AdSense, sell merchandise and participate in��Amazon‘s Associates Program, an affiliate marketing program. If you click on this site’s Amazon links and purchase books or other items, you don’t pay anything extra, but we make a little money.

The post Breaking Bad appeared first on HumbleDollar.

November 29, 2019

Gifts With a Twist

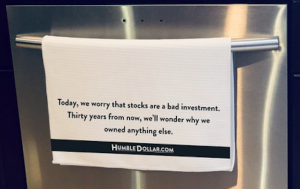

WANT TO GIVE yourself or a friend the gift of financial wisdom? Check out our new line of dish towels. Yes, you read that right: We’re talking dish towels.

Every time you dry your pots and pans with HumbleDollar’s high-quality, microfiber dish towels, you’ll be reminded of what it takes to succeed financially. They offer the daily affirmation we all need���and they make a great gift for family and friends. Each dish towel costs $15, plus $4.99 for shipping. A portion of the proceeds helps cover HumbleDollar’s costs.

Just click on the links below and you’ll be taken to Amazon, where you can purchase the dish towels. There are five to choose from, each with a different financial message:

Just click on the links below and you’ll be taken to Amazon, where you can purchase the dish towels. There are five to choose from, each with a different financial message:

The goal isn’t to beat the market, prove how clever we are or grow absurdly rich. Rather, the goal is to have enough to lead the life we want.

If we try to keep up with the Joneses, we’ll fall ever further behind our unpretentious neighbors with the seven-figure portfolio.

Today, we worry that stocks are a bad investment. Thirty years from now, we’ll wonder why we owned anything��else.

It’s almost impossible to get rich overnight, but��surprisingly easy to get rich over time.

If we spend our days doing what we love and our evenings with those we love, we have a rich life���even if we aren���t rich.

And, if you’re really a mood to give friends and family members a financial nudge this holiday season, don’t forget about my books: The two most recent are From Here to Financial Happiness and How to Think About Money.

HumbleDollar makes money in four ways: We accept��donations,��run advertisements served up by Google AdSense, sell merchandise and participate in��Amazon‘s Associates Program, an affiliate marketing program. If you click on this site’s Amazon links and purchase books or other items, you don’t pay anything extra, but we make a little money.

The post Gifts With a Twist appeared first on HumbleDollar.

Food for Thought

FULL DISCLOSURE: I wrote this out of frustration, bordering on desperation.

More than a year ago, I bought a condo and took out what was supposed to be a short-term mortgage, which we���d pay off once we sold our home of 45 years. Silly me. You guessed it: I still have the mortgage and I still own the old house, with not even a single offer received. The No. 1 reason for buyers��� lack of interest: The kitchen is too small. Nobody gets past the kitchen.

My house has one other drawback: There���s no toilet on the first floor. You would think a society obsessed with working out could walk up a flight of stairs once in a while. Over 70 million Americans have a fitness center membership. I need just one who wants to live in New Jersey.

Clearly, by today���s standards, our kitchen is indeed small. On the other hand, it was large enough for a family of six, for cooking three meals a day and for preparing 135 Thanksgiving, Christmas and Easter dinners. Here���s the kicker: More than 50 years ago, someone expanded the kitchen by four feet from its original 1929 size.

No doubt the necessities of the 21st century require a great deal of counter space. Without that space, where would we put our mini-waffle maker, panini maker, programmable pressure cooker, rice cooker, air fryer and bread maker?

Our kitchen has a small eating area and is next to a formal dining room, which is separated by an actual wall. When we bought the house, there was a swinging door, which we removed as our only concession to the open plan concept. I think there���s something to be said for having a place to eat and nothing else. Here���s a datapoint that shocked even me: ���60 years ago, the average dinnertime was 90 minutes. Today it is less than 12 minutes.��� Perhaps eating in a wide-open space that encompasses kitchen, dining area and family room has something to do with that.

With all the space we demand for our kitchens, you would think they receive heavy use. Not so much. Only 36% of Americans cook and eat at home daily. Others don���t cook but eat at home���probably on the couch.

It���s not only large kitchens that we demand. New homes were an average 1,048 square feet in 1920, 1,177 square feet in 1940, 1,500 square feet in 1970 and 2,657 square feet in 2014. Even as��we demand more space, the number of people in the space has declined. Now I better understand the plaintive cry, ���I need my space.��� Average family size was 3.76 people in 1940, 3.58 in 1970 and 3.14 in 2018.

More and bigger is an American thing. But those big houses with large kitchens cost more to buy and to maintain. Property taxes, insurance, utility bills and general maintenance of home and property are all proportional to the size of a house, not to mention the mortgage payment. My woefully inadequate house carries a tax bill of $14,500, while a newer house across the street tops $20,000.

Have Americans opted for that professional kitchen and 2,600-square-foot house and, in the process, traded away their ability to save for retirement? We used to call that house poor. But that was in the olden days, when we used to sit around the dining room table and talk about such things.

Richard Quinn blogs at QuinnsCommentary.com. Before retiring in 2010, Dick was a compensation and benefits executive. His previous articles include Fashion Statement,��You’re on Your ��Own��and��What’s Your Plan.��Follow Dick on Twitter��@QuinnsComments.

Richard Quinn blogs at QuinnsCommentary.com. Before retiring in 2010, Dick was a compensation and benefits executive. His previous articles include Fashion Statement,��You’re on Your ��Own��and��What’s Your Plan.��Follow Dick on Twitter��@QuinnsComments.

Do you enjoy��reading articles by Dick and HumbleDollar’s other writers? Please support our work with a��donation.

The post Food for Thought appeared first on HumbleDollar.

November 28, 2019

Athos���s Retirees

TUCKED AWAY on Greece���s rugged north Aegean coast lies a place seemingly frozen in time, where men lead simple lives, much the same as they have for the past 1,000 years. It���s a rocky, narrow peninsula covered in wooded valleys and terraced farms that comes to an abrupt end at a dramatic 6,000-foot peak���Mount Athos.

Here, the men live in strict, self-enforced isolation. No women have set foot on the peninsula for more than 1,000 years and even female animals are removed upon their discovery. Nonresident males must apply for a permit before boarding a ferry to the peninsula. Mount Athos���or��Agion Oros in Greek, which translates as ���holy mountain������is the exclusive domain of 20 Orthodox monasteries and their resident monks, as well as a smattering of hermits and wandering ascetics, all of whom have retired from the world.

In a sense, Mount Athos is the world���s most ancient retirement community. The oldest monastery there, Megistri Lavra, was founded more than 1,000 years ago, in 963, though archeological remains suggest there were monastic communities on the peninsula even earlier.

Those who choose to retire to Mount Athos may do so at any age. They settle in a monastery or perhaps one of the smaller monastic communities known as��skiti��or��kell��. There, they live out the remainder of their days free of charge, with three square meals a day (except during fasts), a bed and a roof over their head. The accommodation is stunning. Perched high on rocky cliffs or forested hills, Athos���s monasteries offer unparalleled views over the north Aegean, the sort beachgoers pay hundreds of euros for elsewhere along the coast.

Despite the scenery and free accommodation, a monk���s life is not one of leisure. To become a monk, you must first find a monk within one of the monasteries to take responsibility for your spiritual health. Once a spiritual father has accepted this responsibility, the ���novitiate��� must pass through a rigorous catechism, or Orthodox education, to ensure his beliefs and practices are proper and well informed. Then the novitiate will begin a trial period during which he���s generally stuck with the worst jobs, such as cleaning the bathrooms. When the novitiate has proven himself and been accepted by the monastery authorities, he can be tonsured as a monk. Even then, all monks must work to earn their keep. Some work in the gardens, others cook and clean, while still others work in an entirely spiritual capacity, spending their days in prayer.

Some monks take up special vocations, involving a skilled craft. Father Dorian, an English-born monk, is a bookbinder at one of the monasteries. He works in a well-equipped and surprisingly modern studio, which has a spectacular view over the monastery���s terraced gardens to the sea. He spends his days repairing old books sent to him from around the peninsula, as well as assembling new books written by the monastery���s holy fathers. Before becoming an Athonite monk, Father Dorian knew nothing about bookbinding. He learned from his own mentor and is now in the process of passing his knowledge on to a novitiate, a Spanish convert from Buddhism.

In another monastery, an English convert-turned-monk named Father Makarios is an iconographer. He paints highly stylized portraits of the Virgin Mary, Jesus and the saints. Though he may have painted before becoming a monk, Father Makarios had to learn the intricacies of depicting his subject matter within the particular framework of Orthodox religious art.

It may seem at first glance that the ���retirees��� of Mount Athos don���t have much in common with those of us who retire without renouncing the world. But I���d argue they offer some valuable lessons to the rest of us:

Live modestly. Athonite monks give up all their worldly possessions and live communally. While we don���t have to follow such a strict example, it���s wise to downsize, live comfortably within our means and appreciate the simple things.

Find a hobby or pick up a new skill. No, it doesn���t have to be bookbinding or orthodox iconography. But refining a skill or engaging in a new hobby is a great way to spend time and enrich yourself in retirement.

Come to terms with mortality. Yes, this one���s a bit morbid, but the monks of Athos spend a great deal of their time preparing spiritually for their own departure from this world and, as such, set a good example for those of us left behind. Retirement is as good a time as any to reflect on life and nurture a full appreciation for it, with all its chaos and harmony, peace and pandemonium, as we gradually move from a state of being toward one without.

Peter Minnium Jr.

graduated from Pitzer College in 2015 with a degree in history and has been completing his education ever since. After a stint as an English language professor at Universidad de la Sierra Ju��rez in Oaxaca, Mexico, he has been pursuing his passion for underexplored cultures and languages on a $15-a-day budget���so far in Mexico, Central America, Greece, Indonesia, Nepal and lately India. His parents hope he runs out of money soon and pursues a less itinerant lifestyle

. A version of this article first appeared on Concierge Financial Planning���s

website

.

Peter Minnium Jr.

graduated from Pitzer College in 2015 with a degree in history and has been completing his education ever since. After a stint as an English language professor at Universidad de la Sierra Ju��rez in Oaxaca, Mexico, he has been pursuing his passion for underexplored cultures and languages on a $15-a-day budget���so far in Mexico, Central America, Greece, Indonesia, Nepal and lately India. His parents hope he runs out of money soon and pursues a less itinerant lifestyle

. A version of this article first appeared on Concierge Financial Planning���s

website

.

The post Athos���s Retirees appeared first on HumbleDollar.

November 27, 2019

Missing the Target

USE THE RIGHT tool for the job and you���ll get the best result. If you need to connect two boards, you could use a hammer and a nail or a screwdriver and a screw. Either methods work���and they���re certainly better than banging in a screw with a hammer, which I���ve seen tried. It was not effective.

Participants in 401(k) plans, alas, display similar behavior with target date funds, or TDFs. A TDF offers a diversified portfolio in a single fund, with the mix of stocks and bonds changing as you approach retirement. When used correctly, the fund���s asset allocation should be appropriate for your age���aggressive while you���re young and becoming more conservative as you age. There���s no need to trade or adjust the mix. The fund does that automatically. The evidence, however, suggests many people use TDFs incorrectly.

Vanguard Group found that 52% of 401(k) participants have invested in a TDF, making the funds a popular choice for retirement money. But it seems many folks don���t stop at one fund. Morningstar studied TDF users and found many also invest in other funds���sometimes another TDF and sometimes other funds offered in their 401(k) plan. Result: These additional funds change the retirement saver���s asset allocation, so it may no longer make sense, given the employee���s expected retirement date.

Indeed, as a plan administrator, I���ve seen participants hold as many as 12 TDFs. Some participants have told me their financial planner recommended buying multiple TDFs. What can I say? It sounds like another case of using a hammer with a screw.

But what if you don���t like the risk profile of a particular TDF? Morningstar recommends you choose a single fund with a target date closer to today if you want a more conservative portfolio or, alternatively, a date further away if you want something more aggressive. In other words, you don���t need to own more than one fund to adjust your risk.

Check with your 401(k) plan���s administrator to find out how the plan uses TDFs. Many plans automatically enroll you in an appropriate TDF when you become eligible to contribute, unless you choose an alternative. Some plans may, by default, also deposit company contributions in a TDF. Don���t want to own the default TDF? You can probably change the fund selection with a few clicks of your mouse.

Mark Eckman is a data-oriented CPA with a focus on employee benefit plans. His previous articles were Alphabet Soup,��Financial Pilates and��Giving Voice. As Mark approaches retirement, he’s realizing that saving and investing were just the start���and maybe the easy part. His priorities: family, food and fun.��Follow Mark on Twitter��@Mark236CPA.

Mark Eckman is a data-oriented CPA with a focus on employee benefit plans. His previous articles were Alphabet Soup,��Financial Pilates and��Giving Voice. As Mark approaches retirement, he’s realizing that saving and investing were just the start���and maybe the easy part. His priorities: family, food and fun.��Follow Mark on Twitter��@Mark236CPA.

HumbleDollar makes money in four ways: We accept��donations,��run advertisements served up by Google AdSense, sell merchandise and participate in��Amazon‘s Associates Program, an affiliate marketing program. If you click on this site’s Amazon links and purchase books or other items, you don’t pay anything extra, but we make a little money.

The post Missing the Target appeared first on HumbleDollar.

November 26, 2019

Oldies but Goodies

BAD INVESTMENT and personal finance books get cranked out every year with catchy titles and celebrity authors. But skip such pulp fiction. Instead, give yourself or someone you know the gift of timeless investment wisdom with one���or all���of the following classics.��

Why? Perhaps you���ve heard that indexing is the way to go. Or that you should insist on low-cost funds. Or that stocks are the best asset class, and should be bought and held. But you���re not quite convinced or you hold these truths lightly.

Three of the books recommended below provide the rock-solid intellectual underpinnings for all these propositions and more. They are among the founding documents of modern investing. Other investment classics, such as Ben Graham���s��The Intelligent Investor��and Peter Lynch���s��One Up on Wall Street,��fade in significance, because virtually no one can consistently beat the market through security selection.��

As a bonus, I���ve thrown in a fourth book���a delight for the intellectually curious, showing how we got here from ancient Greek games of dice to behavioral finance. Read or gift these books. Hardcover, paperback or digital, it doesn���t matter: Their truths are etched in stone, yet the words jump lightly off the page. That said, I don���t recommend the audio versions, as you���ll want to see the accompanying charts.

A Random Walk Down Wall Street ��by Burton Malkiel. (First edition: 1973.��Updated: 2019.)

By now, you know that actively managed funds as a group will trail the market averages. Burt Malkiel, an economist who would go on to high positions at Yale and Princeton, demonstrated that was true decades before it caught on���and two years before Vanguard Group founder Jack Bogle started the first index mutual fund.

Despite the title, Malkiel doesn���t argue that the movement of stock prices is completely random. After all, there is an upward bias from earnings and dividend growth. Rather, he proves that you can���t consistently beat the market with knowledge of past price movements (technical analysis) or publicly available information (fundamental analysis).

Malkiel���chief investment officer at robo-advisory firm Wealthfront���also argues that any strategy that does boost returns will cease working once enough investors try to follow it. Solution: Mimicking the market averages.

Stocks for the Long R un ��by Jeremy Siegel. (First edition: 1994. Updated: 2014.)

Not everyone accepts that stocks are the essential investment for building wealth or realizes that the risks of owning them shrink over long holding periods. Jeremy Siegel wrote the book that proves it.

Siegel, a professor at the University of Pennsylvania���s Wharton School, tracked U.S. share prices back to 1802 and showed not only that stocks leave bonds, gold and cash in the dust, but also they���ve appreciated at a remarkably consistent rate through three major time periods. Despite wars, depressions and traumatic transitions from rural to industrial to a post-industrial economy, stocks as a group returned about 6.5% a year after inflation in 1802-1870, 1871-1925 and 1926-2012.

Going further, he demonstrates that the safest long-term investment is a diversified portfolio of stocks. Over 20-year-plus holding periods, stocks have ���both a higher return and lower after-inflation risk than bonds.���

Siegel advises investors to keep most of their assets in index mutual funds and exchange-traded index funds (ETFs), in a mix of capitalization-weighted funds and those with a value orientation. Siegel is an advisor to WisdomTree, a provider of smart-beta ETFs, many with a value tilt.

Common Sense on Mutual Funds ��by John Bogle. (First edition: 1999. Updated: 2009.)

In addition to creating the first index fund at year-end 1975���much ridiculed then and for many years afterward���the late Jack Bogle long preached the gospel of low investment costs, and he lived to get the last laugh.��

You see index mutual fund expenses plunging to zero in some cases? Thank Jack Bogle for starting the trend (though it was his archrival Fidelity Investments that introduced the first zero-cost index funds last year). Bogle was not a fan of ETFs, saying they would encourage too much trading, but he deserves credit for the low-cost indexing boom they embody.

In��Common Sense, he skewers the for-profit mutual fund industry for its sales loads, high expense ratios, hidden fees and marketing tactics. He also demonstrates the futility of active management and enumerates how costs are a major predictor of results.��

In fact, costs and asset allocation are by far the biggest drivers of investment returns. Forget about technical analysis, market timing or paying up for today���s star stock pickers. Stellar short-term performance almost certainly will revert to the mean���that is, toward the market averages and usually lower still, once fund expenses and portfolio turnover costs are factored in.

Against the Gods: The Remarkable Story of Risk ��by Peter Bernstein. (Published: 1996.)

Where did Malkiel get the statistical framework to demonstrate that short-term stock price movements are unpredictable, or Siegel to analyze the standard deviation of long-term investment results, or Bogle the notion of reversion to the mean?

The late Peter Bernstein���s brightly written historical tour de force lays it all out, starting with the ancient Greeks, who would throw marked bones, thinking that the results they revealed were determined by fate. Eventually, gambling men joined with Renaissance mathematicians in getting a handle on probability, with great implications for the development of insurance. That, in turn, enabled greater human risk-taking and larger endeavors.

Other central figures, such as Charles Darwin���s cousin, Sir Francis Galton, measured everything from people to sweet peas to discover reversion to the mean.��All this statistical progress led to Modern Portfolio Theory, the mathematical demonstration of why you shouldn���t put all your eggs in one basket. But it also led to behavioral finance, which grapples with why humans make irrational choices when rational solutions are evident. It���s a fascinating tale.

William Ehart is a journalist in the Washington, D.C., area. Bill’s previous articles for HumbleDollar include Mild Salsa, Weight Problem��and Not My Guru. In his spare time, he enjoys writing for beginning and intermediate investors on why they should invest and how simple it can be, despite all the financial noise. Follow Bill on Twitter @BillEhart.

William Ehart is a journalist in the Washington, D.C., area. Bill’s previous articles for HumbleDollar include Mild Salsa, Weight Problem��and Not My Guru. In his spare time, he enjoys writing for beginning and intermediate investors on why they should invest and how simple it can be, despite all the financial noise. Follow Bill on Twitter @BillEhart.

HumbleDollar makes money in four ways: We accept��donations,��run advertisements served up by Google AdSense, sell merchandise and participate in��Amazon‘s Associates Program, an affiliate marketing program. If you click on this site’s Amazon links and purchase books or other items, you don’t pay anything extra, but we make a little money.

The post Oldies but Goodies appeared first on HumbleDollar.

November 25, 2019

Don’t Get an F

MEDICAL EXPENSES are a big worry for retirees���leading many to purchase supplemental insurance. But you need to think carefully about which Medigap policy you buy.

What does this insurance get you? Medicare Part B, which covers doctor���s visits and other outpatient care, typically only pays 80% of the expenses that retirees incur. To plug this and other coverage gaps, many folks buy a Medigap insurance plan. Want to keep your current doctors and not be restricted to the network of medical professionals offered in a Medicare Advantage plan, otherwise known as Medicare Part C? You���ll want to stick with Medicare Part B and supplement it with a Medigap insurance plan sold by a private insurer.

After signing up for Medicare Part B, most people have just six months during which they���re ���guaranteed issue��� for Medigap. ���Guaranteed issue��� means there���s no medical underwriting when choosing a Medigap plan. After those six months, you could be denied for health reasons. One potential pitfall: If you opt for a Part C Medicare Advantage plan when you���re first eligible for Medicare, you may forever be locked out of the Medigap market if you later want to switch out of Medicare Advantage. The reason: Your health may have deteriorated and you can���t pass the medical underwriting.

How do you decide which Medigap plan is best for you? There are 10 different varieties of Medigap plan. In 2018, Medigap Plan F was chosen by 54% of all enrollees. While Medigap plans are standardized in terms of the coverage they provide, costs can vary significantly. Even though Plan F is the most popular, Plan G is the fastest growing���for good reason. Plan G is less expensive than Plan F. The only difference between the two is that Plan F pays the Part B deductible of $185, whereas Plan G doesn���t���and yet, for that convenience, Plan F typically charges more than $185 extra.

In 2020, Medigap Plan F will no longer be offered to new Medicare enrollees. Result? Plan G is where most future enrollees will be going in 2020 and beyond���assuming they want comprehensive coverage. Those currently enrolled in Plan F might not be able to change to Plan G, because they���ll be subject to medical underwriting.

But if you can pass the medical underwriting, consider switching. Why? The premiums for Plan F will likely start rising relative to Plan G���for three reasons.

First, current Plan G enrollees are, on average, healthier. One indication: They���re less worried about the Part B deductible, because they don���t think they���ll have enough medical expenses to pay it in full. Second, since Plan F won���t get new enrollees in 2020 and beyond, the ���book of business��� will be aging and will likely be in worse health. Indeed, in 10 years, the youngest participant in Plan F will be 75 years old. Third, as premiums continue to rise for Plan F, those healthy enough to pass the medical underwriting will switch to Plan G, further exacerbating the health disparity between the two groups.

What if you���re among those last few enrollees in 2019 who can choose Plan F? I can���t think of any reason to pick it over Plan G. Hoping to switch from F to G? It���s important to call an independent broker, who represents multiple insurance companies, including those offering both Medical Advantage plans and Medigap policies. Before you drop your current policy, make absolutely sure you can get on a new plan���and do so at a reasonable cost.

James McGlynn CFA, RICP, is chief executive of Next Quarter Century LLC��in Fort Worth, Texas, a firm focused on helping clients make smarter decisions about long-term-care insurance, Social Security and other retirement planning issues. He was a mutual fund manager for 30 years. James is the author of��Retirement Planning Tips for Baby Boomers. His previous articles include Late Fee,��Where to Begin��and��As the Years Go By.

James McGlynn CFA, RICP, is chief executive of Next Quarter Century LLC��in Fort Worth, Texas, a firm focused on helping clients make smarter decisions about long-term-care insurance, Social Security and other retirement planning issues. He was a mutual fund manager for 30 years. James is the author of��Retirement Planning Tips for Baby Boomers. His previous articles include Late Fee,��Where to Begin��and��As the Years Go By.

HumbleDollar makes money in four ways: We accept��donations,��run advertisements served up by Google AdSense, sell merchandise and participate in��Amazon‘s Associates Program, an affiliate marketing program. If you click on this site’s Amazon links and purchase books or other items, you don’t pay anything extra, but we make a little money.

The post Don’t Get an F appeared first on HumbleDollar.

November 24, 2019

The Unwanted Payday

IT’S LATE NOVEMBER. Is there anything you can still do to trim your 2019 tax bill? There might be. One overlooked aspect of mutual funds is how they can significantly���though quietly���impact shareholders��� tax returns.

By way of background, mutual funds���including exchange-traded funds (ETFs)���are required to pay out to shareholders, on a pro-rata basis, all of the income that they generate each year. This includes interest paid by bonds, dividends paid by stocks and capital gains created when a fund sells an investment at a profit.

Suppose you���re a fund shareholder���and suppose the fund bought a share of Apple stock on Jan. 1, held it for 10 months, and then sold it at the end of October. How much income would this investment have generated for the fund and therefore how much would it be required to pay out to you, as a shareholder?

During those 10 months, Apple paid dividends of $3.04 per share. Meanwhile, between the purchase and the sale, Apple���s share price increased from $157.92 to $248.76, for a profit of $90.84. As a result, the fund’s total income from this investment was:

Dividends: $3.04

Capital gains: $90.84

Total: $93.88

By law, this fund would be required to pay out that $93.88 to its shareholders by the end of this year, along with the net gains from all of its other investments, minus the fund���s operating expenses.

This may seem discouraging: Your tax bill is in the hands of your fund manager, who���s permitted to buy and sell freely, generating tax headaches for you. But there are three important facts to know, so you can take back control of this situation:

1. Some funds are far more tax-efficient than others. Broadly diversified index funds have many well-known advantages, including��strong performance. But a lesser-known advantage is that they are, almost universally, more tax-efficient than their actively managed peers.

Why? Index funds, for the most part, employ a buy-and-hold strategy. They don���t see the same sort of trading activity as funds run by stock-pickers. This translates into fewer capital gains and thus smaller tax bills for you, the shareholder. This is yet another reason to favor simple index funds like S&P 500 funds and total U.S. stock market funds.

According to��an analysis��by the research firm Morningstar, this effect has been amplified in recent years. As investors have moved billions out of actively managed funds and into index funds, it���s put selling pressure on many actively managed funds. To pay the money owed to departing shareholders, these fund managers have been forced to sell some of their holdings, triggering gains. With the market at new highs, and actively managed funds losing popularity, I expect this trend to continue.

True, the tax bills generated by actively managed funds are often modest. Problem is, they���re also entirely unpredictable. In that same analysis by Morningstar, the firm relates how one well-regarded fund���the Sequoia Fund���ran into trouble. The fund manager had become enamored of a company called Valeant Pharmaceuticals, to the point where it accounted for nearly 30% of the fund���s assets. Unfortunately, Valeant got caught up in a series of scandals, destroying the stock���s value. Investors fled. That forced the fund manager to begin selling the fund���s other investments. In the end, the Sequoia Fund has lost nearly half its value since 2015. To add insult to injury, it has left shareholders with massive tax bills. This is an extreme example. Still, it illustrates why investing in an actively managed fund is like handing a blank check to your fund manager.

2. Even if you currently own an actively managed fund, you might still be able to sidestep a big part of this year���s tax bill���if you act quickly.��This time of year, many fund companies publish “distribution” estimates for each of their funds. For example, you can find Vanguard���s distribution estimates listed��here��and Fidelity���s��here. Not only will they tell you the projected size of the distributions, but also they���ll tell you the exact date on which they���ll be making those distributions (called the ���pay date���).

Don���t like what you see? The good news is, you can avoid receiving your share of a taxable distribution by simply selling the fund before the pay date. You want to make this decision carefully, to confirm that selling aligns with your overall investment plan and to be sure that it doesn���t generate other, unexpected taxes. For instance, even if you can avoid the distribution by selling, you might trigger an even larger tax bill���because you���ll owe capital-gains taxes if your fund shares are worth more today than your cost basis. The latter will consist of the money you���ve invested over the years, plus any fund distributions that you reinvested in additional fund shares.

3. The above discussion applies only to taxable accounts.��If you own a fund inside a retirement account, like an IRA or 401(k), these kinds of distributions wouldn���t affect you. Don���t like an actively managed fund that you own? In a retirement account, there���s no tax cost if you sell.

Adam M. Grossman���s previous articles��include No Comparison,��A Graceful Exit��and��Time Out

. Adam is the founder of��

Mayport Wealth Management

, a fixed-fee financial planning firm in Boston. He���s an advocate of evidence-based investing and is on a mission to lower the cost of investment advice for consumers. Follow Adam on Twitter��

@AdamMGrossman

.

HumbleDollar makes money in four ways: We accept��donations,��run advertisements served up by Google AdSense, sell merchandise and participate in��Amazon‘s Associates Program, an affiliate marketing program. If you click on this site’s Amazon links and purchase books or other items, you don’t pay anything extra, but we make a little money.

The post The Unwanted Payday appeared first on HumbleDollar.

November 23, 2019

Bullheaded

LOGIC AND DATA make it abundantly clear that we���re highly unlikely to beat the market averages���and that indexing is the best strategy for the vast majority of investors. Yet half of U.S. stock fund assets remain actively managed and, for money that isn���t in mutual funds, the percentage is likely far higher.

That brings me to today���s contention: Maybe we should spend less time making the case for indexing. Instead, perhaps we should focus on the more obvious conundrum: If beating the market is a game that we���re extraordinarily unlikely to win, why do so many folks keep trying?

Follow the money. Market-beating efforts may backfire for most investors, but they remain a huge moneymaker for Wall Street. What else can explain the hysteria and silly arguments constantly emanating from investment ���professionals���? These folks have all but given up claiming that active management is a reliable route to superior returns, which it most certainly isn���t.

Instead, they want us to believe there���s an index-fund bubble and that indexing is worse than Marxism, so we���ll pay up for active management and fatten their coffers. Let���s face it: It���s a strange contention���that it���s somehow our patriotic duty to actively manage our portfolios, even though we���re likely sacrificing our investment performance.

Unnecessary confusion. Wall Street���s arguments may be fatuous, but they help to make muddy waters even murkier. Wall Street has long sought to cloak the simple business of managing money in language that befuddles everyday Americans.

Consider a simple example. When financial experts discuss how to divide money between stocks and bonds, they���ll talk about ���your asset allocation between equities and fixed income.��� That may sound a whole lot cleverer and more mysterious, but it���s just disguising a straightforward notion with words sure to scare off the uninitiated.

Hidden costs. Some investment expenses are clearly disclosed, including a fund���s annual expenses, the brokerage commission you���ll pay to buy or sell a stock (often zero these days) and what percent of assets is charged by your fee-only financial planner.

But other costs are tough to figure out. Examples: how much you lose to the bid-ask spread every time you trade a stock, what���s the markup or markdown when you buy or sell a bond, and how much your funds are incurring in total trading costs. If investors were fully aware of these costs, it would be even clearer what a bargain indexing is.

Overconfidence. There are, of course, investors who realize how much active management costs and how unlikely they are to win the beat-the-market game, and yet they insist on playing. Why? In a word: overconfidence. Just as many folks believe they���re better-than-average drivers and smarter than most, they also believe they can outpace the market, even as most others fail.

Experience should deflate this overconfidence, but for many investors it never does���because they have no idea how their portfolio is really performing. And even if they do, they don���t compare their portfolio to an appropriate benchmark and don���t factor in the amount of risk they���re taking. To be fair, figuring all this out can be a tricky. Financial firms could help, but (surprise, surprise) they don���t: It seems Wall Street doesn���t want to provide investors with anything more than rudimentary performance information.

Reading tea leaves. Investors��� overconfidence is also fueled by a host of behavioral mistakes. We often imagine we see patterns in today���s share price movements and believe those patterns foretell what���s to come. Looking back, what occurred in the markets seems obvious���and we may even feel we predicted what happened, a mental mistake known as hindsight bias.

But perhaps the most insidious behavioral error is availability bias. Every year, most stocks underperform the stock market averages, because the averages are skewed higher by a minority of stocks with huge gains. Yet it���s those big winners that stick in our minds, and they make beating the market seem easy. What if we try our hand at finding the next hot stocks? The odds suggest we���ll end up picking duds instead���and our results will lag behind the market averages.

Tax locked. The stampede into index funds began in earnest some 15 years ago. Today, some folks would no doubt like to join the stampede but haven���t���because they���re reluctant to dump the individual stocks and actively managed funds they already own.

What explains this reluctance? Even if their currently holdings have been market laggards, these investors may be loath to sell, because unloading their current positions would trigger large capital-gains tax bills. Obviously, this isn���t an issue with investments held in a retirement account. But it���s a real dilemma with a taxable account���and hanging on to those old active bets and avoiding taxes is, alas, often the right decision.

Follow Jonathan on Twitter��

@ClementsMoney

��and on

Facebook

.��His most recent articles include Count the Cash,��Signal Failure��and��Cash Back

. Jonathan’s

��latest books:��From Here to��Financial��Happiness��and How to Think About Money.

HumbleDollar makes money in four ways: We accept��donations,��run advertisements served up by Google AdSense, sell merchandise and participate in��Amazon‘s Associates Program, an affiliate marketing program. If you click on this site’s Amazon links and purchase books or other items, you don’t pay anything extra, but we make a little money.

The post Bullheaded appeared first on HumbleDollar.