Jonathan Clements's Blog, page 252

November 17, 2021

Challenging Myself

For the record, although I recently left the��workforce��early to pursue a long-simmering passion for writing, I won���t be starting Social Security payments early. Nor���unless something changes health-wise���do I intend to begin distributions from my IRAs any time soon. Before I go down those two routes, I plan to live off my taxable-account savings and minimal dividend income for as long as I can.

In the meantime, I���m busy pulling together my ���challenge list��� of things I want to experience and achieve in the years ahead. Note that I call this a challenge list, not a bucket list���a term I find horrid. Do we really want to be counting down a list of to-do items before we kick the bucket?

Not me. I want to be stretched in the years ahead. I want to be learning new skills and plumbing unexplored parts of myself, as well as the world. I want to be doing things that demonstrate to me, and maybe to society as well, that age is but a number. People shouldn���t limit what they try just because of the year they were born.

After all, we stretched ourselves in our working careers. Why should we stop now that we���re no longer clocking in?��Research��has consistently shown that seniors who engage in stimulating activities���ones that challenge their bodies and their brains���tend to stay sharp and vital longer.

William Shatner just flew into space at age 90. My mother keeps herself mentally sharp at 89 by reading the paper every day and doing 1,000-piece jigsaw puzzles.

My own challenge list is a mix of experiences, activities and goals that will push me in new directions, physically and mentally. I���ve already started to tick some items off the list.

My own challenge list is a mix of experiences, activities and goals that will push me in new directions, physically and mentally. I���ve already started to tick some items off the list.The first challenge I set myself was a big one. On the first day of retirement, I hitched my 30-foot trailer to the back of my F-150, threw the dog in the backseat (she jumped in, actually), and set off on a month-long, cross-country adventure to Colorado.

It���s something I���d wanted to do since my middle son moved to Denver three-plus years ago to take a job after college. Since my girlfriend had to work, and none of my retired friends wanted to do something so crazy, I took the trip solo. And it was incredible.

There���s nothing like spending the whole month of September in Colorado to kickstart a new, creative phase of your life. The big skies. The rugged mountains. The broad vistas burning with the gold and reds of fall foliage. It all gives you a sense of life���s possibilities and our limitless human potential.

Will I do a cross-country RV trip solo again? Probably not. Driving home alone for 31 hours over three-and-a-half days, with a three-ton travel trailer hooked to the back, isn���t easy.

But I did it. I met the challenge and came back charged up and feeling good about myself.��I call it��repassioning. First item on the challenge list���check. What else is on my list?

I want to write books, and hope to get a few of them published. My first nonfiction book, The Long Walk Home, will be published early next year by Blydyn Square Books.

I want to publish articles and blog posts like this one. And look here���I���m doing it.

I want to sharpen my photography skills.

I want to learn Canva or another design program so I can do my own graphics and visuals for my personal blog.

I want to do a road-biking trip through the French countryside and hike in the Scottish Highlands.

I want to go fly fishing in Canada and Argentina.

I want to get into yoga.

I want to keep jogging and get as much mileage as I can on this arthritic left hip of mine before I submit to getting a new one.

And on and on. My challenge list grows every week. I���ll never get to all of them, but that���s all right. The point is not so much accomplishing all these things as setting them out there and giving them a shot.

When it comes time for me to kick the bucket, I want to make sure it���s a big bucket I���m kicking. And that it has plenty of dents from all the places we've gone together.

James Kerr led global communications, public relations and social media for a number of Fortune 500 technology firms before leaving the corporate world to pursue his passion for writing and storytelling. His book, ���The Long Walk Home: How I Lost My Job as a Corporate Remora Fish and Rediscovered My Life���s Purpose,��� is forthcoming in early 2022 from Blydyn Square Books.��Check out his blog at

PeaceableMan.com

. His previous article was Reclaiming My Life.

James Kerr led global communications, public relations and social media for a number of Fortune 500 technology firms before leaving the corporate world to pursue his passion for writing and storytelling. His book, ���The Long Walk Home: How I Lost My Job as a Corporate Remora Fish and Rediscovered My Life���s Purpose,��� is forthcoming in early 2022 from Blydyn Square Books.��Check out his blog at

PeaceableMan.com

. His previous article was Reclaiming My Life.The post Challenging Myself appeared first on HumbleDollar.

November 16, 2021

Why I Own Bonds

This isn���t a good time to sell. Bonds have already factored in the market���s expectation that rates will rise. Interest rates have climbed this year, causing a decline in bond prices. It may be too late to gain any benefit from changing my asset allocation.

There���s no better fixed-income alternative. Bonds have better yields than money market funds. Certificates of deposits have liquidity issues���there���s a penalty for early withdrawals. That penalty can mean forfeiting all the interest you���ve earned.

Today���s higher bond yields mean greater interest income.

Even if interest rates continue to rise, reinvesting my interest payments allows me to take advantage���and should boost my returns over the long term.

Having bonds in my investment portfolio is a good way to reduce volatility and risk. When stocks fell almost 16% from January through March 2020 because of the COVID-19 pandemic, bonds worldwide returned just over 1%.

I���d rather own a bond fund than buy individual bonds. I���d have to own a large number of bonds to achieve the diversification that I get with my bond funds. Also, it would take a lot of time and effort to research and manage those individual bonds.

As a retiree who depends on his investment portfolio for income, an all-stock portfolio would be too risky.

Maybe most important, thanks to my bonds, I sleep better because I���m less bothered by the ups and downs of the stock market.

The post Why I Own Bonds appeared first on HumbleDollar.

Not an Investment

IN A RECENT TWITTER post, a man claimed that if all the Social Security taxes he and his employers pay were invested instead, he���d accumulate $1.9 million by age 67. That sum could then generate $95,000 in annual income, he added, which is more than his anticipated Social Security benefit. He concluded that Social Security was ���theft.���

Claims like these bother me greatly because they���re often widely read and believed���and they���re nonsense.

Social Security is an insurance program, not an investment plan. It provides much more than retirement income to the worker alone. The Twitter commenter���s claim is like me saying that the $196,124 I paid in Medicare taxes was theft because I haven���t collected that much in health care benefits. I hope I never do.

Of the 65 million Americans collecting Social Security, only 47 million are retired workers. The rest are spouses, ex-spouses, survivors and children of contributing workers, plus disabled individuals.

Looking at my own Social Security records, my wife and I have received in benefits every penny paid in taxes���both by me and my employers. In fact, we got it all back within the first seven years. Since then, we���ve collected $200,000 more.

Someone less fortunate may collect for a short period or not at all. That���s why Social Security is insurance that, in some respects, acts like a pension. For each individual, the goal is to be an actuarial loss���but, no, not everybody can live longer than average.

Social Security benefits are based on your earnings and the program���s benefit formula, not on the payroll taxes paid. Many individuals collect benefits without ever paying a penny in taxes, either directly or by an employer on their behalf.

The investment gurus are going to run the numbers and easily prove the $1.9 million claim, or something like that, is accurate. Yup���if everything works out perfectly from day one. Namely, that the individual has the discipline to save every equivalent penny. That the money is invested wisely. And that he or she doesn���t suffer any major vicissitudes of life, as President Franklin Roosevelt called them. If all these conditions are met, sure, then they���re correct.

Call me cynical, but not many Americans have demonstrated that sort of discipline for long-term saving and investing. That may be why there are always calls for higher Social Security benefits and larger cost-of-living adjustments.

The Social Security trust fund is often misrepresented. The U.S. government has almost $29 trillion of outstanding��debt. Of that, $6 trillion is held by intragovernmental trusts, including some $3 trillion in Social Security reserves. Those trusts are effectively accounting items within government agencies.

The Treasury does issue special bonds to the Social Security trust fund. It also credits those bonds with interest���$76 billion in 2020. In addition, the trust receives income from the taxation of Social Security benefits���$41 billion more. Social Security will redeem those bonds when the income from payroll taxes is inadequate to fully meet its obligations. Where will the government get the cash? Probably with more debt, charged to another account.

Some people are convinced Congress stole the trust money. They say the trust would have plenty of money if it hadn���t. That���s simply not true.

Your payroll taxes, on average, pay for only about 15% of your��total benefits. That���s why it was decided that a maximum 85% of our Social Security benefits would be taxed.

Representing Social Security as theft, a rip-off or a Ponzi scheme is reprehensible, in my opinion. That���s like saying term life insurance is a rip-off if you don���t die within the insured period.

No, the real failure is that Congress has ignored for decades the need to shore up Social Security���s finances. Adjustments are necessary as demographics and other factors change. These could have been gradual and relatively minor���if the costs had been spread over generations of workers. Now, we���re in a bind.

Current and future workers must carry the burden of balancing the books. Either that or Social Security must receive an influx of cash from general tax revenue. That would change forever the very idea of a worker-funded insurance program. It would place Social Security among the many programs competing for their share of the federal budget���something Roosevelt greatly feared.

Richard Quinn blogs at QuinnsCommentary.net. Before retiring in 2010, Dick was a compensation and benefits executive.��Follow him on Twitter��@QuinnsComments��and check out his earlier��articles.

Richard Quinn blogs at QuinnsCommentary.net. Before retiring in 2010, Dick was a compensation and benefits executive.��Follow him on Twitter��@QuinnsComments��and check out his earlier��articles.

The post Not an Investment appeared first on HumbleDollar.

November 15, 2021

Trust Betrayed

But it���s one thing to know this theoretically���and quite another to find out it���s happening in your own family.

I previously wrote about now both my late father and his close friend were victims of financial abuse. After we discovered what was happening, I thought my three siblings and I had straightened out the family finances.

My youngest brother and I live in the U.S., while my parents were in Thailand. We all agreed that my two middle brothers, who live in Bangkok, should be co-guardians of my parents and their finances. My father was dying of Parkinson���s and my mother was deteriorating mentally and physically, so it made sense to let my brothers have complete control.

We split my parents��� money, enough to last the rest of their lives, between my two brothers in 2019. We had regular Zoom calls to discuss my parents��� physical condition and financial situation. One of my brothers sent us an accounting every quarter, while the other didn���t. When, in early 2020, we finally confronted the brother who hadn���t provided any sort of accounting, he admitted that the money he oversaw was gone.

We consulted an attorney and were advised that we could go to the police to have him arrested. In the end, we decided against it for my mom���s sake. It would have devastated her. My other brother still has the other half of my parents��� money in his care, which should be enough for my mom, now that my father has passed.

Losing my father was hard. I still miss him every day. But we knew it was coming and mentally we could prepare. Losing trust in my brother was in some ways harder. While we can���t recover the money, we have the comfort of knowing that Mom is still okay financially. Many seniors aren���t so fortunate.

The post Trust Betrayed appeared first on HumbleDollar.

All in the Execution

My suggestion to my friend: Have another conversation with your dad���and ask these four questions:

What are your expectations? Someone who creates a will is known as a testator. The primary role of an executor is to settle the testator���s estate. The executor must arrange to pay outstanding debts and taxes. What remains must end up in the hands of those stipulated in the will. But how will all this get done? Some people may wish their executor to perform specific duties in a particular manner, using certain professionals and advisors. Others may not care how their executor carries out the responsibilities. After all, it���s no longer their problem.

Can I have a copy of the will? After you agree to be an executor, get a copy of the will. Reviewing the document will give you a better understanding of what���ll be involved. Should the beneficiaries or the distribution of assets differ from what you imagined, it���s better to discover that before the testator dies. This will give you time to discuss unusual circumstances or requests. That will lessen the odds that you���ll be frustrated or that any beneficiary will end up with hurt feelings.

Can I have a list of assets? It���s the responsibility of the executor to locate all the estate���s assets. On that score, unless the testator is very organized, you���ll have questions. Better to get those questions answered while the testator is around to help. What if you wait too long? You could find yourself rummaging through financial statements and legal documents in filing cabinets, monitoring the mail as it slowly arrives, or perhaps paying an accountant or lawyer to gather the information.

What sort of funeral do you want? This is a hard question to ask. But the fact is, preferences about funeral arrangements vary. One person may request a quiet graveside remembrance, while another may want an elaborate celebration of life. Discuss these wishes with the testator. I recall the strange look I gave my mom when she told me that she���d recently purchased a burial plot. But when my mom passed away, I realized the gift she gave our family by taking away that decision.

Also ask the testator if he or she intends to donate any organs and tissues. There���s no age limit for such donations. People in their 70s and older have donated and received organs successfully.

The post All in the Execution appeared first on HumbleDollar.

Six Principles

This is a daunting challenge���with high stakes. These decisions determine how much folks will have when they retire. How can you make the most of these plans? There���s plenty of good advice available on how to pick the right investments. But if I was going to strip it down to the essentials, I���d offer these six guiding principles:

1. Don���t chase performance. This is probably the most common mistake investors make. Too often, they choose funds based solely on past performance. Such rearview mirror investing often disappoints, as the best-performing funds in one period are rarely the best performing in the next. This behavior is especially dangerous during market bubbles, such as the technology stock bubble of the late 1990s, which burst in early 2000, hurting many investors.

2. Beware company stock. If your employer���s stock is one of the investment options, it should comprise no more than 10% of your total 401(k) allocation. This is because a single stock is far riskier than a diversified mutual fund. For employees, holding company stock is worth an average 42% less than its stated value, once you adjust for the much higher risk involved, according to estimates by economist Lisa Meulbroek.

By owning shares of the company where you work, both your livelihood and your retirement savings will be at risk should your company go bust. Never forget the lessons of Enron and Lehman Brothers.

3. Gravitate toward target-date funds. If your 401(k) offers target-date funds���also called lifecycle or age-based funds���they���re a great option. A target-date fund pools together multiple funds���including stock, bond and money market funds���in a risk-appropriate manner. Financial professionals determine the fund���s investment mix based on the retirement year that the fund is targeting.

There are many other attractive features of target-date funds. Asset allocation automatically adjusts as you age, becoming more conservative over time. The funds are also rebalanced automatically. Finally, this is a great way to simplify a portfolio. You can literally have your entire 401(k) invested in a single target-date fund and be well diversified. In short, target-date funds are the perfect choice for those who want to ���set it and forget it.���

4. Beware na��ve diversification. While it���s always prudent to diversify, don���t blindly buy equal amounts of every available fund in your 401(k). Such na��ve diversification will often lead to unintended consequences.

For example, if your 401(k) has eight stock funds and two bond funds, buying equal amounts of each will lead to an allocation that���s 80% stocks and 20% bonds. This is a relatively aggressive asset allocation and may not be what you intended.

A single fund, such as a target-date fund, may be all you need. Alternatively, a two-fund portfolio���a global stock fund and a total bond-market fund���may give you sufficient diversification. International funds invest solely outside the U.S., but global funds generally invest in both U.S. and international markets, so they give you worldwide stock exposure.

5. Lean toward low-cost, broadly diversified index funds. The majority of actively managed funds underperform index funds over the long haul. This is due to higher expenses and the behavioral traps that often trip up active managers.

By sticking with low-cost index funds, you���ll outperform 70% to 80% of mutual funds over the long run. But beware: Not every index fund is low cost. Be sure to look at a fund���s expense ratio before investing.

6. Avoid home-country bias. As U.S.-based investors, it���s tempting to stick to U.S. stock funds and shun international ones. This is a mistake on two counts. First, by diversifying globally, your portfolio will be less volatile because U.S. and international stocks are imperfectly correlated.

Second, U.S. and international stocks historically have taken turns when it comes to market leadership. Yes, U.S. stocks have greatly outperformed over the past decade. But if history is any guide, international stocks will lead the way over the decade ahead.

John Lim is a physician and author of "How to Raise Your Child's Financial IQ," which is available as both a free PDF and a Kindle edition.��Follow John on Twitter @JohnTLim��and check out his earlier articles.

John Lim is a physician and author of "How to Raise Your Child's Financial IQ," which is available as both a free PDF and a Kindle edition.��Follow John on Twitter @JohnTLim��and check out his earlier articles.The post Six Principles appeared first on HumbleDollar.

November 14, 2021

Mind the Gap

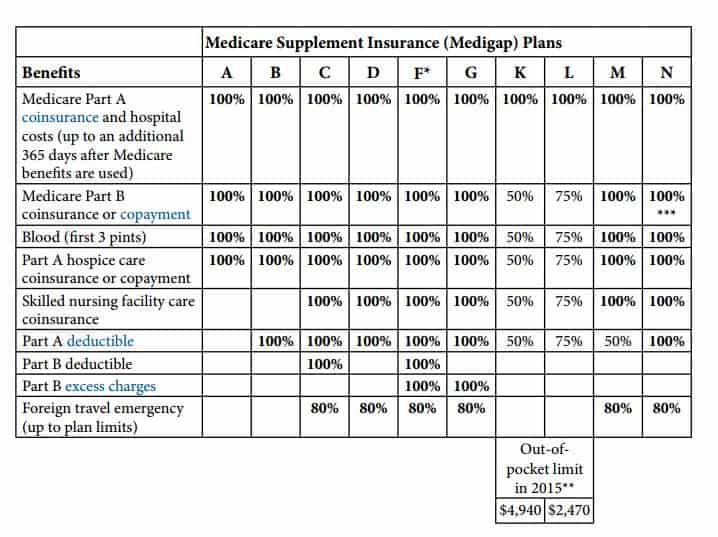

Medicare only pays about 80% of medical care. We thought it would be complicated deciding how to cover the other 20%, but we may have been too pessimistic. After viewing Matt���s presentation and doing some research on our own, we quickly came to two conclusions.

First, traditional Medicare plus a Medigap policy was preferable to Medicare Advantage. My wife had grown used to going to any doctor she wanted, without referrals or concerns about which tests were and weren���t covered. We were also concerned that, if she went with Medicare Advantage and her health deteriorated, she might not be able to swap back to traditional Medicare because she wouldn���t be able to obtain Medigap coverage. Quite simply, traditional Medicare plus Medigap coverage offers more complete coverage and more options. The higher cost seems worth it.

Second, while there are numerous Medigap plans, only two seem to make any sense: Plans G and N. They���re almost identical, but G comes with no copays and coverage for Medicare B��excess charges. I think we all understand the benefit of no copays, but the whole excess charge coverage is a little confusing.

Our subsequent 30-minute appointment with Matt covered much of the above, including how you need to factor in the insurance company���s potential rate increases when making your selection. Matt then mentioned that Plan G would cost ���about $100 a month and Plan N about $70 a month.��� At the end, he asked if we wanted to move forward with him and ���lock in a rate.���

I responded that, before we move forward, could he provide quotes for Plan G and Plan N? To that, he replied, ���I just did, about $70 for N and $100 for G.��� I then became confused. My wife very reluctantly said we needed some time to think about it.

When we got off the phone, we had a ���heated discussion��� about my lack of listening skills and the fact I was dragging my feet. I replied that when insurance agents provide an auto or home insurance quote, they don���t preface it with ���about.��� Why should Medigap insurance be any different? Thankfully, a little while later, Matt���s assistant called us back to get some more details and then provided the exact quote for Plan G, which was��� $147.51 a month.

Apparently, there was a miscommunication about our zip code. While I was a little disappointed with having to pay ���about��� $50 more a month, I was ecstatic to realize that my listening skills were just fine. The afterglow lasted all day, which at one point had me running up some stairs two at a time ����la Rocky, while singing, ���We are the champions.���

It looks like the winner is Medicare Plan G purchased from Aetna at $147.51 a month. But we haven���t yet signed up. My wife is holding off until we find out if her former employer, Ernst & Young, provides any health insurance benefits to retirees. In the end, that appears to be the hardest part of the process.

The post Mind the Gap appeared first on HumbleDollar.

Spending Nervously

Americans sure seem ready to spend. According to Creditcards.com, approximately four in 10 shoppers are willing to go into or add to debt for this year's holiday spending. Here are more fun holiday shopping facts: Parents will spend $276 on average per child under age 18, while men will spend 55% more than women on gifts for their significant other.

Research shows that giving to others and donating to charity often bring great happiness to the giver. And why not give? Consumer finance data suggest our finances are quite strong this holiday season. Maybe splurging in the weeks ahead isn���t all that reckless.

On the other hand, many people don���t feel as financially secure as perhaps they should. Friday���s consumer sentiment survey from the University of Michigan found that folks are currently the most financially pessimistic they���ve been since 2011. More economic data comes our way in the next few days, including the monthly retail sales report on Tuesday.

Spending is forecast to be huge this holiday season. In late October, the National Retail Federation published its winter holiday sales outlook. The group expects that this year will shatter shopping records. But will consumers spend gleefully because the economy has rebounded���or spend cautiously because they���re worried it won���t last? Wall Street will be watching.

The post Spending Nervously appeared first on HumbleDollar.

Helping Wisely

1. Transparency.��This applies in several ways. First, you should let your children know your objectives for these gifts. Do you want to see them spend it on something specific���such as a home down payment���or are they free to use it as they see fit? If they use the funds in a way that seems frivolous to you, is that a problem or is that entirely their choice? There���s no right answer on this, but it���s important to set expectations.

Another aspect of transparency: While you don���t have to share your entire balance sheet, it helps to let your children know how gifts today might relate to any future inheritance. That���s because children can draw very different conclusions from the gifts they receive. On the one hand, generous gifts might be an indication of a substantial inheritance down the road. But on the other, generous gifts might result in very little being left at the end. From a child���s perspective, it���s impossible to tell the difference. Children may not be��entitled��to this information, but they���ll sleep easier if they aren���t constantly wondering.

2. Predictability.��I���ve observed three approaches to giving: one-time gifts, regular annual gifts and periodic, unscheduled gifts. In my opinion, the first two work well, but the third should be avoided. Why? Kids are grateful for any assistance. But everyone likes to be able to plan. For that reason, I recommend being as predictable as possible.

If you go the route of a one-time gift, let recipients know they shouldn���t expect more. Alternatively, if you want to start giving annually, set expectations as clearly as possible. Tell children, for example, that they���ll each receive $5,000 every New Year���s Day and they can count on that. Obviously, you���ll want to pick a number you know you can afford more or less indefinitely. That���s why I���d start with a reasonable sum. You can always increase it later, but you want to avoid ever having to decrease it.

As I��noted��a few weeks ago, I think it makes sense to go slow with any gifting plan. This will allow you to see how things are working and give you a chance to adjust course before increasing the amounts.

Another reason to be consistent and predictable: These aren���t just financial transactions. Adult children interpret gifts as an expression of parents��� feelings toward them. This might seem surprising, but I���ve seen more than one case in which arbitrary gift amounts caused undue stress for recipients. When a gift is higher than expected, the recipients might spend the next year wondering if they���ll receive that same generous amount next time. On the other hand, if a gift is smaller than before, the recipients might wonder if they did something to upset their parents. I have seen all of the above, and it���s not pleasant. Fortunately, it���s easily avoided.

3. Equity.��Suppose you have two children. One is a schoolteacher and the other a brain surgeon. If you���re making gifts, should they be treated equally or instead treated according to their needs? When there���s a wide disparity like this, it might seem silly to treat them equally. In fact, the brain surgeon might be happy to see the schoolteacher treated more generously. But this is an extreme example. In most cases, the differences aren���t as stark���and it might not be easy to judge other people���s needs.

Consider two brothers, one earning $300,000 and the other $75,000. At first glance, parents might assume the higher-income child needs no help and that gifts should be directed only to the brother with more modest means. But the numbers might surprise you. In this example, all else being equal, the higher-income child would pay $54,000 in federal taxes, while the lower-income sibling would pay just $5,600. And if they each have a child in a private college, the higher-income family��might pay��full freight���about $78,000���while the lower-income family would pay just $5,750. The result? The higher-income family will, of course, still have more disposable income. But after paying nearly 10 times more in taxes and 13 times more in tuition, the difference might be less than you���d assume.

Differences in income are just one way in which families��� needs can differ. What if one child is unmarried while another has several children? Or maybe one child lives in a more expensive city than another? As you can see, it quickly becomes a minefield to assess other people���s needs. But perhaps most important, high-income children have feelings, too. As parents, we might feel we���re doing the right thing by helping the child with greater financial needs. But again, these aren���t just financial transactions. That's why I think the best solution is simply to treat children equally.

While I think equity is the best policy, I want to be clear: This is a guideline and not a rule. There are many cases in which it will make sense to do things differently���if one child has special needs, for example. But if you do, I would again stress transparency. Let everyone know the plan.

Adam M. Grossman��is the founder of Mayport, a fixed-fee wealth management firm. Sign up for Adam's Daily Ideas email, follow him on Twitter @AdamMGrossman��and check out his earlier articles.

Adam M. Grossman��is the founder of Mayport, a fixed-fee wealth management firm. Sign up for Adam's Daily Ideas email, follow him on Twitter @AdamMGrossman��and check out his earlier articles.The post Helping Wisely appeared first on HumbleDollar.

November 13, 2021

Phoning It In

There are some state-specific mobile apps that do this, like New York���s Excelsior Pass, as well as proprietary apps like Clear and Azova. But there wasn���t one likely winner to become a widely used system���until now. It���s called the SMART Health Card.

The SMART Health Card is a verifiable health record from the CommonTrust Network, a non-profit registry of data sources that encompasses health systems, testing sites, vaccination providers and public health registries. A growing number of U.S. states, international governments and retail pharmacies���including Walmart, CVS, Rite Aid and Sam���s Club���have joined the network and become SMART Health Card issuers for vaccinations.

All use SMART Health IT, an open standards program now supported in software platforms from Microsoft, Google, Apple, Amazon and others. Apple���s latest iOS 15.1 release, and Google Android 5 or later, also both use it.

Here���s how two states, California and Washington State, both of which adopted SMART Health Cards, have made it easy to add proof of vaccination to your Apple wallet:

Head to the state���s vaccine digital record site, which is��here for California and��here for Washington.

Fill in your name, date of birth and cellphone number, and then choose a four-digit PIN and hit submit. The site will text you a link to its site that���s uniquely yours.

Tap on the link texted to you. In the web page that opens, enter your PIN.

The web page will load a QR code and more. Screenshot or print the QR code, then scroll down and tap the Apple Health button at��the bottom.

In the Apple Health app screen that opens, tap ���add to wallet.���

Once that's done, you can access your vaccination SMART Health card like any other card in your phone���s wallet. You���ll also see your COVID vaccination information in the Apple Health app. Other states may adopt different methods while using the same SMART Health technology.

Restaurants and event venues can use the SMART Health verifier app to ensure your QR code has not been tampered with and is uniquely yours based on your name and birth date.

There are different procedures if your state is one of the CommonTrust Network issuers but already gave you a printed SMART Health QR code with your vaccination status. In that case, scan that card with your iPhone���s camera and follow the steps outlined here.

The steps to create a digital SMART card on Android��phones are similar, only a bit more complicated. It may be simpler to use this CommonHealth��app.

The post Phoning It In appeared first on HumbleDollar.

{kind=link}