William Krist's Blog

September 30, 2025

Tech 2030: A Roadmap for Europe-US Tech Cooperation

The United States and Europe confront a common challenge: staying ahead of China in the global innovation race. But the US has moved far ahead in key digital technologies while Europe lags.

The Trump administration recognizes the key role of technology for geopolitical competition. It has made US global leadership on tech and artificial intelligence a core pillar of its national security agenda — most recently in the AI Action Plan. As the US doubles down on tech innovation, Europe risks not just lagging in the short term, but stagnating for the long term.

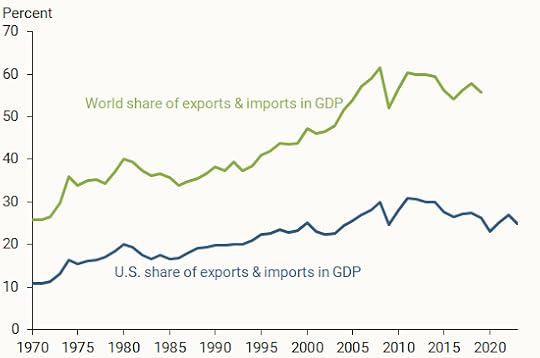

European decline is not in the US national security interest. The continent remains far and away the US’s largest trade partner, with $1.3 trillion in goods moving across the Atlantic Ocean in 2023, almost 40% more than US trade with China. US investment in Europe and European investment in the US run into the trillions. The US needs a prosperous Europe — its large market, investment, innovation, and talent — to compete with China. US companies benefit from access to the continent’s 450 million consumers, key to the US trade surplus of $71.1 billion in services.

As digital services make up an ever-growing portion of this unparalleled economic partnership, a Europe that lags in tech innovation will be neither economically competitive nor a good trade partner. If Europe can take the hard and necessary steps to accelerate its competitiveness in tech to complement areas where the US lead is already far ahead, it will be a stronger partner to the United States. Growing divergence, however, will only benefit Beijing’s global ambitions to create and control the global tech infrastructure. Going it alone, for either the US or Europe, is simply too high a risk for both.

Europe still has much to offer to the US. European companies will not compete directly with the US on scale, but European researchers and innovators have made significant technological breakthroughs that have benefited US tech growth. A Danish software engineer built Google’s Chrome browser engine, while a Hungarian engineer created Microsoft Office. European talent invented video communications. European companies and research institutes dominate lithography imagery, which is needed to make the most sophisticated semiconductors. Quantum computing? Europeans lead the quantum efforts for several major US players.

The benefit goes both ways: US tech companies are some of the largest foreign investors in Europe, with direct investments of $113 billion in the information sector and $29.7 billion in hardware manufacturing in 2024. They play a key role in delivering services, hardware, cloud infrastructure, and more. Amazon employs more than 200,000 Europeans and Apple supports more than 1.7 million jobs. The US hyper-scalers are spending heavily to build data centers in Europe. Earlier this year, Google agreed to invest billions in Poland to support tech innovation and training, artificial intelligence (AI) integration, and cybersecurity — amounting to an estimated 8% increase in Poland’s gross domestic product (GDP).

Europe and the US not only need each other, they share the same analysis of the key strategic questions. They agree that technology represents the key front line of both the economic and security future. Governments no longer drive innovation: Technology companies power productivity growth. As the Trump administration deregulates and stakes a claim for the future of technology, Europe is moving to pare back and simplify its extensive digital regulations.

Most important, the allies share a common assessment that dependence on China threatens Western tech leadership. Brussels has moved to impose tariffs on the import of Chinese electric vehicles and wean itself from Chinese technology in its telephone networks. Washington is imposing strict export controls on key technologies to China. DeepSeek, a Chinese artificial intelligence start-up, shook the assumption that the US will continue to lead. President Trump called it “a wake-up call.”

The key to winning the tech race is the Europe-US alliance: A partnership between the US and Europe is the only way to provide independence from China. The giant, integrated transatlantic economy gives the allies a competitive advantage.

But the US and Europe have yet to set up a competing agenda to Beijing’s “Made in China 2025” plan for its industrial ambitions. Europe must act fast to double down on innovation and the US should take advantage of the opportunities to build strategic complementarity with Europe. If they do so, both sides will profit — and importantly, it will be the US and Europe that set the rules of the new tech-based order rather than China. It is time to think long term but act swiftly.

This paper outlines a pragmatic roadmap for how the US and Europe can maximize their joint comparative advantages to ensure that democracies define and build the future digital order.

Make Good Deals

Below are a few key challenges on which Brussels and Washington can quickly find common ground.

1. Agree on AI Export Controls

The US has to restore trust that it will not pull a “kill switch” and block transfers of cutting-edge tech to Europe. President Trump’s AI Action Plan goes some way to addressing these concerns. It promotes export to allies but also calls for better export control enforcement on crucial components. The US wishes to “align protection measures globally.” These measures should be managed in a way that allows all European countries to continue to benefit from US tech.

Europe, in turn, should prioritize the adoption of a unified export control framework for critical and emerging technologies. Under present rules, Brussels can only advise national governments, leading to long, drawn-out negotiations and inconsistent implementation. End-user controls should be harmonized, creating a single Europe-wide control list of technologies.

2. Keep Data Flowing

“Good” rules and existing agreements should be kept, notably the transatlantic Data Privacy Framework, which allows seamless transfer of private data across the Atlantic Ocean. That road to agreement was long and painful. Europe’s highest court has ruled the framework is “adequate” and data transfers can continue. Both sides should refrain from any legislative changes that might undermine the framework and fight to maintain it if it is challenged again. The free flow of data across the Atlantic Ocean is fundamental to the Trump administration’s goals of AI innovation and strong economic security. The current framework provides legal certainty not just for tech, but for other critical sectors such as finance, health care, and hospitality.

3. Align on AI Standards

President Trump’s AI Action Plan is “opportunity first.” AI holds tremendous potential for good, and Americans and Europeans agree that it presents risks. The transatlantic allies should work together. The AI Action Plan, which calls to export to allies and to “align protection measures globally,” can help.

At the same time, access to both European and US AI ecosystems must be scrutinized for national security risks. Many Western companies continue to conduct AI research in China and Russia, and academic collaboration continues with limited constraints, posing ongoing, serious research security risks.

The National Institute of Standards and Technology’s Center for AI Standards and Innovation should cooperate with European peers. The Trump administration emphasizes innovation and competitiveness. Without compromising its ambitions to develop safe, ethical AI, Europe should adapt its implementation strategy for the AI Act to ensure the right tools are in place to enable smooth, effective compliance.

4. Partner on Quantum

Europe and the US are investing billions in quantum computing, a paradigm-shifting technology. Quantum will unlock solutions to present unsolvable problems, such as drug development and fusion energy. Quantum could also undermine present encryption security.

Although the US is ahead with private-sector funding, Europe ranks second only to China in public quantum investment, with nearly €7.7 billion committed. Quantum facilities in Finland, France, and the Netherlands are first class.

China, too, is prioritizing quantum technologies. It is preparing to launch new experimental quantum communication satellites. The first long-distance quantum-secured communication route opened last year between Shanghai and Beijing.

Before quantum is deployed widely, the allies should discuss their respective approaches. The US is advancing the standardization of encryption algorithms resistant to quantum hacking. Washington should coordinate with European standards bodies.

5. Blast Off Together into Space

The US has taken a strong lead in building reusable rockets and low-orbit satellite communications — two key technologies that Ukraine is leveraging on the battlefield against Russia through Starlink. This significant advantage could be lengthened by collaborating with Europe.

Europe brings significant capabilities, including the Galileo navigation system, the Ariane rocket launch program, and Copernicus Earth observation satellites. Coordinated transatlantic investments in satellite constellations, launch infrastructure, and space debris mitigation can support secure communications, navigation, and climate monitoring.

Without collaboration, the risk is that Europe will pour its energies into space projects that overlap with American plans. It will be much more productive to work together than to compete against each other.

6. Strike a Semiconductor Pact

The US and European Union (EU) must urgently develop a joint strategy to counter China’s chip ambitions. The Netherlands’ ASML holds a monopoly on ultraviolet photolithography machines — critical for producing the world’s most advanced chips — while the US leads in chip design. Aligning the design strengths of US companies with the chipmaking equipment dominance of European firms is economically strategic and essential for national security.

The United Kingdom (UK) should be included in any chip pact. Arm, born in Cambridge, revolutionized the design of power-efficient chips that run all our mobile phones. The bottom line is that Europe cannot do without US- and UK-designed chips, and the US cannot live without access to European chip-imaging prowess.

Beyond chips, the US and Europe have made progress in recent years in ripping China’s Huawei out of their telecommunication networks and promoting the use of trusted vendors. They should extend that support to the provision of subsea and fiber optic cables and the development of fifth- and sixth-generation 5G and 6G networks, both in their home jurisdictions and third countries, while working to prevent untrusted vendors from accessing those networks.

7. Leverage the NATO Security Summit

A June 2025 NATO Summit produced an agreement to spend 5% of GDP on defense, offering new pathways for partnerships with US and European tech. The defense-spending target comprises two tiers: 3.5% for hard defense and 1.5% for broad security-related investments. Within the 1.5%, allies agreed to prioritize critical infrastructure protection, cyber defense, and information technology modernization. NATO also released a Rapid Adoption Action Plan, committing allies to “expedite technology adoption procedures and allocate adequate resources to that end.”

The US and Europe must deepen collaboration between their respective defense industries. European firms such as Germany’s Rheinmetall, France’s Thales, and the UK’s BAE Systems are global leaders in next-generation defense systems. Structured research and development (R&D), shared procurement, and interoperability would enhance military readiness. US tech companies have strong expertise in cybersecurity that NATO members can leverage as part of the 1.5% security-related investment. A transatlantic defense partnership would reduce R&D duplication, boost production, and ensure that democracies — not authoritarian regimes — lead the evolution of military technologies.

8. Revive Cooperation on Critical Minerals and Supply Chains

The allies need to coordinate investment to offer a compelling, values-driven alternative to China’s Belt and Road Initiative. They need to pool development finance and trade policy and leverage private sector capacity. A key opportunity is critical minerals, which today represent a strategic vulnerability for the transatlantic community. China’s dominance must be addressed. If it is not, Beijing will be afforded a giant opportunity for strategic advantage.

Although the Minerals Security Partnership includes the United States, Europe, and 13 other countries, it is making slow progress. A jolt is needed. Together, the allies should launch a “Free Road Initiative.” This could help global partners develop and diversify their supply chain options. One flagship project, the Lobito Corridor in Africa, is an initiative to secure the flow of critical minerals and offer minerals-rich countries alternatives to Chinese investments. A second flagship project could be the India–Middle East–Europe Economic Corridor (IMEC), which promises to secure and diversify supply chains with the Middle East and India, important trading partners for Europe and the US.

Europe: Prioritize Competitiveness

Brussels has made no secret of its desire to regulate the digital world, only to realize that the cost of its rules was hobbling its tech industry. Some European tech companies now say they spend up to a third of engineering resources on complying with the digital rulebook. The “Competitiveness Compass,” a European Commission plan to boost European productivity, represents a positive plan for prioritizing growth.

But it remains unclear just how far Brussels is willing to go. There is talk of “pausing” the AI Act, but not of revising or junking it. The EU can, and should, learn lessons from the US’s AI Action Plan. The Commission has several new laws, implementing codes, and guidelines in the pipeline. A soon-to-be-proposed Digital Fairness Act could add a new raft of obligations on digital platforms, putting them at a disadvantage to brick-and-mortar competitors. The EU should get real on what regulation can achieve and put down the quill.

1. Sensible Implementation

Enforcement and implementation of the main digital regulations — the General Data Protection Regulation (GDPR), the Digital Markets Act (DMA), and the Digital Services Act (DSA) — have proven patchy. Compliance remains challenging.

A new US-EU trade framework has been agreed. It is a start, as it prevents a trade war. Against this new backdrop, the EU should consider the use of the penalties it has prescribed in the DMA and DSA very carefully. From the EU’s perspective, the primary goal of its new digital rules is to ensure that digital products released on the European market are safe, ethical, transparent, and trustworthy. Yet, regardless of the motivation, both the DMA and DSA are deeply unpopular in Washington and seen as a direct attack on US firms. Issuing massive fines against US tech companies will go down badly. Similarly, those countries with digital services taxes (DSTs) should consider the long-term value of such taxes. Washington views EU digital rules as a factor in the trade relationship. Fines and taxes will not make European tech firms more competitive but will antagonize the US.

2. Digital Pragmatism rather than Digital Sovereignty

To meet its own digital goals, Europe faces a classic “buy or build” scenario. “Digital sovereignty,” if defined as building up European capabilities, can be a good outcome. If it becomes a protectionist creed that excludes non-European suppliers, it will hold Europe back.

Europe can and should endeavor to improve its secure digital infrastructure, address what French President Emmanuel Macron called “shameful strategic dependencies,” and reduce reliance upon the US overall.

It is impractical for Europe to digitize without working with US companies. Open-source models should be prioritized, as the US has done in its AI Action Plan. Significant investment in tech will be required — up to €800 billion, according to former Italian Prime Minister and European Central Bank Chief Mario Draghi.

3. Follow the Competitiveness Compass

Europe knows the steps required to restore competitiveness, but has been slow to start the work. Recent announcements, such as the Competitiveness Compass and the new scale-up fund, are promising. The Commission has plenty of recommendations from reports from Draghi and Enrico Letta, another former Italian prime minister. Stand-out items include the following:

Complete the digital single market, benefiting consumers and boosting cross-border trade.

Introduce the 28th regime for an EU-wide corporate registration, allowing companies to operate across the continent efficiently and grow.

Finalize the Savings and Investments Union to awaken the slumbering capital markets in Europe and allow European tech hopefuls to raise funds.

Explore how to best leverage “open” offerings from reliable vendors for AI. The European Commission’s AI gigafactory plans envisage providing access to open-source large language models for small companies.

Europe should approach its challenges with a sense of urgency but not in a blind panic. Much remains to play for in AI, quantum, and other emerging technologies.

US Tech Must Lead

The new US-EU trade framework, albeit with a high tariff threshold, is to be welcomed. Tariff threats undermined US demands for Europe to step up spending on its own defense. The tariff threats also hurt US tech leaders and encouraged Europeans to seek domestic alternatives.

US tech has engaged with the US administration on a range of issues: the Stargate Project and AI innovation, security and export controls, regulation on the use of data, and content moderation. Most, if not all, US tech firms want to see an EU digital single market come to fruition.

f the transatlantic trade war flares up again, tech firms would be big losers. It is to the benefit of US tech leaders to advocate for policies that defend their interests without putting them at the center of any potential European backlash.

Conclusion

The transatlantic alliance represents a strength, providing strategic depth in competition with China. Tension is a feature of any long-term relationship, and the transatlantic relationship has not always seen plain sailing. The Suez Crisis, France’s departure from the NATO command, the invasion of Iraq, and the Edward Snowden affair all caused turbulence. Yet in every case, the allies have found a way forward.

Right now, patience is required. There is a new trade framework with many details to be worked out. It is still comparatively early days in the presidential cycle and the new European Commission’s term. Both need time. The war in Ukraine continues. The Middle East burns. President Trump and his administration have yet to stabilize their position on key policy areas. The European Commission is just formulating its competitiveness plans.

China aims for tech dominance — to reinforce dictatorial control. The National Endowment for Democracy calls this goal “data-centric authoritarianism.” Instead of using AI and other technologies to improve lives, Beijing leverages tech to stifle dissent. AI, biotech, quantum, and digital currencies give the Chinese Communist Party unprecedented power to monitor its population.

The allies must respond. Although little chance exists of another formal transatlantic tech forum like the Trade and Technology Council, other venues could offer opportunities to counter China’s growing technological influence. France hosts the 2026 Group of Seven (G7) presidency. This could ignite a clash between French demands for digital sovereignty and Trump administration fears that this will harm American interests. Instead, the G7 could prioritize aligning against China’s growing influence.

If the US and Europe do not collaborate, we risk seeing a splintered tech world with siloed regulatory regimes, conflicting technical standards, and geopolitical walls around data, computer power, and workforce. This would slow innovation and increase uncertainty for companies and governments. It would allow China to race ahead, leaving the West chasing behind.

Tech-Agenda-2030

To read the report as it was published on the Center for European Policy Analysis website, click here.

To read the full report as a PDF, click here.

The post Tech 2030: A Roadmap for Europe-US Tech Cooperation appeared first on WITA.

September 26, 2025

How 100% Pharmaceutical Tariffs Will Impact Domestic Manufacturing and Supply Chains

A new trade policy from President Donald Trump introduces a significant tariff on imported pharmaceuticals, directly impacting manufacturing strategies and supply chains for companies serving the United States market. This development adds another layer of complexity to an industry already navigating supply chain pressures, regulatory changes, and capital market demands.

In a statement released on Thursday via Truth Social, the president detailed a plan to impose a 100% tariff on all imported branded or patented pharmaceutical products, effective October 1, 2025. This move follows months of discussion around potential sectorial tariffs, with rates previously suggested to be as high as 250% to incentivize domestic production. The president stated his reasoning clearly, noting, “because we want pharmaceuticals made in our country”.

“The details of the 232 tariffs on pharmaceutical products and APIs have yet to be released, but President Trump’s social media post last night indicates that the Department of Commerce is preparing to announce 100% tariffs on what is expected to be a broad swath of drugs and ingredients,” adds Jason Waite, international trade lead at Alston & Bird.

The policy includes a critical provision for pharmaceutical developers: the tariff can be avoided if a company has initiated the construction of a manufacturing facility within the US. “There will, therefore, be no Tariff on these Pharmaceutical Products if construction has started,” the president wrote. In other words, as Waite states, “Significantly, it appears as if generic drugs may escape the tariffs, and that companies building plants in the United States may enjoy some form of exemption.” This ultimatum to onshore production presents a pivotal challenge for industry leaders, from those managing outsourcing and supply chains to executives making long-term capital investment decisions.

It remains unclear if this new 100% rate will be applied in addition to a previously announced 15% tariff on pharmaceuticals imported from the European Union. This lack of clarity introduces further uncertainty for global manufacturing and logistics planning. Indeed, Waite points out that “there are many questions about exactly how companies will be able to avail themselves of [the aforementioned] exemption, but, overall, the President’s announcement suggests a recognition of the complexities of the pharma market and manufacturing, and the impending emergence of a novel tariff regime intended to meet some of the challenges that industry has brought to the Administration’s attention over the past five months.”

How are industry and investment trends responding?

For professionals tracking major industry moves and investment strategies, the tariff announcement crystallizes a trend that has been building for months, Many major pharmaceutical companies, anticipating such policy shifts, have already committed to substantial investments in US-based manufacturing infrastructure.

AstraZeneca announced a $50-billion investment in late July, expressing confidence in its ability to produce nearly all its drugs for the US market domestically. Other significant commitments have come from Johnson & Johnson ($55 billion), Roche ($50 billion), Bristol Myers Squibb ($40 billion), Eli Lilly ($27 billion), Novartis ($23 billion), and Sanofi (at least $20 billion). Eli Lilly recently broke ground on two new plants as part of its investment.

While these multi-billion-dollar projects signal a clear direction, questions remain about whether these new facilities will have the capacity and technical capability to manufacture every patented product currently marketed in the US. For those in drug development and manufacturing, this raises critical considerations about technology transfer, scalability, and the complexities of establishing new production lines for diverse product portfolios.

Echoing Waite, PharmTech editorial advisory board member Eric Langer, managing partner at BioPlan Associates, says “In the near term, the lack of clarity around how these tariffs will be implemented is likely to increase uncertainty. Uncertainty creates roadblocks to investments, and bio/pharma investments are not quickly executed. So, the investment announcements may be more aspirational or speculative, and the near term impacts minimal.”

Langer notes that this invest-or-tariff model could also be used by other countries in the longer-term. “This could result in zero net gains in terms of expanding US pharma manufacturing,” he points out. “Worse, it could end up creating inefficient manufacturing sites that are built simply to avoid tariffs in major markets.”

Building plants in the US will take time, notes PharmTech editorial advisory board member Rory Budihandojo, an independent GMP consultant. “And the finished drug product cost will be potentially higher than manufacturing them in other countries; the increased production cost will be passed on to consumers.”

Linda Girgis, MD, a primary care physician with a private practice in South River, NJ, agrees with Budihandojo. “Raising tariffs 100% can hurt patient already being squeezed by the high cost of pharmaceuticals,” she says. Many patients are already unable to afford certain medications and are forced to take cheaper alternatives that may not be as effective, or no medications at all.”

What are the regulatory and supply chain implications for bio/pharma?

This policy shift intersects directly with ongoing industry-wide conversations about securing supply chains and navigating the regulatory landscape. The vulnerability of established drug supply chains has been a recurring theme, and this tariff serves as a powerful catalyst for onshoring initiatives.

To support this domestic manufacturing push, FDA recently launched its PreCheck initiative. This program is designed to streamline the process for companies seeking to build new manufacturing sites in the US. For regulatory affairs professionals, understanding and leveraging such initiatives will be crucial for managing timelines and ensuring compliance, echoing the industry’s interest in programs like the European Commission’s efforts to streamline drug lifecycle management.

The ultimatum effectively ties market access to domestic investment, forcing companies to re-evaluate their global manufacturing footprint. This will have far-reaching effects on everything from the development of small molecules and active pharmaceutical ingredients to the sourcing of excipients, areas already facing significant supply chain pressures.

Dr. Girigs notes that disruptions to the drug supply chain can have disastrous health effects for many patients, adding that “medications for chronic medical problems need to be taken on a daily basis and, if they become unavailable, can lead to medical complications and/or death.”

What about pharmaceuticals that aren’t fully generic or entirely new?

“We should discuss drugs approved under 505(b)(2)—a category that is neither fully generic nor entirely new,” says PharmTech editorial advisory board member Aloka Srinivasan, PhD, principal and managing partner, Raaha LLC, and an expert on generics. “Generics, which are pharmaceutical equivalents of innovator products, are approved under 505(j). New chemical entities, which require the full spectrum of nonclinical and clinical studies, are approved under 505(b).”

Srinivasan adds that the 505(b) pathway, however, applies to pharmaceutical alternatives to existing products. “These drugs are approved with a limited set of data and may or may not be under patent protection,” she explains. “For example, if the innovator product is a 10 mg tablet, a company might develop a 10 mg capsule or an oral solution. By demonstrating equivalence to the original tablet through minimal studies like in case of generics, the company can establish safety and efficacy and obtain FDA approval under the 505(b) pathway. Most 505(b) have some patent protection, though they are not as extensive as new chemical entities.”

Although these products are technically considered “new” by the FDA, according to Srinivasan, they are very close to generics and can offer advantages, such as improved patient compliance. “Additionally, they may help reduce costs of drugs and give patients better choices,” she continues. “It will be interesting to observe how such products are impacted in the market and whether 100% tariff on such products affects the broader drug landscape.”

Budihandojo does think it will make more sense to manufacture generics in the US than overseas “due to the quality and data integrity issues we are seeing in overseas drug production in India and China (where most generics are being produced). The lower profit margin for manufacturing generics potentially leads to manufacturers trying to cut corners to save cost, impacting quality.” He adds that generic manufacturing in the US makes it easier for FDA to “oversee” production quality and compliance.

What is boils down to, says Srinivasan, is that nobody is able to clearly understand the 100% tariff. “President Donald Trump announced Thursday that brand-name or patented pharmaceutical products will be subject to a 100% tariff starting October 1 – unless the drugmaker is building a manufacturing plant in the US,” she notes. “The definition is not clear, there are several brand named products with no patents; will they be exempt? Also, several products may have patents but not a ‘brand name.’ We need more clarity around these.”

To read the article as it was published on the PharmTech website, click here.

The post How 100% Pharmaceutical Tariffs Will Impact Domestic Manufacturing and Supply Chains appeared first on WITA.

September 17, 2025

World Trade Report 2025: Making Trade and AI Work Together To The Benefit of All

Artificial intelligence (AI) is beginning to reshape the global economy. Like previous general-purpose technologies, or technological breakthroughs with global impact – such as electricity or the internet – AI has the potential to transform how economies function by altering the ways in which goods and services are produced, exchanged and consumed. However, its future trajectory and impact remain uncertain. In addition, the effects of AI raise critical questions about the future role of trade in supporting inclusive growth, because AI could either foster innovation, boost economic growth, and prompt income convergence between and within economies – or it could deepen existing economic and technological divides.

The World Trade Report 2025 examines the complex and fast-evolving relationship between AI and international trade, and explores how these forces can shape inclusive growth. The central message of this report is that AI can become a powerful driver of inclusive, trade-led growth – where inclusive growth refers to economic growth that expands market opportunities while ensuring that the gains from trade are widely shared both across economies and within societies – but only if economies invest in the right enabling policies and cooperate to prevent fragmentation of the regulations governing the digital economy. A rules-based multilateral trading system, with the WTO at its core, is essential to ensure that the benefits of AI are widely shared.

AI and trade can be catalysts for more inclusive growth

AI presents new opportunities to reduce trade costs and expand participation in global markets, especially for small companies. AI tools are already enhancing trade efficiency by improving visibility within supply chains, automating customs clearance, reducing language barriers, strengthening market intelligence, improving contract enforcement and helping firms, including micro, small and medium-sized enterprises (MSMEs), to navigate complex regulations. WTO research, based on a joint survey conducted in 2025 with the International Chamber of Commerce (ICC) specifically for this report finds that among firms currently using AI, nearly 90 per cent report tangible benefits in trade related activities, and 56 per cent report that it has enhanced their ability to manage trade risks.

AI is also boosting productivity across sectors, which underpins economic growth. Empirical studies show that the use of AI brings about tangible efficiency gains in tasks as diverse as customer support, management consulting and software development, though the extent of these gains can vary by context. One recent estimate, based on research on specific tasks, suggests that AI could add around 0.68 percentage points to annual growth in total factor productivity, which measures how efficiently an economy uses its inputs – typically labour and capital – to generate output.

WTO simulations suggest that AI could lead to significant increases in global trade and real income. These simulations are based on an extension of the standard WTO Global Trade Model with AI services and incorporate trade cost reductions, a shift in tasks from labour to AI and productivity gains related to this shift. They suggest that AI could lead to significant increases in trade and GDP by 2040, with global trade projected to rise by 34 to 37 per cent across different scenarios. The largest growth occurs in the trade of digitally deliverable services (42 per cent), including AI services. This trade increase reflects (i) reduced operational trade costs, (ii) the strong projected growth of AI services combined with the high tradability of AI services, related to its geographic concentration of production in a few regions, and (iii) the above-average productivity growth in more tradable sectors, in particular digitally deliverable services. The development and deployment of AI are also projected to generate substantial global GDP increases, ranging from 12 to 13 per cent across scenarios.

The impact of AI on inclusive growth will depend on how the digital divide across economies – which includes disparities in digital infrastructure, capabilities and hardware – is addressed, and on how the technology spreads globally. WTO economists simulated four AI uptake scenarios to capture different degrees of policy and technological catch-up between economies, and the differences between scenarios were substantial. In the benchmark scenario, where low-income economies do not catch up with high-income economies in terms of digital technology and infrastructure, high-income economies see their incomes rise by 14 per cent, compared to 11 per cent for middle-income economies and 8 per cent for low-income economies. However, this gap narrows considerably if digital infrastructure improves in low-income economies, with income growth projected at 11 per cent for low-income economies, and 12 per cent in both middle- and high-income economies. Meanwhile, in a scenario that includes improvements in both infrastructure and broad AI adoption, low-income and middle-income economies are projected to benefit even more, with GDP gains rising to 15 per cent for low-income economies and to 14 per cent for middle-income economies.

Furthermore, AI could contribute to a moderate reduction in income inequality among workers. As a result of the shift in tasks from human labour to AI, the skill premium, measuring the ratio of wages of high-skilled relative to low-skilled workers, could decline slightly. Globally, while the real wages of all labour groups are expected to rise, the skill premium is projected to decline by 3 to 4 per cent across various scenarios. The overall narrowing of the wage premium reflects the fact that the task substitution from human labour to AI is more pronounced for medium-skilled and high-skilled occupations than for low-skilled ones, meaning that the relative demand for medium-skilled and high-skilled labour declines.

Trade contributes to making AI more accessible. Most economies depend on international markets for AI-enabling inputs, from raw materials to semiconductors and high-performance computing equipment, to training data and cloud services. In 2023, global trade in AI‑enabling goods – including raw materials, semiconductors and intermediate inputs – totalled US$ 2.3 trillion. Trade also facilitates the delivery of AI-enabled tools – from remote diagnostics to financial inclusion apps, especially in economies with limited domestic capabilities.

Participation in AI value chains opens a range of development opportunities. Some economies are emerging as hubs for upstream inputs, such as critical minerals and energy, while others are positioning themselves as regional centres for data hosting, cloud services or the local adaptation of AI models. Even foundational AI inputs, such as training data, offer entry points for less technologically advanced economies to engage in AI development. Many developing economies are already contributing through labour‑intensive activities, including data collection, annotation and moderation; however, ensuring fair compensation and adequate labour protection remains a challenge.

AI-enabled services show potential to create new trade opportunities, as many applications are digital and scalable. Applications such as AI-powered content creation, telemedicine, and data analytics enable firms to scale efficiently and compete globally. While challenges remain, basic digital connectivity may allow economies with limited physical infrastructure to participate more actively in global markets. AI-enabled services create dynamic learning effects and help to accelerate structural transformation, particularly in low-income and middle-income economies.

Trade can facilitate the diffusion of AI innovation, as economies that are more open to trade tend to experience stronger innovation spillovers. Bilateral trade flows in digitally deliverable services are closely correlated with cross-border AI patent citations – i.e., when one patent filed to protect intellectual property (IP) rights references another, a proxy for knowledge flows because they document when one invention builds on another. WTO analysis shows that a 10 per cent increase in digitally deliverable services trade is associated with a 2.6 per cent increase in AI patent citations across borders.

The risk of a widening digital divide

The transformative potential of AI for trade is significant, but it is far from guaranteed. Without targeted investment, inclusive policy frameworks and international coordination, AI could exacerbate existing divides and even create new ones, and this would undermine the development potential of AI.

Global access to AI is highly unequal, and this limits the ability of many economies to participate in AI-driven trade. Digital infrastructure, computing capacity, qualified workers and regulatory readiness are concentrated in a handful of economies. This imbalance is mirrored in trade-related policies: high-income and upper middle-income economies have a much more advanced policy framework for AI and digital trade, and these economies provide significantly more financial support for AI-related production. In contrast, low-income economies have only recently begun to develop regulation regarding data flows and AI. Such disparities constrain the capacity of poorer economies to harness the potential of AI.

AI may shift comparative advantages in ways that reinforce inequality. AI technology favours capital and data-intensive production, which could erode the competitiveness of economies that rely on low-skilled and low-cost labour. Meanwhile, AI development capacity remains concentrated within a limited number of firms and economies, and it may further raise returns to capital, widening existing divides. WTO simulations show that the rental rate on capital – that is, the cost of using capital inputs – rises significantly relative to wages, by about 14 percentage points. This is mainly because AI services both substitute for labour and rely heavily on capital. As a result, demand for capital increases more than demand for labour, pushing up the rental rate on capital.

While trade can help to diffuse AI, uneven adoption risks reinforcing existing divides. AI uptake is concentrated in large, urban, digitally connected firms. Smaller firms and less-connected regions face a range of hurdles, from infrastructure gaps to compliance costs. The 2025 WTO–ICC survey results show that only 41 per cent of small firms report using AI, compared to over 60 per cent of large firms. Among low-income and lower middle-income economies, fewer than one-third of firms use AI.

Labour market disruptions could compound the risks of a widening divide. AI has the potential to affect the labour market significantly, particularly in services in which digitally delivered trade has offered promising development opportunities for lower income economies. While certain tasks, such as transcription, translation and support functions, are increasingly susceptible to automation, the overall impact on jobs will depend on how AI complements or substitutes specific tasks, and on the capacity of workers and firms to adapt. In some scenarios, AI may boost the productivity of service workers in developing economies, enhancing their global competitiveness. But without the right policies, these shifts could also narrow export opportunities or intensify reshoring pressures in advanced economies.

The role of domestic policy in creating an enabling environment for more inclusive AI

AI’s impact on inclusive growth depends on the design of trade and trade-related policies. Tariffs, export controls, services regulation, and data governance all shape the availability, affordability and diffusion of AI and AI-enabling goods and services. Uneven policy adoption across income groups risks widening structural gaps in AI readiness, especially those linked to the digital divide.

The new WTO AI Trade Policy Openness Index (AI-TPOI) reveals significant variation in AI-related trade policies across and within income groups. The AI-TPOI, compiled by WTO economists (see Annex D), captures three policy areas relevant to AI diffusion: barriers to services trade, restrictions on trade in AI-enabling goods, and limitations on cross-border data flows. On average, lower middle-income and upper middle-income economies tend to maintain the most restrictive policies. While low-income economies appear relatively more open, this may reflect limited regulatory capacity and underdeveloped digital infrastructure rather than deliberate openness. Even among economies with low tariffs, restrictive data localization requirements or export controls can inhibit access to AI tools and markets.

Beyond openness, complementary policies also shape how trade and AI contribute to inclusive growth. Such policies include, among others, IP protection, competition frameworks, infrastructure and energy policies, education systems and government support. These policies, however, remain mostly concentrated in high-income and upper middle-income economies.

IP and competition policies related to AI are expanding rapidly. The number of economies adopting at least one AI-related IP policy rose from 41 in 2017 to 140 in 2024. But significant disparities remain across income groups. In parallel, competition policy measures targeting AI have surged since the release of ChatGPT in November 2022, with 44 new measures recorded. Yet over 80 per cent were in high-income and upper middle-income economies, demonstrating again that the policy uptake is unequal.

Making AI development more sustainable and inclusive would require increasing the already substantial investments in the energy and digital infrastructure dedicated to AI development. Data centres already consume 1.5 per cent of global electricity, showing the importance of existing infrastructure investments, including in renewable energy, to support AI development. Yet policy activity in support of renewable energy is highly uneven. High-income economies account for 69 per cent of all global renewable energy policies, while low-income economies represent just 1.5 per cent.

Education policy, which helps economies develop the capabilities necessary to benefit from AI, also reflects a global imbalance between higher- and lower-income economies. High-income and upper middle-income economies invest more in education overall, and are increasingly developing AI-specific programmes. In contrast, fewer than one third of developing economies have adopted national AI education strategies, which is likely to widen the skills gap across income groups.

Targeted government support is increasingly playing a role in shaping AI development. The share of global subsidies targeting AI-related products has increased considerably since 2010, exceeding 15 per cent at its recent peak. High-income and upper middle-income economies account for over 98 per cent of these measures, and this demonstrates that there is a substantial risk of further concentration of AI capabilities.

Without concerted action, disparities in policy action risk locking in long-term inequalities. The uptake of AI-targeted policies is highly uneven across income groups, with the major share of such policies being implemented by high-income and upper middle-income economies. International cooperation on such policies could help to narrow disparities, and ensure that trade remains a force for inclusive progress in the AI era.

The role of the WTO in supporting more inclusive approaches to trade and AI

International cooperation on AI is still in its early stages, and remains largely aspirational, with little attention given to trade or trade policy. Most AI-related initiatives primarily involve high-level declarations, broad principles or voluntary guidelines that emphasize the ethical use, safety, transparency and interoperability of AI. Most also make little or no reference to international trade, despite the fact that trade is the “oil” that keeps the AI engine running, as it enables the cross-border flow of essential inputs, from data and infrastructure to the hardware, human talent and services that power AI development and deployment.

Greater international cooperation, and particularly stronger cooperation on AI and trade, could support wider participation in AI development and deployment. Trade cooperation can foster a more stable and predictable environment for AI-related investment and innovation. This can help mitigate issues such as unequal access to technologies, regulatory fragmentation and concentrated market power, that hinder broader and more affordable participation in AI development and deployment.

So far, regional trade agreements (RTAs) have been the main avenue for advancing trade related AI cooperation among economies. However, such agreements, mostly negotiated by high-income economies, remain limited in both number and scope. They typically recognize the potential of AI to support economic growth or digital transformation, with fewer identifying areas for cooperation, such as research and regulation.

Although not specific to AI, the WTO framework already contributes to AI development and deployment by supporting innovation and enabling more open and predictable trade in relevant goods and services. AI development and deployment rely on access to global markets, cross-border data flows and technological diffusion, areas that are directly impacted by trade policy. In that context, several WTO agreements underpin the global AI ecosystem by lowering hardware costs through the Information Technology Agreement (ITA), promoting regulatory transparency and international standards via the Agreement on Technical Barriers to Trade (TBT), facilitating AI-related services trade under the General Agreement on Trade in Services (GATS), and supporting IP protection and technology diffusion through the Agreement on Trade-Related Aspects of Intellectual Property Rights (TRIPS).

Beyond rules and market access, the WTO can also help broaden participation in AI-related trade through mechanisms that promote transparency, dialogue and capacity-building on trade-related aspects of AI. For example, the joint WTO-International Trade Centre (ITC)-United Nations ePing alert system, which tracks sanitary and phytosanitary (SPS) and TBT measures supports stakeholders in tracking trade-related AI developments. Meanwhile, regular discussions in WTO committees allow members to raise concerns, share experiences and learn from each other’s regulatory approaches to AI, thereby promoting regulatory alignment. WTO-led initiatives, such as Digital Trade for Africa help developing economies build the infrastructure, regulatory capacity and skills they need to participate more effectively in the digital economy – foundations that are increasingly relevant for AI-related trade. The joint WTO SecretariatInternational Trade Centre (ITC) Women Exporters in the Digital Economy (WEIDE) Fund is helping women in developing economies to trade more and better through digital tools. Recent Aid for Trade projects in areas such as transport, infrastructure and agriculture already incorporate AI, helping beneficiary economies to optimize logistics and manufacturing processes or to promote sustainable farming.

Efforts to broaden participation in AI-related trade would also benefit from greater engagement by WTO members. As global AI governance continues to shape up, the WTO could help to guide its development to ensure that trade supports broader access to AI, through improved market access for AI-related goods and services and greater transparency and dialogue on trade-related AI policies. For instance, market access for AI-enabling goods remains uneven, with bound tariffs reaching up to 45 per cent in some low-income economies. Broader participation in the ITA and updated GATS commitments would contribute to making AI more affordable. Striking an appropriate balance between these binding commitments – aligned with each WTO member’s implementation capacity – and policy flexibility remains, however, essential to maintain the predictability that credible commitments provide, while promoting more inclusive AI outcomes. The question of AI and inclusive trade has been a key focus of discussions in some WTO bodies, in particular in the context of the Work Programme on e-Commerce and the Informal Working Group on MSMEs.

For trade policy to help broaden economies’ participation in AI, deeper collaboration of the WTO with other international organizations and initiatives will be needed. Since many trade related AI challenges are rooted in broader policy issues, strengthening coherence between trade policy and other public policy areas is essential to address concerns such as the digital divide, market concentration, labour market impacts, and environmental sustainability. While ensuring such coherence depends on national policy choices, increased collaboration among international organizations can play a supportive role by promoting dialogue, encouraging shared approaches and facilitating the pooling of resources to tackle problems. Coordinated international efforts can thus help to support broader global participation in the AI-driven economy through more open, predictable, forward-looking and flexible trade policies.

A moment of strategic choice

The future impact of AI will depend on choices made today. Whether AI becomes a force for inclusiveness both across and within economies or for division will depend on the choices made now. In order to realise its potential, investment in digital infrastructure, workers’ skills and competitive ecosystems will be required, as well as domestic reform, international cooperation and institutions capable of adapting to fast-moving technological change, underpinned by a commitment to openness, inclusivity and shared prosperity.

The WTO can play a central role in ensuring AI supports inclusive trade-led growth. This means not only advancing trade openness and rule-making, but updating the functions of the WTO itself, promoting transparency and interoperability, and continuing to provide a trusted forum for members to align trade policy with responsible, inclusive digital transformation.

This is a moment of strategic choice for shaping how AI will influence trade and growth. With the right frameworks in place, supported by investment, domestic reform and international cooperation, AI could expand opportunities and strengthen the multilateral trading system. But without deliberate action to close capacity gaps, update trade rules and foster regulatory alignment, the risks of AI may be compounded, and its benefits may remain concentrated among the few.

wtr25_e

To read the report as it was published on the World Trade Organization website, click here.

The post World Trade Report 2025: Making Trade and AI Work Together To The Benefit of All appeared first on WITA.

September 15, 2025

America’s Quiet Turn Towards State Capitalism

The relationship between the United States government and corporate America is undergoing a profound transformation. Under President Donald Trump’s second administration, Washington is abandoning its traditional free-market posture in favour of a more interventionist model where compliance with national-security objectives is increasingly monetised. This evolving approach includes some elements of state-directed capitalism, as practised in countries such as China and Russia. This shift is notable in that it is not driven by economic crisis or wartime necessity but by the aims of generating revenue and deliberately reasserting political control over strategic sectors.

Transactional approach

Over the past few months, the administration has taken extraordinary steps to embed itself within the private sector. The government has acquired a ‘golden share’ in U.S. Steel as a condition for approving its acquisition by Japan’s Nippon Steel. Trump has struck a deal with Nvidia and Advanced Micro Devices, issuing export licenses in return for 15% of the companies’ China-related revenues from H20 chip sales. In July, the Pentagon purchased a 15% stake in MP Materials, a major rare-earth-mining firm, becoming its largest shareholder. Most recently, in August, the administration took a 10% equity stake in Intel, a chipmaker valued at US$8.9 billion, marking one of the most significant US-government interventions in a private company since the auto-industry bailouts implemented in the wake of the 2008 Great Financial Crisis.

These pay-to-play arrangements reflect the administration’s increasingly transactional approach to corporate America – an approach that challenges the foundations of the traditionally market-oriented US system. It blurs the line between regulatory oversight and commercial negotiation. The deals often rest on tenuous legal grounds, with little oversight or transparency. Yet few companies are willing to challenge the government. For many, these arrangements serve as political insurance – a way to ‘buy certainty’ in a volatile regulatory environment. For others, they are a defensive move to avoid more aggressive pressure or exclusion from government contracts. In effect, firms are paying to prevent worse outcomes. These quid-pro-quo deals are potential templates for broader application across strategic industries, with discussions under way about similar arrangements for defence contractors.

Shades of state capitalism

Two models of state intervention appear to be emerging. The first model, often framed as ‘patriotic capitalism’, treats companies or sectors as national champions and instruments of state power. Here, the American state behaves much like its Chinese counterpart, integrating firms into geopolitical strategies. For example, in August, Howard Lutnick, the secretary of commerce, called Lockheed Martin ‘an arm of the US government’, as the company is highly dependent on federal contracts. In its deal with MP Materials, the Pentagon will acquire rare-earth elements at guaranteed prices to establish an end-to-end supply chain of critical minerals in the US, very much mimicking China’s domestic tactics. Similarly, earlier this year, the US government announced plans to invest lavishly in the shipbuilding sector to counter China’s dominance in the industry. Unlike China’s reliance on massive subsidies, the Trump administration prefers to use regulatory leverage over strategic companies and empower government-backed institutions, such as the International Development Finance Corporation. For example, in the deal with MP Materials, the Department of Defense has secured US$1bn in private financing from JPMorgan Chase and Goldman Sachs to build a magnet-manufacturing facility in Texas.

The second model, which is currently dominant, is more transactional and opportunistic – targeting companies such as Nvidia or Apple because they are too large or too profitable not to chip in. This resembles Russia’s system of state capitalism, where firms are expected to share profits with the state in exchange for market access or protection. To make these deals impossible to refuse, the US government is increasingly resorting to lawfare – launching lawsuits under various pretexts. For instance, Apple has secured a tariff exemption in exchange for a US$600bn investment pledge, even as it faces a Department of Justice antitrust lawsuit over smartphone market dominance.

Alternatively, the government can use other regulatory levers to pressure firms by blocking their access to public contracts (the Kremlin’s favourites include investigations into embezzlement and the withholding of fire-safety certificates). As the Russian example shows, there is no such thing as a one-off tax – companies will remain on the hook as new demands will follow, often amid a growing number of lawsuits.

Global pay-to-play deals

What is most concerning is the spillover of this model into the international arena. The Trump administration is already testing global pay-to-play deals as part of its efforts to reorient global trade in favour of the US. This creates two distinct risks: firstly, that multinational corporations – both American and foreign – may become geopolitical instruments caught in the crossfire between Beijing, Brussels and Washington; and secondly, that US firms may actively exert pressure on foreign governments to align with the administration’s political agenda.

European companies with a US nexus – through dollar-denominated transactions or reliance on the American market and technology – are increasingly being pressured to align with US export controls. The Bureau of Industry and Security, which manages US export controls, has already escalated pressure on firms in allied countries. In August the administration removed the South Korean companies Samsung and SK Hynix from the ‘Validated End-User’ list, stripping them of the ability to ship US-made chips and chipmaking tools from South Korea to China-based factories without a licence, and in September it revoked the licence authorisation of Taiwanese multinational TSMC (Taiwanese Semiconductor Manufacturing Company). While it is not new for the US to exert extraterritorial pressure on foreign companies, it is less common for Washington to do so on key firms in allied countries. As with Nvidia’s deal, European tech firms may face demands to forgo revenue or invest in American supply chains to avoid secondary tariffs.

There is a risk that Chinese investors could gain access to sensitive US sectors if they strike the right deal and offer a high-enough price, despite scrutiny from the Committee on Foreign Investment in the US. Despite ongoing national-security concerns, TikTok, owned by Chinese company ByteDance, is increasingly being used as a bargaining chip in the US–China tariff conflict, with the administration signalling interest in acquiring a stake via a ‘golden share’ arrangement. US companies may also be pushed to re-enter the Russian market if doing so serves Trump’s political objectives. With Moscow expressing a desire to see Boeing return, it is conceivable that the administration could pressure the company to resume its operations in Russia as part of a broader peace settlement.

In return, the transactional approach allows US firms to pursue their own corporate interests by rallying behind the Trump administration’s political objectives. The boundaries between the public and the private are becoming increasingly entwined. Capitalising on Trump’s anti-climate agenda, some US firms have urged Washington to use trade negotiations with the European Union to weaken Brussels’ Corporate Sustainability Due Diligence Directive of 2024 (which puts obligations on non-EU companies to ensure their supply chains do not harm the environment or violate human rights). Others may seek to influence the administration on the EU’s 2022 Digital Services Act, which has already negatively affected American Big Tech companies. Acutely aware of Trump’s aspiration to end the Russia–Ukraine war, ExxonMobil executives have already sought government backing for a potential return to the Russian market and reportedly received a ‘sympathetic hearing’.

What we are witnessing is not merely a shift in policy but a systemic transformation in how the US government views its relationship with industry. The long-standing American model – where the market leads and the state follows – may be giving way to a new paradigm where economic power is politicised and corporate autonomy is conditional on national alignment. While it remains unlikely that the US will fully embrace state capitalism, one thing is certain: the rules of engagement between business and government are being rewritten – and the global implications are only just beginning to unfold.

To read the full analysis as it was published on the The International Institute for Strategic Studies website, click here.

The post America’s Quiet Turn Towards State Capitalism appeared first on WITA.

Trade Review Process Could Rock the Calm in US-Mexico Relations

One of the more surprising developments of President Trump’s tenure in office thus far has been the relatively calm U.S. relationship with Mexico, despite expectations that his longstanding views on trade, immigration, and narcotics would lead to a dramatic deterioration.

Of course, Mexico has not escaped the administration’s tariff onslaught and there have been occasional diplomatic setbacks, but the tenor of ties between Trump and President Claudia Sheinbaum has been less fraught than many had anticipated. However, that thaw could be tested soon by economic disagreements as negotiations open on a scheduled review of the U.S.-Mexico-Canada trade agreement (USMCA).

State of play

Both the U.S. and Mexico appear to have found a way to cooperate on the key bilateral security issues — like immigration and organized crime — allowing them to compartmentalize these subjects from negotiations over the future of the economic relationship. But the upcoming USMCA review could still be complicated by broader foreign policy questions about supply-chain security, American economic diplomacy in the hemisphere, and the tradeoffs involved in granting market access to the U.S.

When Secretary of State Marco Rubio visited Mexico last week, the U.S. attacked a boat in international waters that was allegedly transporting narcotics for a Venezuelan cartel. In his press conference, Rubio had warnings for Caracas, but was complimentary about his host country, noting that the U.S. has “had a great relationship with the Government of Mexico” adding that “it is the closest security cooperation we have ever had, maybe with any country but certainly in the history of U.S.-Mexico relations.”

The stabilization of ties is in good part a reflection of Sheinbaum’s success in balancing a steadfast insistence on her country’s sovereignty with her ability to deliver on key American demands — such as the extradition of more than 50 alleged drug traffickers to the U.S. in August.

Sheinbaum’s strategy has helped Mexico’s position — for example, the 30% retaliatory tariffs announced on the country in late July have been suspended for 90 days. No such relief was granted to Canada, which got hit right away with 35% tariffs. Similarly, Mexico is doing significantly better than Brazil, where political and foreign policy differences have led to Trump hitting the South American giant with a 50% tariff.

Beyond Sheinbaum’s deft handling of the relationship, there are other factors in play. One is probably the sheer lack of bandwidth as the Trump administration has embarked on a range of tariff, trade, and “deal” initiatives spurred by economic, ideological, and geopolitical motives, such as the recent imposition of a 50% tariff on India. All this frenzied activity has meant that America’s largest trading partner (Mexico accounted for $840 billion of trade in 2024) kept getting pushed to the back of the line for a scarce commodity in Washington — attention.

The sheer volume of bilateral trade points to another factor that might have kept things from spiraling out of control. Mexico plays a critical role in U.S. industrial supply chains, particularly in the automotive sector, where parts and completed vehicles can cross national borders inside USMCA multiple times during the production process. Fear of the ensuing disruptions has likely helped to at least dampen some of the White House’s enthusiasm for tariffs as a method to deliver quick results.

Where does the USMCA review come in?

But that period of calm could end soon with a long-scheduled review of USMCA (which was itself the result of a 2019 renegotiation under Trump of the original 1992 North American Free Trade Agreement). This will set in train a period of contentious talks as the parties review (and effectively renegotiate yet again) a treaty that the U.S. is already ignoring in many respects. The deadline for renegotiation is Oct. 4. Tariffs on items that do not comply with USMCA rules have jumped to 25% (versus 2.5% earlier), and a complicated mechanism for tariff rebates on auto parts imported from Mexico has a two-year sunset clause, hinting strongly at a desire to force that industry to return to the U.S.

Amid all the trade turmoil emanating from Washington, Mexico’s Economy Secretary Marcelo Ebrard has been arguing that, as long as tariffs on his country are lower than those imposed on others, Mexico will still come out ahead. However, even that is now in doubt. The White House’s quest for investment deals with wealthy, industrialized countries could lead to lower tariffs on those countries’ exports to the U.S. than apply to those from Mexico.

For example, the deals with the EU, Japan, and South Korea contain provisions that could lower tariffs on their automobile exports to the U.S. to 15%. Such a step would hurt not just Mexico, but also U.S. automobile manufacturers who have large operations in that country. Ford CEO Jim Farley pointed this out, saying that these deals would give Japanese automakers a big cost advantage over American automakers who have integrated supply chains across all three USMCA members.

Similarly, lower tariffs on imports from outside the USMCA would reduce the incentive for European and Asian auto and parts manufacturers to locate more of their plants in Mexico. This paradoxically puts Mexico in a position where it could become the strongest proponent of what originated as an American idea — the importance of reducing the U.S.’s supply-chain geographic and security vulnerabilities by “nearshoring;” that is, locating a larger portion of the production facilities servicing American markets within USMCA.

Treasury Secretary Scott Bessent invoked a “Fortress North America” in February when he asked Canada to join Mexico in matching U.S. tariffs on China. And Rubio’s first official trip to Bogotá saw him give an address entitled “An Americas First Policy” where he said “relocating our critical supply chains to the Western Hemisphere would clear a path for our neighbors’ economic growth and safeguard Americans’ own economic security.”

Both statements are in line with Mexico’s preferences, as suggested by the recent move to impose 50% tariffs on Chinese automobiles, but could run into two separate obstacles at the upcoming review. The first is that influential constituencies like the autoworkers’ union want to push for higher purely American content, i.e., reshoring industry within the borders of the U.S. alone rather than just nearshoring to USMCA countries.

In a brief published in July, I suggested that it might be possible to reconcile the “nearshoring” and “reshoring” agendas by raising the percentage of automobile content required to be manufactured in the U.S., while simultaneously requiring significantly higher USMCA content in electronics and telecommunications. The latter would benefit Mexican manufacturing because the country functions largely as a final assembly point for those industries. And combining an element of automotive reshoring with nearshoring in other critical industries would assuage American concerns about both jobs and supply chain security.

However, this would depend on Washington taking the idea of a deeper North American market that confers both security and regional developmental benefits more seriously instead of treating access to American consumers as a reward for investing in the U.S.

So even if calm continues to prevail on the non-trade issues that precipitated the first round of U.S. tariffs on Mexico in February, other issues arising from different understandings of economics-security linkages could still complicate the USMCA review.

To read the full analysis as it was published on the Responsible Statecraft website, click here.

The post Trade Review Process Could Rock the Calm in US-Mexico Relations appeared first on WITA.

September 12, 2025

Beyond the Dragon’s Grip: A Strategic Rebalancing of EU-China Relations

Europe’s energy dependency on Russia was neither unforeseeable nor unremarked. For years, warnings circulated from policy experts, frontline Member States, and transatlantic allies about the dangers of relying on a single, authoritarian supplier for critical energy needs. Yet those warnings were dismissed or downplayed, sacrificed at the altar of economic eciency and diplomatic convenience. When the crisis finally came – Russia’s full-scale invasion of Ukraine in 2022 – the cost of complacency was immediate and severe: soaring prices, supply disruptions, and a race against time to rebuild an energy architecture that had been left strategically hollow.

This moment should have marked more than an energy reckoning. It should have triggered a broader reassessment of Europe’s structural vulnerabilities – particularly its deepening dependence on China. From critical raw materials and clean energy technologies to pharmaceuticals, digital infrastructure, and advanced manufacturing, China has become an indispensable – yet increasingly unreliable – pillar of the European economy. In many sectors, there is no fallback. There is no redundancy. And there is no clear strategy to change that.

The risks are not speculative. China has shown a growing willingness to weaponise interdependence, using trade barriers, export controls, and targeted retaliation as instruments of geopolitical coercion. Its control over vital technologies and inputs – rare earths, batteries, solar panels, and semiconductors – gives it asymmetric leverage over Europe’s economic resilience and political sovereignty. If tensions over Taiwan escalate, or if Beijing chooses to retaliate against European policies it deems unfriendly, entire sectors of the European economy could grind to a halt.

Yet unlike the Russian energy crisis, which forced Europe into a reactive – but ultimately decisive – pivot, the looming threat of a China shock has yet to galvanise a unified or proportionate response. The current EU framework, which labels China simultaneously as a ‘partner, competitor, and systemic rival’, reflects institutional hesitation more than strategic clarity. It masks division. It delays action. It invites drift at a moment that demands discipline.

This paper argues that Europe cannot aord another crisis of foresight. Strategic autonomy is no longer an aspirational slogan – it is a prerequisite for sovereignty in an era of weaponised interdependence. It is the ability to act decisively in defence of European interests without being paralysed by fear of economic retaliation. It is not about cutting ties, but about reducing exposure. Not about closing borders, but about building resilience. Not about confrontation, but about preparation.

The time to act is before the next rupture – not during it. As the window narrows, this paper outlines the contours of a European response: a strategic diversification and managed decoupling plan rooted in clear sectoral priorities, coordinated investment, and institutional preparedness. Drawing on the lessons of the past and the imperatives of the future, it makes the case for why Europe must lead its own transformation – before geopolitical reality forces its hand once again.

Beyond-the-Dragons-Grip

To read the report as it was published on the European Liberal Forum website, click here.

To read the full report as a PDF, click here.

The post Beyond the Dragon’s Grip: A Strategic Rebalancing of EU-China Relations appeared first on WITA.

September 9, 2025

Tariff Analysis Deep Dive: The Most Important Changes For the Auto Industry

Regional ‘reciprocal’ tariffs

Since they were first announced on ‘Liberation Day’ in April, US president Donald Trump’s so-called reciprocal tariffs have been paused and delayed multiple times. In May, Trump said he would negotiate the rates down with countries who were engaging in “good faith” talks. Then, they hit a stumbling block when a US federal court ruled that Trump did not have the authority to impose the reciprocal tariffs on individual countries, but just 24 hours later, the administration’s appeal allowed the tariffs to carry on. The reciprocal rates then went up and down as countries went to the negotiating table. These tariffs (separate from the section 232 tariffs) were due to be implemented from August 1, but experienced more delays.

Tariffs on Canada and Mexico have been complicated, to say the least. With the USMCA up for review next year, the expectation is that tariff-reducing concessions could be made during negotiations. However, at the beginning of August, the US raised tariffs on Canada to 35%, keeping tariffs of 25% on Mexico. For both countries, USMCA-qualifying automotive parts are exempt from tariffs temporarily, while vehicles that are USMCA-compliant are currently tariffed at 25%. Cars built in the US and Mexico can claim back the value of US-sourced parts, although there is still a lack of clarity around this.

US-China talks had tensions rising, with duties racketing up to three-figures, but the countries reached a truce by mid-May, with 30% tariffs on Chinese imports, and 10% on US imports. On August 11, the US and China extended their tariff truce until November 10, holding tariff caps at 30% on Chinese imports and 10% on US imports.

The European Union reached a framework for a deal with the US at the end of July, which reduces the cost of shipping vehicles and parts from the EU to the US from a rate of 27.5% to 15%. Currently, this 15% tariff is not yet in place, with EU documents suggesting it will apply retroactively from August. As it stands, automotive exports from the EU would be taxed higher than those from the UK, which has a 10% tariff after reaching a deal in June, but the UK’s automotive goods have a cap of 100,000 vehicles annually. In response to the deal, industry lobby group European Automobile Manufacturers Association (ACEA), which represents 16 OEMs including BMW, Daimler Truck, Ford of Europe and more, said many elements still need to be clarified. In early August, the EU halted retaliatory tariffs on the US for six months while the two countries attempted to finalise the deal. Also as part of this framework, the EU committed to drop its tariff on automotive imports from 10% to 0%. While this has not yet been finalised, it could be significant for large exporters from the US to EU, such as BMW and Mercedes-Benz. For logistics firms, the new US-EU framework removes cost pressures on transatlantic shipments but adds little clarity for long-term planning.

The US and South Korea agreed on tariffs of 15% for vehicle imports and automotive parts imports in late July, replacing the previously threatened 25% rate. This came into effect on August 1, but as of early September, the agreement remains provisional and has not been formally finalised. Once legally signed off, it will put South Korea on an even keel in terms of tariff rates with the likes of the EU and Japan. South Korea also committed to a $350bn investment in the US, with a share of $200bn allocated for semiconductors and nuclear energy, and $150bn going towards shipbuilding in the US.