J. Bradford DeLong's Blog, page 2185

October 5, 2010

It Does Not Seem to Me That Charles Ferguson Has Gotten It Right...

Oh, back in 2005 Rajan was right and Summers was wrong.

But it did not go down like Charles Ferguson says it does.

Charles Ferguson:

Larry Summers and the Subversion of Economics - The Chronicle Review - The Chronicle of Higher Education: Summers remained close to Rubin and to Alan Greenspan, a former chairman of the Federal Reserve. When other economists began warning of abuses and systemic risk in the financial system deriving from the environment that Summers, Greenspan, and Rubin had created, Summers mocked and dismissed those warnings. In 2005, at the annual Jackson Hole, Wyo., conference of the world's leading central bankers, the chief economist of the International Monetary Fund, Raghuram Rajan, presented a brilliant paper that constituted the first prominent warning of the coming crisis. Rajan pointed out that the structure of financial-sector compensation, in combination with complex financial products, gave bankers huge cash incentives to take risks with other people's money, while imposing no penalties for any subsequent losses. Rajan warned that this bonus culture rewarded bankers for actions that could destroy their own institutions, or even the entire system, and that this could generate a "full-blown financial crisis" and a "catastrophic meltdown."

When Rajan finished speaking, Summers rose up from the audience and attacked him, calling him a "Luddite," dismissing his concerns, and warning that increased regulation would reduce the productivity of the financial sector. (Ben Bernanke, Tim Geithner, and Alan Greenspan were also in the audience.)

Let's roll the videotape:

Lawrence Summers: I speak as a repentant, brief Tobin tax advocate, and someone who has learned a great deal about the subject, like Don Kohn, from Alan Greenspan, and someone who finds the basic, slightly Luddite premise of this paper to be largely misguided. I want to use an analogy, not unlike the one Hyun Song Shin did, but to a rather different conclusion.

One can think of the history of transportation over the last two centuries as reflecting a gradual and determined move away from arm’s length transactions. People once supplied their own power. Then, they started carrying on transportation using tools that they owned. Then, they increasingly relied on tools that other people owned that were provided by intermediaries.

In that process, the volume of transportation activity increased very substantially. Over time, people became almost entirely complacent about the safety of the transportation arrangements on which they relied. Large sectors of the economy came to be organized in reliance on the capacity of planes to fly and trains to move. The degree of dependence on individual hubs—like O’Hare Airport—increased substantially. The worst accidents came to be substantially greater conflagrations than they had ever been in an earlier era.

Yet, we all would say almost certainly that something very positive and overwhelmingly positive has taken place through this process. Something that is overwhelmingly positive for individuals is that the number of people who die in transportation-related episodes is substantially smaller than it was in an earlier era.

The best single way to think about the process of financial innovation is as representing a similar process of movement across spaces, spanned not by physical space, but by different states of nature. It seems to me that the overwhelming preponderance of what has taken place has been positive. It is probably true that—as we didn’t use to have transportation safety regulation and we do now—an evolving system does require an evolving regulatory response.

But it seems to me that one needs to be very careful about stressing the negative aspects of the evolution, relative to the positive aspects of the evolution. I was going to make the same point that Don Kohn made about the Japanese financial system and the Scandinavian financial system standing out for the magnitude of damage done and the reliance on vanilla banking, relative to other activities.

Something similar could be said about the history of U.S. business cycles. The history of the business cycles prior to 1970 would place very substantial reliance on problems that came out of the financial sector and the regulation of the financial sector.

I was surprised by the tone of the recommendation around the incentives because it seems that if you take what is the central, most plausible area of concern that is suggested by what takes place in the paper, it is the notion that speculation involves negative feedback over a certain range, then positive feedback once you get outside of that corridor, and that process is very substantially exacerbated by hedge fund phenomena. Indeed, if one looks at the Shleifer-Vishny paper that Mr. Rajan refers to, hedge funds and the behavior induced by hedge funds and hedge fund liquidations are the central example. Yet, hedge funds would be the primary example we have of a financial institution where those who were running it did in fact have, as Raghu Rajan recognized in his comment on Long-Term Capital Management, very substantial wealth that was involved.

While I think the paper is right to warn us of the possibility of positive feedback and the dangers that it can bring about in financial markets, the tendency toward restriction that runs through the tone of the presentation seems to me to be quite problematic. It seems to me to support a wide variety of misguided policy impulses in many countries.

I would say as a final example of what has come out of the discussion for the 1987 crisis is that if those who wish to protect their assets had bought explicit puts rather than portfolio insurance, the situation would have been substantially more stable. That also argues for the benefits of more open and free financial markets, rather than for the concerns they bring.

The Average Is Not the Typical...

Why oh why can't we have a better press corps?

Michael Kinsley writes:

The Least We Can Do: According to a survey from the Federal Reserve Board, the average American household aged 65 to 74 has assets worth more than $1 million. Typically these amounts get spent down as people get older and sicker, so let’s say the second member of the typical couple dies leaving $500,000...

Notice the slippage?

As Steve Heston emails, the 2007 Federal Reserve Survey of Consumer Finances http://www.federalreserve.gov/pubs/bulletin/2009/pdf/scf09.pdf reports that the average wealth of a family with a head 65-74 was $1.015 million in 2007 (it is less now). But the median family with a head 65-74 had $239 thousand--in short, they owned their house and perhaps $100 thousand more.

This matters because MIchael Kinsley is calling for a broad-based low-rate estate tax:

The Least We Can Do: In 2009... the estate tax... up to 45 percent on estates worth more than $3.5 million, and raised only $25 billion—in other words, only a small proportion of the population paid it, but the few who did pay really got socked.

This would not be what I am suggesting here. I am suggesting a tax... [on] anyone who inherits any significant amount of money--but at a much lower rate....

Here is another justification for taxing the money people leave behind when they die.... [F]or years, this couple has been collecting benefits from Social Security and Medicare. These are supposed to be insurance programs. Social Security protects you against the risk of being old and poor.... But if a couple dies leaving assets worth half a million dollars, the risk they were insuring against—poverty in old age--evidently didn’t materialize. The money they received from Social Security... is instead passed along.... Why shouldn’t they give it back? Or some part of it? Social Security sent out checks worth $682 billion last year, so there is real money here...

And Kinsley is under the illusion that the typical American elderly couple has four times the bequeathable wealth that it does.

The art of tax policy is, as Colbert said, to collect the most feathers with the minimum of hissing. And in order to do that you need to know where the feathers are, and how many of them there are.

Jan Hatzius and Paul Krugman

As reported by Ezra Klein:

Will America come to envy Japan's lost decade?:

Jan Haltzius started things off by questioning whether the Federal Reserve would really step up to the plate:

If we talk about what else could be done, I think the Federal Reserve could certainly do more. The question is whether what they'll do will have a substantial effect. It'll have some effect. But the numbers for the total amount of asset purchases really required to move the needle a lot is very large. There's a natural bias towards caution among monetary policymakers in this kind of environment.

So usually what happens is that you're in a liquidity trap and you're at the zero bound and you send the staffers away to try and figure out the optimal policy. They go away and model things and come back with some monstrously large number of the amount that needs to be purchased, and the policymakers say, 'Well, I'm not sure you've properly taken into account all the tail risks of this? How do you account for the tail risk that people will lose confidence?' So then the policymakers take a step back towards caution, and that's why in this kind of situation, stimulus tends to be underprovided compared to what's necessary. I think we'll do quite a lot, but it will still fall short of what we need.

Then Paul Krugman jumped in:

There's a trap, and it's the same thing that happened with fiscal stimulus. You do something in the right direction that's inadequate, and then people say, well, that didn't work, and instead of increasing the dosage and proving it right, you give the thing up altogether.

All of this is very familiar if you studied Japan in the '90s. In fact, we're doing worse than the Japanese did. Our monetary policy is a bit more aggressive, but our fiscal policy has been less aggressive. We have a larger output gap than they did, and we've had a surge in unemployment that they never had, and our political will to act has been exhausted much faster than theirs was. On the current track, we're going to look at Japan's lost decade as a success story compared to us. What we should be doing is a really big dose of stimulus on all of these fronts. Throw the kitchen sink at it. But if you ask me for ways to solve this problem that lives within the constraints of policymakers who don't want to be bold, I don't know that I have an answer for that.

Ezra Klein comments:

So the political system is biased toward caution, which isn't a particularly good bias to have amid a financial crisis that requires massive, unconventional economic policy interventions. But because the policies were too cautious, they don't solve the problem, and that discredits them, which leaves the government without tools and the economy in tatters. It's a bit like taking too few antibiotics, noticing that you're still sick, and swearing off antibiotics altogether.

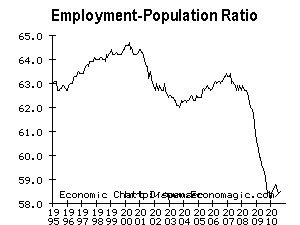

The Output Gap

Ezra Klein sends us to Neil Irwin and Alicia Parlapiano:

Compared with a healthy economy, about 7 million working-age people and 5 percent of the nation’s industrial capacity are sitting idle, not producing what they could. The economy is growing again, but at a rate — less than 2 percent in recent months — that’s too slow to keep up with a population that keeps increasing and workers who keep getting more efficient.

This is the output gap, the divide between the amount the United States can produce and what it is actually producing. The gap, currently $900 billion, explains why we feel so miserable more than a year into what is technically classified as an economic recovery.

October 4, 2010

The Time for Infrastructure Investment Is ASAP

Andrew Samwick:

The Time for Infrastructure Investment Is ASAP | Capital Gains and Games: What Ezra does not say explicitly is that the most opportune time to launch this program of infrastructure investment was when the downturn was first upon us. And at that time, the key task for writers in The Washington Post (and other places)was to argue that a serious infrastructure investment program was a better way to deal with downturns than the other proposals in vogue at the time; namely, something "timely, targeted, and temporary."

But late is better than never. As the proverb goes:

The best time to plant a tree is 20 years ago. The second best time is today.

What is rare about this opportunity is that, unfortunately, it still exists 32 months after we should have started taking advantage of it.

Nick Rowe Wants to Go Back to Our Home Timeline Too...

Hoisted from Comments: Nick Rowe:

Can I Please Go Back to My Home Timeline Now?: I would never have believed it either. It was the one thing I was most wrong on (marking my beliefs to market). Easiest problem in the world to fix, I would have said, and the one that is the most fun to fix. You just get to print money, and spend it on what you want, or give it so someone else to spend on what they want, or lend it to someone to spend on what they want. Like a kid in a candy store with a big wad of cash: the only problem would be trying to choose what to spend it on, and not eating too much so you inflate yourself.

You have to print the "money" in such a way that you don't raise the precautionary demand for "money" by as much "money" as you print, and so it is not quite the easiest problem in the world--especially since we don't really know what is the best kind of "money" to be printing right now.

But, in outline and in general, yes. I still do not believe it.

If Government Were Run Like a Business...

Ezra Klein:

Ezra Klein - Infrastructure: The best deal in the economy: People say that the government should be run more like a business. So imagine you are CEO of the government. Your bridges are crumbling. Your schools are falling apart. Your air traffic control system doesn't even use GPS. The Society of Civil Engineers gave your infrastructure a D grade and estimated that you need to make more than $2 trillion in repairs and upgrades.

Sorry, chief. No one said being CEO was easy.

But there's good news, too. Because of the recession, construction materials are cheap. So, too, is the labor. And your borrowing costs? They've never been lower. That means a dollar of investment today will go much further than it would have five years ago -- or is likely to go five years from now. So what do you do?

If you're thinking like a CEO, the answer is easy: You invest. You get it done. Happily, that's what the administration is proposing to do. But its plan is too modest. The $50 billion bump in infrastructure spending it has proposed is only for surface transportation. The infrastructure bank envisioned in the proposal is also likely to be limited to transportation. And as for our water systems, our schools, our levees? This is not a time for half-measures. It's a rare opportunity to do what we need to do and to save money doing it.

As the Austerians Cry "Fire! Fire!" in Noah's Flood

Calculated Risk:

Calculated Risk: Rates keep falling: 2-Year Treasury Yield Hits Record Low: Just a look at falling treasury yields and mortgage rates... From Reuters: US 2-Year Treasury Yield Hits Record Low

The two-year U.S. Treasury note yield fell to a record low of 0.403 percent on Monday ... the 30-year T-bond rose almost a full point in price to yield 3.676 percent, down 4 bps.

The 10-year yield is down to 2.49% and, according to Freddie Mac (for the week ending Sept 30th): "The 30-year fixed-rate mortgage rate [4.32 percent] dropped to tie the survey’s all-time low and the 15-year fixed-rate [3.75 percent] set another record low." And mortgage rates have probably fallen further over the last week.

Can Ben Bernanke be impeached?

links for 2010-10-04

J. Bradford DeLong's Blog

- J. Bradford DeLong's profile

- 90 followers