The World Model Landscape

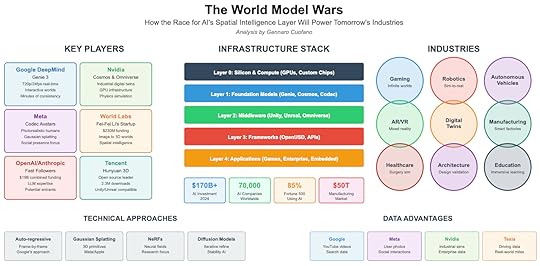

The Next Trillion-Dollar Layer – Tech giants and startups alike are pivoting toward world models — AI that can simulate, predict, and generate 3D, physics-aware environments — positioning them as the foundational infrastructure for AR, robotics, autonomous vehicles, and virtual worlds.Major Players & StrategiesGoogle DeepMind – Genie 3 leads in real-time interactive world generation with long-term consistency and controllable events.Nvidia – Cosmos + Omniverse marry physics-based generation with industrial digital twins, backed by GPU dominance.Meta – Codec Avatars for photorealistic human presence; a social-first foothold in virtual spaces.Microsoft – Enterprise distribution layer, integrating world models via Azure and Microsoft 365.World Labs (Fei-Fei Li) – Single-image-to-3D tech, strong academic credibility, rapid unicorn rise.Tencent – Open-source Hunyuan 3D, compatible with Unity/Unreal, 2.3M+ downloads.Unity & Unreal – Game engine incumbents adding AI-native capabilities.Apple – Silent but investing in spatial computing via Vision Pro and proprietary 3D tech.Technical ApproachesAuto-regressive generation (Google) – strong temporal consistency.Gaussian splatting (Meta/Apple) – efficient 3D rendering.NeRFs – photorealism, but slow rendering.Diffusion models – high controllability, slower for real-time use.Data as the Moat – Scale and quality of spatial data (Google’s YouTube, Tesla’s driving footage, Meta’s social graph, Apple’s LiDAR) will determine who can productionize world models at consumer scale.Early Adoption ZonesGaming – Infinite world generation could cut development costs by 50–70%.Robotics – 10x faster training, 90% less real-world data needed.Autonomous Vehicles – Millions of simulated “edge cases” for safer self-driving.Architecture/Construction – Predictive digital twins reducing costly rework.Manufacturing – Real-time supply chain and factory simulation.Industry StackLayer 0 – Specialized silicon (Nvidia GPUs, custom chips from Meta/Google/Apple).Layer 1 – Foundation models (general-purpose and physics-specialized).Layer 2 – Middleware (Unity, Unreal, Omniverse, Isaac Sim).Layer 3 – Application frameworks (domain-specific languages, OpenUSD standards).Layer 4 – End-user applications (games, industrial control, AR/VR).Timeline2024–2026 – Land grab with proprietary models and VC flood.2026–2028 – Shakeout to a few dominant general models + specialized niches.2028–2030 – Platform wars, ecosystem control, standards battles.2030+ – Invisible infrastructure embedded in every device.Risks & Challenges – Massive compute demands, verification for safety-critical uses, privacy implications of persistent world awareness, creative industry disruption, and authenticity verification in indistinguishable simulated vs real content.Strategic AdviceEnterprises – Audit spatial data, run pilots, build multi-provider relationships.Startups – Focus on niche use cases, tooling, verification, or novel applications; don’t compete on foundation models.Investors – Bet across the stack, prioritize unique data ownership and sustainable compute economics.Societal Impact – Education, accessibility, science, and cultural preservation could leap forward. Risks of reality preference inversion, liability in predictive errors, and deepening simulation dependence loom.Core Insight – World models will be to the next era of computing what the internet was to information and mobile to communication. Whoever wins will control how humanity interacts with, predicts, and creates reality itself. Second place may be irrelevant.

The Next Trillion-Dollar Layer – Tech giants and startups alike are pivoting toward world models — AI that can simulate, predict, and generate 3D, physics-aware environments — positioning them as the foundational infrastructure for AR, robotics, autonomous vehicles, and virtual worlds.Major Players & StrategiesGoogle DeepMind – Genie 3 leads in real-time interactive world generation with long-term consistency and controllable events.Nvidia – Cosmos + Omniverse marry physics-based generation with industrial digital twins, backed by GPU dominance.Meta – Codec Avatars for photorealistic human presence; a social-first foothold in virtual spaces.Microsoft – Enterprise distribution layer, integrating world models via Azure and Microsoft 365.World Labs (Fei-Fei Li) – Single-image-to-3D tech, strong academic credibility, rapid unicorn rise.Tencent – Open-source Hunyuan 3D, compatible with Unity/Unreal, 2.3M+ downloads.Unity & Unreal – Game engine incumbents adding AI-native capabilities.Apple – Silent but investing in spatial computing via Vision Pro and proprietary 3D tech.Technical ApproachesAuto-regressive generation (Google) – strong temporal consistency.Gaussian splatting (Meta/Apple) – efficient 3D rendering.NeRFs – photorealism, but slow rendering.Diffusion models – high controllability, slower for real-time use.Data as the Moat – Scale and quality of spatial data (Google’s YouTube, Tesla’s driving footage, Meta’s social graph, Apple’s LiDAR) will determine who can productionize world models at consumer scale.Early Adoption ZonesGaming – Infinite world generation could cut development costs by 50–70%.Robotics – 10x faster training, 90% less real-world data needed.Autonomous Vehicles – Millions of simulated “edge cases” for safer self-driving.Architecture/Construction – Predictive digital twins reducing costly rework.Manufacturing – Real-time supply chain and factory simulation.Industry StackLayer 0 – Specialized silicon (Nvidia GPUs, custom chips from Meta/Google/Apple).Layer 1 – Foundation models (general-purpose and physics-specialized).Layer 2 – Middleware (Unity, Unreal, Omniverse, Isaac Sim).Layer 3 – Application frameworks (domain-specific languages, OpenUSD standards).Layer 4 – End-user applications (games, industrial control, AR/VR).Timeline2024–2026 – Land grab with proprietary models and VC flood.2026–2028 – Shakeout to a few dominant general models + specialized niches.2028–2030 – Platform wars, ecosystem control, standards battles.2030+ – Invisible infrastructure embedded in every device.Risks & Challenges – Massive compute demands, verification for safety-critical uses, privacy implications of persistent world awareness, creative industry disruption, and authenticity verification in indistinguishable simulated vs real content.Strategic AdviceEnterprises – Audit spatial data, run pilots, build multi-provider relationships.Startups – Focus on niche use cases, tooling, verification, or novel applications; don’t compete on foundation models.Investors – Bet across the stack, prioritize unique data ownership and sustainable compute economics.Societal Impact – Education, accessibility, science, and cultural preservation could leap forward. Risks of reality preference inversion, liability in predictive errors, and deepening simulation dependence loom.Core Insight – World models will be to the next era of computing what the internet was to information and mobile to communication. Whoever wins will control how humanity interacts with, predicts, and creates reality itself. Second place may be irrelevant.

The post The World Model Landscape appeared first on FourWeekMBA.

No comments have been added yet.