Jonathan Clements's Blog, page 381

November 23, 2018

We’re Stuffed

THERE’S A RETAIL chain called The Container Store. As the name implies, it sells all types of containers, storage units and custom closets to help people organize their stuff, much of which they likely don’t need.

Let’s say you want a separate plastic box for each pair of shoes. You can have it. Did you know men own an average 12 pairs of shoes and women an average 27 pairs? Amazingly, 85% of women own shoes they purchased but have never worn.

We own too much stuff. I was speaking with a cable installer recently. He told me he had just finished hooking up 11 televisions in one home. The average home has 2.3 televisions, which is actually declining, as younger people instead stream on other devices.

Don’t think you have too much stuff? Try moving out of your home of many years and cleaning out your closets—which we just did. My wife found five boxes of shoes she didn’t recall she had and which she had never worn. Even I found two boxes of unworn shoes—but I’m innocent, because my wife bought them for me.

The problem with all the stuff we have is that somewhere along the line we likely spent good money on it. That means we couldn’t use that money for something else—like savings or paying down debt.

In an Experian survey, 68% of respondents said a key reason they carry credit cards is to buy the things they need. It’s the “need” part that is debatable. The majority of respondents (62%) reported having one to five credit cards, with three being the average. Their credit card debt averaged $2,326.71, with an average monthly charge of $779.83.

Americans paid banks some $104 billion in credit-card interest and fees in the last year, up 11% from a year ago and 35% over the past five years. Apparently, the frugality brought on by the Great Recession has waned. Being somewhat of a nerd, I calculated that if just one year of interest payments were instead invested, after 40 years, Americans could have $1,069,714,665,461 in the bank, assuming a 6% return. The last time I heard that kind of number it was the federal deficit.

How do we use our credit cards? Up to 27 million U.S. adults report putting medical expenses on their credit cards, according to a NerdWallet analysis, costing them an average of $471 in interest for a year’s worth of out-of-pocket medical spending. That’s more than $12 billion total. Paying for personal emergency medical expenses ranked sixth among the reasons folks cited for ending up with credit card debit.

What was the top reason? Survey respondents put the blame on themselves, saying they spent more than they could afford on unnecessary purchases. Once you live that way, maybe it’s no great surprise you also end up charging those out-of-pocket health care costs.

And then, of course, there are the shoes. I tried looking up the price of an average pair of women’s shoes. Good luck with that. Let’s just say the cost of 27 pairs of shoes likely exceeds average out-of-pocket health care expenses.

Our penchant for accumulating stuff may be our undoing down the road—and I haven’t even included the cost of those containers we buy to store what we don’t need and don’t recall owning. Except for the chronically poor, everyone can afford to save if they simply decide what stuff they can live without—provided they decide before they actually buy it.

Richard Quinn blogs at QuinnsCommentary.com. Before retiring in 2010, Dick was a compensation and benefits executive. His previous blogs include Clueless, Hard Earned and Time to Choose. Follow Dick on Twitter @QuinnsComments.

The post We’re Stuffed appeared first on HumbleDollar.

November 22, 2018

Signed and Sealed

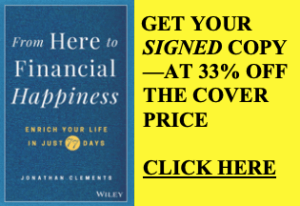

WANT A COPY of From Here to Financial Happiness signed by yours truly? It might make for an enriching holiday gift for a friend or family member—or perhaps for yourself.

Just follow this simple four-step process:

Shoot an email to Jonathan(at)JonathanClements.com specifying how many

copies you want and what mailing address they should be sent to. We can’t ship books to addresses outside the U.S.—sorry.

copies you want and what mailing address they should be sent to. We can’t ship books to addresses outside the U.S.—sorry.You’ll receive an invoice from PayPal asking for $20 per copy. That $20, which covers the book, shipping and handling, is 33% off the cover price.

Pay the invoice using a credit card, debit card or PayPal. You don’t need a PayPal account to purchase books. Your copies will be shipped once your invoice is paid.

If you want copies for Christmas, please pay your invoice by Dec. 1. Unfortunately, at this juncture, I can’t promise delivery by Hanukkah.

The post Signed and Sealed appeared first on HumbleDollar.

November 21, 2018

Good Old Days

SAY “1040” and most of us think of the income tax returns we file each year on April 15. But it’s only because of chance that we fill out 1040s, instead of 1039s or 1041s: That number was up next in the sequential numbering of forms developed by the Bureau of Internal Revenue, the predecessor of today’s IRS.

It all began on Jan. 5, 1914, when the Department of the Treasury unveiled the new Form 1040 for tax year 1913. The feds set March 1, 1914—less than two months away—as the deadline for filing the form with the local tax collector’s office.

Today’s 1040 differs completely from 1913’s. Let’s focus first on tax brackets: 1913’s brackets began at 1% on taxable income of up to $50,000. The next ones were: 2% on income between $50,000 and $75,000; 3% on income between $75,000 and $100,000; 4% on income between $100,000 and $250,000; 5% on income between $250,000 and $500,000; and a top rate of 6% on income above $500,000. Contrast 1913’s comparatively miniscule rates with those set by last year’s Tax Cuts and Jobs Act (TCJA): 10%, 12%, 22%, 24%, 32%, 35% and 37%.

The first 1040 was just four pages. Page No. 1 summarized your income and deductions, and was where you computed your income tax (eight lines). The second page listed the details of your income (12 lines). The third page listed your deductions (seven lines). What was the fourth page? It provided instructions—all on a single page.

Page three’s list of deductions was skimpy, compared to today’s sumptuous array of write-offs. It included a deduction of $3,000 for single taxpayers and $4,000 for married couples. While spouses could file joint or separate returns, in no case could their combined deductions be more than $4,000. (So yes, the marriage penalty—which has been mostly erased—dates back to the first modern return.) The $3,000/$4,000 write-off alone was sufficient to relieve the vast majority of Americans of the need to pay income taxes.

Other authorized deductions included:

Personal interest paid (a deduction almost completely deep-sixed by the Tax Reform Act of 1986)

Uninsured losses from “fires, storms, or shipwreck” (mostly abolished by TCJA; unsurprisingly, no mention of plane crashes)

Business losses (TCJA ended carrybacks for net operating losses and allows only carryforwards)

All other taxes paid, including real estate taxes (capped by TCJA at $10,000 for those itemizing their deductions)

Bad debts

Reasonable depreciation of business property (“reasonable” was replaced long ago by numbingly complex rules explaining how to calculate depreciation write-offs for buildings and equipment)

What remained to be done after taxpayers filled out their forms? In 1914, they had to sign “under oath or affirmation” before “any officer authorized by law to administer oaths.” Nowadays, we simply sign.

Back then, taxpayers filed just over 350,000 1040s. IRS sleuths audited 100% of tax returns. Today, an underfunded IRS is understaffed—and your chances of being audited are slim.

J ulian Block writes and practices law in Larchmont, New York, and was formerly with the IRS as a special agent (criminal investigator). His previous blogs include Two’s a Crowd, Stepping Up and Give and Receive. Information about his books is available at JulianBlockTaxExpert.com. Follow Julian on Twitter @BlockJulian.

The post Good Old Days appeared first on HumbleDollar.

November 20, 2018

A Little Perspective

TODAY WAS PAINFUL. How painful? Think of the financial losses:

Homeowners who closed on their house sale might have lost as much as 6% of the proceeds to real-estate commissions.

Car buyers who picked up their new vehicle probably gave up more than 10% of the purchase price just by driving off the dealership lot.

Those who signed separation agreements with their soon-to-be-ex spouse likely surrendered 50%.

Investors who bought load funds might have been nicked for 5.75%.

Employees who got their paycheck were dunned 7.65% for payroll taxes, maybe 12% for federal income taxes and perhaps 3% for state income taxes.

Those who then spent their paycheck might have lost another 5% to sales taxes. And if the money they spent was $100 in cash withdrawn from an out-of-network ATM, they could have lost another $3 to bank fees, or 3%.

Oh yeah, the S&P 500 also slipped 1.82%. Thank goodness for small losses.

Follow Jonathan on Twitter @ClementsMoney and on Facebook . His most recent articles include Simple Isn’t Easy, Fanning the Flames and Just Asking.

The post A Little Perspective appeared first on HumbleDollar.

Money Date Night

IN AN EFFORT to understand each other’s financial background, my fiancée and I began holding a money date night. These finance-focused conversations started out slowly. But they’ve become our way to talk about money and our future together.

As a financial planner, I don’t want to dominate the financial side of our lives. I believe household finances should be managed together and not individually. We view this date night as an opportunity to learn about our individual feelings toward money and what our goals are. Having a chance to voice our beliefs around this sensitive topic has brought us closer together.

Want to try it yourself? A money date night might sound like a tedious, painful experience. But done right, it can be a fun and engaging way to connect with your partner or spouse.

It’s important for both partners to have an idea of the family’s finances—not least because misunderstandings over money are among the most common reasons for divorce. What does a money date night look like? This isn’t meant to be a full-on financial planning session. Instead, the conversation should remain light. There will be a review of the family’s financial goals, the previous month’s spending and a look at any upcoming out-of-the-ordinary expenses.

Before the money date begins, update the family balance sheet—the list of all your assets and debts—and pull together a cash flow statement showing how much income you receive each month and where it goes. This should be done beforehand, so you don’t waste time that could be spent talking.

To start the money date, grab your beverage of choice. Find a comfortable spot to sit, where you can have an uninterrupted discussion. This would also be a good moment to put phones in another room and turn the television off.

Your family’s financial goals are a great way to open the conversation. This is a chance to discuss any dreams or ambitions you’ve had recently. To avoid getting too deep in the weeds, stick to the top three goals—and make them as specific as possible. Some examples:

Contribute the maximum allowable amount to your retirement accounts.

Donate 10% of gross income to charitable causes or a donor advised fund.

Reduce eating out so you can contribute more to your annual travel fund.

A review of last month’s financials should be discussed next. Did you spend less than you made? What expenses surprised you? How much money did you put in investment accounts? This should be viewed as an opportunity for both parties to get on the same page, especially if one partner handles the family’s finances.

Finally, talk about the irregular expenses you see on the horizon, such as vehicle maintenance, weddings to attend, medical procedures and home remodeling projects. What can you do today to budget for these pending financial needs? You might set up an automatic monthly transfer from your checking account to a designated savings account, so you have cash to handle these unexpected costs.

How often should you have a money date night? I favor doing them monthly—or quarterly at a minimum. If you do it any less often, the family’s finances may get off track—and there’s a greater risk of financial misunderstandings.

Ross Menke is a certified financial planner and the founder of Lyndale Financial, a fee-only financial planning firm in Nashville, Tennessee. He strives to provide clear, concise advice, so his clients can achieve their life goals. His previous blogs include Slow Going and Flying Solo. Follow Ross on Twitter @RossVMenke.

The post Money Date Night appeared first on HumbleDollar.

November 19, 2018

Heading Home (IV)

DURING THE FIRST three weeks of house hunting, I looked at a dozen different properties. None met all the criteria I’d set for my “ideal” home, but a couple came close. My price point of $380,000 limited me to looking at smaller, starter-type homes. The competition for those houses was often fierce. On at least three occasions, a home I wanted to view would appear as a “new listing” one day and be marked as “pending sale” the next.

I became obsessed with checking Zillow every few hours. One Wednesday morning, I awoke to find a listing that was just 10 minutes old. It was a small house in the neighborhood I was hoping to live in and had an asking price of $370,000. I contacted my agent and asked if we could schedule a viewing for later that same day.

When I saw the house a few hours later, I knew it was the one I wanted to buy. It was a single-level, 1,100 square foot house located at the end of a long private driveway. The setting was quiet and private, and the house had been owned by just one person since being built in the late 1980s.

I spent two hours looking at every square inch of the house and yard. There was a perfect area for the dogs. There were three bedrooms, two bathrooms and an oversized double-car garage. While some parts of the house were clearly stuck in the ‘80s, many areas had been updated. It was a house I could move into without having to do any major renovations. Best of all, it was located just six blocks from where my mother lived. I told my agent I wanted to make an offer that day.

Knowing how quickly homes were selling, deciding on a price to offer wasn’t easy. My agent suggested offering $375,000, the value of the home listed on the property tax assessment. Because I was currently renting an apartment, I didn’t have any contingencies in my offer. I could close at any time and I could come up with the money for the down payment quickly. I submitted my offer, along with a $4,000 earnest money check, and crossed my fingers.

The seller wanted 48 hours to review offers. In the end, three other potential buyers also submitted bids on the house, but it was mine that was ultimately accepted. I was overjoyed to have found a house that not only exceeded my expectations, but also didn’t go over the budget I’d established.

The next two weeks were filled with home inspections, radon tests and paperwork. I was able to secure all the funds for my down payment easily and my loan paperwork was wrapped up within two weeks of making the offer. With a closing date still five weeks out, I had plenty of time to second-guess my decision and wrestle with the long-term financial implications of becoming a homeowner once again. But deep down, I knew I’d made the right choice.

Kristine Hayes is a departmental manager at a small, liberal arts college. This is the fourth in a series of articles about her recent home purchase. The previous installments were Heading Home (I), Heading Home (II) and Heading Home (III).

The post Heading Home (IV) appeared first on HumbleDollar.

November 18, 2018

Deadly Serious

THE MUSICIAN PRINCE died in 2016 at age 57, leaving behind a legacy of musical genius. Unfortunately, he also left behind an ongoing legal and financial mess. The issue: For reasons no one understands, Prince neglected to prepare even the most basic estate plan, leaving potential heirs squabbling over his fortune.

Under the latest tax law, passed late last year, only those with more than $11.2 million in assets ($22.4 million for a married couple) are subject to federal estate taxes. Still, you don’t have to be a wealthy rock star to need an estate plan. I believe every adult—regardless of net worth—should have at least a basic plan. Here are 10 reasons:

1. State estate taxes. Even if your estate won’t top the $11.2 million federal threshold, your state might impose its own estate tax. Eighteen states, in fact, have some type of estate or inheritance tax. In some states, the limit is harmonized with the federal limit, meaning that you would only face a state-level tax if your estate met the federal threshold. But in many states, the limit is far lower. In Massachusetts, for example, it’s just $1 million.

2. An ever-changing tax regime. While today’s $11.2 million federal estate tax exemption is extremely generous, there’s no guarantee this generosity will last. While estate tax revenue is virtually meaningless to the federal budget, it’s politically symbolic and has seen frequent changes. As recently as 2000, the limit was less than $1 million and the top rate was a hefty 55%, compared with today’s 40%. In 2010, on the other hand, there was no estate tax at all. The lesson: Don’t conclude that today’s estate tax regime is the one that will apply to you.

3. Naming a guardian. Should something happen to both you and your spouse, perhaps the single most important function of an estate plan is the appointing of a guardian for your children. This is even more critical if you’re a single parent. While your loved ones may have the best of intentions, it isn’t unusual for custody disagreements to arise when parents pass away.

Should children live with their grandparents or perhaps with an aunt or uncle? Should priority be given to those who live locally? To those who share your values? To those in a more comfortable position financially? It’s unlikely that everyone will see it the same way. That’s why it’s so important to document your preference.

4. Choosing a health care proxy. Another critical function of an estate plan is to name a health care proxy. If you were to become incapacitated, a written health care proxy would ensure that a designated loved one would have authority to make medical decisions on your behalf. This need not be complicated—in fact, free proxy forms are available on the internet—but it is important. If you became incapacitated, that would be bad enough. You certainly wouldn’t want your family sparring with each other, or with hospital staff, as a result.

5. Picking an executor. The executor’s role is largely administrative and often falls to the spouse or a child. If you have children from more than one marriage, however, you should consider appointing an impartial executor—one who does not have a stake in the outcome. While this impartial individual will need to be paid, it’ll be well worth the cost if that impartiality helps your heirs avoid a costly dispute.

6. Ensuring equity among children. If you died without a will, a court would probably divide your assets equally among your children. But that may not make the most sense. Suppose your children are in different situations financially. Should everyone receive equal shares? The answer, of course, is that it depends. But since you’re in the best position to make that determination, take the time now to think it through.

7. Charitable intentions. If you have substantial assets, perhaps you wouldn’t want everything to go to your children. Maybe there are charities, religious organizations or educational institutions that are important to your legacy. If you don’t put it on paper, no one will ever know.

8. Personal possessions. If you’re like most people, you have items of sentimental value—jewelry, for example. Wouldn’t you want some say over how these items are allocated?

Vacation homes are similarly tricky, often holding great sentimental value for children. But how would they share a home among themselves? How would they share the maintenance costs, especially if they are in different positions financially? What if one of your children wanted to sell the house and one wanted to hold it? A thoughtful estate plan would include mechanisms to handle these questions amicably.

9. Cost savings. In Prince’s case, it’s been more than two years and none of his heirs has received a penny. In the meantime, because it’s such a tangled mess, attorneys and other advisors have collected nearly $6 million in fees. No question, this is an unusual case. But the point remains: It’s hard enough to suffer a loss. Don’t compound that pain by leaving your family guessing about—and possibly fighting over—what you would have wanted.

10. Creditor protection. In the event one of your children has a legal dispute, a well-written estate plan could help protect your assets from that child’s creditors. If he or she gets divorced, for example, a trust structure could ensure that more of your assets stay with your child.

Adam M. Grossman’s previous blogs include Five Messy Steps, Hole Story and Seeking Zero . Adam is the founder of Mayport Wealth Management , a fixed-fee financial planning firm in Boston. He’s an advocate of evidence-based investing and is on a mission to lower the cost of investment advice for consumers. Follow Adam on Twitter @AdamMGrossman .

The post Deadly Serious appeared first on HumbleDollar.

November 17, 2018

Simple Isn’t Easy

ALLAN ROTH likes to describe himself as argumentative—and, on that score, it’s hard to argue with him. But it’s also hard to argue with the points he makes, because he has this nasty habit of being right.

Roth is the author of How a Second Grader Beats Wall Street, a financial planner who charges by the hour, and a contributor of financial articles to AARP.org, Financial-Planning.com, NextAvenue.org and other sites. I caught up with him last month at the Bogleheads’ conference in Philadelphia. Here are just some of his trenchant comments:

On financial advisors. “Every time a dollar changes hands, there’s a conflict,” Roth contends. That’s clear with commission-charging brokers and insurance agents, who have an incentive to get customers to trade and to buy products that generate the highest commissions.

But as Roth notes, fee-only advisors are also conflicted. If they’re charging, say, 1% of a client’s portfolio, they may advise against paying down debt, because that would reduce the size of the portfolio they manage. They may also advocate complicated strategies simply to justify their own fee. Even hourly advisors, like Roth, have an incentive to string things out, so they can bill for more hours.

On simplicity. “There are so many forces pushing us toward complexity,” he says. It isn’t just advisors looking to justify their fee. Anxious to get published, academics are constantly trying to uncover new factors that explain market returns. Seduced and bullied by yo-yoing markets, investors are forever making portfolio changes.

Roth, by contrast, favors buying and holding a simple three-fund investment mix—a total stock market index fund, a total international stock index fund and a total bond market index fund. But as he points out, “How could an advisor charge even 0.3% to put you in one or three funds, and keep charging you every year to stay the course?”

On active investors. “I love active investors,” Roth says. “I owe my financial future to Jack Bogle—but I also owe it to active investors, because they keep markets efficient.”

On investor behavior. “Minimize expenses and emotions, maximize diversification and discipline” is Roth’s succinct formula for investment success. “It’s easy to say. It’s a lot harder to do.”

He continues: “Indexing is fine for controlling costs. But you can panic just as easily with a broad market index fund as any other investment.” Roth allows that even he had moments of doubt in early 2009, as share prices plunged toward their bear market lows.

“Humans are predictably irrational,” he says. “When stocks drop, I can tell you that people—including financial advisors—will panic. That creates an opportunity for those who can go against the herd.” One way to make money: Regularly rebalance your portfolio, both between stocks and more conservative investments, and within these asset classes. That’ll help you to buy low and sell high.

On the role of bonds. “The purpose of fixed income has never been income,” Roth opines. “The purpose of fixed income is to keep up with inflation and taxes, and to be the stable portion of a portfolio. It’s the shock absorber. It allows you to buy stocks when stocks plunge.”

While many investors are disenchanted with today’s low bond yields, Roth argues they’re better off today than they were in the early 1980s, when high-quality bonds offered double-digit yields. “People may feel better earning a 10% yield when inflation is 12%,” he says. “But they’re better off today earning 3% if inflation is only 2%—and that’s especially true after taxes.”

While many investors are disenchanted with today’s low bond yields, Roth argues they’re better off today than they were in the early 1980s, when high-quality bonds offered double-digit yields. “People may feel better earning a 10% yield when inflation is 12%,” he says. “But they’re better off today earning 3% if inflation is only 2%—and that’s especially true after taxes.”

Despite that, many investors today are shunning high-quality bonds and instead chasing yield with master limited partnerships, high-yield junk bonds and high dividend stocks. “We have such short memories,” he says. “The stuff that blew up in 2008 is the stuff people are now moving toward.”

On dividends. Investors today are disgruntled with not only bond yields, but also stock dividends. But Roth contends that yields are far higher than many investors realize—thanks to stock buybacks. He concedes that corporations buy back their stock “for all the wrong reasons and at the wrong time.”

Still, he says that the true yield on U.S. stocks today may be 4½%, comprised of a 2% cash yield and perhaps 2½% in annual share buybacks. Like a cash dividend, the latter represents money returned to shareholders, who benefit from the shrinking number of shares outstanding.

But what if you want more than 2% in cash from your portfolio each year? Easy, Roth says. Just do a little selling: “It’s more tax-efficient to buy the total market index fund and sell 2½% every year than to buy a high dividend fund.”

The reason: While 100% of a dividend is taxable, less than 100% of a realized capital gain will be taxed, because you’ll have some sort of cost basis on the shares. Moreover, not all dividends qualify for favorable tax treatment (though that’s also true for short-term capital gains). On top of that, you have to pay taxes on your dividends every year, but you can control when you sell your shares—and, in some years, you might choose not to sell, thus sidestepping the capital-gains tax bill.

Follow Jonathan on Twitter @ClementsMoney and on Facebook . His most recent articles include Fanning the Flames, Just Asking, Warning Shot and Ignore the Signs.

The post Simple Isn’t Easy appeared first on HumbleDollar.

November 16, 2018

Pillow Talk

WHAT’S IT LIKE to be married to a personal finance expert? Trust me, it isn’t easy—especially if you’re a fiercely independent but less-than-perfect manager of your own money.

Before I met Jonathan, I was a divorcee who hadn’t shared her financial life with anybody for a few years, but who had been bumbling along just fine on her own. When we started dating, we hardly ever spoke about money. The most he knew about my spending habits was that I was very good at justifying purchases, proudly telling him about my latest bargain. I’m a T.J. Maxx-and-thrift-shop kind of person, so that must have reassured him.

Nonetheless, he probably noticed that I visited those outlets perhaps a bit too often. This did not deter him from marrying me. He knew the basics: I wasn’t in debt, my credit score was excellent, and I had been smart and lucky in real estate.

What was in store for us, a couple who were slightly mismatched in the personal finance department? At the beginning of our relationship, I avoided asking for financial advice. That just seemed off limits. I heard him extoll the virtues of various behaviors from time to time, which I’d quietly absorb. I decided to follow his advice about opening a Roth IRA, but didn’t consult him or tell him about it. I just didn’t want our relationship to involve money.

About a year later, I confessed to opening a Roth IRA with Scottrade (now part of TD Ameritrade). He asked me how it was performing. I let him look at the account statement—a huge step for me—and he noted with bemusement that the $1,000 I’d contributed was still sitting in a money market fund and had never been invested. I was embarrassed and followed his advice to roll the Roth over to Fidelity Investments, where my other retirement accounts were. It has since grown and I’m sheepishly grateful.

Once we were married, I opened up a little more, and let him change my investment choices and occasionally rebalance my portfolio. I had total faith in him, of course, but felt a little loss of control. Perhaps sensing my desire to keep our finances separate and private, he didn’t query me very often on how I was doing. All the while, I knew deep down that there was so much I could learn from him, but I wasn’t quite ready.

We’ve now been married for more than four years and have had a few more in-depth conversations about finances, including where we want to live upon retirement, whether we’re on track as a couple, our individual career decisions and how they’ll affect our financial lives, and various ways to cut household spending.

I still rarely ask him for advice, but I think some of his lessons are beginning to sink in. I’m trying to turn myself into a saver, rather than a spender. It isn’t easy, but it is exciting to feel it’s within reach. One of Jonathan’s favorite pieces of advice has begun to stick: “If you have an overwhelming urge to buy something you don’t need, walk out of the store for 10 minutes and see if the moment passes.”

I’m not yet Ms. Thrifty. But I also no longer feel I need to keep my finances to myself—and I realize that, over time, I may adopt some better habits. I think that was my hope all along.

Lucinda Karter is a literary agent in New York. Her previous blog was Closet Saver. She’s a fan of Pilates, tennis and Jonathan Clements—but she has to say that, because she’s married to him. Follow Lucinda on Twitter @LucindaKarter.

The post Pillow Talk appeared first on HumbleDollar.

November 15, 2018

Taking Their Money

“UNCLE” PHAN, my father’s closest friend and my godfather, committed suicide a few years ago. I regret not seeing him often enough when he was alive and not letting him know how much I appreciated his humor and generosity.

I also regret not knowing his financial and emotional situation.

Uncle Phan retired as a surgeon 20 years ago and took a lump sum distribution instead of a lifetime monthly pension. It should have been enough to last the rest of his life, but he became a victim of financial scams by close relatives and supposed friends. He also suffered depression and it all proved too much for him. At the time of this death, Uncle Phan was penniless and living alone in a small shack.

Earlier this year, my father had a stroke that forced him to shutter his own medical practice. Working with my brothers, we went through his financial records, as we wound down the business. We discovered that he, too, was a victim of financial scams and exploitations that had been going on for years. He had been paying out large sums to current and former employees, each with a sob story of need, including his assistant to whom he had been a mentor.

My father had always been a diligent saver and careful spending. Maybe that’s why we didn’t notice for so long. He was the one who taught his four children to favor saving over thoughtless spending. Yet, in his later years, here he was doling out large sums without thorough recordkeeping and, worse still, without regard to preserving the savings he and my mother needed for the rest of their lives.

Luckily, my parents had a financial backup, in the form of a monthly pension my father continues to receive. My mother also has her own savings from the medical clinic.

Through these experiences, I’ve learned some unfortunate truths:

Studies show that, as we age, our brain becomes less able to detect fraud. Changes occur in the region of the brain that helps us decide whether or not to trust someone.

A majority of financial exploitation is carried out by people the victim knows.

One study found that financial literacy declines by about 2% every year after age 60. Confidence in financial decision making, however, doesn’t decline with age. That combination—reduced ability but continued confidence—helps explain poor financial decisions by older adults.

My father’s and Uncle Phan’s financial decision making had been deteriorating for years. That made them easy targets for their abusers. Perhaps those who took their money weren’t even aware they were asking for money from people with a diminished capacity. I now see that it can happen to anyone, in any family.

In my father’s case, two things helped to lessen the impact of the money squandering. First, while Phan took his pension as a lump sum, my father took his as a lifetime monthly pension. He could only give away what he had on hand, so the financial damage was limited to his past monthly pension payments, while his future distributions remained protected.

Second, while Phan had no children to safeguard him, we were able to catch my father’s spending habits before he made himself and my mother destitute. In the end, there’s no substitute for a family support system.

These experiences have caused me to take precautions now to protect my and my husband’s retirement savings. While we currently manage our own portfolio, I’ve laid out three steps to implement in the next five years:

We’ll arrange to have our money managed by either a low-cost financial company, such as Vanguard Group, or a fee-only financial advisor.

We will build on our already good communication with our adult sons. Today, they have a list of all our financial accounts, in case something happens to us. In future, I want to make sure they are kept apprised of our financial status on an ongoing basis.

We’ll include both our sons in the discussions we will have with our financial advisor, especially when we review our assets and how our annual withdrawals are impacting our portfolio’s likely longevity.

Jiab Wasserman recently retired at age 53 from her job as a financial analyst at a large bank. She and her husband, a retired high school teacher, currently live in Granada, Spain, and blog about financial and other aspects of retirement—as well as about relocating to another country—at YourThirdLife.com . Her previous blog for HumbleDollar were Why Wait and Won in Translation.

The post Taking Their Money appeared first on HumbleDollar.