Jonathan Clements's Blog, page 234

January 25, 2022

Still Stretching

THE SECURE ACT, which took effect Jan. 1, 2020, made inheriting an IRA even more complicated. Before 2020, beneficiaries typically had the option of taking distributions from an inherited IRA over their lifetime, potentially squeezing many more years of tax-favored growth from these accounts.

The SECURE Act drew a new line, eliminating some beneficiaries��� ability to make use of the so-called stretch IRA. Beneficiaries now are divided into two groups. Some have to empty an inherited IRA within 10 years of the original owner���s death. Others are permitted to stretch out their withdrawals for longer, often over their estimated lifetimes.

I want to focus on this second group���called eligible designated beneficiaries���who can still defer taxable distributions for longer than 10 years. It includes more people than you might think. Under the SECURE Act, eligible designated beneficiaries include:

Surviving spouses

Disabled individuals

Chronically ill individuals

Minor children of the IRA owner

Individuals who are less than 10 years younger than the IRA owner.

Surviving spouses continue to have the most flexibility because they���re allowed either to roll over an inherited IRA into their own IRA account, and potentially delay all withdrawals until age 72, or to leave the money in the inherited IRA. The key advantage: Spouses have the flexibility to either stretch withdrawals over their own life expectancy or over the deceased account holder���s ���life expectancy,��� as calculated by the IRS, which could be beneficial if that happens to be longer.

Disabled and chronically ill individuals can also stretch withdrawals over either their life expectancy or the remaining life expectancy of the deceased. Unlike a spouse, however, they aren���t allowed to roll over the IRA into their own account. Instead, they must use an inherited IRA account to shelter assets until they���re withdrawn.

Minor children of the IRA owner���but not grandchildren���can stretch their withdrawals, but not for a lifetime. Their 10-year withdrawal clock starts when they reach the age of majority���which differs by state���or as late as age 26 if they���re completing their education.

Beneficiaries who are less than 10 years younger than the IRA owner can still take advantage of lifetime withdrawals. This is where it gets interesting. The ���less than 10 years younger��� rule happens to include any beneficiary who is older than the account owner. This means older siblings, friends or domestic partners could be entitled to stretch their IRA withdrawals over their own life expectancy.

I���ve found this aspect of the law isn���t yet widely understood. For instance, I just completed a continuing education course on the new rules for IRAs that incorrectly stated that parents and grandparents don���t qualify for lifetime distributions. They all would qualify because, presumably, they���d all be older than the original IRA owner.

Applying the same rule, cohabiting adults who are within 10 years of the deceased's age also qualify for the stretch rules. The surviving adult would be able to take lifetime withdrawals if listed as the IRA���s sole beneficiary.

The new rules also apply to Roth IRAs, but with one additional condition, which concerns the five-year rule. If the Roth account was established less than five years before the account owner���s passing, the beneficiary must wait to withdraw assets until that requirement is met to ensure the withdrawals are tax-free. This is one more reason to establish Roth IRAs as early as possible.

Who loses out under the SECURE Act? Younger beneficiaries, such as the grandchildren of IRA owners. Before 2020, they might have stretched inherited IRA withdrawals over six or seven decades, allowing the account to enjoy enormous compound growth. Now, their inheritance must be withdrawn from the sheltering arms of an IRA in no more than 10 years. Under the new rules of the game, our grandparents are welcome to take a stretch, but not our more limber grandchildren.

James McGlynn, CFA, RICP, is chief executive of

Next Quarter Century LLC

��in Fort Worth, Texas, a firm focused on helping clients make smarter decisions about long-term-care insurance, Social Security and other retirement planning issues. He was a mutual fund manager for 30 years. James is the author of��

Retirement Planning Tips for Baby Boomers

. Check out his earlier articles.

James McGlynn, CFA, RICP, is chief executive of

Next Quarter Century LLC

��in Fort Worth, Texas, a firm focused on helping clients make smarter decisions about long-term-care insurance, Social Security and other retirement planning issues. He was a mutual fund manager for 30 years. James is the author of��

Retirement Planning Tips for Baby Boomers

. Check out his earlier articles.

The SECURE Act drew a new line, eliminating some beneficiaries��� ability to make use of the so-called stretch IRA. Beneficiaries now are divided into two groups. Some have to empty an inherited IRA within 10 years of the original owner���s death. Others are permitted to stretch out their withdrawals for longer, often over their estimated lifetimes.

I want to focus on this second group���called eligible designated beneficiaries���who can still defer taxable distributions for longer than 10 years. It includes more people than you might think. Under the SECURE Act, eligible designated beneficiaries include:

Surviving spouses

Disabled individuals

Chronically ill individuals

Minor children of the IRA owner

Individuals who are less than 10 years younger than the IRA owner.

Surviving spouses continue to have the most flexibility because they���re allowed either to roll over an inherited IRA into their own IRA account, and potentially delay all withdrawals until age 72, or to leave the money in the inherited IRA. The key advantage: Spouses have the flexibility to either stretch withdrawals over their own life expectancy or over the deceased account holder���s ���life expectancy,��� as calculated by the IRS, which could be beneficial if that happens to be longer.

Disabled and chronically ill individuals can also stretch withdrawals over either their life expectancy or the remaining life expectancy of the deceased. Unlike a spouse, however, they aren���t allowed to roll over the IRA into their own account. Instead, they must use an inherited IRA account to shelter assets until they���re withdrawn.

Minor children of the IRA owner���but not grandchildren���can stretch their withdrawals, but not for a lifetime. Their 10-year withdrawal clock starts when they reach the age of majority���which differs by state���or as late as age 26 if they���re completing their education.

Beneficiaries who are less than 10 years younger than the IRA owner can still take advantage of lifetime withdrawals. This is where it gets interesting. The ���less than 10 years younger��� rule happens to include any beneficiary who is older than the account owner. This means older siblings, friends or domestic partners could be entitled to stretch their IRA withdrawals over their own life expectancy.

I���ve found this aspect of the law isn���t yet widely understood. For instance, I just completed a continuing education course on the new rules for IRAs that incorrectly stated that parents and grandparents don���t qualify for lifetime distributions. They all would qualify because, presumably, they���d all be older than the original IRA owner.

Applying the same rule, cohabiting adults who are within 10 years of the deceased's age also qualify for the stretch rules. The surviving adult would be able to take lifetime withdrawals if listed as the IRA���s sole beneficiary.

The new rules also apply to Roth IRAs, but with one additional condition, which concerns the five-year rule. If the Roth account was established less than five years before the account owner���s passing, the beneficiary must wait to withdraw assets until that requirement is met to ensure the withdrawals are tax-free. This is one more reason to establish Roth IRAs as early as possible.

Who loses out under the SECURE Act? Younger beneficiaries, such as the grandchildren of IRA owners. Before 2020, they might have stretched inherited IRA withdrawals over six or seven decades, allowing the account to enjoy enormous compound growth. Now, their inheritance must be withdrawn from the sheltering arms of an IRA in no more than 10 years. Under the new rules of the game, our grandparents are welcome to take a stretch, but not our more limber grandchildren.

James McGlynn, CFA, RICP, is chief executive of

Next Quarter Century LLC

��in Fort Worth, Texas, a firm focused on helping clients make smarter decisions about long-term-care insurance, Social Security and other retirement planning issues. He was a mutual fund manager for 30 years. James is the author of��

Retirement Planning Tips for Baby Boomers

. Check out his earlier articles.The post Still Stretching appeared first on HumbleDollar.

January 24, 2022

A Tale of Two Stocks

HI, MY NAME IS MIKE and I���m a stock picker. Actually, I stopped picking a few years ago after I hit rock bottom and finally realized I had a problem. But there���s no such thing as an ex-stock picker.

I still frequent Seeking Alpha, read the occasional Barron���s article and, every now and then, have the urge to buy an individual stock. I still occasionally fall off the wagon, but nothing like the ol��� days. Back then, I picked two stocks, but instead of earning a stream of rising dividends, I earned a valuable lesson.

Stock No. 1: In the early 2000s, I formed an investment group using what was then the hottest website in the U.S��� Craigslist. Over the next few months, I met with a group of diverse investors at what was then the hottest restaurant in the U.S��� California Pizza Kitchen. Over numerous Thai crunch salads, we discussed various investments ideas, including ���condo-izing��� a small apartment building, Vector Tobacco, Audible and���what I thought was the best one���Medallion Financial Corp.

Medallion Financial provided loans to buy taxicab medallions in New York, Boston, Chicago, Newark and Cambridge. For those who don���t live in these cities, a medallion is the license required to operate a taxicab. It���s a piece of metal about six inches across that is physically��mounted to the hood of a taxicab. Every taxicab has to have one.

It was also a license to print money for those who owned one. New York City drastically limited the number of taxis in Midtown Manhattan. Anyone who has ever tried to hail a taxicab outside Penn Station on a rainy Friday during rush hour could attest to its worth.

While this country doesn���t like the idea of a cartel trying to set the price of oil, New York didn���t seem to mind allowing a cartel to monopolize the number of taxicabs. The sale of new medallions seemed to have more to do with the city needing to periodically rectify its finances than it did with meeting the needs of potential customers stuck for a ride.

Medallion Financial traced its roots to Leon Murstein, who purchased one of the first taxi medallions ever sold by New York City back in 1937. The company his grandson formed subsequently got into the finance side of the business, while also owning a significant number of medallions itself.

The loans Medallion made seemed virtually risk-free. If the owner could not make the payments, the medallion could be ripped from the hood of the taxicab and resold���almost always at a higher price. The fact that the new owner, most likely an immigrant, would have to drive their medallion-adorned taxi 12 hours a day, seven days a week to make payments was a matter that investors like myself didn���t concern themselves with.

The historic price of a medallion was a huge reason for the value of the company. Since the first medallion was sold by New York City in 1937 for $10, the price of a medallion had increased to more than $1 million by 2014. That���s an annualized��15.5% return, or 50% more a year than the S&P 500, including dividends.

I bought some shares. The company and I both rode up the disturbingly constant increase in medallion prices until a company called Uber came along. Well, needless to say, the price of a medallion has since dropped precipitously, as has the stock of Medallion Financial. It got so bad that the company changed its ticker symbol from TAXI to MFIN.

Stock No. 2: Thornburg Mortgage was a publicly traded real estate investment trust that I read about in a James Glassman article in The Washington Post in 2004. It was a unique mortgage company in that it only sold adjustable-rate mortgages to rich people who put at least 20% down. Thornburg then serviced these mortgages itself���it didn���t package and resell them. This enabled Thornburg to stay in direct contact with the customer, and easily alter or renew the mortgage. The company used options to hedge away any interest rate risk. It was an extremely well-run and profitable company.

As the financial crisis began to unfold in 2007, Thornburg���s business model performed magnificently. Its predominantly rich customers continued to make their mortgage payments. The 20% down covered the costs of the few defaults. Everything should have been copacetic, except that the crisis caused the value of all mortgage-backed securities to plummet. Investors treated the performing mortgages that Thornburg carried the same as the subprime garbage.

Once that happened, the short-term loan market that Thornburg relied on for financing dried up. Nobody would lend the company money. A death spiral ensued: dividend suspension, an 18% interest rate loan and a subsequent secondary stock sale.

It was a testament to the business model and underwriting ability of management that, during the months that this took to unfold, its portfolio of mortgages performed quite well, with few delinquencies. This, unfortunately, did not help. The company eventually ceased operations and filed for Chapter 11 bankruptcy reorganization while it liquidated.

Both of the above stocks served as a death knell, signaling the beginning of the end of my investment in individual stocks. In both cases, I had performed a thorough fundamental analysis and invested in a conservatively managed company with a wide moat���unlike my investment in Enron, which may be the makings for another article. In both cases, my diligence was rewarded with a significantly lower share price.

No matter how rigorous your analysis, no investor can foresee all the developments that may affect the business model of even the best-run companies. I���ve learned that this makes stock picking problematic, at best. Though there is this one pink sheet company that looks promising���.

Michael Flack blogs at��AfterActionReport.info. He���s a former naval officer and 20-year veteran of the oil and gas industry. Now retired, Mike enjoys traveling, blogging and spreadsheets. Check out his earlier articles.

Michael Flack blogs at��AfterActionReport.info. He���s a former naval officer and 20-year veteran of the oil and gas industry. Now retired, Mike enjoys traveling, blogging and spreadsheets. Check out his earlier articles.

I still frequent Seeking Alpha, read the occasional Barron���s article and, every now and then, have the urge to buy an individual stock. I still occasionally fall off the wagon, but nothing like the ol��� days. Back then, I picked two stocks, but instead of earning a stream of rising dividends, I earned a valuable lesson.

Stock No. 1: In the early 2000s, I formed an investment group using what was then the hottest website in the U.S��� Craigslist. Over the next few months, I met with a group of diverse investors at what was then the hottest restaurant in the U.S��� California Pizza Kitchen. Over numerous Thai crunch salads, we discussed various investments ideas, including ���condo-izing��� a small apartment building, Vector Tobacco, Audible and���what I thought was the best one���Medallion Financial Corp.

Medallion Financial provided loans to buy taxicab medallions in New York, Boston, Chicago, Newark and Cambridge. For those who don���t live in these cities, a medallion is the license required to operate a taxicab. It���s a piece of metal about six inches across that is physically��mounted to the hood of a taxicab. Every taxicab has to have one.

It was also a license to print money for those who owned one. New York City drastically limited the number of taxis in Midtown Manhattan. Anyone who has ever tried to hail a taxicab outside Penn Station on a rainy Friday during rush hour could attest to its worth.

While this country doesn���t like the idea of a cartel trying to set the price of oil, New York didn���t seem to mind allowing a cartel to monopolize the number of taxicabs. The sale of new medallions seemed to have more to do with the city needing to periodically rectify its finances than it did with meeting the needs of potential customers stuck for a ride.

Medallion Financial traced its roots to Leon Murstein, who purchased one of the first taxi medallions ever sold by New York City back in 1937. The company his grandson formed subsequently got into the finance side of the business, while also owning a significant number of medallions itself.

The loans Medallion made seemed virtually risk-free. If the owner could not make the payments, the medallion could be ripped from the hood of the taxicab and resold���almost always at a higher price. The fact that the new owner, most likely an immigrant, would have to drive their medallion-adorned taxi 12 hours a day, seven days a week to make payments was a matter that investors like myself didn���t concern themselves with.

The historic price of a medallion was a huge reason for the value of the company. Since the first medallion was sold by New York City in 1937 for $10, the price of a medallion had increased to more than $1 million by 2014. That���s an annualized��15.5% return, or 50% more a year than the S&P 500, including dividends.

I bought some shares. The company and I both rode up the disturbingly constant increase in medallion prices until a company called Uber came along. Well, needless to say, the price of a medallion has since dropped precipitously, as has the stock of Medallion Financial. It got so bad that the company changed its ticker symbol from TAXI to MFIN.

Stock No. 2: Thornburg Mortgage was a publicly traded real estate investment trust that I read about in a James Glassman article in The Washington Post in 2004. It was a unique mortgage company in that it only sold adjustable-rate mortgages to rich people who put at least 20% down. Thornburg then serviced these mortgages itself���it didn���t package and resell them. This enabled Thornburg to stay in direct contact with the customer, and easily alter or renew the mortgage. The company used options to hedge away any interest rate risk. It was an extremely well-run and profitable company.

As the financial crisis began to unfold in 2007, Thornburg���s business model performed magnificently. Its predominantly rich customers continued to make their mortgage payments. The 20% down covered the costs of the few defaults. Everything should have been copacetic, except that the crisis caused the value of all mortgage-backed securities to plummet. Investors treated the performing mortgages that Thornburg carried the same as the subprime garbage.

Once that happened, the short-term loan market that Thornburg relied on for financing dried up. Nobody would lend the company money. A death spiral ensued: dividend suspension, an 18% interest rate loan and a subsequent secondary stock sale.

It was a testament to the business model and underwriting ability of management that, during the months that this took to unfold, its portfolio of mortgages performed quite well, with few delinquencies. This, unfortunately, did not help. The company eventually ceased operations and filed for Chapter 11 bankruptcy reorganization while it liquidated.

Both of the above stocks served as a death knell, signaling the beginning of the end of my investment in individual stocks. In both cases, I had performed a thorough fundamental analysis and invested in a conservatively managed company with a wide moat���unlike my investment in Enron, which may be the makings for another article. In both cases, my diligence was rewarded with a significantly lower share price.

No matter how rigorous your analysis, no investor can foresee all the developments that may affect the business model of even the best-run companies. I���ve learned that this makes stock picking problematic, at best. Though there is this one pink sheet company that looks promising���.

Michael Flack blogs at��AfterActionReport.info. He���s a former naval officer and 20-year veteran of the oil and gas industry. Now retired, Mike enjoys traveling, blogging and spreadsheets. Check out his earlier articles.The post A Tale of Two Stocks appeared first on HumbleDollar.

January 23, 2022

All Fall Down

THE S&P 500 JUST HAD its worst week since March 2020's COVID-19 crash. Ironically, the decline happened as coronavirus cases were finally dropping after the December surge. Vanguard S&P 500 ETF (symbol: VOO) fell 5.7%, while Vanguard Small-Cap ETF (VB) lost 7.3%.

Returns were not as bad overseas. Vanguard FTSE All-World ex-U.S. ETF (VEU) dropped 3.1%. Coming as a surprise to some index fund investors, Vanguard FTSE Emerging Markets ETF (VWO) is actually positive so far in 2022. Investors who hold a globally diversified portfolio have benefited this month as international stocks have missed the brunt of the selling pressure.

The bond market was down slightly last week after a surge in interest rates to kick off the year. The 10-year Treasury note neared 1.9% on Tuesday before settling just shy of 1.75% on Friday. Traders flocked to the safety of Treasurys as the stock selloff worsened over the second half of the week.

I noticed that the yield to maturity���a measure of a bond���s current interest rate���jumped to 2.1% on iShares Core U.S. Aggregate Bond ETF (AGG). Suddenly, bonds don���t seem like such a raw deal. In mid-2020, when the 10-year Treasury rate was just 0.6%, the yield to maturity on the U.S. aggregate bond index was less than 1%.

Still, inflation expectations over the next decade are near 2.3%, while the market sees consumer prices climbing 2.7% a year over the next five years. You can grab Series I��savings bonds at 7.12% through April, but that rate will retreat later this year and beyond, assuming inflation eases.

Buckle up for continued wild market moves. The Volatility Index (VIX) rose to nearly 30 last Friday, the highest since early December. There���s a Federal Reserve rate decision on Wednesday. The market currently expects five quarter-point interest rate hikes by year-end. This is the common reason cited for the sharp pullback in growth stocks recently.

It���s always helpful to remember that corrections happen frequently in the stock market. The S&P 500 drops 14% during an average year. Last year was an odd one: The S&P 500���s biggest drawdown���a price decline from peak to trough���was just 5.2%. The current selloff from 2022���s lone S&P 500 all-time high on Jan. 3 is already 8.3%.

Returns were not as bad overseas. Vanguard FTSE All-World ex-U.S. ETF (VEU) dropped 3.1%. Coming as a surprise to some index fund investors, Vanguard FTSE Emerging Markets ETF (VWO) is actually positive so far in 2022. Investors who hold a globally diversified portfolio have benefited this month as international stocks have missed the brunt of the selling pressure.

The bond market was down slightly last week after a surge in interest rates to kick off the year. The 10-year Treasury note neared 1.9% on Tuesday before settling just shy of 1.75% on Friday. Traders flocked to the safety of Treasurys as the stock selloff worsened over the second half of the week.

I noticed that the yield to maturity���a measure of a bond���s current interest rate���jumped to 2.1% on iShares Core U.S. Aggregate Bond ETF (AGG). Suddenly, bonds don���t seem like such a raw deal. In mid-2020, when the 10-year Treasury rate was just 0.6%, the yield to maturity on the U.S. aggregate bond index was less than 1%.

Still, inflation expectations over the next decade are near 2.3%, while the market sees consumer prices climbing 2.7% a year over the next five years. You can grab Series I��savings bonds at 7.12% through April, but that rate will retreat later this year and beyond, assuming inflation eases.

Buckle up for continued wild market moves. The Volatility Index (VIX) rose to nearly 30 last Friday, the highest since early December. There���s a Federal Reserve rate decision on Wednesday. The market currently expects five quarter-point interest rate hikes by year-end. This is the common reason cited for the sharp pullback in growth stocks recently.

It���s always helpful to remember that corrections happen frequently in the stock market. The S&P 500 drops 14% during an average year. Last year was an odd one: The S&P 500���s biggest drawdown���a price decline from peak to trough���was just 5.2%. The current selloff from 2022���s lone S&P 500 all-time high on Jan. 3 is already 8.3%.

The post All Fall Down appeared first on HumbleDollar.

Resolved: New Journeys

WE RETIRED AND MOVED to Spain in 2018. We were excited and eager to explore our new home and a new culture. We traveled a lot, mostly in Spain, but also the rest of Europe and Asia. But since the pandemic started, our travel has been limited.

Indeed, COVID-19 sped our return to Dallas.��I���m happy that we���re now closer to our sons, and can see family and friends in person. But having lived in Dallas for 28 years, I already know the city well. Still, I plan to keep exploring���but this year I���ve resolved to take my retirement journey in two different directions.

First, during the ultra-strict Spanish lockdown in early 2020, I discovered my love of drawing and painting, and even set up online art shops. Creating art has helped me deal with the stress of the pandemic and of my mother's��situation. It has become my way of turning off the outside noise. This year, I���ve resolved to continue to draw and paint in my sketchbook every day. Whether that will translate into making more money isn���t important to me, though I���ll admit that I get excited and enjoy the extra validation that comes with selling a piece of art.

My second journey for 2022 is returning to graduate school. Like my husband Jim, I was recently admitted to the Master of Arts in Interdisciplinary Studies program at the University of Texas at Dallas. My focus will be gender studies and economics.

Why? I spent my career in the male-dominated world of finance and banking, and I���ve written about my experiences and the challenges��women face. I���ve also been interviewed about the gender pay gap. It���s an issue I���m passionate about and want to explore in depth. Classes are set to start in late January. I hope that, by drawing on multiple academic disciplines, I���ll have the opportunity to turn my personal experience and interest into a more complete understanding of the issue���and then I want to work to broaden opportunities for women who are still in the game.

Indeed, COVID-19 sped our return to Dallas.��I���m happy that we���re now closer to our sons, and can see family and friends in person. But having lived in Dallas for 28 years, I already know the city well. Still, I plan to keep exploring���but this year I���ve resolved to take my retirement journey in two different directions.

First, during the ultra-strict Spanish lockdown in early 2020, I discovered my love of drawing and painting, and even set up online art shops. Creating art has helped me deal with the stress of the pandemic and of my mother's��situation. It has become my way of turning off the outside noise. This year, I���ve resolved to continue to draw and paint in my sketchbook every day. Whether that will translate into making more money isn���t important to me, though I���ll admit that I get excited and enjoy the extra validation that comes with selling a piece of art.

My second journey for 2022 is returning to graduate school. Like my husband Jim, I was recently admitted to the Master of Arts in Interdisciplinary Studies program at the University of Texas at Dallas. My focus will be gender studies and economics.

Why? I spent my career in the male-dominated world of finance and banking, and I���ve written about my experiences and the challenges��women face. I���ve also been interviewed about the gender pay gap. It���s an issue I���m passionate about and want to explore in depth. Classes are set to start in late January. I hope that, by drawing on multiple academic disciplines, I���ll have the opportunity to turn my personal experience and interest into a more complete understanding of the issue���and then I want to work to broaden opportunities for women who are still in the game.

The post Resolved: New Journeys appeared first on HumbleDollar.

Seven Money Rules

I DESCRIBED A SET��of ideas last year that I called truisms of financial planning. They���re concepts I���ve found helpful in navigating the world of personal finance. Below are seven more.

1. Jeff Bezos is a bad role model.��So are Bill Gates, Elon Musk and pretty much every other billionaire. Of course, they���re all great geniuses, so why would I say that? The problem is how they made their money. In each case, they owned exactly one stock. It just happened to be an exceptionally good one. But that���s exactly the opposite of what works for most people most of the time. For everyone else, our best bet, according to the data, is to diversify and to avoid loading up on any one stock. We've known this at least since Harry Markowitz's��work��in the 1950s.

I recognize, though, that diversification can be difficult. That's been especially true over the past year, when we've seen some folks make small fortunes betting on individual stocks. Look to your left and look to your right, and there���s probably someone you know who's hit the Tesla lottery. That's great for them. Problem is, it would be hard to replicate.

To understand why, imagine that instead of Tesla, an investor had bet on Peloton, a stock that rose alongside Tesla early in the pandemic. Today, that Peloton investor wouldn't be so happy. Its stock is down more than 80% from its high last year. The bottom line: Never mind the billionaires and the gunslinger stock-pickers. Instead, diversify. Always diversify���even when it looks like doing the opposite will be the easier road to profits.

2. When the stock market is at a high point, you can still expect it to go higher.��Think back to early 2000, at the peak of the tech bubble. It looked like the market was at risk of a decline. And that's exactly what happened.

But today, it's much higher than it was even at its peak 22 years ago. In my view, that was to be expected. Why? While it's impossible to know where the market will go this year or next, I think it's safe to expect it to go higher over the long term. And I don't say that just because that's what's always happened in the past. That's not a good enough reason.

Instead, there's a logical reason to expect stocks to rise over time. Ultimately, share prices are driven by corporate profits. And profits are driven by, among other things, population growth and gains in worker productivity.

Amazon offers a good illustration. The e-commerce giant wouldn't be nearly as profitable���and thus its stock price wouldn't be nearly as high���if it didn't have as many robots staffing its fulfillment centers. Corporations, on average, experience productivity gains every year. And that's why, if you have a long time horizon, you shouldn't just��hope��stock prices go higher. Rather, you should��expect��them to.

3. As investors, we are all products of our environments.��Writing in��The Psychology of Money, author Morgan Housel makes the point that each generation of investors is shaped by the economic conditions they experienced as young adults. Those in Generation X, for example, benefited from a booming market when they got out of college. For that reason, they have a much more optimistic money mindset than those who came of age in the gloomy 1970s.

But this kind of effect isn't just generational. The family you grew up in, and the financial experiences you've had yourself, also contribute to your beliefs and outlook as an investor. And that colors how we see investment decisions.

4. It's the risks we don't know are risks that pose the biggest risk.��Most people follow the major news stories of the day, including those that we perceive as risks. As a result, and counterintuitively, the risks we all acknowledge as risks slowly begin to feel less risky. We've had time to adjust to them. An example is the current bout of inflation, which has been in the news for many months.

But it's the news items that are currently below the radar that tend to have more of an impact on investment markets. If Russia invaded Ukraine tomorrow, for example, it wouldn't be altogether surprising because we've been hearing about it for a while. The markets might take it in stride. But if some other military conflict came out of nowhere, the stock market would probably drop, just as it did when the coronavirus came out of nowhere two years ago.

The lesson: There are always more risks than we can see. And we can never know which ones will come to the surface or when. That's why I abide by Howard Marks's��motto: ���You can't predict. You can prepare.���

5. Over time, ���safe��� investments tend to become unsafe, and ���unsafe��� investments tend to become safe.��I'm referring here to cash and bonds, which are safe in the short term but can erode due to inflation over the long term, and to stocks, which can be unsafe in the short term but have always delivered positive returns over the long term. Neither is perfect. That's why it's important to hold both.

6. Tactical portfolio management is mostly a bad idea, but that doesn't mean you can't ever make tactical decisions.��Tactical investment strategies, if you aren't familiar with the term, require predictions and market timing���two of the easiest ways to lose money, in my experience. But that doesn't mean there aren't situations in which you��can��be tactical. Examples include when to claim Social Security, whether to execute Roth conversions and which asset classes to sell each year in retirement.

To be sure, each of those decisions involves making a prediction. But these kinds of predictions are very different from trying to guess where the stock market is going���which is nearly impossible. The fact is, you aren't completely in the dark: Deciding whether to complete a Roth conversion, for example, requires guessing about your future tax rate���and that's not entirely impossible to predict.

7. The market sometimes gets things right, but it can't always see around the corner.��Back in 2017, as investors anticipated a cut in the corporate tax rate, stocks rose. That was a completely logical reaction. And in 2020, when the Fed dropped interest rates, stocks also rose. That, too, was a nearly textbook response. But the market isn���t always so smart.

When the pandemic first hit, the government began printing money to issue stimulus payments. The market perceived those actions as positive, and in the short term, that was the case. But what the market couldn���t see was how the government���s actions would ultimately end up having a negative impact.

Flooding the market with new dollars, as we've seen, sparked inflation. And that inflation has prompted the Fed to announce its intention to raise rates again. That, in turn, has caused stocks to drop. The bottom line: Sometimes the market is right, but you can never be sure.

That is, by the way, a reason the market's behavior in response to elections is virtually impossible to predict. There are just too many variables and too many unknowns. When it comes to the stock market, it's impossible to know whether any given event will bring out Dr. Jekyll or Mr. Hyde.

What's the best course of action for investors in an environment like this? Again, you can't predict, but you can prepare.

Adam M. Grossman��is the founder of Mayport, a fixed-fee wealth management firm. Sign up for Adam's Daily Ideas email, follow him on Twitter @AdamMGrossman��and check out his earlier articles.

Adam M. Grossman��is the founder of Mayport, a fixed-fee wealth management firm. Sign up for Adam's Daily Ideas email, follow him on Twitter @AdamMGrossman��and check out his earlier articles.

1. Jeff Bezos is a bad role model.��So are Bill Gates, Elon Musk and pretty much every other billionaire. Of course, they���re all great geniuses, so why would I say that? The problem is how they made their money. In each case, they owned exactly one stock. It just happened to be an exceptionally good one. But that���s exactly the opposite of what works for most people most of the time. For everyone else, our best bet, according to the data, is to diversify and to avoid loading up on any one stock. We've known this at least since Harry Markowitz's��work��in the 1950s.

I recognize, though, that diversification can be difficult. That's been especially true over the past year, when we've seen some folks make small fortunes betting on individual stocks. Look to your left and look to your right, and there���s probably someone you know who's hit the Tesla lottery. That's great for them. Problem is, it would be hard to replicate.

To understand why, imagine that instead of Tesla, an investor had bet on Peloton, a stock that rose alongside Tesla early in the pandemic. Today, that Peloton investor wouldn't be so happy. Its stock is down more than 80% from its high last year. The bottom line: Never mind the billionaires and the gunslinger stock-pickers. Instead, diversify. Always diversify���even when it looks like doing the opposite will be the easier road to profits.

2. When the stock market is at a high point, you can still expect it to go higher.��Think back to early 2000, at the peak of the tech bubble. It looked like the market was at risk of a decline. And that's exactly what happened.

But today, it's much higher than it was even at its peak 22 years ago. In my view, that was to be expected. Why? While it's impossible to know where the market will go this year or next, I think it's safe to expect it to go higher over the long term. And I don't say that just because that's what's always happened in the past. That's not a good enough reason.

Instead, there's a logical reason to expect stocks to rise over time. Ultimately, share prices are driven by corporate profits. And profits are driven by, among other things, population growth and gains in worker productivity.

Amazon offers a good illustration. The e-commerce giant wouldn't be nearly as profitable���and thus its stock price wouldn't be nearly as high���if it didn't have as many robots staffing its fulfillment centers. Corporations, on average, experience productivity gains every year. And that's why, if you have a long time horizon, you shouldn't just��hope��stock prices go higher. Rather, you should��expect��them to.

3. As investors, we are all products of our environments.��Writing in��The Psychology of Money, author Morgan Housel makes the point that each generation of investors is shaped by the economic conditions they experienced as young adults. Those in Generation X, for example, benefited from a booming market when they got out of college. For that reason, they have a much more optimistic money mindset than those who came of age in the gloomy 1970s.

But this kind of effect isn't just generational. The family you grew up in, and the financial experiences you've had yourself, also contribute to your beliefs and outlook as an investor. And that colors how we see investment decisions.

4. It's the risks we don't know are risks that pose the biggest risk.��Most people follow the major news stories of the day, including those that we perceive as risks. As a result, and counterintuitively, the risks we all acknowledge as risks slowly begin to feel less risky. We've had time to adjust to them. An example is the current bout of inflation, which has been in the news for many months.

But it's the news items that are currently below the radar that tend to have more of an impact on investment markets. If Russia invaded Ukraine tomorrow, for example, it wouldn't be altogether surprising because we've been hearing about it for a while. The markets might take it in stride. But if some other military conflict came out of nowhere, the stock market would probably drop, just as it did when the coronavirus came out of nowhere two years ago.

The lesson: There are always more risks than we can see. And we can never know which ones will come to the surface or when. That's why I abide by Howard Marks's��motto: ���You can't predict. You can prepare.���

5. Over time, ���safe��� investments tend to become unsafe, and ���unsafe��� investments tend to become safe.��I'm referring here to cash and bonds, which are safe in the short term but can erode due to inflation over the long term, and to stocks, which can be unsafe in the short term but have always delivered positive returns over the long term. Neither is perfect. That's why it's important to hold both.

6. Tactical portfolio management is mostly a bad idea, but that doesn't mean you can't ever make tactical decisions.��Tactical investment strategies, if you aren't familiar with the term, require predictions and market timing���two of the easiest ways to lose money, in my experience. But that doesn't mean there aren't situations in which you��can��be tactical. Examples include when to claim Social Security, whether to execute Roth conversions and which asset classes to sell each year in retirement.

To be sure, each of those decisions involves making a prediction. But these kinds of predictions are very different from trying to guess where the stock market is going���which is nearly impossible. The fact is, you aren't completely in the dark: Deciding whether to complete a Roth conversion, for example, requires guessing about your future tax rate���and that's not entirely impossible to predict.

7. The market sometimes gets things right, but it can't always see around the corner.��Back in 2017, as investors anticipated a cut in the corporate tax rate, stocks rose. That was a completely logical reaction. And in 2020, when the Fed dropped interest rates, stocks also rose. That, too, was a nearly textbook response. But the market isn���t always so smart.

When the pandemic first hit, the government began printing money to issue stimulus payments. The market perceived those actions as positive, and in the short term, that was the case. But what the market couldn���t see was how the government���s actions would ultimately end up having a negative impact.

Flooding the market with new dollars, as we've seen, sparked inflation. And that inflation has prompted the Fed to announce its intention to raise rates again. That, in turn, has caused stocks to drop. The bottom line: Sometimes the market is right, but you can never be sure.

That is, by the way, a reason the market's behavior in response to elections is virtually impossible to predict. There are just too many variables and too many unknowns. When it comes to the stock market, it's impossible to know whether any given event will bring out Dr. Jekyll or Mr. Hyde.

What's the best course of action for investors in an environment like this? Again, you can't predict, but you can prepare.

Adam M. Grossman��is the founder of Mayport, a fixed-fee wealth management firm. Sign up for Adam's Daily Ideas email, follow him on Twitter @AdamMGrossman��and check out his earlier articles.The post Seven Money Rules appeared first on HumbleDollar.

January 21, 2022

Take It to the Limit?

LIKE SOME OF YOU reading this, I get a thrill from seeing my 401(k) contributions start at zero in January and tick up to the annual limit. I���ve been fortunate to maximize my contributions for most of my 24 working years. Last year, my contributions topped out at the 2021 limit of $19,500. In 2022, I���m aiming to make the maximum contribution of $20,500. For those age 50 and older, you can contribute up to $27,000 in 2022.

Up to now, I���ve considered it a no-brainer to contribute the 401(k) max. While I���m not making any changes this year, I am starting to think differently as I inch closer to retirement. If you���re in a similar situation, here are three factors you may want to consider when deciding how much to contribute.

First, if you���re in a low-tax bracket or live in a low-tax state, the tax benefit of contributing pretax dollars to a 401(k) account could be minimal. If you think your tax rate will be higher in retirement, you could be better off investing through a standard brokerage account and paying tax on your earnings now. You could also opt for a Roth 401(k) if your employer offers that option. Factors that might drive your future tax rate higher include a retirement account that���ll generate significant income or plans to move to a higher-tax state.

A second factor to consider is how you���ll invest the funds. If you will be conservative when investing 401(k) contributions, the benefit of deferring tax on investment earnings will be minimal. It may be worth paying the small annual tax bill and having immediate access to your savings.

Finally, you should consider how long the funds will be in the 401(k) account. If you have many years���or even decades���before you���ll withdraw the funds, contributing to the 401(k) will be beneficial from a tax standpoint. But if the funds will sit in the 401(k) account for only a few years, the tax savings on your investment earnings will likely be modest.

Up to now, I���ve considered it a no-brainer to contribute the 401(k) max. While I���m not making any changes this year, I am starting to think differently as I inch closer to retirement. If you���re in a similar situation, here are three factors you may want to consider when deciding how much to contribute.

First, if you���re in a low-tax bracket or live in a low-tax state, the tax benefit of contributing pretax dollars to a 401(k) account could be minimal. If you think your tax rate will be higher in retirement, you could be better off investing through a standard brokerage account and paying tax on your earnings now. You could also opt for a Roth 401(k) if your employer offers that option. Factors that might drive your future tax rate higher include a retirement account that���ll generate significant income or plans to move to a higher-tax state.

A second factor to consider is how you���ll invest the funds. If you will be conservative when investing 401(k) contributions, the benefit of deferring tax on investment earnings will be minimal. It may be worth paying the small annual tax bill and having immediate access to your savings.

Finally, you should consider how long the funds will be in the 401(k) account. If you have many years���or even decades���before you���ll withdraw the funds, contributing to the 401(k) will be beneficial from a tax standpoint. But if the funds will sit in the 401(k) account for only a few years, the tax savings on your investment earnings will likely be modest.

The post Take It to the Limit? appeared first on HumbleDollar.

Project Mickey

I DON'T MAKE New Year's resolutions. I exercise to feel good, not to lose a certain number of pounds or notch some personal athletic record. I save because my future self will appreciate the sacrifice I make today, not because I���m targeting some specific level of wealth. I���ve never had a defined life plan. My career has been opportunistic. Yet, despite all that, my wife and I settled on and pursued two goals early in our marriage that had a lasting impact on our family���s finances���and on the stories we share with our kids as they, too, become adults.

In 2000, our daughter was born. In early 2002, we were expecting again. After a prenatal visit early in the pregnancy, my wife called me during a hectic day at work.

���We���re having twins,��� she said.

I told her to be serious. She was. I took the afternoon off to come home and process the news with her. We knew how much it cost for one kid. We were two working parents, but it was a financial struggle. Now, the cost would be multiplied by three.

I told her to be serious. She was. I took the afternoon off to come home and process the news with her. We knew how much it cost for one kid. We were two working parents, but it was a financial struggle. Now, the cost would be multiplied by three.

As 2003 ended, our oldest was three and our two youngest were one-year-olds, and the expenses felt huge. Daycare and preschool cost $24,000 a year. It represented a hefty line item in our family���s budget. We also paid $24,000 every year on our mortgage, though that included regular extra-principal payments. Fortunately, we had no student debt and no credit card debt, and we owned our two cars. Despite the financial commitments of a growing family, we made it a priority to save for the future.

Every year-end, we talked about our personal and financial objectives for the following year���how much to save in your retirement plan, how much in mine, how much for this home improvement project, how much for that trip. As 2003 turned into 2004, our discussion took an unusual turn. We both felt the pull to try something different. After more discussion, my wife proposed a new idea: pay off the mortgage early.

Home and away. We had bought our home when we moved to Overland Park, Kansas, in 1997. We were only six years into a 30-year mortgage. We���d paid $175,000 for the house, borrowing $167,100 for 30 years at 7.875%. Less than 12 months later, we refinanced to 7.25%. In 2002, we modified the loan, lowering our rate still further, so we now paid 5.625% on the remaining $143,168 balance. Our required monthly payments were $1,200, but we continued sending $2,000 each month, the same payment we���d made when our mortgage rate was higher.

We compared the 5.625% to what we thought the stock market might deliver. After the 2000-02 bear market, share prices had moved steadily upward. Perhaps stocks were indeed the better bet. But in the end, we had an emotional reason for continuing with the extra-large mortgage payments.

To us, financial freedom didn���t mean retiring early. We were two 30-somethings with three kids age three and under. The idea of not working was impractical and silly. Instead, at the time, achieving some level of financial freedom meant owning our house and never having to worry about where we would put our heads. If I lost my job, losing our home wouldn���t be a risk. If we wanted to pursue different careers, we could afford to earn less. It was easy and fun to think about what we could do with an additional $20,000-plus that wouldn���t be going toward house payments anymore.

In addition, we felt confident this would be our home for the long haul. We loved our city. We had put down roots in a new place we called our own, and we both wanted our kids to grow up in one house. It was big enough to meet our needs for a long time. We had already moved multiple times and we had no desire to do it again. More important, we wanted to be in control of our money rather than letting it control us. Paying off the mortgage was a crucial step in that direction, plus it felt like something different from what everyone around us was doing. It was a long-term financial goal���daunting yet achievable���that we could both get behind. Maybe we could even turn it into something fun.

By 2004, when we began in earnest, $130,000 remained on the mortgage. We worked down the balance to $125,000 with several payments, and then the excitement waned. The numbers were still too big and the undefined end date seemed too far off. We needed something to help us refocus, something long term to keep us moving forward and excited.

We had always been a traveling family. Earlier, in 2001, we had driven with our one-year-old daughter to Arlington, Virginia, to spend time with family. When I reviewed the route, I noted it would be our daughter���s first time passing through eight states. Wouldn���t it be fun, I now mused, to visit all 50 states with our kids by the time they finished high school? It would be a good excuse to see new places, show our kids the country, open them up to new perspectives and create a love of travel. The likelihood that they wouldn���t remember anything at such a young age was of no consequence. We were after shared experiences and stories we could tell later.

By 2004, the kids had visited 16 states, every one of them by car. Our budget didn���t allow for flights for five people. Could we somehow weave together our mortgage and travel goals? My wife proposed that we fly to Disney World to celebrate once we paid off our home loan. Celebrating the achievement with a once-in-a-childhood trip to Disney seemed like an idea that we could all get behind. As a bonus, we would also experience Florida���another state to add to the kids��� list. Suddenly, our two goals became one.

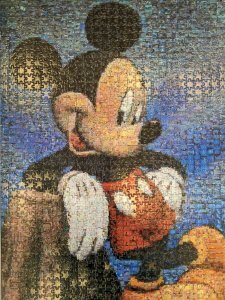

Matters of principal. Later that week, my wife came home with a 1,000-piece puzzle of Mickey Mouse and explained her idea. We would assemble the puzzle, then take it apart, placing contiguous pieces in separate baggies. One thousand pieces, divided by 125 reductions in the loan balance of $1,000 each, meant eight pieces per bag. Every time we reduced the mortgage principal by $1,000, we would put eight more puzzle pieces together. We would glue the pieces to a poster board and then put the partially completed puzzle away, while we awaited the next time we could add pieces.

About the same time that we started this project, I changed jobs, moving to a corporate credit union. My pay didn���t change much and our progress continued. We would go overboard from time to time, postponing some small, immaterial purchases to make larger payments on the mortgage. If expenses became too large, we instituted a checkbook lockdown until they moderated. My new job was located near a branch of the bank that held our loan. I would drive to the bank branch over my lunch hour to deposit the check and receive the receipt. By the end of 2004, the mortgage had declined to $97,000. We could see Mickey���s ears and part of his face.

About the same time that we started this project, I changed jobs, moving to a corporate credit union. My pay didn���t change much and our progress continued. We would go overboard from time to time, postponing some small, immaterial purchases to make larger payments on the mortgage. If expenses became too large, we instituted a checkbook lockdown until they moderated. My new job was located near a branch of the bank that held our loan. I would drive to the bank branch over my lunch hour to deposit the check and receive the receipt. By the end of 2004, the mortgage had declined to $97,000. We could see Mickey���s ears and part of his face.

In 2005, my twins joined their big sister at her school, and I changed jobs again, joining an investment advisory firm. It meant a pay cut, but my wife and I agreed that was an okay price to pay because it was the type of role I had envisioned when pursuing my Chartered Financial Analyst designation several years earlier. Still, that didn���t make it any easier to reach our goal of being mortgage-free, but that was a tradeoff we were willing to make. By the end of the following year, the mortgage had declined to $52,000. We could see Mickey���s gloves and pants.

The years passed, the principal declined, the puzzle filled in and the goal grew nearer. Every month, we brought out the poster board, tallied up how much we had paid off and added more pieces to the puzzle. The kids didn���t grasp the ���why,��� but they liked puzzles and always clamored to add more pieces. As the end approached, they came to understand the celebration that was to come.

We continued traveling, and we did it inexpensively. We drove to see our extended families, and slept on guest beds and floors. We met friends in state parks for long weekends. We camped, something both our families had done growing up. Neither had a lot of money to spare when we were young, and camping offered a way to have a vacation and get away. We drove everywhere, all five of us in a little Subaru Forester, getting creative with three car seats and boosters in the tight space. We did have one indulgence. Every January, my mother-in-law would stay with our kids for a few days, while my wife and I flew somewhere warm.

Paying off the mortgage wasn���t done at the expense of other savings priorities. We made sure to contribute to our workplace retirement plans. We funded 529 college savings accounts for each of the kids. We set aside money for home repairs, both expected and otherwise. We were willing to do without extra ���wants��� that others often see as needs.

By the end of 2007, the loan balance was down to $27,000. We thought the final payoff might happen in 2008, so we began researching Disney World. We decided to build savings to the point where we could pay off the entire balance with one final check. In 2008, we booked the trip for October.

Our plan was to spend a week and visit the four Disney parks: Magic Kingdom, Hollywood Studios, Animal Kingdom and Epcot. Normally, we would have chosen to stay somewhere nearby to save money. But instead, we stayed on the Disney property and saved time by avoiding the commute to and from the parks.

We also decided to buy Disney���s meal plan. Paying individually for each meal would have left us feeling figuratively spent and in a sour mood. By buying the plan, even if it was likely overpriced, we knew each meal was covered, leaving us in a much better frame of mind to remember the trip���s purpose���a fun family celebration. If the kids wanted an expensive menu item for dinner, or ice cream in the middle of the day, no problem. The approach worked beautifully: happy kids, happy parents.

Free at last. In truth, the trip���s timing was far from ideal. In September, the long-simmering housing crisis erupted, markets crashed and a global financial crisis was upon us. I had been with my employer for three years. Suddenly, everything looked uncertain. We were investment managers and markets were collapsing, with no end in sight. Was my job safe? At least no one was going to take our house. In November, we wrote a check to the bank for $9,400. The next day, my wife walked into the lobby to present our final payment, 11 years after we first took out a loan to purchase the house. We let the kids put in place the last pieces of Mickey���s golden shoes.

Being mortgage-free didn���t lead to any immediate changes. We couldn���t openly celebrate. Amid the financial hardship caused by the Great Recession, it seemed insensitive. We didn���t know who might be worried about their job or home. We did, however, call our insurance guy to share the news���because we���d now have to pay the premium on our homeowner���s policy directly, rather than as part of our monthly mortgage payment. The financial freedom we sought came in subtle ways. We redirected the extra cash flow into a new and bigger car for our growing family, trading in an older car for a Honda Odyssey. We increased college savings for our kids, whose tight age difference meant we���d be paying college costs for three students simultaneously for at least two years.

We continued traveling. After covering all the states in the middle of the map by car, flying became necessary to visit the states we���d yet to experience. Having a few extra dollars set aside made those trips possible. In 2011, we visited Delaware, Pennsylvania and New Jersey. In 2013, Washington and Oregon. In 2014, California. In 2015, we toured New England. Waiting in line for a ride at a fun park in Killington, Vermont, we fell into conversation with the family in front of us. When we explained our 50-state goal, the parents expressed surprise and shared that they had only ever been to five nearby states, while we were in the process of clicking off six states over 10 days. It was then that our kids began realizing the magnitude of their travels.

Three years ago, my wife left a job that had turned toxic. It was late spring, our oldest was graduating high school and our younger kids were entering their junior years. She took the summer off to spend as much time as she could with them. We also had the money saved to visit Hawaii, state No. 49. When our oldest entered college that fall, we were ready to shoulder university tuition.

The following year, my wife again took the summer off before finding a better position in the nonprofit world. That was when we traveled to Alaska, reaching our goal. A paid-off house made us comfortable with the short-term drop in income, even as we visited our 50th state.

Admittedly, paying off our mortgage early probably wasn���t the best financial decision. My wife and I didn���t���and don���t���care. Today, the completed puzzle sits in a closet. Our kids will likely decide what to do with it after we���re gone. It stands as a lesson for them���and for us���that you can set big goals and reach them little by little by little. What about the celebratory trip to Disney? Along with our travels to 49 other states, it continues to provide memories and stories, which we share around the dining-room table when the kids are home.

Phil Kernen, CFA, is a portfolio manager and partner with

Mitchell Capital

, a financial planning and investment management firm in Leawood, Kansas. When he's not working, Phil enjoys spending time with his family and friends, reading, hiking and riding his bike. You can connect with Phil via

LinkedIn

. Check out his earlier articles.

Phil Kernen, CFA, is a portfolio manager and partner with

Mitchell Capital

, a financial planning and investment management firm in Leawood, Kansas. When he's not working, Phil enjoys spending time with his family and friends, reading, hiking and riding his bike. You can connect with Phil via

LinkedIn

. Check out his earlier articles.

In 2000, our daughter was born. In early 2002, we were expecting again. After a prenatal visit early in the pregnancy, my wife called me during a hectic day at work.

���We���re having twins,��� she said.

I told her to be serious. She was. I took the afternoon off to come home and process the news with her. We knew how much it cost for one kid. We were two working parents, but it was a financial struggle. Now, the cost would be multiplied by three.As 2003 ended, our oldest was three and our two youngest were one-year-olds, and the expenses felt huge. Daycare and preschool cost $24,000 a year. It represented a hefty line item in our family���s budget. We also paid $24,000 every year on our mortgage, though that included regular extra-principal payments. Fortunately, we had no student debt and no credit card debt, and we owned our two cars. Despite the financial commitments of a growing family, we made it a priority to save for the future.

Every year-end, we talked about our personal and financial objectives for the following year���how much to save in your retirement plan, how much in mine, how much for this home improvement project, how much for that trip. As 2003 turned into 2004, our discussion took an unusual turn. We both felt the pull to try something different. After more discussion, my wife proposed a new idea: pay off the mortgage early.

Home and away. We had bought our home when we moved to Overland Park, Kansas, in 1997. We were only six years into a 30-year mortgage. We���d paid $175,000 for the house, borrowing $167,100 for 30 years at 7.875%. Less than 12 months later, we refinanced to 7.25%. In 2002, we modified the loan, lowering our rate still further, so we now paid 5.625% on the remaining $143,168 balance. Our required monthly payments were $1,200, but we continued sending $2,000 each month, the same payment we���d made when our mortgage rate was higher.

We compared the 5.625% to what we thought the stock market might deliver. After the 2000-02 bear market, share prices had moved steadily upward. Perhaps stocks were indeed the better bet. But in the end, we had an emotional reason for continuing with the extra-large mortgage payments.

To us, financial freedom didn���t mean retiring early. We were two 30-somethings with three kids age three and under. The idea of not working was impractical and silly. Instead, at the time, achieving some level of financial freedom meant owning our house and never having to worry about where we would put our heads. If I lost my job, losing our home wouldn���t be a risk. If we wanted to pursue different careers, we could afford to earn less. It was easy and fun to think about what we could do with an additional $20,000-plus that wouldn���t be going toward house payments anymore.

In addition, we felt confident this would be our home for the long haul. We loved our city. We had put down roots in a new place we called our own, and we both wanted our kids to grow up in one house. It was big enough to meet our needs for a long time. We had already moved multiple times and we had no desire to do it again. More important, we wanted to be in control of our money rather than letting it control us. Paying off the mortgage was a crucial step in that direction, plus it felt like something different from what everyone around us was doing. It was a long-term financial goal���daunting yet achievable���that we could both get behind. Maybe we could even turn it into something fun.

By 2004, when we began in earnest, $130,000 remained on the mortgage. We worked down the balance to $125,000 with several payments, and then the excitement waned. The numbers were still too big and the undefined end date seemed too far off. We needed something to help us refocus, something long term to keep us moving forward and excited.

We had always been a traveling family. Earlier, in 2001, we had driven with our one-year-old daughter to Arlington, Virginia, to spend time with family. When I reviewed the route, I noted it would be our daughter���s first time passing through eight states. Wouldn���t it be fun, I now mused, to visit all 50 states with our kids by the time they finished high school? It would be a good excuse to see new places, show our kids the country, open them up to new perspectives and create a love of travel. The likelihood that they wouldn���t remember anything at such a young age was of no consequence. We were after shared experiences and stories we could tell later.

By 2004, the kids had visited 16 states, every one of them by car. Our budget didn���t allow for flights for five people. Could we somehow weave together our mortgage and travel goals? My wife proposed that we fly to Disney World to celebrate once we paid off our home loan. Celebrating the achievement with a once-in-a-childhood trip to Disney seemed like an idea that we could all get behind. As a bonus, we would also experience Florida���another state to add to the kids��� list. Suddenly, our two goals became one.

Matters of principal. Later that week, my wife came home with a 1,000-piece puzzle of Mickey Mouse and explained her idea. We would assemble the puzzle, then take it apart, placing contiguous pieces in separate baggies. One thousand pieces, divided by 125 reductions in the loan balance of $1,000 each, meant eight pieces per bag. Every time we reduced the mortgage principal by $1,000, we would put eight more puzzle pieces together. We would glue the pieces to a poster board and then put the partially completed puzzle away, while we awaited the next time we could add pieces.

About the same time that we started this project, I changed jobs, moving to a corporate credit union. My pay didn���t change much and our progress continued. We would go overboard from time to time, postponing some small, immaterial purchases to make larger payments on the mortgage. If expenses became too large, we instituted a checkbook lockdown until they moderated. My new job was located near a branch of the bank that held our loan. I would drive to the bank branch over my lunch hour to deposit the check and receive the receipt. By the end of 2004, the mortgage had declined to $97,000. We could see Mickey���s ears and part of his face.In 2005, my twins joined their big sister at her school, and I changed jobs again, joining an investment advisory firm. It meant a pay cut, but my wife and I agreed that was an okay price to pay because it was the type of role I had envisioned when pursuing my Chartered Financial Analyst designation several years earlier. Still, that didn���t make it any easier to reach our goal of being mortgage-free, but that was a tradeoff we were willing to make. By the end of the following year, the mortgage had declined to $52,000. We could see Mickey���s gloves and pants.

The years passed, the principal declined, the puzzle filled in and the goal grew nearer. Every month, we brought out the poster board, tallied up how much we had paid off and added more pieces to the puzzle. The kids didn���t grasp the ���why,��� but they liked puzzles and always clamored to add more pieces. As the end approached, they came to understand the celebration that was to come.

We continued traveling, and we did it inexpensively. We drove to see our extended families, and slept on guest beds and floors. We met friends in state parks for long weekends. We camped, something both our families had done growing up. Neither had a lot of money to spare when we were young, and camping offered a way to have a vacation and get away. We drove everywhere, all five of us in a little Subaru Forester, getting creative with three car seats and boosters in the tight space. We did have one indulgence. Every January, my mother-in-law would stay with our kids for a few days, while my wife and I flew somewhere warm.

Paying off the mortgage wasn���t done at the expense of other savings priorities. We made sure to contribute to our workplace retirement plans. We funded 529 college savings accounts for each of the kids. We set aside money for home repairs, both expected and otherwise. We were willing to do without extra ���wants��� that others often see as needs.

By the end of 2007, the loan balance was down to $27,000. We thought the final payoff might happen in 2008, so we began researching Disney World. We decided to build savings to the point where we could pay off the entire balance with one final check. In 2008, we booked the trip for October.

Our plan was to spend a week and visit the four Disney parks: Magic Kingdom, Hollywood Studios, Animal Kingdom and Epcot. Normally, we would have chosen to stay somewhere nearby to save money. But instead, we stayed on the Disney property and saved time by avoiding the commute to and from the parks.

We also decided to buy Disney���s meal plan. Paying individually for each meal would have left us feeling figuratively spent and in a sour mood. By buying the plan, even if it was likely overpriced, we knew each meal was covered, leaving us in a much better frame of mind to remember the trip���s purpose���a fun family celebration. If the kids wanted an expensive menu item for dinner, or ice cream in the middle of the day, no problem. The approach worked beautifully: happy kids, happy parents.

Free at last. In truth, the trip���s timing was far from ideal. In September, the long-simmering housing crisis erupted, markets crashed and a global financial crisis was upon us. I had been with my employer for three years. Suddenly, everything looked uncertain. We were investment managers and markets were collapsing, with no end in sight. Was my job safe? At least no one was going to take our house. In November, we wrote a check to the bank for $9,400. The next day, my wife walked into the lobby to present our final payment, 11 years after we first took out a loan to purchase the house. We let the kids put in place the last pieces of Mickey���s golden shoes.

Being mortgage-free didn���t lead to any immediate changes. We couldn���t openly celebrate. Amid the financial hardship caused by the Great Recession, it seemed insensitive. We didn���t know who might be worried about their job or home. We did, however, call our insurance guy to share the news���because we���d now have to pay the premium on our homeowner���s policy directly, rather than as part of our monthly mortgage payment. The financial freedom we sought came in subtle ways. We redirected the extra cash flow into a new and bigger car for our growing family, trading in an older car for a Honda Odyssey. We increased college savings for our kids, whose tight age difference meant we���d be paying college costs for three students simultaneously for at least two years.

We continued traveling. After covering all the states in the middle of the map by car, flying became necessary to visit the states we���d yet to experience. Having a few extra dollars set aside made those trips possible. In 2011, we visited Delaware, Pennsylvania and New Jersey. In 2013, Washington and Oregon. In 2014, California. In 2015, we toured New England. Waiting in line for a ride at a fun park in Killington, Vermont, we fell into conversation with the family in front of us. When we explained our 50-state goal, the parents expressed surprise and shared that they had only ever been to five nearby states, while we were in the process of clicking off six states over 10 days. It was then that our kids began realizing the magnitude of their travels.

Three years ago, my wife left a job that had turned toxic. It was late spring, our oldest was graduating high school and our younger kids were entering their junior years. She took the summer off to spend as much time as she could with them. We also had the money saved to visit Hawaii, state No. 49. When our oldest entered college that fall, we were ready to shoulder university tuition.

The following year, my wife again took the summer off before finding a better position in the nonprofit world. That was when we traveled to Alaska, reaching our goal. A paid-off house made us comfortable with the short-term drop in income, even as we visited our 50th state.

Admittedly, paying off our mortgage early probably wasn���t the best financial decision. My wife and I didn���t���and don���t���care. Today, the completed puzzle sits in a closet. Our kids will likely decide what to do with it after we���re gone. It stands as a lesson for them���and for us���that you can set big goals and reach them little by little by little. What about the celebratory trip to Disney? Along with our travels to 49 other states, it continues to provide memories and stories, which we share around the dining-room table when the kids are home.

Phil Kernen, CFA, is a portfolio manager and partner with

Mitchell Capital

, a financial planning and investment management firm in Leawood, Kansas. When he's not working, Phil enjoys spending time with his family and friends, reading, hiking and riding his bike. You can connect with Phil via

LinkedIn

. Check out his earlier articles.The post Project Mickey appeared first on HumbleDollar.

Life���s Not a Beach

WE���VE BEEN BRAINWASHED by advertisers and financial firms into believing that retirees are a homogeneous group who all want the same things. They aren't. Instead, they have differing needs, values and wants, and this divergence is getting greater because of things like increasing longevity, dwindling job security and the elimination of pensions.

Let���s consider the standard bell-shaped distribution curve���and then apply it to people���s retirement behaviors. On the far left and far right of the curve are the outliers, people who are approaching retirement quite differently. On the far left are the early retirees, people who adopted the FIRE���financial independence-retire early���philosophy and retired long before age 65. Joining them are the comfort-oriented retirees who never want to work again. They just want to relax and enjoy a safe, simple, predictable retirement.

On the far right of the curve are people who intend to work right until the very end. We���re talking about folks like Warren Buffett and Mick Jagger. They have more than enough money to retire but have decided against it because they enjoy the work they do. Also found here are growth-oriented retirees who want to be challenged and keep growing. They view this time of their life as an opportunity to do things they always liked but didn���t have time for before, when they were working fulltime.

But what about all the people in the middle, perhaps slightly to the left or slightly to the right of ���average���? They���re all over the place. Many continue to work because they need the money to make ends meet. Others choose to work because they don���t want to cut back their lifestyle.

The important takeaway here: Retirees across the distribution curve are fundamentally different from each other. Not everyone enjoys the same type of retirement. Each retiree has different needs, values and wants that are driving them to do what they do. A one-size-fits-all approach to retirement won���t work.

For the past 50 years, retirement commercials have been showing the couple on the beach or the golf course. But this is nonsense. Not every retiree wants to live like that, nor can every retiree afford to. Watching such commercials causes retirees a lot of stress. Deep down, most retirees know that most retirements���including theirs���won���t look like that. In fact, most of them have no idea what their retirement will look like.

Many people, through choice or otherwise, are deviating from the old 20th century ���full stop��� retirement model���and probably, over the past 50 years, most retirees never had that sort of retirement. We need to recognize that.