Cosmo P. DeStefano's Blog, page 3

June 28, 2024

Winning the Long Game: Investing Requires Patience

Imagine achieving a 10% annual return on your investments, only to discover you’re actually earning a mere 3.6%. This staggering gap is the reality for many investors who fall victim to short-termism: focusing on near-term results to the detriment of long-term growth.

It is a well-documented phenomenon that mutual funds far outperform mutual fund investors in those same funds. Morningstar regularly looks at ‘investor returns’ which is the dollar-weighted results experienced by investors.

They found that if a fund’s assets swelled after a period of strong performance, investors often bought in too late to realize most of those gains. And if the fund declined, investors would ride it down for a period of time (hoping for a recovery that didn’t materialize) and sell out at a loss.

In other words, investors are often buying high and selling low.

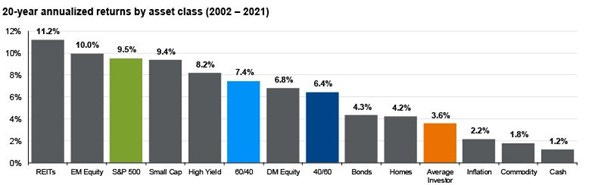

JP Morgan reported that over 20 years, the S&P 500 had an annualized return of 9.5% while the average investor had an annualized return of just 3.6% (62% less).

Similarly, the Dalbar Group found that when the S&P 500 dipped 4.4% in 2018, the average equity investor lost more than twice that amount—9.4%. And in 2019, when the S&P 500 gained 31%, the average equity investor gained 26% (16% less).

Why does this performance lag occur? Investors constantly cycle through a cacophony of emotions which wreaks havoc on their ability to stay invested. They bounce in and out of the market and back and forth between investments. Short-termism has them in its grip.

In theory, we all know we should buy long-term investments and hold on to them. In practice, we only hold purportedly long-term investments for a short while and then we get enticed by the next hot investment.

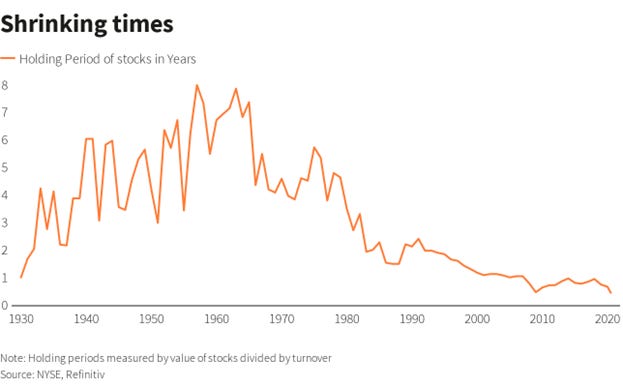

How short has the long-term become?

During the 1950s and 1960s, the average stock was held for more than seven years. By the 1980s the average was down to less than three years, and by the turn of the millennium it had fallen to less than one year. By June 2020 the average holding period had declined to just five and a half months.

Some high-frequency traders have reduced holding periods to slightly more than the blink of an eye—the founder of a high-frequency trading firm, Tradebot, told a group of students in 2008 that his firm’s average holding period for stocks was 11 seconds!

So, while the S&P 500 average long-term return is 10% per year, investors don’t earn that. Impatience and the lure of the next hot stock keep the average investor bouncing between investments. The 10% return is real, but investors don’t stick around long enough to get it.

It is tough to get a long-term return when measuring holding periods in months rather than years

Behavioral economics has shown us that our investing brains oftentimes lead us to make decisions that are illogical, but that make perfect emotional sense. Unfortunately, this lack of behavioral discipline during volatile times coupled with the absence of a well-defined strategy is a formula for below-average returns.

When it comes to long-term investing, quite often “Take No Action” is the best course. Design your financial plan to include a disciplined, long-term investment strategy to mitigate short-termism and the resulting diminished returns of sub-optimal investing decisions.

Then block out the noise and stick to your plan.

Rather than constantly chasing a better investment, put some of that attention on being a better investor. You’ll likely grow more wealth and cause less heartache over the long term.

As always, invest often and wisely. Thank you for reading.

The content is for informational purposes only. It is not intended to be nor should it be construed as legal, tax, investment, financial, or other advice. It is merely my own random thoughts.

May 17, 2024

For Richer or Poorer: Joint vs. Separate Finances

Newlyweds make a litany of decisions that will affect the trajectory of their lives together: where to live, how to divide chores, whether to have children, toilet seat up or down.

But one of the most fundamental financial decisions a couple faces is whether to merge accounts or treat money as something to be managed separately. Continuing research highlights that the separate or joint account quandary is much more than simply a legal ownership distinction.

The relationship dynamics that couples establish during the ‘honeymoon years’ often foreshadow how their relationship will progress in the later years.

The first few years of a marriage are critical to its success. Research has shown that the quality of a relationship peaks around the wedding day and then begins a long, and sometimes steep decline in the early years.

It’s not news to anyone that money is a major cause of arguments for couples. Fidelity found that nearly one in four couples identify money as their greatest relationship challenge. And while nearly 9 in 10 couples said they communicate well, more than 25% of partners resent being left out of financial decisions.

But is this a foregone conclusion or can couples, especially those just starting out, be more proactive in minimizing money disagreements and lessen or reverse that decline?

A recent study set out to determine if something as simple as bank account structure impacted how satisfied couples are in their relationship. After following engaged and newlywed couples for two years, the study found that financially interdependent couples had stronger relationship quality.

Why would combining accounts matter?

In addition to showing a correlation between shared accounts and relationship strength, the study found three potential reasons why couples with shared accounts may be better off.

Relative to separate accounts, joint accounts can improve each spouse’s feelings about how they handle money and prompt people to consider how they might justify their spending to their partner.

Couples can speak more openly about money and better align their financial goals.

Couples are more likely to adhere to communal norms. (e.g., responding to each other’s needs without expecting something in return.)

There is a wealth of common sense in these findings. Transparency and simplicity lead the way.

Are there drawbacks?

A joint account, however, is not a magical relationship elixir. There are potential reasons not to commingle money.

Lack of privacy. I am not suggesting you hide anything of significance from your partner but it’s worth noting that it is much harder to surprise your spouse with birthday gifts or Christmas presents if you only have joint accounts.

Life stages. If you and your spouse have multiple financial accounts and built a more significant net worth before you met, it might make sense to keep some of those accounts separate.

Retirement accounts. Not all accounts can be combined. For example, IRA and 401k’s are individual accounts and by law cannot be commingled.

Start the conversation

While merged finances aren’t necessarily ideal for all couples, some degree of joint accounts does seem to be a meaningful contributor to a long-lasting relationship. The correct mix is up to you, as a couple, to decide.

Not sure how to begin a conversation with your spouse? Check out this guide from Fidelity, Couples & Money: A Starter Guide.

I think ‘yours,’ ‘mine,’ and ‘ours’ can be a workable solution, but it doesn’t eliminate the need for open communication about your joint financial goals. In fact, working with a mix of accounts is best served by having an overarching and cohesive financial plan with a shared vision and a shared path to your financial future.

When it comes to planning out your financial path, here is how I summed it up in Life is Expensive: How Do People Do It?

The wealthy focus on the positive over the negative and keep the complaining to a minimum. They think long-term, have well-defined and realistic goals, work hard, eat healthy, exercise regularly, maintain a trusted social network, get a good night’s sleep, save and invest monthly, and oh yes, enjoy their spending.

Intelligent people know what to do. Intellectually curious people learn how to do it. But successful people are the ones who actually do it—repeatedly without fail. PCR: Plan, Course-correct, Repeat.

It is hard enough to meet financial goals while rowing in the boat together, but it’s exponentially tougher if the two of you are rowing in opposite directions. Get on the path to financial freedom…together.

As always, invest often and wisely. Thank you for reading.

The content is for informational purposes only. It is not intended to be nor should it be construed as legal, tax, investment, financial, or other advice. It is merely my own random thoughts.

February 23, 2024

Income Has No Limit. Or Does It?

While the prospect of boundless earning potential is undoubtedly enticing, it’s not a free pass to become a spendthrift. Wealth isn’t just about what you make; it’s about what you don’t spend.

Recently I’ve noticed several financial commentators posting on this topic. Here are two examples:

Remember this life-changing fact: There’s a limit to how much you can cut, but NO LIMIT to how much you can earn!

After all, you can only cut your spending so much, but your income has no limits.

Plenty of financial writers have echoed this exact sentiment for years. Unfortunately, a lot of people don’t read past the headline.

Some erroneously infer from these snippets that you need not worry about spending because you can always earn more. That’s a slippery slope.

Should high school athletes stop worrying about getting an education and saving money because they can make wads of cash playing professionally? Theoretically possible, but not very probable.

An interesting side note on student-athletes. According to an NCAA report, there are more than 7 million high school athletes and about 6% (less than 500,000) make it to the NCAA. Less than 2% of that 6% will make it into the professional arena—most of them will go pro in something other than sports.

Education can help increase lifetime earnings

Increasing your income shouldn’t be your sole focus, but it can be a key driver of your wealth accumulation. Professional athletes are an extreme example, but for the average person, increasing earnings (within reason) is likely attainable. One way to increase your earnings is through education. A person’s annual earnings generally increase as formal education increases.

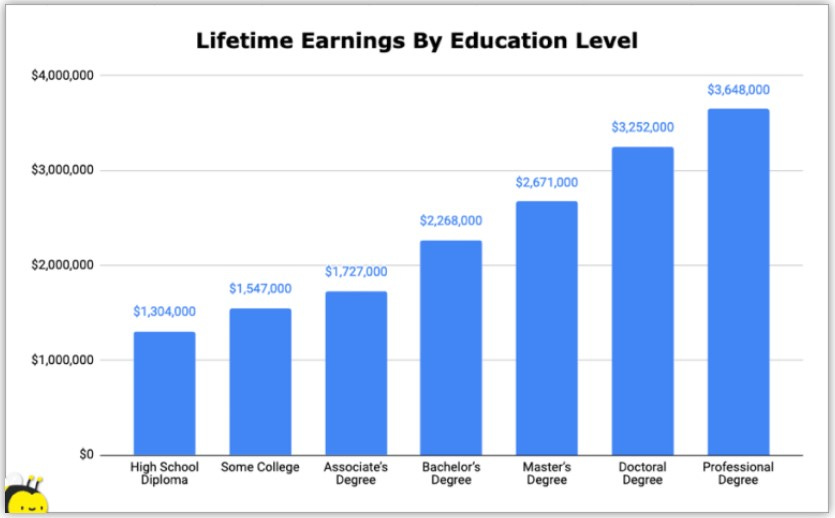

An average American will make $1.7m in lifetime earnings, and that average varies based on one’s education level. For example, those with bachelor’s degrees earn an average of 74% more than high school diplomas. Several other factors will impact earnings (e.g., market demand, experience, industry limitations, time constraints, etc.) but education is among the most influential.

Note in the chart below that while bachelor’s degrees earn a healthy average of $2.3m, it’s not $5m, $50m, or $100m. Average lifetime earnings hit a practical ceiling—at all education levels.

Education doesn’t end at school

While formal education provides a structured path to acquiring knowledge, skills, and hopefully a secure living, self-education allows people to explore their interests and deepen their skills on their own, unlocking their potential for greater financial success and personal fulfillment.

My brother-in-law used his high school diploma to explore several trades before identifying a need in his town for a talented barber. He headed back to school, earned his barbering license, and took a chance by opening his own shop.

He worked hard at his craft, earned his master barber license, and opened a second shop. For thirty years he’s not only pursued a fulfilling career but has grown a thriving business providing gainful employment for several others including his three sons.

There’s an old saying, give a person a fish and they eat for a day. Teach them how to fish and they eat for a lifetime. Unfortunately, too many people are just looking for a fish and couldn’t care less about the fishing lessons.

Increased income doesn’t end with labor

There are a finite number of hours in a day and only so much capacity for your labor to earn an income. True wealth is achieved when you learn to also make money while you sleep. Build a portfolio of income-producing assets (stocks, bonds, real estate, etc.) and continually reinvest the income from those assets.

Eventually, compounding growth combined with diligent saving and planning, will get you to where you want to go.

Balance spending with income

You can only cut spending so much, but income has no limits makes for a great sound bite, but it’s not a self-contained strategy. Understand that its meaning is more nuanced.

Yes, income is theoretically unlimited, but given finite assets over a finite lifetime, there are practical limitations to what we can reasonably achieve. Otherwise, we’d all be billionaires by age 30.

Nothing ventured, nothing gained

I do not mean to dissuade you from looking for ways to increase your income. In fact, I encourage you to go for it! Create additional sources of revenue, pursue a side hustle, and chase that golden goose.

As boxing trainer Micky extolled Rocky Balboa while chasing his dream, “You’re gonna eat lightning and you’re gonna crap thunder!”

But just in case you can’t catch that lightning in the bottle, do make sure your financial planning is balanced between income growth and conscious spending. Do not put all your attention on the former to the exclusion of the latter.

As with most financial advice, get past the sound bites and rules of thumb. Roll up your sleeves, educate yourself, work hard, and never stop learning.

As always, invest often and wisely. Thank you for reading.

The content is for informational purposes only. It is not intended to be nor should it be construed as legal, tax, investment, financial, or other advice. It is merely my own random thoughts.

January 19, 2024

Leverage Is a Powerful Tool

Leverage (borrowed money) is a simple strategy so you can use a small amount of your capital (combined with the borrowed cash) to make a larger investment.

It’s a convenient financing tool, but it won’t turn a bad investment into a good one. Leverage simply magnifies the outcome—good or bad. The benefit of using OPM (other people’s money) to skinny down the amount of cash you need to get into an investment might improve your cash flow in the short term, but that’s not the whole picture.

Infrequently, and usually without much warning, credit evaporates, margin calls happen, and leverage can become financially fatal.

With excessive leverage it’s like a financial game of Russian roulette: mostly you win, but occasionally you take a bullet to the head. That’s an asymmetric proposition that doesn’t make any sense to me.

A lot of investors are risk-averse and don’t use leverage, at least not in the traditional sense of directly borrowing money to invest in the market. But almost all investors do use another form of leverage: a less obvious one.

When is a million dollars, not a million dollars?

Tax-deferred growth in a Traditional IRA or 401k, as well as unrealized gains in taxable accounts, allow you to keep using more of your cash today but eventually, taxes will need to be paid. It is, in effect, an interest-free “loan” from the government.

Never forget that a significant portion of the balances in those tax-deferred accounts is not yours to spend. The government is your partner in those accounts and although it may be decades from now, your partner will eventually come calling for its share.

Leverage is anathema to long-term investing

When (not if) chaos strikes the markets, creating the highest demand for rational thinking, leverage can force irrational behavior.

At the extremes, using short-term debt to acquire long-term assets will magnify gains and losses. But either way, whether asset values increase or decrease, lenders expect 100% of the debt to be paid back.

Debt can be so disastrous it can force you completely out of the business of investing

On October 19, 1987, a day that came to be known as Black Monday, stock markets around the globe plunged. In the U.S., the S&P 500 Index fell 20.5% and the Dow Jones Industrial Average (DJIA) fell 22.6%: the largest single day percentage drop in the history of both indexes.

There are lots of reasons for the crash, but Black Monday was primarily caused by programmatic trading rather than fundamental economic problems, leading to a relatively quick recovery. The DJIA started rebounding just one month later and reached its pre-Black Monday level by September 1989.

For those investors, without significant leverage, it was a painful crash, but not a fatal blow.

For those investors using excessive amounts of leverage, Black Monday was catastrophic.

Over-leveraged investors were ruined not as a result of losing everything in their brokerage accounts, but because they lost 200% of everything. That’s the thing about OPM, the other people want to be paid back even though your investment tanked.

Leverage does not discriminate. From small retail investors to large institutional behemoths, no one is immune to its potential for ruin.

The bigger they are, the harder they fall

Leading up to the financial crisis of 2008/09, bank leverage ratios rose from about 12-to-1 in 2004 to 33-to-1 in 2008. When the housing bubble burst and markets collapsed, century-old banking institutions, some of the largest in the U.S. (Lehman Brothers and Bear Stearns) were wiped out. Several others, including JPMorgan Chase, Goldman Sachs, Morgan Stanley, and Bank of America had to be bailed out by the taxpayers.

By comparison, 2023 saw leverage contribute to only five bank failures, but the total assets of those five banks ($549b) were more than the combined assets of all 165 banks that failed in 2008 and 2009 ($544b).

Charlie Munger once said that there are only three ways a smart person can go broke: liquor, ladies, and leverage. His business partner, Warren Buffett chimed in by noting that the first two only made the list because they begin with the letter “L.”

The key to investing is that you cannot allow yourself to be forced to sell, letting someone else pull the rug out from under your feet.

Plan Accordingly

When it comes to leverage, assume the worst market conditions for your investment occur, and ask yourself if you could financially and emotionally tolerate it. If the answer is no, then you’ve got too much debt.

The best hedge against an unknowable future is prudent planning in the use of leverage. As we’ve seen throughout history, the lack of liquidity when debt comes due can turn a bad situation into a full-on rout.

Just like a chainsaw or a bottle of bourbon, leverage is a powerful tool. If used carefully and judiciously, it can make your life easier and amplify positive returns. If used indiscriminately, leverage can undermine your decision-making or worse, wipe out your investment portfolio.

Let’s be careful out there.

As always, invest often and wisely.

The content is for informational purposes only. It is not intended to be nor should it be construed as legal, tax, investment, financial, or other advice. It is merely my own random thoughts.

December 23, 2023

Is There a Santa Claus?

Virginia Hanlon, a precocious 8-year-old wrote to the New York Sun newspaper and asked the following question: “Some of my little friends say there is no Santa Claus. Please tell me the truth, is there a Santa Claus?”

Here is the Sun’s response:

Virginia, your little friends are wrong. They have been affected by the skepticism of a skeptical age. They do not believe except they see. They think that nothing can be which is not comprehensible by their little minds. All minds, Virginia, whether they be men's or children's, are little. In this great universe of ours, man is a mere insect, an ant, in his intellect as compared with the boundless world about him, as measured by the intelligence capable of grasping the whole of truth and knowledge.

Yes, Virginia, there is a Santa Claus.

He exists as certainly as love and generosity and devotion exist, and you know that they abound and give to your life its highest beauty and joy. Alas! how dreary would be the world if there were no Santa Claus! It would be as dreary as if there were no Virginias. There would be no childlike faith then, no poetry, no romance to make tolerable this existence. We should have no enjoyment, except in sense and sight. The external light with which childhood fills the world would be extinguished.

Not believe in Santa Claus! You might as well not believe in fairies! You might get your papa to hire men to watch in all the chimneys on Christmas Eve to catch Santa Claus, but even if you did not see Santa Claus coming down, what would that prove? Nobody sees Santa Claus, but that is no sign that there is no Santa Claus. The most real things in the world are those that neither children nor men can see. Did you ever see fairies dancing on the lawn? Of course not, but that's no proof that they are not there. Nobody can conceive or imagine all the wonders there are unseen and unseeable in the world.

You tear apart the baby's rattle and see what makes the noise inside, but there is a veil covering the unseen world which not the strongest man, nor even the united strength of all the strongest men that ever lived could tear apart. Only faith, poetry, love, romance, can push aside that curtain and view and picture the supernal beauty and glory beyond. Is it all real? Ah, Virginia, in all this world there is nothing else real and abiding.

No Santa Claus! Thank God he lives and lives forever. A thousand years from now, Virginia, nay 10 times 10,000 years from now, he will continue to make glad the heart of childhood.

From the New York Sun editorial page, published on September 21, 1897, and reprinted annually until the newspaper ceased operations 52 years later.

I’ll be back to writing about personal finance in the new year and may it be a prosperous one for all!

As always, invest often and wisely.

(If you previously subscribed but are not seeing my email newsletter, please check your spam folder [or Promotions tab] and mark this address Cosmo’s WYW Insights as ‘not spam.’ Thank you, and please share this newsletter with a friend.)

December 8, 2023

From Reflection to Action: A Year-End Financial Tune-Up

Planning is everything

With 2024 fast approaching, it’s an opportune time to revisit and reassess your financial goals and your strategy to reach them.

Take a moment to reflect on where you spent money this year, and how much. Consider jotting down the details for a clearer perspective.

Did you stay on budget or find yourself spending more than planned? Whether it was home improvements, a memorable vacation, or contributing to college savings accounts, did you achieve your family’s financial goals?

Also, consider what changed in your life this year. Births, marriage, divorce, and retirement can all have an impact on both your spending and your overall strategic financial plan.

Don’t have a plan? This is a great time to create one. Be honest with yourself. Whether money is tight or you find yourself with a surplus, build a financial plan to better align spending with your near-term priorities and longer-term goals.

As we discussed here, true financial freedom is having enough. Without goals and a plan, quantifying ‘enough’ is exponentially harder if not impossible.

PCR: Plan, Course-correct, Repeat.

Check in on your investments

Cash and your emergency fund

If you tapped into your emergency fund during the year, it is a good time to refill it, or if you don’t have an emergency fund, start one. Having these funds at the ready can help you cover surprise expenses, such as car repairs or medical expenses, without relying on high-interest credit cards or selling long-term investments.

Is your cash working for you? While borrowing rates are up, so too are savings rates. With today’s money market funds and CDs paying 5%+, your cash can provide not only an emergency cushion but a very reasonable return as well.

Top off retirement contributions

If your financial situation allows, it may be a good idea to increase your contributions to your retirement account(s). This can be a good annual practice until you’re contributing the maximum amount allowable to an IRA, 401(k), 403(b) or their Roth counterparts.

For example, if you have access to a 401(k) through your employer, you’ll have until the end of the year to contribute up to the $22,500 limit for 2023. People above the age of 50 can make additional catch-up contributions of up to $7,500 for a total of $30,000.

If you have a health savings account (HSA), consider maxing-out that contribution as well--$3,850 for an individual and $7,750 for a family. Whether you use the HSA for long-term saving or near-term spending, it is triple tax-advantaged: Funding is tax deductible, growth isn’t taxed, and withdrawals are tax-free if spent on qualified medical expenses.

(Pro-tip: If you are a prodigious accumulator of wealth, most HSA plans have investment alternatives but research has found that only 12% of account holders invest in assets other than cash. Think about your options.)

The tax advantages all these accounts offer can help your money grow exponentially over time.

Tax-loss harvesting

As you are plotting year-end moves, inevitably you will hear about investors considering tax-loss harvesting in their taxable brokerage accounts. “Harvesting” refers to the selling of investments at a loss to offset capital gains from other investments. You then use the sale proceeds to buy a different investment so overall you stay invested in the market. The last point is critical—it’s what distinguishes the harvesting strategy from market timing.

(Pro-tip: Harvesting can help minimize taxes, but be mindful of something called a “wash sale.” The IRS is fine with you selling at a loss, but it doesn’t like it when you sell at a loss and then quickly buy back the same investment (or a ‘substantially identical’ investment). In fact, buying back the investment within 61 days (beginning 30 days before the sale and ending 30 days after the sale), can trigger a wash sale and defer the loss. The wash sale rules are tricky, speak with a professional.)

It’s also a good time to pause and reflect on the premise of this strategy. Harvesting implies you have losses to be harvested. With the markets once again approaching all-time highs, why do you have underwater investments in the first place?

Think about it. If you had been purchasing “the market” (e.g., an S&P 500 ETF or similar broad-based index funds), then you would not have a significant loss on your fund shares since the market is approaching its highest level now!

This means that losses you do have are likely in your individual stock selections. This is just a friendly reminder that picking individual stock winners is difficult (even for professionals) and a humbling experience.

Charitable giving

Bunch your donations

If you plan to donate the same amount of money each year, consider “bunching” the donations into a single year. This could increase your potential itemized deduction for that year.

(Pro tip: For large gifts, consider using a donor-advised fund to spread out the giving while simultaneously taking advantage of “bunching.”)

Donate appreciated assets

If you have large, unrealized capital gains, rather than selling and donating the cash, consider donating the appreciated assets. If you itemize, you can deduct the full fair market value of the appreciated assets, and you won’t need to report the gain as taxable income.

Block out the noise

This month the ‘news’ stories will start to appear touting the “best-performing investments of 2023.” Making portfolio decisions based on headlines is like buying a house based on the color of the front door.

Don’t chase the hot hand, the hot stock, the hot story. Stay calm and remain cool. Have faith in your planning process.

Don’t be too quick to jump into the high flyers or dump the underperforming ones. Twelve months seems like a long time but with investing, that’s a short look. Often, today’s shooting stars become tomorrow’s laggards and vice versa. There are good reasons for changing between investments but chasing performance isn’t one of them.

Above all, remember that investing is a tool, not a plan.

Review (or create) your financial plan, make any necessary adjustments, and then get back to living your best life now.

As always, invest often and wisely.

The content is for informational purposes only. It is not intended to be nor should it be construed as legal, tax, investment, financial, or other advice. It is merely my own random thoughts.

(If you previously subscribed but are not seeing my email newsletter, please check your spam folder [or Promotions tab] and mark this address Cosmo’s WYW Insights as ‘not spam.’ Thank you, and please share this newsletter with a friend.)

November 17, 2023

Is it Your Income or Spending Calling the Shots?

The paycheck-to-paycheck tango is familiar to many, and it has a common refrain: ‘If only I made more money.’ But is this dance a result of an income shortfall or spending habits gone astray?

Let’s say you meet an extremely successful professional who earns $1 million every year, spends $1 million every year, and is lamenting the fact that they can’t save a dime for retirement. They are living paycheck to paycheck. After you get through feeling sorry for them, would you suggest this person doesn’t make enough or rather spends too much?

The answer seems obvious: Income level looks mighty fine so that person should rein in their spending, put some money aside, and invest it for the future.

What about a person who makes $65,000 per year and spends $65,000 per year? The common refrain, ‘If only I made more’ quickly springs to a lot of minds but that shouldn’t change the overall thought process. Rather than jumping on the ‘income too low’ side of the equation, give the ‘spends too much’ side its due.

A two-sided struggle

The struggle to make ends meet is real, but the reason why shouldn’t start with the blanket assumption that everything spent is absolutely necessary and so by default, it must be an ‘income too low’ problem.

Living paycheck to paycheck is influenced by a combination of both income and spending factors. It's essential to consider each side of the equation when addressing financial challenges.

On the income side, individuals may face difficulties if their earnings are insufficient to cover ‘necessary’ expenses. This could be due to factors such as a low-paying job, limited work hours, or unstable employment.

On the spending side, it's important to assess whether expenses are aligned with one's income, which includes recognizing the difference between ‘necessary’ and ‘nice-to-have’ expenditures. Overspending on non-essential items, accumulating high levels of debt, or not budgeting effectively can contribute to living paycheck to paycheck.

Spend on the future

The income side might be tough to adjust, but it’s not impossible. For example, you might explore new job opportunities, negotiate a salary increase, or start a side hustle.

When you look at spending, recognize that once basic needs are covered, you are left with personal choices. If left unchecked, those choices often default to spending on items today which in effect is choosing not to ‘spend’ on saving for the future.

In 2000, a study on wealth accumulation noted that many Americans say they earn just enough to get by and struggle to get caught up on bills, implying they don’t earn enough to also save money (not unlike today):

Yet in other developed countries, the savings rate at all income levels is much higher than in the United States. Even in Canada—in many respects similar to the United States—the personal saving rate is almost twice as high as in the United States. Such international comparisons alone suggest that saving depends on much more than lifetime earnings.

While savings rates among countries have been shifting since this study was published, the key takeaway has not changed. Your savings rate is heavily dependent on your personal spending choices and is the single most important factor impacting your lifetime wealth accumulation journey—especially in the early years.

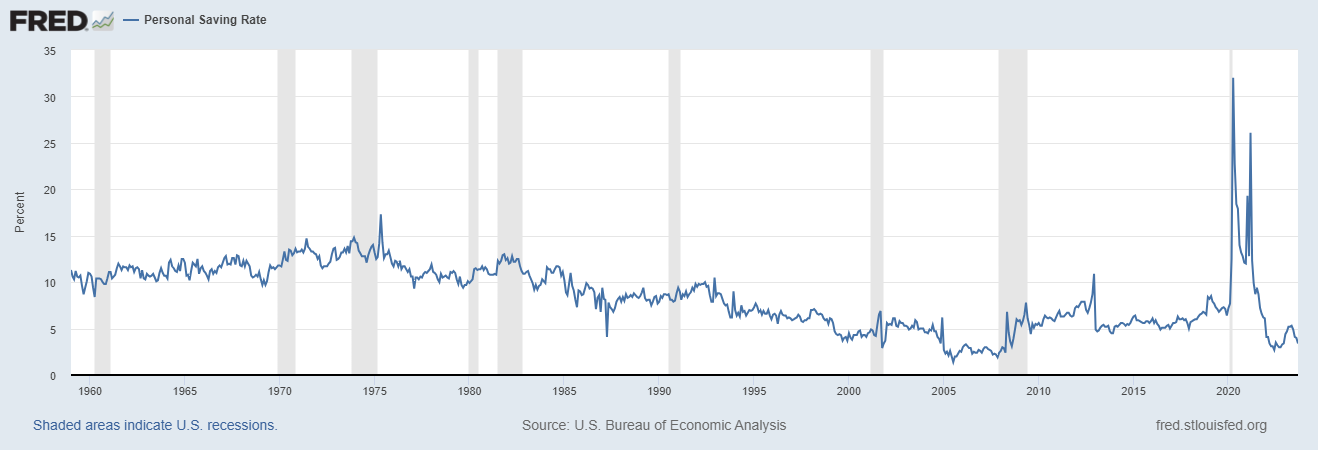

The recent trend has not been encouraging. The personal savings rate (which since 1960 has averaged 8.8% of disposable income) is getting close to an all-time low.

In September 2023, the saving rate was 3.4%, less than half the long-term average and continuing a 6-month downward trend.

Monthly US Personal Savings Rate: 1959-2023:

Get up and dance

You can use ‘I don’t make enough’ as an excuse or as a call to action.

Yes, life is expensive (as we discussed here), but by giving equal weight to both sides of the income/spending equation, you can see with clear eyes all your cash flowing in and out, and make better-informed decisions.

Find the balance that works for you—managing expenses sensibly, increasing income where possible, and developing a financial plan that aligns with both short-term needs and long-term goals.

When saving and spending bring you equal happiness, you are well on your way to breaking the cycle of paycheck to paycheck.

As always, invest often and wisely.

The content is for informational purposes only. It is not intended to be nor should it be construed as legal, tax, investment, financial, or other advice. It is merely my own random thoughts.

(If you previously subscribed but are not seeing my email newsletter, please check your spam folder [or Promotions tab] and mark this address Cosmo’s WYW Insights as ‘not spam.’ Thank you, and please share this newsletter with a friend.)

October 27, 2023

Generalization In A Specialized World

Opening your mind to thinking outside the box begins by acknowledging that you are inside a box.

Our experiences shape our ideas, beliefs, and our world view. The narrower our experiences, the smaller the box and the more confined that view remains.

A deep generalist or broad specialist

Many people advocate for deep specialization, arguing that it allows for the mastery of a particular field gaining a thorough understanding of its complexities and nuances.

Others champion the idea that a broader view enriched by varied experiences can lead to more informed and adaptable solutions.

There is merit to both views and most valuable when understood as mutually inclusive.

Specialization can indeed lead to a high level of expertise in a specific area, which can be invaluable when dealing with intricate financial concepts, investment strategies, or economic analysis.

The drawback of deep specialization without a broad perspective, however, is the risk of tunnel vision. Deep expertise tends not to cultivate broader thinking. If your toolbox contains only a hammer, then all your problems begin to look like nails.

Interdependence

Financial planning is inherently interconnected with other aspects of life, and a purely mathematical approach will fail to address the full spectrum of a person’s needs and aspirations, wants and apprehensions.

Specialization is easier to understand—keep marching forward on the well-traveled path. If mathematicians are faced with a defined problem with fixed parameters, they continue applying mathematical laws until they arrive at the correct answer. This rules-based thinking is remarkably efficient in linear domains such as math, chess, or golf.

When you add ambiguity and uncertainty, however, stringent rules-based decision-making falters, and broader thinking becomes increasingly important.

Leading up to the 2008 global financial crisis, we had regulators for lots of specialties: banking and capital markets, securities, insurance, consumer rights, mortgages, real estate, etc. But credit lending packaged inside of innovative securities (at the very heart of the crisis) spanned all those domains and there was no regulator for that.

The siloed approach to regulation missed this linkage and was blind to the cascading failure that not only cut deep but across the varied financial disciplines.

Make a connection

There is a theory in cognitive science called connectionism which has advanced our understanding of the human mind. Connectionist models, inspired by neuroscience, psychology, and computer science, propose that cognitive processes can be explained by interconnected networks of simple processing units, akin to neurons in the brain.

These networks learn and adapt through the adjustment of connections, much like how our brains form and strengthen neural pathways.

Online platforms like Netflix, Amazon, and social media networks use connectionist models to analyze user behavior and preferences to personalize content recommendations. Connectionism is also a fundamental factor in the exploding field of artificial intelligence and deep learning.

Mental models

Extending the concept of connectionism, mental models are cognitive frameworks used by people to understand and interact with their environment.

A mental model is an explanation of how something works that we can easily carry around in our head.

They are powerful thinking tools. They improve the way we reason about issues, help us solve problems, make decisions, and understand life more fully.

Mental models are not about what to think but rather how to think, incorporating the best of specialization with a broad perspective.

For example, supply and demand is a mental model that helps us understand how the economy works. Compound interest is a mental model that helps us understand that investment returns and time both matter. Margin of safety is a mental model that helps us understand that things don’t always work out as planned.

Worldly wisdom

Rote memorization of facts will not lead to genuine understanding. Layering these facts upon a latticework of mental models combined with your experiences, both firsthand and observed, integrates the data with life.

This latticework approach, championed by legendary investor Charlie Munger, involves developing a diverse set of mental models from various fields of study. Munger describes this approach as “worldly wisdom” that helps an individual make better decisions in a wide range of situations (not limited to investing).

Mental models to add to your toolbox

Here is a sample of mental models from wide-ranging disciplines that can help with our financial life.

Physics: This natural science teaches us that complex adaptive systems are continuously adapting and all such systems, including the stock market, can never reach a state of perfect equilibrium. Even at times of relative calm, the market and market participants are in a permanent state of flux.

Biology: Economies, industries, and individual companies may trudge along without noticeable changes, but invariably change happens. Gradually or sometimes suddenly, the familiar paradigm shifts and quite often collapses.

Sociology: When we realize that all market participants constitute a group, it becomes obvious that understanding group behavior is a precursor to understanding why markets and economies behave as they do. Bubbles and busts are driven more by herd mentality than market fundamentals.

Psychology: Modern portfolio theory is predicated on rational market participants. But in reality, the financial markets witness a daily exchange of fear and greed as people trade based on their emotions.

Literature: Read intelligently. If you find that you can easily grasp the content of what you are reading, you are essentially stockpiling information. When you read something that compels you to pause, reflect, and reread to clarify your understanding, it’s likely that this process is deepening your insight.

Reading history, for example, can teach us where we have been and provide clues to where we might be going. (I discussed learning from market history here.)

Reading intelligently not only makes you smarter, it encourages you to maintain a healthy skepticism, rather than unquestioningly accepting every bit of information at face value.

Don’t go through life with your eyes wide shut

For many individuals, personal financial planning is bewildering, and investing often turns into a frenzied pursuit of the perfect strategy. Blindly racing down a well-worn path, however, is not always the best solution.

People who constantly survey in all directions for insights will find themselves making more enlightened choices and navigating a path that better aligns with their personal goals.

Whether your perspective is that of a generalist or a specialist, the ultimate goal of attaining wisdom is to change a closed mind into an open one. If you aspire to be a better investor, thinker, and person, cultivate open-mindedness, be inquisitive, show enthusiasm, stay true to your core values, and read intelligently every chance you get.

As always, invest often and wisely.

The content is for informational purposes only. It is not intended to be nor should it be construed as legal, tax, investment, financial, or other advice. It is merely my own random thoughts.

(If you previously subscribed but are not seeing my email newsletter, please check your spam folder [or Promotions tab] and mark this address Cosmo’s WYW Insights as ‘not spam.’ Thank you, and please share this newsletter with a friend.)

October 6, 2023

Life Is Expensive: How Do People Do It?

It all begins with understanding this simple and absolute truth: You will not accumulate any measure of wealth or even get your head above water if you don’t spend less than you earn.

To reach financial security you first need to become a savvy saver.

Break the cycle of paycheck to paycheck

Do you feel like you earn just enough to get by and struggle to get caught up on bills? Reevaluate by tracking your expenses.

I know it sounds tedious and boring but if you don’t know where your last dollar went, it’s hard to plan where your next dollar will go. Tracking improves your money perspective.

Write down all your spending for the next 90 days. Be meticulous. What can you reduce or cut out? What might you be able to spend more on? Three months of spending detail should give you a solid base to start making better-informed decisions.

Don’t think of saving as sacrificing. Think of it as spending today to buy your financial security. Just ask yourself one question: What am I willing to pay for it?

Take control of your money. It might feel overbearing even awkward at first, but if you want the rainbow, you must endure the rain.

Do you want to live or merely survive?

If you are tired of feeling behind, start doing the things that will get you ahead. Live below your means. Spend less than you earn and be deliberate with the difference.

First, use the difference to build an emergency fund. Three to six months of spending needs in ‘safe’ cash investments (e.g., bank savings, CDs, or a money market fund).

Second, work on paying down any high interest rate debt (e.g. credit cards, store cards, etc.). Pay more than the monthly minimum. Stop using debt to finance your living expenses. Given enough time, even a small leak can sink a large ship. So, if you find yourself in a debt hole, quit digging.

Last, once the emergency fund is in place and your debt is under control, go hard at investing. Keep it simple. Start with a low-cost index fund like Vanguard’s Total Stock Market Index Fund (VTI). The key is to add to it every month.

When it comes to reducing debt and investing, each is a powerful way to accumulate wealth and equally important enough to do both at the same time.

Wealthy is not a destination, it’s a habit

Answer two questions. First, can you afford to save $5 per month? – I’m willing to bet your answer is a resounding, I can do that. Second, can you save $5,000 per month? – an equally resounding, no way.

Well, now we have established a range: somewhere between $5 and $5,000, you can start (or increase) your monthly savings.

Those of you who are thinking “But $5 won’t get me anywhere” are missing the point. It’s not about the $5. It’s about the habit of the $5. Every month without fail you save and invest.

It’s a small first step. Followed by another step, and then another. Eventually, as you progress, you will develop the desire to increase your monthly savings. Good financial habits beget good financial habits.

Taking steps in the right direction rarely ends up in the wrong place.

Don’t let your spending upkeep be your savings downfall

How much money you make isn’t nearly as important as what you do with the cash. Early on you have more control over what you spend than what you earn, so focusing most of your efforts there will produce better results.

Be disciplined to live on less than you earn, and be patient and secure in the knowledge that compounding returns will work for you over time. Forge good money habits so that bad habits don’t have a chance to take hold and weigh you down.

Then, when your income rises or you get a bonus, you’ll have a fighting chance to save and invest a sizable portion of it while also minimizing lifestyle creep— ‘too much month at the end of the money.’

Flip the script

There is a negativity bias in psychology. We and the news outlets tend to dwell more on the negative than the positive. It’s a lot easier and more attention-grabbing to report on something going suddenly wrong than something going slowly right.

Developing good money habits refocuses us to embrace the journey rather than dwelling on how we’re feeling on a random day.

Just like when you are searching for a city to move to, focus on the climate not today’s weather.

Habits of the wealthy

The wealthy focus on the positive over the negative and keep the complaining to a minimum. They think long-term, have well-defined and realistic goals, work hard, eat healthy, exercise regularly, maintain a trusted social network, get a good night’s sleep, save and invest monthly, and oh yes, enjoy their spending.

Intelligent people know what to do. Intellectually curious people learn how to do it. But successful people are the ones who actually do it—repeatedly without fail. PCR: Plan, Course-correct, Repeat.

Just. Get. Started.

What you just read might be mildly entertaining, maybe thought-provoking, but it will be utterly useless if you take no action.

Dare to try. Dare to believe in yourself. Dare to just do it. Or not.…the choice is your responsibility, and so too are the results of your actions (or inaction).

Following this get-comfortable-slowly path might not make you rich, but it will likely keep you from ever being poor.

As always, invest often and wisely.

The content is for informational purposes only. It is not intended to be nor should it be construed as legal, tax, investment, financial, or other advice. It is merely my own random thoughts.

(If you previously subscribed but are not seeing my email newsletter, please check your spam folder [or Promotions tab] and mark this address Cosmo’s WYW Insights as ‘not spam.’ Thank you, and please share this newsletter with a friend.)

September 15, 2023

Weathering Financial Storms: Navigating Tail Risk with Confidence

We spent the better part of a decade discussing whether the Fed and world banks would move interest rates to 0% or even negative to keep economies chugging along. But then a virus quite literally shut down the global economy with 114 million job losses worldwide. The shock of those lost working hours was four times greater than that of the global financial crisis. Suddenly, without warning, interest rates were among the least of our problems.

Tail risks (commonly referred to as ‘black swans’ thanks to the work of Nassim Nicholas Taleb) are characterized by their extreme nature, unpredictability, and the substantial impact they can have on investment portfolios and the overall economy.

This unpredictability in the financial markets leads to the black swan paradox: No matter how remote the possibility, investors cannot rule out events just because they haven’t seen them before. Because sometimes, stuff just happens.

Imagine your investment portfolio as a ship navigating the tumultuous seas of the financial market. While smooth sailing is the aspiration, a storm or rouge wave can arise suddenly, posing a threat to even the most well-constructed plans. This is where tail risk hedging comes into play.

It's not about avoiding risk altogether. It's about strategically mitigating the impact of extreme, unforeseen events that could capsize your financial voyage. By implementing a carefully crafted tail risk hedging strategy, you're essentially fortifying your portfolio against worst-case scenarios while preserving the potential for growth.

Good defense leads to good offense

Strategic risk mitigation is about reducing systematic risk in a portfolio through asset deployment that is thoughtfully evaluated rather than simply letting dynamic market activity alone dictate your portfolio results.

Contrast this with a tactical allocation which is an attempt to reduce systematic risk by actively moving in and out of certain ‘safer’ allocations, with the lofty goal of avoiding the opportunity cost of that safety when the markets are up.

Such a tactical approach to risk mitigation is a dichotomous one. Sometimes referred to in the industry as moving the portfolio between “risk on” and “risk off.” It’s analogous to buying insurance, later canceling the policy, then buying insurance again. Doing this cost-effectively, by definition, requires market timing and the ability to accurately forecast the near-term.

Effective risk mitigation, however, should never require forecasting. In fact, we seek to mitigate risk precisely because the future is inherently unknown and unknowable. If we could accurately predict the future, we wouldn’t have risk to mitigate!

All risk mitigation strategies ultimately require a tradeoff between the degree of loss protection provided (stuffing cash in a fireproof vault provides a lot of protection), versus the opportunity cost of allocating capital to the protection rather than to the rest of the portfolio (the vault also provides zero growth).

Asset allocation

A 60/30/10 (stock/bond/cash) portfolio allocation is a simplistic example of a strategic allocation to mitigate risk, specifically the risk that the stock market drops at a time when you need to withdraw money.

A tactical approach might say I’ll start with 60/30/10 then when I feel the market turning, I’ll move to 80/20/0 or 20/60/20 or whatever the flavor of the day is. Unfortunately, this requires market timing and accurate forecasting which as we noted above, is highly unlikely.

Therefore, the better we are at designing and implementing our strategic, cost-effective risk mitigation policy, the fewer tactical levers we will need to pull on, and the better off we will be.

Portfolio diversification

Another strategy to mitigate black swans is to diversify not only between asset classes (e.g. stocks and bonds) but also within asset classes. For example, rather than picking a handful of individual stocks, consider investing in a broad-based index fund that holds hundreds of individual stocks. (For more on diversification, see my previous article here).

More exotic strategies

There are other risk hedging strategies such as purchasing put options or other derivatives that provide insurance against extreme market drops. While effective, these strategies can come at a high cost due to the premiums associated with options and the ongoing maintenance required.

The message from all of this is that we are not attempting to raise our compounded return by taking greater risk. We are attempting to raise our CAGR over time by lowering the effect of risk—that nasty tail risk with the catastrophic aftermath.

Successful investing isn’t about waiting for the stormy seas to calm. It’s about learning to ride the waves.

Our risk mitigation strategy should allow us to weather any storm—including no storm at all. We strive for a reasonable return during calm weather with the ability to shelter us from the effects of the tail risk storms that unpredictably but invariably arrive.

Arguably, tail risks are the only risks that matter since they are the kind that can destroy your capital base and knock you out of the investment game permanently.

If the stock market were to suddenly drop 30-50% in the near term, are you and your portfolio prepared to ride it out? If not, today is a good day to reevaluate your black swan mitigation strategy.

Our wealth accumulation voyage is a long one, and in order to reach the sunny shore of financial freedom, you first need to survive the storm.

As always, invest often and wisely.

The content is for informational purposes only. It is not intended to be nor should it be construed as legal, tax, investment, financial, or other advice. It is merely my own random thoughts.