J. Bradford DeLong's Blog, page 2138

December 13, 2010

There Are at Most 13 Deficit Hawks in the Senate

A deficit hawk is somebody willing to vote against bills that increase the national debt--that do not contain within themselves provisions to recapture revenue and cut spending that lead to a reduction in the projected national debt within, say, ten years.

There are at most 13 deficit hawks in today's U.S. Senate:

Bipartisan support as tax deal advances in Senate: By James Politi in Washington: The deal struck by the White House and Republican leaders to prevent the expiry of Bush-era tax cuts advanced with overwhelming bipartisan support in its first vote in the Senate, building momentum in favour of the legislation.

The agreement would extend income tax rates for two years and unemployment benefits for 13 months, while cutting the payroll tax by 2 percentage points. It would deliver an extra $200bn in fiscal stimulus to the economy compared with economists’ expectations and bolster growth in 2011, but it would add to the US debt burden.

The margin in the procedural vote to end debate, known as “cloture”, was comfortable. By the evening, at least 82 of 100 senators had voted in favour of the deal, with 13 against. The vote paves the way for final passage by the Senate as soon as Tuesday and makes it harder for House of Representatives members to oppose it this week...

Lawrence H. Summers: Farewell Address at the Economic Policy Institute

It's a pleasure to be here at EPI this morning.

For 25 years, your distinctive and important voice has helped underscore in our national debate the central importance of economic policies that support a growing, striving, proud American middle class. It is by what happens to the middle class that our economic policies have to be judged. Success for the middle class means:

A better life for our citizens

Upholding the 250 year American tradition of children whose lives are better than their parents'

And central to America's continuation as a role model for the world.

I want to say a brief word about what we have done over the past two years to strengthen the economic position of the middle class, and then turn to what I see as the great challenges that we face in the years ahead if the American economy is to work for all our people.

Just as scholars continue to debate how close we came to nuclear conflict during the Cuban missile crisis, they will continue to debate just how close the American financial system and economy came to all-out collapse in the six months between September of 2008 and April of 2009. What we do know is:

That during that time the stock market fell more sharply than in the six months after Black Tuesday in 1929

That global trade declined more rapidly than in the first year of the Great Depression

And that the economy was not self equilibrating and that a variety of vicious cycles were pulling it down even deeper, at a rate of 700,000 jobs a month at the worst of it.

Had it not been for President Obama's willingness to support a sufficiently aggressive response – from the late stage of the presidential campaign to his first days and months in office – I have little doubt that we would be looking at a vastly different world today. His stalwart advocacy of efforts to support the economy through the Recovery Act, to rescue the financial system, to ensure the health of key industries, and to maintain stability in the global system halted the vicious cycles in less time and at less cost than virtually anyone thought possible.

Yet, while the economy may be out of the intensive care unit, the patient now faces the long road of not just recovering from previous affliction but beginning to address chronic ailments. The slow process of recovery has caused some to conclude that perhaps we have entered a new and weakened normal state of affairs – a state in which we must lower our sights, lower our aspirations, and not be able to pass on to the next generation the kinds of dramatic improvement in American economic potential that were passed down to us.

President Obama rejects this view, and so should the rest of us. With the right approach, we can and we will resurrect, rebuild and renew the American economy. To do this, we need to do two profoundly important things in the years ahead. Both are necessary, neither is sufficient.

First, we must generate forward momentum in the economy to fully recover from the Great Recession, and second, we must put in the place a framework that assures that our growth, productivity and living standards remain an example to a rapidly changing world.

First, we must do everything we can to ensure that this recovery is as rapid as possible. Without rapid recovery, every other one of our goals will be compromised. In the absence of recovery, there is no prospect of reducing medium-term budget deficits while simultaneously increasing investments in our human capital, without which we will not compete successfully with the rest of the world or grow living standards for the middle class, and above all, putting the 8 million Americans who should have jobs back to work.

What is holding our economy back?

When unemployment has been above 9% for 19 straight months,

When the job vacancy rate is at near record low levels,

When 8 million houses and countless square feet of office and retail space sit empty,

When capacity utilization in the nation's factories and on its railways and highways is nearly as low as it has been in any period since the Second World War,

There cannot be any question that the constraint on our economy now and for the next several years will be lack of demand.

I am under no illusion that increased demand alone is sufficient to restore America's economic health, but it is an unquestionably necessary component of a full recovery. Unfortunately, the approaches we have become used to over the last fifty years for supporting demand in a market economy are not open to us today. Base interest rates cannot fall below their current level of zero. And, in the face of excess capacity and excess debt, it is not clear that, even if they were possible, falling interest rates would be effective in convincing consumers and businesses to spend more.

We need non-traditional approaches.

Take exports. It is always the case that when we export more successfully we are more prosperous. But when the economy is demand-constrained as it is now, increases in exports have a more potent effect because with excess capacity more exporting does not mean less of anything else. That is why agreements like the one we recently concluded with Korea are important, as is the breadth of the support it has received. It is also why the President has set a goal of doubling our exports over the next five years and pointing to ways we can do so:

Enforcing our trade agreements,

Relaxing export controls,

Standing up diplomatically for American producers,

And insisting in global fora on the rebalancing of the global economy.

Promoting exports, though, will not be enough to assure adequate demand.

In the decade prior to the current downturn, the American household and business sectors, if you added them together, spent close to two percent of GDP more than they earned. They were net borrowers. As a consequence of the developments of recent years, this situation has changed dramatically. Private spending now falls nearly 6 percent short of private sector income. That means to private sector has swung in its deficit by about 7.5 percent from about a two percent deficit to a little less than a six percent surplus. That swing, all of which means less demand, is one of the reasons we are suffering the aftermath of the worst recession in 50 years.

It is right and necessary for government to counteract private sector deleveraging. Even with all the fiscal measures of the last several years, total borrowing in the American economy has failed to grow for the last 2 years. That is the first two year period since the Second World War when total borrowing in the U.S. economy has not increased. Let me be clear: Even with our deficits, the amount of extra debt is less than the amount of reduced borrowing in the private sector. Increased federal borrowing has offset, but only partially, deleveraging in the private sector. This is why the recent tax agreement concluded between the President and congressional leaders is so important. It averts what could have been a serious collapse in purchasing power and adds far more fiscal support than most observers thought politically possible through:

An extension of unemployment insurance,

A payroll tax holiday,

Refundable tax credits and business expensing.

That's why independent estimates of job creation over the next year or two are being revised up by 1.5 million or more.

These measures not only support jobs but also our medium-term goal of deficit reduction. By retiming allowances, business expensing actually raises revenue collections after 2013. Accelerating recovery, the additional effect of these measures, is the best form of deficit reduction. Indeed, a one percent increment to GDP in 2013 or any year afterward reduces the deficit by more than $40 billion.

To be sure, this legislation is a compromise. The President strongly opposed continuation of the high-income tax cuts and especially opposed the estate tax relief that benefits only 6,400 of the country's least needy families. These concessions were the price exacted by the Congressional minority for the fiscal support that will provide a significant impetus to the economy. But be clear that compromises that were necessary with a weak economy in 2010 should be inconceivable as recovery accelerates in 2012.

Now the extraordinary gap that I referenced a moment ago has opened up between private saving and private investment. The tax compromise will help, but it is not enough. At a time when real interest rates even over 30 years are less than 2 percent, at a time when construction unemployment is nearly 20 percent, and at a time when building material costs are depressed, what better time to invest in renewing and upgrading our nation's infrastructure – working off a backlog of deferred maintenance and insufficient investment? A substantial, sustained effort to rebuild America should be at the top of Washington's priority next year.

These measures, taken together, will accelerate recovery. Accelerating recovery and increasing demand will mean more workers with jobs, more employers in a position to provide training, more capital investment in capacity for the future, more revenues for state and local governments to make the investments that are crucial for them. Without increased demand we are not in a position to pursue our longer-term objectives.

In a demand constrained economy like the one we have today and will have for several years, economics is turned topsy-turvy. As Keynes pointed out in his celebrated Paradox of Thrift, individual efforts to save more lead to less total saving. More educated workers get jobs but with demand constraints those job opportunities come at the expense of their less educated neighbors. With demand constraints, increases in productivity may act to exacerbate deflationary pressures and increases in efficiency may result in more unemployment rather than more output. That is why we have to drive recovery and remove the demand constraint on the economy.

At the same time, it is essential that we recognize that fiscal and monetary policy or increases in demand never made a society prosperous, fair, or strong. We need to renew the American economy for a century that will be very different from its predecessor. A key lesson that management strategists have distilled for businesses is this: you don't succeed by producing exactly the same thing that other people are producing in the same way just at a lower cost. You succeed, by establishing your own uniqueness and excellence. Think of the distinctiveness of products like Google's search engine; the iPad or a Harley-Davidson. Think of the distinctive way that Southwest or Nucor or even Walmart deliver their products and services. The United States has led the global economy by building on its unique capacities. By building on our distinctive strengths, we can continue to lead in the next century.

There is no going back to the past. Technology is accelerating productivity in mass production to the point where even China has seen manufacturing employment decline by more than ten million jobs over the most recent decade for which data is available. We are moving towards a knowledge and service economy.

Another inescapable truth is that the world is shrinking. When I worked in Jakarta just 30 years ago I tried to follow the Red Sox. When the Red Sox played on Tuesday night, I learned how they did on Friday because I had to wait until the Herald Tribune arrived days later. It is a different: a smaller world. What does it mean to adapt to this? Just as the American North prospered even as the southern part of the United States caught up, even as we drew strength in the generation after World War II as Europe and Japan's economies converged towards our own, we will need to find ways to prosper as the emerging markets of the world take their place on the global stage.

What should our approach be? Some suggest that we have no alternative but to compete with the world on price even if it means striving to win races to the bottom.

They would have workers sacrifice wages, benefits, and bargaining rights to hold onto their jobs.

They would slash taxes on businesses even as their profits rise in order to lure them to stay in the United States.

They would shred social safety nets in the name of self-reliance.

Such Social Darwinism was bad morality and bad economics in the 19th century and it is no better in the 21st.

Consider this: The flatness of the world notwithstanding, by far the largest part of the activities Americans engage in and the goods they buy remain quite local. It is health care and retail services, recreation and education, haircuts and insurance policies, hotels and houses and I could go on. Moreover, where we compete with other countries, our strength is collective. Few of us can hope to succeed as individuals in a global economy where any particular task or skill can be purchased at very low prices in much of Asia and beyond. Rather, our strength must come from establishing uniqueness, establishing that which is difficult to replicate, that which comes from more collective action. Any idea or machine or even individual capacity can be transplanted. Far harder to transplant, imitate, or emulate are our great institutions – the national laboratories and the national parks and the national highway system, great universities and great cities and great technology clusters, a diverse culture, deep capital markets, and a tremendous ethic.

Where competition is concerned, the lesson for us as a nation is the same as the lesson for business: far better to compete by innovating, leading, and competing on strength, than by standing still, and reducing prices. Let me highlight what I see in this regard as the three essential priorities for the years ahead. President Clinton used to say that in a world where ideas can move, capital can move, a nation's distinctive strength lay in its people. Our biggest failing as a nation over the last 50 years has been with respect to education. We were once the envy of the world; now we struggle to get into the top half of OECD nations. The Duke of Wellington famously observed that the Battle of Waterloo had been won on the playing fields of Eton, and I would suggest that in this less elitist age, the battle for America's future will be won or lost in its public schools. For too long we have been caught in a sterile debate between those who believe in more accountability and those who see the need for more resources. In truth, no one who has seen the conditions in our urban schools can deny the need for more resources, and no one who believes in incentives can deny the need for more accountability. Through Race to the Top the Administration has sought to reform elementary and secondary education both by providing resources and by increasing accountability. These kinds of efforts will need to be magnified in the future.

Even as we strengthen elementary and secondary education, we must also expand higher education opportunities. The US used to lead the world in the share of young people who became college graduates. It is no longer in the top ten. Worse yet, over the last generation, income gaps in this land of equal opportunity in college attendance have actually widened, as a consequence of both issues of affordability and, I would submit, issues of subtle discrimination. To take just one example, I would suggest to you that the least diverse classrooms in American are in the SAT prep schools that help some, but not all, students raise their admissions test scores. This is why the Administration has made major new investments to expand educational opportunities. Since taking office, the Administration has funded an unprecedented doubling of the Pell Grant program, which will help more than 8 million of low income students attend college, at the same time as winning enactment of the American Opportunity Tax Credit.

Let me pause on this for just a second: in less tumultuous times I would suggest to that the largest increase in federal support for college attendance by students from low and middle income backgrounds would be recognized as a signal, defining accomplishment. It is a signal of the magnitude of the issues we have contended with that this has not earned the attention it deserves. Education is closely linked with a second major priority for the years ahead: innovation, the other central pillar of economic growth. Here we have had for a very long time in the United States a distinctive ecology which is the reason we are the leading economy in the world.

On the one hand, we have recognized, venerated, and acted on the observation that it is individualists – the Edisons, the Fords, the Gates and Zuckerbergs – who, with a uniquely anti-bureaucratic temperament, who would not dream of a filing a grant application, who drive an enormous amount of the economy's progress. We have maintained a culture where it is still true today that with all our financial system's failings, and they are many, we are the only country in the world where you can raise your first hundred million without owning a tie if you have a sufficiently good idea. And that is a great strength of our economy.

But at the same time as maintaining a culture that supports the entrepreneur, that salutes the rebel, that allows people to establish themselves as major figures in business without even bothering to complete a college degree – at the same time as having support for the individual, we also recognize that fundamental innovation and progress will not happen without the public sector playing its essential role. There would be no internet without DARPA. No car industry without highways. No pharmaceutical revolution with the NIH. Maintaining and increasing our American capacity for innovation thus requires both fundamental support for entrepreneurial innovation and for the key foundations of science and technology. That's why we have to make it easier to patent a new idea or innovation; make it easier for entrepreneurs and small businesses to raise capital; make it easier for the most promising minds and the most promising entrepreneurs to come to this country from around the world. But we must also take the steps that will not happen without satisfactory public action, to invest in energy efficiency, and the renewable energy technologies of the future.

If we are able to maintain what is distinctive about the United States, a simultaneous capacity for strong public actions and for great entrepreneurs to emerge in the years ahead, we will be in a much stronger position to assure our leadership.

The third and final thing we must do is renew the public compact between the present and the future. Budget deficits are a tax on our future, unless used to finance productive investments. I am not one who sees financial collapse on the imminent horizon. Indeed, I believe that at this point the risks of deflation or stagnation in the United States exceed the risks of uncontrolled growth or high inflation. But unless we change our course, we are at risk of a profound demoralization of government.

At one level this means a decay of essential public functions and a loss of our national self-confidence. At a deeper level, we risk a vicious cycle in which an inadequately resourced government performs badly leading to further demands that it be cut back, exacerbating performance problems, deepening the backlash, and creating a vicious cycle. That is why while recovery is our first priority, it is essential that we establish long-run parity between revenues and expenditures.

Now this is a more complex matter than is often supposed. One of the more important and less well-known ideas to come out of the economics profession over the last generation or so is the phenomenon known as Baumol's Disease. In certain areas, rapid productivity growth is possible. In other areas it is much more difficult. It always has and always will take 8 teachers to teach 96 students for one hour in classes of twelve. Productivity improvement simply is not possible in the way that it is in other activities. Similar phenomena apply to almost anything that involves direct human interaction. Nursing care is another example.

Moynihan's Corollary to Baumol's Disease is the observation that there is a tendency in activities in which Baumol's disease is most pronounced to migrate to or be located in the public sector. To take just one example, every five years the share of GDP devoted to government spending on health care goes up by 1 percentage point. As we contemplate our long-run fiscal future we must contemplate this reality rather than to suppose that there is some past static pattern of expenditures of revenues and expenditure that can be maintained indefinitely.

That is why Bowles-Simpson so important.

That is why President Obama committed to health care cost reduction in the context of the recently enacted health care legislation

If ever there was an area where President Kennedy's doctrine applies – that “man's problems were made by man, that therefore they can be solved by man” – it is to the budget deficit. The United States improved its structural deficit by nearly 4 percentage points of GDP between 1993 and 2000. Greece and Ireland are being called on to make fiscal adjustments in the range of 10 percent of GDP. Once our temporary fiscal support expires, we need an improvement only in the 2 to 3 percent of GDP range to begin the process of putting our debt on a declining path relative to our income.

President Obama has already taken several important steps in this direction: a multi-year freeze in spending outside national security, a serious effort to root out wasteful outdated spending in every area, particularly defense. A particularly welcome feature of the recent commission report is its bipartisan recognition of the idea that tax expenditures are just like expenditures, and need to be held to the same standard of efficiency, fairness, and tough tests on government intrusion into the economy.

They say that markets climb walls of worry. So it is with our nation. America's history, in a certain sense, has been one of self-denying prophecy – a history of alarm and concern, but alarm and concern averted by decisive actions to assure our prosperity. As one former CIA director warned of our largest competitor, that industrial growth rates of eight or nine percent per year for a decade would dangerously narrow the gap between our two countries. That was Allen Dulles in 1959 referring to the Soviet Union. And when the Soviet Union collapsed instead, the Harvard Business Review of 1990 proclaimed in every issue – every issue – in one way or another that the Cold War was over, and that Germany and Japan had won. Now we hear the same thing with respect to China.

Predictions of America's decline are as old as the republic. But they perform a crucial function in driving the kind of renewal that is required of each generation of Americans. I submit to you that as long as we're worried about the future, the future will be better. We have our challenges. But we also have the most flexible, dynamic, entrepreneurial society the world has ever seen. If we can make the right choices, our best days as competitors and prosperous citizens still lie ahead.

Life in the Great Recession

Jim Hamilton of UCSD:

Econbrowser: Extending unemployment benefits: >Here I make two quick observations on the policies being discussed.

The first point has been widely noted, but it bears repeating since I keep hearing comments from people who seem to be unaware of it. When you hear that current unemployment benefits can in some cases be collected for up to 99 weeks, and that Congress is discussing an extension of this program, it is perhaps natural to think this means that some people might be eligible for longer than 99 weeks. But this is not the case. Instead what is being discussed is whether the current limits will be kept in place for another two years or whether the limits will be decreased immediately.

The second point to which I'd like to call attention has also been around awhile, but is appropriately still being discussed (e.g., Calculated Risk, Washington Post). The source appears to be these observations made by Wal-Mart CEO Bill Simon in September:

And you need not go further than one of our stores on midnight at the end of the month. And it's real interesting to watch, about 11 p.m., customers start to come in and shop, fill their grocery basket with basic items, baby formula, milk, bread, eggs, and continue to shop and mill about the store until midnight, when electronic--government electronic benefits cards get activated and then the checkout starts and occurs. And our sales for those first few hours on the first of the month are substantially and significantly higher.

And if you really think about it, the only reason somebody gets out in the middle of the night and buys baby formula is that they need it, and they've been waiting for it. Otherwise, we are open 24 hours — come at 5 a.m., come at 7 a.m., come at 10 a.m. But if you are there at midnight, you are there for a reason.

One thing you might take away from such accounts is that the spending multiplier out of compensation for the unemployed is pretty high.

But this story makes it hard for me to say no to the folks waiting in line at midnight for other reasons.

Christopher Hitchens on Henry Kissinger

Nixon and Kissinger. Worse than we imagined, even though we knew that they were worse than we imagined.

Hitchens:

The Nixon tapes remind us what a vile creature Henry Kissinger is: [T]he latest revelations from the Nixon Library might perhaps turn the scale [against Kissinger] at last.... Chatting eagerly with his famously racist and foul-mouthed boss in March 1973, following an appeal from Golda Meir to press Moscow to allow the emigration of Soviet Jewry, Kissinger is heard on the tapes to say:

The emigration of Jews from the Soviet Union is not an objective of American foreign policy. And if they put Jews into gas chambers in the Soviet Union, it is not an American concern. Maybe a humanitarian concern.

(One has to love that uneasy afterthought...)

In the past, Kissinger has defended his role as enabler to Nixon's psychopathic bigotry, saying that he acted as a restraining influence on his boss by playing along and making soothing remarks. This can now go straight into the lavatory pan, along with his other hysterical lies. Obsessed as he was with the Jews, Nixon never came close to saying that he'd be indifferent to a replay of Auschwitz. For this, Kissinger deserves sole recognition....

I wonder how long the official spokesmen of American Jewry are going to keep so quiet. Nothing remotely as revolting as this was ever uttered by Jesse Jackson or even Mel Gibson, to name only two famous targets of the wrath of the Anti-Defamation League. Where is the outrage? Is Kissinger—normally beseeched for comments on subjects about which he knows little or nothing—going to be able to sit out requests from the media that he clarify this statement? Does he get to keep his op-ed perch in reputable newspapers with nothing said? Will the publishers of his mendacious and purloined memoirs continue to give him expensive lunches as if nothing has happened?

After I published my book calling for his indictment, many of Kissinger's apologists said that, rough though his methods might have been, they were at least directed at defeating Communism.... that Kissinger did many favors for the heirs of Stalin and Mao: telling President Gerald Ford not to invite Alexander Solzhenitsyn to the White House, for example, and making lavish excuses for the massacre in Tiananmen Square. He is that rare and foul beast, a man whose record shows sympathy for communism and fascism...

Department of "Huh?!" (London Economist Edition)

The Economist notes that the problems of the hyper-Keynesian emerging markets are the problems of full employment and prosperity, while the problems of anti-Keynesian Europe are the much worse problems of the edge of depression:

The world economy: Three-way split: [T]he performance of the world economy in 2011 depends on what happens in three places: the big emerging markets, the euro area and America.... These big three are heading in very different directions, with very different growth prospects and contradictory policy choices....

Begin with the big emerging markets, by far the biggest contributors to global growth this year. From Shenzhen to São Paulo these economies have been on a tear. Spare capacity has been used up. Where it can, foreign capital is pouring in. Isolated worries about asset bubbles have been replaced by a fear of broader overheating.... [M]onetary conditions are still extraordinarily loose....

The euro area is another obvious source of stress, this time financial as well as macroeconomic. In the short term growth will surely slow, if only because of government spending cuts. In core countries, notably Germany, this fiscal consolidation is voluntary, even masochistic. The embattled economies on the periphery, such as Ireland, Portugal and Greece, have less choice and a grim future.... [T]he financial consequences of a shift to a world where a euro-area country can go bust are only just becoming clear.... The euro zone’s political leaders, alas, are a fractious and underwhelming lot. An even bigger mess seems all but certain in 2011...

But is their bottom line that America should emulate emerging markets and--with nominal GDP 10% below trend and unemployment kissing 10%--plump for more immediate economic stimulus? No:

America’s economy, too, will shift, but in a different direction. Unlike Europe’s, America’s macroeconomic policy mix has just moved decisively away from austerity.... America is injecting itself with another dose of stimulus steroids just when Europe is checking into rehab and enduring cold turkey.

The result of this could be that American output grows by as much as 4% next year. That is nicely above trend and enough to reduce unemployment, although not quickly. But America’s politicians are taking a risk, too. Even though their country’s long-term budget outlook is famously dire, Mr Obama and the Republicans did not even try to find an agreement on medium-term fiscal consolidation this week. Various proposals to fix the deficit look set to gather dust (see article). Bondholders, who have been very forgiving of the printer of the world’s chief reserve currency, greeted the tax deal by selling Treasuries. Some investors, no doubt, see faster growth on the way; but a growing number are worried about the size of America’s fiscal hole. If those worries take hold, the United States could even see a bond-market bust in 2011...

Tacitus: The Death of the Emperor Galba

Publius Cornelius Tacitus, History I:41, 49:

Viso comminus armatorum agmine vexillarius comitatae Galbam cohortis (Atilium Vergilionem fuisse tradunt) dereptam Galbae imaginem solo adflixit: eo signo manifesta in Othonem omnium militum studia, desertum fuga populi forum, destricta adversus dubitantis tela. iuxta Curtii lacum trepidatione ferentium Galba proiectus e sella ac provolutus est. extremam eius vocem, ut cuique odium aut admiratio fuit, varie prodidere. alii suppliciter interrogasse quid mali meruisset, paucos dies exolvendo donativo deprecatum: plures obtulise ultro percussoribus iugulum: agerent ac ferirent, si ita [e] re publica videretur. non interfuit occidentium quid diceret. de percussore non satis constat: quidam Terentium evocatum, alii Laecanium; crebrior fama tradidit Camurium quintae decimae legionis militem impresso gladio iugulum eius hausisse. ceteri crura brachiaque (nam pectus tegebatur) foede laniavere; pleraque vulnera feritate et saevitia trunco iam corpori adiecta...

[...]

Galbae corpus diu neglectum et licentia tenebrarum plurimis ludibriis vexatum dispensator Argius e prioribus servis humili sepultura in privatis eius hortis contexit. caput per lixas calonesque suffixum laceratumque ante Patrobii tumulum (libertus in Neronis punitus a Galba fuerat) postera demum die repertum et cremato iam corpori admixtum est. hunc exitum habuit Servius Galba, tribus et septuaginta annis quinque principes prospera fortuna emensus et alieno imperio felicior quam suo. vetus in familia nobilitas, magnae opes: ipsi medium ingenium, magis extra vitia quam cum virtutibus. famae nec incuriosus nec venditator; pecuniae alienae non adpetens, suae parcus, publicae avarus; amicorum libertorumque, ubi in bonos incidisset, sine reprehensione patiens, si mali forent, usque ad culpam ignarus. sed claritas natalium et metus temporum obtentui, ut, quod segnitia erat, sapientia vocaretur. dum vigebat aetas militari laude apud Germanas floruit. pro consule Africam moderate, iam senior citeriorem Hispaniam pari iustitia continuit, maior privato visus dum privatus fuit, et omnium consensu capax imperii nisi imperasset.

The Becker-Murphy Theory of Rational Addiction

Andrew Gelman writes:

Rational addiction: Ole Rogeberg sends in this:

and writes:

No idea if this is amusing to non-economists, but I tried my hand at the xtranormal-trend. It's an attempt to spoof the many standard "incantations" I've encountered over the years from economists who don't want to agree that rational addiction theory lacks justification for some of the claims it makes. More specifically, the claims that the theory can be used to conduct welfare analysis of alternative policies.

Mike Konczal on the Moderate Republican Stimulus That Is McConnell-Obama

I don't think it is moderate Republican--a moderate Republican stimulus has a bunch of infrastructure spending in it that this thing does not, and a moderate Republican stimulus has a debt-limit increase, and a moderate Republican stimulus has stand-by spending caps and tax increases as of 2015 if the deficit is still high.

Mike:

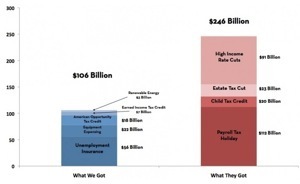

Moderate GOP Stimulus: Re-examining the Who Got What Tax Deal Chart. « Rortybomb: There is no continuation of the Temporary Assistance for Needy Families Emergency Fund (TANF EF) from the stimulus bill in the tax cut compromise. Regular TANF was created as part of the Clinton-era welfare reform to get people off welfare by getting them back to work. This approach becomes problematic when unemployment is high through faults of monetary and fiscal policy, rather that people choosing not to work. In a Great Recession TANF runs out of both money and conceptual scope very quickly. So this Emergency Fund, at the low cost of five billion dollars distributed to states allowed locals on the ground to expand and continue TANF to meet the needs of fighting poverty and putting people to work in the Great Recession.... Who really got what in this deal?.... I want to argue the chart should look like this....

[T]he Child Tax Credit. From the Republican Pledge To America (pdf), the Republicans both take credit for the creation of the child tax credit and note the damage that will happen if it isn’t extended (“During the 1990s, a Republican Congress enacted pro-family policies such as marriage penalty relief and the child tax credit. Unless action is taken, a $3.8 trillion tax hike will go into effect on January 1, 2011 that will unravel these policies”).... [T]his is a “got” for the GOP.

The second is more interesting: Should the payroll tax cut be a “get” for the Republican Party?... [If] you want to know what the GOP wants to get the economy jump-started, ask them, by all accounts these kinds of payroll taxes are what the GOP wanted. From whitehouse.gov (h/t Jed Lewison at DailyKos):

Q: So the only reason that the payroll tax holiday will provide more stimulus is because it’s twice as large. Making Work Pay was capped. Why didn’t you preserve Making Work Pay? Is it because, as the President said some months ago, it’s just a kind of invisible tax cut and didn’t provide any political benefit for the White House?

MR. SUMMERS: No, it came out of the process of compromise with the Republicans who were more attracted to the payroll tax holiday concept, and that was a proposal that, as had been coming out of here, we had been giving considerable thought to in the context of the President’s budget.

Weakest Stimulus And that isn’t a mistake. This takes the weakest part of the stimulus, tax cuts, makes it weaker and puts it in front of the stimulus package. According to Mark Zandi’s estimates it has a weaker multipler than the anemic Making Work Pay tax credit.... It turns away from the idea of investing in public goods and infrastructure spending, laying out the groundwork of the 21st century economy, and instead mails checks to people. That’s the GOP response to any problem – tax cuts! – and now it is branded the Democratic stimulus response.... Viewed through this lens, this is the Moderate Republican Stimulus Package 2.0. I wonder how it is going to work.

All I can say is that I really hope Greg Mankiw is right about the high marginal propensity to spend out of tax cuts...

Department of Things I Never Thought I Would See: Dani Rodrik Bails on the Euro...

Dani:

Thinking the Unthinkable in Europe by Dani Rodrik - Project Syndicate: When Greece was bailed out by a joint eurozone-IMF rescue package back in May, it was clear that the deal had bought only a temporary respite. Now the other shoe has dropped. With Ireland’s troubles threatening to spill over to Portugal, Spain, and even Italy, it is time to rethink the viability of Europe’s currency union. These words do not come easily, as I am no Euroskeptic.... I believed that monetary union made perfect sense in the context of a broader European project that emphasized – as it still does – political institution-building alongside economic integration. Europe’s bad luck was to be hit with the worst financial crisis since the 1930’s while still only halfway through its integration process. The eurozone was too integrated for cross-border spillovers not to cause mayhem in national economies, but not integrated enough to have the institutional capacity needed to manage the crisis.

Consider what happens when banks in Texas, Florida, or California make bad lending decisions.... If the banks are merely illiquid, the Federal Reserve in Washington is ready to act as a lender of last resort. If they are judged to be insolvent, they are allowed to fail or are taken over by federal authorities.... Similarly, in case of bankruptcy, federal laws and courts readily adjudicate claims... private debt is not socialized by state governments (but by the federal government, if at all), and does not threaten public finances at the state level. State governments in turn have no legal power to abrogate debt contracts vis-à-vis out-of-state creditors, and no incentive to do so (given the help they get from the federal government). So, even in the throes of a financial crisis, banks and non-financial firms can continue to borrow if their balance sheets are sound, uncontaminated by the “sovereign risk” of their state government.

Meanwhile, the federal government makes up for a good chunk of the drop in state incomes by transfers or reduced taxes....

So the real problem in Europe is not that Spain or Ireland has borrowed a lot, or that too much Spanish and Irish debt sits on banks balance sheets elsewhere in Europe. After all, who cares about Florida’s current-account deficit – or even knows what it amounts to? No, the real problem is that Europe has not created the union-wide institutions that an integrated financial market requires.

This reflects the absence of adequate political institutions at the center. The European Union has taught us valuable lessons over the last few decades: first, that financial integration requires eliminating volatility among national currencies; next, that eradicating exchange-rate risk requires doing away with national currencies altogether; and now, that monetary union is impossible, among democracies, without political union. It should have been expected that the political side of the equation would take time to fall into place. It is easy to blame European politicians for lack of leadership. But let us not underestimate the magnitude of the task that European governments took on... the closest analogue to it is America’s own historical experience with building a federal republic. As the long American struggle for “states’ rights” – and indeed the Civil War – shows, creating a political union out of a collection of self-governing entities is hardly a smooth or speedy process....

[I]t may now be too late for the eurozone. Ireland and the southern European countries must reduce their debt burden and sharply enhance their economies’ competitiveness. It is hard to see how they can achieve both aims while remaining in the eurozone. The Greek and Irish bailouts are only temporary palliatives: they do nothing to curtail indebtedness, and they have not stopped contagion. Moreover, the fiscal austerity they prescribe delays economic recovery. The idea that structural and labor-market reforms can deliver quick growth is nothing but a mirage. So the need for debt restructuring is an unavoidable reality.

Even if the Germans and other creditors acquiesce in a restructuring – not from 2013 on, as German Chancellor Angel Merkel has asked for, but now – there is the further problem of restoring competitiveness. This problem is shared by all deficit countries, but is acute in Southern Europe. Membership in the same monetary zone as Germany will condemn these countries to years of deflation, high unemployment, and domestic political turmoil. An exit from the eurozone may be at this point the only realistic option for recovery.

A breakup of the eurozone may not doom it forever. Countries can rejoin, and do so credibly, when the fiscal, regulatory, and political prerequisites are in place. For the moment, the eurozone may well have reached the point where an amicable divorce is a better option than years of economic decline and political acrimony.

December 12, 2010

Physicist Chad Orzel Comes Perilously Close to WInning the Internet...

It's twue! It's twue!:

Literary Interlude: Bearded Mentor Figures in the Literature of the Fantastic : Uncertain Principles: It's time now to talk about two of the greatest mentor figures in the literature of the fantastic. You know their stories well, I'm sure, but the parallels between them are eerie:

Both are gruff but kindly mentor figures who provide crucial guidance for the young and naive protagonist of the story as he moves out into a scary world to complete an important quest.

Both fall into a chasm while battling a fearsome monster to allow the protagonist time to flee.

Both return from their apparent death when least expected, just in time to save the day.

*Both have awesomely impressive beards.

I am speaking, of course, of Gandalf from J. R. R. Tolkien's The Lord of the Rings, and Yukon Cornelius from the animated tv special Rudolf the Red-Nosed Reindeer

J. Bradford DeLong's Blog

- J. Bradford DeLong's profile

- 90 followers