J. Bradford DeLong's Blog, page 204

March 31, 2019

The confirmation of Brett Kavanaugh was a huge mistake. O...

The confirmation of Brett Kavanaugh was a huge mistake. Of course, the confirmations of the other four corrupt Republican justices were huge mistakes as well:

Robert Barnes: Brett Kavanaugh Pivots as Supreme Court Allows One Execution, Stops Another: "The Supreme Court on Thursday night stopped the execution of a Buddhist inmate in Texas because he was not allowed a spiritual adviser by his side, when last month it approved the execution of a Muslim inmate in Alabama under the almost exact circumstances.... Kavanaugh...

...on Thursday was the only justice to spell out his reasoning: Texas could not execute Patrick Murphy without his Buddhist adviser in the room because it allows Christian and Muslim inmates to have religious leaders by their sides.... But Kavanaugh was on the other side last month when Justice Elena Kagan and three other justices declared 'profoundly wrong' Alabama���s decision to turn down Muslim Domineque Ray���s request for an imam to be at his execution, making available only a Christian chaplain.... Kavanaugh and the court���s other conservatives did not address Kagan���s argument, saying only that Ray had brought his challenge too late. Kavanaugh said in a footnote Thursday he was satisfied with the timing of Murphy���s litigation. But the difference in when Ray and Murphy brought their requests was not substantial...

#noted

THE SPICE MUST FLOW! NO HARD BORDER IN IRELAND!!: John Ho...

THE SPICE MUST FLOW! NO HARD BORDER IN IRELAND!!: John Holbo: On Twitter: "May loses by >50 votes hence can���t quit as she would have if she had won. Could have been worse. If >100 loss -> May becomes dictator for life. >200 loss would make her god-emperor. Dodged that bullet...

#noted

March 30, 2019

Alexandra Petri: The Zuckerberg Hearings, Condensed: "Sen...

Alexandra Petri: The Zuckerberg Hearings, Condensed: "Senator 1: Mr. Zuckerberg, we hear that you started Facebook in your dorm room...

...Mark Zuckerberg: Senator, yes.

Senator 1: I will now haltingly read a question that an aide who understands this technology better than I do has prepared, but I will mangle it slightly so that its premise is obviously wrong.

Zuckerberg: Senator,��the answer to the specific question you have��asked��is, ���No, Facebook has never done that.���

Senator 1: I feel like there is something more I ought to ask, but I won���t.

Senator 2: Mr. Zuckerberg, I hear that you started Facebook in your dorm room.

Zuckerberg: Senator, yes.

Senator 2: And are you still in college, young man?

Zuckerberg: (With faint contempt) Senator, no.

Senator 2: (With a triumphant look) Every computer screen contains millions of megapixels. Facebook has 2.1 billion users. So��how many millions of bytes, or milibytes, do you include in this face book?

Zuckerberg: Senator, that question involves a specific number and I will have to get back to you...

#noted

Hoisted from the Archives: What I Wrote in Advance of the FOMC's September 2018 Meeting

What a difference six months makes! And now the Fed really wishes it had not raised interest rates in the second half of 2018 and yet is unwilling to move them now back to the summer-of-2018 level. Why they are unwilling I do not know:

Hoisted from the Archives: Next week the Federal Open Market Committee���the principal policymaking body of the United States's Federal Reserve system���is overwhelmingly likely to raise the benchmark interest rate it controls, the Federal Funds rate that governs short-term safe nominal bonds, by one quarter of a percentage point from the range of 1.75-2% per year to the range of 2-2.25% per year. That would make it a little more expensive to borrow and spend and a little more attractive to cut spending and save. Thus there would be a little less spending in the economy, and so a few fewer jobs. Economic growth would be a little slower. The economy would be a little less resilient in the face of adverse shocks to resources or confidence that might generate a recession. These are all minuses���small minuses from a 25 basis point increase in the Federal Funds rate, but minuses.

Offsetting these minuses is supposed to be a plus: raising the Federal Funds rate by 25 basis points next week is supposed to lesson the chances of a disruptive upward outbreak of inflation. But I really do not see this plus as valuable enough to offset the minuses, even though they are small minuses.

This particular widely-anticipated move, however, will not shake the economy in any way: it is already baked into the cake in the sense that economic and financial decision-makers have already taken it into account and readjusted their portfolios and plans assuming it will come to pass. It is a continuation of the existing policy, another step on a well-marked path. The relevant question is: Is this the best policy path?

The Federal Reserve is on this policy path right now because the typical member of the Federal Open Market Committee (hereafter FOMC) believes that:

The current 2% per year inflation rate is appropriate, and is a good choice for the Federal Reserve's target.

The unemployment rate at 3.9% that is already so low that employers are having a hard time finding workers without offering wages that would accelerate inflation.

With actual and expected inflation around 2% per year, the "neutral" Federal Funds rate is roughly 2.9% per year.

When the Federal Funds rate is at the "neutral" rate, monetary policy is not putting pressure on the economy for either excess supply or excess demand in the labor market���there is pressure neither toward a situation in which employers increasingly have a hard time finding workers without offering them wages that would accelerate inflation nor toward a situation in which workers increasingly have a hard time finding jobs and sit pointlessly and destructively idle.

Thus it is important that the Federal Reserve be moving the Federal Funds rate without hesitation from its current 1.75-2% per year to the "neutral" of about 2.9% per year.

It is likely that the Federal Reserve should then keep raising the Federal Funds rate higher: the unemployment rate at 3.9% is probably too low to be sustainable without eventually generating rising inflation.

Of these six beliefs, (4) is essentially a definition of what the "neutral" Federal Funds rate is, and (5) and (6) then follow from (1)-(4) and the Federal Reserve's belief that its primary mission is to stabilize inflation at a low level, and not to seek higher employment levels when doing so would conflict with that mission.

The problem���or at least the problem as I see it���is that (1), (2), and (3) are all extremely debatable, and (1), that 2% per year is a proper inflation target, is surely erroneous.

I, at least, see (1) as surely erroneous because, as Jeffrey Frankel put it late last month: "In the past, the Fed has moderated recessions by cutting short-term interest rates by around 500 basis points. But, with those rates currently standing at only 2%, such a move is impossible..." Thus successful recession-fighting would turn on the competence, ability, and willingness of others to use the government budget to keep the economy on an even keel when the next recession comes. Yet there is unpleasant stabilization policy arithmetic that suggests a lack of ability to do so and even more unpleasant failure to learn the lessons of 2008-2018 that has produced a lack of willingness to do so. The only feasible plan to repair the situation would be for the Federal Reserve to raise its inflation target from 2% per year to 4% per year���the costs to the economy in the long run from returning to the inflation rates of the 1990s would be vastly less than the consequences of accepting the crippling of the ability to fight recessions.

But the Federal Reserve does not see it that way.

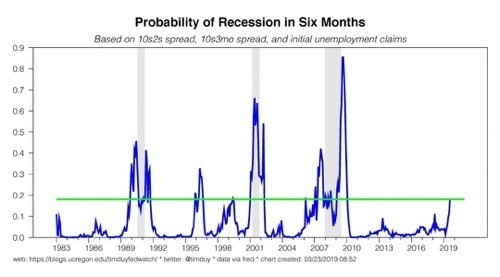

I, at least, see (2), that the unemployment rate at 3.9% that is already so low that employers are having a hard time finding workers without offering wages that would accelerate inflation, as not surely erroneous bur probably wrong. I think this for two reasons. First, while the unemployment rate is especially low today, the share of 25-54 year olds with jobs is not especially high. And as Adam Ozimek of Moody's reiterated yet again earlier this month, the 25-54 employment share and other wider measures of labor-market slack that see no high labor-pressure economy right now have done a better job of capturing the reality of inflationary pressures over the past generation. Second, the higher wage growth that we would be seeing in a high labor-pressure economy is not there. Employers are not yet willing to offer workers wages higher than last year's level plus inflation plus productivity growth. [Wage pressure is still markedly weaker][6] than it was at the last business cycle peak in 2007.

But the Federal Reserve does not see it that way.

And I, at least, see (3), the belief that the current Federal Funds rate is a full 1%-point lower than "neutral", as debatable. I would just note, as current , that the FOMC has steadily lowered its estimate of the "neutral" rate by fully 1.5%-points over the past five years. And I would also note that history shows us that there is a lot of momentum in the trajectory of FOMC estimates of the structure of the economy: the way to bet is that a process of revision in one direction or the other will continue. It is a committee, after all.

I could well be wrong. But I think it is more likely than not that, ten years from today, those on the FOMC will wish that they would have cut interest rates next week rather than raising them.

[6] https://blogs.uoregon.edu/timduyfedwa... "Tim Duy: Monday Morning Potpourri: 'A baseline expectation is that in a normal labor market, wage growth will be in the vicinity of real wage growth plus inflation.... Further labor market tightness should yield one of two outcomes���either real wages rise at the expense of profits margins or nominal wages and inflation rise in a lockstep pattern. The Fed would likely welcome the first outcome but would be unhappy with the second..."

https://www.icloud.com/keynote/0pKHWBaD4_nfu0Zj8PmRK2VTg

#hoiste4dfromthearchvies #monetarypolicy #highighted

Adam-Troy Castro: Young People Read Old SFF: "Nobody disc...

Adam-Troy Castro: Young People Read Old SFF: "Nobody discovers a lifelong love of science fiction through Asimov, Clarke, and Heinlein anymore, and directing newbies toward the work of those masters is a destructive thing, because the spark won't happen. You might as well advise them to seek out Cordwainer Smith or Alan E. Nourse���fine tertiary avenues of investigation, even now, but not anything that's going to set anybody's heart afire, not from the standing start. Won't happen...

#noted #sciencefiction

Kim Clausing's is the best defense of globalization and o...

Kim Clausing's is the best defense of globalization and openness I have read in years. And former Obama CEA Chair Jason Furman agrees:

Jason Furman: Review of Kim Clausing: "Open: The Progressive Case for Free Trade, Immigration, and Global Capital": "If I had to assign policymakers one up-to-date guide to the latest economic policy issues on taxes and trade it would be this one...

...Kimberly Clausing has done research in both areas and has been a leader in the economics of international corporate taxation, including profit shifting by multinationals, and it shows throughout this book. Open makes a strong, fact-based case for openness towards trade and immigration. The case ranges from explaining long-standing ideas like comparative advantage to a sensible evaluation of the latest literature, including a balanced assessment of the "China shock" literature that has found a large and persistent impact from Chinese imports but also serious methodological issues that make it a potentially less reliable guide to untangling the causal impact of changing trade policies towards China.Open, however, is not a polemic for the status quo and in fact nearly one-third of the book is a case for policy agenda to better prepare workers for the global economy, reform the tax system, and reshape globalization more broadly. Clausing does not offer any one simple solution, but then again I don't think that there is one...

#noted

Almost a decade old, but well worth reading. Sam Bowles a...

Almost a decade old, but well worth reading. Sam Bowles argues that liberal culture and order do not so much dissolve natural human sociability and compassion in the market nexus, but rather enable positive-sum ties of solidarity by weakening the zero-sum intra-clan sorority combined with inter-clan enmity:

Sam Bowles (2011): Is Liberal Society a Parasite on Tradition?: "Market-like incentives may crowd out ethical motivations, illustrating the parasitic liberalism thesis and the cultural and institutional processes by which it might work....Cross-cultural behavioral experiments...cast doubt on the thesis: liberal societies are distinctive in their civic cultures, exhibiting levels of generosity, fairmindedness, and civic involvement that distinguish them from non-liberal societies.... The idealized view of tradition embodied in the "parasitic liberalism" thesis overlooks aspects of non-liberal social orders that are antithetical to a liberal civic culture. Thus while markets and other liberal institutions may indeed undermine traditional institutions as claimed, by attenuating familistic and other parochial norms and identities, this may enhance rather than erode the values necessary for a well functioning liberal order...

#noted

Pharmaceutical price reform is one of the very few equita...

Pharmaceutical price reform is one of the very few equitable growth issues where there are actually Republican legislators willing to talk: CPPC: Senate Finance Committee Grills Drug Executives on Rising Prices, Criticize Them for Terrible Practices: "Senator Chuck Grassley (R-IA) opened by saying that America has a problem with high prescription drug prices, that a balance can be struck between innovation and affordability, and that the Committee was here to discuss solutions. He and Senator Wyden have launched a bipartisan investigation into the high price of insulin...

...Senator Ron Wyden (D-OR) delivered a blistering attack on the assembled CEOs. He bluntly said that drugs did not become outrageously high by accident, and that drug prices are high because that is where pharmaceutical companies and their executives want them. It is outrageous that patients are being forced to ration their medicine or choose between paying for prescription drugs and paying for food and rent. Wyden especially criticized AbbVie for raising the price of its arthritis medication Humira, the top selling drug in the country (which has risen from $19,000 to $38,000 over six years). "Can patients opt for a less expensive alternative?" he demanded. "They can't, because AbbVie protects the exclusivity of Humira like Gollum with his ring!" Humira has used a great many patents on every stage of Humira's development to create a 'patent thicket' that thwarts competition and enables the company to charge whatever it chooses...

#noted

Equitable Growth's Will McGrew has a pinned tweet pushing...

Equitable Growth's Will McGrew has a pinned tweet pushing back against the meme that there are "really" no worrisome ethnicity or gender wage gaps because researchers can make such gaps disappear by adding sufficient variables to the right-hand side of a regression analysis. But when you add additional explanatory variables���when you "control"���you need to be very careful that you are only controlling for things that confound the relationship you are trying to study. When you control for things that mediate that relationship, you land up in garbage-in-garbage-out territory:

Will McGrew: Wage Gaps: "Some claim that the wage gap disappears if you control for all relevant variables. This is 100% false. According to the evidence, workplace segregation and discrimination are the largest causes of the wage gap faced by Black women...

#noted

Joan R. Rose��s and Nikolaus Wolf: Regional Economic Deve...

Joan R. Rose��s and Nikolaus Wolf: Regional Economic Development In Europe, 1900-2010: A Description Of The Patterns: "Regional employment structures and regional GDP and GDP per capita in 1990 international dollars, stretching over more than 100 years.... Variation in the density of population and economic activity, the spread of industry and services and the declining role of agriculture... changes in the levels of GDP and GDP per capita... patterns of convergence and divergence over time and their explanations... a secular decrease in spatial coherence... a U-shaped development in geographic concentration and regional income inequality, similar to the finding of a U-shaped pattern of personal income inequality...

#noted

J. Bradford DeLong's Blog

- J. Bradford DeLong's profile

- 90 followers