J. Bradford DeLong's Blog, page 1161

August 19, 2014

Robert Skidelsky's Superb Biography of John Maynard Keynes: From the Archives from a Decade Ago

Over at Equitable Growth: Robert Skidelsky's Biography of John Maynard Keynes: Archive Entry From Brad DeLong's Webjournal: August 06, 2004:

Over at Equitable Growth: Robert Skidelsky's Biography of John Maynard Keynes: Archive Entry From Brad DeLong's Webjournal: August 06, 2004:

Sitting next to Lord Skidelsky in the Sala Maggioranza of the Italian Treasury (after they turned off the air conditioning, I took off my tie when he took off his jacket) impelled me to reread his Keynes biography.

And, after rereading, I find that I cannot improve on what I wrote about them three years ago: my thoughts then were totally enthusiastic and totally adulatory. And my thoughts are the same now. (I haven't yet reread volume three). In his first two volumes, Skidelsky gives us John Maynard Keynes's life, entire. And he does so with wit, charm, control, scope, and enthusiasm. You read these books and you know Keynes--who he was, what he did, and why it was so important. READ MOAR

The place to start is with Skidelsky's observation that John Maynard Keynes appeared to live more lives than any of the rest of us are granted.

Keynes was an academic, but also a popular author. His books were read much more widely outside of academia than within it. Keynes was a politician--trying to advance the chances of Britain's Liberal Party between the wars--but also a bureaucrat: at times a key civil servant in the British Treasury. He was a speculator, trying to make his fortune on the stock market, but also at the core of the "Bloomsbury Group" of artists and intellectuals that did so much to shape interwar culture.

For the litterati it is Keynes of Bloomsbury--his loves, enthusiasms, acts of patronage, and wit--who is the most interesting. For economists like myself, it is Keynes the academic who is the real Keynes: he was the founder of the half-science half-witchcraft discipline of macroeconomics. For those interested in the political and economic history of the twentieth century, it is Keynes the author and politician who is primary. In either case, John Maynard Keynes is the man who has the best claim to be the architect of our modern world--whether it is how our central banks think about economic policy, what our governments believe that they must try to do, the institutions through which they work, or the habit of thought that views the economy not as Adam Smith's "system of natural liberty" but as a complicated machine that needs adjustment and governance, all of these trace large parts of their roots to the words and deeds of John Maynard Keynes.

How did this man come to be?

That is the question answered by the first volume of Skidelsky's biography: Hopes Betrayed. Hopes Betrayed is a bildungsroman, a story of growth and development. Skidelsky writes the best narrative interpretation of growing up as a smart and privileged children of academics in late Victorian Britain than I can ever conceive of being written. He writes of how Keynes was one of a relatively small number of brilliant students thrust as a leaven into the mass of Britain's upper class at Eton, and thus became part of "an intellectual elite thrust into the heart of a social elite" (HB, page 77). An entire cohort of Britain's upper class thus learned before they were twenty that Keynes could be very smart, very witty, very entertaining--and very helpful if there was a hard problem to be thought through or something to be done.

Skidelsky then writes of Keynes at Cambridge, his joining the secret society of the Apostles, and his eager grasping with both hands of the philosophy of the aesthete common among the students of the philosopher G.E. Moore. As Keynes put it in 1938, he believed that one should arrange one's life to achieve the most good, where "good" was nothing more or less than

states of mind... states of mind... not associated with action or achievement or with consequences [but]... timeless, passionate states of contemplation and communion…. a beloved person, beauty, and truth.

Thus Keynes left Cambridge convinced that "one’s prime objects in life were love, the creation and enjoyment of aesthetic experience, and the pursuit of knowledge. Of these love came a long way first..." (HB, page 141).

This embrace of aestheticism was and remained the key to the "Bloomsbury" avatar of John Maynard Keynes, for whom the lodestars were to "be in love with one’s friends, with beauty, with knowledge" and who was and remained an enthusiastic member of the Bloomsbury group, sharing "its intellectual values and its artistic enthusiasms," and participating "in its wild fancy dress parties" (HB, page 234). Keynes was a man who could celebrate this appointment to the British Treasury with

...a party for seventeen… at the Café Royale.... Afterwards they went back to 46 Gordon Square for Clive [Bell]’s and Vanessa [Bell, the sister of Virgina Woolf]’s party. There they listened to a Mozart trio... and went upstairs for the last scene of a Racine play performed by three puppets made by Duncan [Grant], with words spoken by the weird-voiced Stracheys. ‘The evening ended with Gerald Shove enthroned in the center of the room, crowned with roses...’ (HB, page 300).

But at the same time Keynes's pursuit of knowledge was shading over into politics and policy as well. For Keynes it was never enough to pursue knowledge in order to achieve a good state of mind, one had also to be sure to cause the knowledge to be applied to make the world a better place. And how one could act in politics and policy was greatly constrained by the limits of our knowledge. One argument from Edmund Burke, especially resonated with Keynes. As he wrote:

Burke ever held, and held rightly, that it can seldom be right... to sacrifice a present benefit for a doubtful advantage in the future.... It is not wise to look too far ahead; our powers of prediction are slight, our command over results infinitesimal. It is therefore the happiness of our own contemporaries that is our main concern; we should be very chary of sacrificing large numbers of people for the sake of a contingent end, however advantageous that may appear... We can never know enough to make the chance worth taking... (ES, page 62).

Keynes's industry and intelligence thus made him a trusted and effective member of Britain's intellectual and administrative elite well before the eve of World War I. Sir Edwin Montagu, especially, pushed him forward both before and during the war. Before the war Keynes decided that he wanted the life of an academic rather than of an administrator: Cambridge rather than the India Office or the Treasury. Yet he kept a strong presence in both worlds, writing his practical and policy-oriented book Indian Currency and Finance in spare moments as he worked on the deeper and philosophical project that was his Treatise on Probability.

Thus it was no surprise that Keynes found an important and powerful job at the Treasury during the national emergency that was World War I. How do you mobilize the financial resources of Britain to support the war effort? How large a war effort could the British economy stand? How could an international trade system geared to consumer satisfaction be harnessed as an instrument of national power? These are all deep and complicated questions. These are what Keynes worked on. But as the death toll from World War I mounted up toward ten million, Keynes became angrier and angrier at this monstrous botch of human lives and social energy that was World War I--and angrier and angrier at the politicians who could see no way forward other than mixing more blood with mud at Paaschendale.

Keynes's friend David Garnett wrote him a letter condemning his work for the government, calling Keynes

an intelligence they need in their extremity.... A genie taken incautiously out... by savages to serve them faithfully for their savage ends, and then--back you go into the bottle.... Oh... our savages are better than other savages.... But don’t believe in the profane abomination.

The interesting thing was that Keynes "agreed that there was a great deal of truth in what I had said..." (HB, page 321). And then the whole project of post-World War I reconstruction went wrong at Versailles--when the new German government was treated as a foe rather than a democratic ally, when the object seemed to be to extract as much in plunder and reparations from Germany as possible ("until the pips squeak").

Skidelsky quotes South African politician Jan Christian Smuts on the atmosphere at Versailles:

Poor Keynes often sits with me at night after a good dinner and we rail against the world and the coming flood. And I tell him that this is the time for Grigua’s prayer (the Lord to come himself and not to send his Son, as this is not a time for children). And then we laugh, and behind the laughter is [Herbert] Hoover’s horrible picture of thirty million people who must die unless there is some great intervention. But then again we think that things are never really as bad as that; and something will turn up, and the worst will never be. And somehow all these phases of feeling are true and right in some sense... (HB, page 373).

Under this unbearable pressure, Keynes exploded. Keynes exploded with a book called The Economic Consequences of the Peace. It condemned the political maneuvering of Versailles and the treaty that resulted in the strongest possible terms. He excoriated short-sighted politicians who were interested in victory rather than peace. He outlined his alternative proposals for peace: "German damages limited to £2000m; cancellation of inter-Ally debts; creation of a European free trade area… an international loan to stabilize the exchanges...."

And he prophesied doom--if the treaty were carried out and Germany kept poor for a generation:

If we aim deliberately at the impoverishment of Central Europe, vengeance, I dare predict, will not limp. Nothing can then delay for long that final civil war between the forces of reaction and the despairing convulsions of revolution, before which the horrors of the late German war will fade into nothing, and which will destroy... the civilization and progress of our generation... (HB, page 391).

The Economic Consequences of the Peace made Keynes famous. His horror at the terms of the peace treaty won him friends like Felix Frankfurter, a powerful molder of opinion in the United States. In his book, propelled by "passion and despair," Keynes "spoke like an angel with the knowledge of an expert" and showed an extraordinary mastery not just of economics but also of the words that were needed to make economics persuasive. Before The Economic Consequences of the Peace Keynes was primarily an academic (with some government experience) with a lot of influential literary friends. Afterwards he was a celebrity. He was not only the private Keynes: "the Cambridge don selling economics by the hour, the lover of clever, attractive, unworldly young men, the intimate of Bloomsbury." He was also--because of what he had done with his pen after Versailles--"the monetary reformer, the adviser of governments, the City magnate, the feared journalist whose pronouncements caused bankers and currencies to tremble... conferences jostled with holidays, intimacy merged into patronage. In 1925 the world-famous economist would marry a world-famous ballerina in a blaze of publicity..." (HB, page 400).

So after World War I Keynes used what power he had to--don't laugh--try to restore civilization. In Skidelsky's--powerful and I believe correct--interpretation, Keynes before 1914:

believed (against much evidence, to be sure) that a new age of reason had dawned. The brutality of the closure applied in 1914 helps explain Keynes’s reading of the interwar years, and the nature of his mature efforts... to restore the expectation of stability and progress in a world cut adrift from its nineteenth-century moorings... (ES, page xv).

Skidelsky's narrative of the mature Keynes--Keynes in the 1920s--is far from being a one-note recounting of the brave but losing struggle against the approaching Great Depression, against political insanity, and against the Nazi Party's attempted revenge for the German defeat in World War I. Bloomsbury takes up a good chunk of the narrative. Skidelsky's book includes love letters from Keynes to his future wife Lydia Lopokova:

In my bath today I considered your virtues—how great they are. As usual I wondered how you could be so wise. You must have spent much time eating apples and talking to the serpent! But I also thought that you combined all ages—a very old woman, matron, a debutante, a girl, a child, an infant; so that you are universal. What defence can you make against such praises? (page 181).

But when he tries to paint a picture of what it was like to be a member of the Bloomsbury culture group in the 1920s, even Skidelsky cannot quite reach the full range. So he resorts to the imaginings of one of the characters of novelist Anthony Powell, who thinks that Bloomsbury must have been "...every house stuffed with Moderns from cellar to garret. High-pitched voices adumbrating absolute values, rational statse of mind, intellectual integrity, civilized personal relationships, significant form…. The Fitzroy Street Barbera is uncorked. 'Le Sacre du Printemps' turned on, a hand slides up a leg.... All are at one now, values and lovers" (page 11).

Virginia Woolf had a different, less happy and romantic view. She wrote of her:

vivid sight of Maynard by lamplight--like a gorged seal, double chin, ledge of red lip, little eyes, sensual, brutal, unimaginate. One of those visions that come from a chance attitude, lost as soon as he turned his head. I suppose though it illustrates something I feel about him. He’s read neither of my books...

(page 15)

There is a clear lesson: if your circle includes Nobel Prize-winnning caliber novelists with wicked pens, read their books and praise them as often as possible.

The bulk of this second volume--The Economist as Saviour--is, however, devoted to Keynes's political and intellectual struggle for stable money and full employment, and against deflation, overvalued exchange rates, and the sacrifice of the happiness of today's populations in the hopes of regaining the imagined benefits of the classical gold standard at some time in the distant future. Keynes spent more than a decade arguing against central bankers who "think it more important to raise the dollar exchange a few points than to encourage flagging trade." He tried to prevent Britain's return to the gold standard in 1925 at an overvalued exchange rate, for by overvaluing the exchange rate Britain's Treasury Minister, Winston Churchill, was willing

...the deliberate intensification of unemployment. The object of credit restriction, in such a case, is to withdraw from employers the financial means to employ labor at the existing level of prices and wages. This policy can only attain its end by intensifying unemployment without limit, until the workers are ready to accept the necessary reduction in money wages under the pressure of hard facts.... Deflation does not reduce wages 'automatically.' It reduces them by causing unemployment. The proper object of dear money is to check an incipient boom. Woe to those whose faith leads them to use it to aggravate a Depression! (page 203).

But in the end Keynes failed in the 1920s. He was unable to persuade British governments that economic policy should be decided upon by rational thought rather than by obedience to old poorly-understood verities. He failed to achieve any material easing of the terms of the Versailles treaty. He failed to prevent deflation and high unemployment in Britain. He failed to convince people that the Great Depression was a man-made catastrophe that could be cured relatively easily. His pen--though strong--was not strong enough. His allies were too few. And among central bankers and cabinet ministers, understanding of the situation in which they were embedded was rare.

So the 1930s saw a change of emphasis. Fewer short polemical articles were written. Instead, Keynes concentrated his attention on writing a book, a book which he thought "...will largely revolutionize--not, I suppose, at once but in the course of the next ten years--the way the world thinks about economic problems. When my new theory has been duly assimilated and mixed with politics and feelings and passions, I can’t predict what the upshot will be in its effects on actions and affairs. But there will be a great change..." (pages 520-521). And he was right.

His General Theory of Employment, Interest, and Money did change the world. It ends with a bold claim for the importance of ideas rather than interests that, in context, has to be read not as a considered judgment but as his desperate hope:

Practical men, who believe themselves to be quite exempt from any intellectual influences, are usually the slaves of some defunct economist. Madmen in authority, who hear voices in the air, are distilling their frenzy from some academic scribbler of a few years back. I am sure that the power of vested interests is vastly exaggerated compared with the gradual encroachment of ideas.... But, soon or late, it is ideas, not vested interests, which are dangerous for good or evil... (page 570).

The extraordinary thing is that Keynes was right.

The other extraordinary thing is that Skidelsky has told the story so well.

Skidelsky is superb at getting at the heart of what the key contribution of Keynes's General Theory. As Skidelsky puts it, Keynes's key contribution was to find not a middle way but a genuine Third Way between "laissez-faire and central planning... conservatism and socialism." His proposals did not split the difference, but instead promised to achieve the benefit each of the traditional poles of politics had claimed but had never been able to deliver. Socialists promised full employment without economic freedom. (And Communists promised full employment without either economic or political freedom.) Conservatives promised economics (and sometimes political) freedom without full employment. Keynes, by contrast, promised both. His doctrines were thus politically irresistible: they would have been extraordinarily attractive to politicians and bureaucrats even if the doctrines and theories had not been true. Fortunately for all of us, they were true--or at least true enough to be very useful indeed in their historical context.

Skidelsky is also very good at focusing on the underlying liberal--classical liberal, that is--nature of Keynes's thought. Brought up in the laissez-faire classical liberal tradition, Keynes came to see it as a con: based on false claims about the world. But, Keynes believed, a good and smart government could make the claims of laissez-faire true enough.

Keynes saw the market economy as having two great flaws. The first was that demand for investment was extraordinarily and pointlessly volatile, as business leaders and investors attempted the hopeless task of trying to pierce the veil of time and ignorance. The second was that the fluctuations in the wage level that classical economic theory relied on to bring the economy back into balance after such an investment fluctuation either did not work at all or worked too slowly to be relevant for economic policy. (No, I am not going to be drawn into a debate about "unemployment disequilibrium.") But Keynes believed that if these problems could be fixed, then the standard market-oriented toolkit of economists would once again be worthwhile and relevant. And he showed a way to fix them or at least come close enough to fixing them, a way that we still use today--as you can see if you watch what Alan Greenspan's Federal Open Market Committee does next week.

So buy these books. Read these books. These are great books. Time spent with them is time well-spent. Robert Skidelsky deserves great honors for having devoted so much of his life to writing down the story of John Maynard Keynes, and writing it down so well.

3315 words

Liveblogging World War I: August 19, 2014: The War on Belgium

From Barbara Tuchman's The Guns of August:

From Barbara Tuchman's The Guns of August:

The Belgians even more than von Bülow tried von Kluck’s temper. Their army by forcing the Germans to fight their way through delayed the schedule of march and by blowing up railroads and bridges disrupted the flow of ammunition, food, medicine, mail, and every other supply, causing the Germans a constant diversion of effort to keep open their lines to the rear. Civilians blocked roads and worst of all cut telephone and telegraph wires which dislocated communication not only between the German armies and OHL but also between army and army and corps and corps. This “extremely aggressive guerrilla warfare,” as von Kluck called it, and especially the sniping by franc-tireurs at German soldiers, exasperated him and his fellow commanders. From the moment his army entered Belgium he found it necessary to take, in his own words, “severe and inexorable reprisals” such as “the shooting of individuals and the burning of homes” against the “treacherous” attacks of the civil population.

Burned villages and dead hostages marked the path of the First Army. On August 19 after the Germans had crossed the Gette and found the Belgian Army withdrawn during the night, they vented their fury on Aerschot, a small town between the Gette and Brussels, the first to suffer a mass execution. In Aerschot 150 civilians were shot. The numbers were to grow larger as the process was repeated by von Bülow’s army at Ardennes and Tamines, by von Hausen’s in the culminating massacre of 664 at Dinant. The method was to assemble the inhabitants in the main square, women usually on one side and men on the other, select every tenth man or every second man or all on one side, according to the whim of the individual officer, march them to a nearby field or empty lot behind the railroad station and shoot them. In Belgium there are many towns whose cemeteries today have rows and rows of memorial stones inscribed with a name, the date 1914, and the legend, repeated over and over: “Fusillé par les Allemands”....

General von Hausen, commanding the Third Army... could not get over the “hostility of the Belgian people.” To discover “how we are hated” was a constant amazement to him. He complained bitterly of the attitude of the D’Eggremont family in whose luxurious château of forty rooms, with green-houses, gardens, and stable for fifty horses, he was billeted for one night. The elderly Count went around “with his fists clenched in his pockets”; the two sons absented themselves from the dinner table; the father came late to dinner and refused to talk or even respond to questions, and continued in this unpleasant attitude in spite of Hausen’s gracious forbearance in ordering his military police not to confiscate the Chinese and Japanese weapons collected by Count D’Eggremont during his diplomatic service in the Orient. It was a most distressing experience.

The German campaign of reprisals... had been prepared ahead of time.... It was... essential to enter France with every available battalion; Belgian resistance which required troops to be left behind interfered with this objective.... As soon as the Germans entered a town its walls became whitened, as if by a biblical plague, with a rash of posters plastered on every house warning the populace against acts of “hostility.”... “Any one approaching within 200 meters of an airplane or balloon post will be shot on the spot.” Owners of houses where hidden arms were discovered would be shot. Owners of homes where Belgian soldiers were found hidden would be sent to “perpetual” hard labor in Germany. Villages where acts of “hostility” were committed against German soldiers “will be burned.” If such an act took place “on the road between two villages, the same methods will be applied to the inhabitants of both.”... "All punishments will be executed without mercy, the whole community will be regarded as responsible, hostages will be taken in large numbers.”...

Von Kluck complained that somehow the methods employed “were slow in remedying the evil.” The Belgian populace continued to show the most implacable hostility. “These evil practices on the part of the population ate into the very vitals of our Army.” Reprisals grew more frequent and severe. The smoke of burning villages, the roads clogged with fleeing inhabitants, the mayors and burgomasters shot as hostages were reported to the world by the crowds of Allied, American, and other neutral correspondents who, barred from the front by Joffre and Kitchener, flocked to Belgium from the first day of war....

On August 19 as the fusillade of shots cracked through Aerschot twenty-five miles away, Brussels was ominously quiet. The government had left the day before. Flags still decked the streets refracting the sun through their red and yellow fabric. The capital in its last hours seemed to have an extra bloom, yet to be growing quieter, almost wistful. Just before the end the first French were seen, a squadron of weary cavalry riding slowly down the Avenue de la Toison d’Or with horses’ heads drooping. A few hours later four motorcars filled with officers in strange khaki uniforms drove by. People stared and raised a feeble cheer: “Les Anglais!” Belgium’s Allies had come at last—too late to save her capital. On the 19th refugees continued to stream in from the east. The flags were being taken down; the populace had been warned; there was a menace in the air...

Ferguson, MO: Black Town, White Power: Live from La Farine CCCXI: August 19, 2014

Jeff Smith: In Ferguson, Black Town, White Power: "St. Louis County contains 90 municipalities...

Jeff Smith: In Ferguson, Black Town, White Power: "St. Louis County contains 90 municipalities...

...most with their own city hall and police force. Many rely on revenue generated from traffic tickets and related fines. According to a study by the St. Louis nonprofit Better Together, Ferguson receives nearly one-quarter of its revenue from court fees.... With primarily white police forces that rely disproportionately on traffic citation revenue, blacks are pulled over, cited and arrested in numbers far exceeding their population share....

Majority-black Ferguson has a virtually all-white power structure: a white mayor; a school board with six white members and one Hispanic, which recently suspended a highly regarded young black superintendent who then resigned; a City Council with just one black member; and a 6 percent black police force.... The North County Labor Club, whose overwhelmingly white constituent unions (plumbers, pipe fitters, electrical workers, sprinkler fitters)... operates a potent voter-turnout operation that backs white candidates over black upstarts.... When the state patrol and the national television cameras leave Ferguson, its residents will still be talking about how they can move forward. And they may be ready to expand the conversation so that it’s not just about black and white, but green.

Matthew Yglesias: White political domination of Ferguson is doomed: "In Ferguson... African-Americans are not a minority...

...The town is 67 percent black, it just happens to have a government that's overwhelmingly dominated by whites including the mayor, the police chief, the school board, and the bulk of the city council... depend[ing] crucially on an atmosphere of public apathy and mass indifference to local politics.... As Zachary Roth has written, typically, fewer than 15 percent of eligible voters cast ballots in municipal elections in Ferguson. Ian Milhiser observes that the low turnout is in part a consequence of the city choosing to hold municipal elections in April of odd-numbered years. That makes patronage-based get-out-the-vote campaigns incredibly effective in controlling the levers of power...

August 18, 2014

Self-Aggregation and Curation for August 18, 2014: Equity Prices, Secular Stagnation, Smackdowns, NAFTA, and Such...

Sent on Aug 18, 2014 at 08:34 pm http://tinyletter.com/braddelong/archive...

Sent on Aug 18, 2014 at 08:34 pm http://tinyletter.com/braddelong/archive...

VoxEU has produced an eBook on secular stagnation. I review it. And I am coming round to the conclusion that this is a macroeconomic weakness that has plagued the global market economy in all times of trend deflation or low inflation since at least 1895, and perhaps 1865.

Robert Shiller writes about the mystery of high stock market elevations. I say the real mystery is why the average level of stock market valuations has been so low, given how attractive they are to patient capital and how much patient capital there ought to be.

Well, it seems that my letting my neoliberal freak flag fly on NAFTA has annoyed Robert Scott and Jeff Faux of the EPI. Lots to think about here...

The first good Brad DeLong Smackdown in months! Very welcome!! On adverse selection, and whether the health exchanges will in fact survive.

Talking Points Memo publishes a section of Rick Perlstein's excellent The Invisible Bridge on America 1973-76. And the press corps and the New York Times--yes, we are looking at you, Alexandra Alter--fails to cover itself with glory by playing opinions-of-shape-of-earth-differ journamalism rather than saying that bogus plagiarism allegations are bogus.

More on Making Sense of Friedrich A. von Hayek: A follow-up by me provoked by Lars Syll's sending me to Robert Solow's meditations; Milton Friedman, Friedrich Hayek, Augusto Pinochet, and Hu Jintao: Authoritarian Liberalism vs. Liberal Authoritarianism

I confuse myself about why Obama's CEA believes the work of recovery is mostly done. And then I take a look at the mancession and mancovery, and see signs--perhaps--of peak male.

Paul Krugman smacks me down for believing in the relative mental autonomy of even right-wing policy intellectuals.

And I respond by noting that Milton Friedman, Herb Stein, and Arthur Burns could overcome the elective affinity between their libertarian instincts and Goldbugist doctrines. So why--with notably rare exceptions--can't their successors do the same?

The 24-Year-Old Michael DeLong is campaign manager for Democrat Lianne Thompson in the mid-September CCC special election...

PLUS MOAR at the Equitablog and at Grasping Reality

Subscribe to the Email:

Enter your email address

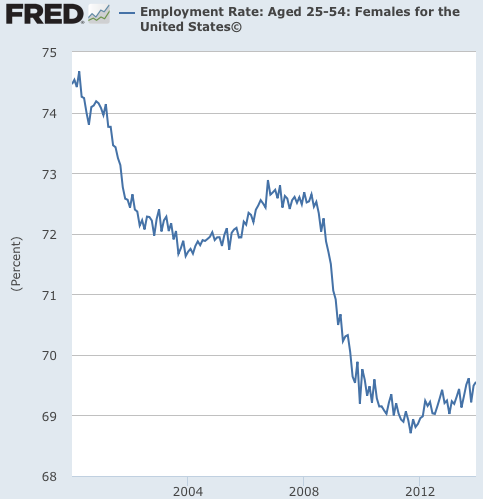

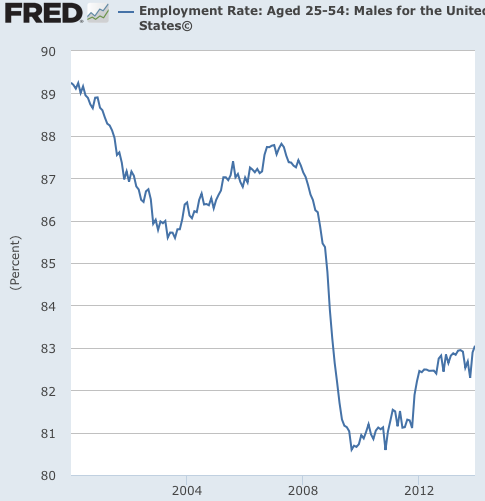

Male and Female Prime-Age Employment Rates since 2000

Over at Equitable Growth: Apropos of: In Which I Make Myself Very Confused About Cyclical Recovery: Monday Focus for August 18, 2014, Larry Summers emails: plot male and female prime-aged employment rates separately, and be afraid:

Females 25-54: A 3.0%-point decline from 72.5% in December 2007 to 69.5% in October 2008, and then near-flatline: 69.9% today. 1/9 of the decline from peak to trough recovered. Current 2.6%-point shortfall vis-a-vis December 2007.

Males 25-54: A 6.7%-point from 87.3% in December 2007 to 80.6% in October 2009, and then a 2.8%-point recovery to 83.4%. 2/5 of the decline from peak to trough recovered. Current 3.8%-point shortfall vis-a-vis December 2007.

As I said, none of these shortfalls are directly attributable to aging--and only very small amounts to increased at-home care of elderly relatives and increased education. And just what are these "non aging-related cohort effects" supposed to be, anyway? The collapse of real estate values and thus of potential retirement savings should have led to more desired labor force participation, not less:

I defy you to get any non-aging related cohort effect trend for females, and to get one for males greater than 1%-point/decade. That would, without hysteresis, give us half of the work of recovery done for males, 1/9 done for females, 1/3 overall.

Yes. I am afraid. I am very afraid...

Reviewing Lawrence Summers's et al.'s VoxEU Ebook on "Secular Stagnation": The Honest Broker for the Week of August 23, 2014

Over at Equitable Growth: The Setup:

Let's start with Paul Krugman, who made me aware of this ebook by writing:

Paul Krugman: All About Zero: "Way back in 2008 I (and many others) argued...

...that the financial crisis had pushed us into a liquidity trap... in which the Fed and its counterparts elsewhere couldn’t restore full employment even by reducing short-term interest rates all the way to zero.... In practice the zero lower bound has huge adverse effects on policy effectiveness... [and] drastically changes the rules... [as] virtue becomes vice and prudence is folly. We want less saving, higher expected inflation, and more.... Liquidity-trap analysis has been overwhelmingly successful in its predictions: massive deficits didn’t drive up interest rates, enormous increases in the monetary base didn’t cause inflation, and fiscal austerity was associated with large declines in output and employment.... READ MOAR

Secular stagnation adds... the strong possibility that this Alice-through-the-looking-glass world is the new normal.... This raises problems even for advocates of unconventional policies, who all too often predicate their ideas on the notion that normality will return in the not-too-distant future. It raises even bigger problems with people and institutions that are eager to “normalize” .... Do we know that secular stagnation is here? No. But the case is strong enough that it should color almost every policy discussion.

Start with the observation that in the entire twentieth century only during the Great Depression was the nominal interest rate the U.S. government paid on its debt less more than the trend rate of nominal GDP growth--and the deflation of the Great Depression is not going to come again:

And note that this is a twentieth-century fact only: in the slower real-growth and (usually) precious-metal commodity-money standard nineteenth century, the interest rate on U.S. government debt was more likely to be above than below the trend rate of nominal GDP growth:

Note that this does not mean that in the twentieth century ex-the Great Depression the U.S. economy was "dynamically inefficient": it would not have been possible to raise consumption in every (or, indeed, in most) states of the world by investing less at the start and maintaining a lower capital-output ratio throughout. Only if there were a large external price-taking entity willing to (a) accept deposits from the U.S. and pay them the U.S. Treasury rate, and (b) pay the outsized equity premium return to U.S. citizens willing to accept their equity risk would any such transaction have been possible. There never was any such entity. The best way to conceptualize it, I think, is that U.S. wealthholders were (and are) prepared to pay U.S. taxpayers via the intermediary of the U.S. government an extraordinarily outsized fee--vastly more than could be justified by any utility value of risk-bearing derived from a declining marginal utility of consumption--for allowing them to use its financial instruments to transfer their purchasing power into the future in a (relatively) safe and secure way.

But this does mean that the issues that Larry Summers has brought to the forefront of the current economists' discussion under the rubric of "secular stagnation" have in fact been present since the beginning of large-scale gold-mining in the Witwatersrand in the mid-1890s and the accompanying non-adjustment of nominal interest rates to the acceleration of inflation and nominal GDP growth generated by that shift in monetary regime.

The "Secular Stagnation" Argument:

The voxEU ebook Secular Stagnation begins with a chapter by Lawrence Summers that sets out the playing field:

Lawrence Summers: Reflections on the ‘New Secular Stagnation’ Hypothesis: "The experience of Japan in the 1990s and now that of Europe and the US suggests...

...theories that take the average level of output and employment over a long time period as given are close to useless.... The ‘new secular stagnation hypothesis’ responds to recent experience and the manifest inadequacy of conventional formulations by raising the possibility that it may be impossible for an economy to achieve full employment, satisfactory growth, and financial stability simultaneously simply through the operation of conventional monetary policy. It thus provides a possible explanation for the dismal pace of recovery in the industrial world, and also for the emergence of financial stability problems as an increasingly salient concern....

If a financial crisis represents a kind of power failure, one would expect growth to accelerate after its resolution as those who could not express demand because of a lack of credit were enabled to do so. Unfortunately, it appears that the difficulty that has arisen in recent years in achieving adequate growth has been present for a long time, but has been masked by unsustainable finances. Here it is instructive to consider the performance of the US and Eurozone economies prior to onset of financial crisis in 2007.

Let us begin with the US. It is certainly fair to say that growth was adequate--perhaps even good--during the 2003–2007 period. It would not be right to say either that growth was spectacular or that the economy was overheating during this period. And yet this was the time of vast erosion of credit standards, the biggest housing bubble in a century, the emergence of substantial budget deficits, and what many criticise as lax monetary and regulatory policies.

Imagine that US credit standards had been maintained, that housing had not turned into a bubble, and that fiscal and monetary policy had not been simulative. In all likelihood, output growth would have been manifestly inadequate because of an insufficiency of demand. Prior to 2003, the economy was in the throes of the 2001 downturn, and prior to that it was being driven by the internet and stock market bubbles of the late 1990s. So it has been close to 20 years since the American economy grew at a healthy pace supported by sustainable finance...

In this formulation, "sustainable finance" as a placeholder that needs definition and elaboration. What does Summers mean by "sustainable finance" in this context? One piece of the definition is clear:

"Sustainable finance" requires an economy-wide willingness to invest enough in the formation of risky capital assets to carry employment up to its NAIRU level without requiring irrational and unsustainable expectations of the ongoing real price appreciation of the capital assets invested in.

The fact that NAIRU-level employment in the U.S. in the later 1990s was achieved only via irrational and unsustainable expectations of the appreciation of high-tech capital assets and in the mid-2000s was achieved only by irrational and unsustainable expectations of house price appreciation tells us that finance then was not "sustainable". And in the absence of such bubbly expectations and asset price patterns, the U.S. economy to a small extent in the early 1990s, to a significant extent in the early 2000s, and to a complete extent now has been unable to pull itself up to the NAIRU level of employment and up to previous confident expectations of where potential output growth would take us.

What is the next analytic step? Think of an economy with three kinds of financial assets: cash that pays a nominal interest rate of zero, relatively-safe interest-bearing government bonds with nominal interest rates that substitution for cash keeps from dropping below or even to zero, and claims--call them equities--on risky private capital investments that must given their returns--warranted profits plus rational or irrational expected capital-asset price appreciation plus inflation--offer a high enough spread vis-à-vis government bonds to induce new issues. The problem, then, is that without bubbles warranted profits plus inflation do not reach a high enough premium over the zero nominal bound on cash to allow for enough investment to attain the NAIRU employment level. There are then five obvious solutions:

Have the government undertake more of the long-term capital formation in the economy, thus spreading the risk-bearing capacity of the private sector over a smaller required number of private investment projects and so reducing the risk premium until the NAIRU level of employment is attainable via "sustainable finance".

Raise the return on private investment.

Raise the share of income citizens seek to spend on consumption.

Have the government explicitly or implicitly bear some risk either via loan guarantees or lender-of-last-resort backstops, thus reducing the amount of risk-bearing capacity each project needs and so reducing the private risk premium until the NAIRU level of employment is attainable via "sustainable finance".

Have the inflation target rise, so that the wedge between warranted profits plus inflation and zero is large enough for the NAIRU level of employment to be attainable via "sustainable finance".

Summers expresses doubts about (4) and (5):

Low nominal and real interest rates undermine financial stability in various ways. They increase risk-taking as investors reach for yield, promote irresponsible lending as coupon obligations become very low and easy to meet, and make Ponzi financial structures more attractive as interest rates look low relative to expected growth rates.... Operating with a higher inflation rate target... ways such as quantitative easing that operate to reduce credit or term premiums... are also likely to increase financial stability risks...

And he advocates (1), (2), and (3), calling for:

increased public investment...

so that risk-bearing capacity can be spread over fewer required investment projects, and:

a commitment to maintain basic social protections so as to maintain spending power, and measures to reduce inequality and so redistribute income towards those with a higher propensity to spend...

to similarly reduce the amount of required investment projects, plus:

reductions in structural barriers to private investment and measures to promote business confidence...

to raise warranted profits.

One possible further analytical step--one Summers does not take--would be to note that the industrial market economy seemed to run into significant cyclical and political distress in the years before the 1895 trend break and shift to a more inflationary monetary regime, returned to a time of troubles as governments attempted to enforce deflation on their economies in the 1920s and 1930s, and has endured a renewed time of troubles with the Plaza-driven deflation of the yen and the post-Volcker decision to reduce North Atlantic inflation rates from 4%/year to less than 2%/year. It would then draw the conclusion that what we need now is what we needed in both the late 1920s and the early 1890s: a higher trend inflation target.

Another possible analytical step--one that Summers takes but does not develop--would be to develop more fully his argument that a higher trend inflation rate and a government that takes active steps to reduce risk premiums both risk increasing financial instability through various channels.

Indeed, I believe that a stronger argument against the "all we need is a higher inflation target" solution (5) is made by Paul Krugman:

You can get traction if you can credibly promise higher inflation.... But what does it take to credibly promise inflation? It has to involve a strong element of self-fulfilling prophecy: people have to believe in higher inflation, which produces an economic boom, which yields the promised inflation. A necessary (though not sufficient) condition for this to work is that the promised inflation be high enough that it will indeed produce an economic boom if people believe the promise will be kept. If it is not high enough, then the actual rate of inflation will fall short of the promise even if people do believe in the promise, which means that they will stop believing after a while, and the whole effort will fail.... I have come to think of [this] as the ‘timidity trap’...

And Krugman takes aim at (1) as well:

What about fiscal policy? Here the standard argument is that deficit spending can serve as a bridge across a temporary problem, supporting demand while, for example, households pay down debt and restore the health of their balance sheets, at which point they begin spending normally again....But what if a negative real natural rate isn’t a temporary phenomenon? Is there a fiscally sustainable way to keep supporting demand?

But gives no answers:

In this chapter I’ll leave these questions hanging...

Elaboration:

How is this framework developed by and these themes launched by Summers elaborated by the other contributors to VoxEU's Secular Stagnation? In various ways. Eggertsson and Mehrota build a formal model and begin the process of exploring exactly what the mechanisms are. Guntram Wolff backs up Summers's and Krugman's fears that monetary policy and announcement of a higher inflation target cannot do the job: the Inflation Expectations Imp is no easier to summon than is the Business Confidence Fairy.

Caballero and Farhi and Blanchard, Furceri, and Pescatori develop the issues by worrying the issue of the relative supply and demand of safe and risky assets as something that affects the risk premium and thus the ability of an economy to achieve a NAIRU employment level with sustainable finance. Richard Koo suggests that if only leverage could be reduced and balance sheets righted the problems that Summers identifies would vanish. (I am skeptical, largely because I see the problems as perhaps present since the 1870s.) And Jimeno, Smets, and Yiangou call--yet again--for structural reform and accelerated deleveraging.

Nick Crafts sees Summers as more-or-less a hypochondriac as far as the U.S. is concerned, but on target for western Europe because: "European demographics are less favourable.... Productivity growth in Europe will underperform.... Fiscal consolidation... will bear relatively heavily on Europe.... [And] in a depressed economy, the Fed is more likely to take appropriate policy action than the ECB..." Thus: "Europeans should be much more afraid than Americans..."

Barry Eichengreen dismisses the possibility that a slowed rate of technological progress has reduced the rate of profit. Perhaps the inventions that really matter for our utility have already been made. But the rate of profit depends on the pace of innovation in those sectors on which we spend our money even if progress there has little effect on our utility. And the incentives to innovate in the sectors on which we spend our money remain very high. He dismisses the idea of a permanent global savings glut because he sees China as shifting from foreign asset accumulation for domestic consumption.

However, Eichengreen fears that the right-wing dismissal of the value of government has led the North Atlantic to eat its publicly-provided seed corn. And he also fears the hysteresis consequences for potential output of the failure to stimulate aggregate demand enough via fiscal, banking, housing, and monetary policies. Thus the secular stagnation he fears is a self-inflicted one: much less interesting to an intellectual economist than Summers's variety, and much easier to cure from a technocrat economist point of view, but, alas!, quite probably harder for us to deal with here on the ground where we live in the Sewer of Romulus, A very different place from the Republic of Plato.

Growth and Distribution:

Somewhat orthogonal to the macro-finance-inflation-demand concerns of the main thrust of the book are Robert Gordon, Joel Mokyr, and Ed Glaeser.

Robert Gordon sees an aging society, the plucking of all the low-hanging fruit from raising education levels, A widening gap between real GDP and societal welfare as income inequality continues its inexorable technology-driven march upwards, and continued failure to either raise taxes to a level that can fund the benefits that citizens demand or to lower benefits to a level consistent with the taxes that the rich who control the loophole-generating mechanisms of government. These four headwinds, he says, Will reduce the pace of American economic growth significantly. And he sees no reason to imagine that total factor productivity growth will offset these headwinds by jumping up from the rate it has exhibited over the past four decades to the higher Second Industrial Revolution rate it exhibited over 1920-1970.

Joel Mokyr, by contrast, sees the future of technology as carrying us to a near-singular state:

Compared to the tools we have today for scientific research, those of Galileo and Pasteur look like stone-age tools.... It is not just ‘IT’ or ‘communications’.... This very human shortfall of imagination is largely responsible for much of today’s pessimism. In many other respects, too, the labour-market outlook is not wholly bleak... if telecommuting and driverless cars can cut the commuting time... at least one major (and uncounted) tax on workers will be eliminated. Such an improvement would not be reflected in the aggregate output and productivity statistics...

And thus sees worries about 'secular stagnation' of any form as fundamentally wrongheaded.

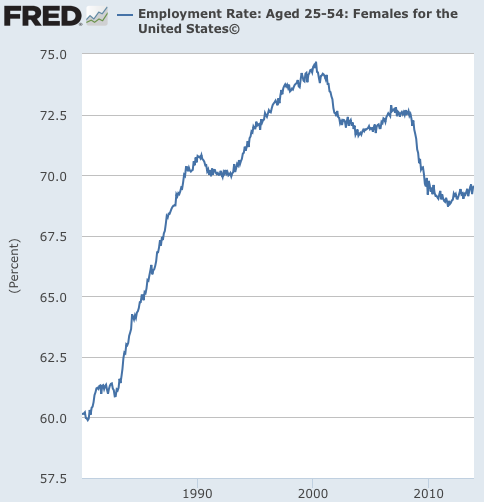

Ed Glaeser does not see any form of true secular stagnation--"innovation seems unrelenting, at least to me, and I believe that such innovation is the stuff of longer-term economic growth.... I also believe that the benefits of future innovation will continue to flow to a wide swath of humanity, at least in their capacity... as consumers". What he does see as a crisis is the decline in prime-aged male employment in the U.S. from 95% in the 1950s to 87% before 2008, and 83% today. Largely agnostic about causes, he calls for a two-bladed scissors approach: supply-side sticks to make being idle less comfortable via reduced disability insurance and other social-welfare programs that cushion being without an income for the long term, and "targeted investments in education and workforce training" and perhaps in employment-heavy economic sectors.

Conclusion:

It is very clear to me that Larry Summers did both well and ill when he chose the phrase "secular stagnation" has the label for his argument. He did well because his argument is clearly the same and its macroeconomic aspects as the argument that Alvin Hansen made in his presidential address, and using a phrase that harkens back to that is apposite and useful. He did ill because Hansen saw the root cause as technological exhaustion. I see no signs of technological exhaustion. Yet that label leads people to look for signs of actual technological exhaustion, and this leads to what I see is barking up the wrong or at least a different tree. There should really be three conversations: a macroeconomic structure for demand management conversation, a demography and inequality conversation, and an information economy conversation. Mashing them together does not do much to enlighten.

Instead, I see the root causes as the confluence of an unreasonably high premium return on equities and other risky assets with a deflation or a very low inflation price trend. And where Summers sees this as operating since the mid-1990s and the start of the dot-com boom, I see it as operating since 1895, if not 1865.

What questions do I have? I have many. What answers am I confident of? I am confident of none. What guesses do I have? I have made many in the pages above, but let me make one more: if he returned up to Paul Volker is 4%/year inflation target and beefed up our financial-sector capital requirements, I would give 3-1 odds that in 15 years "secular stagnation" with no longer make our list of the top 10 big North Atlantic macroeconomic issues. But maybe I am wrong: maybe our bubble worries would then be an order of magnitude more severe...

3180 words

Noted for Your Lunchtime Procrastination for August 18, 2014

Over at Equitable Growth--The Equitablog

Nick Bunker: Who bears the burden of labor-market slack?

Over at Equitable Growth: In Which I Make Myself Very Confused About Cyclical Recovery: Monday Focus for August 18, 2014 - Washington Center for Equitable Growth

Morning Must-Read: Mark Thoma (2011): Income Redistribution: The Key to Economic Growth? - Washington Center for Equitable Growth

Morning Must-Read: Nick Bunker: The Downside of Declining Domestic Migration - Washington Center for Equitable Growth

Over at Grasping Reality: Monday DeLong Smackdown: The Wellsprings of Bad Monetary Economics in Goldbugism (Brad DeLong's Grasping Reality...) - Washington Center for Equitable Growth

Evening Must-Read: Alon Levy: Zoning and Market Pricing of Housing - Washington Center for Equitable Growth

Afternoon Must-Read: Wolfgang Munchau: Draghi is running out of legal ways to fix the euro - Washington Center for Equitable Growth

Under What Circumstances Should You Worry That the Stock Market Is "too High"?: The Honest Broker for the Week of August 16, 2014 - Washington Center for Equitable Growth

Nighttime Must-Read: Ethan Zuckerman: The Internet's Original Sin - Washington Center for Equitable Growth

Evening Must-Read: Daniel Davies: D-squared Digest--FOR Bigger Pies and Shorter Hours and AGAINST More-or-Less Everything Else - Washington Center for Equitable Growth

Plus:

Things to Read at Lunchtime on August 18, 2014 - Washington Center for Equitable Growth

Must- and Shall-Reads:

Ethan Zuckerman: The Internet's Original Sin: "It's not too late to ditch the ad-based business model and build a better web. What we wanted to do was to build a tool that made it easy for everyone, everywhere to share knowledge, opinions, ideas and photos of cute cats. As everyone knows, we had some problems, primarily business model problems.... At the end of the day, the business model that got us funded was advertising... [the] revenue source is investor storytime: Investor storytime is when someone pays you to tell them how rich they’ll get when you finally put ads on your site.... The key part of investor storytime is persuading investors that your ads will be worth more than everyone else’s ads.... Demonstrating that you’re going to target more and better than Facebook requires moving deeper into the world of surveillance..."

Wolfgang Münchau: Wolfgang Munchau: Draghi is running out of legal ways to fix the euro "The ECB is failing to deliver on its inflation target not because it has run out of instruments but because it has based its policy on a poorly performing economic model... [and so] has committed three errors.... The ECB should have embarked on large asset purchases and cut interest rates to zero early on.... Mr Draghi’s promise to buy eurozone government debt... made everybody, including the ECB itself, complacent... [and] ended all crisis resolution. The third mistake was to misjudge the dynamics of the fall in inflation rates late last year.... By pussyfooting around... the ECB has signalled that it is safe to bet against the inflation target.... To undo this would take some heavy lifting.... The ECB should start by ditching the inflation target and replacing it with a price-level target.... The ECB should starting buying equities and junk bonds. It should subsidise mortgages and consumer credit. It could fund an investment programme in transport infrastructure, energy networks and scientific research.... All these measures would be effective. Most would be illegal. The one thing the central bank can do without any legal problems would be to drop the silly macroeconomic model--known as the Smets-Wouters model, after its authors--on which it has been relying for too long. My guess is that the ECB will not do any of these..."

Alon Levy: Zoning and Market Pricing of Housing: "The question of the effects of the supply restrictions in zoning on housing prices has erupted among leftist urbanist bloggers again. On the side saying that US urban housing prices are rising because of zoning.... On the side saying that zoning doesn’t matter and the problem is demand (and by implication demand needs to be curbed).... This is not a post about why rising prices really are a matter of supply. I will briefly explain why they are, but the bulk of this post is about why, given that this is the case, cities need to apportion the bulk of their housing via market pricing and not rent controls, as a matter of good political economy. Few do, which is also explainable in terms of political economy..."

Nick Bunker: The downside of declining domestic migration: "Over the past 30 years or so, U.S. workers have become less likely to move.... An emerging hypothesis is that migration is declining because the benefits of migration are, too... structural changes in the labor market.... Research by economists at the International Monetary Fund shows a negative side to the decline in mobility. The paper considers migration as a way for workers to respond to a job loss.... Instead of moving on, workers drop out..."

Mark Thoma (2011): Income Redistribution: The Key to Economic Growth?: "There is an equivalent of a Laffer curve for inequality, but the variable of interest is economic growth rather than tax revenue. We know that a society with perfect equality does not grow at the fastest possible rate.... We also know that a society where one person has almost everything while everyone else struggles to survive... will not grow at the fastest possible rate either.... We may be near or even past the level of inequality where growth begins falling.... But... why take a chance? I’d prefer to see policies implemented to reduce inequality--given the present, elevated level of inequality, a reduction is unlikely to have much of an impact on incentives. But at a minimum we should resist further increases.... I’ve never favored redistributive policies, except to correct distortions in the distribution of income resulting from market failure, political power, bequests and other impediments to fair competition and equal opportunity. I’ve always believed that the best approach is to level the playing field.... But increasingly I am of the view that even if we could level the domestic playing field, it still won’t solve our wage stagnation and inequality problems.... We’ve given the market economy 40 years to solve the problem of growing inequality, and the result has been even more inequality.... If we want to preserve a growing and socially healthy economy, and avoid moving to lower growth points on the inequality curve, then we will need to do much more redistribution of income than we have done over the last several decades..."

Tim Harford: Monopoly is a bureaucrat’s friend but a democrat’s foe: "No policy can guarantee innovation, financial stability, sharper focus on social problems, healthier democracies, higher quality and lower prices. But assertive competition policy would improve our odds.... Such structural approaches are more effective than looking over the shoulders of giant corporations and nagging them.... As human freedoms go, the freedom to take your custom elsewhere is not a grand or noble one – but neither is it one that we should abandon without a fight."

Kris James Mitchener and Kirsten Wandschneider: Great Depression recovery: The role of capital controls: "The IMF has recently revised its position on capital controls, acknowledging that they may help prevent financial crises.... During the Great Depression capital controls appear not to have been successfully used as tools for rescuing banking systems, stimulating domestic output, or for raising prices. Rather they appear to have been maintained as a means for restricting trade and repayment of foreign debts."

And Over Here:

Over at Equitable Growth: In Which I Make Myself Very Confused About Cyclical Recovery: Monday Focus for August 18, 2014 (Brad DeLong's Grasping Reality...)

Monday DeLong Smackdown: The Wellsprings of Bad Monetary Economics in Goldbugism (Brad DeLong's Grasping Reality...)

Michael Daly: The Day Ferguson MO Cops Were Caught in a Bloody Lie: Live from La Farine CCCX: August 18, 2014 (Brad DeLong's Grasping Reality...)

Liveblogging World War II: August 18, 1944: Falaise (Brad DeLong's Grasping Reality...)

Liveblogging World War I: August 17, 1914: Belgium and Lorraine (Brad DeLong's Grasping Reality...)

Weekend Reading: Josh Brown and Jeff Macke: Joe Granville: The Man Who Moved Markets (Brad DeLong's Grasping Reality...)

Under What Circumstances Should You Worry That the Stock Market Is "too High"?: The Honest Broker for the Week of August 16, 2014 (Brad DeLong's Grasping Reality...)

Alexander Hamilton at the Constitutional Convention: Weekend Reading (Brad DeLong's Grasping Reality...)

Liveblogging World War II: August 16, 1944: Falaise Pocket (Brad DeLong's Grasping Reality...)

Morning Must-Read: Noah Smith: Silicon Valley Can Solve the Big Problems (Brad DeLong's Grasping Reality...)

Weekend Reading: McSweeney’s Internet Tendency: Unused Audio Commentary By Howard Zinn And Noam Chomsky, Recorded Summer 2002 For The Fellowship Of The Ring (Platinum Series Extended Edition) Dvd. Part One. (Brad DeLong's Grasping Reality...)

And:

Brad DeLong: The Honest Broker: Mr. Piketty and the “Neoclassicists”: A Suggested Interpretation: For the Week of May 17, 2014 (DeLong: Long Form)

Julia Ioffe: What White St. Louis Thinks About Ferguson

Orwell's review of Mein Kampf

Should Be Aware of:

Joshua Gans: The ownership of the machines: "The story in the video is that if you don’t think the robots can replace you (a) look back at the horses and (b) look forward at what’s happening in robot technology now. But because it does its job so clearly, I thought it would be useful to consider a little more carefully the economics of all this and whether, indeed, there will be mass unemployment in the future.... For a human to be displaced by a robot in a job the robot (a) has to have a quality advantage and (b) the human productivity must be so low that even if the wage drops to minimum (by law or subsistence or opportunity cost), they will be uncompetitive.... The Brynjolfsson-McAfee line is that they will need to acquire other skills and, more to the point, it is not clear the market can work (or at least work fast enough for our liking) to make that happen.... A collective agency will step in to ensure those people can pay for the product so that normal market based prices will be formed and transactions will take place. That agency is obvious in democratic society: the government.... I have faith that if it is in the interests of both business and consumers that money go from the employed to unemployed, it will.... But there is another mechanism which goes back to the title of this post. The presumption is always that the bourgeoisie rather than the proletariat owns the machines. But why should that be the case?"

John Scalzi: Thoughts On the Hugo Awards, 2014 "What did I really think of the 'sad puppy' slate of nominees championed by Larry Correia?... They played within the rules, so game on, and the game is to convince people that your work deserves the Hugo. It does not appear the voters were convinced.... Correia was foolish to put his own personal capital as a successful and best selling novelist into championing Vox Day and his novelette, because Vox Day is a real s---hole of a human being, and his novelette was, to put it charitably, not good.... Doing that changed the argument from something perfectly legitimate, if debatable--that conservative writers are often ignored for or discounted on award ballots because their personal politics generally conflict with those of the award voters--into a different argument entirely, i.e., 'f--- you, we got an undeserving bigot s---hole on the Hugo ballot, how you like them apples?'... Correia will be happy to tell you that his Hugo loss doesn’t matter to him.... I do wonder if he considered how other people that were seen as part of his slate feel the same way.... If he really wanted to make the argument that a particular set of writers are ignored by award voters, that he went about making the argument in just about the worst way possible. Bad strategy, bad tactics, bad result."

Daron Acemoglu and James Robinson: Do People Really Dislike the State So Much? "David Nugent... the department and city of Chachapoyas in Northeastern Perú... the extension of state authority and power to integrate Chachapoyas more firmly into the Peruvian state. Nugent shows that though this might have been highly adverse for the castas, it was not so for everyone. Most important, what put this dynamic of expansion into motion was not some autonomous impulse from Lima coercively imposed, but local demands from Chachapoyas. Chachapoyas was the fiefdom of the castas, but Perú had a constitution which enshrined things like the rule of law, security of property. During the 1920s Nugent shows how social mobilization in Chachapoyas, mostly started by a few elites who had got an education in Lima, began to demand the end of casta rule. Critically, they demanded the expansion of state power as a tool to free the society from the rule of the castas who they saw as violators of their basic rights as Peruvian citizens.... So this is James Scott’s thesis upside down! Rather than fleeing from the state and resisting it, ordinary people are demanding the expansion of its authority in order to attain freedom from arbitrary and coercive local elites..."

Over at Equitable Growth: In Which I Make Myself Very Confused About Cyclical Recovery: Monday Focus for August 18, 2014

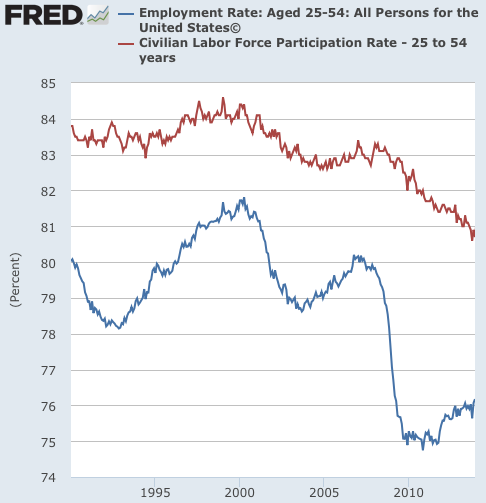

Over at Equitable Growth: Will somebody please tell me that I have made a gross arithmetic error in what is below, and can be much more optimistic?

Let me start with this graph:

Perhaps a few more 25-54 year olds are in school today than in 2000 or 2007. But only a few. As best as I can see, no more 25-54 year olds are having kids than in 2000 or 2007. And only a very few more 25-54 year olds are staying home to care for elderly relatives than in 2000 or 2007. But I look at this graph--my standard graph for trying to ascertain the cyclical- and hysteresis- state of the U.S. labor market without confusing the demographic effects of population aging with those of the Great Recession Lesser Depression of 2008-?. I see a huge excess decline in participation driven by "hysteresis" that is permanent damage to economic potential produced by the catastrophe. And I see, over and above that, only 1/3 of the work accomplished of cyclical recovery back to a normal spread between prime-aged participation and prime-aged employment.

Thus I really do not understand the triumphalism of the very sharp Steve Braun et al. from the CEA here:

Steve Braun et al.: The decline in the labour force participation in the US: In part due to the vigorous, multi-front response...

...to the economic crisis, the US has enjoyed a sustained economic recovery that has exceeded most contemporaneous and historical financial crisis benchmarks. Up until a year ago, the unemployment rate was falling by an average of 0.7 percentage points per year, roughly tracking the more successful historical experiences, and well exceeding the norm following a financial crisis. In the past year, the pace of the decline in the unemployment rate has doubled. As a result, the official unemployment rate is 83% of the way back to its pre-Global Crisis average. A variety of other indicators--such as broader measures of labour market underutilisation that include discouraged workers or marginally attached workers as well as unemployment rates for different demographic groups--show similar magnitudes of recovery...

So the labor market is, they say, 5/6 of the way back to normal--the current unemployment rate of 6.2% is 3.8%-points down from the peak of 10.0%, and has only 0.8%-point left to go before it hits a pre-crisis NAIRU of 5.4%. When it does, we will attain a "cyclically normal" labor market with a participation rate at 63.4%, 0.5%-points higher than today's 62.9%, and an associated employment-to-population ratio of 60.0%.

By that metric, we have done 3/4 of the work of cyclical recovery: from a 5.5%-point gap between employment and participation at the trough to a 3.9%-point gap now and a 3.4%-point gap at NAIRU. We will have made 1.7%-points back from the trough on the employment-to-population ratio when cyclical recovery is complete. The permanent damage to employment from the Great Recession Lesser Depression appears to be less than 0.9%-points of participation because there are also ongoing "cohort effects unrelated to aging" that reduce participation.

Let me stress that this is not senior and not-so-senior White House officials under pressure from political operatives putting as positive a spin on things as they can without actually losing their... No: what I mean to say is this: this is what the CEA's Steven Braun, John Coglianese, Jason Furman, Betsey Stevenson, and Jim Stock actually believe is true about the world--that the labor market is recovering successfully and strongly from the disaster of 2008-9.

But I look at 25-54. The employment rate is down from 79.9% in 2007 to 76.6% in July 2014--3.3%-points less, compared to 4.0%-point a fall from 63% to 59% over the entire population. The participation rate is down from 80.8% in July 2014 compared to 83.1% for 2007--2.3%-points, compared to the 3.1%-point fall from 66.0% to 62.9% over the entire population.

A normal NAIRU spread would put the 25-54 employment-to-population ratio at 78.7%, 2.5%-points below the 81.2% cyclically-adjusted 25-54 participation ratio. When cyclical recovery is complete, we would then expect to make back 3.7%-points back from the trough on the 25-54 employment-to-population ratio. So far we have made back only 1.0%-point.

So which is it? Has hysteresis done 1.8%-points of damage to 25-54 employment or 0.9%-points to total employment? Have we done 3/4 of the work of recovery relative to the proper labor force-trend share benchmark? Or have we done only 1/3 of the work of recovery?

The 25-54 data and the economy-wide aging trend-adjusted data used by the CEA appear to be telling us very different things both about the cyclical state of the labor market and about the damage done by hysteresis. How to reconcile? Which is right?

806 words

Monday DeLong Smackdown: The Wellsprings of Bad Monetary Economics in Goldbugism

Finally! The Internet comes through with a high-quality DeLong smackdown! Hooray!

Finally! The Internet comes through with a high-quality DeLong smackdown! Hooray!

Paul Krugman: Inflation OCD: "Brad DeLong... falls short...

...trying to attribute it to bad models or just finding it incomprehensible.... There’s something deeper at work here.... Clinging to beliefs that have been wrong, wrong, wrong for so long--beliefs that would have cost you money if you acted on them--and remember, Eric Cantor, the lost white knight of the Reformicons, did in fact do just that--shows that there is some underlying reason those beliefs are a necessary part of the right-wing identity.

What has to be going on is that the general hatred of government activism, the constant complaint that bureaucrats are taking away your hard-earned wealth and giving it to moochers and looters, carries with it an overwhelming need to see fiat money as theft. Even alleged moderate Republicans do it. It’s a form of obsessive-compulsive political disorder, and not susceptible to rational argument.

And this in turn means that the market monetarists have a hopeless task. James Pethokoukis... needs to ask why that obsession persists... after five years of utter empirical failure...

There are two topics on which, in my experience, conservatives become completely unhinged.... Health care, where the possibility of a successful government-backed program is unacceptable despite the fact that everyone, even America for its seniors, does it, and... monetary policy. It’s time to stop pretending that these are rational discussions, and start looking for the roots of the compulsion.

Yes, but...

First, historically, we do see fiat currencies inflated away. Under enormous military pressure from the armies of France and Sweden, and seeing its project of saving the souls of the people of northern Europe by using its army to teach them to be good Catholics, the seventeenth-century Imperial Spain of Felipe IV Habsburg removes the silver from its vellon currency so it can mint more to pay for supplies, and is then surprised to see the resulting inflationary spiral. Since the inflation is undermining the sinews of the Counterreformation, it is thus a theological matter, and responsibility for controlling it is given by King Felipe to... the Spanish Inquisition. Which nobody expects. Certainly not here. An inflationary spiral is, in the grand sweep of history, the most likely failure mode of a fiat monetary system, or one that becomes fiat.

Second, given this history, it makes sense to begin a monetary analysis with a crude quantity theory--most of the time the velocity of money is not that sensitive to interest-rate movements and interest rates do not move that much. And it makes sense to use a crude fiscal theory of the price level to assess the likelihood that political necessity will overwhelm the desire of the Master of Coin to keep his reputation and trigger the inflationary failure mode. Is is true that such a failure is close to zero-sum: creditors lose, and debtors gain and taxpayers gain as much to first-order. But since the creditors are the rich and the rich are the creditors, inflation is something for the rich to fear, and the rich because they are the rich have the megaphones.

Third, one important piece of the puzzle is that this time--or, rather, since the end of World War I--it is different. Before the Great Depression, all previous episodes of commercial and industrial distress had been associated not with low but with high interest rates on safe paper financial assets. They had seen an excess demand for gold or for things as good as gold, by Walras's Law the counterpart of that excess in a general-glut excess supply of currently-produced goods and services, and all interest- and dividend-paying securities going to substantial discounts as those caught short tried to dump their other assets to raise liquidity.

To my knowledge there was no example of a depressed economy at the zero lower bound on safe nominal short-term interest rate before the Great Depression. And to my knowledge there was no theorizing about the possibility of such a configuration before Fisher (1933) and Keynes (1936)--in Wicksell all I can find are worries that the central bank will not reduce the market rate of interest to a natural rate that has fallen, not worries that the central bank cannot rebalance the economy because the natural rate is less than zero. The liquidity trap is something that has been seen three and only three times in world history. Previous episodes of a depressed economy and a shortage of enterprise were better modeled as due to monetary stringency--high interest rates--or a fear of confiscation of entrepreneurial wealth by the powerful.

If, therefore, you were Alissa Zinovievna Rosenbaum--fleeing Bolshevik Russia for New York in 1926, with Lenin and Nicholas II Romanov (for whom the cossacks worked) as your major reference points for what the government did--the ideas that (a) the government's central purpose was to keep everybody shut up and in line and (b) fiat money was a tool it used to steal everybody's stuff through inflation would be quite reasonable. Her claim--"those pieces of paper in your wallet... which should have been gold"--in what Paul Ryan used to say was his favorite speech, that we need to have not just a currency linked to gold but to do all transactions in gold is quite nutty in our day given that the world has changed. But the real offenses in her writings are elsewhere. Cf. Mallory Ortberg:

Mallory Ortberg: Ayn Rand's Harry Potter and the Goblet of Fire: "'“Cho Chang'...

...Harry called from across the hallway, and quickly closed the distance between them, like some sort of sexually compelling locomotive. “The Yule Ball is tomorrow. I wish to acquire you for it. Say yes, now, with your mouth, before I cruelly crush it against my own, like some sort of sexual flower.”

“Oh. Harry,” Cho said, “I’m sorry but someone’s already asked me. And well, I’ve, I’ve said I’ll go with him.”

“I refuse to allow you to live in the world of the mediocre,” Harry said, eyes flashing flint and fire. “You are the only acceptable mate for me. I will hold you in my arms in front of our peers at the Yule Ball. Reconcile yourself to your fate, and wear something red or purple.”

“Harry, I’m sorry, but--”

“You’ll wear your hair down,” he said carelessly. “It suits you best that way. I have nothing left to say to you at present. I don’t think I’ll kiss you just yet. Go make whatever feminine preparations you have to make before tomorrow night.”

Given the long-run historical record and given the temporal stickiness of ideas, that conservatives start from theories--the naive mechanical quantity theory of money, the naive fiscal theory of the price level, and a form of Lafferism that sees security of property and low tax rates as the principal requisites of commercial and industrial prosperity--that were by and large adequate for the pre-World War I era but have not been adequate sense is, to me, not surprising. And that it should be difficult to argue them out of these frames of mind is, to me, not surprising.

What is surprising is the professional economists of note and reputation.

In an earlier day, the professional Republican economists had no problem pushing the goldbugs to the margins of, well, Reason magazine and its World War II Revisionism issue--Arthur Burns, Milton Friedman, and Herb Stein disliked the goldbugs of their day even more than Paul Krugman dislikes the goldbugs of ours, for they saw them as not only analytical idiots but also as dangerous in their potential to discredit the Good Old Cause via their ravings. And they argued Republican politicians into a commitment to use at least monetary policy to stabilize aggregate demand at full employment for two generations.

But not today.