AI Company Cmpetitive Moat Stack

AI companies are not competing on single products anymore—they’re competing across entire stacks. The firms that endure will be the ones that build defensible moats at multiple layers of the ecosystem, from chips all the way up to consumer experiences. The AI Company Competitive Moat Stack helps clarify how these layers fit together, and why controlling more than one creates lasting advantage.

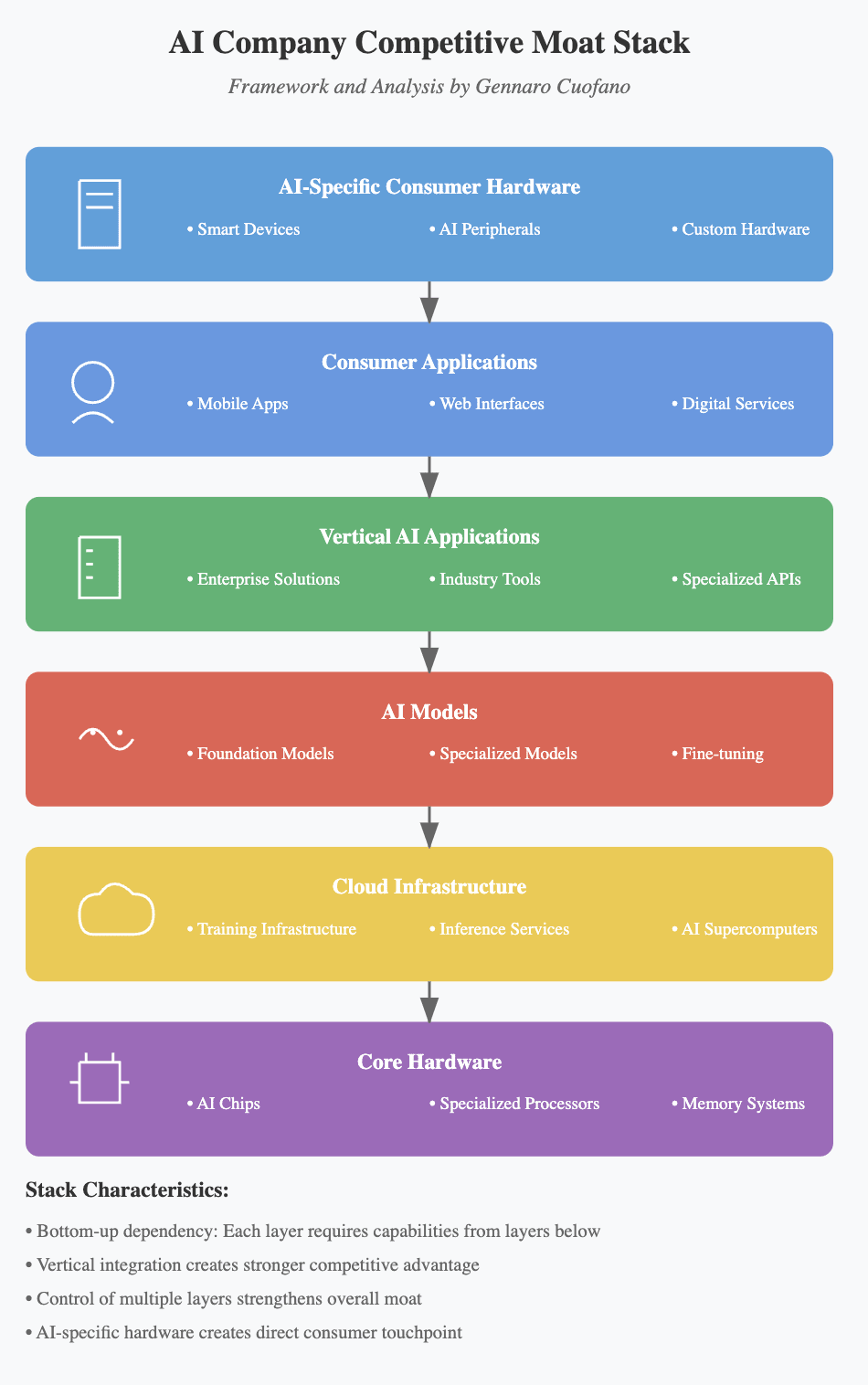

Core Hardware: The Foundation of AI ScaleAt the base of the stack is core hardware—AI chips, specialized processors, and memory systems. This is the bedrock of performance and cost efficiency. Companies like Nvidia and AMD dominate here, but new entrants are emerging with domain-specific processors optimized for inference or training. Control of hardware is rare but decisive: it shapes the economics of the entire AI industry.

Cloud Infrastructure: The Compute LayerOn top of hardware sits cloud infrastructure—training platforms, inference services, and AI supercomputers. This layer determines accessibility: who can train, fine-tune, and deploy models at scale. Giants like AWS, Microsoft Azure, and Google Cloud have leveraged their existing infrastructure to dominate, but specialized providers are emerging with optimized AI clouds. Moat strength here comes from both scale (economies of GPU supply) and integration (APIs, developer ecosystems).

AI Models: The Intelligence LayerThe AI model layer is where the intelligence lives. Foundation models like GPT or Claude create broad capabilities, while specialized models and fine-tuned systems deliver domain-specific performance. This layer is intensely competitive and fast-moving, with open-source communities narrowing the gap between startups and incumbents. The defensibility here often comes less from the model itself and more from the data pipelines, proprietary fine-tuning, and customer adoption cycles.

Vertical AI Applications: Industry-Specific MoatsAbove the models are vertical applications—enterprise solutions, industry tools, and specialized APIs. This is where AI becomes embedded in workflows and value chains. Successful players here understand not just the technology, but the regulatory, cultural, and operational realities of specific industries (finance, healthcare, legal, manufacturing). Unlike generic models, vertical applications can build long-term defensibility by becoming mission-critical to business operations.

Consumer Applications: The Distribution LayerThe consumer layer makes AI visible and usable. Mobile apps, web interfaces, and digital services provide the touchpoints where adoption happens. This layer thrives on design, usability, and network effects. Companies that dominate here—whether through chat interfaces, productivity apps, or entertainment—shape user behavior and build loyalty. Strong consumer apps also feed data back into models, reinforcing the stack from the top down.

AI-Specific Consumer Hardware: Direct Touchpoint with the MarketAt the top is AI-specific consumer hardware—smart devices, peripherals, and custom hardware built around AI experiences. This is a powerful moat because it creates direct, daily interaction with consumers. Just as the iPhone anchored Apple’s ecosystem, AI-native hardware could become the anchor for the next generation of platforms, making the stack more resilient and sticky.

Why the Stack MattersThe moat stack shows that AI competition is layered, interdependent, and cumulative. Each layer depends on the ones below, and the companies that control multiple layers strengthen their position dramatically. For example:

Nvidia spans hardware and infrastructure.OpenAI combines models with distribution (via ChatGPT).Apple is uniquely positioned to bridge consumer hardware, apps, and AI integration.The lesson: vertical integration creates durability. While many players will specialize in one layer, those who manage to integrate two or more will shape the direction of the industry.

The post AI Company Cmpetitive Moat Stack appeared first on FourWeekMBA.

{kind=link}